Module 21 Operational Budgeting and Profit Planning.

23

Module 21 Operational Budgeting and Profit Planning

-

Upload

austen-holland -

Category

Documents

-

view

226 -

download

2

Transcript of Module 21 Operational Budgeting and Profit Planning.

Module 21

Operational Budgeting and Profit Planning

Budget

Financial plan for an organization Operating plans: sales, purchasing,

production, selling, general, and administrative expenses

Cash inflows/outflows Ends with complete financial reports:

income statement & balance sheet, cash flow statement, stockholders equity.

Typical Process for a Merchandiser

Selling Expense Budget

Pro Forma StatementsIncome Statement & Balance Sheet

Sales Budget

Purchases Budget

Special Budgets

General and Administrative

Expense Budget

Cash Budget

Sales Budget Sales plan is the starting point for

the budgeting process Includes a forecast of sales revenue Normally includes a forecast of unit

sales The best available information is

used to forecast sales: Market conditions in sales territories by

period Merchandise lines available Promotion and advertising plans Expected pricing policies (markups)

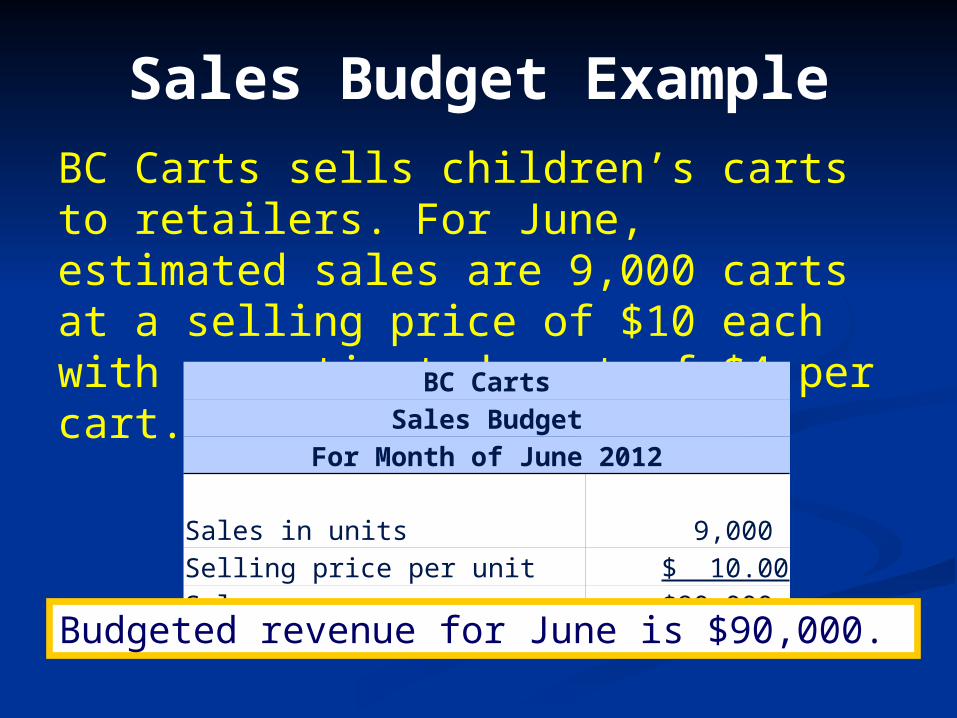

Sales Budget ExampleBC Carts sells children’s carts to retailers. For June, estimated sales are 9,000 carts at a selling price of $10 each with an estimated cost of $4 per cart. BC Carts

Sales BudgetFor Month of June 2012

Sales in units 9,000 Selling price per unit $ 10.00Sales revenue $90,000

Budgeted revenue for June is $90,000.

