Mobile Payment Systems: Legal and Regulatory...

37

Presenting a live 90‐minute webinar with interactive Q&A Mobile Payment Systems: Mobile Payment Systems: Legal and Regulatory Challenges Best Practices for Minimizing Risks and Liabilities With Wireless Financial Transactions Today’ s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific THURSDAY, FEBRUARY 9, 2012 Today s faculty features: Duncan B. Douglass, Partner, Alston & Bird, Atlanta Jarrett Helms, McKinsey & Company, Atlanta The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Transcript of Mobile Payment Systems: Legal and Regulatory...

Presenting a live 90‐minute webinar with interactive Q&A

Mobile Payment Systems: Mobile Payment Systems: Legal and Regulatory ChallengesBest Practices for Minimizing Risks and Liabilities With Wireless Financial Transactions

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, FEBRUARY 9, 2012

Today s faculty features:

Duncan B. Douglass, Partner, Alston & Bird, Atlanta

Jarrett Helms, McKinsey & Company, Atlanta

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-888-450-9970 and enter your PIN when prompted Otherwise please send us a chat or e mail PIN -when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

Mobile Payment Systems:Mobile Payment Systems: The US Market and Its Legal and Regulatory Challengesand Regulatory Challenges

Jarrett Helms, Payments Practice Experty pMcKinsey & Company

Duncan Douglass, PartnerAlston & Bird LLPAlston & Bird LLP

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company and Alston & Bird is strictly prohibited

Defining the U.S. Mobile gPayments Market

GCI-AAA123-20110606-

There are numerous forms of mobile payments, we will concentrate on using the mobile device at the traditional point-of-sale

NFC

Traditional POS

Mobile Commerce“Near Field Communication”

MobilePOS

Other POS

Communication based POS purchases Payment processing

from a mobile device (e.g., card swipe “ l ”)

NFC alternatives (e.g., SMS, barcodes, “bump”, Bluetooth, etc)

“sleeve”)

Mobile purchase of digital content (e g

Money Transfer & Bill

PDigital

Content

The use of a mobile device to initiate bill

t

digital content (e.g., music, books, games, apps, etc)

PayMobile e-

commerce

Contentpayment or money transfers Mobile purchase of

physical goods and services (e.g. shopping via a b )

McKinsey & Company | 7SOURCE: Team analysis

browser or app)

GCI-AAA123-20110606-

A rich ecosystem of mobile payment services is evolving that will benefit from mobile wallet capabilities

IAlternatives to the Alternatives to the

Potential mobile wallet applicationsEXAMPLES

Mobile Mobile

In-person retail card /

cash alternative

traditional card / cash based POS

experience (e.g., NFC, bar codes, etc.)

traditional card / cash based POS

experience (e.g., NFC, bar codes, etc.) Payment processing

from a mobile d i ( d

Payment processing from a mobile

d i ( dMobile Incentives

Mobile POS

Deploying coupons, offers, etc. via mobile device (e.g., location

based offers)

Deploying coupons, offers, etc. via mobile device (e.g., location

based offers)

device (e.g., card swipe “sleeve”)

device (e.g., card swipe “sleeve”)

Mobile Wallet

Banking and bill

pay

P2P / social

E-C

based offers)based offers)

Enabling online banking and billEnabling online banking and bill

Mobile purchase of digital content (e.g.,

music, books, games, apps, etc)

Mobile purchase of digital content (e.g.,

music, books, games, apps, etc)

Commerce“check-

out”

banking and bill payment via mobile

device

banking and bill payment via mobile

deviceServices that

streamline the ability to pay for mobile /

ecommerce

Services that streamline the ability

to pay for mobile / ecommerce

McKinsey & Company | 8SOURCE: McKinsey Payments Practice

transactions initiated via mobile

transactions initiated via mobile

GCI-AAA123-20110606-

Mobile payments themselves are unlikely to generate significant new payments revenues …

US Mobile Payment Transaction Value1

Billions

60 100% Existing card-based spend via mobile

Cash displacement

% of merchant terminals that are NFC enabled

44 BN represents less 40

50

60

044

100% g p

pthan 1% of total card spend

4420

30

40

50%300

In general, mobile payments will simply shift the form factor of a

29

8210

10

20

0

80

simply shift the form factor of a card transaction from a plastic card to the mobile device. This does not change the economics of the base transaction

020162011 15141312

McKinsey & Company | 9

1 includes only NFC based transactions originated in the US2 Effectively zero volume; mobile NFC pilots may have generated some volume

SOURCE: McKinsey US Payments Map, team analysis

GCI-AAA123-20110606-

…So why is there a big fuss over mobile payments?

