Mod 2 - TVM - Compounding - Slides

22

7/7/15 1 Michael R. Roberts William H. Lawrence Professor of Finance The Wharton School, University of Pennsylvania Time Value of Money: Compounding Copyright © Michael R. Roberts Copyright © Michael R. Roberts Last Time Time Value of Money • Intuition – time units like different currencies • Tools – time line and discount factor • Discounting – Moving CFs back in time • Lesson: Don’t add CFs with different time units…ever!

description

Compounding - Slides

Transcript of Mod 2 - TVM - Compounding - Slides

7/7/15

1

Michael R. Roberts William H. Lawrence Professor of Finance The Wharton School, University of Pennsylvania

Time Value of Money: Compounding

Copyright © Michael R. Roberts

Copyright © Michael R. Roberts

Last TimeTime Value of Money• Intuition – time units like different

currencies• Tools – time line and discount factor• Discounting – Moving CFs back in time• Lesson: Don’t add CFs with different time

units…ever!

7/7/15

2

Copyright © Michael R. Roberts

This TimeTime Value of Money• Compounding

USING THE TOOLS: COMPOUNDING

Copyright © Michael R. Roberts

7/7/15

3

Compounding

0 1 2 3 4

CF0 CF1 CF2 CF3 CF4

CF2 1+R( )2

CF3 1+R( )1

CF1 1+R( )3

CF0 1+R( )4

Compounding CFs moves them forward in time

Copyright © Michael R. Roberts

Compounding

0 1 2 3 4

CF0 CF1 CF2 CF3 CF4

CF2 1+R( )2

CF3 1+R( )1

CF1 1+R( )3

CF0 1+R( )4

Compounding CFs moves them forward in time

t > 0 because we are moving cash flows forward in time

Copyright © Michael R. Roberts

7/7/15

4

Compounding

0 1 2 3 4

CF0 CF1 CF2 CF3 CF4

CF2 1+R( )2

CF3 1+R( )1

CF1 1+R( )3

CF0 1+R( )4

Compounding CFs moves them forward in time

We can add/subtract these CFs because they are in the same time units (date 4)

Copyright © Michael R. Roberts

Future Value

0 1 2 3 4

CF0 CF1 CF2 CF3 CF4

CF2 1+R( )2 = FV4 CF2( )

CF3 1+R( )1 = FV4 CF3( )

CF1 1+R( )3 = FV4 CF1( )

CF0 1+R( )4 = FV4 CF0( )

Future value, FVt(�) of CFs is compounded value of CFs as of t

These are future values of CFs as of year 4

Copyright © Michael R. Roberts

7/7/15

5

How much money will I have after three years if I invest $1,000 in a savings account paying 3.5% interest per annum?

Example 1 – Savings

Copyright © Michael R. Roberts

How much money will I have after three years if I invest $1,000 in a savings account paying 3.5% interest per annum?

Example 1 – Savings

Copyright © Michael R. Roberts

0 1 2 3

?1,000

Step 1: Put cash flows on a time line

7/7/15

6

How much money will I have after three years if I invest $1,000 in a savings account paying 3.5% interest per annum?

Example 1 – Savings

Copyright © Michael R. Roberts

0 1 2 3

1,000

Step 2: Move cash flow forward

1,000 1+ 0.035( )3

How much money will I have after three years if I invest $1,000 in a savings account paying 3.5% interest per annum?

Example 1 – Savings

Copyright © Michael R. Roberts

0 1 2 3

1,000

Step 2: Move cash flow forward

1,108.7179

7/7/15

7

How much money will I have after three years if I invest $1,000 in a savings account paying 3.5% interest per annum?

Example 1 – Savings

Copyright © Michael R. Roberts

0 1 2 3

1,000

Step 2: Move cash flow forward

1,108.7179

This is the future value of the 1,000

How much money will we have four years from today if we save $100 a year, beginning today, for the next three years, assuming we earn 5% per annum?

Example 2 – Savings

Copyright © Michael R. Roberts

7/7/15

8

How much money will we have four years from today if we save $100 a year, beginning today, for the next three years, assuming we earn 5% per annum?

