Moncler - borsaitaliana.it · moncler – november 8, 2013 important disclosures appear at the back...

56

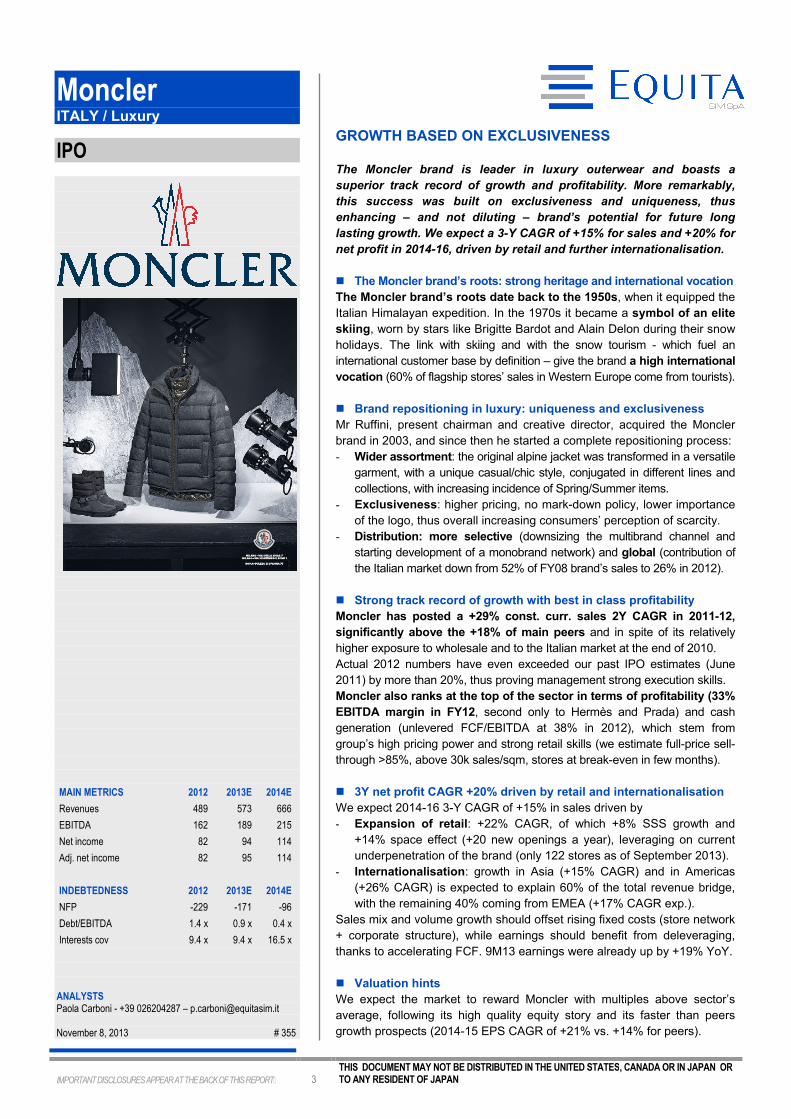

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER 1 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN Moncler ITALY / Luxury IPO ANALYSTS Paola Carboni - +39 026204287 – [email protected] November 8, 2013 # 355 GROWTH BASED ON EXCLUSIVENESS The Moncler brand is leader in luxury outerwear and boasts a superior track record of growth and profitability. More remarkably, this success was built on exclusiveness and uniqueness, thus enhancing – and not diluting – brand’s potential for future long lasting growth. We expect a 3-Y CAGR of +15% for sales and +20% for net profit in 2014-16, driven by retail and further internationalisation. The Moncler brand’s roots: strong heritage and international vocation The Moncler brand’s roots date back to the 1950s, when it equipped the Italian Himalayan expedition. In the 1970s it became a symbol of an elite skiing, worn by stars like Brigitte Bardot and Alain Delon during their snow holidays. The link with skiing and with the snow tourism - which fuel an international customer base by definition – give the brand a high international vocation (60% of flagship stores’ sales in Western Europe come from tourists). Brand repositioning in luxury: uniqueness and exclusiveness Mr Ruffini, present chairman and creative director, acquired the Moncler brand in 2003, and since then he started a complete repositioning process: - Wider assortment: the original alpine jacket was transformed in a versatile garment, with a unique casual/chic style, conjugated in different lines and collections, with increasing incidence of Spring/Summer items. - Exclusiveness: higher pricing, no mark-down policy, lower importance of the logo, thus overall increasing consumers’ perception of scarcity. - Distribution: more selective (downsizing the multibrand channel and starting development of a monobrand network) and global (contribution of the Italian market down from 52% of FY08 brand’s sales to 26% in 2012). Strong track record of growth with best in class profitability Moncler has posted a +29% const. curr. sales 2Y CAGR in 2011-12, significantly above the +18% of main peers and in spite of its relatively higher exposure to wholesale and to the Italian market at the end of 2010. Actual 2012 numbers have even exceeded our past IPO estimates (June 2011) by more than 20%, thus proving management strong execution skills. Moncler also ranks at the top of the sector in terms of profitability (33% EBITDA margin in FY12, second only to Hermès and Prada) and cash generation (unlevered FCF/EBITDA at 38% in 2012), which stem from group’s high pricing power and strong retail skills (we estimate full-price sell- through >85%, above 30k sales/sqm, stores at break-even in few months). 3Y net profit CAGR +20% driven by retail and internationalisation We expect 2014-16 3-Y CAGR of +15% in sales driven by - Expansion of retail: +22% CAGR, of which +8% SSS growth and +14% space effect (+20 new openings a year), leveraging on current underpenetration of the brand (only 122 stores as of September 2013). - Internationalisation: growth in Asia (+15% CAGR) and in Americas (+26% CAGR) is expected to explain 60% of the total revenue bridge, with the remaining 40% coming from EMEA (+17% CAGR exp.). Sales mix and volume growth should offset rising fixed costs (store network + corporate structure), while earnings should benefit from deleveraging, thanks to accelerating FCF. 9M13 earnings were already up by +19% YoY. Valuation hints We expect the market to reward Moncler with multiples above sector’s average, following its high quality equity story and its faster than peers growth prospects (2014-15 EPS CAGR of +21% vs. +14% for peers).

Transcript of Moncler - borsaitaliana.it · moncler – november 8, 2013 important disclosures appear at the back...

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 1 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

Moncler ITALY / Luxury

IPO

ANALYSTS Paola Carboni - +39 026204287 – [email protected] November 8, 2013 # 355

GROWTH BASED ON EXCLUSIVENESS

The Moncler brand is leader in luxury outerwear and boasts a

superior track record of growth and profitability. More remarkably,

this success was built on exclusiveness and uniqueness, thus

enhancing – and not diluting – brand’s potential for future long

lasting growth. We expect a 3-Y CAGR of +15% for sales and +20% for

net profit in 2014-16, driven by retail and further internationalisation.

� The Moncler brand’s roots: strong heritage and international vocation

The Moncler brand’s roots date back to the 1950s, when it equipped the

Italian Himalayan expedition. In the 1970s it became a symbol of an elite

skiing, worn by stars like Brigitte Bardot and Alain Delon during their snow

holidays. The link with skiing and with the snow tourism - which fuel an

international customer base by definition – give the brand a high international

vocation (60% of flagship stores’ sales in Western Europe come from tourists).

� Brand repositioning in luxury: uniqueness and exclusiveness

Mr Ruffini, present chairman and creative director, acquired the Moncler

brand in 2003, and since then he started a complete repositioning process:

- Wider assortment: the original alpine jacket was transformed in a versatile

garment, with a unique casual/chic style, conjugated in different lines and

collections, with increasing incidence of Spring/Summer items.

- Exclusiveness: higher pricing, no mark-down policy, lower importance

of the logo, thus overall increasing consumers’ perception of scarcity.

- Distribution: more selective (downsizing the multibrand channel and

starting development of a monobrand network) and global (contribution of

the Italian market down from 52% of FY08 brand’s sales to 26% in 2012).

� Strong track record of growth with best in class profitability

Moncler has posted a +29% const. curr. sales 2Y CAGR in 2011-12,

significantly above the +18% of main peers and in spite of its relatively

higher exposure to wholesale and to the Italian market at the end of 2010.

Actual 2012 numbers have even exceeded our past IPO estimates (June

2011) by more than 20%, thus proving management strong execution skills.

Moncler also ranks at the top of the sector in terms of profitability (33%

EBITDA margin in FY12, second only to Hermès and Prada) and cash

generation (unlevered FCF/EBITDA at 38% in 2012), which stem from

group’s high pricing power and strong retail skills (we estimate full-price sell-

through >85%, above 30k sales/sqm, stores at break-even in few months).

� 3Y net profit CAGR +20% driven by retail and internationalisation

We expect 2014-16 3-Y CAGR of +15% in sales driven by

- Expansion of retail: +22% CAGR, of which +8% SSS growth and

+14% space effect (+20 new openings a year), leveraging on current

underpenetration of the brand (only 122 stores as of September 2013).

- Internationalisation: growth in Asia (+15% CAGR) and in Americas

(+26% CAGR) is expected to explain 60% of the total revenue bridge,

with the remaining 40% coming from EMEA (+17% CAGR exp.).

Sales mix and volume growth should offset rising fixed costs (store network

+ corporate structure), while earnings should benefit from deleveraging,

thanks to accelerating FCF. 9M13 earnings were already up by +19% YoY.

� Valuation hints

We expect the market to reward Moncler with multiples above sector’s

average, following its high quality equity story and its faster than peers

growth prospects (2014-15 EPS CAGR of +21% vs. +14% for peers).

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT� 2 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

THIS DOCUMENT IS BEING FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED, IN

WHOLE OR IN PART, TO ANY OTHER PERSON. IN PARTICULAR, NEITHER THIS DOCUMENT NOR ANY COPY HEREOF MAY BE TAKEN OR

RETRANSMITTED IN OR INTO THE UNITED STATES OR REDISTRIBUTED, DIRECTLY OR INDIRECTLY, IN THE UNITED STATES OR TO ANY US

PERSON. ANY FAILURE TO COMPLY WITH THIS RESTRICTION MAY CONSTITUTE A VIOLATION OF US SECURITIES LAWS.

THIS DOCUMENT IS BEING DISTRIBUTED ONLY BY OR WITH THE APPROVAL OF AN AUTHORISED PERSON OR TO (I) PERSONS WHO ARE

OUTSIDE THE UNITED KINGDOM;(II) PERSONS IN THE UNITED KINGDOM WHO HAVE PROFESSIONAL EXPERIENCE IN MATTERS RELATED TO

INVESTMENTS AND WHO ARE INVESTMENT PROFESSIONALS WITHIN THE MEANING OF ARTICLE 19(5) OF THE FINANCIAL SERVICES AND

MARKETS ACT 2000 (FINANCIAL PROMOTION) ORDER 2005 (AS AMENDED) OF THE UNITED KINGDOM (THE "ORDER"); (III) PERSONS WHO

FALL WITHIN ARTICLE 49(2)(A) TO (D)("HIGH NET WORTH COMPANIES, UNINCORPORATED ASSOCIATIONS ETC.") OF THE ORDER; AND (IV)

ANY OTHER PERSONS TO WHOM THIS DOCUMENT MAY OTHERWISE LAWFULLY BE DIRECTED (ALL SUCH PERSONS TOGETHER BEING

REFERRED TO AS "RELEVANT PERSONS"). THE INVESTMENTS TO WHICH THIS DOCUMENT RELATES ARE AVAILABLE ONLY TO, AND ANY

INVITATION, OFFER OR AGREEMENT TO SUBSCRIBE, PURCHASE OR OTHERWISE ACQUIRE SUCH INVESTMENTS WILL BE ENGAGED IN

ONLY WITH, RELEVANT PERSONS. ANY PERSON WHO IS NOT A RELEVANT PERSON SHOULD NOT ACT OR RELY ON THIS DOCUMENT OR

ANY OF ITS CONTENTS.

THIS DOCUMENT IS FOR DISTRIBUTION IN ITALY ONLY TO QUALIFIED INVESTORS WITHIN THE MEANING OF ARTICLE

100 OF LEGISLATIVE DECREE NO. 58 OF 28 FEBRUARY 1998 AS AMENDED, AND ARTICLE 34-TER, PARA. 1, LETT B), OF CONSOB

REGULATION NO. 11971 OF 1999, AS AMENDED. THIS DOCUMENT IS NOT ADDRESSED TO ANY MEMBER OF THE GENERAL PUBLIC IN ITALY.

