Monthly Economic Insight - media.tmbbank.com

31

Classification: Confidential (C-3) Monthly Economic Insight Prepared by TMB Analytics Date: 18 October 2017

Transcript of Monthly Economic Insight - media.tmbbank.com

Classification: Confidential (C-3)

Monthly Economic Insight

Prepared by TMB Analytics

Date: 18 October 2017

Executive Summary

▪ Global economic outlook was brightened up by strong growth among large economies leading

by US, EU and Japan. Additionally, global trades looked robust as shown in strong exports in

many countries, including Thailand. However, the China services sector started to show sign of

slower pace of expansion from downbeat PMI index (from 52.7 to 50.6).

▪ In August, Thai economic recovery has continued to broaden and gain momentum, buoyed by

growing export of goods and improving private demands.

▪ Private consumption continued to expand moderately, supported by strong growth in services.

Private investment expanded, though remained tepid, mainly from equipment investment.

▪ August exports continued expanding at 13.2% mainly due to trading partners’ economic

recovery. For the fist eight months of 2017, it grew by 9%, the highest growth rate in 6 years.

Export to all markets expanded constantly, and most of export products registered positive

growth. On import side, it grew by 14.9% in August. For the first eight months it grew by 15.4%

owing to an increase in both energy and export-related products.

-2-

Executive Summary

▪ Manufacturing production increased 3.7%yoy in August, export as key of growth, stronger

production from vehicle and part, electronics, rubber product and chemicals. Entrepreneurs

sentiment improve for the first time in five months from new orders both domestic and

export markets. However, most firms continued to be concern about currency appreciation.

▪ Number of foreign tourists were 3.13 million (+9%yoy). 8M17, arrivals recorded 23.5 million

(+5%yoy). Chinese has been and still is top source with 28% market shares. Positive

Drivers included more airlines link from sources market (China, Taiwan, Indonesia, India

and Turkey) to Thailand.

▪ September inflation rate increased to 0.9% from higher prices of energy, tobacco and

alcoholic drinks from excise tax reform, and some fresh food in flooded area.

▪ Year-to-date, Thai baht appreciated against the USD by 8.3% (strongest in Asian) due to

geopolitical risk over Korean peninsula, uncertainty over Fed’s rate hike outlook and strong

current account surplus (from exports of goods and services). However, major central

banks could start to tighten monetary policies which could boost fund outflows from

Thailand. For the rest of 2017, the dollar is expected to trade within ranges of 32.80-33.30

THB/USD.-3-

Classification: Confidential (C-3)

Economic Updates

Updates on Global Economy

Updates on Thai Economy

Classification: Confidential (C-3)Classification: Confidential (C-3)

Global Economy

-6-Source: IMF, Various Central Banks, Bloomberg, and TMB Analytics’ projection

Developed Economies Keep Expanding

Manufacturing in US and EU expand faster

2.22.1

2.0 1.8

-1.0

0.0

1.0

2.0

3.0

2011 2012 2013 2014 2015 2016 2017 2018

Services continue to grow with acceleration

US Real GDP growth YoY

EU Real GDP growth YoY

Real GDP growth outlook

%

45

50

55

60

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

US Manufacturing PMI

EU Manufacturing PMI

45

50

55

60

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

US services PMI

EU Services PMI

↑ Expansion

↓ Contraction

↑ Expansion

↓ Contraction

45

50

55

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

45

50

55

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

6.76.5

1.51.2

-1.0

0.0

1.0

2.0

3.0

6.0

7.0

8.0

9.0

10.0

2011 2012 2013 2014 2015 2016 2017 2018

-7-Source: IMF, Various Central Banks, Bloomberg, and TMB Analytics’ projection

Asian Economies Also Keep Growing

Japan Manufacturing expand rapidly Services sectors still grow in China and Japan

China Real GDP growth YoY

Japan Real GDP growth YoY

%

Japan Manufacturing PMI

China Manufacturing PMI*

China services PMI*

Japan Services PMI

↑ Expansion

↓ Contraction

China PMI* from Caixin

Real GDP growth outlook

-8-

EU Political Uncertainty

Delayed

Trumponomics

CB Ready to

Tighten Policy

Robust Thai

Economic growth

EM Fund Flows

THB

IN OUTIN

Bullish Bearish

Likelihood

Severity*

High Medium

Source: TMB Analytics

*Impact to financial market

Medium

IN

What Does Matter in 2017: Key Events to Keep Eyes on

Medium

1H2017 2H2017

UK trigger Article

50 German

Election

French

Election

-9-

Theresa May

failed to win

majority in

parliament (317/650 seats)

UK

ElectionItaly

Election

1Q2018

“Bye Bye EUSee you (Softer)Hard Brexit”

“En Marche!” (Forward!)

