Minor International - listed...

46

Minor International 2Q09 Analyst Meeting 17 August 2009 Pratana Mongkolkul, CFO

Transcript of Minor International - listed...

Minor International2Q09 Analyst Meeting

17 August 2009

Pratana Mongkolkul, CFO

Today’s Agenda

I. Key Issues & Business Performance

II. 2Q09 Financial Results

III. Key Strategic & Industry Update

IV. Pipeline Expansion & Cashflow Outlook

V. Q&A

I. Key Issues & Key Business Performance

New Developments in 2Q09

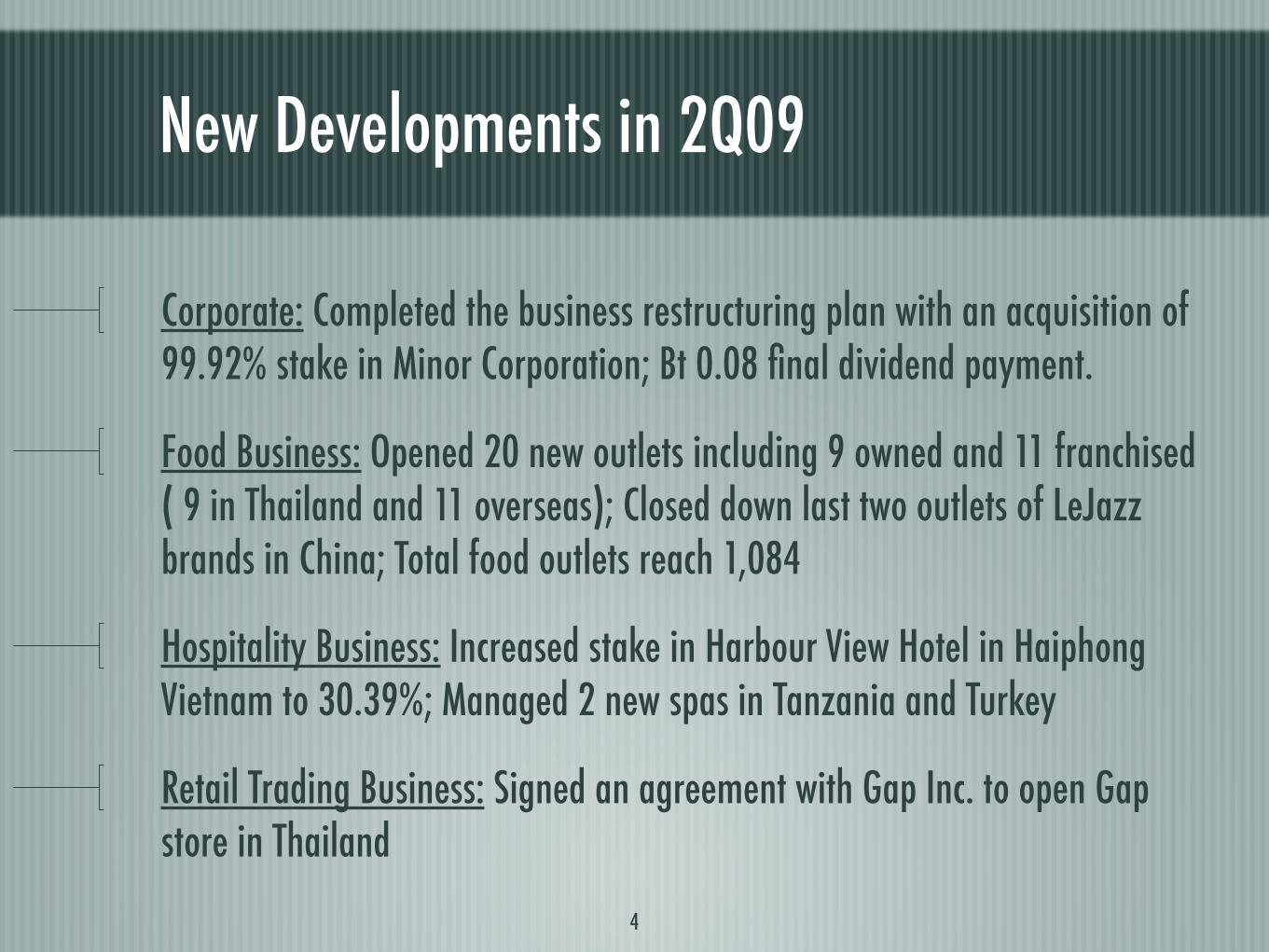

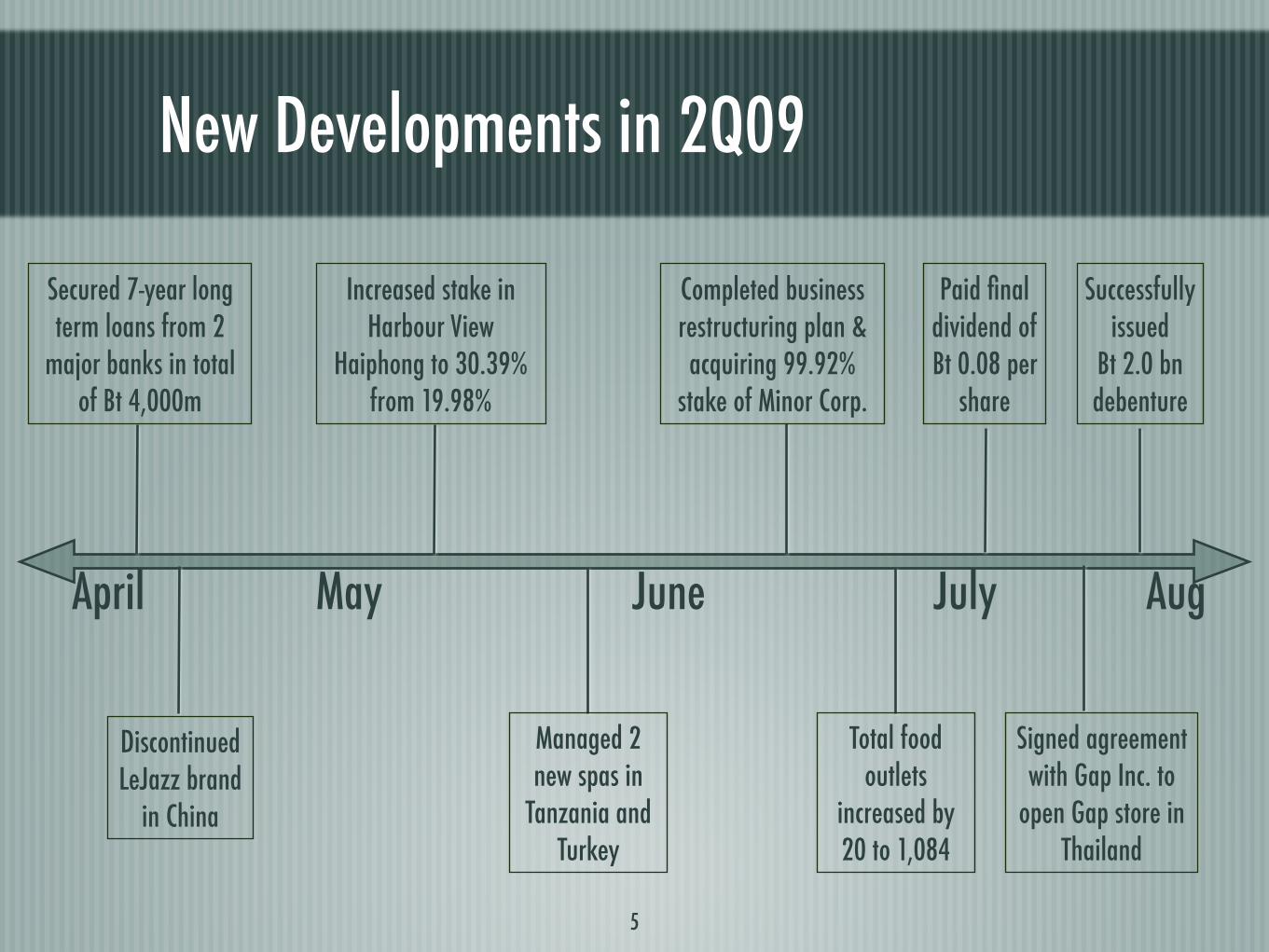

Corporate: Completed the business restructuring plan with an acquisition of 99.92% stake in Minor Corporation; Bt 0.08 final dividend payment.

Food Business: Opened 20 new outlets including 9 owned and 11 franchised ( 9 in Thailand and 11 overseas); Closed down last two outlets of LeJazz brands in China; Total food outlets reach 1,084

Hospitality Business: Increased stake in Harbour View Hotel in Haiphong Vietnam to 30.39%; Managed 2 new spas in Tanzania and Turkey

Retail Trading Business: Signed an agreement with Gap Inc. to open Gap store in Thailand

4

New Developments in 2Q09

5

April May June July

Discontinued LeJazz brand

in China

Successfully issued

Bt 2.0 bn debenture

Aug

Completed business restructuring plan & acquiring 99.92%

stake of Minor Corp.

