modern auditing

76

U NDERSTANDING I NTERNAL C ONTROL U NDERSTANDING I NTERNAL C ONTROL THE IMPORTANCE OF INTERNAL CONTROL The importance of internal control to management and independent auditors has been rec- ognized in the professional literature for many years. A 1947 publication by the AICPA enti- tled Internal Control cited the following factors as contributing to the expanding recognition of the significance of internal control: ■ The scope and size of the business entity have become so complex and widespread that management must rely on numerous reports and analyses to effectively control operations. ■ The check and review inherent in a good system of internal control affords protection against human weaknesses and reduces the possibility that errors or irregularities will occur. ■ It is impracticable for auditors to make audits of most companies within economic fee limitations without relying on the client’s system of internal control. During the five decades following this publication, management, independent auditors, and, external parties, such as investors and regulators, have placed even greater impor- tance on internal control. In 1977, Congress passed the Foreign Corrupt Practices Act (FCPA). Under this Act, man- agement and directors of companies subject to reporting requirements of the Securities Exchange Act of 1934 are required to comply with antibribery and accounting standards provi- sions and maintain a satisfactory system of internal control. The FCPA is administered by the Securities and Exchange Commission (SEC), and management and directors who do not com- ply with its provisions are subject to fines, penalties, and/or imprisonment. Ten years later, the National Commission on Fraudulent Financial Reporting (Treadway Commission) reemphasized the importance of internal control in reducing the incidence of fraudulent financial reporting. The commission’s final report, issued in October 1987, included the following: ■ Of overriding importance in preventing fraudulent financial reporting is the “tone set by top management” that influences the corporate environment within which financial reporting occurs. ■ All public companies should maintain internal control that will provide reasonable assur- ance that fraudulent financial reporting will be prevented or subject to early detection. ■ The organizations sponsoring the Commission, including the Auditing Standards Board (ASB), should cooperate in developing additional guidance on internal control systems. In 1988, the ASB issued SAS 55, Consideration of the Internal Control Structure in a Financial Statement Audit (AU 319). The SAS significantly expanded both the meaning of internal control and the auditor’s responsibilities in meeting the second standard of field- work. In 1990, the AICPA issued a 263-page audit guide with the same title as the SAS to assist auditors in applying SAS 55. Finally, following up on the last recommendation of the Treadway Commission referred to previously, in 1992 the Committee of Sponsoring Organizations (COSO) of the Tread- 10 [] [

-

Upload

jklein2588 -

Category

Documents

-

view

233 -

download

2

description

chapter 10

Transcript of modern auditing

UNDERSTANDINGINTERNAL CONTROLUNDERSTANDINGINTERNAL CONTROL

THE IMPORTANCE OF INTERNAL CONTROL

The importance of internal control to management and independent auditors has been rec-ognized in the professional literature for many years. A 1947 publication by the AICPA enti-tled Internal Control cited the following factors as contributing to the expanding recognitionof the significance of internal control:

■ The scope and size of the business entity have become so complex and widespreadthat management must rely on numerous reports and analyses to effectively controloperations.

■ The check and review inherent in a good system of internal control affords protectionagainst human weaknesses and reduces the possibility that errors or irregularities willoccur.

■ It is impracticable for auditors to make audits of most companies within economic feelimitations without relying on the client’s system of internal control.

During the five decades following this publication, management, independent auditors,and, external parties, such as investors and regulators, have placed even greater impor-tance on internal control.

In 1977, Congress passed the Foreign Corrupt Practices Act (FCPA). Under this Act, man-agement and directors of companies subject to reporting requirements of the SecuritiesExchange Act of 1934 are required to comply with antibribery and accounting standards provi-sions and maintain a satisfactory system of internal control. The FCPA is administered by theSecurities and Exchange Commission (SEC), and management and directors who do not com-ply with its provisions are subject to fines, penalties, and/or imprisonment.

Ten years later, the National Commission on Fraudulent Financial Reporting (TreadwayCommission) reemphasized the importance of internal control in reducing the incidence offraudulent financial reporting. The commission’s final report, issued in October 1987,included the following:

■ Of overriding importance in preventing fraudulent financial reporting is the “tone set bytop management” that influences the corporate environment within which financialreporting occurs.

■ All public companies should maintain internal control that will provide reasonable assur-ance that fraudulent financial reporting will be prevented or subject to early detection.

■ The organizations sponsoring the Commission, including the Auditing Standards Board(ASB), should cooperate in developing additional guidance on internal control systems.

In 1988, the ASB issued SAS 55, Consideration of the Internal Control Structure in aFinancial Statement Audit (AU 319). The SAS significantly expanded both the meaning ofinternal control and the auditor’s responsibilities in meeting the second standard of field-work. In 1990, the AICPA issued a 263-page audit guide with the same title as the SAS toassist auditors in applying SAS 55.

Finally, following up on the last recommendation of the Treadway Commission referredto previously, in 1992 the Committee of Sponsoring Organizations (COSO) of the Tread-

10[ ]

[

Chapter 10 focuses on the elements of a strong system of internal control. This chapteraddresses the following aspects of the auditor’s knowledge and the auditor’s decision process.

way Commission issued a report entitled Internal Control—Integrated Framework. Accord-ing to COSO, the two principal purposes of its efforts were to:

■ Establish a common definition of internal control serving the needs of different parties.■ Provide a standard against which business and other entities can assess their con-

trol systems and determine how to improve them.

Then the ASB issued Statements and Standards for Attestation Engagements No. 2,which allowed auditors to conduct an audit and report on a client’s system of internal con-trol over financial reporting. Then in 1995 the ASB amended AU 319 with SAS 78, Consid-eration of Internal Control in a Financial Statement Audit, to conform professional stan-dards to the framework and language used in the COSO Report.

Financial statement users have questioned whether it is more important to have assur-ance on the financial statements themselves or assurance over the system that producesan entity’s financial statements. About a decade after the ASB created the first standardsfor attest engagement on internal controls, the U.S. Congress passed the Sarbanes–OxleyAct of 2002. Section 404 of this Act and PCAOB Standard No. 2 require managements ofpublic companies to assess the adequacy of internal controls over financial reporting, andtheir auditors must audit both management’s assessment of internal controls over finan-cial reporting and the actual effectiveness of the system of internal controls over financialreporting (in addition to auditing the financial statements themselves).

[PREVIEW OF CHAPTER 10]Chapter 10 continues the discussion of important audit planning and risk assessment pro-cedures and addresses one major issue: understanding the entity’s system of internal con-trol. The following diagram provides an overview of the chapter organization and content.

[390] PART 2 / AUDIT PLANNING

Introduction toInternal Control

Components ofInternal Control

UnderstandingInternal Control

Understanding Internal Control

Appendices

Definition and ComponentsEntity Objectives and Related Internal Control Relevant to an AuditLimitations of an Entity’s System of Internal ControlRoles and Responsibilities

Control EnvironmentRisk AssessmentInformation and CommunicationControl ActivitiesMonitoringAntifraud Programs and ControlsApplication to Small and Midsized EntitiesSummary

What to Understand about Internal ControlEffects of Preliminary Audit StrategiesProcedures to Obtain an UnderstandingDocumenting the Understanding

Information Technology and Internal ControlComputer General ControlsComprehensive Flowcharting Illustration

Hadel Studio ● (516) 333 ● 2580

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [391]

After studying this chapter you should understand the following aspects of an auditor’s knowledge base:K1. Know the definitions of internal control and the five interrelated components of internal control.K2. Know the inherent limitations of internal control and explain the roles and responsibilities of various

parties for an entity’s internal controls.K3. Know the purpose of understanding internal control needed to plan an audit and how that understand-

ing is used.

focus on auditor knowledge

After studying this chapter you should understand the factors that influence the following audit decisions.D1. What are the key components of a strong control environment, including relevant IT aspects?D2. What are the key components of strong risk assessment activities, including relevant IT aspects?D3. What are the key components of an effective information and communication system, including relevant

IT aspects?D4. What are the key components of strong control activities, including relevant IT aspects?D5. What are the key components of strong monitoring activities, including relevant IT aspects?D6. What are the key components of a strong antifraud program and controls?D7. What audit procedures are used to obtain an understanding of internal controls?D8. What are the requirements and alternative methods for documenting the understanding of internal

control?

focus on audit decisions

[INTRODUCTION TO INTERNAL CONTROL]In this section, we examine the contemporary definition of internal control andfive interrelated components of internal control. In addition, we consider whichentity objectives addressed by internal control are relevant to a financial statementaudit, briefly describe the components of internal control, acknowledge certaininherent limitations of internal control, and specify the roles and responsibilitiesof various parties for an entity’s internal control.

DEFINITION AND COMPONENTS

The COSO report defines internal control as follows:

Internal control is a process, effected by an entity’s board of directors, management, and otherpersonnel, designed to provide reasonable assurance regarding the achievement of objectivesin the following categories:■ Reliability of financial reporting■ Compliance with applicable laws and regulations■ Effectiveness and efficiency of operations

Source: Committee of Sponsoring Organizations of the Treadway Commission, Internal Control—Inte-grated Framework (Jersey City, NJ; American Institute of Certified Public Accountants, 1992).

