Alternative Real Estate Finance - The Potential of Islamic Finance

Joseph L. Pagliari, Jr. Clinical Professor of Real Estate

November 6, 2013 URBAN LAND INSTITUTE

Urban Development/Mixed-Use Council Chicago, Illinois

Monetary Policy and Its Potential Impact

on Real Estate

1 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

2 Interest Rates| The Long View

3 Interest Rates| Current Yield Curve

4 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

5 Today’s Rates Imply How Future Rates May Evolve

Assume:

Maturity Rate1 year 2.00%2 years 2.50%

Then:

expected to be ~ 3.00%

x = 3.002%

Today's Market

The implied one-yearrate in 12 months is

( )( ) ( )

( )( )

2

2

1 .02 1 1 .025

1 .0251

1 .02

3.00%

x

x

x

+ + = +

+= −

+

≈

• This represents an equilibrium view on the evolution of future interest rates.

• This view is based on the consensus view of market participants. Trades made at the average expectation.

• The bond market’s consensus view has been wrong in the past!

• The bond market’s consensus view is muddied by Quantitative Easing

6 Today’s Rates |Implications for Future Rates

7 Today’s Rates |Implications for Future Rates (continued)

8 Today’s Rates |Implications for Future Rates (continued)

9 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

10 Treasury’s v. TIPS → Implications for Future Inflation

11 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

12 The Role of Quantitative Easing

Interest Rates (i)

Supply of Money (Q)

Demand Supply Supply

under QE

i1

Q1

i2

Q2

• In equilibrium, interest rates are based on the consensus view of market participants. Trades made at the average expectation.

• The bond market’s consensus view is muddied by Quantitative Easing, which serves to reduce interest rates as a means of stimulating the economy.

13 Quantitative Easing & Components of Bond Yields

• In principle, the current yield (i) on bonds equals:

where: rTB = investor’s real-return requirement for Treasury bonds, and E [ρ] = the investor’s expectation of the inflation rate (over the bond’s life).

• The aspiration of QE includes lowering investor’s real-return requirement without increasing the investor’s expectation of the inflation rate. (So far, so good.)

• Ultimately, QE will be unwound. What then?

– rTBs ↑ ⇒ may be bad for commercial real estate (as well as other asset classes)

– E [ρ] ↑ ⇒ may be neutral to good for commercial real estate (provided space markers are in equilibrium (i.e., low vacancy))

( ) [ ]( )[ ]

1 1 1TBs

TBs

i r E

r E

ρ

ρ

= + + −

≈ +

14 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

15 Path of NCREIF Market Values, Incomes & Cap Rates:

Sources: NCREIF and instructor’s calculations.

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

8.5%

9.5%

$0

$50

$100

$150

$200

$250

$300

$350

$40019

78

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Cap

italiz

atio

n R

ate

Mar

ket V

alue

and

Res

cale

d N

OI

NCREIF Property Index: Market Values, Rescaled NOI and Capitalization Rates Based on a $100 Investment for the Period 1978 through 2012

Capitalization Rates (Right Axis) Market Values Rescaled NOI Average Capitalization Rate (Right Axis)

16 What About “Real Time” Indices?

• The NCREIF Index is appraisal-based. • Other indices show more price recovery, e.g ., Green Street:

Source: Green Street Advisors, Commercial Property Price Index, October 4, 2013

17 What About Differences by Property Types?

• Apartments & malls have recovered most (and hotels the least). • However, all property types show similar recovery:

Apartments & Retail: > 100% of peak prices

Hotels: > 80% of peak

prices

Source: Green Street Advisors, Commercial Property Price Index, October 4, 2013

18 Of Course, Averages Can Be Misleading

• Said another way: significant differences by quality

60%

70%

80%

90%

100%

110%

120%

130%

140%

$50

$75

$100

$125

$150

$175

$200

$225

$250

2000 2002 2003 2005 2006 2007 2009 2010 2011 2013

Rat

io o

f N

on-M

ajor

to M

ajor

-Mar

ket A

sset

Val

ues

(Unl

ever

ed) A

sset

Val

ues f

or C

ore

Prop

ertie

sIllustration of Asset Appreciation in Major v. Non-Major Markets

From December 2000 through August 2013

Major Markets

Non-Major Markets

Ratio of Non-Major to Major Markets

Source: Real Capital Analytics and Instructor's calculations.

