Microsoft word new base 998 special 09 february 2017 energy news

26

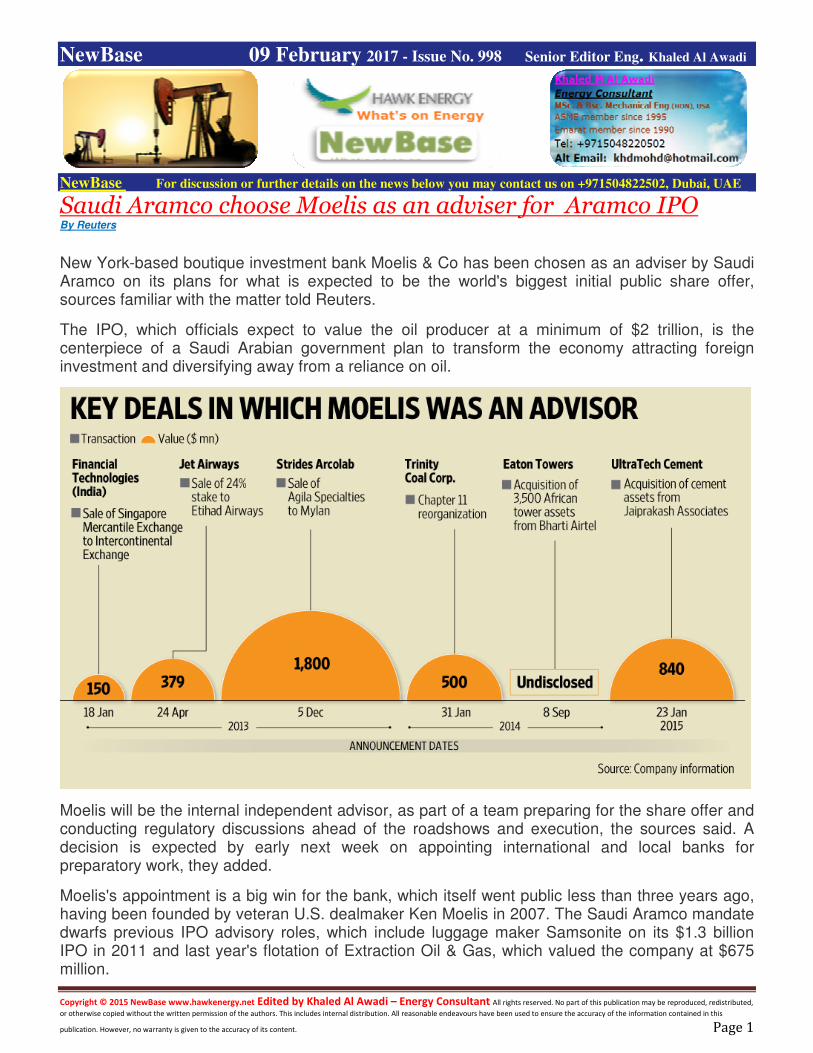

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this publication. However, no warranty is given to the accuracy of its content. Page 1 NewBase 09 February 2017 - Issue No. 998 Senior Editor Eng. Khaled Al Awadi NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE Saudi Aramco choose Moelis as an adviser for Aramco IPO By Reuters New York-based boutique investment bank Moelis & Co has been chosen as an adviser by Saudi Aramco on its plans for what is expected to be the world's biggest initial public share offer, sources familiar with the matter told Reuters. The IPO, which officials expect to value the oil producer at a minimum of $2 trillion, is the centerpiece of a Saudi Arabian government plan to transform the economy attracting foreign investment and diversifying away from a reliance on oil. Moelis will be the internal independent advisor, as part of a team preparing for the share offer and conducting regulatory discussions ahead of the roadshows and execution, the sources said. A decision is expected by early next week on appointing international and local banks for preparatory work, they added. Moelis's appointment is a big win for the bank, which itself went public less than three years ago, having been founded by veteran U.S. dealmaker Ken Moelis in 2007. The Saudi Aramco mandate dwarfs previous IPO advisory roles, which include luggage maker Samsonite on its $1.3 billion IPO in 2011 and last year's flotation of Extraction Oil & Gas, which valued the company at $675 million.

-

Upload

khaled-al-awadi -

Category

Business

-

view

148 -

download

2

Transcript of Microsoft word new base 998 special 09 february 2017 energy news

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 1

NewBase 09 February 2017 - Issue No. 998 Senior Editor Eng. Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE

Saudi Aramco choose Moelis as an adviser for Aramco IPO By Reuters

New York-based boutique investment bank Moelis & Co has been chosen as an adviser by Saudi Aramco on its plans for what is expected to be the world's biggest initial public share offer, sources familiar with the matter told Reuters.

The IPO, which officials expect to value the oil producer at a minimum of $2 trillion, is the centerpiece of a Saudi Arabian government plan to transform the economy attracting foreign investment and diversifying away from a reliance on oil.

Moelis will be the internal independent advisor, as part of a team preparing for the share offer and conducting regulatory discussions ahead of the roadshows and execution, the sources said. A decision is expected by early next week on appointing international and local banks for preparatory work, they added.

