MOBA Network Initiating Coverage - s3-eu-west-1.amazonaws.com

38

Important information: All information regarding limitation of liability and potential conflicts of interest can be found at the end of the report Redeye, Mäster Samuelsgatan 42, 10tr, Box 7141, 103 87 Stockholm. Tel. +46 8-545 013 30, E-post: [email protected] Update Equity Research 1 June 2020 KEY STATS Ticker MOBA Market First North Stockholm Share Price (SEK) 140 Market Cap (MSEK) 240 Net Cash 20E (MSEK) 23 Free Float 20 % Avg. daily volume (‘000) 1 BEAR BASE BULL 85 170 300 KEY FINANCIALS (SEK) 18/19 19/20E 20/21E 21/22E 22/23E Net sales 23 32 43 57 69 EBITDA 12 15 21 28 34 EBIT 11 14 19 25 31 EPS (adj.) 5.6 5.3 7.8 10.6 12.7 EV/Sales 6.6 6.5 4.6 3.2 2.4 EV/EBITDA 12.8 13.7 9.4 6.4 4.9 EV/EBIT 13.9 15.4 10.6 7.2 5.4 P/E 20.7 26.2 17.9 13.2 11.0 ANALYSTS Jonas Amnesten [email protected] Tomas Otterbeck [email protected] 3 4 4 75 85 95 105 115 125 135 145 12-dec 11-mar OMXS 30 M.O.B.A. Network MOBAlizing Network Effects Redeye initiates coverage of M.O.B.A. Network, an attractive play on rapid growth in gaming and Esports that is benefiting both from a nearer-term lockdown boost and longer- term megatrends. The company keeps activity high on its proprietary platform by connecting its communities to strong gaming IPs, while user content and network effects create strong traffic on its websites. Further M&A could help take the share to new heights. Proof of concept M.O.B.A. was founded in 2018 to harness the attractive niche of gaming-related communities, which attract millions of visitors each month. Its sites date as far back as 2009, though. These were created by League of Legends (LoL)-focused subsidiary CriticalClick, which was acquired in September 2018. Since then the company has improved operations and added game IPs to increase revenues. The result is clear, with FY 2018/19 and H1’19/20 growth of over 50%, and 40%, respectively. Corona boost With its gaming/Esport community focus, M.O.B.A. is capitalizing on increased interest in gaming, as well as gamers’ rising purchasing power. The Coronavirus Crisis has boosted user activity in the communities, while Q3’s greater focus on direct sales has turned programmatic deals into to direct deals. April’s 47% Y/Y growth despite the Crisis shows the benefits of the strong Network and brands. Diversifying beyond LoL Although LoL is one of the most popular games in the world, M.O.B.A. is diversifying its substantial exposure as about 95% of all traffic in its network relates to LoL sites. Similarly, its largest community - Mobafire.com - generates some 80% of traffic. The company is adding new websites, such as Runeterrafire.com, that focus on different games and could benefit from the large network of gamers visiting the communities. Attractive position The quality of M.O.B.A.’s communities and its exposure to the gaming/Esports industry are valuable assets. The improvement possibilities of the existing business are also substantial. However, high expectations demand that it continues growing rapidly in the coming years. M&As are not included in our base case estimates, or valuation, but are the likeliest catalyst for the share and could provide confirmation of the company’s strategy creating shareholder value. We regard the stock’s current trading level as, somewhat, unjust and point to potential upside of about 20% to our base case valuation of SEK 170. M.O.B.A. Network Sector: Betting/Entertainment REDEYE RATING FAIR VALUE RANGE Financials People Business

Transcript of MOBA Network Initiating Coverage - s3-eu-west-1.amazonaws.com

Important information: All information regarding limitation of liability and potential conflicts of interest can be found at the end of the report Redeye, Mäster Samuelsgatan 42, 10tr, Box 7141, 103 87 Stockholm. Tel. +46 8-545 013 30, E-post: [email protected]

Update

Equity Research 1 June 2020

KEY STATS

Ticker MOBA Market First North Stockholm

Share Price (SEK) 140 Market Cap (MSEK) 240 Net Cash 20E (MSEK) 23 Free Float 20 %

Avg. daily volume (‘000) 1

BEAR BASE BULL 85

170

300

KEY FINANCIALS (SEK)

18/19 19/20E 20/21E 21/22E 22/23E Net sales 23 32 43 57 69 EBITDA 12 15 21 28 34 EBIT 11 14 19 25 31 EPS (adj.)

17/18 18/19 19/20E 20/21E 21/22E 22/23E EPS (adj.) 5.6 5.3 7.8 10.6 12.7 EV/Sales 6.6 6.5 4.6 3.2 2.4 EV/EBITDA 12.8 13.7 9.4 6.4 4.9 EV/EBIT 13.9 15.4 10.6 7.2 5.4 P/E 20.7 26.2 17.9 13.2 11.0

ANALYSTS

Jonas Amnesten [email protected] Tomas Otterbeck [email protected]

34 4

75

85

95

105

115

125

135

145

12-dec 11-mar

OMXS 30

M.O.B.A. Network

MOBAlizing Network Effects Redeye initiates coverage of M.O.B.A. Network, an attractive play on rapid growth in

gaming and Esports that is benefiting both from a nearer-term lockdown boost and longer-

term megatrends. The company keeps activity high on its proprietary platform by

connecting its communities to strong gaming IPs, while user content and network effects

create strong traffic on its websites. Further M&A could help take the share to new heights.

Proof of concept

M.O.B.A. was founded in 2018 to harness the attractive niche of gaming-related

communities, which attract millions of visitors each month. Its sites date as far back as

2009, though. These were created by League of Legends (LoL)-focused subsidiary

CriticalClick, which was acquired in September 2018. Since then the company has

improved operations and added game IPs to increase revenues. The result is clear, with FY

2018/19 and H1’19/20 growth of over 50%, and 40%, respectively.

Corona boost

With its gaming/Esport community focus, M.O.B.A. is capitalizing on increased interest in

gaming, as well as gamers’ rising purchasing power. The Coronavirus Crisis has boosted

user activity in the communities, while Q3’s greater focus on direct sales has turned

programmatic deals into to direct deals. April’s 47% Y/Y growth despite the Crisis shows

the benefits of the strong Network and brands.

Diversifying beyond LoL

Although LoL is one of the most popular games in the world, M.O.B.A. is diversifying its

substantial exposure as about 95% of all traffic in its network relates to LoL sites. Similarly,

its largest community - Mobafire.com - generates some 80% of traffic. The company is

adding new websites, such as Runeterrafire.com, that focus on different games and could

benefit from the large network of gamers visiting the communities.

Attractive position

The quality of M.O.B.A.’s communities and its exposure to the gaming/Esports industry are

valuable assets. The improvement possibilities of the existing business are also

substantial. However, high expectations demand that it continues growing rapidly in the

coming years. M&As are not included in our base case estimates, or valuation, but are the

likeliest catalyst for the share and could provide confirmation of the company’s strategy

creating shareholder value. We regard the stock’s current trading level as, somewhat,

unjust and point to potential upside of about 20% to our base case valuation of SEK 170.

M.O.B.A. Network Sector: Betting/Entertainment

REDEYE RATING

FAIR VALUE RANGE

Financials

People

Business

REDEYE Equity Research M.O.B.A. Network 1 June 2020

2

Investment Thesis Communities

M.O.B.A.’s communities benefit from substantial user content, as well as network effects.

User content is cheap, as it requires limited rescores from the company, and has a strong

positive effect from an SEO (Search Engine Optimization) perspective too. The community

also creates network effects as the number of users and volume of relevant content grows.

This will become even more attractive as it increases in size, creating considerable moats if it

becomes one of the leading communities in its niche.

A fast-growing company in a fast-growing sector

M.O.B.A. focuses on communities in the sustainable gaming sector - particularly brands that

are suitable for Esport. The gaming sector is set to grow rapidly in the coming years, and

Esports will grow even faster. Several megatrends drive this growth:

• Increased demand for free time entertainment

• Games come of age with increased spending power, as well as a larger part of the

population considering themselves gamers

• Increased internet penetration in emerging markets

M.O.B.A. has also proven that it can grow both visitor traffic and revenues substantially faster

than the underlying market.

Strong gaming IPs

M.O.B.A. owns communities that focus on some of the most influential gaming IPs in the

world, with the largest community, Mobafire.com, focusing on the League of Legends (LoL)

game. LoL is ranked No.1 in the world - both as the most popular core PC game and as the

most watched game on Twitch, according to Newzoo.com. We expect strong IPs like LoL to

benefit from an extended lifetime, which should ensure long-lasting activity in the

communities.

Adding communities and economies of scale

The group can grow by adding new communities, either through in-house launches on its

proprietary platform or acquisitions. It develops and launches new in-house communities in

conjunction with releases of new games. To get them off to strong starts, M.O.B.A. cross-

promotes these launches to its existing communities in the same genre. New websites are

increasing diversification, with the newly launched site Runeterrafire.com seeing rapid

growth.

Furthermore, the company is working to improve its existing websites. This has led to traffic

growth of several hundred percent at Counterstats.net, Smitefire.com, and Leaguespy.gg. We

also believe that there is considerable room to improve the average revenue per user as well.