Paid final dividend of Bt 0.08 per

share

Increased stake in Harbour View

Haiphong to 30.39% from 19.98%

Managed 2 new spas in

Tanzania and Turkey

Total food outlets

increased by 20 to 1,084

Signed agreement with Gap Inc. to

open Gap store in Thailand

Secured 7-year long term loans from 2

major banks in total of Bt 4,000m

MINT’s Business Portfolio Snapshot

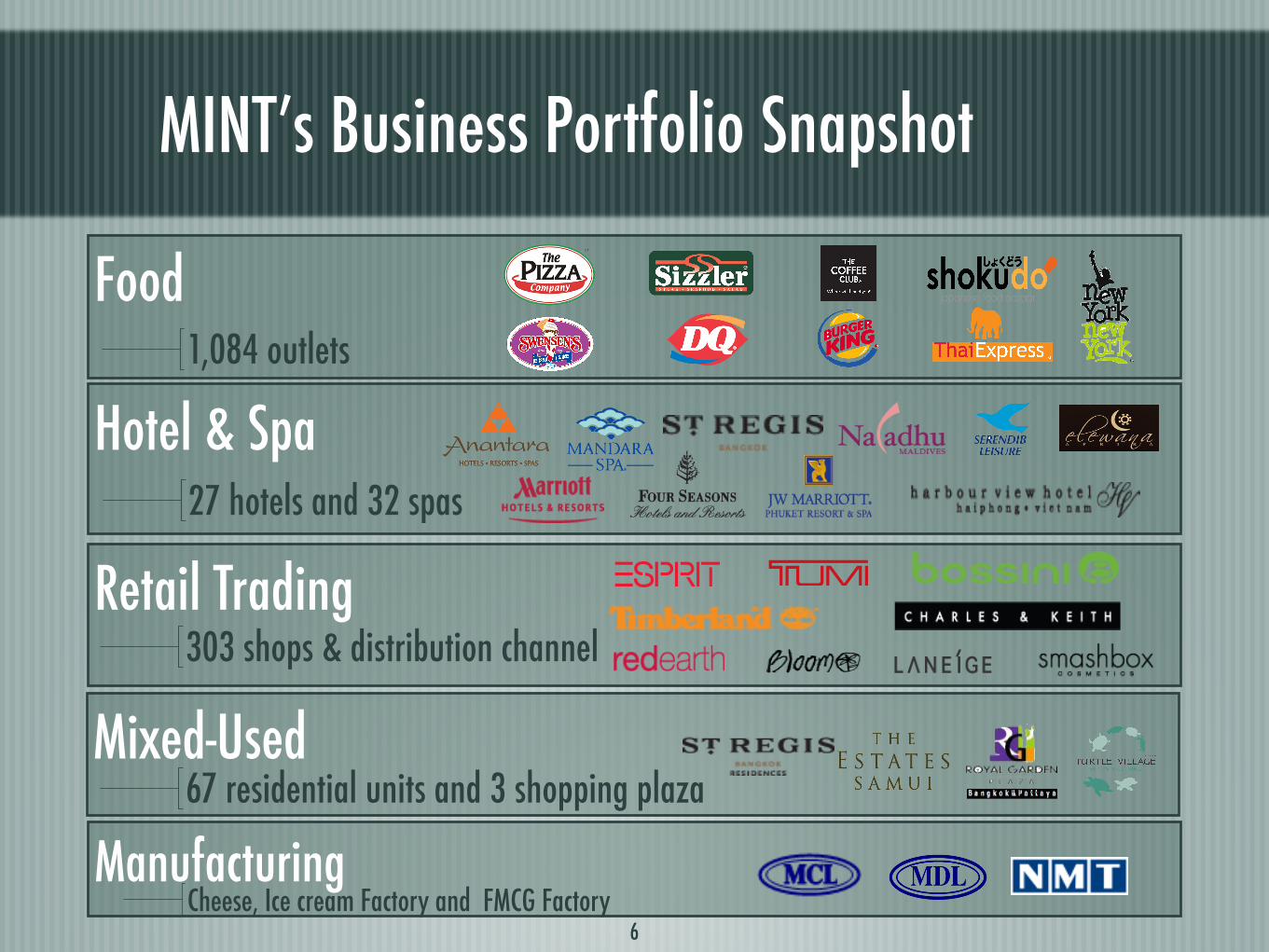

Food

Hotel & Spa

Mixed-Used

Manufacturing

Retail Trading

6

1,084 outlets

27 hotels and 32 spas

303 shops & distribution channel

67 residential units and 3 shopping plaza

Cheese, Ice cream Factory and FMCG Factory

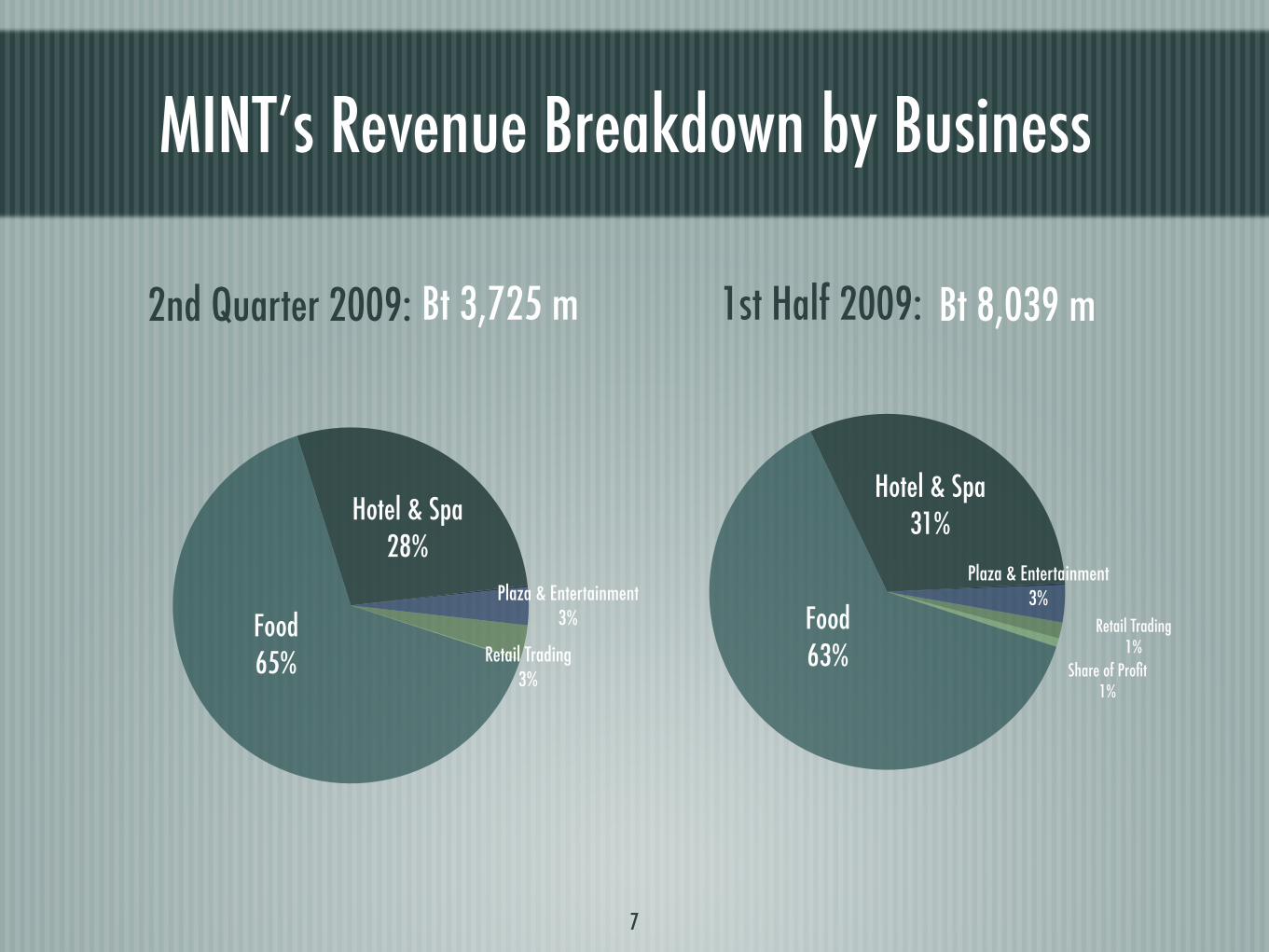

MINT’s Revenue Breakdown by Business

2nd Quarter 2009: Bt 3,725 m 1st Half 2009: Bt 8,039 m

Food63%

Hotel & Spa31%

Plaza & Entertainment3%

Retail Trading1%

Share of Profit1%

Food65%

Hotel & Spa28%

Plaza & Entertainment3%

Retail Trading3%

7

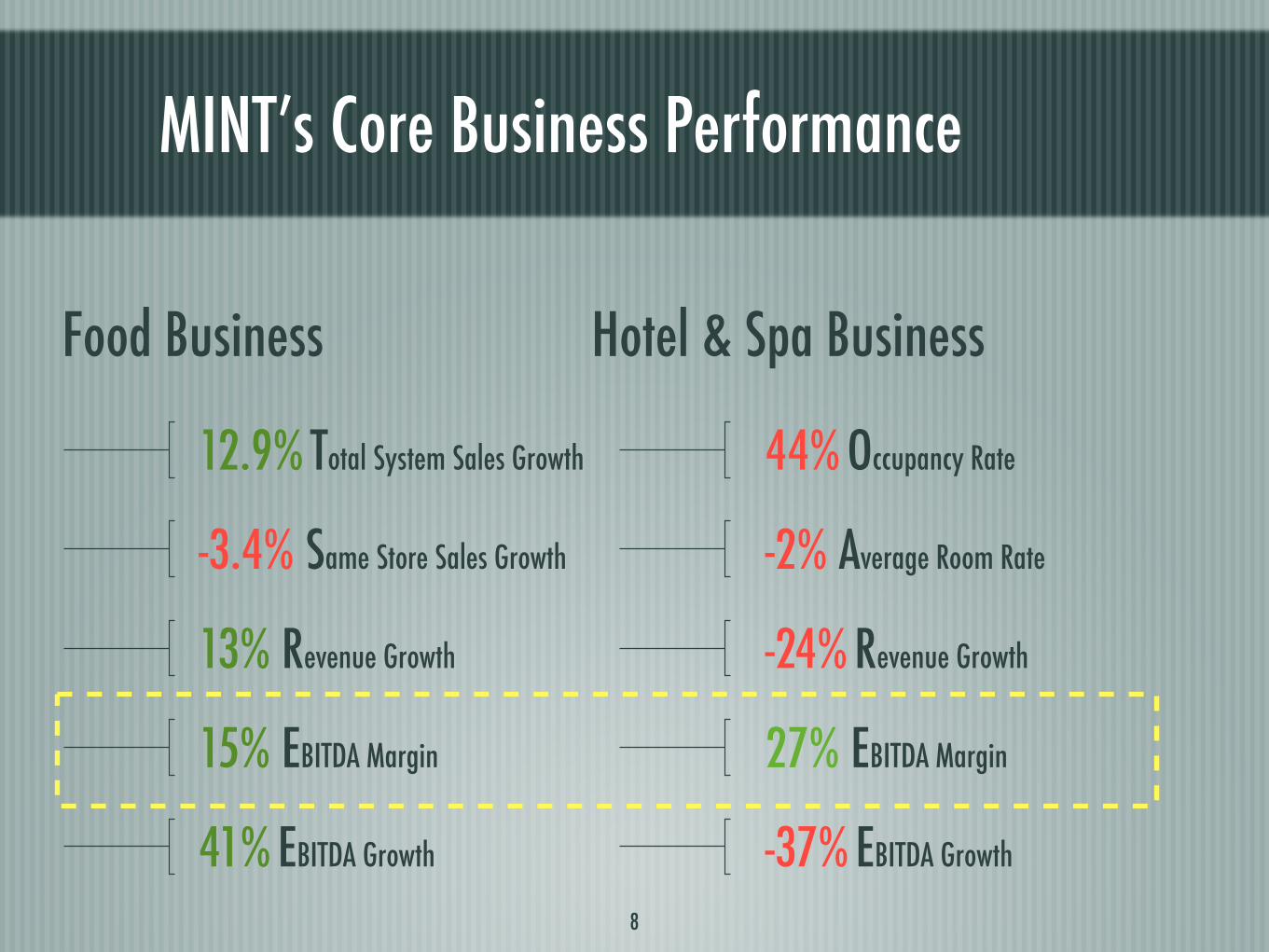

MINT’s Core Business Performance

12.9% Total System Sales Growth

-3.4% Same Store Sales Growth

13% Revenue Growth

15% EBITDA Margin

41% EBITDA Growth

8

Food Business

44% Occupancy Rate

-2% Average Room Rate

-24% Revenue Growth

27% EBITDA Margin

-37% EBITDA Growth

Hotel & Spa Business

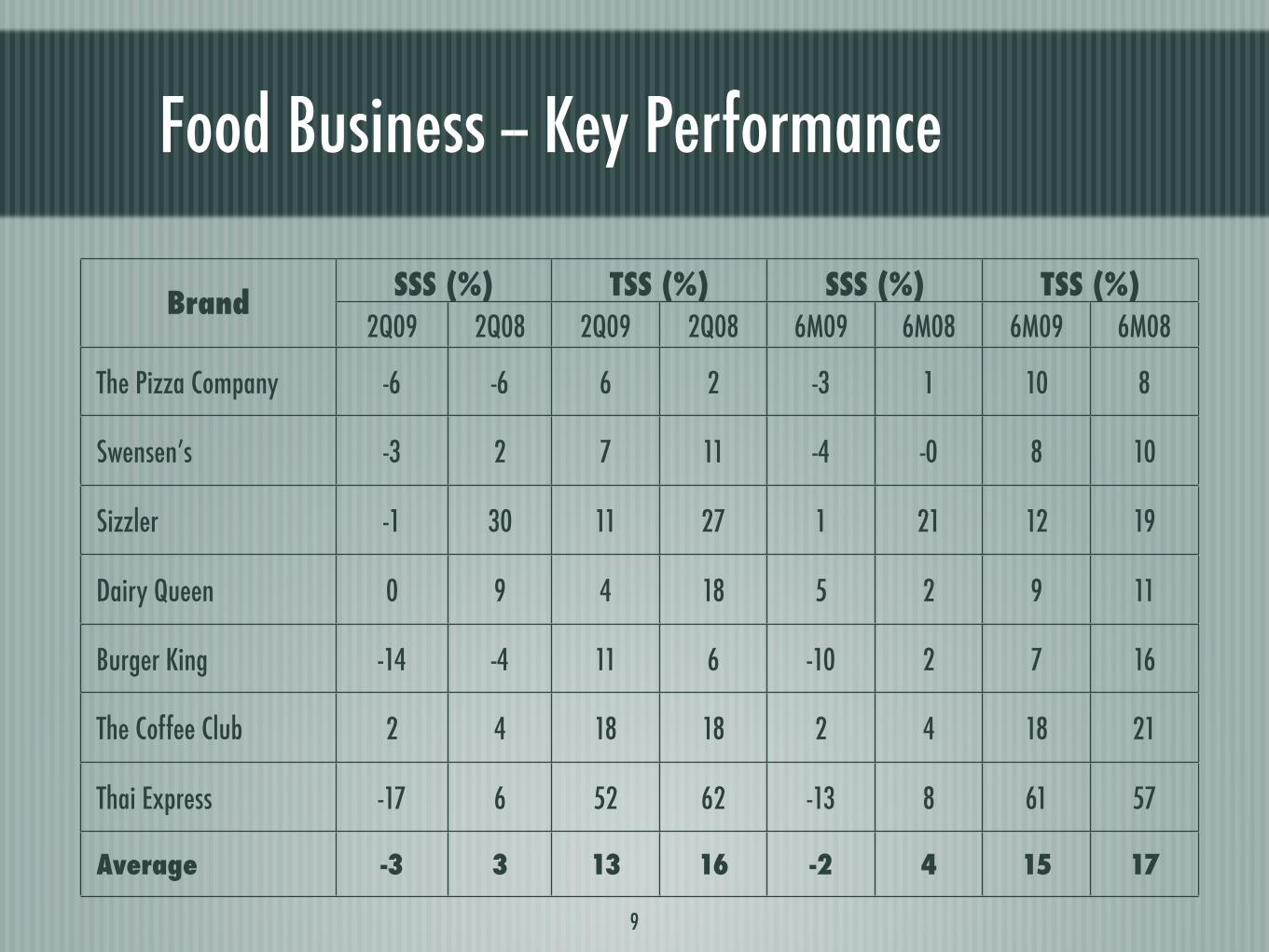

Food Business -- Key Performance

9

BrandSSS (%) TSS (%) SSS (%) TSS (%)

2Q09 2Q08 2Q09 2Q08 6M09 6M08 6M09 6M08

The Pizza Company -6 -6 6 2 -3 1 10 8

Swensen’s -3 2 7 11 -4 -0 8 10

Sizzler -1 30 11 27 1 21 12 19

Dairy Queen 0 9 4 18 5 2 9 11

Burger King -14 -4 11 6 -10 2 7 16

The Coffee Club 2 4 18 18 2 4 18 21

Thai Express -17 6 52 62 -13 8 61 57

Average -3 3 13 16 -2 4 15 17

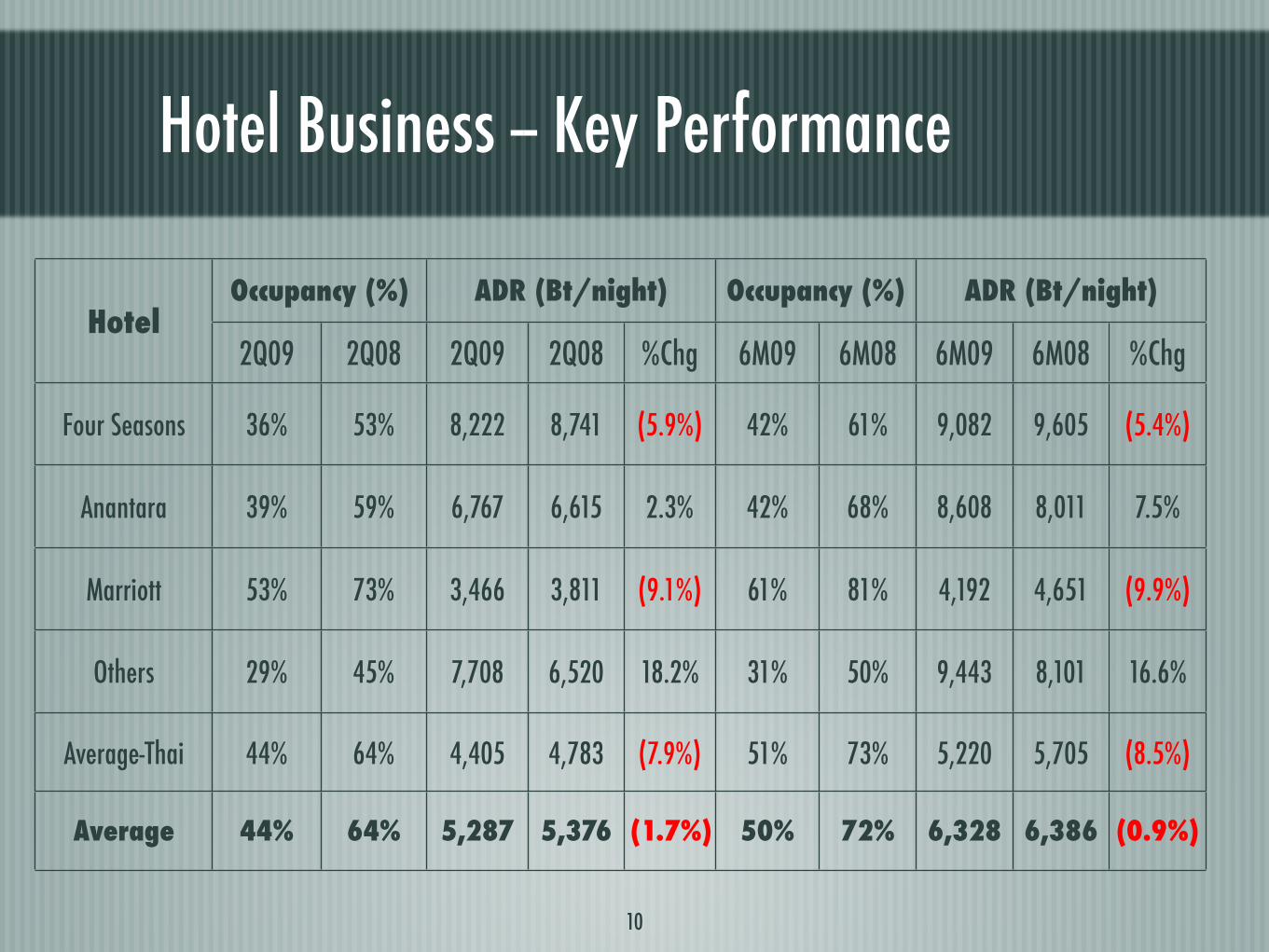

Hotel Business -- Key Performance

10

HotelOccupancy (%) ADR (Bt/night) Occupancy (%) ADR (Bt/night)

2Q09 2Q08 2Q09 2Q08 %Chg 6M09 6M08 6M09 6M08 %Chg

Four Seasons 36% 53% 8,222 8,741 (5.9%) 42% 61% 9,082 9,605 (5.4%)

Anantara 39% 59% 6,767 6,615 2.3% 42% 68% 8,608 8,011 7.5%

Marriott 53% 73% 3,466 3,811 (9.1%) 61% 81% 4,192 4,651 (9.9%)

Others 29% 45% 7,708 6,520 18.2% 31% 50% 9,443 8,101 16.6%

Average-Thai 44% 64% 4,405 4,783 (7.9%) 51% 73% 5,220 5,705 (8.5%)

Average 44% 64% 5,287 5,376 (1.7%) 50% 72% 6,328 6,386 (0.9%)

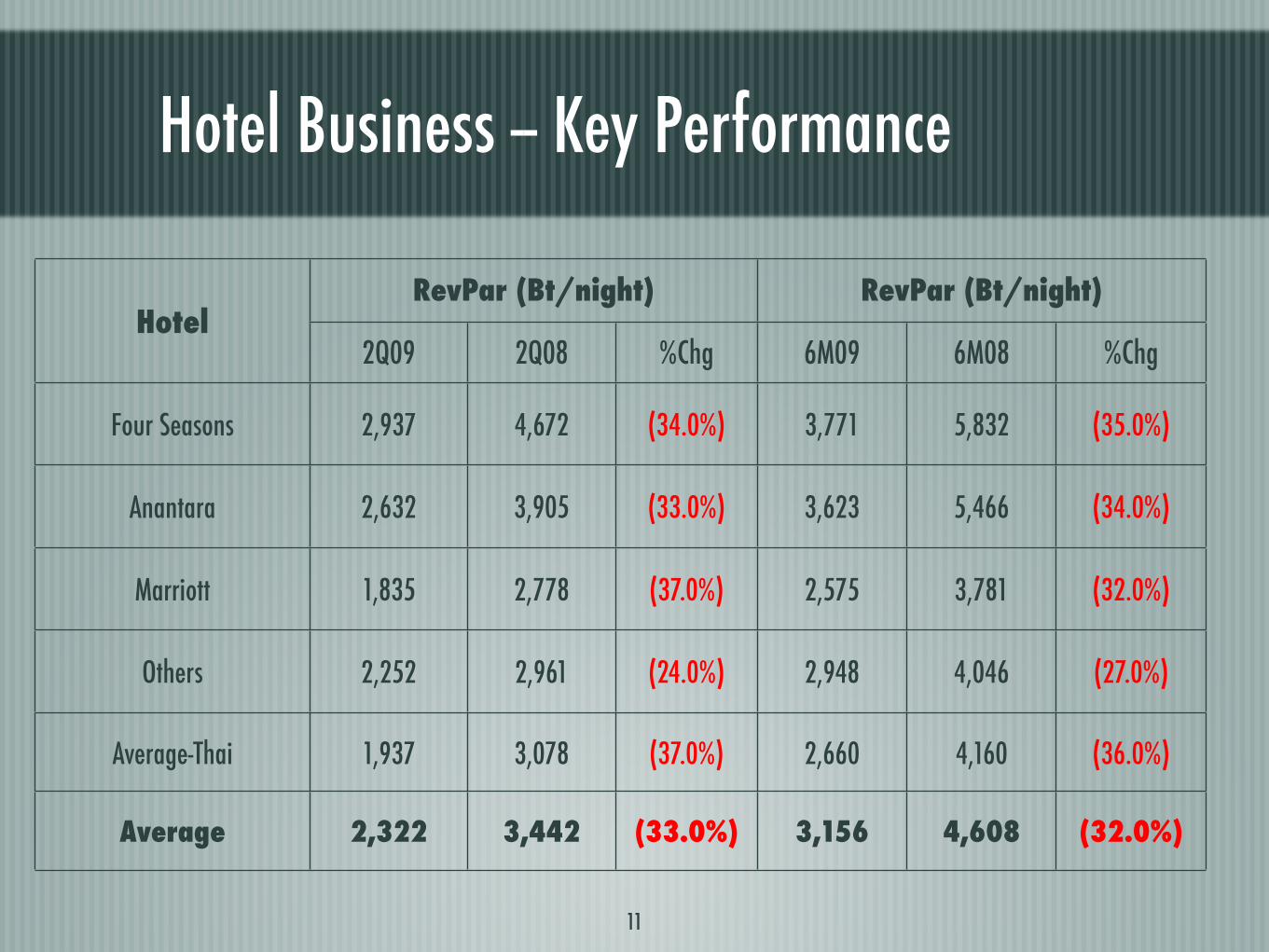

Hotel Business -- Key Performance

11

HotelRevPar (Bt/night) RevPar (Bt/night)

2Q09 2Q08 %Chg 6M09 6M08 %Chg

Four Seasons 2,937 4,672 (34.0%) 3,771 5,832 (35.0%)

