Money and Inflation The Quantity Theory of Money Economics Senior Seminar 2005.

45

Money and Money and Inflation Inflation The Quantity Theory of The Quantity Theory of Money Money Economics Senior Seminar 2005 Economics Senior Seminar 2005

-

date post

18-Dec-2015 -

Category

Documents

-

view

225 -

download

2

Transcript of Money and Inflation The Quantity Theory of Money Economics Senior Seminar 2005.

Money and InflationMoney and Inflation

The Quantity Theory of MoneyThe Quantity Theory of Money

Economics Senior Seminar 2005Economics Senior Seminar 2005

22

The “Equation of Exchange”The “Equation of Exchange”

MMVV = = PPYYMoney supplyMoney supply x x velocityvelocity = = price levelprice level x x incomeincome

We can treat velocity as fairly constantWe can treat velocity as fairly constant

We know that income is affected by real We know that income is affected by real inputs like the availability of labor, capital, inputs like the availability of labor, capital, and technology—and technology—not not the money supplythe money supply

3

Velocity

Source: Mankiw, Principles of Macroeconomics, 3rd ed. (2004), instructor ancillaries

44

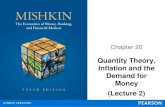

Money Supply and PricesMoney Supply and Prices

MMVV = = PPYY If If velocityvelocity is constant and is constant and incomeincome is not is not

determined by the money supply (in the long determined by the money supply (in the long run), then:run), then: All that’s left is All that’s left is MM and and PP, and they have to move , and they have to move

together.together.

When MWhen M↑↑, P, P↑↑..

5

Money Supply and the Price Level

Source: Mankiw, Principles of Macroeconomics, 3rd ed. (2004), instructor ancillaries

6

Money Supply and the Price Level

Source: Mankiw, Principles of Macroeconomics, 3rd ed. (2004), instructor ancillaries

77

Early KeynesiansEarly Keynesians

Early Keynesians suggested that apparent Early Keynesians suggested that apparent money supply increases were ineffective in money supply increases were ineffective in stopping the Great Depressionstopping the Great Depression

During the Depression, rates on U.S. During the Depression, rates on U.S. Treasury securities dropped very lowTreasury securities dropped very low

Investment also stayed low despite low Investment also stayed low despite low interest ratesinterest rates