“Progressive Movement”

Emmanuel Macron beat Marine Le Pen in presidential election

and won 350/577 seats in parliament

Angela Merkel’s

CDU/CSU* party is

facing a new

challenge to form

3-way coalition

with FDP and Green

5 stars movement

party is losing popularity

Dutch

Election

Mark Rutte beat

Geert Wilders,

destroyed hope for Nethexit

*CDU = Christian Democratic Union of Germany

*CSU = Christian Social Union in Bavaria

Renewed Concerns Over German Election Result

September 24

-10-

Funding

Source: Bloomberg, ING, GovTrack, RealClearPolitics, FlatIcon, CBO, Wikipedia, and TMB Analytics

“39% of R-Congress are very Conservative … They will oppose my great plans !!!”

Trumpcare

Delayed!!

Tax Reform Infrastructure

Will also be Delayed!!

+0.3 Trillion USD over 10 years

Border

Adjustment Tax

-1 Trillion USD over 10 years

-1.2 Trillion USD over 10 years

+1.0 Trillion USD over 10 years

Trumponomics Likely Brings Disappointment This Year

Trump’s great stimulus plan timelines will be extended longer than market’s expectations as Healthcare reforms was delayed indefinitely.

-11-Source: Fed, BoJ, ECB, Bloomberg and TMB Analytics

Short-term rate: Fed Fund

Dovish Hawkish

Short-term rate: Refin RateDovish Hawkish

Short-term rate: PR-BalancesDovish Hawkish

2H/2017 1H/2018 2H/2018

FED

BOJ

ECB

1 Rate Hike 1 Rate Hike 1 Rate Hike

Start B/S run-off

$ -10 bn $ -20 bn $ -30 bn $ -40 bn $ -50 bn

0 Rate Hike 0 Rate Hike 1 Rate Hike

Start QE Tapering

EUR 60 bn EUR 40 bn

0 Rate Hike 0 Rate Hike 0 Rate Hike

Start QE Tapering

JPY 80 Trillion / year

EUR 20 bn

JPY 60 Trillion / year JPY 40 Trillion / year

ECB’s QE Tapering “Judgement Day” in October

“Real Game Changer”

-100

-50

0

50

100

150

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

ST Bonds (TTM < 1y) LT Bonds Net Equity Foreign Flows

-12-Source: Bloomberg, CEIC and TMB Analytics, As of Oct 2017

bn.THB

Allocations move from

DM to EM; debt to

equity as Brexit and Fed hike delay

EM outflows

from fear of

trade protectionism

Inflows to EM

from unclear Trumponomics

YTD Net Inflows = 298.8 bn. THB

Equity = 14.6 bn. THB (5%)Bond = 284 .2bn. THB (95%)

-3

8

18

28

38

South Korea China Indonesia Thailand Phillippines Malaysia

Equity Bond

bn.USD

Thailand

If Bond Rout is Coming … Risk of Fund Flow Reversal ? Foreign fund continuously flows into Thailand as US election reflected higher risk appetite

