Millennial Money - Putnam InvestmentsMillennial Money Building your business for tomorrow, today...

32

Millennial Money Building your business for tomorrow, today Alexandra G. Nawoichik Practice Management Specialist Putnam Retail Management

Transcript of Millennial Money - Putnam InvestmentsMillennial Money Building your business for tomorrow, today...

Millennial MoneyBuilding your business for tomorrow, today

Alexandra G. NawoichikPractice Management SpecialistPutnam Retail Management

For dealer use only. Not for public distribution.PPT290 316775 4/19

2

Understanding Millennial clients

Are Not FDIC Insured May Lose Value Are Not Bank Guaranteed

Are Not Insured by Any Federal Government Agency Are Not Deposits Are Not a Condition to Any

Banking Service or Activity

Investing involves risk including possible loss of principal. Information is current as of the date of this material.

Any opinions expressed herein are from a third party and are given in good faith, are subject to change without notice, and are considered correct as of the stated date of their issue.

Merrill Lynch, Pierce, Fenner & Smith Incorporated is not a tax or legal advisor. Clients should consult a personal tax or legal advisor prior to making any tax or legal related investment decisions.

Bank of America Corporation (“Bank of America”) is a financial holding company that, through its subsidiaries and affiliated companies, provides banking and investment products and other financial services.

Merrill Lynch makes available products and services offered by Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”), a registered broker-dealer and Member SIPC, and other subsidiaries of Bank of America Corporation. Merrill Lynch Life Agency is a licensed insurance agency and a wholly owned subsidiary of Bank of America Corporation.

Merrill Lynch offers a broad range of brokerage, investment advisory and other services. There are important differences between brokerage and investment advisory services, including the type of advice and assistance provided, the fees charged, and the rights and obligations of the parties. It is important to understand the differences, particularly when determining which service or services to select. The views and opinions expressed in this presentation are not necessarily those of Bank of America Corporation; Merrill Lynch, Pierce, Fenner & Smith Incorporated; or any affiliates. Merrill Lynch has not participated in preparing this presentation and accepts no responsibility for the accuracy of the information contained herein.

Nothing discussed or suggested in these materials should be construed as permission to supersede or circumvent any Bank of America, Merrill Lynch, Pierce, Fenner & Smith Incorporated policies, procedures, rules, and guidelines.

Investment products offered through MLPF&S and insurance and annuity products offered through Merrill Lynch Life Agency Inc.:

For dealer use only. Not for public distribution.PPT290 316775 4/19

3

Understanding Millennial clients

Note: See slide 31 for source.

“The young seem curiously unappreciative of the society that

supports them. ‘Don’t trust anyone over 30,’ is one of their

rallying cries. Another, ‘Tell it like it is,’ conveys an abiding

mistrust of what they consider adult deviousness.” – Time

For dealer use only. Not for public distribution.

