The transport geography of logistics and freight distribution

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast

RDA Priorities 2015-2016

RDA name Regional Development Australia Mid North Coast

Project Name Mid North Coast Freight and Distribution Study

RDA Project Priority 1

Document Title: Mid North Coast Freight and Distribution Study

Prepared For: NSW Department of Industry | Regional Development

Prepared By: Regional Development Australia Mid North Coast

This document is the joint intellectual property of RDA Mid North Coast & NSW Department of Industry, allowing

dissemination to other organisations as appropriate. The project methodology used to develop the document remains the

Intellectual Property of RDA Mid North Coast. You may reproduce and publish this document in whole or in part for you and

your organisation’s own personal, educational or non-commercial purposes. You must not reproduce or publish this

document for commercial gain without the prior written consent of RDA Mid North Coast or NSW Department of Industry.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast

Mid North Coast Freight and Distribution Study

Contents Executive Summary ............................................................................................................................... 1

1. Introduction ................................................................................................................................ 1

1.1 Study purpose and objectives ...................................................................................................... 5

1.2 The Study Area ............................................................................................................................ 6

1.3 Structure of this report ................................................................................................................. 7

Section 2 – Definitions and Sustainability Criteria ............................................................................. 8

2.1 Intermodal Terminal ..................................................................................................................... 8

2.2 Road Freight Hubs ..................................................................................................................... 10

2.3 Highway Service Centres .......................................................................................................... 11

Section 3 – The Current and Forecast Freight Task ......................................................................... 12

3.1 Overview of the Freight Task on the Mid North Coast ............................................................... 12

3.2 Outbound Freight ....................................................................................................................... 14

3.3 Inbound Freight ......................................................................................................................... 16

3.4 Forecast Freight Growth ............................................................................................................ 18

3.4.1 Forecast Outbound Freight (2031) ............................................................................................. 18

3.4.2 Forecast Inbound Freight (2031) ............................................................................................... 18

Section 4 – Road or Rail? ................................................................................................................... 20

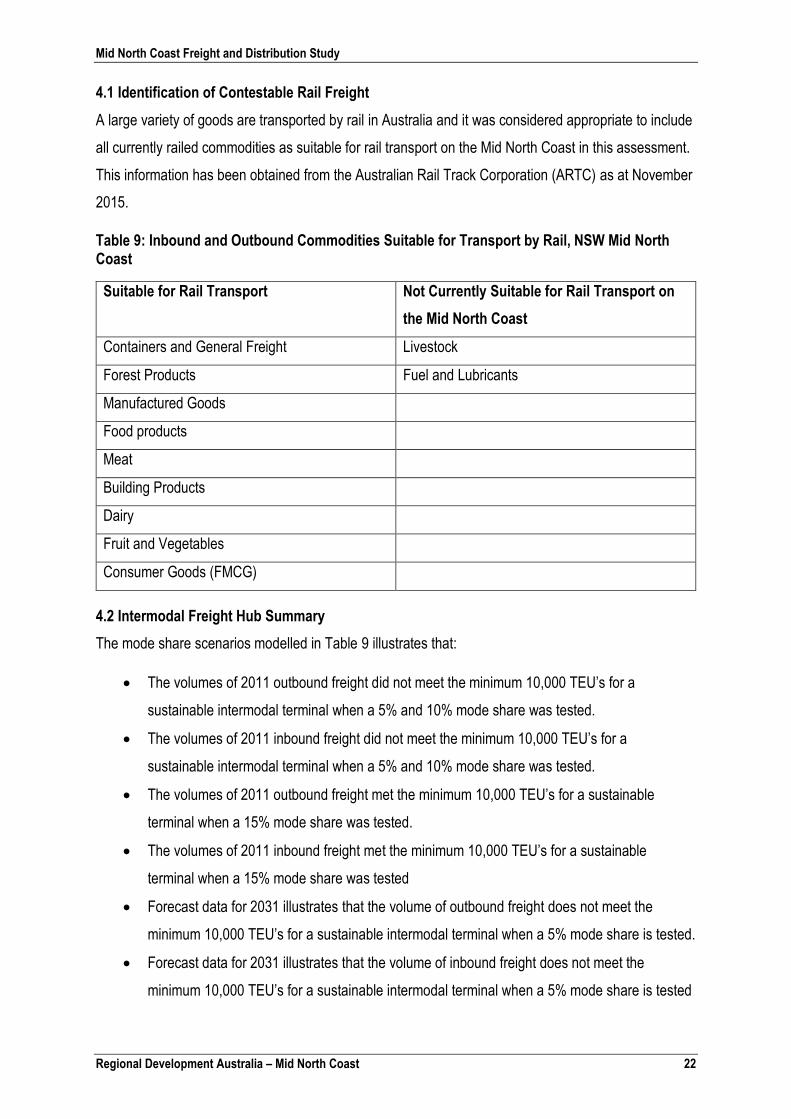

4.1 Identification of Contestable Rail Freight ................................................................................... 22

4.2 Intermodal Freight Hub Summary .............................................................................................. 22

Section 5 - The Road Network ............................................................................................................ 26

5.1 The Existing Road Network ....................................................................................................... 26

5.2 Proposed Freight Transport Infrastructure ................................................................................. 27

5.3 Viability of a Regional Freight Transport Hub ............................................................................ 28

Section 6: The Rail Network ............................................................................................................... 32

6.1 The Existing Rail Network .......................................................................................................... 32

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast

6.2 Proposed Rail Freight Transport Infrastructure .......................................................................... 35

6.3 The viability of a regional intermodal Terminal in the study area ............................................... 37

Section 7 - How a Freight Transport Hub Aligns with Government Strategies .............................. 41

Conclusion ........................................................................................................................................... 44

List of Tables

Table 1: Population by Local Government Area ...................................................................................... 6

Table 2: The top 5 commodities making up the outbound freight task - Mid North Coast (2011) ........... 14

Table 3: The top 5 commodities making up the inbound freight task - Mid North Coast (2011) ............. 16

Table 4: Forecast Outbound Freight Volumes by Commodity Category, Mid North Coast, 2031 .......... 18

Table 5: Forecast Inbound Freight Volumes by Commodity Category, Mid North Coast, 2031 ............. 18

Table 6: Outbound Freight Volumes by Local Government Area (LGA) ................................................ 19

Table 7: Inbound Freight Volumes by Local Government Area (LGA) ................................................... 19

Table 8: Rail Freight Mode Share by Commodity Category in NSW – excluding coal ........................... 20

Table 9: Inbound and Outbound Commodities Suitable for Transport by Rail, NSW Mid North Coast .. 22

Table 10: Evaluating Contestability Mid North Coast ............................................................................. 24

Table 11: Distance to Major Centres ..................................................................................................... 26

Table 12: Proposed Transport Infrastructure on the Mid North Coast ................................................... 27

Table 13: Mid North Coast Population Forecast .................................................................................... 28

Table 14: Existing Rail Infrastructure, NSW Mid North Coast ................................................................ 32

Table 15: Intermodal Terminals in Northern NSW ................................................................................. 34

Table 16: Evaluating Contestability - Summary ..................................................................................... 37

List of Figures

Figure 1: The Study Area: Mid North Coast of NSW ................................................................................ 6

Figure 2: Transport Logistics Options ...................................................................................................... 8

Figure 3: Intermodal Terminal Viability Checklist ..................................................................................... 9

Figure 4: Freight Hub Requirements for Geographical Advantage ........................................................ 10

Figure 5: National Rail and Highway Network ....................................................................................... 26

Figure 6: Australian Rail Track Corporation: North South Corridor Network Diagram, Rev 7 Jun 15 .... 33

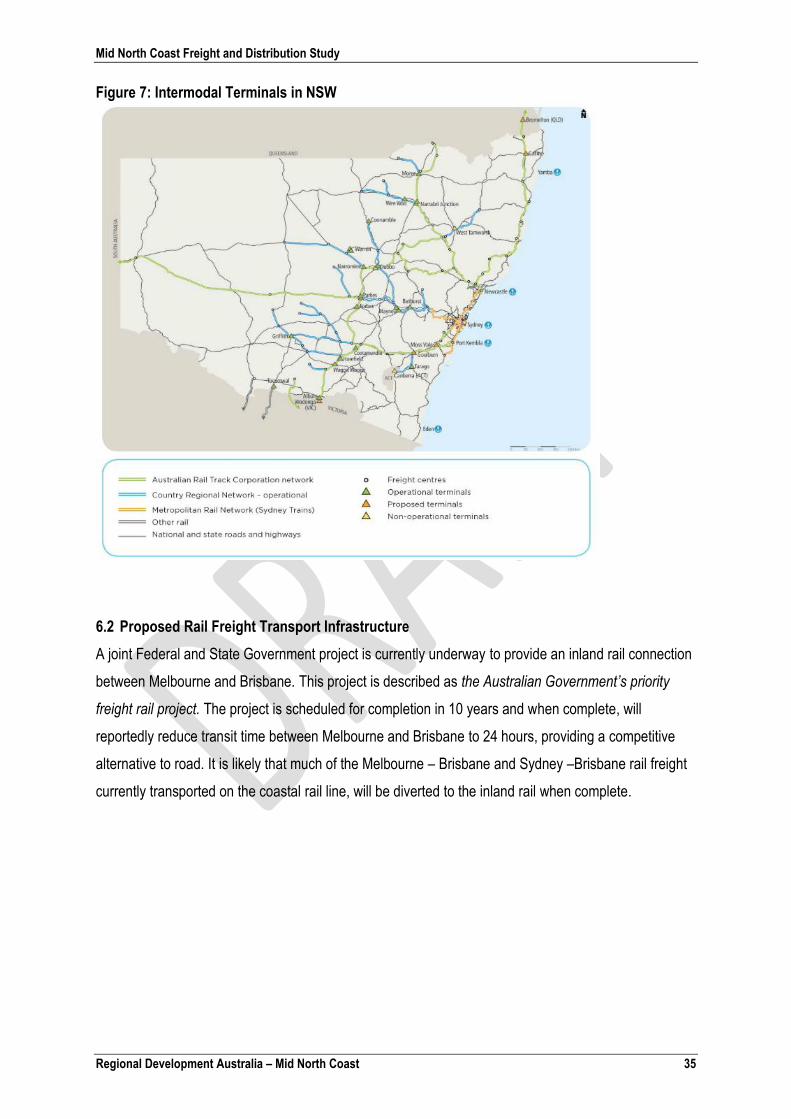

Figure 7: Intermodal Terminals in NSW ................................................................................................. 35

Figure 8: Melbourne - Brisbane Inland Rail Alignment ........................................................................... 36

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 1

Executive Summary

The purpose of this study was to identify the current and forecast freight task on the Mid North Coast of

NSW and determine if there are sufficient volumes of freight to establish viable freight transport

infrastructure, such as intermodal terminal(s) or road freight hub(s) in the study area.

The study area is located on the Mid North Coast of NSW and comprises the local government areas of

Coffs Harbour, Bellingen, Nambucca, Kempsey, Port Macquarie-Hastings and Greater Taree.

An intermodal terminal is a strategic location between a freight service user or exporter / importer and a

destination. It offers a customer road and rail transport access, and short-term storage. A freight hub is

a place where cargo is exchanged between vehicles or transport modes and may be a cluster of

logistics operators and light manufacturing industries.