M.O.B.A.’s clear M&A focus in the gaming community niche is evident in its successful

acquisition of CriticalClick in 2018. Today many communities in the sector operate at a

“hobby” level that offers substantial potential for synergies and optimization if

commercialized under M.O.B.A.’s umbrella. Accordingly, we see good scope for the company

to make value-adding acquisitions through new game titles, rich media, and mobile. This is,

however, not included in our base case estimates or base case valuation.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

3

Catalysts Acquisitions

M.O.B.A. has a clear M&A strategy, though it has only acquired CriticalClick so far. If this

starts to deliver results, we believe investors will value this highly and bid up the share

significantly. Both through its Board (Fredrik Burvall, Jonas Bertilsson, and Maria Andersson

Grimaldi) and CEO, it benefits from extensive experience in adding value via M&A.

Potential target

M.O.B.A. could be a potential acquisition target for companies seeking to access attractive

traffic volumes from the rapidly growing gaming community. Especially for gaming or US

based companies where several M&A has been concluded to a high valuation.

Corona boosted traffic volumes

With the Coronavirus Crisis having put much of the world into isolation, gaming activity, and

traffic on game-related websites have increased. M.O.B.A.’s communities should particularly

benefit, given their focus on social games. Increased activity could potentially boost revenues

in the coming quarters and even create a longer-lasting uptick. If traffic volumes are

maintained at a higher level than before the Crisis and continues to show sequential growth,

this will confirm a strong underlying shift due to product improvements.

Expansion of the services

The new business area M.O.B.A. Services is developing new services. First out is direct sales,

partnership, and sponsorship, which potentially could multiple M.O.B.A.´s revenues.

Quarterly reports

Quarterly reports showing underlying user activity growth being converted to revenues would

be positive for the case. So too would the platform’s scalability increase profit margins.

Counter-Thesis – Bear Points Short history

M.O.B.A. has notable ambition and has delivered on its commitments so far. Moreover, the

acquired CriticalClick has a 10-year track record of successfully creating and managing

communities. However, as M.O.B.A. has only made one acquisition in two years, and

CriticalClick has only operated under M.O.B.A.’s umbrella since September 2018, the existing

set-up and M&A strategy still needs to prove itself further.

Community and game dependency

M.O.B.A. has significant dependence on a single community and a single game. The

company’s largest community in terms of visitor traffic - and probably in terms of revenues

too - is Mobafire.com, which generates some 80% of total traffic. Dependence on the game

‘League of Legends’ is even greater as websites that focus on this title generate about 95% of

the company´s traffic. However, these dependences are declining with the rapid growth of the

company’s other websites, and we regard League of Legends as a brand with a long lifetime.

Dependent on ads

We expect user activity in the communities to be relatively recession-resistant. However, the

majority of M.O.B.A.’s revenues depend on pricing in the ads market, which is sensitive to

economic downturns. The company is mitigating some of this risk by increasing direct sales.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

4

Table of Content

Company description ............................................................................................................................... 5

Business Model ......................................................................................................................................... 6

The Product ............................................................................................................................................ 6

Revenue Model ...................................................................................................................................... 7

Expansion opportunities ...................................................................................................................... 8

Market ....................................................................................................................................................... 10

The Gaming market ............................................................................................................................ 11

The Digital Advertising market .......................................................................................................... 13

Communities ............................................................................................................................................ 14

Management, board and ownership .................................................................................................... 20

Management team .............................................................................................................................. 20

Board of directors ................................................................................................................................ 21

Ownership structure............................................................................................................................ 22

Financials .................................................................................................................................................. 23

Financial projections ........................................................................................................................... 25

Valuation ................................................................................................................................................... 28

DCF Valuation....................................................................................................................................... 29

Relative Valuation ................................................................................................................................ 30

Summary Redeye Rating ....................................................................................................................... 34

Rating changes in the report ............................................................................................................. 34

Redeye Rating and Background Definitions ....................................................................................... 36

Redeye Equity Research team .............................................................................................................. 37

Management ........................................................................................................................................ 37

Technology Team ................................................................................................................................ 37

Life Science Team ............................................................................................................................... 37

Disclaimer ................................................................................................................................................. 38

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

5

Company description M.O.B.A. Network (M.O.B.A.) was founded in January 2018 to find suitable acquisition

candidates active within the gaming (computer game) sector, an area that M.O.B.A.’s

management and Board of Directors have previous experiences regarding business

development and expansion. M.O.B.A. is since December 2019 listed on Nasdaq First North

Growth Market and has 16 employees working from Sweden, the US, Canada, Serbia as well

as Romania.

• Business idea: Being the home of some of the world´s most popular and high-quality

gaming/Esport communities.

• Vision: Be the world´s best and largest gaming/Esport community

• Mission: Offer platform and tools to enable gamers to share strategies, bringing

games closer to each other around the globe

In September 2018, the Canadian company CriticalClick Inc. was acquired with established

brands, a solid knowledge base, and profitability with good margins. M.O.B.A. assessed good

opportunities to add its own experiences from the expansion of similar businesses with the

aim of developing CriticalClick through growth, efficiency, and other rationalization gains.

CriticalClick

Since 2009, CriticalClick has developed online-based meeting places, so-called communities,

for users of popular network-based computer games such as League of Legends, DOTA 2,

SMITE, and more. The business currently operates ten communities, some of which can be

regarded as the largest in the world. During some months, the meeting places generate more

than 50 million site visits.

The revenue is generated by internet-based advertising on the websites that constitute the

meeting places. Members of communities are usually well-informed and buoyant consumers

that can be difficult to reach through conventional marketing, and therefore constitute

attractive target groups for a wide range of advertisers.

History

• 2009: The founders of CriticalClick establish mobafire.com – an idea of creating a

community for the game League of Legends.

• 2010: The Company CriticalClick is created after that Mobafire shows good revenue,

and the founders plan for new communities.

• 2011-2016: CrititcalClick launches new communities; Dotafire, Smitefire, and

Heroesfire. The Company pays dividends of SEK 4.3m to the founders for the

financial year 2016.

• 2017: CriticalClick enters into collaboration with Venatus Media that is responsible

for the Company's advertising sales. This is the Company’s first major commercial

agreement and will soon result in further revenue increases. The Company is also

launching two new projects targeting League of Legends, Counterstats.net, and

Leaguespy.net. The Company pays dividends of SEK 4.1m to the founders.

• 2018: M.O.B.A. Network AB was founded in January, intending to be the parent

company of potential operating companies. M.O.B.A. Network acquires CriticalClick

in September. The Company launches its latest project, artifactfire.com. Before the

acquisition, the Company pays dividends of SEK 6.4 million to the founders.

• 2019: M.O.B.A. Network AB conducts an unrestricted share issuance before the

listing of the Company’s share, where after the number of shareholders amounts to

approximately 500.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

6

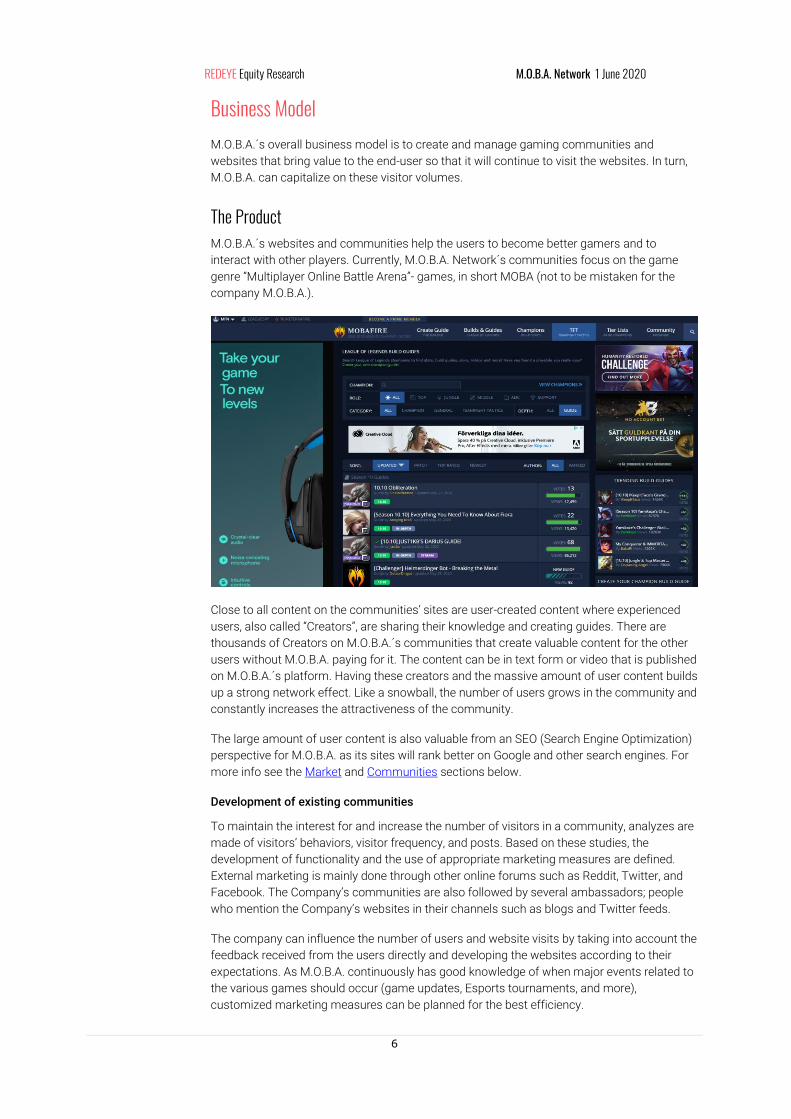

Business Model M.O.B.A.´s overall business model is to create and manage gaming communities and

websites that bring value to the end-user so that it will continue to visit the websites. In turn,

M.O.B.A. can capitalize on these visitor volumes.