IN NO CIRCUMSTANCES SHOULD THIS DOCUMENT CIRCULATE AMONG, OR BE DISTRIBUTED TO (I) A MEMBER OF THE GENERAL PUBLIC;

(II) INDIVIDUALS OR ENTITIES FALLING OUTSIDE THE DEFINITION OF “QUALIFIED INVESTORS” AS SPECIFIED ABOVE; OR (III) TO

DISTRIBUTION CHANNELS THROUGH WHICH INFORMATION IS , OR IS LIKELY TO BECOME AVAILABLE TO A LARGE NUMBER OF PERSONS.

THIS DOCUMENT IS BEING FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT REPRODUCED OR REDISTRIBUTED, IN

WHOLE OR IN PART, TO ANY OTHER PERSON. IN PARTICULAT, NEITHER THIS DOCUMENT NOR ANY COPY HEREOF MAY BE TAKEN OR

RETRANSMITTED IN OR INTO JAPAN OR REDISTRIBUTED, DIRECTLY OR INDIRECTLY, IN JAPAN OR TO ANY RESIDENT THEREOF. ANY

FAILURE TO COMPLY WITH THIS RESTRICTION MAY CONSTITUTE A VIOLATION OF SECURITIES LAWS OF JAPAN.

THE DISTRIBUTION OF THIS DOCUMENT IN OTHER JURISDICTIONS MAY BE RESTRICTED BY LAW AND PERSONS INTO WHOSE POSSESSION

THIS DOCUMENT COMES SHOULD INFORM THEMSELVES ABOUT, AND OBSERVE, ANY SUCH RESTRICTION. ANY FAILURE TO COMPLY WITH

THESE RESTRICTIONS MAY CONSTITUTE A VIOLATION OF THE LAWS OF ANY SUCH OTHER JURISDICTION.

THIS DOCUMENT DOES NOT CONSTITUTE AN OFFER OR INVITATION OR FORM PART OF AN OFFER OR INVITATION TO SUBSCRIBE FOR OR

PURCHASE ANY SECURITIES, AND NEITHER THIS DOCUMENT NOR ANYTHING CONTAINED HEREIN SHALL FORM THE BASIS OF ANY

CONTRACT OR COMMITMENT WHATSOEVER.

This report has been prepared by EQUITA S.I.M. S.p.A. to provide background information about Moncler S.p.A. (the “Company”). EQUITA S.I.M.

S.p.A. or an affiliated company of EQUITA S.I.M S.p.A: is or may be a member of the underwriting group in respect of a proposed offering of

securities of the Company. This report has been produced independently of the Company and the forecasts, opinions and expectations

contained herein are entirely those of EQUITA S.I.M S.p.A. While all reasonable care has been taken to ensure that the facts stated herein are

accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, EQUITA S.I.M. S.p.A. has not verified the

contents hereof and no reliance should be placed on the accuracy, fairness or completeness of the information contained in this document. No

person accepts any liability whatsoever for any loss howsoever arising from any use of this document or its contents or otherwise arising in

connection therewith, and neither EQUITA S.I.M. S.p.A., the Company, nor any of their respective directors, officers or employees, shall be in any

way responsible for the contents hereof, apart from the liabilities and responsibilities which may be imposed on them by the FSMA, or the

regulatory regime thereunder. EQUITA S.I.M. S.p.A. and/or persons connected with it may have acted upon or used the information herein

contained, or the research or analysis on which it is based, before its publication. EQUITA S.I.M. S.p.A. may in the future participate in an offering

of Company’s securities. Any opinions, forecasts or estimates herein constitute a judgement as at the date of this report. There can be no

assurance that future results or events will be consistent with any such opinions, forecasts or estimates. This information is subject to change

without notice and its accuracy is not guaranteed. It may be incomplete or condensed and it may not contain all material information concerning

the Company. Any decision to purchase securities in any proposed offering should be made solely on the basis of the information to be

contained in the final offering document to be published in due course in relation to the proposed offering.

BY ACCEPTING THIS REPORT, YOU AGREE TO BE BOUND BY THE FOREGOING LIMITATIONS.

IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT� 3 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

Moncler ITALY / Luxury

IPO

MAIN METRICS 2012 2013E 2014E

Revenues 489 573 666

EBITDA 162 189 215

Net income 82 94 114

Adj. net income 82 95 114

INDEBTEDNESS 2012 2013E 2014E

NFP -229 -171 -96

Debt/EBITDA 1.4 x 0.9 x 0.4 x

Interests cov 9.4 x 9.4 x 16.5 x ANALYSTS Paola Carboni - +39 026204287 – [email protected] November 8, 2013 # 355

GROWTH BASED ON EXCLUSIVENESS

The Moncler brand is leader in luxury outerwear and boasts a

superior track record of growth and profitability. More remarkably,

this success was built on exclusiveness and uniqueness, thus

enhancing – and not diluting – brand’s potential for future long

lasting growth. We expect a 3-Y CAGR of +15% for sales and +20% for

net profit in 2014-16, driven by retail and further internationalisation.

� The Moncler brand’s roots: strong heritage and international vocation

The Moncler brand’s roots date back to the 1950s, when it equipped the

Italian Himalayan expedition. In the 1970s it became a symbol of an elite

skiing, worn by stars like Brigitte Bardot and Alain Delon during their snow

holidays. The link with skiing and with the snow tourism - which fuel an

international customer base by definition – give the brand a high international

vocation (60% of flagship stores’ sales in Western Europe come from tourists).

� Brand repositioning in luxury: uniqueness and exclusiveness

Mr Ruffini, present chairman and creative director, acquired the Moncler

brand in 2003, and since then he started a complete repositioning process:

- Wider assortment: the original alpine jacket was transformed in a versatile

garment, with a unique casual/chic style, conjugated in different lines and

collections, with increasing incidence of Spring/Summer items.

- Exclusiveness: higher pricing, no mark-down policy, lower importance

of the logo, thus overall increasing consumers’ perception of scarcity.

- Distribution: more selective (downsizing the multibrand channel and

starting development of a monobrand network) and global (contribution of

the Italian market down from 52% of FY08 brand’s sales to 26% in 2012).

� Strong track record of growth with best in class profitability

Moncler has posted a +29% const. curr. sales 2Y CAGR in 2011-12,

significantly above the +18% of main peers and in spite of its relatively

higher exposure to wholesale and to the Italian market at the end of 2010.

Actual 2012 numbers have even exceeded our past IPO estimates (June

2011) by more than 20%, thus proving management strong execution skills.

Moncler also ranks at the top of the sector in terms of profitability (33%

EBITDA margin in FY12, second only to Hermès and Prada) and cash

generation (unlevered FCF/EBITDA at 38% in 2012), which stem from

group’s high pricing power and strong retail skills (we estimate full-price sell-

through >85%, above 30k sales/sqm, stores at break-even in few months).

� 3Y net profit CAGR +20% driven by retail and internationalisation

We expect 2014-16 3-Y CAGR of +15% in sales driven by

- Expansion of retail: +22% CAGR, of which +8% SSS growth and

+14% space effect (+20 new openings a year), leveraging on current

underpenetration of the brand (only 122 stores as of September 2013).

- Internationalisation: growth in Asia (+15% CAGR) and in Americas

(+26% CAGR) is expected to explain 60% of the total revenue bridge,

with the remaining 40% coming from EMEA (+17% CAGR exp.).

Sales mix and volume growth should offset rising fixed costs (store network

+ corporate structure), while earnings should benefit from deleveraging,

thanks to accelerating FCF. 9M13 earnings were already up by +19% YoY.

� Valuation hints

We expect the market to reward Moncler with multiples above sector’s

average, following its high quality equity story and its faster than peers

growth prospects (2014-15 EPS CAGR of +21% vs. +14% for peers).

Moncler –November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 4 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

BUSINESS DESCRIPTION

The Moncler Group is leader in luxury outerwear (85% of

FY12 group revenues) with a unique positioning and strong

international vocation.

The group insources the higher value-added phases of the

production process (design and product development, sales

campaign, sourcing of raw materials, quality control,

communication and marketing) and outsources manufacturing

activities – all located in Europe.

The brand is distributed in 66 countries, both through

wholesale (49% of FY12 revenues) and retail (51% of FY12

revenues). As of September 2013, the monobrand distribution

network consisted of 98 DOS stores and 24 shop-in-shop

wholesale.

The group has raised its penetration abroad in the last few

years, with Italy now accounting for only 26% of 2012

revenues.

MAIN FIGURES € mn 2011 2012 2013E 2014E 2015E 2016E

Revenues 364 489 573 666 768 872

Growth 29% 34% 17% 16% 15% 14%

EBITDA 112 162 189 215 254 291

Growth 23% 45% 17% 14% 18% 15%

Adjusted EBITDA 114 162 187 215 254 291

Growth 26% 41% 16% 15% 18% 15%

EBIT 102 146 168 188 221 252

Growth 20% 43% 15% 12% 18% 14%

Profit before tax 89 129 148 175 213 251

Growth n.a. 44% 15% 18% 22% 18%

Net income 56 82 94 114 139 164

Growth n.a. 47% 14% 21% 22% 18%

Adj. net income 58 82 95 114 139 164

Growth n.a. 43% 15% 20% 22% 18%

MARGIN 2011 2012 2013E 2014E 2015E 2016E

Ebitda Margin 30.7% 33.0% 32.9% 32.2% 33.0% 33.4%

Ebitda adj Margin 31.5% 33.0% 32.6% 32.2% 33.0% 33.4%

Ebit margin 28.0% 29.8% 29.3% 28.2% 28.7% 28.9%

Pbt margin 24.6% 26.3% 25.8% 26.2% 27.7% 28.8%

Ni rep margin 15.4% 16.9% 16.4% 17.1% 18.1% 18.8%

Ni adj margin 15.9% 16.9% 16.5% 17.1% 18.1% 18.8%

VARIOUS - € mn 2011 2012 2013E 2014E 2015E 2016E

Capital emloyed 394 421 455 470 502 524

FCF 26 49 54 72 108 142

Capex 35 26 34 34 35 35

Trade working capital 18 37 56 82 104 122

INDEBTNESS - €mn 2011 2012 2013E 2014E 2015E 2016E

NFP -270 -229 -171 -96 -17 90

D/E 2.18 x 1.19 x 0.60 x 0.26 x 0.03 x n.m.

Debt/EBITDA 2.4 x 1.4 x 0.9 x 0.4 x 0.1 x n.m.

Interests cov 9.0 x 9.4 x 9.4 x 16.5 x 33.4 x 224.2 x

REMUNERATION 2011 2012 2013E 2014E 2015E 2016E

ROE 45.0% 42.9% 33.2% 30.4% 28.7% 26.7%

ROCE 16.2% 22.2% 23.5% 26.0% 28.7% 31.5%

Source: EQUITA SIM estimates and company data FCF calculated as: change in NFP plus dividends distributed during the period

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 5 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

TABLE OF CONTENTS

INVESTMENT SUMMARY ............................................................................................. 6

HIGH QUALITY, FOR BOTH CONSUMERS AND INVESTORS ............................... 12

GROUP’S ORIGINS AND PRESENT SHAREHOLDER BASE .................................. 13

THE IPO ........................................................................................................................ 13