Mobile payments offer more opportunities to attackers than incumbents, threatening direct consumer relationships for issuing banks and providing new revenue streams for entrants

Area of

ILLUSTRATIVE

ea ochange:

Consumer Merchant Terminal Processor Network Issuer

Cardcontrolled by

an issuing bank

Loaded into

E-wallet controlled by

any of the

McKinsey & Company | 10

1 Optional

SOURCE: Team analysis

any of the following:

GCI-AAA123-20110606-

Integrating digital wallets into mobile devices presents many opportunities to improve customer experience and generate new revenue streams

Key opportunities for in-person mobile payments: NFC Example

Provide enabled devicesTelco’s

Develop ad / loyalty platformsGroupon / Scoutmob

1 3Mobile components

Transaction flow

Telco’sHandset manufacturesNFC chip manufacturersMobile OS developers

Groupon / ScoutmobIssuing BanksCard Networks

EXAMPLES

ConsumerNFC Enabled Device

Coupons / Rewards & Loyalty1

e-Wallet Contactless Terminal Merchant

Transaction flow

PaymentProcessing

Merchant offers1

Develop e-walletTelco’sGoogle / Apple

Develop POS systemsVerifoneViVOtech

2 4Google / AppleIssuing BanksCoupon providersCard NetworksPayPalOther 3rd parties

ViVOtech

The mobile payments ecosystem promises a richer shopping experiencefor consumers with real time contextual

McKinsey & Company | 11

p

1 Optional

SOURCE: Team analysis

for consumers, with real-time, contextual information and offers.

GCI-AAA123-20110606-

New technologies and functionalities have lead to new purchase & payment related products and applications for the mobile device…

Hype around mobile payments tends to be blurred together with hype over other mobile based products and services, but some payments applications are coming online

Couponing / Rewards

Location based

marketing

Mobile ticketing

Transaction based

marketingMobile POS

NFC

McKinsey & Company | 12SOURCE: Team analysis

GCI-AAA123-20110606-

…But further convergence among these new applications is likely, and could create a powerful tool for consumers and merchants alike

The next generation of payments applications could combine the functionality of several existing mobile products to create a more integrated and compelling product

Marketing Money Savings Mobile Payments New Application

Location based

marketing E ll t

Budgetingapplicationsmarketing E-walletpp

=+ +New

Transactional based

marketing

Coupons / Rewards

NFCcombined application

McKinsey & Company | 13SOURCE: Team analysis

GCI-AAA123-20110606-

Driving consumer and merchant adoption is a classic “chicken or the egg” conundrum… you can’t get one without the other

The two-sided market dynamics in payments have historically made it very difficult to build new payment systems. Mobile is no exception. A network effect is needed.

Achieving a network effect for mobile payments is hamperedA network effect depends on:

1. Enough consumers using mobile to make it compelling for merchants

Achieving a network effect for mobile payments is hampered by both real and perceived hurdles:

▪ Basic concerns:– Failure of contactless cards to achieve adoption– Lack of a single standard for mobile payments

A network effect depends on:

A

compelling for merchants to adopt

2. Enough mobile enabled merchants to make adoption meaningful for consumers

– Low, but growing penetration of smartphones– Consumer perception of security

▪ Consumer payment preferences and behaviors:– The mobile wallet will need to allow for the same basic

payment preferences that consumers have today▪ Cost benefits to the merchant:

B

C▪ Cost benefits to the merchant:– Merchants want to know that enough consumers will demand

mobile payments, that it merits upgrading their existing systems, and implementing new marketing programs

The most problematic hurdle is simply the lack of a clear value

C

The most problematic hurdle is simply the lack of a clear value proposition for both merchants and consumers. Mobile payments are not necessarily faster, cheaper, or more reliable; and on their own they may not provide enough value for consumers or merchants to shift payment behavior. To be successful they must partner with other value added