Fiscal policy was their prescriptionFiscal policy was their prescription

88

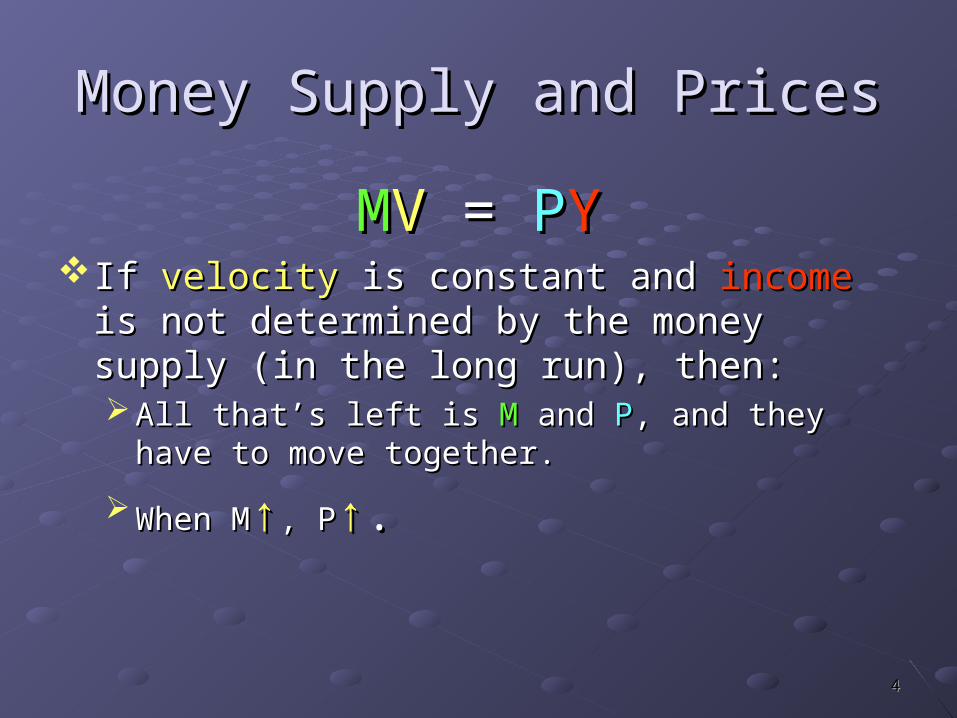

Early MonetaristsEarly Monetarists

In the 1960s, the monetarists showed that In the 1960s, the monetarists showed that Depression-era monetary policy was Depression-era monetary policy was contractionarycontractionary, and that real interest rates , and that real interest rates were actually considerably higher than the were actually considerably higher than the Keynesians had indicated.Keynesians had indicated.

They concluded that in the short run, the Fed They concluded that in the short run, the Fed should have increased the money supply to should have increased the money supply to counteract the contraction caused by bank counteract the contraction caused by bank failures, etc.failures, etc.

99

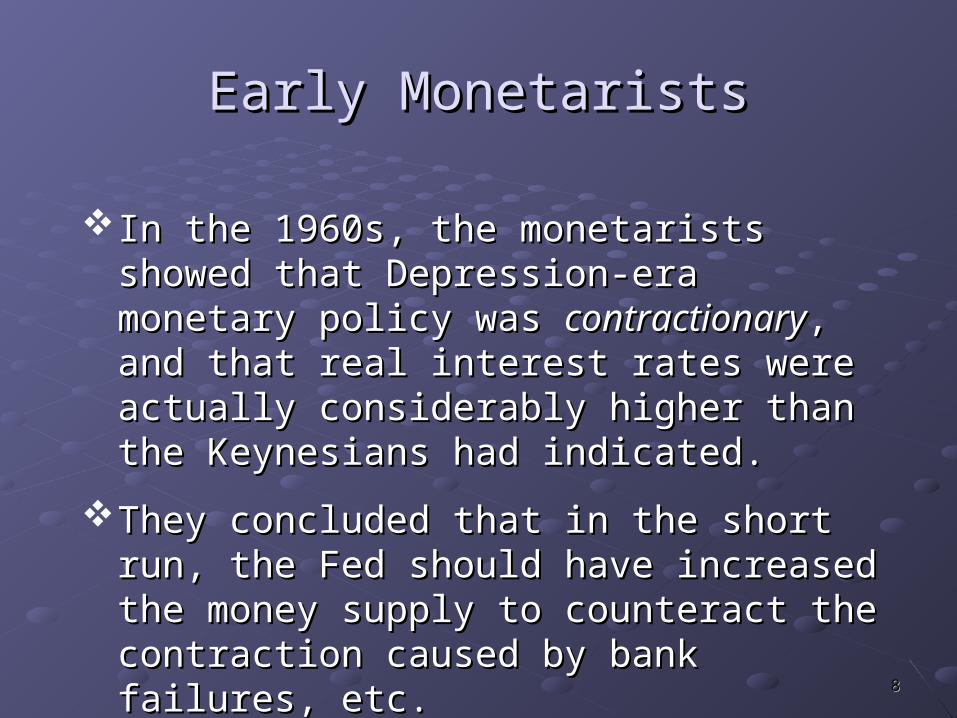

Costs of InflationCosts of Inflation

““Shoeleather costs”Shoeleather costs”With higher interest rates, the opportunity cost With higher interest rates, the opportunity cost

of holding money is higherof holding money is higherSo people make more frequent transactions So people make more frequent transactions

with a bank to hold lower average money with a bank to hold lower average money balancesbalances

1010

Costs of InflationCosts of Inflation

Menu costsMenu costsInflation means that firms have to change Inflation means that firms have to change

their nominal prices more oftentheir nominal prices more often Print and mail new catalogsPrint and mail new catalogs Communicate new prices to sales forceCommunicate new prices to sales force

1111

Costs of InflationCosts of Inflation

Changing relative costsChanging relative costsNot all prices change at the same rate—some Not all prices change at the same rate—some

are “stickier” than othersare “stickier” than othersTherefore, relative prices changeTherefore, relative prices change

Price level increase

Apples Pears

People switch from apples to pears—decisions are distorted!