PPT290 316775 4/19

4

Understanding Millennial clients

“We do have a sense of entitlement, a sense of ownership,

because, after all, this is the world we were born into and we are

responsible for it.” – Evan Spiegel, 2015

For dealer use only. Not for public distribution.PPT290 316775 4/19

5

Understanding Millennial clients

Overview

Who Millennials are

Why Millennials matter to your practice

How to gain Millennial assets

For dealer use only. Not for public distribution.PPT290 316775 4/19

6

Understanding Millennial clients

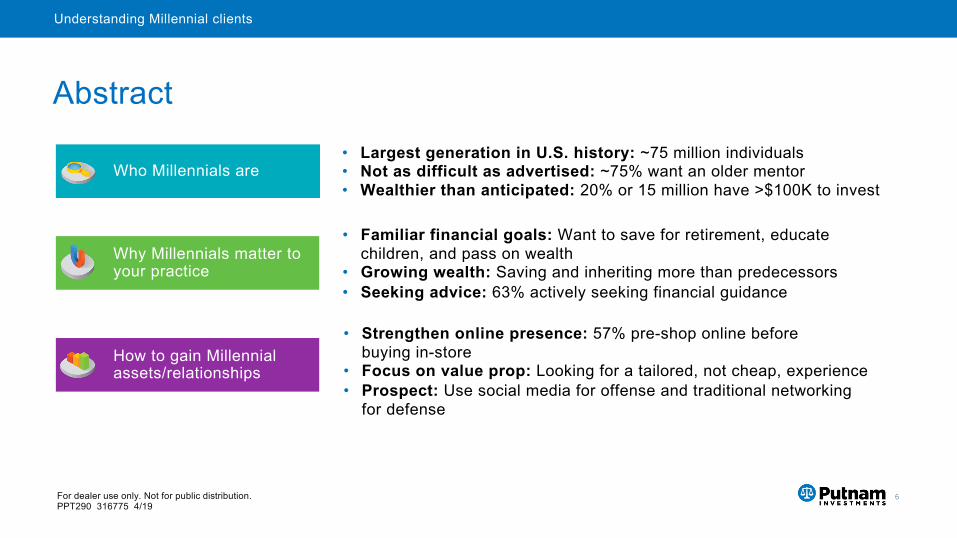

Abstract

Who Millennials are

Why Millennials matter to your practice

How to gain Millennial assets/relationships

• Largest generation in U.S. history: ~75 million individuals• Not as difficult as advertised: ~75% want an older mentor• Wealthier than anticipated: 20% or 15 million have >$100K to invest

• Familiar financial goals: Want to save for retirement, educate children, and pass on wealth

• Growing wealth: Saving and inheriting more than predecessors• Seeking advice: 63% actively seeking financial guidance

• Strengthen online presence: 57% pre-shop online before buying in-store

• Focus on value prop: Looking for a tailored, not cheap, experience• Prospect: Use social media for offense and traditional networking

for defense

Who Millennials are

For dealer use only. Not for public distribution.PPT290 316775 4/19

8

Who Millennials are

Definition

Sources: Pew Research Center, 2016; National Public Radio, 2014.

1946 1952 1958 1964 1970 1976 1982 1988 1994 2000

Baby Boomers:Age 53–71 (~75 million) Generation X:

Age 38–52 (~66 million) Millennials:

Age 17–37 (~75 million)

10,000 Millennials turn 21 each day.

10,000 Baby Boomers turn 65 each day.

For dealer use only. Not for public distribution.PPT290 316775 4/19

9

Who Millennials are

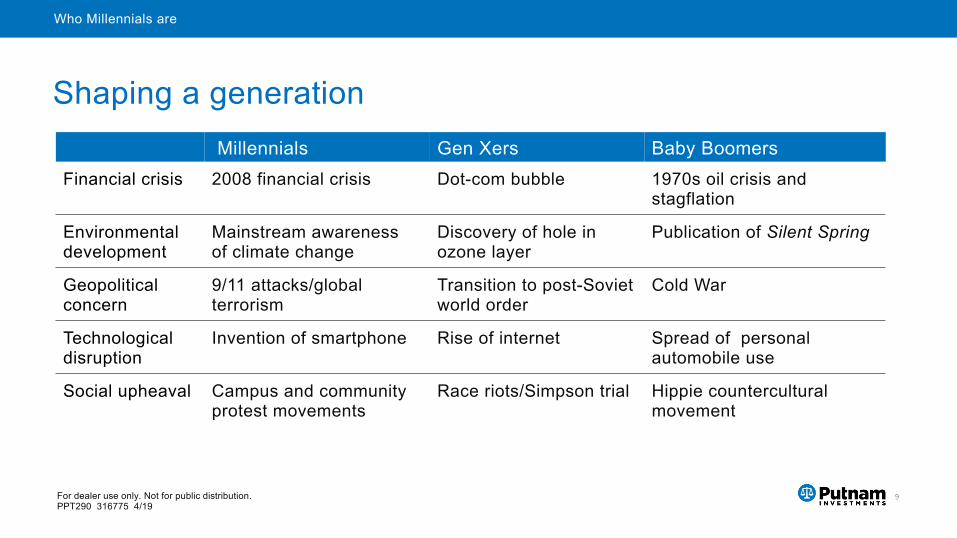

Shaping a generation

Millennials Gen Xers Baby Boomers

Financial crisis 2008 financial crisis Dot-com bubble 1970s oil crisis and stagflation

Environmental development

Mainstream awareness of climate change

Discovery of hole in ozone layer

Publication of Silent Spring

Geopolitical concern

9/11 attacks/global terrorism

Transition to post-Soviet world order

Cold War

Technological disruption

Invention of smartphone Rise of internet Spread of personal automobile use

Social upheaval Campus and community protest movements

Race riots/Simpson trial Hippie countercultural movement

For dealer use only. Not for public distribution.PPT290 316775 4/19

10

Who Millennials are

MYTHMillennials don’t want advice from members of older generations

REALITY75% of Millennials want a mentor. Millennials want their opinions to be heard but love to learn from the experiences of other generations

IMPACTMillennials want true mentorship rather than cursory guidance. 74% of Millennials think advisors don’t offer truly customized advice

Sources: MediaPost, 2012; AMG Funds, 2017.