19 Fundamental Components of Real Estate Returns

• In principle, the foregoing risks can be priced

• RECALL: In the long run, asset-level returns (ka) are primarily a function of the initial cash flow yield and the growth rate (g):

• In the short run, asset-level returns can be heavily influenced by the effects of shifting capitalization rates :

– ∇ : More easily seen in the following graph.

• Note: cap rate = NOI1/P0 ≠ CF1/P0

1

o

CFP

( )∇

1

0a

CFk gP

= +

1

0a

CFk gP

= + + ∇

20 Components of Return: Holding Period & Cap Rates

21 An Overview of Capitalization Rates

Source: Real Capital Analytics.

4%

5%

6%

7%

8%

9%

10%

01Q1 02Q1 03Q1 04Q1 05Q1 06Q1 07Q1 08Q1 09Q1 10Q1 11Q1 12Q1 13Q1

Cap

italiz

atio

n R

ates

Historical Capitalization Rates by Property Type for the Period 2001-Q3 2013

Apartment Industrial Retail CBD Office Suburban Office

EstimatedEstimated Dividend Estimated

Property Capitalization Pay-Out Cash FlowType Rate (1) Ratio (2) (3) Yield (4)

Apartments 6.25% 80.7% 5.04%

Industrial 7.66% 67.7% 5.19%

Office 6.68% 64.7% 4.32%

Retail 7.12% 69.9% 4.98%

All 6.93% 67.2% 4.66%

(1) Source: Real Capital Analytics, "Quarterly Review," Third Quarter, 2013.

(2)

(3) Source: NCREIF and author's calculations.

(4)

An Illustration: Conversion of Cap Rates to Cash Flow Yields

Represents typical portion of NOI converted to cash flow. The difference represents "cap ex" (i.e. , tenant improvements, leasing commissions and capital improvements).

Represents the product of the capitalization rate and the dividend pay-out ratio.

22 Cap Rates → Cash-Flow Yields

• Significant ambiguities surrounding cap rates. • Apartments have a very different “cap ex” behavior:

23 Fundamental Components of Real Estate Returns: Revisited

• Like bond investors, real estate investors want:

• Can compare what investors want (above) to what they are likely to receive (#19):

• Additionally, we can think of the growth rate (g) as: where: λ = the inflation pass-through rate

• Therefore, we can restate our comparison (from above):

[For simplicity, let’s ignore capitalization rate shifts and express expected inflation as merely ρ.]

( )( ) ( )0

0

11 1 1RE

CF gr g

Pρ

++ + − = +

( )( ) ( )0

0

11 1 1RE

CFr

Pλρ

ρ λρ+

+ + − = +

( )( ), 1 1 1a RE REk r ρ= + + −

g = λ * ρ

24 Fundamental Components of Real Estate Returns: Revisited

• Assume the real estate’s space markets are in equilibrium:

• When markets in equilibrium, our earlier comparison simplifies to:

• With a little bit of math, it can be shown that:

• Note that:

– In equilibrium, real estate values (P0) are unaffected by a change in anticipated inflation (because ρ does not appear above).

– In equilibrium, real estate values (P0) are only affected by a change in the required real return (rRE).

– In disequilibrium , real estate values (P0) are affected by both changes in the required real return (rRE) and a change in the anticipated inflation rate (ρ).