Asian Bonds: The dearest destiny of “Foreign” Investors

10

38

0

10

20

30

40

2015 2016 2017YTD

%Bond Outright Trading Activity

Fading’s Fed’s Hike probability

-2.0

-1.0

0.0

1.0

2.0

3.0

-10

-6

-2

2

6

10

14

-13-

THBBillion USD

BoP = Net Demand for THB

Net

Export

Goods

16%

Net

Export

Services

33%

Foreign net

buy 10%

FDI 10%

Thai net buy

18%

TDI

13%

Q1/2017 Source: BoT, CEIC, MoC and TMB Analytics; as of Sep 2017

2018 Outlook

Surplus

Deficit

Continual expansion of Thai tourism

Increasing EPS growth of listed firms

EEC, BOI attract more investment

No More Robust Trade Surplus

Brightening outlook of Foreign Investment Fund Industry

Growing economy lures more investments from Thai firms

Going Forward: Rising Balance of Payment Is Expected

BoP typically governs

THB’s direction

Source: CEIC and TMB Analytics; as of Sep 2017 -14-

Robust Thai economy

30

31

32

33

34

35

36

37

38

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2018Q1 2018Q2

2 Hikes & Robust Thai Economy

USDTHB 2010

USDTHB 2017

33.30period-end2017

32.50period-end2018

▪ 2 Fed’s rate hikes

▪ Continual fund

inflows

Geopolitical Risks

CB’s tightening monetary policies

Pro-growth Trumponomics

GDP

“Strong” THB Factors “Weak” THB Factors

Domestic Fundamentals Lessen External Impacts

1 Fed Hikes and

B/S reduction in December 2017

Macron won

French election

ECB’s

unintentionally

signalQE tapering?

Trump started presidency term

Fed hiked

policy rate by 25bps

-15-

Stronger Fundamental Self-Support Currencies Against USD

Prolong above-2% inflation will support the GBP.

But sell-off from “NO Deal” risk and dovish BOE

could push the pair below 1.25 USD/GBP

GBP/USD

1.291.341.301.25Next 4 quarters

4Q173Q172Q171Q17TMB Forecast

USD/CNY is expected to fluctuate around 6.80

yuan per USD as PBOC lets the pair to move

according to actual transactions

USD/CNY

6.606.656.786.89Next 4 quarters

4Q173Q172Q171Q17TMB Forecast

Stronger EU economy will gradually boost the

EUR, expected to stay above1.15 USD from

faded political rout and hopes for ECB tapering

EU disintegration,

banking problems

Less political risks

& ECB tapering

EUR/USD

1.211.181.141.07Next 4 quarters

4Q173Q172Q171Q17TMB Forecast

Global “risk-on” abandons JPY haven in 2017. the

pair is expected to stay around 110-115 while

dovish BoJ could suppress JPY’s rise in 2H17

Risk-On & yield

curves steepen

Weak US data &

risk-off market

112113112111Next 4 quarters

4Q173Q172Q171Q17TMB Forecast

USD/JPY

Brexit with No Deal,

Rate cut, More QE

Stronger economy &

no QE extension

Reserve outflows &

waning economy

Stable FX policy &

Improving economy

Source: CEIC and TMB Analytics; as of Sep 2017

Factors to Monitor Factors to Monitor

Factors to Monitor Factors to Monitor

70

101

178

6.4

6.8

7.2

7.6

0

50

100

150

200

2017 2018 2019

Average 5YCorporatebond yield

-16-Source: Bloomberg, PBOC, TradingEconomics and TMB Analytics; as of Aug 17

China Corporate Debt: Napping Black Swan

Rollover Risk Looms As Cost of Funds RiseCorporate debt is absurdly high (156% of GDP)

%to GDP

-500

500

1,500

2,500

3,500

Jan-16 Jul-16 Jan-17

Shadow loans MoMBank loans MoM

Could PBOC tame shadow loans rampages?

Billion Yuan

3

24

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015 2016

Trillion Yuan

Shadow banking loans keep swelling up

Billion Yuan

Yearly amount due

on Corporate Bond

rated AA- or lower

Shadow loans = 13% of total debt

%

100162

73 85

160

257

0

100

200

300

400

500

600

2008 2016 2016 2016

Corporate Debt Household Debt

Bank Debt Government Debt

Private

Corp.