Moelis's appointment is a big win for the bank, which itself went public less than three years ago, having been founded by veteran U.S. dealmaker Ken Moelis in 2007. The Saudi Aramco mandate dwarfs previous IPO advisory roles, which include luggage maker Samsonite on its $1.3 billion IPO in 2011 and last year's flotation of Extraction Oil & Gas, which valued the company at $675 million.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 2

But senior dealmakers at the bank, which has offices across the world, have been working on winning a role with Saudi Aramco for years, according to a source familiar with the matter. The bank has an experienced team of advisers based in the Middle East, making its name in the region by advising the Dubai government on the $25 billion debt restructuring of conglomerate Dubai World in 2011.

Local and major international banks including Morgan Stanley , HSBC, Citi were among those that had been asked to pitch for an advisory position with Aramco three weeks ago, Saudi-based industry sources said last month.

Wall Street bank JPMorgan and independent boutique bank Michael Klein had already been picked to advise the country ahead of any listing. Generally government work across the world is poorly paid, but banks often vie for the contracts simply to build a relationship with the state in the hope of getting future business.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 3

The listing of Aramco is slated to take place in 2018, so the appointment of banks to run the share sale as lead managers and book runners is still some way off, the sources said. Saudi Energy Minister Khalid al-Falih said last week the company was evaluating concurrent listings on more than one exchange. A Moelis spokesperson declined to comment and Saudi Aramco was not immediately available to comment.

The world’s most valuable company isn’t Apple or Google’s owner, Alphabet. It’s an outfit in a league of its own: Aramco, as Saudi Arabian Oil Co is better known. This sprawling state-owned producer, sitting atop one-fifth of the globe’s petroleum reserves, pumps more crude than the top four publicly traded oil companies combined. It’s valued at more than $2tn — or about four times the biggest technology giants — though no one really knows what it’s worth because its profits are shrouded in secrecy. The veil could soon be lifted as the Saudi government is planning a partial privatisation of Aramco to create a war chest and prepare the country for the post-hydrocarbon age.

The Situation

The government intends to sell up to 5% of Aramco in 2018, most likely in the second half. The sale’s estimated size of about $100bn would make it the biggest-ever initial public offering, dwarfing the $25bn raised by Chinese Internet retailer Alibaba in 2014.

Bankers are lining up to reap a bonanza of fees. Proceeds from the Aramco sale would bulk up a sovereign wealth fund at the centre of a drive to diversify the economy, a goal that’s gained urgency since the price of crude tumbled from more than $100 a barrel in 2014 to about half that level.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 4

Deputy Crown Prince Mohammed bin Salman’s drive to create jobs for millions of unemployed Saudis in manufacturing, tourism and other fields is seen as crucial to the kingdom’s economic planning.

The company will face unprecedented scrutiny: Disclosures needed to trade Aramco shares on overseas exchanges may include the first independent audit of the kingdom’s reserves and details about its production capacity.

Aramco is considering selling shares in London, New York, Tokyo, Hong Kong or even Canada, as well as the domestic market. Chief executive officer Amin Nasser says the company may list on two or three exchanges and, to make the sale more attractive to investors, Saudi Arabia will reduce the company’s overall tax rate.

The Background

Explorers from the Rockefeller family’s Standard Oil empire first struck oil in Saudi Arabia in 1938. The venture became known as Arabian American Oil and went on to discover Ghawar field, still

the world’s largest onshore deposit. In 1980, the Saudi government bought out the original shareholders, all of them forebears of Exxon Mobil or Chevron, and renamed the company.

Aramco has fuelled decades of prosperity for Saudi Arabia. It generates almost 90% of government income and built the refineries, petrochemical plants and other infrastructure that form the backbone of the world’s 15th-biggest economy.

Saudi Arabia has been the de facto leader of the Organisation of Petroleum Exporting Countries, or Opec, since the group was founded in 1960. It’s often called the “swing producer” because decisions to increase or trim Saudi output drive the price of oil. Saudi crude accounts for about 1 out of every 9 barrels of global production and can be extracted for about a third of the cost of

reserves in the US over the decades.

The Argument

Prince Mohammed’s plan envisions the Aramco IPO as the centrepiece of Saudi Arabia’s biggest economic shakeup since the founding of the country in 1932. Although details of what exactly will be sold remain unclear, Nasser said the IPO will be based on Aramco maintaining the so-called concession, which gives it the right to exploit the kingdom’s oil and gas reserves.

For the biggest oil economy, the clock is ticking. Even with the world’s shift to cleaner fuels, oil is expected to continue providing about a third of world energy for the next two decades. Aramco’s IPO will put a price tag on the future of petroleum just as Saudi Arabia is fixing its sights on the end of its own oil age.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 5

Qatar’s austerity drive to continue inspite improving state finances, minister says… Gulf time

Pressure on Qatar’s state finances is easing because of higher oil prices and the government may not need to issue an international bond this year, but it is still seeking ways to save money, finance minister Ali Sherif Al Emadi said on Tuesday.

"We may not issue a bond this year given where oil prices are – right now we are close to break–even," Mr Emadi said in a briefing on the financial outlook for the world’s top liquefied natural gas exporting nation.

Qatar’s last international bond issue was a US$9 billion sale last May. Mr Emadi said another issue was an option in the 2017 budget, but no decision had been made on whether to exercise it.

His comments illustrated how higher oil prices are to varying degrees improving the outlook for oil and gas exporting countries around the Gulf. Brent oil averaged $45 a barrel last year but is now trading around $55.