Myths surrounding Millennials

For dealer use only. Not for public distribution.

PPT290 316775 4/19

11

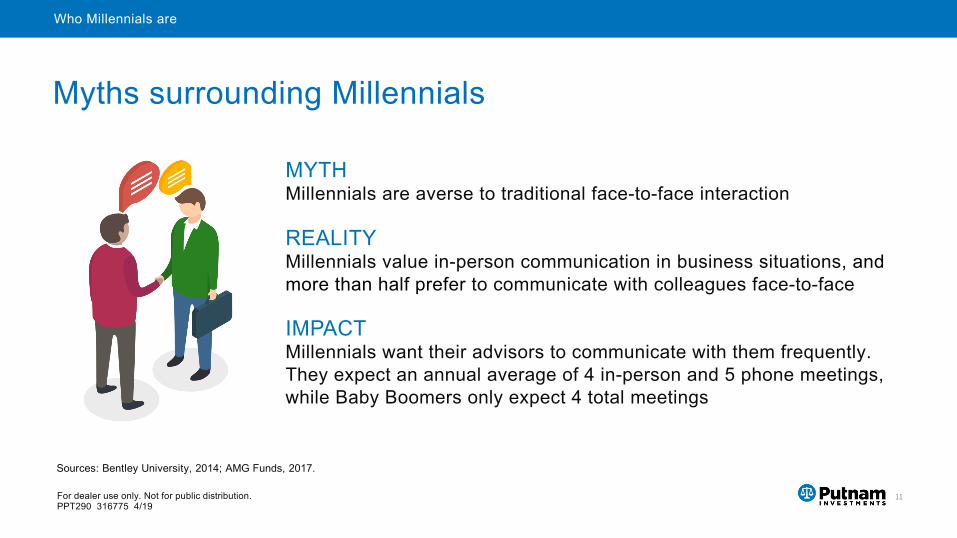

Who Millennials are

Myths surrounding Millennials

MYTH

Millennials are averse to traditional face-to-face interaction

REALITY

Millennials value in-person communication in business situations, and

more than half prefer to communicate with colleagues face-to-face

IMPACT

Millennials want their advisors to communicate with them frequently.

They expect an annual average of 4 in-person and 5 phone meetings,

while Baby Boomers only expect 4 total meetings

Sources: Bentley University, 2014; AMG Funds, 2017.

For dealer use only. Not for public distribution.

PPT290 316775 4/19

12

Who Millennials are

Myths surrounding Millennials

Sources: Deloitte, 2014; Toniic Institute, 2016.

MYTH

Millennials are selfish and entitled

REALITY

Two out of three Millennials report that they are concerned with the

state of the world and feel obligated to change it

IMPACT

Millennials need guidance on making an impact. 60% would like to

invest more than half of their wealth in ESG investments within 5

years, yet only 25% currently do so

For dealer use only. Not for public distribution.

PPT290 316775 4/19

13

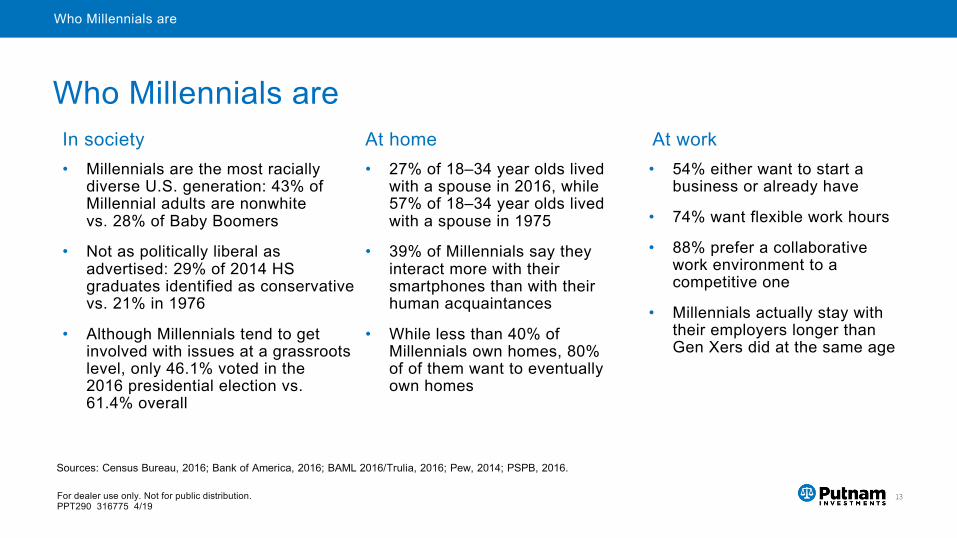

Who Millennials are

Who Millennials are

Sources: Census Bureau, 2016; Bank of America, 2016; BAML 2016/Trulia, 2016; Pew, 2014; PSPB, 2016.