McKinsey & Company | 14SOURCE: Team analysis

products

GCI-AAA123-20110606-

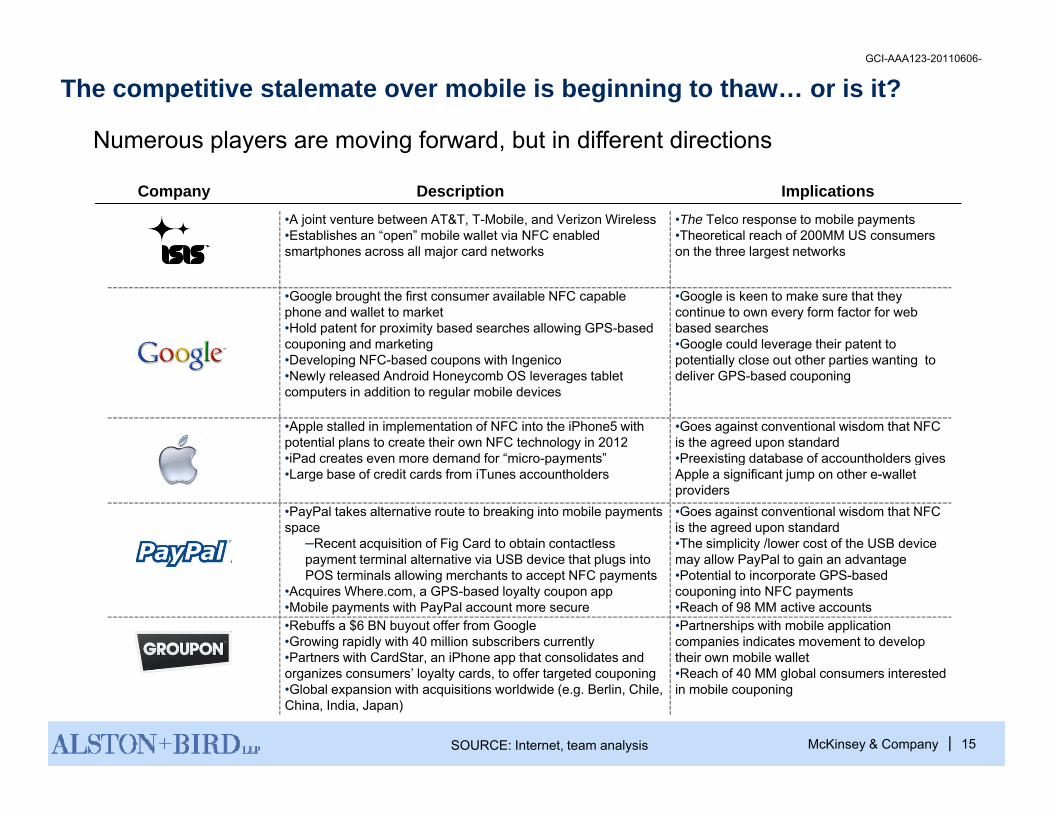

The competitive stalemate over mobile is beginning to thaw… or is it?

Numerous players are moving forward, but in different directions p y g ,

•A joint venture between AT&T, T-Mobile, and Verizon Wireless•Establishes an “open” mobile wallet via NFC enabled smartphones across all major card networks

•The Telco response to mobile payments•Theoretical reach of 200MM US consumers on the three largest networks

Company Description Implications

smartphones across all major card networks on the three largest networks

•Google brought the first consumer available NFC capable phone and wallet to market•Hold patent for proximity based searches allowing GPS-based couponing and marketing D l i NFC b d ith I i

•Google is keen to make sure that they continue to own every form factor for web based searches•Google could leverage their patent to

t ti ll l t th ti ti t•Developing NFC-based coupons with Ingenico•Newly released Android Honeycomb OS leverages tablet computers in addition to regular mobile devices

potentially close out other parties wanting to deliver GPS-based couponing

•Apple stalled in implementation of NFC into the iPhone5 with potential plans to create their own NFC technology in 2012•iPad creates even more demand for “micro payments”

•Goes against conventional wisdom that NFC is the agreed upon standard•Preexisting database of accountholders gives•iPad creates even more demand for micro-payments

•Large base of credit cards from iTunes accountholders•Preexisting database of accountholders gives Apple a significant jump on other e-wallet providers

•PayPal takes alternative route to breaking into mobile payments space

–Recent acquisition of Fig Card to obtain contactless payment terminal alternative via USB device that plugs into