Data obtained from the Bureau of Freight Statistics, Strategic Freight Model (2011) reported that the

study area generated 1,972,000 tonnes of outbound freight and 2,518,000 of inbound freight in 2011.

The highest volumes of outbound freight were generated by:

1. Forest products

2. Dairy Products

3. Meat

4. Containers and General Freight

5. Food Products

The highest volumes of inbound freight were generated by:

1. Fuel and Lubricants

2. Consumer Goods

3. Food Products

4. Building Products

5. Containers and General Freight

The Mid North Coast freight task was characterised by a dispersed market. Both inbound and outbound

freight had dispersed origins and destinations. The outbound freight task produced few commodities

with a significant volume of direct, single origin – destination freight.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 2

Outbound Freight

The biggest outbound freight volume was generated by forest products, with Newcastle Port

the key destination for this commodity.

Significant volumes of outbound freight were generated by Containers and General Freight,

with Queensland being the key destination.

Significant volumes of outbound freight were generated by Food Products, with Victoria being

the key destination.

Inbound Freight

The biggest inbound freight task was generated by Fuel and Lubricants with Newcastle being

the key origin.

Significant volumes of inbound freight were generated by Consumer goods, with Newcastle

being the key origin.

Significant volumes of inbound freight were generated by Food Products with QLD being the

key origin.

Significant volumes of inbound freight were generated by Containers and General Freight with

Queensland being the key origin.

Transport for NSW reported a forecast annualised growth rate of 2.44% for outbound freight and 2.99%

for inbound freight. This equates to a 58% increase in outbound freight and a 75% increase in inbound

freight between 2011 and 2031. The forecast annualised population growth rate was much lower at

0.75% or 15% between 2011 and 2031; thus it can be assumed the forecast growth of outbound freight

will need to be largely driven by inter-regional and international trade servicing demand.

Intermodal Freight Hub Viability Assessment

The intermodal freight hub viability assessment concludes that:

The volumes of 2011 inbound and outbound freight did not meet the minimum 10,000 Twenty-

Foot Equivalent Unit (TEU’s) for a sustainable intermodal terminal when a 5% and 10% mode

share was tested.

The volumes of 2011 inbound and outbound freight met the minimum 10,000 TEU’s for a

sustainable terminal when a 15% mode share was tested.

Forecast data for 2031 illustrated the overall volume of both inbound and outbound freight did

not meet the minimum 10,000 TEU’s for a sustainable intermodal terminal when a 5% mode

share was tested.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 3

Forecast data for 2031 illustrated the overall volume of both inbound and outbound freight

does meet the minimum 10,000 TEU’s for a sustainable intermodal terminal when a 10% and

15% mode share was tested.

The outbound freight task on the Mid North Coast comprised 50% Forest products (2011

data). Transport for NSW (2015) advised that Forest Products can be considered highly

variable as production can stop, start or shift in focus quickly. Given the uncertainty of

production, shippers were often reluctant to fund long term investments in their supply chain.

The variable nature of such a large portion of the Mid North Coast outbound freight task

represented a significant risk to the development of an intermodal freight terminal, based on

this commodity. It was considered this represented a significant limiting factor to the

establishment of an intermodal terminal in the study area.

Road Freight Hub Viability Assessment

The road freight hub viability assessment concluded that:

Three industrial land developments are proposed on the Pacific Highway in the Nambucca,

Port Macquarie - Hastings and Taree LGA’s. These locations were identified as suitable for

development as road freight hubs and were well placed to proceed in a timely fashion.

Existing investment ready industrial land adjacent to the Highway Service Centre in Kempsey

was identified as suitable for development as a road freight hub.

Proposed industrial land in the North Boambee Valley, adjacent to the Pacific Highway bypass

of Coffs Harbour (2018/19 commencement), was identified as suitable for development as a

road freight hub.

Lots in the abovementioned developments were of sufficient size, at all locations, to

accommodate road transport firms.

Services are currently at differing stages of provision, however all services would be available

upon occupation of the abovementioned developments.

Existing businesses adjacent to the Port Macquarie-Hastings LGA proposal (manufacturing)

and the Kempsey LGA development (Highway Service Centre) may assist in attracting future

tenants.

Commercial expressions of interest have been received for the proposal in the Taree LGA and

the Nambucca LGA. A local transport and logistics company has purchased land adjacent to

the Taree LGA proposal. Anchor tenants may assist in attracting future tenants and thus create

demand for road freight services.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 4

No prohibitive regulations were identified.

Transport for NSW identified strong growth in the volume of both inbound and outbound road

freight to 2031 on the Mid North Coast.

The freight task on the Mid North Coast consisted of multiple commodities, destined for dispersed

locations - a scenario better suited to road transport than rail transport.

Development of an intermodal rail terminal in the region was determined as unlikely to be viable and

unlikely to attract private investment due to low volumes, seasonal commodities and insufficient

distance to destination for a competitive advantage over road transport. Despite this rail transport may

be a viable option for specific commodities, for example forest products, manufactured goods or mining

products, and should be considered on a case by case basis.

Road freight was established as the dominant and most suitable transport mode for the Mid North

Coast freight task. Investment in road freight infrastructure could see improved efficiencies for the

industry and was more likely to attract private investment than rail infrastructure. Five suitable locations

for the development of road freight hubs were identified in this study in Greater Taree, Port Macquarie-

Hastings, Kempsey, Nambucca and Coffs Harbour LGA’s and additional sites may be identified in the

future.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 5

Section 1: Introduction

1.1 Study purpose and objectives

The purpose of this study was to identify the current and forecast freight task on the Mid North Coast of

NSW. This study was to establish if sufficient freight volumes exist to establish viable freight transport

infrastructure such as intermodal hub(s) or freight hub(s) in the study area.

The objectives of this study were:

To define freight facilities including intermodal transport hubs, freight transport hubs and

service centres;

To define the current and forecast freight task on the Mid North Coast;

To identify existing commodities contestable for a mode shift to rail transport;

To identify existing and proposed freight transport facilities in the region;

To determine the viability of developing road or rail freight transport hubs in the region.

The deliverables (methodology) were defined in the scope of works for this project as:

Consultation between stakeholders from RMS and relevant Councils, industry and investors to

map out existing and potential opportunities;

Consultation with the transport industry to identify needs and existing gaps in infrastructure;

Economic data collection and analysis in support of transport infrastructure and the potential

flow on of jobs, investment and other economic outcomes;

Identification of suitable locations for freight transport hubs;

Freight volume estimates and minimum freight volumes required for a hub to be successful;

Document what level of participation local councils are willing to provide.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 6

1.2 The Study Area

The study area was the Mid North Coast of NSW, comprising the Local Government Areas of Coffs

Harbour, Bellingen, Nambucca, Kempsey, Port Macquarie-Hastings and Greater Taree. The region is

linear from north to south and stretches from the Great Divide to the east coast.

Figure 1: The Study Area: Mid North Coast of NSW

Port Macquarie-Hastings and Coffs Harbour are the most populated centres, followed by Greater

Taree, Kempsey, Nambucca and Bellingen.

Table 1: Population by Local Government Area

Local Government Area Population Count

Population

Change

(%)

Annualised

Growth Rate (%)

2011 2031

Coffs Harbour 70,950 88,100 24.17% 1.15%

Bellingen 12,900 12,800 -0.78% -0.04%

Nambucca 19,250 20,650 7.27% 0.37%

Kempsey 29,150 30,500 4.63% 0.24%

Port Macquarie Hastings 75,250 90,800 20.66% 0.99%

Greater Taree 48,100 51,900 7.90% 0.40%

Total 255,600 294,750 15.32% 0.75%

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 7

Local Councils are very supportive of freight transport hubs whereby industry capacity can be realised.

Data used in this report has been collected at the regional level (incorporating all LGA’s) and at Local

Government Level.

1.3 Structure of this report

Section 1: Introduction

Section 2: Defines an intermodal freight hub, road freight hub and highway service centre; and

provides sustainability criteria for the development of a regional intermodal terminal and road

freight hub.

Section 3: Describes the current and forecast freight task in the study area

Section 4: Identifies commodities contestable for a mode shift to rail transport

Section 5: Describes the existing road network, proposed road transport network; and

assesses the viability of a road freight transport hub

Section 6: Describes the existing rail network, proposed rail transport infrastructure; and

assesses the viability of a regional intermodal terminal

Section 7: Describes how freight infrastructure aligns with Government strategy

Conclusion

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 8

Section 2 – Definitions and Sustainability Criteria

This section of the report defines an intermodal terminal, road freight hub and highway service centre;

and provides sustainability criteria for the development of a regional intermodal terminal and road

freight hub.

2.1 Intermodal Terminal

An intermodal terminal is a strategic location between a freight service user or exporter / importer and a

destination. It offers a customer road and rail transport access, and short-term storage1.

A place within a regional community;

A business entity that generates a commercially sustainable outcome;

An element within a land-based supply chain.

Intermodal terminals may be located within various supply chains operating in NSW. Regional-based

exporters and importers may choose from a range of transport options to meet their freight needs as

illustrated in Figure 2.

Figure 2: Transport Logistics Options

Source: Sea Freight Council of NSW, nd, Developing Freight Hubs, A Guide to Sustainable Intermodal Terminals for

Regional Communities, available online

http://www.pacificintermodal.com.au/PacificIntermodal/userfiles/file/Developing_Freight_Hubs.pdf

1 Sea Freight Council of NSW, nd, Developing Freight Hubs, A Guide to Sustainable Intermodal Terminals for Regional Communities

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 9

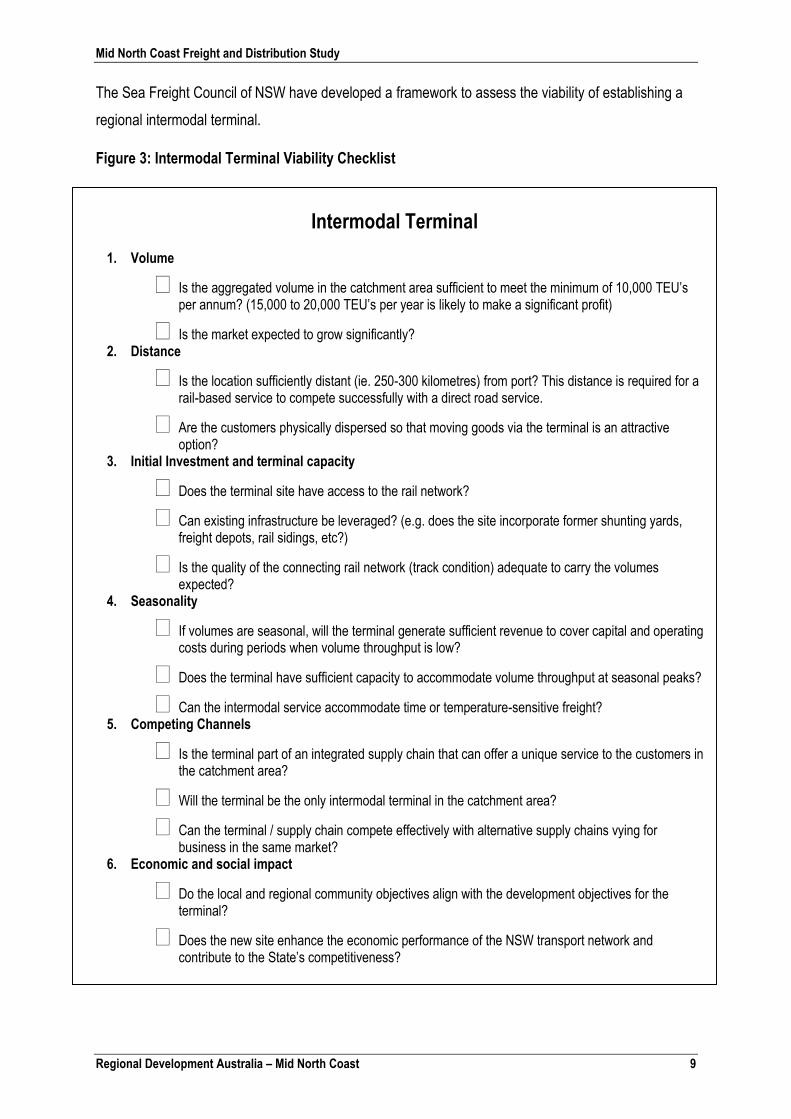

The Sea Freight Council of NSW have developed a framework to assess the viability of establishing a

regional intermodal terminal.