The Product M.O.B.A.´s websites and communities help the users to become better gamers and to

interact with other players. Currently, M.O.B.A. Network´s communities focus on the game

genre “Multiplayer Online Battle Arena”- games, in short MOBA (not to be mistaken for the

company M.O.B.A.).

Close to all content on the communities’ sites are user-created content where experienced

users, also called “Creators”, are sharing their knowledge and creating guides. There are

thousands of Creators on M.O.B.A.´s communities that create valuable content for the other

users without M.O.B.A. paying for it. The content can be in text form or video that is published

on M.O.B.A.´s platform. Having these creators and the massive amount of user content builds

up a strong network effect. Like a snowball, the number of users grows in the community and

constantly increases the attractiveness of the community.

The large amount of user content is also valuable from an SEO (Search Engine Optimization)

perspective for M.O.B.A. as its sites will rank better on Google and other search engines. For

more info see the Market and Communities sections below.

Development of existing communities

To maintain the interest for and increase the number of visitors in a community, analyzes are

made of visitors’ behaviors, visitor frequency, and posts. Based on these studies, the

development of functionality and the use of appropriate marketing measures are defined.

External marketing is mainly done through other online forums such as Reddit, Twitter, and

Facebook. The Company’s communities are also followed by several ambassadors; people

who mention the Company’s websites in their channels such as blogs and Twitter feeds.

The company can influence the number of users and website visits by taking into account the

feedback received from the users directly and developing the websites according to their

expectations. As M.O.B.A. continuously has good knowledge of when major events related to

the various games should occur (game updates, Esports tournaments, and more),

customized marketing measures can be planned for the best efficiency.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

7

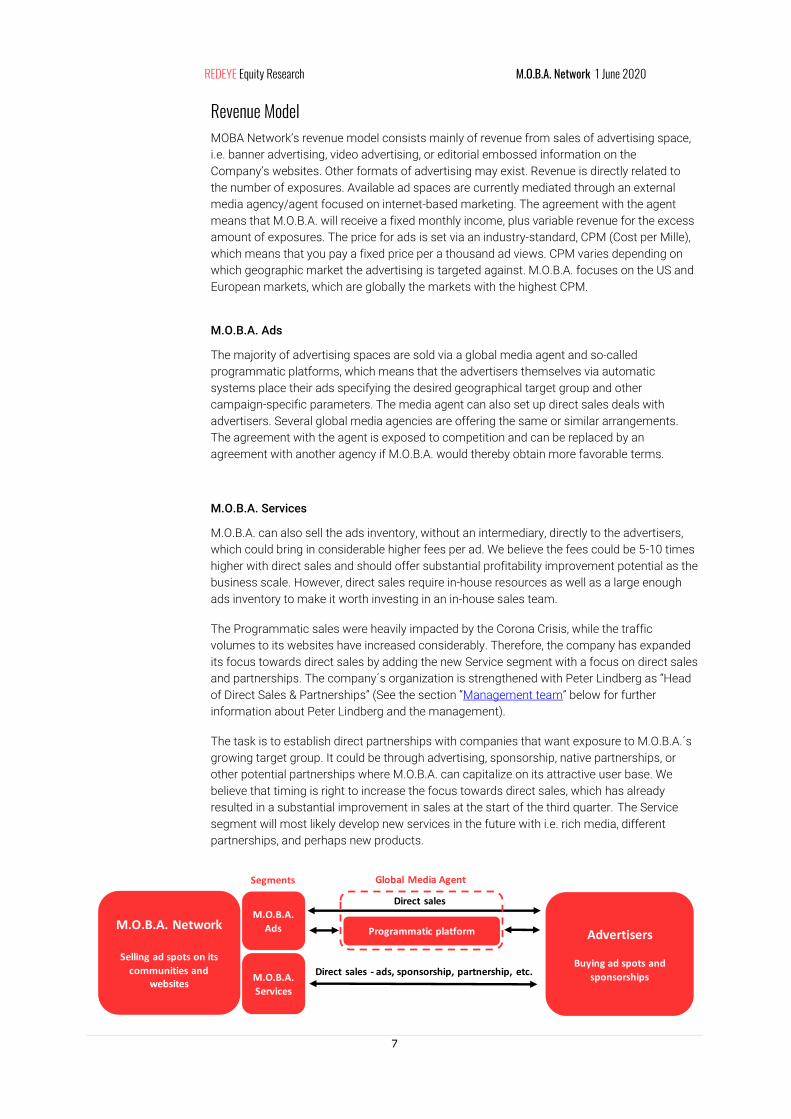

M.O.B.A. Network

Selling ad spots on its

communities and websites

Programmatic platform Advertisers

Buying ad spots and

sponsorships

Direct sales

M.O.B.A.

Ads

M.O.B.A.

Services

Direct sales - ads, sponsorship, partnership, etc.

Global Media AgentSegments

Revenue Model MOBA Network’s revenue model consists mainly of revenue from sales of advertising space,

i.e. banner advertising, video advertising, or editorial embossed information on the

Company’s websites. Other formats of advertising may exist. Revenue is directly related to

the number of exposures. Available ad spaces are currently mediated through an external

media agency/agent focused on internet-based marketing. The agreement with the agent

means that M.O.B.A. will receive a fixed monthly income, plus variable revenue for the excess

amount of exposures. The price for ads is set via an industry-standard, CPM (Cost per Mille),

which means that you pay a fixed price per a thousand ad views. CPM varies depending on

which geographic market the advertising is targeted against. M.O.B.A. focuses on the US and

European markets, which are globally the markets with the highest CPM.

M.O.B.A. Ads

The majority of advertising spaces are sold via a global media agent and so-called

programmatic platforms, which means that the advertisers themselves via automatic

systems place their ads specifying the desired geographical target group and other

campaign-specific parameters. The media agent can also set up direct sales deals with

advertisers. Several global media agencies are offering the same or similar arrangements.

The agreement with the agent is exposed to competition and can be replaced by an

agreement with another agency if M.O.B.A. would thereby obtain more favorable terms.

M.O.B.A. Services

M.O.B.A. can also sell the ads inventory, without an intermediary, directly to the advertisers,

which could bring in considerable higher fees per ad. We believe the fees could be 5-10 times

higher with direct sales and should offer substantial profitability improvement potential as the

business scale. However, direct sales require in-house resources as well as a large enough

ads inventory to make it worth investing in an in-house sales team.

The Programmatic sales were heavily impacted by the Corona Crisis, while the traffic

volumes to its websites have increased considerably. Therefore, the company has expanded

its focus towards direct sales by adding the new Service segment with a focus on direct sales

and partnerships. The company´s organization is strengthened with Peter Lindberg as “Head

of Direct Sales & Partnerships” (See the section “Management team” below for further

information about Peter Lindberg and the management).

The task is to establish direct partnerships with companies that want exposure to M.O.B.A.´s

growing target group. It could be through advertising, sponsorship, native partnerships, or

other potential partnerships where M.O.B.A. can capitalize on its attractive user base. We

believe that timing is right to increase the focus towards direct sales, which has already

resulted in a substantial improvement in sales at the start of the third quarter. The Service

segment will most likely develop new services in the future with i.e. rich media, different

partnerships, and perhaps new products.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

8

Expansion opportunities The communities that have been built up over ten years are today based on the same

scalable platform, meaning that the basic format can easily be reused and adapted to build

new meeting places around several successful game titles. The Board of directors at

M.O.B.A. sees clear expansion opportunities through introductions to new communities and

the acquisition of suitable websites.

Launch of new communities

New communities are based on the company’s existing platform, where the content is

adapted to the current game. After that, the company’s Community Managers must maintain

proper responsiveness to users' wishes and other trends in the gaming market. New

communities can be marketed through existing communities, as users often have an interest

in news, as well as through search engines and established player reviews through social

media or other channels.

M.O.B.A.´s decision to launch a new community is preceded by a number of assessments;

whether the company possesses sufficient insight into the current underlying game, whether

the current game is sufficiently versatile and complex to motivate practitioners and followers

to engage in a community by discussing strategies and functions, commenting on contests

and events, and whether the game currently has or can be expected to reach a sufficient

number of practitioners to justify the effort. With the success of the Mobafire.com

community for the League of Legends, we see an exciting opportunity for more communities

focused on games released by Riot Games.

Focus on popular games

As a result of M.O.B.A.´s selective strategy on suitable communities, the company is focusing

much on popular game titles, as illustrated in the table below. We expect strong game titles

like the League of Legend to have a very long lifetime, which ensures long-lasting activity on

the communities.

Most Watched Games on Twitch* Most Popular Core PC Games*

Game Hours (m) No. Game

League of Legends 123.2 1 League of Legends

Call of Duty: Modern Warfare 96.3 2 Tom Clancy's Rainbow Six: Siege

Counter-Strike: Global Offensive 66.5 3 Counter-Strike: Global Offensive

Fortnite 65.9 4 Call of Duty: Modern Warfare

Grand Theft Auto V 55.9 5 Minecraft

Dota 2 41.7 6 PLAYERUNKNOWN'S BATTLEGROUNDS

Animal Crossing: New Horizons 30.6 7 Apex Legends

Escape From Tarkov 27.2 8 Overwatch

Hearthstone 23.8 9 Hearthstone

Minecraft 22.8 10 Grand Theft Auto V

Source: Newzoo

* March 2020

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

9

M&A Strategy

M.O.B.A. has stated a clear M&A strategy where it looks for additional acquisitions like the

one of CriticalClick, where operations are not commercialized or optimized. In general, we

believe it would be more “hobby” driven communities or websites with a focus on

gaming/Esports related games. With the considerable current exposure towards the League

of Legends game, we expect any acquisition to have low exposure towards that game, to

lower the dependency risk. We also believe that M.O.B.A. can realize substantial synergies

both on the revenues (cross prompting, improved ad deals) and on the costs (optimized

operations).

