Monthly NCM Report for Feb 2011 - proshareng.com · The Monthly NCM Report for Feb 2011 www...

55

ISSN 1597 - 8842 Vol. 1 No. 62 The Monthly NCM Report for Feb 11 Issued on Mar 04, 2011

Transcript of Monthly NCM Report for Feb 2011 - proshareng.com · The Monthly NCM Report for Feb 2011 www...

ISSN 1597 - 8842 Vol. 1 No. 62

The Monthly NCM Report for Feb 11Issued on Mar 04, 2011

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 2

Contents

Executive Summary 3

Introduction 7

All-Share Index Movement 13

Market Dynamics 14

Comparison of 2009 and 2010 Market Performance 16

Sectoral Index Movements 18 NSE -30 Index, NSE -Food Index, NSE -Banking Index, NSE -Insurance Index & NSE -Oil Index

Sectoral Analysis 24

Transactions Volume and Value Trend 25

Top Ten Trades in the Month 27

Top Ten Traded Sectors in the Month 28

Top Ten Gainers in the Month 28

Top Ten Year to Date Appreciation 29

Top Ten Decliners in the Month 29

Top Ten Year to Date Depreciation 30

Corporate Declarations in the Month 31

Forecast Results in the Month 42

Dividends Declared 43

Outlook/ Analyst Opinion 43

Time Lines (April Market News/Information) 45

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 3

The Monthly NCM Report for February 2011

ISSN 1597 - 8842 Vol. 1 No. 62

Executive Summary

Market trend in the month of February maintained consistent downward trend as market experienced continuous bleeding while the outlook recorded lots of red (negatives) positions with doted greens (positive), indicating intense bearish atmosphere with strong hold of bears on the back of continued profit taking and speculative tendency.

More so, the market terrain was heavily characterised with huge sell activities, feeble market confidence and low strength to drive active/profitable bargain activities as bearish sentiments dominated the market activities with fading investors’ commitment.

The rollover effect of profiteering exercise in the previous month initiated the downtrend in the month of February which later extended to unrelenting selling, induced by weak confidence as market lacked the will to drive bargain transactions.

The first six trading sessions in the month witnessed huge sell activities with single day of rally as bears dominated the terrain on the back of profit taking tendency as noted above, dipping market net worth by N99.15 billion while the key benchmark indices recorded -1.56% loss.

During this period, market recorded 2.06 billion units of volume traded, on average of 343.94million units, which accounted for 31.76% of total volume traded in the month, indicating intense selling momentum. The trend was in reverse of comparable period in the previous month as shown below.

First six trading days in the month Indicators Feb-11 Jan-11

Volume (billion Units) 2.06 3.41 Value (billion Naira) 22.21 32.18 Market CAP (billion Naira) -99.15 330.51

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 4

ASI -1.16% 4.12% Proshare

The All Share Index gained the highest points by 1.03% on February 9th 2011, closing at 26,685.30 while speculative tendency took over the consistent profiteering recorded in early stage of the month. The trend in the ASI movement revealed intense speculative activities as market swings up and down, suggesting mixed sentiments due to low state of market confidence. The growing activities towards treasury bills and bonds coupled with attractive interest rate in the money market following the tightening of MPR by CBN could be attributable to this trend (prolonged bearish trend) as this was perceived to have reduced the liquidity and patronage position in the market.

As a result of prolonged bearish sentiments which were induced by profit taking, the key benchmark indices extended four weekly negative positions in a row as observed in one of our weekly reports. Also, the divestment move by banks from their subsidiaries could be a contributory factor to the prolonged bearish trend.

Also, the recapitalisation of market operators as suggested by regulatory body had contributory impact to the long downward trend in the market as many brokers or operators assumed selling positions to raise capital for 70million minimum share capital which led to the suspension of 57 stock broking firms last month. Follow this link to know current status. https://www.proshareng.com/news/13185

The long delay in the announcement of corporate financial reports for the year ended December 31st 2010 had its dose of impact on the low equity bargain recorded during the period while the inactive status of some foreign hedge funds due to withdrawal, further depressed market performance.

Nevertheless, calm returned to market after 5days of speculative activities and sideways movements i.e. between February 17th and February 22nd 2011, as market recorded steady and consistent moderate buying while ASI consequently experienced 4 days uninterrupted uptrend, growing market capitalisation by N89.00billion during the period.

The activities towards blue chip stocks particularly in Food and Beverages, Banking, Breweries, Building Materials sectors coupled with activities recorded on penny stocks mainly in Insurance sector impacted the outlook. The announcement of good earnings with rewards from few blue chips and expectation of impressive Q4 reports from others remained the only driver for the short-lived rally.

Speculative tendency resumed with more momentum as market experienced high volatility towards the end of the month, depressing market to fresh low at 26,181.18 in the month with significant loss of N233.38billion between Feb 22nd and 28th 2011 while speculators scrambling for short profit, indicating low commitment and confidence.

It was also observed that significant volume of 1.85 billon units, representing 29% and 26% total volume and value respectively was recorded at the tail end of the month which revealed sell off tendency as ASI dipped by -2.73%. Although, closing of books for the months could be responsible for this huge sell off while the month closed bearish

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 5

with aggregate loss of -3.03%. The trend might continue if the commitment level remained very low.

However, the position of management of NSE to ensure strict compliance with rules and regulations by the Exchange remained unchanged. Also, the enforcement of separation of clients’ account from brokers’ trading accounts remained the same as this is set to protect investors’ stake in the market- this in our opinion would mitigate some unethical and sharp practices by brokers and of course signal to investors’ confidence- a panacea to market recovery, all things being equal. In addition, the recent review and update of rules for listed companies, which was last reviewed in 1975 according to records, gave some insights that NSE is likely to maintain high level of discipline in the market this year- which will of course bring sanity to market as enforcement of post listing rules will aid quick investment decision http://www.proshareng.com/news/12955 On the final note, the employment of new NSE CEO is expected to add more colours to the ongoing reforms in the Nigerian Capital Market when he finally settles down, we believe that market would receive dose of impact -positively or negatively, only investors’ reaction or market performance will tell as events are unfolding, while we are believing that the new CEO will tread the path of creating more efficient and transparent Exchange as advised http://www.proshareng.com/articles/2208

A number of developments we believed should have impact in the month as predicted in the past monthly reports. Some of which are:

Impact Assessment Table Factors expected to move market in February 2011 Outcomes

AMCON Buying of toxic assets influenced bargain activities

IFRS Full compliance is yet to commence

Banks lending to real sector

Banks are yet to start lending to real stock. This situation might remain the same with recent hike in monetary policy rates.

Margin loans Banks remained conservative towards Margin loans

Monetary Policy Rates

Increased money and bond market activities as investors seek free risk attractive returns.

Renewed and sincere efforts towards reinvigorating market confidence

Sanctions against 61 stock broking firms with negative share capital was commendable

Informed and planned regulatory reforms i.e. less of unstructured reforms The terrain remained calm

Merger and acquisition in the banking sectors

Processes are on course as deals and agreements are about to take final shape.

Liquidity challenges Still persist

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 6

Continued cleanup of market irregularities by NSE

NSE maintained strict posture while the recapitalisation of market operators is still alive

Banking Sector audited Results

Significant volume and value growth witnessed in the sector in anticipation of audited results. Also the long delay of the results reduced investment commitment.

Ownership of the rescued banks Agreements are yet to be concluded, some of them are likely to seal deals soon.

Developments in the coming months:

Positive corporate actions Liquidity challenges Recapitalization process in the banking sector Merger & Acquisition in the banking sector Conclusion of bids on rescued banks Monetary Policy Rates Inflation outlook New NSE CEO- charting of new course New banking regime- likely to have effect on the market as more banks are likely

to divest from their subsidiaries Increased institutional investing Continued cleanup of market irregularities by NSE

Thank you for reading and do take time to share with us your thoughts on the market, analyst at [email protected].

We value your feedback and comments.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 7

Introduction “Nigerian Capital Market turns bearish by -3.03% with growing speculative tendency. Equity market experienced low bargain activities in the month of February as sell tendency dominated the market atmosphere. The prolonged bearish trend witnessed in the month started with profit taking motive, which was later taken over by speculative tendency as low commitment ensued while market lacked the strength to drive active and profitable bargain.

The impressive rally and growth recorded in the previous month could be responsible for the early sell activities witnessed in the month of February, which also could be taken as market correction. During this period, market CAP recorded N99.15billion loss while ASI dipped by -1.16%.

More so, short term traders took over market arena shortly after correction exercise as atmosphere was filled with mixed sentiments while bulls and bears jostled for position, swinging market in both directions.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 8

Furthermore, the trend remained unstable after hitting its high during the month at 26,685.30 to score the highest points of 1.03% on 9th February 2011. Market experienced consistent weekly negative positions throughout the month while every gain recorded during the month was equally reversed as ASI hit the lowest points in 34days at 26,016.84 to technically enter bearish mode in both short term and mid-long term due to overwhelmed sell volumes.

However, the comparable period in the previous year 2010 was fairly better as the outlook was more positive, though series of volatility due to high speculative tendency was observed. Nevertheless, the period marginally closed positive by +0.52% with YTD of +10.30% (February 2010) as against current -3.03% and YTD of +3.64% (February 2011). The current market trend further revealed strong bearish sentiments.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 9

Market pattern basically reveals that market is technically weak and bearish in both short term and mid-long term as could be seen from the NSE ASI moving averages trend with index of 26,061.84 as at February 28th, 2011 trading below its 20 and 50 days of 26,606.23 and 26,282.07 respectively, while trading above 200 days of 25,305.84. This suggests market trend is technically bearish mid long term.