REPOSITIONING IN THE LUXURY ARENA: UNIQUENESS AND EXCLUSIVITY .. 14

THE MONCLER BRAND TODAY: “THE GLOBAL DUVET JACKET” ........................ 17

A SUPERIOR TRACK RECORD OF GROWTH ….. ................................................... 22

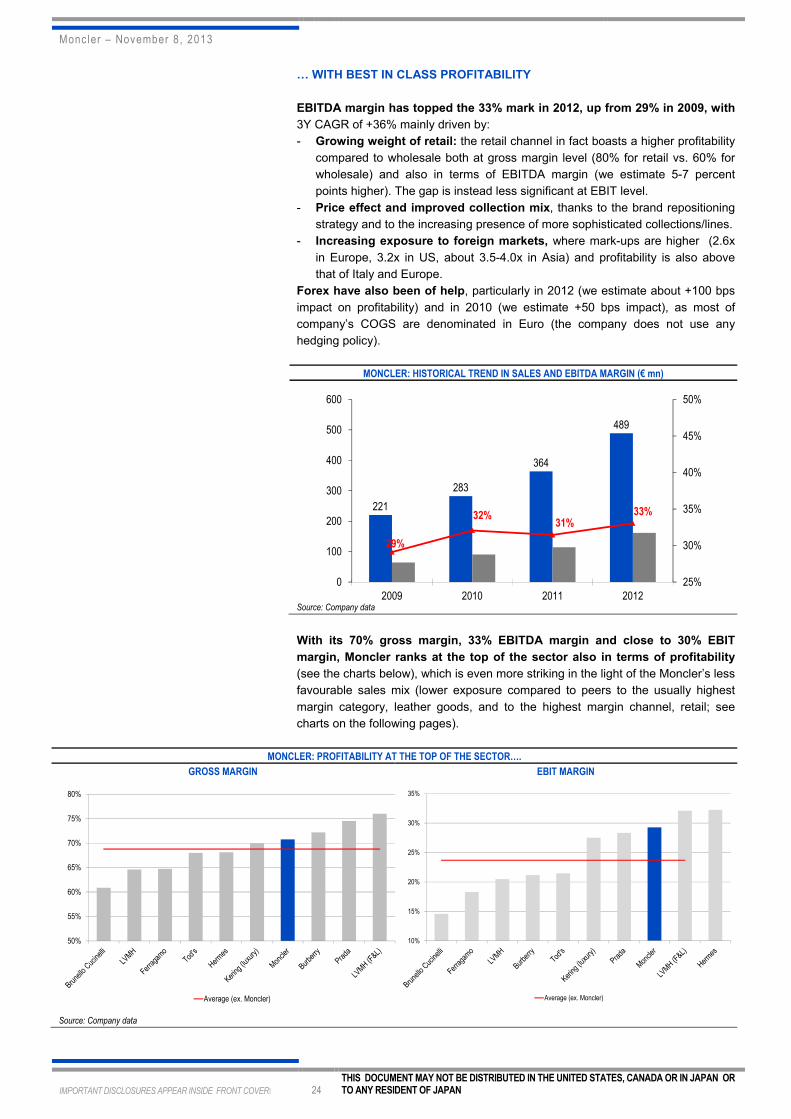

… WITH BEST IN CLASS PROFITABILITY ................................................................ 24

VISIBLE GROWTH PROSPECTS ............................................................................... 27

SEASONALITY OF RESULTS ..................................................................................... 31

9M RESULTS LARGELY UNDERPIN OUR FY13 ESTIMATES ................................ 33

2014-2016 ESTIMATES: +20% CAGR IN EARNINGS, DRIVEN BY RETAIL AND

FOREIGN MARKETS ................................................................................................... 37

SWOT ANALYSIS ......................................................................................................... 42

VALUATION HINTS ...................................................................................................... 43

STATEMENT OF RISKS .............................................................................................. 46

APPENDIX 1: STILL POSITIVE LONG TERM PROSPECTS FOR LUXURY ............ 47

APPENDIX 2: MONCLER’S OPERATIONS ................................................................ 50

APPENDIX 3: STRONG AND LOYAL MANAGEMENT TEAM ................................... 54

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 6 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

INVESTMENT SUMMARY

MONCLER’S HISTORY: STRONG HERITAGE AND REPOSITIONING IN LUXURY

The Moncler brand’s roots date back to the 1950s, when it equipped the Italian

Himalayan expedition, as a high performance technical jacket born for Alpine use. In

the 1970’s it became a symbol of an elite skiing, worn by stars like Brigitte Bardot

and Alain Delon during their holidays in the midst of the snow.

The story of the Moncler brand then became a story of fast growth (3-year

sales CAGR = 30% in 2010-12, based on 2009 divisional data) and

internationalization (74% of sales outside of Italy in FY12), thanks to the

remarkable success of the restyling and repositioning process undertaken by the

present chairman and creative director, Remo Ruffini, who acquired the brand in

2003. Since the beginning, Mr. Ruffini’s strategy was centred on brand’s

exclusiveness, through

- A wider assortment: the original alpine jacket was transformed in a versatile

garment, with a unique casual/chic style, conjugated in different lines and

collections, with increasing incidence of Spring/Summer items.

- Greater exclusiveness: higher pricing (€ 800-1000 for the Autumn/Winter

collection), no mark-down policy, lower importance of the logo, thus overall

increasing consumers’ perception of scarcity. As a further luxury statement, the

Main Collection has been flanked by two haute couture collections presented

at the main European fashion weeks (Paris and Milan).

- More selective distribution (downsizing the multibrand channel and starting

development of a monobrand network) and more global presence (contribution

of the Italian market down from 52% of FY08 brand’s sales to 26% in 2012).

THE MONCLER BRAND TODAY: THE “GLOBAL DUVET JACKET”

The Moncler brand now rightfully forms part of the luxury arena by virtue of its

strong heritage, exclusiveness, very high quality, high price positioning, strong

recognisability and iconic products.

In our opinion the strength of the Moncler brand lies in:

- the uniqueness of its proposition and positioning. Moncler has managed to

win leadership in outerwear thanks to an across-the-board style – which we

can define as casual/chic, informal but refined at the same time – that, in its

various conjugations and lines - make it suitable for different occasions and for

different consumers; a contemporary style, designed to survive fashion

- its strong international vocation, thanks to the link with skiing and with the

snow tourism, which, by definition, fuel an International customer base. This

has been a key success factor for the rapid international expansion of the

brand outside its domestic market. As a matter of fact, 60% of revenues in

group’s Western European flagship stores are generated by tourists. Light

duvet jackets for example are a key success factor for the brand vis à vis

customers from warmer regions such as Brazil, Middle East, Hong Kong.

DISTRIBUTION PLATFORM LEVERAGING ON RETAIL AND WHOLESALE

The retail channel accounted for 51% of Moncler’s 2012 revenues.

Sales in this channel are generated by a network of 98 free standing DOS (as of

September 2013), of which 56 are in the Emea region (of which 17 in Italy), 6 are

in the Americas (US), and 36 are in Asia (of which 15 in Mainland China).

The chart below summarizes the estimated contribution of each single

combination of channel/region to Moncler’s revenues, based on FY12 numbers.

As one can see, the most important revenue sources for the group are the retail

channel in Asia and the wholesale channel in Emea.

CHANNEL BKD 2012

Source: Company data

Wholesale49%

Retail51%

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 7 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

MONCLER: MAIN CONTRIBUTORS TO TOTAL SALES

Source: Company data

A SUPERIOR TRACK RECORD WITH UNTAPPED GROWTH POTENTIAL

MONCLER: HISTORICAL TREND IN SALES AND EBITDA MARGIN (€ mn)

Source: Company data

Two years after the past IPO attempt of June 2011 (which ended with the entry of

Eurazeo in the company’s share capital), Moncler comes to the market today boasting:

- a clearer equity story, offering a pure bet on luxury, thanks to the disposal of

the “Casual Brands” division (four brands positioned in the medium/high-end

casual wear segment), which has been just signed (closing on November 8th).

- an even stronger brand positioning, with an enhanced sales mix in terms of

distribution channels (retail up to 51% of revenues vs. 27% in 2010, growing at

+82% 2Y CAGR) and geographies (Americas and Asia up to 42% of revenues

vs. 24% in 2010, growing at +73% 2Y CAGR), consistently with the strategic

guidelines highlighted by management two years ago.

- a superior track record of growth, with +30% 3Y sales CAGR in the 2010-

2012 period, significantly above the +11% CAGR of the global luxury market as

a whole and the +18% of main listed peers. The company has also beaten our

past IPO estimates by more than 20%, whereas the other main listed luxury

peers have exceeded 18-month-earlier consensus estimates by only 6%.

- best in class profitability, with Ebitda margin of 33%, at the top of the sector,

second only to Hermès and Prada which however can rely on a much stronger

exposure to leather goods and retail. We mainly attribute the superior

profitability of Moncler to its higher mark-ups (we estimate 10% above the

sector average, particularly abroad) and to its strong retail skills (full-price sell-

through that we estimate at 85-90%, no mark-down policy, best-in-class sales

densities - we estimate above € 30,000/sqm -, stores at break-even usually a

few months after inauguration).

15%

12%

24%8%5%

27%

5%5%

�� Emea

�� America

�� Asia

��Italy

dark = retail pale = wholesale

221

283

364

489

29%

32%31%

33%

25%

30%

35%

40%

45%

50%

0

100

200

300

400

500

600

2009 2010 2011 2012

Sales

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 8 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

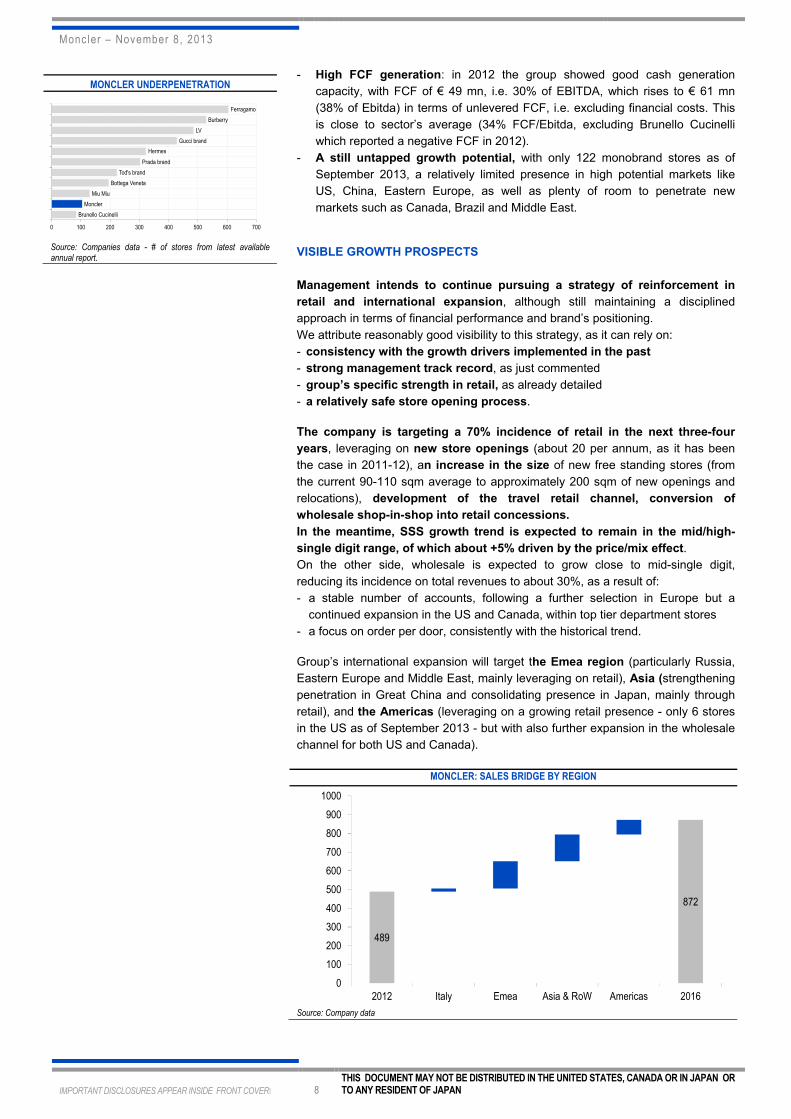

- High FCF generation: in 2012 the group showed good cash generation

capacity, with FCF of € 49 mn, i.e. 30% of EBITDA, which rises to € 61 mn

(38% of Ebitda) in terms of unlevered FCF, i.e. excluding financial costs. This

is close to sector’s average (34% FCF/Ebitda, excluding Brunello Cucinelli

which reported a negative FCF in 2012).

- A still untapped growth potential, with only 122 monobrand stores as of

September 2013, a relatively limited presence in high potential markets like

US, China, Eastern Europe, as well as plenty of room to penetrate new

markets such as Canada, Brazil and Middle East.

