Monopoly Lecture Notes (Economics)

51

Pricing in Product Market: A Case of Monopoly Market Structure

-

Upload

fellowbuddycom -

Category

Education

-

view

1.690 -

download

1

Transcript of Monopoly Lecture Notes (Economics)

Pricing in Product Market: A Case of Monopoly Market Structure

Overview Define Monopoly Natural Monopoly, Bilateral Monopoly Emergence of Monopoly Natural Monopoly Bilateral Monopoly Production and Pricing Decisions A Rule of Thumb for Pricing Pricing in Monopoly Market Measuring Monopoly Power Effect of Tax on Monopoly Welfare Cost of Monopoly Public Policy and Monopoly

Monopoly

Derived from Greek Words: monos polein (alone to sell)

A market structure in which there is one seller who either sets the price or the quantity but not both.

Exp: Enterprises supplying Public Utility Services – Water Supply & Electricity (closely resemble)

[Gas Pipeline (Mahanagar Gas- Gas connection provided in building –Mumbai), Public Transport: BEST BUS (Mumbai) Railways]

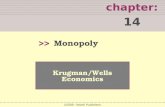

Monopoly ……A firm is considered a monopoly if:

– Monopolist is the sole seller of its product. – Not having close substitutes of its products. Why?

(Availability of substitute: with rise in price of monopoly product demand for substitute will go up)

Exp: Coca Cola corp: Producer of ‘Coke’Colgate-Palmolive: only produce of Colgate toothpaste but it is not a monopoly due to availability of substitutes (Close up, Pepsodent etc.)

• The monopolist is the supply-side of the market and has complete control over the amount offered for sale

• Monopolist controls price but must consider consumer demand

Monopolists are price setters:

They select their own price and supply the entire quantity demanded.

Product has no close substitutes, so rise in price can not reduce demand.

Prevalence of barriers to entry restricts other firms to enter the market.

• Monopoly does not imply that there is a single Producer (as monopolist need not produce own product).

• There is a SINGLE SELLER (of group of sellers) that sets the price.Exp: OPEC- consists of 11 major producers that collectively set the price of oil

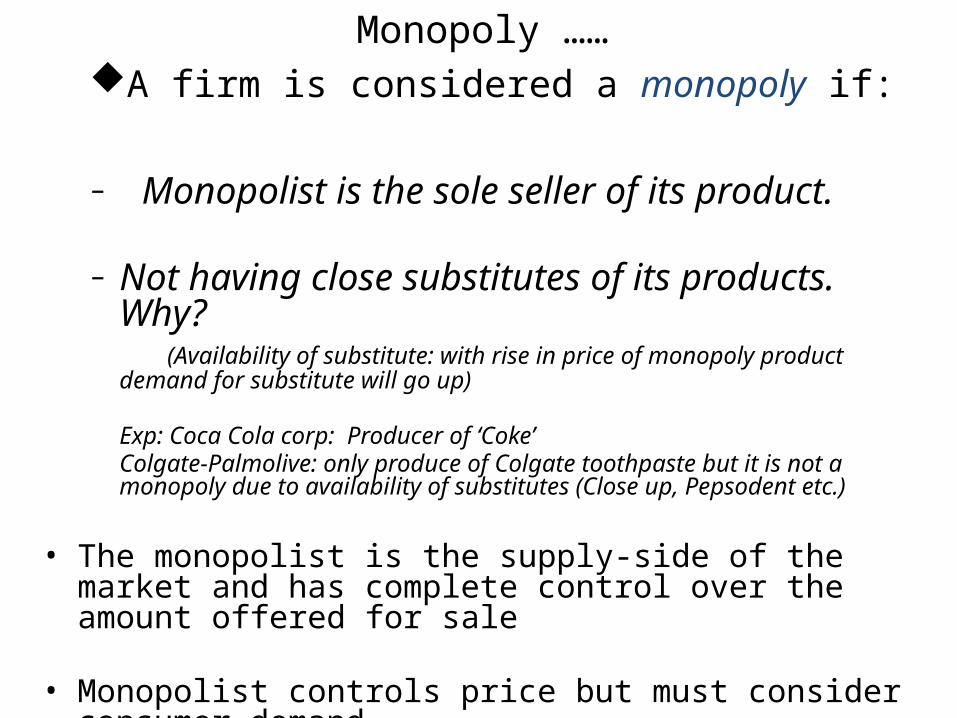

Pure Monopoly: Rare in Practice

Monopoly

A Pure Monopoly exists when a single firm is the only producer or seller of a product that has no close substitute. Entry into the industry is difficult or impossible. Firm is the industry

Pure Monopoly: Rare in Practice

Examples: Monopolies (Taxis in New York City)

• Case of Monopoly created by licensing (not pure monopoly)

-One can’t drive a cab without license (called Medallion).

- Licenses are limited in number, people having licenses got monopoly power to earn profit.

The number of taxicabs is set by law at 11,787.

No new taxi licenses have been issued for over half a century.

Until 1937- any qualified taxi driver could get the license by paying a nominal licensing fee.

Later limit on number of license issued imposed effectively fixing total supply of license.

Current owners of license can sell them to others who are keen to operate a taxicab.

Over time, Mismatch between supply and Demand: Rise in Price of Medallion.

(INCREASE in PRICE to even $50,000 from an initial licensing fee of $5)

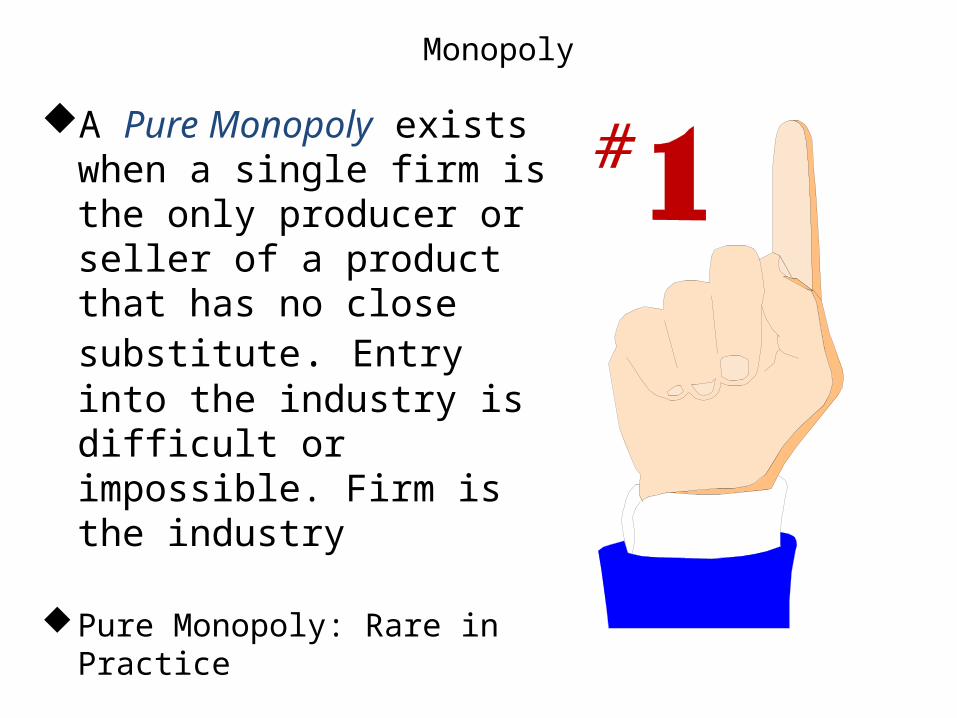

The American Medical Association (AMA)

• Strongest and longest lasting Cartel

• AMA prevents individual doctors from reducing prices

• With Assistance from State Legislature AMA restricted supply of doctors and therefore, restricted output of medical services.

• Flexner report (1910): Recommended reduction in number of Medical Schools, implying fall in

doctor to population ratio .

• In contrast, demand for health care services increased due to rise in per capita income and various insurance scheme.

• Outcome: Income of doctors went up.

Input Monopolies

• Monopolies through ownership of key resources

Aluminium Company of America (ALCOA) once controlled most domestic bauxite deposits.

International Nickel Company once owned 90 per cent of World’s Nickel

De Beers Consolidated Mines Ltd (South Africa)- Handles about 80 per cent of World’s uncut Diamonds.

Why to Learn About Monopoly?

A part of total domestic output is supplied under monopoly condition

Helps to understand more common market structures such as Monopolistic Competition and Oligopoly.