The Market – Game On

The market this month recorded a total volume of 6.49 billion units valued at N60.60 billion (US$410.75 million) exchanged in 119,477 deals compared with 7.90bn units valued at N54.04bn (US$366.28bn) exchanged in 113,116 deals in February 2010. Comparing, the volume and value traded in the month reveals a 17.81% below the volume and 12.14% above value recorded in the previous year’s comparable period respectively.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 10

During the month, All-Share Index recorded a negative trend of -3.03%, a relative low performance to the positive growth of +0.52% upbeat recorded in February 2010. More so, the trend is significantly negative when compared with the -0.34% loss recorded in the previous month December 2010.

Market capitalisation this month declined by N260.19 billion (US$1.76 billion) as against depreciation by N27.19 billion (US$184.28m) recorded in December 2010. Market Capitalisation gained higher figure of N352.81 billion (US$2.39b) in the previous year’s comparable period (February 2009).

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 11

The Market – Game Changers:

The capitalisation issue of market operators which led to suspension of some dealers due to low share capital could be taken as of one of the contributory factors for the downtrend in the market as brokers engaged in heavy sell to raise capital for their capital base requirements as demanded by NSE in the month under review. The major factors remained low commitment as a result of long delay in corporate results of most active sector in the market, the attractive interest in the money market coupled with influx of bonds in market, high speculative tendency due to feeble market confidence and low liquidity. The market recorded series of huge sell in the early stage of the month on the back of profiteering while speculative tendency took over the terrain as market swings up and down. We envisage that the low price position, expectation of impressive Q4 earnings from banking sector and conclusion of merger talks might trigger reversal trend in the market. The contributory factors for performance in the month of February 2011 can be located in the following indices as outlined below: Negative Factors in the market

No lending to the private sector and still in doubt Liquidity squeeze and the current politics - created uncertainty in the economy Increased investment in money market due to attractive rates Investor’s confidence yet to gain momentum. Low commitment Partly withdraw of hedge funds Hike in the Central Bank of Nigeria's benchmark interest rate. Influx of Federal government and state bonds with other fixed income instrument in

market. Absence of Margin loans

Positive Factors in the market

Positive progress in recapitalisation by shareholders

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 12

Second round of toxic assets purchase by AMCON Demutualisation of NSE Proposed new trading platform Buying of toxic assets in the banking sector by bad bank Ongoing recapitalisation process in the banking sector Possibility of merger and acquisition in banking sector Steady Institutional and value investing Investment by fund managers Expectation of Impressive Q4 results from banking sector and some blue chips The Federal Government commitment to revive economic infrastructures

Market Concerns: The confidence and commitment level remained low while continued speculative tendency with prolonged bearish sentiments witnessed during the month. More so, liquidity level is still low which might not get better anytime soon as banks remained conservative and the hike of MPR with other monetary rates will not help situation. Although we envisage slight improvement in liquidity outlook as we move closer to election time.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 13

The NSE All-Share Index Movement The Nigerian equities started the month with continued profit taking tendency as rollover effect of profiteering witnessed at the tail end of the previous month. The impressive rally and growth recorded in the previous month could be attributed to the profit taking activities as market set for correction. Speculative tendency dictated the tune of market trend as market swings in both directions interchangeably.

Trends in the month revealed that bears dictated the pace in the first six trading days into the month (between 1st and 8th February, 2011), with aggregate loss of -1.16% as against -2.29% in December 2010 and +0.52% in February 2010. The equity market recorded bearish trend as market witnessed significant selling activities particularly in the banking sector while rescued banks led the volume transactions which depressed market considerably. The NSE index in February 2011 closed with four days extended loss position as result of speculative tendency following four days uptrend. The month recorded negative performance, with aggregate loss position of -3.03% to close at 26,016.84 compared with +0.52% appreciations recorded in the preceding year comparable period to close at 22,985.00. The loss in the month was far above the -0.34% recorded in the month of December 2010.

Meanwhile, at the end of the last trading day of the month under review, All-Share Index closed above the figure recorded at the close of 25th February 2010 by +13.19% and 4th January 2010 by 24.85%. Market pattern basically reveals that market is technically weak and bearish in both short term and mid-long term as could be seen from the NSE ASI moving averages trend with index of 26,061.84 as at February 28th, 2011 trading below its 20 and 50 days of 26,606.23 and 26,282.07 respectively, while trading above 200 days of 25,305.84. This

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 14

suggests market trend is technically bearish mid long term.

Source: NSE, Proshare Research

At the close of the last trading day of the month, All-Share Index traded below its 20 and 50 days of 26,606.23 and 26,282.07 respectively, while trading above 200 days of 25,305.84. This suggests market trend is technically bearish mid long term.

Source: NSE, Proshare Research

February 2011 Market Dynamics

The market dynamics as graphically illustrated below showed the appreciation and depreciations on the daily basis.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 15

Low investors’ commitment, delay in Q4 corporate results of banking stocks and some blue chips, , attractive interest in money market, influx of federal and states bonds, high speculative tendency, low liquidity and feeble market confidence, merger and acquisition in the banking sector, the recapitalisation of market operators, withdrawal of hedge funds, continued efforts towards establishing healthy market and corporate governance in NSE.

Source: NSE, Proshare Research

MARKET DYNAMICS IN THE PRECEDING YEAR COMPARABLE PERIOD (FEBRUARY, 2010)

Source: NSE, Proshare Research

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 16

Comparison of 2010 and 2011 Market Performance

The market performance in February 2011, when compared with the 2010 comparable period; showed negative trend with bearish sentiment. In the period under review, ASI recorded -3.03% decline compared with +0.52% upswing recorded in 2010 February. The outlook in the current period suggests negative monthly performance when compared with comparable period of preceding year trend. The market closed at approximately in the range of 26,000.

Source: NSE, Proshare Research

Dates NSE ASI Market

Capitalisation (trillion)

Market Capitalisation ($

billions)

Jan-02-10 20,838.90 4.99 31.19

Feb-01-10 22,865.16 5.51 34.44

Feb-25-10 22,985.00 5.54 34.63

Monthly Return 0.52% 0.54% 11.02% Yearly Return 10.30% 11.02% 11.02%

Jan-04-11

25,102.93 8.02 53.47

Feb-01-11 26,723.49 8.54 56.93

Feb-28-11 26,016.84 8.32 55.47

Monthly Return -2.64% -2.58% -2.58% Yearly Return 3.64% 3.74% 3.74%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 17

Source: NSE, Proshare Research

From the table above, the year to date performance as at 28th February 2011 closed at +3.64% against the previous year comparable period of 25th February, 2010 at +10.30% appreciation, indicating a low performance against the trend recorded last year.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 18

Sectoral Index Movements

NSE 30 NSE Food

NSE Banking

NSE Insurance

NSE Oil

01/02/2011 1,165.70 854.91 432.91 185.84 352.2 02/02/2011 1,175.94 855.86 440.89 186.13 356.19 03/02/2011 1,174.11 853.92 439.35 184.81 357.77 04/02/2011 1,173.00 849.09 439.17 185.41 358.72 07/02/2011 1,167.99 850.68 436.10 187.45 359.35 08/02/2011 1,166.19 844.15 439.56 183.44 359.35 09/02/2011 1,164.36 842.58 441.34 180.87 357.23 10/02/2011 1,159.60 839.41 438.02 180.73 357.23 11/02/2011 1,164.31 842.57 439.55 181.74 355.12 14/02/2011 1,160.28 839.81 438.11 182.97 353.54 16/02/2011 1,153.64 837.28 435.04 178.64 351.9 17/02/2011 1,163.65 845.19 442.92 177.06 349.81 18/02/2011 1,166.72 863.57 441.13 177.52 345.58 21/02/2011 1,169.78 878.68 442.32 181.54 344.51 22/02/2011 1,174.80 876.11 441.66 185.79 343.47 23/02/2011 1,174.11 874.77 440.59 184.56 343.47 24/02/2011 1,156.31 889.54 429.91 185.43 345.94 25/02/2011 1,148.12 881.34 428.5 185.13 346.89 28/02/2011 1,138.79 871.84 424.2 184.85 346.89

Monthly % Change -2.31% 1.98% -2.01% -0.53% -1.51%

In the month under review, four sectoral indices moved down considerable except NSE Food & Beverages which top with 1.98% gain while NSE 30 is topping the negative side by -2.31%, followed by NSE Banking by -2.01%, NSE Insurance and NSE Oil & Gas dropped by -0.53% and -1.51% respectively.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 19

February and January Sectoral Indexes Compared

Source: NSE, Proshare Research When compared the current trend with the previous impressive positive outlook recorded in January with NSE sectoral index movements, none of the sectoral indices outperformed previous outlook recorded in the month of January 2010.

NSE -30 INDEX

Source: NSE, Proshare Research

The trend recorded in the blue chips stocks is reflected in the index movement. There were active consistent sell transactions and slight interruptions at the few points in the index performance during the month due to the volatility resulting from profiteering in the period. The sector experienced significant sell in the early state with trends reversal in mid-stage to embark on a sharp fall at the tail end of the month. The trend revealed

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 20

high speculative tendency in the sector while the index dipped by -2.31% as against +6.60% gain recorded in the month of January.