• 54% either want to start a

business or already have

• 74% want flexible work hours

• 88% prefer a collaborative

work environment to a

competitive one

• Millennials actually stay with

their employers longer than

Gen Xers did at the same age

At work

• 27% of 18–34 year olds lived

with a spouse in 2016, while

57% of 18–34 year olds lived

with a spouse in 1975

• 39% of Millennials say they

interact more with their

smartphones than with their

human acquaintances

• While less than 40% of

Millennials own homes, 80%

of of them want to eventually

own homes

At home

• Millennials are the most racially

diverse U.S. generation: 43% of

Millennial adults are nonwhite

vs. 28% of Baby Boomers

• Not as politically liberal as

advertised: 29% of 2014 HS

graduates identified as conservative

vs. 21% in 1976

• Although Millennials tend to get

involved with issues at a grassroots

level, only 46.1% voted in the

2016 presidential election vs.

61.4% overall

In society

Why Millennials matter to your practice

For dealer use only. Not for public distribution.PPT290 316775 4/19

15

Why Millennials matter to your practice

Savers Accumulators AttainersInvestable assets Less than $100K Between $100K and

$250KMore than $250K

Total number of prospects ~60 million ~15 million

Financial tendencies

Have modest financial goals

Prioritize shorter-term financial needs over longer-term financial goals

Set ambitious long-term goals

Prioritize financial advice but have limited financial knowledge

Engage well with financial technology

Have significant financial knowledge and want to be involved in investment decisions

Sources: LinkedIn, 2015; ThinkAdvisor, 2016.

Breaking down Millennials

For dealer use only. Not for public distribution.PPT290 316775 4/19

16

Why Millennials matter to your practice

Less positive market experienceAt same time in careers, Boomers had experienced average annual GDP growth of 2.8%, Gen Xers 3.3%, and Millennials 1.9%

Greater burden of college debt2016 graduates average $37,172 in student loan debt

Changing attitudes toward home ownershipMore Millennials are saving for travel (46%) than for a home (38%)

Delayed marriageIn 1980, two-thirds of those age 25–34 were married. In 2015, two-fifths of those in that age range were married

Greater life expectancyA 25-year-old male is expected to live to ~86, and a 25-year-old female is expected to live to ~89

Millennials have shifting challenges and priorities

Sources: St. Louis Fed, 2017; Forbes, 2016; Bank of the West, 2017; Bloomberg, 2017; Society of Actuaries, 2016.

For dealer use only. Not for public distribution.PPT290 316775 4/19

17

Why Millennials matter to your practice

Including an interest in sustainable investing

Impact investing and/or Environmental, Social and Governance (ESG) managers may take into consideration factors beyond traditional financial information to select securities, which could result in relative investment performance deviating from other strategies or broad market benchmarks, depending on whether such sectors or investments are in or out of favor in the market. Further, ESG strategies may rely on certain values based criteria to eliminate exposures found in similar strategies or broad market benchmarks, which could also result in relative investment performance deviating.

Source: Toniic, 2016.

Are Millennials interested in sustainable investing?79% of Millennials describe themselves as sustainable investors seeking both financial and social impact returns

How widespread is Millennial sustainable investing?~50% of Millennials either don’t know their current allocation to sustainable investments or have 0–10% of their assets in sustainable investments

Will Millennials sacrifice return in favor of sustainability?13% say they are interested in opportunities aligned with their values, regardless of financial return

Which sustainable investing topics most interest Millennials?Agriculture ~30%Energy ~40%Environment ~30%

For dealer use only. Not for public distribution.PPT290 316775 4/19

18

Why Millennials matter to your practice

7%

20%

12%

42%

56%

10%

6%

3%

31%

65%

However, Millennials have life goals similar to previous generations

Source: Transamerica Center for Retirement Studies, 2016.

Saving for retirement

Paying off mortgage

Paying off student loans

Contributing to an education fund

Building a financial legacy 15%

21%

20%

36%

54%

Millennials Gen X Baby boomers

Financial priorities right now

For dealer use only. Not for public distribution.

