Morgan Stanley Asia Pacific Summit - CommBank · Morgan Stanley Asia Pacific Summit Stuart Grimshaw...

46

Morgan Stanley Asia Pacific Summit Stuart Grimshaw Group Executive, Financial & Risk Management Commonwealth Bank of Australia 23 October 2002

Transcript of Morgan Stanley Asia Pacific Summit - CommBank · Morgan Stanley Asia Pacific Summit Stuart Grimshaw...

Morgan Stanley Asia Pacific Summit

Stuart Grimshaw

Group Executive, Financial & Risk Management

Commonwealth Bank of Australia

23 October 2002

The material that follows is a presentation of general

background information about the Bank‟s activities

current at the date of the presentation, 23 October

2002. It is information given in summary form and

does not purport to be complete. It is not intended to

be relied upon as advice to investors or potential

investors and does not take into account the

investment objectives, financial situation or needs of

any particular investor. These should be considered,

with or without professional advice when deciding if

an investment is appropriate.

Disclaimer

Speaker’s Notes

Speaker‟s notes for this presentation are

attached below each slide.

To access them, you may need to save

the slides in PowerPoint and view/print

in “notes view.”

Agenda

The Australian Economy

Why Invest in Commonwealth Bank?

How is Commonwealth Bank Positioned Against the

Current Outlook?

The Australian Economy

Performance & Outlook

Interest Rates & Credit Outlook

Housing Market

Australia’s Economy has been Resilient

%%

%

Source: Commonwealth Research

V A L U E O F R E T A I LT R A D E

0

5

1 0

1 5

J u l -9 5 J u l -9 7 J u l -9 9 J u l -0 1

0

5

1 0

1 5

% p a% p a

R E L A T IV E G D P G R O W T H

(a n n u a l % c h a n g e )

-3

0

3

6

9

S e p - 8 7 S e p - 9 0 S e p - 9 3 S e p - 9 6 S e p - 9 9 S e p - 0 2

%

U S

A u s t ra l ia

G D P

(a n n u a l % ch a n g e )

-2

0

2

4

6

S e p -8 8 S e p -9 1 S e p -9 4 S e p -9 7 S e p -0 0

%

L o n g -ru n

a ve ra g e

P R O F I T S( % o f G D P )

8

1 2

1 6

2 0

S e p -9 0 S e p -9 3 S e p -9 6 S e p -9 9 S e p -0 2

C o rp o ra te

p ro fi ts *

(p r i v n o n - fa rm )

S m a l l b u s in e s s

in c o m e * * % G D P ( fc )

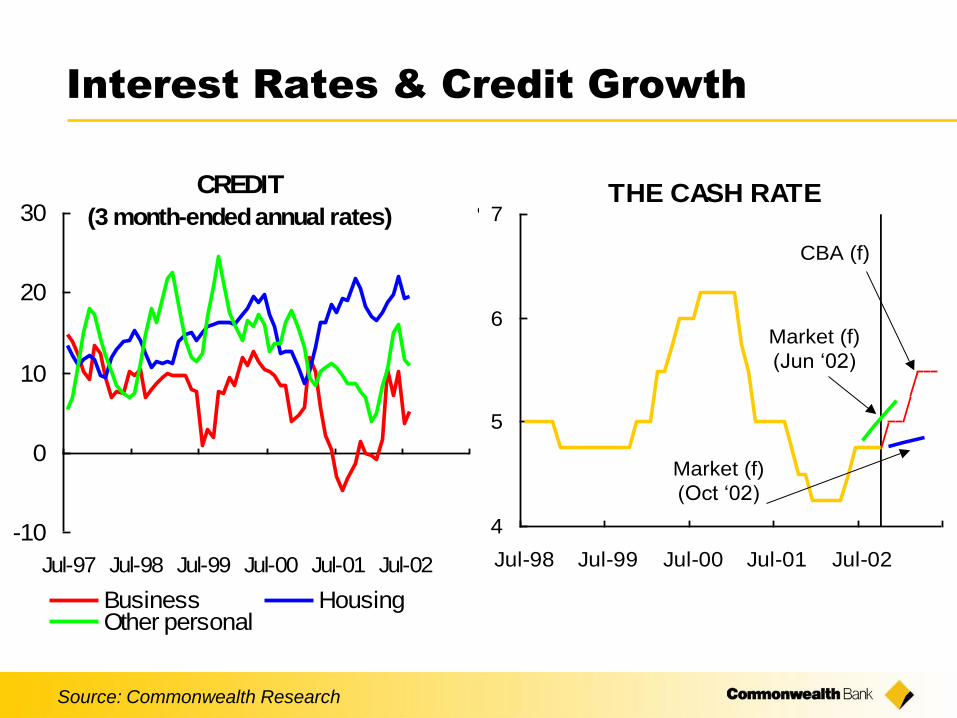

Interest Rates & Credit Growth

Source: Commonwealth Research

CREDIT

(3 month-ended annual rates)