NSE -FOOD INDEX

Source: NSE, Proshare Research

The stocks in the sector experienced series of speculative tendency in the early stage with continued patronage to record outstanding positive outlook in the month, the performance in the sector rated best. The performance of 1.98% is considered significantly low when compared with January 2011 posture of +9.66%. This is against appreciations by +12.72% recorded in January 2010 comparable period. The outlook in the sector throughout the month suggested better prospect and returns in months ahead.

NSE -BANKING INDEX

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 21

Source: NSE, Proshare Research

NSE-Banking index closed the month of February with falling posture as the sector experienced concentrated profit taking tendency and sell off, while the rescued banks led the sell activities to dip by -2.01%, a negative performance when compared with +4.38% appreciation recorded in January. The negative outlook recorded was largely driven by the long delay in announcing the Q4 results.

NSE -INSURANCE INDEX

Source: NSE, Proshare Research

The sector experienced high volatility due to speculative tendency coupled with consistent profit taking which emanated from impressive price appreciation recorded in the previous month of January. They penny of the sector increased the speculative

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 22

activities while the sector declined from high of +12.55% recorded January 2011 to current position of -0.53%. However, the sector will ripe any time soon for trend reversal as the sector possesses potential of price appreciation, considering penny nature of the sector.

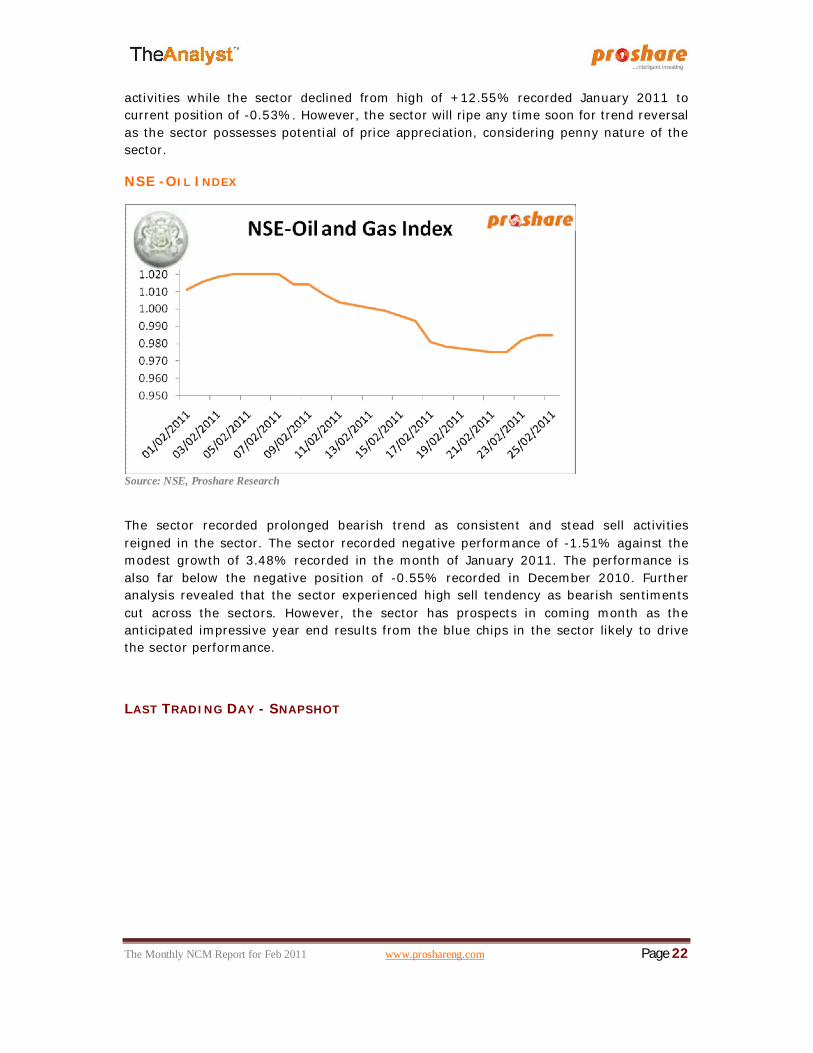

NSE -OIL INDEX

Source: NSE, Proshare Research

The sector recorded prolonged bearish trend as consistent and stead sell activities reigned in the sector. The sector recorded negative performance of -1.51% against the modest growth of 3.48% recorded in the month of January 2011. The performance is also far below the negative position of -0.55% recorded in December 2010. Further analysis revealed that the sector experienced high sell tendency as bearish sentiments cut across the sectors. However, the sector has prospects in coming month as the anticipated impressive year end results from the blue chips in the sector likely to drive the sector performance.

LAST TRADING DAY - SNAPSHOT

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 23

http://www.proshareng.com/investors/theAnalyst.php

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 24

SECTORAL ANALYSIS

SECTOR PREFORMANCE

Sector YTD %Change

MARITIME 21.09% ROAD TRANSPORTATION 18.18%

HEALTHCARE 9.00% FOOD/BEVERAGES & TOBACCO 7.71%

BREWERIES 7.29% MEDIA 6.48%

BANKING 5.02% AIRLINE SERVICES 4.74%

REAL ESTATE 4.18% THE FOREIGN LISTINGS 4.14%

INSURANCE 2.96% PETROLEUM(MARKETING) 2.45%

AUTOMOBILE & TYRE 2.18% ENGINEERING TECHNOLOGY 1.36%

CONSTRUCTION 0.91% SECOND-TIER SECURITIES 0.72%

AVIATION 0.00% FOOTWEAR 0.00%

CHEMICAL & PAINTS -0.23% PRINTING & PUBLISHING -0.43%

OTHER FINANCIAL INSTITUTIONS -1.02% PACKAGING -1.50%

BUILDING MATERIALS -1.68% MORTGAGE COMPANIES -2.16% COMMERCIAL/SERVICES -2.54%

HOTEL & TOURISM -2.60% TEXTILES -2.67%

COMPUTER & OFFICE EQUIPMENT -2.88% CONGLOMERATES -3.56%

INFORMATION & COMMUNICATION TECHNOLOGY -3.91% AGRICULTURE -3.93%

INDUSTRIAL/DOMESTIC PRODUCTS -4.63% LEASING -9.87%

Source: NSE, Proshare Research

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 25

Transactions Volume and Value Trend

Market Feb '10' Feb '11' % Change Average Daily Volume of Stocks Traded (in millions) 416.05 341.95 -17.81% Average Daily Value of Stocks Traded (in N'millions) 2,844.46 3,189.81 12.14%

Average Daily Value of Stocks Traded (in USD$ millions) 18.96 20.32 7.16%

Total Volume of Stocks Traded (in millions) 7904.94 6497.1 -17.81% Total Value of Stocks Traded (in N'millions) 54,044.74 60,606.40 12.14%

Total Value of Stocks Traded (in USD$ billion) 360.30 386.03 7.14%

New Listing and Delisting Feb '10' Feb '11' Number of Equities Delisted 1 0

Number of New Listings 0 0

Source: NSE, Proshare Research

The transaction volume in the month of February when compared with the preceding year comparable period closed lower by -17.81% to close at 6.49 billion units compared with 7.90 billion units traded in February 2010. This could be an indication that the investors’ patronage of the market in the month under review was significantly different.

Also, the transaction value in the month under review closed higher by 12.14% at N60, 606.40 billion ($386.03 million) compared with N54, 044.74 billion ($360.30 million) of February 2010.

February 2011 vs. 2010 Daily Volume Chart

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 26

Source: NSE, Proshare Research

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 27

Top Ten Trades for the Month of February 2011

Zenith bank Plc topped the transaction volume for the month. Banking stocks generally dominated the charts with nine of the stocks in the sector emerging in the top ten trades chart for the month.

Company Total Trades Total Volume Total Value ZENITHBANK 8,085.00 686,856,999.00 10,784,743,152.54 UBA 4,647.00 497,211,392.00 5,022,757,452.86 FIRSTBANK 14,279.00 426,175,813.00 6,591,023,257.60 FIRSTINLND 2,708.00 365,005,954.00 382,686,849.97 OCEANIC 3,794.00 284,146,496.00 927,449,919.89 GUARANTY 9,989.00 275,936,251.00 5,394,584,836.94 PLATINUM 2,511.00 259,700,153.00 543,225,299.39 INTERCONT 2,649.00 250,748,600.00 632,293,593.17 FIDELITYBK 2,672.00 235,313,265.00 727,060,699.45 JAPAULOIL 2,232.00 218,408,314.00 390,564,290.03

Recall Top Ten Trades for the Month of February 2010

Company Total Trades Total Volume Total Value FIRSTINLND 2569 551,775,485.00 429,007,344.89

IHS 40 488,698,625.00 1,969,443,956.75 ZENITHBANK 4878 468,812,491.00 7,380,615,475.04 FIRSTBANK 16214 340,771,006.00 5,117,075,253.83