Acquisitions are not all about acquiring assets and domain. M.O.B.A. want through

acquisitions add people with the right skills and experience to the group. In return, M.O.B.A.

can help the acquired company to scale and let the entrepreneurs focus on the product. A

win-win for both parties and the right formula for making value-adding acquisitions, we

believe. M.O.B.A. also benefits from having extensive experience in adding value via M&A,

both through its Board (Fredrik Burvall, Jonas Bertilsson, and Maria Andersson Grimaldi) and

CEO (Björn Mannerqvist).

The company’s current financial position is strong with SEK 32m in cash, and we believe that

the company can take on an acquisition in the size of SEK 50m without taking in external

capital or paying with stocks. However, given that the company has a clear acquisition

strategy, we expect some dilution in the share if the right deal emerges as well as earn-outs.

The company also have a credit (with low interest) with a large Nordic bank which also could

offer financing on a case by case basis.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

10

Human Development Index, world average

Source: http://hdr.undp.org

0.54

0.56

0.58

0.60

0.62

0.64

0.66

0.68

0.70

0.72

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

HD

I

% Gamers per age population in the USA

Source: Newzoo, populationpyramid.net & Redeye Research

100 50 0 50 100

51-65

36-50

21-35

10-20

% that play games % that dont play games

96% 4%

78% 22%

71% 29%

37% 63%

Market M.O.B.A.´s communities are focus on the gaming and the Esport industries, which are driven

by several megatrends. Some of these trends are globally improved living standards,

demographic shifts, and digitalization. We expect to see an underlying annual growth for

M.O.B.A. Network´s market segment in the range of 10-20% in the coming years.

The company does not report geographical demographics, but based on the traffic data, we

estimate that the US is the largest market with more than 15% of the visitor traffic. The US

market is followed by Germany and Brazil, both around 5%.

Improved living standards

Global living standards are improving steadily, here visualized by the rising average World

Human Development Index. For the gaming industry, this leads to the following:

• More free time and increased demand for entertainment

• More money to spend on entertainment globally

Demographic shift – Games come of age

Demographic shift increases the average age of gamers. Popularity for games grew large

during the 80s and 90s; these are now in their mid-thirties with a lifetime peak of spending

power. We believe that the adult population that today sees games as a normal part of their

leisure time will also do so when they come close to retirement. The “gaming” generation also

passes on their interest to their children, which will lead to more even more adults playing

games in the future. In the US there are today about 160 million people in the ages 10-65 that

play games at least one time per month. Demographic shifts will lead to an increasing share

of people closer to retirement playing games, creating a massive opportunity and a growing

target group.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

11

Digitalization

The increased internet usage, as well as increased internet capacity, continued to drive the

digitalization of the world, with more and more services going online.

The rise of digital distribution has led to easier access to games and lower costs for selling

games, which leads to an increased share of profits for game developers. The Improved

profits lead to greater reinvestment opportunities and thus improving the gaming experience

and drive innovation.

The digitalization is also greatly impacting the advertisements industry, with rapid growth for

the digital advertisement segment. The growth is expected to continue in the years to come,

see the section “The Digital Advertising market” for further details.

The Gaming market The result of the mentioned megatrends is a robust and consistent growth for the gaming

market, with an expected annual growth of 10% for the period 2018-2022, as illustrated in the

graph below.

Global internet user penetration 2014-2021

Source: Statista

0%

10%

20%

30%

40%

50%

60%

2014 2015 2016 2017 2018 2019 2020 2021

Global Gaming Market in USD bn

Source: Newzoo

0

50

100

150

200

250

2018 2019 2020E 2021E 2022E

US

D b

n

Console Tablet Smartphone PC Browser PC

$ 139bn$ 152bn

$ 165bn$ 178bn

$ 196bn

10% CAGR 2018-2022

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

12

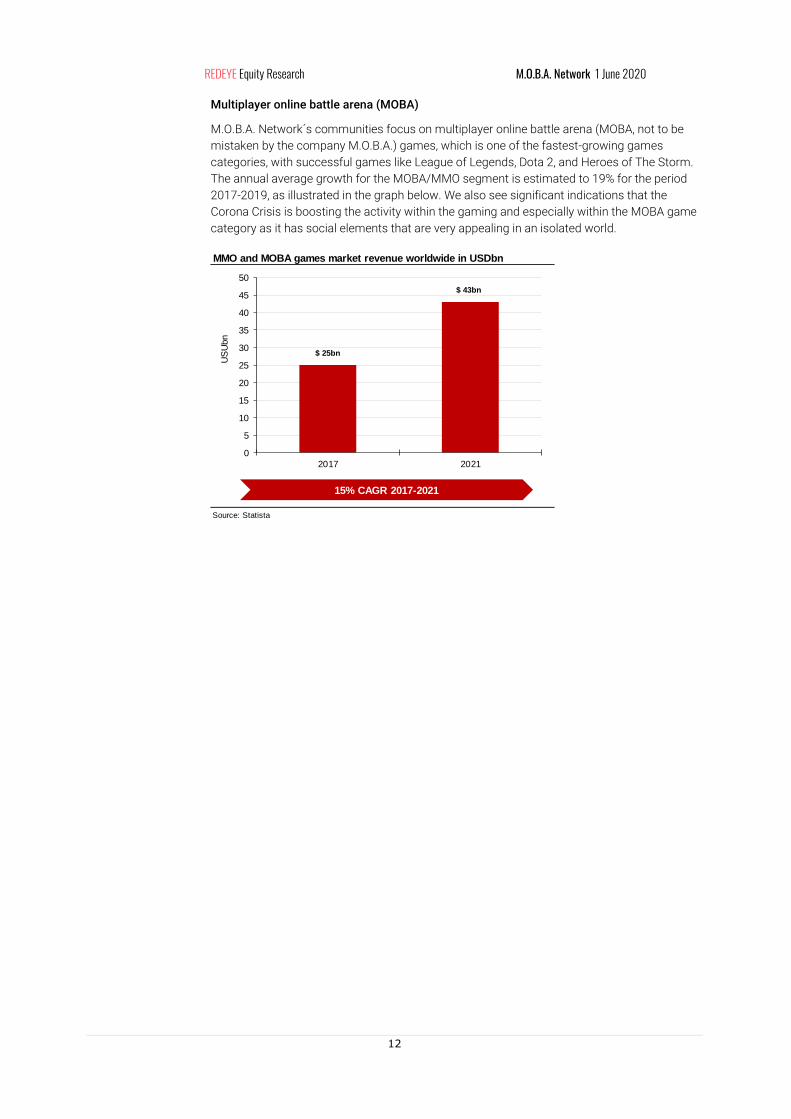

Multiplayer online battle arena (MOBA)

M.O.B.A. Network´s communities focus on multiplayer online battle arena (MOBA, not to be

mistaken by the company M.O.B.A.) games, which is one of the fastest-growing games

categories, with successful games like League of Legends, Dota 2, and Heroes of The Storm.

The annual average growth for the MOBA/MMO segment is estimated to 19% for the period

2017-2019, as illustrated in the graph below. We also see significant indications that the

Corona Crisis is boosting the activity within the gaming and especially within the MOBA game

category as it has social elements that are very appealing in an isolated world.

MMO and MOBA games market revenue worldwide in USDbn

Source: Statista

0

5

10

15

20

25

30

35

40

45

50

2017 2021

US

Ubn

$ 25bn

$ 43bn

15% CAGR 2017-2021

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

13

Highest prize pools per eSport titles 2019 eSport global revenue (mUSD)

Source: esportearnings Source: statista

223

9585

74

33

0

50

100

150

200

250

Annual

prize p

ool (m

US

D)

130 194325

493655

865

1096

14881650

1790

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Reve

nue (

mU

SD

)

CAGR 2018-2022: 20%

Esport

Electronic Sport (Esport) was born in 1972 when the earliest known video game competition

took place at Stanford University in the US for the game Spacewar. After that, Esports entered

arcade halls until games started to be played online. Since then, several players such as

Nintendo, Playstation, and Xbox have launched new hardware platforms. Today, Esports

engages over 335 million people worldwide and has developed into a billion-dollar industry

with sponsored teams, tournaments, and leagues that are broadcasted and fill arenas.

The M.O.B.A. Network´s communities focus much on the Esport vertical as both Dota 2 (1st),

and League of Legends (4th) are popular Esports games with massive prize pools as a result,

as illustrated in the left-hand graph below. The Esport market is growing rapidly with an

expected average annual growth of 20% for the period 2018-2022, as illustrated in the right-

hand graph below. This development is also converted to increased activities for

communities. According to Newzoo, the Esport communities consist of 160 million

individuals and is growing 15% annually.

The Digital Advertising market M.O.B.A.´s revenues derived from sales of advertising space on the company’s websites. The

revenues are, in the long-term, directly related to how many views are achieved of advertisers

advertising messages. In recent years, network-based marketing and advertising have

increased significantly. The digital advertising market is growing with an expected average

annual growth of 11% for the period 2017-22, as illustrated in the graph below.