Figure 3: Intermodal Terminal Viability Checklist

Intermodal Terminal

1. Volume

Is the aggregated volume in the catchment area sufficient to meet the minimum of 10,000 TEU’s per annum? (15,000 to 20,000 TEU’s per year is likely to make a significant profit)

Is the market expected to grow significantly? 2. Distance

Is the location sufficiently distant (ie. 250-300 kilometres) from port? This distance is required for a rail-based service to compete successfully with a direct road service.

Are the customers physically dispersed so that moving goods via the terminal is an attractive option?

3. Initial Investment and terminal capacity

Does the terminal site have access to the rail network?

Can existing infrastructure be leveraged? (e.g. does the site incorporate former shunting yards, freight depots, rail sidings, etc?)

Is the quality of the connecting rail network (track condition) adequate to carry the volumes expected?

4. Seasonality

If volumes are seasonal, will the terminal generate sufficient revenue to cover capital and operating costs during periods when volume throughput is low?

Does the terminal have sufficient capacity to accommodate volume throughput at seasonal peaks?

Can the intermodal service accommodate time or temperature-sensitive freight? 5. Competing Channels

Is the terminal part of an integrated supply chain that can offer a unique service to the customers in the catchment area?

Will the terminal be the only intermodal terminal in the catchment area?

Can the terminal / supply chain compete effectively with alternative supply chains vying for business in the same market?

6. Economic and social impact

Do the local and regional community objectives align with the development objectives for the terminal?

Does the new site enhance the economic performance of the NSW transport network and contribute to the State’s competitiveness?

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 10

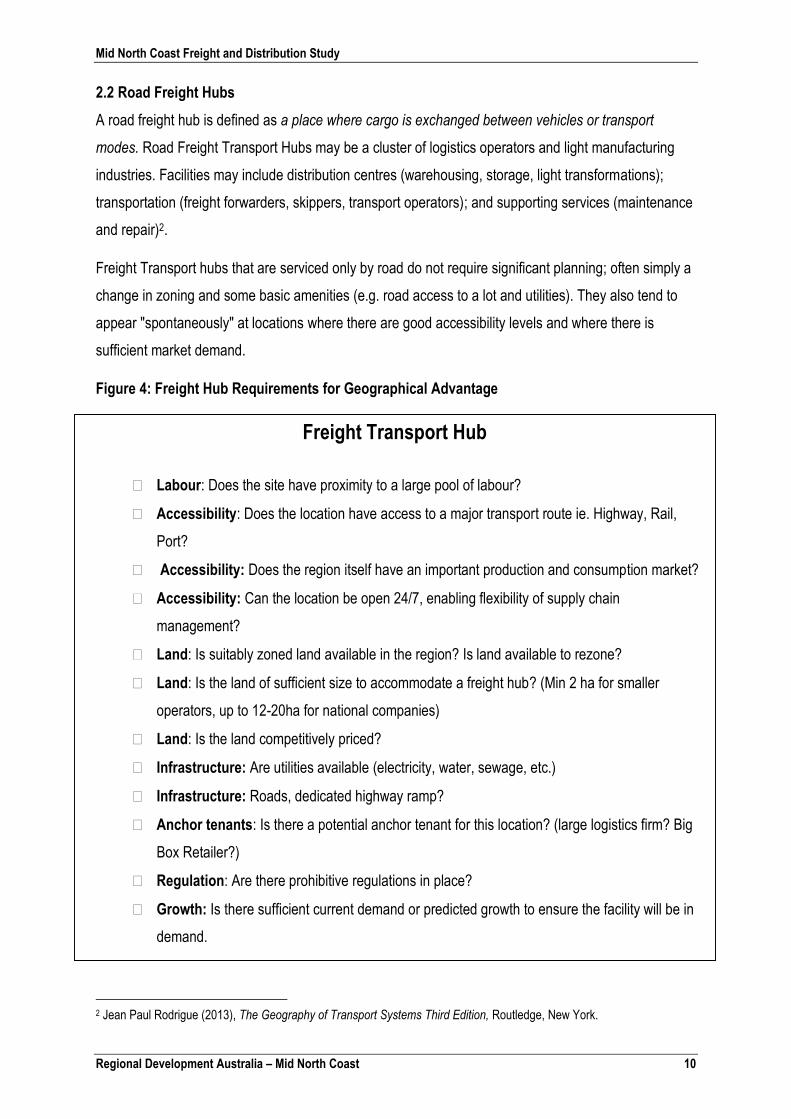

2.2 Road Freight Hubs

A road freight hub is defined as a place where cargo is exchanged between vehicles or transport

modes. Road Freight Transport Hubs may be a cluster of logistics operators and light manufacturing

industries. Facilities may include distribution centres (warehousing, storage, light transformations);

transportation (freight forwarders, skippers, transport operators); and supporting services (maintenance

and repair)2.

Freight Transport hubs that are serviced only by road do not require significant planning; often simply a

change in zoning and some basic amenities (e.g. road access to a lot and utilities). They also tend to

appear "spontaneously" at locations where there are good accessibility levels and where there is

sufficient market demand.

Figure 4: Freight Hub Requirements for Geographical Advantage

2 Jean Paul Rodrigue (2013), The Geography of Transport Systems Third Edition, Routledge, New York.

Freight Transport Hub

Labour: Does the site have proximity to a large pool of labour?

Accessibility: Does the location have access to a major transport route ie. Highway, Rail,

Port?

Accessibility: Does the region itself have an important production and consumption market?

Accessibility: Can the location be open 24/7, enabling flexibility of supply chain

management?

Land: Is suitably zoned land available in the region? Is land available to rezone?

Land: Is the land of sufficient size to accommodate a freight hub? (Min 2 ha for smaller

operators, up to 12-20ha for national companies)

Land: Is the land competitively priced?

Infrastructure: Are utilities available (electricity, water, sewage, etc.)

Infrastructure: Roads, dedicated highway ramp?

Anchor tenants: Is there a potential anchor tenant for this location? (large logistics firm? Big

Box Retailer?)

Regulation: Are there prohibitive regulations in place?

Growth: Is there sufficient current demand or predicted growth to ensure the facility will be in

demand.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 11

2.3 Highway Service Centres

A Highway Service Centre is defined in the NSW Governments Standard Instrument Local

Environmental Plan as:

…a building or place used to provide refreshments and vehicle services to highway users. It may

include any one or more of the following:

A restaurant or café;

Take away food and drink premises;

Service stations and facilities for emergency vehicle towing and repairs;

Parking for vehicles;

Rest areas and public amenities3.

Roads and Maritime also requires:

That the centre is open 24 hours a day, seven days a week;

That all traffic arrangements are safe and efficient;

At least 25 heavy vehicle parking spaces (nominally to suit B-Doubles, with capacity to expand

to cater for longer combinations in the future) be provided;

A number of parking spaces for recreation vehicles and coaches;

The provision of children’s play areas and tourist information;

That use of toilets and other amenities be free of obligation to purchase goods or services;

Separate undercover fuel areas for heavy and light vehicles;

That no alcohol be sold on site4.

Highway service centre and rest stop locations along the Pacific Highway were identified in the RMS

Pacific Highway Rest Stop Strategy. The strategy is included as Appendix A of this report.

It is considered the location of highway service centres and rest stops provide a service to the transport

industry, however they do not contribute directly to the inbound or outbound freight task. As such no

further consideration is given to highway service centres and rest stops in this study.

3 http://www5.austlii.edu.au/au/legis/nsw/consol_reg//silep531/sch99.html 4 Roads and Maritime Service, 2014, Highway Service Centres along the Pacific Highway, RMS 14.143 available online http://www.rms.nsw.gov.au/documents/projects/key-build-programs/pacific-highway/highway-service-centres-along-the-pacific-highway.pdf

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 12

Section 3 – The Current and Forecast Freight Task

This section of the report details the current and forecast, inbound and outbound freight task on the Mid

North Coast and identifies:

The key commodities and volumes which made up the outbound and inbound freight task in

the study area;

The commodity types best suited to the road and rail markets;

The percentage of freight transported by each mode.

The key focus of this section was to determine if sufficient freight volumes existed in the study

area, to consider rail as a mode of transport.

The data used to analyse the freight task on the Mid North Coast was obtained from Transport for

NSW, Bureau of Statistics and Analytics, Strategic Freight Model. The model was developed in

response to Task 1A-3 of the NSW Freight and Ports Strategy to maintain a single agency for

streamlined data collection and strategic analysis5.

The original source data ranged (in age) from between 2004 to 2010. Based on input growth rates by

commodity, all data were then adjusted to provide a base year estimate for 2011 and to forecast 20

years into the future in ten year increments (i.e. 2021 and 2031). The forecast years are consistent with

most other significant data collection and modelling activities between NSW and the Commonwealth

(such as the ABS Census and the BTS population and employment forecasts)5.

3.1 Overview of the Freight Task on the Mid North Coast

The Mid North Coast of NSW generated 1,972,000 tonnes of outbound freight and 2,518,000 tonnes

(excluding intra-regional freight - freight transported between the Local Government Areas) of inbound

freight in 2011.

The highest volumes of outbound freight were generated by:

1. Forest products

2. Dairy Products

3. Containers and General Freight

4. Food Products

5. Meat

5 Transport for NSW, 2014, Bureau of Freight Statistics: Strategic Freight Model Background Information, Version 0.1.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 13

The highest volumes of inbound freight were generated by:

1. Fuel and Lubricants

2. Consumer Goods

3. Food Products

4. Building Products

5. Containers and General Freight

The outbound and inbound freight task on the Mid North Coast, including key origin destination

information, is provided in sections 3.2 and 3.3 of this report. The freight task was characterised by:

A dispersed market. Both inbound and outbound freight had dispersed origins and destinations.

Outbound

The outbound freight task produced few commodities with a significant volume of direct, single

origin – destination freight.

The biggest outbound freight volume was generated by Forest Products, with Newcastle Port

the key destination.

