Mobile Wallets: Driving “at scale” adoption Lessons from ...

20

Discussion Document | September 07, 2021 Mobile Wallets: Driving “at scale” adoption - Lessons from China and Sweden NATIONAL CONSULTATION ON “FRONTIER TECHNOLOGY POLICY EXPERIMENTATION AND REGULATORY SANDBOXES FOR SUSTAINABLE DEVELOPMENT” FOR THE MALDIVES CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited

Transcript of Mobile Wallets: Driving “at scale” adoption Lessons from ...

Discussion Document | September 07, 2021

Mobile Wallets: Driving “at scale” adoption -

Lessons from China and Sweden

NATIONAL CONSULTATION ON “FRONTIER TECHNOLOGY POLICY EXPERIMENTATION AND

REGULATORY SANDBOXES FOR SUSTAINABLE DEVELOPMENT” FOR THE MALDIVES

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

2McKinsey & Company

Context and objectives of the document

▪ This document briefly describes and contrasts how mobile

wallet adoption has rapidly accelerated in two different

markets – China and Sweden

▪ Initial growth in China occurred largely in the absence of

regulations with the regulator putting guidelines in place in

2017 well after the market had already taken off

– Growth led by 3rd party ecosystem players, with banks

taking a back seat

– QR the preferred form factor

– Digital payments stand alone remains loss making even

for very large players

– Monetization is done through a combination of financial

services and analytics services

▪ In contrast, in Sweden, the growth was led by a bank led

consortium Swish with a limited role played by Fintech’s

▪ As Maldives looks to accelerate adoption of mobile payments

and reduce cash usage, it will need to consider the

appropriate regulatory framework and potential

economics for key stakeholders

3McKinsey & Company

Contents

The China experience

The Sweden experience

Key considerations for Maldives

4McKinsey & Company

The China experience – Key Messages

▪ China third party payment players account for nearly half of the total retail payment volume – the

market is a clear duopoly between Alipay and WeChat Pay. Limited number of small players do

exist, which differentiate by building their niche in product offerings

▪ Both players adopted a largely similar journey to growth

– Leveraged large customer base and built capabilities outside of their core business – turning

into ecosystem players

– Entered payments business to make payments easy for their existing customers – a critical

success factor for their business model

– Followed up by rapid expansion through inclusion of multiple use cases e.g. mobility, red

envelope, telephone top ups, QR code payments etc.

– Used payments as a loss leader and offered additional services to further monetize the large

customer base, e.g. unsecured loan by Webank, consumer credit bureaus e.g. Zhima credit by Ali

▪ Achieved rapid growth owing to 5 factors – some of which are unique to China

▪ With the increasing penetration by third party players, regulators now casting more and more control

over the third-party payments market

– Payments regulation getting tighter and weeding out non-compliant small players

– Ensuring visibility of online transactions e.g. establishment of Nets Union as a central clearing

house for online payments

– Scope of payments regulation also becoming wider, expanding from license compliance to multiple

fields

1

2

3

4

5McKinsey & Company

Growth of third party players was driven by 5 reasons, some of which are unique to China3

Late mover

advantage

▪ China was overwhelmingly cash- based until the early 2000’s and

e-payments only took off with increasing penetration of the internet on mobile – leading

to leap frog from cash to digital

Platform play – building

a one stop shop

and its existing

high penetration

▪ Alibaba & Tencent ecosystems play offers a one stop shop and is critically enabled by

payments, also allowing cross-subsidizing (e.g. simultaneous scale-up of mobile payments

and the taxi-app wars)

▪ Alipay and Wechatpay leveraged their existing large customer base on their ecosystems

to scale up

Reason Details

Unique

infrastructure

▪ Quick onboarding of customers by linking of bank accounts and easy pull out of money

into the wallet enabled by -

– High penetration of debit cards (3.6 per person)

– Strict ID, phone number verification performed by banks and not the payment players