The COSO report also emphasized that the following fundamental concepts areembodied in the foregoing definition:

■ Internal control is a process that is integrated with, not added onto, an entity’sinfrastructure. It is a means to an end, not an end in itself.

■ People implement internal control. It is not merely a policy manual and forms,but people at every level of an organization.

■ Internal control can be expected to provide only reasonable assurance, notabsolute assurance, because of its inherent limitations.

■ Internal control is geared to the achievement of objectives in the overlappingcategories of financial reporting, compliance, and operations.

Implicit in the last bullet is the assumption that management and the board do infact formulate and periodically update entity objectives in each of the three cate-gories.

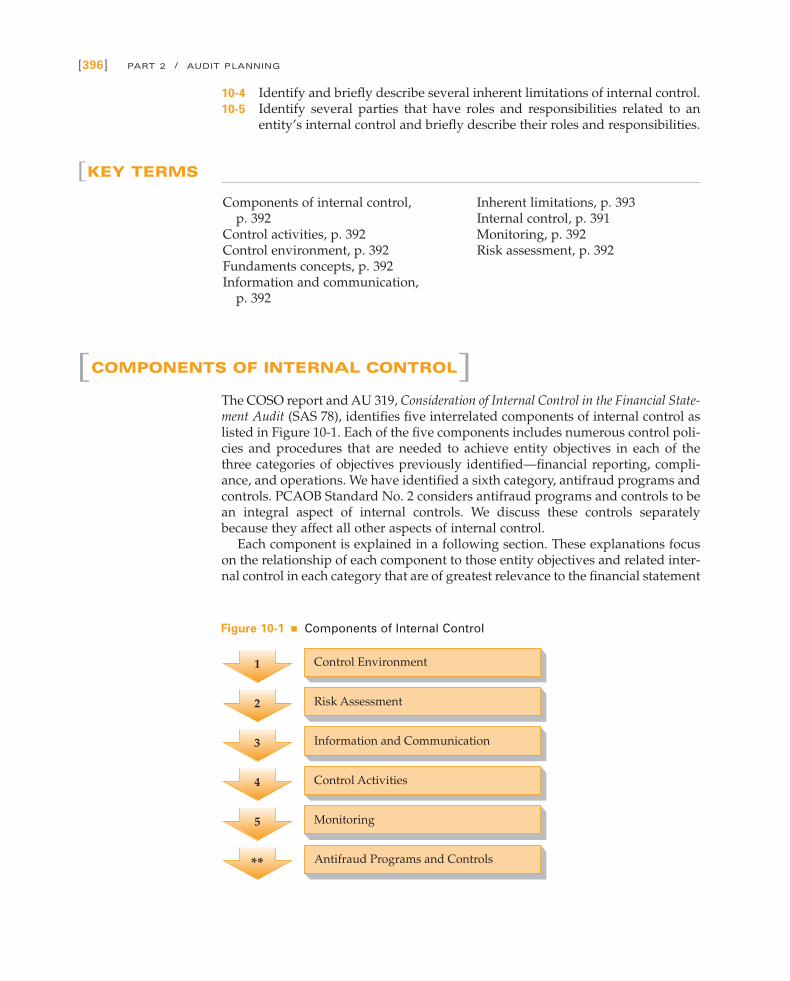

To provide a structure for considering the many possible controls related to theachievement of an entity’s objectives, the COSO report (and AU 319.07) identifiesfive interrelated components of internal control:

■ Control environment sets the tone of an organization, influencing the controlconsciousness of its people. It is the foundation for all other components ofinternal control, providing discipline and structure.

■ Risk assessment is the entity’s identification and analysis of relevant risks toachievement of its objectives, forming a basis for determining how the risksshould be managed.

■ Control activities are the policies and procedures that help ensure that man-agement directives are carried out.

■ Information and communication are the identification, capture, and exchangeof information in a form and time frame that enable people to carry out theirresponsibilities.

■ Monitoring is a process that assesses the quality of internal control perform-ance over time.

These five components are described in detail in later sections of this chapter.

ENTITY OBJECTIVES AND RELATED INTERNALCONTROL RELEVANT TO AN AUDIT

As previously noted, management adopts internal control to provide reasonableassurance of achieving three categories of objectives: (1) reliability of financialinformation, (2) compliance with applicable laws and regulations, and (3) effec-tiveness and efficiency of operations. Because not all of those objectives andrelated controls are relevant to an audit of financial statements, one of the audi-tor’s first tasks in meeting the second standard of fieldwork is to identify thoseobjectives and controls that are relevant. Generally, this includes those that pertaindirectly to the first category—reliability of financial reporting. In addition, Section404 of the Sarbanes–Oxley Act of 2002 only focuses on internal control over finan-cial reporting.

Other objectives and related controls may also be relevant if they pertain todata the auditor uses in applying audit procedures. Examples include objectivesand related controls that pertain to:

[392] PART 2 / AUDIT PLANNING

■ Know the defini-tions of internal con-trol and the five inter-related componentsof internal control.

Auditor Knowledge 1

■ Nonfinancial data used in analytical procedures, such as the number of employ-ees, the entity’s manufacturing capacity and volume of goods manufactured,and other production and marketing statistics.

■ Certain financial data developed primarily for internal purposes, such as budg-ets and performance data, used by the auditor to obtain evidence about theamounts reported in the financial statements.

Chapter 2 of this text explained the auditor’s responsibilities for detectingerrors and irregularities, including management and employee fraud, and fordetecting certain illegal acts. Thus, an entity’s objectives and controls related tothese matters are also relevant to the auditor. In particular, objectives and controlsin the category of compliance with applicable laws and regulations are relevantwhen they could have a direct and material effect on the financial statements.

LIMITATIONS OF AN ENTITY’S SYSTEM OFINTERNAL CONTROL

One of the fundamental concepts identified earlier in the chapter is that internalcontrol can provide only reasonable assurance to management and the board ofdirectors regarding the achievement of an entity’s objectives. AU 319.16-18, Con-sideration of Internal Control in a Financial Statement Audit, identifies the followinginherent limitations that explain why internal control, no matter how welldesigned and operated, can provide only reasonable assurance regarding achieve-ment of an entity’s control objectives.

■ Mistakes in judgment. Occasionally, management and other personnel may exer-cise poor judgment in making business decisions or in performing routineduties because of inadequate information, time constraints, or other proce-dures.

■ Breakdowns. Breakdowns in established control may occur when personnel mis-understand instructions or make errors owing to carelessness, distractions, orfatigue. Temporary or permanent changes in personnel or in systems or proce-dures may also contribute to breakdowns.

■ Collusion. Individuals acting together, such as an employee who performs animportant control acting with another employee, customer, or supplier, may beable to perpetrate and conceal fraud so as to prevent its detection by internalcontrol (e.g., collusion among three employees from personnel, manufacturing,and payroll departments to initiate payments to fictitious employees, or kick-back schemes between an employee in the purchasing department and a sup-plier or between an employee in the sales department and a customer).

■ Management override. Management can overrule prescribed policies or proce-dures for illegitimate purposes such as personal gain or enhanced presentationof an entity’s financial condition or compliance status (e.g., inflating reportedearnings to increase a bonus payout or the market value of the entity’s stock, orto hide violations of debt covenant agreements or noncompliance with lawsand regulations). Override practices include making deliberate misrepresenta-tions to auditors and others such as by issuing false documents to support therecording of fictitious sales transactions.

■ Cost versus benefits. The cost of an entity’s internal control should not exceedthe benefits that are expected to ensue. Because precise measurement of both

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [393]

■ Know the inherentlimitations of internalcontrol and explainthe roles and respon-sibilities of variousparties for an entity’sinternal controls.

Auditor Knowledge 2

costs and benefits usually is not possible, management must make both quan-titative and qualitative estimates and judgments in evaluating the cost-bene-fit relationship.1

For example, an entity could eliminate losses from bad checks by accepting onlycertified or cashier’s checks from customers. However, because of the possibleadverse effects of such a policy on sales, most companies believe that requiringidentification from the check writer offers reasonable assurance against this typeof loss.

ROLES AND RESPONSIBILITIES

The COSO report concludes that everyone in an organization has some responsi-bility for, and is actually a part of, the organization’s internal control. In addition,several external parties, such as independent auditors and regulators, may con-tribute information useful to an organization in effecting control, but they are notresponsible for the effectiveness of internal control. Several responsible partiesand their roles are as follows:

■ Management. It is management’s responsibility to establish effective internalcontrol. In particular, senior management should set the “tone at the top” forcontrol consciousness throughout the organization and see that all the compo-nents of internal control are in place. Senior management in charge of organi-zational units (divisions, etc.) should be accountable for the resource in theirunits. The CEO and CFO of public companies must also make an assessment ofthe adequacy of internal controls over financial reporting.

