Mid-Atlantic Mutual Advantage Patient Protection and Affordable Care Act 2015 Small Employer Focus...

54

Mid-Atlantic Mutual Advantage Patient Protection and Affordable Care Act 2015 Small Employer Focus August 4, 2015 Nemacolin Woodlands Resort FARMINGTON, PENNSYLVANIA

-

Upload

victoria-beasley -

Category

Documents

-

view

214 -

download

0

Transcript of Mid-Atlantic Mutual Advantage Patient Protection and Affordable Care Act 2015 Small Employer Focus...

Mid-Atlantic Mutual Advantage

Patient Protection and Affordable Care Act2015 Small Employer Focus

August 4, 2015

Nemacolin Woodlands

ResortFARMINGTON, PENNSYLVANIA

Welcome and Introduction

ROB BERGERCentral Pennsylvania Association of Health Underwriters

Immediate Past President

Benecard NVA

Director, Sales

[email protected] | 717-215-4750

2

Legal Disclaimer

The contents of this presentation should not be construed as legal or tax advice, or a legal or tax opinion on any specific facts or circumstances. These materials are intended for general information purposes only, and you are urged to consult a lawyer or tax counsel concerning your own situation and any specific legal questions you may have.

3

Agenda

ACA History What’s Happening Now

Skinny Plans / Minimum Value Plan Notice 2015-17 Supreme Court Decision

What’s Coming Next Age Banding for Mid-Market – 50-99 Cadillac Tax

Question and Answer Bad Television…

4

5

History

In March 2010, Congress passed Health Care Reform Legislation Patient Protection Affordable Care Act PPACA, ACA, HCR

Purpose was to cover the uninsured Just under 50 million uninsured in 2010 That number has declined since CURRENT UNINSURED

How do you cover the uninsured? Expand Medicaid Provide $ to make it easier to acquire insurance Remove barriers – pre-existing conditions Create “incentives” – penalties/taxes

6

Carrots and Sticks

Carrots Subsidies – free money

Sticks Individual mandate penalty

Essentially honor system Employer shared responsibility penalties – pay or play

7

Subsidies

If you earn between 138% and 400% of FPL eligible for “free” money to buy insurance Must purchase on the exchange/marketplace Must not have other coverage (adequate and affordable)

available to you Premium Subsidies (HHI)

Advanced premium tax credit Cost sharing subsidy

8

Subsidies for Whom

Advanced Premium Tax Credits HHI < 400% of Federal Poverty Level (FPL) Indexed to family size

Members in Household 2015 Household Income - FPL

1 $47,080

2 $63,720

3 $80,360

4 $97,000

5 $113,640

9

Individuals

Effective 1/1/2014 all US citizens must procure MEC MEC = Minimum Essential Coverage Group health plans, Medicaid, Tri-Care, Medicare, CHIP,

Exchange plans Adults who fail to obtain coverage =>

penalty/tax/shared responsibility

10

Individual Penalty

Individual penalty/tax/shared responsibility is the greater of 2014: $95 or 1% of household MAGI 2015: $325 or 2% 2016: $695 or 2.5% Indexed thereafter… Penalties for dependents too!

11

Employer Shared Responsibility

Applicable Large Employer (ALE) is subject to an assessable payment (PENALTY) if: Fails to offer minimum essential coverage (MEC) to 95% (70% in

2015) of FT employees (and dependents) or The coverage does not meet Minimum Value {Adequate} or the

coverage costs more than 9.5% income {Affordable} AND An employee receives a subsidy (Premium Tax Credit or Cost

Sharing Subsidy)

12

Pay or Play Penalty

MEC Coverage Penalty (“Pay”) Failure + Subsidy certification yields a monthly penalty

Count all Full Time Employees (30 hours per week) Subtract the first 30 (80 in 2015) Multiply by $166.66 ($2,000 per year – indexed, when?)