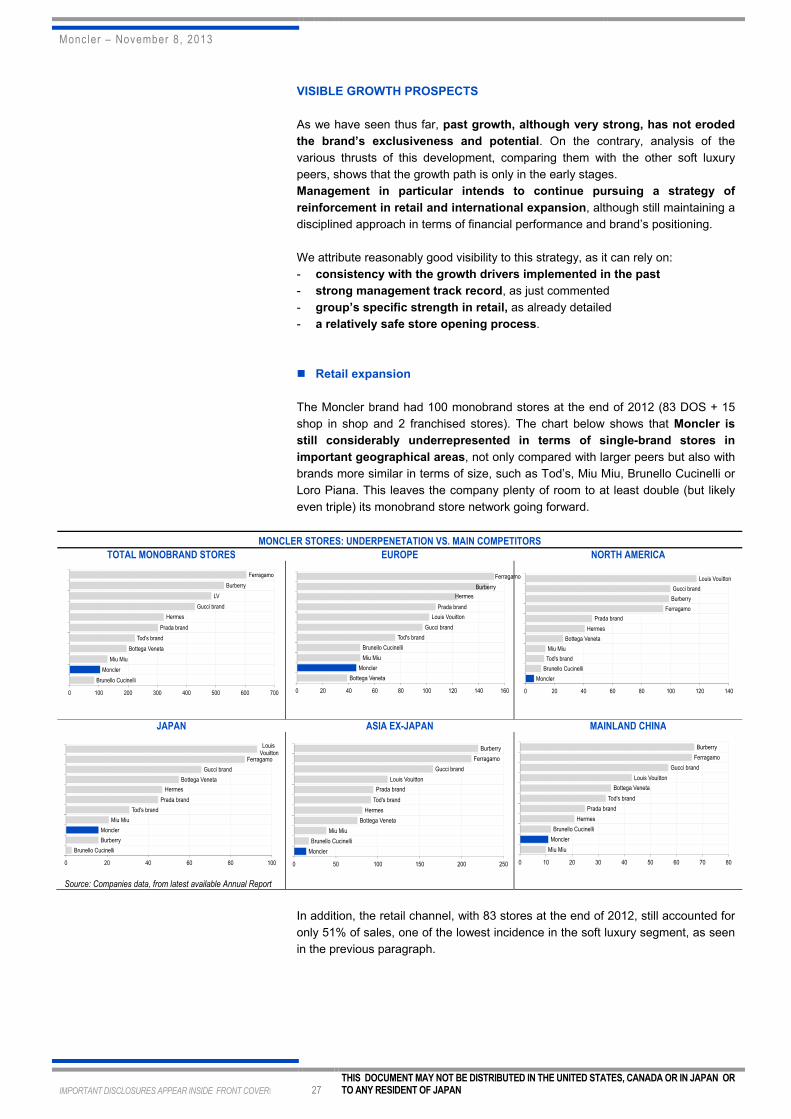

VISIBLE GROWTH PROSPECTS

Management intends to continue pursuing a strategy of reinforcement in

retail and international expansion, although still maintaining a disciplined

approach in terms of financial performance and brand’s positioning.

We attribute reasonably good visibility to this strategy, as it can rely on:

- consistency with the growth drivers implemented in the past

- strong management track record, as just commented

- group’s specific strength in retail, as already detailed

- a relatively safe store opening process.

The company is targeting a 70% incidence of retail in the next three-four

years, leveraging on new store openings (about 20 per annum, as it has been

the case in 2011-12), an increase in the size of new free standing stores (from

the current 90-110 sqm average to approximately 200 sqm of new openings and

relocations), development of the travel retail channel, conversion of

wholesale shop-in-shop into retail concessions.

In the meantime, SSS growth trend is expected to remain in the mid/high-

single digit range, of which about +5% driven by the price/mix effect.

On the other side, wholesale is expected to grow close to mid-single digit,

reducing its incidence on total revenues to about 30%, as a result of:

- a stable number of accounts, following a further selection in Europe but a

continued expansion in the US and Canada, within top tier department stores

- a focus on order per door, consistently with the historical trend.

Group’s international expansion will target the Emea region (particularly Russia,

Eastern Europe and Middle East, mainly leveraging on retail), Asia (strengthening

penetration in Great China and consolidating presence in Japan, mainly through

retail), and the Americas (leveraging on a growing retail presence - only 6 stores

in the US as of September 2013 - but with also further expansion in the wholesale

channel for both US and Canada).

MONCLER: SALES BRIDGE BY REGION

Source: Company data

MONCLER UNDERPENETRATION

Source: Companies data - # of stores from latest available annual report.

489

872

0

100

200

300

400

500

600

700

800

900

1000

2012 Italy Emea Asia & RoW Americas 2016

Brunello Cucinelli

Moncler

Miu Miu

Bottega Veneta

Tod's brand

Prada brand

Hermes

Gucci brand

LV

Burberry

Ferragamo

0 100 200 300 400 500 600 700

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 9 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

With outerwear still accounting for 85% of revenues, the company has also clear

growth opportunities in other product categories. Focus will be mainly on

knitwear, which is more consistent with the brand’s heritage. Offering is also

being widened in leather goods (still at 4-5% of revenues, mainly shoes), as well

as in accessories such as eyewear or suitcases, with recent specific product

initiatives. However, we see these drivers simply as a further support to

revenue growth, without factoring in any drastic acceleration in the

incidence of non-outerwear: management is in fact committed to remain

consistent with group’s DNA and heritage, focused on winter jackets.

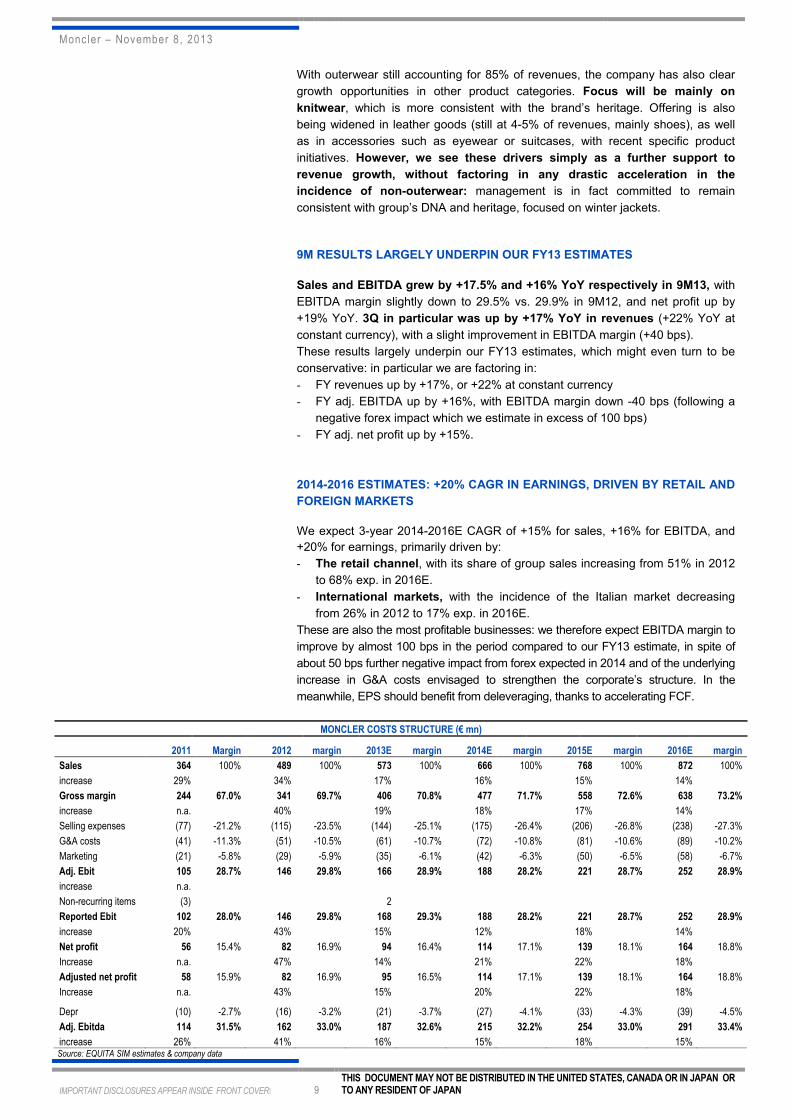

9M RESULTS LARGELY UNDERPIN OUR FY13 ESTIMATES

Sales and EBITDA grew by +17.5% and +16% YoY respectively in 9M13, with

EBITDA margin slightly down to 29.5% vs. 29.9% in 9M12, and net profit up by

+19% YoY. 3Q in particular was up by +17% YoY in revenues (+22% YoY at

constant currency), with a slight improvement in EBITDA margin (+40 bps).

These results largely underpin our FY13 estimates, which might even turn to be

conservative: in particular we are factoring in:

- FY revenues up by +17%, or +22% at constant currency

- FY adj. EBITDA up by +16%, with EBITDA margin down -40 bps (following a

negative forex impact which we estimate in excess of 100 bps)

- FY adj. net profit up by +15%.

2014-2016 ESTIMATES: +20% CAGR IN EARNINGS, DRIVEN BY RETAIL AND

FOREIGN MARKETS

We expect 3-year 2014-2016E CAGR of +15% for sales, +16% for EBITDA, and

+20% for earnings, primarily driven by:

- The retail channel, with its share of group sales increasing from 51% in 2012

to 68% exp. in 2016E.

- International markets, with the incidence of the Italian market decreasing

from 26% in 2012 to 17% exp. in 2016E.

These are also the most profitable businesses: we therefore expect EBITDA margin to

improve by almost 100 bps in the period compared to our FY13 estimate, in spite of

about 50 bps further negative impact from forex expected in 2014 and of the underlying

increase in G&A costs envisaged to strengthen the corporate’s structure. In the

meanwhile, EPS should benefit from deleveraging, thanks to accelerating FCF.

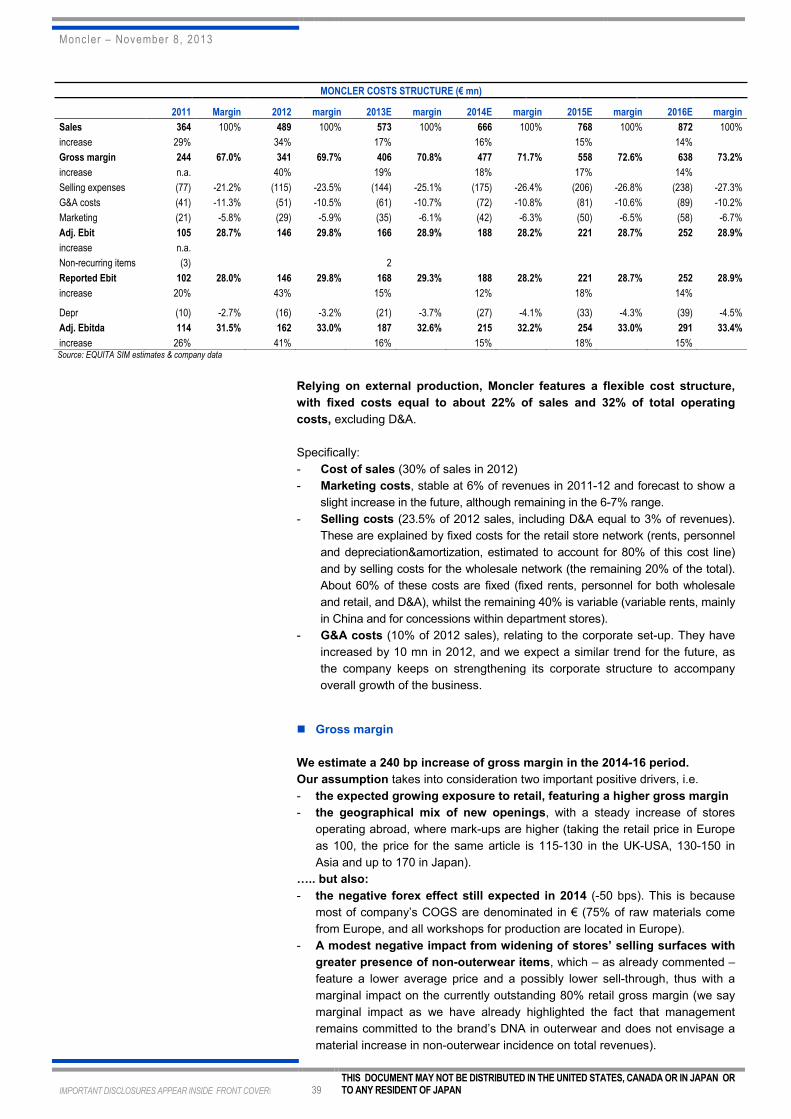

MONCLER COSTS STRUCTURE (€ mn)

2011 Margin 2012 margin 2013E margin 2014E margin 2015E margin 2016E margin

Sales 364 100% 489 100% 573 100% 666 100% 768 100% 872 100%

increase 29% 34% 17% 16% 15% 14%

Gross margin 244 67.0% 341 69.7% 406 70.8% 477 71.7% 558 72.6% 638 73.2%

increase n.a. 40% 19% 18% 17% 14%

Selling expenses (77) -21.2% (115) -23.5% (144) -25.1% (175) -26.4% (206) -26.8% (238) -27.3%

G&A costs (41) -11.3% (51) -10.5% (61) -10.7% (72) -10.8% (81) -10.6% (89) -10.2%

Marketing (21) -5.8% (29) -5.9% (35) -6.1% (42) -6.3% (50) -6.5% (58) -6.7%

Adj. Ebit 105 28.7% 146 29.8% 166 28.9% 188 28.2% 221 28.7% 252 28.9%

increase n.a.