Anantara 2,632 3,905 (33.0%) 3,623 5,466 (34.0%)

Marriott 1,835 2,778 (37.0%) 2,575 3,781 (32.0%)

Others 2,252 2,961 (24.0%) 2,948 4,046 (27.0%)

Average-Thai 1,937 3,078 (37.0%) 2,660 4,160 (36.0%)

Average 2,322 3,442 (33.0%) 3,156 4,608 (32.0%)

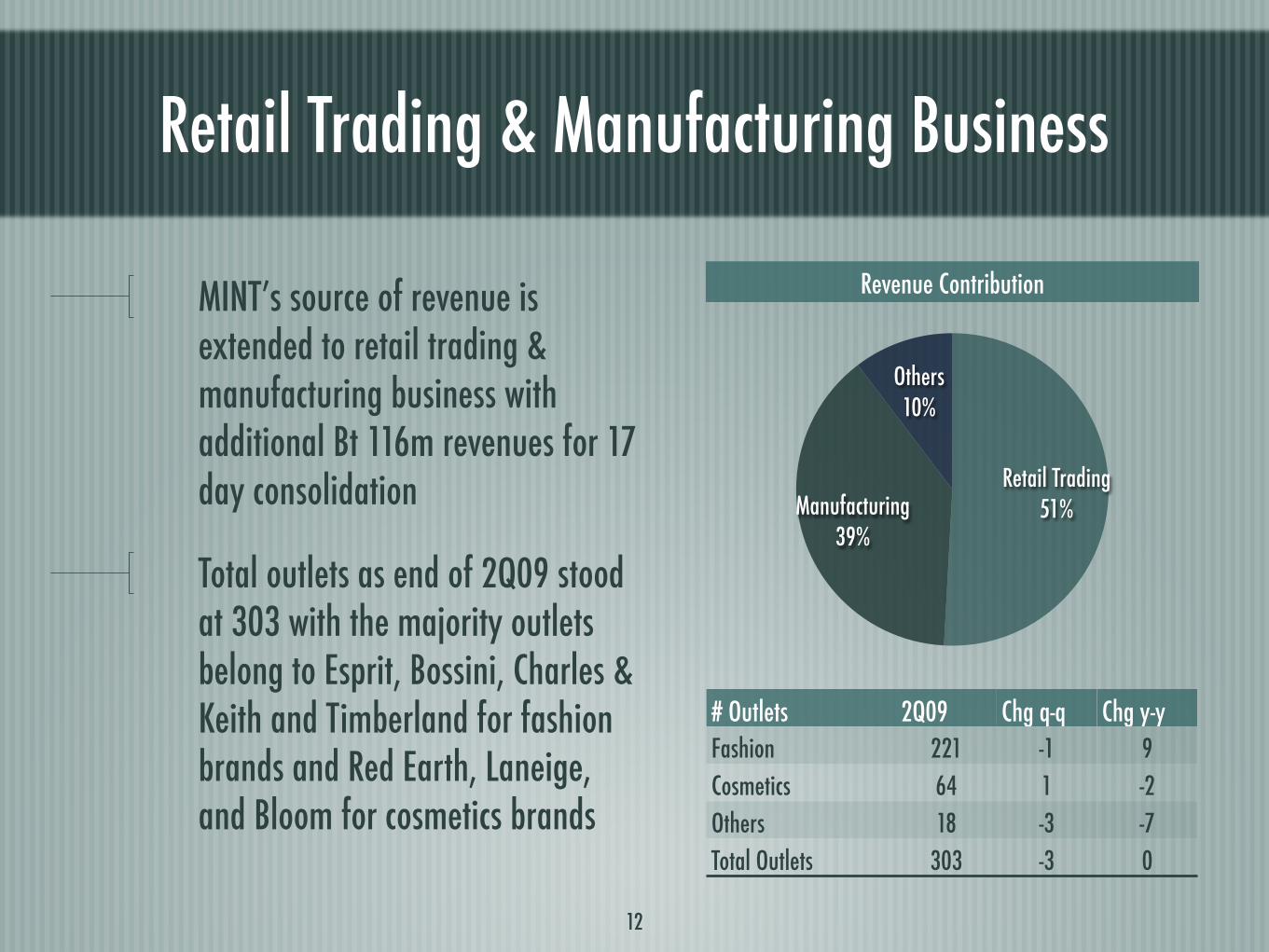

Retail Trading & Manufacturing Business

12

Others10%

Manufacturing39%

Retail Trading51%

# Outlets 2Q09 Chg q-q Chg y-y

Fashion 221 -1 9

Cosmetics 64 1 -2

Others 18 -3 -7

Total Outlets 303 -3 0

MINT’s source of revenue is extended to retail trading & manufacturing business with additional Bt 116m revenues for 17 day consolidation

Total outlets as end of 2Q09 stood at 303 with the majority outlets belong to Esprit, Bossini, Charles & Keith and Timberland for fashion brands and Red Earth, Laneige, and Bloom for cosmetics brands

Revenue Contribution

II. 2Q09 Financial Results

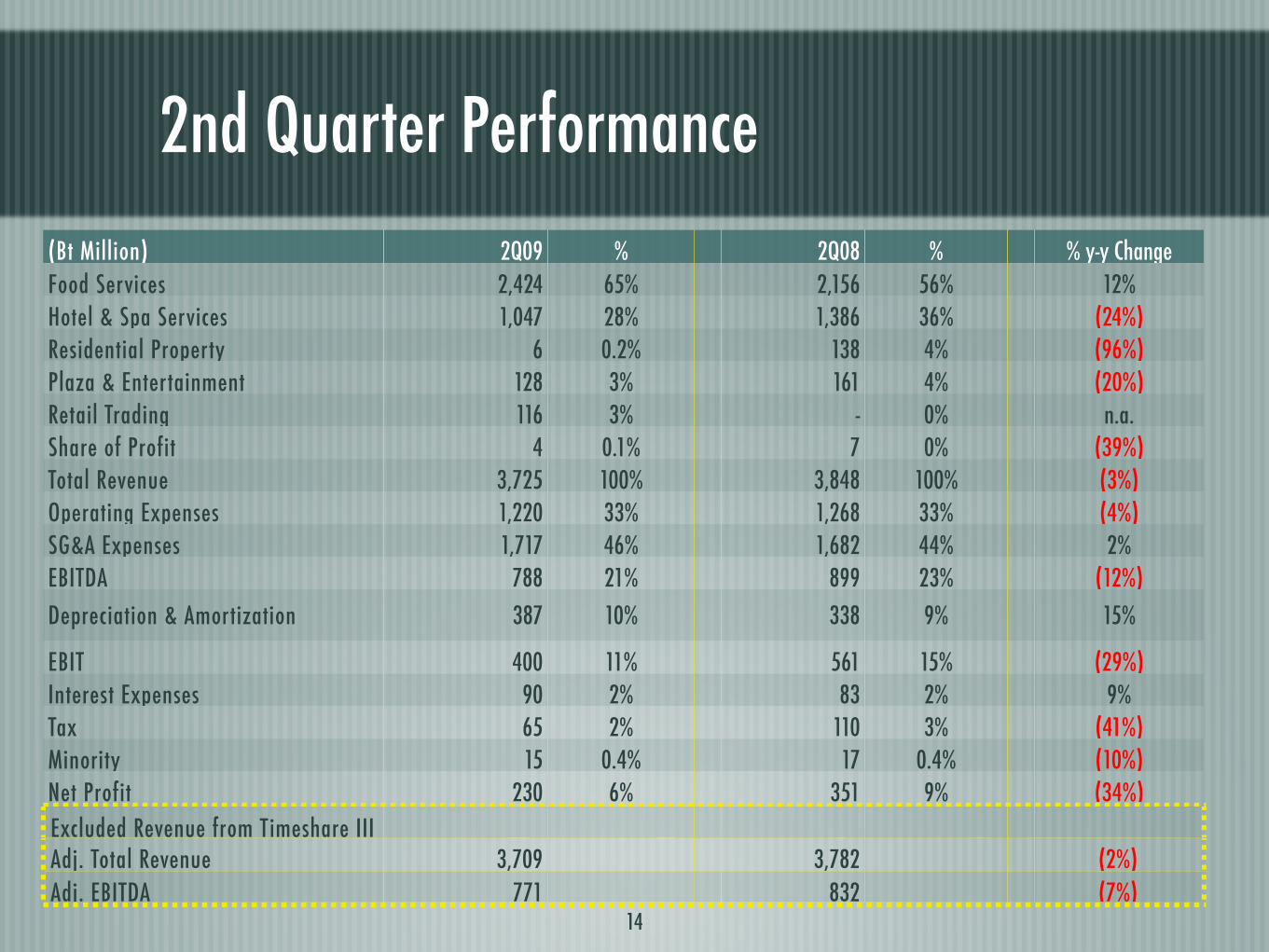

2nd Quarter Performance

14

(Bt Million) 2Q09 % 2Q08 % % y-y Change

Food Services 2,424 65% 2,156 56% 12%Hotel & Spa Services 1,047 28% 1,386 36% (24%)Residential Property 6 0.2% 138 4% (96%)Plaza & Entertainment 128 3% 161 4% (20%)Retail Trading 116 3% - 0% n.a.Share of Profit 4 0.1% 7 0% (39%)Total Revenue 3,725 100% 3,848 100% (3%)Operating Expenses 1,220 33% 1,268 33% (4%)SG&A Expenses 1,717 46% 1,682 44% 2%EBITDA 788 21% 899 23% (12%)

Depreciation & Amortization 387 10% 338 9% 15%

EBIT 400 11% 561 15% (29%)Interest Expenses 90 2% 83 2% 9%Tax 65 2% 110 3% (41%)Minority 15 0.4% 17 0.4% (10%)Net Profit 230 6% 351 9% (34%)

Excluded Revenue from Timeshare IIIAdj. Total Revenue 3,709 3,782 (2%)

Adj. EBITDA 771 832 (7%)

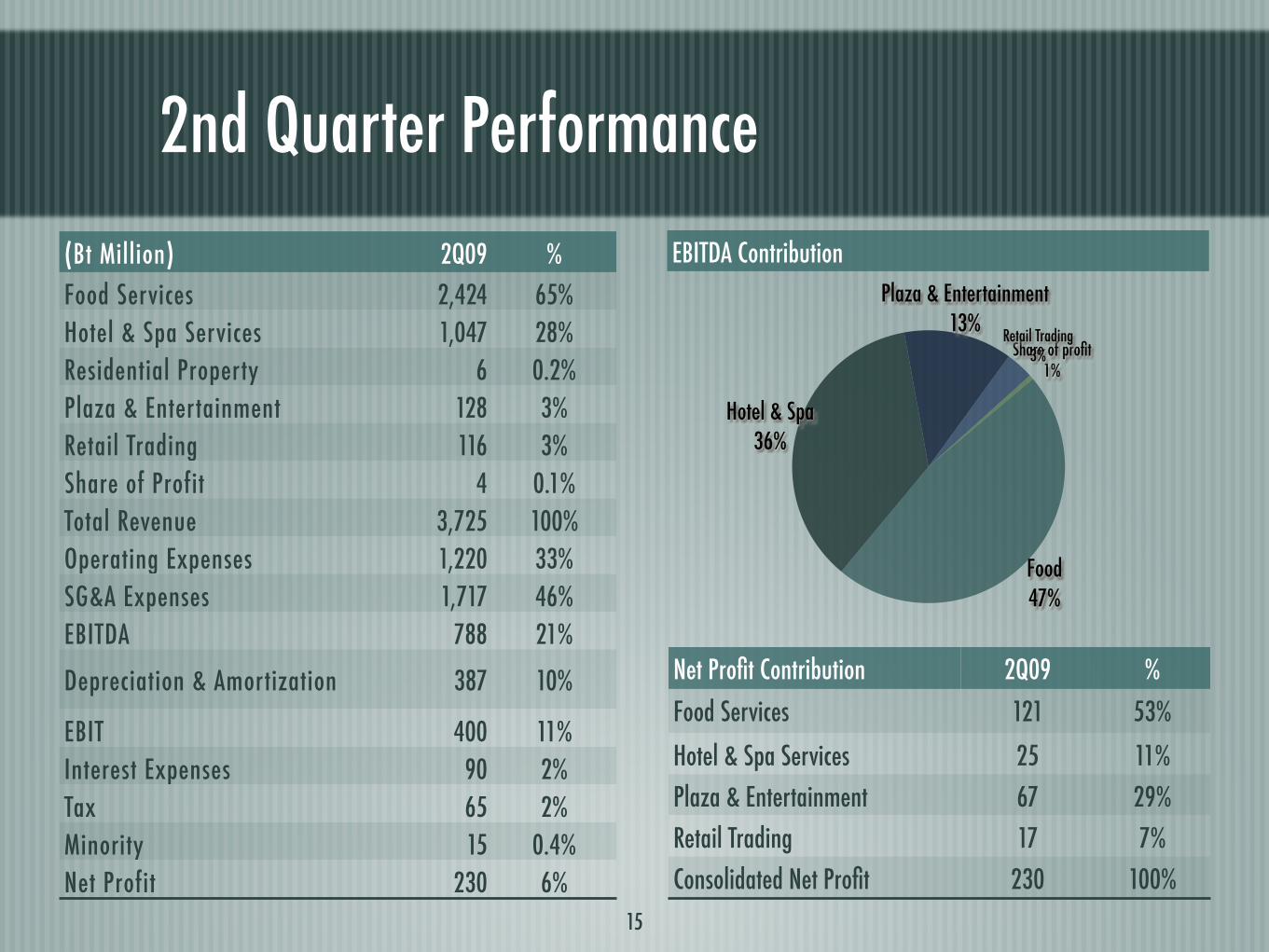

2nd Quarter Performance

15

(Bt Million) 2Q09 %

Food Services 2,424 65%

Hotel & Spa Services 1,047 28%

Residential Property 6 0.2%

Plaza & Entertainment 128 3%

Retail Trading 116 3%

Share of Profit 4 0.1%

Total Revenue 3,725 100%

Operating Expenses 1,220 33%

SG&A Expenses 1,717 46%

EBITDA 788 21%

Depreciation & Amortization 387 10%

EBIT 400 11%

Interest Expenses 90 2%

Tax 65 2%

Minority 15 0.4%

Net Profit 230 6%

Share of profit1%

Retail Trading3%

Plaza & Entertainment13%

Hotel & Spa36%

Food 47%

Net Profit Contribution 2Q09 %

Food Services 121 53%

Hotel & Spa Services 25 11%

Plaza & Entertainment 67 29%

Retail Trading 17 7%

Consolidated Net Profit 230 100%

EBITDA Contribution

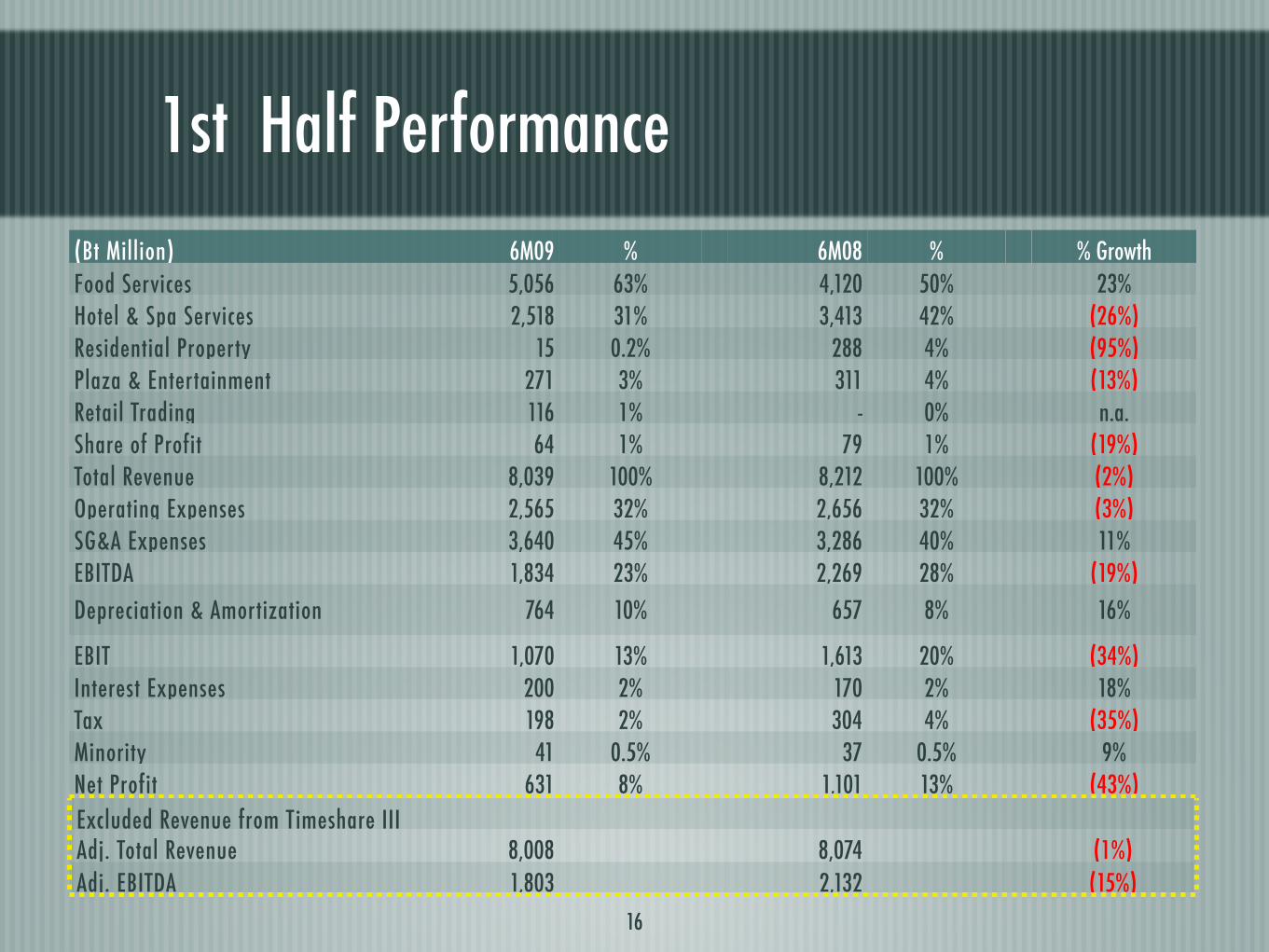

1st Half Performance

16

(Bt Million) 6M09 % 6M08 % % GrowthFood Services 5,056 63% 4,120 50% 23%Hotel & Spa Services 2,518 31% 3,413 42% (26%)Residential Property 15 0.2% 288 4% (95%)Plaza & Entertainment 271 3% 311 4% (13%)Retail Trading 116 1% - 0% n.a.Share of Profit 64 1% 79 1% (19%)Total Revenue 8,039 100% 8,212 100% (2%)Operating Expenses 2,565 32% 2,656 32% (3%)SG&A Expenses 3,640 45% 3,286 40% 11%EBITDA 1,834 23% 2,269 28% (19%)