PPT290 316775 4/19

19

Why Millennials matter to your practice

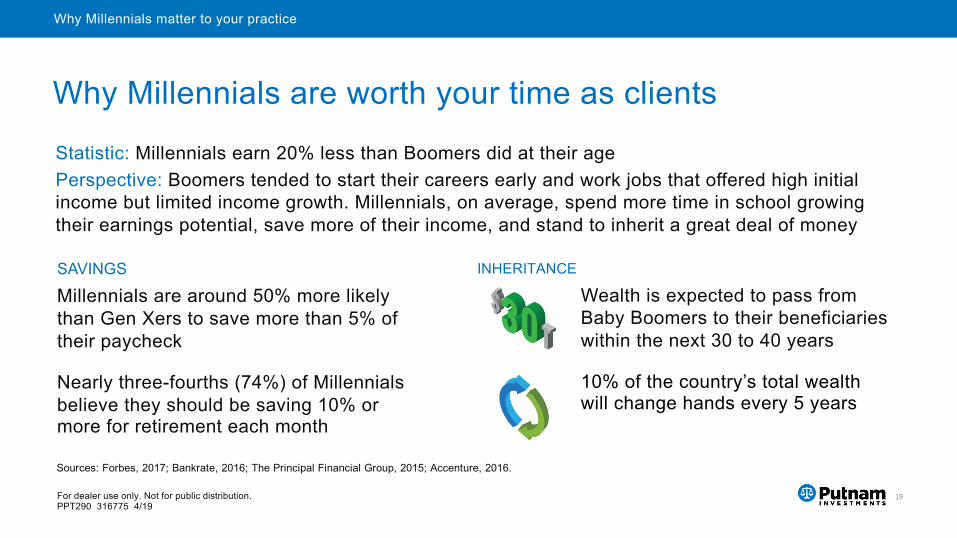

Why Millennials are worth your time as clients

Sources: Forbes, 2017; Bankrate, 2016; The Principal Financial Group, 2015; Accenture, 2016.

SAVINGS

Millennials are around 50% more likely

than Gen Xers to save more than 5% of

their paycheck

Nearly three-fourths (74%) of Millennials

believe they should be saving 10% or

more for retirement each month

INHERITANCE

Wealth is expected to pass from

Baby Boomers to their beneficiaries

within the next 30 to 40 years

10% of the country’s total wealth

will change hands every 5 years

Statistic: Millennials earn 20% less than Boomers did at their age

Perspective: Boomers tended to start their careers early and work jobs that offered high initial

income but limited income growth. Millennials, on average, spend more time in school growing

their earnings potential, save more of their income, and stand to inherit a great deal of money

For dealer use only. Not for public distribution.PPT290 316775 4/19

20

Why Millennials matter to your practice

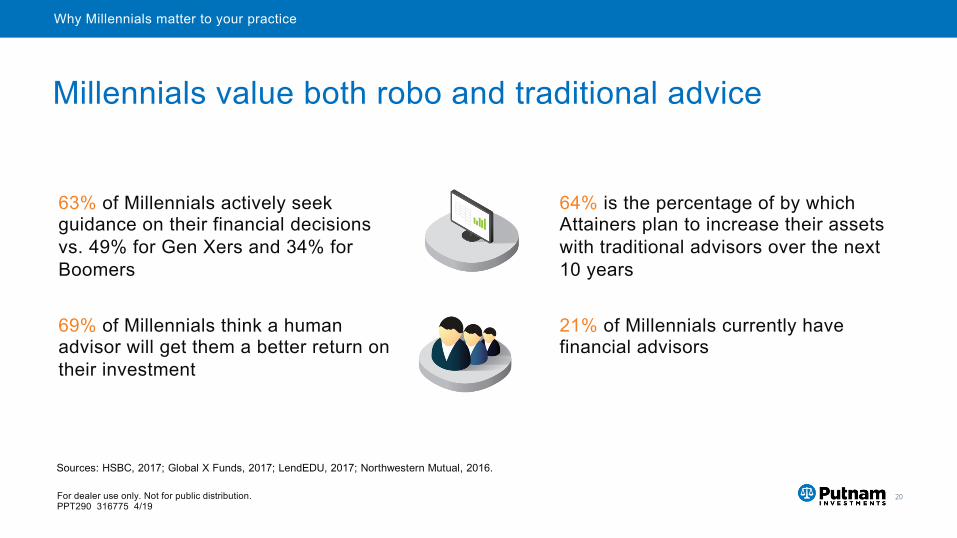

Millennials value both robo and traditional advice

Sources: HSBC, 2017; Global X Funds, 2017; LendEDU, 2017; Northwestern Mutual, 2016.