-10

0

10

20

30

Jul-97 Jul-98 Jul-99 Jul-00 Jul-01 Jul-02

Business HousingOther personal

%THE CASH RATE

4

5

6

7

Jul-98 Jul-99 Jul-00 Jul-01 Jul-02

CBA (f)

Market (f)

(Jun „02)

Market (f)

(Oct „02)

Housing Market

Source: Commonwealth Research

%Index

*CBA Est. House Price Index

EQUITIES AND HOUSE PRICES

(RELATIVE PERFORMANCE)HOUSING LOAN

APPROVALS

Compound Annual Growth Rate: 1986-2002 2000-2002

All Ordinaries Index: 6.2% -3.5%

House Prices: 10.1% 20.5%

0

2

4

6

Jul-86 Jul-89 Jul-92 Jul-95 Jul-98 Jul-01

0

15

30

45

$bn '000

Owner-occupied

(ex refinance)

(rhs)

Investor

(lhs)

50

100

150

200

250

Sep-86 Sep-90 Sep-94 Sep-98 Sep-02

4

6

8

10

12

14

16

18

Mortgage rate (rhs)

All Ords (lhs)

House Prices* (lhs)

Housing Market

Source: Commonwealth Research

$‟0

00 %

pa

%pa

Source: Residex

*assumes principal repayment ratio fixed at 1997/98 level

5

10

15

20

<30 31-50 51-70 71-100 >1005

10

15

20

% %

Income ($'000pa)

DEBT REPAYMENT LEVELS(% of h/hold income, Mar'02)

H O U S E P R I C E S

0

1 0 0

2 0 0

3 0 0

4 0 0

M a r - 6 0 M a r - 6 8 M a r - 7 6 M a r - 8 4 M a r - 9 2 M a r - 0 0

- 2 0

0

2 0

4 0

6 0

R e a l

g r o w t h

( r h s )

L e v e l

( lh s )

S Y D N E Y H O U S E P R I C E S( d e f la t e d b y t h e C P I)

- 4 0

- 2 0

0

2 0

4 0

6 0

1 9 0 0 1 9 1 2 1 9 2 4 1 9 3 6 1 9 4 8 1 9 6 0 1 9 7 2 1 9 8 4 1 9 9 6

Q I- Q III 2 0 0 2

a t a n n u a l r a te

9 0 th

p e r c e n t ile

P R IN C IP A L R E P A Y M E N T S

0

10

2 0

3 0

S e p - 9 7 S e p - 9 9 S e p - 0 1

0

4

8

1 2

C u m u la t iv e

o v e r p a y m e n t

o f p r in c ip a l*

( r h s )

Pr in c ip a l

( % o f m o tg a g e

p a y m e n t)

( lh s )

Why invest in Commonwealth Bank?

Our Track Record

Our Differentiators and Growth Drivers

Recent Result Highlights

Solid Earnings Growth

Reported Profit up 10.7% to $2,655m

Cash Profit up 10.6% to $2,501m

Cash EPS up 10.1% to $1.97

Costs steady year on year

Improved productivity and cost to income ratio

High dividend payout ratio relative to peers

Capital position remains strong

Credit Quality and Provisioning remains strong

Net Profit*

* Net Profit after tax and outside equity interest - cash basis.

Excludes appraisal value uplift and goodwill amortisation.