Digital Advertising Market in USDbn

Source: Statista

0

50

100

150

200

250

300

350

400

450

500

2017 2018 2019 2020 2021 2022

US

Ubn

Banner Advertising Classifieds Video Advertising

Social Media Advertising Search Advertising

$ 252bn

$ 293bn

$ 336bn

$ 374bn$ 407bn

$ 433bn

11% CAGR 2017-2022

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

14

Communities Gamers and Esports supporters highly tend to establish contacts, visit forums, and contribute

to channels of information and exchange experiences. Such meeting places or networks are

referred to as communities.

M.O.B.A´s communities are based on the same concept, and a new community can,

therefore, be created on the company’s existing technology platform. Thus, the scalability of

the business is good and requires only minor investments such as graphic customization,

server space, and to some extent, targeted marketing. Furthermore, the communities offer

substantial amounts of user content as well as network effects. User content is both cheap,

as it requires limited rescores from the company, and attractive from an SEO perspective.

The community also creates network effects as the community grows in the number of users

and the amount of relevant content. The community´s attractiveness will become more

significant as it increases in size, creating considerable moats if it becomes one of the

leading communities within its game niche.

Mobafire.com – launched 2009

Mobafire is the Company’s largest individual community and is aimed for players of the

computer game League of Legends, developed by Riot and released in 2009 when Mobafire

also was launched. Over the years, League of Legends has grown to become the biggest

game within the MOBA genre, and Mobafire has evolved with the game into a very well-

known brand and popular community. In 2016, the game developer Riot announced that the

game at the time had over 100 million active players per month.

Dotafire.com – launched 2011

Dotafire is a community for players of DOTA 2, one of the most famous MOBA games

developed by Valve. DOTA 2 is one of the biggest titles in the world. The competition “The

International” held in Aug 2019 had the largest prize pool in the history of Esports, USD 34m.

Smitefire.com – launched 2012

Smitfire is a community for players of Smite, a MOBA game that figures around mythological

creatures. Smite was released in 2014 by the developer Forge Games and is available on all

major gaming platforms such as PC, Mac, Playstation, and Xbox. Unofficial figures states

that Smite has over 15 million players worldwide.

Heroesfire.com – launched 2014

Heroesfire is a community for players of Heroes of the Storm, a MOBA game where

characters meet from the developer Blizzards previous games Warcraft, Starcraft and Diablo.

Vaingloryfire.com – launched 2014

Vaingloryfire is a community for players of Vainglory, a MOBA game for the mobile platforms

iOS and Android, developed by Super Evil Megacorp. The game was launched in 2014.

Owfire.com – launched 2016

Owfire is a community for players of Overwatch, a so-called first-person shooter game in

team form. Overwatch was developed by Blizzard and was released in 2016. The game is big

within Esports through among others through the Overwatch League, which has a prize pool

of over USD 3.5m.

Leaguespy.gg & Counterstats.net – launched 2017

Leaguespy and Counterstats are websites that aggregate data from the game League of

Legends (via API) and show statistics about the different characters in the game to provide

the visitor an insight into how to best equip themselves to meet the character when playing.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

15

Artifactfire.com – launched 2018

Artifactfire is a community for players of the newly released game Artifact, a strategy card

game based on DOTA 2. Artifact was launched at the end of November in 2018 by the

developer Valve. In connection with the launch of the game, Artifactfire received a large traffic

flow and registered members who use the website’s function to build so-called card decks

and to receive constructive criticism from the members of a community.

Runeterrafire.com – launched 2020

Runeterrafire is a website that allows the users to create so-called “card-decks” based on the

game cards from the game Legends of Runeterra. In addition, beginners are offered

information about each card and character in the game.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

16

DomainGame

focus

Traffic

(million)*

Traffic

Growth** (%)

Main markets

(% of Traffic)

Avg. Visit

Duration

Bounce

Rate

mobafire.com League of

Legends30.82 35%

US (15%), Brazil

(5%) & Germany

(4%)

00:03:53 34%

counterstats.net League of

Legends4.83 403%

US (14%),

Germany (7%) &

Poland (5%)

00:01:22 72%

smitefire.com Smite 1.58 100%US (36%), UK (7%)

& Canada (6%)00:04:57 42%

leaguespy.gg League of

Legends0.40 100%

US (12%), Brazil

(11%) & France

(5%)

00:02:02 58%

dotafire.com DOTA 2 0.36 62%

US (15%),

Philippines (12%)

& Germany (7%)

00:02:17 53%

runeterrafire.com

Legends

of

Runeterra

0.24 n.m.

US (16%), Brazil

(7%) & France

(5%)

00:02:27 39%

heroesfire.com Heroes of

the Storm0.22 47%

US (19%),

Germany (8%) &

Brazil (7%)

00:04:25 45%

vaingloryfire.com Vainglory 0.02 -67%

US (18%), Turkey

(8%) & Russia

(8%)

00:02:53 54%

Total 38.5 53%

Source: Redeye Research, Similarweb.com

*Monthly traffic based on traffic data estimates from Similarweb.com

**Last six months

M.O.B.A. Network: Top domains

Traffic data

We show visitor traffic KPIs for M.O.B.A.´s website domains below. These are based on

estimates from Similarweb.com1. Overall traffic to the sites is growing rapidly – up 53% in the

last six months. This is a considerably faster growth rate than that of either peer

communities (which we comment further on below) or the underlying market. This suggests

that M.O.B.A.’s efforts to improve the sites are paying off.

The data also reveals M.O.B.A.’s significant dependence on Mobafire.com. This community

generates about 80% of the company´s visitor traffic. This probably corresponds closely to

revenue streams, making M.O.B.A.´s revenues highly sensitive to Mobafire.com’s

performance. The same goes for its dependence on the ‘League of Legends’ (LoL) game

since as much as 95% of traffic is generated from LoL-focused sites.

Furthermore, we note that none of the sites/communities released after Mobafire.com has

yet grown to a size that impacts the group’s overall traffic substantially. It may be that

CriticalClick put its greatest efforts into the successful Mobafire.com site, but in our view, it

also shows the challenge of making new sites succeed. However, M.O.B.A’s increased efforts

to improve its other brands are beginning to pay off as these sites are now seeing excess

growth.

1 M.O.B.A. confirms that Similarweb.com´s estimates give a correct picture of the domains’ relative performance. However, the actual traffic numbers are about 25% higher. M.O.B.A. reports 50m visits in April, for example, compared to Similarweb.com’s 38.5m.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

17

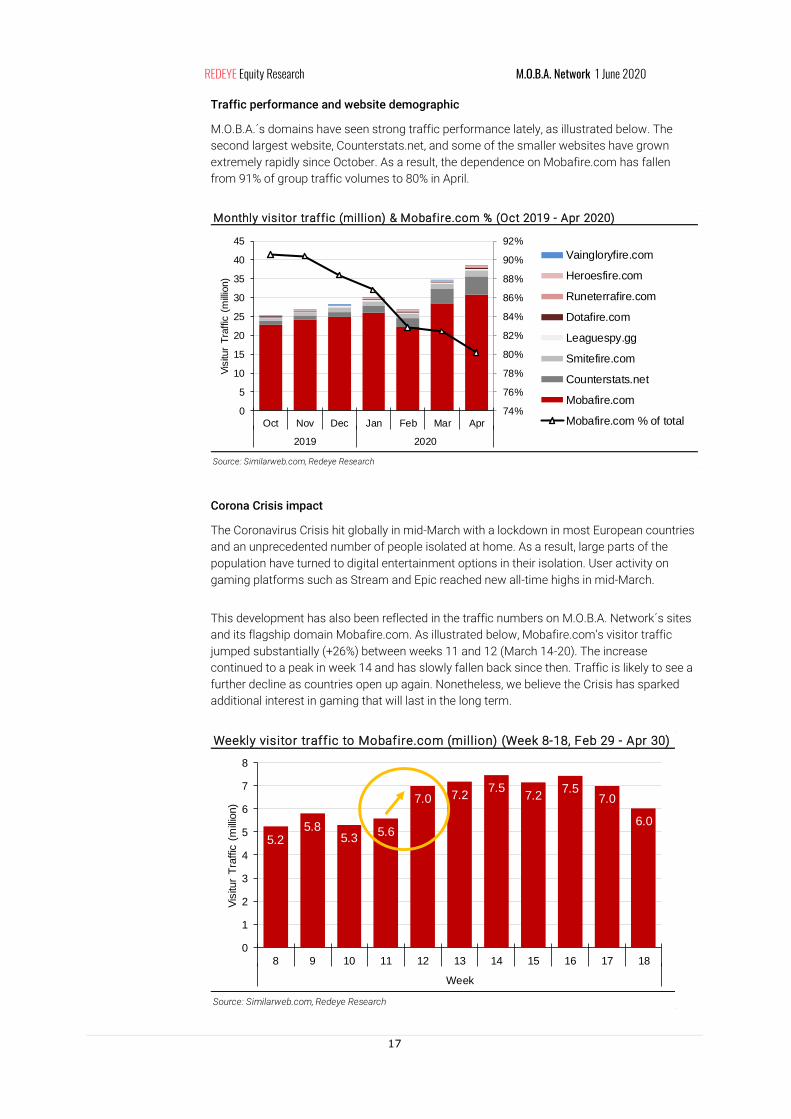

Traffic performance and website demographic

M.O.B.A.´s domains have seen strong traffic performance lately, as illustrated below. The

second largest website, Counterstats.net, and some of the smaller websites have grown

extremely rapidly since October. As a result, the dependence on Mobafire.com has fallen

from 91% of group traffic volumes to 80% in April.