Significant volumes of outbound freight were generated by Containers and General Freight,

with Queensland being the key destination.

Significant volumes of outbound freight were generated by Food Products, with Victoria being

the key destination.

Inbound

The biggest inbound freight task was generated by Fuel and Lubricants with Newcastle being

the key origin.

Significant volumes of inbound freight were generated by Consumer goods, with Newcastle

being the key origin.

Significant volumes of inbound freight were generated by Food Products with Queensland

being the key origin.

Significant volumes of inbound freight were generated by Containers and General Freight with

Queensland being the key origin.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 14

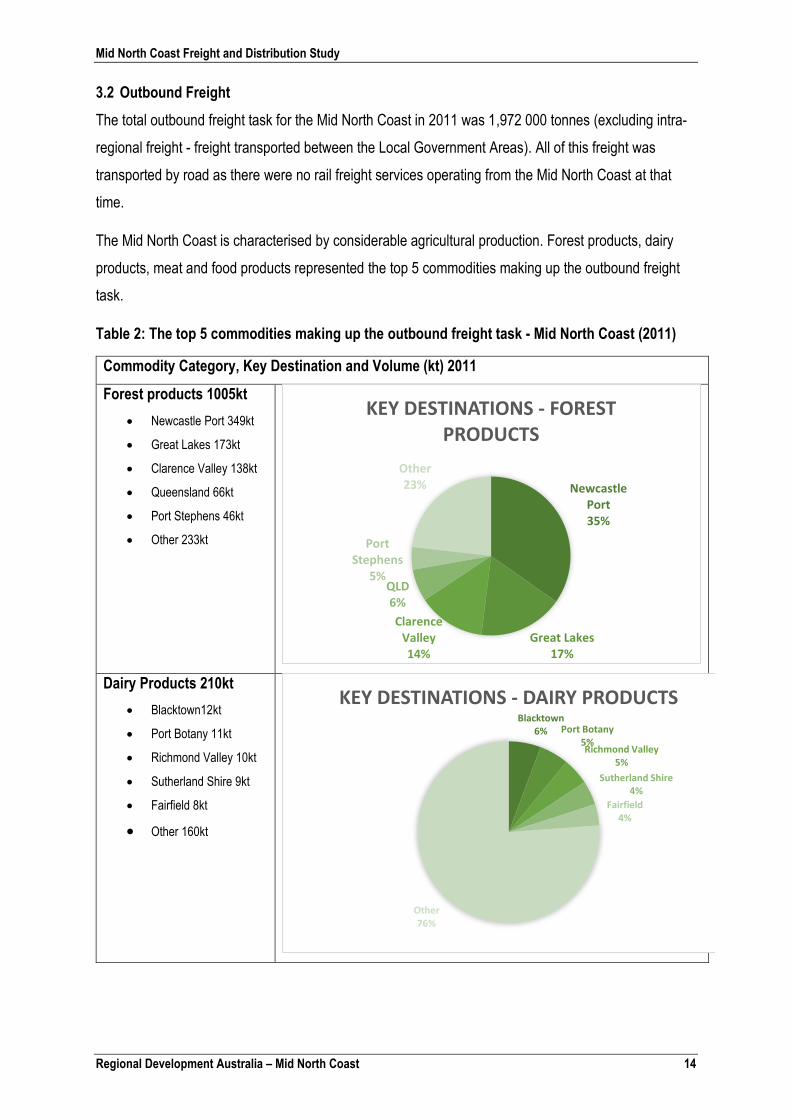

3.2 Outbound Freight

The total outbound freight task for the Mid North Coast in 2011 was 1,972 000 tonnes (excluding intra-

regional freight - freight transported between the Local Government Areas). All of this freight was

transported by road as there were no rail freight services operating from the Mid North Coast at that

time.

The Mid North Coast is characterised by considerable agricultural production. Forest products, dairy

products, meat and food products represented the top 5 commodities making up the outbound freight

task.

Table 2: The top 5 commodities making up the outbound freight task - Mid North Coast (2011)

Commodity Category, Key Destination and Volume (kt) 2011

Forest products 1005kt

Newcastle Port 349kt

Great Lakes 173kt

Clarence Valley 138kt

Queensland 66kt

Port Stephens 46kt

Other 233kt

Dairy Products 210kt

Blacktown12kt

Port Botany 11kt

Richmond Valley 10kt

Sutherland Shire 9kt

Fairfield 8kt

Other 160kt

Newcastle Port 35%

Great Lakes17%

Clarence Valley 14%

QLD6%

Port Stephens

5%

Other23%

KEY DESTINATIONS - FOREST PRODUCTS

Blacktown 6% Port Botany

5%Richmond Valley

5%

Sutherland Shire 4%

Fairfield 4%

Other76%

KEY DESTINATIONS - DAIRY PRODUCTS

Mid North Coast Freight and Distribution Study

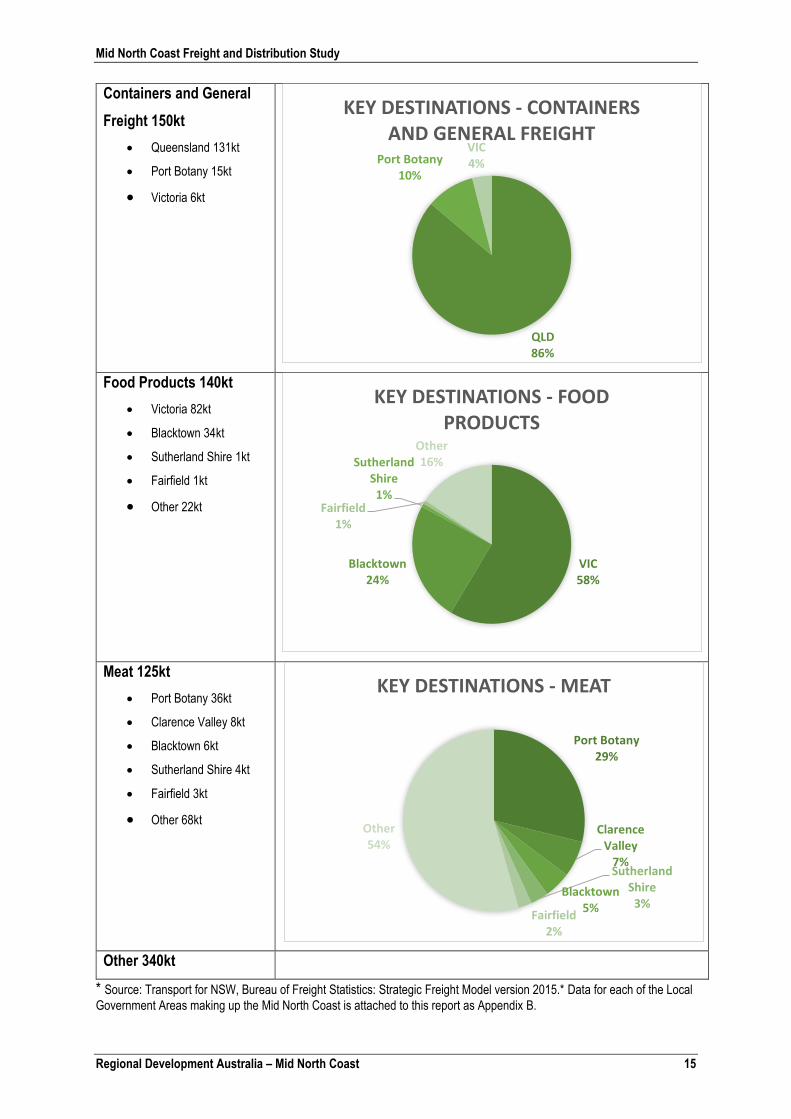

Regional Development Australia – Mid North Coast 15

Containers and General

Freight 150kt

Queensland 131kt

Port Botany 15kt

Victoria 6kt

Food Products 140kt

Victoria 82kt

Blacktown 34kt

Sutherland Shire 1kt

Fairfield 1kt

Other 22kt

Meat 125kt

Port Botany 36kt

Clarence Valley 8kt

Blacktown 6kt

Sutherland Shire 4kt

Fairfield 3kt

Other 68kt

Other 340kt

* Source: Transport for NSW, Bureau of Freight Statistics: Strategic Freight Model version 2015.* Data for each of the Local

Government Areas making up the Mid North Coast is attached to this report as Appendix B.

QLD86%

Port Botany10%

VIC4%

KEY DESTINATIONS - CONTAINERS AND GENERAL FREIGHT

VIC58%

Blacktown 24%

Sutherland Shire 1%

Fairfield 1%

Other16%

KEY DESTINATIONS - FOOD PRODUCTS

Port Botany29%

Clarence Valley

7%

Blacktown 5%

Sutherland Shire 3%

Fairfield 2%

Other54%

KEY DESTINATIONS - MEAT

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 16

3.3 Inbound Freight

The total inbound freight task for the Mid North Coast in 2011 was 2, 518 000 tonnes (excluding intra-

regional freight), which was 28% greater than the outbound freight task. All of this freight was

transported by road as there were no rail freight services operating into the Mid North Coast at that

time.

The inbound freight task consisted of Fuel and Lubricants, Consumer goods, Food Products, Building

Products and Containers and General Freight.

Table 3: The top 5 commodities making up the inbound freight task - Mid North Coast (2011)

Commodity Category, Key Origin and Volume (kt) 2011

Fuel and Lubricants

(605kt)

Newcastle (556kt)

Queensland (49kt)

Consumer Goods (565kt)

Newcastle (111kt)

Queensland (56kt)

Sydney (40kt)

Baulkham Hills

(23kt)

Blacktown (20kt)

Other (315kt)

Newcastle 92%

QLD8%

KEY ORIGINS - FUEL & LUBRICANTS

Newcastle 20%

QLD10%

Sydney 7%

Baulkham Hills 4%Blacktown

3%

Other56%

KEY ORIGINS - CONSUMER GOODS

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 17

Food Products (335kt)

Queensland (314kt)

Victoria (8kt)

Bankstown (1kt)

Blacktown (1kt)

Fairfield (1kt)

Other (10kt)

Building Products (245kt)

Newcastle (28kt)

Bankstown (19kt)

Blacktown (19kt)

Fairfield (15kt)

Holroyd (12kt)

Other (152kt)

Containers & General

Freight (203kt)

Queensland (199kt)

Victoria (3kt)

Port Botany (1kt)

Source: Transport for NSW, Bureau of Freight Statistics: Strategic Freight Model version 2015.

QLD94%

VIC3%

Bankstown 0%

Blacktown 0%

Fairfield 0%

Other3%

KEY ORIGINS - FOOD PRODUCTS

Newcastle 11%

Bankstown 8%

Blacktown 8%

Fairfield 6%

Holroyd5%

Other62%

KEY ORIGINS - BUILDING PRODUCTS

QLD98%

VIC1%

Port Botany1%

KEY ORIGINS - CONTAINERS AND GENERAL FREIGHT

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 18

3.4 Forecast Freight Growth

This section of the report details the forecast growth in the freight task by commodity to 2031.