( )( ) ( )0

0

11 1 1RE

CFr

Pρ

ρ ρ+

+ + − = +

1λ⇒ =

0

0RE

CFrP

=

( )1λ =

25 Let’s Revisit the Growth Components of Return

• Recall: long- run asset-level returns (ka) are primarily a function of the initial cash flow yield and the growth rate (g):

• In turn, the growth rate can be viewed as a function of inflation (ρ):

λ = the inflation pass-through rate • Historically, λ ~ 75%

• So, real estate’s ability to (at least partially) hedge inflation may be important

1

o

CFP

1

0a

CFk gP

= +

g = λ * ρ

26 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

27 Inflation | The Long View

28 Inflation | Even Longer View → Taming Volatility ?

Reagan/Volcker

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1978 1982 1986 1990 1994 1998 2002 2006 2010

Annual Inflation Rates & NCREIF Returns for the Period 1978-2012

Inflation Average = 3.91%

NCREIF Average = 9.37%

Sources: InflationData.com, NCREIF and author's calculations

29 Real Estate’s Correlation with Inflation?

RE’s long-term correlation with inflation ~28%

When Inflation is greater than average, RE’s correlation with inflation ~76%

RE’s real (i.e., inflation-adjusted) return ~5.5%

30 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

31 The Collapse of the CMBS Market

$0

$50

$100

$150

$200

$250

$300

$350

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 1H '12

1H '13

Annual CMBS Issuance ($ billions)

Non-U.S. U.S.

Source: Commercial Mortgage Alert

32 A Wave of Refinancings: ~$2.0 trillion Coming Due

33 The Aggressive Vintages Coming Due Later

Source: Morgan Stanley Research, “Commercial Real Estate 2010.”

34 CMBS Loan Delinquencies by Vintage

Source: Moody’s “U.S. CMBS: Delinquency Tracker,” October, 2012

• Decreasing rate of default for CMBS loans:

35 Delinquencies Lead to Workouts or Foreclosure • So far, we’re at ~ $400 billion of workouts or foreclosures • About 1/2 have been resolved

Source: Real Capital Analytics, “Quarter in Review, October 2013”

• But, when do these forbearance agreements expire?

• In the midst of the refinancing wave?

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

'08 '09 '10 '11 '12 '13

Billions

Cumulative Distress for All Property Types

TroubledREORestructuredResolved

36 Lessening CMBS Underwriting Standards to the Rescue?

Source: Moody’s, “U.S. CMBS Review,” 3rd Quarter 2013.

• Another case of “here we go again”?

37 Real Estate Debt Funds to the Rescue?

Source: Preqin, “The Growth of Real Estate Debt Funds,” Real Estate Spotlight, November 2012.

• Is there enough “powder” here? Not yet!