Depreciation & Amortization 764 10% 657 8% 16%

EBIT 1,070 13% 1,613 20% (34%)Interest Expenses 200 2% 170 2% 18%Tax 198 2% 304 4% (35%)Minority 41 0.5% 37 0.5% 9%Net Profit 631 8% 1,101 13% (43%)

Excluded Revenue from Timeshare IIIAdj. Total Revenue 8,008 8,074 (1%)Adj. EBITDA 1,803 2,132 (15%)

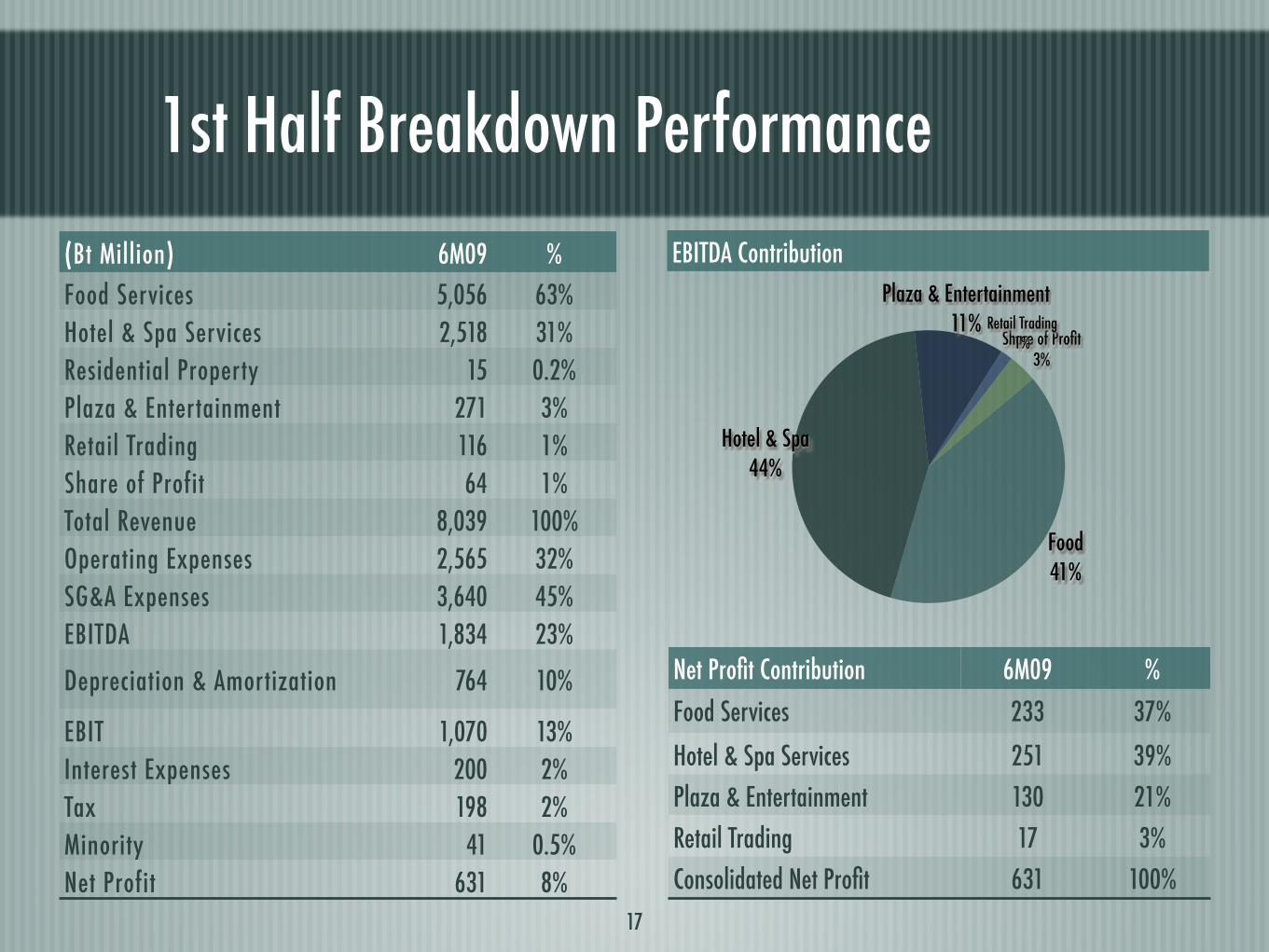

1st Half Breakdown Performance

17

(Bt Million) 6M09 %

Food Services 5,056 63%

Hotel & Spa Services 2,518 31%

Residential Property 15 0.2%

Plaza & Entertainment 271 3%

Retail Trading 116 1%

Share of Profit 64 1%

Total Revenue 8,039 100%

Operating Expenses 2,565 32%

SG&A Expenses 3,640 45%

EBITDA 1,834 23%

Depreciation & Amortization 764 10%

EBIT 1,070 13%

Interest Expenses 200 2%

Tax 198 2%

Minority 41 0.5%

Net Profit 631 8%

Share of Profit3%

Retail Trading1%

Plaza & Entertainment11%

Hotel & Spa44%

Food 41%

Net Profit Contribution 6M09 %

Food Services 233 37%

Hotel & Spa Services 251 39%

Plaza & Entertainment 130 21%

Retail Trading 17 3%

Consolidated Net Profit 631 100%

EBITDA Contribution

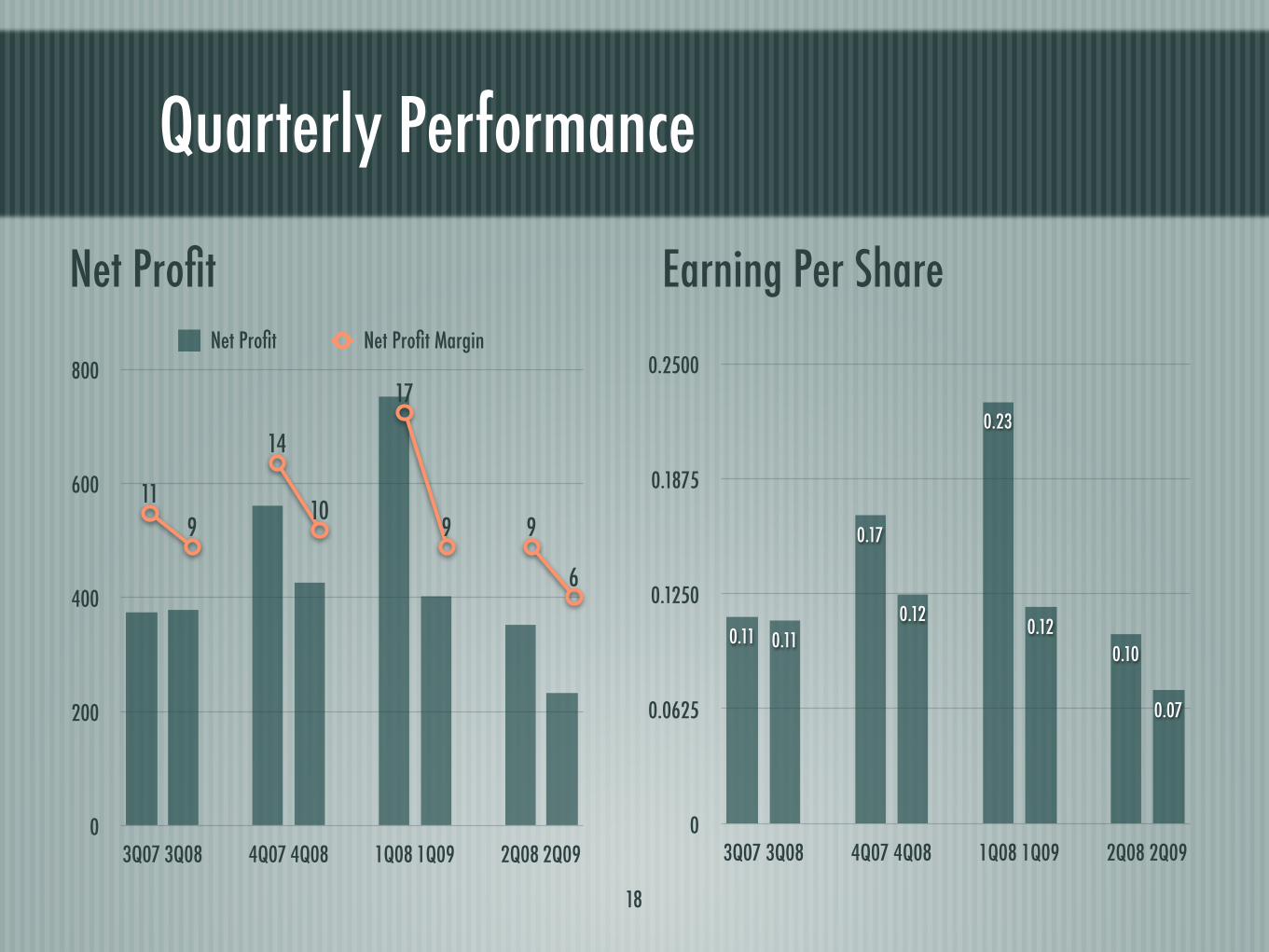

0

200

400

600

800

3Q07 3Q08 4Q07 4Q08 1Q08 1Q09 2Q08 2Q09

Net Profit

11

9

14

10

17

9 9

6

Net Profit Margin

0

0.0625

0.1250

0.1875

0.2500

3Q07 3Q08 4Q07 4Q08 1Q08 1Q09 2Q08 2Q09

0.07

0.10

0.12

0.23

0.12

0.17

0.110.11

18

Net Profit Earning Per Share

Quarterly Performance

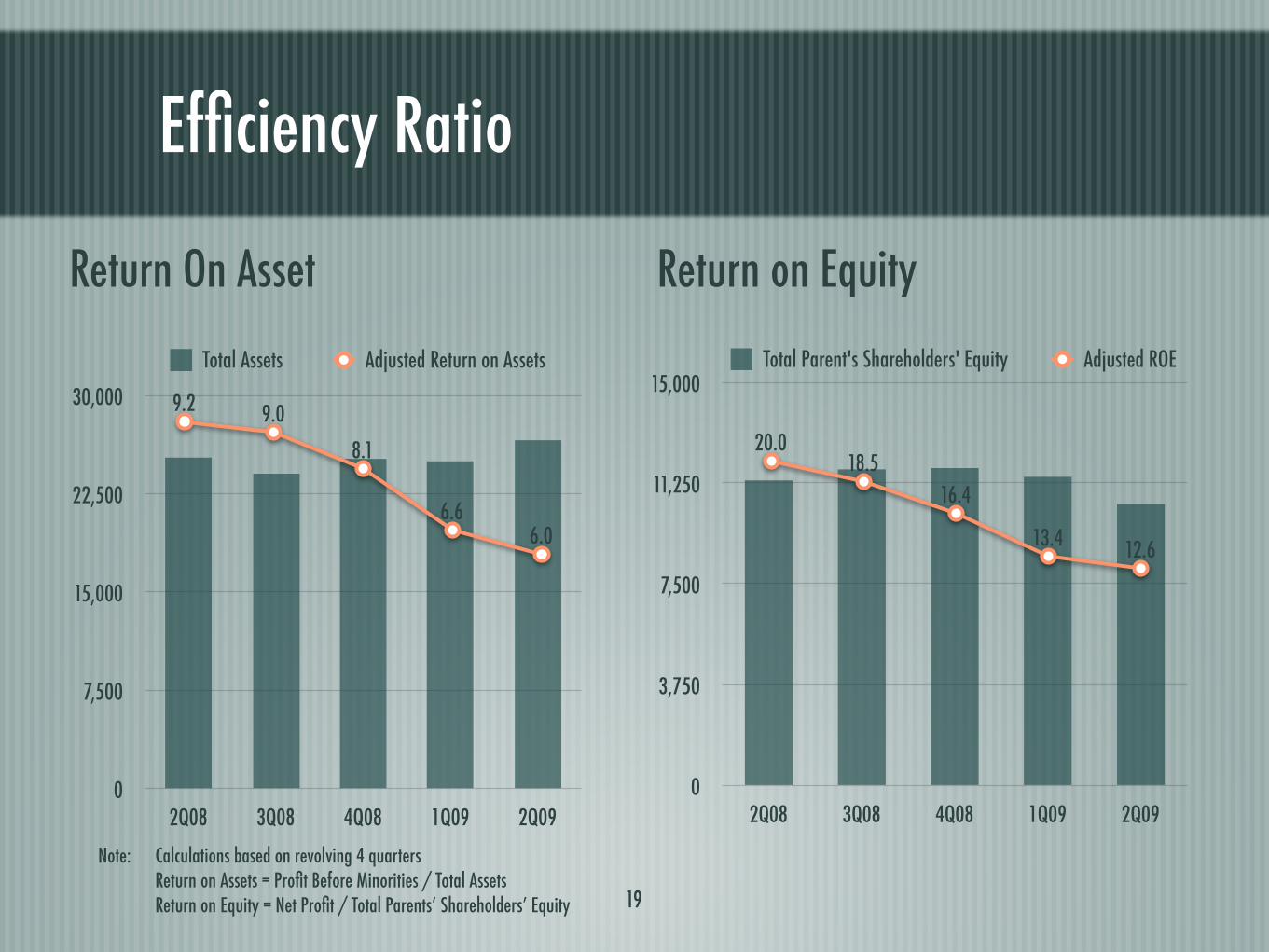

19

Return On Asset Return on Equity

0

7,500

15,000

22,500

30,000

2Q08 3Q08 4Q08 1Q09 2Q09

Total Assets

0

3,750

7,500

11,250

15,000

2Q08 3Q08 4Q08 1Q09 2Q09

Total Parent's Shareholders' Equity

Note:! Calculations based on revolving 4 quarters ! Return on Assets = Profit Before Minorities / Total Assets Return on Equity = Net Profit / Total Parents’ Shareholders’ Equity

