Middle East: Does it need more greenfield refineries? · Trusted commercial intelligence...

26

woodmac.com Trusted commercial intelligence Johnny Stewart, September 18th Middle East: Does it need more greenfield refineries? Abu Dhabi International Downstream Summit

Transcript of Middle East: Does it need more greenfield refineries? · Trusted commercial intelligence...

woodmac.comTrusted commercial intelligence

Johnny Stewart, September 18th

Middle East: Does it need more greenfield refineries?

Abu Dhabi International Downstream Summit

Over the last 40 years, Wood Mackenzie has evolved

naturally along the energy value chain to capture all

the key components affecting global markets.

Our integrated approach allows us

to spot trends and forecast future

dynamics before anyone else

Upstream

Oil & Gas

Energy

Markets

Gas

Power

Refining &

Oil Products

LNG

NGL Chemicals

Macro

Economics

Metals & Mining

1973 2015

Helping risk-bearing businesses understand and manage their risk

Wood Mackenzie joined the Verisk family in June 2015,

forming a strategic alliance between two industry leaders.

Through partnerships with other Verisk businesses, such as

Verisk Maplecroft, we deliver an unrivalled commercial

intelligence portfolio for the world’s natural resource markets,

helping clients make complete risk-adjusted decisions that

will strengthen their operations.

woodmac.com 4

Agenda

1 Global refined product demand growth is to slow

2 Understanding greenfield refinery projects – A focus on the Middle East

3 Are recent projects sustainable?

4 Are joint ventures a better approach?

5 Conclusions

woodmac.com 5

Global oil demand growth rate to half over the next twenty years

-

2

4

6

8

10

12

14

2017 2019 2021 2023 2025 2027 2029 2031 2033 2035

millio

n b

/d

Transport other petchem ethane Other

Source: Wood Mackenzie

Global oil demand Cumulative growth in global oil demand

75

80

85

90

95

100

105

110

115

120

2000 2005 2010 2015 2020 2025 2030 2035

millio

n b

/d

H1 2017 forecast 2000-16

H2 2016 Linear (2000-16)

Source: Wood Mackenzie

Average annual growth

2000-16: 1.2 mbd, 1.4%

2016-35: 0.6 mbd, 0.6%

50%

10%

Growth

2016-35

Oil demand into transportation stable from 2030; oil feedstock into petrochemical