53%

SOE

109%

0.6

0.8

1

1.2

1.4

1.4

1.5

1.6

1.7

1.8

Jan-16 Jul-16 Jan-17 Jul-17

Russell 3K Value/Growth (LHS)

UST10Y-UST2Y (RHS)45.0

50.0

55.0

60.0

Jan-15 Jan-16 Jan-17

EU_Services_PMI

EU_Mfg_PMI

-17-

▪ New US government

policies create more

volatility to economic

projections

▪ Subdued inflation could be

persist until consumer

spending grows stronger

▪ Economy is projected to

expand 2.2% in 2017 from

1.6% in 2016

United States Eurozone

Activity

3.0%QoQ SAAR Real

GDP 2Q17

Price

1.9%YoY SA CPI

Aug 17

Labor Mkt

4.2%Unemployment

Rate Sep 17

▪ UK economy keep growing,

amid lessening economic

ramifications from Brexit

▪ Expansions among

manufacturing and service

sectors sustain EU’s growth

▪ Growth in 2017 is expected

to be around +2.0% better

than +1.6% in 2016

EU Activity

2.3%YoY SWDA GDP 2Q17

UK Activity

Industry

Latest Releases Latest Releases

Source: Bloomberg, and TMB Analytics’ projection

1.7%YoY SWDA GDP 2Q17

58.1EU Mfg. PMI

Sep 17

Fading Reflation: Flattening yields curve Steady Expansions in EU Mfg. and Services

Solid Growth Momentum Among Developed Economies

(%)

↑ Expansion

↓ Contraction

Trump’s

Victory spark

Reflation trades

Fading

Trumponomics

= Dying Reflation

+0.8%

+4.9%

-8%

90

95

100

105

110

Jan-17 Apr-17 Jul-17

Nikkei225

TOPIX

USDJPY

-18-Source: Bloomberg, and TMB Analytics’ projection

▪ Economy is likely to

sustain above 1.0%

expansion in 2017

▪ Inflation and consumer

spending gradually improve

▪ Recently, strong Yen could

hamper rising trend of

inflation and hurt Japanese

exporters’ profit margin

Japan China

Activity

2.5%YoY NSA

GDP 2Q17

Price

0.7%YoY SA Core

CPI Aug 17

Export

18.1%YoY NSA

Aug 17

▪ GDP is likely to grow by

6.3% in 2017 where growth

story still broadly unchanged

▪ Rebound in industrial sector

galvanize rising profits and

debt-repayment ability

▪ Inflation picks up, eases

concern over economic

growth

Activity

6.9%YoY Real

GDP 2Q17

Price

1.8%YoY CPI

Aug 17

Production

50.6Caixin Services

PMI Sep 17

Higher profits reflects higher producer prices

Latest Releases Latest Releases

Strong Yen punishes prospects of exporters

Stabilizing Asian Economies Amid Strengthening Currencies

(%)(%)