38 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

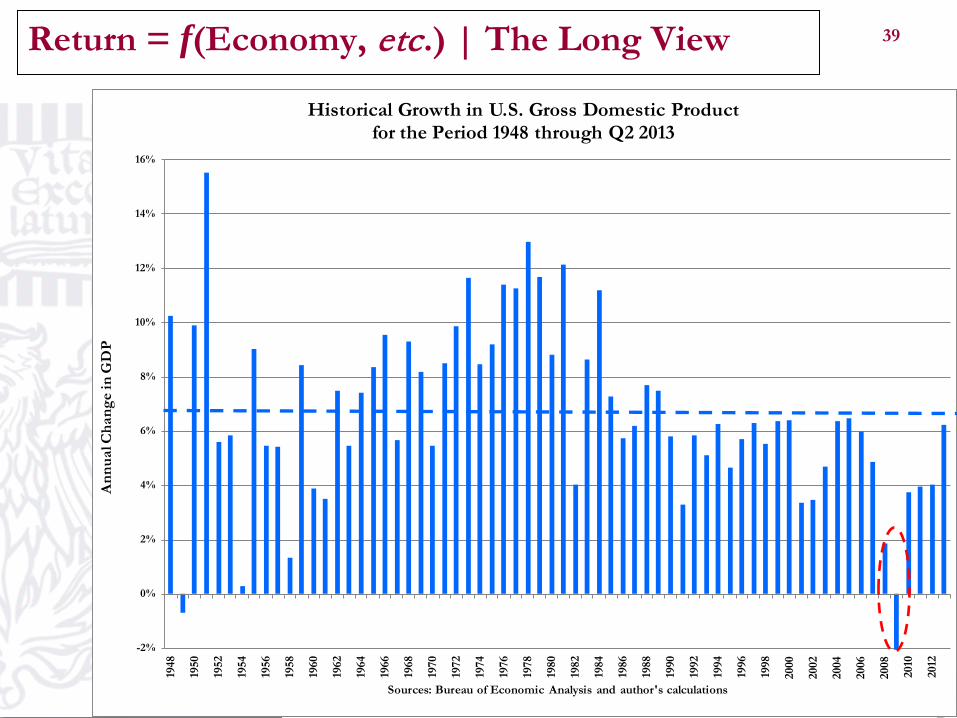

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%19

48

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Ann

ual C

hang

e in

GD

P

Sources: Bureau of Economic Analysis and author's calculations

Historical Growth in U.S. Gross Domestic Productfor the Period 1948 through Q2 2013

39 Return = f(Economy, etc.) | The Long View

-4%

-2%

0%

2%

4%

6%

8%

10%19

48

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Ann

ual C

hang

e in

Con

stan

t GD

P

Sources: Bureau of Economic Analysis and author's calculations

Historical Growth in U.S. Gross Domestic Productin Constant (2005) Dollars for the Period 1948 through Q2 2013

40 Return = f(Economy, etc.) | The Long View

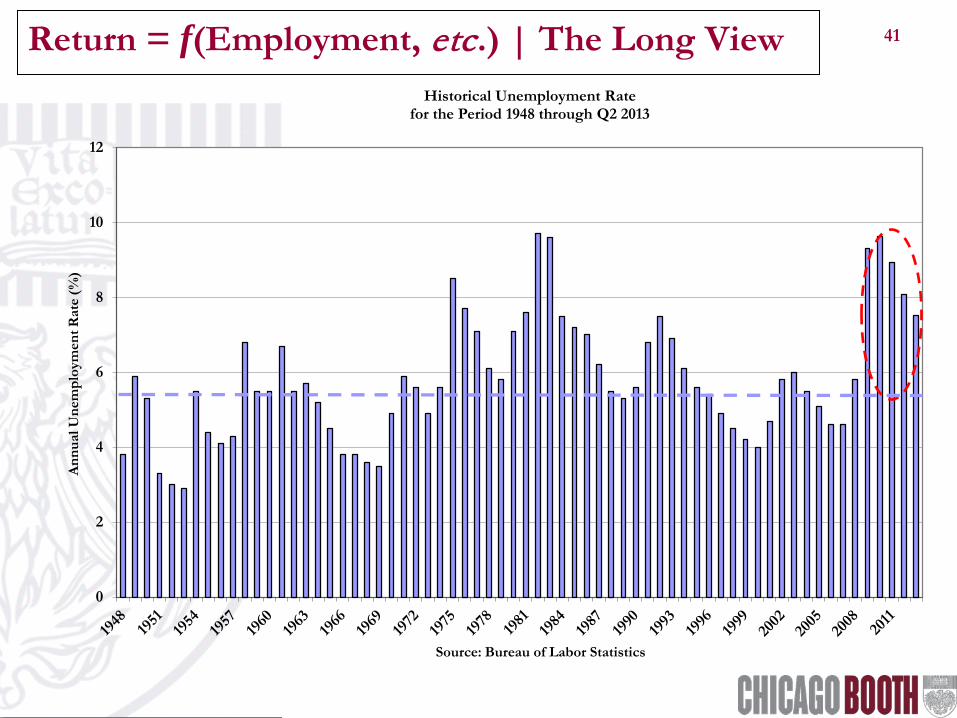

0

2

4

6

8

10

12

Ann

ual U

nem

ploy

men

t Rat

e (%

)