Non-recurring items (3) 2

Reported Ebit 102 28.0% 146 29.8% 168 29.3% 188 28.2% 221 28.7% 252 28.9%

increase 20% 43% 15% 12% 18% 14%

Net profit 56 15.4% 82 16.9% 94 16.4% 114 17.1% 139 18.1% 164 18.8%

Increase n.a. 47% 14% 21% 22% 18%

Adjusted net profit 58 15.9% 82 16.9% 95 16.5% 114 17.1% 139 18.1% 164 18.8%

Increase n.a. 43% 15% 20% 22% 18%

Depr (10) -2.7% (16) -3.2% (21) -3.7% (27) -4.1% (33) -4.3% (39) -4.5%

Adj. Ebitda 114 31.5% 162 33.0% 187 32.6% 215 32.2% 254 33.0% 291 33.4%

increase 26% 41% 16% 15% 18% 15% Source: EQUITA SIM estimates & company data

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 10 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

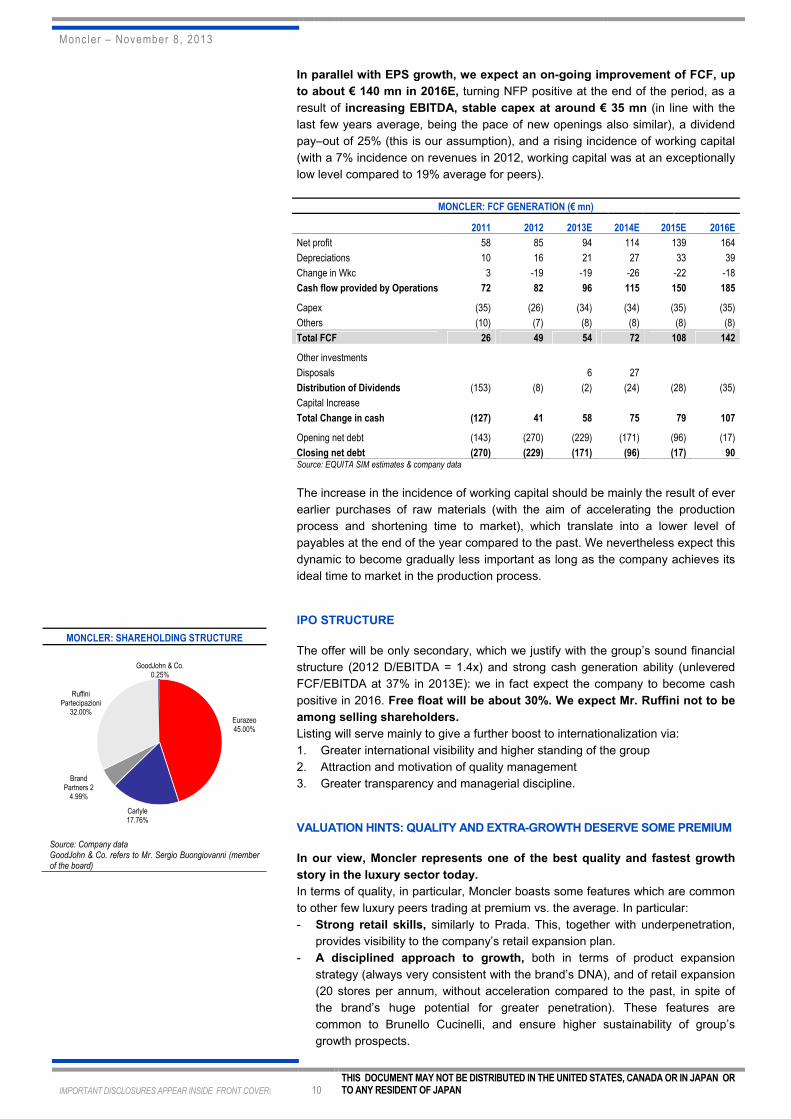

In parallel with EPS growth, we expect an on-going improvement of FCF, up

to about € 140 mn in 2016E, turning NFP positive at the end of the period, as a

result of increasing EBITDA, stable capex at around € 35 mn (in line with the

last few years average, being the pace of new openings also similar), a dividend

pay–out of 25% (this is our assumption), and a rising incidence of working capital

(with a 7% incidence on revenues in 2012, working capital was at an exceptionally

low level compared to 19% average for peers).

MONCLER: FCF GENERATION (€ mn)

2011 2012 2013E 2014E 2015E 2016E

Net profit 58 85 94 114 139 164

Depreciations 10 16 21 27 33 39

Change in Wkc 3 -19 -19 -26 -22 -18

Cash flow provided by Operations 72 82 96 115 150 185

Capex (35) (26) (34) (34) (35) (35)

Others (10) (7) (8) (8) (8) (8)

Total FCF 26 49 54 72 108 142

Other investments

Disposals 6 27

Distribution of Dividends (153) (8) (2) (24) (28) (35)

Capital Increase

Total Change in cash (127) 41 58 75 79 107

Opening net debt (143) (270) (229) (171) (96) (17)

Closing net debt (270) (229) (171) (96) (17) 90 Source: EQUITA SIM estimates & company data

The increase in the incidence of working capital should be mainly the result of ever

earlier purchases of raw materials (with the aim of accelerating the production

process and shortening time to market), which translate into a lower level of

payables at the end of the year compared to the past. We nevertheless expect this

dynamic to become gradually less important as long as the company achieves its

ideal time to market in the production process.

IPO STRUCTURE

The offer will be only secondary, which we justify with the group’s sound financial

structure (2012 D/EBITDA = 1.4x) and strong cash generation ability (unlevered

FCF/EBITDA at 37% in 2013E): we in fact expect the company to become cash

positive in 2016. Free float will be about 30%. We expect Mr. Ruffini not to be

among selling shareholders.

Listing will serve mainly to give a further boost to internationalization via:

1. Greater international visibility and higher standing of the group

2. Attraction and motivation of quality management

3. Greater transparency and managerial discipline.

VALUATION HINTS: QUALITY AND EXTRA-GROWTH DESERVE SOME PREMIUM

In our view, Moncler represents one of the best quality and fastest growth

story in the luxury sector today.

In terms of quality, in particular, Moncler boasts some features which are common

to other few luxury peers trading at premium vs. the average. In particular:

- Strong retail skills, similarly to Prada. This, together with underpenetration,

provides visibility to the company’s retail expansion plan.

- A disciplined approach to growth, both in terms of product expansion

strategy (always very consistent with the brand’s DNA), and of retail expansion

(20 stores per annum, without acceleration compared to the past, in spite of

the brand’s huge potential for greater penetration). These features are

common to Brunello Cucinelli, and ensure higher sustainability of group’s

growth prospects.

MONCLER: SHAREHOLDING STRUCTURE

Source: Company data GoodJohn & Co. refers to Mr. Sergio Buongiovanni (member of the board)

Eurazeo45.00%

Carlyle17.76%

Brand Partners 24.99%

Ruffini Partecipazioni32.00%

GoodJohn & Co.0.25%

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 11 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

- A low fashion content, which is a strong loyalty building element for

consumers. This feature recalls Brunello Cucinelli and Tod’s products.

- Highly recognizable and iconic products, which can be changed in few

details or in fabrics and colours - offering consumers always new occasions to

buy – while remaining always recognizable and up to date (similar to Tod’s).

- Best in class profitability (Ebitda margin at 33% on revenues, similarly to

Prada, compared to a 27% average for the sector) and high FCF generation

(37% unlevered FCF/Ebitda exp. in 2013E).

- Pure luxury play status, compared to other leading global brands such as

Gucci or Louis Vuitton, which are within big conglomerates.

MULTIPLE COMPARISON

Price Perf. EV/EBITDA Ebitda margin Sales growth P/E EPS Cagr Asia

€ 3M 2013E 2014E 2015E 2013E 2014E 2015E 2013E 2014E 2015E 2013E 2014E 2015E 2014E-15E Ex-Jap

Hermes 255 -2% 19.1 16.9 14.7 36% 36% 36% 9% 11% 12% 32.9 29.5 26.1 12% 32%

Brunello Cucinelli 23 9% 27.7 23.6 20.1 18% 19% 19% 14% 13% 13% 54.7 45.1 38.4 19% 12%

LVMH 140 1% 10.0 8.6 7.9 25% 25% 25% 8% 12% 9% 19.1 16.3 14.7 14% 28%

Richemont 93 0% 13.0 11.5 10.1 28% 29% 29% 8% 10% 9% 19.1 17.0 15.3 12% 41%

Tiffany 78 -4% 11.0 9.8 8.8 24% 24% 25% 5% 8% 9% 21.6 19.1 16.9 13% 21%

Burberry 1,494 -4% 10.4 9.2 8.2 26% 27% 24% 16% 14% 19% 17.8 15.5 14.1 12% 31%

Kering (luxury) 165 -8% 9.9 8.6 7.7 29% 29% 29% 1% 7% 9% 16.0 14.7 13.1 10% 31%

Swatch 575 3% 11.8 10.2 8.8 28% 29% 30% 12% 10% 9% 18.1 16.1 14.4 12% 49%

Tod's 124 -9% 14.1 12.7 11.1 26% 26% 27% 4% 7% 10% 25.2 22.5 19.7 13% 25%

Prada 77 7% 14.8 12.1 10.2 34% 35% 36% 12% 15% 13% 25.6 21.1 18.2 19% 36%

Ferragamo 25 -2% 15.5 13.3 11.0 22% 22% 24% 10% 11% 11% 28.6 24.5 20.5 18% 37%

Average 14.3 12.4 10.8 27% 27% 28% 9% 11% 11% 25.3 22.0 19.2 14% 31%

Average ex-BC & RMS -2% 12.3 10.7 9.3 27% 27% 28% 9% 10% 11% 21.2 18.5 16.3 Moncler 33% 32% 33% 17% 16% 15% 21% 16% Source: Bloomberg consensus and EQUITA SIM estimates. Closure prices of Nov 7th , 2013

Moncler also deserves a premium in our view for its faster growth prospects,

with expected EPS CAGR in 2014-15 of +21% vs. 14% average for the sector.

For this reason, we would focus valuation on 2015 rather than on 2013-14, in

order to try to capture most of the company’s extra-growth potential.

Overall, for all the reasons just mentioned, we think the company should

merit a multiple above the luxury sector average.

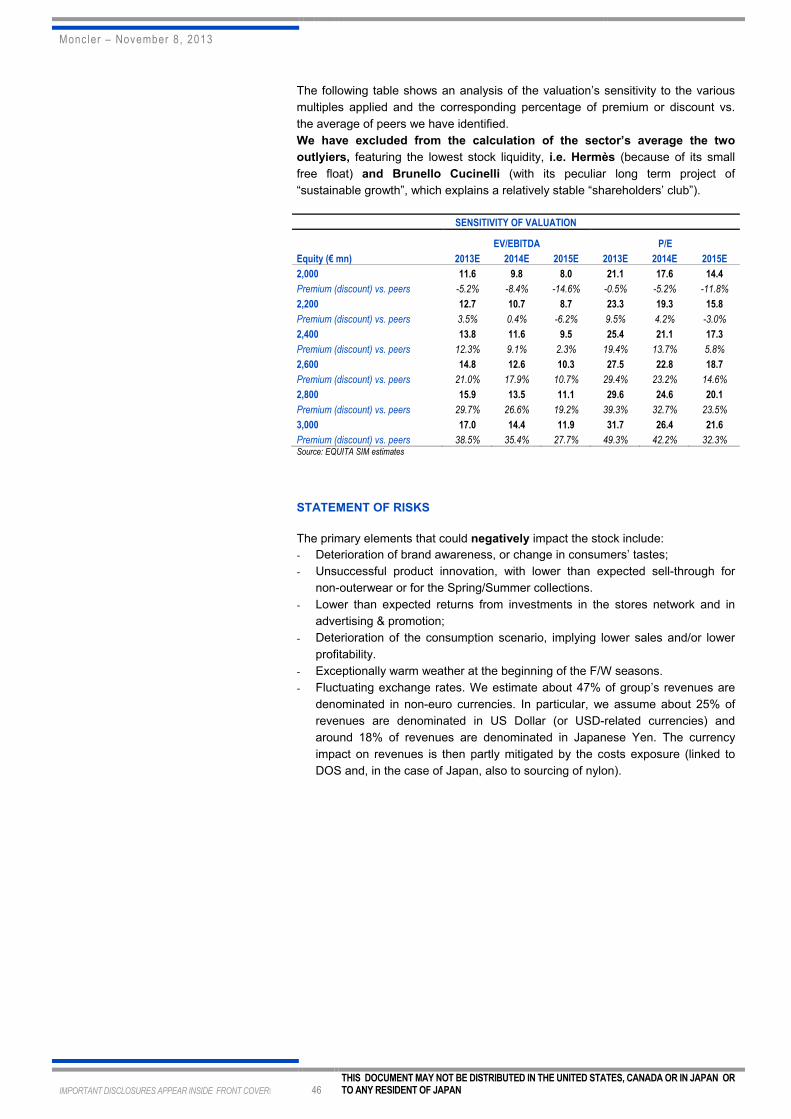

The following table shows an analysis of the valuation’s sensitivity to the various

multiples applied and the corresponding percentage of premium or discount vs.

the average of peers we have identified.

