Money Rates - Textbook MediaFlow Present values ... The real rate of interest ... foreign currency...

29

Chapter 4 Money Rates

Transcript of Money Rates - Textbook MediaFlow Present values ... The real rate of interest ... foreign currency...

Chapter 4

Money Rates

4-2 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-3 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-4 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Present Value and Interest

Rates

Interest rates and present values move in

opposite directions

4-5 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Present Value and Time to Cash

Flow

Present values become more volatile as

the time to receiving a cash flow

increases

– When interest rates change, the present value of

a near-term cash flow (e.g., 1-year in the future)

changes very little

– When interest rates change, the present value of

a long-term cash flow (e.g., 30-years in the

future) changes by a large amount

4-6 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-7 © 2002, 2012 Frank M. Werner and James A.F. Stoner

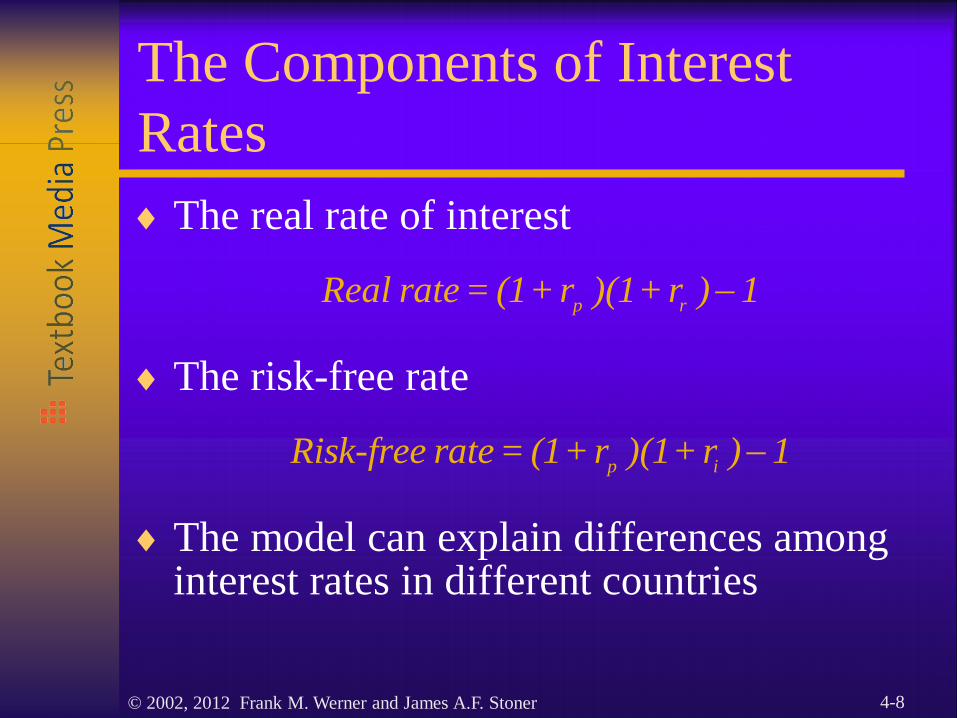

The Components of Interest

Rates

The Fisher Model

– rp = pure rate of interest

– ri = inflation premium

– rr = risk premium

1)r+)(1r+)(1r+(1=rate Nominalrip

4-8 © 2002, 2012 Frank M. Werner and James A.F. Stoner

The Components of Interest

Rates

The real rate of interest

The risk-free rate

The model can explain differences among interest rates in different countries

1)r+)(1r+(1=rate Realrp

1)r+)(1r+(1=rateRisk-free ip

4-9 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Prices and Yields of U.S. Treasury

Securities

4-10 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-11 © 2002, 2012 Frank M. Werner and James A.F. Stoner

The Yield Curve in November

2010

4-12 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Yield Curve Shapes

4-13 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Term Structure of Interest Rates

The expectations hypothesis – the term structure reflects expectations of inflation

The liquidity preference hypothesis – liquidity risk increases with maturity, hence so does investors’ required rate of return

The segmentation or hedging hypothesis – each maturity is a separate market with its own supply and demand, hence its own interest rate

4-14 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-15 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Risk Structure of Interest Rates

Default risk

Interest-rate risk

Reinvestment risk

Marketability risk

Call risk

4-16 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Tax Structure of Interest Rates

– Who Taxes What?