Forecast data were modelled using the Transport for NSW Strategic Freight Model, which was sourced

from a range of data sets including the Hyder/Sd&D regional NSW freight supply chain studies

(various); The Metropolitan Freight Movement Model (FMM by Bureau of Transport Statistics) and The

interstate freight task (various BITRE datasets for the road and rail task)5.

The forecast freight volume data illustrated in Tables 3 and 4, predicts annualised growth rates

between 1.89% and 3.26%. The average annualised growth rate for all outbound freight from the Mid

North Coast was 2.44%, and 2.99% for inbound freight. Average annualised population growth for the

Mid North Coast was significantly lower at 0.75%, thus it can be assumed forecast growth of outbound

freight will need to be largely driven by inter-regional and international trade servicing demand.

3.4.1 Forecast Outbound Freight (2031)

Table 4: Forecast Outbound Freight Volumes by Commodity Category, Mid North Coast, 2031

Commodity Category 2011 Volume 2031 Volume % Increase Annualised Growth Rate %

Forest Products 1005 1435 42.79% 1.89%

Dairy Products 210 375 78.57% 3.10%

Containers and General Freight 150 275 83.33% 3.24%

Food Products 140 250 78.57% 3.10%

Meat 125 230 84.00% 3.26%

Other 340 550 61.76% 2.56%

Total 1970 3115 58.12% 2.44%

* Source: Transport for NSW, Bureau of Freight Statistics: Strategic Freight Model version 2015.

3.4.2 Forecast Inbound Freight (2031)

Table 5: Forecast Inbound Freight Volumes by Commodity Category, Mid North Coast, 2031

Commodity Category 2011 Volume 2031 Volume % Increase Annualised Growth Rate %

Fuel and Lubricants 605 1095 80.99% 3.17%

Consumer Goods 565 1015 79.65% 3.13%

Food Products 335 605 80.60% 3.16%

Building Products 245 445 81.63% 3.19%

Containers and General Freight 205 365 78.05% 3.08%

Other 565 885 56.64% 2.39%

Total 2520 4410 75.00% 2.99%

* Source: Transport for NSW, Bureau of Freight Statistics: Strategic Freight Model version 2015.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 19

Freight volume growth rates by Local Government Area (LGA) (Tables 5 and 6), illustrate the highest

outbound freight volume increases are forecast for Kempsey, Greater Taree and Bellingen, followed by

Coffs Harbour, Port Macquarie Hastings and Nambucca. The highest inbound freight volume increases

are forecast for Bellingen, Greater Taree and Coffs Harbour, followed by Kempsey, Port Macquarie-

Hastings and Nambucca.

Table 6: Outbound Freight Volumes by Local Government Area (LGA)

Local Government Area - Outbound Freight

2011 Volume (kt)

2031 Volume (kt)

% Increase Annualised Growth Rate

Bellingen 105 165 57.14% 2.41%

Coffs Harbour 575 820 42.61% 1.89%

Greater Taree 470 775 64.89% 2.67%

Port Macquarie-Hastings 720 1015 40.97% 1.82%

Kempsey 480 845 76.04% 3.02%

Nambucca 150 210 40.00% 1.79%

Table 7: Inbound Freight Volumes by Local Government Area (LGA)

Local Government Area - Inbound Freight

2011 Volume (kt)

2031 Volume (kt)

% Increase Annualised Growth Rate

Bellingen 105 195 85.71% 3.31%

Coffs Harbour 735 1255 70.75% 2.86%

Greater Taree 605 1035 71.07% 2.87%

Port Macquarie-Hastings 1030 1705 65.53% 2.69%

Kempsey 350 590 68.57% 2.79%

Nambucca 225 345 53.33% 2.28%

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 20

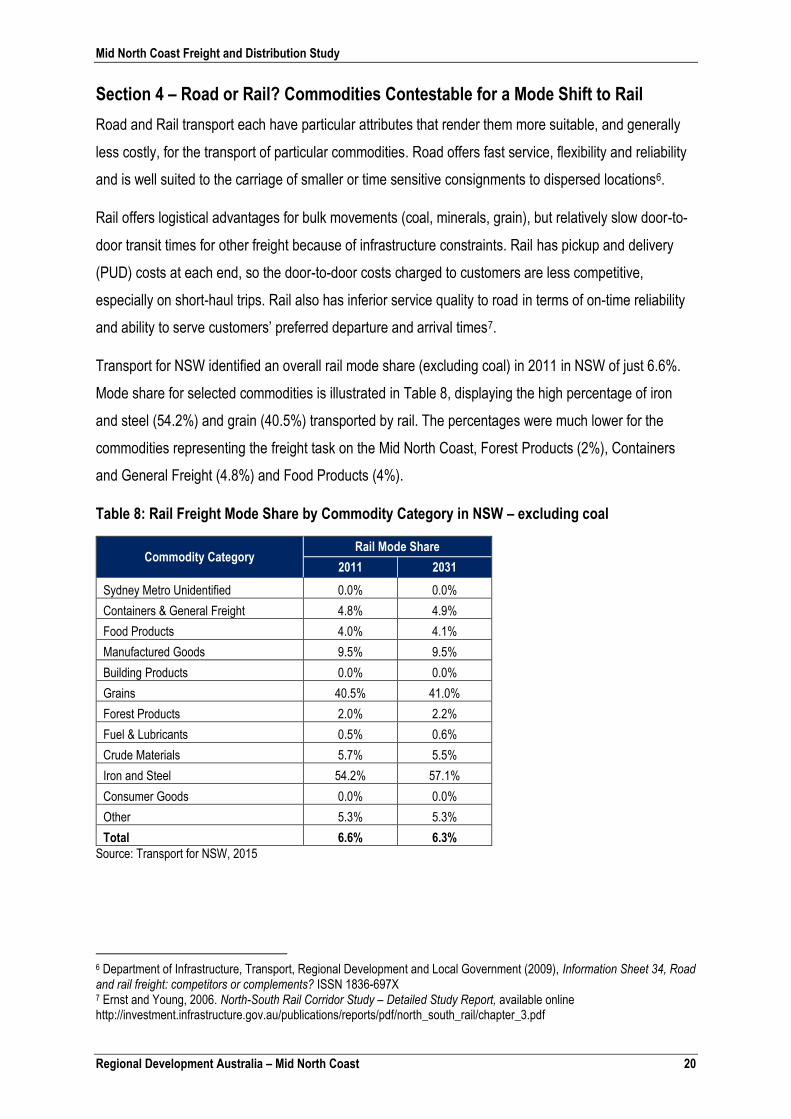

Section 4 – Road or Rail? Commodities Contestable for a Mode Shift to Rail

Road and Rail transport each have particular attributes that render them more suitable, and generally

less costly, for the transport of particular commodities. Road offers fast service, flexibility and reliability

and is well suited to the carriage of smaller or time sensitive consignments to dispersed locations6.

Rail offers logistical advantages for bulk movements (coal, minerals, grain), but relatively slow door-to-

door transit times for other freight because of infrastructure constraints. Rail has pickup and delivery

(PUD) costs at each end, so the door-to-door costs charged to customers are less competitive,

especially on short-haul trips. Rail also has inferior service quality to road in terms of on-time reliability

and ability to serve customers’ preferred departure and arrival times7.

Transport for NSW identified an overall rail mode share (excluding coal) in 2011 in NSW of just 6.6%.

Mode share for selected commodities is illustrated in Table 8, displaying the high percentage of iron

and steel (54.2%) and grain (40.5%) transported by rail. The percentages were much lower for the

commodities representing the freight task on the Mid North Coast, Forest Products (2%), Containers

and General Freight (4.8%) and Food Products (4%).

Table 8: Rail Freight Mode Share by Commodity Category in NSW – excluding coal

Commodity Category Rail Mode Share

2011 2031

Sydney Metro Unidentified 0.0% 0.0%

Containers & General Freight 4.8% 4.9%

Food Products 4.0% 4.1%

Manufactured Goods 9.5% 9.5%

Building Products 0.0% 0.0%

Grains 40.5% 41.0%

Forest Products 2.0% 2.2%

Fuel & Lubricants 0.5% 0.6%

Crude Materials 5.7% 5.5%

Iron and Steel 54.2% 57.1%

Consumer Goods 0.0% 0.0%

Other 5.3% 5.3%

Total 6.6% 6.3%

Source: Transport for NSW, 2015

6 Department of Infrastructure, Transport, Regional Development and Local Government (2009), Information Sheet 34, Road and rail freight: competitors or complements? ISSN 1836-697X 7 Ernst and Young, 2006. North-South Rail Corridor Study – Detailed Study Report, available online http://investment.infrastructure.gov.au/publications/reports/pdf/north_south_rail/chapter_3.pdf

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 21

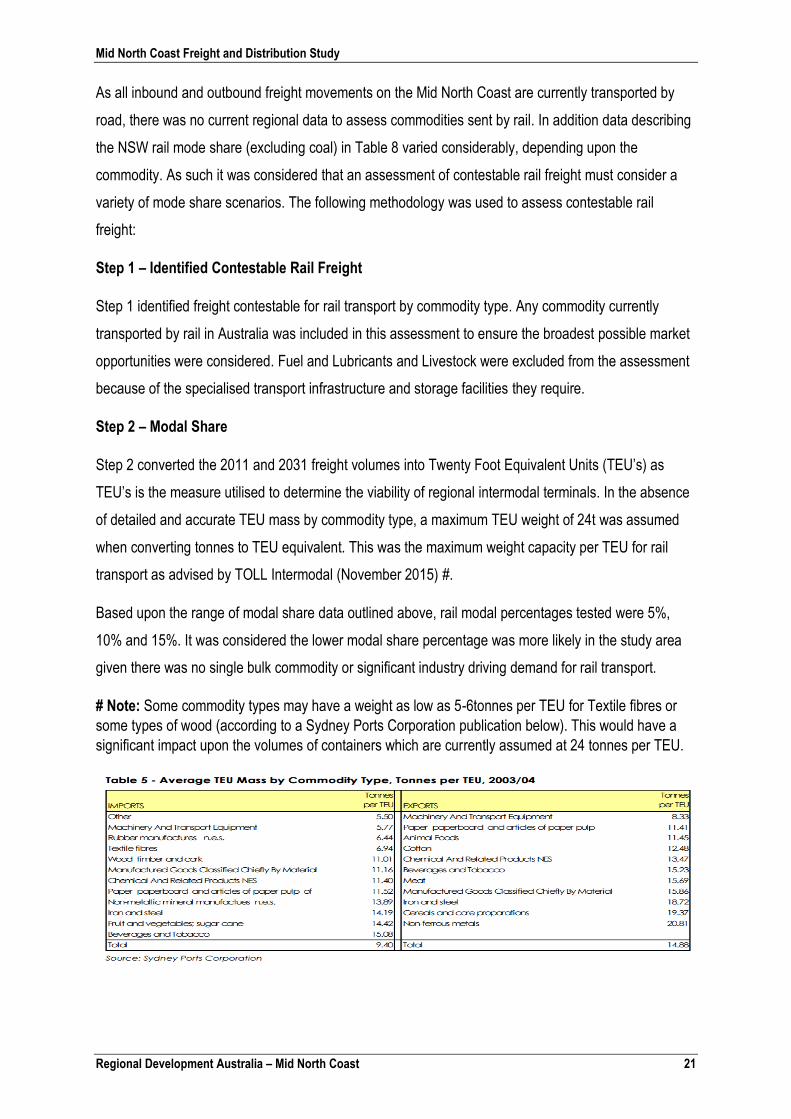

As all inbound and outbound freight movements on the Mid North Coast are currently transported by

road, there was no current regional data to assess commodities sent by rail. In addition data describing

the NSW rail mode share (excluding coal) in Table 8 varied considerably, depending upon the

commodity. As such it was considered that an assessment of contestable rail freight must consider a

variety of mode share scenarios. The following methodology was used to assess contestable rail

freight:

Step 1 – Identified Contestable Rail Freight

Step 1 identified freight contestable for rail transport by commodity type. Any commodity currently

transported by rail in Australia was included in this assessment to ensure the broadest possible market

opportunities were considered. Fuel and Lubricants and Livestock were excluded from the assessment

because of the specialised transport infrastructure and storage facilities they require.