1,109 1,153 1,1921,309

Full Year = 2,262 Full Year = 2,501

875 918 9751092

156164

12197

7871 96

120

0

200

400

600

800

1,000

1,200

1,400

Dec 2000 Jun 2001 Dec 2001 Jun-02

Banking Life & Super Funds M anagement

ROE and EPS

Dec 00 Jun 01 Dec 01 Jun 02

9488

91

103

12.46%13.10% 13.14%

14.61%

0

10

20

30

40

50

60

70

80

90

100

110

EPS

0%

5%

10%

15%

20%

25%

ROE

Earnings per share - cash bas is ROE - cash bas is

Dividend Growth

20 2024

36 3845 46 49

58 6168

20 22

36

4652

57 58

66

75

82

72

0

25

50

75

100

125

150

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Cen

ts

0

10

20

30

40

50

60

70

80

90

100

%

First Half Second Half Payout Ratio

Asset Quality Overview

First Half Second Half

Charge for Bad & Doubtful Debts (6 months) $290m $159m

Charge for Bad & Doubtful Debts to RWA(annualised)

0.42% 0.23%

Impaired Assets (net of interest reserved) $983m $884m

Specific Provisions $309m $270m

General Provision $1,334m $1,356m

General Provision to RWA 0.96% 0.96%

Segmentation: Aligned Domestic

Structure with Customer Needs

Retail BankingServices

PremiumFinancialServices

Investment &InsuranceServices

Institutional &BusinessServices

CustomerGroup

Personalbankingcustomers,Small businessbankingcustomers

Premium clientsincludingprofessionalsand business

Agents, Brokers,Financial Advisers

Institutional,Corporate,Commercialbusinesscustomers

Channels Branch, Ezy-Banking, ATM,EFTPOS,Phone, On-line,Mortgagebrokers

Relationshipmanagers,Premiuminvestmentcentres, phone,on-line.

Agents, Branches,Brokers, FinancialAdvisers, Premiuminvestment centres,DirectDealerships,Institutional Clients

Relationshipmanagers,Business centres

Support Finance, Risk Management, Human Resources, Strategy, Technology, Legal, Secretariat

Jun 2001 Dec 2001 Jun 2002

Home Loans^ 20.4% 20.1% 20.1%

(Residentially Secured)

Credit Cards 21.4% 21.4% 21.6%

Retail Deposits^ 24.0% 24.1% 24.2%

Retail FUM (Plan for Life) 16.1% 16.1% 15.7%

Superannuation/Annuities 16.3% 16.4% 16.4%

Retail Broking 9.0% 8.5% 9.2%

Inforce Premiums 14.4% 14.5% 14.4%

^ Due to delays in implementing new APRA reporting methodology,

no market share data has been available since March 2002.

Australian Market Share

Scale : Strong Market Share Positioning

Rank

1

1

1

1

1

2

2

*

*

* March 2002 data

*

*

Australia’s Most Accessible Bank

Over 146m DirectBanking calls

Almost 2m registered NetBank users

Around 126,000 EFTPOS terminals

Over 10,000 third party advisers,

brokers and agents

Around 4,000 ATMs

Nearly 4,000 postal and private

agencies

Over 1,000 branches

Over 700 EzyBanking store locations

Around 700 personal lenders

Over 700 financial planners

Around 200 mobile bankers

Over 70 business banking centres

13 premium banking centres

Customer

ChoiceBusiness

Banking

Financial

Planners

Brand: We Have More Relationships

Than Any Other Financial Institution

Source: Research International, April 2002

Popularity of Australian Financial Institutions….