•Goes against conventional wisdom that NFC is the agreed upon standard•The simplicity /lower cost of the USB device may allow PayPal to gain an advantagepayment terminal alternative via USB device that plugs into

POS terminals allowing merchants to accept NFC payments•Acquires Where.com, a GPS-based loyalty coupon app•Mobile payments with PayPal account more secure

may allow PayPal to gain an advantage•Potential to incorporate GPS-based couponing into NFC payments•Reach of 98 MM active accounts

•Rebuffs a $6 BN buyout offer from Google•Growing rapidly with 40 million subscribers currently•Partners with CardStar, an iPhone app that consolidates and

•Partnerships with mobile application companies indicates movement to develop their own mobile wallet

McKinsey & Company | 15SOURCE: Internet, team analysis

, pporganizes consumers’ loyalty cards, to offer targeted couponing•Global expansion with acquisitions worldwide (e.g. Berlin, Chile, China, India, Japan)

•Reach of 40 MM global consumers interested in mobile couponing

GCI-AAA123-20110606-

Backed by major brands, consumer and merchant applications are emerging to test demand for mobile payment technologies at the POS

PartnersValue proposition Revenue Model

Additi l d ti iConsumer example

An e-wallet integrated into a marketing platform which will allow

Consumers will be able to store all the documents from their wallets into one mobile app as well as receive, store and redeem

Additional advertising and marketing spend

store, and redeem coupons/offers at the POS

Mobile application that

PartnersValue proposition

Merchants can integrate

Revenue Model

Merchant feeMerchant example

Mobile application that allows users to pay for a restaurant or bar tab using an app on their smartphone

this payment app with their POS system allowing for more convenient and efficient transactions resulting in increased sales

McKinsey & Company | 16

increased sales

SOURCE: Corporate websites, team analysis

GCI-AAA123-20110606-

NFC is the front-runner standard for mobile payments, but other alternatives exist, causing marketplace confusion & investment delays

Standard Used by Pros/Cons

▪ Pro: Has the most momentum behind it, and is already deployed

▪ Con: Necessitates hardware upgrades for

▪ Industry consortium including: Visa, MasterCard, Isis, N

FC

Ease of integration

Likelihood of adoption

pgthe merchant

▪ Used globally, but no current US

, ,Microsoft, Sony

NSM

S

▪ Pro: No contactless terminal needed▪ Pro: No smart phone needed▪ Con: Clumsy and slow to use

systems

▪ PayPal

Sas

onic

▪ Con: Clumsy and slow to use

▪ Pro: Only needs a USB plug-in, making integration easier

▪ Pro: No card information is stored or sharedPayPal▪ Sparkbase

Ultr

aco

de

▪ Amazon

Pro: No card information is stored or shared▪ Con: No phone signal, no payment

▪ Pro: Easiest to integrate of any solution

▪ Appleple

Bar

c Amazon

▪ Apple has been unclear about their release of an NFC enabled iPhone, and there are

th t th d l

▪ Con: Works best for closed loop accounts

? ?McKinsey & Company | 17SOURCE: Team analysis

▪ Apple

App rumors that they may develop an

alternate standard. This uncertainty promotes market stagnation

? ?

GCI-AAA123-20110606-

The scramble for mobile acquisitions has started primarily with e-wallets

Valuations of mobile companies are extremely high and large industry players

4/28/2010: PayPal acquires 5/17/2011: SK C&C USA 6/13/2011: NuWallet

are making the first major moves in the mobile payments arena

7/7/2011: Zong is4/28/2010: PayPal acquires FigCard as a means of bypassing NFC hurdles and more directly working with POS merchants to provide a streamlined payment

5/17/2011: SK C&C USA launches Corfire with mobile wallet platform based on NFC technology

6/13/2011: NuWallet introduces mobile payments solution that allows users to make online purchases via their mobile devices more efficiently by storing the

7/7/2011: Zong is purchased by eBay in a continuing effort to build PayPal a full scale mobile offering able of competing in the POS

experience consumers information within the app

May JuneApril July

5/11/2011: Visa announces plans to launch NFC based mobile wallet to be launched 6/13/2011: Payfone partners with Verizon

2011

in Fall 2011

5/26/2011: Release of Google Wallet with Google Offers

5/27/2011: PayPal sues Google

yWireless to develop new mobile payment system for Verizon customers enabling online purchases from smartphones, tablets, and PCs through various payment methods.