Source: Bureau of Labor Statistics

Historical Unemployment Rate for the Period 1948 through Q2 2013

41 Return = f(Employment, etc.) | The Long View

0

2

4

6

8

10

12

Ann

ual U

nem

ploy

men

t Rat

e (%

)

Sources: Bureau of Labor Statistics and author's calculations

Historical Unemployment Rate for the Period 1948 through Q2 2013

42 Return = f(Employment, etc.) | The Long View

Stylized Normal Distribution (based on historical µ and σ)

~2.5 σ-Event: Financial Crisis

43 In Real Estate, the Local Market Matters!

Source: Jim Costello and Mark Seely, “Industrial, Economic & Workforce Trends,”

CBRE Client Conference, October 28, 2010.

By itself, Detroit accounts for ~ 100,000 jobs lost

Lost Jobs:

44 What Might Derail the Economy? The Long View on Oil Prices

• The economy remains fragile.

• What else might go wrong?

• Possibilities: – Crude oil

prices? – Terrorist

attack(s)? – Contagious

financial crisis?

– Natural disasters (Sandy)?

– Partisan political bickering increases (fiscal cliff)?

$0

$20

$40

$60

$80

$100

$120

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Ann

ual A

vera

ge C

rude

Oil

Pric

es p

er B

arre

l in

Con

stan

t (2

010)

Dol

lars

Source: InflationData.com

Domestic Crude Oil Prices (in Constant 2012 Dollars)for the Period 1948 through Q2 2013

45 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

46 Housing Market’s Correlation with Commercial Real Estate

See: “The US Property Market in 2010,” David Geltner, PREA Quarterly, Winter 2010.

• Residential market slightly led the downturn in the commercial real estate markets • Most commercial real indices showed a similar correction

47 Residential Real Estate Still in the Doldrums

$0

$50,000

$100,000

$150,000

$200,000

$250,000

0

200

400

600

800

1,000

1,200

1,400

Rea

l (20

00 $

) Med

ian

Sale

s Pri

ces

Ann

ual N

ew H

ome

Sale

s (un

its)

Sources: U.S. Census Bureau, Morningstar and Instructors' Calculations

Annual New Homes Sold & Median Sales Prices: 1963 - 2012

New Homes SoldMedian Sales Price ('00 $ - Right Axis)

