Molly Reardon ES 567 Final Project Spring 2010 amber/go340/students/reardon

Upload

reynold-harringtonCategory

view

216download

0

Wednesday, April 19, 2023

Linking Small farmers to high value markets

Ashok Gulati & Thomas ReardonCo-directors of IFPRI/MSU joint program on “Markets in Asia”

Conference on

Taking Action for the World’s Poor and Hungry People

Jointly organized by the State Council Leading Group Office of Poverty Alleviation and Development and IFPRI

Beijing Oct. 17-19, 2007

Page 2INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Four key messages…

• Small farmers to stay in Asia for next 15-20 years…

• Changing Asian platter towards high value agriculture (Benett’s law: share of HVA such as fruits and vegetables, dairy, meat and

fish to go up);

• Rapid transformation and scaling up of wholesale markets, processors, and organized retailers (Consolidating top) while farms are still fragmenting

• Opportunity for small holders if they can connect to new markets, else a major challenge to remain afloat.

Page 3INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Small farms to stay in Asia…

Source FAO (2001,2004); And for China Fan and Chan Kang (2003)

Avg farm size over time: The shrinking block

0.6

2.3

1.1 1

5.3

3.6

0.4

1.4

0.9 0.8

3.1

2.2

0

1

2

3

4

5

6

China (1980-99) India (1971-96) Indonesia (1973-93)

Nepal (1992-02) Pakistan (1971-2000)

Phillipines (1971-91)

ha

1st period

2nd period

Page 4INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Indian farm reality: fragmenting farms and swelling bottom

0%

20%

40%

60%

80%

100%

1970-71 1980-81 1990-91 1995-96 2000-01

Area of Holdings-India

Less than 2 hectares 2-4 hectares 4 and above hectares

0%

20%

40%

60%

80%

100%

1970-71 1980-81 1990-91 1995-96 2000-01

Number of holdings-India

Avg Size 2.3 1.82 1.55 1.41 1.37

Source: Agricultural Census Division, India

Page 5INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Changing Asian Platter: Diversification and “westernization” of diets Average Annual Growth in per capita consumption (1991-2005) in Selected 8 Countries in

South and South East Asia

3.7

1.9

2.7

3.9

2.4

3.1

-0.4

1.4

1.2

2.5

3.1

1.8

1.0

8.0

9.5

8.1

6.2

6.5

8.1

-1.9-0.2

-4.0 -2.0 0.0 2.0 4.0 6.0 8.0 10.0 12.0

Vegetables

Fruits

Milk

Meat

Fish

Eggs

Grains

average annual growth (%)

China

All but China

All 8 Nations

Notes: Grains include cereals and pulses, Consumption measured as grams/capita/day, the 8 countries include Bangladesh, China, India, Indonesia,

Pakistan, Philippines, Thailand and Viet Nam. Source: FAOSTAT, © FAO Statistics Division 2007, 30 July 2007

Page 6INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Trade is still a tiny part of the story…

• Trade is a very small part of the consumption of high value agriculture (usually less than 3% in most countries of south and south-east Asia);

• Change is being driven primarily by domestic factors of growth, urbanization, …..

• And domestic production is responding…(e.g., in India share of HVA in total value of agriculture output increased

from 32% in 1981-83 to 48% in 2003-05; similar changes have occurred in China, Indonesia, etc…)

Page 7INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Next 10 years….

• Although staples are important from food security point of view, future sources of growth and prosperity in agriculture will come increasingly from high value products, driven by domestic demand, production & markets;

• But being perishable in nature, it needs a fast moving infrastructure and institutions that can compress the value chains and reduce risk