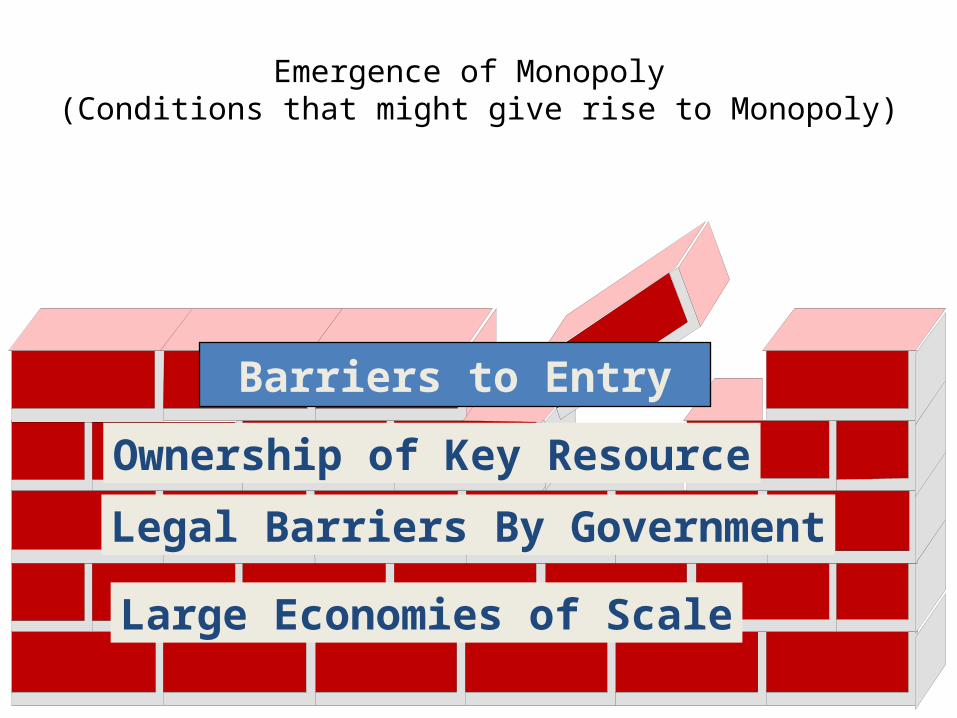

Emergence of Monopoly (Conditions that might give rise to Monopoly)

Ownership of Key Resource

Legal Barriers By Government

Large Economies of Scale

Barriers to Entry

Emergence of Monopoly

Barriers to Entry prevails in the Market. Why?(Implication: Imposition of Barrier to Entry ---

No competition-----Ensure growth of Profit)

– Monopolist can exercise monopoly power to influence the market price (of its product)

[(Unlike in Perfect Competition, Monopoly is a price Setter not Price Taker (set own price and supply entire quantity demanded)]

Emergence of Monopoly

Ownership of Strategic Raw Material

(Control over critical Inputs, exclusive knowledge of production technique):

If one firm controls supply of a critical input?

Other firms can’t enter the industry as not having access to it.

Exp: Role of Aluminum Company of America (ALCOA) in the production of Aluminum through CONTROL OVER SUPPLY OF BAUXITE in the early Twentieth Century

(SIGNED LONG TERM CONTRACTS WITH COMPANIES SUPPLYING BAUXITE SO THAT BAUXITE CAN NOT BE SOLD TO ANYONE ELSE).

Economies of Scale

Firm having downward sloping Average Cost Curve. HIGHER PRODUCTION LEADS TO LOWER UNIT COST OF PRODUCTION. New firms can not compete with the existing low cost producers.

Exp: Electricity supply, Water, Gas, Transport services etc(To have more than one firm implies overlapping distribution systems and higher per unit cost).

Government-Created MonopoliesPatent and copyright laws are a major source of

government-created monopolies.(countries grant an inventor sole control over the use of an invention for certain number of years. India: 7 years)

– Xerox corporation for Photocopying – Certain new pharmaceutical drugs

Governments also restrict entry by giving a single firm the exclusive right to SELL a particular good in certain markets. – Local cable television– Post Office – License to Liquor Store

Emergence of Monopoly

• Entry Lags: Large gestation period prevents new firms in entering the industry (Exp: Steel industry).

• Adoption of Limit Pricing Policy: Pricing policy aiming at prevention of New entry.(If price is very low, can other firms compete?)

• Limit Pricing along with Heavy advertising and continuous product differentiation render entry unattractive.

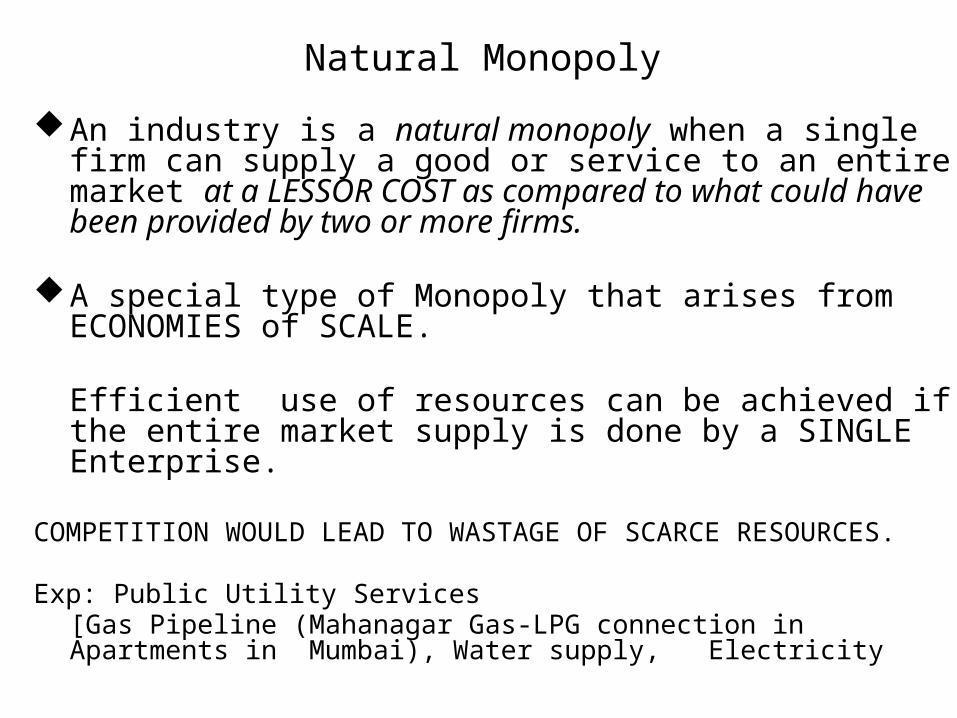

Natural Monopoly

An industry is a natural monopoly when a single firm can supply a good or service to an entire market at a LESSOR COST as compared to what could have been provided by two or more firms.

A special type of Monopoly that arises from ECONOMIES of SCALE.

Efficient use of resources can be achieved if the entire market supply is done by a SINGLE Enterprise.

COMPETITION WOULD LEAD TO WASTAGE OF SCARCE RESOURCES.

Exp: Public Utility Services[Gas Pipeline (Mahanagar Gas-LPG connection in Apartments in Mumbai), Water supply, Electricity

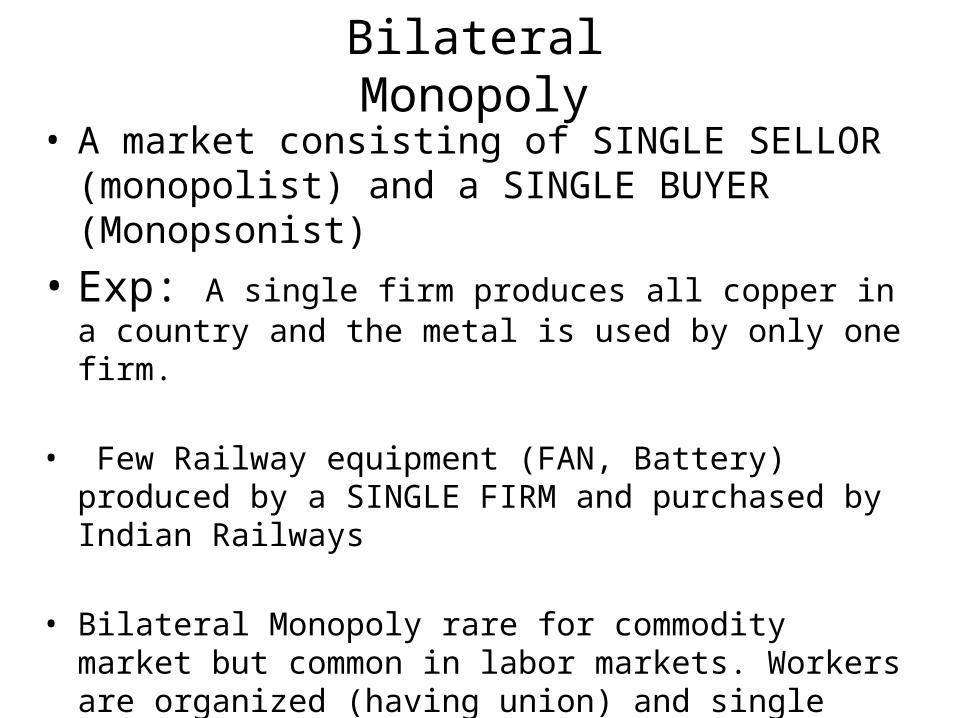

Bilateral Monopoly• A market consisting of SINGLE SELLOR (monopolist) and

a SINGLE BUYER (Monopsonist)• Exp: A single firm produces all copper in a country and the

metal is used by only one firm.

• Few Railway equipment (FAN, Battery) produced by a SINGLE FIRM and purchased by Indian Railways

• Bilateral Monopoly rare for commodity market but common in labor markets. Workers are organized (having union) and single employer hires them.