Corona Crisis impact

The Coronavirus Crisis hit globally in mid-March with a lockdown in most European countries

and an unprecedented number of people isolated at home. As a result, large parts of the

population have turned to digital entertainment options in their isolation. User activity on

gaming platforms such as Stream and Epic reached new all-time highs in mid-March.

This development has also been reflected in the traffic numbers on M.O.B.A. Network´s sites

and its flagship domain Mobafire.com. As illustrated below, Mobafire.com’s visitor traffic

jumped substantially (+26%) between weeks 11 and 12 (March 14-20). The increase

continued to a peak in week 14 and has slowly fallen back since then. Traffic is likely to see a

further decline as countries open up again. Nonetheless, we believe the Crisis has sparked

additional interest in gaming that will last in the long term.

Monthly visitor traffic (million) & Mobafire.com % (Oct 2019 - Apr 2020)

Source: Similarweb.com, Redeye Research

74%

76%

78%

80%

82%

84%

86%

88%

90%

92%

0

5

10

15

20

25

30

35

40

45

Oct Nov Dec Jan Feb Mar Apr

2019 2020

Vis

itur

Tra

ffic

(m

illio

n)

Vaingloryfire.com

Heroesfire.com

Runeterrafire.com

Dotafire.com

Leaguespy.gg

Smitefire.com

Counterstats.net

Mobafire.com

Mobafire.com % of total

Weekly visitor traffic to Mobafire.com (million) (Week 8-18, Feb 29 - Apr 30)

Source: Similarweb.com, Redeye Research

5.25.8

5.35.6

7.0 7.27.5

7.27.5

7.0

6.0

0

1

2

3

4

5

6

7

8

8 9 10 11 12 13 14 15 16 17 18

Week

Vis

itur

Tra

ffic

(m

illio

n)

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

18

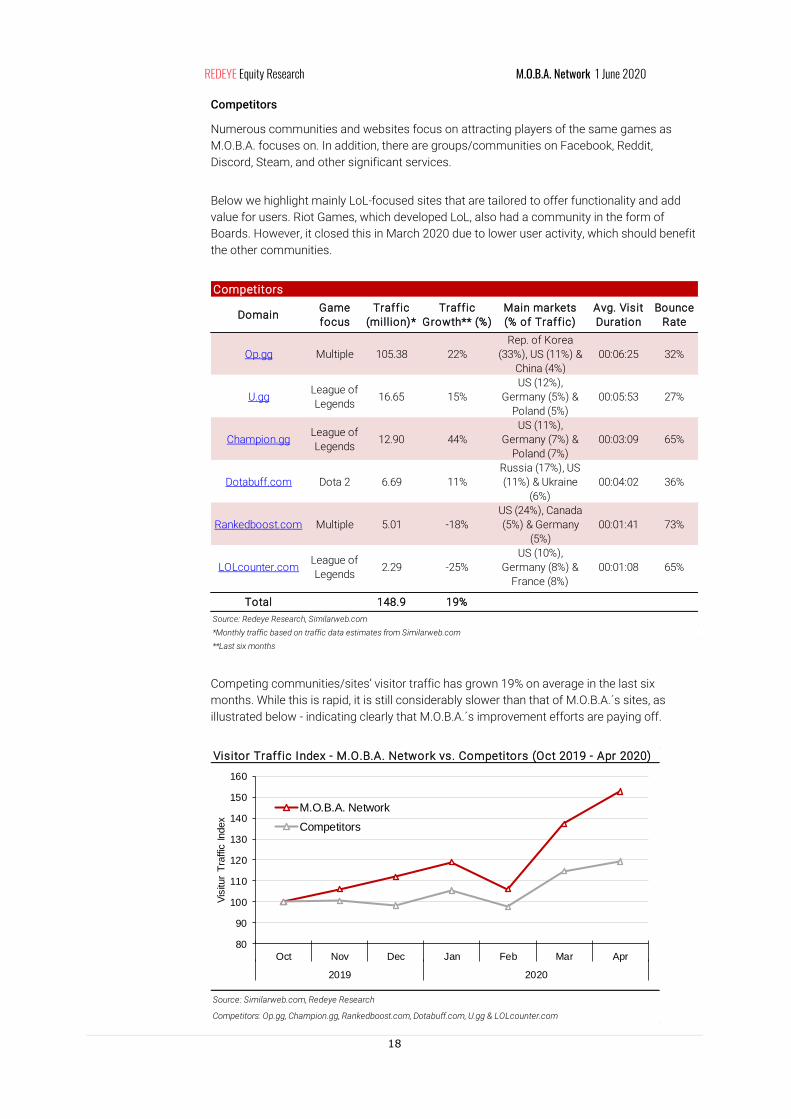

Competitors

Numerous communities and websites focus on attracting players of the same games as

M.O.B.A. focuses on. In addition, there are groups/communities on Facebook, Reddit,

Discord, Steam, and other significant services.

Below we highlight mainly LoL-focused sites that are tailored to offer functionality and add

value for users. Riot Games, which developed LoL, also had a community in the form of

Boards. However, it closed this in March 2020 due to lower user activity, which should benefit

the other communities.

Competing communities/sites’ visitor traffic has grown 19% on average in the last six

months. While this is rapid, it is still considerably slower than that of M.O.B.A.´s sites, as

illustrated below - indicating clearly that M.O.B.A.´s improvement efforts are paying off.

DomainGame

focus

Traffic

(million)*

Traffic

Growth** (%)

Main markets

(% of Traffic)

Avg. Visit

Duration

Bounce

Rate

Op.gg Multiple 105.38 22%

Rep. of Korea

(33%), US (11%) &

China (4%)

00:06:25 32%

U.ggLeague of

Legends16.65 15%

US (12%),

Germany (5%) &

Poland (5%)

00:05:53 27%

Champion.ggLeague of

Legends12.90 44%

US (11%),

Germany (7%) &

Poland (7%)

00:03:09 65%

Dotabuff.com Dota 2 6.69 11%

Russia (17%), US

(11%) & Ukraine

(6%)

00:04:02 36%

Rankedboost.com Multiple 5.01 -18%

US (24%), Canada

(5%) & Germany

(5%)

00:01:41 73%

LOLcounter.comLeague of

Legends2.29 -25%

US (10%),

Germany (8%) &

France (8%)

00:01:08 65%

Total 148.9 19%

Source: Redeye Research, Similarweb.com

*Monthly traffic based on traffic data estimates from Similarweb.com

**Last six months

Competitors

Visitor Traffic Index - M.O.B.A. Network vs. Competitors (Oct 2019 - Apr 2020)

Source: Similarweb.com, Redeye Research

Competitors: Op.gg, Champion.gg, Rankedboost.com, Dotabuff.com, U.gg & LOLcounter.com

80

90

100

110

120

130

140

150

160

Oct Nov Dec Jan Feb Mar Apr

2019 2020

Vis

itur

Tra

ffic

Index

M.O.B.A. Network

Competitors

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

19

Estimated Revenue per Visit, Minute and Page view during the full year of 2019

Source: Similarweb.com, Redeye Research

6.30

2.5

1.20

0.68

0.18 0.10 0.09

0

1

2

3

4

5

6

7

Revenue (SEK) per

Visit

Reve

nue (

SE

K)

Everysports Media Group

HLTV.org

Enthusiast Gaming

M.O.B.A. Network

0.86

0.34

0.2

0.070.02 0.02 n.m.

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Revenue (SEK) per

Minute

0.95

0.31 0.3

0.06 0.03 0.03 0.02

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Revenue (SEK) per

Page view

Capitalizing on traffic

To understand how well M.O.B.A. capitalizes on its traffic volumes, we gathered traffic data

(number of visits, minutes spent per visit, and page views per visit) for several other

communities. Please note that the data is based on estimates from Similarweb.com: the goal

is to give a rough picture of the potential for improving capitalization.

We then compared traffic data to revenues, as illustrated below. The companies we looked at

include several major services (Facebook, LinkedIn, and Twitter). We also added several

smaller community-focused companies that are gaming, sports, and Esports-related

(Enthusiast Gaming, Everysport Media Group, and HLTV.org). Enthusiast Gaming owns over

100 gaming-related sites and communities. Everysport Media Group owns several sports-

related sites and communities. HLTV.org is an Esports-related community that Better

Collective acquired earlier in 2020.

The graphs below show that M.O.B.A. is in line with other gaming-related communities, such

as Enthusiast Gaming and HLTV.org. Its revenue model is similar to Enthusiast Gaming, while

HLTV.org has a significant focus on leads for betting companies. However, we see a huge

difference. One reason is that, for example, LinkedIn makes most of its revenues from

premium functions and other services, while only around 20% is marketing-related. Facebook,

on the other hand, generates close to all its revenues from marketing, which is more like

M.O.B.A.´s business model. However, Facebook has much more data and information about

its users, which is very valuable from a marketing perspective.

Note that Everysport Media Group manages to capitalize on its traffic volumes quite well

despite being a small company. In our view, this reflects its strong affiliate partnerships.

As a result, we see considerable scope for M.O.B.A. and the gaming communities to improve

the capitalization of their traffic volumes. New solutions and partnerships are crucial to

achieving higher revenue per visitor, we judge. This makes the timing of M.O.B.A.´s new

segment, M.O.B.A. Services, very suitable. Increased marketing interest in M.O.B.A.´s target

group, gamers, should also improve user values. However, we do not expect these to expand

without substantial investment and effort.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

20

Management, board and ownership

Management team CEO - Björn Mannerqvist

Björn Mannerqvist has worked with digital marketing and SEO all over the world for 20 years.