Page 8INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

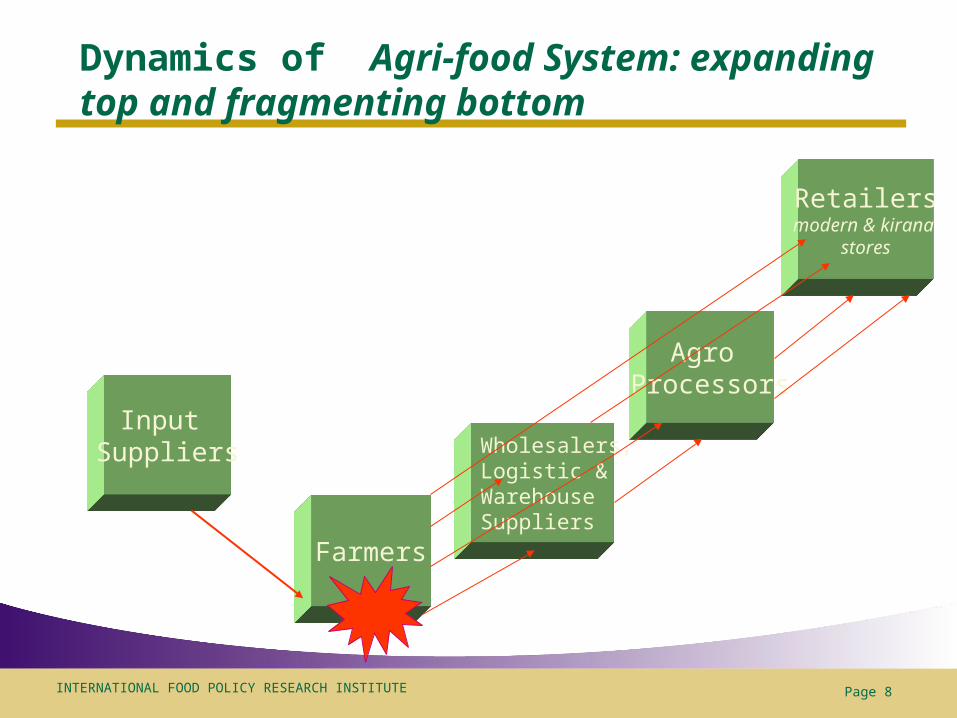

Dynamics of Agri-food System: expanding top and fragmenting bottom

Input Suppliers

Farmers

Wholesalers,Logistic & Warehouse Suppliers

Agro Processors

Retailersmodern & kirana

stores

Page 9INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

All segments of the chain changing fast…

• Wholesale markets (WM): from trucks in 1970s to public WM in 1980s to scaling up in 1990s and restructuring in 2000s (China, India…., etc.)

• Processing industry: from small scale to large scale driven by increasing demand for processed food as well as by technological innovations (like tetrapak) to increase the shelf life

• Organized Retailing in food: diffusion in three waves in emerging markets …taking off in south-Asia now…

Page 10INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

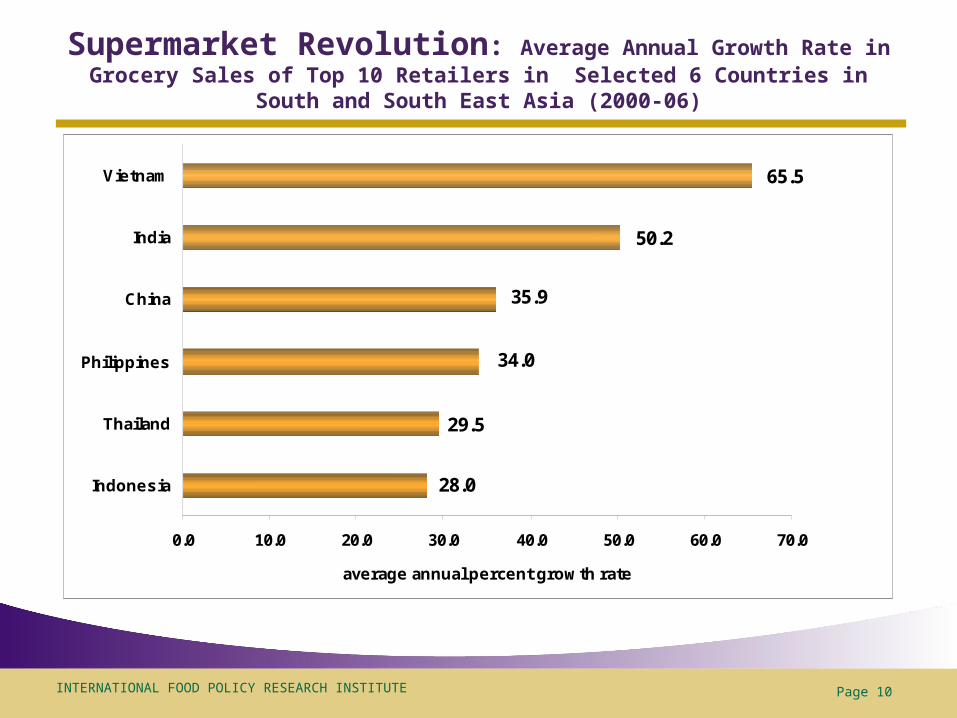

Supermarket Revolution: Average Annual Growth Rate in Grocery Sales of Top 10 Retailers in Selected 6 Countries in South and South East Asia

(2000-06)

65.5

50.2

35.9

34.0

29.5

28.0

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0

Indonesia

Thailand

Philippines

China

India

Vietnam

average annual percent growth rate

Page 11INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

What ensures production & price risk coverage for the small farmers?

Market Information incl.

Food safety

Retailers & Agro

processors

Input delivery &Extension services

Credit &Insurance

Farmers

Page 12INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Can the large players connect to small holders?

• Mother dairy in India …. (Co-op. model)

• BRAC in Bangladesh…. (NGO model with multifarious activities supporting small holders…..)

• ITC (e-choupal) in India… (Multinational model) $1.25 billion investment linking 4 million farmers, largely middle and small…moving from soya to fresh veg.

• Celebrate Life Agriventures Philippines Inc… a farmer company in Philippines exporting bananas to Japan

• Mahagrapes….a farmers’ company in India exporting grapes to UK..

• Metro cash and carry in China… buying from producer groups

Page 13INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

How do we judge: which way to go??Solving the “Rubik cube” puzzle

•Innovative Institutions and Organizations Linking smallholders to Modern Value Chains•Mapping and Designing Institutions for CISS

C-Competitiveness I-Inclusiveness S-Sustainability S-Scalability