Rebased at 100-8.0

-4.0

0.0

4.0

8.0

-40

-20

0

20

40

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

China Industrial Enterprises total profits yoy

China PPI YoY

Thai Economy

6.6

8.0

3.13.3

1.81.6

5.1

2.0

7.2

5.1

3.2 3.2

2.2

3.8

4.9

2.2

GDP 2560E

GDP 2561F

3.5%

3.8%

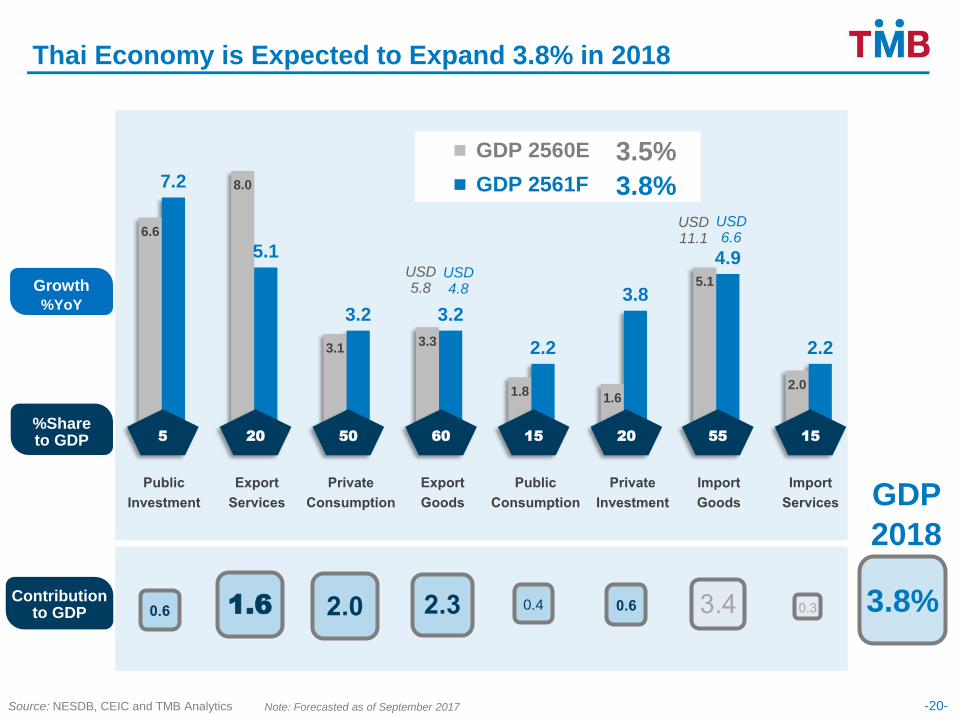

Thai Economy is Expected to Expand 3.8% in 2018

Source: NESDB, CEIC and TMB Analytics -20-

USD 5.8

USD 4.8

5 20 50 60 15 20 55 15

%Share to GDP

PublicInvestment

ExportServices

PrivateConsumption

ExportGoods

PublicConsumption

PrivateInvestment

ImportGoods

ImportServices

Note: Forecasted as of September 2017

Growth

%YoY

Contribution to GDP

USD 11.1

USD 6.6

1.6 2.3 0.4 0.33.40.62.00.6

GDP

2018

3.8%

65

70

75

80

85

-30

-20

-10

0

10

20

Aug-15 Feb-16 Aug-16 Feb-17 Aug-17

Services Durable Cons Confidence (RHS)

%yoy Index

Domestic Demand Continually Improved

Source: BOT, OAE and TMB Analytics

▪ Overall private consumption continued to

expand even though durable consumption

slowed down due to farm income contraction.

Consumer confidence remained low.

▪ Farm income contracted from the same period

last year as increase in agricultural production

was overwhelmed by decrease in the price.

▪ Private investment expanded slightly from last

year mainly from equipment investment

consistent with improving business sentiment.

Slow Down in Durable Consumption Growth Positive Private Investment Growth

Drop in Farm Income from Strong Price Plunge

44

47

50

53

-4

-1

2

5

Aug-15 Feb-16 Aug-16 Feb-17 Aug-17

Private Investment Biz Sentiment (RHS)

%yoy Index

-30

-15

0

15

30

45

Aug-15 Feb-16 Aug-16 Feb-17 Aug-17

Price Quantity Farm Income

%yoy

-21-

-22-Source: Ministry of Finance and TMB Analytics

Expect more mid-year budget disbursement in 4Q2017

Capital Budget Disbursement RateCapital Budget Disbursement

▪ In August, investment budget recorded higher level of disbursement in line with its cycle in

the final quarter of 2017FY. The total investment disbursement of the first 11 months of

FY2017 still edged up by 4% yoy.

▪ Investment contracts amounting to 50% of total mid-year capital budget has already been

sign. Therefore, we expect mid-year budget to be disbursed more rapidly in the rest of the

year.

Note : data include Mid-year budget since Apr 2017

10,000

20,000

30,000

40,000

50,000

60,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2015 2016 2017

57

0

20

40

60

80

100

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

FY2015

FY2016

FY2017

FY2017 Target87%

Million THB

2.88

3.13

92k

42k

71k9k 17k 17k 1k 0k

-0k

+10%

+10%

+10%

-0% +11% +13% +19%+9% +0%

Au

g'1

6

Ch

ina (

31

%)

Ea

stA

sia

(E

xc

l.C

hin

a)

(15%

)

AS

EA

N (

25

%)

Eu

rop

e (

14

%)

Am

eri

ca

s (

3%

)

So

uth

Asia

(5%

)

Mid

dle

Eas

t (3

%)

Afr

ica

(1

%)

Oc

ean

ia (

2%

)

Au

g'1

7

Aug'16

Million

Million

Aug'17

Ch

ina

(3

1%

)