Qatar’s 2017 budget, announced in mid–December, projected its deficit would shrink to 28.3 billion riyals from 46.5bn riyals planned for 2016. Since the 2017 budget assumed an average oil price of about $45, the deficit is now close to disappearing, Mr Emadi said.

However, he made clear that an austerity drive would continue. The 2017 budget envisages spending will drop to 198.4bn riyals, 2 per cent lower than the 2016 plan, because of a 9 per cent cut in government operating expenses and a 1.5 per cent fall in the total salary bill.

"We are becoming more efficient on the operating side of the government but we need to do more on investment and the capex side," Mr Emadi said.

For the sake of fiscal discipline, Qatar will not use assets from its sovereign wealth fund to fund its deficit, and the government is scaling back state projects which it thinks the private sector can handle instead, he said.

In the past 18 months, between $8bn and $9bn of such projects were given to the private sector, he added without elaborating.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 6

Mr Emadi said the government was spending close to half a billion dollars a week on capital projects, focusing on preparations to host the 2022 World Cup football tournament. Ninety per cent of World Cup projects have been awarded and two–thirds of them will be delivered in the next 24 months, he said.

He predicted Qatar’s economy would grow 3.4 or 3.5 per cent this year. It will face a drag in 2018 when Qatar, along with other countries in the region, introduces a value–added tax to boost non–oil revenues; mr Emadi estimated the tax would absorb between 1 and 2 per cent of gross domestic product.

Also, the country’s population, which has been swollen by foreign workers on infrastructure projects, is expected to peak between 2017 and 2019, Mr Emadi said. However, officials believe government projects will underpin growth until the World Cup and are adjusting spending plans to ensure there is no sudden reduction in economic stimulus after 2022.

"What we’re trying to do is really prioritise 2022, so we have a good and moderate growth rate … After (2022) it will mainly be infrastructure projects. The airport can have some sort of expansion and part of the rail (network) can have some sort of expansion. We have highways that need to be done after 2022, the sewage system."

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 7

Namibia: BW Offshore farms into Kudu field, offshore Namibia Source: BW Offshore

BW Kudu (a wholly owned subsidiary of BW Offshore) has entered into a Farm-Out Agreement for a 56% stake of the Kudu licence offshore Nam ibia. National Petroleum Corporation of Namibia (NAMCOR), the Namibian state-owned oil company, will hold the remaining 44% of the licence.

BW Kudu will become operator of the Kudu licence. BW Kudu will pay for past costs upon transfer of the field interest to the company. The final investment decision is planned for Q4 2017.

'BW Offshore will now start the work with the Namibian government, NAMCOR, NamPower (the Namibian power utility), large infrastructure investors and other stakeholders to get this very exciting project to FID' said Carl K. Arnet, CEO of BW Offshore.

The Kudu field was discovered by Chevron in 1974 approx. 170 km off the coast of Namibia. A further seven appraisal wells have been drilled since then by various oil companies including Shell and Tullow who subsequently withdrew from the project.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 8

The Kudu field is estimated to contain 1C-2C-3C Contingent Resource range within the main reservoir ('K3') of 755-1330-2308 Bscf respectively. The Kudu Gas to Power project calls for gas to be produced by a Floating Production Unit before being exported by pipeline to a new 885 MW gas to power plant onshore Namibia.

'Kudu represents another opportunity for BW Offshore to take a proactive development role in a project that will produce for 15-25 years. Falling development costs after the 2014 drop in oil prices has helped in making the project economically feasible.

The electricity generated by the power station will reshape electricity supply in south-western Africa, providing a secure long-term supply to support the development of Namibia and potentially neighboring countries', added Carl K. Arnet.

NAMCOR's Managing Director Immanuel Mulunga said the project will play a fundamental role in shaping the energy dynamics of Namibia. 'The Kudu Gas-to- Power Project is a key strategic power generation project for Namibia, which will significantly reduce reliance on imported power while at the same time accelerating economic development.'

He further remarked that the project has the potential of strengthening Namibia's international standing: 'The Kudu Gas to Power Project will not only enable Namibia to entirely cater for its own power needs but become a net exporter of power to regional markets'.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 9

U.S. Oil Output Heads to 48-Year High as Shale Surge Resumes By Mark Shenk

The U.S. will pump the most crude next year since 1970 as domestic producers benefit from OPEC supply cuts.

Domestic output will average 9.53 million barrels a day in 2018, the Energy Information Administration said in its monthly Short-Term Energy Outlook released Tuesday. Shale explorers are benefiting from prices that rose above $50 a barrel after the Organization of Petroleum Exporting Countries and 11 other nations agreed to trim production in an effort to ease a global supply glut.

"Shale operators are more bullish with crude trading above $50," Michael Lynch, president of Strategic Energy & Economic Research in Winchester, Massachusetts, said by telephone. "I’m sure that from Riyadh to Caracas people in oil ministries are watching the U.S. rig count with avid interest and a bit of dismay."

U.S. oil drillers boosted the rig count by 17 to 583 last week, the most since October 2015, according to Baker Hughes Inc. The country will produce 8.98 million barrels this year, little changed from last month’s EIA forecast. The biggest increase in output will come from the lower 48 states, where cost reductions have allowed explorers to produce profitably in some areas like the Permian Basin of West Texas at $50 and below.

