MftiFtitSttManufacturing Footprint Strategy · design production distribution and related services...

25

M f t i F t i tSt t Manufacturing Footprint Strategy Making the Right Things in the Right Places MANUFACTURING FOOTPRINT STRATEGY Making the Right Things in the Right Places IfM Briefing Day Tuesday 15 May 2012 Paul Christodoulou Principal Industrial Fellow [email protected] Don Fleet Principal Industrial Fellow [email protected] © Copyright Institute for Manufacturing 1

Transcript of MftiFtitSttManufacturing Footprint Strategy · design production distribution and related services...

M f t i F t i t St tManufacturing Footprint StrategyMaking the Right Things in the Right Places

MANUFACTURING FOOTPRINT STRATEGYMaking the Right Things in the Right Places

IfM Briefing DayTuesday 15 May 2012

Paul ChristodoulouPrincipal Industrial [email protected] y

Don FleetPrincipal Industrial [email protected]

© Copyright Institute for Manufacturing 1

AIMS & AGENDA

1. Why lean, offshoring & outsourcing are not enough

2. What leading companies are doing

3. A structured approach

4. Summary & questions

© Copyright Institute for Manufacturing 2

WHY LEAN, OFFSHORING & OUTSOURCING ARE NOT ENOUGH

•Networks inherited not designed•Networks inherited not designed

•Huge potential benefits

•Difficult & risky•Difficult & risky

•Very high stakes

© Copyright Institute for Manufacturing 3

AGENDA

1. Why lean, offshoring & outsourcing are not enough

2. What leading companies are doing

3 A structured approach3. A structured approach

4. Summary & questions

Conventional wisdom:• Move up value chain

• Focus on knowledge creation• Outsource & offshore

© Copyright Institute for Manufacturing 4

Outsource & offshore

DEFINING MANUFACTURING AS A BROADER VALUE CHAIN

“The full cycle from understanding markets through product

design production distribution and related services within andesign, production, distribution and related services within an

economic and social context”

ServiceDistributionProductionDesignResearch ServiceDistributionProductionDesignResearch

This makes it possible to be in manufacturing without owning a factory!

© Copyright Institute for Manufacturing 5

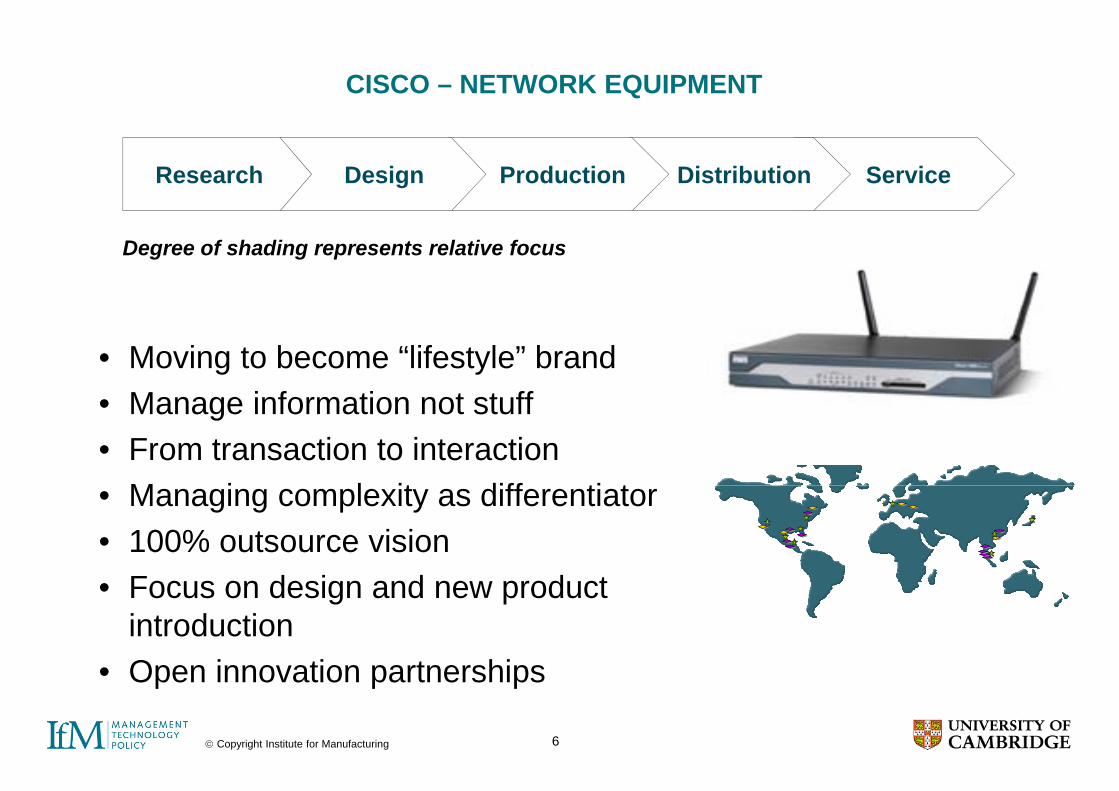

CISCO – NETWORK EQUIPMENT

ServiceDistributionProductionDesignResearch

Degree of shading represents relative focus

• Moving to become “lifestyle” brandM i f ti t t ff• Manage information not stuff