Profit Maximization Condition for Monopoly: Short Run

• Profits will be maximized at the level of output where marginal revenue equals marginal cost

(i) Necessary Condition for Profit MaximizationMR = MC

(ii) Sufficient Condition: MC cuts MR from Below

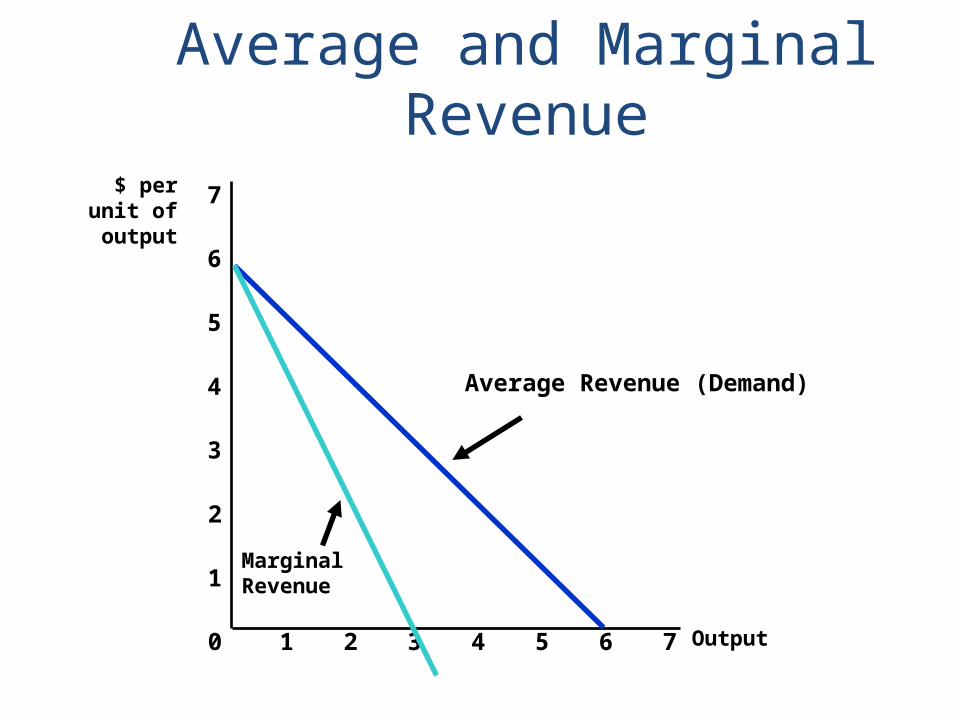

Total, Marginal, and Average Revenue

Revenue is zero when price is $6-Nothing is sold

At lower prices, revenue increases as quantity sold increases

When demand is downward sloping, the price (average revenue) is greater than marginal revenue

For sales to increase, price must fall

Average and Marginal Revenue

Output1 2 3 4 5 6 70

1

2

3

$ perunit ofoutput

4

5

6

7

Average Revenue (Demand)

MarginalRevenue

Lostprofit

P1

Q1

Lostprofit

MC

AC

Quantity

$ perunit ofoutput

D = AR

MR

P*

Q*

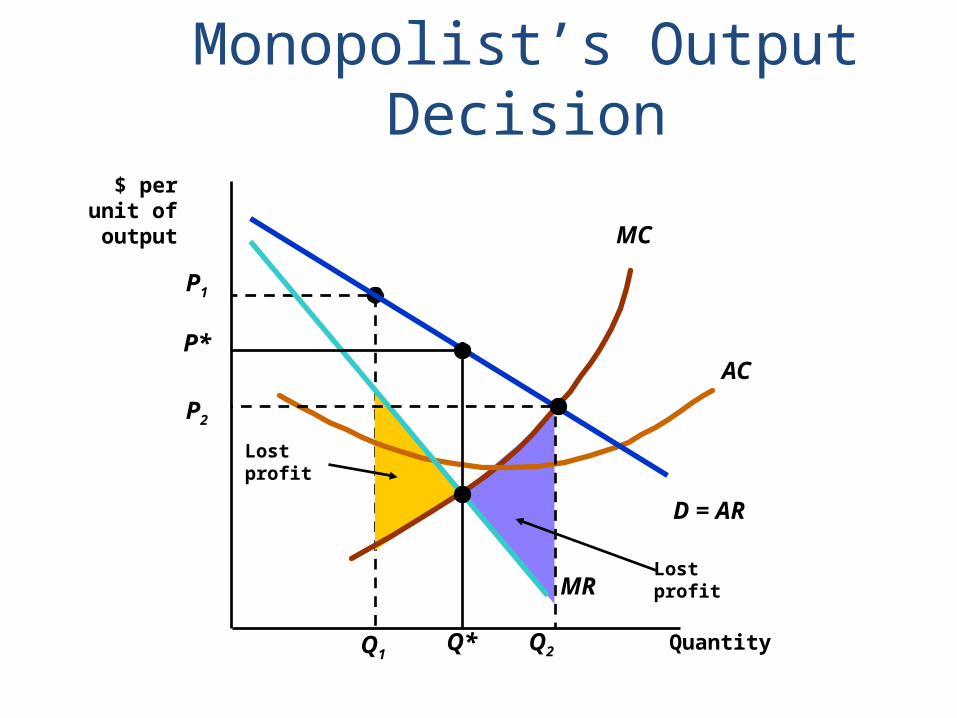

Monopolist’s Output Decision

P2

Q2

Monopolist’s Output Decision

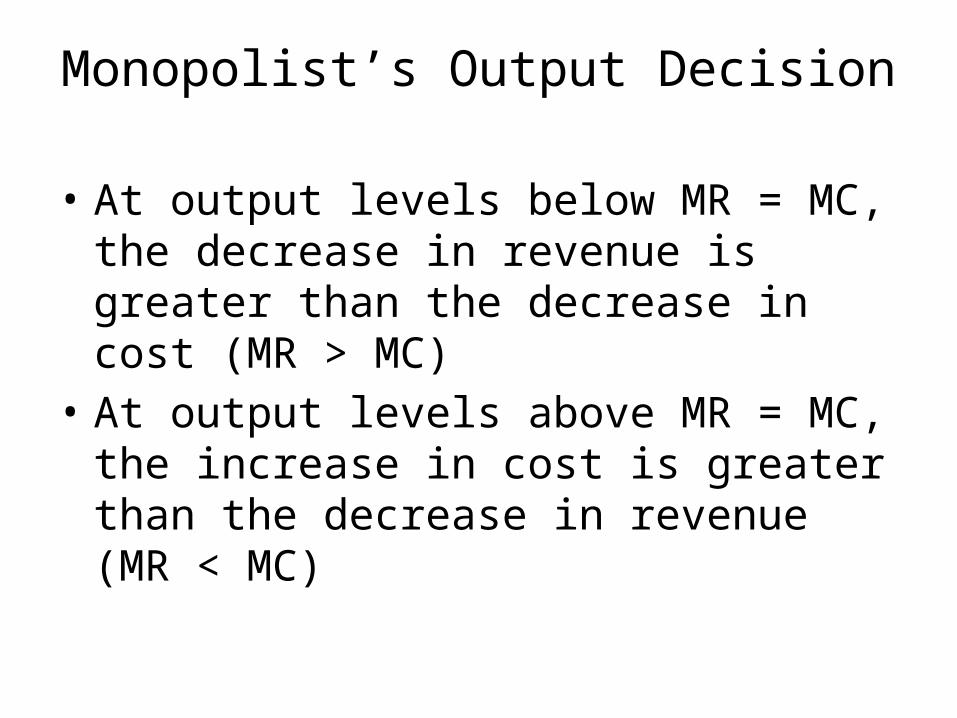

• At output levels below MR = MC, the decrease in revenue is greater than the decrease in cost (MR > MC)

• At output levels above MR = MC, the increase in cost is greater than the decrease in revenue (MR < MC)

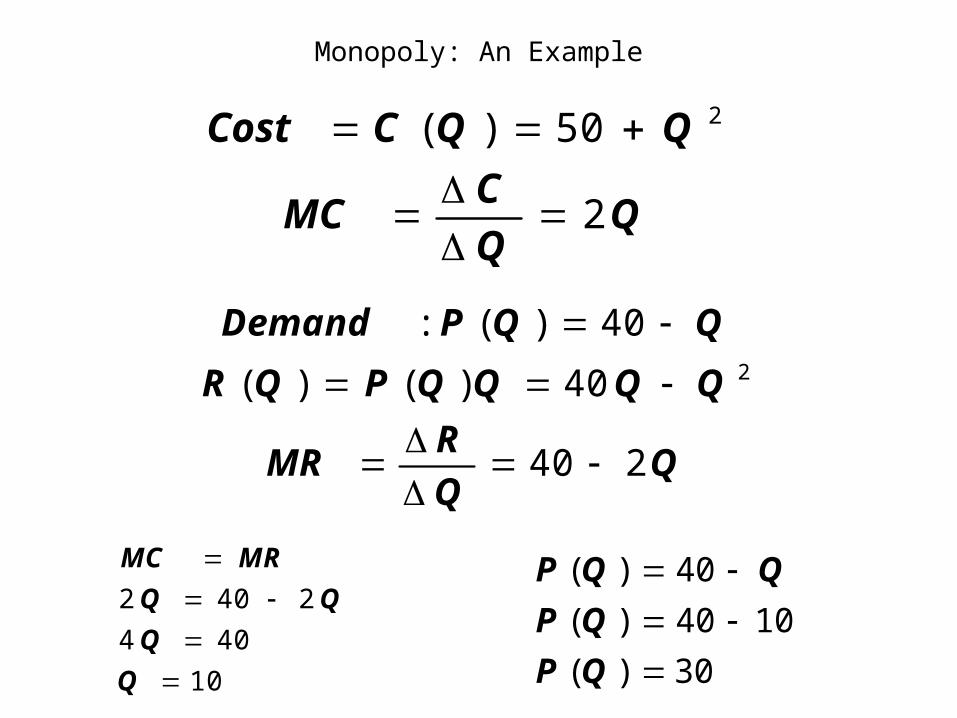

QQCMC

QQCCost

2

50)( 2

QQRMR

QQQQPQR

QQPDemand

240

40)()(

40)(:2

Monopoly: An Example

10404

2402

QQMRMC

30)(1040)(

40)(

QPQP

QQP

Monopoly: An Example• By setting marginal revenue equal to marginal

cost, profit is maximized at P = $30 and Q = 10

• This can be seen graphically by plotting cost, revenue and profit– Profit is initially negative when produce little or no

output– Profit increase and q increase, maximized at

Q*=10

Quantity0 5 15 20

$

100

150

200

300

400

50

R

10

Profitsr

r'

c

c’