Adoption of

technology

advancements

▪ Adoption of technologies e.g. QR code and multiple innovations helped the Chinese players

to offer very high convenience compared to bank cards and cash

▪ QR codes also superior to NFC enabled payment methods

▪ Fee structure in China is low and closer to cash, hence enabling high adoption with

increase in convenience through mobile walletsFee structure

6McKinsey & Company

Adoption of QR code technology greatly increased the ease of transactions over traditional cards3

Prior to the rise of third-

party payment, online

payment with bank cards

was cumbersome consumers

usually need to go through

multiple steps of verification,

either by text messages. USB

dongles or other physical

token generating devices

Online shopping

Pay specific amount in online ecommerce website or

public area shopping

Quick Pay – scanned

by merchant

Pay offline merchants by provide user’s QR code for

them to scan

Quick Pay – scanning merchant

Pay offline merchant by scanning their QR code and

input the amount

P2P Payment

Using QR code for P2P payment e.g. paying a friend the

lunch money

Various Payment methods

7McKinsey & Company

QR codes pose multiple benefits compared to traditional cards or NFC enabled payment

methods

3

QR code Traditional card NFC

Consumer

Convenience –

widespread usage of

smartphone

Security – two-factor

authentication

Convenience

Internet connection

required

Inconvenience – need for

PIN input and physical

card

Metal materials may

trigger disturbance

Merchant

Cheap and easy to set up Requires POS terminals /

merchant bank set up

Cheaper than debit card

but higher than QR code

3rd party

Rich amount of user data

being collected

Data limited to card

transaction details

Substantial amount of

data collected

Ease of usage – quick

scan functionality

Fast process

Able to integrate with

wearables

Adoption driven by

consumer use

Credit option

Rewards program

8McKinsey & Company

Contents

The China experience

The Sweden experience

Key considerations for Maldives

9

Case study: In Sweden, the creation of Swish accelerated the adoption of mobile payments

using A2A

Source: Press search; Company website; Riksbank

0

20

40

100

80

60

SwishDebit cardCash

2014 2016 2018

Which means of payment have you used in the past month? Percent of Swedish population

Swish user flow:

1. Open app and enter recipient’s phone number and

account number

2. Authenticate payment once redirected to mobile banking

app (using electronic ID issued by consortium of banks

that links to national ID system)

3. Swish confirms and sends the money in real time via text

to the recipient

ImpactTrend

of Swedish

population uses

Swish

>77%

users as of July

20208.0M

has been

exchanged on the

platform in

December 2019

SEK

30.5B

Transactions in

December 201958M

Swish facilitates free, real-time direct-to-

account payments by linking bank accounts

to mobile phones

Swish was started in 2012 by a consortium

of banks (SEB, Danske Bank, Handelsbanken,

Norea, Swedbank, Sparbankerna, and

Länsförsäkringar Bank) in collaboration with the

Riksbank

It began as a P2P platform, but expanded to

B2C in 2014, eCommerce in 2016, in-store

payments with the launch of QR codes in

2017

Consumers can quickly, securely, and easily

send money to mobile numbers

Merchants are charged a yearly fee and 2

SEK per payment which can vary depending

on company size and requirements.

Swish has grown rapidly (in 2010, 10% of the

population had used Swish in the past month;

by 2016, this had growth to 60%); however,

debit cards remain the most popular

payment method

In 2018, 7 out of 10 Swedes uses Swish

Deep-dive > Full merchant channel focus

2nd most positively viewed brand in Sweden

behind Volvo but ahead of Ikea

10McKinsey & Company

Ownership structure for SWISH – a consortium of banks that deal with merchants and customers –

SWISH merely provides the technology

SOURCE: Expert interviews; company information

1 Listed banks are the owners, additional banks are connected to Swish

▪ Each bank1 responsible for issuing Swish to its customers, enabling

them to send and receive Swish payments

▪ Each bank1 responsible for acquiring online and offline merchants to

Swish, enabling them to receive Swish payments from consumers

(i.e. one bank may act as both issuer and acquirer with respect to the

same transaction)

▪ SEB, Nordea, Handelsbanken and Swedbank each own 20% and

Danske Bank and Länsförsäkringar each own 10% of Swish. Owners

provide capital, know-how, distribution, etc. and receive part of the

revenue generated by Swish. May also receive dividend from Swish

(has never happened yet)