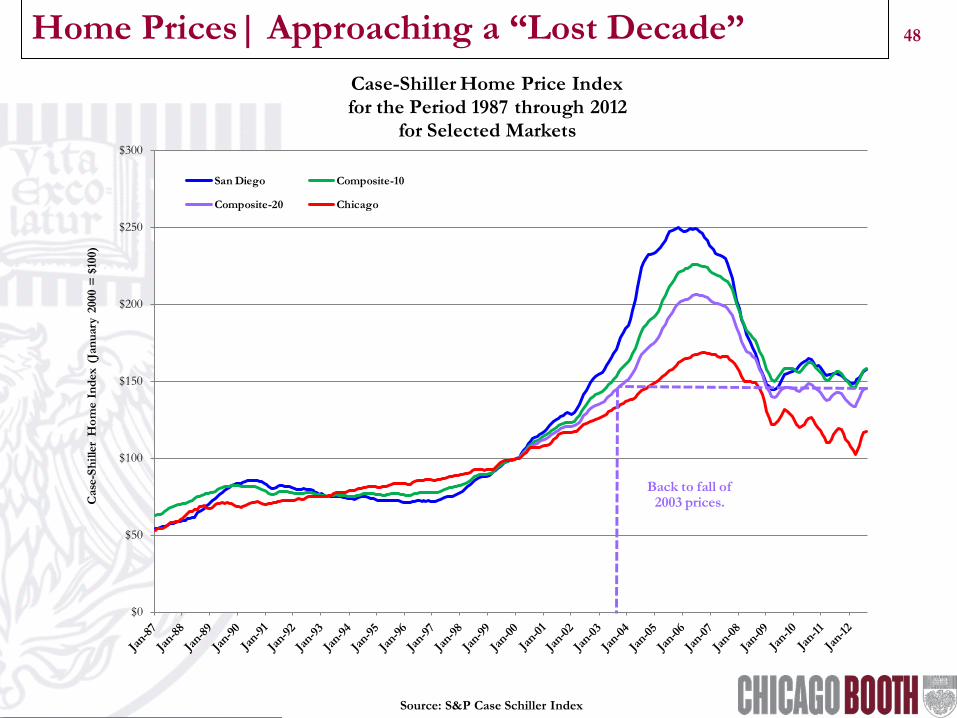

48 Home Prices| Approaching a “Lost Decade”

Source: S&P Case Schiller Index

$0

$50

$100

$150

$200

$250

$300

Cas

e-Sh

iller

Hom

e In

dex

(Jan

uary

200

0 =

$10

0)Case-Shiller Home Price Indexfor the Period 1987 through 2012

for Selected Markets

San Diego Composite-10

Composite-20 Chicago

Back to fall of 2003 prices.

49 Residential Real Estate Is Highly Localized In addition to the average appreciation rate, volatility matters:

Source: S&P Case Schiller Index and instructor’s Calculations

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

0% 20% 40% 60% 80% 100% 120% 140% 160% 180% 200%

Tota

l Pri

ce D

eclin

e fr

om P

eak

Pric

es

Bubble Growth: Maximum Price Increase from January 2000

"Bubble" Growth and Subsequent Decline for Certain US Housing Markets for the Period 2000 through 2012

Net Annual Appreciation Rate of 4%

Net Annual Appreciation Rate of

2.5%

Net Annual Appreciation Rate of

0%

The Rate of Inflation (ρ)

Phoenix

Detroit

Boston

ChicagoAtlanta

Tampa

Miami

Washington

Denver

San Francisco

San DiegoLos Angeles

Dallas

Portland

Cleveland

New York

Las Vegas

Charlotte

Minneapolis

Composite-20

Composite-10Seattle

50 Can We Have an Economic Recovery without a Housing Recovery?

• Consider the depth of the housing market and its impact on:

– the construction industry: • unemployment is disproportionately male and less-educated

– the banking sector: • when will banks start lending again?

– consumer confidence: • if your largest investment is faltering, how confident will you be?

• The administration has already attempted at directly reviving the housing market;

– however, the positive effects seem to have been little.

• Is there the political will to make another attempt? – Should there be?

• Both parties are advocating some reform of the GSEs – Likely to hurt any short-term rebound in home prices

51 The “Shadow” Supply of Housing

• As estimated by the International Monetary Fund:

52 A Rebound in Home Prices? • An expected recovery in home prices gains momentum:

y = 0.5078x - 884.66R² = 0.468

0

100

200

300

400

500

600

700

800

900

1000

0

50

100

150

200

250

1890 1910 1930 1950 1970 1990 2010

Popu

latio

n (i

n m

illio

ns)

Inde

x or

Pri

ces,

Cos

ts &

Inte

rest

Rat

es

Year

Path of Real Home Prices and Building Costs as well as Population and Interest Rates from 1890

Home Prices

Building Costs

Population

Interest Rates

Source: Robert Shiller - Irrational Exuberance and instructor's calculations.

53 Path of Real Home Prices | The Long View

54 Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances

55 The Financial Strain on State & Local Budgets

• It is no surprise that many state & local budgets are under enormous financial strain. As examples of just two perspectives, consider:

– Muni bond swap (MCDX) rates, and – Muni bond spreads over Treasuries

Sources: Markit, Goldman Sachs.

56 The Residential Real Estate Channel

• The fall in home prices contributes to the current strain on state and local budgets.