* Customers under 25 years of age

^ Excludes Youth customers

39 40

21

14

27

22

42

53

0

10

20

30

40

50

60

Overall Youth* Premium Retail^

%

NAB Group ANZ Group CBA Group Westpac Group St George Group

Brand: We Achieve Consistently High

Ratings from Retail Customers

Source: Research International Brand Monitor

Average across all brand attributes for CBA

Vs average of ANZ, NAB and Westpac%

• In touch with its

customers

• Is leading the way

• Is doing new and

different things

• Has knowledgable

and competent staff

• Has friendly and

reliable staff

0

5

1 0

1 5

2 0

2 5

3 0

3 5

4 0

J a n

'0 1

M a r M a y J u l S e p N o v J a n

'0 2

M a r M a y J u l

C B A O t h e r M a jo r B a n k s

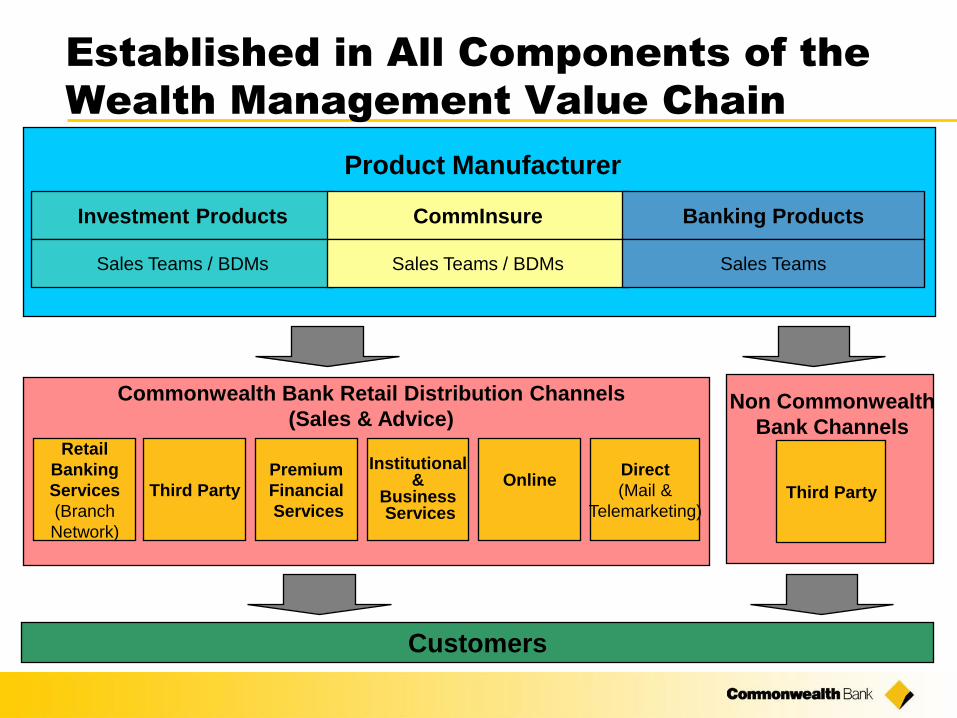

Established in All Components of the

Wealth Management Value Chain

Investment Products

Sales Teams / BDMs

CommInsure

Sales Teams / BDMs

Retail

Banking

Services

(Branch

Network)

Third Party

Premium

Financial

Services

Institutional&

BusinessServices

OnlineDirect

(Mail &

Telemarketing)

Customers

Commonwealth Bank Retail Distribution Channels

(Sales & Advice)

Product Manufacturer

Banking Products

Sales Teams

Third Party

Non Commonwealth

Bank Channels

0%

5%

10%

15%

20%

25%

7.30

7.45

7.60

7.75

7.90

8.05

8.20

8.35

0%

20%

40%

60%

80%

100%

34%

36%

38%

40%

42%

44%

Brand - Colonial First State

AMP

AMP

AMP

BTColonial

or

Colonial

First

State

Colonial

First

State

AXA

Colonial

First

State

ING

Consumer Brand Awareness - Unaided

3

Consumer Brand Awareness - Total

Consumer Purchase Intention

2

2

Adviser Brand Awareness - Overall

Opinion of Organisation

Platinum

1

Perpetual

Source: Consumer Charts - Newspoll June 2002; Adviser Chart - ASSIRT Service Level Survey 2002

Colonial

First

State

Funds Under Management

$103bn

29 28

2731 33 33

1723

24 26 25

2722

181921

0

20

40

60

80

100

120

Dec 2000 Jun 2001 Dec 2001 Jun 2002

$bill

ions

Australian Retail Funds Australian Wholesale Funds

International Funds Internal Life Assets

Average FUM

Innovation through

FirstChoice Masterfund Product

You and your

Financial

Adviser

Colonial First

State FirstChoice

Your financial

future

Structure

Value

Simplicity

Service

Investments PensionEmployer

Super

Personal

Super

Premium and Business Opportunity

Business (Middle Market)

Premium Customers

Source : Commonwealth Bank illustration

Current market share

Natural market share

Current number of premium customers

Potential number of premium customers

Premium: A Differentiated Business

Model

Banking

Platform

Broking

Platform

Borrowing Services

Lending Services

Transactional Banking

Advisory Services

Direct Investment

Indirect Investment

Debt Products

Equity Products

Personal

Banker

Commercial

Banker

Investment/

Equities

Expert

Event Based

Adviser

Insurance

Expert

Client

Primary Relationship ManagerSecondary Relationship Manager & specialised advice

Business: Increasing Cross-sell

Corporate Segment Example Bundled Products Example

26%

Working

Capital

Services

26% of corporate clients use

products from all three areas

Financial

Markets

Corporate

Finance

Business Banking

Financial

Markets

Working

Capital

Services

Interest rate risk

management

FX products

Investments

Bill financing

Cash funded loans

Overdrafts

Transaction services

Productivity: Focus on Efficiency

Remove all remaining back-office

functions from branches

Streamline home loan processes

Streamline Business Banking

processes

Rationalise investment products

& systems

Organisational design

...to achieve:

• A better service

experience for

customers, through

greatly improved

turnaround times

• Elimination of

duplication and

inefficiencies

• Annual benefits from

FY 2004, following an

incremental net cost

of ~$120m in FY2003

Five productivity initiatives...