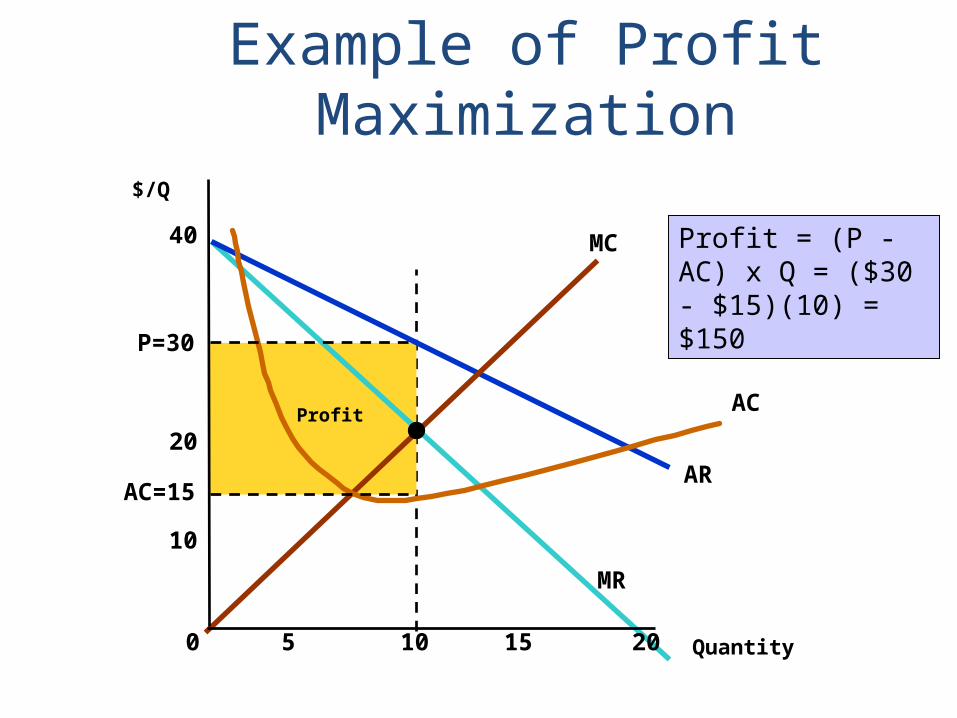

Example of Profit Maximization

C

When profits are maximized, slope of rr’ and cc’ are equal: MR=MC

Profit

AR

MR

MC

AC

Example of Profit Maximization

Quantity0 5 10 15 20

P=30

$/Q

10

20

40

AC=15

Profit = (P - AC) x Q = ($30 - $15)(10) = $150

Monopoly in Long run

• Profit maximizing rate of output and selling price is determined by the equality between MC and MR(MC=MR)

• Monopolists will NOT STAY IN BUSINESS if s/he makes LOSSES in the long run.

• May earn SUPERNORMAL PROFIT (more than normal profit) even in the long run due to entry barrier.

• Size of plant and degree of utilization of plant depends on market demand.

May reach optimal scale (minimum point of LAC or remain suboptimal scale (falling part of LAC) or surpass the optimal Scale (expand beyond the minimum LAC) depending on the market conditions.

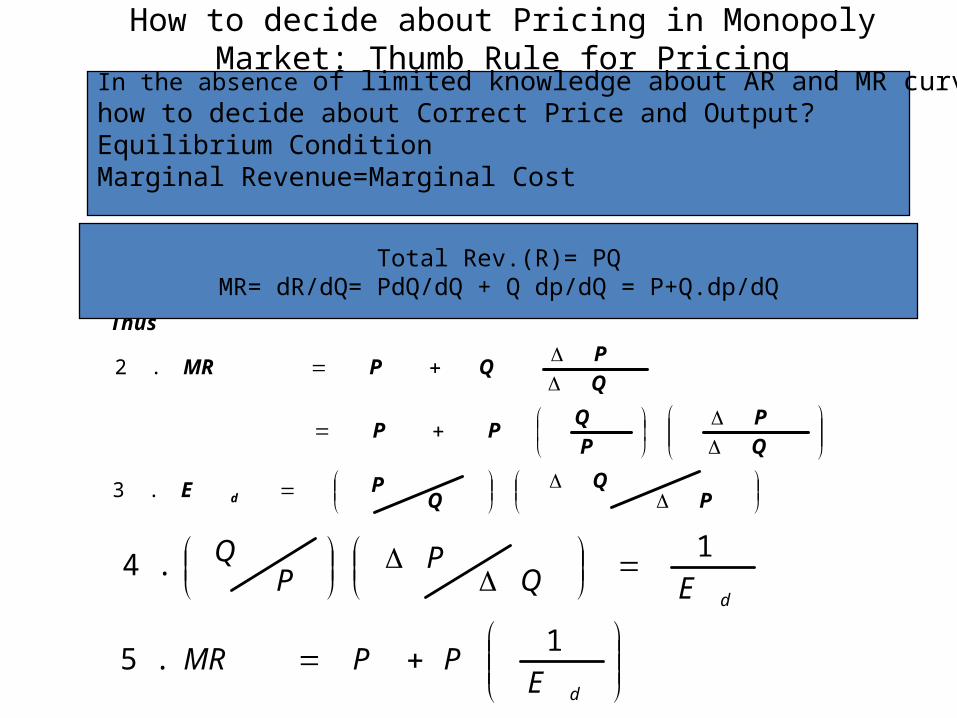

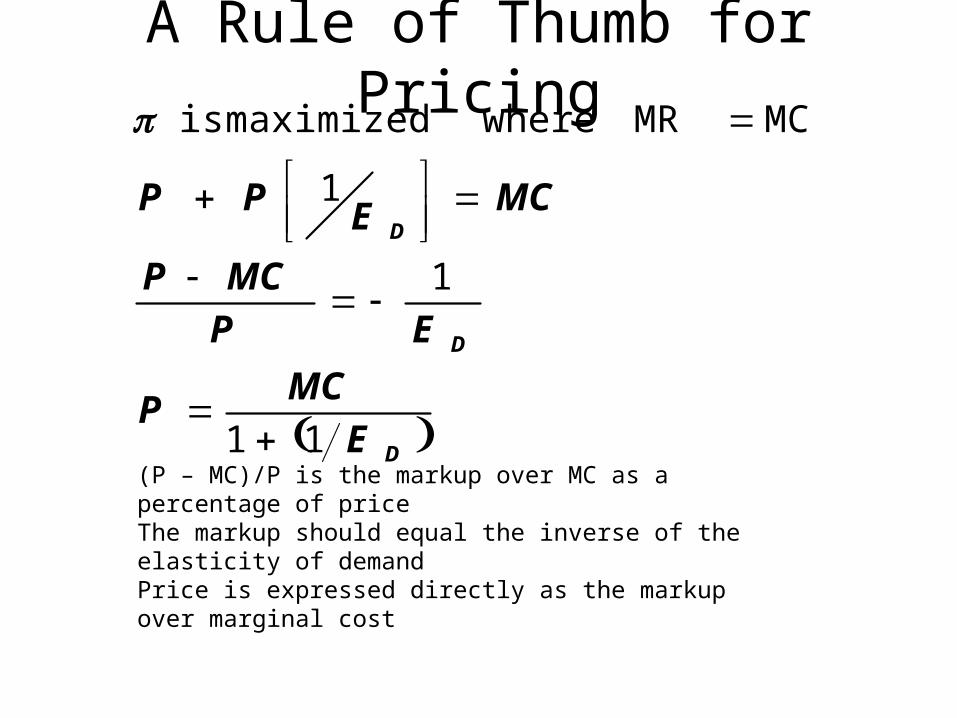

How to decide about Pricing in Monopoly Market: Thumb Rule for Pricing

PQ

QPE

QP

PQPP

QPQPMR

Thus

d.3

.2

d

d

EPPMR

EQP

PQ

1.5

1.4

Total Rev.(R)= PQMR= dR/dQ= PdQ/dQ + Q dp/dQ = P+Q.dp/dQ

In the absence of limited knowledge about AR and MR curves, how to decide about Correct Price and Output?Equilibrium ConditionMarginal Revenue=Marginal Cost

A Rule of Thumb for Pricing

D

D

D

EMCP

EPMCP

MCE PP

11

1

1

MC MR wheremaximized is

(P – MC)/P is the markup over MC as a percentage of priceThe markup should equal the inverse of the elasticity of demandPrice is expressed directly as the markup over marginal cost