– Fall in home prices contributes to declining consumer confidence

• Which leads to a decrease in consumer spending • Which leads to a decrease in sales taxes

– Fall in home prices is accompanied by a fall in the volume of home sales

• Which leads to a decrease in transfer taxes

– But (ad valorem) property taxes are largely a zero-sum game: • If everyone’s property increases by x%, your property tax bill is unchanged.

• As a result of the foregoing, a due diligence/underwriting item of increasing

importance will be the financial condition of state & local entities. – Will be important to:

• Tenants, • Lenders, and • Investors.

57 Increasing Realization: Taxing the Rich Doesn’t Work

• At the state & local levels, “tax the rich” policies are increasingly problematic:

– The income of the rich is more variable than lower brackets

– The rich move to other states (e.g ., Florida and Texas) with lower income taxes

• Calls for “broadening the (income) tax base” will be met with political resistance.

• In order to cope, state & local authorities considering a range of service cuts &/or increasing other forms of taxation (e.g ., property and transfer taxes)

– Both the cuts and the tax increases adversely affect commercial real estate values

Source: Robert Frank, “The Price of Taxing the Rich,” The Wall Street Journal, March 26, 2011

58 Another Symptom of Financial Distress: State Pension Liabilities

Source: Rachel Barkley, “State & Local Pensions 101,” Morningstar, October 19, 2012.

59 Will Aggressiveness Change with State Fortunes?

Source: Jim Costello and Mark Seely, “Industrial, Economic & Workforce Trends,”

CBRE Client Conference, October 28, 2010.

60

Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances • Appendices

– Growth at What Price?

– CMBS Dysfunction

61 How Should We Think About Risk?

The

Req

uire

d R

ates

of R

etur

n: E

(k)

Market-Level Volatility: σ

Pricing Illustration of High- v. Low-Barrier Markets In Order to Produce Identical Risk-Adjusted Returns

E(k)L

E(k)H

σH

rf

σL

• In principle, all investments should offer identical risk-adjusted returns. • Let’s frame the discussion in terms of high- v. low-barrier markets:

E(k)Market

62 Let’s Be a Bit More Specific:

• Identical risk-adjusted rates of return = identical Sharpe Ratios

T

he R

equi

red

Rat

es o

f Ret

urn:

E(k

a)

Market-Level Volatility: σ

Pricing Illustration of High- v. Low-Barrier Markets In Order to Produce Identical Risk-Adjusted Returns

E(ka,L )

E(ka,H )

σH

rf

σL

( ) ( ), ,a H f a L f

H L

E k r E k rσ σ

− −=

Sharpe Ratios

The

Req

uire

d R

ates

of R

etur

n: E

(ka)

Market-Level Volatility: σ

Pricing Illustration of High- v. Low-Barrier Markets In Order to Produce Identical Risk-Adjusted Returns

E(ka,L )

E(ka,H )

σH

rf

σL

( ) ( )1 1

0 0H f L f

H L

H L

CF CFE g r E g rP P

σ σ

+ − + −

=

63 Let’s Be a Bit More Specific (continued):

• We can include the expanded view of returns (assuming constant cap rates):

Sharpe Ratios

64 How Should We Think About Investment Opportunities?

• Based on your beliefs (hopefully supported by research), consider the potential mispricing of markets:

65

Monetary Policy → Commercial Real Estate

• Monetary Policy: Quantitative Easing

– Historical Path of Interest Rates

– Implied Forward Rates

– Nominal v. Real Yields

– Quantitative Easing

• Where Might Changing Monetary Policy Affect Real Estate Returns:

– Commercial Real Estate Pricing

– Inflation & Commercial Real Estate

– Loan Maturities

– The Economy

– The Housing Market

– State & Local Finances • Appendices

– Growth at What Price?

