Modelling, Analysis and Simulation - TU/eberry/papers/MAS-E0303.pdf · Centrum voor Wiskunde en...

317

Centrum voor Wiskunde en Informatica MAS Modelling, Analysis andSimulation Modelling, Analysis and Simulation CAFE project _ Final report volume II Secure protocols and architecture Edited by A. Bosselaers, R. Carter, R. Hirschfeld, R. Michelsen, S. Mjølsnes REPORT MAS-E0303 FEBRUARY 28, 2003

Transcript of Modelling, Analysis and Simulation - TU/eberry/papers/MAS-E0303.pdf · Centrum voor Wiskunde en...

Centr um voor Wi sk unde en I nf or ma ti ca

MASModelling, Analysis and Simulation

Modelling, Analysis and Simulation

CAFE project _ Final report volume IISecure protocols and architecture

Edited by A. Bosselaers, R. Carter, R. Hirschfeld,R. Michelsen, S. Mjølsnes

REPORT MAS-E0303 FEBRUARY 28, 2003

CWI is the National Research Institute for Mathematics and Computer Science. It is sponsored by the Netherlands Organization for Scientific Research (NWO).CWI is a founding member of ERCIM, the European Research Consortium for Informatics and Mathematics.

CWI's research has a theme-oriented structure and is grouped into four clusters. Listed below are the names of the clusters and in parentheses their acronyms.

Probability, Networks and Algorithms (PNA)

Software Engineering (SEN)

Modelling, Analysis and Simulation (MAS)

Information Systems (INS)

Copyright © 2001, Stichting Centrum voor Wiskunde en InformaticaP.O. Box 94079, 1090 GB Amsterdam (NL)Kruislaan 413, 1098 SJ Amsterdam (NL)Telephone +31 20 592 9333Telefax +31 20 592 4199

ISSN 1386-3703

CAFE Project − Final Report Volume II

Secure Protocols and Architecture

Edited by A. Bosselaers, R. Carter, R. Hirschfeld, R. Michelsen, S. Mjølsnes

Published by CWI, P.O. Box 94079, 1090 GB Amsterdam, The Netherlands

ABSTRACT

This is the final public report of the CAFE project (ESPRIT 7023). CAFE developed a secure conditional

access architecture and implemented a multi-currency electronic purse system based on smart cards and infrared

wallets. The electronic purse was tested in user trials at the European Commission premises in Brussels. Part I

of the report covers background surveys, a simplified functional description of the system, and the operation

and results of the user trials. Part II describes in detail the security architecture and the technical protocols

developed by the project.

2000 Mathematics Subject Classification: 69C30, 69D56, 69E30, 69M34, 69M55

1998 ACM Computing Classification System: C.3.0, D.4.6, E.3.0, K.4.4, K.6.5

Keywords and Phrases: Conditional access, electronic purse, electronic wallet, smart cards, e-commerce, digital

cash, consumer payments, multi-currency

Note: Many CAFE project participants contributed to the writing of this report, and it would be impossible to

accurately list its authors. The editors listed are those who were involved in the final preparation and editing

of the document.

Final Report Volume II

Technical Speci�cations

ESPRIT ���� CAFE

Document PTS����

April� ����

CAFE Final Report Volume II

ii

CAFE Final Report Volume II

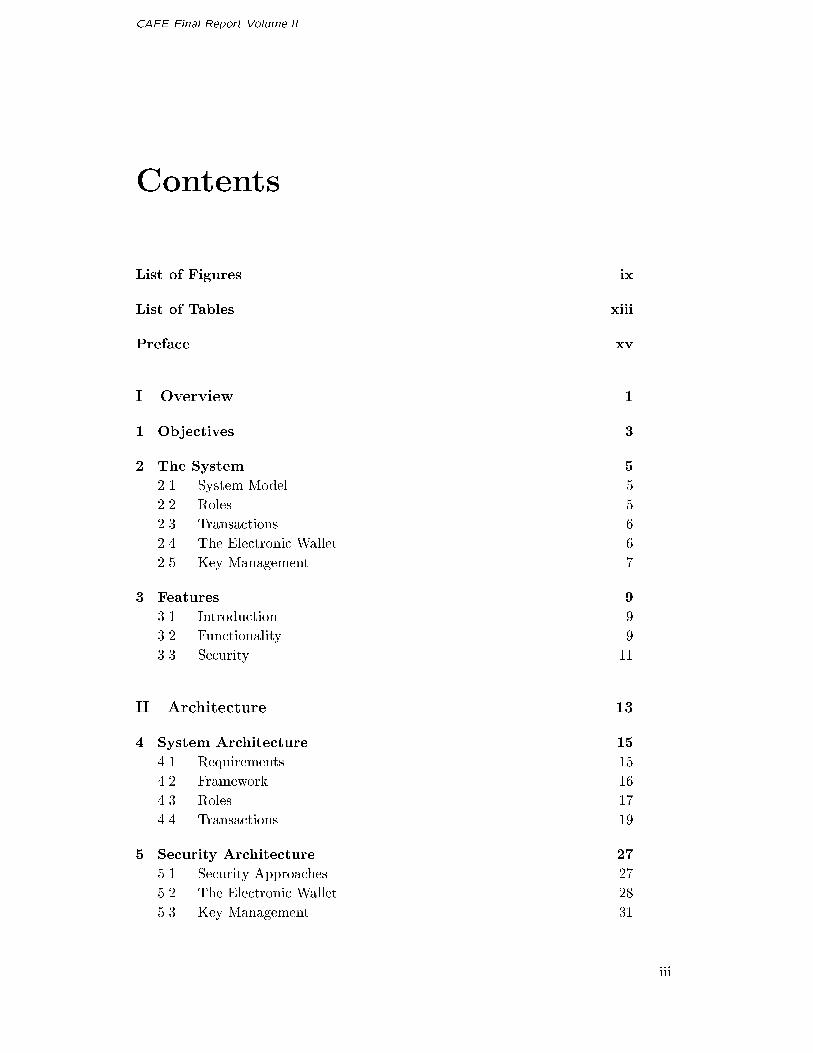

Contents

List of Figures ix

List of Tables xiii

Preface xv

I Overview �

� Objectives �

� The System �

��� System Model � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� Roles � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� Transactions � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� The Electronic Wallet � � � � � � � � � � � � � � � � � � � � � � � � �

��� Key Management � � � � � � � � � � � � � � � � � � � � � � � � � � �

� Features �

��� Introduction � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� Functionality � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� Security � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