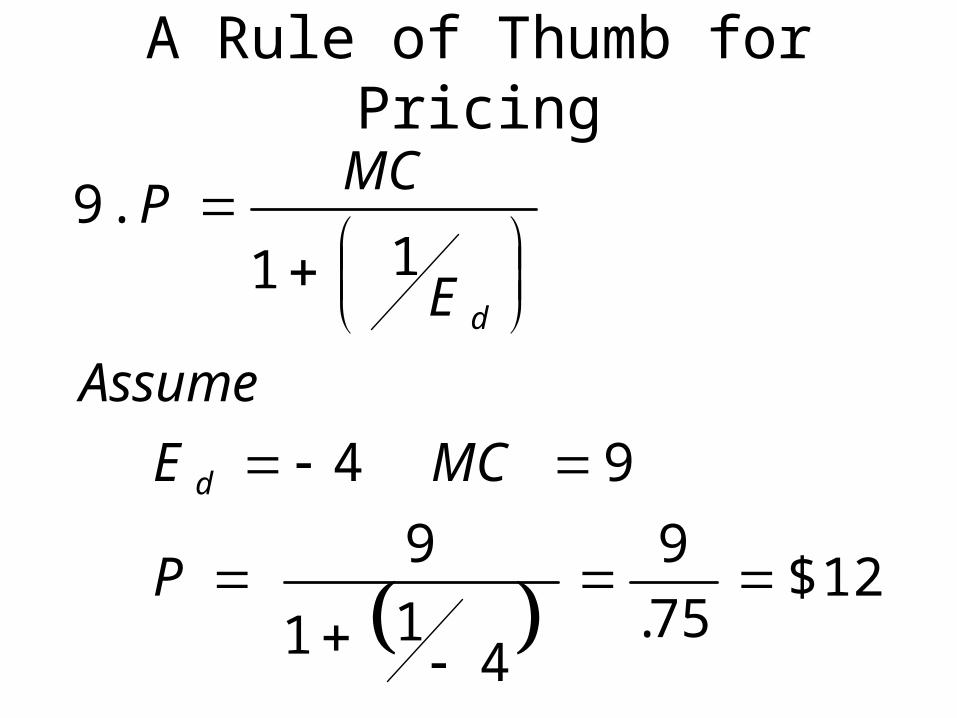

A Rule of Thumb for Pricing

12$75.9

411

994

119

.

P

MCEAssume

E

MCP

d

d

Measuring Monopoly Power• Why to Measure Monopoly Power?• Monopolist is free to decide about Price and Quantity of

output.• Implication: Production can be less than required amount

from Social point of view• In case of Perfect Competition: Price =MC

• Monopoly: Price>MC

• -Rationale to assess the difference between Profit Maximizing Price and Marginal Cost

• Methods to Measure Monopoly Power– The Herfindahl Index– Lerner Index– Concentration Ratio

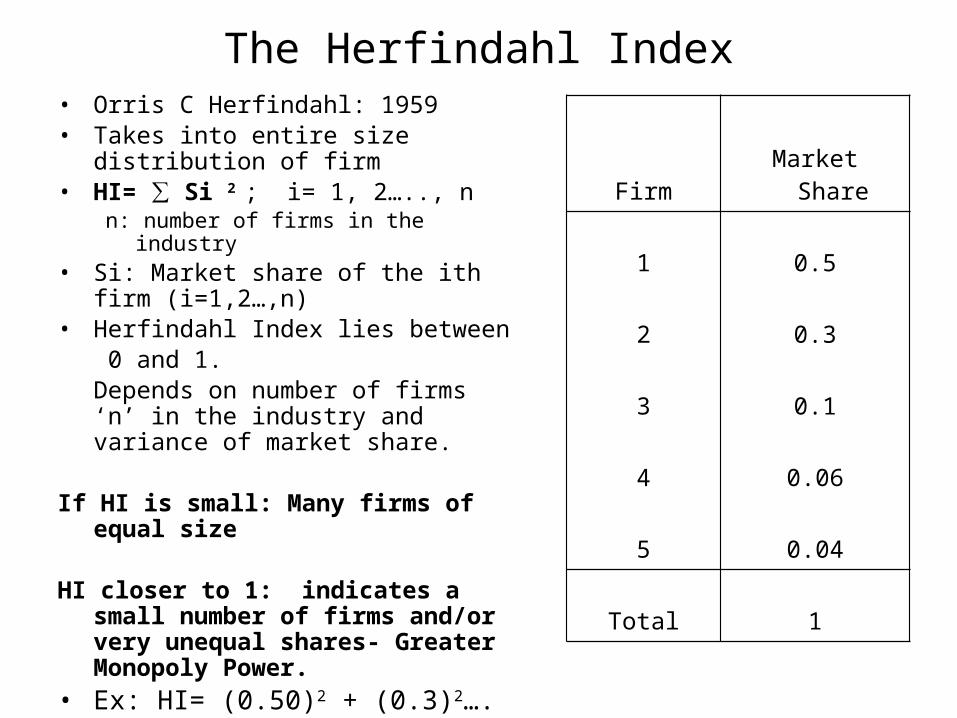

The Herfindahl Index• Orris C Herfindahl: 1959• Takes into entire size distribution of firm• HI= ∑ Si 2 ; i= 1, 2….., n

n: number of firms in the industry• Si: Market share of the ith firm (i=1,2…,n)• Herfindahl Index lies between

0 and 1. Depends on number of firms ‘n’ in the

industry and variance of market share.

If HI is small: Many firms of equal size

HI closer to 1: indicates a small number of firms and/or very unequal shares- Greater Monopoly Power.

• Ex: HI= (0.50)2 + (0.3)2….+(0.04)2

• = 0.3552

Firm Market Share

1 0.5

2 0.3

3 0.1

4 0.06

5 0.04

Total 1

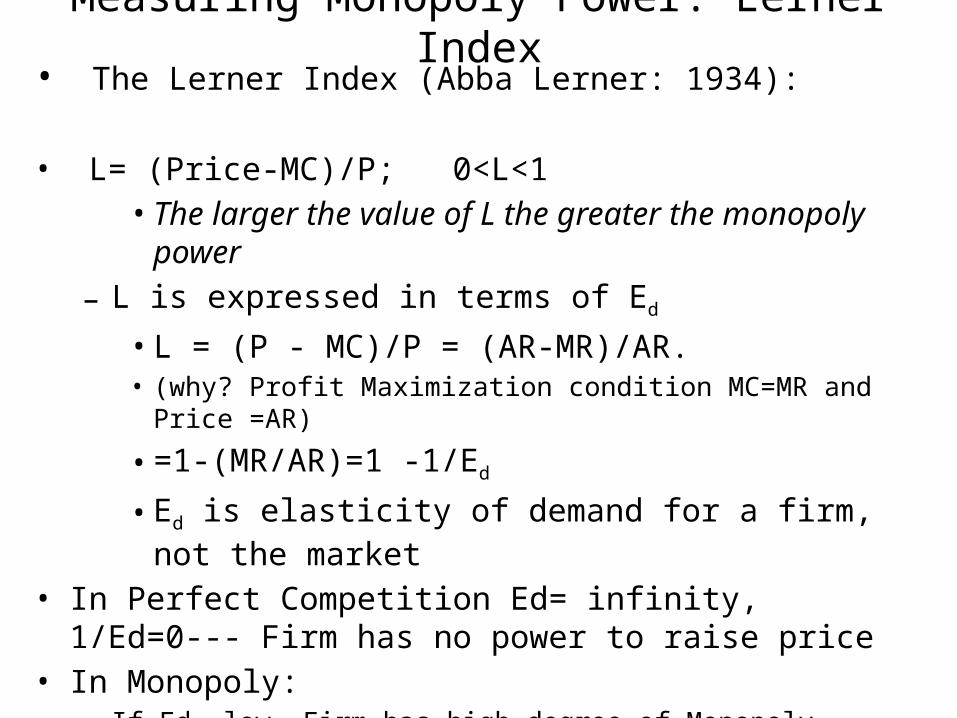

Measuring Monopoly Power: Lerner Index• The Lerner Index (Abba Lerner: 1934):

• L= (Price-MC)/P; 0<L<1• The larger the value of L the greater the monopoly power

– L is expressed in terms of Ed

• L = (P - MC)/P = (AR-MR)/AR. • (why? Profit Maximization condition MC=MR and Price =AR)

• =1-(MR/AR)=1 -1/Ed

• Ed is elasticity of demand for a firm, not the market• In Perfect Competition Ed= infinity, 1/Ed=0--- Firm has no power

to raise price• In Monopoly:

– If Ed= low, Firm has high degree of Monopoly power

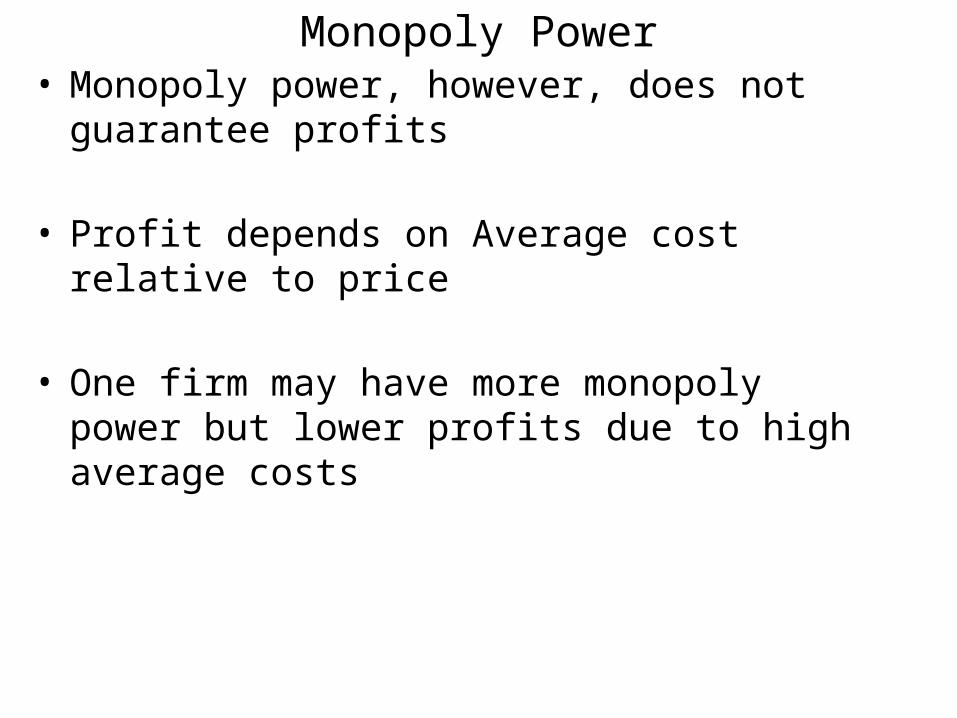

Monopoly Power• Monopoly power, however, does not guarantee

profits

• Profit depends on Average cost relative to price

• One firm may have more monopoly power but lower profits due to high average costs

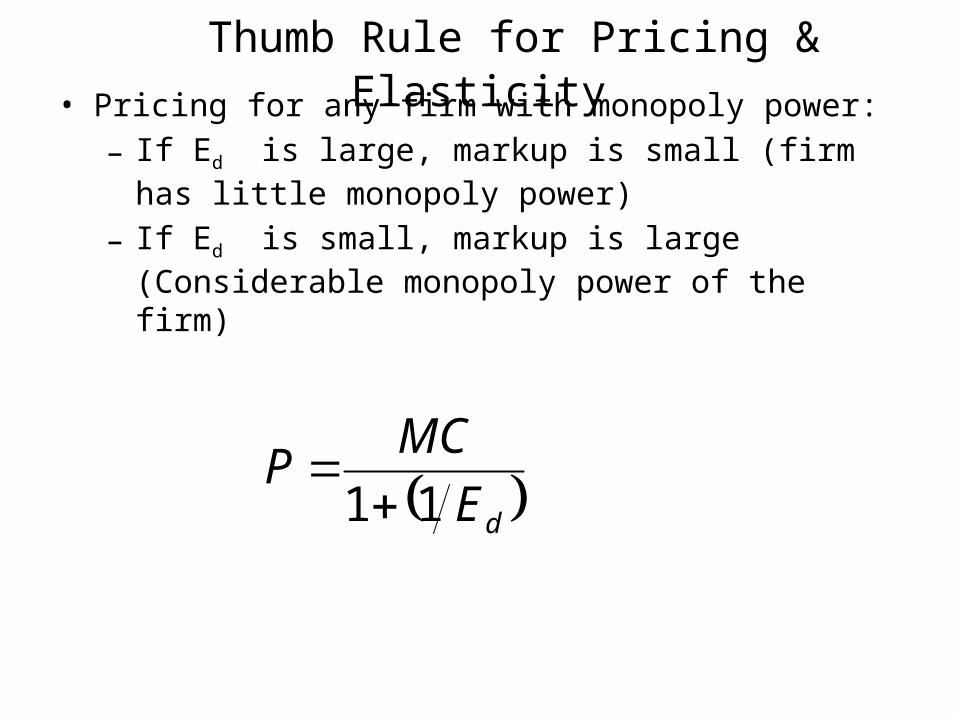

Thumb Rule for Pricing & Elasticity• Pricing for any firm with monopoly power:

– If Ed is large, markup is small (firm has little monopoly power)

– If Ed is small, markup is large (Considerable monopoly power of the firm)

dEMCP11

D

MR

$/Q

Quantity

MC

Q*

P*P*-MC

P*

MR

D

$/Q

Quantity

MC

Q*

P*-MC

The more elastic isdemand, the less the

markup.

Elasticity of Demand and Price Markup

MC. above 11%-10about set Prices .5

)(11.19.01011

.4

stores individualfor 10 3.productSimilar 2.firms Several 1.

MCMCMCP

Ed

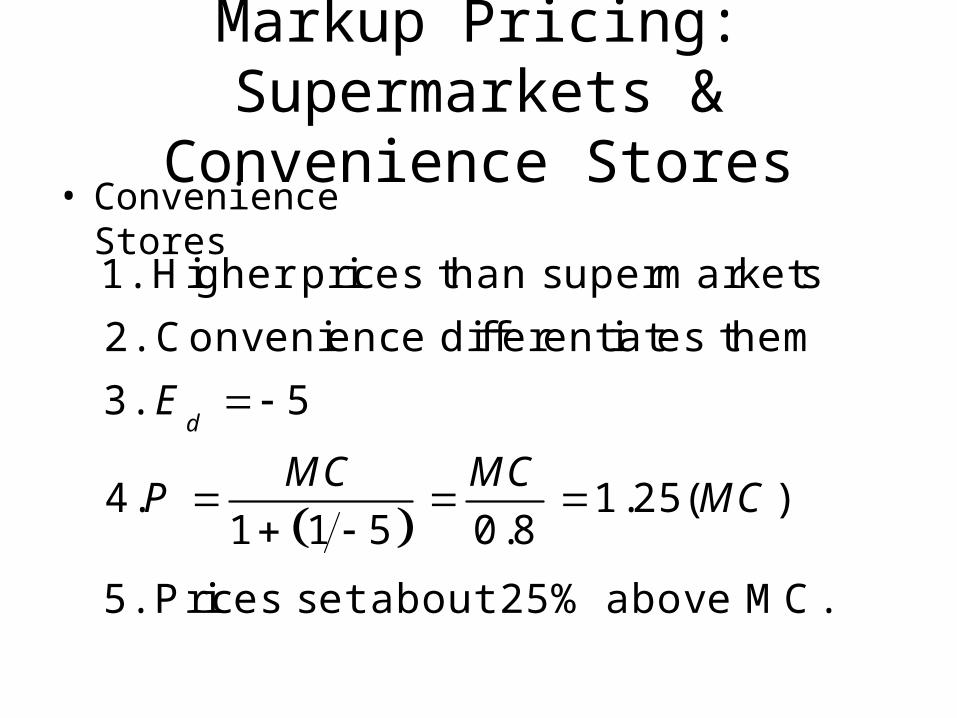

Markup Pricing: Supermarkets & Convenience Stores

• Supermarkets

Markup Pricing: Supermarkets & Convenience Stores

• Convenience Stores

1. Higher prices than supermarkets2. Convenience differentiates them3. 5

4. 1.25( )1 1 5 0.8

5. Prices set about 25% above MC.

dE

MC MCP MC

Markup Pricing: Supermarkets & Convenience Stores

• Convenience stores have more monopoly power, higher mark up but failed to make larger profits. Why?

– Volume is far smaller and average fixed costs are larger

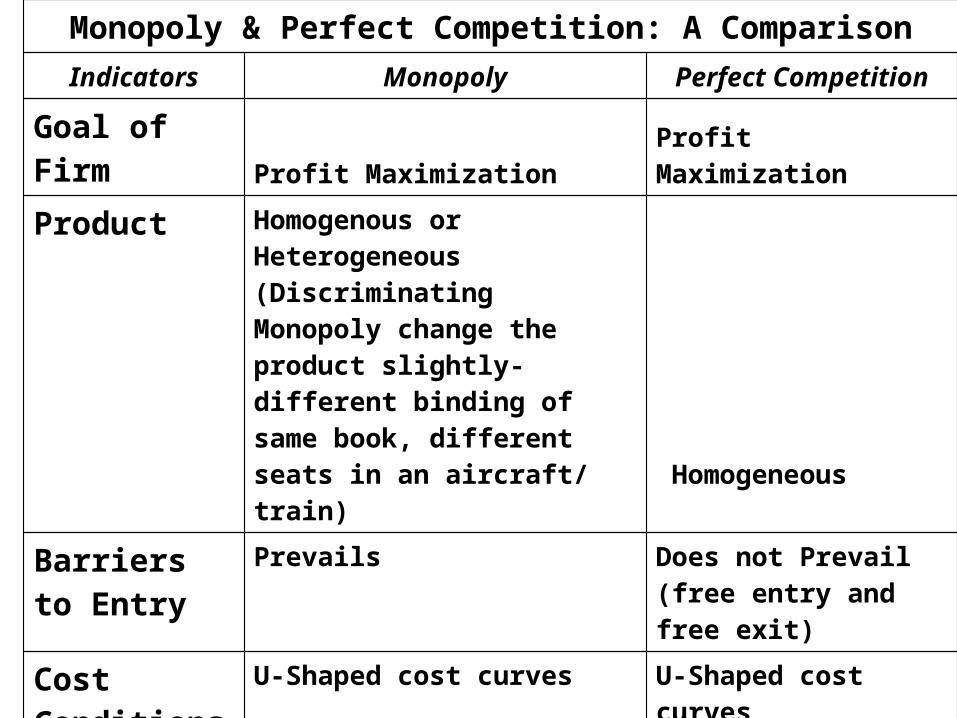

Monopoly & Perfect Competition: A Comparison

Indicators Monopoly Perfect Competition

Goal of Firm Profit Maximization Profit MaximizationProduct

Homogenous or Heterogeneous(Discriminating Monopoly change the product slightly-different binding of same book, different seats in an aircraft/ train)