Adequate and Affordable (“Play”) Failure + Subsidy certification yields a monthly penalty

Count all the affected Employees Multiply by $250.00 ($3,000 per year – indexed)

13

About the Uninsured…

U.S. Census Bureau 49.9 million residents, 16.3% of the population, were uninsured

in 2010 Kaiser Family Foundation

Nearly half of the approximately 30 million adults who remained uninsured were eligible for assistance under the law

~11 million adults newly insured by 12/15/2014 Gallup Poll

~87% in exchanges receive subsidies - can only afford insurance. Something like 8.2 million people in 34 states are in that boat.

14

15

Skinny Plans

Intended to avoid $2,000 penalty Meets MEC, but not adequate/affordable

Very inexpensive Can be combined with a buy-up option to meet

adequate requirement (minimum value) What might be covered?

Preventive services Often paired with mini/limited medical

16

Minimum Value Plans

Intended to avoid all pay or play penalties Offers MEC and Minimum Value

Minimum value = 60% actuarial value Actuarial calculator met 60% without

hospitalization/physician services Not the intent of MV November 2014 Notice 2014-69 removed this option for

any plans not entered into by 11/4/14 Not an available option for 2015 moving forward

17

Notice 2015-17

Premium Payment Plans Provides relief from excise tax for small employers that

provided payment to employees for individual policies. Transition relief available through June 30, 2015 Confirmed that increased wages in lieu of employer-

sponsored health benefits is acceptable as long as the increased wages are not conditioned on the purchase of health coverage

18

Supreme Court: King v Burwell

Supreme Court ruled on June 25, 2015 (6-3) Federally Facilitated Exchange subsidies legal

What does this mean? ACA Employer Mandate remains

ALE employers moving forward with full compliance States won’t have to change marketplace structure to

access subsidies – business as usual Was the last real chance to derail a major

component of the ACA Funding

19

Supreme Court: Obergefell vs Hodges

Supreme Court ruled on June 26, 2015 (5-4) State prohibitions on same-sex marriage violate the

Equal Protection and Due Process clauses of the 14th amendment of the U.S. Constitution.

Every state must allow same-sex couples to marry Every state must recognize same-sex marriages

performed in other states.

20

Same-Sex Marriages

What does this mean for benefits? No guidance yet - how or when this will be implemented Should bring consistency to employers with employees

in multiple states No reason to wait to implement additional spousal

coverage and taxation benefits, but no legislated due date

EEOC Guidance on Wellness

Employer Wellness programs are an exception to ERISA and ACA expanded some of those provisions

EEOC has never provided guidance and has been an uncertain area since EEOC enforces ADEA Guidance supports much of ACA These are proposed and they are open for comment

through June 19, 2015

EEOC Guidance on Wellness

Highlights EEOC’s concern is that incentives/rewards will be so

valuable employees coerced to participate Does not require participation Does not deny coverage under any of its health plans for

non-participation Does not penalize non-participation (other than failure to

receive reward) When part of group health plan a notice must be provided

EEOC Guidance on Wellness

Notice Requirements Describes medical information captured Who will receive it How the information will be used Restrictions on its uses The methods the covered entity will employ to prevent

improper disclosure of medical information Confirms the maximum incentive is 30% of total cost

of employee only coverage

25

Small Group Definition

1/1/2016 small group definition changes 50 employees to 100 for underwriting purposes

Applicable Large Employer (ALE) does not change – remains at 50 full time equivalent

employees subject to pay or play mandate

26

Mid Market Impact

1/1/2016 groups of 50-99 subject to small group underwriting

Underwriting rating factors limited to: Age (from 1:5 to 1:3) Geography Tier or Family Size Tobacco Usage (50% surcharge)

No Medical Underwriting Member specific rates based on above factors vs tiered

rates27

What does this mean?

Some employers will benefit from the new methodology and others won’t.

Other criteria that are eliminated: Gender SIC codes Composite Medical Underwriting

So, many employers must benefit, right?