II Architecture ��

� System Architecture ��

��� Requirements � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

��� Framework � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

��� Roles � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

��� Transactions � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

� Security Architecture ��

��� Security Approaches � � � � � � � � � � � � � � � � � � � � � � � � ��

��� The Electronic Wallet � � � � � � � � � � � � � � � � � � � � � � � � �

��� Key Management � � � � � � � � � � � � � � � � � � � � � � � � � � ��

iii

Contents CAFE Final Report Volume II

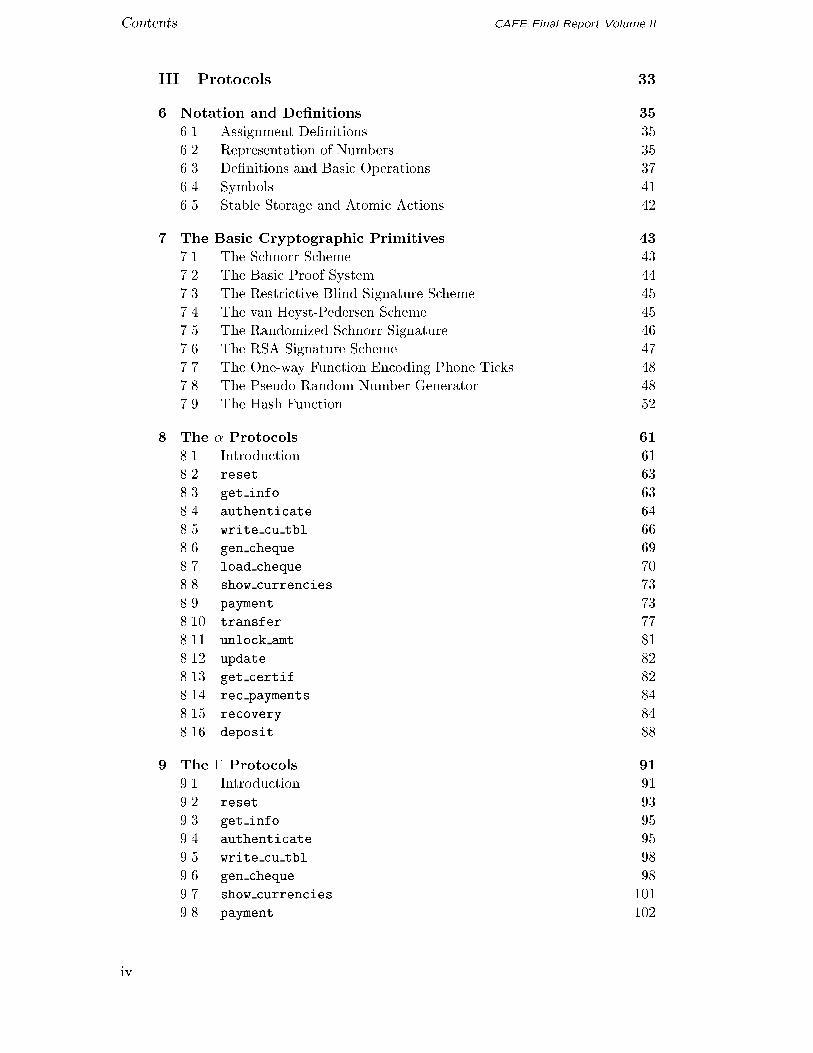

III Protocols ��

� Notation and Denitions ��

��� Assignment De�nitions � � � � � � � � � � � � � � � � � � � � � � � ��

��� Representation of Numbers � � � � � � � � � � � � � � � � � � � � � ��

��� De�nitions and Basic Operations � � � � � � � � � � � � � � � � � ��

��� Symbols � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

��� Stable Storage and Atomic Actions � � � � � � � � � � � � � � � � ��

� The Basic Cryptographic Primitives ��

��� The Schnorr Scheme � � � � � � � � � � � � � � � � � � � � � � � � ��

��� The Basic Proof System � � � � � � � � � � � � � � � � � � � � � � ��

��� The Restrictive Blind Signature Scheme � � � � � � � � � � � � � ��

��� The van Heyst�Pedersen Scheme � � � � � � � � � � � � � � � � � � ��

��� The Randomized Schnorr Signature � � � � � � � � � � � � � � � � ��

��� The RSA Signature Scheme � � � � � � � � � � � � � � � � � � � � ��

��� The One�way Function Encoding Phone Ticks � � � � � � � � � � �

�� The Pseudo Random Number Generator � � � � � � � � � � � � � �

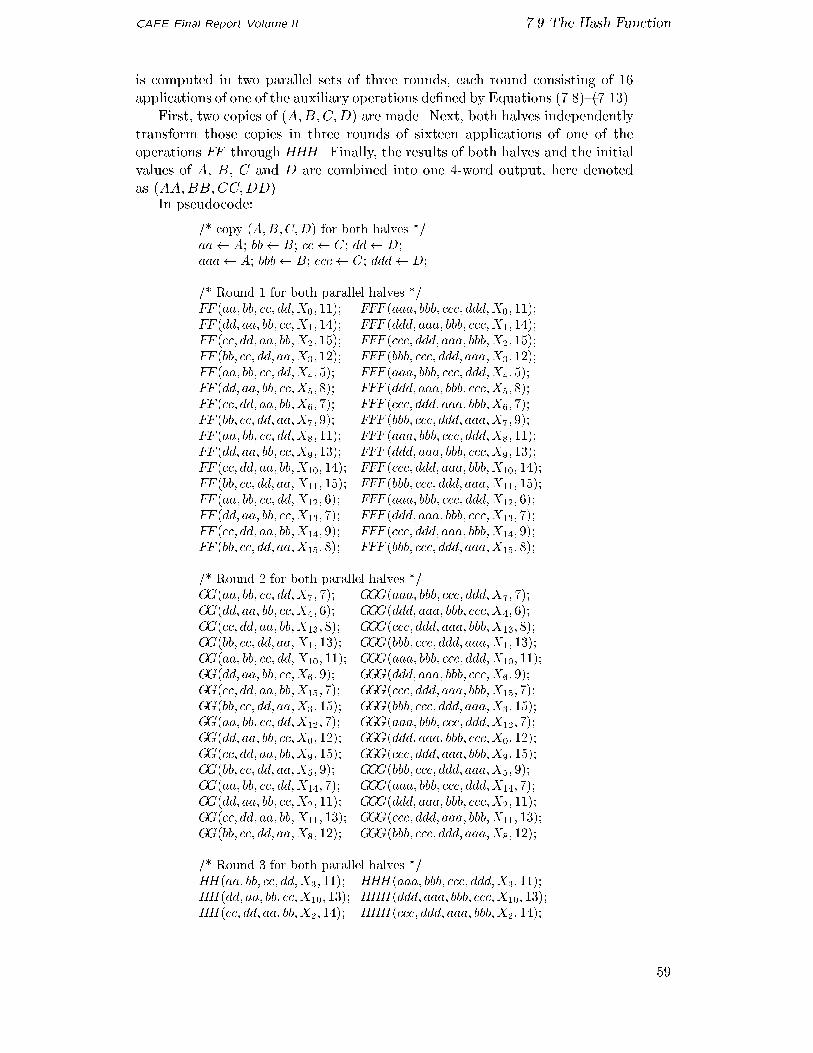

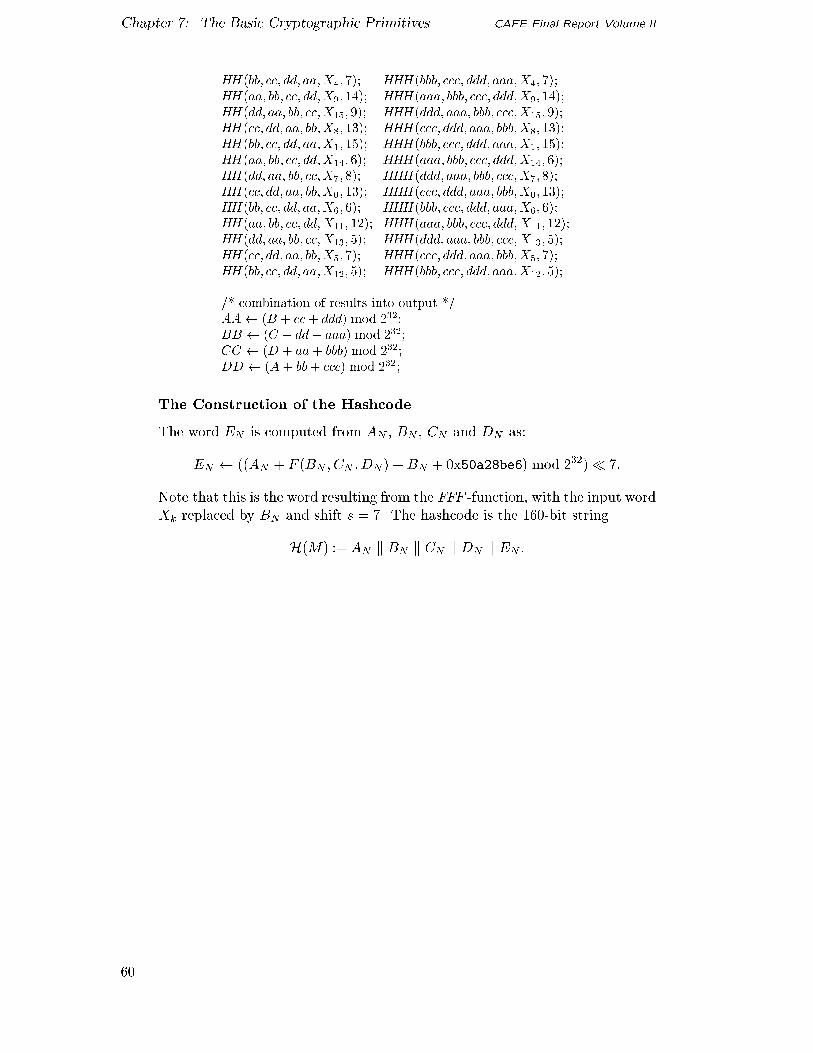

�� The Hash Function � � � � � � � � � � � � � � � � � � � � � � � � � ��

The � Protocols ��

�� Introduction � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

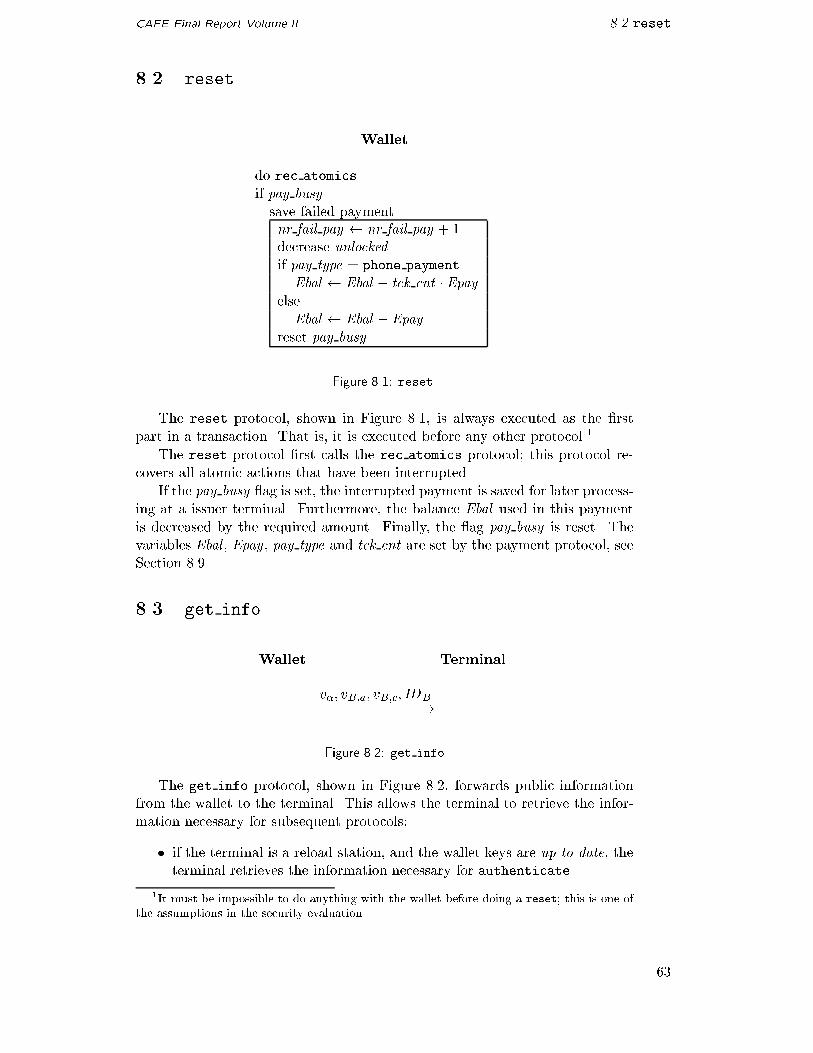

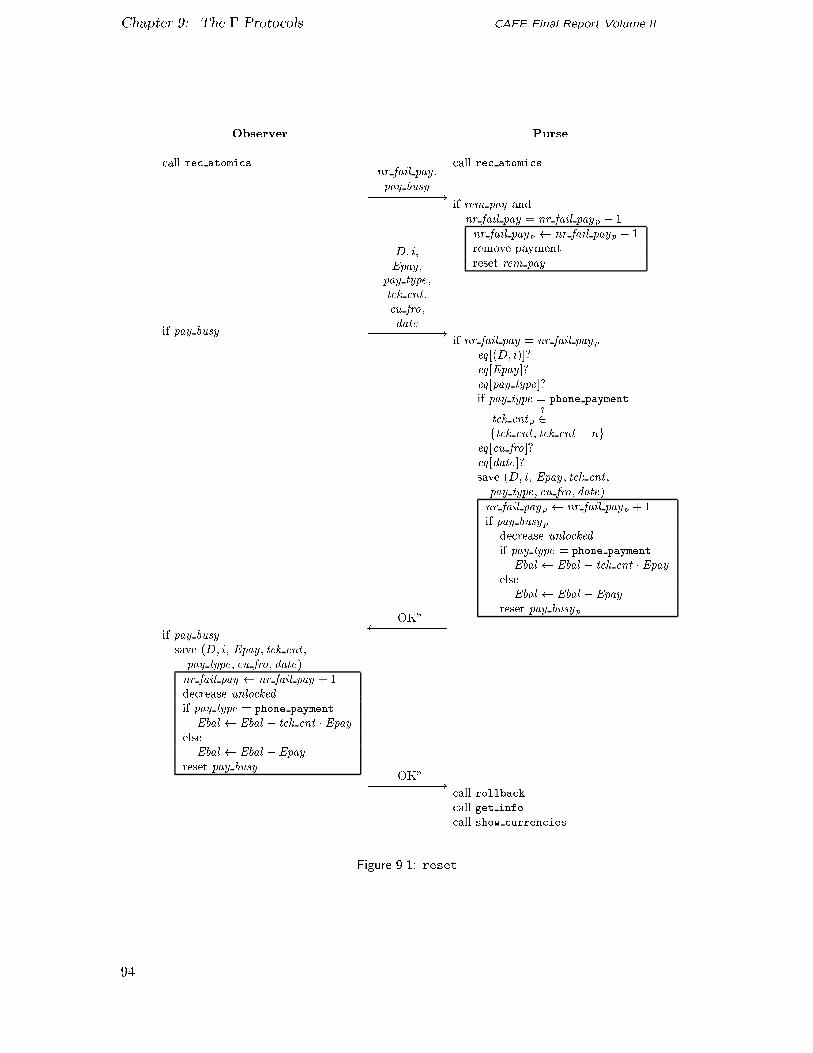

�� reset � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

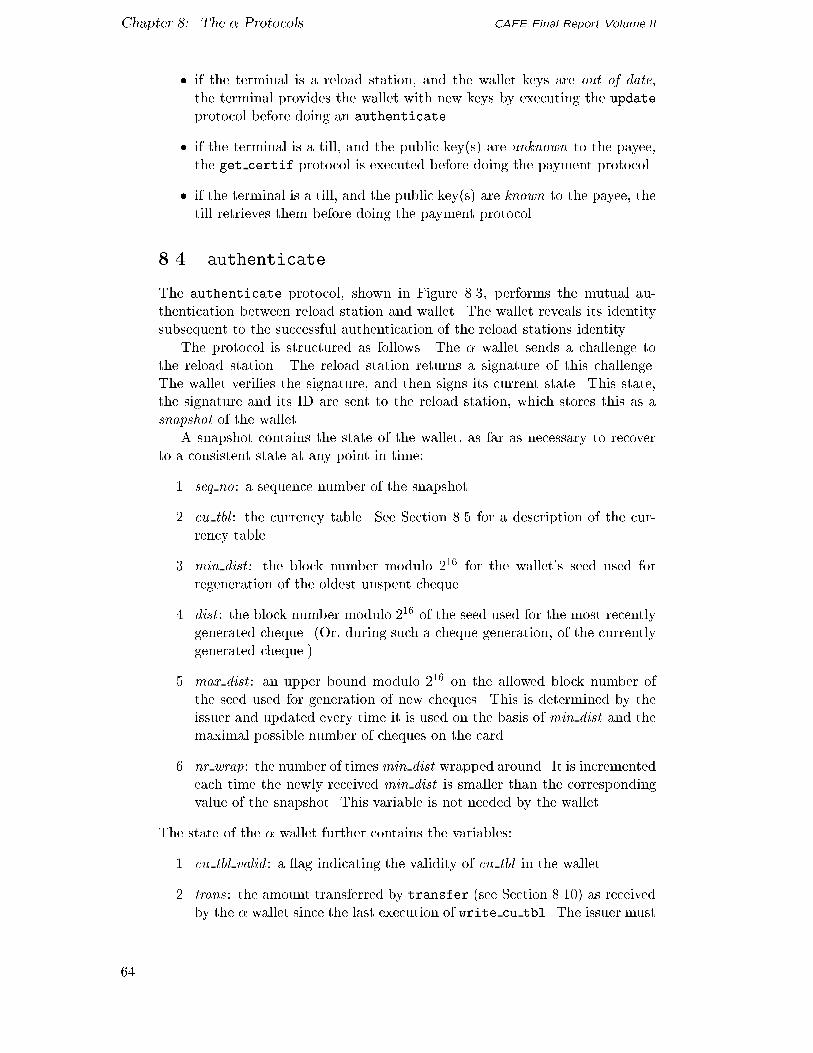

�� get info � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

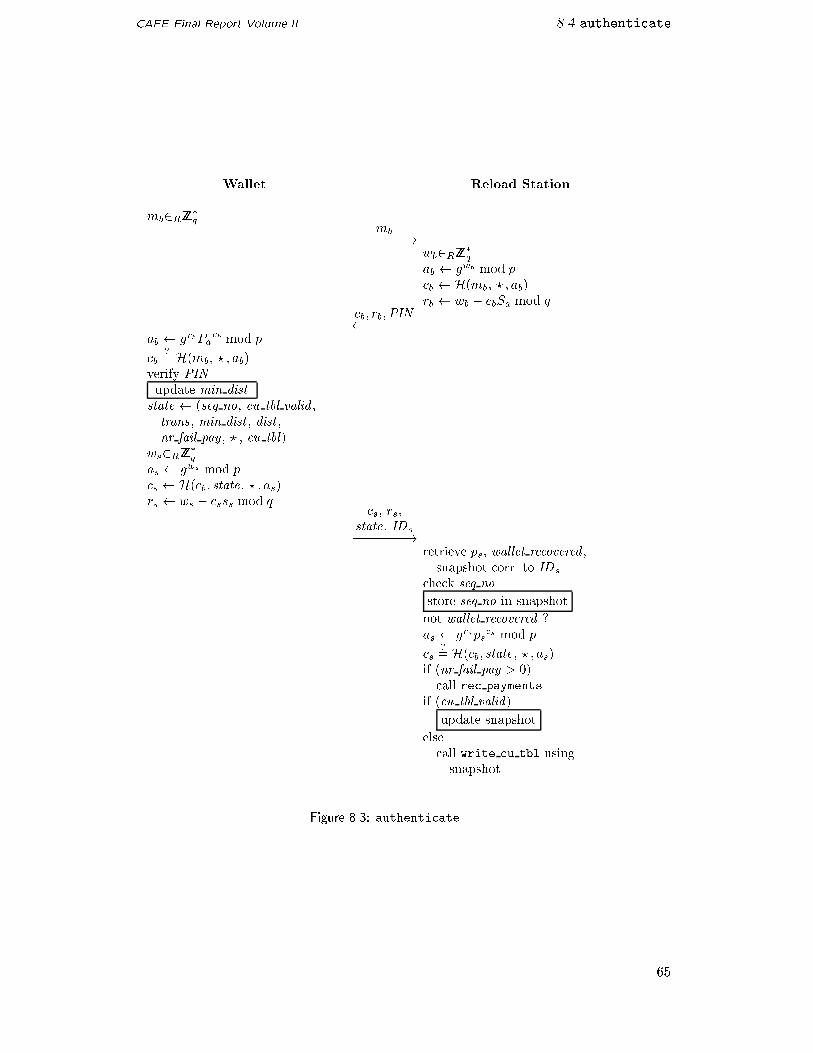

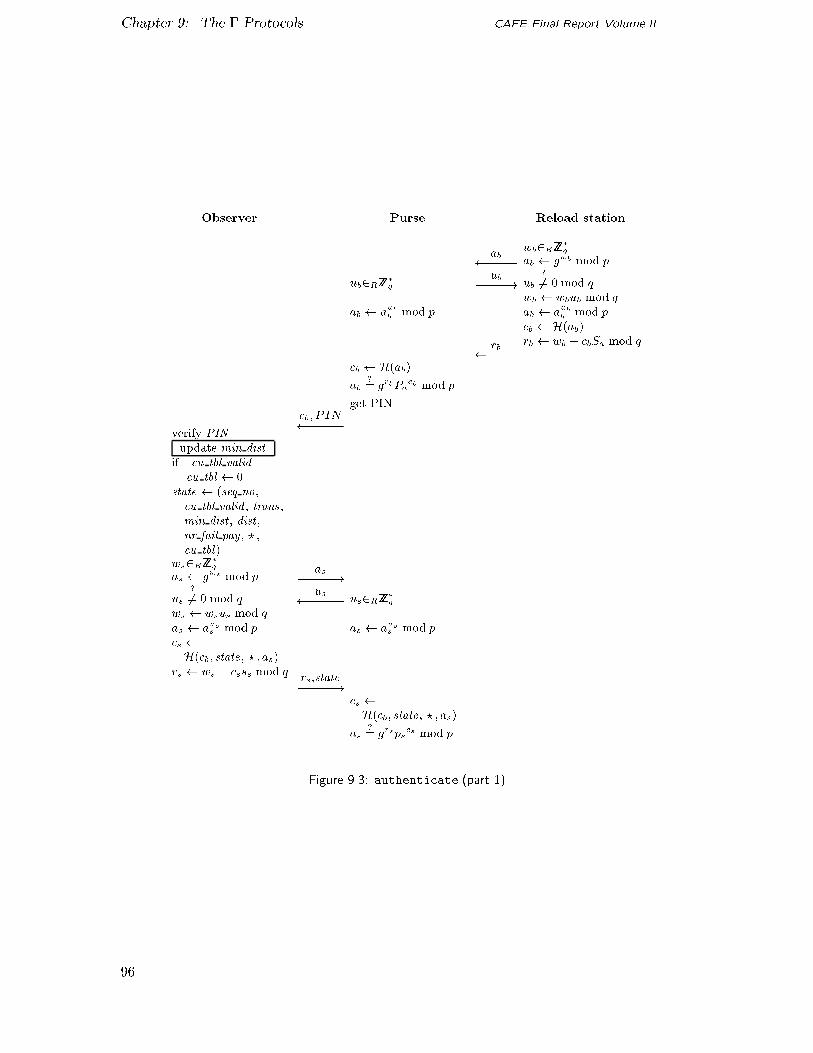

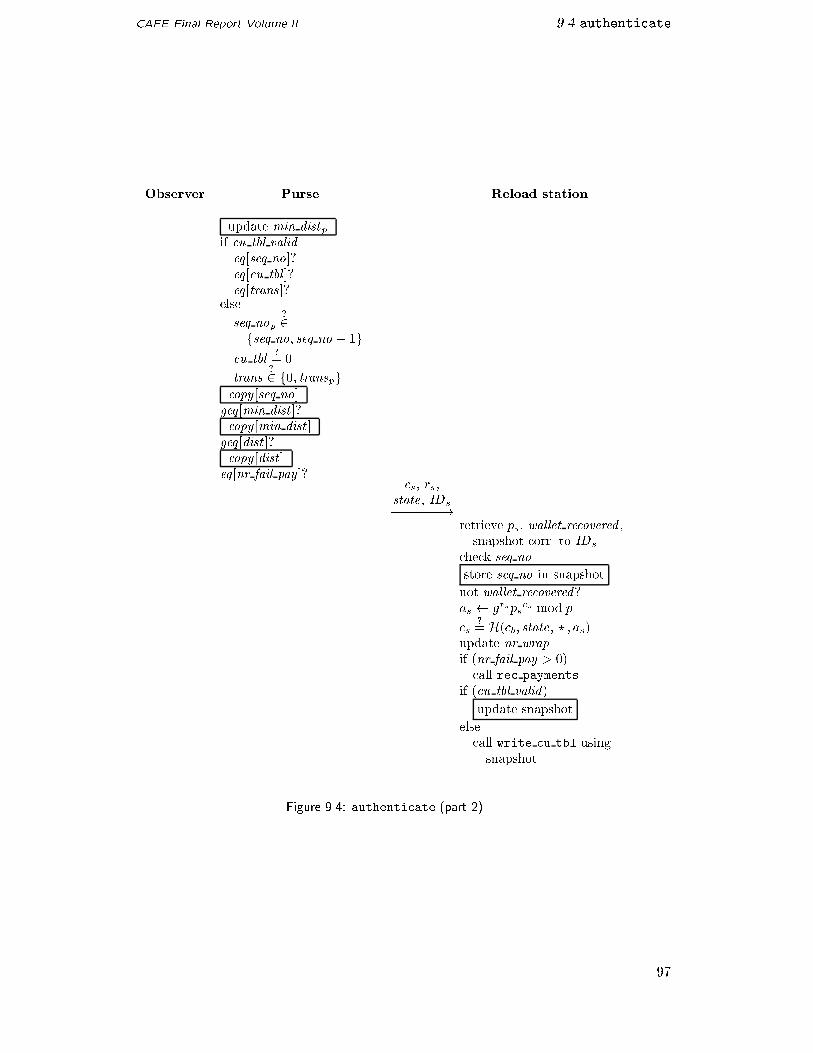

�� authenticate � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

�� write cu tbl � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

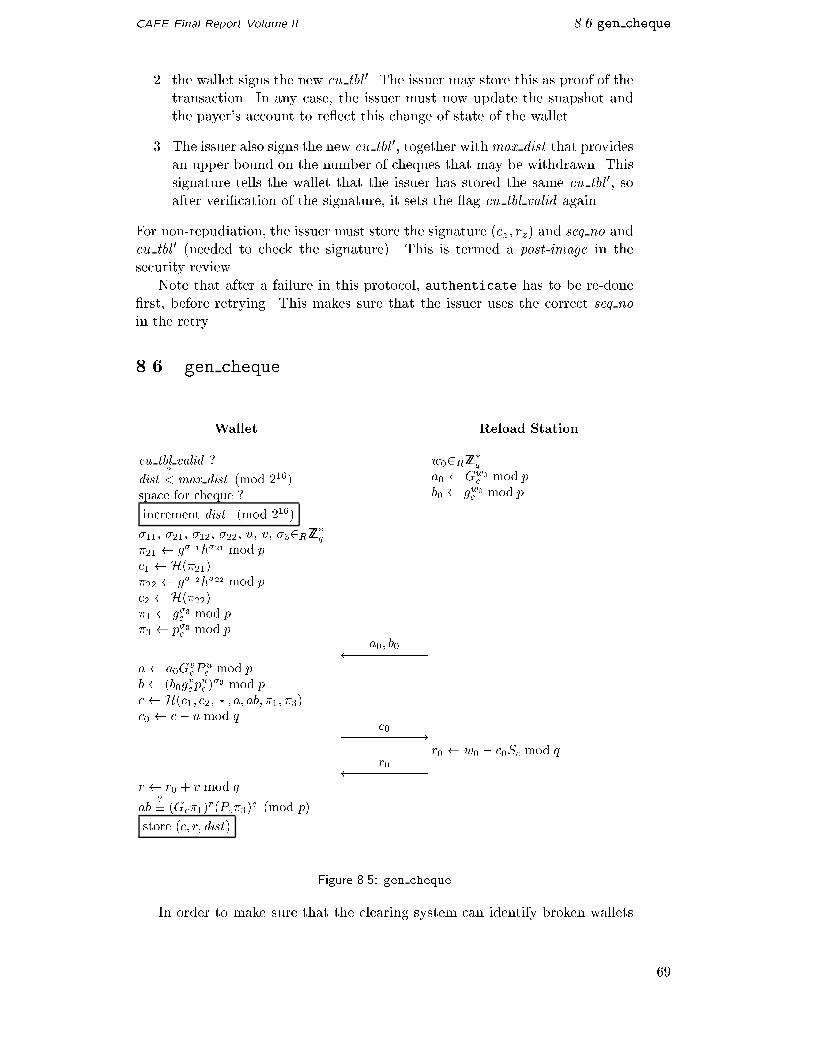