■ Board of directors and audit committee. Board members, as part of their generalgovernance and oversight responsibilities, should determine that managementmeets its responsibilities for establishing and maintaining internal control. Theaudit committee (or in its absence, the board itself) has an important oversightrole in the financial reporting process.

■ Internal auditors. Internal auditors should periodically examine and evaluate theadequacy of an entity’s internal control and make recommendations forimprovements. They are part of the monitoring component of internal control,and active monitoring by internal auditors may improve the overall controlenvironment.

■ Other entity personnel. The roles and responsibilities of all other personnel whoprovide information to, or use information provided by, systems that includeinternal control should understand that they have a responsibility to communi-cate any problems with noncompliance with controls or illegal acts of whichthey become aware to a higher level in the organization.

■ Independent auditors. When performing risk assessment procedures, an inde-pendent auditor may discover deficiencies in internal control that he or shecommunicates to management and the audit committee, together with recom-mendations for improvements. This applies primarily to financial reportingcontrols, and to a lesser extent to compliance and operations controls. If the

[394] PART 2 / AUDIT PLANNING

1 The PCAOB has taken the position that cost-benefit is not a valid reason not to have adequate inter-nal controls over financial reporting relating to assertions that could have a material effect on the finan-cial statements.

auditor of a private company follows a primarily substantive approach, he orshe may learn enough to understand the specific risks of misstatement, but maynot evaluate the effectiveness of many control procedures. A private companyaudit in accordance with GAAS is performed primarily to enable the auditor toproperly plan the audit. Neither does it result in the expression of an opinionon the effectiveness of internal control, nor can it be relied upon to identify allor necessarily even most significant weaknesses in internal control.

■ Other external parties. Legislators and regulators set minimum statutory and reg-ulatory requirements for establishing internal controls by certain entities. TheSarbanes–Oxley Act of 2002 is an example. Another example is the FederalDeposit Insurance Corporation Improvement Act of 1991, which requires thatcertain banks report on the effectiveness of their internal control over financialreporting and that such reports be accompanied by an independent accoun-tant’s attestation report on management’s assertions about effectiveness.

[LEARNING CHECK

(The following questions draw from the opening vignette as well as from thechapter material.)

10-1 a. Who administers the Foreign Corrupt Practices Act of 1977, and towhom does it pertain?

b. What provisions of the Act relate to internal control and how?10-2 a. What recommendations did the National Commission on Fraudulent

Financial Reporting make regarding internal control?b. What is COSO? What were the two principal purposes of its efforts

regarding internal control, and why did it undertake these efforts?10-3 a. State the COSO definition of internal control.

b. Identify five interrelated components of internal control.c. Which entity objectives and related internal controls are of primary rele-

vance in a financial statement audit?

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [395]

Managements of public companies are responsible for both fair presentation in the financialstatement and maintenance of an effective system of internal control over financial reporting.The PCAOB Auditing Standard No. 2 establishes the following responsibility for managementwith respect to the company’s internal control. Management must:

■ Accept responsibility for the effectiveness of the company’s internal control over financialreporting.

■ Evaluate the effectiveness of the company’s internal control over financial reporting usingsuitable criteria (generally COSO).

■ Support its evaluation with sufficient evidence, including documentation.■ Present a written assessment of the effectiveness of the company’s internal control over finan-

cial reporting as of the end of the company’s most recent fiscal year.

management’s responsibilities in an audit of

internal control over financial reporting

10-4 Identify and briefly describe several inherent limitations of internal control.10-5 Identify several parties that have roles and responsibilities related to an

entity’s internal control and briefly describe their roles and responsibilities.

[KEY TERMS

[COMPONENTS OF INTERNAL CONTROL]The COSO report and AU 319, Consideration of Internal Control in the Financial State-ment Audit (SAS 78), identifies five interrelated components of internal control aslisted in Figure 10-1. Each of the five components includes numerous control poli-cies and procedures that are needed to achieve entity objectives in each of thethree categories of objectives previously identified—financial reporting, compli-ance, and operations. We have identified a sixth category, antifraud programs andcontrols. PCAOB Standard No. 2 considers antifraud programs and controls to bean integral aspect of internal controls. We discuss these controls separatelybecause they affect all other aspects of internal control.

Each component is explained in a following section. These explanations focuson the relationship of each component to those entity objectives and related inter-nal control in each category that are of greatest relevance to the financial statement

Components of internal control,p. 392

Control activities, p. 392Control environment, p. 392Fundaments concepts, p. 392Information and communication,

p. 392

Inherent limitations, p. 393Internal control, p. 391Monitoring, p. 392Risk assessment, p. 392

[396] PART 2 / AUDIT PLANNING

Hadel Studio ● (516) 333 ● 2580

Antifraud Programs and Controls**

Monitoring5

Control Activities4

Information and Communication3

Risk Assessment2

Control Environment1

Figure 10-1 ■ Components of Internal Control

audit—namely, those that are designed to prevent or detect material misstate-ments in the financial statements.

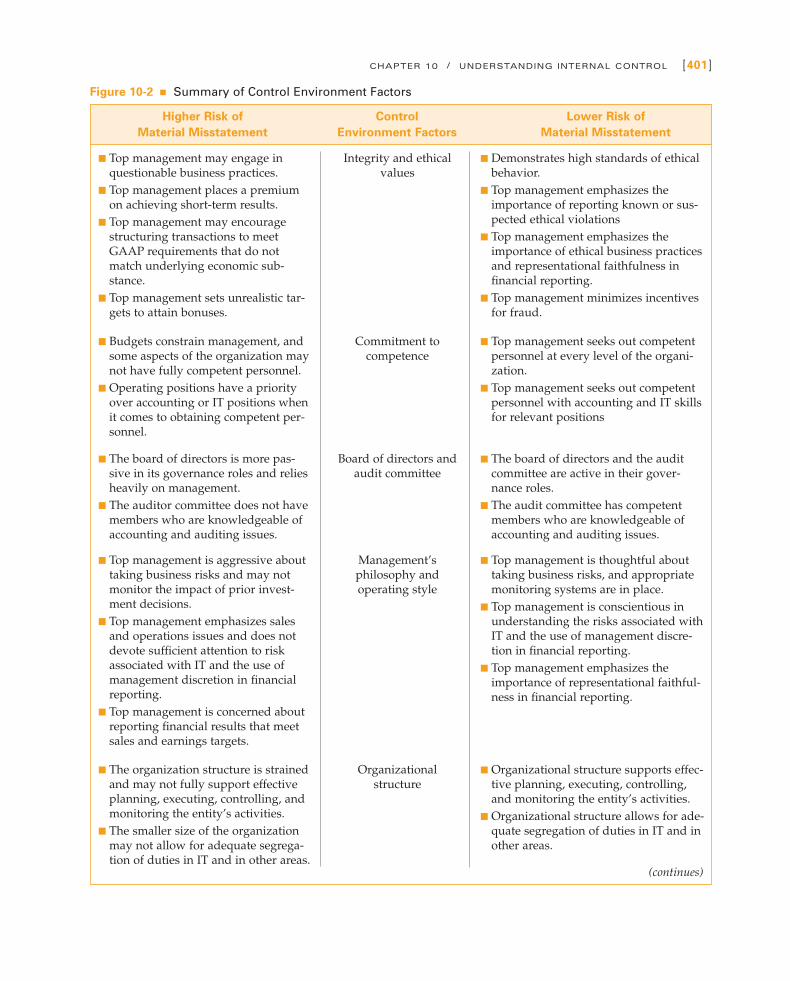

CONTROL ENVIRONMENT

A strong control environment comprises numerous factors that work together toenhance the control consciousness of people who implement controls throughoutan entity. Among these are the following (AU 319.25):

■ Integrity and ethical values■ Commitment to competence■ Board of directors and audit committee■ Management’s philosophy and operating style■ Organizational structure■ Assignment of authority and responsibility■ Human resource policies and practices

The extent to which each factor is formally addressed by an entity will vary basedon such considerations as its size and maturity. These factors constitute a majorpart of an entity’s culture. Brief discussion of each of these control environmentfactors follows.

Integrity and Ethical Values

The COSO report notes that managers of well-run entities have increasinglyaccepted the view that “ethics pay—that ethical behavior is good business.” Inorder to emphasize the importance of integrity and ethical values among all per-sonnel of an organization, the CEO and other members of top management should:

■ Set the tone by example, by consistently demonstrating integrity and practicinghigh standards of ethical behavior.

■ Communicate to all employees, verbally and through written policy statementsand codes of conduct, that the same is expected of them, that each employee hasa responsibility to report known or suspected violations to a higher level in theorganization, and that the violations will result in penalties.

■ Provide moral guidance to any employees whose poor moral backgrounds havemade them ignorant of what is right and wrong.