Source: Department of Tourism, BOT, and TMB Analytics

*Note:± x % represents the growth of tourist arrival (yoy)( %) represents the share of tourist arrivals

Inbound Market Showing Strong Growth

+9.0%

-23-

9%yoy…Tourism Sector Showing Healthy Growth Chinese Arrivals Exceed 3 Mill, 2nd Highest During 8M17

10.5 9.0

60.5 65.1

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Dec-1

4

Ma

r-15

Jun

-15

Se

p-1

5

Dec-1

5

Ma

r-16

Jun

-16

Se

p-1

6

Dec-1

6

Ma

r-17

Jun

-17

Growth of No. of Tourists (%yoy)

Aug'17Aug'16

+250k

Occupancy Rate (%)

Number of Tourists (Mill people)

2.883.13

▪ August 2017, number of foreign tourists were 3.13 million (+9%yoy), East Asia and ASEAN represented 71% of

international tourists in this month.

▪ 8M17, arrivals were recorded 23.5 million (+5%yoy). Chinese has been and still is top source with 28% market shares,

followed by Malaysia, Korea, Laos, Japan, India, and Russia. Those 7 nations dominated 60% of inbound arrivals.

▪ Positive Drivers included more airlines link major Chinese cities with secondary tourist destinations in Thailand,

increasing flight from major supply cities in India and also new routes from Taiwan, Indonesia and Turkey to BKK

contributed the growth in number of international tourist arrivals.

▪ Occupancy rate gradually improved to 65.1%, hotel market seems to be recovering.

CLMV

(2016 -0.2)

+8.5

Rubber

+16.0(2016 -3.8)

-24-Source: MOC CEIC and TMB Analytics

What is 2017 outlook for Thai Export?

Total

(2016 +0.5)

+5.8

Japan

(2016 +2.4)

+6.0

China

(2016 -0.8)

+19.0

USA

(2016 +1.7)

+6.0EU

(2016 +0.5)

+5.0

Growth mainly from

global demand

recovery as less

uncertainty and political risk this year

Strong demand consumption

Oil price

recovery helps

raw mat and commodities

Recovered

investment in Asia

help supply chain with Japan

Continual

economic recovery

Protectionism

unlikely to take

an effect this year

Thai Export: Recovery….A Significant Boost

Computer&Parts

(2016 -2.0)

+9.0

Vehicle

+4.0(2016 +4.6)

Electrical appliances

+10.0(2016 -1.3)

Rising demand

for tire mfg from China

Same growth as

last year comes

mainly from supply of auto parts

Global economic recovery and increase in

oil price which is expected to be 55 dollar per barrel at the end of 2017

Market

Product

High

economic growth

Slightly Positive

mainly owing to

sugar both volume and price

ASEAN5

(2016 -1.4)

+4.5

Agro

Products

(2016 -6.5)

+2.0

Chemical

+10.0(2016 -7.5)

-25-

-26-

Key productsOutlook Major exporting market

Consumption & Commodity

Agricultural & Agro

%YTD Share

Rubber 5.0

2016 YTD Aug

• Vegetable & Fruits(34.7%), Sugar(34.2%)

• HDD (17.8%), Electrical Machinery (20.5), Electronics Parts (10.3%)

• Basic Metal (45.0), Basic Steel (27.2)

August Growth (%) % YTD Share

• Polymer Products (131.5), Glove (22.1),Smoked Rubber Sheet (21.3)

• China (68.6),ASEAN5 (30.8), USA(17.3)

• CLMV (71.6),CHINA (5.6), ASEAN5 (-9.6)Agro 4.1

Rice 2.1

Chemical 7.0

Electronic Com 17.6 • CHINA (21.5) USA(2.3),

EU(25)(12.3)

Steel 4.0 • EU25 (18%), USA (50.4), JAPAN (34.2)

Source: MOC, and TMB Analytics

10.6%8.6%

17.0%

30.7%

9.2%11.6%

8.5%

17.8%

13.2%

4.8%

17.4%

24.6%

11.6%

7.1%3.4%

-7.3%

-20%

-5%

10%

25%

40%

WORLD ASEAN5 CLMV CHINA JAPAN USA EU25 MIDDLEEAST

YTD Jul Aug

Thai Export to Major Markets

13.6 25.8

44.333.9

17.348.4

10.411.2

18.726.3

21.928.3

• Rice(48.4%)

• Basic Chemical (28.8)

• Middle East (148.3), China (39.1), Africa (28.6)

• China(29.8), CLMV(34.3) ASEAN(8.4)

TMBA’s View

• A drop in export to ASEAN5, EU(25)

and Middle East due to car producers,

which the overall car export this

month shrank by 33%.