64% is the percentage of by which Attainers plan to increase their assets with traditional advisors over the next 10 years

63% of Millennials actively seek guidance on their financial decisions vs. 49% for Gen Xers and 34% for Boomers

69% of Millennials think a human advisor will get them a better return on their investment

21% of Millennials currently have financial advisors

How to gain Millennial assets

For dealer use only. Not for public distribution.PPT290 316775 4/19

22

How to gain millennial assets

• 57% of Millennials said that they always or frequently conduct online pre-shopping research

• 62% of millennials say that if a brand engages with them on social networks, they are more likely to become a loyal customer. They expect brands to not only be on social networks, but to engage them

• 69% of UHNW Millennials select their FAs based on recommendations from family, friends, and colleagues

Sources: Oppenheimer, 2017; Deloitte, 2014; RetailDive, 2017.

How Millennials select advisors

For dealer use only. Not for public distribution.PPT290 316775 4/19

23

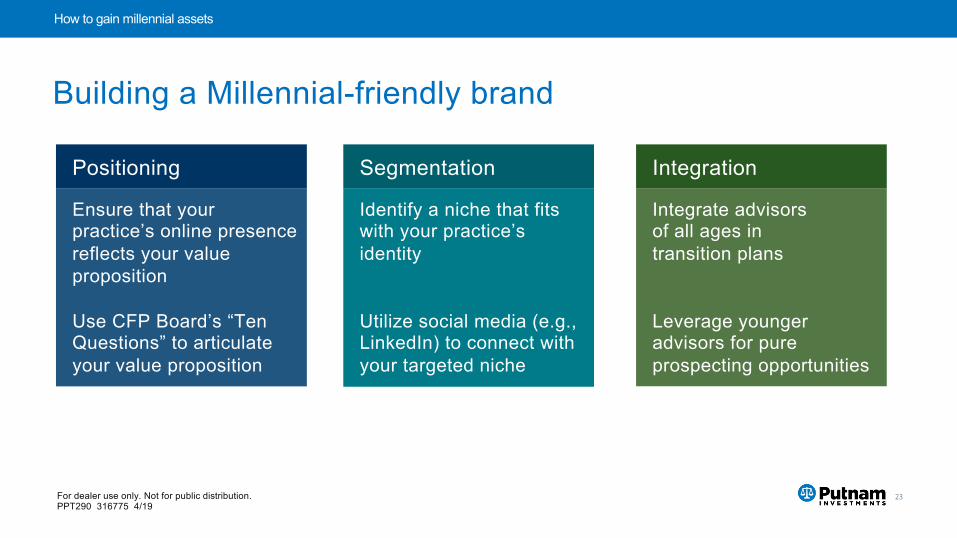

How to gain millennial assets

Building a Millennial-friendly brand

Positioning

Ensure that your practice’s online presence reflects your value proposition

Use CFP Board’s “Ten Questions” to articulate your value proposition

Segmentation

Identify a niche that fits with your practice’s identity

Utilize social media (e.g., LinkedIn) to connect with your targeted niche

Integration

Integrate advisors of all ages in transition plans

Leverage younger advisors for pure prospecting opportunities

For dealer use only. Not for public distribution.PPT290 316775 4/19

24

How to gain millennial assets

Working with Millennials

Sources: AMG Funds, 2017; Toniic Institute, 2016; AMG Funds, 2017; Accenture, 2017; JPMorgan/GIIN, 2011.

Emphasize goalsCoachSet expectations• 70% of Millennials think

computer-generated portfolios almost always outperform human portfolios, while 63% think computer-generated portfolios are almost always less risky

• 62% of people (all ages) surveyed by JPM and GIIN said they would sacrifice returns for impact

• Millennials are four times as likely as Baby Boomers to consider themselves knowledgeable about investments

• Yet they require extensive counsel. 50% of Millennials say they would never take an FA’s advice without consulting another source

• Millennials expect an average annual return of 13.7% from a portfolio allocated 30% to equities. Baby Boomers and Gen Xers expect an average annual return of 8.6% from a portfolio allocated 46% to equities

• 38% of Millennials say advisor pushback is the main reason they don’t invest more in ESG