Investors care about after-tax yields

4-17 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-18 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Exchange Rate Systems

Historically – the gold standard

Bretton Woods (1944) – a fixed exchange rate system based on the U.S. dollar

Why Bretton Woods broke down – the underlying economics of countries changed relative to one another – Economies in Europe and Japan strengthened

– The U.S. ran balance of payments deficits in the mid-1960s

– U.S. holdings of gold fell significantly

4-19 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Exchange Rate Systems

in Place Today

Floating exchange rate system – currency values adjust continuously in the public markets

Managed (dirty) float – government influences a floating exchange rate

Pegged float – a currency is fixed against another which floats

4-20 © 2002, 2012 Frank M. Werner and James A.F. Stoner

The Euro

Sixteen members of the European Union have replaced their currencies with the Euro, a common currency

4-21 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-22 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Foreign Exchange Market

Quotations

Direct (American) rates – the price of a

foreign currency in domestic money

Reciprocal (European, Continental) rates

– the number of units of a foreign

currency needed to buy one unit of

domestic currency

Cross rates – the price of one foreign

currency in terms of another, calculated

via their relationships to a third currency

4-23 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Exchange Rate Quotations

4-24 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-25 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Spot and Forward Rates

Spot rate – a rate quoted for an immediate

trade

Forward rate – a rate quoted for a contract

to be entered into today binding the

parties to a trade to take place in the

future

4-26 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Forward Discount or Premium

Forward discount – the amount by which

forward rates are less than spot rates

Forward premium – the amount by which

forward rates are greater than spot rates

Calculation

forward months

12

spot

spotforward

4-27 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Money Rates

Introductory concepts – interest rates, present value, and time

The components of interest rates

The term structure of interest rates

Other interest rate structures

Exchange rate systems

Foreign exchange market quotations

Spot and forward rates

Business exposure to exchange rates

4-28 © 2002, 2012 Frank M. Werner and James A.F. Stoner

Business Exposure to

Exchange Rates

Transaction exposure – exposure to losses

on day-to-day transactions

Translation exposure – exposure to losses

of accounting income and book values

Economic exposure – exposure to

changes in the value of monetary assets

and liabilities and to reduction in cash

flow

4-29 © 2002, 2012 Frank M. Werner and James A.F. Stoner

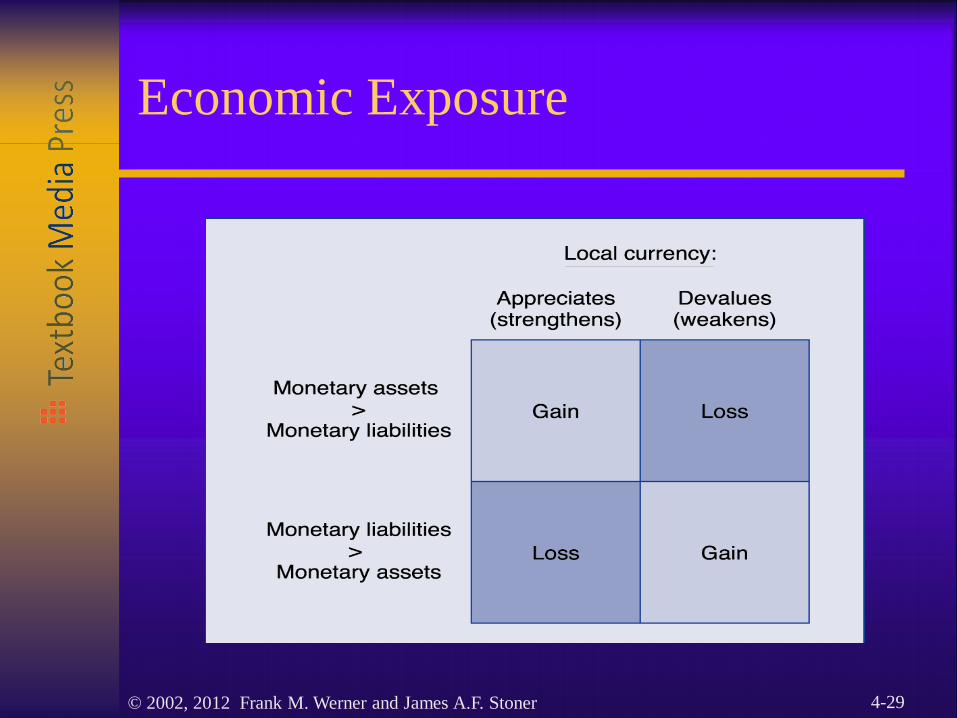

Economic Exposure