▪ Each Swish payment is initiated by a consumer, connected to Swish

through the issuing bank, and processed by Swish and will either be

forwarded by Swish to another consumer or to an online or offline

merchant

▪ If the payment is forwarded to a merchant, the merchant will send

goods / services in the other direction (and issue a repayment of the

funds through Swish if goods / services are returned by the

consumer)

1

2

3

4

5

Consumer Merchant

1 2

5

Issuing Acquiring

3

Ownership

Payment

Payment

Payment

4

4A

4B

Goods / services

Transactions

11McKinsey & Company

Contents

The China experience

The Sweden experience

Key considerations for Maldives

12McKinsey & Company

Key considerations for Maldives

1

What is the expectation around the dominant payment form

factor – QR or NFC? If QR, will you have one standard QR or

multiple closed loop QRs?

2

Should mobile payment growth be left to market forces or

actively triggered by the government? If so to what extent

should the government be involved e.g. setting up a national

QR (Codi Mexico), or facilitating a utility creation?

3

How will customers be persuaded to rapidly adopt digital

payment solution and move away from cash? Are there

transactions that can be mandated to be electronic only?

4 How will MDRs be priced compared to card schemes? Will

this be left to market forces or prescribed?

5 Who will onboard merchants to mobile payments? How will

you address small merchant concerns around taxes?

6 What is the potential role for foreign players to accelerate

market development?

13McKinsey & Company

Reet Chaudhuri

www.mckinsey.com

linkedin.com/in/reet-chaudhuri-b1b635/

14McKinsey & Company

BACKUP PAGES

15McKinsey & Company

Economics of QR payments for Alipay and WeChat Pay are not compelling given

incentives provided both to users and merchants

$100 transaction Payment flow internal transfer/ ops cost

SOURCE: McKinsey Payments Practice, expert interviews

▪ Alipay and WeChat Pay have historically handled the transaction process with banks, instead of working with networks such as

UnionPay; however, this changed with recent regulation that created NUCC to clear all 3rd-party payments

▪ Timing-wise, merchant receives $100 real-time; T+1 (or with an agreed time frame), 3PP deducts MDR from merchant’s account

▪ Once the consumer sets up 3rd party payment, they can choose to use a bank card or e-wallet as the default payment option

Scenario 2:

Payment with E-

wallet balance

Scenario 1:

Payment with

directly linked

credit or debit

cards

Merchant 3rd Party Payment Issuer

MerchantPays $100

Consumer

3PP revenue = ~$0.3

Merchant

account

~$99.4

(MDR 0.6%)

Issuer

fee ~$0.3

$100.00~$99.4

3PP negotiates rate

with banks

Consumer’s

E-wallet3PP revenue = ~$0.6

$100.00Merchant’s

account

~$99.4

(MDR 0.6%)