9.2 9.0

8.1

6.66.0

Adjusted Return on Assets

20.018.5

16.4

13.4 12.6

Adjusted ROE

Efficiency Ratio

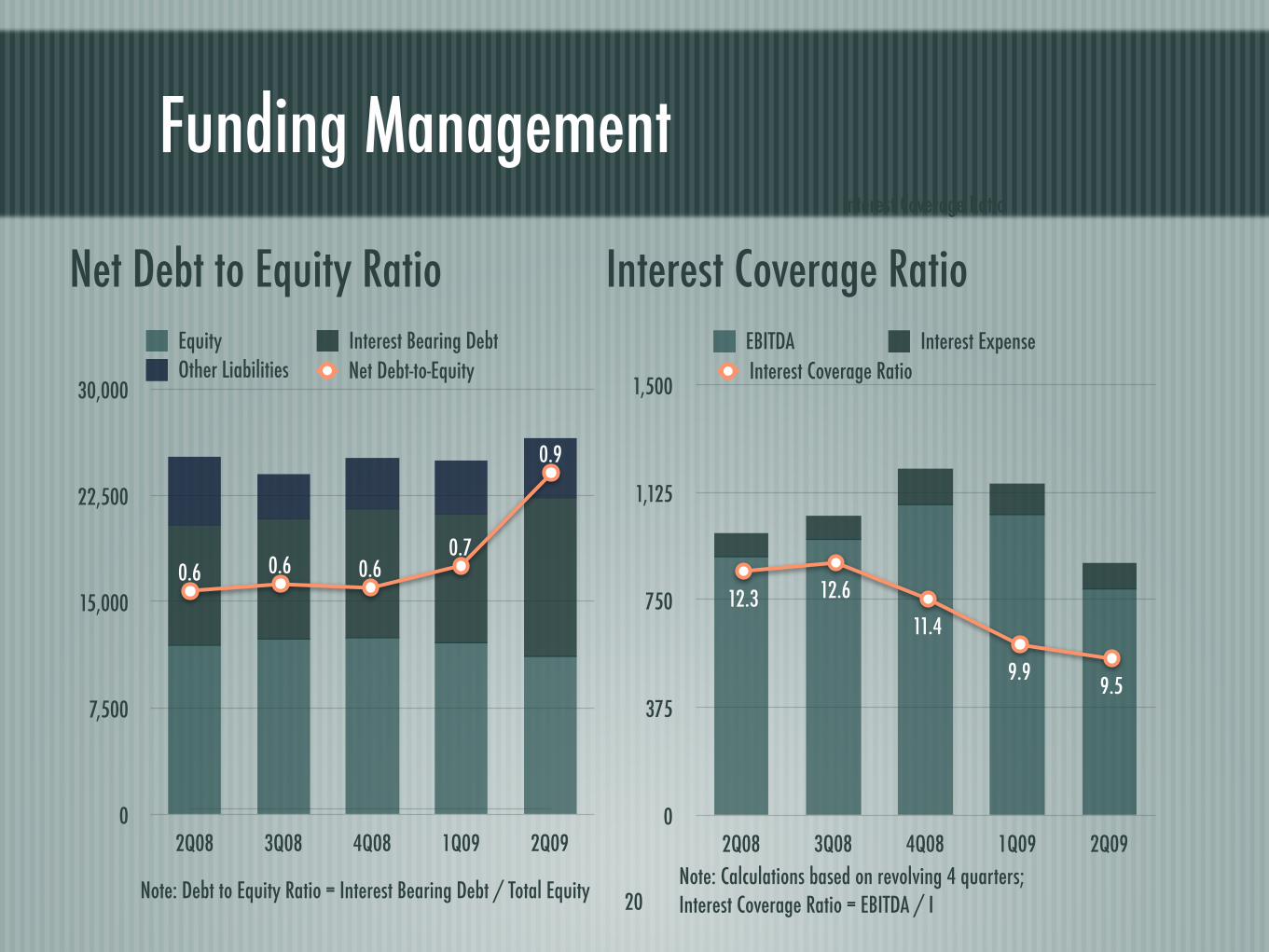

Funding Management

0

7,500

15,000

22,500

30,000

2Q08 3Q08 4Q08 1Q09 2Q09

0.6 0.6 0.60.7

0.9

Net Debt-to-Equity

Note: Debt to Equity Ratio = Interest Bearing Debt / Total Equity

Equity Interest Bearing DebtOther Liabilities

20

0

375

750

1,125

1,500

2Q08 3Q08 4Q08 1Q09 2Q09

EBITDA Interest Expense

Note: Calculations based on revolving 4 quarters; Interest Coverage Ratio = EBITDA / I

12.3 12.6

11.4

9.99.5

Interest Coverage Ratio

Interest Coverage Ratio

Net Debt to Equity Ratio Interest Coverage Ratio

III. Key Strategic & Industry Update (Food & Hotel Business)

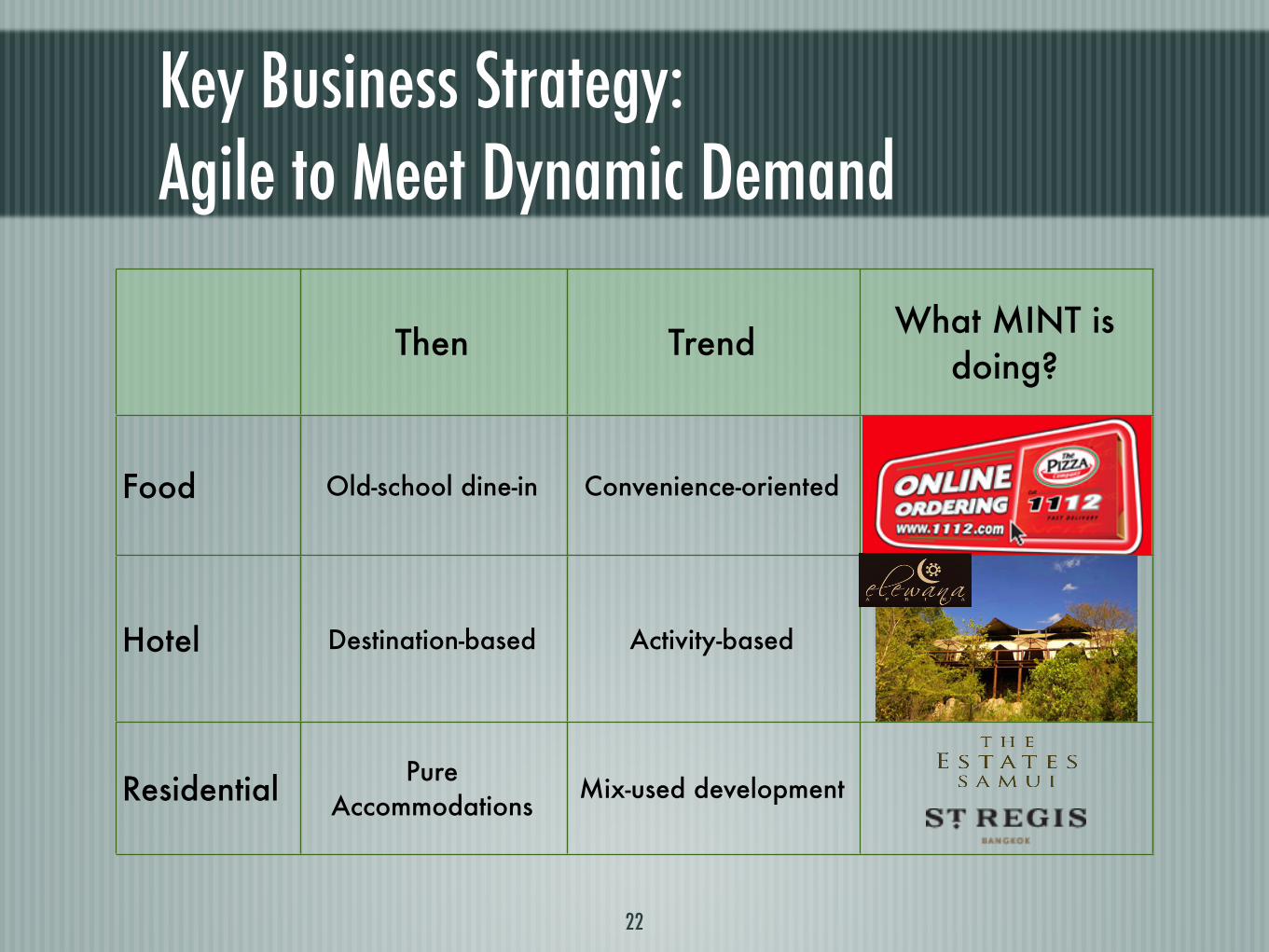

Key Business Strategy: Agile to Meet Dynamic Demand

22

Then TrendWhat MINT is

doing?

Food Old-school dine-in Convenience-oriented

Hotel Destination-based Activity-based

ResidentialPure

AccommodationsMix-used development

Food Service Industry

Food Business Trends

24

Growing health & wellness food segment

Consumers driven by convenient channel

Premium food concept/variety

Flavors added by international travelers demand

Demand for day parts (Breakfast/snacks)

MINT Food Marketing Strategy

25

Increasing Penetration

Growing with Modern Trade

Aggressive Value Promotion Office Building

! Number of dockets of MINT’s all Thai food brands increased 4% in 1H09

Household

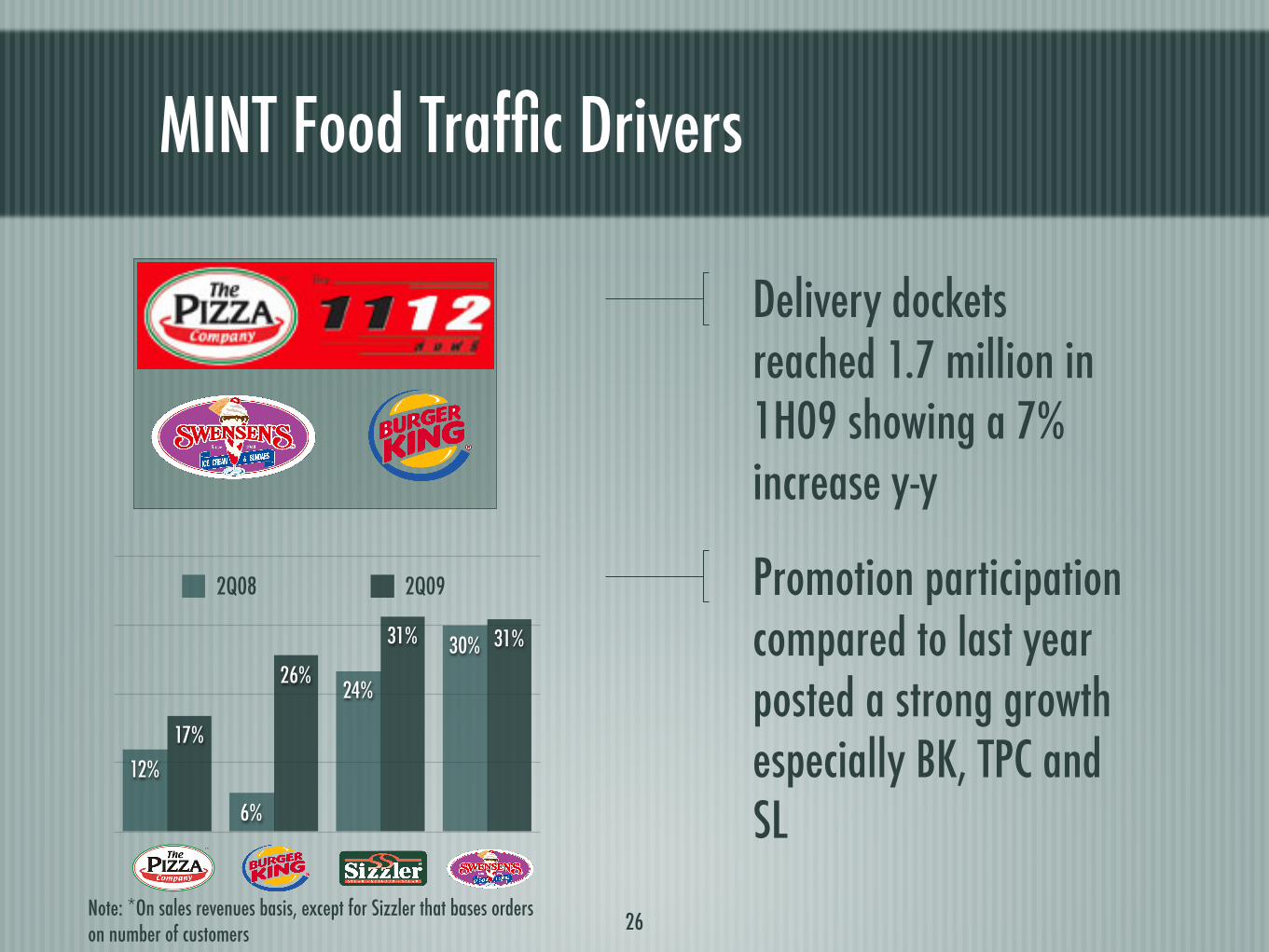

MINT Food Traffic Drivers

Delivery dockets reached 1.7 million in 1H09 showing a 7% increase y-y

Promotion participation compared to last year posted a strong growth especially BK, TPC and SL

26Note: *On sales revenues basis, except for Sizzler that bases orders on number of customers

TPC BK SL SW

31%31%

26%

17%

30%

24%

6%

12%

2Q08 2Q09

Tourism & Hotel Industry

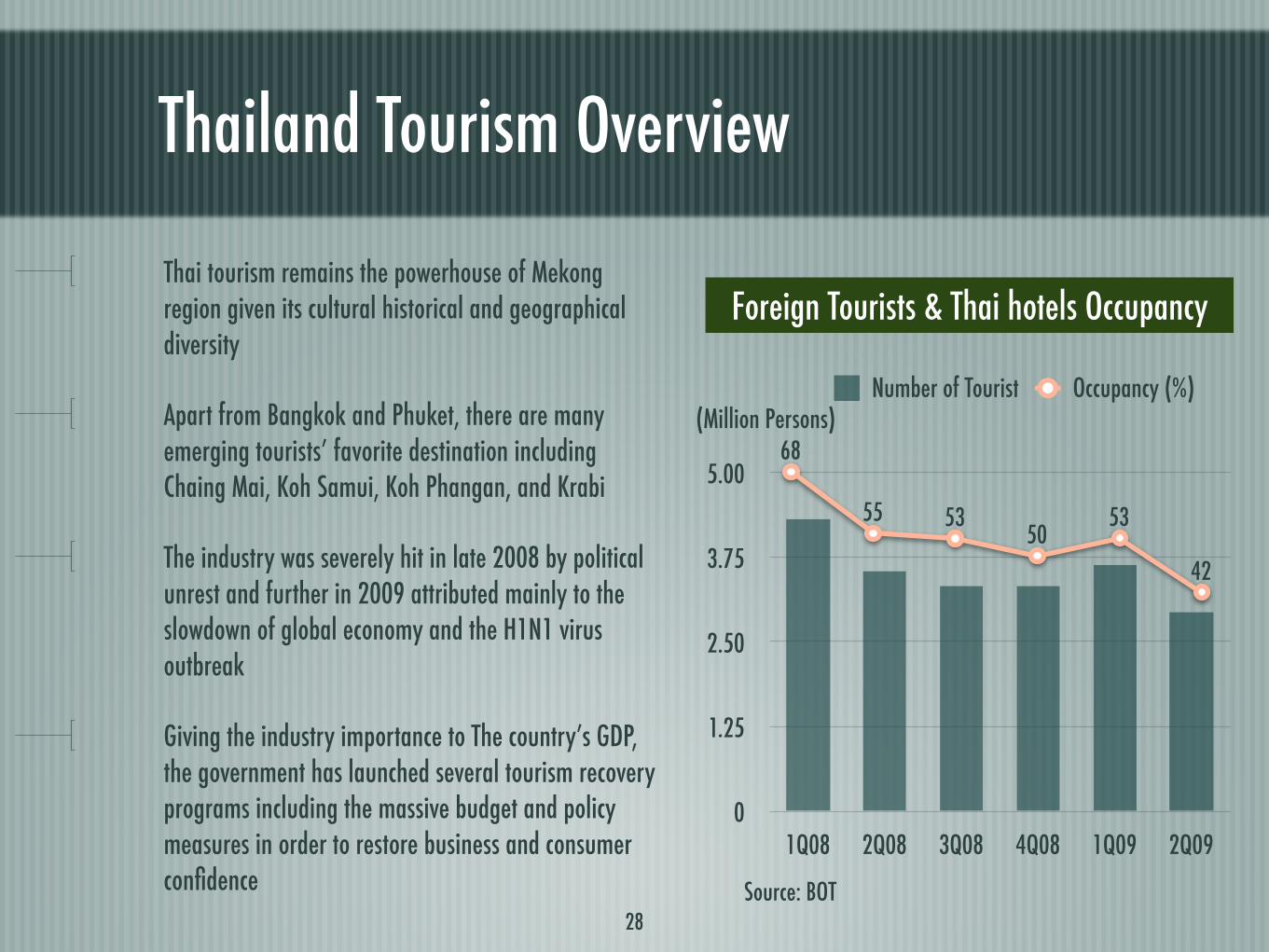

Thailand Tourism Overview

28

Thai tourism remains the powerhouse of Mekong region given its cultural historical and geographical diversity

Apart from Bangkok and Phuket, there are many emerging tourists’ favorite destination including Chaing Mai, Koh Samui, Koh Phangan, and Krabi

The industry was severely hit in late 2008 by political unrest and further in 2009 attributed mainly to the slowdown of global economy and the H1N1 virus outbreak

Giving the industry importance to The country’s GDP, the government has launched several tourism recovery programs including the massive budget and policy measures in order to restore business and consumer confidence

0

1.25

2.50

3.75

5.00

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09

Number of Tourist

68

55 5350

53

42

Occupancy (%)(Million Persons)

Foreign Tourists & Thai hotels Occupancy

Source: BOT

Resiliency of Thailand’s Tourism Industry

C h a l l e n g e s Favorable Outlook

Global economic crises in major economies; US, UK, etc.

Emerging markets with high purchasing power; China, India, Russia, etc.