Purchases Budget

Indicates the merchandise to be purchased to meet sales needs and ending inventory requirements

Considers Budgeted sales Desired ending inventory Planned beginning inventory

Purchases Budget Example

BC Carts desires to have 20% of the carts needed for the next month’s sales in stock at the end of each month. At the beginning of June, 1,800 carts are on hand. Each cart costs $4. Sales are planned to increase 10% per month. BC Carts

Purchases BudgetFor Month of June 2012

Units Dollars

Sales needs 9,000. $36,000.Desired ending inventory 1,980. 7,920.Total 10,980. 43,920. Less beginning inventory (1,800) (7,200)Purchases 9,180. $36,720.

Number of units times the cost per

unit of $4

Sales for July: 9,000 + (9,000 × 0.10) = 9,900 cartsEnding inventory = 9,900 × 0.20 = 1,980 carts

Selling Expense

Presents the expenses the organization plans to incur in connection with sales and distribution

Costs are broken into variable and fixed costs

Variable selling costs Developed as a percent of sales or an

amount per unit sold Fixed selling costs

Often based on an estimate obtained from the sales manager

Selling Expense Budget Example

BC CartsSelling Expense BudgetFor Month of June 2012

Budgeted sales $90,000Variable selling expenses Commissions (4%) $3,600 Miscellaneous (1.5%) 1,350 Total variable expenses 4,950Fixed selling expenses Depreciation 3,500 Advertising 2,000 Miscellaneous 1,200 Total fixed expenses 6,700 Total selling expenses $11,650

BC Carts estimates commissions at 4%

of sales and miscellaneous

variable costs at 1.5%. Estimated

fixed selling costs are $3,500 for

depreciation, $2,000 for advertising, and

$1,200 for miscellaneous costs.

BC Carts estimates commissions at 4%

of sales and miscellaneous

variable costs at 1.5%. Estimated

fixed selling costs are $3,500 for

depreciation, $2,000 for advertising, and

$1,200 for miscellaneous costs.

Commissions: $90,000 × 0.04 = $3,600 Miscellaneous: $90,000 × 0.015 = $1,350

General and Administrative Expense Budget

Presents the expenses planned in connection with the general administration of the organization

Example expenses: Compensation Insurance Depreciation Utilities Miscellaneous

General and Administrative Expense

Budget ExampleBC Carts estimates the following monthly general and administrative costs: $5,000 for salaries, $800 for insurance, $1,100 for depreciation, $600 for utilities, and $900 for miscellaneous.

BC CartsGeneral and Administrative Expense Budget

For Month of June 2012Salaries $5,000Insurance 800Depreciation 1,100Utilities 600Miscellaneous 900Total general and administrative expenses $8,400

Cash Budget Summarizes all cash receipts and

disbursements expected to occur during the budget period

Because of issues related to the timing of sales and collections on account Collections on sales do not equal sales

revenue Because of issues related to the

timing of payments for purchases and other expense items Disbursements do not equal expenses

Cash Receipts Budget Example

BC Carts budgeted its June sales at $90,000. It estimates that 40% of sales are cash and 60% are on credit. 30% of credit sales are collected in the month of sale and 70% are collected in the following month. Beginning cash balance is $15,000 and sales during May were $86,000.

30% Collected current month30% Collected current month

70% Collected following month70% Collected following month

$86,000 × 0.60 × 0.70 = $36,120

Collections on sales

Cash sales $36,000

Credit sales

Current month (30% of credit sales) 16,200

Prior month (70% of credit sales) 36,120

Total $88,320

40% Cash Sales40% Cash Sales

CASH RECEIPTS BUDGET FOR JUNE, 2012CASH RECEIPTS BUDGET FOR JUNE, 2012

$90,000 × 0.60 × 0.30 = $16,200

$90,000 × 0.40$90,000 × 0.40

SalesSales60% Credit Sales60% Credit Sales

Cash Disbursements Budget Example

BC Carts estimates that 25% of its current month inventory purchases will be paid during the month incurred and 75% are paid in the following month. During May, purchases were $32,000. Budgeted purchases for June are $36,720 (from the purchases budget.)