This year’s supply cuts by OPEC and other nations will bring the market into balance. Global oil demand will rise to 98.09 million barrels a day this year, compared with production of 98.03 million.

World Balance

“Global oil supply and demand is now expected to be largely in balance during 2017 as the gradual increase in world oil inventories that has occurred over the last few years comes to an end,” EIA Acting Administrator Howard Gruenspecht, said in an e-mailed statement. “Improved economic growth in both developed and emerging market countries is expected to contribute to higher global oil demand over the next two years.”

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 10

Angola: Eni starts production of the East Hub Development Project, deep offshore Angola, ahead of scheduleSource: Eni

Eni has started production of the East Hub Development Project, in Block 15/06 of the Angolan deep offshore, ahead of development plan estimates and with a time-to-market among the best in the sector.

Production is taking place through the Armada Olombendo Floating Production Storage and Offloading (FPSO) vessel, which can generate up to 80,000 barrels of oil per day and compress up to 3.4 million cubic meters of gas per day. With 9 wells and 4 manifolds at a water depth of 450 meters, the FPSO Olombendo will put into production the Cabaça South East field, 350 kms northwest of Luanda and 130 kms west of Soyo.

Eni starts production of the East Hub Development Project, deep offshore Angola, ahead of schedule

Production from the East Hub Project will add to production from the existing West Hub Project in the Sangos, Cinguvu and Mpungi fields, where another vessel, the FPSO N’Goma, is operating. In total, Block 15/06 will reach a peak of 150,000 barrels of oil per day this year.

'We are proud of what we have achieved in Block 15/06,' said Eni CEO Claudio Descalzi. 'Leveraging our extensive experience in exploration, we have been able to discover a total of 3 billion barrels of oil in place through 10 commercial discoveries. Moreover, thanks to strong field development and project management, we are beginning production of the East Hub with a time-to-market of only 3 years, and 5 months ahead of schedule. Cabaça South East brings our number of fields in production to 5, with 2 more expected to start before the end of 2018. This is

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 11

yet another example of Eni’s Angolan and worldwide capability to deliver state-of-the-art projects, and was made possible by Eni’s new operational model, where we play an increasingly active role in the integrated development of our projects.'

Location of East and West Hub developments in Block 15/06 (Source: Eni)

Block 15/06 is operated by Eni with a 36.84% share, while Sonangol Pesquisa e Produção controls 36.84% and SSI Fifteen Limited controls 26.32%. Eni has been present in Angola since 1980 through its subsidiary Eni Angola. Equity production amounted to 124,000 barrels of oil equivalent per day in 2016.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 12

NewBase 09 February 2017 Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Oil stable after drop in U.S. gasoline stocks, but market remains bloated Reuters + NewBAse

Oil prices stabilized on Thursday, boosted by an unexpected draw in U.S. gasoline inventories, although bloated crude supplies meant that fuel markets remained under pressure. Brent crude futures LCOc1, the international benchmark for oil prices, were trading at $55.27 per barrel at 0137 GMT, up 15 cents from their last close. U.S. West Texas Intermediate (WTI) crude CLc1 was up 14 cents at $52.48 a barrel.

The U.S. Energy Information Administration (EIA) said on Wednesday that gasoline stocks USOILG=ECI fell by 869,000 barrels last week to 256.2 million barrels, versus analyst expectations for a 1.1 million-barrel gain. Traders said that this surprise increase in U.S. gasoline inventories had helped push up crude, though most added that fuel markets were still bloated and that this would likely prevent further big price rises. "We remain highly skeptical of the overnight price action," said Jeffrey Halley, senior market analyst at futures brokerage OANDA, referring to rising crude. U.S. commercial crude inventories soared by 18.8 million barrels to 508.6 million barrels, according to the EIA. U.S. bank Goldman Sachs said that high fuel inventories as well as rising U.S. crude production mean that oil markets will remain over-supplied for some time.

Oil price special

coverage

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 13

"The 4Q16 global oil market surplus led to further rises in global inventories in January, and as a result the draws that we expect will start from a high base," the bank said. "U.S. production has also rebounded faster than our rig modeling suggested...and we view the faster shale rebound as creating downside risk to our 2018 WTI price forecast of $55 per barrel, but not to our expectation that the global oil market will shift into deficit in 1H17," it added. Ongoing high inventories undermine efforts by the Organization of the Petroleum Exporting Countries and other producers including Russia to cut output by almost 1.8 million bpd during the first half of this year in order to prop up prices and rebalance the market. As a result, both Brent and WTI are down around 5 percent since early January, when the OPEC-led cuts started to be implemented. Jump in US crude imports to reverse in March

The recent jump in U.S. crude imports could reverse from March as major oil exporters start cutting production, Goldman Sachs analysts said in a note.

The latest Energy Information Administration (EIA) report released on Wednesday found that U.S. crude inventories surged in the week ended Feb 3 by 13.8 million barrels – the second largest weekly build up on record.

However, the rise did not shock the market, since preliminary data from the American Petroleum Institute (API) late on Tuesday had indicated an even bigger increase.

Goldman Sachs attributed the recent jump to an increase in imports, especially those from the Gulf Coast. However, output cuts by the Organization of the Petroleum Exporting Countries (OPEC) and other producing nations could reverse this trend.

"Given the relatively high compliance to the proposed cuts so far, we believe that this import channel will reverse from March onward," the analysts said in the note.

