MiFID II Academy: Product Governance

23

MiFID II Academy: Product Governance Floortje Nagelkerke 12 April 2016

Transcript of MiFID II Academy: Product Governance

MiFID II Academy: Product Governance

Floortje Nagelkerke 12 April 2016

Introduction

2017201620152014

2 July MiFID II and MiFIR entered into force

1 AugustLevel 2 Consultation on advice on delegated acts and Discussion Paper on technical standards closed

19 DecemberLevel 2 Consultation on technical standards commenced. ESMA provided final report on technical advice to the Commission on delegated acts

2 March Level 2 Consultation on technical standards closed

28 SeptemberLevel 2 regulatory technical standards submitted to Commission

11 DecemberLevel 2 implementing technical standards submitted to Commission

3 JulyMember States to adopt and publish measures transposing MiFID II into national law

3 January 2017Original MiFID II and MiFIR Level 1 and Level 2 implementation date

Consultation period

Consultation period

6 June Consultation by Ministry of Finance of implementation of MiFID II into the AFS

Timing: MiFID II / MiFIR

MiFID II Academy - Product Governance - 12 April 2016

2018

3 January 2018MiFID II and MiFIR Level 1 and Level 2 implementation date (delayed from 2017)

3

Dutch transposition

MiFID II Academy - Product Governance - 12 April 2016

MiFID II implementation

• Article 93 MiFID II: Member States shall adopt and publish, by 3 July 2016, the laws, regulations and administrative provisions necessary to implement this Directive

• Consultation Ministry of Finance July 2015

– closed on 6 July 2015

– Lot of the detail will be implemented into the Decree on Conduct of Business Supervision of Financial Undertakings (Besluit Gedragstoezicht financiëleondernemingen Wft)

– All RTS/ITS will be regulations which will have direct effect into Dutch law

• How to keep informed:

– AFM MiFID review page - https://www.afm.nl/nl-nl/professionals/onderwerpen/mifid-ll

– http://www.regulationtomorrow.com/the-netherlands/

– http://www.nortonrosefulbright.com/knowledge/technical-resources/pegasus/norton-rose-fulbright-briefings-slides-and-webex-recordings/

– http://ec.europa.eu/finance/securities/isd/mifid2/index_en.htm

– http://www.esma.europa.eu/page/Markets-Financial-Instruments-Directive-MiFID-II

4

MiFID II Academy - Product Governance - 12 April 2016

Product governance

Product governance: source and scope

• Source of legislation:

– Recital 71 MiFID II;

– Article 16 (3) MiFID II, paragraphs 2-6;

– Article 24 (2) MiFID II;

– ESMA’s technical advice (19 December 2014), paragraph 2.7; and

– Delegated Directive adopted by the Commission on 7 April 2016, Chapter III (Product Governance Requirements)

– Currently applicable in the Netherlands: Article 32 of the Decree on Conduct of Business Supervision of Financial Undertakings (Besluit Gedragstoezicht financiële ondernemingen Wft);

• Applicable to all investment firms with establishment in the EEA (and its EEA branches) and to branches in the EEA of non-EEA entities, and UCITS managers and AIFMs when they offer investment services

• Applicable in relation to all types of clients (retail, professional and eligible counterparties)

• Applicable to all financial instruments, including structured deposits

MiFID II Academy - Product Governance - 12 April 20166

Product governance: general principles 1

• There are no existing detailed provisions regarding product governance or sales processes in MiFID I; only high-level organisational requirements in the MiFID I Implementing Directive

• Guidance under MiFID I:

– EC Commission Consultation Paper on the Review of MiFID - section 7.3.3 “Organisational requirements for the launch of products, operations and services”;

– ESA’s Joint Position on ‘Manufacturers’ Product Oversight and Governance Processes’ (November 2013);

– IOSCO (International Organisation of Securities Commissions) report ‘Regulation of retail structured products’ (December 2013); and

– ESMA opinion on ‘Structured Retail Products – Good practices for product governance arrangements’ (March 2014)

MiFID II Academy - Product Governance - 12 April 2016

Level 1

7

Product governance: general principles 2

• MiFID II introduces a completely new EU-wide product governance regime which applies to both sides of the product development and sales process, namely to (if different):