Competition from neighboring countriesDual destinations, given Thailand’s

preferred destination for leisure

Fluctuating energy prices Expansion of low-cost carriers

Domestic political tension Short-term detraction: ex. Bali

Outbreak of H1N1 fluLess dissemination with sufficient

medication & treatment

29

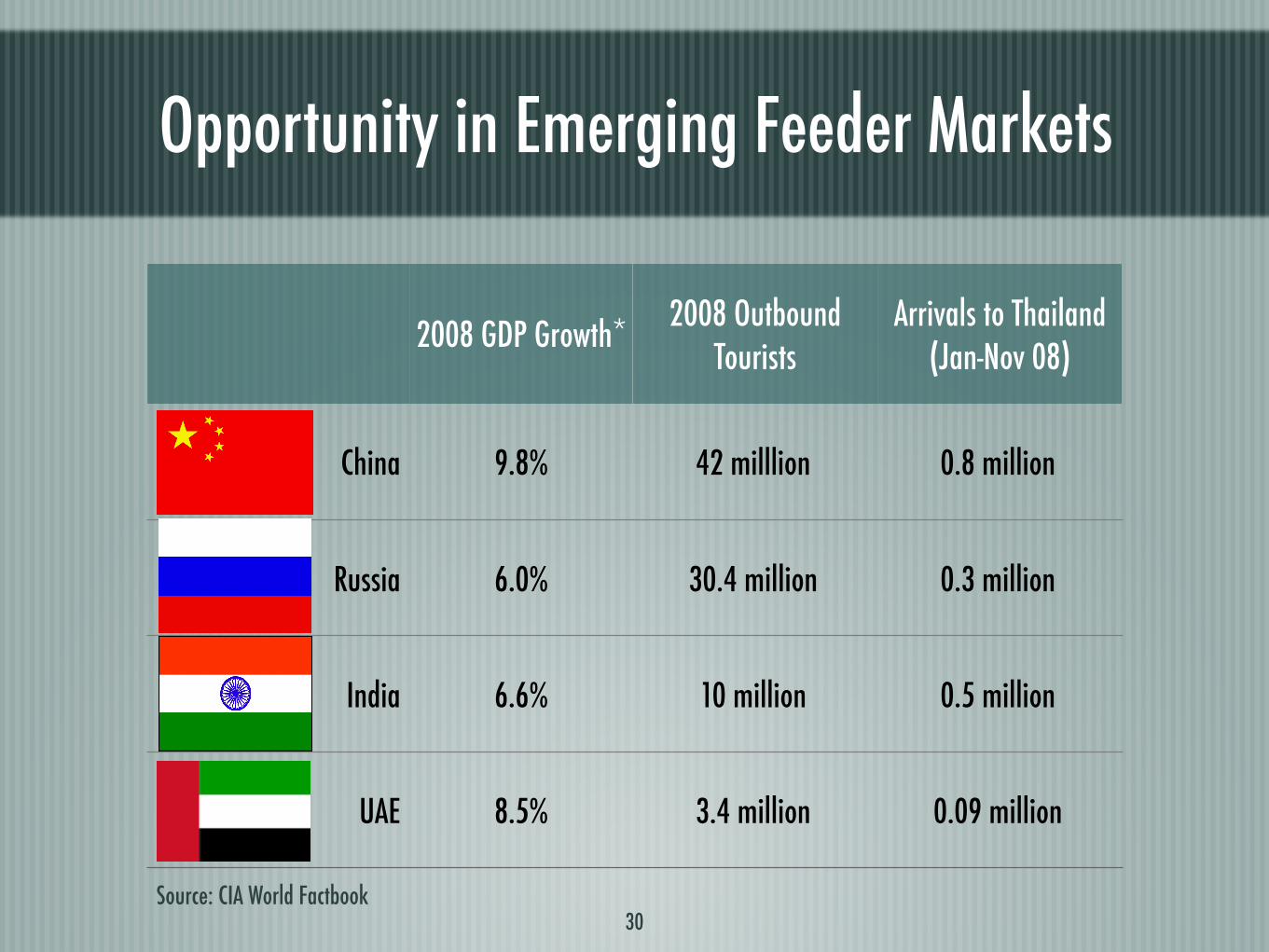

Opportunity in Emerging Feeder Markets

30

2008 GDP Growth*2008 Outbound

TouristsArrivals to Thailand

(Jan-Nov 08)

China 9.8% 42 milllion 0.8 million

Russia 6.0% 30.4 million 0.3 million

India 6.6% 10 million 0.5 million

UAE 8.5% 3.4 million 0.09 million

Source: CIA World Factbook

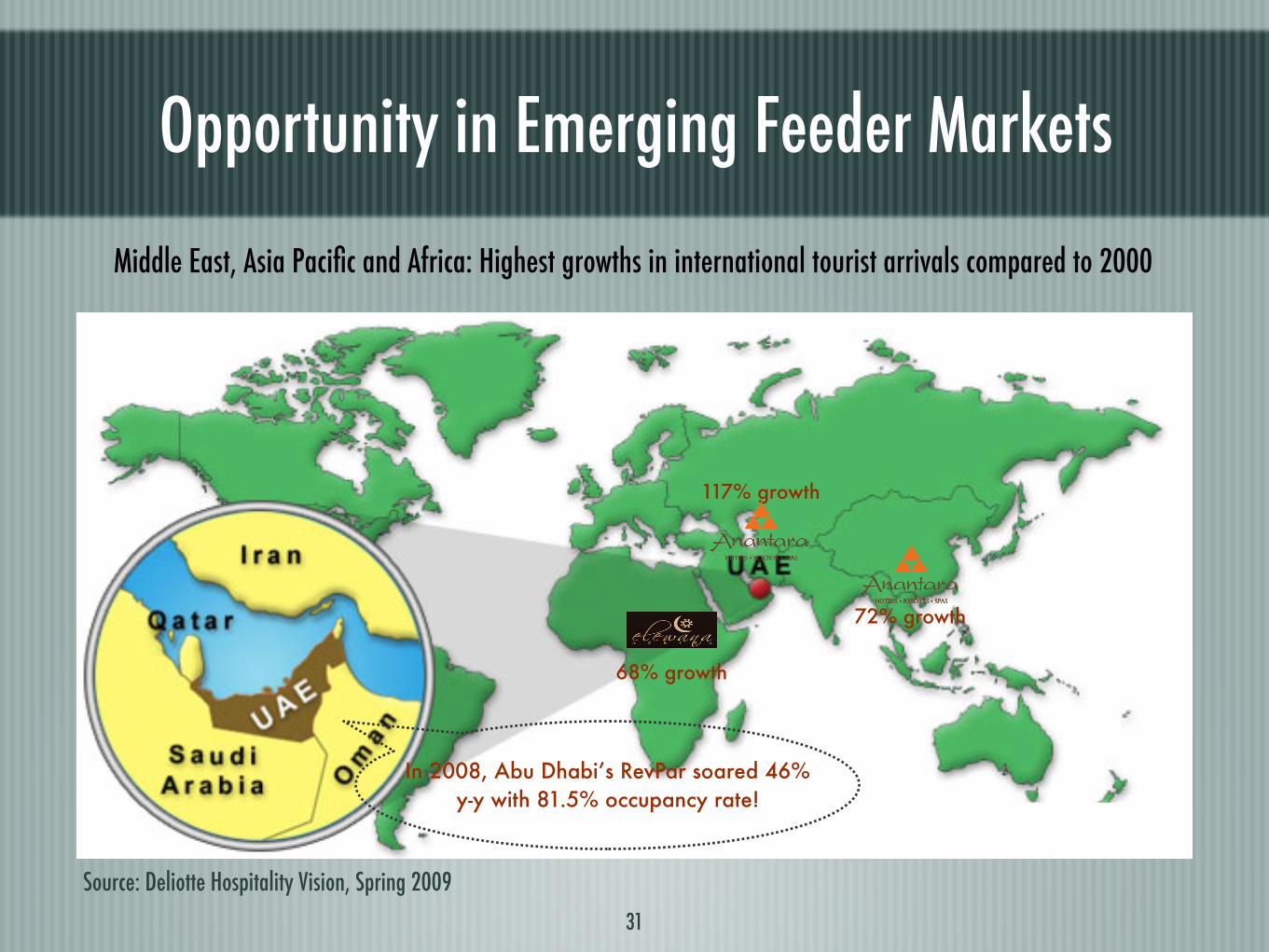

Opportunity in Emerging Feeder Markets

31

Source: Deliotte Hospitality Vision, Spring 2009

Middle East, Asia Pacific and Africa: Highest growths in international tourist arrivals compared to 2000

117% growth

68% growth

72% growth

In 2008, Abu Dhabi’s RevPar soared 46% y-y with 81.5% occupancy rate!