The analysts explained that the average crude transit time from the Arabian Gulf to the U.S. Gulf Coast is 47 days. With freight data showing a decline in vessel demand in January, this means arrival to the U.S. should slow down by early March.

"As a result, we do not view the recent excess U.S. builds as derailing our forecast for a gradual draw in inventories, with in fact the rest of the world already showing signs of tightness."

Goldman Sachs also noted that a key manufacturing indicator, the Purchasing Managers' Index (PMI), has continued to show strength globally since late-2016. This may support global demand and accelerate the rebalancing of the oil market.

The bank's global demand growth forecast is at 1.5 million barrels per day in 2017.

Oil prices rose following the release of the EIA report, with investors covering short positions as the rise in U.S crude inventories was not as massive as many had feared, and as gasoline futures got a boost from a surprise decline in inventories of the fuel.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 14

OPEC Ministers Say the Market Might Need More Oil Cuts by Mohammed Sergie

OPEC and other major crude-producing nations may need to extend output cuts into the second half of the year to re-balance the market, oil ministers for Iran and fellow group member Qatar said.

Global oil supplies have decreased as the Organization of Petroleum Exporting Countries and producers outside the group comply with a six-month deal to curb output that took effect on Jan. 1, Qatar’s Energy Minister Mohammed Al Sada said Wednesday at a news briefing in Doha. “It’s too early to make a judgement,” he said, adding that markets may re-balance in the third quarter.

“We kept it open to reconsider the rollover, and rollover is an option if needed,” Al Sada told Bloomberg TV in Qatar’s capital.

In principle, OPEC will have to cut output in the second half, Iran’s Oil Minister Bijan Namdar Zanganeh said, according to the Fars news agency. The issue needs further study before the group can make a decision, Zanganeh said, after meeting in Tehran with his counterpart from Venezuela, also an OPEC member.

The organization agreed in November to impose quotas on its members for the first time in eight years, in an effort to stem a supply glut that had depressed crude prices. OPEC enlisted support from 11 other producers on Dec. 10 in an historic deal to remove as much as 1.8 million barrels of oil a day from the market. OPEC expects to decide whether to extend the cuts at its bi-annual meeting in Vienna in May.

Benchmark Brent crude fell as much as 61 cents in London on Wednesday and was trading at $54.86 a barrel at 1:06 p.m. local time, on course for a third daily decline after industry data showed U.S. stockpiles surged.

Most OPEC members are happy with a crude price of about $60 a barrel, Zanganeh said, according to the Tasnim news agency. OPEC’s compliance with the accord on output has been very good, and non-OPEC producers have begun cutting production and pledged to reach their targets quickly, the Oil Ministry’s Shana news service reported him as saying. Iran is the third-biggest producer in OPEC, behind Saudi Arabia and Iraq, while Qatar ranks 11th.

A committee in charge of monitoring compliance with the deal is due to release its first report on Feb. 17, disclosing January production levels for participating

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 15

countries, Qatar’s Al Sada said. The five-member committee, led by Kuwait, will use as many as six sources of data to measure output, he said.

Last month, Saudi Arabia’s Energy and Industry Minister Khalid Al-Falih said an extension of the agreement probably wouldn’t be necessary, given high levels of compliance and expectations of strong demand. Nonetheless, “all players have indicated their willingness to extend, if necessary,” he said on Jan. 16 in Abu Dhabi.

The oil market would be re-balanced when global inventories, currently near record highs, approached their five-year average level, Al Sada said. The third quarter of this year would be a “good estimate” for when this is likely to happen, he said.

Investment in the oil industry has tumbled during the past three years, and a failure to reverse this trend could hurt future supply and cause a shortage three years from now, Al Sada said. Current oil demand is healthy and will increase by 1.1 million to 1.2 million barrels a day in 2017, he said.

Volatility is lingering near a two-year low and hedge funds continue to ramp up their bullish bets on the price of crude. Some are beginning to worry.

“We see the potential for a sharp liquidation event this quarter,” Citigroup Inc. analysts, led by Aakash Doshi, said in a recent note to clients. “Stretched oil longs could trigger a squeeze in a crowded one-sided trade and crude volatility also seems too low.” They also highlight deteriorating short-interest in crude-focused exchange-traded funds.

The longest losing streak in oil in more than a month is already raising speculation that increasing supply from U.S. shale producers is offsetting the effects of cuts by OPEC. Still, the OIV index, a gauge of volatility in the West Texas Intermediate crude market, remains close to levels not seen since 2014.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 16

NewBase Special Coverage

News Agencies News Release 09 Feb. 2017

BP Lags Behind Peers as Spending Spree Pushes Back Cash Goal News Agencies

BP said fourth-quarter earnings more than doubled as it made progress adjusting to lower energy prices.

Underlying replacement cost profit rose to US$400 million from $196m in the same period last year. The figure, which excludes non-operating items and fluctuations in the value of inventories, is the industry’s preferred measure. Net income was $497m compared with a loss of $3.31 billion a year earlier.

The chief executive Bob Dudley said Tuesday that BP delivered "solid results in tough conditions".

BP took a fourth-quarter charge of $799m for the 2010 Deepwater Horizon disaster, bringing total charges to $62.6bn.