■ Reduce or eliminate incentives and temptations that might lead individuals toengage in dishonest, illegal, or unethical acts. Examples of incentives for nega-tive behavior include placing undue emphasis on short-term results or meetingunrealistic performance targets, or bonus and profit-sharing plans with termsthat might elicit fraudulent financial reporting practices. A strong control envi-ronment encourages employees to stay well away from questionable account-ing practices and it places a strong emphasis on representational faithfulness infinancial reporting.

The control environment represents the tone set by management of an organization that influ-ences the control consciousness of its people. It is the foundation for all other components ofinternal control, providing discipline and structure.

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [397]

■ What are the keycomponents of astrong control envi-ronment, includingrelevant IT aspects?

Audit Decision 1

Commitment to Competence

To achieve entity objectives, personnel at every level in the organization must pos-sess the requisite knowledge and skills needed to perform their jobs effectively.Commitment to competence includes management’s consideration of the knowl-edge and skills needed, and the mix of intelligence, training, and experiencerequired to develop that competence. For example, meeting financial reportingobjectives in a large publicly held company generally requires higher levels ofcompetence on the part of the chief financial officer and accounting personnelthan would be the case for a small privately held company. It is also important forsenior management to attend to the competence and training of individuals whodevelop or work with IT.

Board of Directors and Audit Committee

The composition of the board of directors and audit committee and the mannerin which they exercise their governance and oversight responsibilities have amajor impact on the control environment. Factors that impact the effectiveness ofthe board and audit committee include their independence from management; theaccounting knowledge, experience and stature of their members; the extent oftheir involvement and scrutiny of management’s activities; the appropriateness oftheir actions (e.g., the degree to which they raise and pursue difficult questionswith management). An effective audit committee can enhance the independenceand professional skepticism of an external auditor. The lack of an audit commit-tee in a private company may not be a weakness if the board as a whole can carryout the audit committee’s responsibilities.

Management’s Philosophy and Operating Style

Many characteristics may form a part of management’s philosophy and operatingstyle and have an impact on the control environment. The characteristics of man-agement’s philosophy and operating style include:

■ Approach to taking and monitoring business risks.■ Reliance on informal face-to-face contacts with key managers versus a formal

system of written policies, performance indicators, and exception reports.■ Attitudes and actions toward financial reporting.■ Conservative or aggressive selection from available accounting principles.■ Conscientiousness and conservatism in developing accounting estimates.■ Conscientiousness and understanding of the risks associated with IT.

The last four characteristics are of particular significance in assessing the controlenvironment over financial reporting. For example, if management is aggressivein making judgments about accounting estimates (e.g., provision for bad debts,obsolete inventory, or depreciation expense) in ways that shift expenses from oneperiod to another, earnings may be materially misstated.

Organizational Structure

An organizational structure contributes to an entity’s ability to meet its objectivesby providing an overall framework for planning, executing, controlling, and mon-

[398] PART 2 / AUDIT PLANNING

itoring an entity’s activity. Developing an organizational structure for an entityinvolves determining the key areas of authority and responsibility and the appro-priate line of reporting. These will depend in part on the entity’s size and thenature of its activities. An entity’s organizational structure is usually depicted inan organization chart that should accurately reflect lines of authority and report-ing relationships. Management should attend not only to the structure of theentity’s operations, but also to the organizational structure of information tech-nology and accounting information systems (see the discussion of segregation ofduties regarding IT on p. 447). An auditor needs to understand these relationshipsto properly assess the control environment and how it may impact the effective-ness of particular controls.

Assignment of Authority and Responsibility

The assignment of authority and responsibility includes the particulars of howand to whom authority and responsibility for all entity activities are assigned,and should enable each individual to know (1) how his or her actions interrelatewith those of others in contributing to the achievement of the entity’s objectivesand (2) for what each individual will be held accountable. This factor alsoincludes policies dealing with appropriate business practices, knowledge andexperience of key personnel, and resources provided for carrying out duties.

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [399]

A company’s audit committee plays an important role within the control environment andmonitoring components of internal control over financial reporting. An effective audit com-mittee helps set a positive tone at the top. The company’s board of directors is primarilyresponsible for evaluating audit committee effectiveness. However, PCAOB Standard No. 2also states that the auditor should evaluate the effectiveness of the auditor committee as partof understanding the control environment and monitoring. The external auditor should focuson the audit committee’s oversight of the company’s external financial reporting and internalcontrol over financial reporting. When making this evaluation, the auditor might consider:

■ The independence of the audit committee from management.■ The clarity with which the audit committee’s responsibilities are articulated.■ How well the audit committee and management understand those responsibilities.■ The audit committee’s involvement and interaction with the independent auditor.■ The audit committee’s interaction with key members of financial management.■ Whether the right questions are raised and pursued with management and the auditor.■ Whether questions indicate an understanding of the critical accounting policies and judg-

mental accounting estimates.■ The audit committee’s responsiveness to issues raised by the auditor.

Ineffective oversight by the audit committee of the company’s external financial reportingshould be regarded as at least a significant deficiency and is a strong indicator of a materialweakness in internal control over financial reporting.

external auditor evaluation of audit committees

Often when individuals or managers are not held accountable for their respon-sibilities, little attention is given to the accounting system and the completenessand accuracy of information that flows from the accounting system. If a manageris not held accountable for the results of his or her operating unit, there is littleincentive to correct errors in accounting for transactions. Although written jobdescriptions should delineate specific duties and reporting relationships, it isimportant to understand informal structures that may exist and how individualsare held accountable for their responsibilities.

The auditor should also be aware of how management assigns authority andresponsibility for IT. This includes methods of assigning authority and responsi-bility over computer systems documentation, and the procedures for authorizingand approving system changes. A lack of accountability over making changes inprogrammed control procedures creates an environment that is conducive to uti-lizing IT to cover employee fraud.

Human Resource Policies and Practices

A fundamental concept of internal control previously stated is that it is imple-mented by people. Thus, for internal control to be effective, it is critical thathuman resource policies and procedures be employed that will ensure that theentity’s personnel possess the expected levels of integrity, ethical values, and com-petence. Such practices include well-developed recruiting policies and screeningprocesses in hiring; orientation of new personnel to the entity’s culture and oper-ating style; training policies that communicate prospective roles and responsibili-ties; disciplinary actions for violations of expected behavior; evaluation, counsel-ing, and promotion of people based on periodic performance appraisals; andcompensation programs that motivate and reward superior performance whileavoiding disincentives to ethical behavior.

Summary of Control Environment

The control environment is critical because it has a pervasive effect on the otherfour components of internal control. For example, if senior management does nothire competent individuals and fails to underscore the importance of ethics andcompetence in the performance of work that supports the accounting system,employees may not perform other control procedures with adequate professionalcare. If top management, in assigning authority and responsibility, does not holdother managers accountable for their use of resources, there is little incentive toeffectively implement the remaining components of internal control. If, however,top management emphasizes the importance of internal control and the need forreliable information for decision making, it increases the likelihood that otheraspects of internal control will operate effectively. Top management can also takesteps that minimize the incentives to engage in fraud, whether fraudulent finan-cial reporting or misappropriation of assets. Figure 10-2 summarizes some of thefactors that can strengthen other aspects of internal control and lower the risk ofmaterial misstatement or weaken other aspects of internal control and increase therisk of material misstatement.

[400] PART 2 / AUDIT PLANNING

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [401]

Figure 10-2 ■ Summary of Control Environment Factors

Higher Risk of Control Lower Risk of

Material Misstatement Environment Factors Material Misstatement

■ Top management may engage inquestionable business practices.

■ Top management places a premiumon achieving short-term results.

■ Top management may encouragestructuring transactions to meetGAAP requirements that do notmatch underlying economic sub-stance.

■ Top management sets unrealistic tar-gets to attain bonuses.

Integrity and ethicalvalues

■ Demonstrates high standards of ethicalbehavior.

■ Top management emphasizes theimportance of reporting known or sus-pected ethical violations

■ Top management emphasizes theimportance of ethical business practicesand representational faithfulness infinancial reporting.

■ Top management minimizes incentivesfor fraud.

■ Budgets constrain management, andsome aspects of the organization maynot have fully competent personnel.

■ Operating positions have a priorityover accounting or IT positions whenit comes to obtaining competent per-sonnel.

Commitment tocompetence

■ Top management seeks out competentpersonnel at every level of the organi-zation.

■ Top management seeks out competentpersonnel with accounting and IT skillsfor relevant positions

■ The board of directors is more pas-sive in its governance roles and reliesheavily on management.

■ The auditor committee does not havemembers who are knowledgeable ofaccounting and auditing issues.

Board of directors andaudit committee

■ The board of directors and the auditcommittee are active in their gover-nance roles.

■ The audit committee has competentmembers who are knowledgeable ofaccounting and auditing issues.

■ Top management is aggressive abouttaking business risks and may notmonitor the impact of prior invest-ment decisions.

■ Top management emphasizes salesand operations issues and does notdevote sufficient attention to riskassociated with IT and the use ofmanagement discretion in financialreporting.

