Money and credit economics class 10

16

By Pawan Rai Class - 10 th A

Transcript of Money and credit economics class 10

By Pawan Rai

Class- 10th A

Before the development of a medium of

exchange, people would barter to obtain the

goods and services they needed. This is

basically how it worked: two individuals

each possessing a commodity the other

wanted or needed would enter into an

agreement to trade their goods.

This early form of barter, however, does

not provide the transferability and

divisibility that makes trading efficient.

For instance, if you have cows but need

bananas, you must find someone who not

only has bananas but also the desire for

meat. What if you find someone who has

the need for meat but no bananas and

can only offer you apple? To get your

meat, he or she must find someone who

has bananas and wants apple.

The lack of transferability of bartering for goods, as you

can see, is tiring, confusing and inefficient. But that is not

where the problems end: even if you find someone with

whom to trade meat for bananas, you may not think a

bunch of them is worth a whole cow. You would then

have to devise a way to divide your cow and determine

how many bananas you are willing to take for certain

parts of your cow.

To solve these problems came commodity money, which

is a kind of currency based on the value of an underlying

commodity.

Money act as an intermediate in the exchange process.

Currency is authorized by the government as medium of

exchange.

The use of money spans a large part of our everyday life. In transactions, goods are being bought and sold with use of money. In some transactions, services are being exchanged with money. When both parties have to agree to sell and buy each others commodities this is known as Double coincidence of wants. In contract, in an economy where money is in use, money by providing the crucial intermediate step eliminates the need for double coincidence of wants. Once he has exchanged his goods for money, he can purchase other goods in market. Since money as an intermediate in the exchange process. It is called a medium of exchange.

Before the introduction coins, a variety of objects was

used as money. For example, since the very early ages,

Indians used grains and cattle as money. Thereafter came

the use of metallic coins.

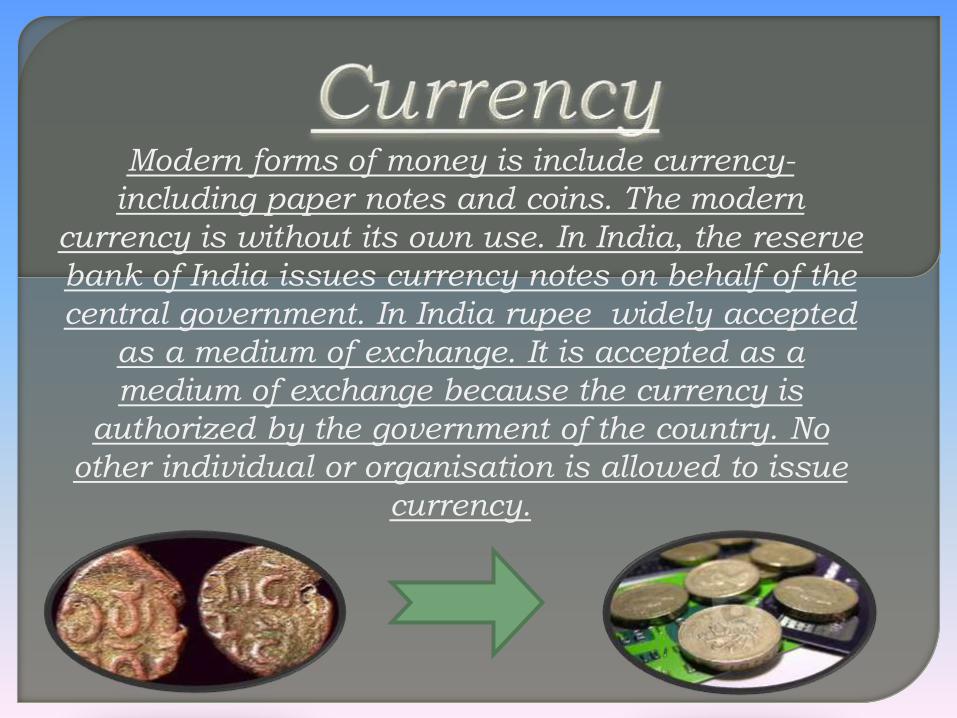

Modern forms of money is include currency-

including paper notes and coins. The modern

currency is without its own use. In India, the reserve

bank of India issues currency notes on behalf of the

central government. In India rupee widely accepted

as a medium of exchange. It is accepted as a

medium of exchange because the currency is

authorized by the government of the country. No

other individual or organisation is allowed to issue

currency.

The other form in which people hold money is as deposits

with banks. At a point of time, people need only some

currency for their day-to-day needs. Banks accept the

deposits and also pay an interest rate on the deposits.

Since the deposits in the bank accounts can be withdrawn

on demand, these deposits are called demand deposits.

For payments payer can made a cheque if he has an

account in bank . A cheque is a paper instructing the bank

to pay a specific amount from the person’s account to

person in whose name cheque has made. Thus, demand

deposits share the essential features of money. The

modern form of money- currency and deposits- are closely

linked to the working of the modern banking system.

There is an interesting mechanism at

work here. Banks keep only a small

proportion of their deposits as cash

with themselves. Banks use the major

portion of the deposit to extend loans.

The difference between what is charged

from borrowers and what is paid to

depositors is their main source of

income.

A large number of transactions in our day to day

activities involve credit in some form or the other.

CREDIT: It refers to an agreement in which lender

supplies the borrowers with money, goods,

services in return for the promise of future

payments.

Credit plays a vital and positive role as well

as a negative role.

Whether credit will be useful or not depends upon

the risks in the situation & on whether there is

some support, in case of loss.

Credit—in its negative role—(debt-trap)

In the rural areas the main demand for

the credit is for the crop production.

Crop production involves considerable

cost on seeds, fertilizers, pesticides,

water, electricity, repair of equipment

etc..

Farmers usually take crop loans at the

beginning of the season and repay loan

after harvest.

Repayment of the loan is dependent on the income from farming.

At times repayment of the loan becomes difficult and credit instead of improving the earnings,

pushes the borrower into a situation from which recovery is very difficult & painful .this situation is called DEBT TRAP

- Interest rate

- Collateral

- documentation requirement.

- the mode of repayment.

Banks are not present everywhere in rural India. Even they are, getting a loan from bank is much more difficult than taking a loan from the informal sources. In recent

years, people have tried out some new ways of providing loans to the poor. SHG is one

of them. A typical SHG has 15-20 members, usually belonging to one neighborhood, who

meet and save regularly.

![[ ] E22 PK Money, Credit](https://static.fdocuments.us/doc/165x107/54b7718b4a795941588b4568/-e22-pk-money-credit.jpg)