While BP’s fourth-quarter earnings improved, they still missed analyst estimates of $567.7m after higher oil prices failed to fully compensate for lower income from refining.

Unlike peers Royal Dutch Shell and ExxonMobil, which said cash flow now covered spending and dividends at current oil prices, BP said it would not achieve that until the end of the year, and then only if Brent crude rises to about $60 a barrel.

"Almost all of the majors have missed earnings estimates and the big theme for the quarter has been weaker refining," said Brendan Warn, a London-based analyst at BMO Capital Markets. "Maybe people were expecting things to turn around too soon."

BP’s adjusted downstream profit before interest and tax, which includes refining and trading, fell 28 per cent in the fourth quarter to $877m, it said. The partial shutdown of its US Whiting refinery, the company’s largest, hurt sales in the period, while the expense of the turnaround drove up costs. The company also posted a "small loss" from oil trading, said the chief financial officer Brian Gilvary.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 17

Oil and gas production totalled 2.19 million barrels of oil equivalent a day in the quarter, down 5.5 per cent from a year earlier. Crude’s recovery drove adjusted earnings from the upstream business to $400m, compared with a $728m loss a year earlier.

Bp now needs benchmark Brent crude to rise to $60 a barrel this year to be able to fund investments and dividends without borrowing, up from a previous estimate of $50 to $55. That means BP is moving in the opposite direction to Exxon Mobil Corp. and Royal Dutch Shell Plc, which said cash flow already covers spending.

“The 2017 breakeven oil-price guidance is disappointing given the trend to reduce this number in recent years,” said Rohan Murphy, an analyst at Allianz Global Investors, which owns 0.6 percent of BP shares. “Investments come with capex burdens but in the current uncertain environment, increasing the portfolio’s 2017 breakeven seems a step too far.” BP did balance its books toward the end of last year, giving the company confidence to make acquisitions. But the hunt for security of future supply forced it to push its target back for 2017 as a whole. The buying spree at the end of 2016 -- taking in fields around Africa that are yet to begin production -- will result in a cash shortfall this year, Chief Financial Officer Brian Gilvary said in an interview. “The new entry into Mauritania, Senegal and Zohr, all of those will require some cash this year and therefore there is a slight imbalance of just over $1 billion,” Gilvary said Tuesday. “Cash that’s required to invest in those for this year” pushes the company’s breakeven oil price to $60, he said. Acquisitions Binge

In December, BP agreed to a $2.2 billion expansion of output in Abu Dhabi and a $916 million investment in fields in Mauritania and Senegal. That was followed by a $1.4 billion acquisition of Australian filling stations. It also snapped up a 10 percent stake in the giant Zohr gas field in Egypt

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 18

for $375 million in November and a bigger chunk of Indonesia’s Tangguh liquefied natural gas project for $313 million shortly afterward. The higher breakeven price “reflects increased spending associated with the acquisitions,” said Barclays Plc analyst Lydia Rainforth. “Whilst we understand the rationale behind each of the acquisitions on its own, it does appear that this represents a change in priorities” that could hurt the shares in the near term, she said. BP dropped as much as 3.2 percent in London trading and was down 2.7 percent at 463.5 pence as of 1 p.m. local time, extending its decline this year to 9 percent. The Stoxx 600 Oil & Gas Index has fallen 4.4 percent in the period.

BP’s oil and gas production figures show the need for new projects. Output averaged 2.19 million barrels of oil equivalent a day in the fourth quarter, down 5.5 percent from a year earlier. Cash flow from operations fell 58 percent to $2.4 billion.

Tuesday’s share decline and the company’s estimated breakeven price bring the sustainability of the dividend back into focus. The dividend yield has risen to 7 percent, the highest since Nov. 29, the day before OPEC’s decision to reduce oil production drove up crude prices. Shell is yielding 6.3 percent. A higher yield indicates a bigger risk the payout will be cut. Gilvary sought to allay concerns, insisting the dividend was “underpinned.” The start of output at new projects will increase cash flow and the balance sheet can cover payouts even if oil remains at $55 a barrel this year, he said.

Like several of its peers, the company reported earnings that missed expectations after income from refining and trading fell. Profit adjusted for one-time items and inventory changes totaled $400 million in the fourth quarter, falling short of the $567.7 million average estimate of analysts. Adjusted downstream profit before interest and tax slid 28 percent to $877 million.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 19

“Almost all of the majors have missed earnings estimates and the big theme for the quarter has been weaker refining,” said Brendan Warn, a London-based analyst at BMO Capital Markets. “Maybe people were expecting things to turn around too soon.”