Example 2 – Savings

Copyright © Michael R. Roberts

0 1 2 3 4

?100 100 100100

Step 1: Put cash flows on a time line

Example 2 – Savings

0 1 2 3 4

100 1+ 0.05( )2

100 1+ 0.05( )

100 1+ 0.05( )3

100 1+ 0.05( )4

100 100 100100 ?

Copyright © Michael R. Roberts

Step 2: Move CFs forward in time

7/7/15

9

Example 2 – Savings

0 1 2 3 4

110.25

105.00

115.763

121.551

100 100 100100 ?

Copyright © Michael R. Roberts

Step 2: Move CFs forward in time

Example 2 – Savings

0 1 2 3 4

110.25

105.00

115.763

121.551

100 100 100100

+

+

+

+

= 452.564

Copyright © Michael R. Roberts

Step 3: Add up cash flows

7/7/15

10

Interpretation 1: We will have $452.56 at the end of four years if we save $100 starting today for the next three years and our money earns 5% per annum.

Example 2 – Savings

0 1 2 3 4

100 100 100100 452.564

Copyright © Michael R. Roberts

Interpretation 2: The future value four years from today of saving $100 starting today for the next three years at 5% per annum is $452.56.

Example 2 – Savings

0 1 2 3 4

100 100 100100 452.564

Copyright © Michael R. Roberts

7/7/15

11

Example 2 – Savings (Account)

Year InterestPre-Deposit

Balance DepositPost-Deposit

Balance0 $100.00 $100.00

Copyright © Michael R. Roberts

Example 2 – Savings (Account)

Year InterestPre-Deposit

Balance DepositPost-Deposit

Balance0 $100.00 $100.001 $5.00

Copyright © Michael R. Roberts

100 × 0.05

7/7/15

12

Example 2 – Savings (Account)

Year InterestPre-Deposit

Balance DepositPost-Deposit

Balance0 $100.00 $100.001 $5.00 $105.00

Copyright © Michael R. Roberts

100 + 5.00=

Example 2 – Savings (Account)

Year InterestPre-Deposit

Balance DepositPost-Deposit

Balance0 $100.00 $100.001 $5.00 $105.00

Copyright © Michael R. Roberts

FV1 100( ) = 100 × 1+ 0.05( )1=

7/7/15

13

Example 2 – Savings (Account)

Year InterestPre-Deposit

Balance DepositPost-Deposit

Balance0 $100.00 $100.001 $5.00 $105.00 $100.00

Copyright © Michael R. Roberts

Example 2 – Savings (Account)

Year InterestPre-Deposit

Balance DepositPost-Deposit

Balance0 $100.00 $100.001 $5.00 $105.00 $100.00 $205.00

Copyright © Michael R. Roberts

105 +100=

7/7/15

14

Example 2 – Savings (Account)

Year InterestPre-Deposit

Balance DepositPost-Deposit

Balance0 $100.00 $100.001 $5.00 $105.00 $100.00 $205.002 $10.25 $215.25 $100.00 $315.253 $15.76 $331.01 $100.00 $431.014 $21.55 $452.56 $0.00 $452.56

Copyright © Michael R. Roberts

More Generally

0 1 2 3 4

CF0 CF1 CF2 CF3 CF4

CF4 1+R( )−2 = PV2 CF4( )

CF3 1+R( )−1 = PV2 CF3( )

CF1 1+R( )1 = FV2 CF1( )

CF0 1+R( )2 = FV2 CF0( )

Can add CFs at any point in time if same units

Copyright © Michael R. Roberts

7/7/15

15

Summary

Copyright © Michael R. Roberts

Lessons

• We use compounding to move cash flows forward in time

• Denote the value of cash flows in the future as future value FVs (CFt)

Copyright © Michael R. Roberts

FVs CFt( ) =CFt 1+R( )s−t for t < s

7/7/15

16

Coming up next

• Problem Set

• Useful shortcuts for PV and FV of common streams of cash flows

Copyright © Michael R. Roberts

Problems

Copyright © Michael R. Roberts

7/7/15

17

Problem Instructions

Copyright © Michael R. Roberts

These problems are designed to test your understanding of the material and ability to apply what you have learned to situations that arise in practice – both personal and professional. I have tried to retain the spirit of what you will encounter in practice while recognizing that your knowledge to this point may be limited. As such, you may see similar problems in future modules that expand on these or incorporate important institutional features.

