Monoply revised

25

MONOPOLY

-

Upload

kinnar-majithia -

Category

Business

-

view

3.682 -

download

2

Transcript of Monoply revised

MONOPOLY

Features of Monopoly

Single seller of an unique product No close substitutes Price Maker- firm has control over price Barriers to entry

Why monopolies arise? Barriers to entry are restrictions on

the entry of new firms into an industry Legal restrictions-licenses and

patents Economies of scale Control of an essential resource- De-

beers owns most of the diamond mines

Natural monopolies

NATURAL MONOPOLIES A monopoly sometimes emerges

naturally when a firm experiences economies of scale as reflected by the downward-sloping, long-run average cost curve

In these situations, a single firm can sometimes supply market demand at a lower average cost per unit than could two or more firms at smaller rates of output

The monopolist can choose either the price or the quantity, but choosing one determines the other

Because the monopolist can select the price that maximizes profit, we say the monopolist is a price maker

More generally, any firm that has some control over what price to charge is a price maker

Competition vs monopoly:

Monopoly Is the sole producer Faces a downward sloping demand curve Is a price maker Reduces price to increase sales

Competition Many producers Faces a horizontal demand curve Is a price taker Sales cannot affect price

Profit maximization for a monopolist: The demand curve for the monopolist is

downward sloping The marginal revenue curve is below the

demand curve The monopolist maximizes profit by

producing the quantity at which marginal revenue equals marginal cost

It then finds uses the demand curve to find the price at which the consumers will buy that commodity

Profit maximization For competition, P= MR= MC For a monopolist, P>MR =MC A monopolist will make economic profit

as long as price is greater than average total cost

A monopolist always operates on the elastic portion of the demand curve

£

Q O

MC

AC

Qm

MR

AR

AC

Profit maximising under monopoly

AR

£

Q O

MC

AC

Qm

MR

AR

AC

Profit maximising under monopoly

AR

Total profit

£

Q O

MC ( = supply under perfect competition)

Q1

MR

P1

P2

Q2

AR = D

Comparison withPerfect competition

Equilibrium of industry under perfect competition and monopoly: with the same MC curve

The Monopolist Minimizes Losses in the Short Run

p

Marginal cost

Average total cost

Average variable cost

Demand D Average revenue

Marginal revenue

0 Q

e

c

b

a

Loss

Quantity per period

Do

llars

per

un

it

A monopolist may not always make profit

Short-Run Losses and the Shutdown Decision

A monopolist is not assured of profit The demand for the monopolists good or

service may not be great enough to generate economic profit in either the short run or the long run

In the short run, the loss-minimizing monopolist must decide whether to produce or to shut down If the price covers average variable cost, the

firm will produce If not, the firm will shut down, at least in

the short run

Monopolist’s Supply Curve

The intersection of a monopolist’s marginal revenue and marginal cost curve identifies the profit maximizing quantity, but the price is found on the demand curve

Thus, there is no curve that shows both price and quantity supplied there is no monopolist supply curve

Dead Weight Loss: Since a monopolist sets its price above the

marginal cost, the high price makes monopoly undesirable.

The monopolist produces a level of output less than the socially efficient level output

The welfare effect of a monopoly is similar to a tax, except that the government gets revenue from the tax whereas the private firm gets the monopoly profit

Dead-Weight Loss:

Price Discrimination Price Discrimination is the business practice of

selling the same good at different prices to different customers even though the cost of producing for the two customers is the same

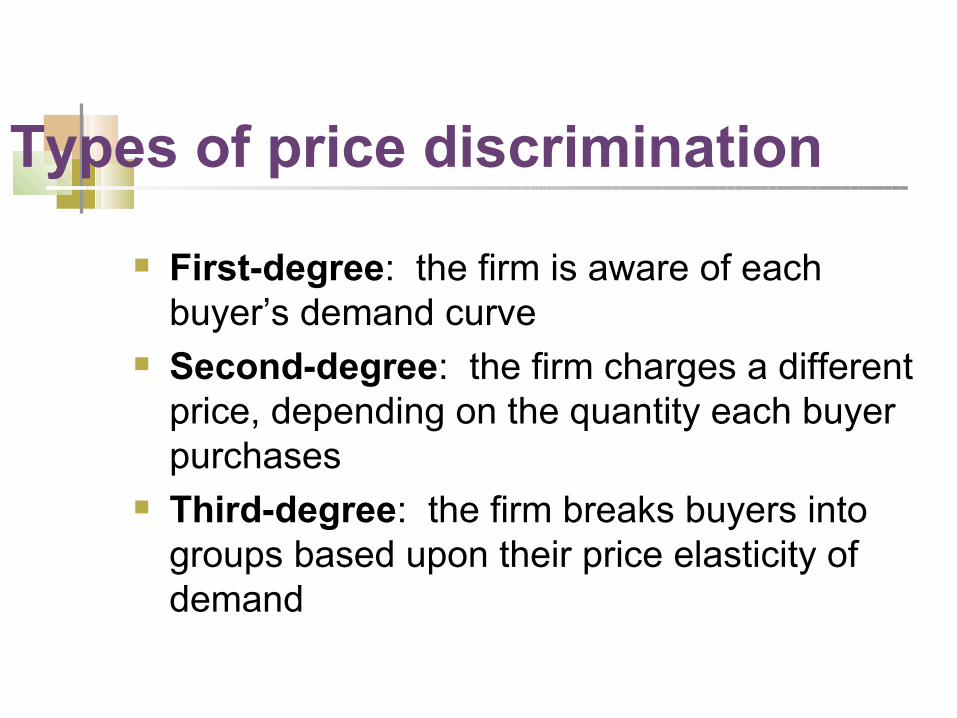

Price discrimination is of three degrees: First degree or perfect price discrimination Second degree or block pricing Third degree price discrimination

First-degree: the firm is aware of each buyer’s demand curve

Second-degree: the firm charges a different price, depending on the quantity each buyer purchases

Third-degree: the firm breaks buyers into groups based upon their price elasticity of demand

Types of price discrimination

Perfect Price Discrimination refers to the situation when the monopolist knows exactly the willingness to pay of each customer and can charge a different price for each unit sold.

In reality perfect price discrimination is not possible .

Block pricing refers to charging a different price for different ranges of quantity sold.

First Degree Price Discrimination(Perfect Price Discrimination)

Each consumer is charged the price he/she is willing to pay.

Producer takes all the consumer surplus

1st. degree price discrimination

Price

Quantity

DemandPL

Q

P1

Q1

1st. degree price discrimination

Price

Quantity

DemandPL

Q

For each consumer price charged=price willing to pay

Monopolist appropriates all consumer surplus

P1P2P3P4..

2nd Degree Price Discrimination(non-linear pricing)

Different price is charged for a different quantity bought (but not across consumers).

set one price for a 1st bundle, a lower price for a 2nd bundle, ....

extract some, but not all of consumer surplusNote:In 3rd deg case=>different prices charged for

different consumersIn 2nd deg case=>different prices charged for

different quantities (for same consumer)

fig

O O OMRX

MRY MRT

MC

DY

5

7

1000 2000 3000

(a) Market X (b) Market Y (c) Total

(markets X + Y)

9

DX

Profit-maximising output underthird degree price discrimination

Price and output in Mkt1 & Mkt2(Maximise Profits)

In Market1

MR1=MC

In Market2

MR2=MC

that is, MR1=MR2=MC

set higher price and sell lower Q in Mkt1 (inelastic D)