Mobile Emerging Markets Tcl

16

A definitive guide to the key Emerging Mobile Markets in 34 countries worldwide by Tariff Consultancy Ltd. From Afghanistan to Vietnam, 34 countries are profiled with over 200 mobile operators included.

-

Upload

keith-breed -

Category

Technology

-

view

1.384 -

download

1

Transcript of Mobile Emerging Markets Tcl

A definitive guide to the key Emerging Mobile Markets in 34 countries worldwide by Tariff

Consultancy Ltd. From Afghanistan to Vietnam, 34 countries are

profiled with over 200 mobile operators included.

Essentials & Key Features of the report: 3.Emerging Mobile Markets Pricing 2009 is a report published by Tariff Consultancy Ltd (TCL). 4.The report provides a comprehensive overview of mobile operators & their products in the 34 Emerging Markets across Europe, Asia, the Middle East & Latin America including China, Brazil & India. 5.For each country TCL provides details of fixed line & mobile penetration (as of the end of 2008) with a profile of all key mobile operators with subscriber numbers. 6.There is also a 5 year subscriber growth forecast to the end of 2013. The following countries are included in the report:

Afghanistan, Argentina, Bangladesh, Brazil, Cambodia, Chile, China, Colombia, Dominican Republic, Ecuador, Egypt, Estonia, Ghana, India, Indonesia, Iraq, Iran, Kenya, Latvia, Libya, Lithuania, Malaysia, Mexico, Morocco, Nigeria, Pakistan, Peru, Philippines, Russia, Sri Lanka, Thailand, Turkey, Ukraine, Vietnam.

Key differences between Emerging Mobile Markets & Developed Mobile Markets

Characteristics of an Emerging Mobile Market versus a Developed Mobile Market

Emerging Mobile Market

• High population growth

• High economic growth

• Low mobile penetration

• Limited network development

• Limited price competition

• Pre Paid services

• Voice services emphasis

Developed Mobile Market

• Modest population growth

• Modest economic growth

• High mobile penetration

• High network development

• High levels of price competition

• Pre Paid and Post Paid services

• Voice & Data services

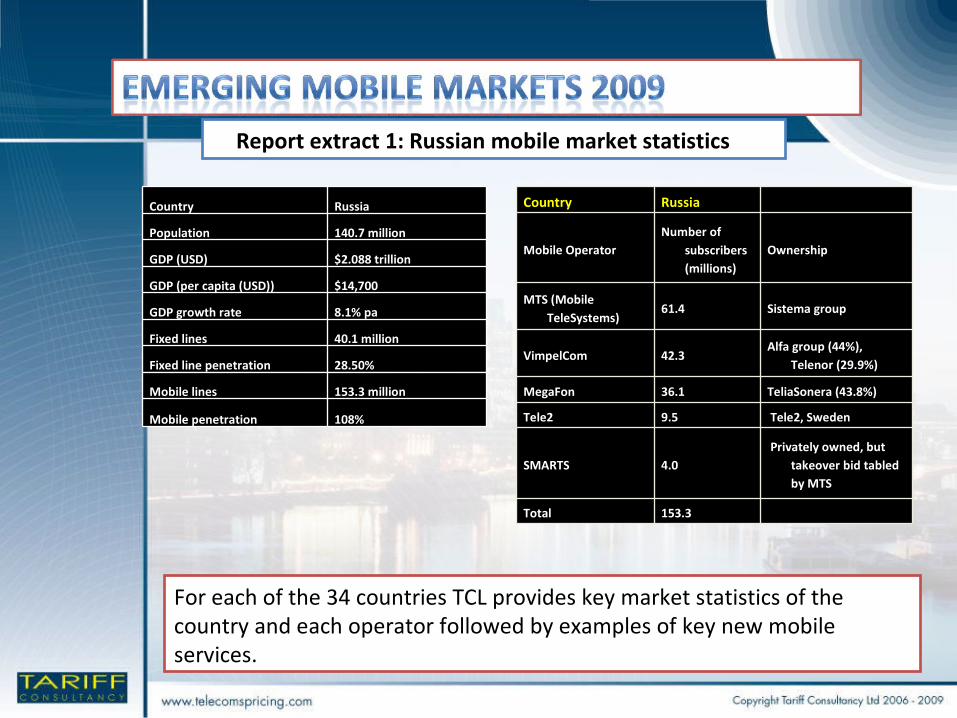

Report extract 1: Russian mobile market statistics

For each of the 34 countries TCL provides key market statistics of the country and each operator followed by examples of key new mobile services.