ACCESS 4113 292,172,797.00 2,657,484,093.72 DIAMONDBNK 2243 258,602,667.00 2,360,976,418.64

GUARANTY 8085 251,929,949.00 4,581,704,224.72 UBA 5069 251,145,746.00 3,360,695,616.11

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 28

SKYEBANK 3551 224,831,699.00 1,693,515,809.98 FIDELITYBK 3111 202,874,338.00 540,592,033.78

Top Ten Traded Sectors for the Month of February

Sector Total Trades Total Volume Total Value % Contribution

BANKING 70,649.00 4,494,288,409.00 37,294,529,111.31 69.17% INSURANCE 4,801.00 450,232,651.00 666,893,649.24 6.93% MARITIME 2,232.00 218,408,314.00 390,564,290.03 3.36% FOOD/BEVERAGES & TOBACCO 9,741.00 157,026,547.00 4,720,877,056.38 2.42% PACKAGING 4,816.00 132,658,996.00 299,881,599.46 2.04% MORTGAGE COMPANIES 736.00 128,215,215.00 89,069,529.43 1.97% BUILDING MATERIALS 2,975.00 103,428,916.00 4,642,988,623.69 1.59% HEALTHCARE 1,755.00 98,763,141.00 254,332,666.02 1.52% MEDIA 198.00 79,467,107.00 41,550,789.67 1.22% PETROLEUM(MARKETING) 5,554.00 72,953,142.00 4,838,250,701.18 1.12% Top 10 Trades 103,457.00 5,935,442,438.00 53,238,938,016.41 Total Trades 119,477.00 6,497,107,332.00 60,606,404,039.36

Source: NSE, Proshare Research

Recall Top Ten Sectors for the Month of January 2010

Sector Total Trades Total Volume Total Value BANKING 70301 4,032,381,421.00 32,853,008,942.78 INSURANCE 10069 1,179,356,236.00 1,185,619,424.02 INFORMATION & COMMUNICATION TECHNOLOGY 1197 735,152,033.00 2,433,233,661.74

FOOD/BEVERAGES & TOBACCO 12425 290,822,691.00 4,811,401,907.48 MORTGAGE COMPANIES 1413 236,988,125.00 159,180,924.50 CONGLOMERATES 4603 208,629,936.00 2,542,200,012.64 BUILDING MATERIALS 4482 135,353,273.00 3,189,465,230.21 CHEMICAL & PAINTS 321 121,829,081.00 579,520,089.75 OTHER FINANCIAL INSTITUTIONS 563 117,067,823.00 108,335,842.03 MARITIME 2348 100,574,642.00 124,215,058.58 Top 10 Sectors 107,722.00 7,158,155,261.00 47,986,181,093.73

Source: NSE, Proshare Research

Top Ten Gainers in the Month

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 29

COMPANY 01-Feb-11 28-Feb-11 Change % Change

CHAMPION 2.45 3.41 0.96 39.18% NEIMETH 1.27 1.51 0.24 18.90% INTBREW 5.75 6.61 0.86 14.96% NESTLE 410.15 460 49.85 12.15% MOBIL 141 155.45 14.45 10.25% CAP 34.03 37.39 3.36 9.87% BERGER 9.97 10.91 0.94 9.43% CUSTODYINS 3.21 3.51 0.3 9.35% WEMABANK 1.6 1.72 0.12 7.50% JAPAULOIL 1.66 1.78 0.12 7.23%

Source: NSE, Proshare Research

Top Ten Year to Date Appreciation

COMPANY 28-Feb-

11 4-Jan-

11 Change % Change

SPRINGBANK 1.63 0.95 0.68 71.58% CHAMPION 3.41 2.23 1.18 52.91% NEIMETH 1.51 1.01 0.5 49.50% NIGERINS 0.87 0.6 0.27 45.00% EVANSMED 1.45 1.05 0.4 38.10% BERGER 10.91 8.36 2.55 30.50% WEMABANK 1.72 1.35 0.37 27.41% NESTLE 460 368.55 91.45 24.81% UTC 0.8 0.65 0.15 23.08% BAGCO 2.8 2.3 0.5 21.74%

Source: NSE, Proshare Research

Top Ten Decliners in the month

COMPANY 01-Feb-11 28-Feb-11 Change % Change

WAPIC 0.8 0.55 -0.25 -31.25% OCEANIC 3.7 2.71 -0.99 -26.76% AFRIBANK 2.87 2.11 -0.76 -26.48% STARCOMMS 1.22 0.9 -0.32 -26.23% UBN 4.8 3.61 -1.19 -24.79% FIRSTINLND 1.06 0.82 -0.24 -22.64% PLATINUM 2.13 1.65 -0.48 -22.54% UNITYBNK 1.56 1.24 -0.32 -20.51%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 30

INTERCONT 2.62 2.15 -0.47 -17.94% GOLDINSURE 0.67 0.55 -0.12 -17.91%

Top Ten Year to Date Depreciation

COMPANY 28-Feb-

11 4-Jan-

11 Change % Change

STARCOMMS 0.9 1.37 -0.47 -34.31% FIDSON 2.38 3.06 -0.68 -22.22% POLYPROD 1.45 1.86 -0.41 -22.04% NSLTECH 1.48 1.88 -0.4 -21.28% NIG-GERMAN 10.53 12.91 -2.38 -18.44% LIVESTOCK 0.54 0.66 -0.12 -18.18% UBN 3.61 4.41 -0.8 -18.14% VITAFOAM 5.4 6.5 -1.1 -16.92% PREMPAINTS 11.5 13.4 -1.9 -14.18% JOHNHOLT 7.58 8.82 -1.24 -14.06%

Corporate Declarations

February 1st, 2011: RED STAR EXPRESS PLC

2nd February, 2011: TRIPPLE GEE PLC

THIRD QUARTER REPORT FOR THE PERIOD ENDED 30-SEP-10

THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm 2009 N'm %

Change

2010 N'm 2009 N'm

% Change

Gross Earnings 3,196 3,170 0.82%

Turnover 371.082

358.831 3.4%

Profit Before Tax 300.325 359.800 -16.53%

Profit Before Tax

(42.520)

(60.794) -30.1%

Taxation (90.097) (107.940) 16.53%

Taxation 0.836

0.198 322.2%

Profit/Loss After Tax 210.227 251.860 -16.53%

Profit/Loss After Tax

(43.357)

(60.992) -28.9%

Balance Sheet Information

Retained Earnings 80.068

235.186 -66.0%

Fixed Assets 783.717

735.349 6.58%

Balance Sheet Information

Investment 4.425

5.925 -25.32%

Fixed Assets 953.556

948.746 0.5%

Stocks 44.072

30.179 46.04%

Stock 17.972

22.682 -20.8%

Trade Debtors 1,104

1,133 -2.56%

Trade debtors 82.727

232.579 -64.4% Cash and Bank Balances 152.677

367.298 -58.43%

Cash and Bank Balances 25.662

9.198 179.0%

Other Debit Balances 382.770

255.440 49.85%

Other Debit Balances 315.833

317.226 -0.4%

Trade Creditors 195.098

183.056 6.58%

Trade creditors 76.855 36.803 108.8%

Other Credit Balances 986

1,060 -6.98%

Short Term Borrowings 419.578

424.575 -1.2%

Working Capital 798.560

798.976 -0.05%

Other Credit Balances 252.750

267.269 -5.4%

Net Assets 1,290

1,283 0.55%

Working Capital

(307.029)

(146.962) 108.9% http://www.proshareng.com/investors/company.php?ref=REDSTAREX

Net Assets 646.527 -19.4%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 32

801.784

http://www.proshareng.com/investors/company.php?ref=TRIPPLEG

2nd February, 2011: UNITED NIGERIA TEXTILE PLC

3rd February, 2011: ACADEMY PRESS PLC

THIRD QUARTER REPORT FOR THE PERIOD ENDED 30-SEP-10

THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm

2009 N'm

% Change

2010 N'm 2009 N'm

% Change

Gross Earning

5,686

6,544 -13.1%

Gross Earnings 1,640

1,390 17.99%

Profit Before Tax

(945.686)

(961.393) -1.6%

Profit Before Tax 101.24

106.68 -5.10%

Taxation Nil Nil 0.0%

Taxation

(30.373)

(32.005) -5.10%

Profit/Loss After Tax

(945.69)

(961.39) -1.6%

Profit/Loss After Tax 70.871

74.678 -5.10%

Balance Sheet Information

Balance Sheet Information

Fixed Assets

3,546

3,696 -4.1%

Fixed Assets 1,031

1,059 -2.64%

Investments

28.631

23.631 21.2%

Investments 0.147

0.147 0.00%

Stock

6,932

7,042 -1.6%

Stocks 679.574

429.796 58.12%

Trade debtors

1,074

1,088 -1.3%

Trade Debtors 467.596

519.639 -10.02%

Cash and Bank Balances

1,183

1,688 -29.9%

Cash and Bank Balances 31.920

18.524 72.32%

Other Debit Balances 1,841

1,590 15.8%

Other Debit Balances 49.697 Nil 0.00%

Trade creditors 535.729

850.512 -37.0%

Trade Creditors 577.080

549.179 5.08%

Short Term Borrowings 608.198

1,057 -42.5%

Short Term Borrowings 31.032

149.633 -79.26%

Other Credit Balances

2,463

3,414 -27.9%

Other Credit Balances 996.428

751.497 32.59%

Working Capital 19.2%

Working Capital 498.430 244.23%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 33

8,318 6,981 144.797

Net Assets

3,260

4,206 -22.5%

Net Assets 655.512

568.263 15.35%

http://www.proshareng.com/investors/company.php?ref=UNTL

http://www.proshareng.com/investors/company.php?ref=ACADEMY

February 4th, 2011: Flour Mills Nigeria Plc

February 9th, 2011: Guinness Nigeria Plc

THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

SECOND QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm

2009 N'm

% Change

2010 N'm 2009 N'm

% Change

Gross Earning

122,707

117,457 4.47%

Gross Earnings 59,227

53,842 10.00%

Profit Before Tax

11,920

12,540 -4.94%

Profit Before Tax 10,792

10,534 2.45%

Taxation

(3,814)