McKinsey & Company | 18SOURCE: Press releases, corporate websites

indicating similar mobile wallet development by PayPal

GCI-AAA123-20110606-

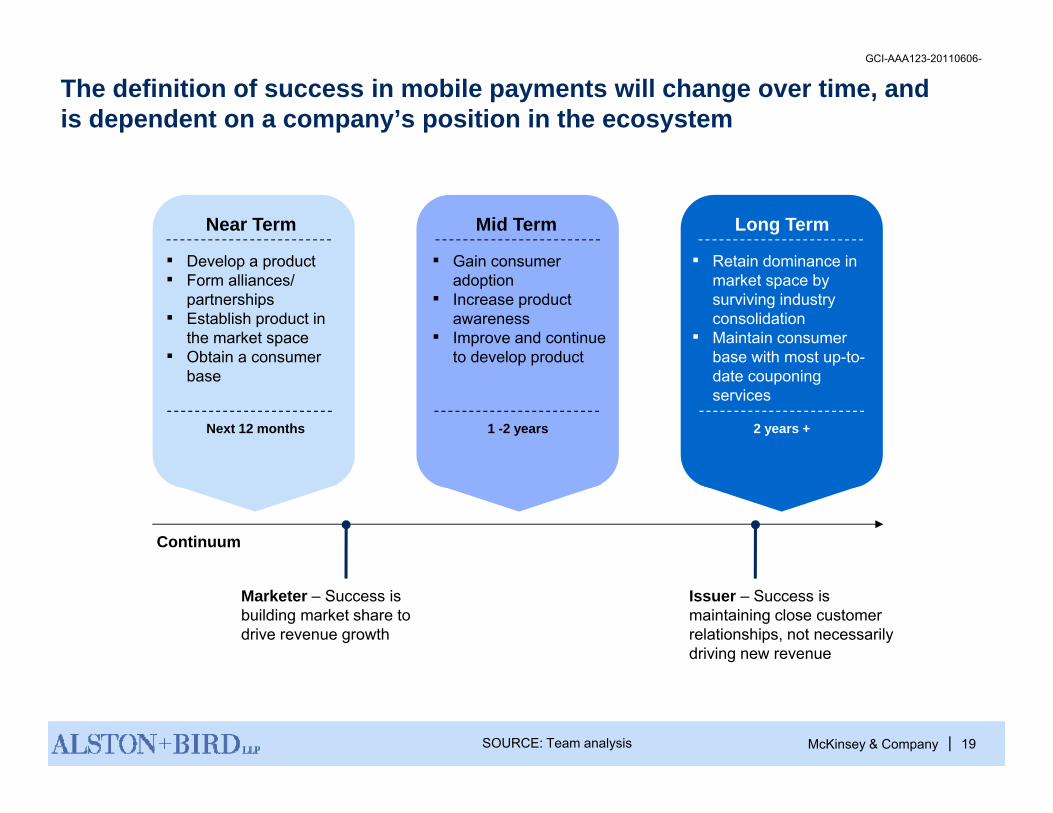

The definition of success in mobile payments will change over time, and is dependent on a company’s position in the ecosystem

Near Term Mid Term Long Term

▪ Develop a product▪ Form alliances/

partnerships▪ Establish product in

the market space▪ Obtain a consumer

▪ Gain consumer adoption

▪ Increase product awareness

▪ Improve and continue to develop product

▪ Retain dominance in market space by surviving industry consolidation

▪ Maintain consumer base with most up to▪ Obtain a consumer

base

Next 12 months

to develop product

1 -2 years 2 years +

base with most up-to-date couponing services

Continuum

Issuer – Success is maintaining close customer relationships, not necessarily driving new revenue

Marketer – Success is building market share to drive revenue growth

McKinsey & Company | 19SOURCE: Team analysis

GCI-AAA123-20110606-

Although many players are interested in developing e-wallets, all are constrained by avoiding significant trade-offs with their core businesses

IssuersKey Ecosystem Assets Constrained by … Players

▪ Maintaining share of wallet – “stay relevant for every payment”