Country Russia

Population 140.7 million

GDP (USD) $2.088 trillion

GDP (per capita (USD)) $14,700

GDP growth rate 8.1% pa

Fixed lines 40.1 million

Fixed line penetration 28.50%

Mobile lines 153.3 million

Mobile penetration 108%

Country Russia

Mobile OperatorNumber of

subscribers (millions)

Ownership

MTS (Mobile TeleSystems)

61.4 Sistema group

VimpelCom 42.3Alfa group (44%),

Telenor (29.9%)

MegaFon 36.1 TeliaSonera (43.8%)

Tele2 9.5 Tele2, Sweden

SMARTS 4.0 Privately owned, but

takeover bid tabled by MTS

Total 153.3

The Key Take Away’s from the report – 1 3.As of the end of 2008 the 34 countries surveyed accounted for approx. 2.1 billion of the total mobile subscriber base worldwide (around 4 billion users) – with an average mobile penetration rate of 46%.4.By the end of 2013 subscribers in the 34 countries will more than double to 4.3 billion users with an average mobile penetration rate of 95%. 5.Although China and India will see the largest absolute increases in subscribers it will be countries such as Afghanistan, Iraq, Cambodia & Indonesia that will have the largest percentage growth rates. 6.The deployment of 3G services is a major trend, but the user adoption of services will continue to be constrained by 3G handset costs. 7.But 3G services are allowing Emerging Market subscribers to use mobile broadband and VoIP services. 8.Operators are moving away from per minute or per KB charges towards flat rate charges, including unlimited call packages, discounts for on-net calls, and bundled flat rate packages (which also include calls to selected international destinations.

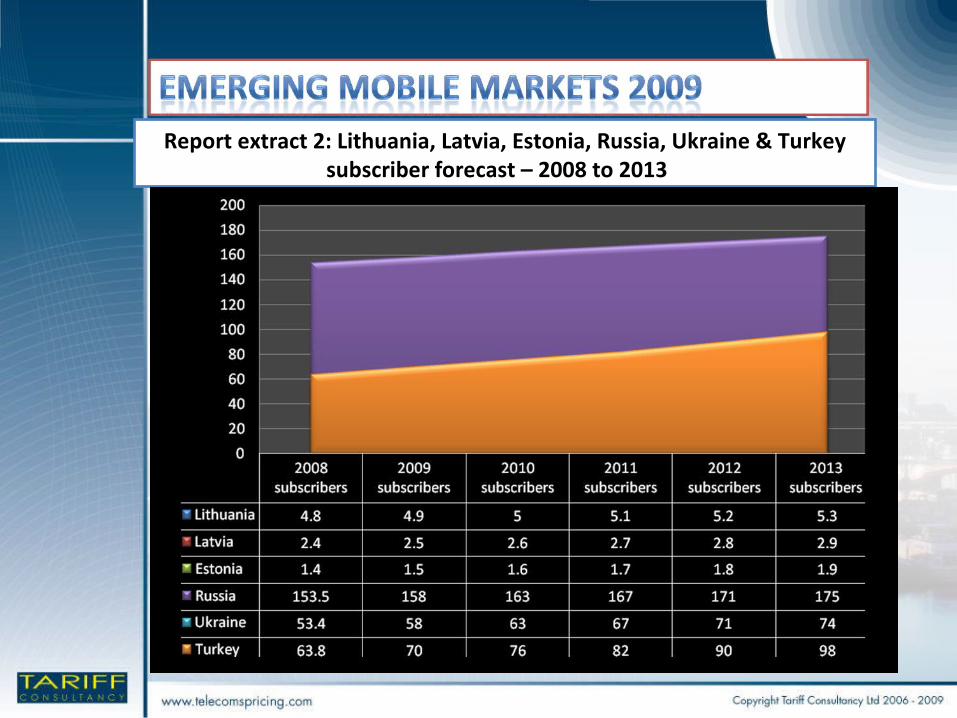

Report extract 2: Lithuania, Latvia, Estonia, Russia, Ukraine & Turkey subscriber forecast – 2008 to 2013