• Slower export to USA came from a

shrank of Jewelry export (-10.1%) and

passenger car (-23%)

• While a drop in export to China mainly

came from steel ( -16.5%), and energy (-29.7%)

August Export Growth supported by both Agri.& Indus. especially Elec. Com.

-27-

Industrial Outputs Rose For Second Straight Month in August

80

85

90

95

100

105

Jan-14 Jan-15 Jan-16 Jan-17

Diffu

sio

n In

de

x

BA

DG

OO

D

▪ MPI increased 3.7%yoy with capacity utilization rate at 62.5% in

August, export as a key driver of growth, mainly supported by

vehicle and part, electronics, rubber products and chemicals.

▪ Entrepreneurs sentiment improve for the first time in five months

from new orders both domestic and export markets. However,

most firms continued to be concern about currency appreciation.

Manufacturing Product Index (MPI)

Negative gr.( MPI < 0%)

Low gr.( 0%<MPI < 3%)

Moderate gr.(3% <MPI<5%)

High gr.(MPI > 5%)

Source: OIE, BOT, FTI, classified industry group and calculated by TMB Analytics

-50

-30

-10

10

30

50

70

Jan-14 Jan-15 Jan-16 Jan-17

%Y

oY

Fuel Industry

Industry Indicator

II.Industrial Confidence

I.Raw Materials ImportAug-17

Q1 Q2 July Aug (%MoM,sa)

Capacity Utilization Rate (%) 100.0 60.0 62.6 59.1 60.0 62.5 2.6

Manufacturing Product Index (MPI) (%YoY) 100.0 1.6 0.3 -0.1 3.4 3.7 2.7

Food 15.3 2.7 2.8 4.9 10.1 0.1 -5.1

Vehicle 11.8 2.2 -4.8 -2.3 2.8 9.4 8.3

Electronic/Computer & Parts 11.2 2.7 13.9 9.4 6.5 4.5 2.0

Autopart 9.8 -1.0 -3.2 3.9 18.9 26.8 10.2

Fashion Products 9.8 -2.8 -5.4 -6.2 -6.0 -9.6 3.4

Steel Products 5.9 5.3 8.8 -11.0 0.5 -7.7 0.0

Rubber Products 5.8 -0.7 -2.6 5.3 17.2 13.7 11.0

Construction Material 5.6 -0.9 -1.2 -2.7 -11.3 -1.8 3.3

Electronic/Electric Home Appliance 4.3 15.1 -2.6 -6.9 -16.4 -14.7 5.1

Beverage 4.0 -0.2 -1.7 -6.8 14.1 10.0 4.7

Petroleum 3.3 2.4 -0.2 7.5 1.8 7.4 1.5

Plastics Products 3.1 4.2 -2.6 -1.7 1.3 2.5 0.6

Papers & Printing 2.7 5.2 -1.2 1.7 -0.7 5.6 4.7

Furniture and Household Products 1.8 -17.3 -2.0 -5.9 -22.9 12.8 49.8

Chemical 1.6 0.5 -1.5 -0.0 0.7 10.7 4.8

Healthcare 1.3 -1.2 13.4 3.9 -0.0 -9.8 0.3

Consumer Goods 1.3 1.1 -5.0 -7.2 -2.2 -2.0 2.0

Tabacco 1.1 -9.2 -5.0 -9.1 16.9 9.8 31.1

Agri.Machinery 0.1 5.8 -14.9 1.4 -26.9 -28.3 9.3

(%)

Weight2016

2017

-2.0

-1.0

0.0

1.0

2.0

15Q1 15Q2 15Q3 15Q4 16Q1 16Q2 16Q3 16Q4 17Q1 17Q2 17Q3

Expect Rate Normalization in 2018 and 1.50% Policy Rate in 2017

Source: MOC, CEIC and TMB Analytics

Headline Inflation Stands above Zero for 2 Consecutive Months

Policy Rate is Expected to be Held at 1.50% as Inflation Remains Low

Higher Inflation from Increase in Energy Price

▪ September inflation picked up due to higher

energy prices, increase in prices of tobacco

and alcoholic drinks from excise tax reform,

and higher price of some fresh food in flooded

area.