(4,012) -45.42%

Taxation 3,453

3,350.000 3.07%

Profit/Loss After Tax

8,106

8,527 -4.94%

Profit After Tax 7,339

7,183 2.17% Balance Sheet Information

Balance Sheet Information

Fixed Assets

24,942

25,553 -2.39%

Fixed Assets 42,246

40,069 5.43%

Stocks

14,283

10,271 39.06%

Stocks 18,296

16,152 13.27%

Trade debtors

4,252

4,264 -0.28%

Trade Debtors 7,237

6,685 8.26%

Cash and Bank Balances

12,906

4,526 185.15%

Cash and Bank Balances 9,927

12,705 -21.87%

Other Debit Balances

46,646

27,417 70.14%

Other Debit Balances 6,622

2,783 137.94%

Trade creditors

3,343

7,335 -54.42%

Trade Creditors 14,677

6,946 111.30%

Short Term Borrowing

2,986

13,782 -78.33%

Other Credit Balances 38,352

37,351 2.68%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 34

Other Credit Balances 30,997 44,454 -30.27%

Working Capital 44,717

47,748 -6.35%

Working Capital 25,074 5,359 367.89%

Equity 31,299

34,199 -8.48%

Net Assets

40,074

35,384 13.25%

http://www.proshareng.com/investors/company.php?ref=GUINNESS

http://www.proshareng.com/investors/company.php?ref=FLOURMILL

9th February, 2011: ADSWITCH PLC

February 11th, 2011: UNIVERSITY PRESS PLC

SECOND QUARTER REPORT FOR THE PERIOD ENDED 31-OCT-10

THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm

2009 N'm

% Change

2010 N'm 2009 N'm

% Change

Gross Earning

22.71

100.39 -77.38%

Gross Earnings 1,472

1,616 -8.91%

Profit/Loss After Tax

(10.78)

7.60 -

241.84%

Profit/Loss After Tax 196.710

307.330 -35.99%

http://www.proshareng.com/investors/company.php?ref=ADSWITCH

Balance Sheet Information

Net Assets 1,153

1,257 -8.27%

http://www.proshareng.com/investors/company.php?ref=UPL

11th February, 2011: CHELLARAMS PLC

February 11th, 2011: NIGERIA ENAMELWARE PLC

THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

SECOND QUARTER REPORT FOR THE PERIOD ENDED 31-OCT-10

2010 N'm

2009 N'm

% Change

2010 N'm 2009 N'm

% Change

Turnover

16,849

14,152 19.1%

Gross Earnings 797.468

792.478 0.63%

Profit Before Tax

268.22

359.814 -25.5%

Profit Before Tax 46.055

48.907 -5.83%

Taxation

(51.00)

(28.50) 78.9%

Taxation

(14.738)

(15.997) 32.11%

Profit/Loss After Tax

217.22

331.314 -34.4%

Profit/Loss After Tax 31.317

32.910 -4.84%

Balance Sheet Information

Balance Sheet Information

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 35

Fixed Assets

3,190

3,081 3.5%

Fixed Assets 39.231

40.808 -3.86%

Stocks

9.316

9.316 0.0%

Stocks 566.104

355.484 59.25%

Trade debtors

1,304

976.397 33.6%

Trade Debtors 32.647

32.729 -0.25%

Cash and Bank Balances

43.518

55.148 -21.1%

Cash and Bank Balances 3.624 Nil 0.00%

Other Debit Balances 5,230 5,298 -1.3%

Other Debit Balances 319.951

998.176 -67.95%

Trade Creditors 1,387 1,535 -9.6%

Trade Creditors 5.750

21.228 -72.91%

Short Term Borrowings

338

196 72.4%

Short Term Borrowings 426.971

606.295 -29.58%

Other Credit Balances

4,445

4,323 2.8%

Other Credit Balances 263.020

564.447 -53.40%

Working Capital

(49.074)

(119.997) -59.1%

Working Capital 233.455

201.599 15.80%

Net Assets

2,984

2,836 5.2%

Net Assets 265.816

234.449 13.38%

http://www.proshareng.com/investors/company.php?ref=CHELLARAM

http://www.proshareng.com/investors/company.php?ref=ENAMELWA

February 11th, 2011: BAGCO PLC

17th February, 2011: AVON CROWNCAPS PLC

THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm

2009 N'm

% Change

2010 N'm 2009 N'm

% Change

Gross Earning

8,694

7,659 13.51%

Turnover 8,836

8,845 -0.1%

Profit/Loss After Tax

668.83

581.58 15.00%

Profit Before Tax 176.041

119.800 46.9%

Balance Sheet Information

Taxation

(82.284)

(37.133) 121.6%

Net Assets 9,941 9,766 1.79%

Profit/Loss After Tax 91.758

82.667 11.0%

http://www.proshareng.com/investors/company.php?ref=BAGCO

Balance Sheet Information

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 36

Fixed Assets 1,087

1,242 -12.5%

Stocks 3,797

5,431 -30.1%

Trade Debtors 1,500

1,543 -2.8%

Cash and Bank Balances 77.178

63.730 21.1%

Other Debit Balances 277.310

374.380 -25.9%

Trade Creditors 200.032

281.539 -29.0%

Short Term Borrowings 1,665

2,215 -24.8%

Other Credit Balances 2,913

4,289 -32.1%

Working Capital 1,342

1,198 12.0%

Net Assets 1,961

1,869 4.9%

http://www.proshareng.com/investors/company.php?ref=AVONCROWN

February 17th, 2011: IHS PLC

17th February, 2011: JOHN HOLT PLC

AUDITED REPORT FOR THE PERIOD ENDED 30-APR-10

FIRST QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm

2009 N'm

% Change

2010 N'm 2009 N'm

% Change

Gross Earnings

17,247

11,340 52.09%

Turnover 1,657

3,157 -47.5%

Profit Before Tax

675.35

1,426.00 -52.64%

Profit Before Tax

(170.00)

2.00 -8600.0%

Taxation

(121.65)

(378.72) 67.88%

Taxation

(15.00)

(15.00) 0.0%

Profit/Loss After Tax

553.71

1,047 -47.11%

Profit/Loss After Tax

(185.00)

(13.00) -1323.1%

Balance Sheet Information

Balance Sheet Information

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 37

Fixed Assets

9,164

5,201 76.20%

Fixed Assets 7,827

7,929 -1.3%

Stocks

3,762

5,876 -35.98%

Investment

8.00

8.00 0.0%

Trade Debtors

5,479

7,036 -22.13%

Stocks 3,372.00

3,861.00 -12.7%

Cash and Bank Balances

1,866

1,287 44.99%

Trade debtors

746

817 -8.7%

Other Debit Balances

6,001

4,109 46.05%

Cash and Bank Balances 109.000

113.000 -3.5%

Trade Creditors

2,141

2,011 6.46%

Other Debit Balances 1,781

1,724 3.3%

Short Term Borrowings

10,399

9,424 10.35%

Trade creditors 308.00 375.00 -17.9%

Other Credit Balances

3,155

1,869 68.81%

Short Term Borrowings 1,876

2,034 -7.8%

Working Capital

(820)

2,771 -

129.57%

Other Credit Balances 7,874

8,073 -2.5%

Net Assets

10,578

9,492 11.44%

Working Capital

(3,044)

(2,913) 4.5%

http://www.proshareng.com/investors/company.php?ref=IHS

Net Assets 3,777

3,962 -4.7%

http://www.proshareng.com/investors/company.php?ref=JOHNHOLT

February 17th, 2010: Poly Products Nigeria Plc

18th February, 2011: NESTLE NIGERIA PLC AUDITED REPORT FOR THE PERIOD ENDED 31-MAR-10

AUDITED REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm

2009 N'm

% Change

2010 N'm 2009 N'm %Change

Gross Earning

2,415.00

2,096.00 15.22%

Gross Earnings 82,726 68,317 21.09%

Profit/Loss Before Tax

83.36

77.73 191.67%

Profit Before Tax 18,244 13,783 32.37%

Taxation

(22.70)

(19.43) 44.11%

Taxation (5,642)

(3,999) -48.31%

Profit/Loss After Tax

60.67

58.30 4.06%

Profit/Loss After Tax 12,602

9,783 28.82%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 38

Balance Sheet Information

Balance Sheet Information

Fixed Assets

781.940

520.810 50.14%

Fixed Assets 40,241 25,404 58.40%

Stock Short Term Invest

368.612

203.614 81.03%

Stock 8,494 10,697 -20.59%

Trade debtors

321.279

247.687 29.71%

Trade Debtors 4,970 1,951 154.74%

Cash and Bank Balances

14.117

72.533 -80.54%

Cash and Bank Balances 3,092

3,664 -15.61%

Other Debit Balances

198.700

46.706 325.43%

Other Debit Balances 3,548

5,533 -35.88%

Trade creditors

519.790

370.987 40.11%

Trade creditors 4,085 4,114 -0.70%

Short Term Borrowing

41.444

50.836 -18.48%

Short Term Borrowing 3,398

4,900 -30.65%

Other Credit Balances 773.087

360.668 114.35%

Other Credit Balances 37,997

27,692 37.21%

Working Capital 33.540

(113.789)