Homogeneous

Barriers to Entry

Prevails Does not Prevail (free entry and free exit)

Cost Conditions

U-Shaped cost curves U-Shaped cost curves

Knowledge about Market

Perfect Knowledge Perfect Knowledge

Price/Output Decision

Either sets the price or output not both

Price is given, decide about output to be produced

Output Produce smaller output and sells at a higher price Output may be greater than that of Monopoly output and price can be lesser than that charged by Monopoly

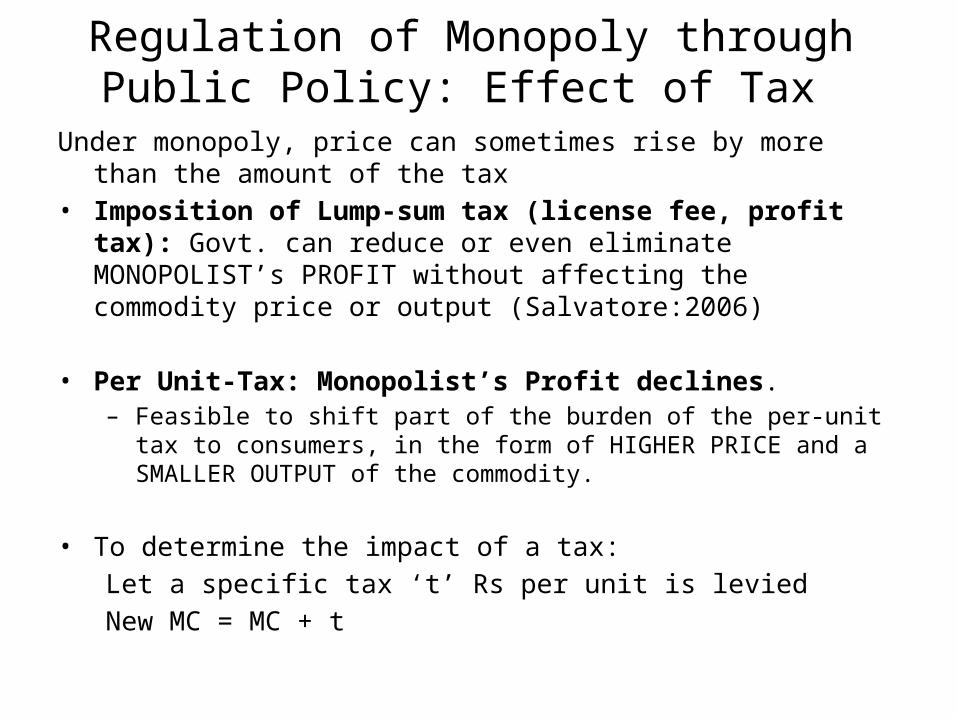

Regulation of Monopoly through Public Policy: Effect of Tax

Under monopoly, price can sometimes rise by more than the amount of the tax

• Imposition of Lump-sum tax (license fee, profit tax): Govt. can reduce or even eliminate MONOPOLIST’s PROFIT without affecting the commodity price or output (Salvatore:2006)

• Per Unit-Tax: Monopolist’s Profit declines. – Feasible to shift part of the burden of the per-unit tax to consumers, in the

form of HIGHER PRICE and a SMALLER OUTPUT of the commodity.

• To determine the impact of a tax:Let a specific tax ‘t’ Rs per unit is levied New MC = MC + t

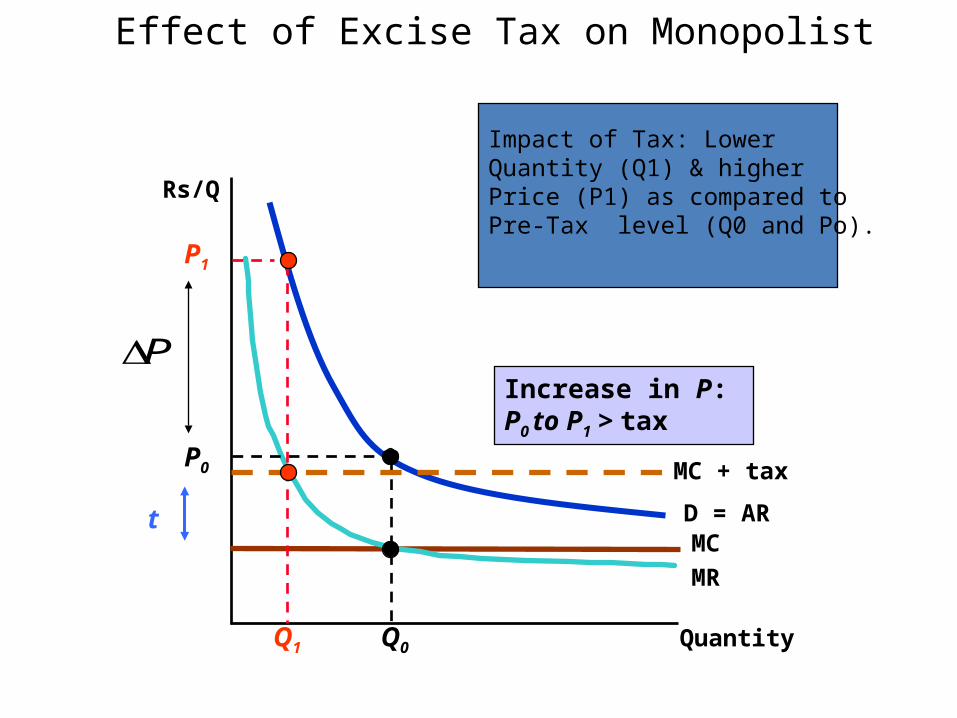

Quantity

Rs/Q

MCD = AR

MR

Q0

P0 MC + tax

t

PIncrease in P: P0 to P1 > tax

Q1

P1

Effect of Excise Tax on Monopolist

Impact of Tax: Lower Quantity (Q1) & higher Price (P1) as compared to Pre-Tax level (Q0 and Po).

Effect of Excise Tax on Monopolist• Amount of PRICE INCREASES with implementation of a TAX

depends on ELASTICITY OF DEMAND

• Price may or may not increase by more than the tax

• Overall Profits for monopolist will fall with a tax

Monopolies & Restrictive Trade Practices • MRTP Act, 1969: To restrict and curb growth of monopoly power in the

country• MRTP Commission set up in 1970

• Govt. imposed restrictions on entry of large business houses in a number of industries, set up a large number of industries in the business sector, and encouraged small and medium industries.

• MRTP Act sought to achieve– Prevention of concentration of economic power – Prohibition of monopolistic and Restrictive and Unfair Trade Practices

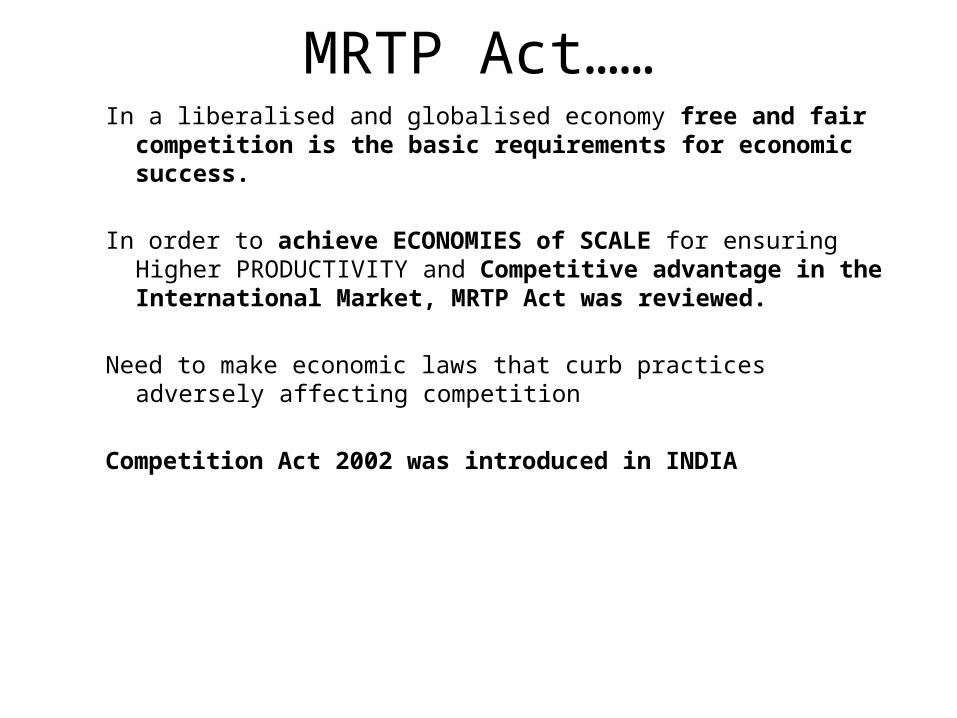

Since 1991, the focus shifted from controlling Monopolies to Promoting Competition. Why?

MRTP Act……In a liberalised and globalised economy free and fair competition is the basic

requirements for economic success.