▪ We expect inflation rate to be averaged at

0.7% in 2017 from increase in energy price.

-29-

%yoy

Sep 2017 0.9%

Avg 2016 = 0.2%

▪ Policy rate is expected to be maintained at

1.50% throughout 2017 to accommodate

economic recovery especially private investment.

Moreover, inflationary pressure remained low.

▪ We expect the rate normalization to begin in

2018 as global interest rate is on an upward

trend following 3 expected fed rate hikes in 2017.

However, there is still concern over recovery of

private investment, which can delay Thai rate

normalization.

%

1.45

2.62

1.0

1.5

2.0

2.5

3.0

15Q1 15Q3 16Q1 16Q3 17Q1 17Q3

TGB2YTGB10Y

Source: MOC, CEIC and TMB Analytics -30-

% TMB’s Projection

0

1

2

3

4

5

15Q1 15Q3 16Q1 16Q3 17Q1 17Q3 18Q1 18Q3

2017 Policy Rate: 1.5%

%

2018 Policy Rate: 2.0%

2017 TGB 2Y: 1.45%

2017 TGB 10Y: 2.62%

Policy Rate will Reach 2.0% in 2018 amid Global Tightening Cycle

TGB yields will gradually rise as BoT hike rate

2018 TGB 2Y: 1.86%

2018 TGB 10Y: 3.05%

30

1.4

2.1

2.9 3 3

3 3

1.52

2.252.5

2.75

33.253.25

0

1

2

3

4

5

6

2004 2006 2008 2010 2012 2014 16 17 18 19 20 21 22 23 24

0.1-0.1

-0.7

-0.5-0.3

0.00.3 0.3

-1.5

-0.5

0.5

1.5

2.5

3.5

2004 2006 2008 2010 2012 2014 16 17 18 19 20 21 22 23 24

Source : Minute of FOMC March 14-15 ,2017 ; Bank of Thailand, TMB Analytics, as of Aug 2017

Federal Funds Rate

Entering rising rate

environment

*Projection of Fed funds rate is from FOMC’s projection as of March 2017

*Projection of Thai policy rate is from TMBA’s projection as of May 2017

Projection%year end

%year end

Thai-US Policy Rate Differentials

Projection

*Thai RP minus US Fed funds rate

▪ Thai economic expansion

leads to rising inflation.

▪ Acceleration in US rate hike

puts pressure on Thai

policy rate as fund outflows

could be intensified

Thai policy rate

Fed funds rate

US policy rate is higher

than Thai policy rate

▪ Thai policy rate uptrend to

begin in 2018

-31-

Brace Yourselves Negative Rate Differential Is Coming!

THANK YOU

Disclaimer

This document is issued by TMB Analytics, a division of TMB Bank PCL. All analyses are based on information available to

the public. Although the information contained herein is believed to be gathered from reliable sources, TMB makes no

guarantee to its accuracy and completeness. TMB may have issued, and may in the future issue, other reports that are

inconsistent with, and reach different conclusions from, the information presented in this report. Opinions or predictions

expressed herein reflect the authors’ views, not that of TMB, as of date of the analysis and are subject to change without

notice. TMB shall not be responsible for the use of contents and its implication.

![Monthly Economic Reviewbsl.gov.sl/MER October 2019- Finalised Version.pdf · Monthly Economic Review October 2019 Publisher: The Monthly Economic Review [MER] is published by the](https://static.fdocuments.us/doc/165x107/5eddde83ad6a402d66691757/monthly-economic-october-2019-finalised-versionpdf-monthly-economic-review-october.jpg)