Step 2 – Modal Share

Step 2 converted the 2011 and 2031 freight volumes into Twenty Foot Equivalent Units (TEU’s) as

TEU’s is the measure utilised to determine the viability of regional intermodal terminals. In the absence

of detailed and accurate TEU mass by commodity type, a maximum TEU weight of 24t was assumed

when converting tonnes to TEU equivalent. This was the maximum weight capacity per TEU for rail

transport as advised by TOLL Intermodal (November 2015) #.

Based upon the range of modal share data outlined above, rail modal percentages tested were 5%,

10% and 15%. It was considered the lower modal share percentage was more likely in the study area

given there was no single bulk commodity or significant industry driving demand for rail transport.

# Note: Some commodity types may have a weight as low as 5-6tonnes per TEU for Textile fibres or

some types of wood (according to a Sydney Ports Corporation publication below). This would have a

significant impact upon the volumes of containers which are currently assumed at 24 tonnes per TEU.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 22

4.1 Identification of Contestable Rail Freight

A large variety of goods are transported by rail in Australia and it was considered appropriate to include

all currently railed commodities as suitable for rail transport on the Mid North Coast in this assessment.

This information has been obtained from the Australian Rail Track Corporation (ARTC) as at November

2015.

Table 9: Inbound and Outbound Commodities Suitable for Transport by Rail, NSW Mid North Coast

Suitable for Rail Transport Not Currently Suitable for Rail Transport on

the Mid North Coast

Containers and General Freight Livestock

Forest Products Fuel and Lubricants

Manufactured Goods

Food products

Meat

Building Products

Dairy

Fruit and Vegetables

Consumer Goods (FMCG)

4.2 Intermodal Freight Hub Summary

The mode share scenarios modelled in Table 9 illustrates that:

The volumes of 2011 outbound freight did not meet the minimum 10,000 TEU’s for a

sustainable intermodal terminal when a 5% and 10% mode share was tested.

The volumes of 2011 inbound freight did not meet the minimum 10,000 TEU’s for a

sustainable intermodal terminal when a 5% and 10% mode share was tested.

The volumes of 2011 outbound freight met the minimum 10,000 TEU’s for a sustainable

terminal when a 15% mode share was tested.

The volumes of 2011 inbound freight met the minimum 10,000 TEU’s for a sustainable

terminal when a 15% mode share was tested

Forecast data for 2031 illustrates that the volume of outbound freight does not meet the

minimum 10,000 TEU’s for a sustainable intermodal terminal when a 5% mode share is tested.

Forecast data for 2031 illustrates that the volume of inbound freight does not meet the

minimum 10,000 TEU’s for a sustainable intermodal terminal when a 5% mode share is tested

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 23

Forecast data for 2031 illustrates that the volume of outbound freight meets the minimum

10,000 TEU’s for a sustainable intermodal terminal when a 10% and 15% mode share is

tested.

Forecast data for 2031 illustrates that the volume of inbound freight meets the minimum

10,000 TEU’s for a sustainable intermodal terminal when a 10% and 15% mode share is

tested.

Outbound freight volumes consist largely of forest products. Forest products represent a

crucial commodity contributing to the volumes needed for a sustainable intermodal terminal.

It should be noted that this study is assessing the freight volumes required, for the establishment of an

economically viable, intermodal rail terminal. The use of rail transport and existing rail infrastructure on

the Mid North Coast, may still be a viable option for individual businesses or commodities, for example

forest products, manufactured goods or mining products, and should be assessed on a case by case

basis.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 24

Table 10: Evaluating Contestability Mid North Coast

Outbound Freight: Commodity Category

Key Destination

Commodity suitable for Rail Transport?

2011 Volume (kt)

Equivalent TEU's (Max weight for rail 24t)

Mode Share 5%

Mode Share 10%

Mode Share 15%

Current Road Volume Meets Freight Hub Threshold? (10,000 TEU's)

2031 Volume (kt)

Equivalent TEU's (Max weight for rail 24t)

Mode Share 5%

Mode Share 10%

Mode Share 15%

Future Freight Volume Meets Freight Hub Threshold (10,000 TEU's)?

Forest Products Newcastle Port 349 14541.67 727.08 1454.17 2181.25 631.00 26291.67 1314.58 2629.17 3943.75

Great Lakes 173 7208.33 360.42 720.83 1081.25 212.00 8833.33 441.67 883.33 1325.00

Clarence Valley 138 5750.00 287.50 575.00 862.50 168.00 7000.00 350.00 700.00 1050.00

QLD 66 2750.00 137.50 275.00 412.50 80.00 3333.33 166.67 333.33 500.00

Port Stephens 46 1916.67 95.83 191.67 287.50 56.00 2333.33 116.67 233.33 350.00

Other 233 9708.33 485.42 970.83 1456.25 288.00 12000.00 600.00 1200.00 1800.00

Sub-total Yes 1005 41875.00 2093.75 4187.50 6281.25 1435.00 59791.67 2989.58 5979.17 8968.75

Dairy Products Blacktown 12 500.00 25.00 50.00 75.00 22.00 916.67 45.83 91.67 137.50

Port Botany 11 458.33 22.92 45.83 68.75 20.00 833.33 41.67 83.33 125.00

Richmond Valley 10 416.67 20.83 41.67 62.50 19.00 791.67 39.58 79.17 118.75

Sutherland Shire 9 375.00 18.75 37.50 56.25 16.00 666.67 33.33 66.67 100.00

Fairfield 8 333.33 16.67 33.33 50.00 14.00 583.33 29.17 58.33 87.50

Other 160 6666.67 333.33 666.67 1000.00 284.00 11833.33 591.67 1183.33 1775.00

Sub-total Yes 210 8750.00 437.50 875.00 1312.50 375.00 15625.00 781.25 1562.50 2343.75

Containers & General Freight

QLD 131 5458.33 272.92 545.83 818.75 236.00 9833.33 491.67 983.33 1475.00

Port Botany 15 625.00 31.25 62.50 93.75 28.00 1166.67 58.33 116.67 175.00

VIC 6 250.00 12.50 25.00 37.50 10.00 416.67 20.83 41.67 62.50

Sub-total Yes 152 6333.33 316.67 633.33 950.00 274.00 11416.67 570.83 1141.67 1712.50

Food Products QLD 0 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

VIC 82 3416.67 170.83 341.67 512.50 148.00 6166.67 308.33 616.67 925.00

Blacktown 34 1416.67 70.83 141.67 212.50 61.00 2541.67 127.08 254.17 381.25

Sutherland Shire 1 41.67 2.08 4.17 6.25 3.00 125.00 6.25 12.50 18.75

Fairfield 1 41.67 2.08 4.17 6.25 2.00 83.33 4.17 8.33 12.50

Other 22 916.67 45.83 91.67 137.50 36.00 1500.00 75.00 150.00 225.00

Sub-total Yes 140 5833.33 291.67 583.33 875.00 250.00 10416.67 520.83 1041.67 1562.50

Meat Port Botany 36 1500.00 75.00 150.00 225.00 64.00 2666.67 133.33 266.67 400.00

Clarence Valley 8 333.33 16.67 33.33 50.00 14.00 583.33 29.17 58.33 87.50

Blacktown 6 250.00 12.50 25.00 37.50 10.00 416.67 20.83 41.67 62.50

Sutherland Shire 4 166.67 8.33 16.67 25.00 7.00 291.67 14.58 29.17 43.75

Fairfield 3 125.00 6.25 12.50 18.75 6.00 250.00 12.50 25.00 37.50

Other 68 2833.33 141.67 283.33 425.00 129.00 5375.00 268.75 537.50 806.25

Sub-total Yes 125 5208.33 260.42 520.83 781.25 230.00 9583.33 479.17 958.33 1437.50

Other 340 14166.67 708.33 1416.67 2125.00 550.00 22916.67 1145.83 2291.67 3437.50

Total 1972 82166.67 4108.33 8216.67 12325.00 Yes 3114.00 129750.00 6487.50 12975.00 19462.50 Yes

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 25

Mid North Coast

Outbound Freight: Commodity Category

Key Destination

Commodity suitable for Rail Transport?

2011 Volume (kt)

Equivalent TEU's (Max weight for rail 24t)

Mode Share 5%

Mode Share 10%

Mode Share 15%

Current Road Volume Meets Freight Hub Threshold? (10,000 TEU's)

2031 Volume (kt)

Equivalent TEU's (Max weight for rail 24t)

Mode Share 5%

Mode Share 10%

Mode Share 15%

Future Freight Volume Meets Freight Hub Threshold (10,000 TEU's)?

Fuel & Lubricants Newcastle 556 1004

QLD 49 89

Sub-total No 605 Not suitable for rail

transport

1093

Consumer Goods Newcastle 111 4625.00 231.25 462.50 693.75 201 8375.00 418.75 837.50 1256.25

QLD 56 2333.33 116.67 233.33 350.00 100 4166.67 208.33 416.67 625.00

Sydney 40 1666.67 83.33 166.67 250.00 73 3041.67 152.08 304.17 456.25

Baulkham Hills 23 958.33 47.92 95.83 143.75 41 1708.33 85.42 170.83 256.25

Blacktown 20 833.33 41.67 83.33 125.00 37 1541.67 77.08 154.17 231.25

Other 315 13125.00 656.25 1312.50 1968.75 563 23458.33 1172.92 2345.83 3518.75

Sub-total Yes 565 23541.67 1177.08 2354.17 3531.25 1015 42291.67 2114.58 4229.17 6343.75

Food Products QLD 314 13083.33 654.17 1308.33 1962.50 566 23583.33 1179.17 2358.33 3537.50

VIC 8 333.33 16.67 33.33 50.00 14 583.33 29.17 58.33 87.50

Bankstown 1 41.67 2.08 4.17 6.25 2 83.33 4.17 8.33 12.50

Blacktown 1 41.67 2.08 4.17 6.25 2 83.33 4.17 8.33 12.50

Fairfield 1 41.67 2.08 4.17 6.25 2 83.33 4.17 8.33 12.50

Other 10 416.67 20.83 41.67 62.50 19 791.67 39.58 79.17 118.75

Sub-total Yes 335 13958.33 697.92 1395.83 2093.75 605 25208.33 1260.42 2520.83 3781.25

Building Products Newcastle 28 1166.67 58.33 116.67 175.00 50 2083.33 104.17 208.33 312.50

Bankstown 19 791.67 39.58 79.17 118.75 35 1458.33 72.92 145.83 218.75

Blacktown 19 791.67 39.58 79.17 118.75 34 1416.67 70.83 141.67 212.50

Fairfield 15 625.00 31.25 62.50 93.75 27 1125.00 56.25 112.50 168.75

Holroyd 12 500.00 25.00 50.00 75.00 22 916.67 45.83 91.67 137.50

Other 152 6333.33 316.67 633.33 950.00 277 11541.67 577.08 1154.17 1731.25

Sub-total Yes 245 10208.33 510.42 1020.83 1531.25 445 18541.67 927.08 1854.17 2781.25

Containers & General Freight QLD 199 8291.67 414.58 829.17 1243.75

359

14958.33 747.92 1495.83 2243.75

VIC 3 125.00 6.25 12.50 18.75 6 250.00 12.50 25.00 37.50

Port Botany 1 41.67 2.08 4.17 6.25 2 83.33 4.17 8.33 12.50

Sub-total Yes 203 8458.33 422.92 845.83 1268.75 367 15291.67 764.58 1529.17 2293.75

Other 565 23541.67 1177.08 2354.17 3531.25 885 36875.00 1843.75 3687.50 5531.25

Total 1913 79708.33 3985.42 7970.83 11956.25 Yes 3317 138208.33 6910.42 13820.83 20731.25 Yes

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 26

Section 5 - The Road Network

This section of the report describes the existing road network, proposed road transport network and

assesses the viability of a road freight hub in the study area.