We have excluded from the calculation of the sector’s average the two outlyiers,

featuring the lowest stock liquidity, i.e. Hermès (because of its small free float) and

Brunello Cucinelli (with its peculiar long term project of “sustainable growth”, which

explains a relatively stable “shareholders’ club”).

SENSITIVITY OF VALUATION

EV/EBITDA P/E

Equity (€ mn) 2013E 2014E 2015E 2013E 2014E 2015E

2,000 11.6 9.8 8.0 21.1 17.6 14.4

Premium (discount) vs. peers -5.2% -8.4% -14.6% -0.5% -5.2% -11.8%

2,200 12.7 10.7 8.7 23.3 19.3 15.8

Premium (discount) vs. peers 3.5% 0.4% -6.2% 9.5% 4.2% -3.0%

2,400 13.8 11.6 9.5 25.4 21.1 17.3

Premium (discount) vs. peers 12.3% 9.1% 2.3% 19.4% 13.7% 5.8%

2,600 14.8 12.6 10.3 27.5 22.8 18.7

Premium (discount) vs. peers 21.0% 17.9% 10.7% 29.4% 23.2% 14.6%

2,800 15.9 13.5 11.1 29.6 24.6 20.1

Premium (discount) vs. peers 29.7% 26.6% 19.2% 39.3% 32.7% 23.5%

3,000 17.0 14.4 11.9 31.7 26.4 21.6

Premium (discount) vs. peers 38.5% 35.4% 27.7% 49.3% 42.2% 32.3% Source: EQUITA SIM estimates

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 12 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

HIGH QUALITY, FOR BOTH CONSUMERS AND INVESTORS

The Moncler brand’s roots date back to the 1950s, when it equipped the Italian

Himalayan expedition, as a high performance technical jacket born for Alpine use. In

the 1970’s it became a symbol of an elite skiing, worn by stars like Brigitte Bardot

and Alain Delon during their holidays in the midst of the snow.

The story of the Moncler brand then became a story of fast

growth (3-year sales CAGR = 30% in 2010-12, based on 2009

divisional data) and internationalization (today 74% of sales

are generated abroad), thanks to the remarkable success of

the restyling and repositioning process undertaken by the

present chairman and creative director, Remo Ruffini, who

acquired the brand in 2003. Since the beginning, Mr. Ruffini’s

strategy was centred on brand’s exclusiveness, working on both product

offering (style, materials, overall brand’s architecture) and distribution (careful

selection in the wholesale channel, internalisation of licenses, start of a

monobrand presence consistent with the brand’s new image).

Today the Moncler brand not only rightfully forms part of the luxury arena

(strong heritage, exclusiveness, very high quality, high price positioning, strong

recognisability and iconic products) – but it also holds:

- a unique positioning as leader in luxury outerwear, with a contemporary

casual/chic style conceived to survive fashion, conjugated in several lines and

collections, suitable to a variegated public and different occasions for use.

- a strong international vocation, thanks to the link with skiing and with the snow

tourism, which, by definition, fuel an International customer base. As a matter of fact,

60% of revenues in group’s Western European flagship stores are generated by

tourists, with most of that coming from Non-European customers.

Two years after the past IPO attempt of June 2011 (which ended with the entry of

Eurazeo in the company’s share capital), Moncler comes to the market today boasting:

- a clearer equity story, offering a pure bet on luxury, thanks to the disposal of

the “Casual Brands” division (four brands positioned in the medium/high-end

casual wear segment), which has been just signed (closing on November 8th).

- an even stronger brand positioning, with an enhanced sales mix in terms of

distribution channels (retail up to 51% of revenues vs. 27% in 2010, growing at

+82% 2Y CAGR) and geographies (Americas and Asia up to 42% of revenues

vs. 24% in 2010, growing at +73% 2Y CAGR), consistently with the strategic

guidelines highlighted by management two years ago.

- a superior track record of growth and profitability (see the table below),

beating our past IPO estimates by more than 20%: the group has closed 2012

with € 489 mn revenues and € 162 mn Ebitda, with Ebitda margin of 33%, at

the top of the sector, second only to Hermès and Prada which however can

rely on a much stronger exposure to leather goods and retail.

- a still untapped growth potential, with only 122 monobrand stores as of

September 2013, a relatively limited presence in high potential markets like

US, China, Eastern Europe, as well as plenty of room to penetrate new

markets such as Canada, Brazil and Middle East.

Moncler represents in our view one of the best quality and fastest growth

story in the luxury sector today.

MONCLER MAIN NUMBERS (€ mn)

2010 Margin 2011 Margin 2012 Margin 3Y CAGR

Sales 283 100% 364 100% 489 100%

Increase 28.1% 28.7% 34.5% 30%

Adj. Ebitda 91 32% 114 31% 162 33%

Increase 41.1% 26.3% 41.2% 36%

Adj. Net profit n.a. n.a. 58 15.9% 82 16.9%

Increase n.a. n.a. 42.7% n.a. Source: Equita SIM estimates and Company data

CHANNEL BKD 2012

Source: Company data

GEOGRAPHICAL BKD 2012

Source: Company data

Wholesale49%

Retail51%

Italy26%

Emea ex Italy32%

Asia and RoW32%

Americas10%

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 13 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

GROUP’S ORIGINS AND PRESENT SHAREHOLDER BASE

To pass from the historical Moncler brand to the group that controls it today it is

necessary to go back to 2003, when the Italian entrepreneur Remo Ruffini -

present chairman and creative director - purchased the Moncler brand from the

Finpart group, within which he had made his mark as the creative director of the

subsidiary Pepper Industries (holding company for the brands that used to be part

of the “Other Brands” division, before their recent spin-off).

Purchase of the brand was followed by the purchase of operations. In 2005, with

the financial support of the Italian merchant bank Mittel, Mr. Ruffini in fact

purchased 100% of Pepper Industries, thus creating a whole group and initiating a

process of evolution and restyling of the main brand, Moncler.

In 2008, with entry as a shareholder of the Carlyle private equity fund, the relaunch

and internationalization plan initiated by Mr. Ruffini underwent acceleration,

particularly as regards strengthening of the retail strategy.

In June 2011, when the first IPO process took place, the sale to a third private

equity firm was finally preferred instead of the equity market: Eurazeo thus

entered the Moncler share capital with a 45% stake which it bought from:

- Carlyle (down from 48% to 17.76% today)

- Mittel (which, through its vehicle Brand Partners 2, went down from 13.5% to the

current 4.99%)

- Mr. Ruffini himself (through its holding company Ruffini Partecipazioni, which

went down from 38% to 32% today).

This is still the company’s current shareholding structure (see chart on the left).

When Carlyle entered the company in 2008, it valued Moncler Group (i.e.

including the “Other Brands” division) € 470 mn EV (i.e. 9x EV/EBITDA).

When Eurazeo entered the company in 2011, it valued the Moncler Group

(still including the “Other Brands” division) € 930 mn equity and € 1.2 bn EV

(following € 150 mn dividends distributed by the company just before the entry of

Eurazeo). The implied multiple at that time was 16x P/E or 10.2x EV/EBITDA,

based on our past estimates for 2011.

Most recently (August 2013), also the Investment Company Tamburi

Investment Partners acquired an indirect stake in Moncler (buying 14% of

Ruffini Partecipazioni from Mr. Ruffini), with an implicit valuation that we

estimate close to € 2 bn equity or € 2.17 bn EV. This would imply a 2013 P/E of

21x and EV/EBITDA of 11.6x (based on our 2013 estimates). An earn-out

mechanism has also been envisaged in favour of Mr. Ruffini.

THE IPO

The offer will be only secondary, which we justify with the group’s sound financial

structure (2012 D/EBITDA = 1.4x) and strong cash generation ability (unlevered

FCF/EBITDA at 40% in 2013E): we in fact expect the company to become cash

positive in 2016.

Free float will be about 30%. We expect Mr. Ruffini not to be among selling

shareholders.

Listing will serve mainly to give a further boost to internationalization via:

1. Greater international visibility and higher standing of the group

2. Attraction and motivation of quality management, including managers already

present in the company. A stock option plan up to 3% of company’s share

capital will be in place after the listing.

3. Greater transparency and managerial discipline.

MONCLER: SHAREHOLDING STRUCTURE

Source: Company data GoodJohn & Co. refers to Mr. Sergio Buongiovanni (member of the board)

Eurazeo45.00%

Carlyle17.76%

Brand Partners 24.99%

Ruffini Partecipazioni32.00%

GoodJohn & Co.0.25%

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 14 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

REPOSITIONING IN THE LUXURY ARENA: UNIQUENESS AND EXCLUSIVITY

In the 1980s the original Moncler duvet jacket had become a metropolitan

garment, in glazed nylon and flashy colours (blue, yellow, orange and green), with

a well visible logo on the front, immediately establishing itself as a must-have for

teenagers: a real fashion phenomenon. However, after the 1980s “explosion”, the

brand gradually lost its sparkle.

We now review the main steps of the repositioning and internationalization

process started by Mr. Ruffini in 2003, which has instead made of Moncler the

leading luxury sportswear brand as we know it today.

MONCLER BRAND REPOSITIONING

Source: Company data

� Wider assortment: beyond the historical sporty winter jackets

1) Wearability and materials: while maintaining and revisiting the historical

roots of the original alpine garment, on which the brand’s strong heritage is

based, at the same time Mr. Ruffini and his team have transformed it, with the

aim of making it an across-the-board brand, capable of being conjugated in

different occasions and for different consumers. In this way the duvet jacket

has become more feminine, slimmer and more chic – and also more versatile,

elegant and contemporary, suitable no longer just for the mountains and sport,

but also for towns and for the various moments of everyday life.

2) Overall architecture of the brand: Moncler Main Collection, the best known

and widest spread, has been developed in several lines with different styles

and price positionings (Première, Sport Chic and Archive), and new product

categories have been added to flank outerwear. The Main Collection has also

been joined by Grenoble, a technical/outdoor sports collection with a total look

proposition. At the same time, as a further luxury statement, the Main

Collection has been flanked by two haute couture collections (Gamme Rouge

for women, launched in 2006, and Gamme Bleu for men, launched in 2009),

designed by internationally famous stylists and presented at the main

European fashion weeks (Paris and Milan).

3) Deseasonalization: the weight of the Spring/Summer collections has steadily

increased in both channels, thanks also to innovative products such as the

“long saison” jacket (an extremely light down jacket, which can either be used

as a summer jacket or as an under-jacket for the colder days. Spring/summer

items now account for 30% in the wholesale channel and 15% in the retail

channel (the incidence is lower in retail as new stores are usually opened in

the F/W season, and also because the selling period of the S/S season is

usually shorter in group’s DOS, carrying winter items at full price also during

the January/February period).