How is Commonwealth Bank Positioned

Against the Current Outlook?

Credit Quality

Capital Position

Investment Market Volatility

Productivity Focus

Commonwealth Bank Group:

Low Credit Risk Profile

Housing Loans

53% of total loan book*

Loan loss rate of < 3bps in 17 of last 20 years

55% average loan to valuation ratio

Extensive stress testing of loan portfolio undertaken

Asset Quality

Impaired assets to risk weighted assets of less than 1%

in line with domestic peers

Relatively low bad debt expense

Well provisioned

* Excluding securitisation (or 57% including securitisation)

Total Individually Rated* Exposures

Credit Risk

61%

Investment

Grade

* Corporate and business lending

0%

20%

40%

60%

80%

100%

Dec 2000 Jun 2001 Dec 2001 Jun 2002

Other BBB A AAA/AA

Offshore* Loans & Advances by Industry

Other

Commercial

Government Agriculture

Finance

Construction

Personal

Leasing

* Excludes New Zealand (ASB )

Aggregate Provisions

* Includes Colonial

$m

illio

ns

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jun

94

Jun

95

Jun

96

Jun

97

Jun

98

Jun

99

Jun

00*

Jun

01*

Jun

02

0

50

100

150

200

250

300

%

General Provision

Specific Prov ision

Total Provisions/Gross Impaired Assets (axis on right)

Jun-01 Jun-02 APRA

Requirement

1,399

+449 -495

+3

1,356

1007

Surplus 349

(ie 35% above

the APRA

requirement)

500

700

1500

1700

1900

2100

900

1100

1300

$mCharged

to P&L

Used for

Specific

Provisions

Other

General Provision

0

500

1000

1500

2000

2500

Jun

1994

Jun

1995

Jun

1996

Jun

1997

Jun

1998

Jun

1999

Jun

2000

Jun

2001

Jun

2002

0

6

12

18

24

30

36

%

Commowealth Bank Group (Other Countries)*

Commonwealth Bank Group (Australia)*

Net Impaired assets as % of Total Shareholder Equity* (axis on right)

Net Impaired Assets

* Excluding Colonial prior to 30 June 2000

Asian Crisis

Acquisition

of Colonial

Two

Accounts

%

Non-Accrual Loans by Size

$5m<$10m $50m<$100m

$20m<$50m$10m<$20m

>=$100m<$5m

1

Customer

2

Customers4

Customers4

Customers

12

Customers

As at 30 June 2002

Non Accruals by Industry

Mining

Manufacturing

Agriculture

Property &

Business ServicesFinance

Transport

Government

Other

As at 30 June 2002

Accommodation,

Cafes & Restaurants

Balances $m % Portfolio % Troublesome % Impaired

Industry Exposures

Exposure to selected industries

$b $b $b

$b $b

$b

Insurance

-

0.8

1.6

2.4

3.2

Jun-00 Jun-01 Jun-02

0%

1%

2%

3%

Services to Agriculture, Forestry,

Fishing & Mining

-0.20.40.60.81.0

Jun-00 Jun-01 Jun-02

0%

2%

4%

6%

8%

Agriculture

-

1.0

2.0

3.0

4.0

5.0

Jun-00 Jun-01 Jun-02

0%

2%

4%

6%

Transport and Storage

-

2.0

4.0

6.0

Jun-00 Jun-01 Jun-02

0%

2%

4%

6%

Metal Mining & Manufacturing

-

1.0

2.0

3.0

Jun-00 Jun-01 Jun-02

0%

5%

10%

15%

Accommodation, Cafes and

Restaurants

-

0.5

1.0

1.5

2.0

2.5

3.0

Jun-00 Jun-01 Jun-02

0%

5%

10%

Strong Capital Position

2H01 1H02 2H02 2H01 1H02 2H02

TotalTier 1

CBA Target Range

Strong credit ratings

Shareholders equity

up $637m

Strong regulatory

capital ratios

Payments to

shareholders of $1,622m0.00%

4.00%

8.00%

12.00%

Tier 1 Capital Total Capital

Economic Equity

Regulatory capital ratios can be misleading:

Risk weights are not risk aligned

Capital required for residential mortgages is overstated

No operational risk charge

No value placed on earnings and risk diversification

Internal models show the Group is strongly capitalised

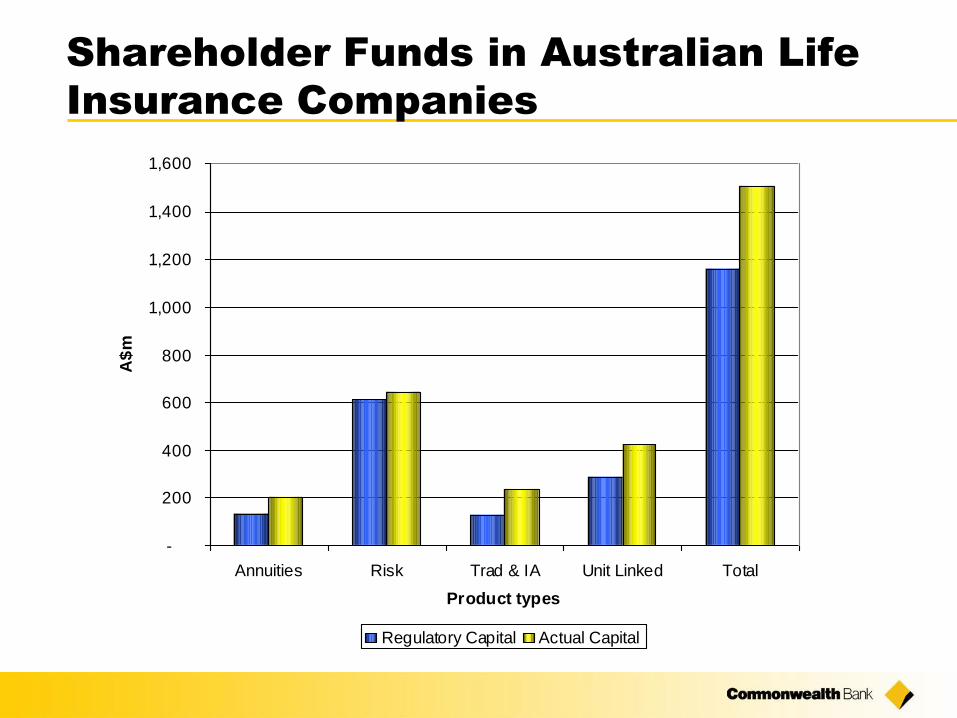

Shareholder Funds in Australian Life

Insurance Companies

-

200

400

600

800

1,000

1,200

1,400

1,600

Annuities Risk Trad & IA Unit Linked Total

Product types

A$

m

Regulatory Capital Actual Capital

Australian life companies: Future capital

requirements can be met by profit growth

-120

-70

-20

30

80

2003 2004 2005 2006 2007

Years

Ca

pit

al R

ele

as

ed

(A

$m

)

AnnuitiesRiskTrad & IAUnit Linked

Risk* GroupUnit Linked

Shareholder Funds in Life Insurance Companies

Income

$0.5 billion$2.1 billion

53%47%

Growth

$2.6 billion

67% 33% 50% 50%

*Risk includes traditional, investment account, annuities, personal risk and group risk.

Greater Cost Control & Targeted

Investment in Priority Areas

Upgrading infrastructure to

improve service

Developing and managing

relationships with all customers

Product simplification &

rationalisation; packaging

products for premium customers,

and manufacture innovative new

products

%

Focus on achieving further

productivity improvements...

...by reducing costs and spending

to improve service quality and

drive revenue growth

53

54

55

56

57

58

59

60

31-D

ec-0

0

30-J

un-0

1

31-D

ec-0

1

30-J

un-0

2

Group Cost to Income Ratio (Normalised)

Summary

The Australian Economy

Has been resilient

Outlook remains positive in global context

Why Invest in Commonwealth Bank?

Our track record

Our differentiators

Our growth drivers

How is Commonwealth Bank Positioned Against

the Current Outlook?

Low credit risk profile

Strong capital position

Productivity focus

Morgan Stanley Asia Pacific Summit

Stuart Grimshaw

Group Executive, Financial & Risk Management

Commonwealth Bank of Australia

23 October 2002