5.1 The Existing Road Network

The Mid North Coast has strong connectivity to the National Highway Network, with a total of 285km of

highway passing through the region. The Pacific Highway provides the primary road connection

between Sydney and Brisbane and is currently being upgraded to a four lane divided road, with

completion scheduled by 2020. The upgraded road will improve conditions for road transport in the

future by providing safer travel: reduced travel times and more consistent and reliable travel.

Table 11: Distance to Major Centres

Regional Centres To Sydney (km) To Brisbane (km)

Taree 308 618

Port Macquarie 383 551

Kempsey 419 503

Nambucca Heads 486 439

Bellingen 522 427

Coffs Harbour 534 392

Figure 5: National Rail and Highway Network

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 27

The outbound and inbound freight task in the study area is met entirely by road transport. The road

transport industry in Australia consists of large multi-national transport companies to smaller family

owned businesses. Freight companies operating on the Mid North Coast currently provide their own

depot, warehousing and storage facilities and it is likely that this situation will continue due to the

uncertainty and reduced control associated with externally owned, multi-user facilities.

5.2 Proposed Freight Transport Infrastructure

Industry and Councils are very supportive of Transport Hubs as a means to encourage economic

development in their region. Each of the Councils on the Mid North Coast were consulted and asked to

identify current proposals in their region.

The proposals nominated by Councils are best described as road freight hubs, as they are essentially

Industrial land developments, with good connectivity to the Pacific Highway. These proposals are

summarised in Table 11.

Table 12: Proposed Transport Infrastructure on the Mid North Coast

Council Name Intermodal Name and Description

Nambucca Valley

Council

Valla Enterprise Zone Growth Area:

50ha site

Located immediately adjacent to the Pacific Hwy upgrade;

Incorporate a double interchange and highway service

centre

Port Macquarie

Hastings Council

Sancrox Employment Lands:

85.4ha – current proposal 70 lots from 3500m2 to 10 hectares.

Located immediately adjacent to the Pacific Hwy

Sancrox overpass due for completion in late 2016 will allow

easy access to the precinct for heavy vehicles.

Greater Taree City

Council

The Northern Taree Entry Freight Interchange.

60 ha site

Located immediately adjacent to the Pacific Hwy with

access via the Cundletown overpass.

Adjacent to the Taree Airport

4 hours drive from Sydney

REMPLAN economic modelling indicates some 200 FTE

positions may be created from the proposal

Estimated cost $3.05 million ($1.8m two lane roundabout

and $1.25m

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 28

In addition to the abovementioned proposals, existing industrial land (or land identified for rezoning)

with good highway connectivity is identified in the following locations:

Coffs Harbour Lot 2 Stadium Drive – 3.4 ha, south eastern roundabout

corner of the Pacific Highway and Stadium Drive

North Boambee Valley – 37 hectares of proposed industrial

land adjacent to the proposed Pacific Highway bypass of

Coffs. The Bypass is scheduled for commencement in

2018/19 and the proposal is in the concept – strategic

planning phase.

Bellingen 2.3ha approved employment lands in Urunga on the eastern

side of the railway line. This land is not currently for sale.

Kempsey South Kempsey Industrial Park – Industrial land adjacent to

the South Kempsey Service Centre. Excellent Highway

access.

5.3 Viability of a Regional Freight Transport Hub

This section provides a discussion of potential road freight hubs on the Mid North Coast based on the

sustainability criteria outlined in Section 2.

5.3.1 Labour: Does the site have proximity to a large pool of labour?

The larger centres of Coffs Harbour, Port Macquarie, Taree and Kempsey have the highest populations

and thus the largest labour pools. Coffs Harbour and Port Macquarie-Hastings have the highest

predicted population growth rates, with a predicted increase by 2031 of 24% for Coffs Harbour and 20%

for Port Macquarie-Hastings.

Table 13: Mid North Coast Population Forecast

Local Government Area Population Count

Population Change

(%)

Annualised Growth Rate

2011 2031

Coffs Harbour 70,950 88,100 24.17% 1.15%

Bellingen 12,900 12,800 -0.78% -0.04%

Nambucca 19,250 20,650 7.27% 0.37%

Kempsey 29,150 30,500 4.63% 0.24%

Port Macquarie Hastings 75,250 90,800 20.66% 0.99%

Greater Taree 48,100 51,900 7.90% 0.40%

Total 255,600 294,750 15.32% 0.75%

Source: The NSW Department of Planning, Population Projections, accessed December 2015

http://www.planning.nsw.gov.au/projections

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 29

Accessibility

Does the location have access to a major transport route? (Highway, Rail, Port)

Each of the sites identified in section 5.2 have access to the Pacific Highway, the national highway

linking Sydney and Brisbane.

Does the region itself have an important production and consumption market?

The study area has important production and consumption markets. The highest volumes of outbound

freight on the Mid North Coast are generated by forest products, dairy products, meat, containers and

general freight and food products. The highest volumes of inbound freight are generated by fuel and

lubricants, consumer goods, food products, building products and containers and general freight.

The study area is characterised by dispersed origin and destination freight, with few commodities of

sufficient volume or direct origin-destination locations. Road offers the most suitable freight transport

service as it is flexible and better suited to the carriage of smaller or time sensitive consignments to

dispersed locations.

Can the location be open 24/7, enabling flexibility of supply chain management?

Proposed freight developments and industrial lands identified in section 5.2 are either currently zoned

for industrial use or are identified in strategic planning documents for rezoning. This land is considered

suitable to accommodate road freight development due to its connectivity to the Pacific Highway.

Land

Is suitably zoned land available in the region? Is land available to rezone?

The proposed freight developments, existing industrial land and proposed industrial land identified in

section 5.2 are suitable to accommodate road freight development. Additional sites with good

connectivity to the Pacific Highway may be identified in the future.

Is the land of sufficient size to accommodate a freight hub? (Min 2ha for smaller

operators, up to 12-20ha for national companies)

The proposals identified in section 5.2 consist of a 50ha, 60ha and 85.4ha parcel. The final subdivision

design is not yet complete for the proposals in Taree and Valla, thus the development can

accommodate a range of lot sizes. The proposal in Port Macquarie-Hastings offers a range of lot sizes

from 3500m2 to 10 ha, with flexibility to consolidate or subdivide lots to meet the needs of small,

medium and large enterprises.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 30

Is the land competitively priced?

The price of private developments identified in section 5.2 is subject to negotiation with the developer.

Infrastructure

Services to the land identified in section 5.2 are at differing stages of provision, however all services

would be available upon occupation of the land.

The proposals identified in section 5.2 have dedicated highway access and it is considered that any

future proposals would require similar infrastructure to facilitate heavy vehicle access.

Anchor Tenants

The proposals identified in section 5.2 have existing adjacent tenants and / or interest from a number of

tenants including manufacturing, transport and industrial businesses. Anchor tenants may assist in

attracting future tenants and thus create demand for road freight services.

Existing businesses are present adjacent to the Port Macquarie-Hastings LGA proposal

(manufacturing); and the Kempsey LGA development (Highway Service Centre); which may assist in

attracting future tenants.

Regulation

It is considered the proposals identified in section 5.2 are either suitably zoned or identified for future

rezoning and thus will not have restrictive regulations.

Growth

Forecast freight growth rates provided by Transport for NSW Strategic Freight Model in section 3.4 of

this report illustrates sufficient growth to support the expansion of the transport and logistics industry in

the study area.

The highest growth rates of annualised outbound freight are forecast for Kempsey, Greater Taree,

Bellingen, Coffs Harbour, Port Macquarie-Hastings then Nambucca. The highest growth rates of

annualised inbound freight are forecast for Bellingen, Greater Taree, Coffs Harbour, Kempsey, Port

Macquarie-Hastings then Nambucca.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 31

Road Freight Hub Summary

Three industrial land developments are proposed on the Pacific Highway in Nambucca, Port

Macquarie and Taree. These locations are identified as suitable for development as road

freight hubs.

The South Kempsey Industrial Park is identified as suitable for development as a road freight

hub.

Proposed industrial land in the North Boambee Valley, adjacent to the Pacific Highway bypass

of Coffs Harbour (2018/19 commencement) is identified as suitable for development as a road

freight hub.

Lots in the abovementioned developments are of sufficient size at all locations to accommodate

road transport firms.

Services are currently at differing stages of provision, however all services would be available

upon occupation of the land.

Existing businesses are present adjacent to the Port Macquarie-Hastings LGA proposal

(manufacturing); and the Kempsey LGA development (Highway Service Centre); which may

assist in attracting future tenants.

Expressions of interest have been received for the proposal in the Taree LGA and the

Nambucca LGA. Anchor tenants may assist in attracting future tenants and thus create

demand for road freight services.

No prohibitive regulations are identified.

Transport for NSW identify strong growth in the volume of both inbound and outbound road

freight to 2031 on the Mid North Coast.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 32

Section 6: The Rail Network

This section of the report describes the existing rail network, proposed rail transport infrastructure and

assesses the viability of a regional intermodal terminal in the study area.

6.1 The Existing Rail Network

The main north-south rail line from Sydney to Brisbane traverses the study area. This line is used for

passenger trains and freight trains, however, freight trains do not currently stop on the Mid North Coast.

Passenger stops are located in Wingham, Taree, Kendall, Wauchope, Kempsey, Eungai, Macksville,

Nambucca Heads, Urunga, Sawtell and Coffs Harbour.

Two major direct origin – destination freight services operate on the North Coast rail line - Pacific

National and Aurizon (formerly Qld Rail) - representing 90% of the freight task. Smaller regional rail

freight operators represent the remaining 10%.

The rail freight task through the region is dominated by the movement of container freight from the Port

of Melbourne to Brisbane and from Sydney’s Port Botany to Brisbane. Return freight predominantly

consists of agricultural produce from Queensland returning to Sydney and Melbourne.