For dealer use only. Not for public distribution.PPT290 316775 4/19

25

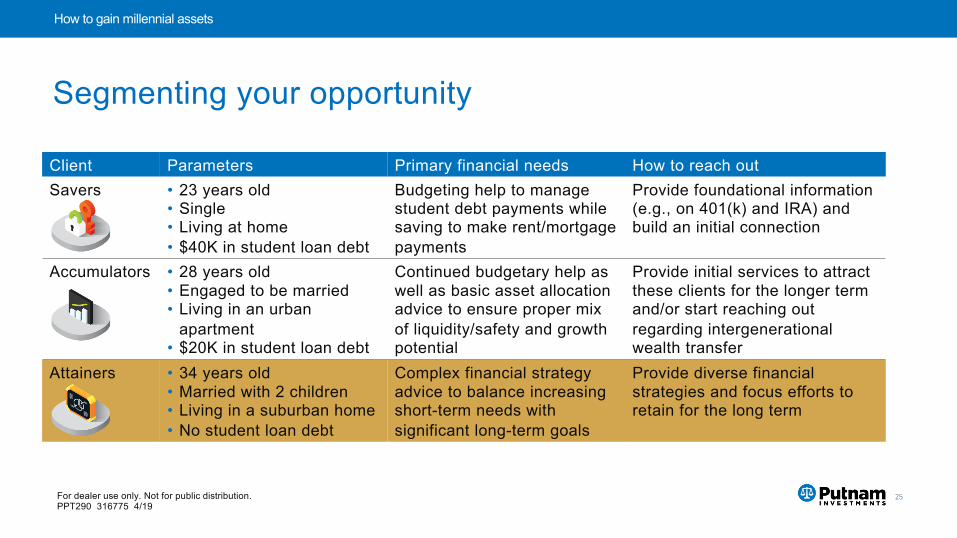

How to gain millennial assets

Client Parameters Primary financial needs How to reach outSavers • 23 years old

• Single• Living at home• $40K in student loan debt

Budgeting help to manage student debt payments while saving to make rent/mortgage payments

Provide foundational information (e.g., on 401(k) and IRA) and build an initial connection

Accumulators • 28 years old• Engaged to be married• Living in an urban

apartment• $20K in student loan debt

Continued budgetary help as well as basic asset allocation advice to ensure proper mix of liquidity/safety and growth potential

Provide initial services to attract these clients for the longer term and/or start reaching out regarding intergenerational wealth transfer

Attainers • 34 years old• Married with 2 children• Living in a suburban home• No student loan debt

Complex financial strategyadvice to balance increasing short-term needs with significant long-term goals

Provide diverse financial strategies and focus efforts to retain for the long term

Segmenting your opportunity

For dealer use only. Not for public distribution.PPT290 316775 4/19

26

How to gain millennial assets

ProspectingFor pure prospects

• Use “Alumni” tab on LinkedIn to find young people in the area who attended your school• Target recently relocated Millennials to build lasting ties• Partner with local employers to offer financial training for new hires

For current client beneficiaries• Make sure you have met all your clients’ beneficiaries; family wealth days can be powerful• Schedule ‘financial checkups’ for college-age children visiting home• Offer to review 401(k) options for (grand)children of current clients• Offer mock interview for clients’ (grand)children during graduation season and help network for

outstanding beneficiaries

Retaining• If possible, implement flexible service/pricing models• Consider Millennials’ preference to communicate more often (9x per year) than their older counterparts• Use retirement calculator to emphasize the power of systematic investing• Create a newsletter/email targeted to Millennial clients; think theSkimm

Action plan for Savers/Accumulators

For dealer use only. Not for public distribution.PPT290 316775 4/19

27

How to gain millennial assets

ProspectingFor pure prospects

• Partner with local tech firms to target up-and-coming local leaders• Refine your prospecting niche using advanced search tools on LinkedIn• Set up a booth at a wedding expo to prospect Millennials facing a major milestone

For current client beneficiaries• Create an “I love you” letter to involve the entire family• Offer to involve adult children in philanthropic activities• Help parents and children create a transition plan for family business

Retaining• Offer childcare at client events to accommodate young parents• Understand Millennial tendency to expect higher returns, lower risk, and social responsibility; set

expectations accordingly• Simplify routine review process, possibly conducting via phone, while emphasizing in-depth meetings

based on client goals/life events

Action plan for Attainers

For dealer use only. Not for public distribution.