■ Top management is concerned aboutreporting financial results that meetsales and earnings targets.

Management’sphilosophy andoperating style

■ Top management is thoughtful abouttaking business risks, and appropriatemonitoring systems are in place.

■ Top management is conscientious inunderstanding the risks associated withIT and the use of management discre-tion in financial reporting.

■ Top management emphasizes theimportance of representational faithful-ness in financial reporting.

■ The organization structure is strainedand may not fully support effectiveplanning, executing, controlling, andmonitoring the entity’s activities.

■ The smaller size of the organizationmay not allow for adequate segrega-tion of duties in IT and in other areas.

Organizationalstructure

■ Organizational structure supports effec-tive planning, executing, controlling,and monitoring the entity’s activities.

■ Organizational structure allows for ade-quate segregation of duties in IT and inother areas.

(continues)

RISK ASSESSMENT

Management’s risk assessment process is depicted in Figure 10-3. Management’spurpose is to (1) identify risk and (2) place effective controls in operation to con-trol those risks. Management needs to seek a balance such that the higher the riskof misstatement in the financial statements, the more effective the controls shouldbe to prevent misstatements, or detect and correct them on a timely basis. In astrong risk assessment system, management should consider:

■ The entity’s business risks and their financial consequences.■ The inherent risks of misstatement in financial statement assertions.■ The risk of fraud and its financial consequences.

To the extent that management appropriately identifies risks and successfully ini-tiates control activities to address those risks, the auditor’s combined assessmentof inherent and control risks for related assertions will be lower. In some cases,

Risk assessment for financial reporting purposes is an entity’s identification, analysis, andmanagement of risk relevant to the preparation of financial statements that are fairly presentedin conformity with generally accepted accounting principles.

Source: AU 319.28.

[402] PART 2 / AUDIT PLANNING

Figure 10-2 ■ (Continued)

Higher Risk of Control Lower Risk of

Material Misstatement Environment Factors Material Misstatement

■ Inadequate communication of author-ity and responsibility hinders lowerlevels of management from coordi-nating their actions with others toachieve organizational objectives.

■ Focus on immediate goals may notallow for appropriate monitoring ofand accountability for organizationalresources.

■ Constraints limit assigning authorityand responsibility in IT or in account-ing in ways that would allow forappropriate segregation of duties andchecks and balances.

Assignment of author-ity and responsibility

■ Authority and responsibility isassigned so that lower levels of man-agement know how their actions inter-relate with others in contributing toorganizational objectives.

■ Authority and responsibility isassigned with appropriate monitoringof and accountability for organizationalresources.

■ Top management assigns authority andresponsibility in IT and in accountingin ways that allow for appropriate seg-regation of duties and checks and bal-ances.

■ Budget constraints limit HR policiesand practices, and entity personnelmay not possess a high level ofintegrity, ethical values, or compe-tence.

Human resourcepolicies and practices

■ HR policies and practices ensure thatentity personnel possess the expectedlevel of integrity, ethical values, andcompetence.

■ What are the keycomponents ofstrong risk assess-ment activities,including relevant ITaspects?

Audit Decision 2

however, management may simply decide to accept some level of risk withoutimposing controls because of cost or other considerations.

Management’s risk assessment should include consideration of the risks asso-ciated with IT discussed in Appendix 10A. For example, management shoulddesign information and controls systems that mitigate the problems associatedwith the impact of IT in reducing the traditional segregation of duties. If manage-ment designs and implements a good system of computer general controls, manyof these overall risks will be reduced to a manageable level.

In a strong risk assessment system, management should also include specialconsideration of the risks that can arise from changed circumstances described inAU 319.29:

■ Changes in operating environment■ New personnel■ New or revamped information systems■ Rapid growth■ New technology■ New lines, products, or activities■ Corporate restructurings■ Foreign operations■ New accounting pronouncements

To the extent that these risks are present, management should put controls inplace to control these risks. For example, when management develops a newinformation system for a segment of the organization, user departments should beinvolved in developing the specifications of the system, there should be signifi-cant testing of the system with test data, and users should be involved in the finaltests to ensure that the new system accomplishes its goals. These are importantcontrol activities that need to respond to the risk that a new information systemmay not function as desired.

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [403]

Fraud RiskInherent RiskBusiness Risk

InternalControls

Hadel Studio ● (516) 333 ● 2580

Figure 10-3 ■ Management’s Risk Assessment Process

INFORMATION AND COMMUNICATION

As noted in the foregoing, a major focus of the accounting system is on transac-tions. Transactions consist of exchanges of assets and services between an entityand outside parties, as well as the transfer or use of assets and services within anentity. It follows that a major focus of control policies and procedures related tothe accounting system is that transactions be handled in a way that supports rep-resentational faithfulness and the application of GAAP in the financial statements.Thus, an effective accounting system should:

■ Identify and record only the valid transactions of the entity that occurred in thecurrent period (existence and occurrence assertion).

■ Identify and record all valid transactions of the entity that occurred in the cur-rent period (completeness assertion).

■ Ensure that recorded assets and liabilities are the result of transactions that pro-duced entity rights to, or obligations for, those items (rights and obligationsassertions).

■ Measure the value of transactions in a manner that permits recording theirproper monetary value in the financial statements (valuation or allocationassertion).

■ Capture sufficient detail of all transactions to permit their proper presentationin the financial statements, including proper classification and required disclo-sures (presentation and disclosure assertion).

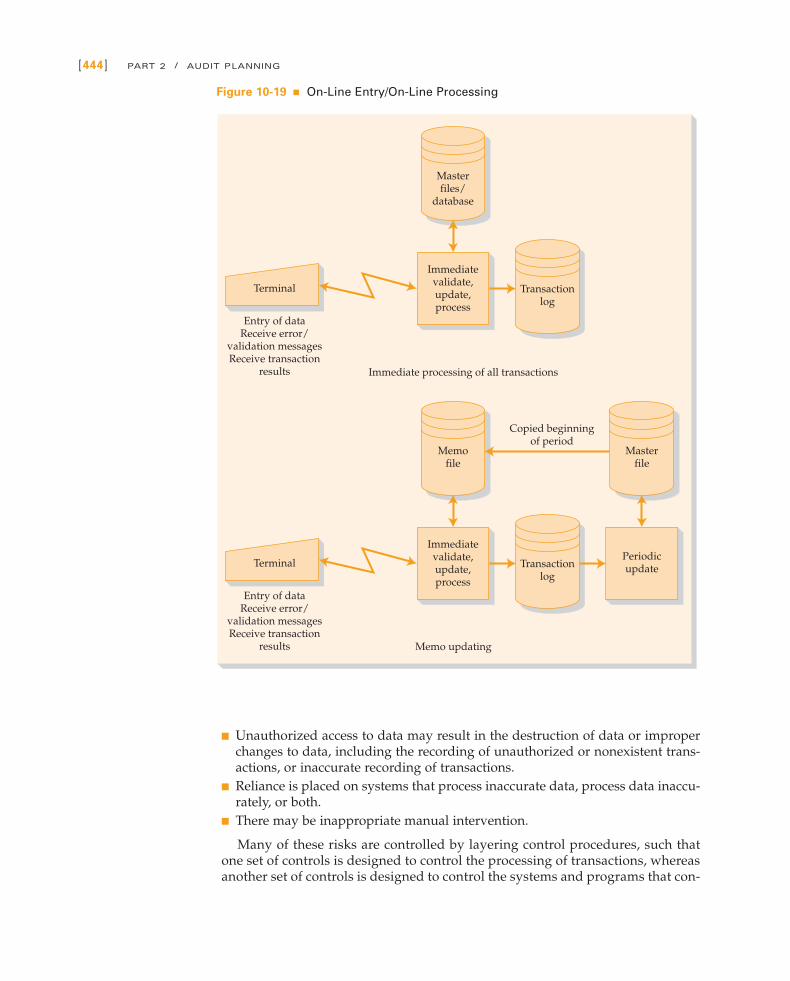

An effective accounting system should provide a complete audit trail or trans-action trail for each transaction. An audit trail or transaction trail is a chain ofevidence from initiating a transaction to its recording in the general ledger andfinancial statements provided by coding, cross-reference, and documentation con-necting account balances and other summary results with original transactiondata. Transaction trails are essential both to management and to auditors. Man-agement uses the trail in responding to inquiries from customers or suppliers con-cerning account balances. It is particularly important for management to ensure aclear transaction trail in IT systems where documentary evidence may be retainedfor only a short period of time. Computer systems that use on-line processingshould create a unique transaction number that can be used to establish such atransaction trail. Auditors use the trail in tracing and vouching transactions asexplained in Chapter 6.

Documents and records represent an aspect of the information and communi-cation system that provides important audit evidence. Documents provide evi-dence of the occurrence of transactions and the price, nature, and terms of the

The information and communication system relevant to financial reporting objectives, whichincludes the accounting system, consists of the methods and records established to identify,assemble, analyze, classify, record, and report entity transactions (as well as events and condi-tions) and to maintain accountability for the related assets and liabilities. Communicationinvolves providing a clear understanding of individual roles and responsibilities pertaining tointernal control over financial reporting.