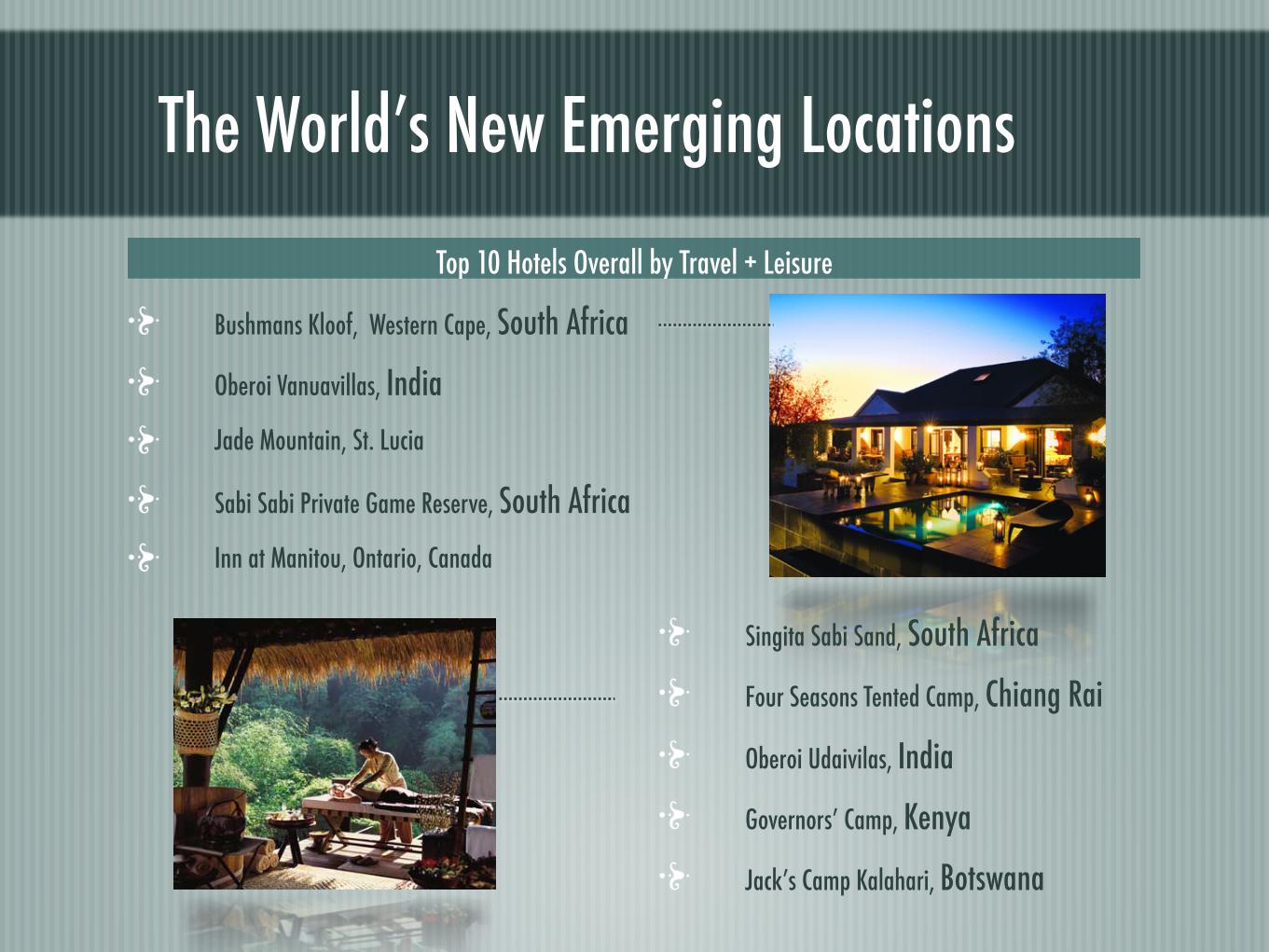

The World’s New Emerging Locations

Bushmans Kloof, Western Cape, South Africa

Oberoi Vanuavillas, India

Jade Mountain, St. Lucia

Sabi Sabi Private Game Reserve, South Africa

Inn at Manitou, Ontario, Canada

Top 10 Hotels Overall by Travel + Leisure

Singita Sabi Sand, South Africa

Four Seasons Tented Camp, Chiang Rai

Oberoi Udaivilas, India

Governors’ Camp, Kenya

Jack’s Camp Kalahari, Botswana

Opportunity for Thai Tourism

Source: UN/WTO

Type of Tourism Top Destinations

Leisure:Culture, Beach, Mountain, Shopping

Thailand, Indonesia, Maldives, China, Vietnam, Malaysia, HK

Wellness & Medical:Beauty, Healthcare, & Retirement Home

Thailand, Taiwan, Province of China, India

Business:MICE Market

Singapore, HK, China, Thailand

Gaming: Casino, Theme Park & Entertainment

Singapore, Macau, Malaysia, Australia

33

Opportunity for MINT’s Hotels

34Source: HVS Asia Pacific Hotel Watch 2009

0

150

300

450

600

Bali Langkawi Phuket Sanya Samui Maldives

Top 6 Resort Markets in Asia Pacific: 2008 RevPar

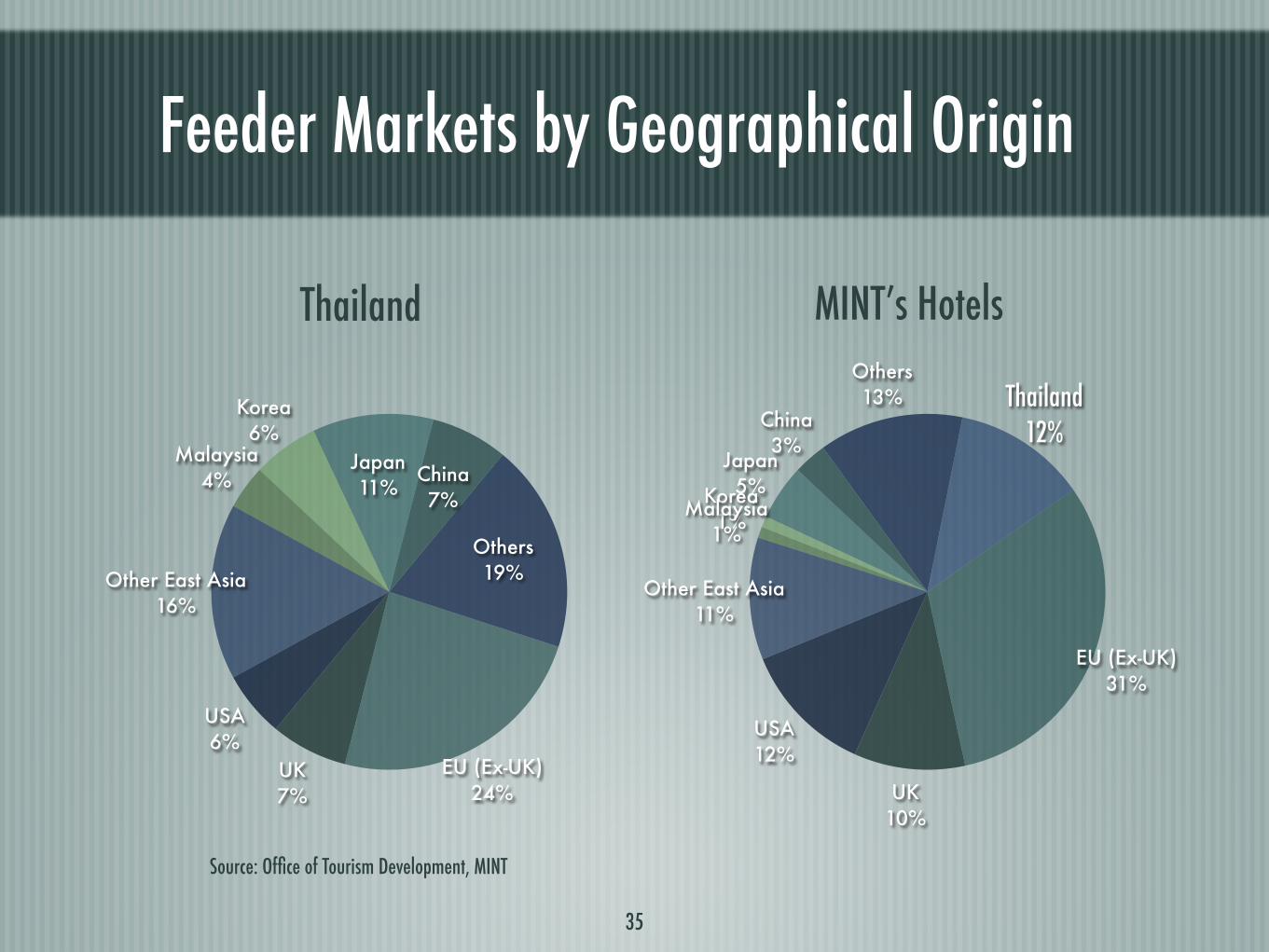

Feeder Markets by Geographical Origin

Thailand MINT’s Hotels

Others19%

China7%

Japan11%

Korea6%

Malaysia4%

Other East Asia16%

USA6%

UK7%

EU (Ex-UK)24%

Source: Office of Tourism Development, MINT

Thailand12%

Others13%

China3%

Japan5%Korea

1%Malaysia

1%

Other East Asia11%

USA12%

UK10%

EU (Ex-UK)31%

35

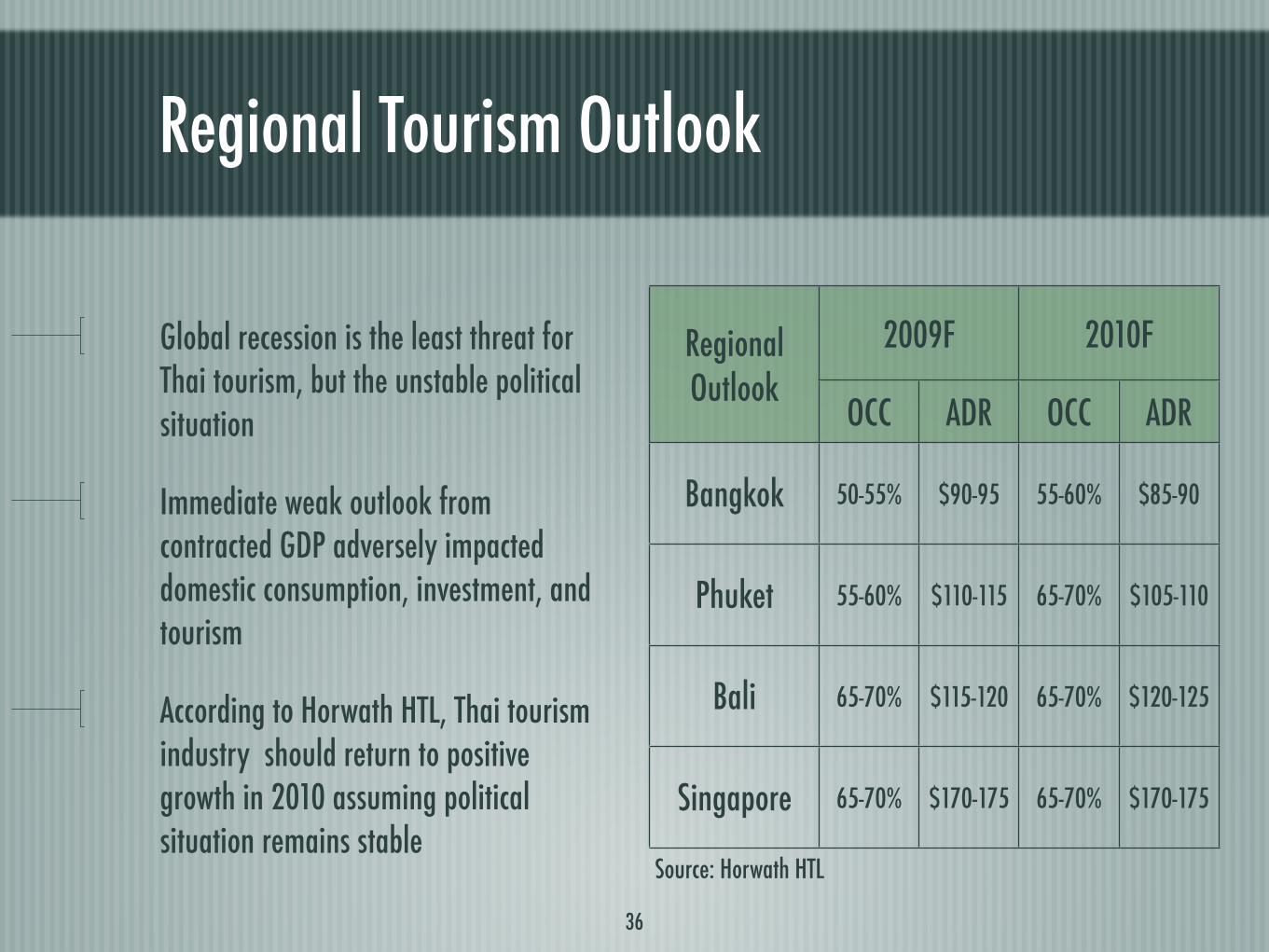

Regional Tourism Outlook

36

Global recession is the least threat for Thai tourism, but the unstable political situation

Immediate weak outlook from contracted GDP adversely impacted domestic consumption, investment, and tourism

According to Horwath HTL, Thai tourism industry should return to positive growth in 2010 assuming political situation remains stable

Regional Outlook

2009F 2010F

OCC ADR OCC ADR

Bangkok 50-55% $90-95 55-60% $85-90

Phuket 55-60% $110-115 65-70% $105-110

Bali 65-70% $115-120 65-70% $120-125

Singapore 65-70% $170-175 65-70% $170-175

Source: Horwath HTL

V. Expansion & Cashflow Outlook

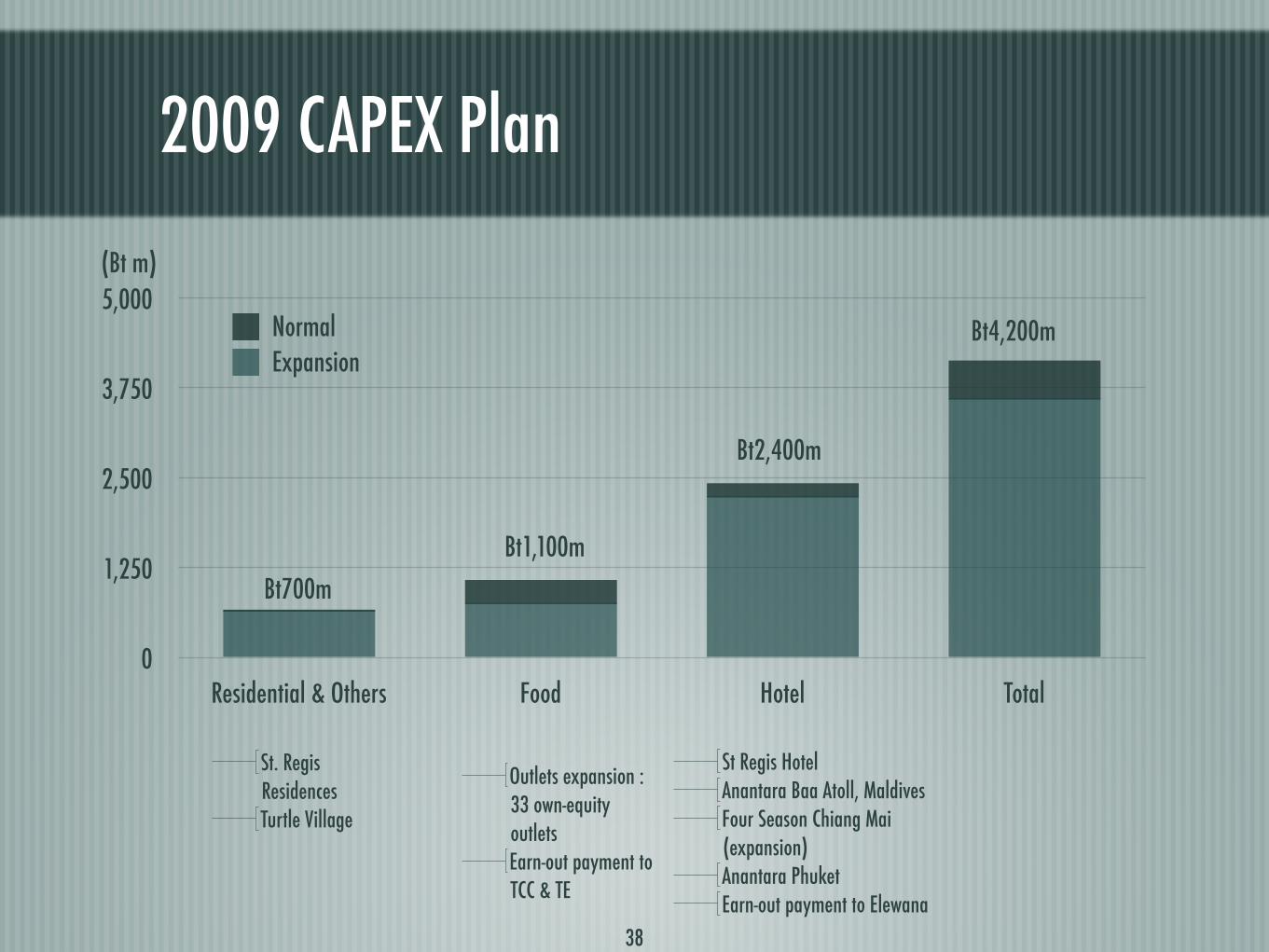

2009 CAPEX Plan

0

1,250

2,500

3,750

5,000

Residential & Others Food Hotel Total

ExpansionNormal

St. Regis ResidencesTurtle Village

Outlets expansion : 33 own-equity outlets Earn-out payment to TCC & TE

St Regis HotelAnantara Baa Atoll, MaldivesFour Season Chiang Mai (expansion)Anantara PhuketEarn-out payment to Elewana

(Bt m)

Bt1,100m

Bt700m

Bt2,400m

Bt4,200m

38

Project Development Progress

Anantara Baa Atoll HotelProject: 82 Keys

Completion: April 2010

3 months delay from expand program of work and complicated in detail design

ST. Regis Hotel & ResidenceProject: Hotel 220 keys; 53 Condo units

Completion: September 2010

Building construction up to 32 storey; overall main equipment completed 60%

Four Seasons Chiang Mai, ExtensionProject: Hotel 12 pool villas

Completion: 4Q 2009 39

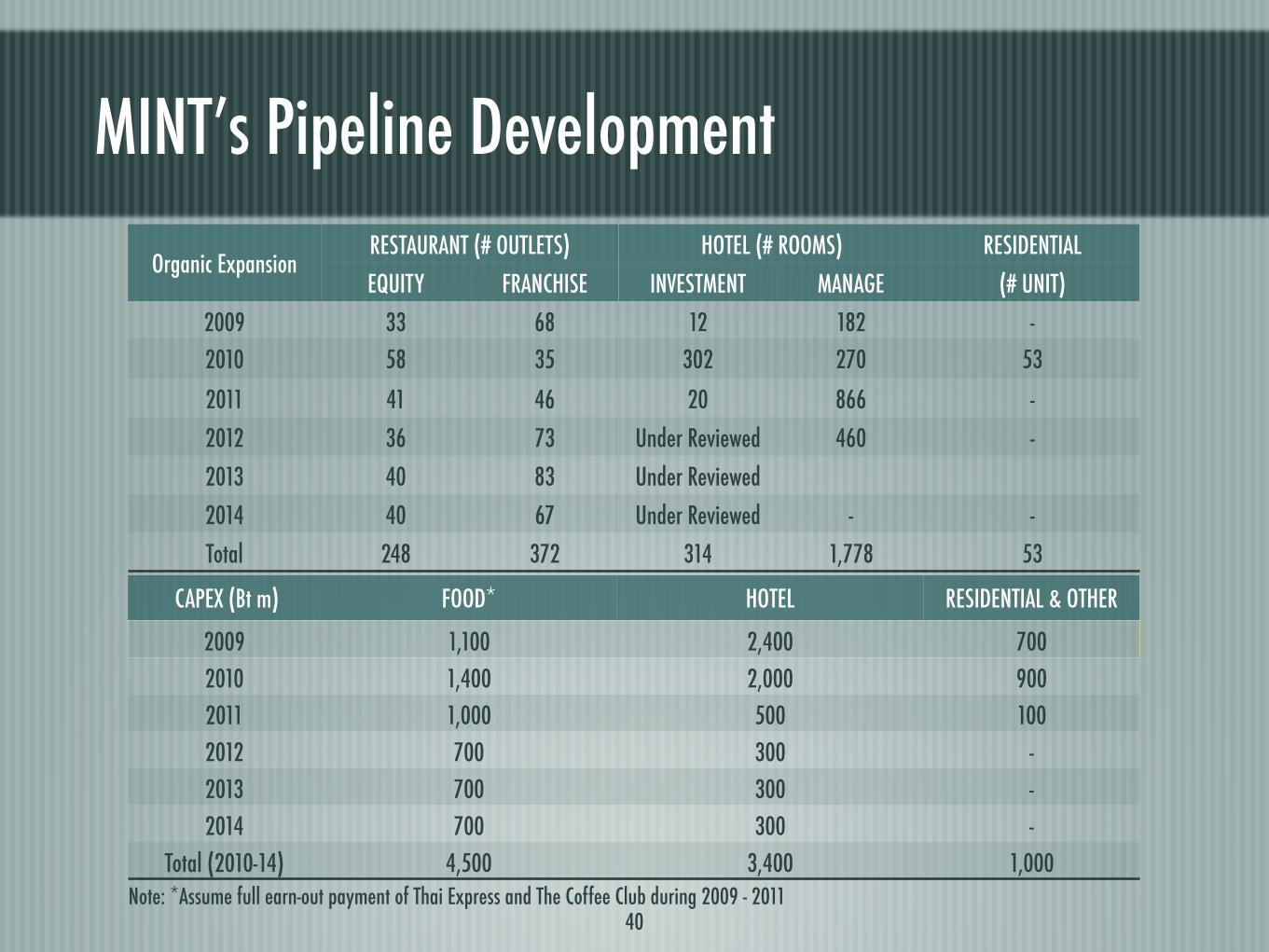

MINT’s Pipeline Development

Organic ExpansionRESTAURANT (# OUTLETS) HOTEL (# ROOMS) RESIDENTIAL

EQUITY FRANCHISE INVESTMENT MANAGE (# UNIT)

2009 33 68 12 182 -

2010 58 35 302 270 53

2011 41 46 20 866 -

2012 36 73 Under Reviewed 460 -

2013 40 83 Under Reviewed

2014 40 67 Under Reviewed - -

Total 248 372 314 1,778 53

CAPEX (Bt m) FOOD* HOTEL RESIDENTIAL & OTHER

2009 1,100 2,400 700

2010 1,400 2,000 900

2011 1,000 500 100

2012 700 300 -

2013 700 300 -

2014 700 300 -

Total (2010-14) 4,500 3,400 1,000

40Note: *Assume full earn-out payment of Thai Express and The Coffee Club during 2009 - 2011

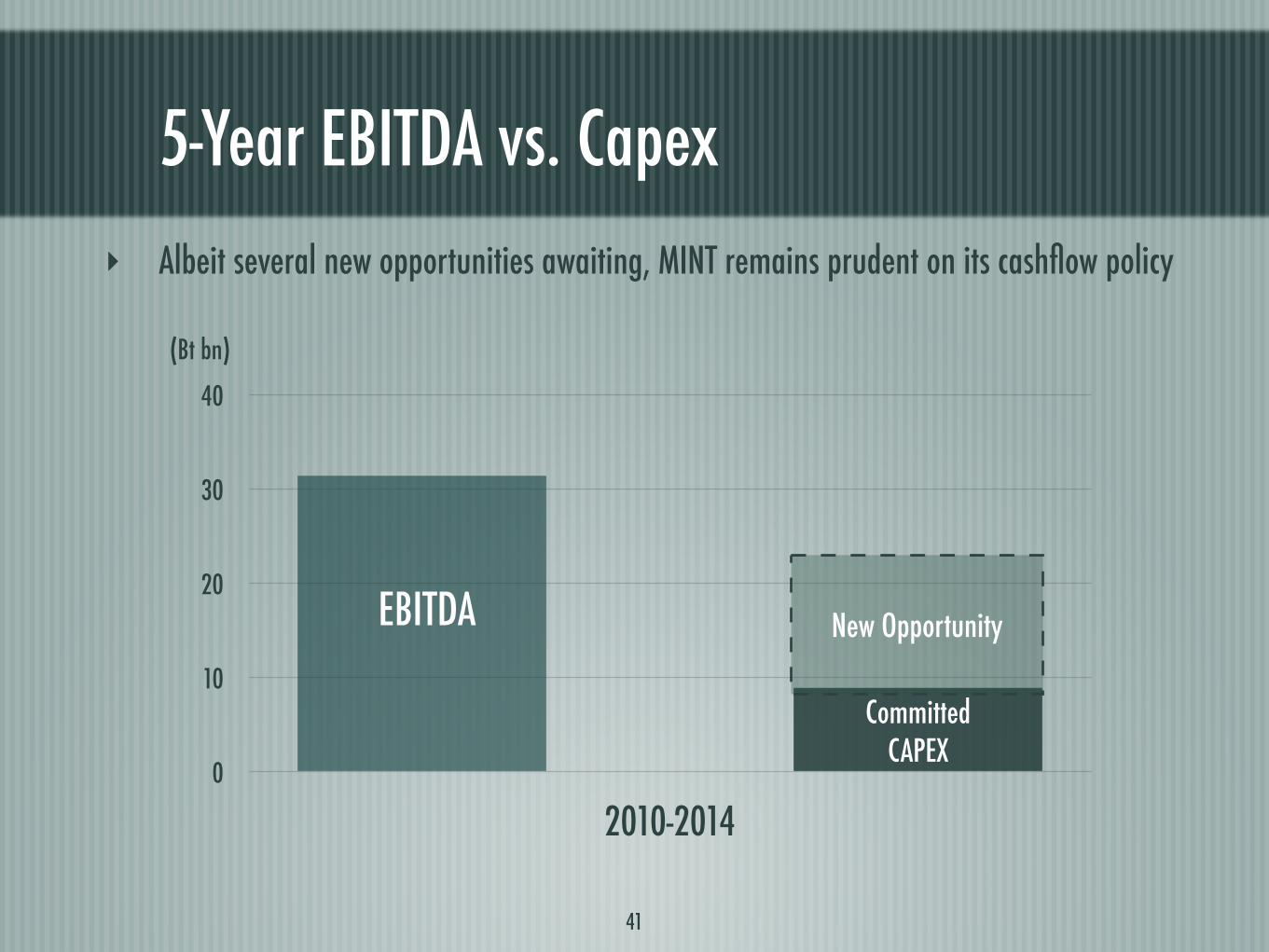

5-Year EBITDA vs. Capex

0

10

20

30

40

2010-2014

(Bt bn)

EBITDA

CommittedCAPEX

New Opportunity

41

! Albeit several new opportunities awaiting, MINT remains prudent on its cashflow policy