He has a broad experience of digital solutions and rapidly growing companies. He is the

former CEO of Future Gaming Group International AB and the former Director of Operations

at Ayima Nordic AB. Currently he is a board member of several Swedish listed companies

including Tourn International AB and Orgo Tech AB.

CFO - Anna Jansson

Over five years experience of CFO-functions in listed companies, including day-to-day

bookkeeping, consolidation of group companies, producing quarterly/annual reports.

Degree of Master of Science in Business and Economics, University of Stockholm.

Head of law & IR - David Nylén

David Nylén has a vast experience of providing legal advice to listed companies, including

matters relating to M&A, IPO, and securities law. Previous professional experience include

work at a law firm, administrative court, and a listed company.

Master of Laws, LLM degree, University of Gothenburg.

Head of Direct Sales & Partnerships - Peter Lindberg

Peter Lindberg has a broad experience from marketing, sales, and leadership with a

longstanding background in various sales and sales leadership roles, including at MTG and

Lagardère Sports. Most recently, he comes from a position as Business Director at content

agency Brand New Story.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

21

Board of directors Chairman - Fredrik Burvall

Experience: Fredrik Burvall has a broad experience from digital companies and complex

organizations. As the CEO of Cherry AB (publ), chairman of Speqta, and board member at

Aspire Global, he has gained extensive experience within leadership, M&A, and Financing.

Current board assignments: Chairman of Speqta, board member Aspire Global,

Gambling.com Group, Enteractive Ltd, and tNN AB.

Previous board assignments: Chairman of Cherry Spelglädje AB. Board member and CEO of

Cherry Casino Syd AB, Playcherry PR & Media AB, and Svenska Klubbspel AB. CEO of Cherry

AB (publ). Board member of Bell Maritime Gaming AB. Board member of Yggdrasil Polska,

Yggdrasil Holding Ltd, Cherry Polska, and Cherry Holding Ltd.

Board member - Maria A. Grimaldi

Experience: Currently CEO of Bublar Group and has a vast experience from the gaming

industry as well as extensive experience of investing in gaming and tech companies.

Previously Senior Investment Manager at Goodbye Kansas Group, the investment arm of the

international gaming company the Goodbye Kansas Group. Previously CEO for the Nordic

Game Association for more than 12 years.

Current board assignments: Bublar Group (NGM), Esportal, and Full Damage Studio

(Chairman)

Previous board assignments: Pan European Game Association, Fishbrain, and Ztorm

Board member - Jonas Bertilsson

Experience: Currently CEO at AB Rugosa Invest and has a broad experience from financing,

M&As, and tech investments. Previously Partner and co-CIO at the investment fund manager

Elementa Management and Investment Director at Varenne. Prior experience also includes

Investment Banking at Carnegie and M&A at Addnode Group, a leading IT-solutions Group.

Current board assignments: Chairman of Nordic e trade AB, Board member of Net Gaming

Europe, and AB Rugosa Invest.

Previous board assignments: Varenne Invest, Pema Sweden, Bed Facory Sweden, and

Mengus Funds

Board member - Henrik Henriksson

Experience: Currently CFO at ETON Shirts. Previously Brand Controller/CFO of ”WEEKDAY" -

New Business Organisation at H&M and Brand Controller/CFO of ”COS" at H&M. . Prior

experience also includes Country Controller at H&M - US, based in New York, US.

Current board assignments (private companies): Atigarden AB, and Torrahf Invest AB

Board member - Manfred Gottschlich

Experience: Experience from investing, operating, and running companies in the areas of food

and beverage, building, and mechanical production.

Current board assignments: Olearys Holding AB, Olearys restaurants AB, Olearys trademark

AB, Interoc Holding AB, Interoc AB, Interoc projektutveckling AB, and Interoc

fastighetsutveckling AB

Previous board assignments: Powerwave Technologies, Lgp Holding AB, Lgp Telecom

Holding AB, and MG Instrument AB

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

22

Ownership structure In total, the Management and Board own around 15% of the shares in M.O.B.A., as illustrated

in the tables below. Five of nine members in the management and the Board owns shares

directly or indirectly. We highly value the large ownership amongst the management and the

Board, as it should ensure shareholder-friendly decisions.

M.O.B.A. also has two large owners in New Equity Venture International AB, and Trottholmen

AB that can add further value to the group. Moreover, the company has two institutions, TIN

Fonder (3.3%) and Alcur Fonder (1.4%), amongst its ten largest owners, which is impressive

given M.O.B.A.’s relatively small market cap and low stock liquidity.

We view the ownership structure as strong and believe it ticks all crucial boxes. However, due

to the quite large ownership amongst insiders and the largest owners, the liquidity in the

stock is below SEK 100k per trading day in the last three months. The very low liquidity

creates a liquidity risk and a large spread in the share price.

Name

Number of

shares

Value in SEKm at share price 120

SEK (excluding warrants)

Management

Björn Mannerqvist 50 000 6.0

Anna Jansson 0 0.0

David Nylen 0 0.0

Peter Lindberg 0 0.0

Board

Fredrik Burvall 2 700 0.3

Jonas Bertilsson 158 384 19.0

Manfred Gottschlich 43 000 5.2

Henrik Henriksson 1 087 0.1

Maria A. Grimaldi 0 0.0

Source: M.O.B.A. Network, Holdings.se, Redeye Research

Holdings of the management and board

Ownership structure M.O.B.A. Network

Name Capital % Management and board Capital %

New Equity Venture International AB 28.5% Management 2.9%

Trottholmen AB 22.4% Board 12.0%

AB B21 12.9% Total 15.0%

AB Rugosa Invest 9.3%

Cloverhill 9.2%

TIN Fonder 3.3%

Digital Spine AB 2.9%

Manfred Gottschlich 2.5%

Alcur Fonder 1.4%

Nordnet Pensionsförsäkring 1.1%

Other owners 6.5%

Source: M.O.B.A. Network (March 31, 2020)

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

23

Financials M.O.B.A. Network´s journey has just started, and the focus since the CriticialClick acquisition

has been to improve CriticalClick´s operations, with a shift towards more commercialized

operations. The main improvements have been to optimize the revenue by getting better

advertisement deals and enhance the value of the traffic to its domains. The impact of these

improvements can be seen in the graph below as the revenue level increased significantly in

the financial year of 2018/2019, with a growth of 56%.

This development has continued into 19/20, as illustrated in the graph below, with net

revenue growth of 47% for Q1’19/20 (Oct-Dec) and 32% for Q2’19/20 (Jan-Mar), despite a

negative Corona effect in March. The company has stated that the growth in April reach 47%

thanks to an increased focus on direct sales. The graph also demonstrates the seasonality

effect where Q1 (Oct-Dec) is the strongest quarter driven by the buying-side´s large marketing

budgets in conjunction with Black-Friday and Christmas. We find the continuous growth

evidence that there is a long-lasting growth driver behind the development.

Revenue and EBITDA margin for CriticaClick (14/15-17/18) & M.O.B.A. (18/19)

Source: M.O.B.A. Network, Redeye Research

9.510.3

9.1

14.9

23.3

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

5

10

15

20

25

Marg

in

Reve

nue (

SE

Km

)

Revenue EBITDA margin

M.O.B.A.CriticalClick

M.O.B.A. Network: Revenues and EBITDA margin

Source: M.O.B.A. Network, Redeye Research

6.35

4.79

5.955.42

9.33

6.32

0%

10%

20%

30%

40%

50%

60%

70%

0

1

2

3

4

5

6

7

8

9

10

Q1'18/19 Q2'18/19 Q3'18/19 Q4'18/19 Q1'19/20 Q2'19/20

Marg

in

SE

Km

Net Revenues Other Revenues EBITDA margin (%)

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

24

Earnings

The EBITDA in Q2´19/20 has not grown at the same pace as the revenues, as illustrated in

the graph below, due to significant investments in improving and optimizing the underlying

operations. Furthermore, the EPS has been negatively impacted by the new issue of shares in

conjunction with the IPO in December 2019.

Balance sheet

M.O.B.A. has a robust financial position with SEK 32m in cash and a net cash position of SEK

19m, which gives the group to take advantage of M&A opportunities that can create

significant equity leverage. We assess that the company could increase the debt level with an

additional SEK 20m to take on a larger acquisition, if necessary, and still maintain a stable

financial position. The company has a case by case M&A financing agreement with a large

Nordic bank, which ensures swift excisions when the right M&A opportunity emerges.