Source: AU 319.34.

[404] PART 2 / AUDIT PLANNING

■ What are the keycomponents of aneffective informationand communicationsystem, including rel-evant IT aspects?

Audit Decision 3

transactions. Invoices, checks, contracts, and time tickets are illustrative of com-mon types of documents. When duly signed or stamped, documents also providea basis for establishing responsibility for executing and recording transactions.Records include employee earnings records, which show cumulative payroll datafor each employee, and perpetual inventory records. Another type of record isdaily summaries of documents issued, such as sales invoices and checks. Thesummaries are then independently compared with the sum of correspondingdaily entries to determine whether all transactions have been recorded. In modernaccounting systems, records are usually in electronic format, and entities may cre-ate printed copies for ease of use.

Communication includes making sure that personnel involved in the financialreporting system understand how their activities relate to the work of others bothinside and outside the organization. This includes the role of the system in report-ing exceptions for followup as well as reporting unusual exceptions to higher lev-els within the entity. Policy manuals, accounting and financial reporting manuals,a chart of accounts, and memoranda also constitute part of the information andcommunication component of internal control.

CONTROL ACTIVITIES

A strong system of control activities contains a number of elements that need tobe placed in operation for the control activities to be effective. Figure 10-4describes one way that control activities relevant to a financial statement audit canbe described.

1. Authorization Controls

A major purpose of proper authorization procedures is to ensure that every trans-action is authorized by management personnel acting within the scope of theirauthority. Each transaction entry should be properly authorized and approved inaccordance with management’s general or specific authorization. General author-ization relates to the general conditions under which transactions are authorized,such as standard price lists for products and credit policies for charge sales. Spe-cific authorization relates to the granting of the authorization on a case-by-casebasis. When transactions are individually processed, authorization is usually pro-vided in the form of a signature or stamp on the source document or in the formof electronic authorization that leaves a computerized audit trail.

Proper authorization procedures often have a direct effect on control risk forexistence and occurrence assertions, and in some cases, valuation or allocationassertions, such as the authorization of an expenditure or the authorization of acustomer’s credit limit. The board of directors may authorize capital expendituresat a designated amount. Expenditures in excess of that amount might indicate

Control activities are those policies and procedures that help ensure that management direc-tives are carried out. They help ensure that necessary actions are taken to address risks toachievement of the entity’s objectives. Control activities have various objectives and areapplied at various organization and functional levels.

Source: AU 319.32.

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [405]

■ What are the keycomponents ofstrong control activi-ties, including rele-vant IT aspects?

Audit Decision 4

existence problems (an invalid transaction) or presentation and disclosure prob-lems (expenses classified as assets).

2. Segregation of Duties

Strong segregation of duties involves segregating (1) transaction authorization,(2) maintaining custody of assets, and (3) maintaining recorded accountability inthe accounting records. Figure 10-5 depicts the traditional segregation of duties.Failure to maintain strong segregation of duties makes it possible for an individ-ual to commit an error or fraud and then be in a position to conceal it in the nor-mal course of his or her duties. For example, an individual who processes cashremittances from customers (has access to the custody of assets) should not alsohave authority to approve and record credits to customers’ accounts for salesreturns and allowances or write-offs (authorize transactions). In such a case, theindividual could steal a cash remittance and cover the theft by recording a salesreturn or allowance or bad-debt write-off.

Sound segregation of duties also involves comparing recorded accountabilitywith assets on hand. For example, sound internal control involves independentbank reconciliations comparing bank balances with book balances for each bankaccount. Perpetual inventory records should also be periodically compared withinventory on hand.

Proper segregation of duties, should also be maintained within the IT department andbetween IT and user departments. Several functions within IT—systems develop-

[406] PART 2 / AUDIT PLANNING

Hadel Studio ● (516) 333 ● 2580

Performance Reviews5

Physical Controls4

Controls over Management Discretion in Financial Reporting6

Segregation of Duties2

Authorization Controls1

Information Processing Controls3

Control over the Financial Reporting Processc

Computer Application Controlsb

General Controlsa

Figure 10-4 ■ Control Activities

ment, operations, data controls, and securities administration—should be segre-gated (see Figure 10-21). In addition, IT should not correct data submitted byuser departments and should be organizationally independent from userdepartments. Segregation of duties within IT is so important that it is considereda critical aspect of general controls (see the discussion of organization and oper-ation control on p. 447).

3. Information Processing Controls

Information processing controls address risks related to the authorization, com-pleteness, and accuracy of transactions. These controls are particularly relevant tothe financial statement audit. Most entities, regardless of size, now use computersfor information processing in general and for accounting systems in particular. Insuch cases, it is useful to further categorize information processing controls asgeneral controls and application controls, which are discussed below.

3a. General Controls

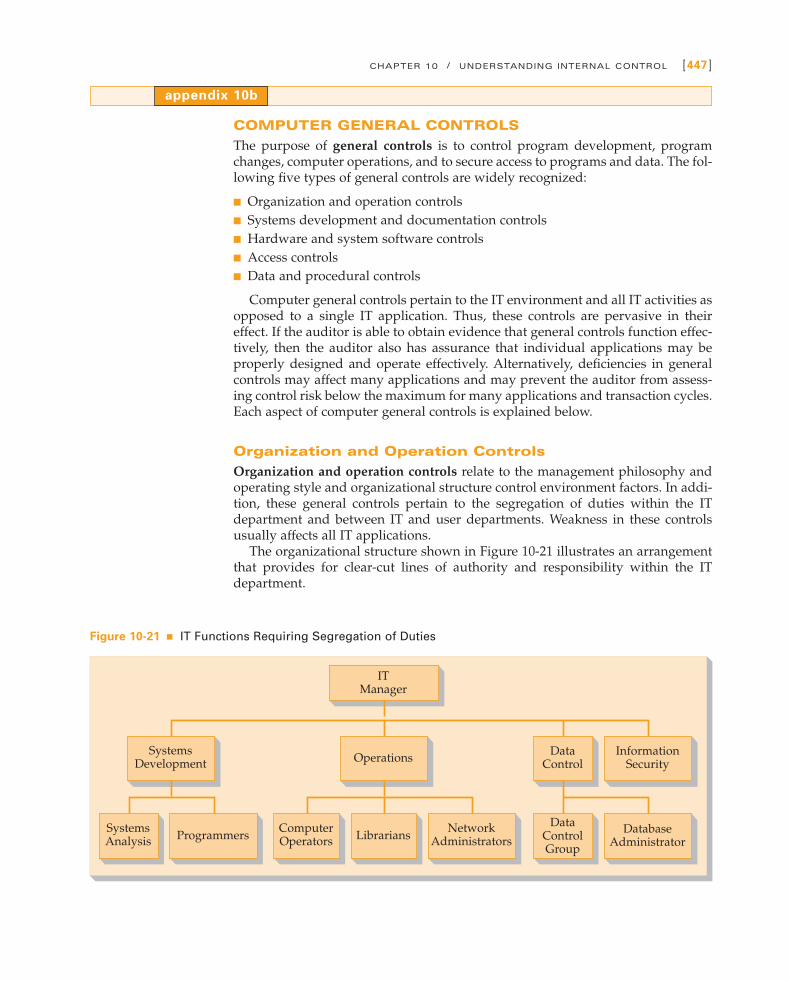

The purpose of general controls is to control program development, programchanges, and computer operations, and to secure access to programs and data.The following five types of general controls are widely recognized:■ Organization and operation controls address the segregation of duties within

the IT department and between IT and user departments. A critical componentis segregating access to programs from access to data files. Weakness in thesecontrols usually affects all IT applications.

■ Systems development and documentation controls relate to (1) review, testing,and approval of new systems and program changes, and (2) controls over doc-umentation.

■ Hardware and systems software controls are an important factor that con-tributes to the high degree of reliability of today’s information technology.

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [407]

Maintainrecorded

accountability

Maintaincustody of

assets

Authorizethe

transaction

Periodic comparison ofrecorded accountability

with assets

Hadel Studio ● (516) 333 ● 2580

Figure 10-5 ■ Traditional Segregation of Duties

Hardware and software controls are designed to detect any malfunctioning ofthe equipment. To achieve maximum benefit from these controls, (1) thereshould be a program of preventive maintenance on all hardware, and (2) con-trols over changes to systems software should parallel the systems develop-ment and documentation controls described above.

■ Access controls are designed to prevent unauthorized use of IT equipment,data files, and computer programs. The specific controls include a combinationof physical, software, and procedural safeguards.

■ Data and procedural controls provide a framework for controlling daily com-puter operations, minimizing the likelihood of processing errors, and assuringthe continuity of operations in the event of a physical disaster or computer fail-ure through adequate file backup and other controls.