– product manufacturers: investment firms that create, develop, issue and/or design investment products, including investment firms advising corporate issuers on the launch of new securities

– product distributors: investment firms that offers and/or recommends investment products and services

MiFID II Academy - Product Governance - 12 April 2016

Level 1

8

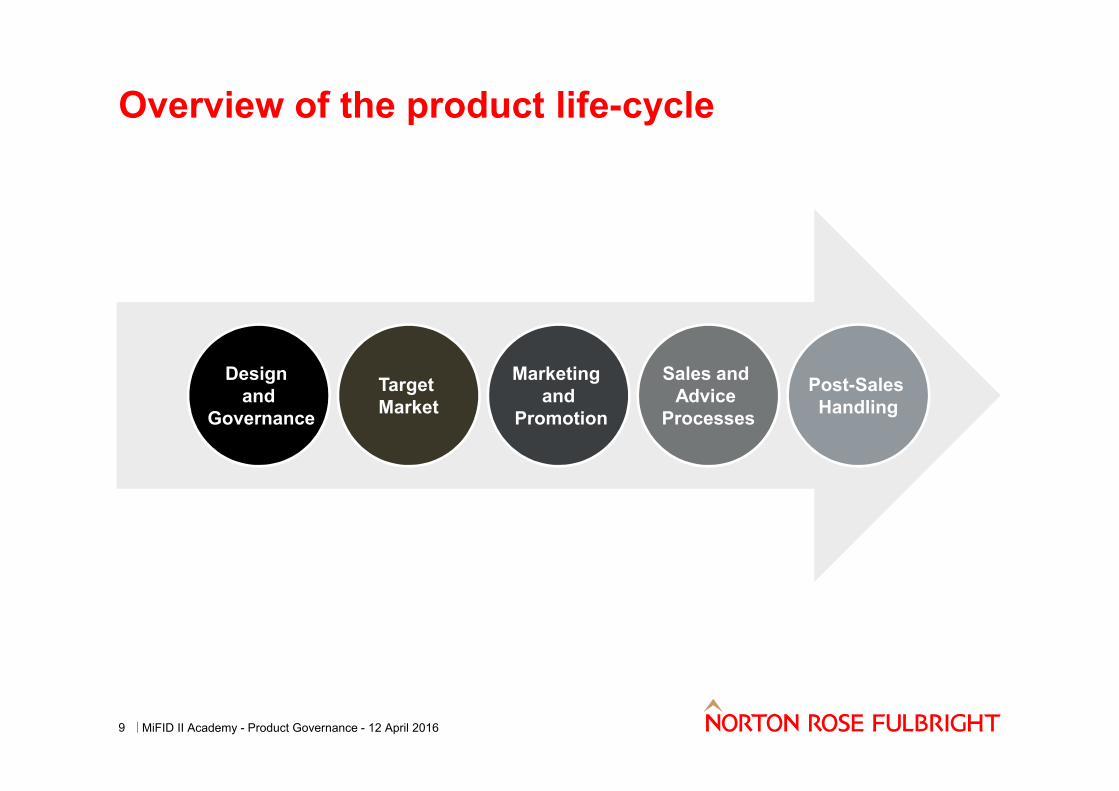

Overview of the product life-cycle

Design and

Governance

Target Market

Marketing and

Promotion

Sales and Advice

Processes

Post-Sales Handling

MiFID II Academy - Product Governance - 12 April 20169

Product governance: general principles 3

– introduction of a product approval process, including appropriate policies and procedures to ensure that the product or service complies with all applicable rules including those relating to disclosure, suitability / appropriateness, inducements and proper management of conflicts of interest (including remuneration);

– the product approval process needs to be undertaken for each financial instrument and significant adaptations of existing financial instruments before marketing or distribution;

– requirement to identify the target market for a product or service;

– requirement for products to only be manufactured where they meet the needs of this target market;

– requirements for all risks related to the target market to be assessed;

MiFID II Academy - Product Governance - 12 April 2016

Level 1

10

Product governance: general principles 4

– ensure the intended distribution strategy is consistent with the identified target market;

– requirement for firms to understand the features of the product or service being sold;