Continued

CASH DISBURSEMENTS BUDGET FOR JUNE, 2012CASH DISBURSEMENTS BUDGET FOR JUNE, 2012

Disbursements

Purchases

Current month (25% of purchases) $ 9,180

Prior month (75% of purchases) 24,000

Total $33,180

Inventory purchases section of the cash disbursements section of the cash budget:

Inventory purchases section of the cash disbursements section of the cash budget:

$36,720 × 0.25 = $9,180$36,720 × 0.25 = $9,180

$32,000 × 0.75 = $24,000$32,000 × 0.75 = $24,000

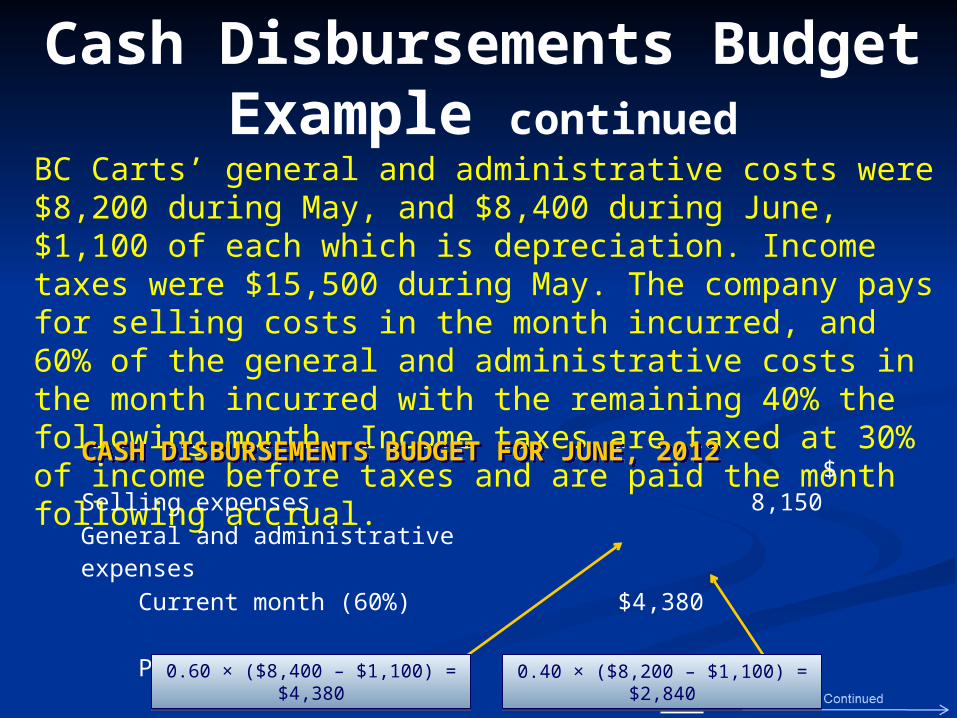

Cash Disbursements Budget Example continued

BC Carts’ general and administrative costs were $8,200 during May, and $8,400 during June, $1,100 of each which is depreciation. Income taxes were $15,500 during May. The company pays for selling costs in the month incurred, and 60% of the general and administrative costs in the month incurred with the remaining 40% the following month. Income taxes are taxed at 30% of income before taxes and are paid the month following accrual. Selling expenses $ 8,150

General and administrative expenses Current month (60%) $4,380 Prior month (40%) 2,840 Income taxes 15,500 General and administrative expenses 22,720

CASH DISBURSEMENTS BUDGET FOR JUNE, 2012CASH DISBURSEMENTS BUDGET FOR JUNE, 2012

0.40 × ($8,200 – $1,100) = $2,8400.40 × ($8,200 – $1,100) = $2,8400.60 × ($8,400 – $1,100) = $4,3800.60 × ($8,400 – $1,100) = $4,380

Financing Section of Cash Budget

BC Carts’ repays $5,000 of the principal on its bank loan on June 30 and December 31, and any accrued interest.