Computer general controls pertain to the IT environment and all IT activities asopposed to a single IT application. Because of the pervasive character of generalcontrols, if the auditor is able to obtain evidence that general controls functioneffectively, then the auditor also has important assurance that individual applica-tions may be properly designed and operate consistently during the period underaudit. For example, strong computer general controls involve regular testing andreview of individual programs that process sales, cash receipts, payroll, and manyother transactions. Alternatively, deficiencies in general controls may affect manyapplications and may prevent the auditor from assessing control risk below themaximum for many applications and transaction cycles. Students not familiarwith the details of computer general controls should study the in-depth discus-sion in Appendix 10B.

3b. Computer Application Controls

The purpose of application controls is to use the power of information technol-ogy to control transactions in individual transaction cycles. Hence, applicationscontrols will differ for each transaction cycle (e.g., sale vs. cash receipts). The fol-lowing three groups of application controls are widely recognized:

■ Input controls■ Processing controls■ Output controls

These controls are designed to provide reasonable assurance that the recording, pro-cessing, and reporting of data by IT are properly performed for specific applica-tions. Thus, the auditor must consider these controls separately for each significantaccounting application, such as billing customers or preparing payroll checks.

In today’s IT environment, application controls execute the function of inde-pendent checks by (1) using programmed application controls to identify trans-actions that contain possible misstatements and (2) having people follow up andcorrect items noted on exception reports. The following discussion explains howprogrammed controls may be used to identify items that should be included onvarious exception reports.

Input Controls Input controls are program controls designed to detect andreport errors in data that are input for processing. They are of vital importance inIT systems because most of the errors occur at this point. Input controls are

[408] PART 2 / AUDIT PLANNING

designed to provide reasonable assurance that data received for processing havebeen properly authorized and converted into machine-sensible form. These con-trols also include the people who follow up on the rejection, correction, andresubmission of data that were initially incorrect.

Controls over the conversion of data into machine-sensible form are intendedto ensure that the data are correctly entered and converted data are valid. Specificcontrols include:

■ Verification controls. These controls often compare data input for computer pro-cessing with information contained on computer master files, or other dataindependently entered at earlier stages of a transaction.

■ Computer editing. These are computer routines intended to detect incomplete,incorrect, or unreasonable data. They include:■ Missing data check to ensure that all required data fields have been completed

and no blanks are present.■ Valid character check to verify that only alphabetical, numerical, or other spe-

cial characters appear as required in data fields.■ Limit (reasonableness) check to determine that only data falling within prede-

termined limits are entered (e.g., time cards exceeding a designated numberof hours per week may be rejected).

■ Valid sign check to determine that the sign of the data, if applicable, is correct(e.g., a valid sign test would ensure that the net book value of an asset waspositive and that assets are not overdepreciated).

■ Valid code check to match the classification (i.e., expense account number) ortransaction code (i.e., cash receipts entry) against the master list of codes per-mitted for the type of transaction to be processed.

■ Check digit to determine that an account, employee, or other identificationnumber has been correctly entered by applying a specific arithmetic opera-tion to the identification number and comparing the result with a check digitembedded within the number.

The correction and resubmission of incorrect data are vital to the accuracy ofthe accounting records. If the processing of a valid sales invoice is stoppedbecause of an error, both accounts receivable and sales will be understated untilthe error is eliminated and the processing completed. Misstatements should becorrected by those responsible for the mistake. Furthermore, strong controls cre-ate a log of potential misstatements, and the data control group periodicallyreviews their disposition.

Processing Controls Processing controls are designed to provide reason-able assurance that the computer processing has been performed as intended forthe particular application. Thus, these controls should preclude data from beinglost, added, duplicated, or altered during processing.

Processing controls take many forms, but the most common ones are pro-grammed controls incorporated into the individual applications software. Theyinclude the following:

■ Control totals. Provision for accumulating control totals is written into the com-puter program to facilitate the balancing of input totals with processing totals

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [409]

for each run. Similarly, run-to-run totals are accumulated to verify processingperformed in stages.

■ File identification labels. External labels are physically attached to magnetic tapeor disks to permit visual identification of a file. Internal labels are in machine-sensible form and are matched electronically with specified operator instruc-tions (or commands) incorporated into the computer program before process-ing can begin or be successfully completed.

■ Limit and reasonableness checks. A limit or reasonableness test would comparecomputed data with an expected limit (e.g., the product of payroll rates timeshours worked would be included on an exception report and not processed if itexceeded an predetermined limit).

■ Before-and-after report. This report shows a summary of the contents of a masterfile before and after each update.

■ Sequence tests. If transactions are given identification numbers, the transactionfile can be tested for sequence (e.g., an exception report would include missingnumbers or duplicate numbers in a sequence of sales invoices).

■ Process tracing data. This control involves a printout of specific data for visualinspection to determine whether the processing is correct. For evaluatingchanges in critical data items, tracing data may include the contents before andafter the processing (e.g., information from shipping data with information onsales invoices).

Output Controls Output controls are designed to ensure that the process-ing results are correct and that only authorized personnel receive the output. Theaccuracy of the processing results includes both updated machine-sensible filesand printed output. This objective is met by the following:

■ Reconciliation of totals. Output totals that are generated by the computer pro-grams are reconciled to input and processing totals by the data control groupor user departments.

■ Comparison to source documents. Output data are subject to detailed comparisonwith source documents.

■ Visual scanning. The output is reviewed for completeness and apparent reason-ableness. Actual results may be compared with estimated results.

The data control group usually controls who can have access to data in a data-base and maintains control over any centrally produced reports for the distribu-tion of output. This group should exercise special care over the access to, or dis-tribution of, confidential output. To facilitate control over the disposition ofoutput, systems documentation should include reports of who has access to vari-ous aspects of a database or some form of a report distribution sheet.

3c. Controls over the Financial Reporting Process

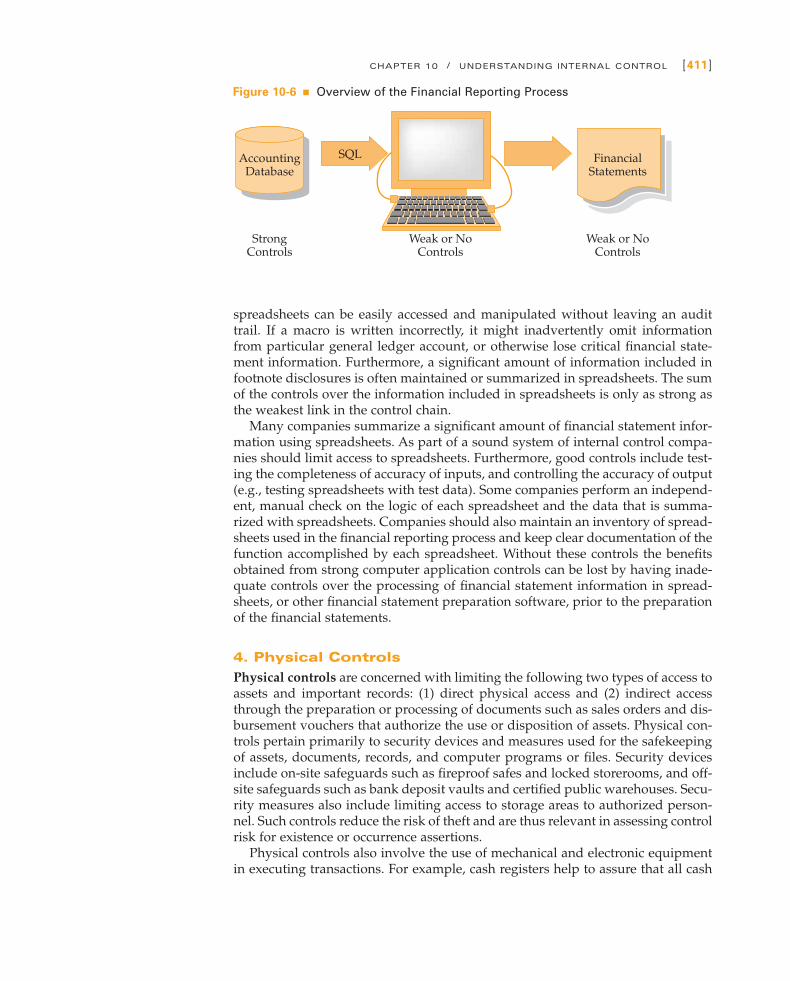

Figure 10-6 provides an overview of the financial reporting process in many busi-nesses. In many cases, computer application controls provide a strong controlover the information that is included in a computer database. When the timecomes to prepare financial statements, a structured query language (SQL) is usedto access the database and download information into a spreadsheet. However,once the data is in a spreadsheet, it may be subject to little or no controls. Data in

[410] PART 2 / AUDIT PLANNING

spreadsheets can be easily accessed and manipulated without leaving an audittrail. If a macro is written incorrectly, it might inadvertently omit informationfrom particular general ledger account, or otherwise lose critical financial state-ment information. Furthermore, a significant amount of information included infootnote disclosures is often maintained or summarized in spreadsheets. The sumof the controls over the information included in spreadsheets is only as strong asthe weakest link in the control chain.