Know that all of the problems can be solved with what you have learned in the current and preceding modules. Good luck!

Which of the following future value notations denotes the value as of period six of a cash flow received today?

a) FV0(CF6)b) FV6(CF0)c) FV4(CF)d) FV0(CF0)e) FV6(CF6)

Problem – Notation 1

Copyright © Michael R. Roberts

0 1 2 3 4

CF0

5 6

FV6(CF0)

7/7/15

18

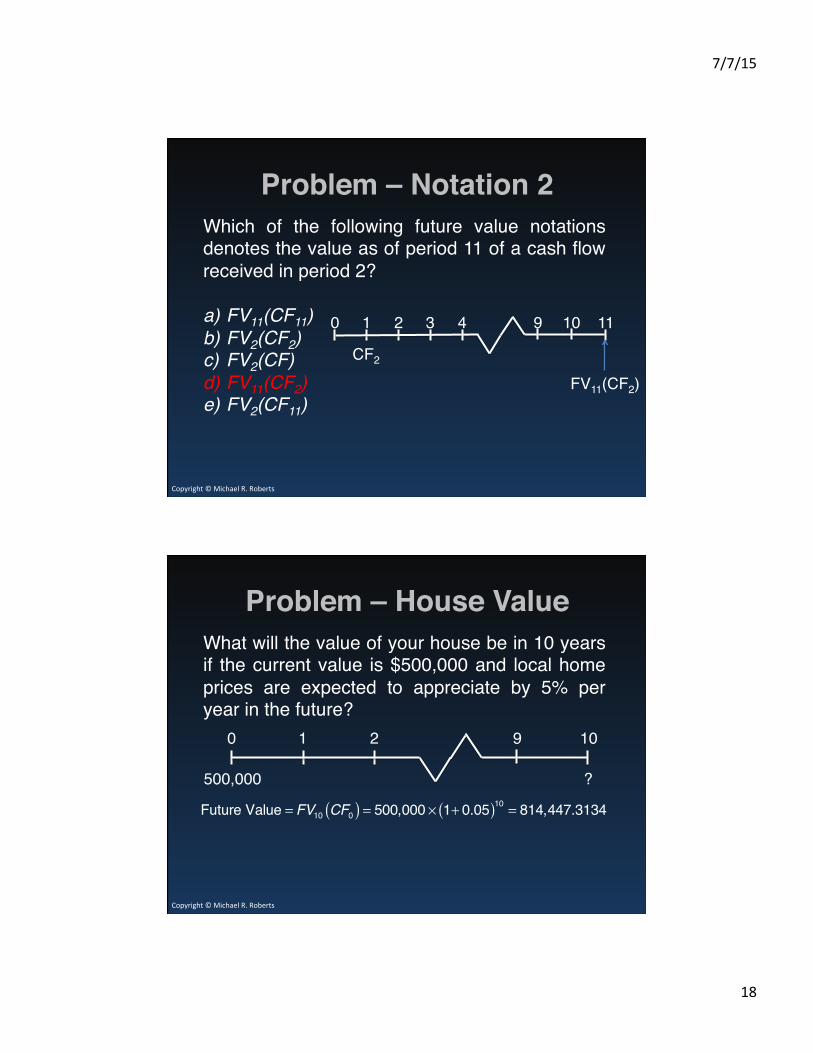

Which of the following future value notations denotes the value as of period 11 of a cash flow received in period 2?

a) FV11(CF11)b) FV2(CF2)c) FV2(CF)d) FV11(CF2)e) FV2(CF11)

Problem – Notation 2

Copyright © Michael R. Roberts

0 1 2 10

CF2

113 4

FV11(CF2)

9

What will the value of your house be in 10 years if the current value is $500,000 and local home prices are expected to appreciate by 5% per year in the future?

Problem – House Value

Copyright © Michael R. Roberts

Future Value = FV10 CF0( ) = 500,000 × 1+ 0.05( )10 = 814,447.3134

0 1 2 9

500,000 ?

10

7/7/15

19

Your expect to earn $60,000 in after-tax income this year and expect that income to grow by 3% per year thereafter. If you save 10% of your income each year, how much will you have at the end of four years if you can invest that money at 6% per annum? Assume that you are paid at the end of each year and that you will receive your first paycheck one year from today?