Short-term financing Loan repayments $5,000 Interest 750

Net cash used for financing $5,750

CASH DISBURSEMENTS BUDGET FOR JUNE, 2012CASH DISBURSEMENTS BUDGET FOR JUNE, 2012

$25,000 × 0.06 × 1/2 $25,000 × 0.06 × 1/2

Budgeted Financial Statements

Pro forma income statement and balance sheet that reflect the “as-if” effects of the budgeted activities on the actual financial position of organization

Reflect the results if all budgetary projections are correct

If income not good enough for top management, then start process again

Production Budget

Additional steps are required to develop master budgets for manufacturing organizations Due to conversion of raw materials into

finished goods Must determine production volume

To support sales To meet finished goods inventory

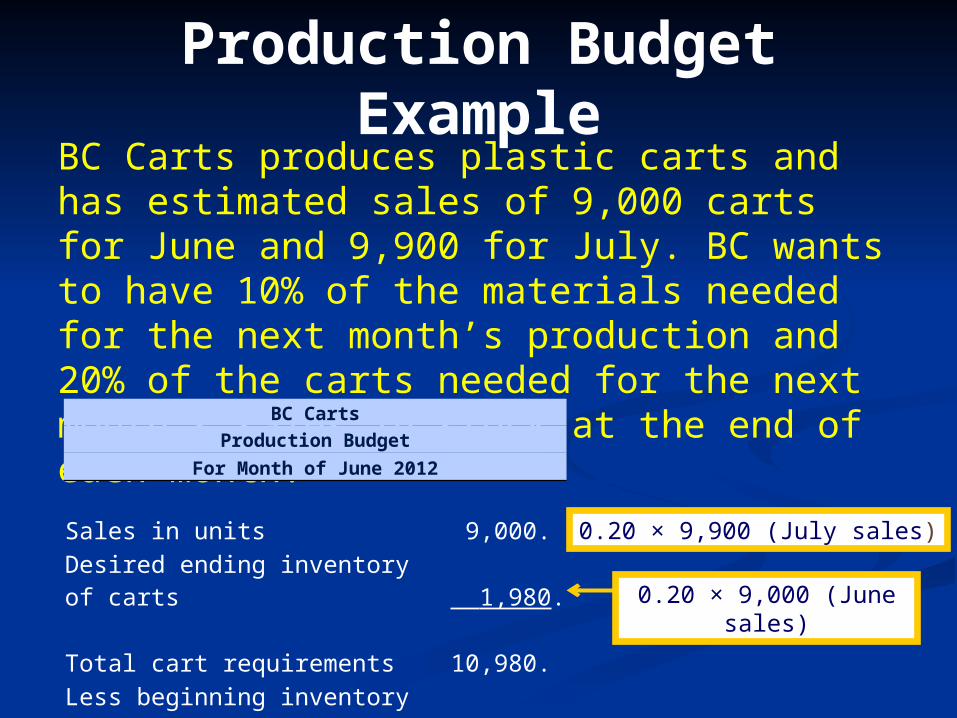

Production Budget Example

BC Carts produces plastic carts and has estimated sales of 9,000 carts for June and 9,900 for July. BC wants to have 10% of the materials needed for the next month’s production and 20% of the carts needed for the next month’s sales in stock at the end of each month. BC Carts

Production Budget

For Month of June 2012

Sales in units 9,000. Desired ending inventory of carts 1,980. Total cart requirements 10,980. Less beginning inventory of carts (1,800)Budgeted production 9,180.

0.20 × 9,000 (June sales)

0.20 × 9,900 (July sales)

Purchases Budget Example

Assume BC Carts plans to produce 10,098 carts in July. It wants to have 10% of the materials needed for the next month’s production in stock at the end of each month. Each cart requires 6 pounds of plastic resin and two wheels. At June 1, BC had 5,508 pounds of resin and 1,836 wheels on hand. Wheels cost $0.30 each and resin costs $0.21 per pound. BC Carts

Purchases Budget

For Month of June 2012

Resin: Pounds of resin needs (6 lbs. x 9,180 carts) 55,080. Desired ending resin inventory 6,059. Total resin requirements in pounds 61,139. Less beginning resin inventory (5,508)Resin purchases in pounds 55,631.