▪ Trusted brands as payment account and instrument providers

Stakeholder

▪ Mobile subscriber market share

▪ Driving data revenues

▪ UICC / OTA provisioning▪ App’ preload▪ Supported devices

▪ Maintaining handset market share

▪ Device feature set (NFC chip)▪ Embedded secure element

Telco’s

Handset f share▪ Embedded secure elementm’facturers

▪ Maintaining OS market share to drive application / license revenue

▪ App’ store / preload▪ Source code / SDK▪ Application processor

Mobile OS developers

Payments networks

Marketing / Advertising

▪ Maintaining overall transaction / wallet share growth

▪ Need to generate advertising impressions (access to as

▪ Wallet eligibility▪ Existing e-wallet userbase

▪ Existing user base (consumers / merchants) / Advertising

platformsimpressions (access to as many networks as possible)

( )consumer interest

▪ Key patents

Retailers ▪ Acceptance▪ Existing e-wallet userbase

▪ Sales volume

McKinsey & Company | 20

Payment intermediaries

▪ Existing e-wallet userbase ▪ Maintaining existing user / transaction base

SOURCE: Team analysis

GCI-AAA123-20110606-

Competitors are adopting varied e-wallet strategies based on current strengths and placement in the market

ple

Current and future mobile wallet applications:

Exam

p

Intermediary Lone Wolf Coalition

Characteristics:

Open Platform

Characteristics: Characteristics: Characteristics:Characteristics:

▪ Continue to provide intermediary processing

▪ Leverage existing ll t b t

Stra

tegy

Characteristics:

▪ Unique stand-alone platforms

▪ Leverage loyal user base to extend

d l tf

Characteristics:

▪ Attempt to consolidate efforts of like parties (issuers, telcoms)B d h b d

Characteristics:

▪ Create an open wallet for other developers to leverageB d h b dwallet base to move

to POS▪ Move e-commerce

capabilities to bricks-and-mortar

rewards platform▪ Drive cross-sell of

other products or sell access to others

▪ Broad reach based on consumer base

▪ Keep known quantities in control

▪ Broad reach based on smartphone ownership

▪ Drive ad or app’ revenue

McKinsey & Company | 21SOURCE: Team analysis

REGULATION OF MOBILE PAYMENTS IN THE U.S.

GCI-AAA123-20110606-

Mobile Payments Operating ModelsOperating Models

Bank-Driven Model – Financial institution offers account access through mobile device-initiated transactions

• Transactions are processed over traditional payment networks/channels• Funding source is payor’s DDA, line of credit or prepaid account with the

financial institution

Mobile Payment Service Provider (MPSP) Driven Model MPSP offers mobileMobile Payment Service Provider (MPSP)-Driven Model – MPSP offers mobile payment capabilities to its service users (which may include small merchants)

• Transactions are processed over MPSP’s systems• MPSP may access existing customer funding source held at/issued by a third

party (e.g., a DDA or payment card) or may establish a dedicated fundingparty (e.g., a DDA or payment card) or may establish a dedicated funding account

Mobile Network Operator-Driven Model – Mobile network operator offers mobile payments capabilities for purchases using mobile devices associated with its

i l t kwireless network• Transactions are processed over the operator’s wireless network

• Charges appear on payor’s wireless bill and/or are funded on a prepaid basis

McKinsey & Company | 23

GCI-AAA123-20110606-

Overview

• As contemplated and piloted to-date, mobile payments initiatives in the U.S. have largely leveraged existing payment and funds transfer methods and operating modelstransfer methods and operating models

• The regulatory regime applicable to existing methods and models thus likely governs mobile payments analogues

• The Regulatory picture becomes less clear in certain operating models that may become prevalent in the future

F l M bil N t k O t M d l h t• For example, Mobile Network Operator Model where customer purchases of third party goods/services are reflected on the customer’s wireless bill

I d i l t f b k h d• Increased involvement of non-banks may pose enhanced regulatory and supervisory challenges

McKinsey & Company | 24

GCI-AAA123-20110606-

Mobile Device:Just Another Form Factor?Just Another Form Factor?