M.O.B.A. Network: EBITDA and EPS

Source: M.O.B.A. Network, Redeye Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q1'18/19 Q2'18/19 Q3'18/19 Q4'18/19 Q1'19/20 Q2'19/20

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

EP

S (

SE

K)

EB

ITD

A (

SE

Km

)

EBITDA EPS

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

25

M.O.B.A. Network: Financial Forecasts

(SEKm) 18/19 Q1'19/20 Q2'19/20 Q3'19/20E Q4'19/20E 19/20E 20/21E 21/22E

Net Revenues 22.5 9.3 6.3 7.6 7.5 30.7 42.2 55.4

Revenues 23.3 9.3 7.4 7.8 7.7 32.2 43.2 56.6

EBITDA 12.0 4.7 3.5 3.7 3.4 15.3 21.1 28.3

EBIT 11.0 4.4 3.1 3.3 2.9 13.6 18.7 25.4

Net Profit 7.1 2.9 1.8 2.2 1.9 8.9 12.9 17.7

EPS, SEK 4.93 1.87 1.07 1.30 1.13 5.37 7.57 10.29

Growth Y/Y (%) 56% 42% 52% 30% 31% 38% 34% 31%

Growth Q/Q (%) 60% -20% 4% -1%

EBITDA (%) 51% 51% 47% 48% 44% 48% 49% 50%

EBIT (%) 47% 47% 42% 42% 37% 42% 43% 45%

Source: Redeye Research

M.O.B.A. Network: Financial Forecasts by Segment

(SEKm) Q3'19/20E Q4'19/20E 19/20E 20/21E 21/22E

Business Segment - M.O.B.A. Ads

Net Revenues - Ads 7.5 7.2 30.3 39.9 50.7

Growth Y/Y (%) - Ads 25% 34% 35% 32% 27%

Growth Q/Q (%) - Ads 18% -3%

EBITDA - Ads 3.6 3.2 13.9 19.2 24.6

EBITDA margin (%) - Ads 48% 44% 46% 48% 49%

Business Segment - M.O.B.A. Services

Net Revenues - Services 0.1 0.3 0.4 2.3 4.7

Growth Y/Y (%) - Services n.m. n.m. n.m. 549% 106%

Growth Q/Q (%) - Services n.m. 150%

EBITDA - Services -0.1 0.0 -0.1 0.9 2.5

EBITDA margin (%) - Services -50% 0% -14% 37% 53%

Services % of total Net Rev. 1% 3% 1% 5% 8%

Source: Redeye Research

Financial projections Our forecasts are affected by many different factors, none of which are guaranteed,

especially from quarter to quarter. Nonetheless, some of them are very likely to occur over

time.

The growth for M.O.B.A. Network and its subsidiary, CriticalClick, has been rapid since the

acquisition in September 2018. We believe that much of this growth has been a result of

several “low-hanging fruits” when it comes to optimizing the operations. However, we still see

significant potential in operational improvements, and the last two quarters indicate a long-

lasting growth driver. Furthermore, there are several additional growth drivers going forward.

In the short-term, we expect that the Corona Crisis will have both positive and negative

effects on the company´s operations. The visitor traffic to M.O.B.A.´s websites has been

significantly boosted by the Corona Crisis as a large part of the world are isolated at home.

On the negative side, the Crisis has hit the advertisement industry with lowered budgets for

several segments.

Segments

With its new segment, “M.O.B.A. Services”, M.O.B.A. is broadening its revenue streams, and as

the business grows, we expect that this segment will become more important. The increased

focus on direct sales, sponsorships, and partnerships should generate higher prices for

M.O.B.A.´s ads, i.e. CPM. We believe this will offer both growth and scalability for the

company as well as an important step in becoming a major media partner. However, given

that it is a new segment, we only make moderate assumptions, and the Service segment will

still only generate about 8% of the sales in 2021/2022, as illustrated below.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

26

Growth drivers

• Underlying market: The underlying markets of gaming, Esport, and digital advertising

is expected to grow in the range of 10-20% in the coming years.

• New communities/sites: CriticalClick launched, on average, one new brand each

year since 2009, and M.O.B.A. has continued to maintain that level. We expect that

the company will be able to increase to two launches each year from 2021 by

expanded operations. The main focus will, however, be to keep up with the game

releases by Riot Games as there are considerable cross-promotion opportunities.

• Product improvements: M.O.B.A. has made several product improvements to

increase both the number of active users as well as the value of each user. We

believe that there still are considerable product improvement possibilities that can

be realized in the near term, such as improved SEO, social channels, e-mails, and

premium functions.

• Direct advertisement sales: M.O.B.A. is mainly selling its ads spots through a

programmatic platform, which is resource-efficient. However, M.O.B.A. has

launched a new segment towards direct sales to sell a part of the ads inventory

directly to the advertisers, which could bring in considerable higher fees per ads.

• New Services towards gaming/Esport: The company newly launched a new

Business Area, M.O.B.A. Services focusing on sponsorship, direct partnerships, and

to develop new services toward the growing gaming/Esport market.

• Acquisitions: M.O.B.A. has communicated that it is aiming to make acquisitions. We

believe that the company has the financial position to make acquisitions of a

relatively large size and that it is very likely that the company will make at least one

acquisition during 2020. We also believe that the company has all the prerequisites

to create value-adding acquisitions within its niche. However, until we know the

condition of the acquisitions, we will not add any acquisitions to our estimates but

merely add it as an important catalyst for M.O.B.A.

Cost allocation

• Employee costs: Currently, only the top management is employed in the company

as the operational team members work as consultants due to the flexible set up of

the operations.

• Other external expenses: This is the largest cost item, including most of the

operational expenses, such as consultant and sales-related expenses. We expect

the expenses for consultants to increase as the operations expand with the annual

relation to sales to be maintained. Furthermore, based on the interim reports before

the adaption to IFRS we can conclude that there are sales-related costs in the size

of around 30% in relation to revenues. We expect that the sales-related cost will

decrease slightly in relation to revenues as the company grows.

• Activated development costs: M.O.B.A. invests much in the development of its

websites and products. We expect that this item will increase slightly slower than

the revenue growth in the long-run as more maintenance than development will be

conducted on its websites and products. Note that the item is included as a revenue

item in M.O.B.A.´s PnL, while we have added it as a positive cost item.

• Other operational expenses: This is a small cost item that does not affect the overall

view.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

27

Revenues by Segment - Trailing Twelve Months

We expect that the rapid growth rate will continue in the coming years and estimate with and

CAGR of 33% for the next three years. The Service segment will help maintain the growth

pace at a high level. The launch of the new segment will, however, have a slight negative

impact on the margins at first but will contribute with a margin improvement as the segment

scales, we believe.

Profit Margin - Trailing Twelve Months

We believe that M.O.B.A. has a highly scalable business with communities that are much

driven by user content and the underlying growth of the gaming market. However, we expect

that M.O.B.A. will continue to invest in product improvements and new sites over the

foreseeable future, with a maintain the TTM EBITDA margin in the interval 45-50% as a result.

M.O.B.A. TTM: Revenues and Margin (Q4'18/19 - Q4'21/22E)

Source: M.O.B.A. Network, Redeye Research

40%

42%

44%

46%

48%

50%

52%

0

10

20

30

40

50

60

70

EB

ITD

A m

arg

in

Reve

nues T

TM

(S

EK

m)

Net Revenues TTM - Ads Net Revenues TTM - Services

EBITDA margin TTM

M.O.B.A. TTM: EBT and Margin (Q4'18/19 - Q4'21/22E)

Source: M.O.B.A. Network, Redeye Research

40%

42%

44%

46%

48%

50%

52%

0

5

10

15

20

25

30

Marg

in

EB

T T

TM

(S

EK

m)

EBT TTM EBITDA margin TTM EBIT margin TTM

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

28

M.O.B.A. Network: Fair value range

Source: Redeye Research

Last price 140

0 50 100 150 200 250 300 350Bear-case: 85Bear-case: 85 Base-case: 170 Bull-case: 300

Valuation Valuation conclusion

We argue that M.O.B.A. Network is well-positioned in an attractive market space, with an

underlying market growth of 10-20%. The company has proven that it can make operational

improvements that will help the company to grow substantially faster than the market.

Furthermore, the company has a clear M&A strategy where is can target “hobby” driven

communities and commercialize the operations. As similar acquisition like the one of

CriticalClick, could add substantial value to the group. On the downside, we still believe that

M.O.B.A. needs to prove its M&A strategy further and broaden its revenues stream. The low

liquidity in the stock is also hampering the valuation.

Nonetheless, we still see significant upside to our base case. The strong underlying growth of

the network, together with improved capitalization on the traffic volumes, could multiply the

revenues. Our Base-case valuation, based on a DCF model, amounts to 170 SEK per share,

about 20% above market levels. Our valuation range amounts to 85-300 SEK per share.

To find support for our DCF valuation, we also compare against the peers´ valuation

multiples. For peers, we have looked at companies in the gaming, Esports, and community

industries, as they are exposed to similar business conditions as M.O.B.A. When making the

comparison, we argue that an EV/EBITDA multiple of around 13x is reasonable on our

estimates for 2021 and 10x for 2022, which lines up well with our DCF valuation.

Bear Case 85 SEK Base Case 170 SEK Bull Case 300 SEK Sales CAGR of about 14% between 2019-2028

Average EBIT margin of approximately 35% during the period

Terminal growth of 2% and terminal EBIT margin of 27%

Our Bear case assumes increased competition both for the communities and for League of Legends, which will pressure the profit margins. In the aftermath of the Corona Crisis, we also expect a recession that will lower the CPM levels and putting additional pressure on the margins. Meanwhile, the new communities will only contribute to limited top-line growth.

Sales CAGR of about 21% between 2019-2028

An average EBIT margin of approximately 43% during the same period

Terminal growth of 2% and terminal EBIT margin of 38%

Our base case assumes that M.O.B.A. will continue to make significant improvements in the business in the coming years, and therefore continue to grow faster than the underlying market. We estimate with moderate revenue contribution for the new Service segment and a slight decline in the profit margins for the group beyond 2023.

Sales CAGR of about 28% between 2019-2028

Average EBIT margin of approximately 48% during the period

Terminal growth of 2% and terminal EBIT margin of 45%

Our bull case scenario assumes a substantial improvement in both revenues and profit margins in the coming years. The development will be driven by increased traffic for its communities as well as several successful launches of new communities, while the M.O.B.A. Service segment will add media partnerships. The improved capitalization on its traffic volumes will multiply the revenues. We also estimate that M.O.B.A. will make several value-adding acquisitions in the coming years.

dsfdsf REDEYE Equity Research M.O.B.A. Network 1 June 2020

29