– requirement for the manufacturers of products to ensure the product or service reaches the target market;

– periodically review the product, the target market and the distribution channel to ensure they all remain appropriate;

– requirements on distributors / sales intermediaries to understand the product approval process, the target market and the features of the product or service; and

– ensuring that the management body or a corresponding governing body has effective control over the aspects mentioned above

MiFID II Academy - Product Governance - 12 April 2016

Level 1

11

Product governance: general principles 5

– when an investment firm acts both as manufacturer and distribution of investments products, it should be required to comply with all relevant obligations for both manufacturers and distributors – if that is the same legal entity, only one single product governance process is needed;

– introduction of specific oversight, control and governance obligations on investment firms that manufacturer financial instruments and on investment firms that distribute such products;

– final distributor in a distribution chain has the obligation to comply with the distributor requirements, but the intermediate distributors will also have certain obligations:

1. ensure the relevant product information is passed down the chain;

2. enable the manufacturer to obtain information on product sales through the chain; and

3. apply the product governance obligations for manufacturers to the service they provide

MiFID II Academy - Product Governance - 12 April 2016

Level 2 (Final)

12

Product governance: general principles 6

MiFID II Academy - Product Governance - 12 April 2016

Level 2 (Final)

13

– obligations apply in an appropriate and proportionate manner, taking into account the nature of the investment product, the investment service and the target market for the product;

– that one criterion to consider in developing a product is the threat it may represent to the orderly functioning or the stability of financial markets;

– some additional potential steps that may be appropriate for manufacturers to take when an event affecting the potential risk / return expectations of a product occurs (i.e. terminating distributor relationships, or liaising with the distributor to modify the distribution process, and informing the relevant national competent authority); and

– oversight by compliance over the product development / governance process

Product governance: general principles 7

MiFID II Academy - Product Governance - 12 April 2016

Level 2 (Final)

14

Manufacturers

procedures and arrangements to manage conflicts of interest in design, creation and development process (including remuneration); analysis each time a financial instrument is manufactured

governance processes for effective oversight and control over design, creation, issuance and development process, including expertise staff and compliance involvement

assessment of target market of each financial instrument – characteristics, needs, objectives of type(s) of end client(s)

assessment of risks posed by products and the circumstances that may cause these to occur, including scenario analysis

impact of charging structure on target market considered

provision of adequate information to distributors so they can understand and sell properly

regular review of the products:

− ensure the product remains consistent with the needs of the target market

− ensure the distribution strategy remains appropriate

− consider any event that could materially affect the risk to the target market

positive obligation to check that products function as intended (rather than waiting for detriment to occur), namely:

− Firms to review all investment products prior to any re-launch or re-issue

− Firms to review investment products when aware of an event which could materially affect the potential risk to investors

− Firms to review investment products at regular intervals

Distributors

determine target market of the financial instrument for its clients

product governance processes to ensure that products and services the firms intend to offer are compatible with characteristics, objectives and needs of the identified target market, and take into account other applicable MiFID conduct of business and organisational requirements

periodic review of product governance arrangements (robust, and fit for purpose)

provision of sales information to manufacturers, to assist manufacturers in meeting their post-sale product governance responsibilities

involvement of compliance function in development and periodic review of product governance arrangements to detect any risk of failure by distributors

endorsement of the management (or similar) body of the range of products / services offered and respective target markets

provision of information to senior management in compliance function’s periodic reports to management body

with third-country manufacturers, ensure the level of product information obtained is of a reliable and adequate standard to ensure that products will be distributed in accordance with the characteristics, objectives and needs of the target market

Information to clients

MiFID II Academy - Product Governance - 12 April 201615

• Information provided to clients should be:

– fair, clear and not misleading; and

– marketing communications must be clearly identifiable as such

• Appropriate information in good time regarding:

– investment firm/services; and

– financial instruments/investment strategies/execution venues; and

– costs and related charges

• Information provision must be:

– in comprehensible form; and

– in such manner that clients can make informed investment decision

• The information may be standardised

Distributor remuneration (inducements)

MiFID II Academy - Product Governance - 12 April 201616

• When marketing and promoting products, inducement rules need to be taken into account:

– ban on independent advisers and portfolio managers receiving and retaining payments from third parties – these payments / benefits can be received but they must be passed on in full to clients as soon as possible following receipt;

– minor non-monetary benefits are excluded from the prohibition but they must not impair a firm’s duty to act in the best interests of its clients, must be capable of enhancing the quality of client service and must be disclosed (should be read strictly and interpreted narrowly) - EC to adopt an exhaustive list of what constitutes a minor non-monetary benefit to prevent regulatory arbitrage amongst Member States;

– firms not providing independent investment advice or portfolio management must comply with the existing inducement rules from MiFID I for all types of third party payments;

– clients need to be accurately and, where relevant, periodically informed about all the fees, commissions and benefits the firm has received in connection with the investment services provided; and

– where applicable, firms must inform clients on how the fee / commission / non-monetary benefit can be transferred to them – and portfolio managers and independent advisers should have a policy for this

Suitability and appropriateness

MiFID II Academy - Product Governance - 12 April 201617

• Firms must obtain the following information from a client or a potential client before providing the above services:

o its knowledge and experience of the investment field in which the investment advice or portfolio management is to be offered;

o its financial situation including his ability to bear losses; ando its investment objectives including the risk tolerance

• Obligation to take reasonable steps to ensure that investment advice and decisions to trade (incl. to buy or to hold) are suitable

• Obligation also applicable to a package of services or bundled products and structured deposits

• Firms must obtain information regarding clients’ experience and knowledge in order to enable it to determine if the products and services envisaged are appropriate:

o the types of financial service, transaction and regulated financial instruments the client is familiar with;

o the nature, volume and frequency of the client’s transactions in regulated financial instruments; and

o the level of education, profession or former profession of the client

• Obligation also applicable to a package of services or bundled products and structured deposits

• Firms may assume that the appropriateness test is satisfied if dealing with professional clients, and not applicable to ECPs

Complaints handling

MiFID II Academy - Product Governance - 12 April 201618

• MiFID introduced high level requirements in relation to the organisation of firms and the handling of complaints raised by retail clients, their record-keeping and resolution – MiFID II continues this regime

• ESMA’s summer 2014 consultation proposed to significantly extend the requirements in relation to complaints handling and its technical advice confirms this. The measures contain strict but high-level requirements (similar to the complaints handling guidelines developed by ESMA / EBAfor the banking industry), including:

– a written complaints procedure for handling complaints;

– the ability for clients to be able to make a complaint without charge;

– communication requirements with client (i.e. in plain language);

– responding without unnecessary delay;

– providing the firm’s response to a complaint, and requiring firms to explain the client’s options and (where relevant) that they may be able to refer the complaint to an Alternative Dispute Resolution entity or take civil action;

– complaint data reporting requirements to a firm’s regulator; and

– meaningful analysis of complaints data by compliance to identify issues

Complaints handling

MiFID II Academy - Product Governance - 12 April 201619

• Complaints handling guidelines apply to both retail and professional clients (both per se and elective professional clients)

• Complaints handling guidelines apply to potential clients as well as clients

Post-sales handling: Other topics

20

Product governance

requirements for the periodic review of products, their target market and the distribution

strategy

Positive obligations to

review products on a regular basis,

including at re-launch or re-issue

and where particular risks are

identified

Management information:

product governance issues

to be covered in periodic

compliance reports

Reporting to clients – in

particular ex-post disclosure on

costs and charges

Relevant information flows

between manufacturers and

intermediaries

MiFID II Academy - Product Governance - 12 April 2016

MiFID II Academy - Product Governance - 12 April 2016

QuestionsT +31 20 4629 426 | [email protected]

DisclaimerNorton Rose Fulbright US LLP, Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP and Norton Rose Fulbright South Africa Inc are separate legal entities and all of them are members of Norton Rose Fulbright Verein, a Swiss verein. Norton Rose Fulbright Verein helps coordinate the activities of the members but does not itself provide legal services to clients.

References to ‘Norton Rose Fulbright’, ‘the law firm’ and ‘legal practice’ are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together ‘Norton Rose Fulbright entity/entities’). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a ‘partner’) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity.

The purpose of this communication is to provide general information of a legal nature. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright.

MiFID II Academy - Product Governance - 12 April 201623