• In many respects, mobile device-initiated payments are functionally the same as existing payment and fund transfer methods thethe same as existing payment and fund transfer methods – the principal innovation being the new form factor

• Mobile payment transactions that rely on traditional retail payments funding (DDA li f dit id t) lik l bj t t thsources (DDA, line of credit, prepaid account) are likely subject to the

same regulatory requirements as their more traditional predecessors

• Regulators have not generally provided formal interpretations that existing l ti l t bil t b t th t t d hi t i lregulations apply to mobile payments, but the text and historical

application of those regulations point to this conclusion

• The recent spate of legislative/regulatory activity applicable to retail payments generally has broad applicability and will likely apply equally to mobile payments (and in some cases do so expressly)

McKinsey & Company | 25

GCI-AAA123-20110606-

TILA/Regulation Z

• Applies in relevant part to any person that issues a credit card and who regularly extends credit to consumers primarily for personal, family or household purposeshousehold purposes

• A “credit card” is “any card, plate, coupon book, or other single credit device that may be used from time to time to obtain credit.”

• A mobile device that accesses a line of credit for funding transactions is most likely a credit card for TILA/Regulation Z purposes, and the issuer of the device (and extender of related credit) is most likely a creditor for TILA/Regulation Z purposesTILA/Regulation Z purposes

McKinsey & Company | 26

GCI-AAA123-20110606-

EFTA/Regulation E

• Generally applies to “any person that directly or indirectly holds an account belonging to a consumer, or that issues an access device and agrees with a consumer to provide electronic fund transfer services”agrees with a consumer to provide electronic fund transfer services

• “account” means a consumer asset account

• “access device” means “a card, code, or other means of access to aaccess device means a card, code, or other means of access to a consumer’s account . . . that may be used by the consumer to initiate electronic fund transfers”

• A mobile device that can be used to initiate electronic fund transfers from t t ( DDA) i t lik l d ia consumer asset account (e.g., a DDA) is most likely an access device

for EFTA/Regulation E purposes and the issuer of the mobile device (and the holder of the account, if different) is most likely subject to the EFTA/Regulation E

McKinsey & Company | 27

GCI-AAA123-20110606-

Bank Secrecy Act/AML RequirementsAML Requirements

• Financial institutions, including money services businesses (MSBs), are subject to various requirements designed to detect and prevent moneysubject to various requirements designed to detect and prevent money laundering and terrorist financing activities

• Banks are expressly covered by BSA requirements

• Many MPSPs are subject to BSA compliance obligations as money transmitters (i.e., MSBs)

• Mobile network operators, depending on their role in facilitating funds transfers, may also be subject to regulation as MSBs if they satisfy the definition of a money transmitter or operator of a credit

d tcard system

McKinsey & Company | 28

GCI-AAA123-20110606-

State Money Transmitter Laws

• Govern the activity of non-depository money service (funds transfer) id lik t itt h k h d d lproviders like money transmitters, check cashers and currency dealers

• Except to the extent that a bank agent exemption may apply, MPSPs and mobile network operators responsible for funds transfersand mobile network operators responsible for funds transfers (including P2P transfers and prepaid funding models) may be subject to state licensure

McKinsey & Company | 29

GCI-AAA123-20110606-

Gramm-Leach-Bliley Act

• Applies to financial institutions, as broadly defined

• Privacy Rule – requires FI to disclose to customer its policies• Privacy Rule – requires FI to disclose to customer its policies regarding disclosure of customer’s non-public information with affiliates and non-affiliates

• Safeguards Rule – requires FI to develop standards to protectSafeguards Rule – requires FI to develop standards to protect customer information

• Applicability of GLBA to non-bank mobile payments provider will vary with the model but should apply to mobile payments entities in parallel towith the model, but should apply to mobile payments entities in parallel to its applicability to providers involved in more traditional payment channels

McKinsey & Company | 30

GCI-AAA123-20110606-

Dodd-Frank Act• Title X - Consumer Financial Protection Act and the creation of the BureauTitle X Consumer Financial Protection Act and the creation of the Bureau

of Consumer Financial Protection with authority to regulate non-bank providers of consumer financial products and services

“Financial Products” include:“Financial Products” include:

• Extending credit

• Issuing stored value or payment instruments

• “providing payments or other financial data processing products . . . including payments made through an online banking system orincluding payments made through an online banking system or mobile telecommunications network”

• Durbin Amendment restrictions on exclusive network arrangements will likely impact all participants in the evolving mobile payments marketplace

• New coverage of cross-border remittance transfers under the EFTA/Regulation E will impact all mobile-initiated remittances to foreign receivers

McKinsey & Company | 31

receivers

GCI-AAA123-20110606-

New FinCEN Prepaid Access Rules

• FinCEN’s new prepaid access rules characterize all “providers of prepaid• FinCEN s new prepaid access rules characterize all providers of prepaid access” as MSBs will pull additional non-bank participants in pre-funded mobile payments schemes under federal supervision for AML compliance

• FinCEN has defined “prepaid access” very broadly to include anyFinCEN has defined prepaid access very broadly, to include any “electronic device or vehicle, such as a card, code, electronic serial number, mobile identification number or personal identification number.”