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 15 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

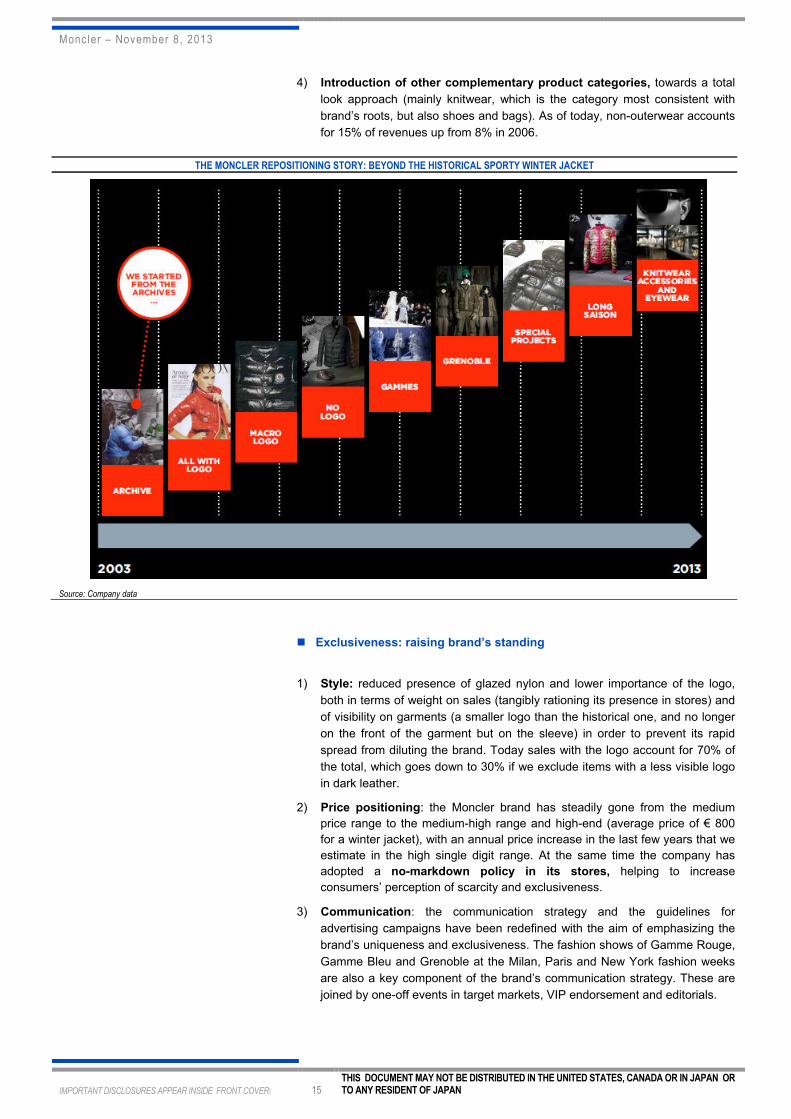

4) Introduction of other complementary product categories, towards a total

look approach (mainly knitwear, which is the category most consistent with

brand’s roots, but also shoes and bags). As of today, non-outerwear accounts

for 15% of revenues up from 8% in 2006.

THE MONCLER REPOSITIONING STORY: BEYOND THE HISTORICAL SPORTY WINTER JACKET

Source: Company data

� Exclusiveness: raising brand’s standing

1) Style: reduced presence of glazed nylon and lower importance of the logo,

both in terms of weight on sales (tangibly rationing its presence in stores) and

of visibility on garments (a smaller logo than the historical one, and no longer

on the front of the garment but on the sleeve) in order to prevent its rapid

spread from diluting the brand. Today sales with the logo account for 70% of

the total, which goes down to 30% if we exclude items with a less visible logo

in dark leather.

2) Price positioning: the Moncler brand has steadily gone from the medium

price range to the medium-high range and high-end (average price of € 800

for a winter jacket), with an annual price increase in the last few years that we

estimate in the high single digit range. At the same time the company has

adopted a no-markdown policy in its stores, helping to increase

consumers’ perception of scarcity and exclusiveness.

3) Communication: the communication strategy and the guidelines for

advertising campaigns have been redefined with the aim of emphasizing the

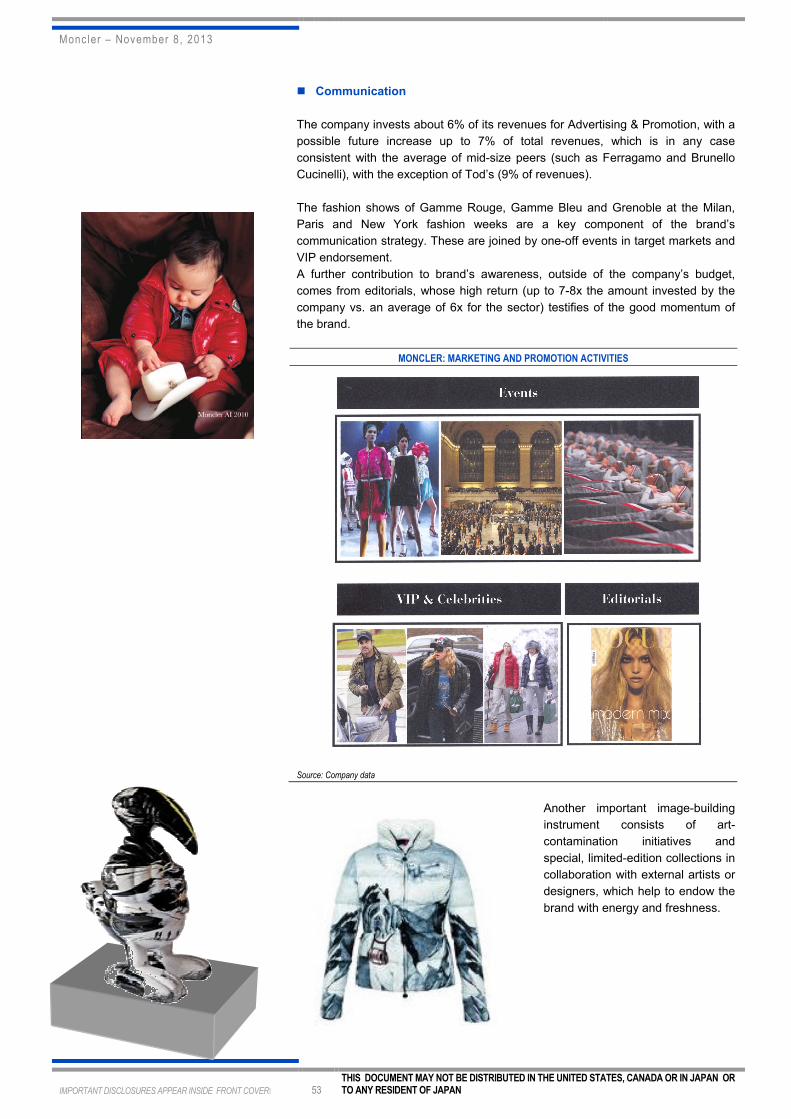

brand’s uniqueness and exclusiveness. The fashion shows of Gamme Rouge,

Gamme Bleu and Grenoble at the Milan, Paris and New York fashion weeks

are also a key component of the brand’s communication strategy. These are

joined by one-off events in target markets, VIP endorsement and editorials.

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 16 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

� Distribution: more selective and global

1) Downsizing of wholesale network of multibrand stores, which decreased

from about 2,800 stores in 2008 to about 1,850 as of today, with more

stringent selection above all in Italy and Japan were the wholesale presence

was most spread. Since the beginning, focus has shifted from the sports

product channel to that of apparel boutiques. The choice of stores now meets

specific criteria of consistency with the brand’s image in terms of choice of

assortment, store location and Moncler’s products visibility.

2) Development of a monobrand network to help strengthen the Moncler brand’s

image and accompany its internationalization. The first sky resort boutique was

opened in 2006, and in 2007 the first urban store. Today (as of September 2013),

the Moncler brand has 122 monobrand stores, of which 98 directly operated

(DOS), located in the main international cities and in some of the most

exclusive skiing localities.

3) Control of distribution, with the internalization in 2009 of licenses for the

Japanese market and for children’s wear, through the creation of two

dedicated joint ventures, 51% and 50.1% owned by the group, respectively

(the JV for the Enfant business has also been recently terminated and

Moncler will fully control the business as from January 1st, 2014).

4) Increasing penetration abroad, in particular in Asia but also in North America

and in the rest of Europe. The brand is now distributed in 66 countries around

the world. The incidence of the Italian market, in fact, has gradually

decreased, particularly in the last few years, going down from 52% of Moncler

brand revenues in 2008 to 26% in 2012.

MONCLER GROUP: EVOLUTION OF THE SALES MIX

GEOGRAPHICAL

Source: Company data

BY CHANNEL

Source: Company data

MONCLER GROUP: SUCCESSFUL PRODUCT EXPANSION

BREAKDOWN BY PRODUCT (2012)

Source: Company data

BREAKDOWN BY SEASON (2012)

Source: Company data

87% 83%73%

62%49%

13% 17%27%

38%51%

2008 2009 2010 2011 2012

Wholesale Retail

Outerwear85%

Non Outerwear15%

Fall/Winter77%

Spring/Summer23%

52% 50%42%

34%26%

34% 33%34%

33%32%

9% 13%18%

25%32%

5% 4% 6% 8% 10%

2008 2009 2010 2011 2012

Italy Emea ex Italy Asia and RoW Americas

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 17 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

THE MONCLER BRAND TODAY: “THE GLOBAL DUVET JACKET”

Thanks to the excellent work done by Mr. Ruffini and his team since 2003 to date,

the Moncler brand is now able to count on:

- Unique positioning in the luxury arena, with high international vocation

- A varied and structured proposition

- Multichannel and global distribution, efficient and consistent with the

brand’s positioning.

� A unique positioning in the luxury arena

Today the Moncler brand rightfully forms part of the luxury arena by virtue of its:

- Strong heritage, due to its historical reputation as a high-performance alpine

garment, associated with the important achievements of professional

mountaineers.

- Exclusiveness, fuelled by the high price positioning (as for outerwear, we

estimate an average price of € 800-1000 for the Autumn/Winter collection and

of € 400-500 for the Spring/Summer collection), by the company’s no-

markdown policy, by the presence only in select stores and by the Group’s

efforts to avoid inflation of the famous logo.

- Very high quality: (1) selected raw materials, sourcing of which is directly

managed by the company, (2) constant and directly managed quality checks

throughout the production process (fully outsourced), and (3) production

totally made in Europe (mainly Eastern Europe) with some items even

handmade in Italy (Gamme Rouge and Gamme Bleu collections).

- Strong recognisability, thanks to its easy visibility (outerwear is always

visible by definition) and to its iconic products (evergreen account for 20% of

Moncler’s revenues). Moncler has in fact become synonymous of duvet; its

brand awareness has always been very strong not only in its domestic market

but also in Japan, and has recently increased considerably in China and in the

US.

- a strong international vocation, thanks to the link with skiing and with the

snow tourism, which, by definition, fuel an International customer base. This

has been a key success factor for the rapid international expansion of the

brand outside its domestic market. Suffice it to say that 60% of revenues in

group’s Western European flagship stores are generated by tourists (similar

to more international brands such as Prada and Salvatore Ferragamo, and

above the 30/40% incidence we estimate for less international brands, such

as Brunello Cucinelli or Tod’s). Most of tourists purchases are generated from

Non-European customers. Light duvet jackets for example are a key success

factor for the brand vis à vis customers from warmer regions such as Brazil,

Middle East, Hong Kong.

In our opinion the strength of the Moncler brand lies in the uniqueness of its

proposition and positioning. Moncler has managed to win leadership in

outerwear thanks to an across-the-board style – which we can define as

casual/chic, informal but refined at the same time – that, in its various conjugations

and lines - make it suitable for different occasions and for different consumers.

Mr. Ruffini often explains this valuable versatility very effectively: the Moncler

duvet jacket must “dialogue with a variegated public, from the grey-suited manager

to the boy on a scooter, from the skiing enthusiast to the lady attending the first

night of La Scala’s opera season”.

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 18 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

� A structured proposition, conjugated in different collections and lines

The overall brand architecture that management has developed since 2003

exactly reflects the across-the-board positioning that is its hallmark.

In effect, the Moncler proposition is organized in several lines and collections,

covering the various segments of the luxury pyramid comprehensively and in a

structured manner, while at the same time meeting different needs in terms of use.

All the collections in turn comprise two seasons: Autumn/Winter (which, overall,

accounts for about 77% of the brand’s total sales in FY12) and

Spring/Summer (23% of the total).

Some collections also feature product categories other than outerwear (about 15%

of 2012 sales, of which we estimate about two thirds is knitwear and about one

third are accessories, mostly shoes).

The proposition is also balanced in terms of gender: excluding the children’s

segment (which we estimate accounted for some 5-10% of FY2012 sales) the

respective weight of the collections for men and women is in fact similar.

MONCLER BRAND: COLLECTION STRUCTURE

Source: Company data

Main Collection: easy to wear

The Main Collection is the most important collection (we estimate it accounts for

some 85-90% of sales). It is also the one most accessible in terms of price

positioning and more versatile in terms of use and wearability. It also includes a

select offering of products other than outwear – in particular knitwear and cut &

sewn items, but also accessories (footwear and, to a lesser extent, bags).

The Main Collection in turn is organized in several lines:

- Première (for women only): the most elegant and refined, and thus also the

most expensive

- Sport Chic (for men and women): it embodies a sober, contemporary style, for

metropolitan use

- Archive (for men and women): based on the brand’s historical roots, with

models taken from the archive and revamped, mostly showing the typical

logo

- Enfant (for children).