accounts for more than half of total oil demand growth to 2035

woodmac.com 6

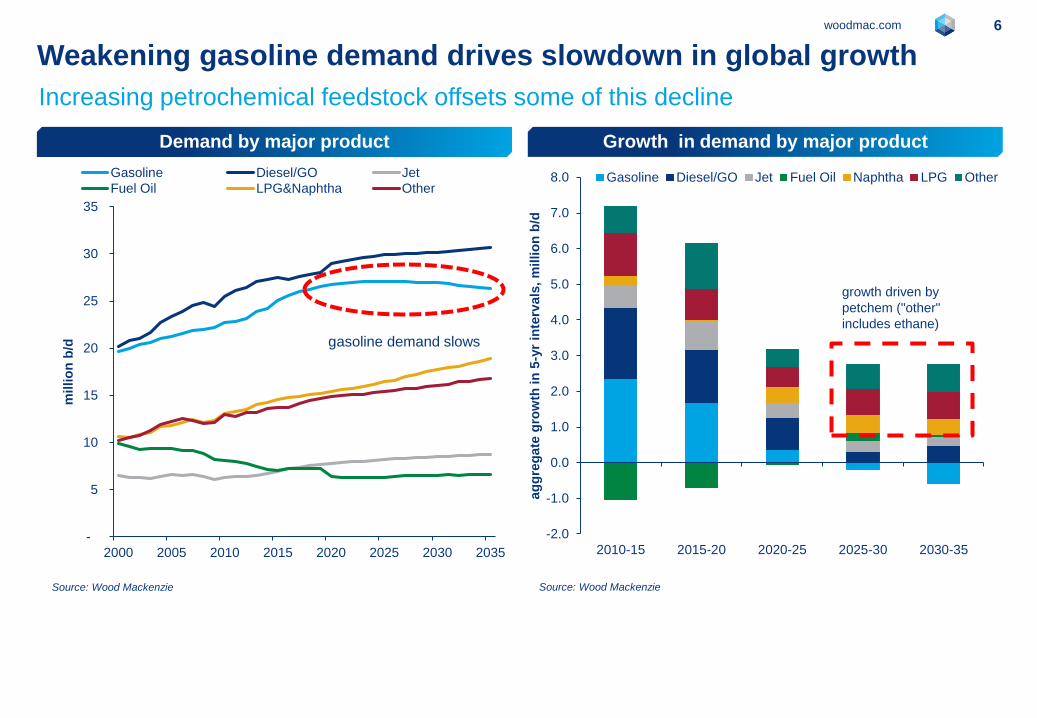

Weakening gasoline demand drives slowdown in global growth

Demand by major product Growth in demand by major product

-

5

10

15

20

25

30

35

2000 2005 2010 2015 2020 2025 2030 2035

millio

n b

/d

Gasoline Diesel/GO Jet

Fuel Oil LPG&Naphtha Other

Source: Wood Mackenzie

gasoline demand slows

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2010-15 2015-20 2020-25 2025-30 2030-35ag

gre

gate

gro

wth

in

5-y

r in

terv

als

, m

illio

n b

/d

Gasoline Diesel/GO Jet Fuel Oil Naphtha LPG Other

Source: Wood Mackenzie

growth driven by

petchem ("other"

includes ethane)

Increasing petrochemical feedstock offsets some of this decline

woodmac.com 7

Global refining supply potential runs ahead of demand through 2022

Source: Wood Mackenzie

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2017 2018 2019 2020 2021 2022

New Capacity Non-refinery Supply Growth Demand Growth

Annual Refinery Capacity and Non-Refinery Supply versus Demand Growth, 2017-2022, kb/d

Greenfield refineries have to compete in an overcrowded marketplace

woodmac.com 8

Agenda

1 Global refined product demand growth is to slow

2 Understanding greenfield refinery projects – A focus on the Middle East

3 Are recent projects sustainable?

4 Are joint ventures a better approach?

5 Conclusions

woodmac.com 9

Middle East product exports will continue to grow

Growth is driven by greenfield projects and upgrading investments at brownfield sites

Middle East All-Supply Demand Balances, kb/d

-1,000

0

1,000

2,000

3,000

4,000

5,000

2000 2005 2010 2015 2020 2025 2030 2035

Bala

nces (

kb/d

)