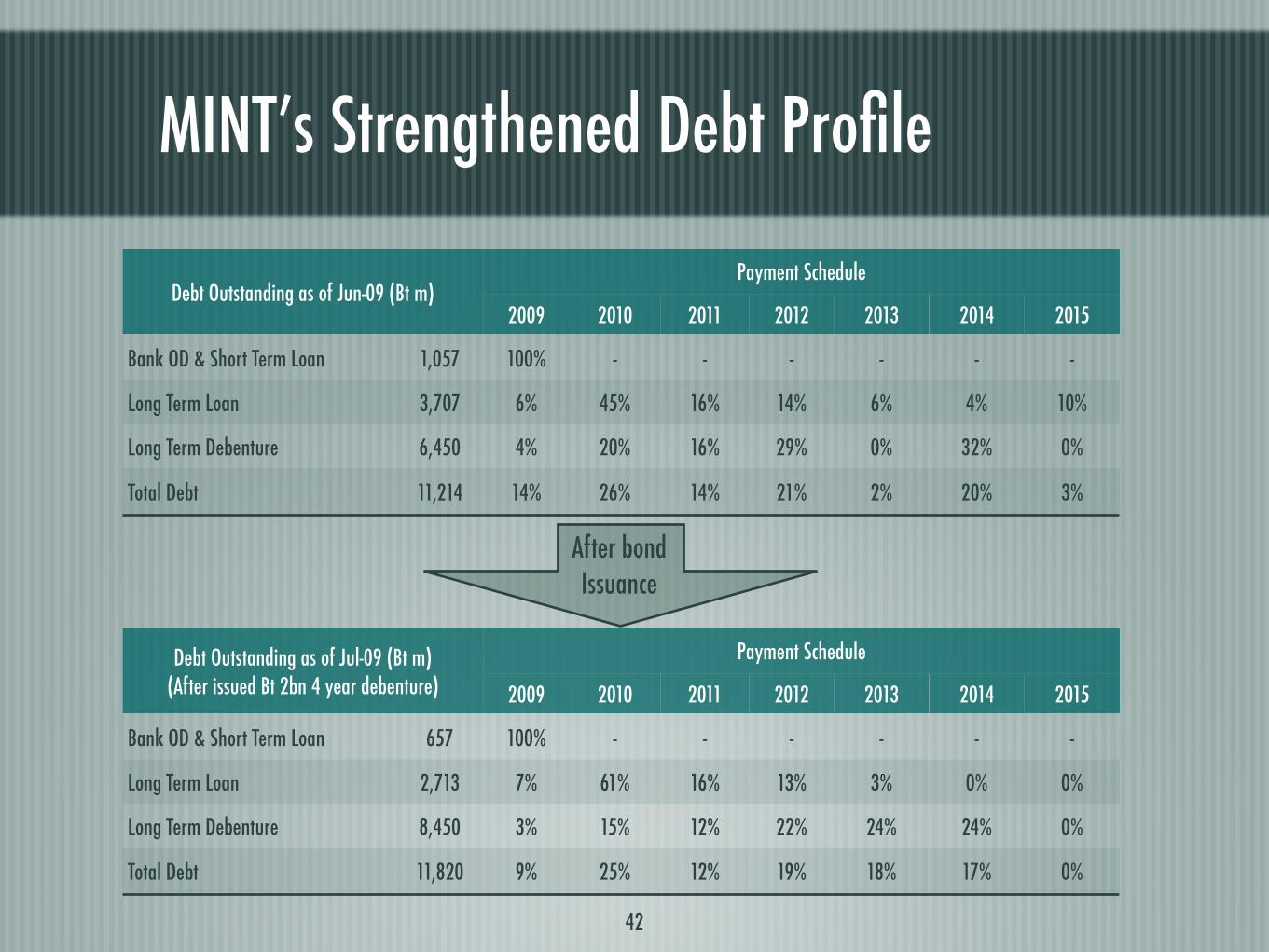

MINT’s Strengthened Debt Profile

42

Debt Outstanding as of Jun-09 (Bt m)Payment Schedule

2009 2010 2011 2012 2013 2014 2015

Bank OD & Short Term Loan 1,057 100% - - - - - -

Long Term Loan 3,707 6% 45% 16% 14% 6% 4% 10%

Long Term Debenture 6,450 4% 20% 16% 29% 0% 32% 0%

Total Debt 11,214 14% 26% 14% 21% 2% 20% 3%

Debt Outstanding as of Jul-09 (Bt m)(After issued Bt 2bn 4 year debenture)

Payment Schedule

2009 2010 2011 2012 2013 2014 2015

Bank OD & Short Term Loan 657 100% - - - - - -

Long Term Loan 2,713 7% 61% 16% 13% 3% 0% 0%

Long Term Debenture 8,450 3% 15% 12% 22% 24% 24% 0%

Total Debt 11,820 9% 25% 12% 19% 18% 17% 0%

After bond Issuance

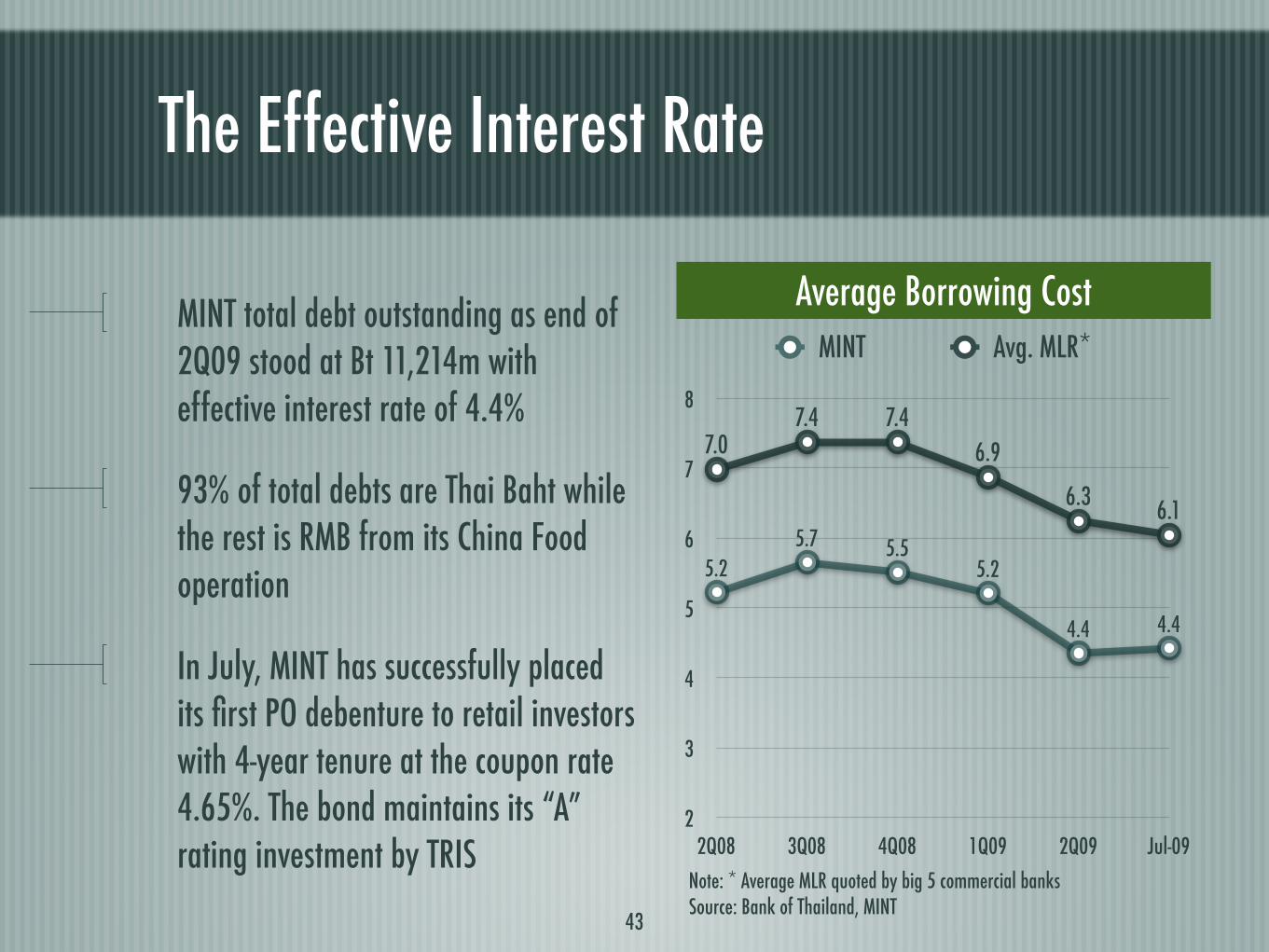

The Effective Interest Rate

2

3

4

5

6

7

8

2Q08 3Q08 4Q08 1Q09 2Q09 Jul-09

7.07.4 7.4

6.9

6.36.1

5.2

5.7 5.55.2

4.4 4.4

MINT total debt outstanding as end of 2Q09 stood at Bt 11,214m with effective interest rate of 4.4%

93% of total debts are Thai Baht while the rest is RMB from its China Food operation

In July, MINT has successfully placed its first PO debenture to retail investors with 4-year tenure at the coupon rate 4.65%. The bond maintains its “A” rating investment by TRIS

Average Borrowing Cost

43

MINT Avg. MLR*

Note: * Average MLR quoted by big 5 commercial banksSource: Bank of Thailand, MINT

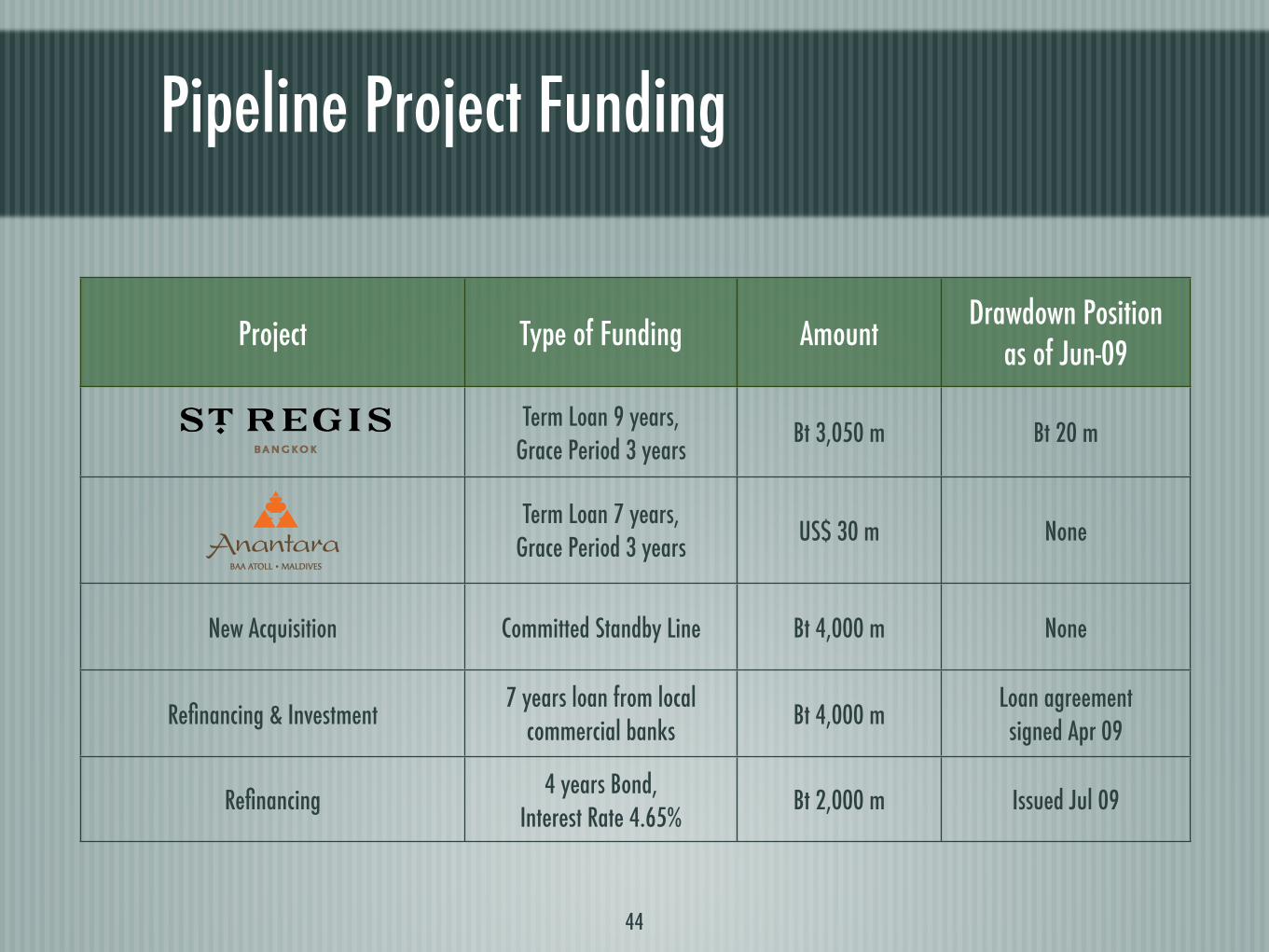

Pipeline Project Funding

Project Type of Funding AmountDrawdown Position

as of Jun-09

Term Loan 9 years, Grace Period 3 years

Bt 3,050 m Bt 20 m

Term Loan 7 years, Grace Period 3 years

US$ 30 m None

New Acquisition Committed Standby Line Bt 4,000 m None

Refinancing & Investment7 years loan from local

commercial banksBt 4,000 m

Loan agreement signed Apr 09

Refinancing 4 years Bond,

Interest Rate 4.65%Bt 2,000 m Issued Jul 09

44

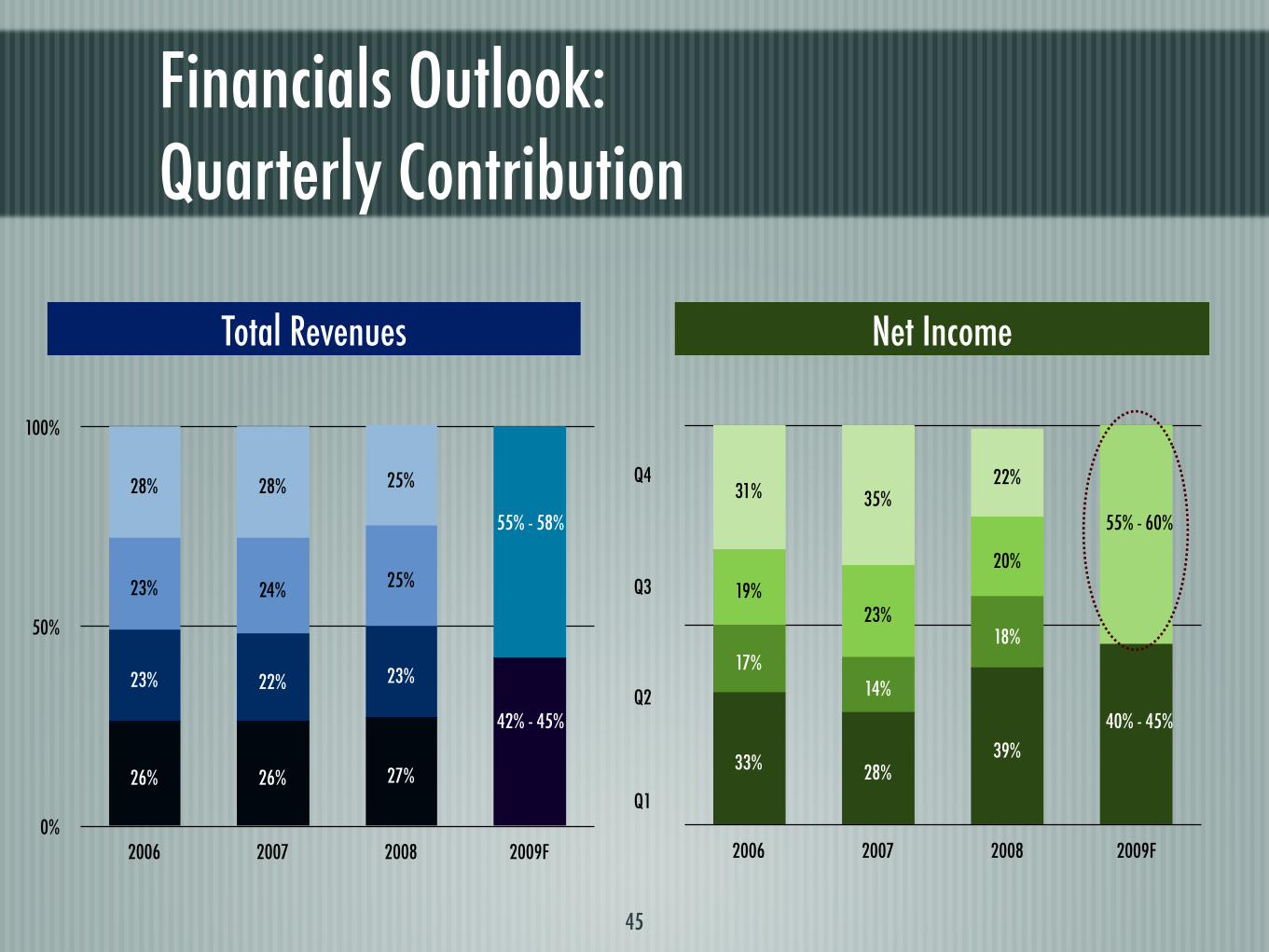

Financials Outlook: Quarterly Contribution

45

0%

50%

100%

2006 2007 2008 2009F

25%28%28%

25%24%23%

23%22%23%

27%26%26%

Q4

Q3

Q2

Q1

2006 2007 2008 2009F

22%35%31%

20%

23%19%

18%

14%17%

39%28%33%

Total Revenues Net Income

42% - 45%

55% - 58%

40% - 45%

55% - 60%

Q&A