28

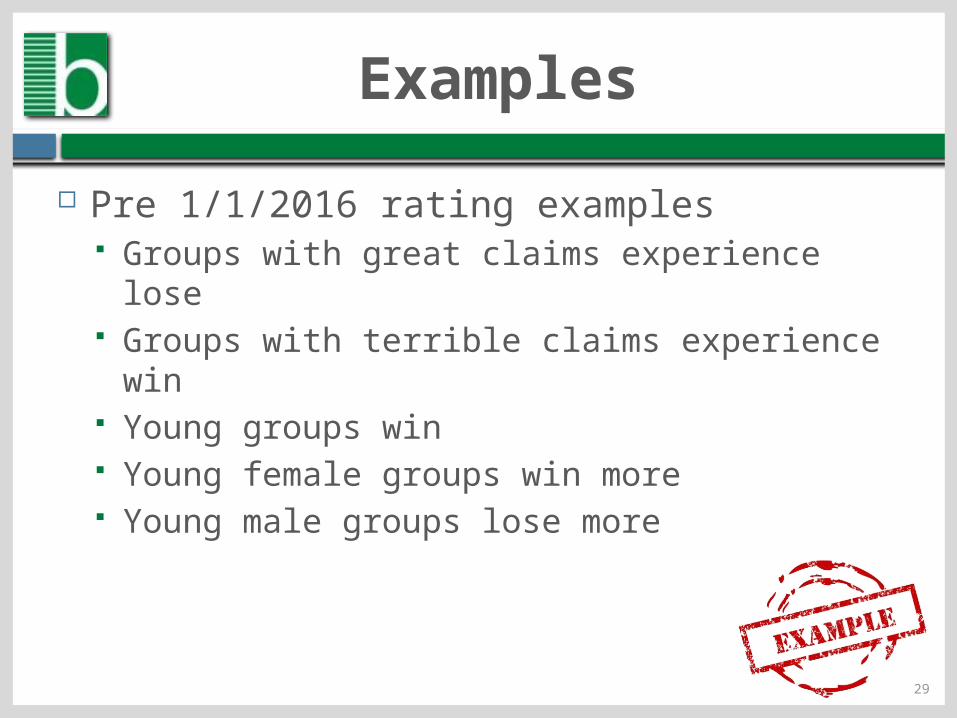

Examples

Pre 1/1/2016 rating examples Groups with great claims experience lose Groups with terrible claims experience win Young groups win Young female groups win more Young male groups lose more

29

Age Consideration

No Composite Rates Each individual in the group will have a rate based on

their age and the ages of their family members (if covered)

Ratio compressed from 1:5 to 1:3 younger employees will most likely have a greater

increase than older employees Rob, what’s that you said about ADEA & EEOC?

30

Fees & Taxes: The List

MEC & Pay or Play : 6055/6; 1094 & 1095-C/B Cadillac Tax PCORI Transitional Reinsurance Health Insurance Industry Fee Risk Adjustment Program Health Insurance Marketplace Fee