1212

Costs of InflationCosts of Inflation

Price “stickiness” is not the only reason for Price “stickiness” is not the only reason for relative price changesrelative price changesWhere the new money enters the economy is Where the new money enters the economy is

important.important.If the government spends the new money first, If the government spends the new money first,

then the things government buys will see then the things government buys will see price increases firstprice increases first Who gains? People who sell to the governmentWho gains? People who sell to the government Who loses? People who are in competition with the Who loses? People who are in competition with the

government, who buy what it buysgovernment, who buy what it buys

1313

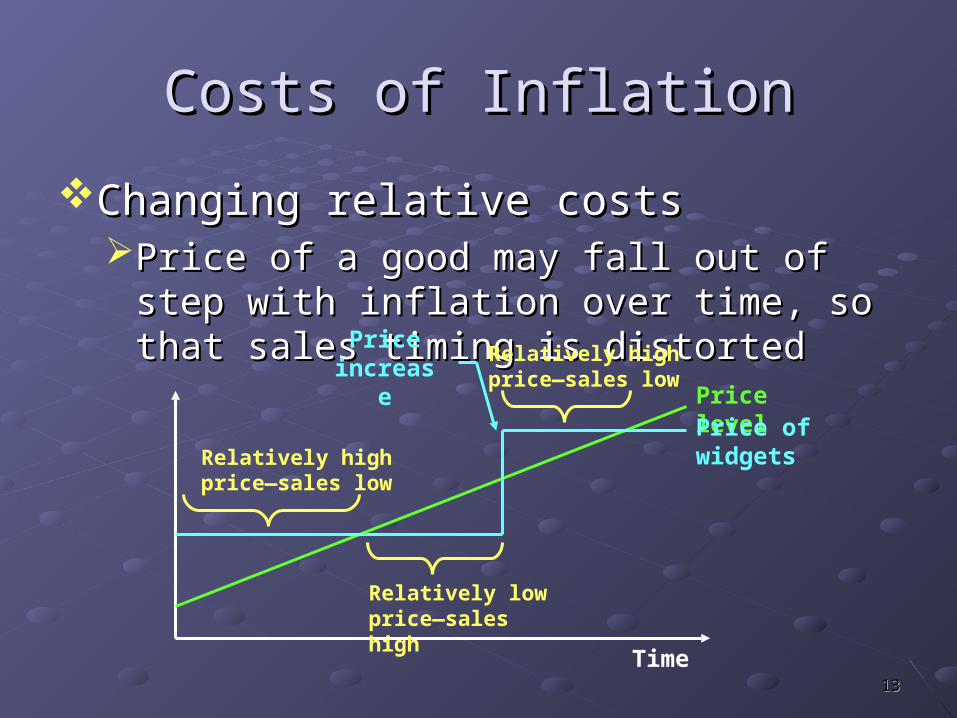

Costs of InflationCosts of Inflation

Changing relative costsChanging relative costsPrice of a good may fall out of step with Price of a good may fall out of step with

inflation over time, so that sales timing is inflation over time, so that sales timing is distorteddistorted

Price level

Time

Price of widgetsRelatively high

price—sales low

Relatively low price—sales high

Relatively high price—sales lowPrice

increase

1414

Costs of InflationCosts of Inflation

Loss of informationLoss of informationInconveniences associated with a changing Inconveniences associated with a changing

standardstandard

1515

Costs of InflationCosts of Inflation

Unexpectedly high inflation is redistributiveUnexpectedly high inflation is redistributiveWith fixed interest rates, lenders lose, as With fixed interest rates, lenders lose, as

purchasing power of repayment is lower than purchasing power of repayment is lower than was anticipated.was anticipated.

Borrowers gainBorrowers gain

Unexpectedly low inflation redistributes as Unexpectedly low inflation redistributes as wellwellLenders gain, borrowers loseLenders gain, borrowers lose

1616

Costs of InflationCosts of Inflation

Inflation can create business cyclesInflation can create business cyclesPushing interest rates down can create the Pushing interest rates down can create the

impression that long-term projects are more impression that long-term projects are more profitableprofitable

People invest in those long-term projects by People invest in those long-term projects by buying capital for thembuying capital for them

When the interest rate comes back up from its When the interest rate comes back up from its artificially low levels, the capital investments artificially low levels, the capital investments lose valuelose value

Stock prices drop, people are laid off.Stock prices drop, people are laid off.