1,500 €

1,000 €

800 €

300 €

Avg Price

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 19 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

Grenoble: a sporty/active concept

This is the collection with the greatest technical content, designed for outdoor

sport and evoking the brand’s main historical products.

In this case the proposition is a total look, with a complete outfit, which includes

trousers, t-shirts, pullovers, coordinated accessories (above all footwear) and, of

course, the strong point, outerwear.

Fashion content is nevertheless in the forefront. This collection is in fact presented

during the New York fashion week.

Grenoble is sold only in DOS and by a few select multibrand retailers.

Gamme Rouge/Gamme Bleu: Haute Couture collections

These are the highest end collections of the Moncler

brand’s proposition, made in Italy, tailored and hand-

made, almost entirely dedicated to outerwear and

designed by famous international stylists.

The first of the two, the Gamme Rouge collection for

women, was launched in 2006. Designed first by

Alessandra Facchinetti and then by Giambattista Valli, it

embodies a sophisticated, modern and refined

interpretation of the duvet jacket.

The second one, the Gamme Bleu collection for men, was launched in 2009. Still

designed by the stylist Thom Browne today, it is a proposition that combines

sartorial quality and a sporty core.

Both collections are shown during the main fashion

weeks (Gamme Rouge in Milan and Gamme Bleu in

Paris), contributing to underpin brand positioning

and image on a global scale.

Retail distribution is highly selective for these two

collections. They are sold only in few select DOS and in

the most exclusive multibrand boutiques (around 250

stores in total).

Special Projects & Capsule Collections

Capsule collections are highly innovative collections realised through

collaborations with avantgarde designers, which give freshness and energy to the

brand and might become source of inspiration for Moncler’s other lines.

The same is true for some special projects like the one launched with Rimowa for

a multi-wheel cabin trolley.

Eyewear

Consistently with its strong attention to product quality and brand positioning, the

company has decided to pursue its growth in the eyewear segment directly and

not through a license, as it is instead typical in the industry.

Moncler has in fact recently signed a Joint-Venture with the eyewear producer and

distributor Allison (51% Moncler and 49% Allison): the first sunglass collection has

been presented at the latest Mido fair in May, and also a prescription collection

has recently been launched at the Silmo fair at the beginning of October.

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 20 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

A global distribution platform leveraging on retail and wholesale

The chart below summarizes the estimated contribution of each single

combination of channel/region to Moncler’s revenues, based on FY12 numbers.

As one can see, the most important revenue sources for the group are the retail

channel in Asia and the wholesale channel in Emea.

MONCLER: MAIN CONTRIBUTORS TO TOTAL SALES

Source: Company data

The retail channel accounted for 51% of Moncler’s 2012 revenues.

Sales in this channel are generated by a network of 98 free standing DOS (as of

September 2013), of which 56 are in the Emea region (of which 17 in Italy), 6 are

in the Americas (US), and 36 are in Asia (of which 15 in Mainland China).

MONCLER: DOS STORE NETWORK (as of Sept. 2013)

Source: Company data

15%

12%

24%8%5%

27%

5%5%

�� Emea

�� America

�� Asia

��Italy

dark = retail pale = wholesale

8

11

1517

16

24

31

39

12

22

31

36

34

6 6

0

5

10

15

20

25

30

35

40

2010 2011 2012 Sept. 2013

Italy Emea Asia Americas

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 21 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

Free standing stores can show different formats:

- Flagship stores: located in top luxury streets, these stores are the most

representative of Moncler’s image and positioning. Thanks to their size (400

sqm on average) - they are also the ones carrying the widest assortment of the

brand’s collections and product range. Main flagship stores are Milan (via

Montenapoleone), Paris, New York, Tokyo, Beijing, Shanghai, Hong Kong.

- Urban boutiques: they are located in the main cities (including Milan, Paris,

Munich, Zurich, London, Los Angeles, Chicago, Osaka, Tokyo, Shanghai,

Beijing, Hong Kong) and their size is in the 90-250-sqm range (we estimate 150-

160 sqm on average). Thanks to their large size, they usually carry a wide

assortment.

- Ski resort boutiques: they are located in the best-known

and most exclusive ski resorts (St Moritz, Cortina,

Courmayeur, Crans-sur-Sierre, Megève, Courchevel,

Aspen, Gstaad, Verbier, Kitzbuhel, and Zermatt) and have

a smaller average size than urban boutiques (in the 35-100

sqm range, with the exception of the flagship in St. Moritz,

recently reopened with a 200 sqm surface – see picture on

the left). These stores have a specific assortment, different

to that of urban boutiques not only for reasons of space, but

also in order to give more emphasis to more technical

products, thus expressing the link with Moncler’s heritage

and DNA.

- Concessions: these are corners located in the main department stores and run

directly by the company. They have an assortment similar to that of urban

boutiques but narrower because of the smaller spaces (between 20 sqm and 65

sqm). The company was running 26 concessions as of September 2013.

- Outlets: they take the unsold stock of the retail network or any production

surplus to the wholesale backlog. The company does not produce on purpose

for the outlet channel. These stores are always located in the main outlet malls

worldwide. The company was running 12 outlets as of September 2013, of

which 3 in Italy. Outlets’ sales account for about 8% of total group’s revenues

On the other side the wholesale channel, accounting for 49% of the Moncler

brand’s sales in 2012, is organized in:

- Multibrand stores: about 1,850 independent boutiques worldwide as of

September 2013 (of which about 50% in Emea and about 30% in Italy),

meticulously selected to assure consistency with brand positioning. As a

reference, the Moncler’s wholesale presence in Italy is below that of the Tod’s

group in terms of number of accounts (about 500, vs. close to 600 for Tod’s).

This network is almost exclusively dedicated to the Main Collection since, as we

have seen, Grenoble and Gamme Rouge/Gamme Bleu have even more

exclusive distribution.

- Shop in Shop: 23 as of September 2013. These are corners in selected top tier

department stores (including Bergdorf Goodman, Bloomingdale’s, Neiman

Marcus, Harrods, Tsum, Harvey Nichols and Shinsegae). Size of these spaces

ranges between 20 and 65 sqm. On top of the 23 corners, the group also has

one franchised store in Seoul (Korea).

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 22 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

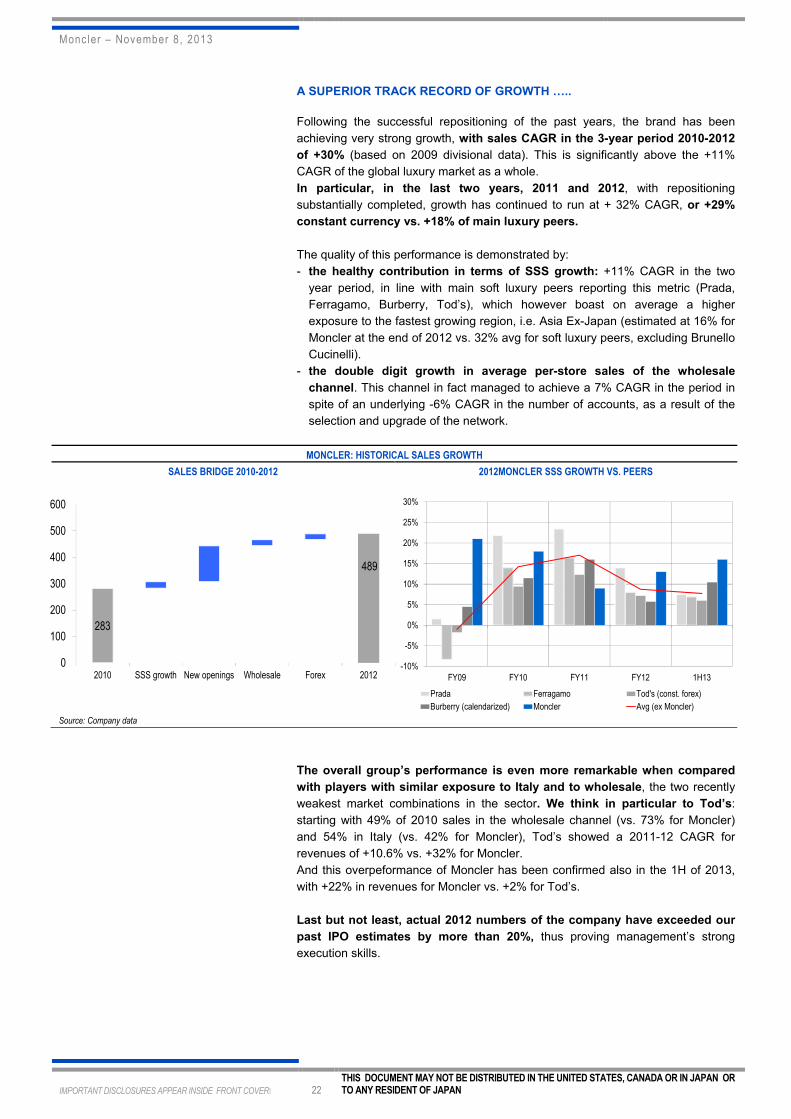

A SUPERIOR TRACK RECORD OF GROWTH …..

Following the successful repositioning of the past years, the brand has been

achieving very strong growth, with sales CAGR in the 3-year period 2010-2012

of +30% (based on 2009 divisional data). This is significantly above the +11%

CAGR of the global luxury market as a whole.

In particular, in the last two years, 2011 and 2012, with repositioning

substantially completed, growth has continued to run at + 32% CAGR, or +29%

constant currency vs. +18% of main luxury peers.

The quality of this performance is demonstrated by:

- the healthy contribution in terms of SSS growth: +11% CAGR in the two

year period, in line with main soft luxury peers reporting this metric (Prada,

Ferragamo, Burberry, Tod’s), which however boast on average a higher

exposure to the fastest growing region, i.e. Asia Ex-Japan (estimated at 16% for

Moncler at the end of 2012 vs. 32% avg for soft luxury peers, excluding Brunello

Cucinelli).

- the double digit growth in average per-store sales of the wholesale

channel. This channel in fact managed to achieve a 7% CAGR in the period in

spite of an underlying -6% CAGR in the number of accounts, as a result of the

selection and upgrade of the network.

MONCLER: HISTORICAL SALES GROWTH

SALES BRIDGE 2010-2012 2012MONCLER SSS GROWTH VS. PEERS

Source: Company data

The overall group’s performance is even more remarkable when compared

with players with similar exposure to Italy and to wholesale, the two recently

weakest market combinations in the sector. We think in particular to Tod’s:

starting with 49% of 2010 sales in the wholesale channel (vs. 73% for Moncler)

and 54% in Italy (vs. 42% for Moncler), Tod’s showed a 2011-12 CAGR for

revenues of +10.6% vs. +32% for Moncler.

And this overpeformance of Moncler has been confirmed also in the 1H of 2013,

with +22% in revenues for Moncler vs. +2% for Tod’s.

Last but not least, actual 2012 numbers of the company have exceeded our

past IPO estimates by more than 20%, thus proving management’s strong

execution skills.

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

FY09 FY10 FY11 FY12 1H13

Prada Ferragamo Tod's (const. forex)

Burberry (calendarized) Moncler Avg (ex Moncler)

283

489

0

100

200

300

400

500

600

2010 SSS growth New openings Wholesale Forex 2012

Moncler – November 8, 2013

IMPORTANT DISCLOSURES APPEAR INSIDE FRONT COVER� 23 THIS DOCUMENT MAY NOT BE DISTRIBUTED IN THE UNITED STATES, CANADA OR IN JAPAN OR TO ANY RESIDENT OF JAPAN

As for Moncler, the comparison with past estimates must refer to the old group’s

set-up, which used to include also the recently disposed casual wear division

(three proprietary brands - Henry Cotton’s, Marina Yachting, Coast+Weber+House

- and the licensed brand 18CRR81 Cerruti). This was in fact the structure of the

Moncler group at the time of the past IPO attempt.

Actual numbers are reported in the Moncler Group’s 2012 consolidated annual

report, and we have compared them with past estimates in the table below.

MONCLER GROUP: STRONG BEAT OF PAST IPO ESTIMATES (€ mn)

2010 2011E 2012E 2011A 2012A BEAT OF 2012

Sales 429 488 550 513 624 13%

Increase 15% 14% 13% 20% 22%

Adj. Ebitda 102 117 134 123 170 27%

Increase 33% 15% 15% 20% 39%

Adj. Net profit 52 60 70 58 76 9%