LPG Naphtha Gasoline Jet/Kerosene Diesel/Gasoil Fuel Oil

Source: Wood Mackenzie

Deficit

Surplus

woodmac.com 10

The Middle East is adding over 2 Mb/d of capacity between 2016 and 2022

Shuaiba closure, April ‘17, reduced regional capacity by 200 kb/d

Greenfield capacity additions & closures Brownfield refinery investments

Persian Gulf, Iran360 kb/d, Jan 2017-Mar 2018

Ruwais, UAE417 kb/d,April 2015

Laffan, Qatar146 kb/d,January 2017

Yanbu YASREF, Saudi Arabia400 kb/d,January 2015

Shuaiba, Kuwait-200 kb/d,April 2017

Karbala, Iraq140 kb/d,January 2021

Jazan, Saudi Arabia400 kb/d,January 2019

SIRAF, Iran360 kb/d,Jan 2021-Jan 2022

SOHAR, Oman80 kb/d,June 2017

Clean Fuels, Kuwait64 kb/d,January 2020

Al-Zour, Kuwait615 kb/d,June 2020

Bahrain, Bahrain93 kb/d,January 2021

Bandar Abbas, IranGasoline IncrementJune 2017

Riyadh, Saudi ArabiaClean FuelsJune 2017

Ras Tanura, Saudi ArabiaClean FuelsApril 2020

Abadan, IranNew refinery trainJanuary 2021

Laffan, QatarGasoline projectJanuary 2018

Ruwais, UAECarbon BlackJanuary 2017

Jebel Ali, UAERefinery UpgradeJanuary 2021

Bazian, Iraq50 kb/d,June 2020

Source: Wood Mackenzie

Dukan, Iraq20 kb/d,June 2017

woodmac.com 11

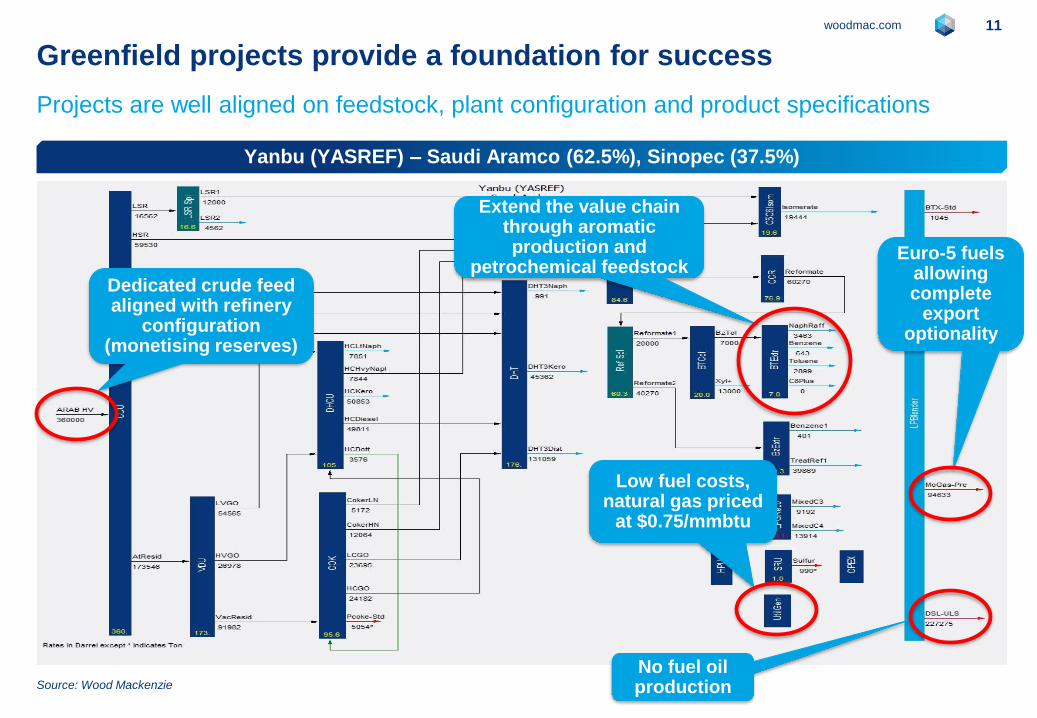

Greenfield projects provide a foundation for success

Projects are well aligned on feedstock, plant configuration and product specifications

Yanbu (YASREF) – Saudi Aramco (62.5%), Sinopec (37.5%)

Source: Wood Mackenzie

Dedicated crude feed aligned with refinery

configuration(monetising reserves)

Low fuel costs, natural gas priced

at $0.75/mmbtu

Euro-5 fuels allowing complete

export optionality

No fuel oil production

Extend the value chain through aromatic production and

petrochemical feedstock

woodmac.com 12

Projects are commercially attractive, supporting other industries

Siraf funded by South Korean and Japanese companies securing petrochemical feedstock