1717

Inflation and Business CyclesInflation and Business Cycles

D

S S’

Loanable funds

Inte

rest

ra

te

i’

i

S=I S’=I’

Increase in willingness to save

D

S S+M

Loanable funds

Inte

rest

rat

e

i’

i

S=I I’S’

Unsustainable separation of saving & investment

Increase in money supplyvs.

1818

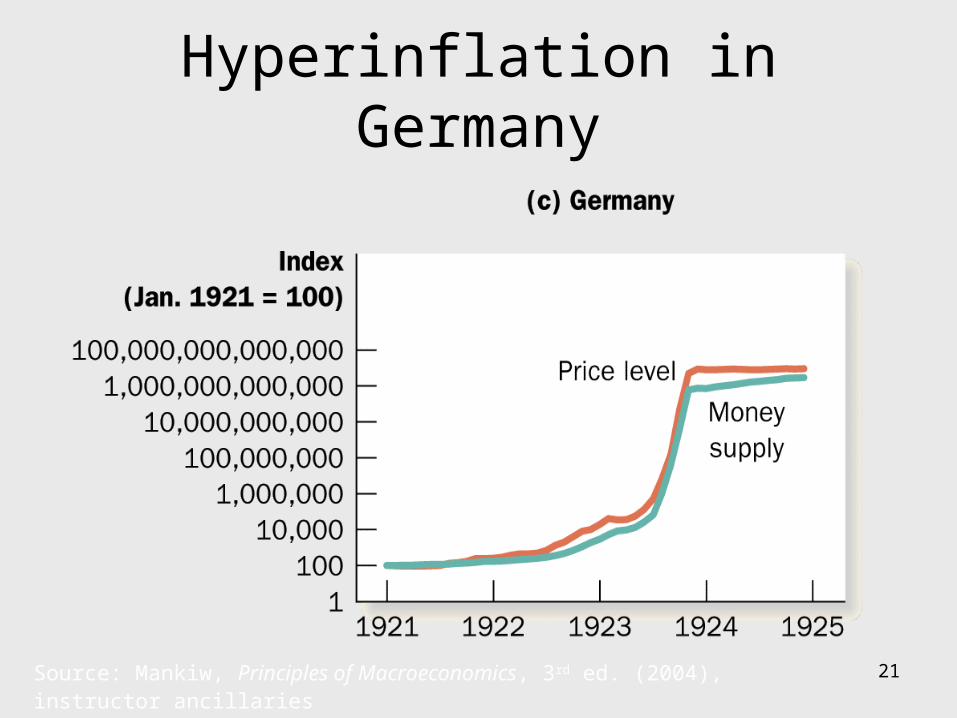

Hyperinflation in GermanyHyperinflation in Germany

At the end of World War I, Germany was At the end of World War I, Germany was required to pay reparations to the Alliesrequired to pay reparations to the Allies

Germany began running large deficitsGermany began running large deficitsUnable to tax or borrow enough to pay, Unable to tax or borrow enough to pay,

Germany began printing large quantities of Germany began printing large quantities of money.money.

Prices started to rise.Prices started to rise.

1919

Hyperinflation in GermanyHyperinflation in Germany

Price of a Price of a newspaper in newspaper in Germany, Germany, 1921-1923:1921-1923:

January 1921January 1921 0.300.30

May 1922May 1922 11

October 1922October 1922 88

February 1923February 1923 100100

September 1923September 1923 1,0001,000

October 1, 1923October 1, 1923 2,0002,000

October 15October 15 20,00020,000

October 29October 29 1,000,0001,000,000

November 9November 9 15,000,00015,000,000

November 17November 17 70,000,00070,000,000

Date Price in marks

Source: Mankiw, Macroeconomics, 5th ed., pp. 105-106

2020

Hyperinflation in GermanyHyperinflation in Germany

21

Hyperinflation in Germany

Source: Mankiw, Principles of Macroeconomics, 3rd ed. (2004), instructor ancillaries