There are currently no operational intermodal terminals on the Mid North Coast, however there are a

number of existing sidings and associated infrastructure in the region.

Table 14: Existing Rail Infrastructure, NSW Mid North Coast

Location Description of Infrastructure Ownership

Taree Railcorp Station

2 sidings

1 private spur?

Mixed

Kendall Stock and Goods Loop Private

Wauchope Railcorp Station

Goods neck

Private

Telegraph Point Small siding, difficult to access Public

Kundabung Goods loop

Kempsey Railcorp station

Pacific National siding

Shell siding

Stock

Mixed

Eungai Small siding (close to residential properties) Public

Nambucca Heads Small siding, difficult to access Public

Raleigh Siding Public

Boambee Beach Siding Engineering Goods Private

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 33

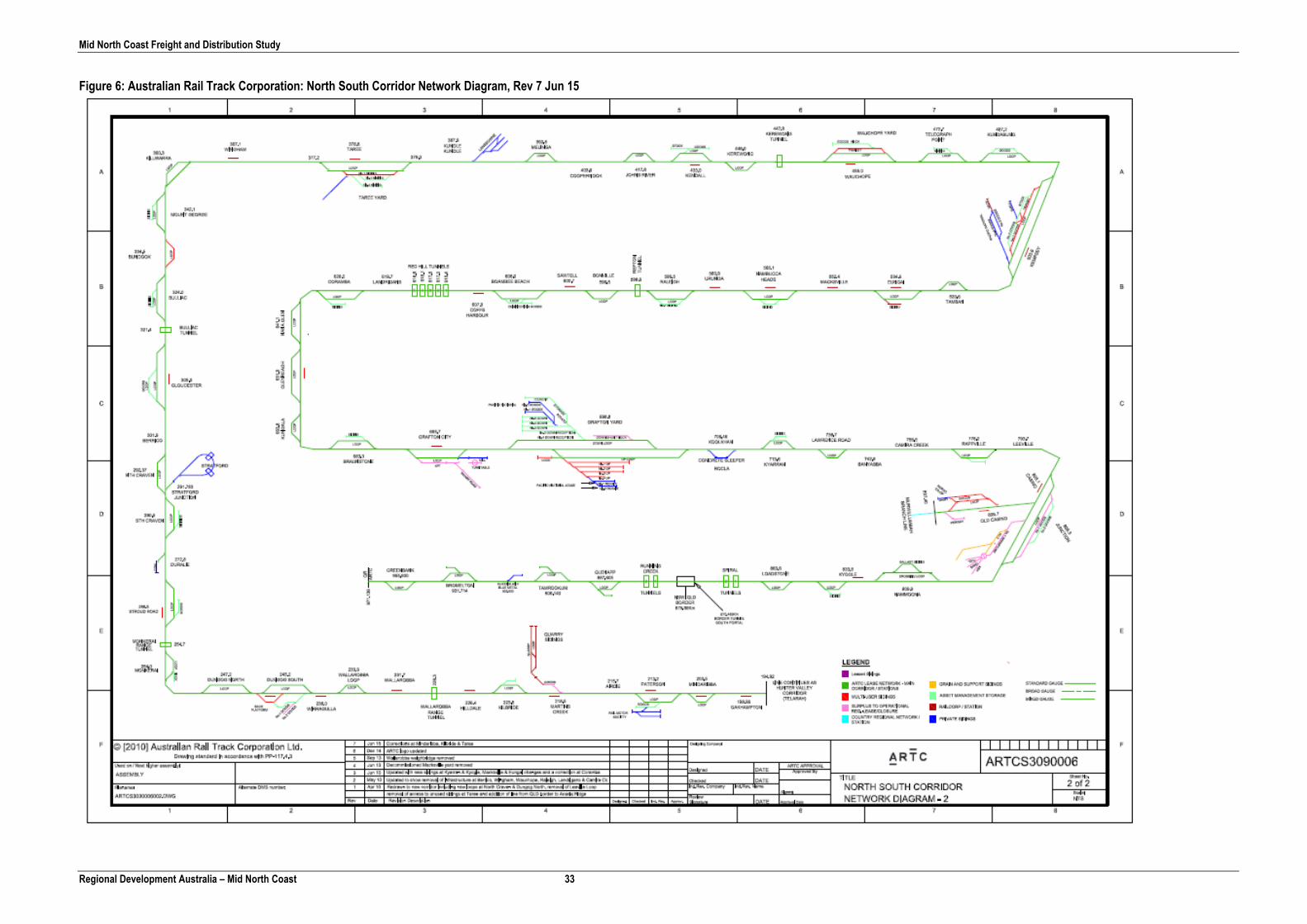

Figure 6: Australian Rail Track Corporation: North South Corridor Network Diagram, Rev 7 Jun 15

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 34

Surrounding Intermodal Terminals

In NSW there are six metropolitan intermodal terminals and 22 regional intermodal terminals. There are

7 Regional Intermodal Terminals in the regions adjoining the Mid North Coast being:

Table 15: Intermodal Terminals in Northern NSW

LGA Name Intermodal Name Status Newcastle Kooragang Is: Mountain

Industries

Sandgate: Crawfords

Kooragang Island:

Walsh Point

Carrington: Toll

Operational

Operational

Non-Operational

Operational

Richmond Valley Casino: Casino Rail

Freight Terminal

Casino: Pacific

Intermodal and Logistics

Industrial Park

Under Construction

Proposed

Tamworth Regional Tamworth (West Tamworth):

Former Hills Transport / Pacific

National site

Non-Operational

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 35

Figure 7: Intermodal Terminals in NSW

6.2 Proposed Rail Freight Transport Infrastructure

A joint Federal and State Government project is currently underway to provide an inland rail connection

between Melbourne and Brisbane. This project is described as the Australian Government’s priority

freight rail project. The project is scheduled for completion in 10 years and when complete, will

reportedly reduce transit time between Melbourne and Brisbane to 24 hours, providing a competitive

alternative to road. It is likely that much of the Melbourne – Brisbane and Sydney –Brisbane rail freight

currently transported on the coastal rail line, will be diverted to the inland rail when complete.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 36

Figure 8: Melbourne - Brisbane Inland Rail Alignment

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 37

6.3 The viability of a regional intermodal Terminal in the study area

This section provides a discussion of potential rail transport hubs on the Mid North Coast based on the

sustainability criteria outlined in Section 2.

Intermodal Terminal Viability Checklist

1. Volume

Is the aggregated volume in the catchment area sufficient to meet the minimum of

10,000 TEU’s per annum? (15,000 to 20,000 TEU’s per year is likely to make a

significant profit)

Is the market expected to grow significantly?

A summary of the mode share analysis is provided as Table 16. The data illustrates that the volume of

both inbound and outbound freight for the Mid North Coast meets the minimum 10,000 TEU volume

under a 15% mode share in 2011 and the 10% and 15% mode share in 2031.

Table 16: Evaluating Contestability - Summary

Outbound Freight (TEU’s) Inbound Freight (TEU’s)

2011 2031 2011 2031

5% Mode Share 4,108 6,487 3,985 6,910

10% Mode Share 8,216 12,975 7,970 13,820

15% Mode Share 12,325 19,462 11,956 20,731

Limitations with the data:

1. Approximately half of the outbound freight volume is made up of forest products. The forest

product industry is reported to be highly variable as production can stop, start or shift focus

quickly8. Consultation with Boral Timber identified that the forest products destined for

Newcastle Port identified in this data (2908-4362 TEU) are no longer sent to this market.

2. The current mode share in NSW (less coal) is just 6.6%, thus it is considered a 5% mode share

is more likely than a 10% or 15% mode share – based on data for the Mid North Coast as a

whole.

8 Transport for NSW, 2015. Containerised Cargo Assessment, Northern NSW.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 38

2. Distance

Is the location sufficiently distant (ie. 250-300 kilometres) from port? This distance

is required for a rail-based service to compete successfully with a direct road

service.

Are the customers physically dispersed so that moving goods via the terminal is an

attractive option?

The distance between the northern and southern boundary of the study area is approximately 280kms.

Intermodal terminals have a catchment radius of approximately 100kms, suggesting 2 terminals could

be possible based solely on catchment distances.

Destination markets need to be at least 250-300kms for rail to compete successfully with road. The

most significant origins and destinations are Newcastle, Sydney and Brisbane. The distance to

Newcastle ranges from 165kms - 416kms from the study area, Sydney 310kms – 560kms and Brisbane

368kms– 647kms.

Depending upon the location of a terminal it is unlikely that a sufficient distance could be achieved to

attract a change of mode. Although distances will be greater than 250km-300kms, it is unlikely

commodities would be trucked to an intermodal terminal, with commodities transferred to rail, when a

truck could complete the full journey in a maximum of 7 ½ hours (based on the maximum distance

Forster to Brisbane – 647kms).

3. Initial Investment and terminal capacity

Does the terminal site have access to the rail network?

Can existing infrastructure be leveraged? (e.g.does the site incorporate former

shunting yards, freight depots, rail sidings, etc?)

Is the quality of the connecting rail network (track condition) adequate to carry the

volumes expected?

Appendix D of the NSW Freight and Port strategy identifies that in regional areas, terminals have

generally evolved around pre-existing infrastructure, often based around a company’s distribution

chain, with few green field sites being developed.

Existing rail infrastructure in the Kempsey LGA provides the most comprehensive infrastructure for

utilisation, should an intermodal terminal be pursued.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 39

4. Seasonality

If volumes are seasonal, will the terminal generate sufficient revenue to cover

capital and operating costs during periods when volume throughput is low?

Does the terminal have sufficient capacity to accommodate volume throughput at

seasonal peaks?

Can the intermodal service accommodate time or temperature-sensitive freight?

The outbound freight task on the Mid North comprises 50% Forest products (2011 data). Transport for

NSW (2015) advises that Forest Products can be considered highly variable as production can stop,

start or shift in focus quickly. Given the uncertainty of production, shippers are often reluctant to fund

long term investments in their supply chain. Instead when they are active, their output can be

considered a windfall for existing operators8.

The variable nature of such a large portion of the Mid North Coast outbound freight task, represents a

significant risk to the development of an intermodal freight terminal on the Mid North Coast. It is

considered this represents a major limiting factor to the establishment of an intermodal terminal in the

study area.

5. Competing Channels

Is the terminal part of an integrated supply chain that can offer a unique service to

the customers in the catchment area?

Will the terminal be the only intermodal terminal in the catchment area?

Can the terminal / supply chain compete effectively with alternative supply chains

vying for business in the same market?

The most significant competition for the rail freight market on the Mid North Coast is the flexibility,

speed and cost competitiveness of the road freight market. The commodity types making up the freight

task are better suited to flexible road transport. In addition the origin – destination distances are

considered insufficient to attract a shift to rail.

6. Economic and social impact

Do the local and regional community objectives align with the development

objectives for the terminal?

Councils on the Mid North Coast are very supportive of transport infrastructure investment as a means

of attracting industry and increasing employment in the region. Improved freight transport infrastructure

aligns with this objective.

Mid North Coast Freight and Distribution Study

Regional Development Australia – Mid North Coast 40