The Key Take Away’s from the report – 2 3.Mobile operators are seeking low income groups as mobile penetration reaches maturity. Tactics include using sub-agents, door to door sales, e-card top-up’s and small denomination recharges.4.Rapid subscriber growth means that market maturity is occurring relatively quickly – but the onset of multiple SIM ownership indicates that high penetration rates are possible (and currently stand at over 120% in Russia).5.Some mobile operators are starting to deploy products for specific segments, in particular the youth segment which accounts for a large proportion of emerging market country populations (up to 55% of Afghanistan’s population). 6.The cost of entry into an Emerging Market continues to increase, with new licence and existing operator acquisition costs being inflated by purchasers from the Gulf States.

Report extract 3: Africa (Nigeria, Morocco, Libya, Kenya, Ghana & Egypt) subscriber forecast – 2008 to 2013

Report extract 4: Pakistan, Iraq, Iran, Bangladesh & Afghanistan subscriber forecast – 2008 to 2013

Report extract 5: Latin American (Venezuela, Peru, Mexico, Ecuador, Dominican Republic, Colombia, Chile & Argentina) subscriber forecast – 2008 to 2013

Mobile penetration rates are to increase steadily over the next 5 years

Mobile penetration across the 34 countries, from 2008 to 2013 – in millions of subscribers.

2008 2009 2010 2011 2012 2013

2109.5 2581 3069.2 3596.6 3981.4 4300.2

20082008

SubscribersSubscribers20092009

SubscribersSubscribers20102010

SubscribersSubscribers20112011

SubscribersSubscribers20122012

SubscribersSubscribers20132013

SubscribersSubscribers

ChinaChina 582582 700700 830830 950950 10001000 10501050India India 269.4269.4 390390 491491 629629 749749 819819IndonesiaIndonesia 115.1115.1 160160 220220 300300 345345 387387Brazil Brazil 135.9135.9 170170 190190 203203 215215 226226

Russia Russia 153.5153.5 158158 163163 167167 171171 175175

Pakistan Pakistan 87.887.8 9696 106106 115115 124124 132132Nigeria Nigeria 53.353.3 6060 7575 9797 110110 124124MexicoMexico 73.873.8 8282 9191 100100 108108 114114PhilippinesPhilippines 62.762.7 7373 8181 9090 9797 105105

BangladeshBangladesh 44.844.8 5656 6868 8080 9191 103103

VietnamVietnam 39.439.4 5050 6565 8080 9191 101101Turkey Turkey 63.863.8 7070 7676 8282 9090 9898IranIran 3535 4848 6060 7474 8686 9898

ThailandThailand 56.456.4 6262 7070 7777 8484 9191

China remains the largest mobile market for the next 5 years, followed by India & Indonesia but it is not the fastest-growing.

Forecast mobile subscriber growth 2008 to 2013 - CAGR percentage by country (low to highest)

1. Emerging Mobile Markets continue to see consistent subscriber growth over the next 5 years, even after the current credit crunch as mobile penetration rates approach mature market levels. Markets remain predominately Pre-Paid.

2. Pricing is becoming more competitive as countries liberalise and new mobile entrants aim to increase market share.

3. The deployment of 3G networks is encouraging the adoption of new data, VoIP and Mobile Broadband services among users who are under-served by fixed network alternatives. Operators like Orange are introducing “Internet Everywhere” packages to emerging markets.

4. Afghanistan followed by Iraq, Cambodia, Indonesia and India have the highest levels of subscriber growth over the next 5 years. • Mobile Broadband services are becoming established with 3G

networks • Discounts for “on-net” calling continues to promote multiple SIM

ownership • Flat-rate services are offering flat rate data, national & international

voice calls

The new main trends for Emerging Mobile Markets into 2009

Contact Points:

Margrit Sessions, Managing DirectorE-mail: [email protected] Keith Breed, Research DirectorE-mail: [email protected]

www.telecomspricing.com