2222

Hyperinflation in GermanyHyperinflation in Germany

Fiscal reform ended the inflationFiscal reform ended the inflationAt the end of 1923, the number of government At the end of 1923, the number of government

employees was cut by a thirdemployees was cut by a thirdA new central bank was createdA new central bank was created

This demonstrated a commitment to not printing This demonstrated a commitment to not printing moneymoney

Source: Mankiw, Macroeconomics, 5th ed., pp. 105-106

2323

Hyperinflation in YugoslaviaHyperinflation in Yugoslavia

From 1971-1991, Yugoslavia had an From 1971-1991, Yugoslavia had an average annual inflation rate of 76%average annual inflation rate of 76%Only Zaire and Brazil had a higher inflation Only Zaire and Brazil had a higher inflation

rate.rate.

In December 1990, the Serbian parliament In December 1990, the Serbian parliament ordered the Serbian National Bank (a ordered the Serbian National Bank (a regional central bank) to issue large regional central bank) to issue large amounts of credits to friends of Slobodan amounts of credits to friends of Slobodan Milosevic.Milosevic.

Source: Steve Hanke in April 28, 1999 Wall Street Journal

2424

Hyperinflation in YugoslaviaHyperinflation in Yugoslavia

This amounted to more than half the This amounted to more than half the planned increase in the money supply for planned increase in the money supply for all of Yugoslavia in 1991all of Yugoslavia in 1991

Croatia and Slovenia broke awayCroatia and Slovenia broke awayIn January 1992, hyperinflation beganIn January 1992, hyperinflation began

Source: Steve Hanke in April 28, 1999 Wall Street Journal

2525

Hyperinflation in YugoslaviaHyperinflation in Yugoslavia

In January 1994, the official monthly In January 1994, the official monthly inflation rate reached 313 million percentinflation rate reached 313 million percentThis was the second-highest monthly rate This was the second-highest monthly rate

(after Hungary in 1946)(after Hungary in 1946)……and the second-longest (after the Soviet and the second-longest (after the Soviet

hyperinflation of the early 1920s)hyperinflation of the early 1920s)People spent their time trying to exchange People spent their time trying to exchange

dinars for marks or dollars on the black dinars for marks or dollars on the black marketmarket

Source: Steve Hanke in April 28, 1999 Wall Street Journal

2626

Hyperinflation in YugoslaviaHyperinflation in Yugoslavia

The Yugoslav mint was producing 900,000 The Yugoslav mint was producing 900,000 bank notes a month, in denominations of bank notes a month, in denominations of up to 500 billion dinarsup to 500 billion dinars

Source: Steve Hanke in April 28, 1999 Wall Street Journal; image from National Bank of Serbia

2727

Hyperinflation in YugoslaviaHyperinflation in Yugoslavia

On January 6, 1994, the government gave On January 6, 1994, the government gave up and declared the German mark legal up and declared the German mark legal tendertenderTying a “superdinar” to the mark reduced Tying a “superdinar” to the mark reduced