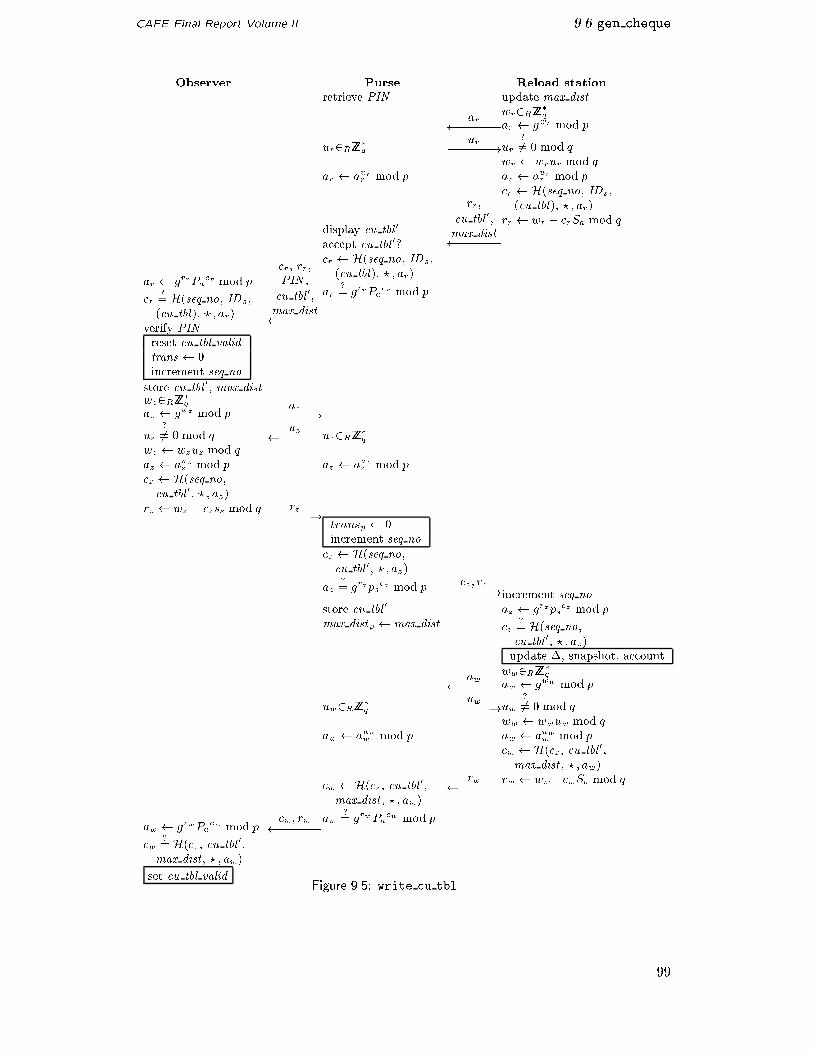

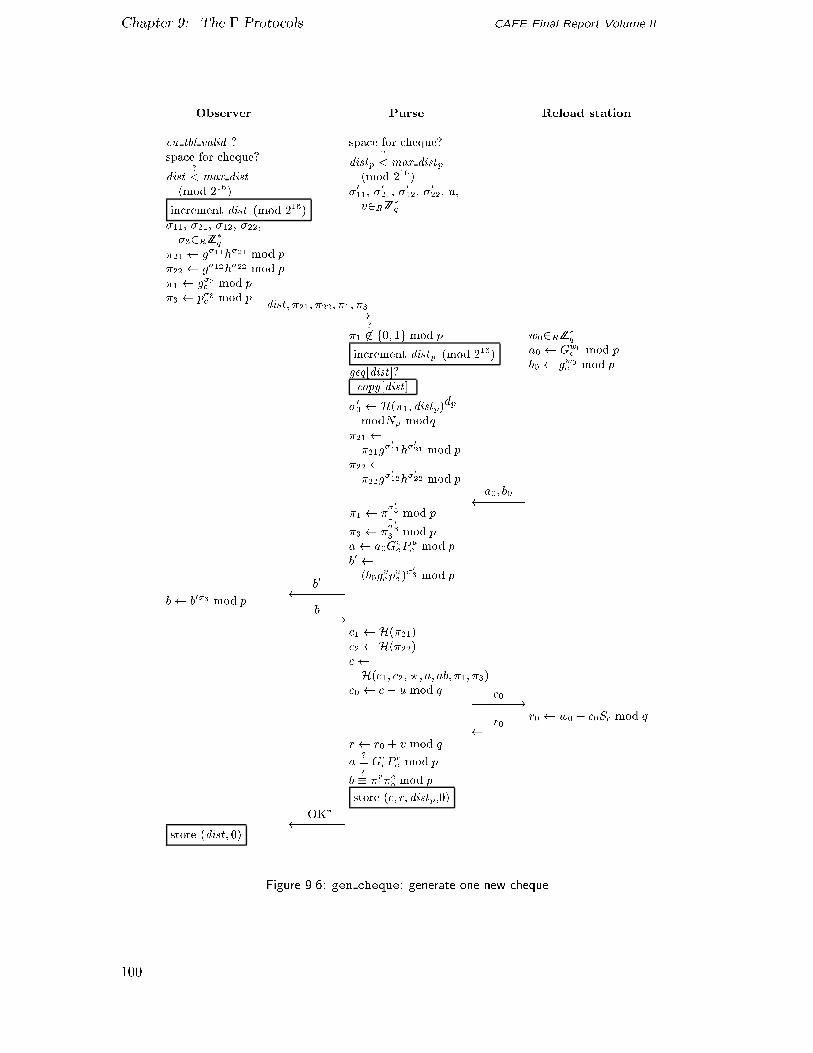

�� gen cheque � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

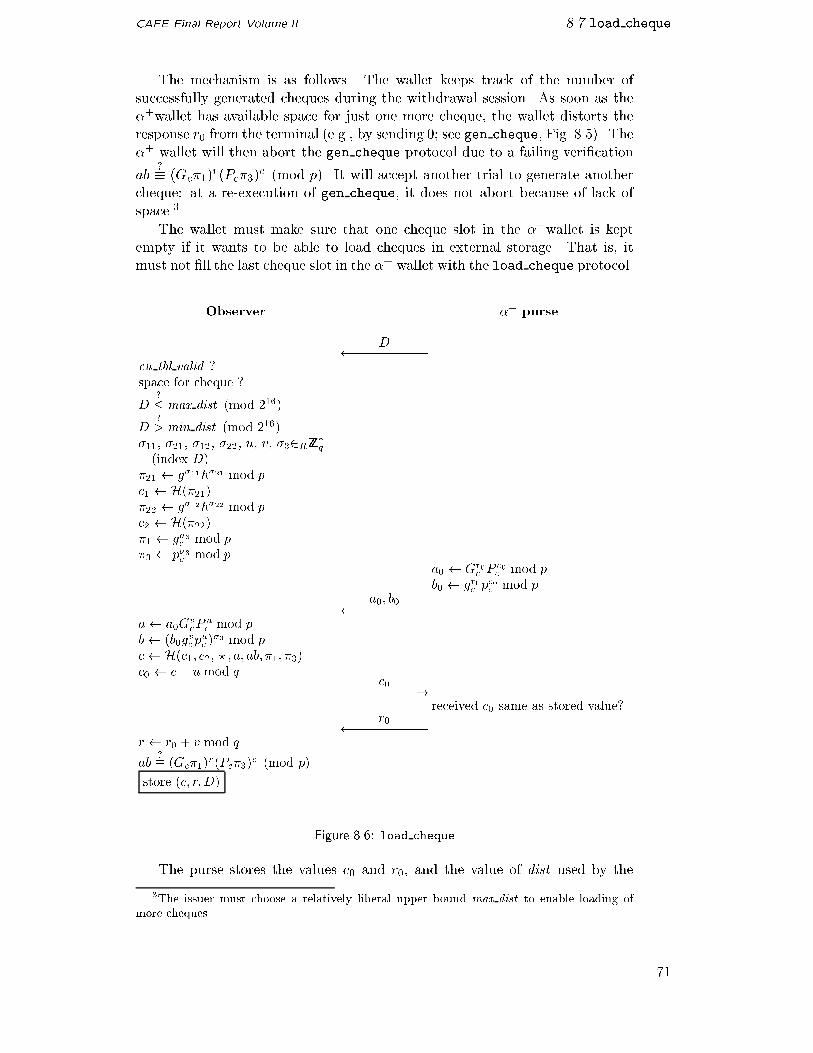

�� load cheque � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

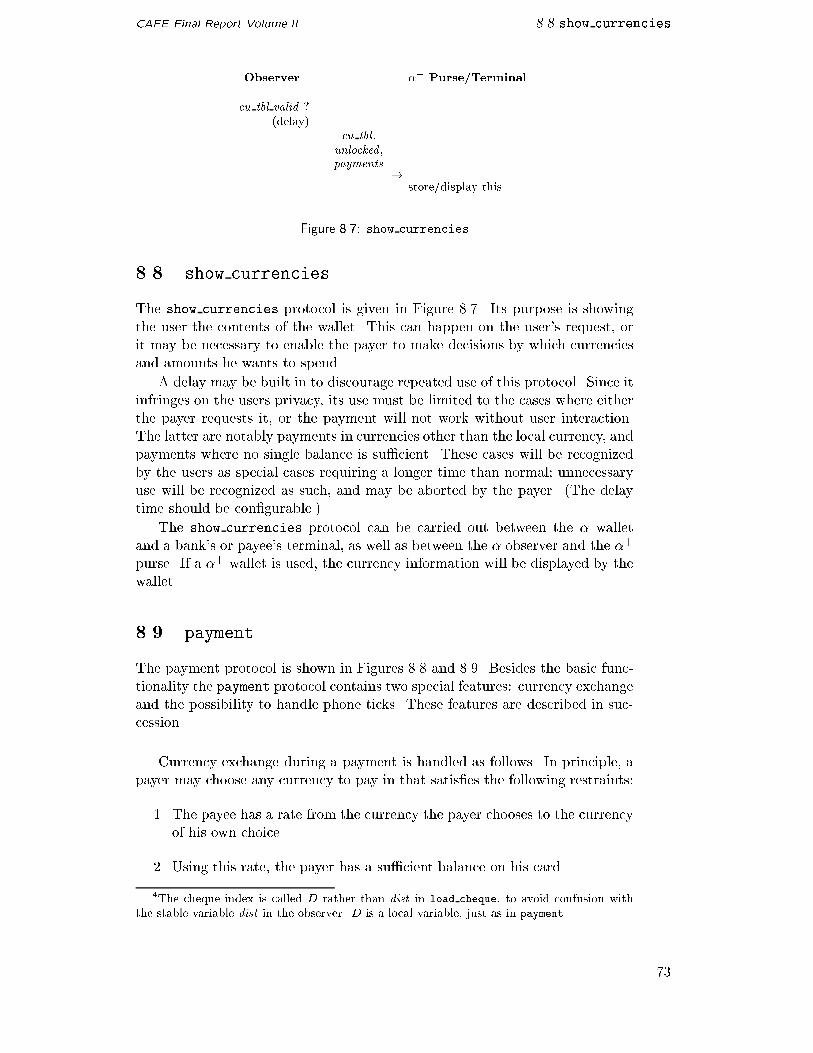

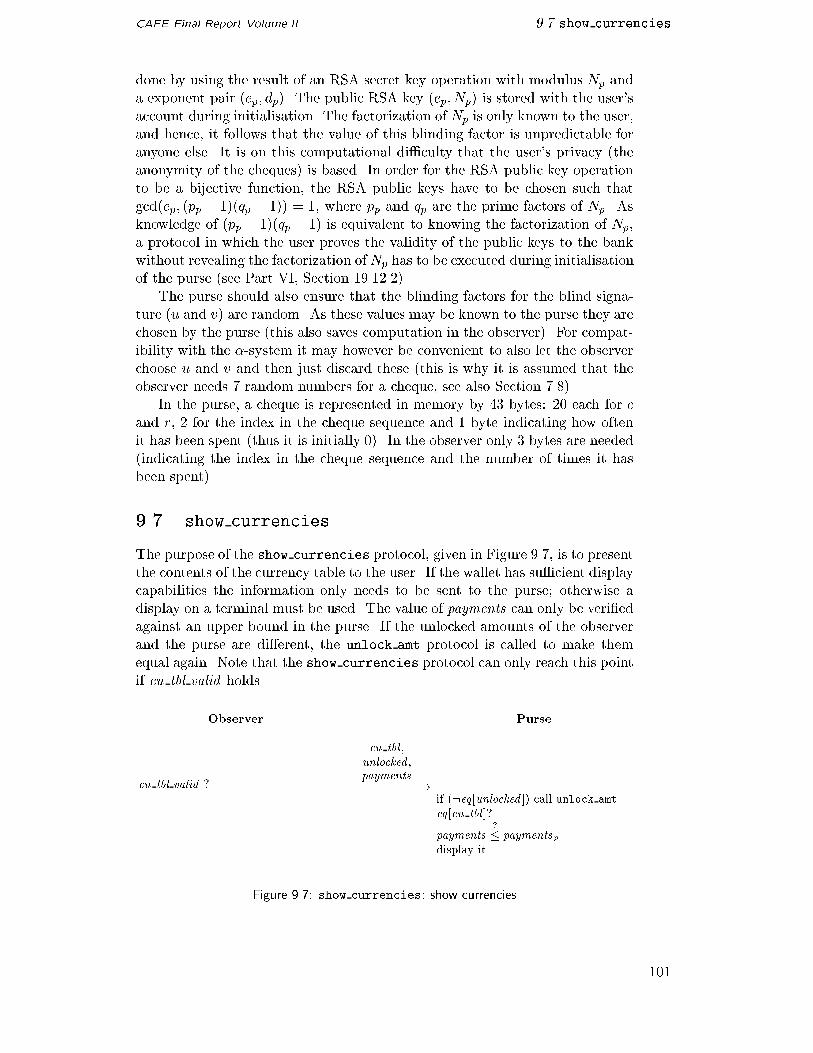

� show currencies � � � � � � � � � � � � � � � � � � � � � � � � � � ��

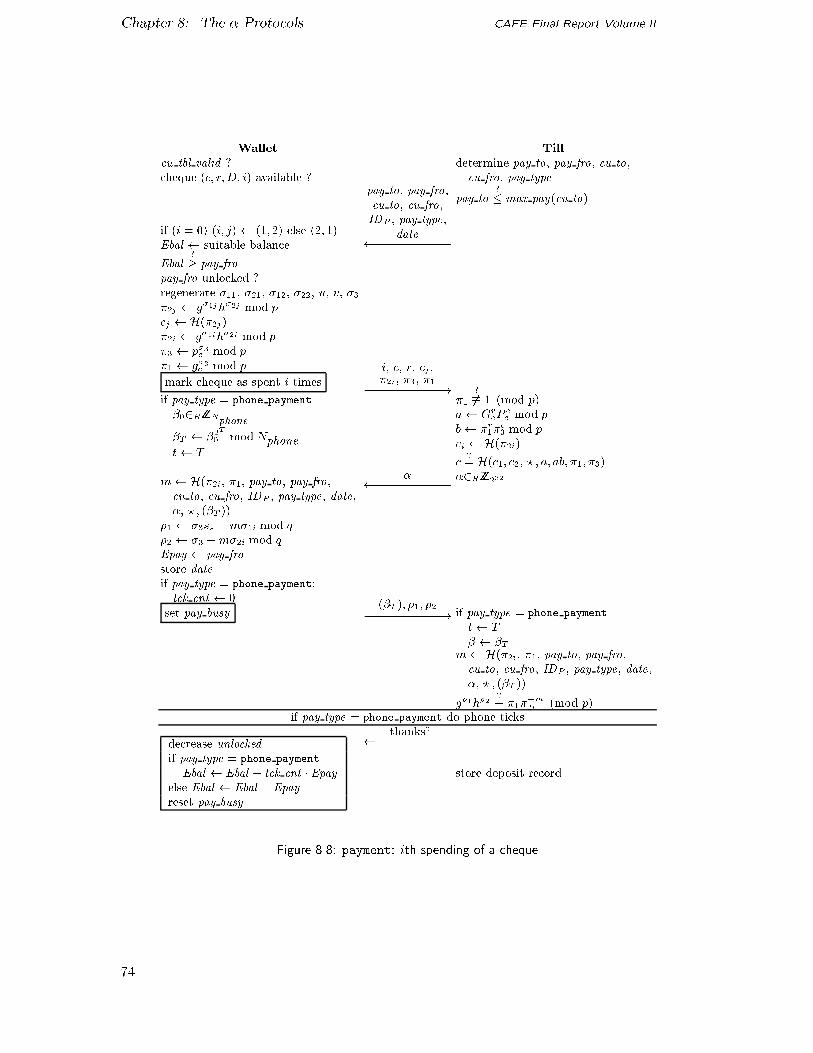

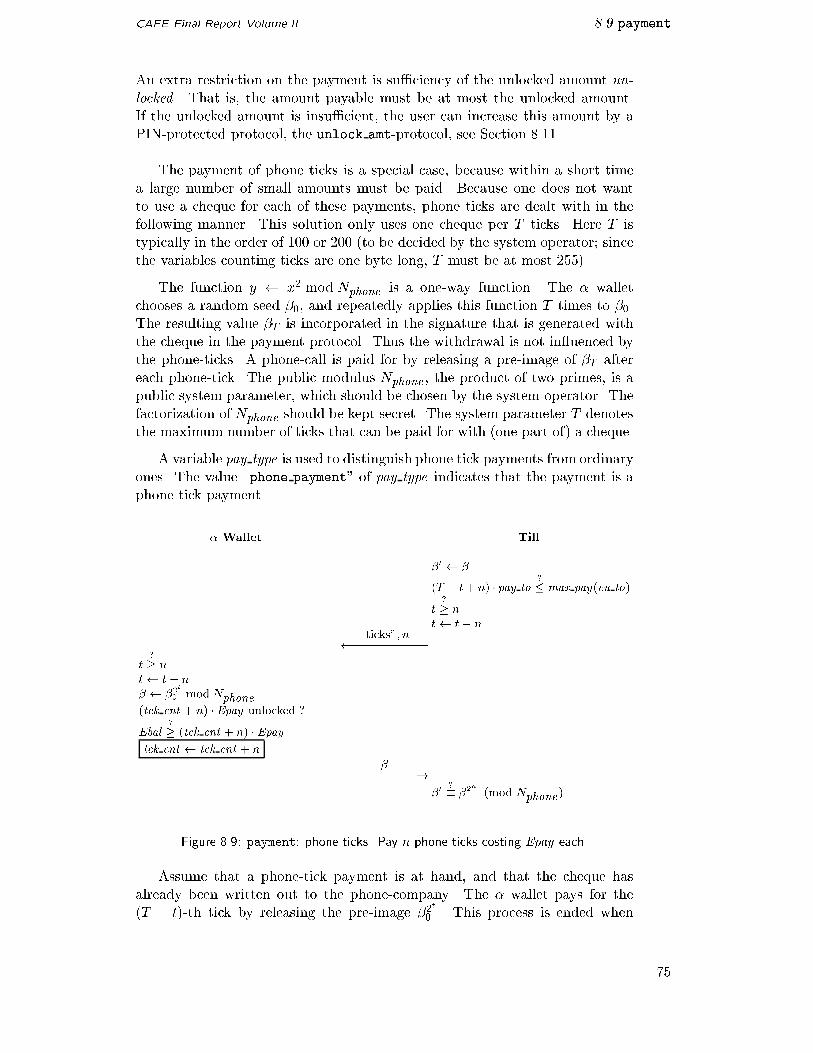

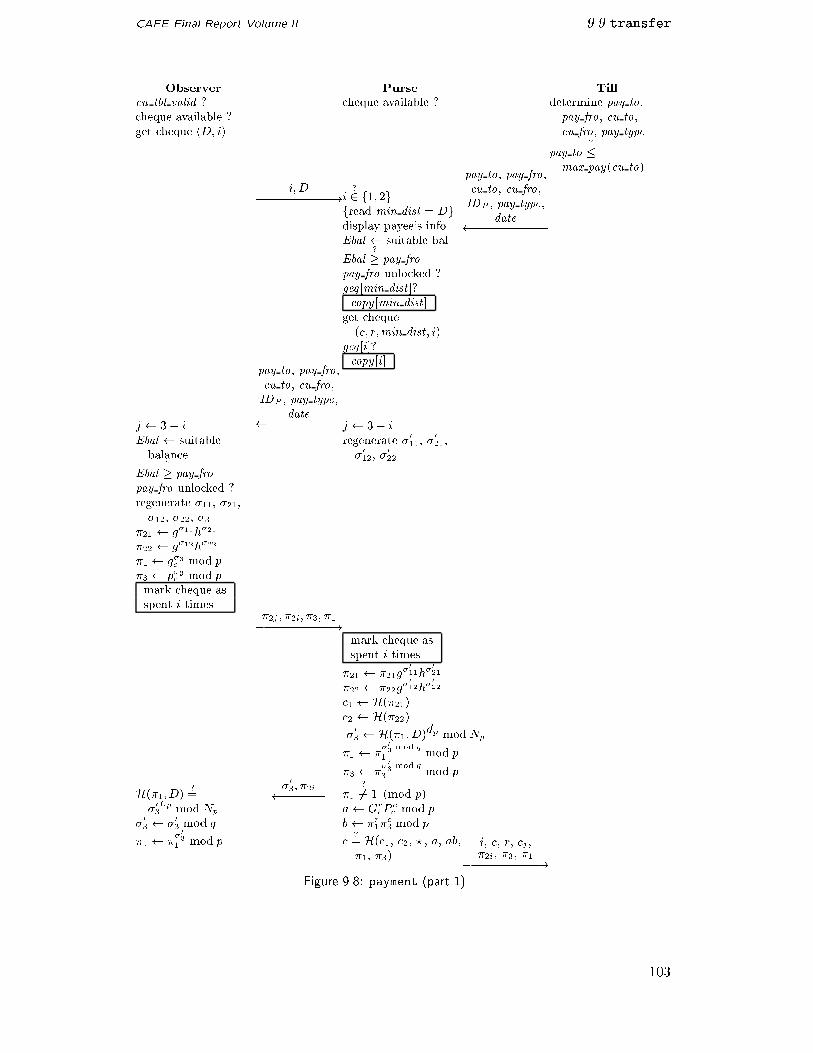

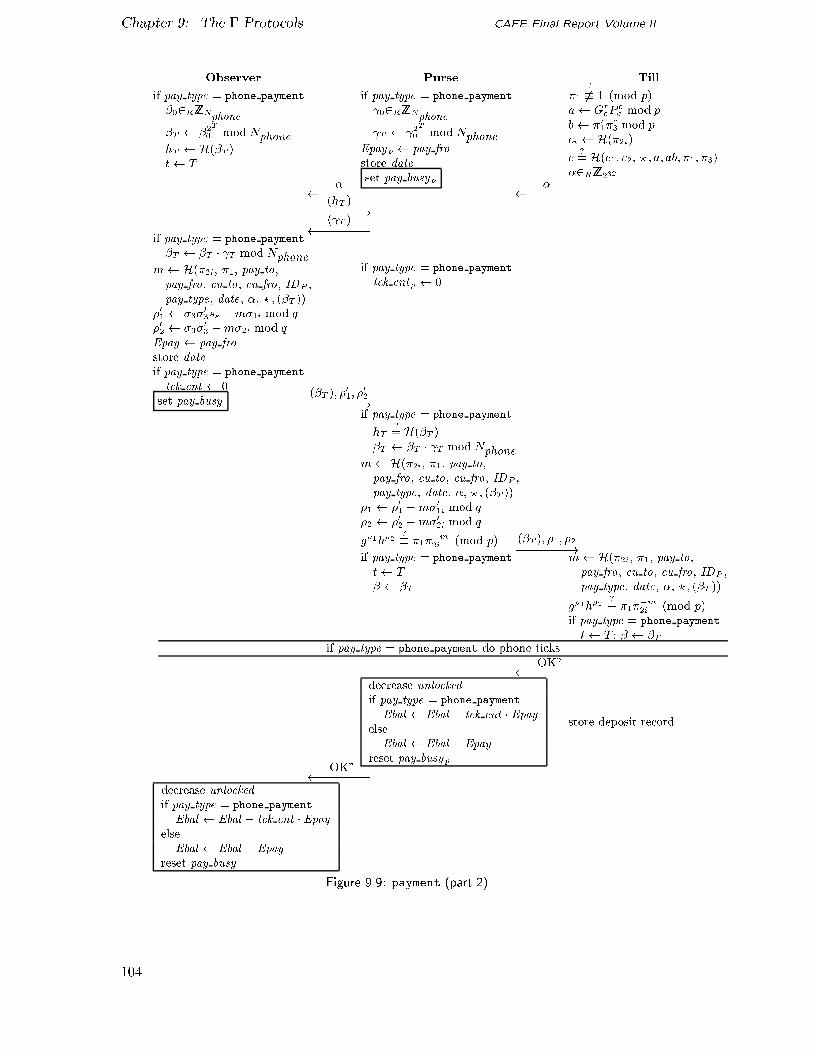

� payment � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

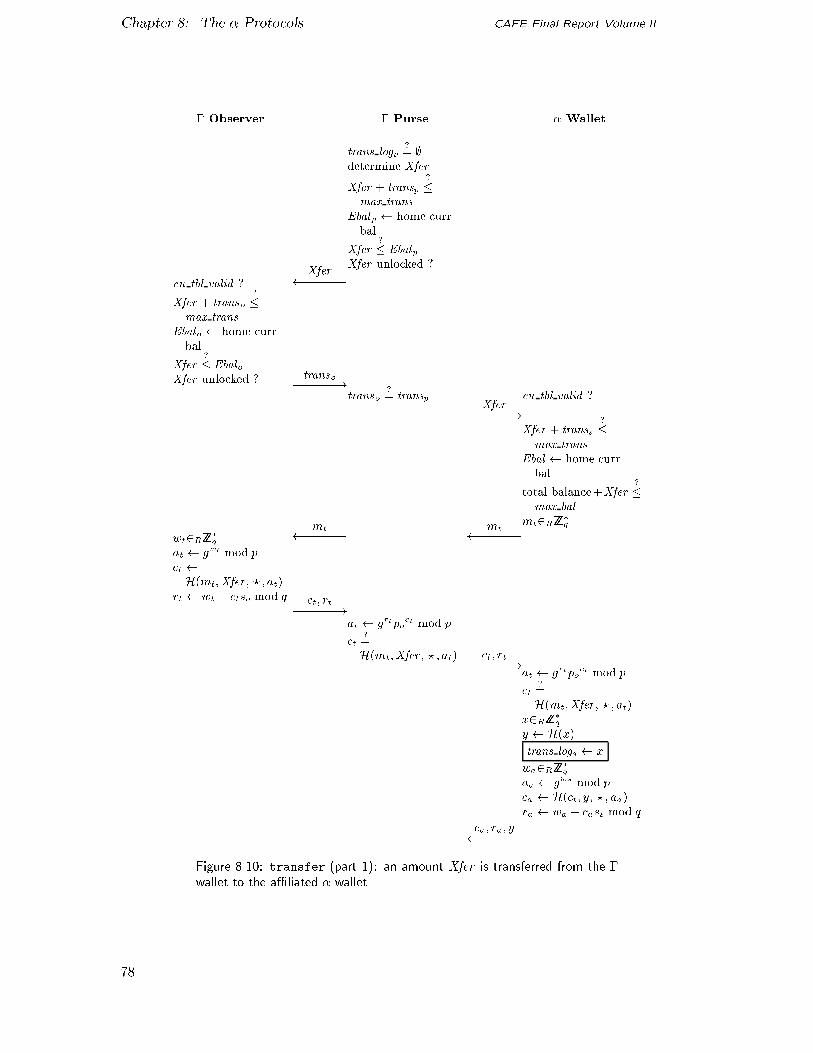

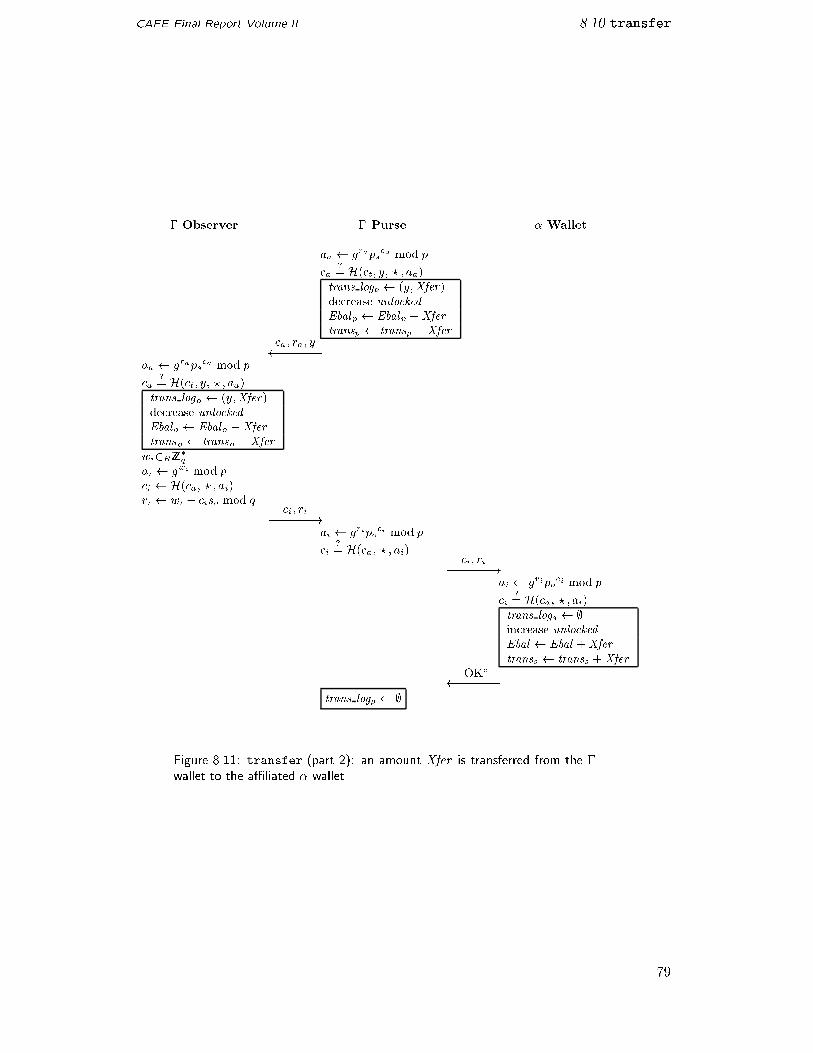

�� transfer � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

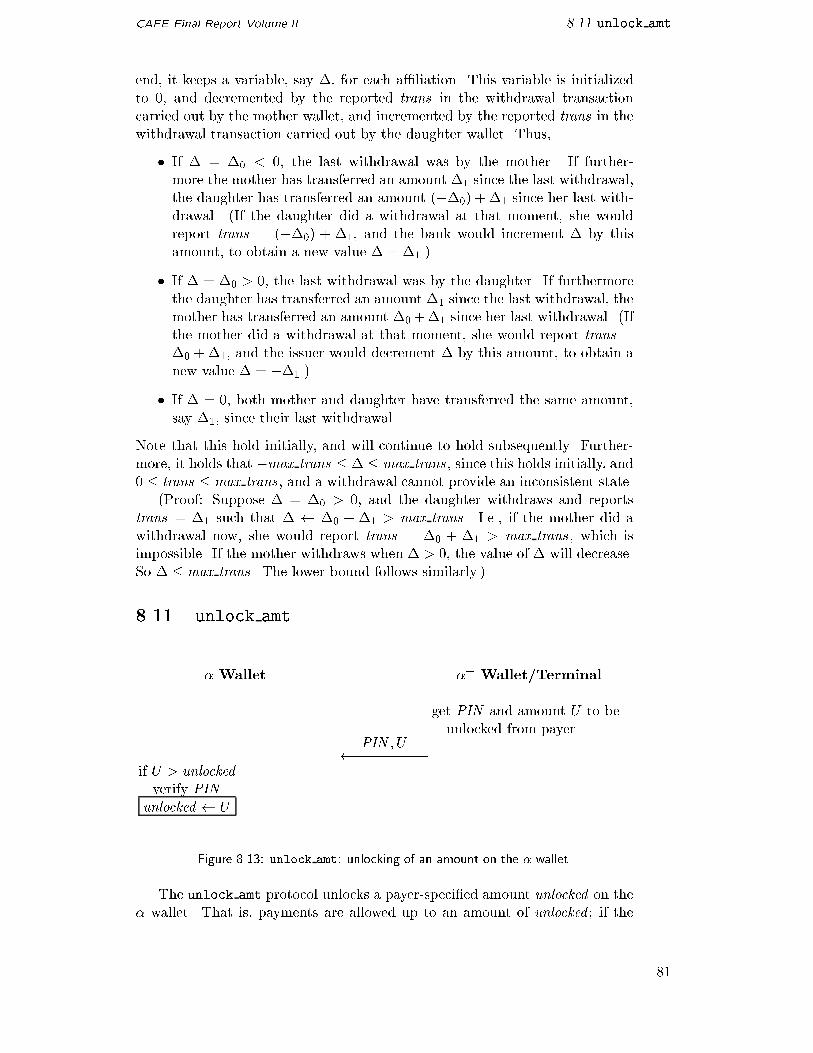

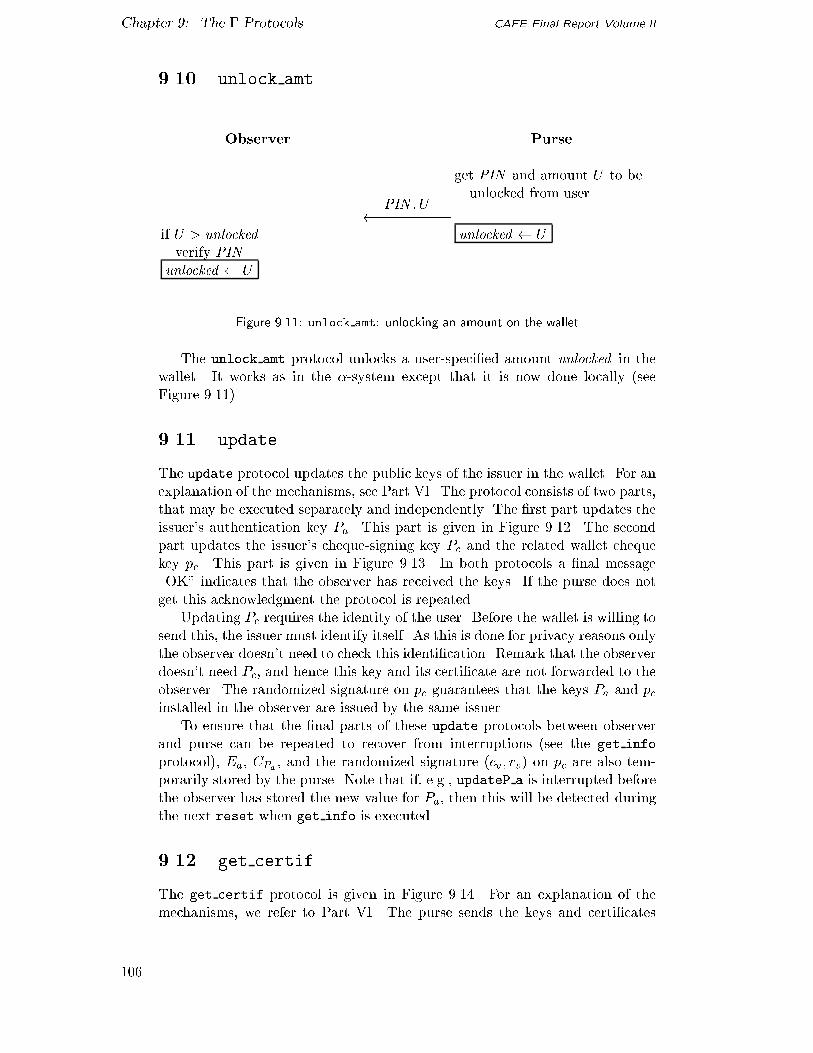

��� unlock amt � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

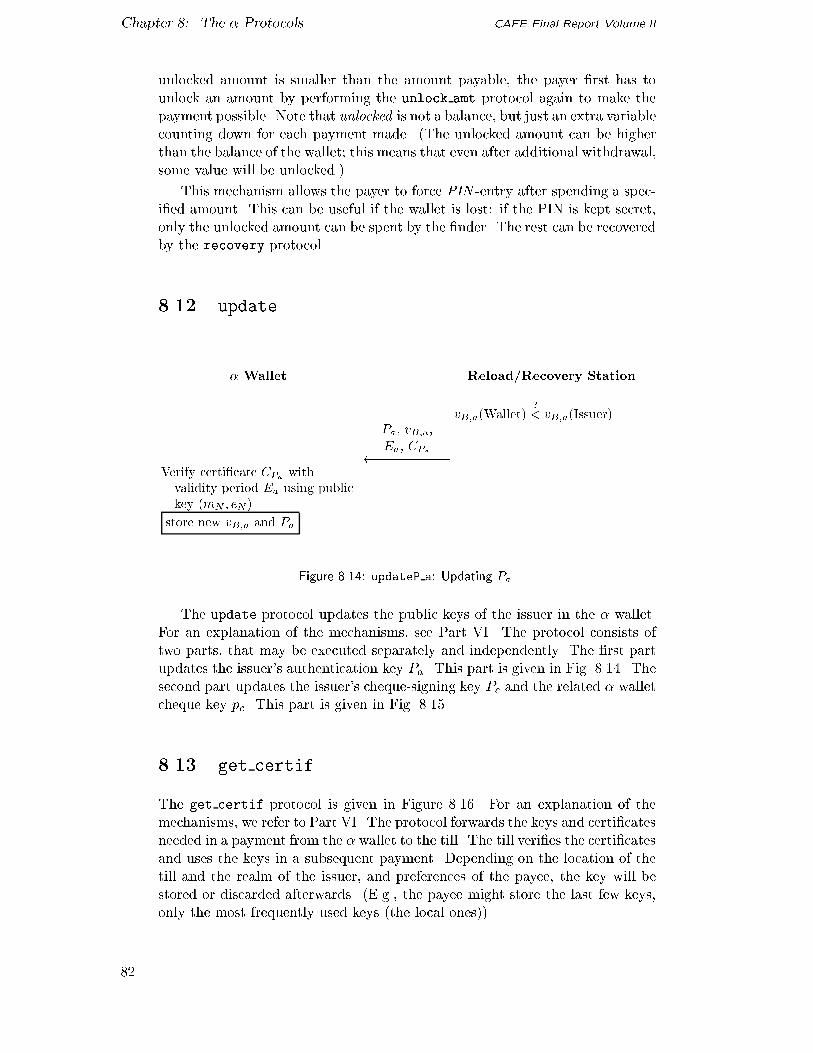

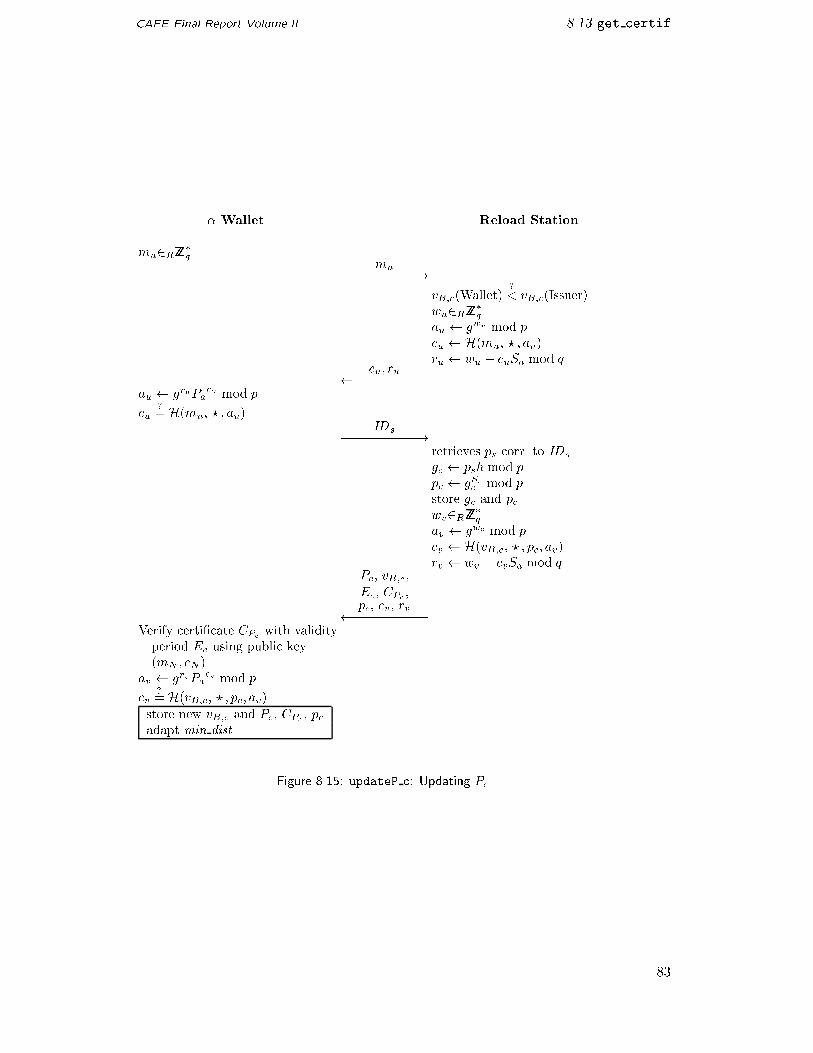

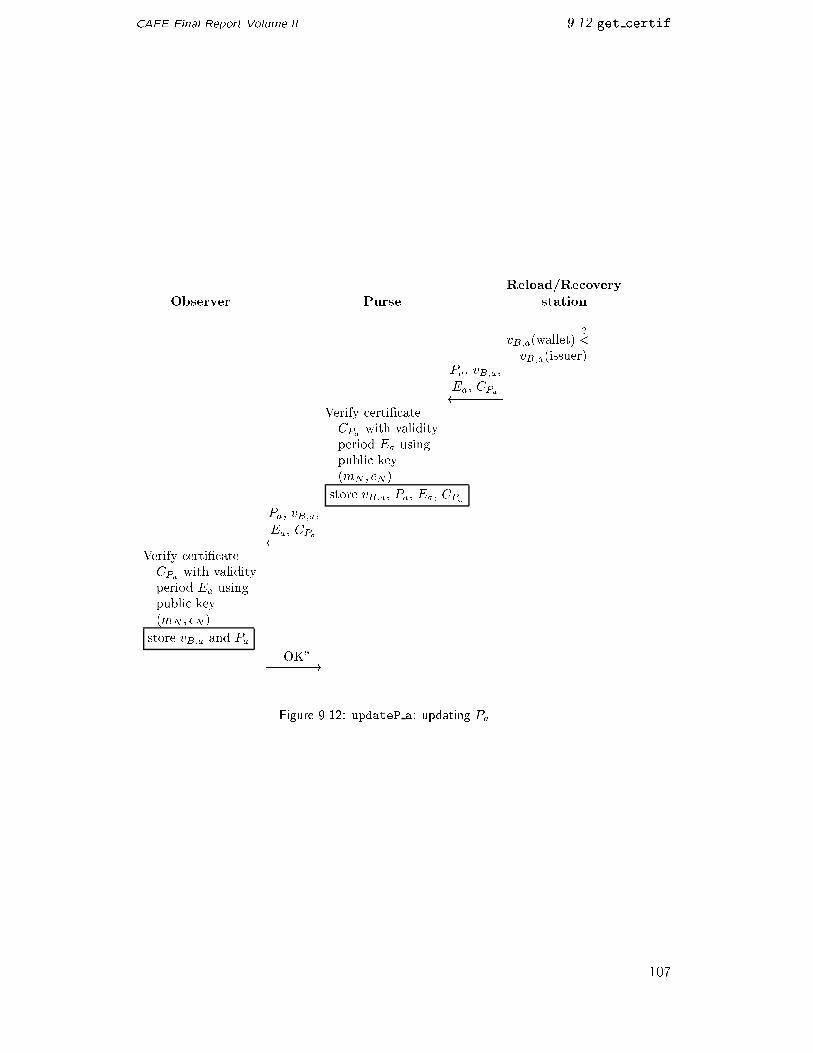

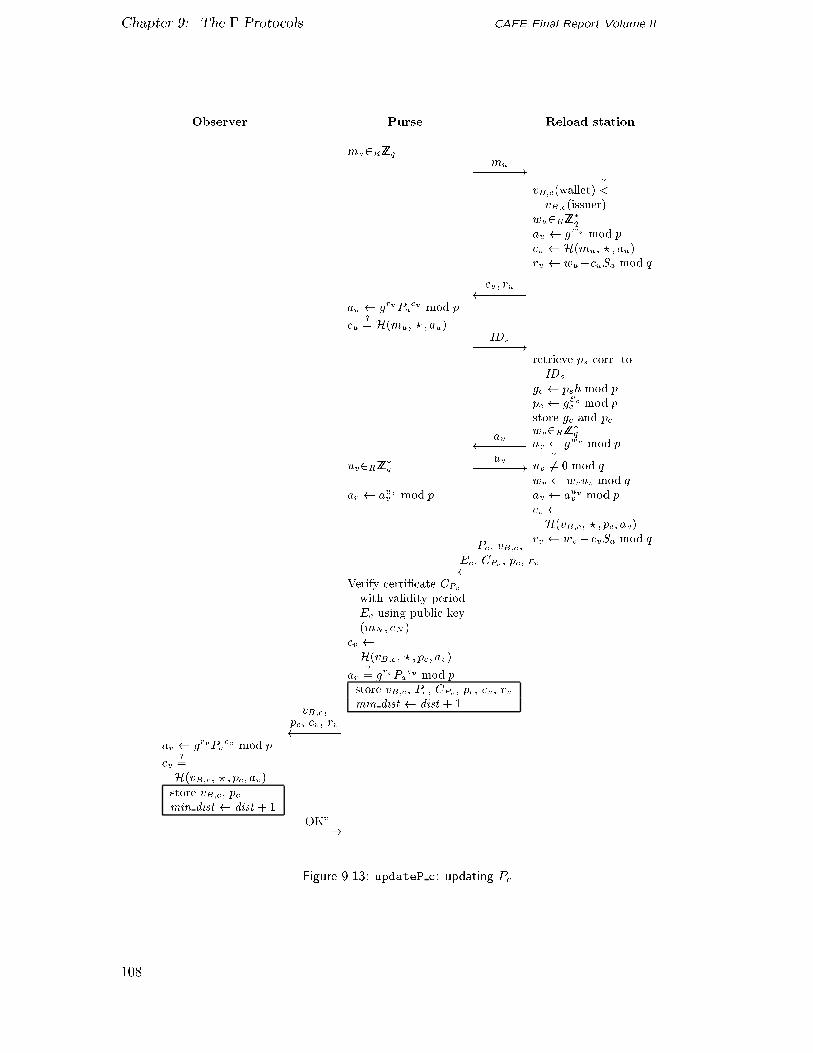

��� update � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� get certif � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

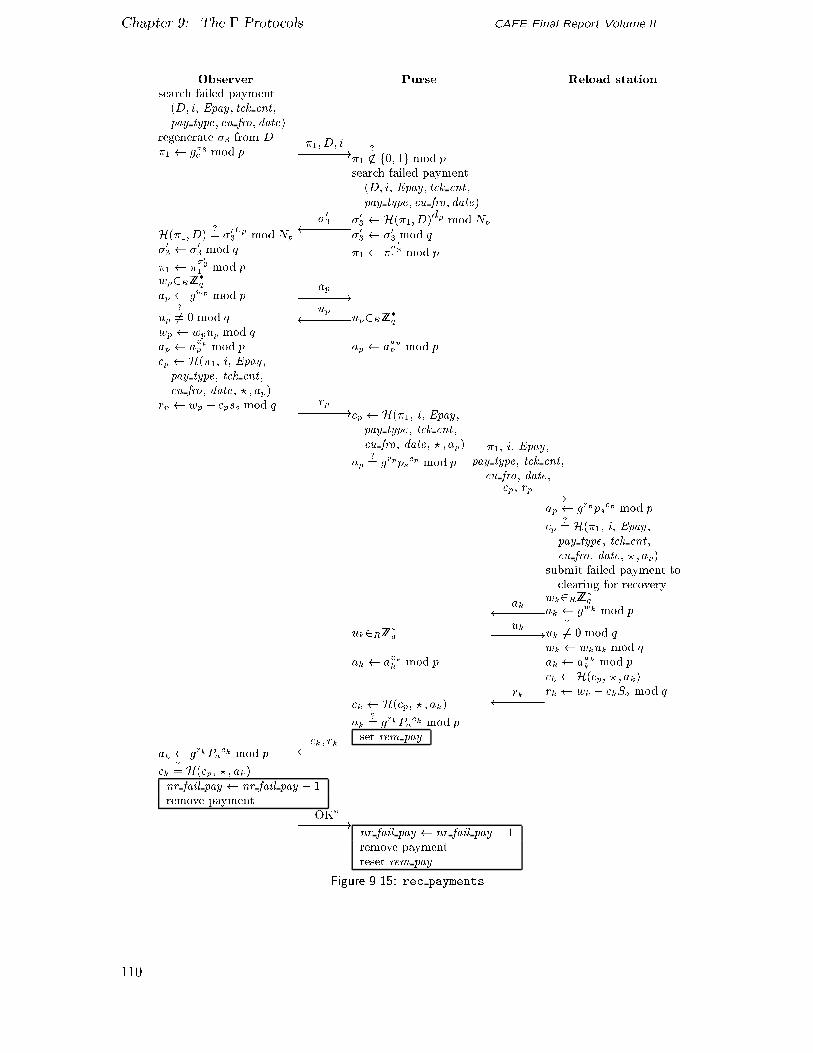

��� rec payments � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� recovery � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

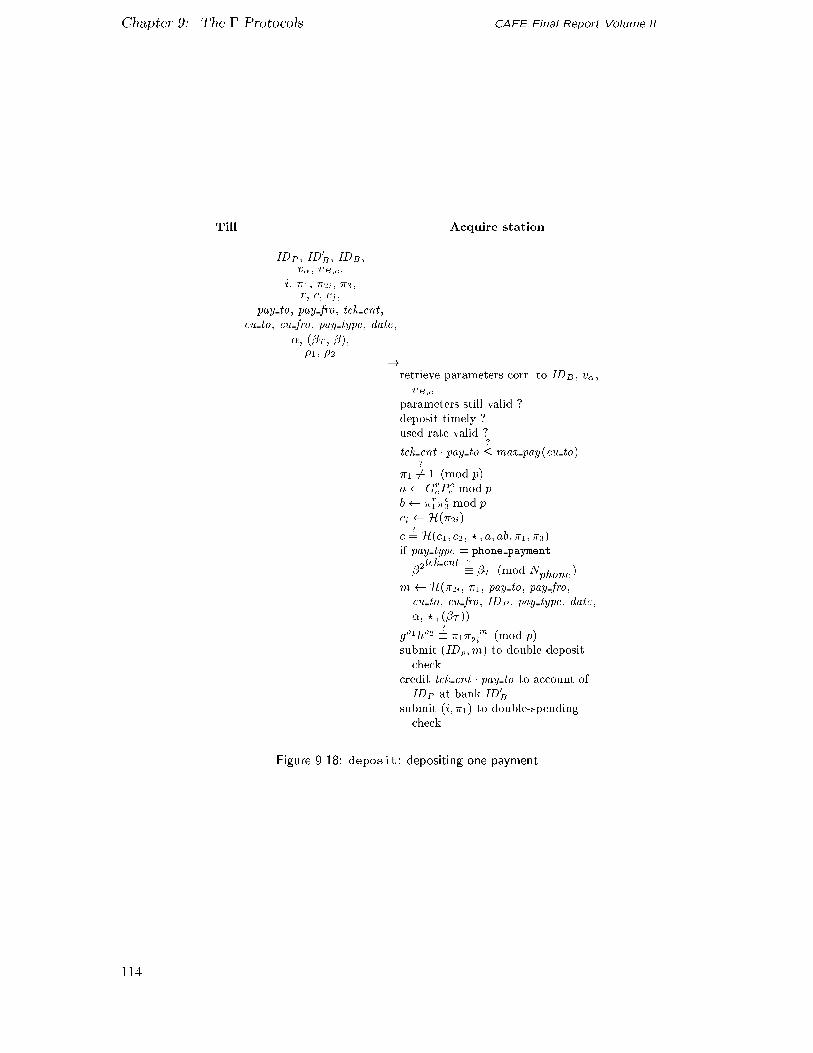

��� deposit � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

� The � Protocols ��

�� Introduction � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� reset � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� get info � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� authenticate � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� write cu tbl � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� gen cheque � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� show currencies � � � � � � � � � � � � � � � � � � � � � � � � � � � �

� payment � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

iv

CAFE Final Report Volume II Contents

� transfer � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� unlock amt � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� update � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� get certif � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� rec payments � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� recovery � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