Many companies summarize a significant amount of financial statement infor-mation using spreadsheets. As part of a sound system of internal control compa-nies should limit access to spreadsheets. Furthermore, good controls include test-ing the completeness of accuracy of inputs, and controlling the accuracy of output(e.g., testing spreadsheets with test data). Some companies perform an independ-ent, manual check on the logic of each spreadsheet and the data that is summa-rized with spreadsheets. Companies should also maintain an inventory of spread-sheets used in the financial reporting process and keep clear documentation of thefunction accomplished by each spreadsheet. Without these controls the benefitsobtained from strong computer application controls can be lost by having inade-quate controls over the processing of financial statement information in spread-sheets, or other financial statement preparation software, prior to the preparationof the financial statements.

4. Physical Controls

Physical controls are concerned with limiting the following two types of access toassets and important records: (1) direct physical access and (2) indirect accessthrough the preparation or processing of documents such as sales orders and dis-bursement vouchers that authorize the use or disposition of assets. Physical con-trols pertain primarily to security devices and measures used for the safekeepingof assets, documents, records, and computer programs or files. Security devicesinclude on-site safeguards such as fireproof safes and locked storerooms, and off-site safeguards such as bank deposit vaults and certified public warehouses. Secu-rity measures also include limiting access to storage areas to authorized person-nel. Such controls reduce the risk of theft and are thus relevant in assessing controlrisk for existence or occurrence assertions.

Physical controls also involve the use of mechanical and electronic equipmentin executing transactions. For example, cash registers help to assure that all cash

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [411]

AccountingDatabase

StrongControls

Weak or NoControls

Weak or NoControls

Hadel Studio ● (516) 333 ● 2580

SQL FinancialStatements

Figure 10-6 ■ Overview of the Financial Reporting Process

receipt transactions are rung up, and they provide locked-in summaries of dailyreceipts. Such controls are relevant in assessing control risk for completenessassertions.

When IT equipment is used, access to the computer, computer records, datafiles, and programs should be restricted to authorized personnel. The use of pass-words, keys, and identification badges provides means of controlling access.When such safeguards are in place, control risk may be reduced for various exis-tence or occurrence, completeness, and valuation or allocation assertions relatedto transaction classes and accounts processed by IT.

Finally, physical control activities include periodic counts of assets and com-parison with amounts shown on control records. Examples include petty cashcounts and physical inventories. These activities may be relevant in assessing exis-tence or occurrence, completeness, and valuation or allocation assertions as dis-cussed further in Part 4 of the text in the context of specific transaction cycles.

5. Performance Reviews

Examples of performance reviews include management review and analysis of

■ Reports that summarize the detail of account balances such as an aged trial bal-ance of accounts, reports of cash disbursements by department, or reports ofsales activity and gross profit by customer or region, salesperson, or product line.

■ Actual performance versus budgets, forecasts, or prior-period amounts.■ The relationship of different sets of data such as nonfinancial operating data

and financial data (for example, comparison of hotel occupancy statistics withrevenue data).

Management’s use of reports that drill down and summarize the transactionsthat make up sales or cash disbursements may provide an independent check onthe accuracy of the accounting information. For example, a university departmentchair might review the details of the payroll that was charged to his or herdepartment on a monthly basis. The quality of this review may provide controlover the occurrence, completeness, and valuation of payroll transactions. Man-agement’s analysis of operating performance may serve another purpose similarto the auditor’s use of analytical procedures in audit planning. That is, manage-ment may develop nonfinancial performance measures that correlate highly withfinancial outcomes, and may allow it to detect accounts that might be misstated.Such misstatements might involve existence or occurrence, completeness, valua-tion or allocation, or presentation and disclosure assertions.

6. Controls over Management Discretion inFinancial Reporting

The PCAOB in Auditing Standard No. 2, An Audit of Internal Control over FinancialReporting Performed in Conjunction with an Audit of Financial Statements, expectspublic companies to establish internal controls in the three following areas:

1. Controls over significant nonroutine and nonsystematic transactions, such asassertions involving judgments and estimates.

2. Controls over the selection and application of GAAP.3. Controls over disclosures.

[412] PART 2 / AUDIT PLANNING

In these circumstances it is rare to find good internal controls in private com-panies. Private companies may have solid internal control over routine transac-tions that are high in volume, and internal controls are often very cost-effective.However, the circumstances identified above often involve significant manage-ment discretion, and the size and nature of the company are such that the auditoris the primary check and balance over these issues. Public companies with moreresources are now establishing internal controls over all aspects of financial state-ment disclosure. As a general rule, key decisions about accounting for individualtransactions, accounting policy, or disclosures should not rest with one individual.It is important that such critical decisions represent the consensus of a knowl-edgeable group.

Internal controls over nonroutine and nonsystematic transactions, such asassertions involving accounting estimates, often have two layers of control. Thefirst stage is control over the data used to make the judgmental computation, andthe second stage is the concurrent review process. For example, if managementmakes an estimate of the allowance for doubtful accounts, the auditor shoulddetermine that the data used in making the assessment should be appropriatelycontrolled. An accounting estimate can be no more reliable than the data used todevelop the accounting estimate. The data should come from a system that is rel-evant to the estimate. Second, there should also be a review process that allows fora followup process that reviews prior accounting estimates with hindsight. Inaddition, there should be an internal process involving individuals who under-stand the business issues related to the accounting estimates that focuses onensuring consistent estimates. The independent review process should focus onthe consistency of the estimation process. The goal is to avoid the abuses wheremanagement has developed accounting estimates that tend to overestimateexpenses in good years and underestimate expenses in years of poor fiscal per-formance.

Some companies are also developing disclosure committees to provide anindependent review of the appropriateness of selection of choices of accountingprinciples, accounting for unusual and nonrecurring transactions, the reasonable-ness of accounting estimates, and the overall level of disclosure in the financialstatements. These committees are often staffed with both (1) individuals who havestrong accounting backgrounds and (2) members of operational management whoare familiar with the company’s operations and transactions. Disclosure commit-tees, and then the audit committee, generally review these critical elements of thefinancial statements before they are released to the auditor. These committees aremost effective when they are staffed by knowledgeable individuals who providean independent check on the initial decisions made by a controller, chief account-ing officer, or a chief financial officer.

MONITORING

Monitoring is a process that assesses the quality of internal control performance over time. Itinvolves assessing the design and operation of controls on a timely basis and taking necessarycorrective actions.

Source: AU 319.38.

CHAPTER 10 / UNDERSTANDING INTERNAL CONTROL [413]

Effective monitoring activities usually involve (1) ongoing monitoring programs,(2) separate evaluations, and (3) an element of reporting deficiencies to the auditcommittee.

Ongoing monitoring activities might take a variety of forms. An active internalaudit function that regularly performs tests of controls using an integrated testfacility or internal auditors may regularly rotate tests of different aspects of thesystem of internal control. In addition, controls may be designed with variousself-monitoring processes. For example, problems with internal control may cometo management’s attention through complaints received from customers aboutbilling errors or from suppliers about payment problems, or from alert managerswho receive reports with information that differs significantly from their first-hand knowledge of operations.

Monitoring also occurs through separate periodic evaluations. Managements ofpublic companies must perform periodic evaluations of internal controls in orderto support an assertion about the effectiveness of the system of internal control.Furthermore, management and the audit committee should be conscious of ITrisks and perform separate evaluations of computer general controls because oftheir pervasive effect on various programmed application controls. The auditcommittee also might charge internal audit with periodic reviews of IT risks andcontrols. Finally, management may receive information from the separate evalua-tion of regulators, such as bank examiners.

The final element of sound monitoring controls involves the reporting of defi-ciencies to the audit committee (or full board of directors). Deficiencies that surfacethrough ongoing monitoring programs or separate evaluations should be regularlybrought to the audit committee for discussion and decisions about corrective actions.

ANTIFRAUD PROGRAMS AND CONTROLS

Antifraud programs and controls are policies and procedures put in place to helpensure that management’s antifraud directives are carried out. An effectiveantifraud program should impact every aspect of the system of internal control.Figure 10-7 summarizes a variety of common aspects of strong antifraud pro-grams and controls.

[414] PART 2 / AUDIT PLANNING

■ What are the keycomponents ofstrong monitoringactivities, includingrelevant IT aspects?

Audit Decision 5

Figure 10-7 ■ Antifraud Programs and Controls

Control Environment

■ Code of conduct/ethical company culture

■ Ethics hotline

■ Audit committee oversight

■ Hiring and promotion

Fraud Risk Assessment

■ Systematic assessment of fraud risks

■ Evaluation of likelihood and magnitude of poten-tial misstatement

Information and Communication

■ Adequacy of the audit trail

■ Antifraud training

Control Activities

■ Adequate segregation of duties

■ Linking controls to fraud risks

Monitoring

■ Developing an effective oversight process

■ “After the fact” evaluations by internal audit