32

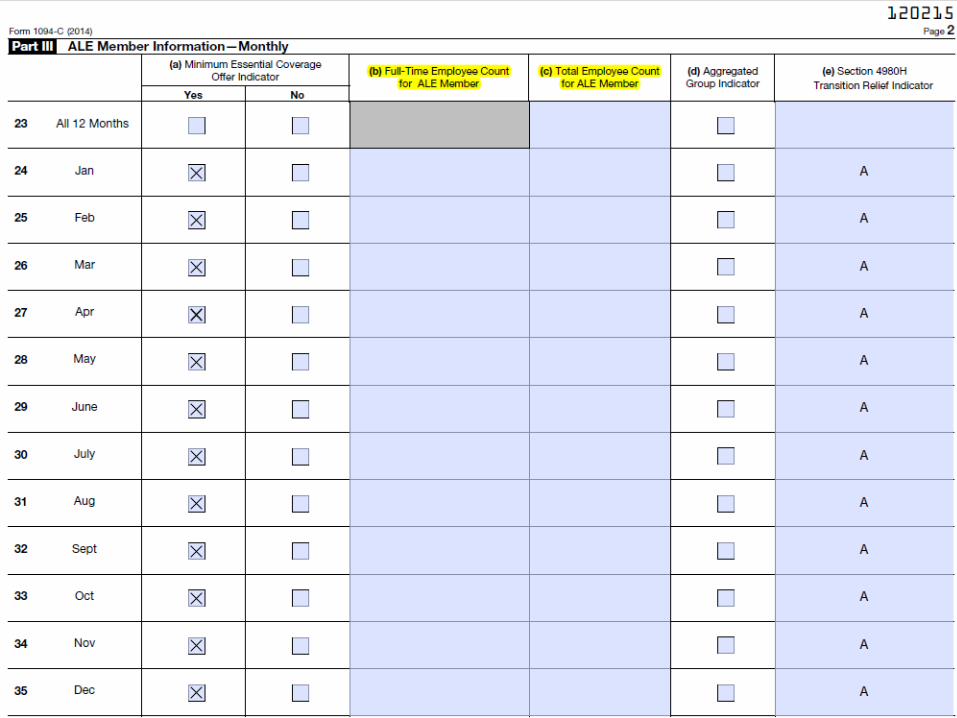

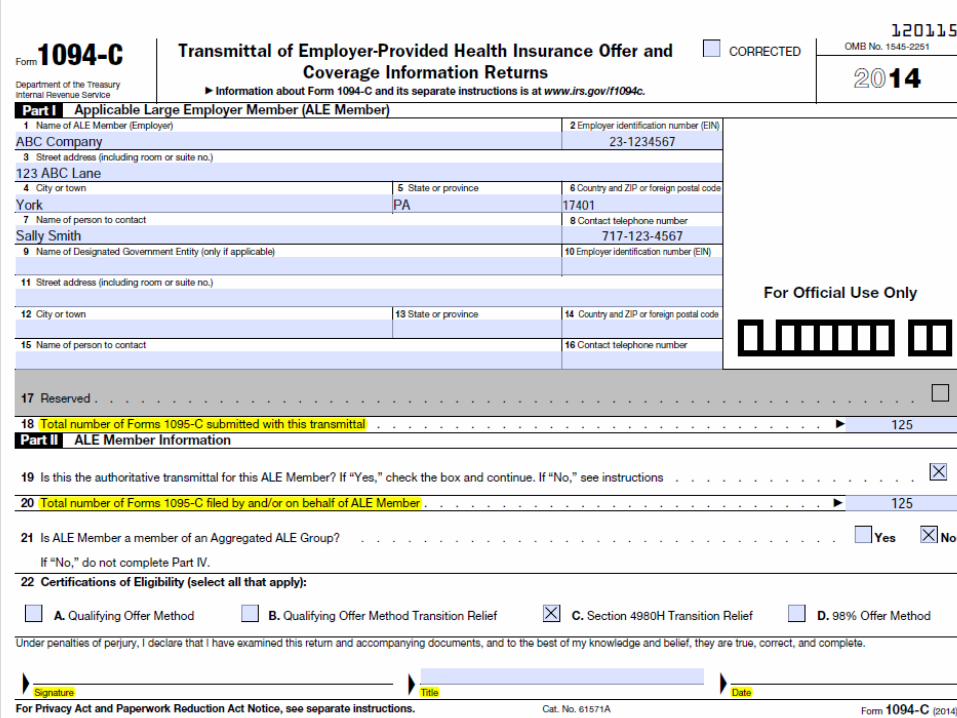

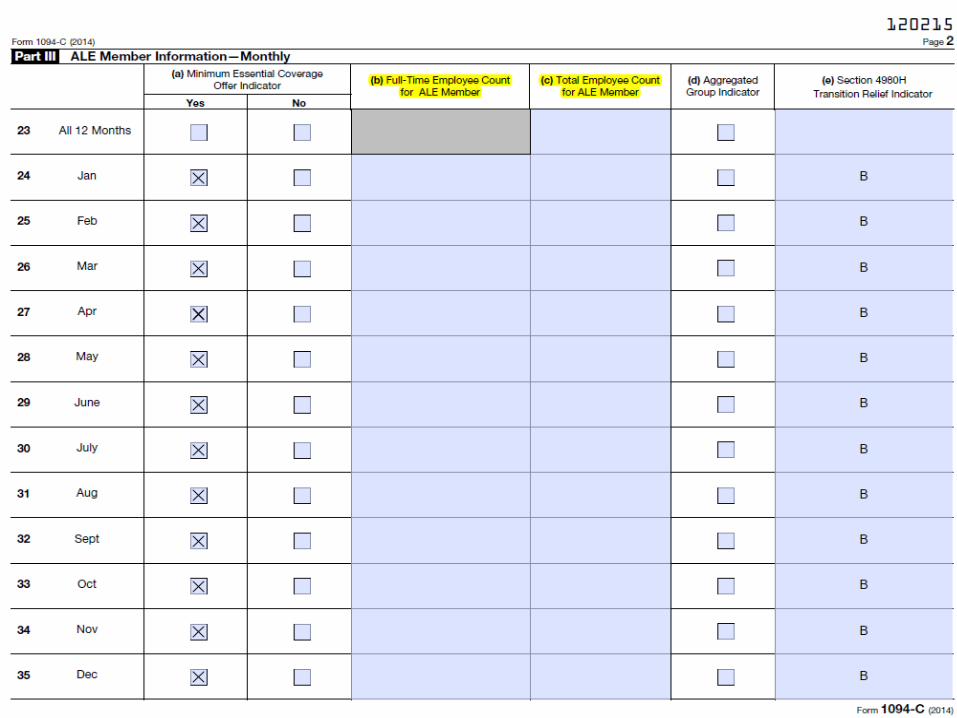

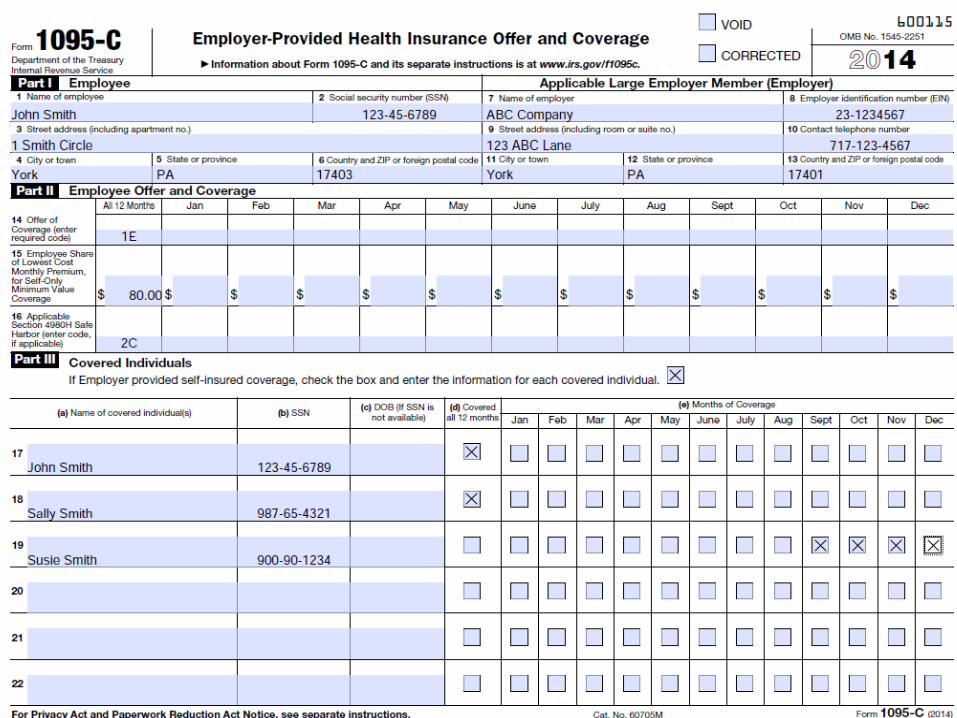

Pay or Play Reporting

Final Forms and Instruction for Employer Reporting 6055 and 6056

Reporting MEC (self-funded employers) Reporting “pay or play”

Forms 1094/1095-C or 1094/1095-B Employers should be evaluating process, data

required and vendor support

33

Cadillac Tax

Cadillac Tax – Not Going Away Proposed regulation issued – February 23, 2015 40% Excise tax on high cost employer-sponsored health

coverage Effective for calendar years starting in 2018

Tax based on calendar year, so for fiscal plan years need to evaluate the plan beginning in 2017.