Siraf condensate park, Iran, 60 kb/d modular refinery

Source: Wood Mackenzie

Dedicated crude feed aligned with

refinery configuration

Yield orientated towards demand

growth products with dependable outlets

Minimal fuel oil production

woodmac.com 13

Agenda

1 Global refined product demand growth is to slow

2 Understanding greenfield refinery projects – A focus on the Middle East

3 Are recent projects sustainable?

4 Are joint ventures a better approach?

5 Conclusions

woodmac.com 14

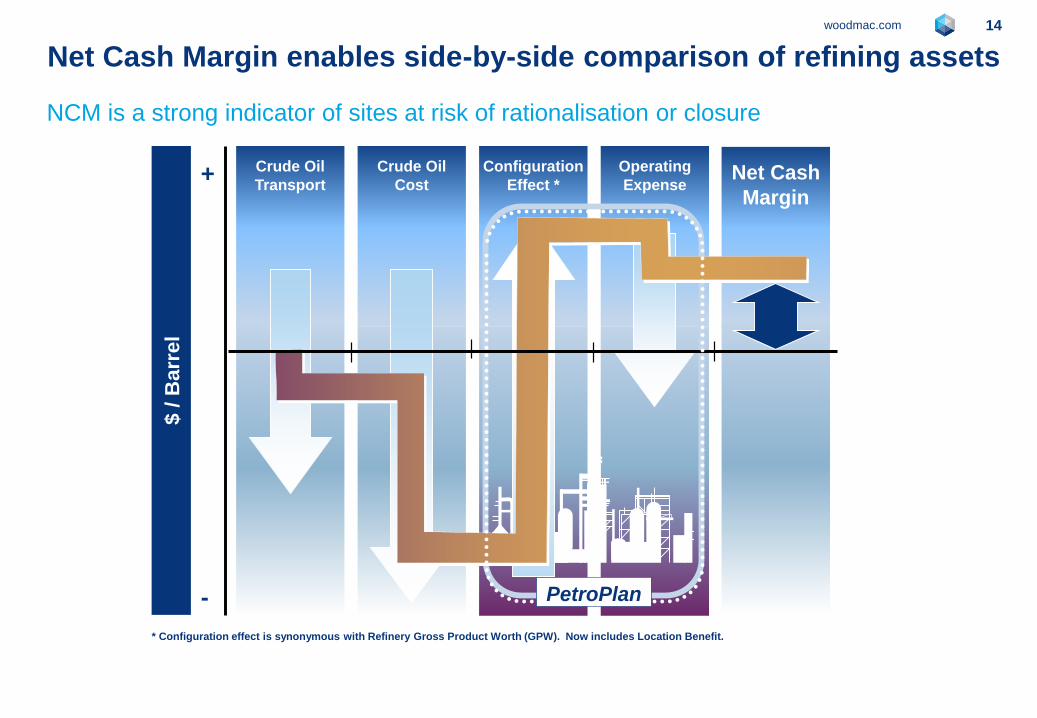

Net Cash Margin enables side-by-side comparison of refining assets

NCM is a strong indicator of sites at risk of rationalisation or closure

Johnny

Net Cash

Margin

Operating

Expense

Configuration

Effect *

Crude Oil

Cost

Crude Oil

Transport$ / B

arr

el

+

- PetroPlan

* Configuration effect is synonymous with Refinery Gross Product Worth (GPW). Now includes Location Benefit.

woodmac.com 15

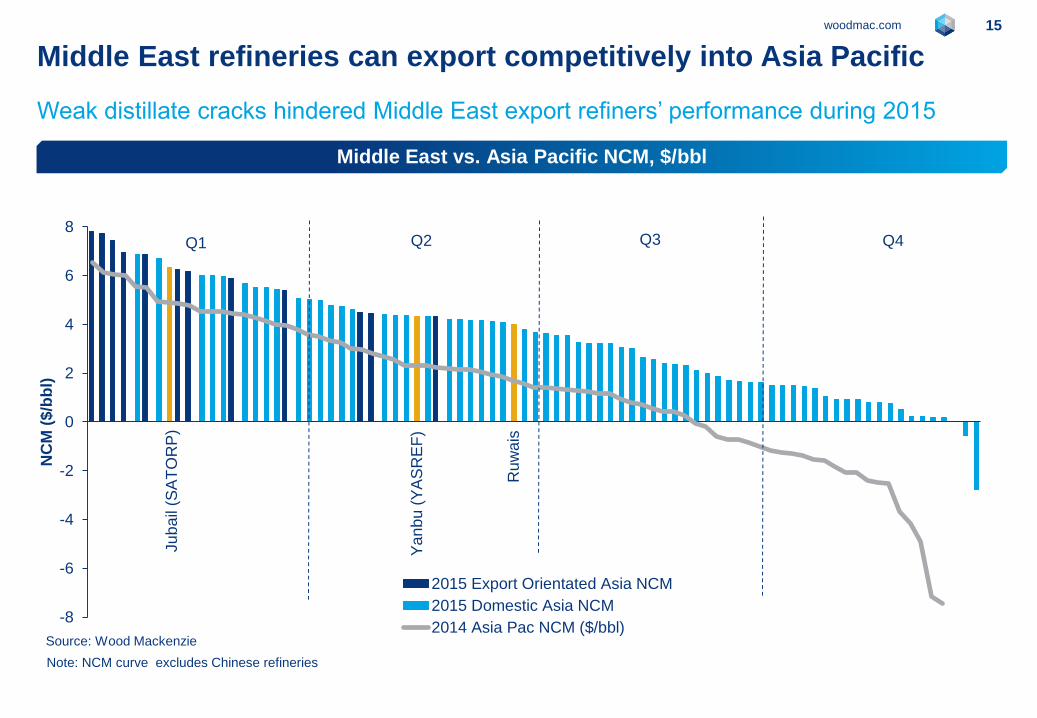

Middle East refineries can export competitively into Asia Pacific

Weak distillate cracks hindered Middle East export refiners’ performance during 2015

Note: NCM curve excludes Chinese refineries

-8

-6

-4

-2

0

2

4

6

8

NC

M (

$/b

bl)