-129.48%

Working Capital 650.024

(165.212) -493.45%

Net Assets

350.327

308.859 13.43%

Net Assets 14,865 10,543 40.99%

http://www.proshareng.com/investors/company.php?ref=POLYPROD

http://www.proshareng.com/investors/company.php?ref=NESTLE

22nd February, 2011: GREAT NIGERIA INSURANCE PLC

24th February 2011: VITAFOAM NIGERIA PLC

THIRD QUARTER REPORT FOR THE PERIOD ENDED 30-SEP-10

FIRST QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm

2009 N'm

%Change

2010 N'm 2009 N'm

% Change

Turnover

1,471

1,305 12.7%

Gross Earnings 3,259

2,504 30.15%

Profit Before Tax and Extra-ordinary Items

40.703

31.501 29.2%

Profit Before Tax 351.940

292.320 20.40%

Exceptional Items Nil

(1,993) 0.0%

Taxation

(111.517)

(94.504) 18.00% Taxation 0.0%

Profit/Loss After 240.424 21.54%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 39

(11.636) (11.636) Tax 197.817

Profit/Loss After Tax

29.066

(1,973) 101.5%

Balance Sheet Information

Balance Sheet Information

Fixed Assets 1,708

1,686 1.30%

Fixed Assets

634.907

666.826 -4.8%

Investments

231

201 14.86%

Stocks

721.637

713.434 1.1%

Stocks 2,281

2,145 6.34%

Trade Debtors

706.826

238.356 196.5%

Trade Debtors 864.550

745.838 15.92%

Cash and Bank Balances

78.035

207.003 -62.3%

Cash and Bank Balances 576.230

431.705 33.48%

Other Debit Balances

4,829

4,755 1.6%

Other Dedit Balances 1,416

915.844 54.61%

Trde Creditors

1,370

1,015 35.0%

Trade Creditors 1,247

798.580 56.15%

Insurance Funds 714.023 575.611 24.0%

Short Term Borrowings 1,137

1,162 -2.15%

Other Credit Balances

1,314

1,206 9.0%

Other Credit Balances 1,939

1,666 16.39%

Net Assets

4,286

4,358.000 -1.7%

Working Capital 2,937

1,654 77.57%

http://www.proshareng.com/investors/company.php?ref=GNI

Net Assets 2,736

2,499 9.48%

http://www.proshareng.com/investors/company.php?ref=VITAFOAM

February 25th, 2010: NAMPAK PLC

25th February, 2010: NEIMETH INTL PHARMACEUTICALS PLC

FIRST QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-DEC-10

2010 N'm

2009 N'm

% Change

2010 N'm 2009 N'm

% Change

Gross Earning

1,090.00

1,146.00 -4.89%

Turnover 1,312

1,353 -3.0% Profit Before Tax 0.71%

Profit Before Tax -149.7%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 40

107.77 107.00 (27.249) 54.817

Taxation

(34.49)

(34.24) 0.72%

Taxation Nil

(17.541) 0.0%

Profit/Loss After Tax

73.28

72.76 0.71%

Profit/Loss After Tax

(27.249)

37.275 -173.1%

Balance Sheet Information

Balance Sheet Information

Fixed Assets

750.51

738.36 1.65%

Fixed Assets 440.134

342.819 28.4%

Stocks

806.22

979.41 -17.68%

Investments 76.757

76.757 0.0%

Trade Debtors

379.85

536.16 -29.15%

Stocks

972

1,054 -7.8%

Cash and Bank Balances

179.03

43.87 308.10%

Trade debtors 1,349

1,464 -7.9%

Other Debit Balances

82.68

163.65 -49.48%

Cash and Bank Balances 216.520

70.348 207.8%

Trade Creditors

638.27

571.38 11.71%

Other Debit Balances 661.201 688.729 -4.0%

Short Tterm Borrowing 61.33 348.47 -82.40%

Trade Creditors 306.492 233.651 31.2%

Other Credit Balances 790.73 237.36 233.14%

Short Term Borrowings 228.671

196.754 16.2%

Working Capital 54.22 -2.56

-2216.12

%

Other Credit Balances 1,633

1,404 16.3%

Net Assets 707.96 639.03 10.79%

Working Capital 907.061

940.111 -3.5%

http://www.proshareng.com/investors/company.php?ref=NAMPAK

Net Assets 923.744

950.740 -2.8%

http://www.proshareng.com/investors/company.php?ref=NEIMETH

February 28th, 2011: NIGERIA ENAMELWARE PLC THIRD QUARTER REPORT FOR THE PERIOD ENDED 31-JAN-11

2011 N'm

2010 N'm

% Change

Gross Earnings 0.49%

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 41

1,832 1,823

Profit Before Tax

73.559

70.227 4.74%

Taxation

(23.539)

(22.473) -4.74%

Profit/Loss After Tax

50.020

47.754 4.75% Balance Sheet Information

Fixed Assets

38.805

40.808 -4.91%

Stocks

444.705

355.484 25.10%

Trade Debtors

38.457

32.729 17.50%

Cash and Bank Balances

27.846 Nil 0.00%

Other Debit Balances

346.928

998.176 -65.24%

Trade Creditors

1.327

21.228 -93.75%

Short Term Borrowings

350.175

606.295 -42.24%

Other Credit Balances

260.720

564.447 -53.81%

Working Capital

252.316

201.599 25.16%

Net Assets

284.519

234.449 21.36% http://www.proshareng.com/investors/company.php?ref=ENAMELWA

Forecast Result in the Month

DECLARED FORECASTS FOR FEBRUARY 2011

Company Year End Period

Gross Earnings in N' billion

PAT in N'

billion Stanbic IBTC Bank Plc December Q1 2011 15.518 2.564

Neimeth Int'l Pharm Plc March Q4 2011 2.058 0.95 Equity Assurance Plc March Q4 2011 1.000 0.139

Chams Plc December Q1 2011 2.507 1.631 Livestock Feeds Plc December Q1 2011 0.78 0.31 Oceanic Bank Plc December Q1 2011 25.492 0.41

Royal Exchange Plc December Q1 2011 1.075 0.13 Starcomms Plc December Q1 2011 9.698 -2.027

Intercontinental Wapic Insurance Plc December Q1 2011 1.660 0.19 Eterna Oil Plc December Q1 2011 4.088 0.211 DN meyer Plc December Q2 2011 0.554 0.16

Interlinked Technologies Plc December Q2 2011 0.343 0.4 Interlinked Technologies Plc December Q4 2011 0.855 0.116

Nestle Nigeria Plc December Full Year 87.267 9.865 C & I Leasing Plc January Q4 2011 9.466 0.255

Nigeria German Chemical Plc April Q4 2011 0.855 0.116 Dangote Flour Mills Plc December Q1 2011 13.848 0.865

Alumaco Plc December Q1 2011 0.206 0.6 Nampak Plc September Q3 2011 3.652 0.265

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 43

Dividends Declared

DIVIDENDS DECLARED FEBRUARY 2011

Company Dividend Declared

Bonus Declared AGM Date Price Adjustment Date

Fidson Healthcare Plc 10kobo 23-Feb-11 3rd - 8th Feb, 2011

Poly Products Plc 30-Mar-11 16th - 30th Mar, 2011 Nestle Nig Plc 10.60kobo 1 for 5 26-Apr-11 18th – 22nd April 2011

IHS Nig Plc 6kobo 29-Mar-11 11th – 15th March

2011

Nigeria Breweries Plc N1.25kobo 18-May-

11 17th – 23rd March

2011 Outlook/Analyst Opinion The trend in the month of February was bearish, characterised with high speculative tendency and series of selling activities on the back of profit taking as presumed.

The prolonged bearish sentiments technically revealed that profiteering could not be the only reason for persistent selling as low commitment and enthusiasm coupled with absence of will to drive active bargain were major obvious factors aside the existing low liquidity issue.

More so, the long delay in the announcement of corporate results in the most active sector of the market contributed immensely to low enthusiasm witnessed in the month as Investors’ expectation remained high in terms of rewards from the sector.

Although, the influx of Federal and state bonds in the market reduced the expected liquidity inflow into the capital market as investors seek risk aversion, which further revealed low confidence level in the market.

However, we are of the opinion that the prolonged bearish sentiments in the last four consecutive weeks is technically providing a window for value investors who will take advantage of low price for mid-long term positions, though market is presently in a bearish mode but a reversal is much possible anytime soon as earnings report from banking sector is likely to ignite the expected sentiments to drive trend reversal.

In addition, we foresee growing liquidity level and increased positive volume turnover in the capital market, all things being equal, as we move closer to general election period while we expect MPR to remain unchanged.

We therefore remained cautiously optimistic about the trend reversal in the coming weeks as we anticipate positive change in the commitment level on heels of good earnings report and improved liquidity level.

Finally, the strict posture of the management of NSE is considered to be right thinking in a right direction to renew the lost/low investors’ confidence and we believe that charting

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 44

a new course and desire for new world class market environment in a transparent manner will drive full market recovery.

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 45

Time Lines - (News/Information in the month and Reaction of Market)

Date Timelines Gainers

Losers ASI and Market Capitalisation Remarks

Feb 1 LSE Lists Nigeria’s $500m Bond- The Nigerian corporate image at the international capital market came alive yesterday as the London Stock Exchange (LSE) admitted the country’s first sovereign $500 million bond for trading on the exchange’s main market.