~$99.4

ILLUSTRATIVE2

Frequently waived as part of ongoing promotions

Frequent

cashbacks

16McKinsey & Company

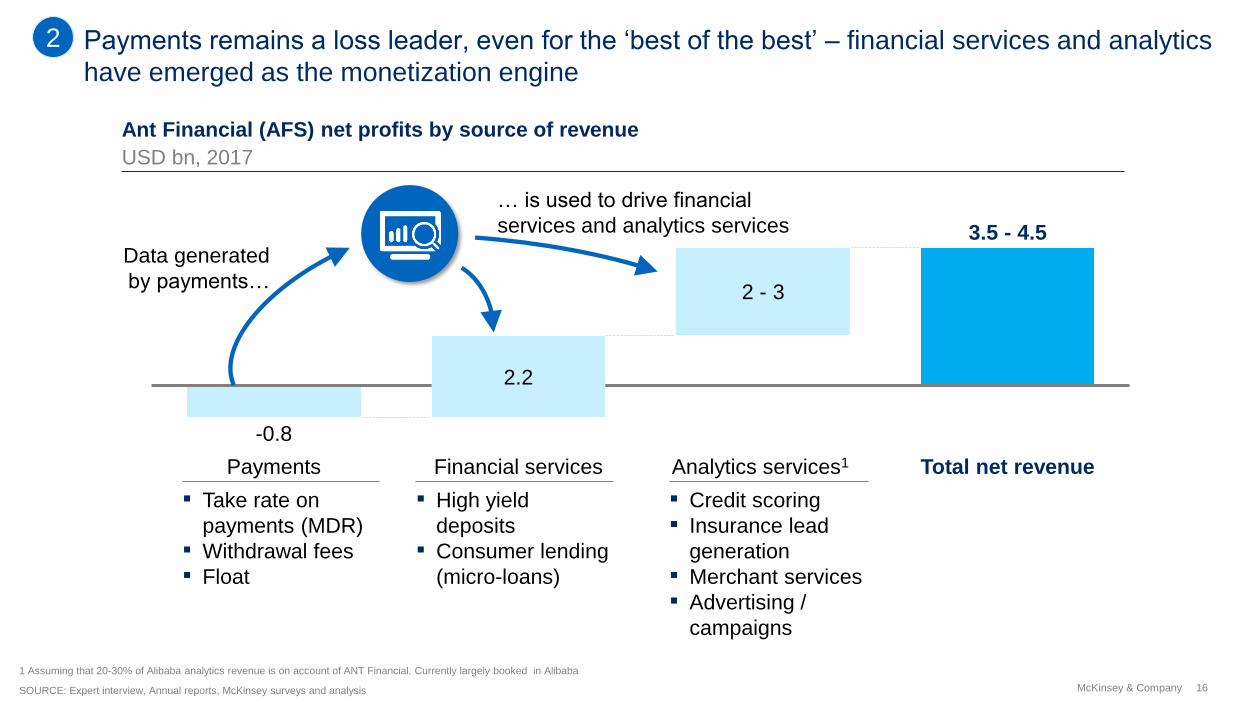

Payments remains a loss leader, even for the ‘best of the best’ – financial services and analytics

have emerged as the monetization engine

Ant Financial (AFS) net profits by source of revenue

USD bn, 2017

SOURCE: Expert interview, Annual reports, McKinsey surveys and analysis

-0.8

Payments Financial services

2 - 3

Total net revenue

2.2

Analytics services1

3.5 - 4.5

▪ Take rate on

payments (MDR)

▪ Withdrawal fees

▪ Float

▪ High yield

deposits

▪ Consumer lending

(micro-loans)

▪ Credit scoring

▪ Insurance lead

generation

▪ Merchant services

▪ Advertising /

campaigns

Data generated

by payments…

… is used to drive financial

services and analytics services

1 Assuming that 20-30% of Alibaba analytics revenue is on account of ANT Financial. Currently largely booked in Alibaba

2

17McKinsey & Company

Alipay and WeChat Pay invested heavily in QR code payment development to acquire merchants

and fueled the growth of mobile payments in China

3

Stage 1 QR code

▪ Customers need to initiate a

payment transaction by scanning

the QR code

▪ The cost for the payment token

is as low as a few yuan

2013

Stage 2 scanner

▪ Every 3rd party payment

company, such as

AliPay, needs to

purchase the scanner by

itself and this scanner

only works for it

2014

Stage 3 mPoS

▪ Agents help to integrate all

major 3rd party payment

company systems and acquire

merchants

with providing free devices to

merchants

▪ Although mPoS machine is

free, agents will charge ~0.3%

per transaction to merchants

accordingly

2015

Stage 4

▪ mPoS will be more

prevailing due

to the advent

of NUCC1

▪ NUCC is tentatively

operating and will centrally

process all dispersed 3rd

party payment transactions

▪ Respective 3rd party

company is not going to

share the revenue as

a role of clearing party

anymore

2017/18

Four main development stages of QR code payment in China

18McKinsey & Company

Payments regulations in China have been getting tighter, weeding out non-compliant small

players and ensuring visibility to online transactions

4

▪ PBOC set up “Nets Union Cleaing

Corp”, a central clearing bank for

online payment services

▪ Regulators can thus keep track of capital

flows and capture online financial

transaction data

▪ All 3rd party payment companies are

required to comply by Jun 18

2014.04 2016.04 2016.07 2016.12 2017.01 2017.08

▪ PBOC classified all payment

institutions into 5 grades by 6

dimensions, in order to

– protect high-performers by imposing

no additional regulations

– Limit poor-performers business area

to force them for improvement

▪ To lower the risk of QR code

application and to unify it:

– CUP specified the

standardization of QR

code payment by defining

its coding method

– CUP justified the validity

of QR code application

▪ To lower the risk

of embezzlement, PBOC aimed

to regulate all non-payment

companies to deposit

provisions in contracted

financial institutions

▪ The first deposit ratio will

be 20% and eventually 100%

▪ To protect commercial bank clients

information , CBRC and PBOC specified

requirement for both banking and 3rd

party payment companies on:

– Client data storage

– Transaction account authorization

– Business risk assessment and

management

▪ Real-name registration

is required for all payment

accounts

▪ Specifies 3 types of payment

accounts: type I, II and III, from

basic to high level registration

requirements

▪ Higher level account has more

payment functionality

Recent changes in China payments regulation

2018.04

▪ New regulations

came into force

that capped the

payment amount

for static QR

code transactions

to RMB 500 per

person per day

19McKinsey & Company

The PBOC introduced a new rule that limits static QR code payment amount but this did not have

a large impact on digital third party payments

4

Static QR code

The consumer uses

smartphone to scan the

fixed QR code provided

by the merchant

Affected by the rule

Dynamic QR code

The merchant scans the

QR code dynamically

generated by consumer’s

digital wallet mobile app

Not affected

▪ PBoC announced a new rule to limit the

payment by static QR codes to RMB 500 per

person per day, which took effect from Apr 1,

2018

▪ It aims to reduce the risk of payment fraud by

illegally tampered QR codes

▪ The impact on offline digital 3rd party payment such as Alipay or WeChat

Pay is, however, limited

– For large/medium merchants such as chain supermarkets, most are

already using dynamic QR code scanning device

– For small merchants, the average ticket size is small anyway (e.g.

RMB 7-8 for grocery purchase). Even if over-limit occurs, the

shopkeeper can offer to use P2P transfer to his/her personal account

as a walkaround

New limit on payment by static QR code Impact on 3rd party payment was limited

“Statistics shows that 95% of QR code transactions are below RMB500.

The average ticket size is around RMB100 only.”

-- 21st Century Business Herald

20McKinsey & Company

The scope of payment regulation in China has become ever wider, expanding from license

compliance to multiple fields

4

Core content Policy implications

▪ Centralized provisions custody system: established for

customers of payment institutions

▪ Online clearing platforms: all transactions must be wired

through centralized platform (NetsUnion) after June 2018

▪ Payment institutions deposit provisions pro rata are

required to the designated account, and interests on the funds

of such an account are not prepaid

▪ Correct and prevent payment institutions from

embezzling and occupying customer provisions, and urge

third-party payment institutions to return

to the original payment business

▪ License application: established a comprehensive market

entry system and a rigid regulatory management mechanism

▪ License renewal: renewal application shall be filed 6 months

ahead of expiration, and audited by Central Bank

▪ Due to the rigorous market entry mechanism, enterprises

which have already been approved

for entry must meet detailed regulatory requirements

▪ User identification mechanism through “real-name”

customer registration: users are required to input and

validate their basic identity information continuously, so as to

ensure customer identities and their true intentions are

effectively verified

▪ The real-name system serves as the baseline to

guarantee account security, maintain normal economic

order, effectively prevent money laundering, etc.

▪ Introduce refined administrative measures, defining

the responsibilities of payment institutions in aspects such

as customer identification, storage of customer identity

information and transaction records, suspicious transaction

report, anti-money laundering and anti-terrorist financing

investigations, as well as supervision and management

▪ Refine responsibilities, clarify obligations, and maintain

normal economic order

Centralized

custody

system

License

compliance

Real-name

registration

Anti-Money

Laundering

China’s third-party mobile payment regulatory scope (till 2017)