– CMBS Dysfunction

66 CRE Loans: Foreclosures v. Forbearance

• Upon a monetary default, lenders can choose to foreclose v. forbear

• Consider the two sources of most defaults:

1. Commercial Banks: Administration decided to encourage banks to forbear → “extend & pretend” 2. CMBS: the tranched nature of security holders complicates the resolution of

delinquent loans. Consider a simple A/B structure:

67 Inherent Conflicts between Security Tranches

>

<

Time

Prices

Under-shooting Market

Over-shooting Market

“True” Prices

68 The Effect of Forbearance: Undershooting Market?

This is the buying opportunity

This is not

69 Security Design: Start with a Bundle

0%

2%

4%

6%

8%

10%

12%

14%

16%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Exp

ecte

d R

etur

n

Risk

An Illustration of Security Design: Starting Point

Assume a $2.0billion market capitalization

rf

70 Security Design: Can Unbundle the Bundle

0%

2%

4%

6%

8%

10%

12%

14%

16%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Exp

ecte

d R

etur

n

Risk

An Illustration of Security Design: Separation

Assume a $1.5billion market capitalization

Assume a $0 .5 billion market capitalization

rf

71 Security Design: Can Bundle the Pieces

0%

2%

4%

6%

8%

10%

12%

14%

16%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Exp

ecte

d R

etur

n

Risk

An Illustration of Security Design: Consolidation

Assume a $1.0billion market capitalization

Assume a $1.0billion market capitalization

Assume a $2.0billion market capitalization

rf

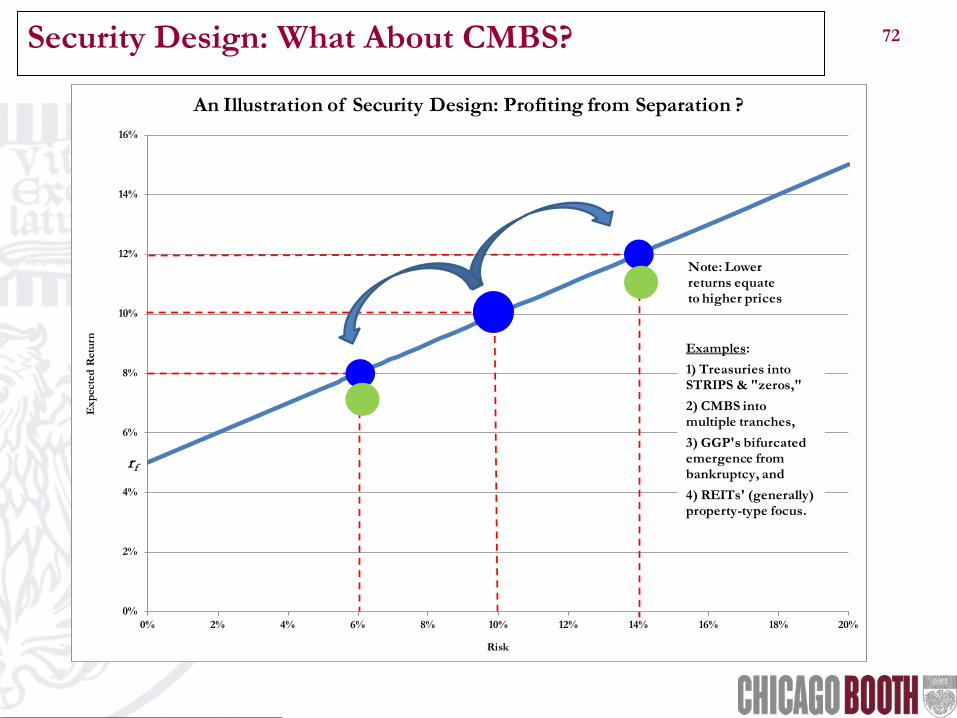

72 Security Design: What About CMBS?

0%

2%

4%

6%

8%

10%

12%

14%

16%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Exp

ecte

d R

etur

n

Risk

An Illustration of Security Design: Profiting from Separation ?

Note: Lower returns equateto higher prices

Examples: 1) Treasuries into STRIPS & "zeros,"2) CMBS into multiple tranches,3) GGP's bifurcated emergence from bankruptcy, and4) REITs' (generally) property-type focus.

rf