Investors dump shares to position for rising interest rates- Stock market in further N168 billion loss •Cost of borrowing expected to rise Financial markets were caught in a two-way pull following last week's increase in benchmark rates by the Central Bank of Nigeria (CBN) to 6.5 percent.

Experts predict improved market indicators this week- Analysts have predicted that there will be significant improvement in major market indicators towards the end of this week.

16 39 At the close of trading session, the NSE All-Share Index dropped further by -0.40% to close at 26,723.49 as against a dip by -1.92% recorded previous session to close at 26,830.67. In the same vein, market capitalization moved down by N34.25billion (US$232.16 million) to close at N8.54 trillion (US$57.88billion) as against depreciation by N168.09billion (US$1.13billion) recorded on preceding session to close at N8.57 trillion (US$58.12 billion).Market report for the day was titled: : Market breadth remains negative as bears tightened grip(http://www.proshareng.com/news/singlenews.php?id=13004)

Feb 2 CBN: Banks No Longer Threat to Economy - The CBN said Tuesday that the banking system no longer posed any systemic risks to the nation’s economy as a result of the ongoing reforms in the industry.

NSE’s market capitalization slides further by N30b - Transactions on the floor of the NSE, yesterday, sustained its downward trend, as more highly capitalized companies continued to suffer price depreciation, resulting to a further slide in market capitalization by N30 billion.

Analysts optimistic about foreign exchange derivative products - The move by the CBN to introduce derivative foreign exchange products will eventually allow for a more stable national currency.

39 23 At the close of trading session, the NSE All-Share Index gained by 0.77% to close at 26,928.67 as against a dip by -0.40% recorded previous session to close at 26,723.49. In the same vein, market capitalization moved up by N65.57billion (US$444.45 million) to close at N8.60 trillion (US$58.33billion) as against depreciation by N34.25billion (US$232.16million) recorded on preceding session to close at N8.54 trillion (US$57.88 billion). Market report for the day was titled: Market regains breadth on renewed bargain tendency as Spring bank Plc leads gainers’ chart(http://www.proshareng.com/news/13012)

Feb 3 Regulators resolution to determine minority investors’ expectations - 29 30 At the close of trading session, the NSE All-Share Index droped by -0.12% to close at 26,895.35 as

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 46

Despite the fact that the NSE interim administrator, Emmanuel Ikazoboh, had

noted that the move by the NBC to delist was in good faith based on the

letter/report sent to the Exchange, minority investors’ attitude over the proposal

seems not unchanged, especially with their unwillingness to dispose off the shares

of the company.

Investors swing positions to maximize returns - Uncertainty in the investment

clime may be pushing investors to opt for more secured investment instruments.

Some investment advisory firms have been encouraging their clients to switch to

money market instrument in order to secure their investment and enjoy more

returns.

Questions raised over MoU terms for rescued banks - The banking industry

and some top executives of the rescued banks are currently engaged in intense

struggle to agree on a share ownership structure with their potential buyers as they

prepare to sign their MoU.

against an upbeat by 0.77% recorded previous session to close at 26,928.67. In the same vein, market capitalization moved down by N10.64billion (US$72.17 million) to close at N8.59 trillion (US$58.26billion) as against appreciation by N65.57billion (US$444.45million) recorded on preceding session to close at N8.60 trillion (US$58.33 billion). Market report for the day was titled: NSE ASI pulls back by -0.12% as banking sector records sell volume(https://www.proshareng.com/news/13015)

Feb 4 Agenda for NSE DG designate- After months of shopping for a new head for the Nigerian Stock Exchange, the Council of the bourse, in conjunction with the Securities and Exchange Commission, has settled for Oscar Onyeama as the substantive Chief Executive.

Nigeria’s economy will surge from third quarter- The Nigerian economy will experience a surge in the third and fourth quarter of this year as the country begins to put behind her the aftermath of the April elections. The economy sectors that would generate significant interest are the equities market and the property development sector.

UBA Asset Management predicts ‘significant growth’ this year- NIGERIAN economy will witness “significant growth and stability” in 2011 despite growing concern across the country.

31 25 The All-Share Index in the week under review dropped by -2.17% to close at 26,763.84 as against a decline by -1.18% recorded last week to close at 27,365.59.

In the same vein, the market capitalization in the week depreciated by N189.45 billion (US$1.28 billion) to close at N8.55 trillion (US$ 57.97billion) as against depreciation of N104.77billion (US$710.10million) recorded last week to close at N8.74 trillion (US59.25 billion). Market report for the week was titled: Bearish sentiments persist as YTD Market performance settles lower at 6.62%(https://www.proshareng.com/news/13020 )

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 47

Feb 7 Recapitalization: Stockbrokers scramble for more funds - Stockbroking firms that were recently suspended by the NSE as a result of inadequate capital are intensifying moves to increase their capital base.

Bond prices to remain stable – Analysts - Analysts at the Financial Derivatives Company Limited have said they expect bond prices to remain stable until the interest rates increase in March.

Interbank rates climb on cash shortage - Nigerian interbank lending rates climbed to 8.00% on average last week, from 5.0% the previous week, as expectations of cash withdrawals by the state-run energy firm NNPC prompted market hedging.

20 34 At the close of trading session, the NSE All-Share Index dropped by -0.34% to close at 26,672.57 as against a decline by -0.49% recorded previous session to close at 26,763.684. In the same vein, market capitalization moved down by N29.17billion (US$197.70 million) to close at N8.52 trillion (US$57.77billion) as against depreciation by N42.03billion (US$284.88million) recorded on preceding session to close at N8.55 trillion (US$57.97 billion). Market report for the day was titled: Sell traders maintain position as NSE ASI slides further by -0.34% (https://www.proshareng.com/news/13031)

Feb 8 SEC set to end ‘one-size-fits-all’ code of corporate governance - SEC has

said the new/revised code of corporate governance for quoted companies slated for

April will end the era of ‘one-size-fits-all’ rules that have been existing since 2003.

NSE, vendors to conclude cost negotiation for new trading platform next

month -Negotiation for a new trading platform for the NSE is to be concluded on or

before the end of next month.

‘Merger not an immediate solution for capital base' - While there are

indications that some stockbroking firms are in merger talks following their inability

to meet the new capital base, some market operators believe that the option of

merger is not the solution.

18 39 At the close of trading session, the NSE All-Share Index dropped by -0.97% to close at 26,413.26 as against a decline by -0.34% recorded previous session to close at 26,672.57. In the same vein, market capitalization moved down by N82.88billion (US$561.71 million) to close at N8.44 trillion (US$57.21billion) as against depreciation by N29.17billion (US$197.70million) recorded on preceding session to close at N8.52 trillion (US$57.77 billion). Market report for the day was titled: Sentiments remain unchanged as NSE ASI hits 20days low (http://www.proshareng.com/news/singlenews.php?id=13037)

Feb 9 SEC prohibits directors, family members from dealing in their companies’

securities - As part of the effort to check the reoccurrence of insider dealing on

the NSE, the new code of corporate governance released yesterday by SEC

prohibits directors of public companies and their immediate families from dealing in

their securities

Banks make fresh moves to divest from non-banking subsidiaries -

23 33 At the close of trading session, the NSE All-Share Index gained by 1.03% to close at 26,685.30 as against a decline by -0.97% recorded on previous session to close at 26,413.26. In the same vein, market capitalization moved up by N86.94billion (US$589.27 million) to close at N8.52 trillion (US$57.80billion) as against depreciation by N82.88billion (US$561.71million) recorded on

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 48

Indications have emerged that some DMBs that have not complied with the CBN’s

directive on divestment from non-banking subsidiaries under the new banking

regime have started fresh moves to comply

Why NBC is delisting 1.3bn shares – SEC - SEC has given reasons why NBC is

delisting its shares valued at N50.33 billion from the trading floor of the NSE.

preceding session to close at N8.44 trillion (US$57.21 billion). Market report for the day was titled: NSE ASI turns green as market giant upbeats by 4.92%(http://proshareng.com/news/singlenews.php?id=13043)

Feb 10 Shareholders’ group blames regulators for slow recovery of capital market- THE Independent Shareholders Association of Nigeria (ISAN) has blamed the regulatory authorities for the slow pace of recovery of the Nigerian capital market.

NSE’s market capitalisation rises by N87 billion- DESPITE price losses that outweighed gains, the bulls upstaged the bears yesterday on the trading floor of the Nigerian Stock Exchange (NSE), as major blue chip stocks recorded price appreciation, resulting to an increase in market capitalisation by N87 billion.

How to attract more firms to NSE, by GTI Capital- EXECUTIVE Director, GTI Capital, Ola Ogedengbe, yesterday, advised the Securities and Exchange Commission (SEC), to carry out what he identified as “detail research” on why several medium and large scale firms in Nigeria are not willing to list their shares on the floor of Nigerian Stock Exchange (NSE).

25 31 At the close of trading session, the NSE All-Share Index dropped by -0.29% to close at 26,607.98 as against an upbeat by 1.03% recorded previous session to close at 26,685.30. In the same vein, market capitalization moved down by N24.71billion (US$167.48 million) to close at N8.50 trillion (US$57.63billion) as against appreciation by N86.94billion (US$589.27million) recorded on preceding session to close at N8.52 trillion (US$57.80 billion). Market report for the day was titled: : Nigerian Capital Market resumes southward trend as Julius Berger Plc leads decliners(http://proshareng.com/news/singlenews.php?id=13049)

Feb 11 Survival of operators under test as SEC ups capital base by 2,400% -

Market operators in Nigeria have to prove their preparedness to face the emerging

competitions with their peers from other market as SEC jacks up the capitalization

requirement by over 1,000%.