In order to achieve ECONOMIES of SCALE for ensuring Higher PRODUCTIVITY and Competitive advantage in the International Market, MRTP Act was reviewed.

Need to make economic laws that curb practices adversely affecting competition

Competition Act 2002 was introduced in INDIA

Constituents of MRTP Act• Monopolistic Trade Practices:

A Trade practice which can have the effect of Maintaining the price of goods or charges for the services at an unreasonable level by limiting, reducing or otherwise controlling Production, supply or distribution of goods

Restrictive Trade Practice:Trade practices which has the effect of Preventing, Distorting or Restricting Competition in any

manner.-Tends to obstruct the flow of Capital or resources into the stream of Production

- Tends to Bring about Manipulation of Prices-----Imposition of Unjustified costs or restrictions on the Consumers.

Unfair Trade Practices (incorporated in 1984)To promote sale adopt certain strategy which causes loss or injury to the ConsumersMake False representations and Misleading Advertisement regarding goods and services

Selling or supplying sub-Standard, unsafe, hazardous products

Hoarding, Destroying or refusing to sell in order to push up the price level

Publication of any advertisement for sale or supply at bargain price (of goods or services that are not intended to be offered for sale or supply at the bargain price)

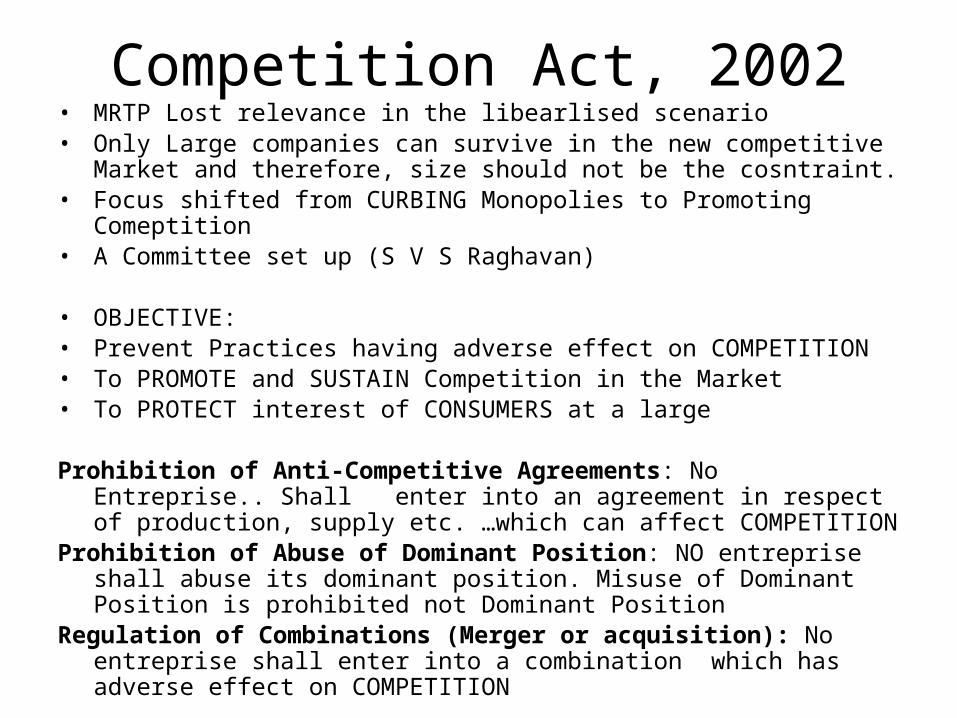

Competition Act, 2002• MRTP Lost relevance in the libearlised scenario• Only Large companies can survive in the new competitive Market and therefore,

size should not be the cosntraint.• Focus shifted from CURBING Monopolies to Promoting Comeptition• A Committee set up (S V S Raghavan)

• OBJECTIVE:• Prevent Practices having adverse effect on COMPETITION• To PROMOTE and SUSTAIN Competition in the Market• To PROTECT interest of CONSUMERS at a large

Prohibition of Anti-Competitive Agreements: No Entreprise.. Shall enter into an agreement in respect of production, supply etc. …which can affect COMPETITION

Prohibition of Abuse of Dominant Position: NO entreprise shall abuse its dominant position. Misuse of Dominant Position is prohibited not Dominant Position

Regulation of Combinations (Merger or acquisition): No entreprise shall enter into a combination which has adverse effect on COMPETITION

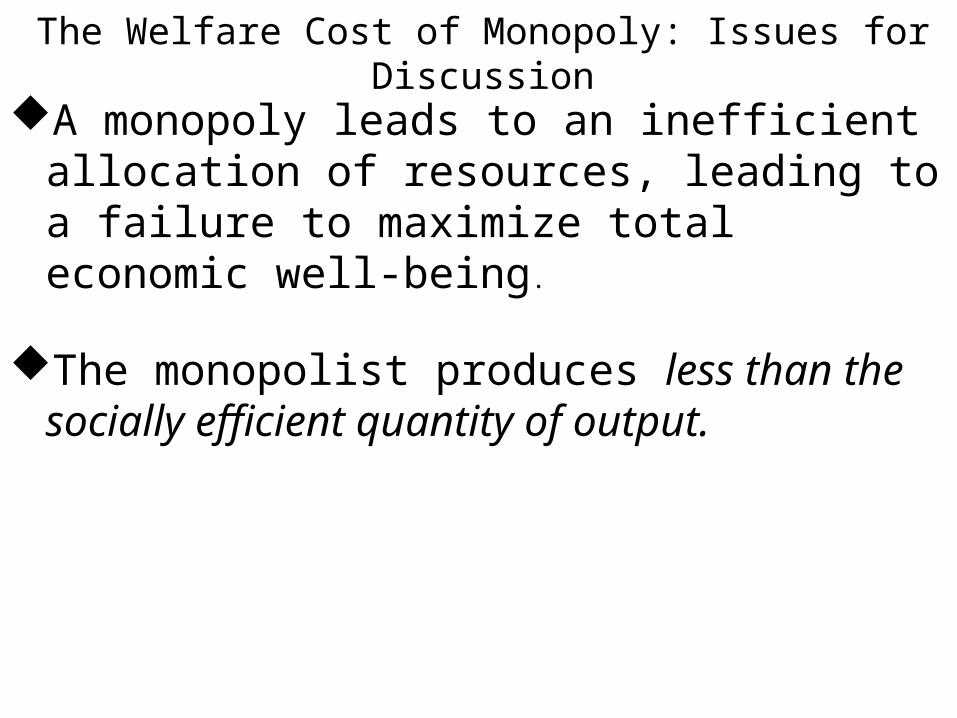

The Welfare Cost of Monopoly: Issues for Discussion

A monopoly leads to an inefficient allocation of resources, leading to a failure to maximize total economic well-being.

The monopolist produces less than the socially efficient quantity of output.

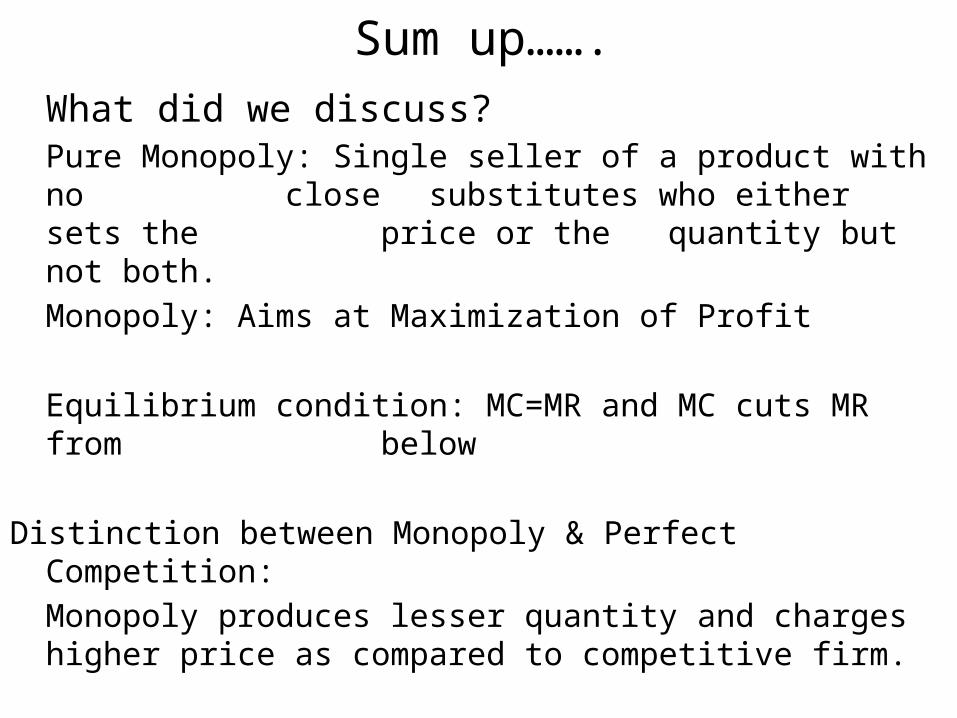

Sum up…….What did we discuss?Pure Monopoly: Single seller of a product with no

close substitutes who either sets the price or the quantity but not both.

Monopoly: Aims at Maximization of Profit

Equilibrium condition: MC=MR and MC cuts MR from below

Distinction between Monopoly & Perfect Competition: Monopoly produces lesser quantity and charges higher price as compared to competitive firm.

Maximization of welfare necessitates regulation of monopoly.

Thanks