McKinsey & Company | 32

GCI-AAA123-20110606-

Review of Mobile Payments Operating Models Through the Regulatory LensModels Through the Regulatory Lens

• Bank-Driven Model • Bank typically holds funding account and uploads traditional credit, debit or prepaid card

account number (or account identifier for ACH applications) to mobile device (which may be a contactless sticker)be a contactless sticker)

• Full complement of existing payments laws should apply in the mobile context• MPSP-Driven Model

• If transaction funding accounts are held at traditional financial institutions, regulatory framework should apply in the same way as it applies to payment service providers

ti i th i t t t d (MPSP b bj t t EFTA/R l ti E doperating in the internet space today (MPSP may be subject to EFTA/Regulation E and is likely an MSB/MT but should be able to avoid broader regulation because MPSP is acting as a service provider)

• If MPSP holds funding accounts (e.g., on a prepaid basis) or extends credit, MPSP should be subject to broader federal and state regulations, similar to those that would

l t b k id id f i i il f ti ( lb it t d ti lapply to a bank or prepaid provider performing similar functions (albeit not prudential oversight)

• Mobile Network Operator-Driven Model• If transaction funding accounts are held at traditional financial institutions, operator may

be subject to certain MSB/MT requirements and may be subject to EFTA/Regulation E j q y j grequirements (if issuing the access device), but will generally be characterized as a service provider

• If the operator holds a prepaid funding account, it will be subject to broader federal and state regulation; if the operator posts mobile payment transactions to the customer’s wireless bill, the operator may be subject to TILA/Regulation Z or may be subject only to

McKinsey & Company | 33

, p y j g y j yTruth-in-Billing Requirements and related FCC regulation (this point is subject to debate)

GCI-AAA123-20110606-

Mobile Payments Models May Present Enhanced Regulatory ChallengesEnhanced Regulatory Challenges

• Compliance concerns – Even where non-bank mobile paymentsCompliance concerns Even where non bank mobile payments providers are subject to federal and state regulations, mobile network operators and MPSPs are often not familiar with payments/financial services legal requirements such as consumer protection laws, BSA/AML obligations (including KYC) state money transmitter lawsBSA/AML obligations (including KYC), state money transmitter laws, and other compliance requirements

• Credit/liquidity risk concerns – Displacement of traditional financial institutions which are subject to prudential oversight by non-bankinstitutions, which are subject to prudential oversight, by non bank mobile payments companies may increase credit and liquidity risk in the payment system

• Federal regulatory authorities have been monitoring the mobileFederal regulatory authorities have been monitoring the mobile payments space but have yet to identify the market is separate or unique from other payment systems

McKinsey & Company | 34

GCI-AAA123-20110606-

Regulation of Mobile Payments – Continuing the Discussionthe Discussion

• While mobile payments remain in the formative stages in the U.S., p y g ,consider whether regulators should be encouraged to begin addressing the issue through interpretive guidance

• Is there a risk that an under-regulated mobile payments system develops in g p y y pthe U.S.?

• Consider whether the existing (and evolving) regulatory framework is suited to regulate the enhanced role non-banks are playing in mobile

t ti l l i d l th t i l b t ti lpayments, particularly in models that involve substantial disintermediation of traditional financial institutions

• Is regulation of mobile payments principally a consumer protection issue (CFPB)?(CFPB)?

• Are there safety and soundness issues that should be addressed in non-bank driven models?

McKinsey & Company | 35

Conclusion / QuestionsConclusion / Questions

GCI-AAA123-20110606-

For more information, contact:

Jarrett HelmsPayments Practice Expert678-221-2320

Duncan DouglassPartner404-881-77686 8 3 0

[email protected] [email protected]

McKinsey & Company | 37