Problem 1 – Savings

Copyright © Michael R. Roberts

Problem 1 – Savings (Cont.)

Copyright © Michael R. Roberts

0 1 2 3

60,000 x 1.033

Period

60,000 60,000 x 1.03

60,000 x 1.032

4

Income

Savings 6,556.366,000.00 6,180.00 6,365.40

FV 6,556.36

=6,556.36

6,000 x 1.063

= 7,146.10

6,180 x 1.062

= 6,943.85

6,365.40 x 1.06

=6,747.32+ + +

FV = 27,393.63

7/7/15

20

Imagine that your goal is to retire 34 year from today with $1,000,000 in savings. Assuming you currently have $5,000 in savings, what rate of return must you earn on that savings to hit your goal?

Problem 2 – Savings

Copyright © Michael R. Roberts

0 1 2 33

5,000

343 4 32

1,000,000

FV34 5,000( ) = 5,000 1+R( )34 = 1,000,000 ⇒R = 1,000,0005,000

⎛⎝⎜

⎞⎠⎟

1/34

−1= 16.86%

, or

PV0 1,000,000( ) = 1,000,0001+R( )34 = 5,000 ⇒R = 1,000,000

5,000⎛⎝⎜

⎞⎠⎟

1/34

−1= 16.86%

How much money do you need to save each year for the next three years, starting next year, in order to have $12,000 at the end of the fourth year? Assume that you save the same amount each year and that you earn 3% per annum.

Problem 3 – Savings

Copyright © Michael R. Roberts

CF CF CF

CF 1+ 0.05( )3 +CF 1+ 0.05( )2 +CF 1+ 0.05( )1 = 12,000⇒CF = 12,000 1.053 +1.052 +1.05⎡⎣ ⎤⎦

−1= 3,625.24

0 1 2 3Period 4

12,000

7/7/15

21

Assume that you will be saving each year for three years, starting next year. If your first year savings is $2,500, at what constant rate must your savings grow each year to hit your target of $12,000 at the end of four years if your savings earn 5% per annum?

Problem 4 – Savings

Copyright © Michael R. Roberts

2,500 2,500(1+g) CF(1+g)2

0 1 2 3Period 4

12,0002,500 1+ 0.05( )3 + 2,500 1+ g( ) 1+ 0.05( )2 + 2,500 1+ g( )2 1+ 0.05( )1 = 12,000⇒ 1+ g( )2 +1.05 1+ g( )− 3.4689 = 0⇒ g = 41.01%

Just prior to making the first payment, you find out your child has received a scholarship that pays for tuition and all expenses. So, instead of spending $130,428 per year for four years beginning immediately, you decide to save that money in an account earning 5% per annum and gift it to her when she graduates in four years. How much money will she receive?

Problem – Education

Copyright © Michael R. Roberts

0 1 2 3

?130,428

Period

130,428 130,428 130,428

4

7/7/15

22

Just prior to making the first payment, you find out your child has received a scholarship that pays for tuition and all expenses. So, instead of spending $130,428 per year for four years beginning immediately, you decide to save that money in an account earning 5% per annum and gift it to her when she graduates in four years. How much money will she receive?

Problem – Education (Cont.)

Copyright © Michael R. Roberts

Solution 1:

FV4 = FV4 CF0( ) +FV4 CF1( ) +FV4 CF2( ) +FV4 CF3( )= 130,428 1+ 0.05( )4 +130,428 1+ 0.05( )3

+ 130,428 1+ 0.05( )2 +130,428 1+ 0.05( )= 590,269.0327

Just prior to making the first payment, you find out your child has received a scholarship that pays for tuition and all expenses. So, instead of spending $130,428 per year for four years beginning immediately, you decide to save that money in an account earning 5% per annum and gift it to her when she graduates in four years. How much money will she receive?

Problem – Education (Cont.)

Copyright © Michael R. Roberts

Solution 2: The present value of the cash flows is:

PV0 = CF0 +PV0 CF1( ) +PV0 CF2( ) +PV0 CF3( )= 130,428 + 130,428

1+ 0.05( ) +130,4281+ 0.05( )2

+ 130,4281+ 0.05( )3

= 485,615.79

FV4 485,615.79( ) = 485,615.79 1+ 0.05( )4 = 590,269.03