34

Cadillac Tax

Applicable Dollar Limits - $10,200 single/$27,500 non-single – will be indexed Coverage includes Group health plans

FSA, HSA, Archer MSA, HRA On-site clinics, executive physical programs

35

Cadillac Tax

Who pays what Employer calculates the tax based on all lines of

coverage Prorates the tax based on insured products (carriers) and

other benefits provided by the employer (FSA, HRA, HSA, etc.)

Tax is on the amount over the applicable dollar limits.

36

PCORI

PCORI - Comparative Effectiveness Fee or the Patient Centered Outcomes Research Fee (10/2019)

Who: Insured, self insured health plans Grandfathered, retiree-only & government entity plan, HRA NOT Stop loss or indemnity reinsurance plans, FSA HRA provided with a fully insured health plan $2.08 /covered member < 10/1/2015, indexed each year

thereafter Insured plans paid by insurance, self funded plans by Plan

Sponsor (Employer)

PCORI - How is Fee Calculated?

There are several acceptable methods for calculating the number of “lives covered” Actual Count – Average of lives for each day of the year Snapshot Method – Average for a single day each

quarter 5500 Method – Average of number of lives on 5500

For HRAs integrated with a fully insured plan, there is an exception that permits employers to pay only on the number of employees, no dependents.

38

PCORI - Due Date and Filing

The fee must be paid annually on Form 720 Due by July 31st of the year following the plan year’s

end For example: Calendar year plan ending 12/31/14

would be required to file by 7/31/15. A Plan ending March 31, 2015 would file by July 31, 2016

PCORI fee is tax deductible

39

Transitional Reinsurance

Transitional Reinsurance Program will reduce the uncertainty of insurance risk by partially offsetting issuers’ risk associated with high-cost enrollees.

The program is effective from 2014-2016.

40

Transitional Reinsurance

Self-funded major medical group health plans are subject to fee (No HRA’s or FSA’s) Calculation methods are similar to PCORI except:

Based on calendar year, not plan year Based on ¾ of year, not entire year (Jan – Sept)

Different from PCORI For self funded plans – TPA may pay on behalf of plan

sponsor Payment – submit the number of covered lives

electronically through www.pay.gov with EFT payment information

41

Transitional Reinsurance

Payment in 2014 Filing due 11/15/14 (lots of extensions in 2014) Amount = $63.00 / covered life if combined payment,

due 1/15/15 OR $52.50 / covered life due 1/15/15 and $10.50 / covered

life due 11/15/15 Is deductible as a normal business expense 2015 - $44 per covered life 2016 - $27 per covered life

42

Other Fees Carrier Paid

Annual Health Insurance Industry Fee Begins in 2014 and continues Estimated to be in the 2-4% of premium range

Risk Adjustment Program and Fee Paid on individual and small-group markets Begins in 2014 and continues Estimated to be $.08 PMPM

43

A good note…

Big tumult is over Nothing big in SCOTUS land Economics will now do its thing

Commonwealth exchange Vermont single-payer Oregon & Hawaii exchanges closed

There are no bad risks, just bad rates

44

Questions

45

Variable Hour Example

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecONGOING Measurement Period - Nov 1 - Oct 31 Stability Period - Jan - Dec.

Measurement Period Nov 1 - Oct 31 Stability Period - Jan - Dec.

NEW HIRE - March 1, 2013Initial Measurement Pd Mar - Feb AdminStability Period - Apr - MarMeasurement Period Nov 1 - Oct 31 Stability Period - Jan - Dec.Admin Pd

2014 2015 2016

Admin PdAdmin Pd

Initial Measurement Period - DOH - 12 months laterInitial Stability Period - 1st of the Month following the 12 months after DOH - 12 monthsInitial Admin Period - 30 Days from end of Initial Measurement PeriodOngoing Measurement Period - Nov - OctOngoing Stability Period Jan-DecAdmin Period - Nov-Dec