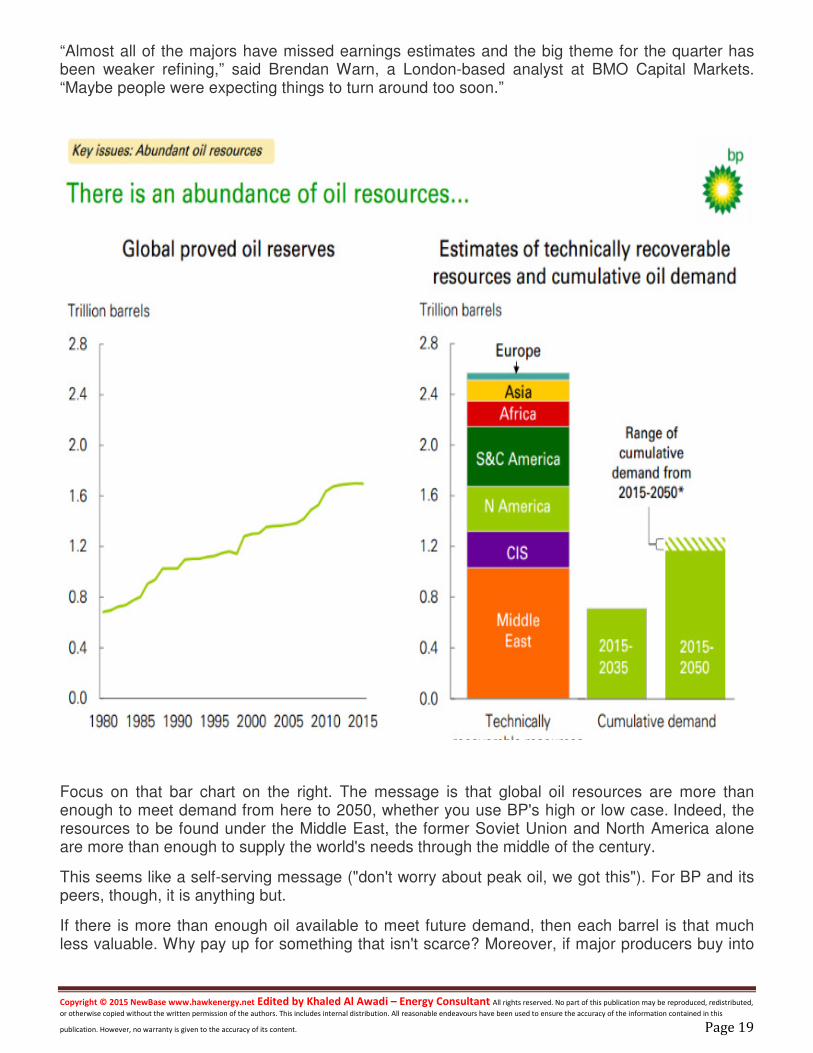

Focus on that bar chart on the right. The message is that global oil resources are more than enough to meet demand from here to 2050, whether you use BP's high or low case. Indeed, the resources to be found under the Middle East, the former Soviet Union and North America alone are more than enough to supply the world's needs through the middle of the century.

This seems like a self-serving message ("don't worry about peak oil, we got this"). For BP and its peers, though, it is anything but.

If there is more than enough oil available to meet future demand, then each barrel is that much less valuable. Why pay up for something that isn't scarce? Moreover, if major producers buy into

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 20

that notion -- the Saudi Arabias and Russias of this world, for example -- then they may decide it's better to pump more oil, more quickly, rather than risk it being left in the ground for good.

From the perspective of an oil company focused on funding dividends for the next 30-odd years, it means one thing: Focus on the lowest-cost oil resources.

As I wrote here last year, the majors -- with their traditional strength in conventional oilfields outside of the OPEC countries, as well as oil sands -- risk being squeezed by a combination of lower-cost OPEC, Russian and North American shale barrels over time. That, along with a desire for shorter project timetables, is why the likes of Chevron Corp. and Exxon are pushing further into U.S. shale.

BP, traditionally known for its deepwater and conventional assets, has been making moves of its own that appear to address this challenge, notably its expansion in Egyptian gas and last year's merger of its mature Norwegian positions into a joint venture with Det Norske Oljeselskap ASA.

It may well be the case that BP's higher breakeven price for 2017 is just a blip -- a necessary, but temporary, loosening of the fiscal reins in order to strengthen the portfolio. Given that its own long-term outlook has put itself, along with its peers, on notice, that had best be the case.

Thoughts On A Potential BP Dividend Cut

Of the many articles and comments focusing on the BP dividend it’s surprising that only handful have touched on the most important point: a dividend cut here would likely be a fantastic long-term opportunity for investors.

Incidentally this is also why I believe green activists to be misguided when calling out fund managers on fossil fuel divestments. The perverse irony is that such coordinated selling without regard to underlying business fundamentals would only serve to make big oil stocks more and more attractive.

It’s kind of like a re-run of the big tobacco playbook from the Nineties that has created vast sums of wealth for ordinary buy-and-hold investors (and incidentally the same theory that formed the basis of the initial Dogs of the Dow strategy).

Before diving in to what a BP dividend cut might mean it’s worth taking in a bit of history here. Between calendar year 1994 and 2009 the annual BP dividend received by British stockholders rose from 4.6 pence per share to 36.42 pence per share; equivalent to an average annual growth rate of around 14.8%. Crucially, there wasn’t a single cut during that period once you account for foreign currency movements.

If you held the stock during that time then the only “cut” was when U.K. based investors saw detrimental foreign currency movements between Sterling and the US dollar. That’s the kind of dependability that at one point led to BP accounting for around 7% of UK pension fund annual income (Royal Dutch Shell was a further 12%). It’s a company that has spewed cash across the cycle as their scale advantages gave them inherent advantages and flexibility that smaller commodity stocks don’t enjoy.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 21

First off is that compared to other oil majors such as Exxon Mobil and Chevron it has been a laggard over the past decade or two. If you made equal $10,000 investments in each one ten years ago and allowed the dividends to accumulate then your Exxon and Chevron blocks would currently be worth around $15,120 and $21,620 respectively.