2015 Export Orientated Asia NCM

2015 Domestic Asia NCM

2014 Asia Pac NCM ($/bbl)Source: Wood Mackenzie

Ju

ba

il(S

AT

OR

P)

Ya

nb

u (

YA

SR

EF

)

Ru

wa

is

Q1 Q2 Q3 Q4

Middle East vs. Asia Pacific NCM, $/bbl

woodmac.com 16

Participation in each part of the supply chain reduces value leakage

and ensures the best return for each barrelME producers now refine, manufacture petrochemicals, ship, market and trade

Value extends from produced barrel to end-consumer

Produce Refine Ship-to-market Trade

Focus on competitive assets integrated with chemicals

Efficient logistics is key Provides optionality, but has implications on refining and shipping

Source: Wood Mackenzie

woodmac.com 17

Agenda

1 Global refined product demand growth is to slow

2 Understanding greenfield refinery projects – A focus on the Middle East

3 Are recent projects sustainable?

4 Are joint ventures a better approach?

5 Conclusions

woodmac.com 18

Disadvantages of joint-venture partnerships

• Integration of culture and management styles

• Conflicts of interest can restrict flexibility

• Imbalance of expertise, assets, investment

• Exit opportunities can prove difficult

• Governance structure and commercial incentives

• Loss of knowledge/intellectual property from key

provider

Benefits of joint-venture partnerships

• Faster development of projects

• Learning and development opportunities

• Knowledge transfer

• Access to stable crude supply

• Access to marketing/products offtake

• Improved integration between sites

• Commercial focus

• Access to finance, technology, expertise

• Shared risk

• Ability to capture value of speciality products

Joint-venture partnerships bring many benefits to both parties

Disadvantages can be overcome with clear communication from the outset

woodmac.com 19

Trusted commercial intelligencewww.woodmac.com

19

The Middle East will continue building greenfield refining capacity

Global demand is slowing and will be outpaced by supply contributions

Middle East will continue building greenfield refining capacity and increase product

exports

Well-configured refineries provide a platform for success but effective participation

through the value chain is vital

The Middle East has a number of factors supporting in-region construction

Joint-venture partnerships typically bring many benefits with limited near term downside

This content is available to purchase. Your company can opt to

subscribe to this content on a global or regional basis.

This content is available to purchase. Your company can opt to

subscribe to this content on a global or regional basis.

This content is available for your company to purchase on a

subscription basis.

woodmac.com 24

Johnny Stewart

Principle Analyst EMEARC

Biography Connect with Johnny

Johnny Stewart is a core member of Wood Mackenzie’s Downstream, Midstream

and Chemicals Research team and is responsible for developing and delivering

research content to clients.

Johnny has worked in Wood Mackenzie’s research division for eight years and is

responsible for analysing refinery supply, infrastructure and investments across

the Middle East, Europe and Africa.

Johnny compiles Wood Mackenzie’s long and short term view on all products

supply/demand balances in the Middle East and is responsible for individual

refinery asset benchmarking and analysis in the region.

Prior to joining Wood Mackenzie’s Downstream, Midstream and Chemicals

Research team, Johnny achieved an Honours Degree in Mechanical Engineering

with Management from The University of Edinburgh, Scotland. +971 56 814 4090

+971 4 376 5361

woodmac.com 25

Disclaimer

Strictly Private & Confidential

This report has been prepared for Abu Dhabi International Downstream Summit by

Wood Mackenzie Limited. The report is intended solely for the benefit of attendees and

its contents and conclusions are confidential and may not be disclosed to any other

persons or companies without Wood Mackenzie’s prior written permission.

The information upon which this report is based has either been supplied to us or comes

from our own experience, knowledge and databases. The opinions expressed in this

report are those of Wood Mackenzie. They have been arrived at following careful

consideration and enquiry but we do not guarantee their fairness, completeness or

accuracy. The opinions, as of this date, are subject to change. We do not accept any

liability for your reliance upon them.

Wood Mackenzie™, a Verisk Analytics business, is a trusted source of commercial intelligence for the world's

natural resources sector. We empower clients to make better strategic decisions, providing objective analysis

and advice on assets, companies and markets. For more information visit: www.woodmac.com

WOOD MACKENZIE is a trade mark of Wood Mackenzie Limited and is the subject of trade mark registrations

and/or applications in the European Community, the USA and other countries around the world.

Europe

Americas

Asia Pacific

Website

+44 131 243 4400

+1 713 470 1600

+65 6518 0800

www.woodmac.com