inflationinflation

Source: Steve Hanke in April 28, 1999 Wall Street Journal

2828

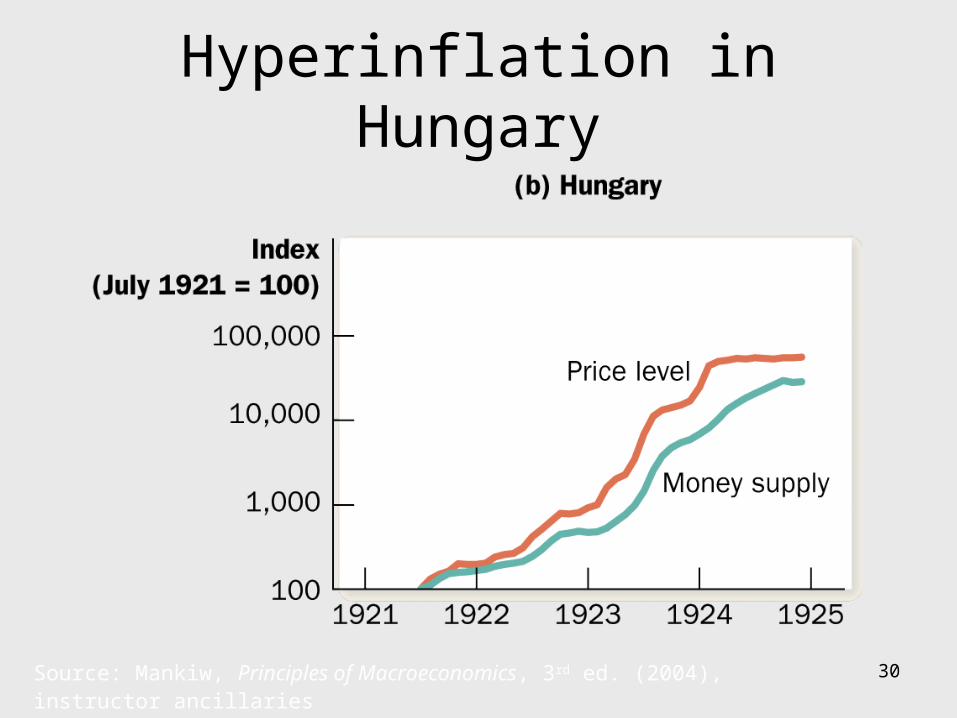

Three Other HyperinflationsThree Other Hyperinflations

Austria (1921-1923) Austria (1921-1923) Hungary (1921-1924)Hungary (1921-1924)Poland (1922-1924)Poland (1922-1924)

29

Hyperinflation in Austria

Source: Mankiw, Principles of Macroeconomics, 3rd ed. (2004), instructor ancillaries

30

Hyperinflation in Hungary

Source: Mankiw, Principles of Macroeconomics, 3rd ed. (2004), instructor ancillaries

3131

Hyperinflation in HungaryHyperinflation in Hungary

1946 hyperinflation was even worse1946 hyperinflation was even worseResulted in largest denomination note ever Resulted in largest denomination note ever

issued by any country:issued by any country:

Image source: Tom Chao’s Paper Money Gallery: http://www.tomchao.com/eu/eu29a.html

100 Million Bil-Pengo (1946): 100,000,000,000,000,000 units

32

Hyperinflation in Poland

Source: Mankiw, Principles of Macroeconomics, 3rd ed. (2004), instructor ancillaries

3333

Inflation TodayInflation Today

1984-19931984-1993 1994-19981994-1998 1999-20031999-2003 20032003

USUS 3.83.8 2.42.4 1.81.8 1.71.7

Advanced Advanced economieseconomies

4.24.2 2.22.2 1.81.8 1.71.7

Developing Developing countriescountries

48.548.5 22.922.9 6.16.1 6.06.0

Transitional Transitional economieseconomies

72.872.8 100.0100.0 20.120.1 8.88.8

Consumer Price Inflation Rates, 1984-2003

Source: http://business.baylor.edu/Steve_Gardner/LECOUT02c.html

3434

Inflation TodayInflation Today

Source: http://www.infoplease.com/ipa/A0762380.html

HIGHEST INFLATION3: 20031. Zimbabwe 383.4%

2. Angola 106.0

3. Myanmar 52.8

4. Haiti 37.3

5. Venezuela 31.1

6. Belarus 30.0

7. Iraq 27.5

8. Malawi 27.4

9. Ghana 26.4

10. Uzbekistan 21.9

3535

Stopping InflationStopping InflationPreserve alternative means of raising fundsPreserve alternative means of raising fundsPrice controlsPrice controls

Hidden inflation—monetary price increases but is not Hidden inflation—monetary price increases but is not measuredmeasured Black market transactionsBlack market transactions Hidden quality deteriorationHidden quality deterioration

Repressed inflation—shortages and queues developRepressed inflation—shortages and queues develop

Central bank independenceCentral bank independence More independent central banks produce less inflationMore independent central banks produce less inflation

Source: http://business.baylor.edu/Steve_Gardner/LECOUT02c.html

3636

Stopping InflationStopping InflationCurrency boardsCurrency boards

Link currency to a trusted foreign currencyLink currency to a trusted foreign currency Can still fail (Argentina) Can still fail (Argentina)

Commodity standardCommodity standard Historically—metals, tobacco, real estate…Historically—metals, tobacco, real estate…

3737

Price StabilityPrice Stability

To minimize uncertainty, Friedman and others To minimize uncertainty, Friedman and others have suggested a have suggested a fixed money growth rate fixed money growth rate rulerule..