��� deposit � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

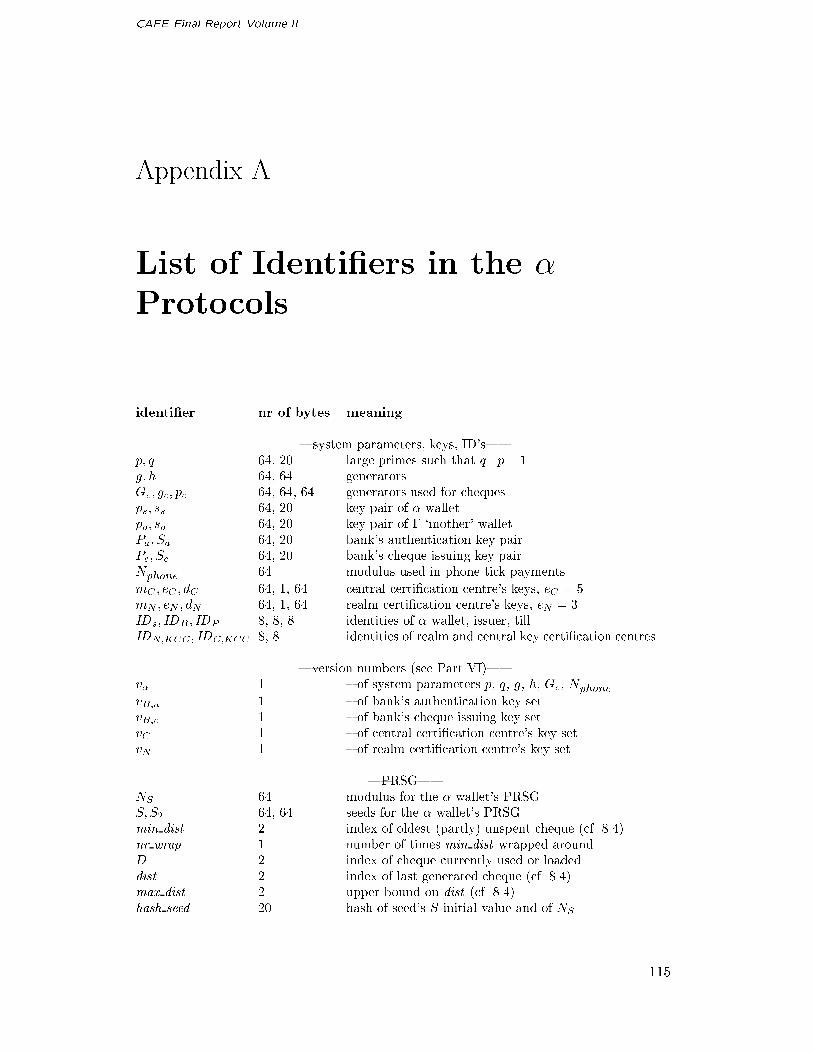

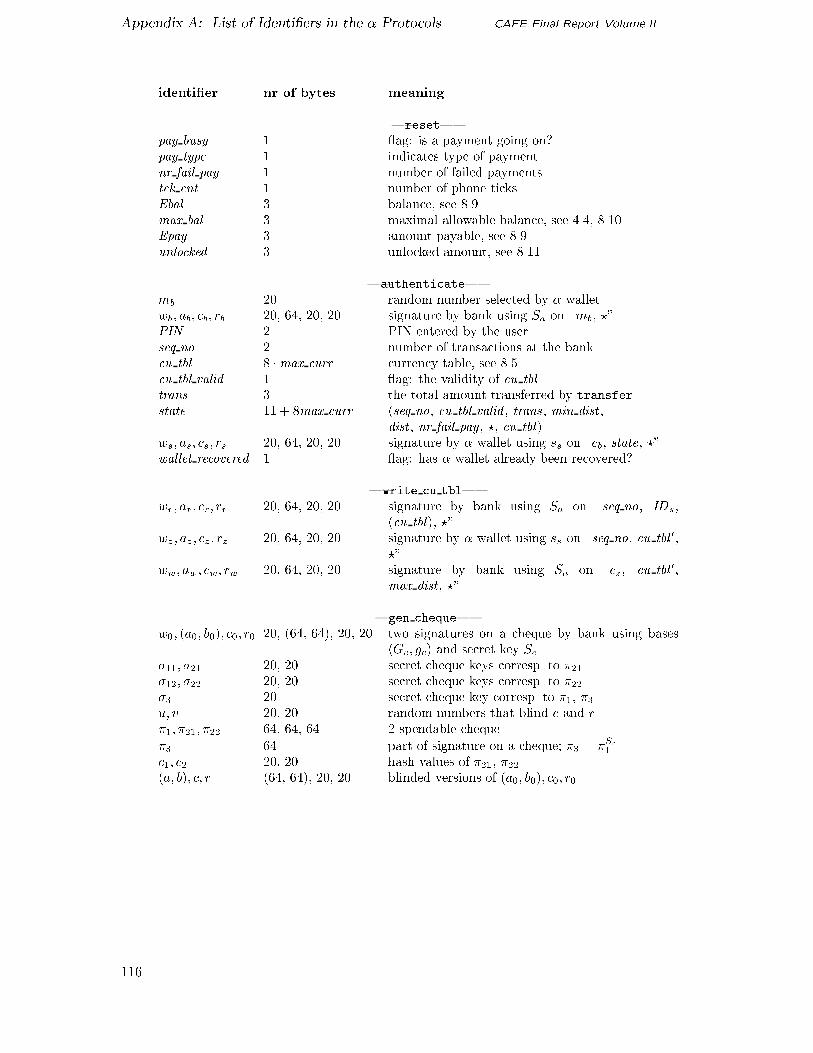

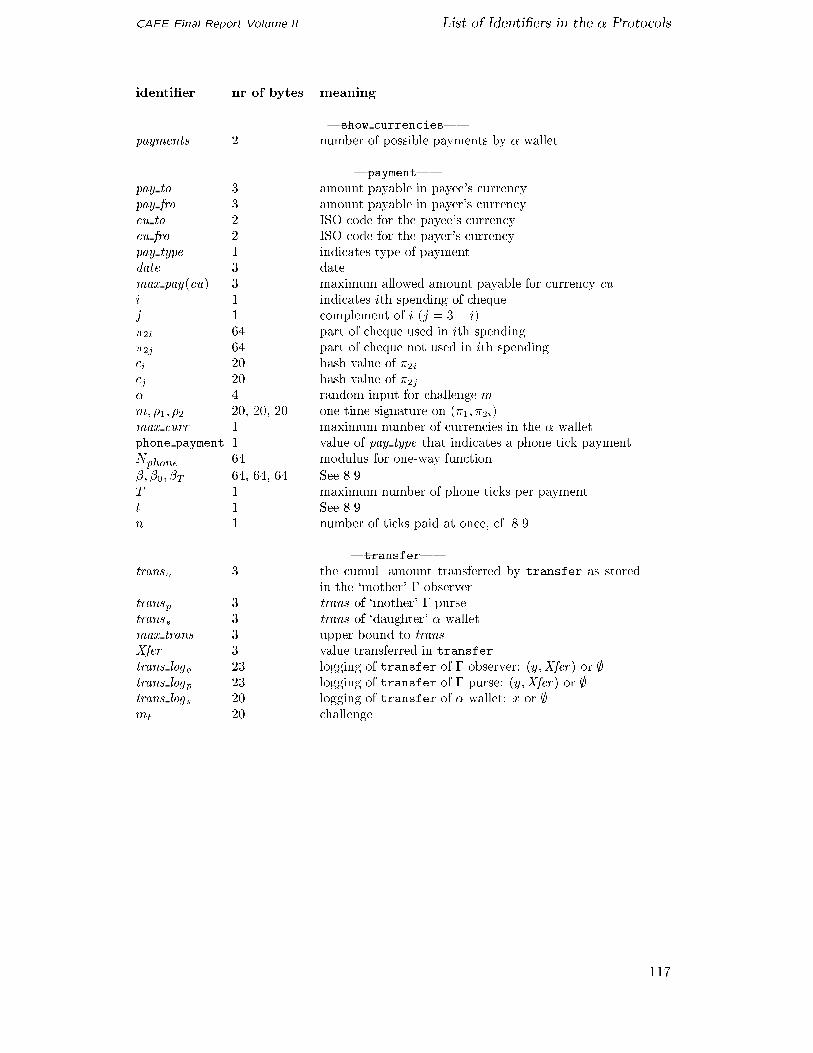

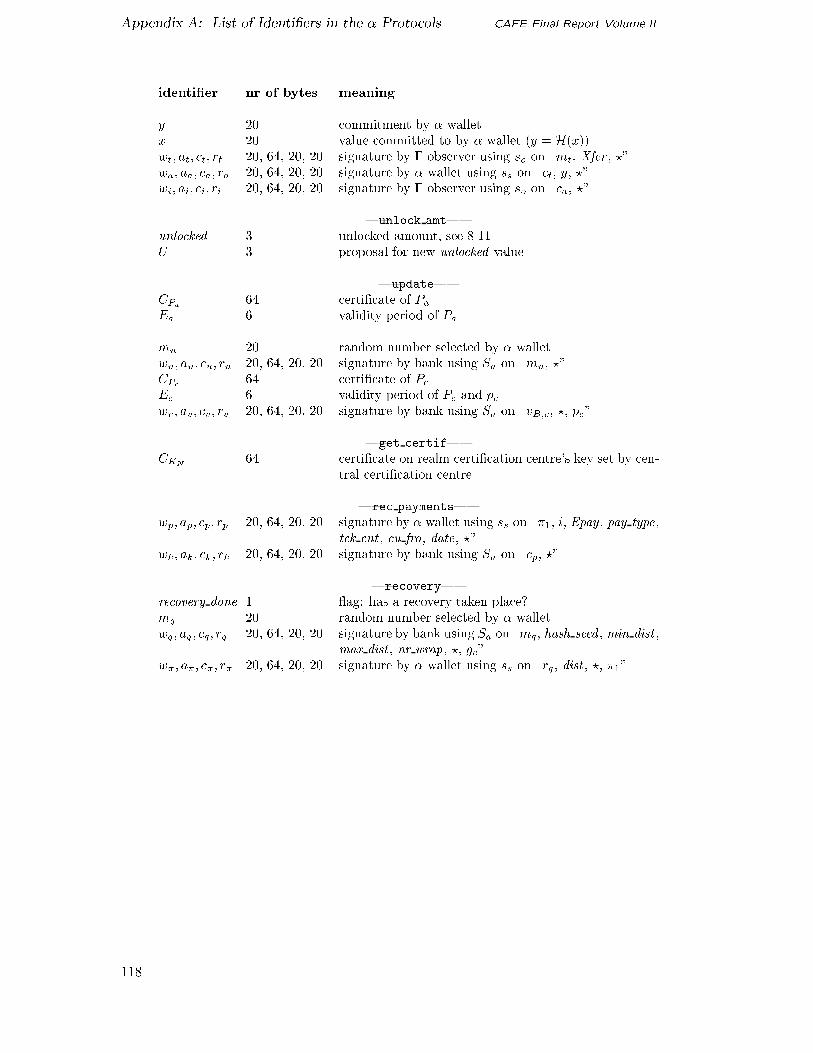

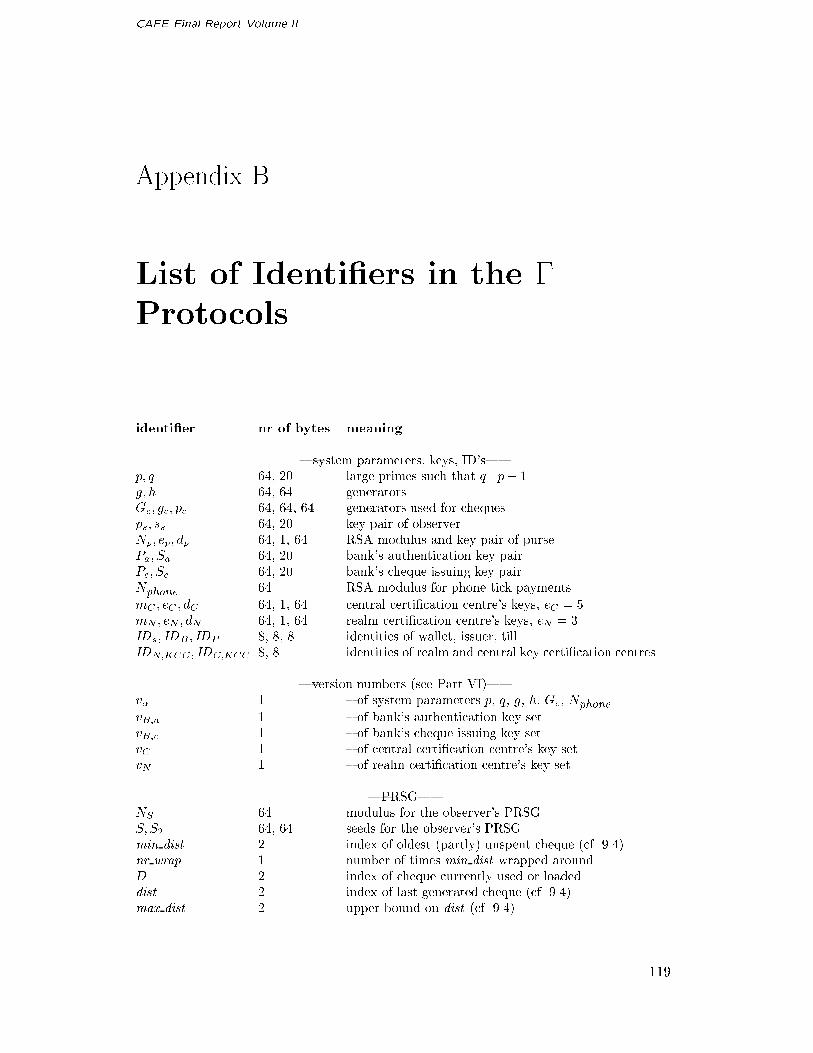

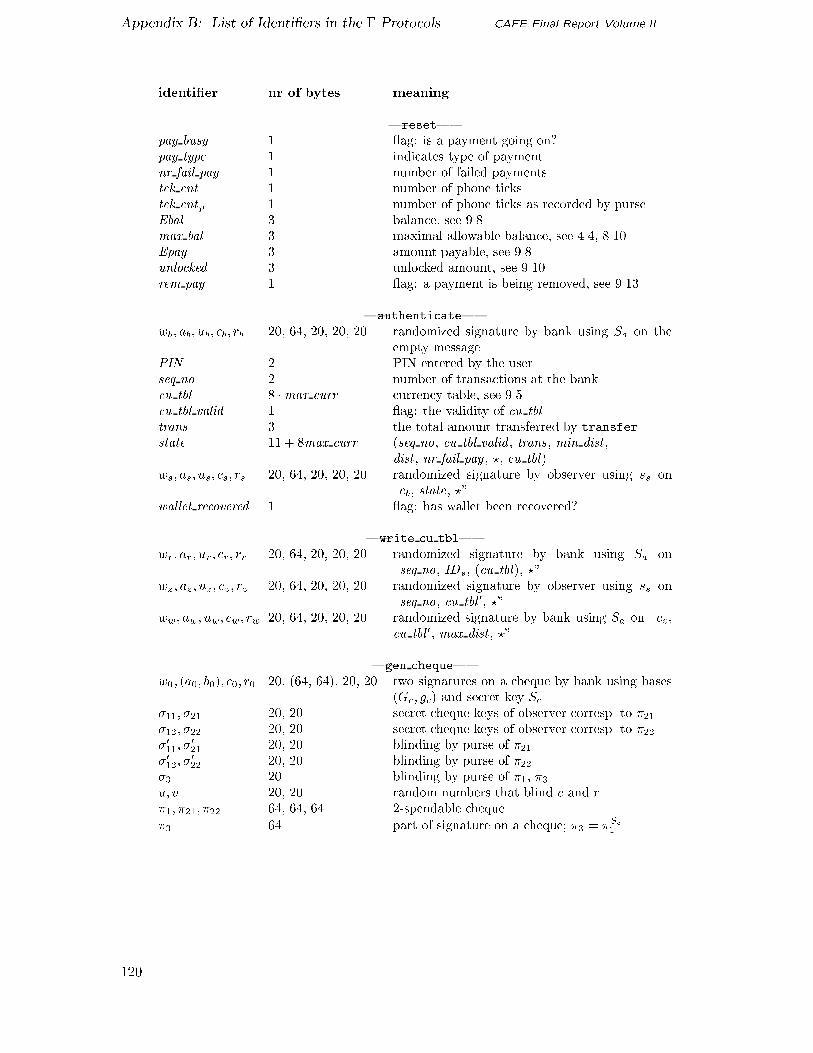

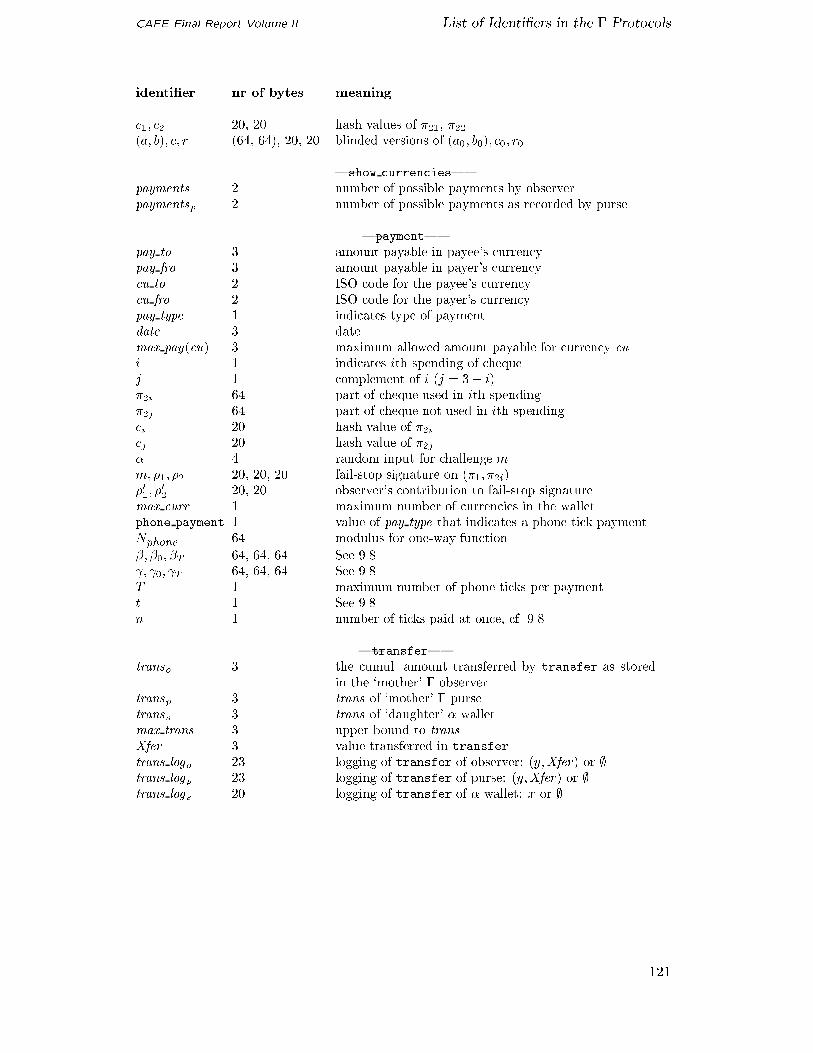

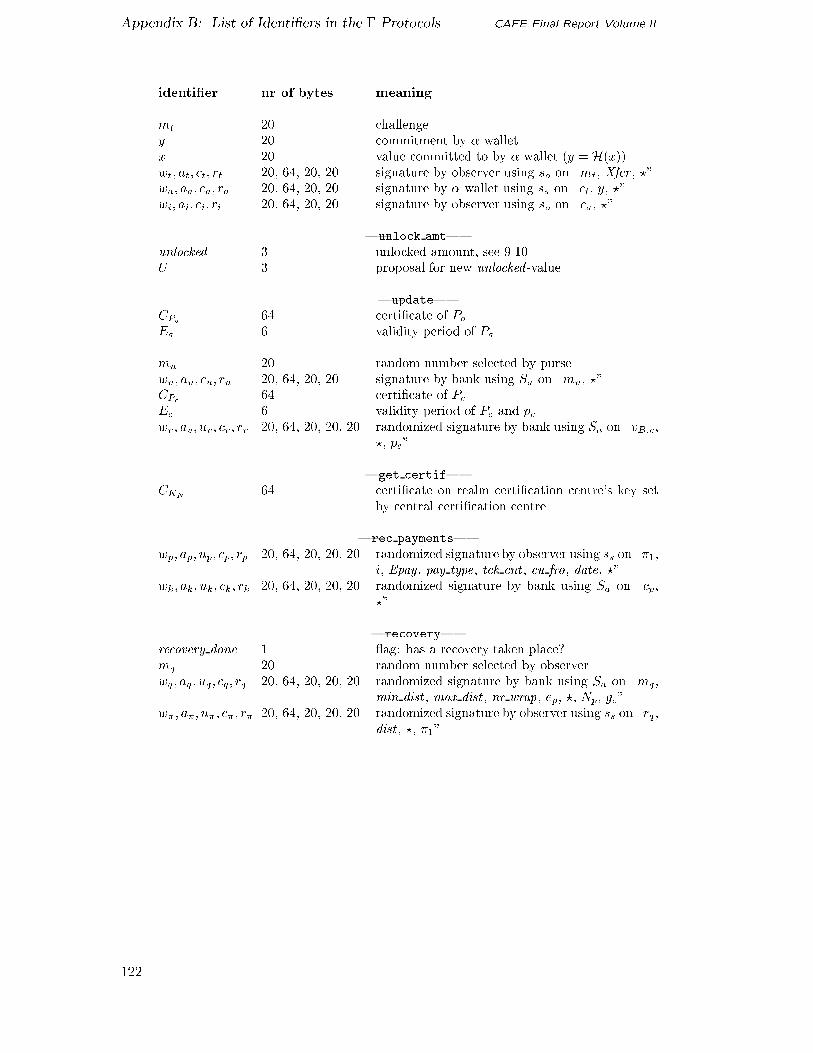

A List of Identiers in the � Protocols ���

B List of Identiers in the � Protocols ���

IV Security Evaluation ���

�� Security Evaluation of Basic Primitives ���

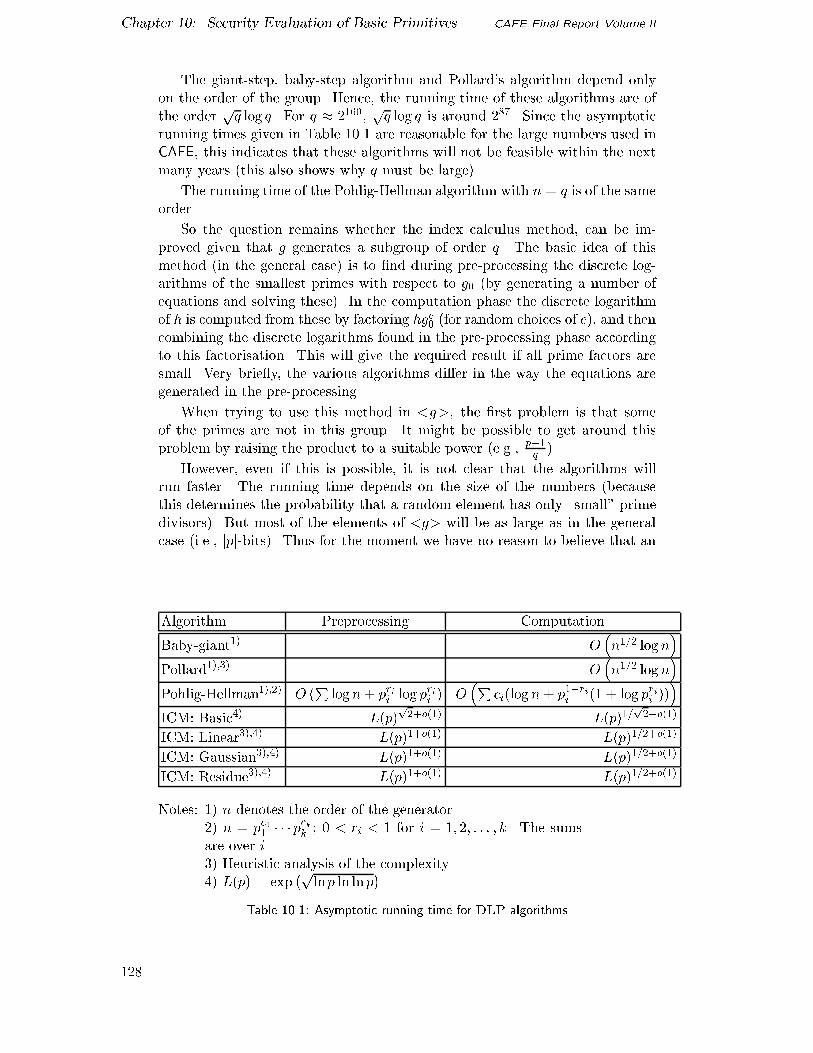

� �� Discrete Logarithms � � � � � � � � � � � � � � � � � � � � � � � � � ���

� �� Primitives Using the Factoring Assumption � � � � � � � � � � � � ���

� �� Security of the Hash Function � � � � � � � � � � � � � � � � � � � ���

�� Security Requirements ���

���� Assumptions � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

���� Bank�s Requirements � � � � � � � � � � � � � � � � � � � � � � � � ��

���� Payer�s Requirements � � � � � � � � � � � � � � � � � � � � � � � � ��

���� Payee�s Requirements � � � � � � � � � � � � � � � � � � � � � � � � ��

�� Security in the � Protocols ���

���� Bank�s Requirements � � � � � � � � � � � � � � � � � � � � � � � � ���

���� Payer�s Requirements � � � � � � � � � � � � � � � � � � � � � � � � ���

���� Payee�s Requirements � � � � � � � � � � � � � � � � � � � � � � � � ��

�� Integrity in the � Protocols ���

���� Bank�s Integrity � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

���� Payer�s Integrity � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

���� Resilience Against Interruptions � � � � � � � � � � � � � � � � � � ���

���� Independence of � Protocols � � � � � � � � � � � � � � � � � � � � ���

V Clearing ���

�� Introduction ���

���� Overview � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

���� De�nitions � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

���� Requirements � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

���� Clearing Architecture � � � � � � � � � � � � � � � � � � � � � � � � ���

v

Contents CAFE Final Report Volume II

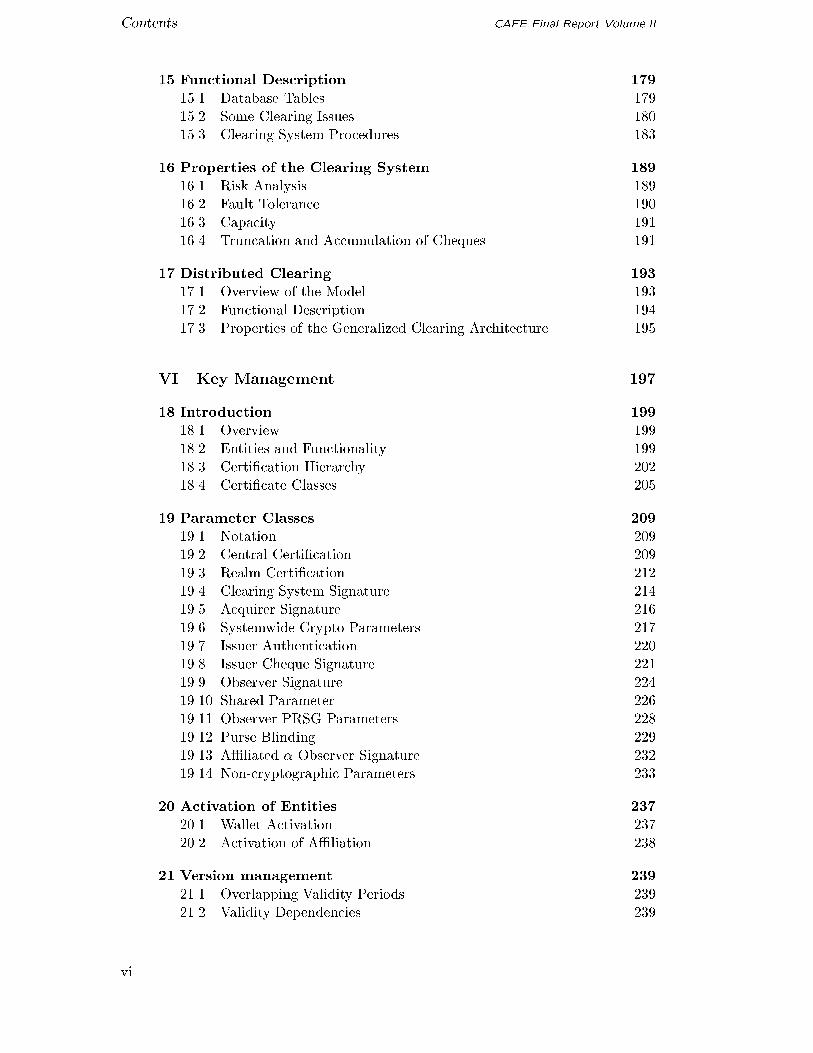

�� Functional Description ���

���� Database Tables � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

���� Some Clearing Issues � � � � � � � � � � � � � � � � � � � � � � � � �

���� Clearing System Procedures � � � � � � � � � � � � � � � � � � � � ��

�� Properties of the Clearing System ��

���� Risk Analysis � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

���� Fault Tolerance � � � � � � � � � � � � � � � � � � � � � � � � � � � �

���� Capacity � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

���� Truncation and Accumulation of Cheques � � � � � � � � � � � � � ��

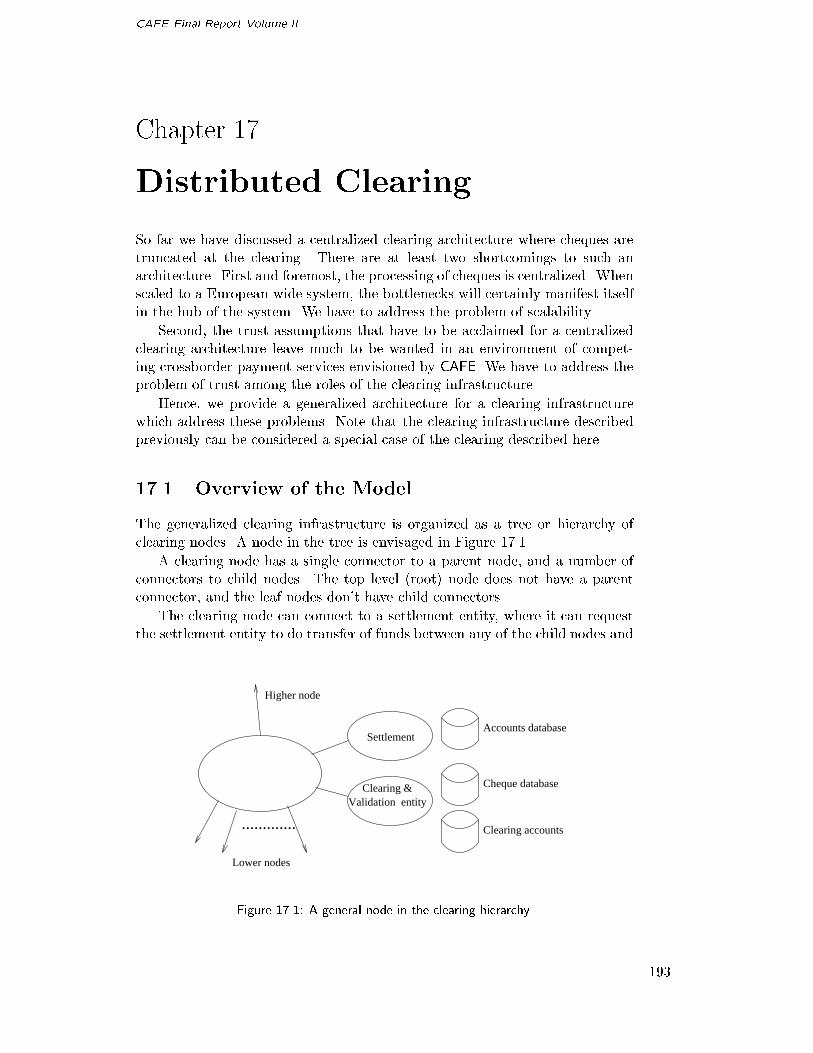

�� Distributed Clearing ���

���� Overview of the Model � � � � � � � � � � � � � � � � � � � � � � � ��

���� Functional Description � � � � � � � � � � � � � � � � � � � � � � � ��

���� Properties of the Generalized Clearing Architecture � � � � � � � ��

VI Key Management ���

� Introduction ���

��� Overview � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� Entities and Functionality � � � � � � � � � � � � � � � � � � � � � �

��� Certi�cation Hierarchy � � � � � � � � � � � � � � � � � � � � � � � � �

��� Certi�cate Classes � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� Parameter Classes ���

��� Notation � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� Central Certi�cation � � � � � � � � � � � � � � � � � � � � � � � � �

��� Realm Certi�cation � � � � � � � � � � � � � � � � � � � � � � � � � ���

��� Clearing System Signature � � � � � � � � � � � � � � � � � � � � � ���

��� Acquirer Signature � � � � � � � � � � � � � � � � � � � � � � � � � ���

��� Systemwide Crypto Parameters � � � � � � � � � � � � � � � � � � ���

��� Issuer Authentication � � � � � � � � � � � � � � � � � � � � � � � � ��

�� Issuer Cheque Signature � � � � � � � � � � � � � � � � � � � � � � ���

�� Observer Signature � � � � � � � � � � � � � � � � � � � � � � � � � ���

��� Shared Parameter � � � � � � � � � � � � � � � � � � � � � � � � � � ���

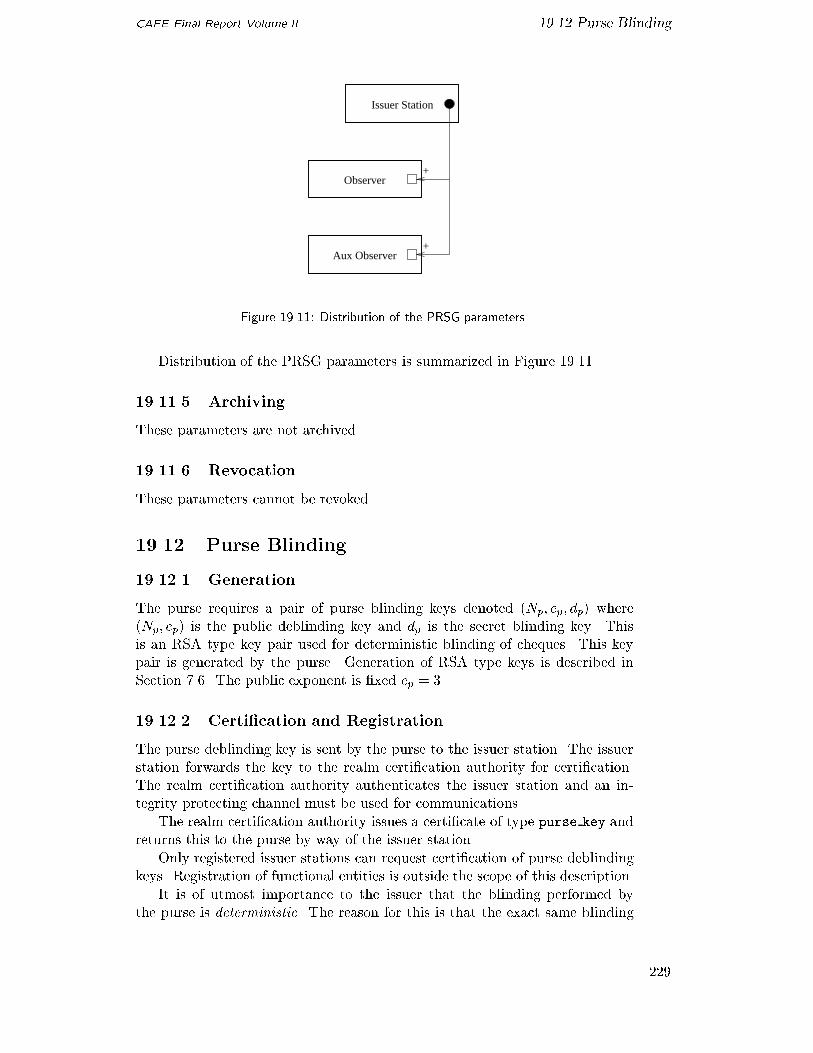

���� Observer PRSG Parameters � � � � � � � � � � � � � � � � � � � � ��

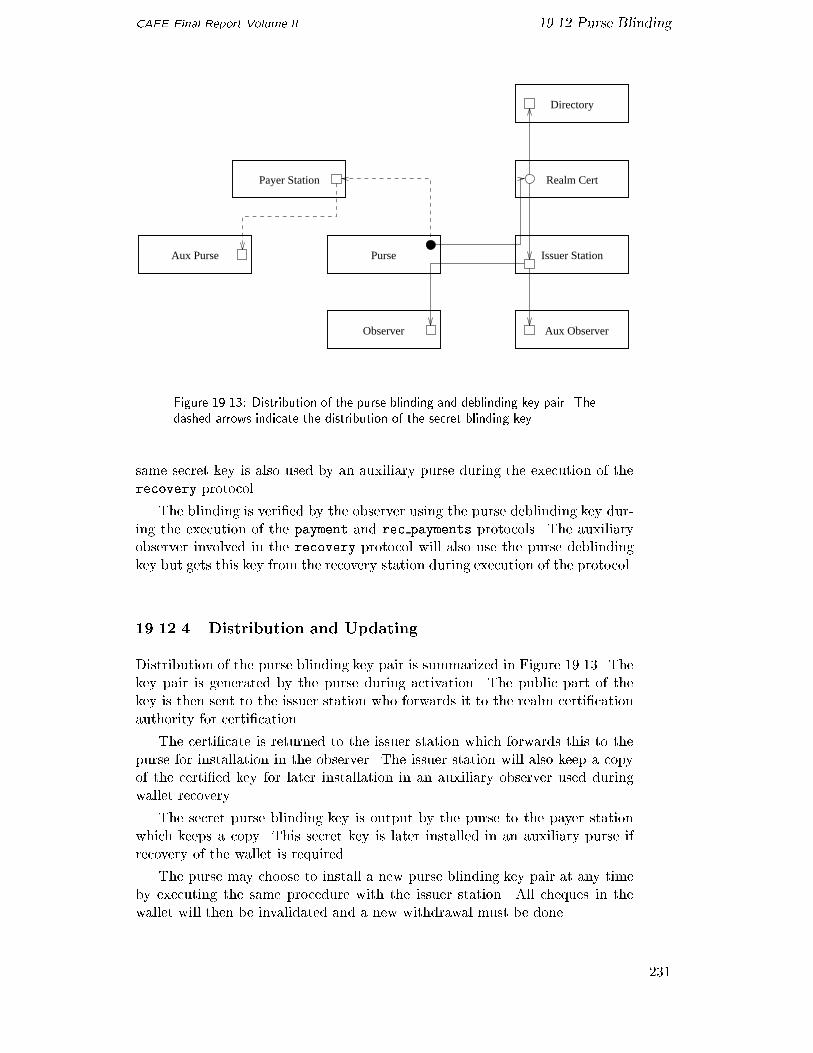

���� Purse Blinding � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

���� A�liated � Observer Signature � � � � � � � � � � � � � � � � � � ���

���� Non�cryptographic Parameters � � � � � � � � � � � � � � � � � � � ���

�� Activation of Entities ���

� �� Wallet Activation � � � � � � � � � � � � � � � � � � � � � � � � � � ���

� �� Activation of A�liation � � � � � � � � � � � � � � � � � � � � � � � ��

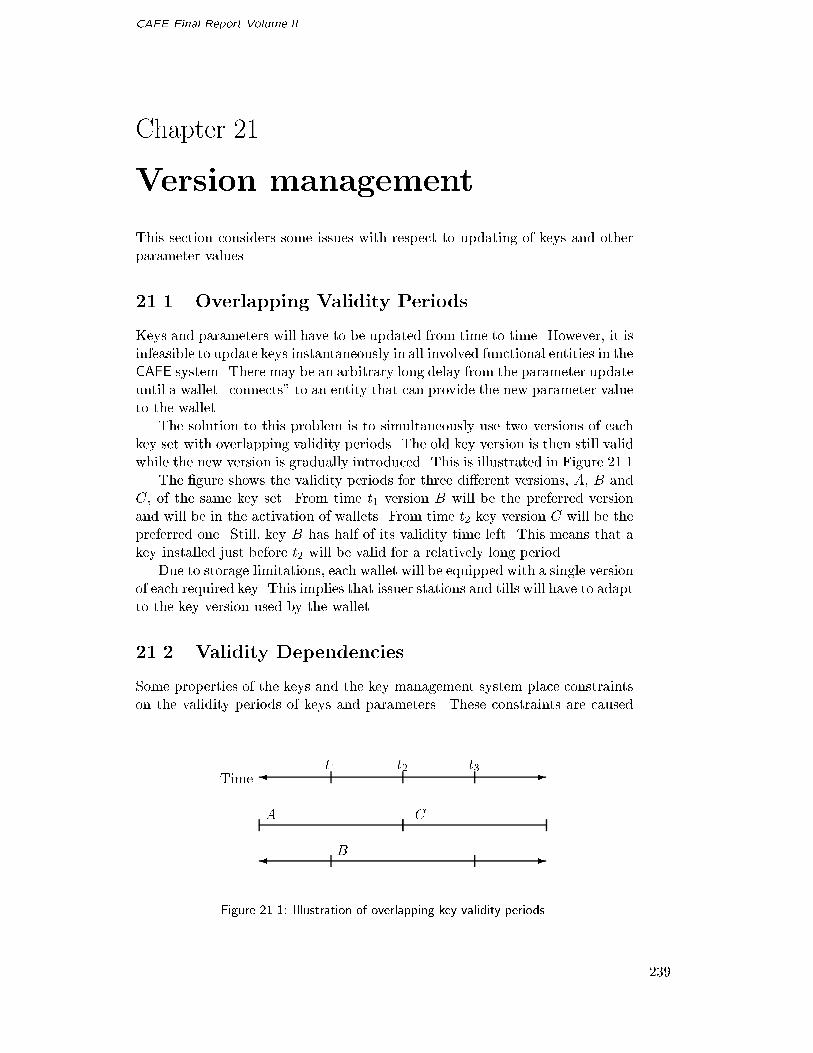

�� Version management ���

���� Overlapping Validity Periods � � � � � � � � � � � � � � � � � � � � ��

���� Validity Dependencies � � � � � � � � � � � � � � � � � � � � � � � � ��

vi

CAFE Final Report Volume II Contents

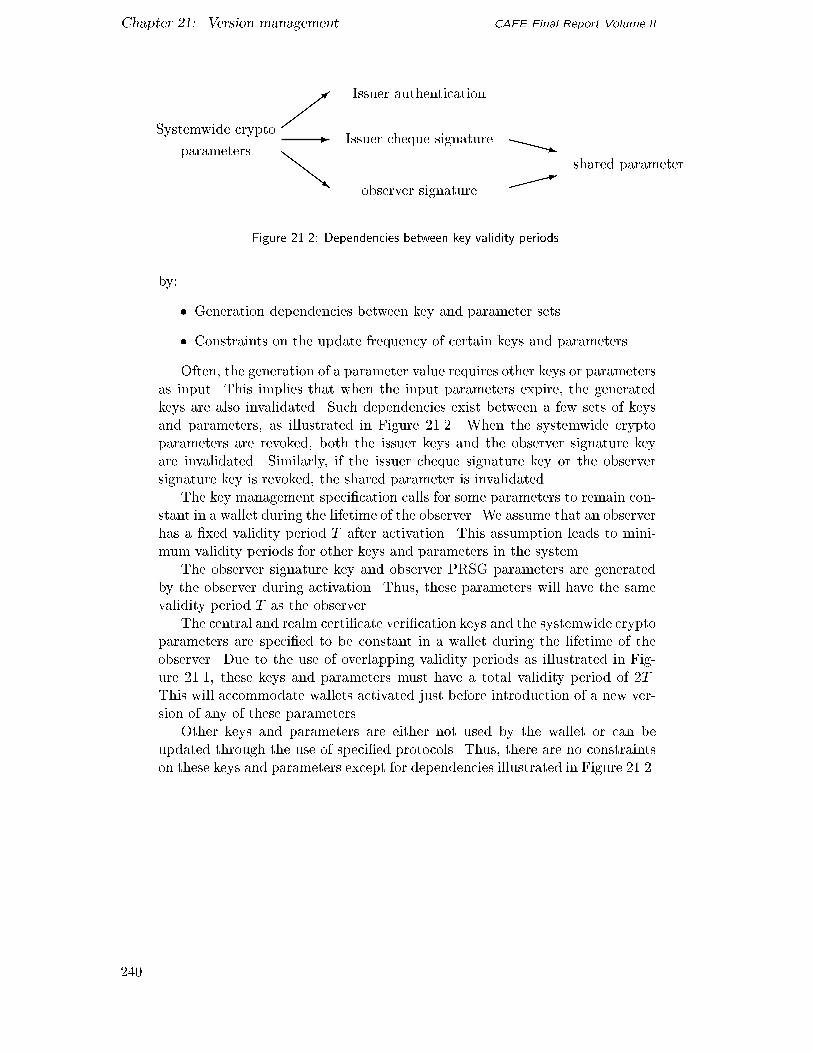

�� Security Properties ������� Types of Attack � � � � � � � � � � � � � � � � � � � � � � � � � � � ������� Forged Certi�cates � � � � � � � � � � � � � � � � � � � � � � � � � ������� Key Compromisation � � � � � � � � � � � � � � � � � � � � � � � � ������� Acquirer Signature � � � � � � � � � � � � � � � � � � � � � � � � � ������� Clearing Signature � � � � � � � � � � � � � � � � � � � � � � � � � ���

�� Key Management for the � System ������� Entities � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ������� Certi�cate Classes � � � � � � � � � � � � � � � � � � � � � � � � � � ������� Central Certi�cation � � � � � � � � � � � � � � � � � � � � � � � � ������� Realm Certi�cation � � � � � � � � � � � � � � � � � � � � � � � � � ������� Systemwide Crypto Parameters � � � � � � � � � � � � � � � � � � ������� Issuer Authentication � � � � � � � � � � � � � � � � � � � � � � � � ������� Issuer Cheque Signature � � � � � � � � � � � � � � � � � � � � � � ������ Wallet Signature � � � � � � � � � � � � � � � � � � � � � � � � � � � ������ Shared Parameter � � � � � � � � � � � � � � � � � � � � � � � � � � ������� Wallet PRSG Parameters � � � � � � � � � � � � � � � � � � � � � � �������� Non�Cryptographic Parameters � � � � � � � � � � � � � � � � � � ���

VII Extensions ���

�� E�ciency Improvements ������� An Alternative Blind Signature Scheme � � � � � � � � � � � � � � ������� k�Spendability Extension � � � � � � � � � � � � � � � � � � � � � � ������� Exploiting Pre� and Post�processing � � � � � � � � � � � � � � � � ��

�� Multi Currency Payments ������� Introduction � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ������� Multiple Issuers � � � � � � � � � � � � � � � � � � � � � � � � � � � ������� Multiple Currencies � � � � � � � � � � � � � � � � � � � � � � � � � ������� General Requirements � � � � � � � � � � � � � � � � � � � � � � � � ������� Protocols and Procedures � � � � � � � � � � � � � � � � � � � � � � ��

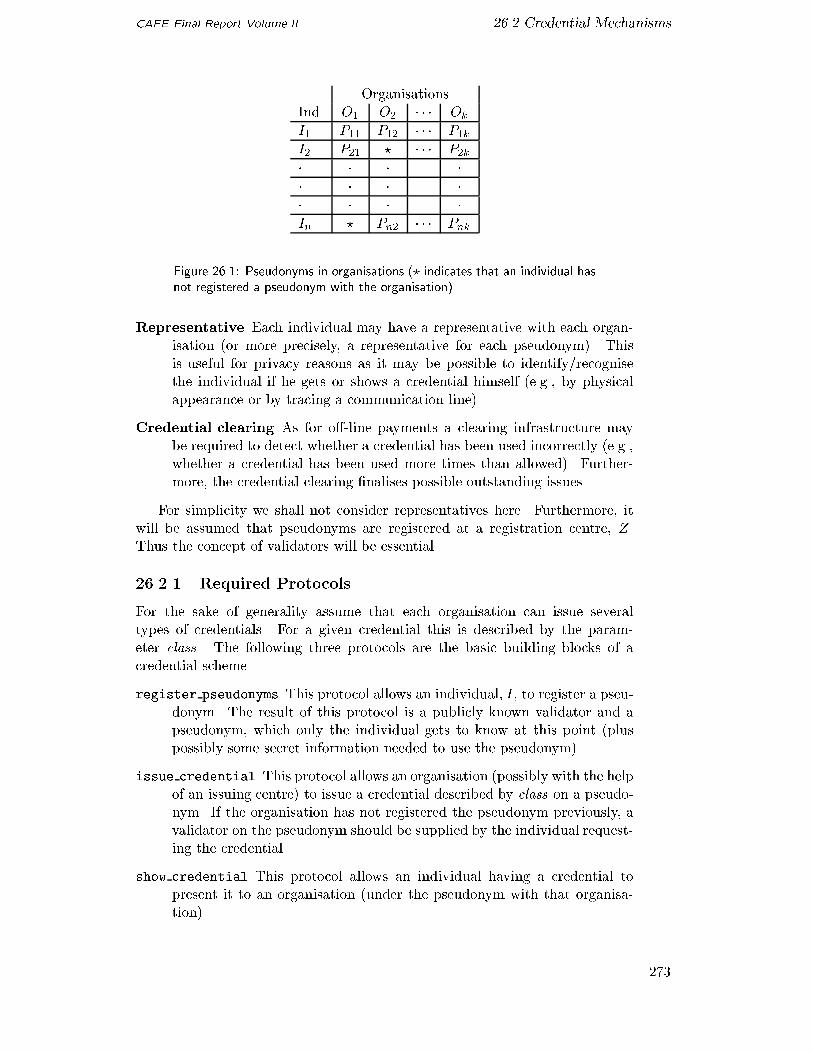

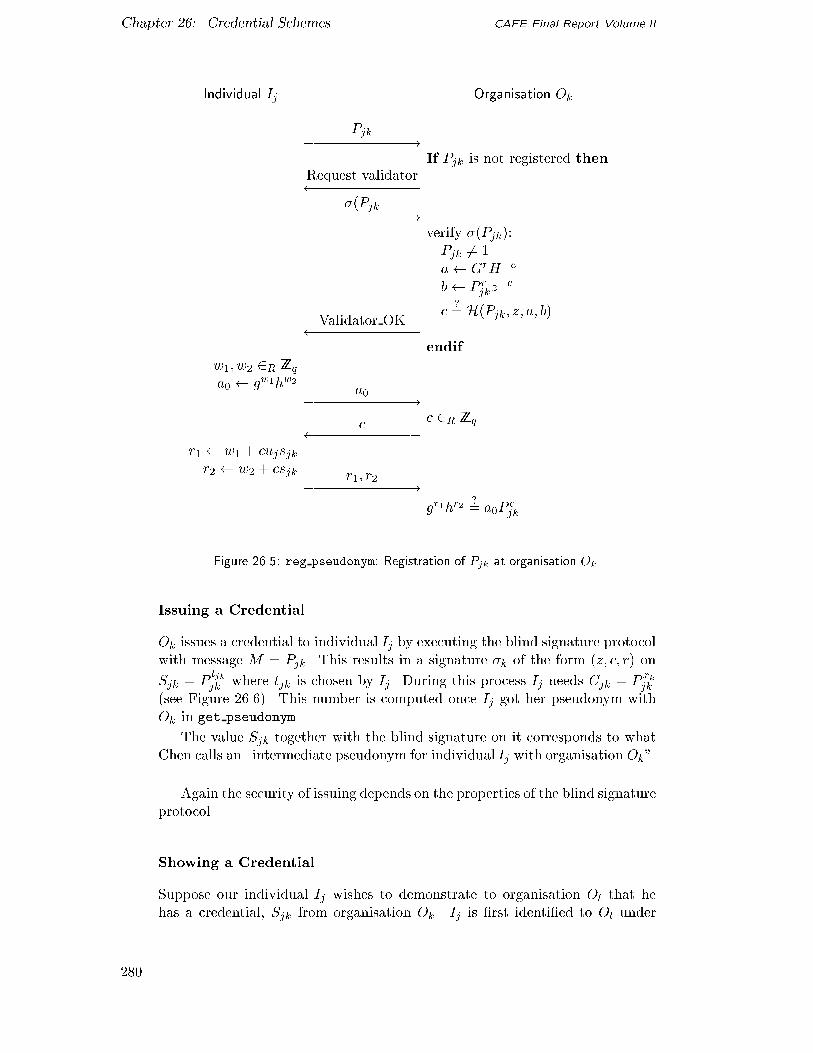

�� Credential Schemes ������� Introduction � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ������� Credential Mechanisms � � � � � � � � � � � � � � � � � � � � � � � ������� Credential Protocols � � � � � � � � � � � � � � � � � � � � � � � � ������� Applications of Credentials � � � � � � � � � � � � � � � � � � � � � ��

Bibliography ���

vii

Contents CAFE Final Report Volume II

viii

CAFE Final Report Volume II

List of Figures

��� Overview of the payment system roles and transactions� � � � � ���� The electronic wallet � � � � � � � � � � � � � � � � � � � � � � � � �

��� The abstraction hierarchy� � � � � � � � � � � � � � � � � � � � � � ��

��� An example from the architecture� � � � � � � � � � � � � � � � � � ���� Complete payment system architecture � � � � � � � � � � � � � � �

��� The withdrawal transaction � � � � � � � � � � � � � � � � � � � � ����� The � and � payment transaction � � � � � � � � � � � � � � � � � ��

��� The �� payment transaction � � � � � � � � � � � � � � � � � � � � ����� The transfer transaction � � � � � � � � � � � � � � � � � � � � � � ���� The � recovery initialization transaction � � � � � � � � � � � � � ��

�� The � recovery transaction � � � � � � � � � � � � � � � � � � � � � ����� The �� or � recovery transaction � � � � � � � � � � � � � � � � � ��

��� Schnorr�s identi�cation protocol� � � � � � � � � � � � � � � � � � � ����� Schnorr�s signature protocol� � � � � � � � � � � � � � � � � � � � � ����� The basic proof system � � � � � � � � � � � � � � � � � � � � � � � ��

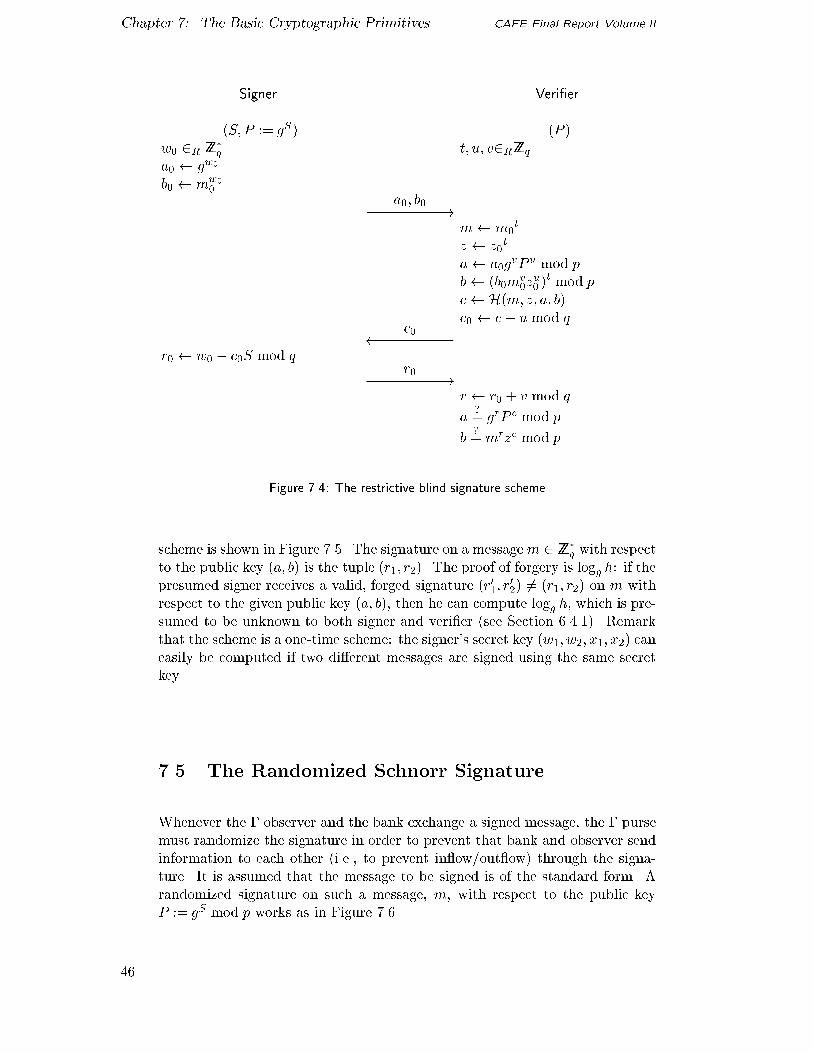

��� The restrictive blind signature scheme � � � � � � � � � � � � � � � ����� van Heyst�Pedersen fail�stop signature scheme � � � � � � � � � � ��

��� The randomized Schnorr signature � � � � � � � � � � � � � � � � � ����� Outline of compress � � � � � � � � � � � � � � � � � � � � � � � � � ��

�� Outline of hash H � � � � � � � � � � � � � � � � � � � � � � � � � � ��

�� ��reset � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���� ��get info � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

�� ��authenticate � � � � � � � � � � � � � � � � � � � � � � � � � � � ���� ��write cu tbl � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

�� ��gen cheque � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��� ��load cheque � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

�� ��show currencies � � � � � � � � � � � � � � � � � � � � � � � � � ��� ��payment of a cheque � � � � � � � � � � � � � � � � � � � � � � � ��� ��payment of phone ticks � � � � � � � � � � � � � � � � � � � � � � ��

�� � to � transfer �part �� � � � � � � � � � � � � � � � � � � � � � � ���� � to � transfer �part �� � � � � � � � � � � � � � � � � � � � � � � �

��� � to � rollback � � � � � � � � � � � � � � � � � � � � � � � � � � � ��� ��unlock amt � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���� ��updateP a � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� ��updateP c � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

ix

List of Figures CAFE Final Report Volume II

��� ��get certif � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� ��rec payments � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� ��recovery init � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� ��recovery � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� ��deposit � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� ��reset � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� ��get info � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� ��authenticate �part �� � � � � � � � � � � � � � � � � � � � � � � �

�� ��authenticate �part �� � � � � � � � � � � � � � � � � � � � � � � �

�� ��write cu tbl � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� ��gen cheque � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�� ��show currencies � � � � � � � � � � � � � � � � � � � � � � � � � � �

� ��payment �part �� � � � � � � � � � � � � � � � � � � � � � � � � � � �

� ��payment �part �� � � � � � � � � � � � � � � � � � � � � � � � � � � �

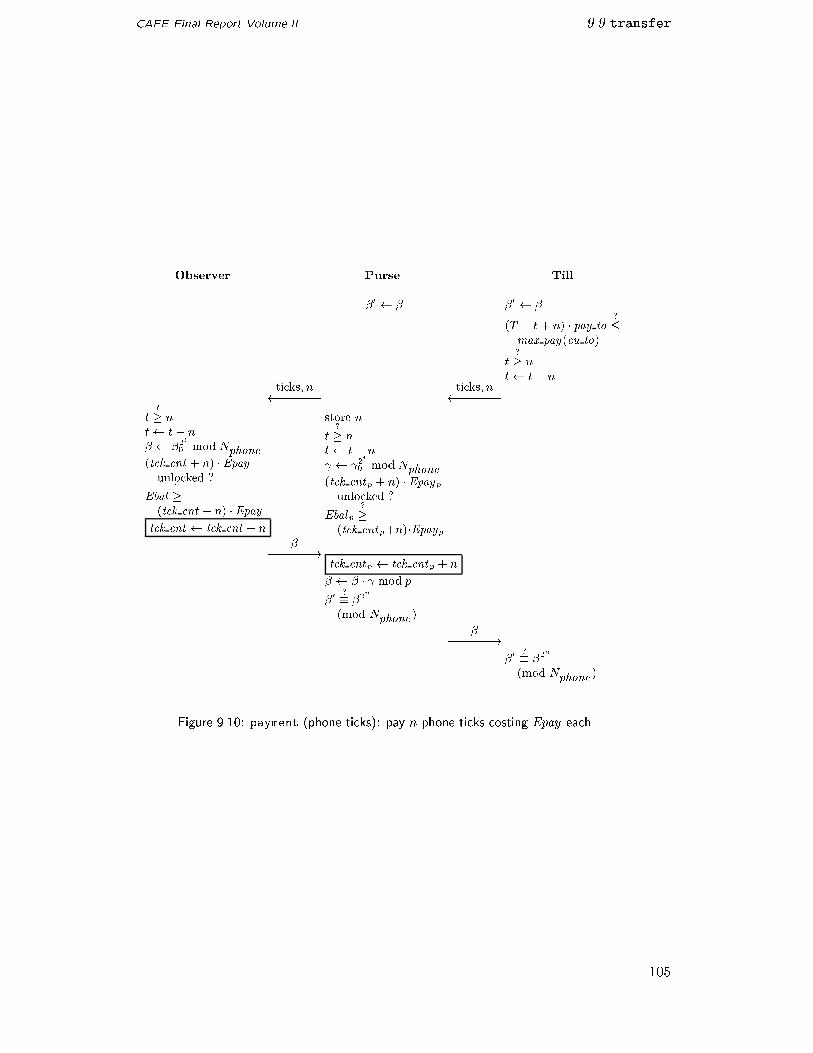

�� ��payment �phone ticks� � � � � � � � � � � � � � � � � � � � � � � � �

��� ��unlock amt � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� ��updateP a � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� ��updateP c � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� ��get certif � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��� ��rec payments � � � � � � � � � � � � � � � � � � � � � � � � � � � ��

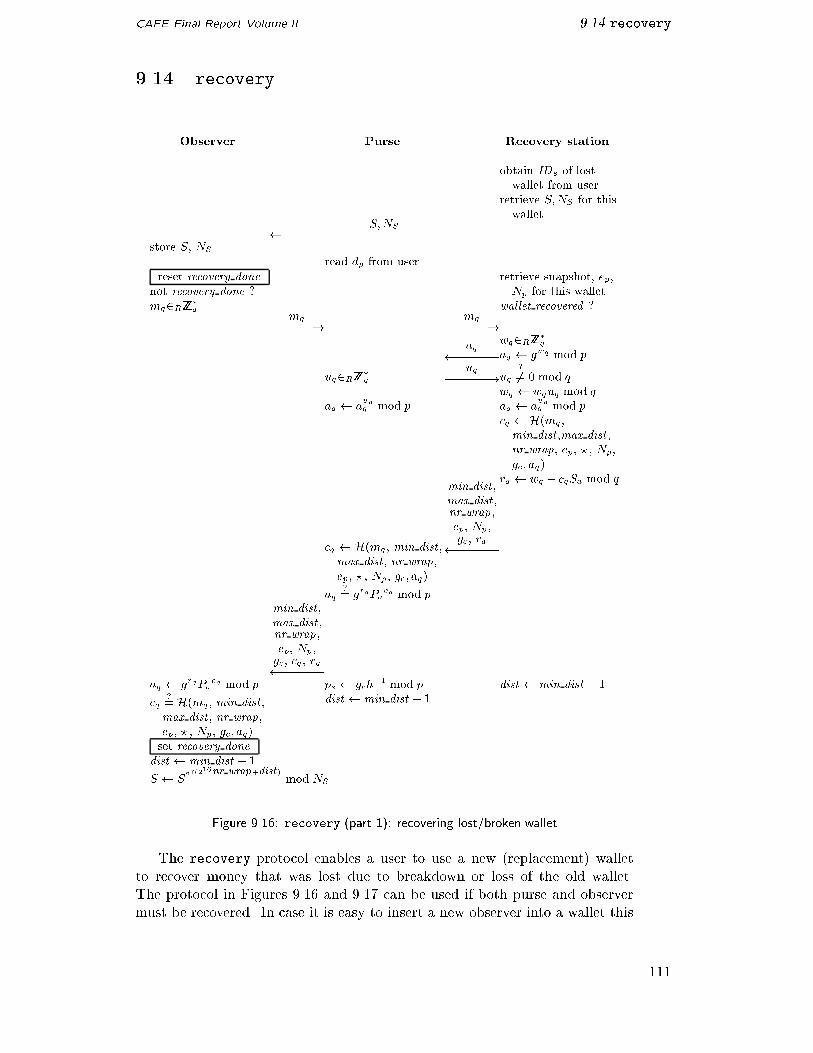

��� ��recovery �part �� � � � � � � � � � � � � � � � � � � � � � � � � � ���

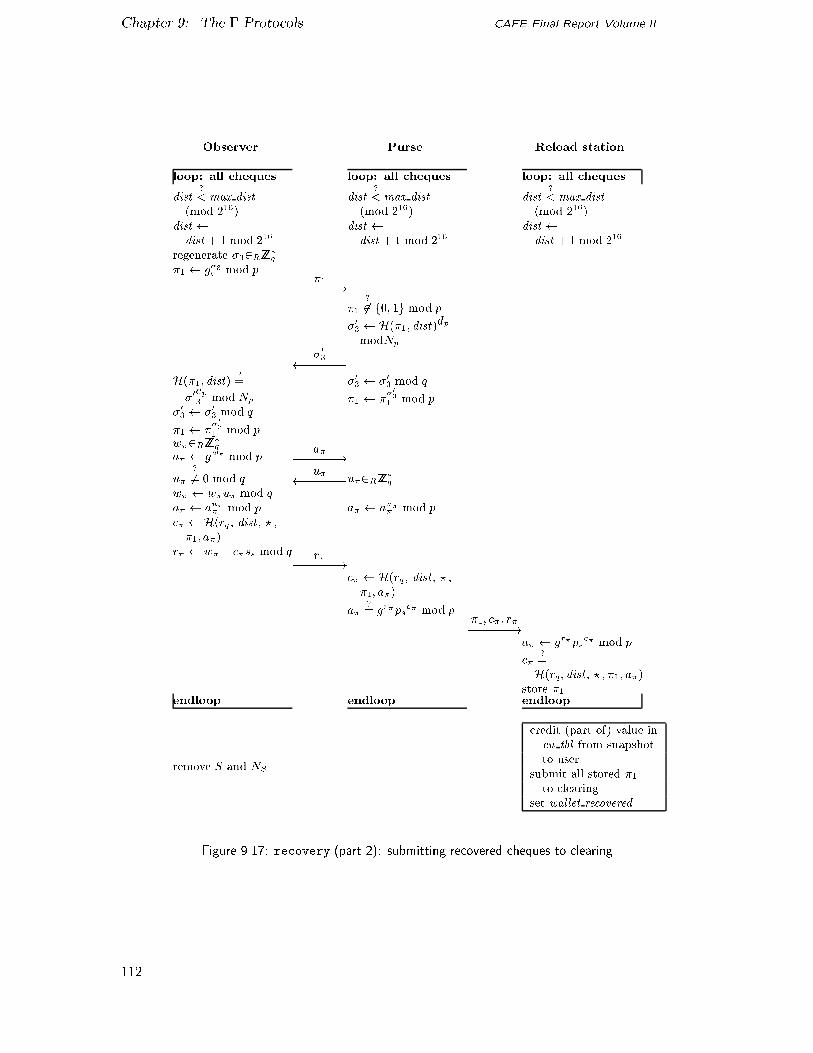

��� ��recovery �part �� � � � � � � � � � � � � � � � � � � � � � � � � � ���

�� ��deposit � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���

���� Payment system with clearing � � � � � � � � � � � � � � � � � � � ���

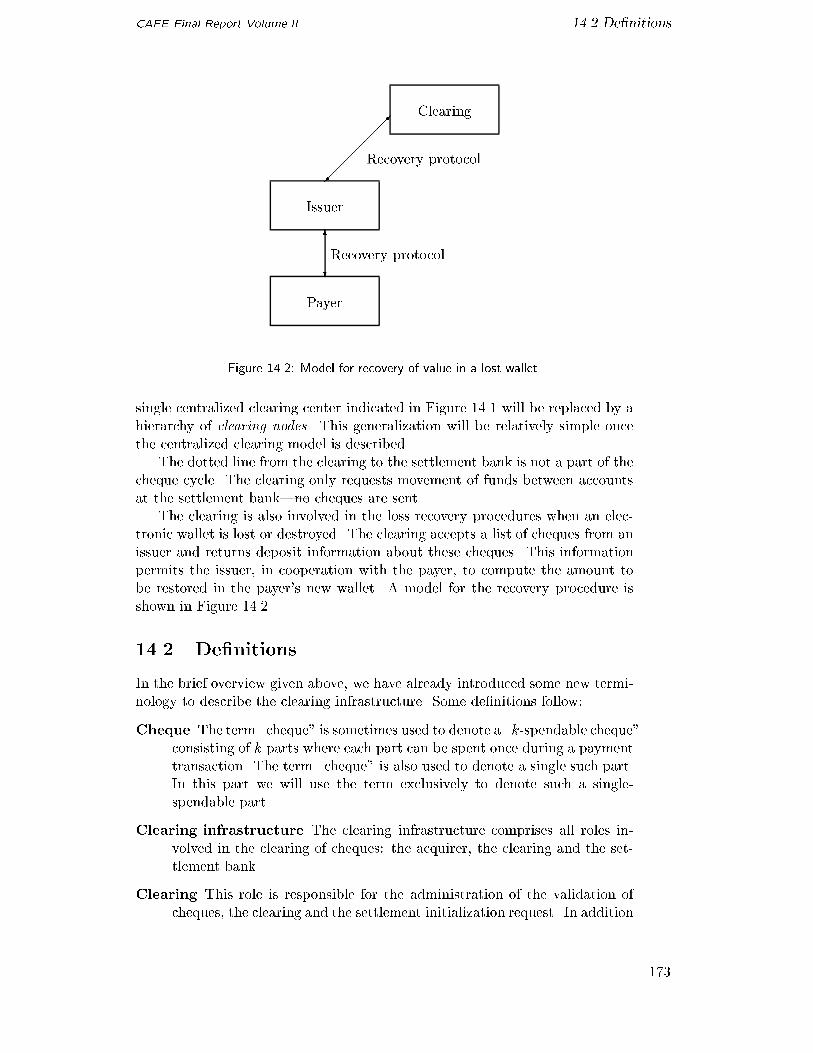

���� Model for recovery of value in a lost wallet� � � � � � � � � � � � � ���

���� The structure of the centralized clearing architecture� � � � � � � ���

���� A general node in the clearing hierarchy� � � � � � � � � � � � � � ��

��� Structure of the key management certi�cation hierarchy� � � � � � �

��� Location of parameter classes in the key certi�cate hierarchy� � � � �

��� Example of a one�to�many distribution� � � � � � � � � � � � � � � �

��� Distribution of the central certi�cate veri�cation key� � � � � � � ���

��� Distribution of the realm certi�cate veri�cation key� � � � � � � � ���

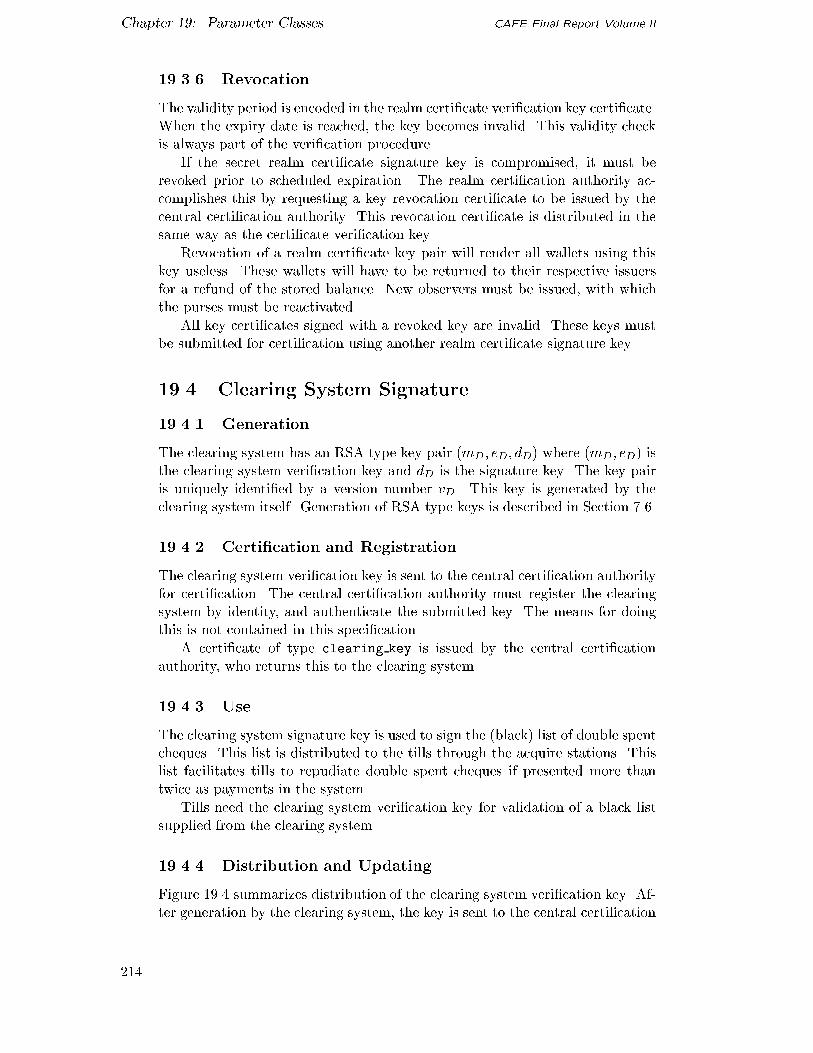

��� Distribution of the clearing system veri�cation key� � � � � � � � ���

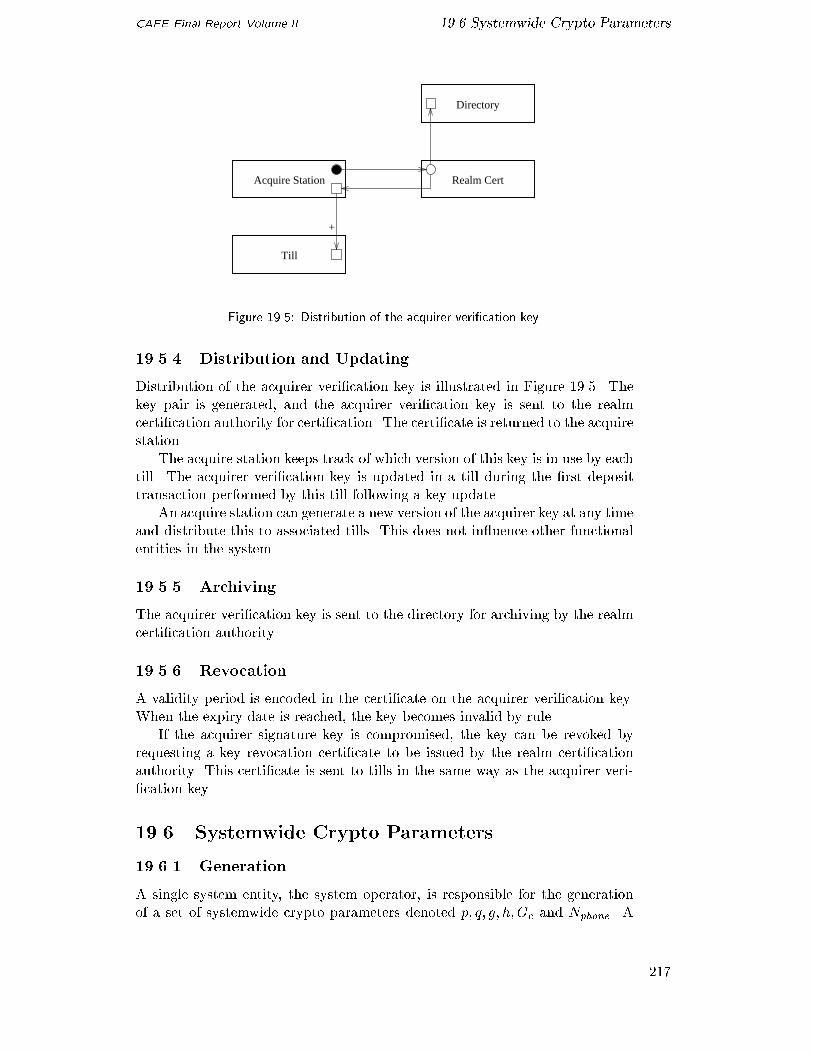

��� Distribution of the acquirer veri�cation key� � � � � � � � � � � � ���

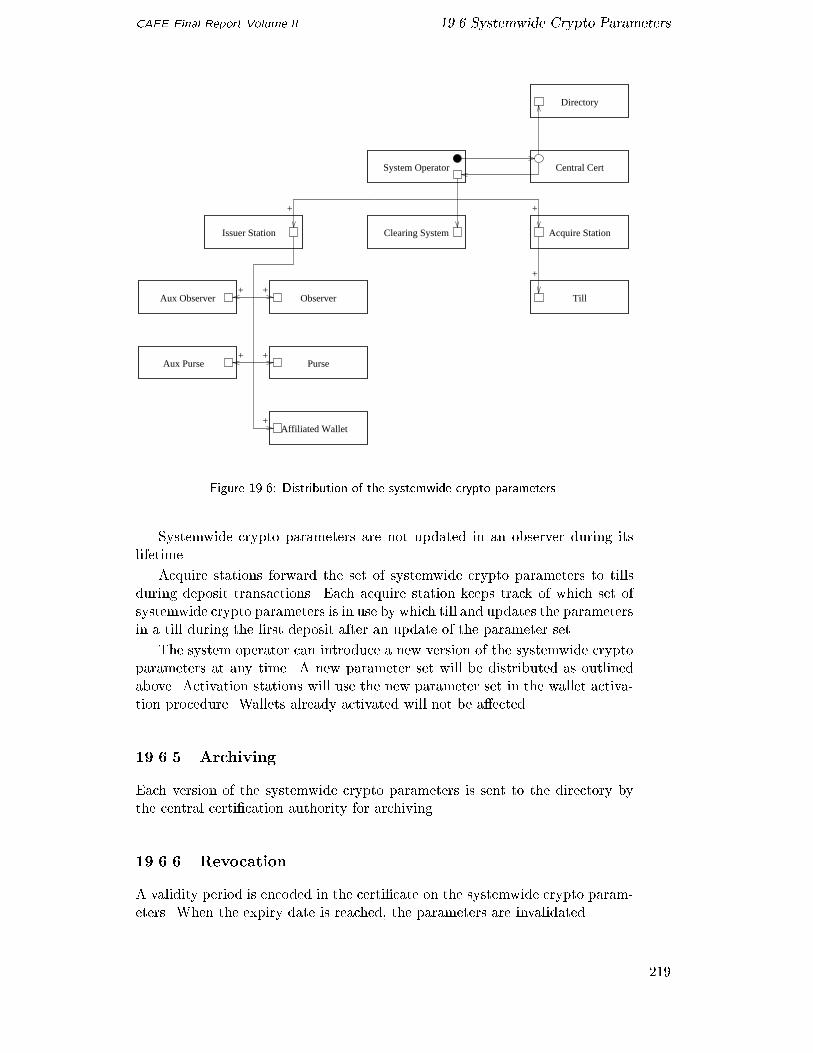

��� Distribution of the systemwide crypto parameters� � � � � � � � � ��

��� Distribution of the issuer authentication key� � � � � � � � � � � � ���

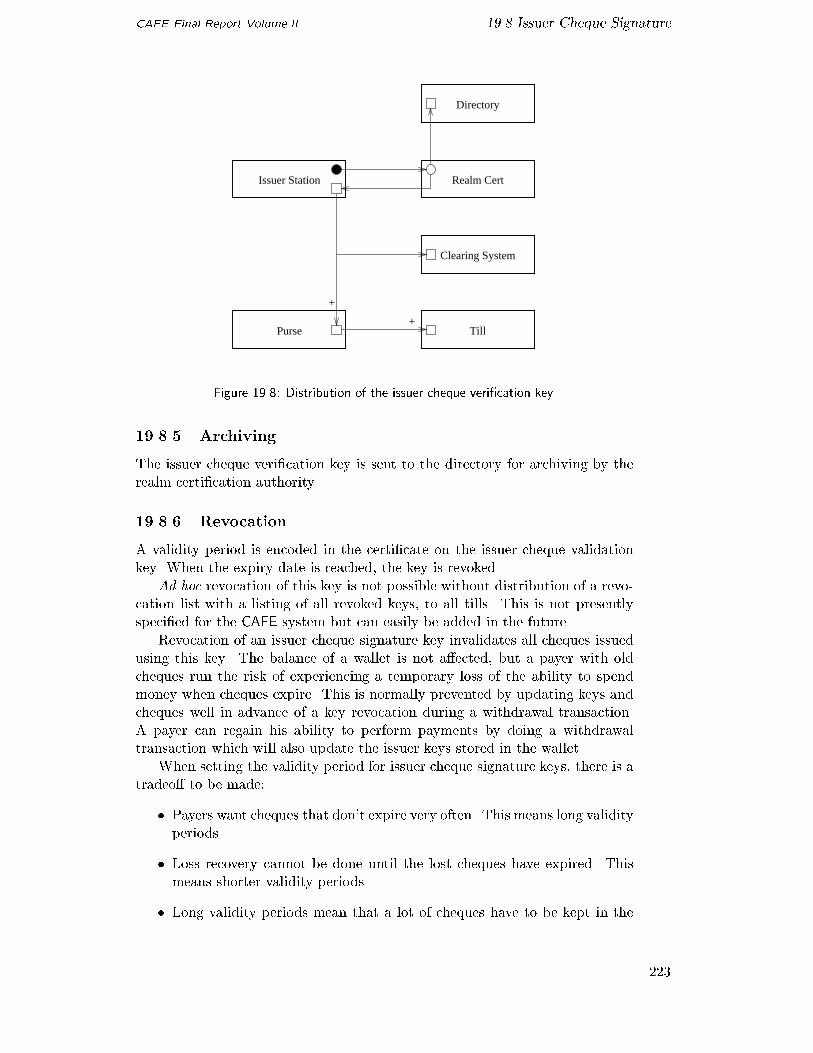

�� Distribution of the issuer cheque veri�cation key� � � � � � � � � ���

�� Distribution of the observer veri�cation key� � � � � � � � � � � � ���

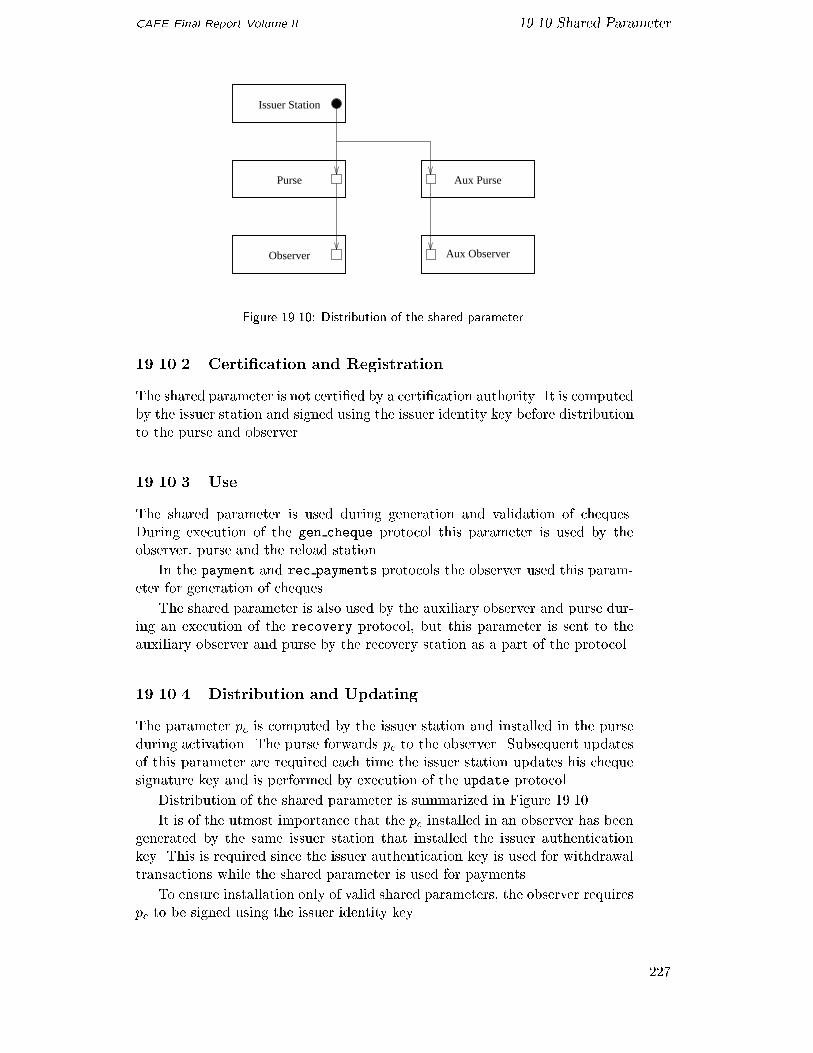

��� Distribution of the shared parameter� � � � � � � � � � � � � � � � ���

���� Distribution of the observer PRSG parameters� � � � � � � � � � ��

���� Protocol for proving validity of blinding key modulus� � � � � � � ��

���� Distribution of the purse blinding key� � � � � � � � � � � � � � � ���

���� Distribution of the a�liated observer veri�cation key� � � � � � � ���

x

CAFE Final Report Volume II List of Figures

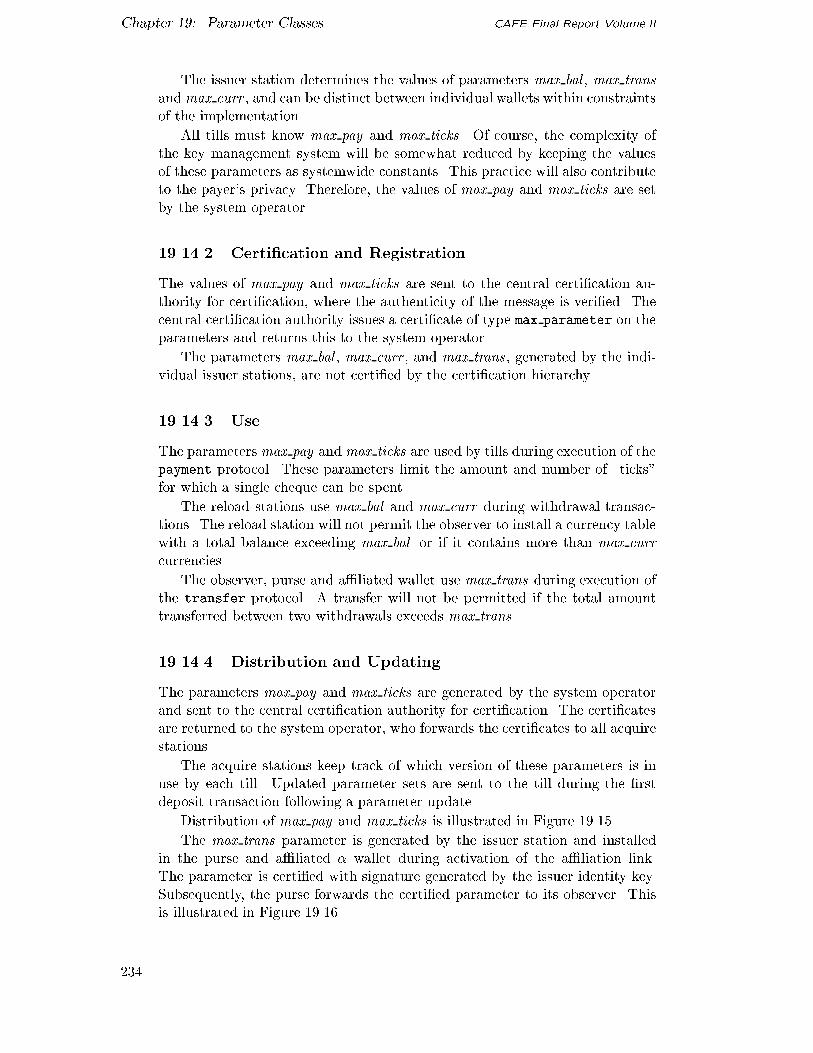

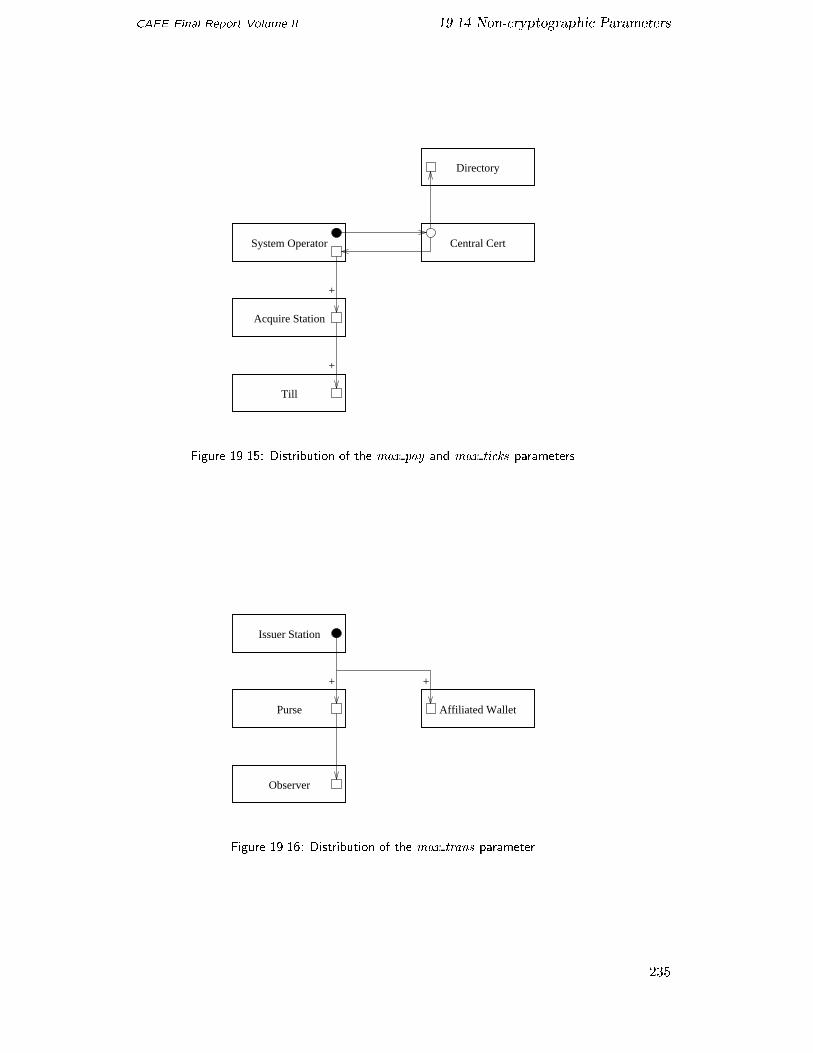

���� Distribution of the max pay and max ticks parameters� � � � � � ������� Distribution of the max trans parameter� � � � � � � � � � � � � � ���

���� Illustration of overlapping key validity periods� � � � � � � � � � � ������ Dependencies between key validity periods� � � � � � � � � � � � � ��

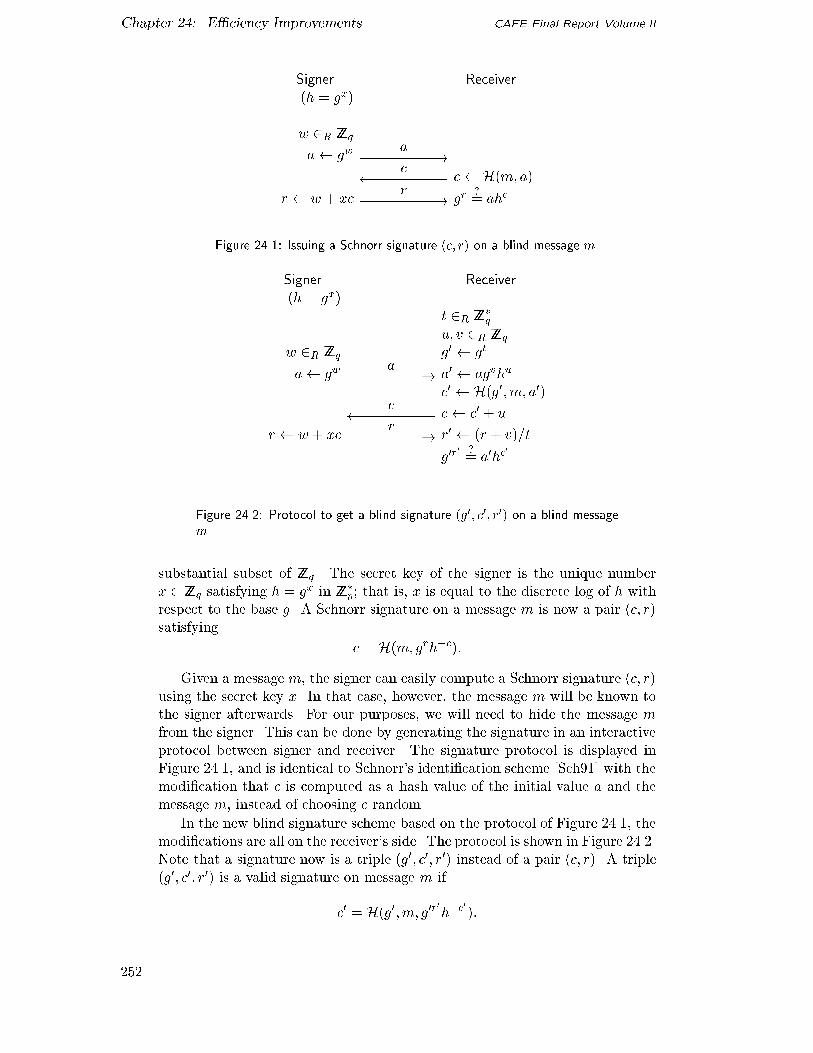

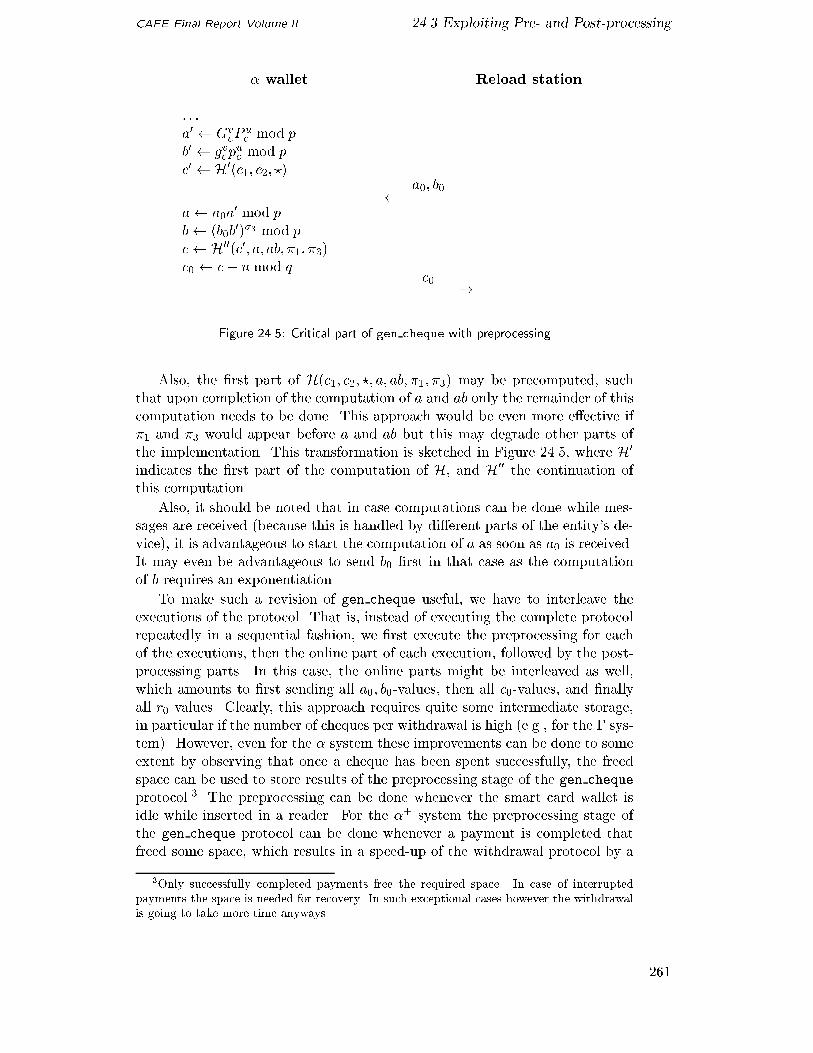

���� Issuing a Schnorr signature �c� r� on a blind message m� � � � � � ������� Protocol to get a blind signature �g�� c�� r�� on a blind message m�������� Committing to ���� � � � � ��k� � � � � � � � � � � � � � � � � � � � � ������� Critical part of gen cheque � � � � � � � � � � � � � � � � � � � � � �� ���� Critical part of gen cheque with preprocessing � � � � � � � � � � ���

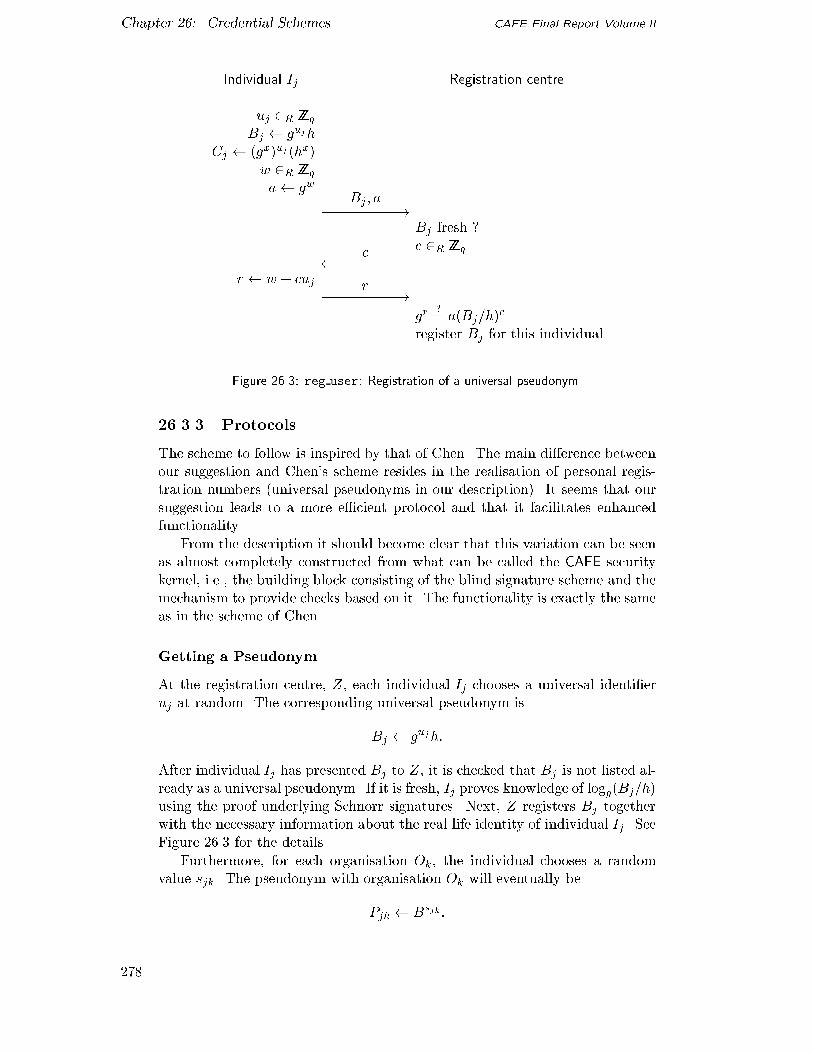

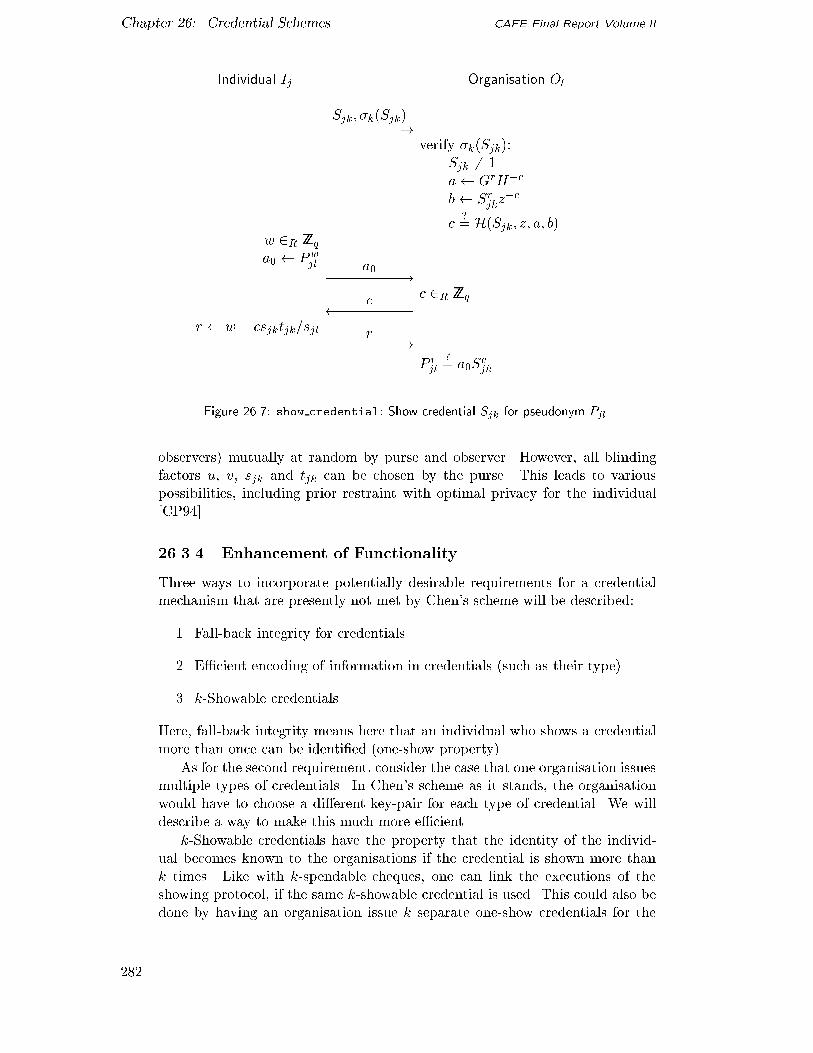

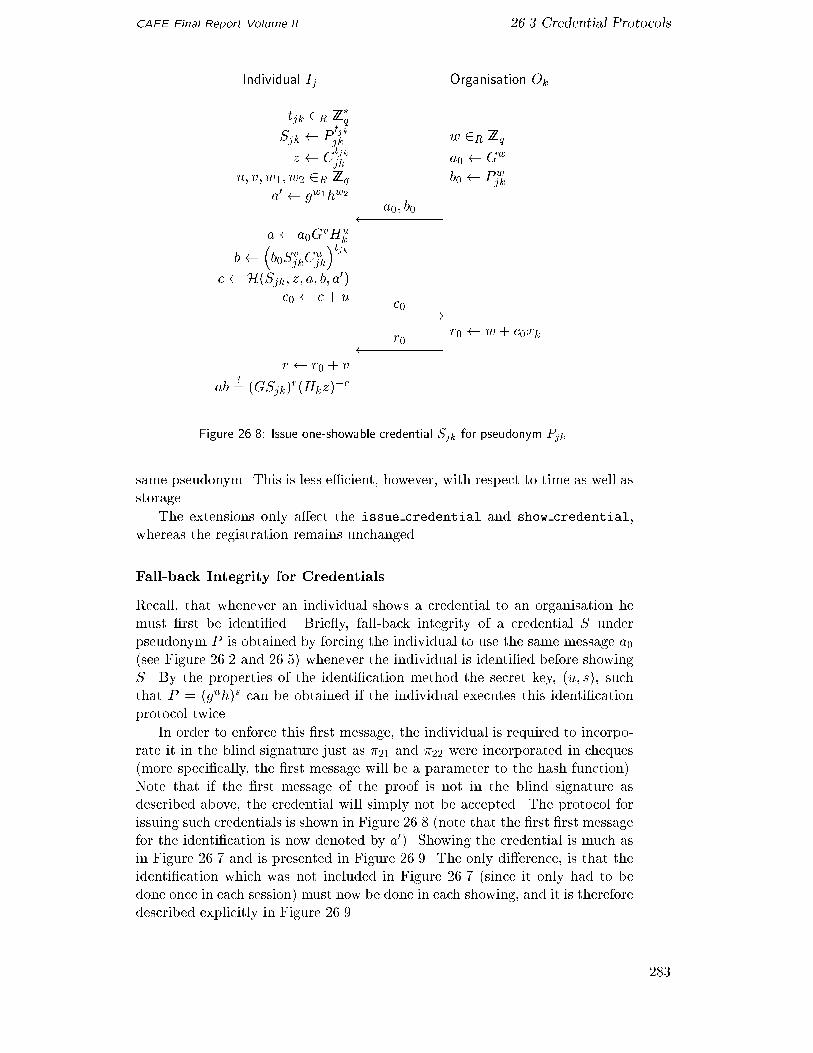

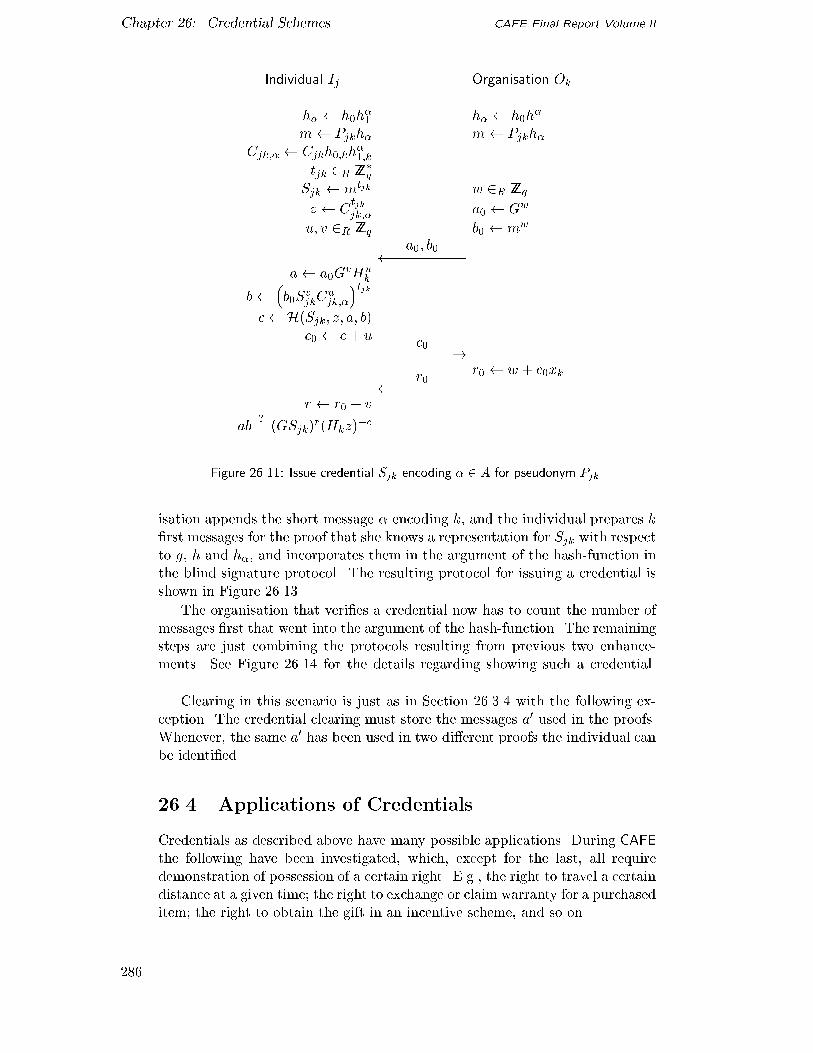

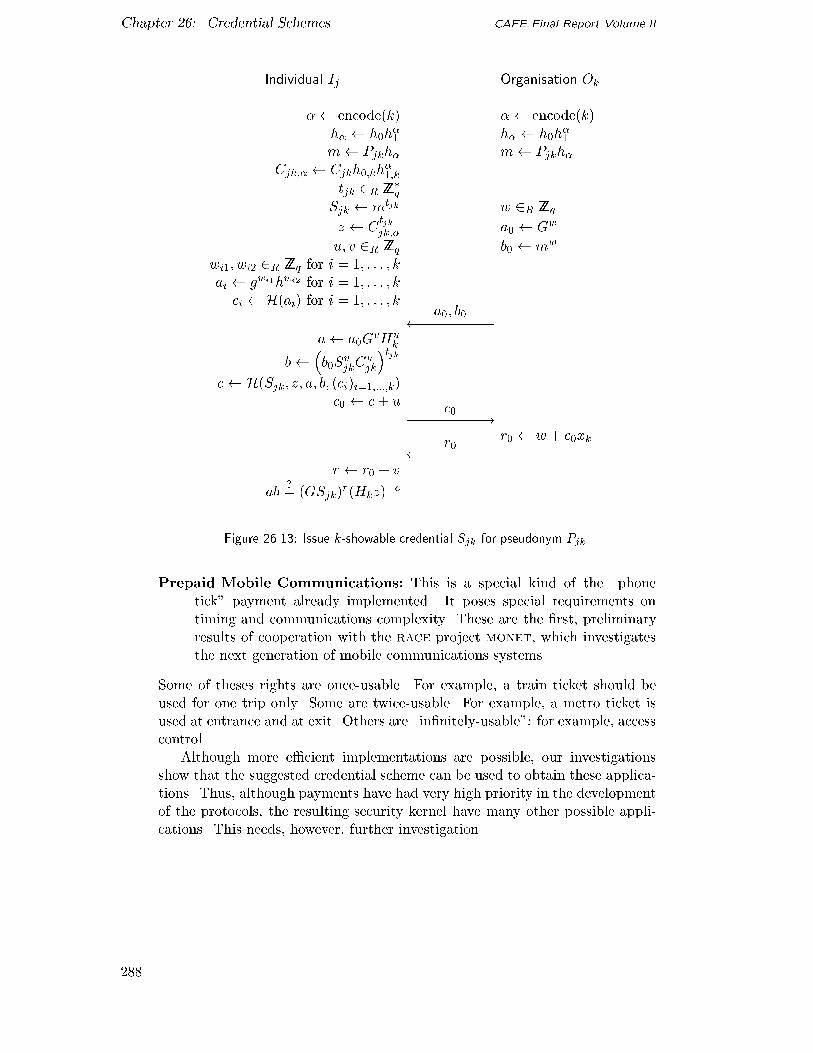

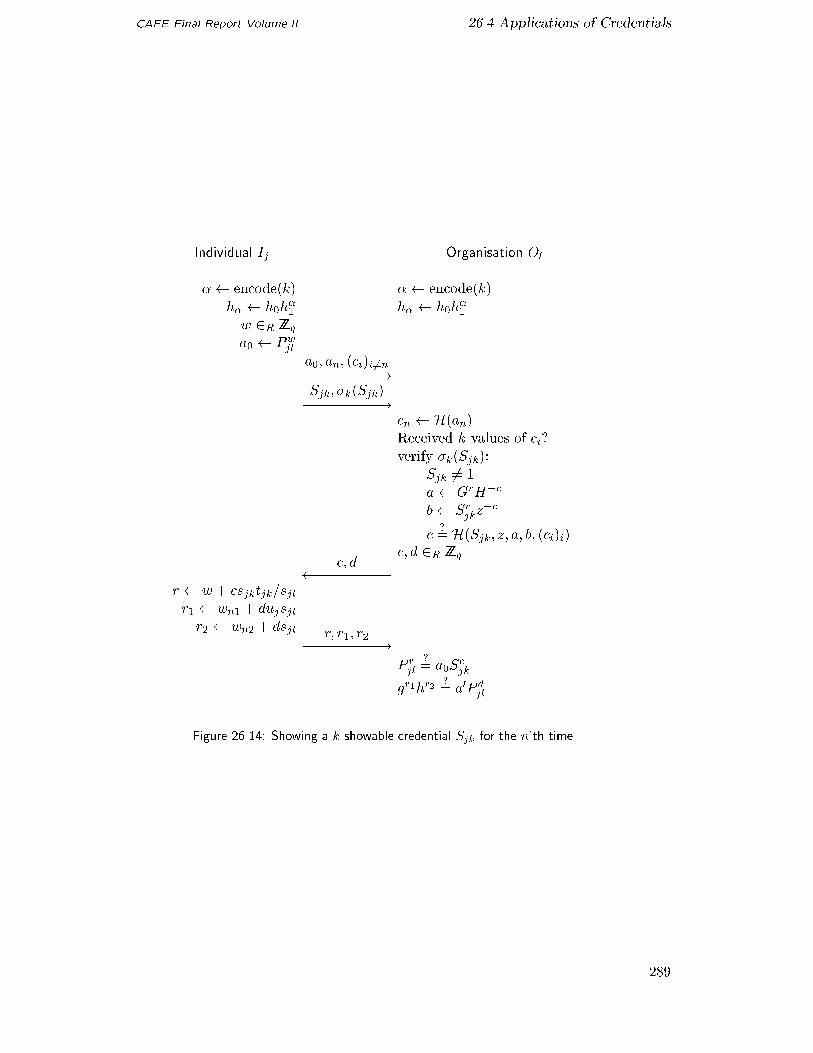

���� Pseudonyms in organisations � � � � � � � � � � � � � � � � � � � � ������� Identi�cation protocol � � � � � � � � � � � � � � � � � � � � � � � � ������� reg user � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ������ get pseudonym � � � � � � � � � � � � � � � � � � � � � � � � � � � ������ reg pseudonym � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���� issue credential � � � � � � � � � � � � � � � � � � � � � � � � � ������ show credential � � � � � � � � � � � � � � � � � � � � � � � � � � ����� Issue one�showable credential � � � � � � � � � � � � � � � � � � � � ����� Showing a one�showable credential � � � � � � � � � � � � � � � � � ������ Clearing a credential � � � � � � � � � � � � � � � � � � � � � � � � ������� Issue credential encoding information � � � � � � � � � � � � � � � ������� Show credential encoding information � � � � � � � � � � � � � � � ������� Issue k�showable credential � � � � � � � � � � � � � � � � � � � � � ������ Showing a k�showable credential � � � � � � � � � � � � � � � � � � �

xi

List of Figures CAFE Final Report Volume II

xii

CAFE Final Report Volume II

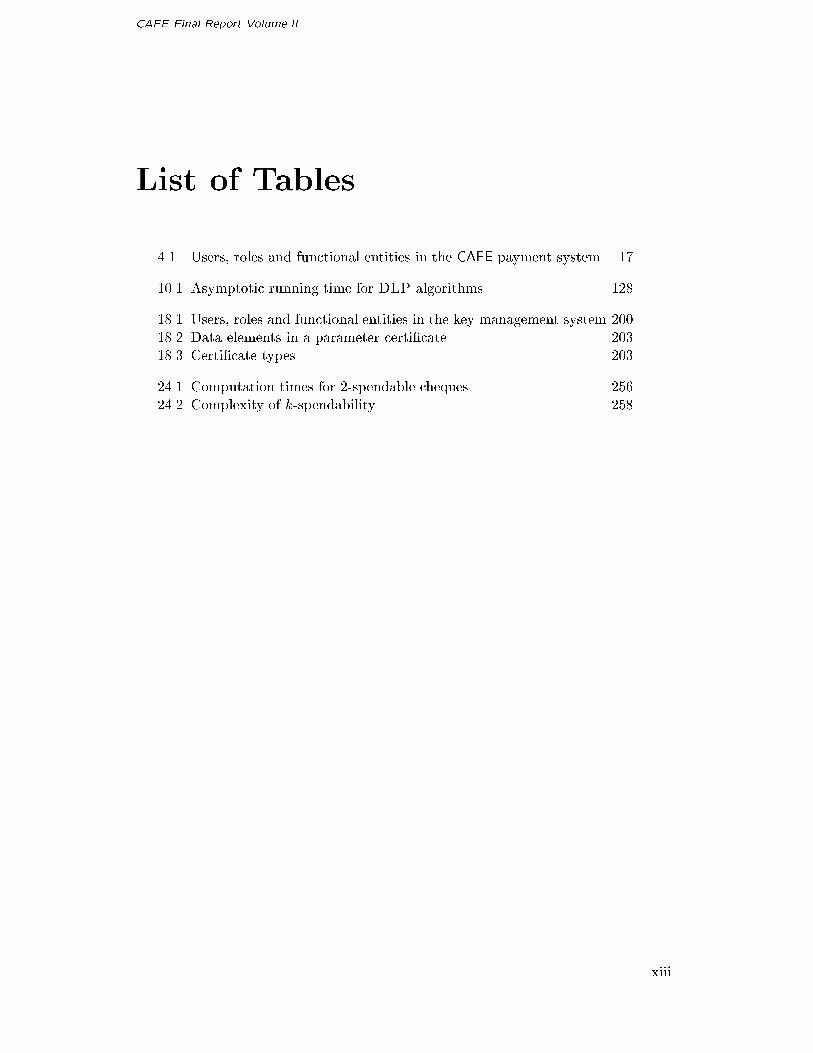

List of Tables

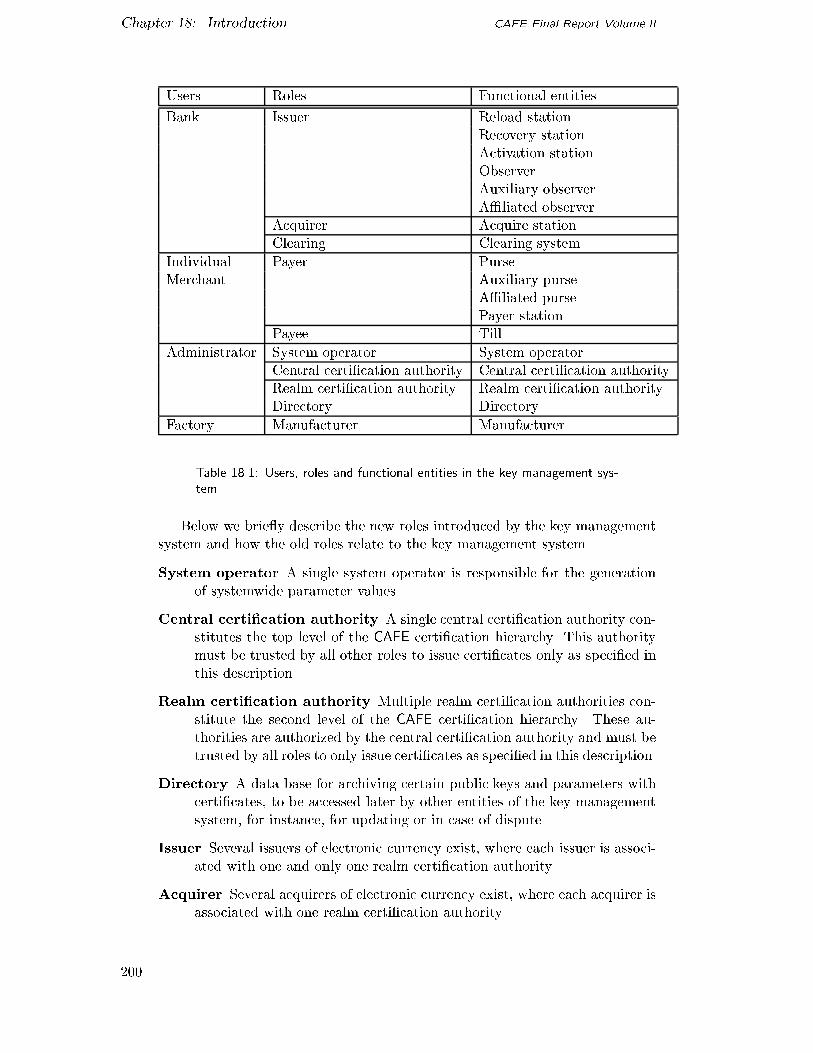

��� Users� roles and functional entities in the CAFE payment system� ��

� �� Asymptotic running time for DLP algorithms � � � � � � � � � � � ��

��� Users� roles and functional entities in the key management system�� ��� Data elements in a parameter certi�cate� � � � � � � � � � � � � � � � ���� Certi�cate types� � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

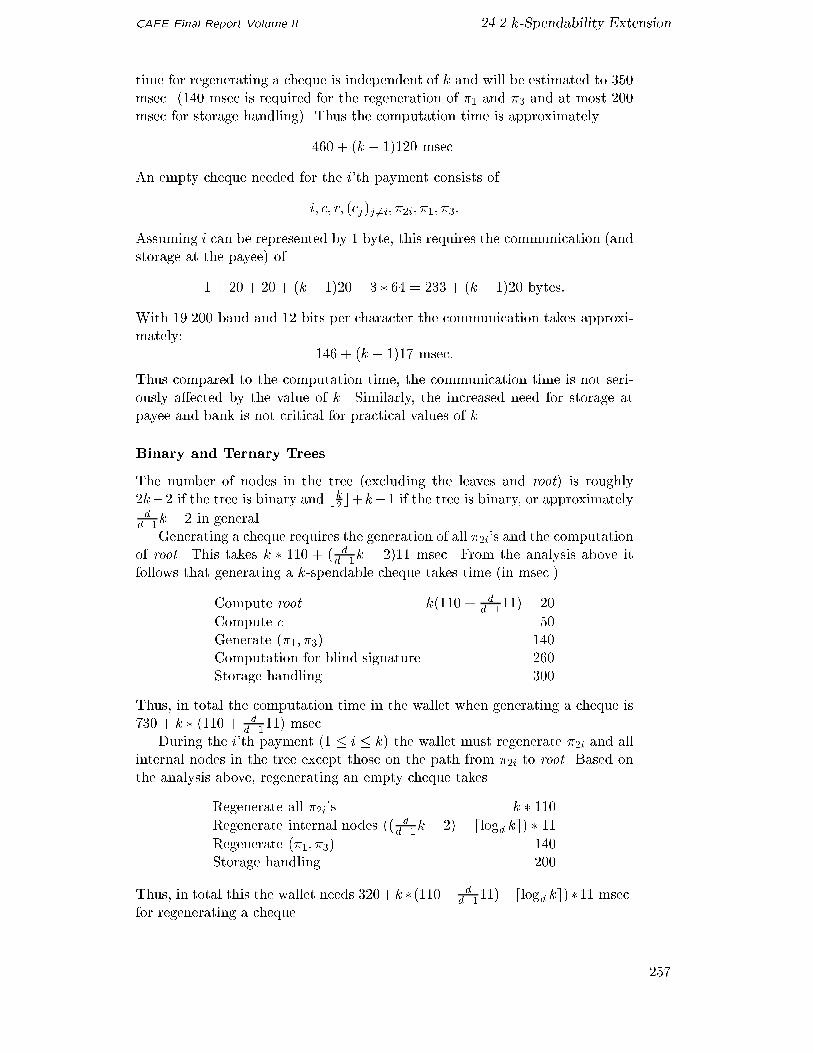

���� Computation times for ��spendable cheques � � � � � � � � � � � � ������� Complexity of k�spendability � � � � � � � � � � � � � � � � � � � � ��

xiii

List of Tables CAFE Final Report Volume II

xiv

CAFE Final Report Volume II

Preface

The report describes in detail the technical construction of an open cross�borderelectronic retail payment system that is fully capable of replacing physical cashand similar paper�based instruments� This fundamentally new currency sys�tem is well prepared for the challenges of the information age� by being basedcompletely on digital computer and communications technology�

To read and understand the entire report in detail requires in�depth knowl�edge from the �elds of computer science and cryptology� However� Part I givesa fairly brief and comprehensive overview� and should be easy to read withoutspecial knowledge�

The target audience of this report is people who take part in the technicalplanning� development� trial and deployment of new payment systems� services�and equipment� Typically� these will be people from banking and �nancial or�ganizations� equipment manufacturers� software houses� service providers� mer�chant chains� and support and consultancy companies�

The line of research concerned with constructing cryptographic protocolsthat can provide the service and security required for digital cash had its startin the early eighties� The single most in�uential researcher and motivator overthe years has been David Chaum� who also laid the �rst stepping stones for theCAFE consortium and served as chairman of the project�

The CAFE project was partly funded by the ESPRIT III program during theperiod from December �� through February ��� Field trials of an imple�mentation started in October �� at European Commission sites in Brussels�

The overall project was structured into four technical workpackages� Se�cure Protocols� Architecture� Demonstrator� and Trials � Surveys� This reportpresents the results of the Secure Protocols and Architecture workpackages�

The report is structured into seven parts� Part I� Overview� gives the basicobjectives� and outlines the structure of the system� with its functionality andsecurity properties� Part II� Architecture� describes the system and securityarchitecture� Part I and II together will give the reader a good understandingof the concepts and principles involved�

Part III� Protocols� contains a complete speci�cation of the essential pro�tocols in the system� The speci�cations are oriented toward the mathematical�cryptographic� computations in the protocols� The prerequisite to interpretthe protocol speci�cations is included in the �rst chapters of this part� Part IV�Security Evaluation� lists the security requirements and gives arguments for thesecurity of the system�

Part V� Clearing� describes the infrastructure for interbank clearing and

xv

Preface CAFE Final Report Volume II

settlement� and how the validity of the currency and the integrity of the sys�tem operation are maintained� Part VI� Key Management� speci�es how thegeneration� certi�cation� distribution and revocation of system and securityparameters are carried out in the system�

Finally� Part VII� Extensions� proposes and discusses additional protocolsand applications that can easily be accommodated by the architecture�

This report is based on several intermediate project papers and reports�but quite extensively edited by S� Mj�lsnes and R� Michelsen� A� Bosselaers�R� Hirschfeld� and R� Carter produced valuable comments on the �nal draftversions of the text�

The EditorsApril� ��

xvi

CAFE Final Report Volume II

Part I

Overview

�

CAFE Final Report Volume II

Chapter �

Objectives

The CAFE project has developed the concept of an electronic wallet containingcurrency� a pocket sized workstation that lets users undertake cash paymentselectronically at shops� payphones� vending machines� toll roads and publictransportation� An electronic wallet transacts either directly or via computernetworks with merchants� tills� service points provided by banks and otherorganizations� or with wallets held by individuals�

For backwards compatibility� the simplest type of wallet was realised in theform of a smart card� The project additionally built more complete wallets�These are self�contained with respect to user interface and external commu�nications� Such features make the wallet more secure and allow application�exibility� We envisage that electronic wallets will eventually connect to or beembedded in multi�application pocket workstations�

The CAFE results and technology represent a major step forward over anyapproach to retail electronic currency systems proposed to date� Former ap�proaches� typically employing pre�paid IC cards� are only suited to closed sys�tems with low security� A single national phone card� where the issuer andthe service provider is the same� typi�es such systems� The CAFE technology�on the other hand� is designed to operate in an open and international retailpayment system� where high security for all parties is demanded�

This report presents the speci�cations of the CAFE system� The report de�tails the security and functional design� Certainly� the aim was to keep theimplementation constraints to a minimum� thereby making it easy to adapt tonew implementation tools and devices steadily becoming available� Neverthe�less� the feasibility of the system has been veri�ed already through implemen�tations �CC�b� and a trial site �CC�a��

�

Chapter �� Objectives CAFE Final Report Volume II

�

CAFE Final Report Volume II

Chapter �

The System

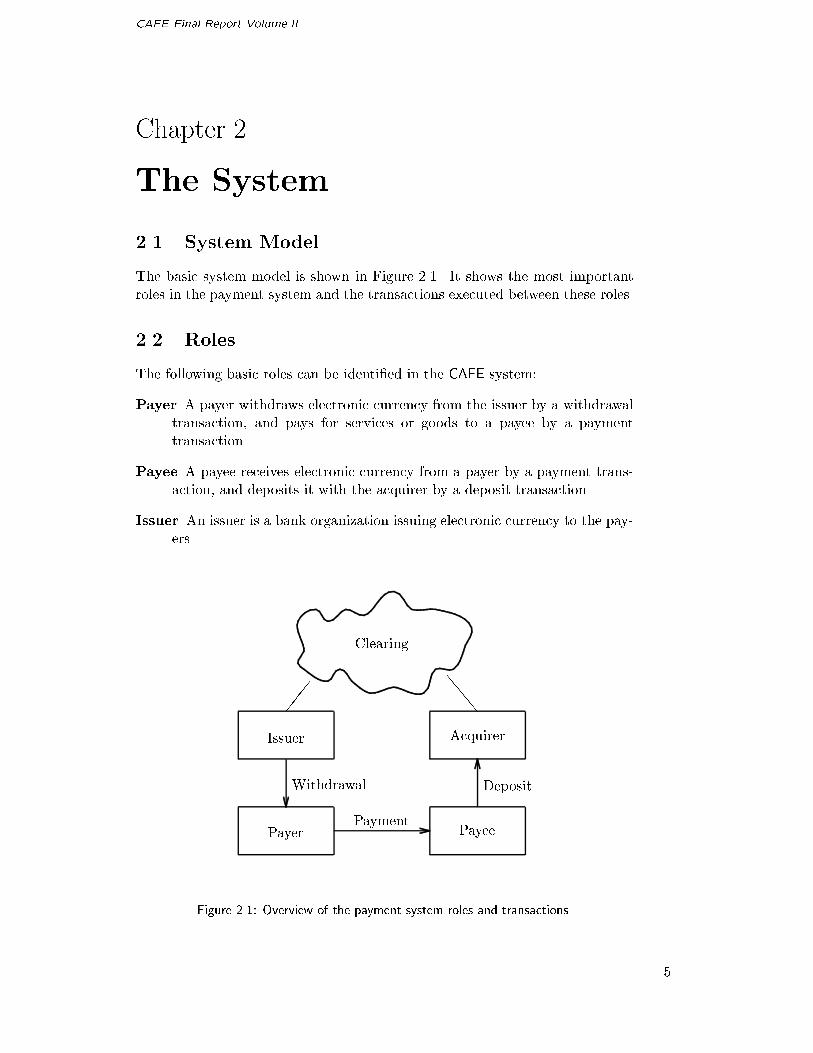

��� System Model

The basic system model is shown in Figure ���� It shows the most importantroles in the payment system and the transactions executed between these roles�

��� Roles

The following basic roles can be identi�ed in the CAFE system�

Payer A payer withdraws electronic currency from the issuer by a withdrawaltransaction� and pays for services or goods to a payee by a paymenttransaction�

Payee A payee receives electronic currency from a payer by a payment trans�action� and deposits it with the acquirer by a deposit transaction�

Issuer An issuer is a bank organization issuing electronic currency to the pay�ers�

���

eee

Payer Payee

Issuer Acquirer

Clearing

Withdrawal Deposit

Payment

Figure ���� Overview of the payment system roles and transactions�

�

Chapter �� The System CAFE Final Report Volume II

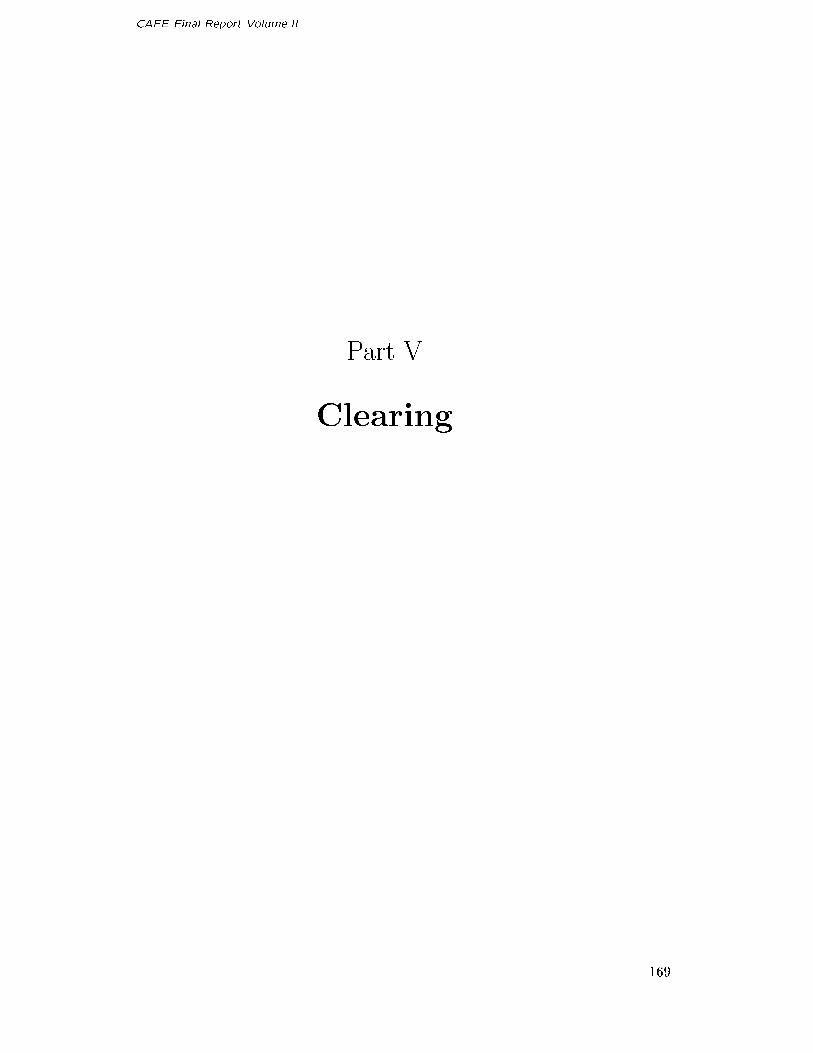

Acquirer The acquirer collects the electronic currency from the payee andforwards the cheques to the clearing�

Clearing The clearing checks the validity of electronic currency� accumulatescurrency claims from acquirers on issuers� and initiates funds transfersbetween banks�

The system is designed for an unrestricted number of both payers and payees�issuers and acquirers� The clearing role envisaged may become a distributed�possibly hierarchical structure�

��� Transactions

The most important transactions in the CAFE payment system are withdrawal�payment and deposit� These transactions realize the key services of the paymentsystem� A more detailed description of these and additional transactions aregiven in Part II�

Withdrawal This transaction is executed between an issuer and a payer� Theissuer debits the payer�s bank account by an amount speci�ed by the payerand issues the corresponding amount in electronic currency� The payermay choose his electronic currency from a list of di�erent currencies�

Payment The payment transaction is executed between a payer and a payee�At the payee�s request� the payer transfers electronic currency to thepayee� The payee veri�es the validity of the received currency and ac�cepts the payment�

Deposit The payee deposits the electronic currency received by a deposittransaction with an acquirer� The acquirer forwards the deposit record tothe clearing system and the payee�s account is credited with an amountcorresponding to the received electronic currency�

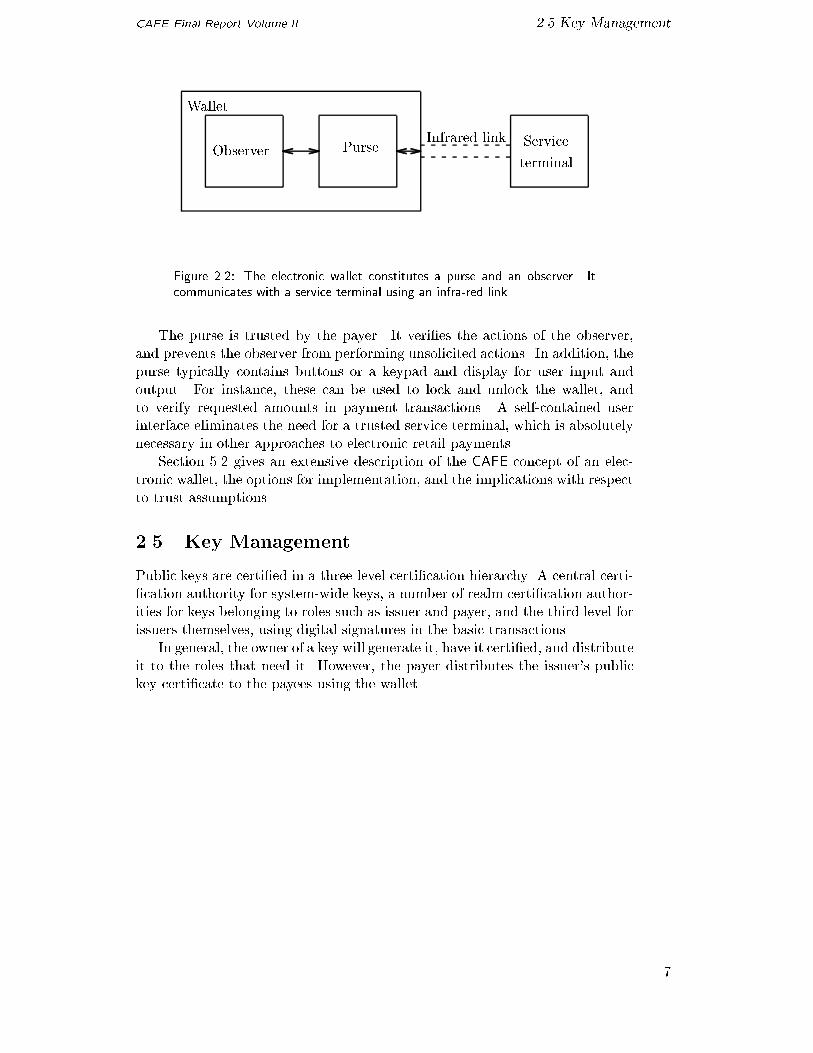

��� The Electronic Wallet

A key component in the CAFE architecture is the electronic wallet as �rst in�troduced in �Cha��� The functional entities of such an electronic wallet com�municating with a service terminal are shown in Figure ����

The electronic wallet is an essential element in the balanced security ofthe proposed CAFE system� It reduces or even eliminates many of the trustrelations required in existing electronic payment systems that are based onmagnetic stripe or IC cards�

The electronic wallet comprises an observer and a purse� The observer istrusted by the issuer and protects the issuer�s interest during o��line transac�tions� The observer restricts the amount of money the payer can spend withinthe balance stored in the observer itself� Hence� the implementation of theobserver must be tamper�resistant�

�

CAFE Final Report Volume II ��� Key Management

ObserverService

terminalPurse

Infrared link

Wallet

Figure ���� The electronic wallet constitutes a purse and an observer� Itcommunicates with a service terminal using an infra�red link�

The purse is trusted by the payer� It veri�es the actions of the observer�and prevents the observer from performing unsolicited actions� In addition� thepurse typically contains buttons or a keypad and display for user input andoutput� For instance� these can be used to lock and unlock the wallet� andto verify requested amounts in payment transactions� A self�contained userinterface eliminates the need for a trusted service terminal� which is absolutelynecessary in other approaches to electronic retail payments�

Section ��� gives an extensive description of the CAFE concept of an elec�tronic wallet� the options for implementation� and the implications with respectto trust assumptions�

��� Key Management

Public keys are certi�ed in a three level certi�cation hierarchy� A central certi��cation authority for system�wide keys� a number of realm certi�cation author�ities for keys belonging to roles such as issuer and payer� and the third level forissuers themselves� using digital signatures in the basic transactions�

In general� the owner of a key will generate it� have it certi�ed� and distributeit to the roles that need it� However� the payer distributes the issuer�s publickey certi�cate to the payees using the wallet�

�

Chapter �� The System CAFE Final Report Volume II

CAFE Final Report Volume II

Chapter �

Features

��� Introduction

The CAFE payment systems are all following the paradigm of untraceable elec�tronic cash �rst proposed by David Chaum �see �Cha���� The model for o��lineelectronic cash o�ering both integrity and privacy was introduced in �CFN ��In the same paper also a system was proposed that seems to �t that model�Various other systems using basically the same ideas have since then been pro�posed� like e�g�� �Ant � CBH� � FY�� OO � OO�� Pai�� Fer�a� Fer�b��In �Bra�� Bra�a� the digital signature schemes of �CP�b� and �HP�� arecombined into an untraceable coin system� that served as the starting point forthe cheque�based CAFE systems of Part III� that use cheques in combinationwith one or more balances� an idea that was �rst introduced in �BC ��

��� Functionality

Cash Electronic currency value in the CAFE system is pre�paid � Normally�the payer�s bank account is debited at the withdrawal� This takes place inadvance of the payment� The payment is analogous to a cash payment in thatthe money is transferred instantaneously without consulting a bank or otherintermediaries� The currency can be deposited with any acquiring bank�

O� line Payment A property of the CAFE security architecture is that thepayment can be made o��line� No connection with the issuer or any other thirdparty is required at payment time� similar to a cash payment� This featureis very important for the cost�e�ciency of low�value payments� It is also veryimportant in building a system that is robust against failures of central facilities�The payee is able to verify� without help from the issuer� that the receivedelectronic currency is valid� Forged payments are prevented at payment by thepayee� but will also be detected when the transaction is cleared� This is similarto current cash�

The mechanism used to enable the payee to check the validity is based onpublic key digital signatures� This is described in some detail in Chapter ��

Signature Transport The CAFE currency is based on signature transportingcheques� At withdrawal� cheques are signed by the issuer and transported to thepayer�s wallet� This guarantees the validity of the cheque and that the payer isa customer of the issuing bank� The issuer�s signature is veri�ed by the wallet�

Chapter �� Features CAFE Final Report Volume II

At payment� the payer�s wallet adds another signature to the cheque� now �lledin with the amount of the payment and the identity of the payee� It is thentransported to the payee� who can check the validity of the payment beforeaccepting it� The transcript of the payment are deposited with the acquirer�

Multiple Currencies The CAFE payment system provides the possibilityto pay in foreign currencies in two di�erent ways� First� the payer�s wallethas several di�erent �pockets� for di�erent currencies� During withdrawal� thepayer chooses which currencies to load� This corresponds to the service ofbuying foreign currencies at a bank today�

The second method is a currency exchange performed at payment� Thepayee accepts a number of currencies at rates set by the acquirer� and if thepayer�s wallet has any of these currencies� a payment can be performed� Thepayer pays using the preferred currency accepted by the payee� the payee de�posits the received cheque and is credited in the home currency�

CAFE therefore permits payers to prepare themselves for payment abroad byloading foreign currencies in advance� but allows the �exibility of paying in anunanticipated currency if the need should arise by using the currency exchangeduring payment�

Loss Tolerance For payers� loss tolerance is probably the most importantspecial feature of the CAFE system� If a payer loses physical notes or coins�or they are stolen� the money value is lost� Not so in the CAFE system� Losstolerance means that the issuer is able to recover the currency from a backup andthe deposit transcripts� A backup procedure is carried out in normal operationsduring withdrawal� If a payer wants to recover lost money he will �reveal� theidentity of the cheques stored after the last withdrawal to the issuer� Thisenables the issuer to trace these cheques to see if they have been spent andrefund any remaining value that was left in the wallet

Fault Tolerance The CAFE system tolerates faults and interruptions duringtransactions without either party losing any money� Interrupted transactionsare automatically recovered by the system�

Incremental Payments A complete payment transaction requires two sig�natures by the wallet� Therefore very fast payments �less than �� seconds� arenot feasible in current implementations� The payphone application is an exam�ple where incremental payment is required� To provide many fast subsequentpayments to one payee� a special extension of the basic payment protocol isused� It allows the payment of a large number of amounts within one paymenttransaction� The total is not required to be known in advance� enabling e��cient pay�as�you�go applications� After an initialization phase� where the valueof one tick and the maximum number of ticks to be used is �xed� the payer sendssubsequent ticks on request� Only the last tick is deposited together with theinformation received during initialization� For example� within one payment fora phone call� the amount is incremented for each unit spent� Rather than one

�

CAFE Final Report Volume II ��� Security

payment for each unit� there is one payment for the complete call consisting ofseveral units �Ped�� Ped���

Open Networks The CAFE protocols are designed to be secure over inse�cure networks� such as public telecommunication networks� Internet� wide andlocal area networks� including infrared links� This implies that withdrawals�payments and deposits can be undertaken without special requirements to thenetwork carrying the transactions�

��� Security

Multiparty Security The CAFE protocols achieve multilateral security byensuring veri�ability for all roles� the issuer� the payer� the payee� and the ac�quirer� In somewhat simplistic terms we can say that the integrity is maintainedunder the assumption that the issuer trusts the observer and the reload station�the payer trusts the purse� the payee trusts the till� and the acquirer trusts theacquire station� For example� the payer does not need to rely on the issuer�sreload station and the observer for the correctness of the withdrawal�

This balanced multiparty security is much more proper for open systemsthan former approaches to payment security�

Privacy If existing electronic payment systems� such as debit and creditcards� are used for everyday low�value payments� the system operator has ac�cess to an extensive pro�le of the payer�s behavior� A payee is forced to identifyits customers to maintain security in such systems� Payers may choose to keepon using cash� because it provides untraceability� Cash usage does not requirepayer identi�cation by the payee or the issuer� Moreover� di�erent paymentsperformed by the same payer are unlinkable with respect to the information dis�seminated in the payments� It is simply not possible for merchants and banksto pick out notes and coins that were spent by the same individual�

The basic CAFE system provides the same privacy as cash� The payer is un�traceable with respect to payment transactions� if the payer so wishes� Neitherthe payee nor the issuer will learn the identity of the payer from the paymentitself� and di�erent payments are unlinkable �Cha��� Blind signatures �Cha��constitute the cryptographic means by which this privacy protection is achieved�

Forgery Protection Currency value in the transaction is represented byelectronic bits� which of course may be easily copied� Potentially� the originaland the copy may both be spent �double spending�� The payee is not able todecide whether he can accept the o�ered money� without contacting the acquirerto ask if these bits have already been deposited� This solution will require anonline payment� which is not cost e�cient for low�value payments in a retailenvironment�

The CAFE system employs two means to counter this threat� tamper�resistantobserver device and �after�the�fact� detection and tracing of the double spender�

��

Chapter �� Features CAFE Final Report Volume II

The tamper�resistance of the observer device protects copying and modi��cations to the currency� and makes it infeasible to spend electronic currencytwice� The tamper�resistance guarantees the integrity of the issuer to the payeein an o�ine payment�

If the tamper�resistance of an observer device is broken� copying and dou�ble spending of currency cannot be prevented� However� double spending willbe detected by the clearing� because the CAFE protocols ensure that doublespending payments are no longer anonymous transactions� The identity ofthe observer device will be computed and the forgery can be cryptographicallyproved from two payment transcripts� This restricts the potential gain of break�ing tamper�resistance� because the forger will be traced� and the system willblacklist double spent cheques�

Robbery Protection A merchant �payee� will no longer need to be con�cerned with cash robberies� The electronic currency accepted in payments is�dedicated� to the payee� and only represents value to the payee� Physicalprotection of the till is not required� However� the currency value can easilybe destroyed due to storage erasure� consequently storage must be su�cientlyprotected against this risk�

Audit In common with all existing electronic payment systems� the CAFE ar�chitecture does not provide anonymity and untraceability to the payee� Hence�all payments received are fully auditable by normal standards� All paymentshave to be deposited to one or more acquiring banks� and will show in thepayee�s account entries� This makes it very di�cult if not impossible to acceptelectronic currency as black money without the bank�s consent and collusion�

Bribery using electronic currency appears unattractive� The payee will runthe risk of incrimination by the payer� because the payer is always able toproduce cryptographic evidence of the payment� In addition� the payee willhave to deposit the bribe to a bank� where it will enter the accounts�

The withdrawal transactions are completely auditable by the issuer by stan�dards� The payer can audit the payment transactions completely by normalstandards� Withdrawal� payment and deposit transactions can be provablylinked if the payer so wishes�

PIN Verication The CAFE observer is involved in all transactions� The ob�server will however not participate in a transaction without being activated bythe payer entering a password or �number �PIN�� The CAFE system permits theuse of two di�erent PINs�one for withdrawal �for accessing the account bal�ance� and the other for payments and transfers �for unlocking a payer�speci�edamount of the wallet balance �Det���� It is possible to use the same PIN� butthis represents a small reduction of the system�s security�

��

CAFE Final Report Volume II

Part II

Architecture

��

CAFE Final Report Volume II

Chapter �

System Architecture

��� Requirements

The Trials � Surveys workpackage of the project collected user and expertrequirements and properties� Here we present a list of important requirementsthat have a major impact on the technical solutions of the architecture� andwhich the system satis�es� Much of the model� requirements� and additionalfunctionality ideas are based on �Cha� BP� PWP ��

Security The payment system and its applications should o�er a high level ofsecurity to all parties� where security means an appropriate combinationof integrity� privacy and veri�ability�

Privacy Payment transactions should protect the privacy of the payer�

Low cost Low value payments should be o��line to minimize payment trans�action cost�

Loss tolerance If the wallet becomes damaged� stolen or lost� the ownershould be able to obtain a complete refund of the lost currency value�

Limited transferability Unlimited transferability may have negative side�e�ects such as the black�market activity� money laundering and lost rev�enues for acquirers� It should however be possible to transfer value ifwallet a�liation has been prearranged�

Cross border The wallet should be able to contain several currencies� andallow for withdrawal and payment in those currencies� Also� the systemshould provide for currency exchange and paying with non�local currency�

Reliability There should be no consequences resulting from interrupted trans�actions when the wallet is used�

Compatibility It should be possible to retro�t existing terminal equipmentto transact with electronic wallets�

Open It must be possible for banks� merchants� and individuals to enter andleave the system at all times�

Standard The system speci�cations must be open and be capable of becomingan international standard�

��

Chapter �� System Architecture CAFE Final Report Volume II

Users

Roles

Functional Entities

Devices

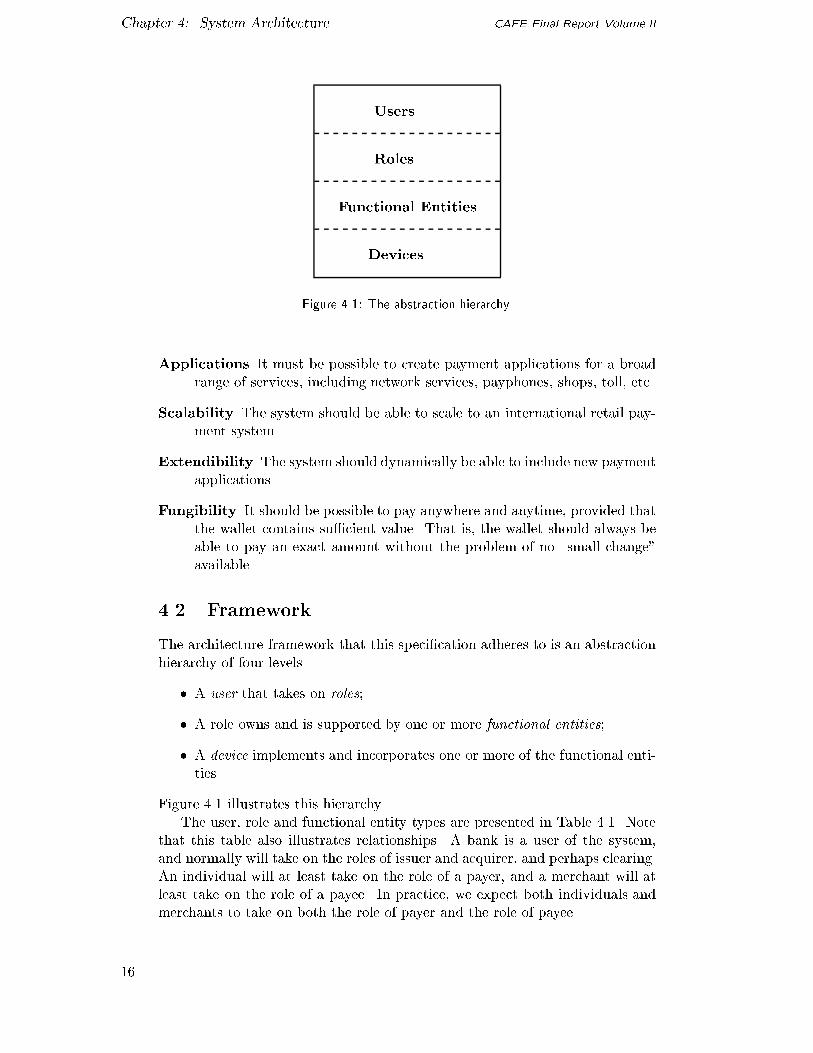

Figure ���� The abstraction hierarchy�

Applications It must be possible to create payment applications for a broadrange of services� including network services� payphones� shops� toll� etc�

Scalability The system should be able to scale to an international retail pay�ment system�

Extendibility The system should dynamically be able to include new paymentapplications�

Fungibility It should be possible to pay anywhere and anytime� provided thatthe wallet contains su�cient value� That is� the wallet should always beable to pay an exact amount without the problem of no �small change�available�

��� Framework

The architecture framework that this speci�cation adheres to is an abstractionhierarchy of four levels�

� A user that takes on roles�

� A role owns and is supported by one or more functional entities�

� A device implements and incorporates one or more of the functional enti�ties�

Figure ��� illustrates this hierarchy�

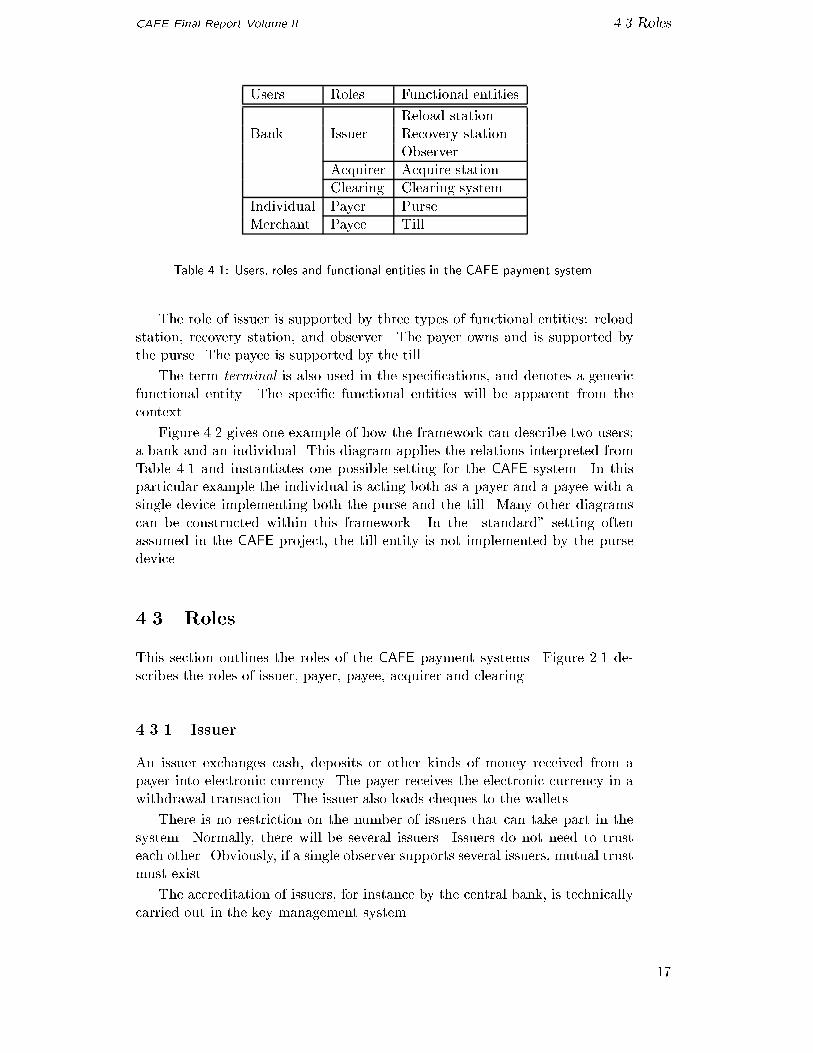

The user� role and functional entity types are presented in Table ���� Notethat this table also illustrates relationships� A bank is a user of the system�and normally will take on the roles of issuer and acquirer� and perhaps clearing�An individual will at least take on the role of a payer� and a merchant will atleast take on the role of a payee� In practice� we expect both individuals andmerchants to take on both the role of payer and the role of payee�

��

CAFE Final Report Volume II ��� Roles

Users Roles Functional entities

Reload stationBank Issuer Recovery station

ObserverAcquirer Acquire stationClearing Clearing system

Individual Payer PurseMerchant Payee Till

Table ���� Users� roles and functional entities in the CAFE payment system�

The role of issuer is supported by three types of functional entities� reloadstation� recovery station� and observer� The payer owns and is supported bythe purse� The payee is supported by the till�

The term terminal is also used in the speci�cations� and denotes a genericfunctional entity� The speci�c functional entities will be apparent from thecontext�

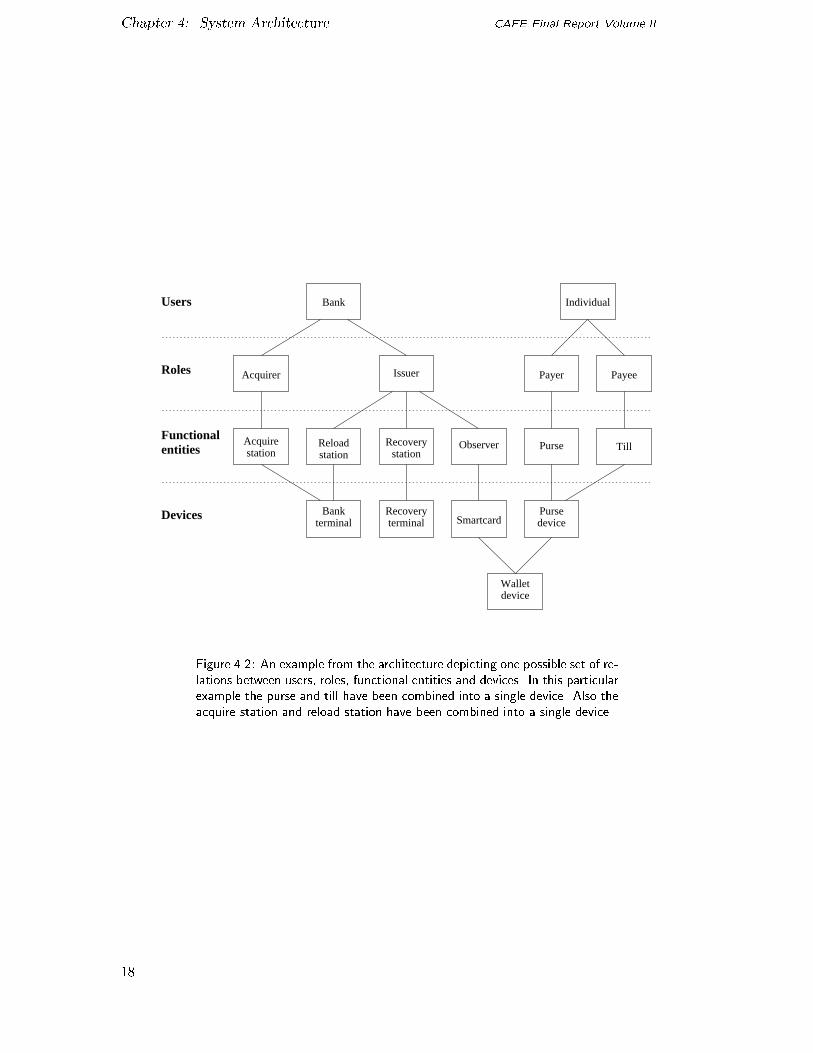

Figure ��� gives one example of how the framework can describe two users�a bank and an individual� This diagram applies the relations interpreted fromTable ��� and instantiates one possible setting for the CAFE system� In thisparticular example the individual is acting both as a payer and a payee with asingle device implementing both the purse and the till� Many other diagramscan be constructed within this framework� In the �standard� setting oftenassumed in the CAFE project� the till entity is not implemented by the pursedevice�

��� Roles

This section outlines the roles of the CAFE payment systems� Figure ��� de�scribes the roles of issuer� payer� payee� acquirer and clearing�

����� Issuer

An issuer exchanges cash� deposits or other kinds of money received from apayer into electronic currency� The payer receives the electronic currency in awithdrawal transaction� The issuer also loads cheques to the wallets�

There is no restriction on the number of issuers that can take part in thesystem� Normally� there will be several issuers� Issuers do not need to trusteach other� Obviously� if a single observer supports several issuers� mutual trustmust exist�

The accreditation of issuers� for instance by the central bank� is technicallycarried out in the key management system�

��

Chapter �� System Architecture CAFE Final Report Volume II

Acquirestation

Recoverystation

Reloadstation

Walletdevice

Individual

Payer Payee

TillPurse

Pursedevice

Bankterminal

Recoveryterminal

Functionalentities Observer

Acquirer Issuer

Bank

SmartcardDevices

Users

Roles

Figure ���� An example from the architecture depicting one possible set of re�lations between users� roles� functional entities and devices� In this particularexample the purse and till have been combined into a single device� Also theacquire station and reload station have been combined into a single device�

�

CAFE Final Report Volume II ��� Transactions

����� Payer

The payer withdraws electronic currency from the issuer and spends it withpayment transactions� The payer is supported by the purse� However� thepayer has to use a wallet� consisting of a purse that connects to an observer� toexecute withdrawal� payment and recovery transactions�

The observer is initialized and provided to the payer by the issuer�

����� Payee

The payee� supported by the till� gets paid by a payer in a payment transaction�The electronic currency can be deposited and redeemed by any acquirer thepayee has a prior agreement with�

Both individuals and organizations can take on the role of a payee� Forindividuals� the till will most conveniently be incorporated in the electronicwallet device� For merchants� the till will be implemented by the cash register�

����� Acquirer

The acquirer collects electronic currency from the payees by accepting deposittransactions� It is the responsibility of the acquirer to submit the collectedcurrency to the clearing and credit the value to the payee� normally directly toa bank account�

A single payee can deposit currency with one or more acquirers� The ac�quirer may aggregate deposit records over a period of time� then sort and submitfor clearing in batches�

���� Clearing

The clearing receives �batches of� deposit data and checks validity and doublespending� It also initiates settlement between di�erent issuers and acquirers�The clearing performs other tasks as well� such as distributing black lists�

The clearing role is supported by either a centralized or a distributed clear�ing system�

��� Transactions

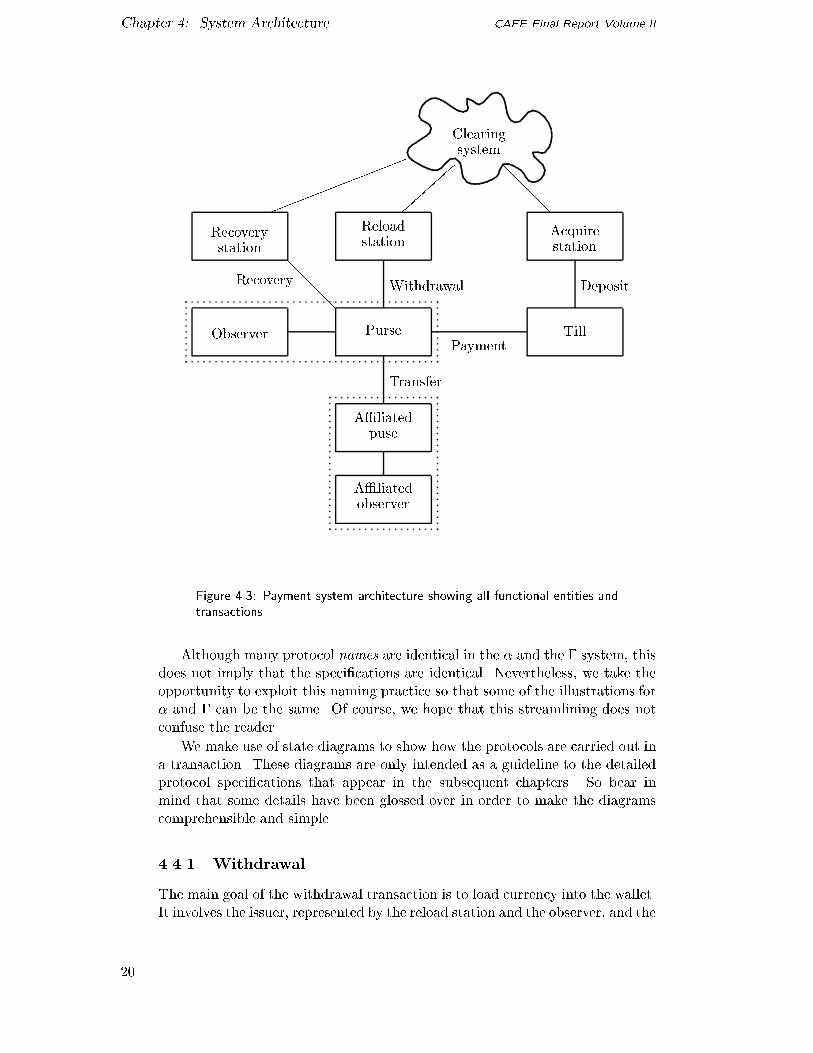

This section describes the payment system transactions� Figure ��� shows thefunctional entities and the transactions that can be executed�

In the transaction descriptions we break down each transaction into individ�ual protocols� A detailed description of each protocol can be found in Part III�

We choose to view the transactions from the wallet�s side� both because thewallet takes part in the most important transactions security�wise� and becausethis description will re�ect su�ciently the actions of other entities�

We will have to distinguish the � wallet� the �� wallet� and the � wallet�A detailed knowledge about the di�erent wallet types is not required in a �rstreading of the transaction description in this section� Please refer to Section ���for a description of these distinct types of wallets�

�

Chapter �� System Architecture CAFE Final Report Volume II

Reloadstation

Acquirestation

Clearingsystem

Recoverystation

Observer

A�liatedpuse

A�liatedobserver

�����

��

��

��

��

����

����

���

Purse Till

Withdrawal

Payment

Deposit

Transfer

Recovery

Figure ���� Payment system architecture showing all functional entities andtransactions�

Although many protocol names are identical in the � and the � system� thisdoes not imply that the speci�cations are identical� Nevertheless� we take theopportunity to exploit this naming practice so that some of the illustrations for� and � can be the same� Of course� we hope that this streamlining does notconfuse the reader�

We make use of state diagrams to show how the protocols are carried out ina transaction� These diagrams are only intended as a guideline to the detailedprotocol speci�cations that appear in the subsequent chapters� So bear inmind that some details have been glossed over in order to make the diagramscomprehensible and simple�

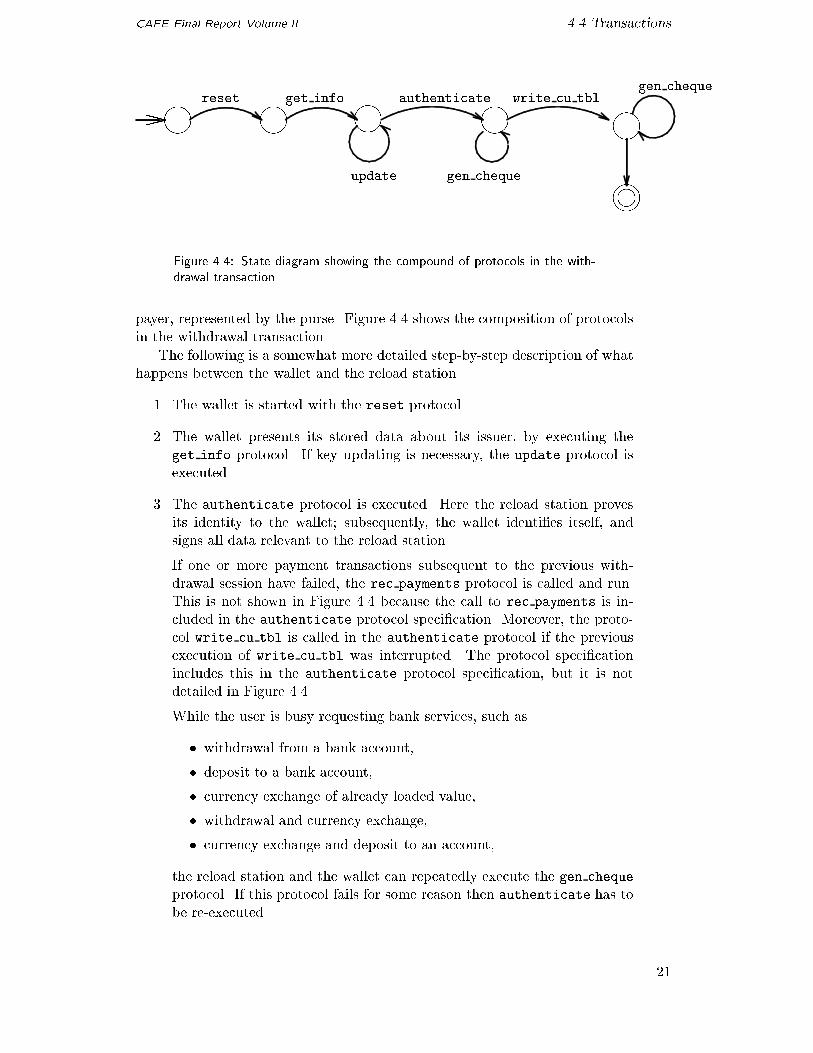

����� Withdrawal

The main goal of the withdrawal transaction is to load currency into the wallet�It involves the issuer� represented by the reload station and the observer� and the