For BP the comparable figure is just $9,760. Even an investment in Royal Dutch Shell stock would’ve returned around $13,850 over the same period. In fact if you pull the charts up back to the late Nineties you’ll find that BP shares haven’t moved much even since then. At the start of 1998 the roughly $38 per ADS share price that investors were paying to get their hands on BP stock is pretty much the same as what they are trading for right now.

From an income perspective the situation is slightly better as the average dividend yield between 1998 and the present day has been around the 4% point. That would’ve had a big effect if you clicked the box to automatically reinvest dividends along the way.

To see what I mean by that then consider that at the start of the period a $10,000 investment would’ve given you an ownership claim of 262 shares throwing off $323 in annual dividend income. Today your holding would’ve grown to 570 shares throwing off $1,368 in dividend income. So despite the fact that your initial capital basically went nowhere you’d have ended up with dividend growth of around 8.15% a year.

The other sore point for a lot of folks is the current dividend situation. In 2014 the average price of a barrel of crude oil was $90 and BP raked in $32 billion in cash from their operating activities. Of that cash inflow approximately $22 billion went out on capital expenditures, to replace lost reserves and so forth, and the annual dividend took up $5.85 billion.

In 2016 the crude oil price averaged around $40 per barrel and BP’s cash flow was slashed to around $13.3 billion over the first nine months of the year. In the outflow column you have the combined capital expenditures and dividend commitments which took up around $15.5 billion over the same time, whilst the company booked a further $5.1 billion in cash outflows connected to the Gulf of Mexico oil spill. You can see the conundrum there from an income investing point of view.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 22

The thing is it’s basically impossible to analyze BP’s performance without taking into account the events surrounding the Gulf of Mexico oil spill back in 2010; the total cost of which will stand at somewhere between $60-65 billion.

Before the disaster BP’s entire market capitalization stood at around $190 billion. In other words the cost of dealing with the spill, plus the effects of the huge oil slump post-2014, has wiped around a third of BP’s market value over the past six or so years.

What’s surprising about that is if you isolate the post-2010 dividends you find that BP has paid out a cumulative total of $12.99 per ADS. That is actually a heck of performance considering the bill for the Gulf of Mexico spill is worth one-third of their entire pre-spill market capitalization, plus their major product has halved in the intervening period.

Let’s look at what would have happened had you invested in the immediate aftermath of the oil spill. In mid-April 2010 you saw the American Depository Shares changing hands for around $60 a piece and the ordinary shares in London going for approximately £6.50 each.

As the events in the Gulf of Mexico unfold it becomes increasingly clear that the scale of this disaster is pretty much unprecedented in corporate history. By the end of June those share prices had crashed some 55% to $27 per ADS and £3 per ordinary share respectively.

In the years that follow though you don’t see BP go under as a $65 billion dollar legal and cleanup tab might imply. Instead $12.99 per ADS gets paid out by way of cash dividends (£1.41 per

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 23

ordinary share) and the share price recovers to $38 per ADS (£5.10 for the ordinary U.K. listed shares).

All-in-all, if you got in around the $30 per ADS mark you saw total annual returns of around 9% assuming the dividends were reinvested along the way.

Okay, you had to deal with three quarters of scrapped dividends as it became morally, politically and economically impossible to maintain that level of shareholder payouts. Also the sheer scale of the cleanup and litigation bill means the company hasn’t reached the pre-spill level of payouts which were in the $3.35 per ADS range. The fact that you would have carved out 9% returns a year over this period, a good chunk of which also covers one of the most pronounced oil prices in decades, is a sign of a pretty strong underlying company.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 24

NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE

Your partner in Energy Services

NewBase energy news is produced daily (Sunday to Thursday) and

sponsored by Hawk Energy Service – Dubai, UAE.

For additional free subscription emails please contact Hawk Energy

Khaled Malallah Al Awadi, Energy Consultant MS & BS Mechanical Engineering (HON), USA Emarat member since 1990 ASME member since 1995 Hawk Energy member 2010

Mobile: +97150-4822502 [email protected] [email protected]

Khaled Al Awadi is a UAE National with a total of 25 years of experience in the Oil & Gas sector. Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years, he has developed great experiences in the designing & constructing of gas pipelines, gas metering &

regulating stations and in the engineering of supply routes. Many years were spent drafting, & compiling gas transportation, operation & maintenance agreements along with many MOUs for the local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE and Energy program broadcasted internationally, via GCC leading satellite Channels.

NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE

NewBase February 2017 K. Al Awadi

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 25

Hilton hotel 1B AZADLIG AVENUE, BAKU, AZ1000, AZERBAIJAN

Please send your request by email at [email protected], or call +994 55 5993345

About Summit

Azerbaijan Oil and Gas Summit will host by FA Events. Summit will cover main oil and gas topics and latest trends. The Summit will gather main market key players and experts around globe.

Social Networking Contact

• Address: Jafar Jabbarli str., 44. Caspian Plaza. Baku, Azerbaijan. AZ1065 Baku Azerbaijan

• Contact Us: +994 55 599 33 45

• Email: [email protected]

The Oil and Gas Summit

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 26

![6ES5 998-0UF23[1]](https://static.fdocuments.us/doc/165x107/544f5260b1af9f23638b5792/6es5-998-0uf231.jpg)