Continued

6 × 10,098 × 0.10

given

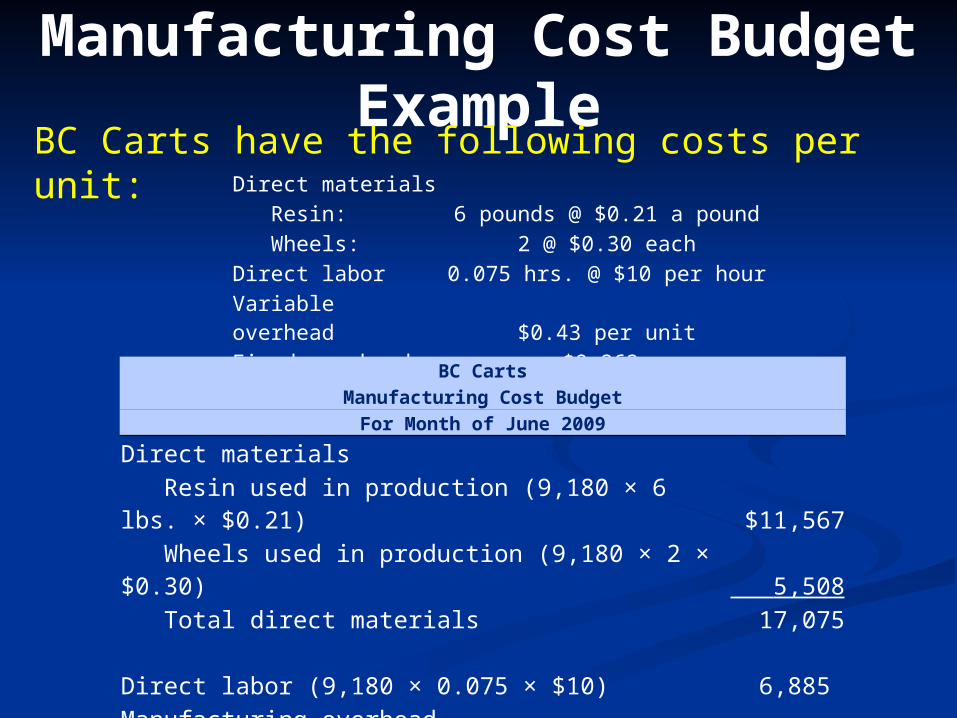

Manufacturing Cost Budget Example

BC Carts have the following costs per unit: Direct materials Resin: 6 pounds @ $0.21 a pound Wheels: 2 @ $0.30 eachDirect labor 0.075 hrs. @ $10 per hourVariable overhead $0.43 per unitFixed overhead $8,262

BC CartsManufacturing Cost Budget

For Month of June 2009

Direct materials Resin used in production (9,180 × 6 lbs. × $0.21) $11,567 Wheels used in production (9,180 × 2 × $0.30) 5,508 Total direct materials 17,075Direct labor (9,180 × 0.075 × $10) 6,885 Manufacturing overhead Variable ($0.43 per unit) 3,947 Fixed 8,262 Total manufacturing costs $36,169

Approaches to Budgeting

Input-output: Planned sales volumes and required inputs

Incremental: Add an increment to past year Example: Increase budgets by 3%.

Zero-based: Every $ justified starting at 0 for everything.

Activity-based: Project sales volume to activity and budget the $ based on activity cost

Rolling (continuous) example: each month, redo each of the next 12 monthly budgets

Participation Extent to which lower level personnel

involved with the budget process: participative or bottom up approach Alternative is top-down or imposed budgets Both approaches require top management

involvement

Since budgets used in performance measures, participation often results in budgetary slack: padding built in to expense or revenue estimates. Slack can provide needed flexibility when

situation has high uncertainty.