More Stockbrokers Comply on N70m Capital Base -More stockbroking firms

have resumed trading on the floors of the NSE having complied with the N70 million

minimum capital stipulated by SEC.

SEC: Foreign Investment Hits N381bn – SEC said Thursday, that the lasting

solution to Nigeria’s huge infrastructure deficit was to continue to grow the capital

market to a world class standard, such that the needed funds could be optimally

raised from it. SEC pointed this out, as it also revealed that the total foreign

29 21 The All-Share Index in the week under review dropped by -0.30% to close at 26,684.49 as against a decline by -2.17% recorded last week to close at26,763.84.

In the same vein, the market capitalization in the week depreciated by N25.36 billion (US$171.88 million) to close at N8.52 trillion (US$ 57.80billion) as against depreciation of N189.45billion (US$1.28billion) recorded last week to close at N8.55 trillion (US57.97 billion). Market report for the week was titled: : Market records N346.99 billion loss in 15days as bearish sentiments persist.( http://proshareng.com/news/13059)

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 49

portfolio investment in 2010 in the country through the nation’s capital market was

N381.34 billion, which accounted for 48% of the aggregate turnover value.

Feb 14 NSE: Analysts predict improved activities this week- In the face of significant

losses recorded in the NSE within the last three weeks; analysts have said that

there may be improved activities this week.

Banks in Liquidity Drain amid Tight Policy - The opening balance of banks at

the interbank naira market, which is a key measure of the liquidity of the system,

crashed at the weekend to about N15 billion from N124 billion the previous week.

Mixed reactions trail SEC’s move to slash stockbroking firms - Discordant

tunes have continued to trail SEC’s move to prune the number of stockbroking

firms operating in the Nigerian Capital Market.

19 32 At the close of trading session, the NSE All-Share Index dropped by -0.32% to close at 26,598.41 as against an upbeat by 0.29% recorded previous session to close at 26,684.49. In the same vein, market capitalization moved down by N27.51billion (US$186.47 million) to close at N8.50 trillion (US$57.61billion) as against appreciation by N24.45billion (US$165.74million) recorded on preceding session to close at N8.52 trillion (US$57.80 billion). Market report for the day was titled: NSE ASI remains weak, trading below its 20days moving average (https://www.proshareng.com/news/singlenews.php?id=13071)

Feb 16 SEC pledges commitment to IFRS adoption- DIRECTOR-GENERAL of Securities and Exchange Commission (SEC), Arunma Oteh, has reinstated the commission’s commitment to the adoption of International Financial Reporting Standards (IFRS) fixed for 2012 in Nigeria.

Rising Rates Take Toll on FGN Bonds- Rising interest rates appear to be hampering efforts by the Federal Government of Nigeria to deepen the bond market, as investors are reducing their stake in the securities at the secondary market.

NSE to Enforce Rules on Compliance Officers- More stockbroking firms stand the chance of losing businesses as the Nigerian Stock Exchange (NSE) prepares to enforce its rule concerning compliance officers who are required to ensure full compliance with all NSE requirements.

14 46 At the close of trading session, the NSE All-Share Index dropped by -0.49% to close at 26,468.58 as against a decline by -0.32% recorded previous session to close at 26,598.41. In the same vein, market capitalization moved down by N41.49billion (US$281.22 million) to close at N8.45 trillion (US$57.33billion) as against depreciation by N27.51billion (US$186.47million) recorded on preceding session to close at N8.50 trillion (US$57.61 billion). Market report for the day was titled: Market CAP dips further by N41 billion as downward trend gains momentum.(http://www.proshareng.com/news/13079)

Feb 17 CBN Now to Approve Top Positions in Banks- Unlike in the past when banks were solely left to take decisions concerning the appointment of senior management officers, the Central Bank of Nigeria (CBN) Wednesday said such appointments would now be subject to its approval.

Banks’ full year, other earnings release to moderate selling pressure-

30 23 At the close of trading session, the NSE All-Share Index gained by 0.60% to close at 26,627.29 as against a decline by -0.49% recorded previous session to close at 26,468.58. In the same vein, market capitalization moved up by N50.72billion (US$343.79 million) to close at N8.51 trillion

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 50

Hindsight of a robust 2010 fourth quarter financial report by banks and other quoted firms is impacting positively on the performance indicators of the secondary market at the Nigerian Stock Exchange (NSE).

More stockbrokers join NSE’s 235 remote trading connections in Lagos- THE use of remote trading by dealing firms has continued to gain acceptance, as there are 235 remote trading connections in Lagos, besides those deployed in branches across the country.

(US$57.68billion) as against depreciation by N41.49billion (US$281.22million) recorded on preceding session to close at N8.45 trillion (US$57.33 billion).Market report for the day was titled: NSE ASI rebounds as sell pressure wanes(https://proshareng.com/news/singlenews.php?id=13083)

Feb 18 Code of corporate governance will be effective from April – SEC- The Securities and Exchange Commission has said the newly approved code of corporate governance for public companies will be effective from April 1, 2011.

AMCON’ll not give more funds to DMBs – Chike-Obi- The Asset Management Corporation of Nigeria will not give additional money to the rescued Deposit Money Banks aside from the five per cent of the original value of unsecured loans it pays to them, the Managing Director, AMCON, Mr. Mustapha Chike-Obi, has said.

Market operators urge investors to trade cautiously- Some market operators have urged investors to trade cautiously following the recent growth in transaction volume at the Nigerian Stock Exchange (NSE), despite the wobbly market performance.

28 33 The All-Share Index in the week under review dropped by -0.17% to close at 26,639.35 as against a decline by -0.30% recorded last week to close at26,684.49.

In the same vein, the market capitalization in the week depreciated by N14.42 billion (US$97.78 million) to close at N8.51 trillion (US$ 57.70billion) as against depreciation of N25.36billion (US$171.88million) recorded last week to close at N8.52 trillion (US57.80 billion). Market report for the week was titled: Market CAP dips further by N14billion for the week as Nestle Plc grows PAT 28.8%.(http://www.proshareng.com/news/singlenews.php?id=13097)

Feb 21 Suspension: Brokers Seek Dialogue with SEC- The leadership of the stockbroking community in the nation’s capital market will this week meet with the management of the Securities and Exchange Commission (SEC) and Nigerian Stock Exchange (NSE) over the suspension of brokering houses and planned consolidation.

CBN partners NASB for IFRS adoption-THE Central Bank of Nigeria (CBN) has declared its resolve to collaborate with the Nigerian Accounting Standards Board (NASB) in ensuring banks in Nigeria comply with International Financial Reporting Standards (IFRS) in the preparation of their financial statements

38 25 At the close of trading session, the NSE All-Share Index gained by 0.26% to close at 26,709.32 as against an upbeat by 0.05% recorded previous session to close at 26,639.35. In the same vein, market capitalization moved up by N22.36billion (US$151.57 million) to close at N8.53 trillion (US$57.85billion) as against appreciation by N3.85billion (US$26.12million) recorded on preceding session to close at N8.51 trillion (US$57.70 billion). Market report for the day was titled: Equity Market sustains uptrend by 0.26% as Nestle Plc leads gainers’

The Monthly NCM Report for Feb 2011 www.proshareng.com Page 51

Margin loans: Stockbrokers express divergent views over AMCON’s intervention – Ahead of the meeting with the AMCON (today), stockbrokers have expressed divergent views on the outcome of the discussions, especially as regards the modalities for acquiring margin loans.

chart(http://www.proshareng.com/news/singlenews.php?id=13114)

Feb 22 Investors urged to ‘take position’ ahead of companies’ results - Investors in the capital market have been urged to take position in good stocks on the NSE ahead of the release of some companies’ f

FDI: Stanbic IBTC set to host investors, corporate managers - Stanbic IBTC Bank Plc and its stockbroking subsidiary, Stanbic IBTC Stockbrokers Limited, have concluded arrangements to host institutional investors keen on making forays into the Nigerian economy through stake holdings in leading quoted firms on the NSE. financial results.

CBN governor rejects IMF advice to devalue naira - CBN Governor, Lamido Sanusi, yesterday rejected the advice by the IMF to weaken the naira, saying the currency is not overvalued.

26 28 At the close of trading session, the NSE All-Share Index gained by 0.14% to close at 26,747.04 as against an upbeat by 0.26% recorded previous session to close at 26,709.32. In the same vein, market capitalization moved up by N12.05billion (US$81.70 million) to close at N8.54 trillion (US$57.93billion) as against appreciation by N22.36billion (US$151.57million) recorded on preceding session to close at N8.53 trillion (US$57.85 billion). Market report for the day was titled: Market CAP gains N89billion in four days on continued moderate buying(http://www.proshareng.com/news/singlenews.php?id=13120)

Feb 23 SEC, stakeholders plan alternative market - Plans are in the offing to offer

investors alternative windows for building wealth to complement the NSE, as the

Nigerian Association of Securities Dealers (NASD) and SEC are in top discussions to

set up the OTC market.

NSE Moves Closer to Global Membership - The renewed efforts by the NSE to

enforce its rules and the appointment of a new CEO are said to have attracted

favourable review from the World Federation of Exchanges (WFE) thus brightening

the Exchange’s chance of early admission into the g

AMCON Plans Second Phase of Asset Purchase - AMCON Tuesday said it is