�

CAFE Final Report Volume II ��� Transactions

����l

����

����

����

����

����

��XXreset get info authenticate

gen chequeupdate

write cu tblgen cheque

Figure ���� State diagram showing the compound of protocols in the with�drawal transaction�

payer� represented by the purse� Figure ��� shows the composition of protocolsin the withdrawal transaction�

The following is a somewhat more detailed step�by�step description of whathappens between the wallet and the reload station�

�� The wallet is started with the reset protocol�

�� The wallet presents its stored data about its issuer� by executing theget info protocol� If key updating is necessary� the update protocol isexecuted�

�� The authenticate protocol is executed� Here the reload station provesits identity to the wallet� subsequently� the wallet identi�es itself� andsigns all data relevant to the reload station�

If one or more payment transactions subsequent to the previous with�drawal session have failed� the rec payments protocol is called and run�This is not shown in Figure ��� because the call to rec payments is in�cluded in the authenticate protocol speci�cation� Moreover� the proto�col write cu tbl is called in the authenticate protocol if the previousexecution of write cu tbl was interrupted� The protocol speci�cationincludes this in the authenticate protocol speci�cation� but it is notdetailed in Figure ����

While the user is busy requesting bank services� such as

� withdrawal from a bank account�

� deposit to a bank account�

� currency exchange of already loaded value�

� withdrawal and currency exchange�

� currency exchange and deposit to an account�

the reload station and the wallet can repeatedly execute the gen cheque

protocol� If this protocol fails for some reason then authenticate has tobe re�executed�

��

Chapter �� System Architecture CAFE Final Report Volume II

����

����

����

���� l��

����XX

reset get info

get certif

paymentshow currencies

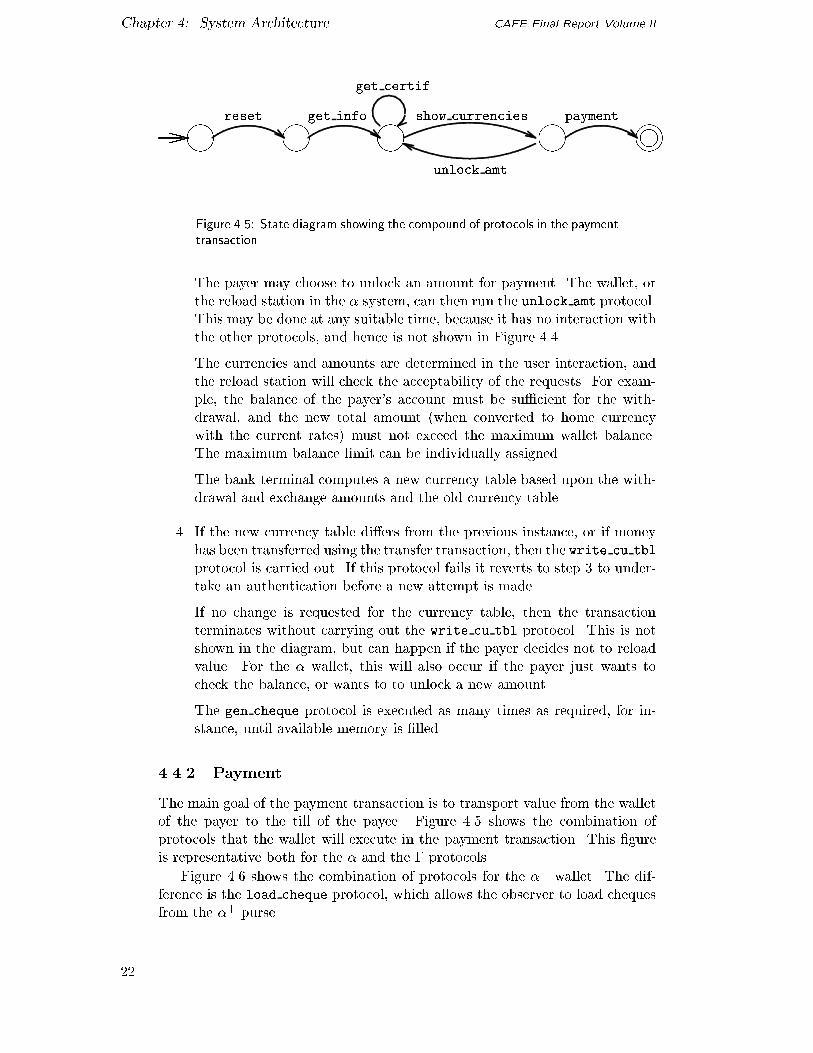

unlock amt

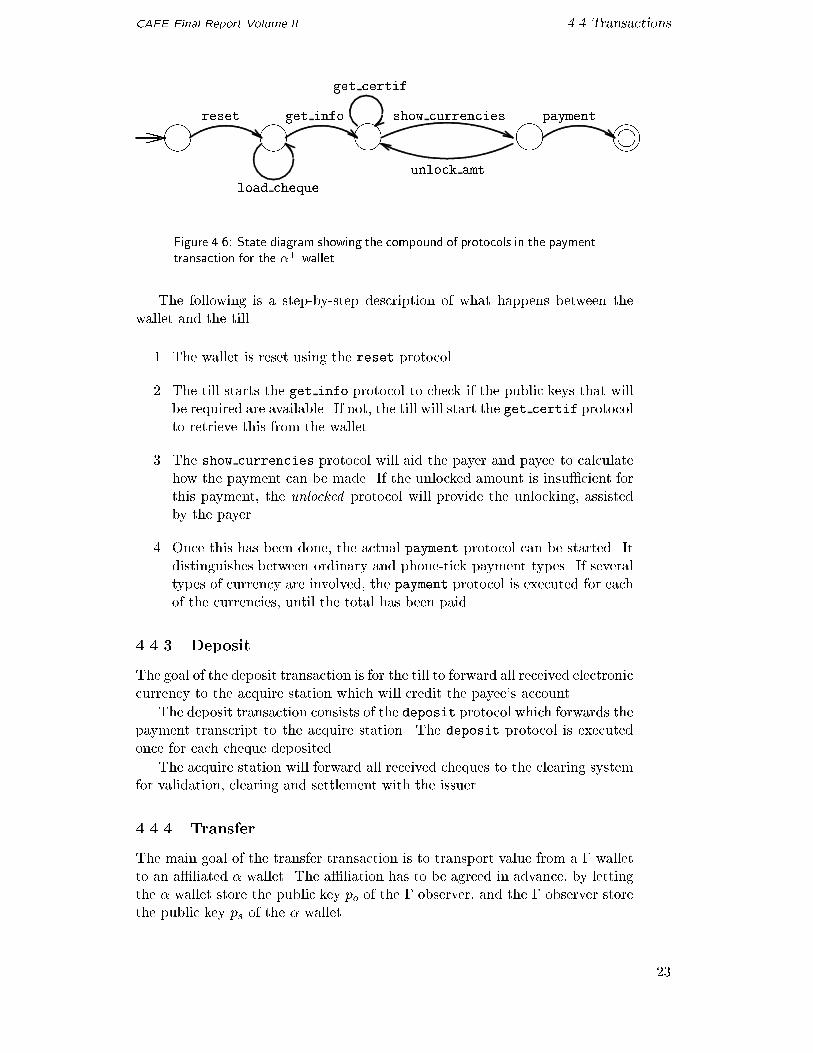

Figure ��� State diagram showing the compound of protocols in the paymenttransaction

The payer may choose to unlock an amount for payment� The wallet� orthe reload station in the � system� can then run the unlock amt protocol�This may be done at any suitable time� because it has no interaction withthe other protocols� and hence is not shown in Figure ����

The currencies and amounts are determined in the user interaction� andthe reload station will check the acceptability of the requests� For exam�ple� the balance of the payer�s account must be su�cient for the with�drawal� and the new total amount �when converted to home currencywith the current rates� must not exceed the maximum wallet balance�The maximum balance limit can be individually assigned�

The bank terminal computes a new currency table based upon the with�drawal and exchange amounts and the old currency table�

�� If the new currency table di�ers from the previous instance� or if moneyhas been transferred using the transfer transaction� then the write cu tbl

protocol is carried out� If this protocol fails it reverts to step � to under�take an authentication before a new attempt is made�

If no change is requested for the currency table� then the transactionterminates without carrying out the write cu tbl protocol� This is notshown in the diagram� but can happen if the payer decides not to reloadvalue� For the � wallet� this will also occur if the payer just wants tocheck the balance� or wants to to unlock a new amount�

The gen cheque protocol is executed as many times as required� for in�stance� until available memory is �lled�

����� Payment

The main goal of the payment transaction is to transport value from the walletof the payer to the till of the payee� Figure ��� shows the combination ofprotocols that the wallet will execute in the payment transaction� This �gureis representative both for the � and the � protocols�

Figure ��� shows the combination of protocols for the �� wallet� The dif�ference is the load cheque protocol� which allows the observer to load chequesfrom the �� purse�

��

CAFE Final Report Volume II ��� Transactions

����

����

����

����

����l��XX

reset get info

get certif

paymentshow currencies

unlock amt

load cheque

Figure ��� State diagram showing the compound of protocols in the paymenttransaction for the �� wallet

The following is a step�by�step description of what happens between thewallet and the till�

�� The wallet is reset using the reset protocol�

�� The till starts the get info protocol to check if the public keys that willbe required are available� If not� the till will start the get certif protocolto retrieve this from the wallet�

�� The show currencies protocol will aid the payer and payee to calculatehow the payment can be made� If the unlocked amount is insu�cient forthis payment� the unlocked protocol will provide the unlocking� assistedby the payer�

�� Once this has been done� the actual payment protocol can be started� Itdistinguishes between ordinary and phone�tick payment types� If severaltypes of currency are involved� the payment protocol is executed for eachof the currencies� until the total has been paid�

����� Deposit

The goal of the deposit transaction is for the till to forward all received electroniccurrency to the acquire station which will credit the payee�s account�

The deposit transaction consists of the deposit protocol which forwards thepayment transcript to the acquire station� The deposit protocol is executedonce for each cheque deposited�

The acquire station will forward all received cheques to the clearing systemfor validation� clearing and settlement with the issuer�

����� Transfer

The main goal of the transfer transaction is to transport value from a � walletto an a�liated � wallet� The a�liation has to be agreed in advance� by lettingthe � wallet store the public key po of the � observer� and the � observer storethe public key ps of the � wallet�

��

Chapter �� System Architecture CAFE Final Report Volume II

����l��

������

��XXreset

rollback

transfer

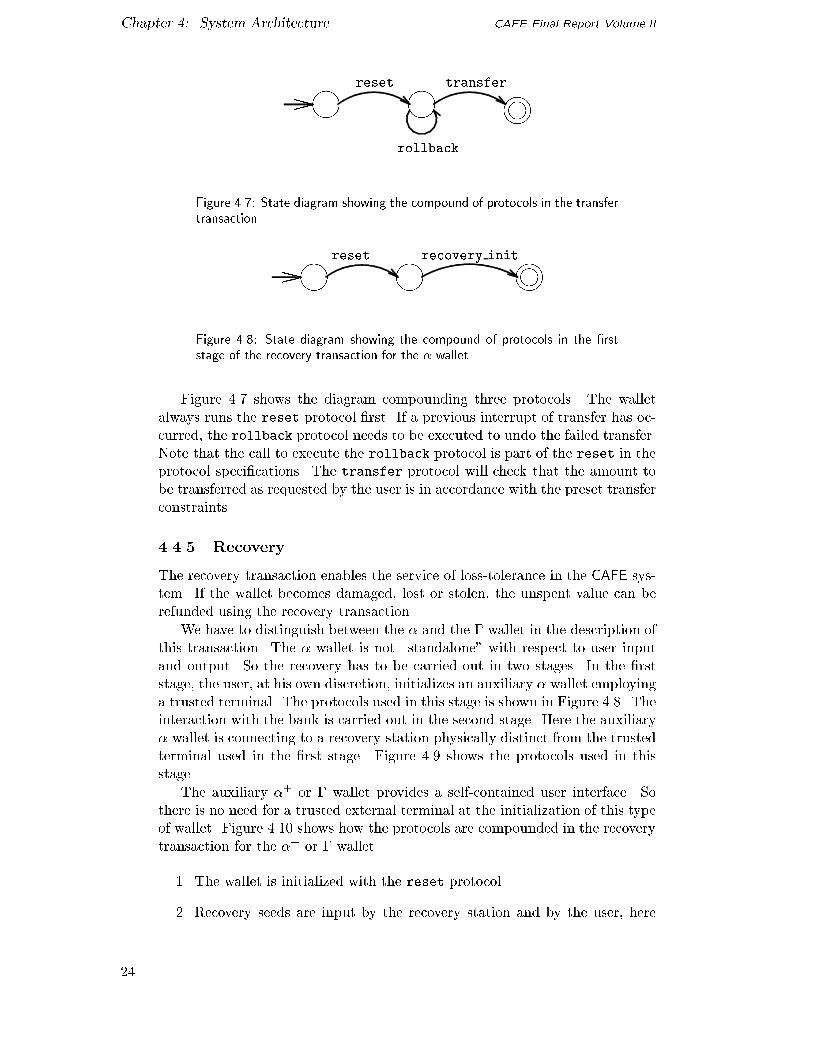

Figure ���� State diagram showing the compound of protocols in the transfertransaction�

����

����

����l��XX

reset recovery init

Figure ���� State diagram showing the compound of protocols in the rststage of the recovery transaction for the � wallet�

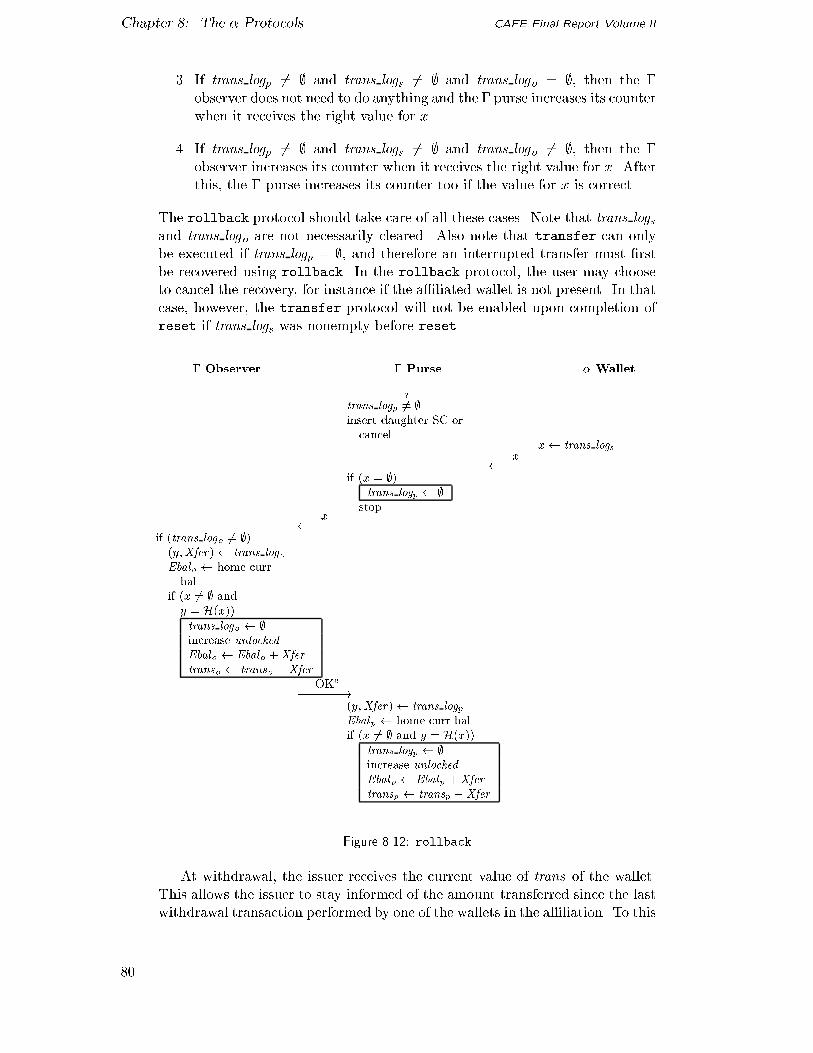

Figure ��� shows the diagram compounding three protocols� The walletalways runs the reset protocol �rst� If a previous interrupt of transfer has oc�curred� the rollback protocol needs to be executed to undo the failed transfer�Note that the call to execute the rollback protocol is part of the reset in theprotocol speci�cations� The transfer protocol will check that the amount tobe transferred as requested by the user is in accordance with the preset transferconstraints�

���� Recovery

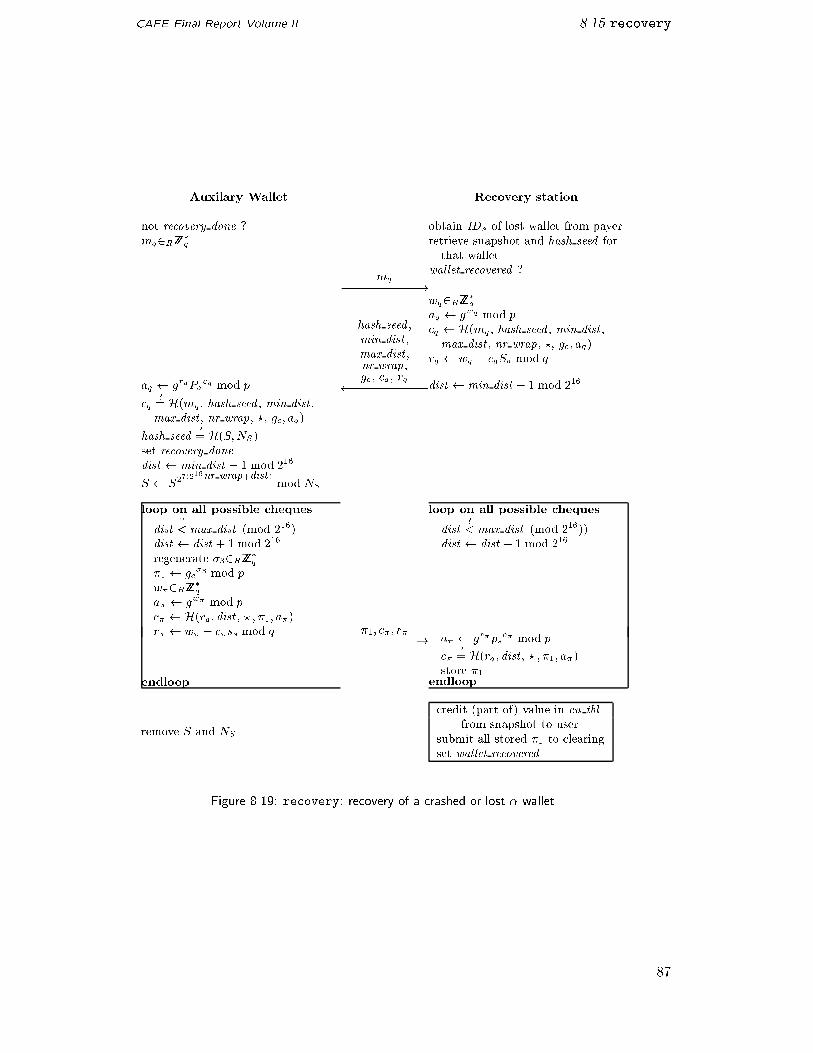

The recovery transaction enables the service of loss�tolerance in the CAFE sys�tem� If the wallet becomes damaged� lost or stolen� the unspent value can berefunded using the recovery transaction�

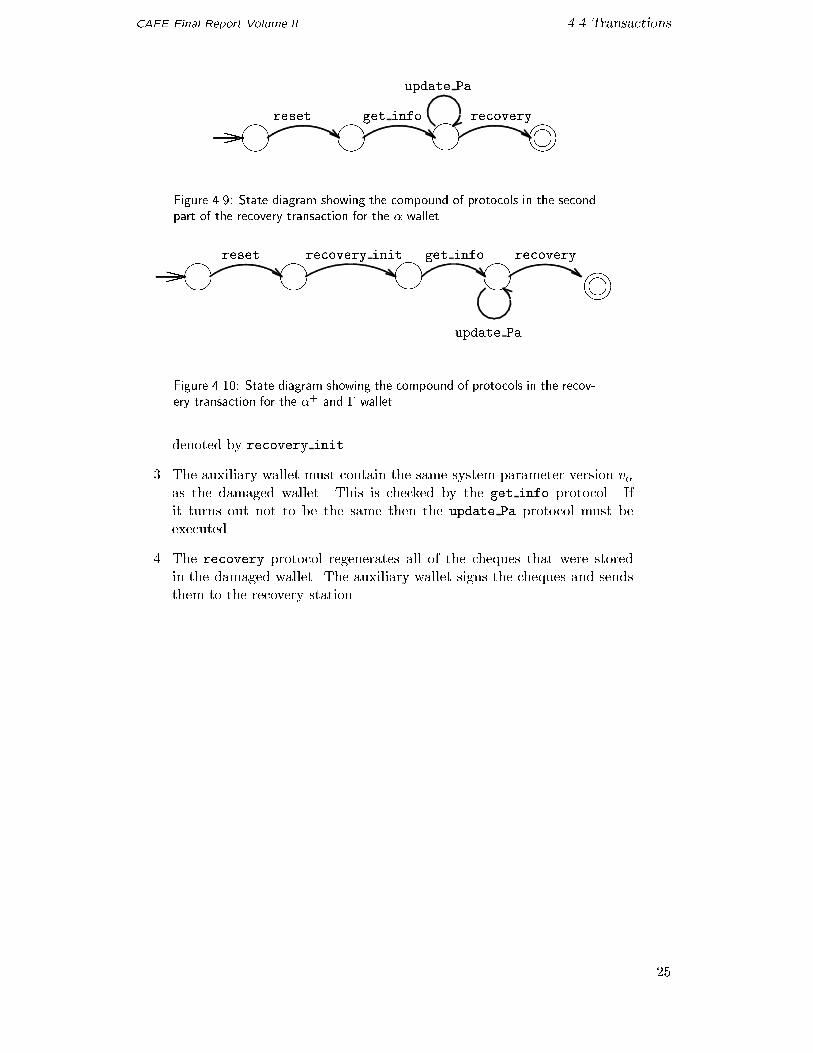

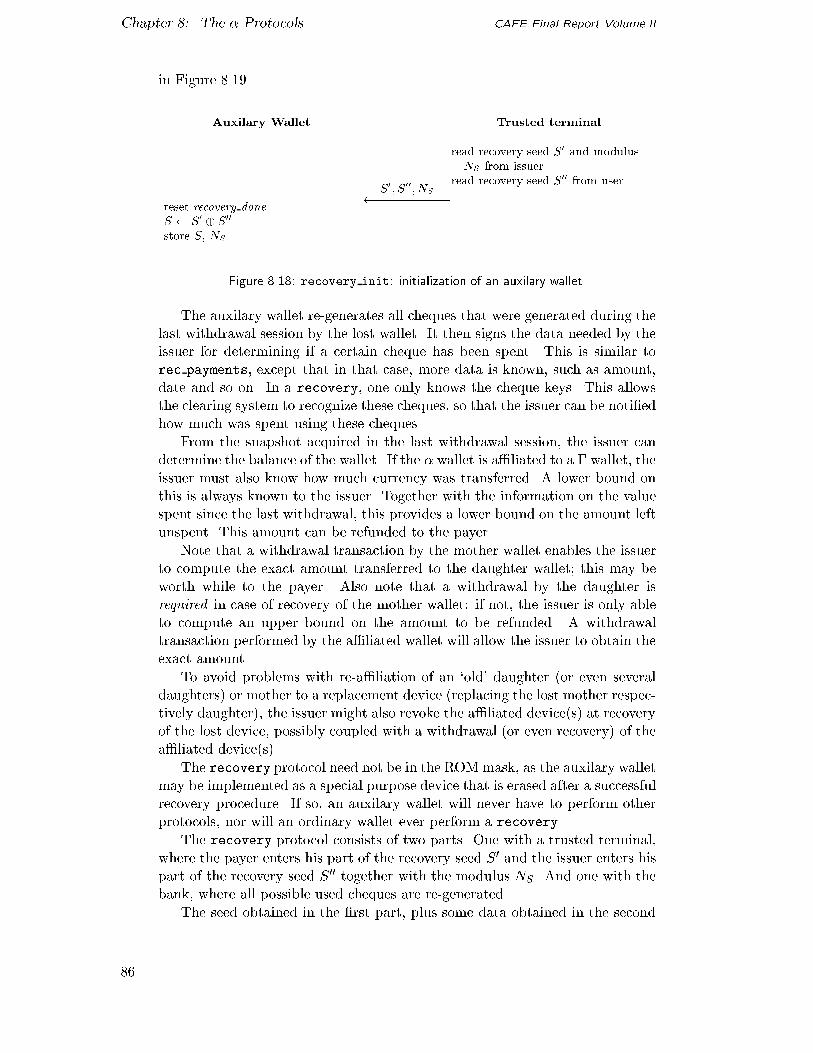

We have to distinguish between the � and the � wallet in the description ofthis transaction� The � wallet is not �standalone� with respect to user inputand output� So the recovery has to be carried out in two stages� In the �rststage� the user� at his own discretion� initializes an auxiliary � wallet employinga trusted terminal� The protocols used in this stage is shown in Figure ��� Theinteraction with the bank is carried out in the second stage� Here the auxiliary� wallet is connecting to a recovery station physically distinct from the trustedterminal used in the �rst stage� Figure �� shows the protocols used in thisstage�

The auxiliary �� or � wallet provides a self�contained user interface� Sothere is no need for a trusted external terminal at the initialization of this typeof wallet� Figure ��� shows how the protocols are compounded in the recoverytransaction for the �� or � wallet�

�� The wallet is initialized with the reset protocol�

�� Recovery seeds are input by the recovery station and by the user� here

��

CAFE Final Report Volume II ��� Transactions

����

����

����

����l��XX

reset get info

update Pa

recovery

Figure ���� State diagram showing the compound of protocols in the secondpart of the recovery transaction for the � wallet�

����l��

������

����

����

��XXreset recovery init get info

update Pa

recovery

Figure ����� State diagram showing the compound of protocols in the recov�ery transaction for the �� and � wallet�

denoted by recovery init�

�� The auxiliary wallet must contain the same system parameter version v�as the damaged wallet� This is checked by the get info protocol� Ifit turns out not to be the same then the update Pa protocol must beexecuted�

�� The recovery protocol regenerates all of the cheques that were storedin the damaged wallet� The auxiliary wallet signs the cheques and sendsthem to the recovery station�

��

Chapter �� System Architecture CAFE Final Report Volume II

��

CAFE Final Report Volume II

Chapter �

Security Architecture

��� Security Approaches

The security of the CAFE architecture is based both on public key cryptog�raphy and on tamper�resistant devices� In this section we describe how thesetechniques are combined into a high security system�

���� Cryptographic Protocols

The di�erent roles in the payment system interact using cryptographic proto�cols� Cryptographic techniques are used to protect the integrity of the systemby providing�

Authentication of parties Cryptographic identi�cation protocols are usedto authenticate peers in a secure way� These protocols are secure againstpowerful attacks such as replay of authentication information obtainedfrom a previous run of the protocol�

Authentication of messages Digital signatures are used to authenticate mes�sages� Authenticated messages ensure that the sender of a certain mes�sage can be established without doubt and also provides non�repudiationof messages and accountability�

Integrity protection of information Cryptographic techniques are used toprotect messages sent between peers from being modi�ed�

���� TamperResistance

The CAFE payment system is based on the currency value being represented bya number of balances in electronic wallets held by payers� These balances mustbe updated only through the execution of well de�ned transactions supportedby cryptographic mechanisms� Modi�cation of balances must not be possiblewithout executing a complete and valid transaction�

To protect against unsolicited modi�cation� the balances are maintainedby a tamper�resistant device that implements the functionality of an observerentity� In this project� the tamper�resistant device is in the form of a smartcard�

The observer must change the balance only if a valid withdrawal or pay�ment transaction has been carried out� The tamper�resistance of the smartcard chip prevents the payer �and others� from bypassing the cryptographic

��

Chapter �� Security Architecture CAFE Final Report Volume II

mechanisms and protocols by changing �increasing� the balances with physicaland electronical means�

���� FallBack Security

It is hard to quantify just how secure a tamper�resistant device is� No integratedcircuit tamper�resistance techniques is believed to survive continuous and sus�tained attacks� The techniques have to keep up with the attacker techniques�If an attacker should succeed to break the tamper�resistance of a device� theCAFE system provides fall�back security based on cryptographic techniques�

While the tamper resistant observer device prevents the payer from spend�ing more money than he has withdrawn� the cryptographic fall back securitypermits identi�cation of counterfeiting payers during the clearing process�

The wallet contains cheques in addition to the balances� The cheques aregenerated and stored in the wallet during the withdrawal transaction� A uniquecheque is spent in each payment transaction� and it is the observer�s task toprevent that the same cheque is used in two di�erent payment transactions� Ifa payer is able to break the tamper resistance of the observer device and forgethe balance� the wallet will soon run out of cheques� If the cheating payer triesto use a cheque twice� he will be identi�ed by the system�

��� The Electronic Wallet

A key concept in the CAFE architecture is the electronic wallet� which is de�scribed in detail in this section�

���� Introduction

In the CAFE project we use the term electronic wallet to denote the functionalentity used by payers to interact with other roles during transactions�

An electronic wallet comprises an observer and a purse� The observer func�tionality is trusted by the issuer� The purpose of the observer is to preventthe payer from spending more money than is available in the wallet� Since theobserver device is embedded in the wallet� and under physical control of thepayer� it has to be tamper resistant�

The purse is an entity trusted by the payer� It is responsible for all wal�let input output� such as communication with service terminals and the userinterface� The purse also veri�es the actions of the observer� The purse willdetect if the observer performs actions not sanctioned by the payer� The pursewill also �reformulate� outgoing messages to prevent that the observer commu�nicates side information� The goal of an observer�s deviating actions may beunsolicited payments or leaking of private information� The purse will see to itthat this cannot happen�

A wallet device consisting of physically distinct observer and purse devices isdesirable when considering trust relations� The issuer must trust the observer�The issuer is the only role that has to trust the observer� Therefore an issuer

�

CAFE Final Report Volume II ��� The Electronic Wallet

may choose an observer device developer and manufacturer that it trusts� Sim�ilarly� the payer is the only role that must trust the purse� Therefore a payercan obtain the purse from a manufacturer or retailer that this individual payertrusts� No functional entity has to be trusted by more roles that do not trusteach other because of potentially con�ict of interest�

A sketch of an electronic wallet communicating with a service terminal isshown in Figure ����

Many di�erent implementations of electronic wallets can be envisaged� Al�though simplistic� the electronic wallet can be realised in the form of smart cardwhere both the observer and the purse functionality are implemented on thesame chip� A more user�friendly wallet implement takes on a form similar toa pocket calculator� where display and keypad are included� The observer willtypically be implemented in the form of an embedded tamper resistant chip ora smart card inserted into the wallet�

The CAFE system is also suitable for payments over open networks� suchas Internet� In this case an electronic wallet can be implemented employing apersonal computer� Typically� the purse functionality will be realised by a soft�ware module running on the computer� while the observer will be implementedby a plug�in PC Card hardware module�

���� � Wallet

Realisation The � �alpha� system provides an upgrade path from existingelectronic retail payment systems based on magnetic stripe and chip cards� Inthe � wallet both the purse and the observer can be implemented in a singletamper resistant chip�typically embedded in a smart card�

The � wallet has limited capabilities� The purse can only communicate withthe environment through the card�s electrical contacts� The payer has to rely onexternal equipment for correctness� such as total amount and PIN entry� Thewallet device will not always remain under the payer�s physical control becauseit has to be inserted into terminal equipment�

The number of cheques will be restricted by a quite strong limit on thestorage space in single�chip implementations� This implies a limitation on thenumber of payment transactions that can be executed before additional chequesare required� In practice the balance is more likely to be spent before the chequesupply is exhausted�

Trust Relations The combination of observer and purse into a single devicemeans that both the issuer and the payer has to trust this device� The issuermust trust that the wallet limits the spending of the payer according to thewallet balance� and the payer must trust the wallet not to implement hiddenfeatures� such as revealing the payer�s identity in a payment transaction�

The payer must also trust a number of service terminals� The till is typicallyimplemented by a point�of�sale terminal with a display and a keypad used forveri�cation of amount to pay and PIN entry for authorization of the paymenttransaction� This terminal must be trusted by the payer to display the cor�rect information� not to copy or store PINs and only to execute the speci�ed

�

Chapter �� Security Architecture CAFE Final Report Volume II

protocols with the wallet�

Similar trust requirements apply for other terminals with which the walletperforms transactions� such as the terminal implementing the reload station�

���� �� Wallet

Realisation The �� wallet is an improvement of the � wallet with respectto user interface� It consists of an � wallet extended with with user interfaceand communication capabilities�

The �� observer is quite similar to the � observer� The �� purse func�tionality is extended with user interface capabilities� The implementation mayhave some buttons for use by the payer to con�rm an action� For instance�acknowledgment of correct amount in a payment transaction� The purse willalso contain facilities for communicating without physical contact � typicallyan infra�red link�

The �� wallet implementation is not limited to a single chip� so the storagespace is not restricted to on�chip memory� This allows for more cheque storagespace� which means that more payment transactions can be performed beforeconnecting to the issuer�

In summary� the �� wallet o�ers the following improvements to the � wallet�

� A single user interface for the payer�

� Display for stand�alone veri�cation of actions�

� A few function�speci�c buttons for stand�alone PIN entry and user ac�knowledge of actions�

� Extendible storage of cheques�

� External communications by an infra�red link enables the payer to havefull physical control over the wallet�

Trust Relations The issuer must trust the observer to limit spending to thebalance stored in the observer�

Still� the payer cannot check the � purse functionality because it is imple�mented on the same chip as the observer� The purse must be trusted not tocontain �hidden� features which may allow the wallet to leak additional infor�mation such as the payer�s identity�

The �� wallet nulli�es the need to trust the service terminals� The payer willnot have to hand over the wallet to the payee� PIN entering and veri�cation ofamounts will be undertaken locally by the payer� using the display and buttonson the wallet device�

���� � Wallet

Realisation The � �gamma� wallet is a fully functional wallet� It containsa � observer� typically implemented by a single tamper resistant chip� andembedded in the � purse device� The purse has processing capabilities� memory

�

CAFE Final Report Volume II ��� Key Management

and input output facilities� A � wallet will typically take the form of a smallpocket device with display� keypad and infra�red link for communicating withservice terminals�

In summary� the � wallet o�ers the following improvements over the ��

wallet�

� Better performance because the purse has computing power and can ex�ecute parts of the protocols�

� Signi�cantly better privacy and security characteristics� because the purseis able to check and verify the actions of the observer�

� A user interface that can be adapted to the payer�s requirements�

Trust Relations The issuer must trust the observer to limit the spendingaccording to the wallet balance�

Almost all trust assumptions by the payer with respect to the observer thatis needed for the � wallet can be removed by employing the � wallet� The payerstill has to trust the � observer to perform PIN veri�cation� according to theprotocol speci�cation�

The payer must trust the � purse to function according to the speci�cation�The purse is responsible for interaction both with the payer and with serviceterminals� In addition� the purse checks all actions performed by the observerto prevent the observer from releasing unsolicited bits of information to serviceterminals�

��� Key Management

This section provides a brief overview of the key management architecture� Thecomplete description of the key management system for the CAFE paymentsystem can be found in Part VI�

���� Certi�cation Authorities

In every cryptographic system cryptographic keys have to be distributed in atrusted manner� Alice can only validate a digital signature allegedly from Bobif she has access to Bob�s public key� If there is any chance that an impostoris able to fool Alice into using a di�erent public key� then Alice can�t trustsignatures allegedly generated by Bob� Alice can only trust Bob�s public keyif she gets it through a secure channel� for instance directly from Bob in aface�to�face meeting�

For an open retail payment system such as CAFE it is clearly impractical torequire that all peers exchange public keys in face�to�face meetings� A publickey is therefore certi�ed by a certi�cation authority using the certi�cation au�thority�s digital signature� If Alice receives a key certi�ed by an authority� shewill trust this key if she has a trusted copy of the certi�cation authority�s publickey� In this way we have reduced the problem from having to establish a securechannel to every other peer in the system to a single certi�cation authority�

��

Chapter �� Security Architecture CAFE Final Report Volume II

���� Certi�cation Hierarchy

In CAFE the keys are certi�ed in a certi�cation hierarchy� The certi�cationhierarchy is organized in three levels�

�� A single central certi�cation authority constitutes the top of the certi��cation hierarchy� The public key of this role must be available to andtrusted by all participants in the system� It is used for certi�cation ofglobal keys and keys of the realm certi�cation authorities