New classicals: active monetary and fiscal New classicals: active monetary and fiscal policy is generally a bad idea.policy is generally a bad idea.

However, even countries that have required However, even countries that have required their central banks to follow such rules have their central banks to follow such rules have allowed them some discretion—because it is allowed them some discretion—because it is understood that money growth will have a understood that money growth will have a short-run impact.short-run impact.

3838

What About Gold?What About Gold?

What if the U.S. were to return to a gold What if the U.S. were to return to a gold standard?standard?

Central bank, and/or private banks, would Central bank, and/or private banks, would be required to exchange dollars for gold at be required to exchange dollars for gold at a fixed ratea fixed rate

Appeal: nature fixes supply of gold, not Appeal: nature fixes supply of gold, not subject to political whimsubject to political whim

3939

What About Gold?What About Gold?

David Ricardo (1817):David Ricardo (1817):

““Though it (paper money) has no intrinsic value, yet, Though it (paper money) has no intrinsic value, yet, by limiting its quantity, its value in exchange is as by limiting its quantity, its value in exchange is as great as an equal denomination of coins…. great as an equal denomination of coins…. Experience, however, shows that neither a state nor Experience, however, shows that neither a state nor bank ever has had the unrestricted power of issuing bank ever has had the unrestricted power of issuing paper money without abusing that power…paper money without abusing that power…

4040

What About Gold?What About Gold?

David Ricardo (1817):David Ricardo (1817):

“…“…in all states, therefore, the issue of paper money in all states, therefore, the issue of paper money ought to be under some check and control; and none ought to be under some check and control; and none seems so proper for that purpose as that of subjecting seems so proper for that purpose as that of subjecting the issuers…to the obligation of paying their notes the issuers…to the obligation of paying their notes either in gold coin or bullion.”either in gold coin or bullion.”

4141

What About Gold?What About Gold?

Problem 1: what about the official dollar-to-Problem 1: what about the official dollar-to-gold ratio?gold ratio?Inflation can occur even under a gold standardInflation can occur even under a gold standardAltering the ratio has been doneAltering the ratio has been done

Jan. 31, 1934: FDR changed the dollar from $20.67 Jan. 31, 1934: FDR changed the dollar from $20.67 per ounce to $35 per ounceper ounce to $35 per ounce

Devaluation may impose a credibility cost…Devaluation may impose a credibility cost…but some avoid announcement and allow black but some avoid announcement and allow black

marketsmarkets

4242

What About Gold?What About Gold?

Problem 2: what about emergencies when Problem 2: what about emergencies when the government leaves the gold standard?the government leaves the gold standard?This has been doneThis has been done

1933: FDR prohibited withdrawals of gold or silver1933: FDR prohibited withdrawals of gold or silver 1971: Nixon ended the last vestiges of the gold 1971: Nixon ended the last vestiges of the gold

standard by preventing foreign central banks from standard by preventing foreign central banks from “cashing in” their dollars for gold“cashing in” their dollars for gold

4343

What About Gold?What About Gold?

Gold standard is not foolproof guard Gold standard is not foolproof guard against untrustworthy governmentsagainst untrustworthy governments--But inflation has been higher without it!--But inflation has been higher without it!

4444

What About Gold?What About Gold?

Inflation can still occur under a gold Inflation can still occur under a gold standardstandardWhen Spain imported gold and silver from the When Spain imported gold and silver from the

New World, the money supply in Europe tripled.New World, the money supply in Europe tripled. Spanish prices were 340% higher in 1600 than they Spanish prices were 340% higher in 1600 than they

had been in 1500had been in 1500 England had a price increase of almost 260%England had a price increase of almost 260% France had a rise of about 220%France had a rise of about 220% This is still far less than even the relatively low-This is still far less than even the relatively low-

inflation US in the 20inflation US in the 20 thth century century

4545

Main PointsMain Points

Increases in the money supply produce Increases in the money supply produce increases in pricesincreases in prices

Price increases cause misallocation of Price increases cause misallocation of resourcesresources

Inflation might be reduced by Inflation might be reduced by preserving alternative means of raising fundspreserving alternative means of raising fundscentral bank independencecentral bank independencetying currency to a foreign currency, or tying currency to a foreign currency, or a commodity standarda commodity standard