PPT290 316775 4/19

28

How to gain millennial assets

Work with Putnam to …

Position my practice

Develop a practice-specific value proposition

Create a LinkedIn profile and review other potential

social media platforms

Schedule a LinkedIn training call with my Putnam

wholesaler to optimize my profile

Target Millennial investors

Use the Alumni tab on LinkedIn to target local

Millennials from my alma mater

Work with my Putnam wholesaler to arrange a family

wealth day for my clients

Connect with my clients’ beneficiaries on LinkedIn

Integrate Millennial clients

Review my investment lineup to identify Millennial-

friendly options

Utilize FundVisualizer and Portfolio Navigator to

develop fund narratives to coach Millennial investors

Be reachable via phone/text to offer meeting flexibility

for busy Millennial clients

Read Putnam’s Wealth Management blog to find

timely Millennial-friendly planning strategies

Encourage younger advisors in my office to connect

with Millennial clients and develop their skills

Why millennials matter to your practice

Appendix

For dealer use only. Not for public distribution.PPT290 316775 4/19

30

Understanding Millennial clients

An Attainer and ESGTHE CLIENT34 years oldMarried with 2 childrenLiving in a suburban homeNo student loan debt

THE SITUATIONDuring your latest meeting with an existing Millennial client, the client mentions that she recently discussed ESG investing with a friend and wants to learn more. The client hasn’t previously expressed an interest in ESG issues, and you have allocated 0% of her money to ESG investments.

YOUR RESPONSESTEP 1: Make sure you are informed. The GIIN/TONIIC websites offer educational materials to teach you the terminology (sustainalytics, SDGs, etc.) and a newsletter to keep you apprised of the latest developments. Understanding the various causes and investment styles under the ESG umbrella will help you better understand what your client wantsSTEP 2: Enquire into client’s interest in the space and ensure it is genuine. ESG investing entails unique risk/return characteristics, so setting expectations is crucialSTEP 3: Maintain a working list of investment ideas (individual securities, funds, etc.) from which to make allocations. Work with the client to craft a goals-based plan to integrate social or impact investing into her portfolio. This client has complex financial planning needs and requires your expertise to manage her long- and short-term goals while fulfilling her ethical investment mandate

QUESTIONS TO ASKTo determine general interest: “If you could commit a small portion of your portfolio to companies and causes that matter to you while still responsibly growing your money for retirement, would you?”To determine familiarity: “Did you know that Sustainable, ESG, and Impact investing all mean different things?”To determine commitment level: “Would you be willing to spend an hour or two reading relevant materials so we are on the same page on how best to invest your money for impact?”

For dealer use only. Not for public distribution.PPT290 316775 4/19

31

Understanding Millennial clients

Putnam Retail Managementputnam.com

Source — slide 3: Time magazine, 1967

Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of the Frank Russell Company.

For informational purposes only. Not an investment recommendation.

Consider these risks before investing: Allocation of assets among asset classes may hurt performance. Stock and bond prices may fall or fail to rise over time for several reasons, including general financial market conditions, factors related to a specific issuer or industry and, with respect to bond prices, changing market perceptions of the risk of default and changes in government intervention. These factors may also lead to increased volatility and reduced liquidity in the bond markets. International investing involves currency, economic, and political risks. Emerging-market securities carry illiquidity and volatility risks. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Growth stocks may be more susceptible to earnings disappointments, and value stocks may fail to rebound. Funds that invest in government securities are not guaranteed. Mortgage-backed investments, unlike traditional debt investments, are also subject to prepayment risk, which means that they may increase in value less than other bonds when interest rates decline and decline in value more than other bonds when interest rates rise. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Default risk is generally higher for non-qualified mortgages. Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Unlike bonds, funds that invest in bonds have fees and expenses. The use of derivatives may increase these risks by increasing investment exposure (which may be considered leverage) or, in the case of over-the-counter instruments, because of the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. The fund's sustainable investment strategy limits the types and number of investment opportunities available to the fund and, as a result, the fund may underperform other funds that do not have a sustainable focus. The fund’s investment strategy of investing in companies that exhibit a commitment to sustainable business practices may result in the fund investing in securities or industry sectors that underperform the market as a whole or underperform other funds that do not invest with a similar focus. Due to changes in the products or services of the companies in which the fund invests, the fund may temporarily hold securities that are inconsistent with its sustainable investment criteria. You can lose money by investing in the fund.

Your clients should carefully consider the investment objectives, risks, charges, and expenses of a fund before investing. For a prospectus, or a summary prospectus if available, containing this and other information for any Putnam fund or product, call the Putnam Client Engagement Center at 1-800-354-4000. Your clients should read the prospectus carefully before investing.