• From transaction to interactionM i l it diff ti t• Managing complexity as differentiator

• 100% outsource visionF d i d d• Focus on design and new product introductionO i ti t hi

© Copyright Institute for Manufacturing 6

• Open innovation partnerships

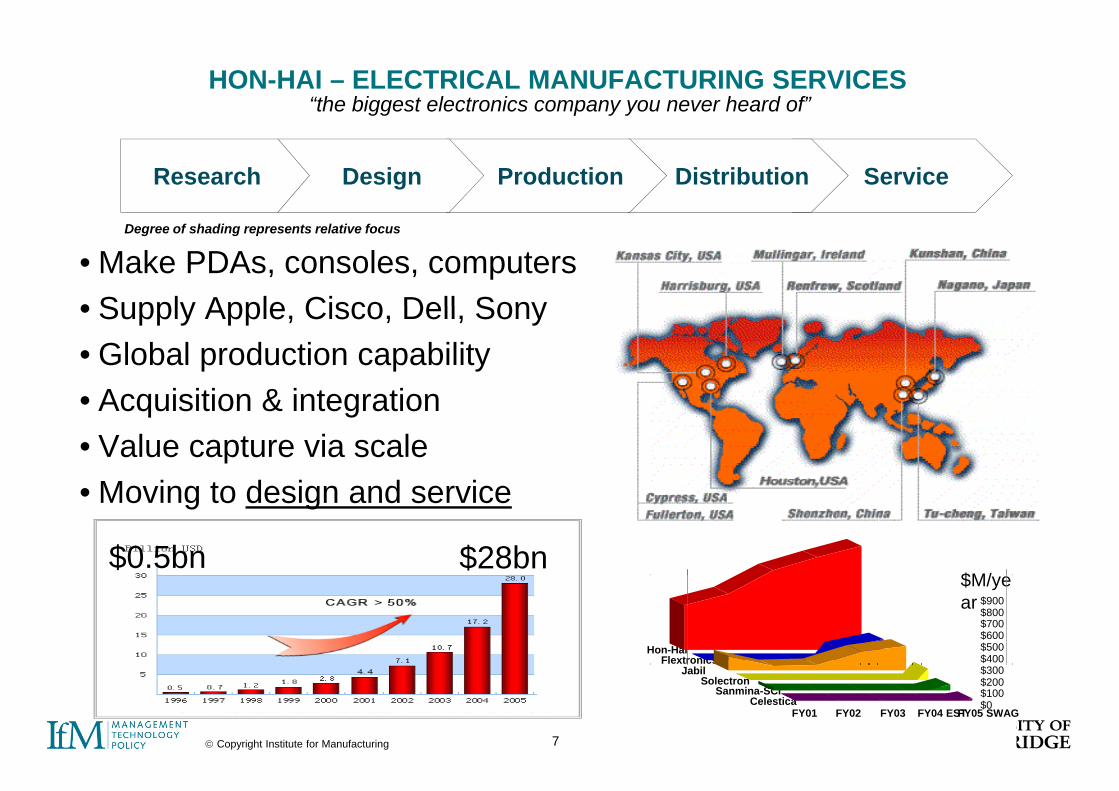

HON-HAI – ELECTRICAL MANUFACTURING SERVICES“the biggest electronics company you never heard of”

ServiceDistributionProductionDesignResearch

• Make PDAs, consoles, computers• Supply Apple Cisco Dell Sony

Degree of shading represents relative focus

• Supply Apple, Cisco, Dell, Sony• Global production capability

Acquisition & integration• Acquisition & integration• Value capture via scale

M i t d i d i• Moving to design and service

$2,000

$M/$0.5bn $28bn

-$2,000

-$1,000

$0

$1,000

Hon-Hai Flextronics Jabil Solectron Sanmina-SCI Celestica

Hon-HaiFlextronics $400

$500$600$700$800$900

$M/year

© Copyright Institute for Manufacturing 7

-$4,000

-$3,000

$ ,Jabil

SolectronSanmina-SCI

Celestica $0$100$200$300

FY01 FY02 FY03 FY04 ESTFY05 SWAG

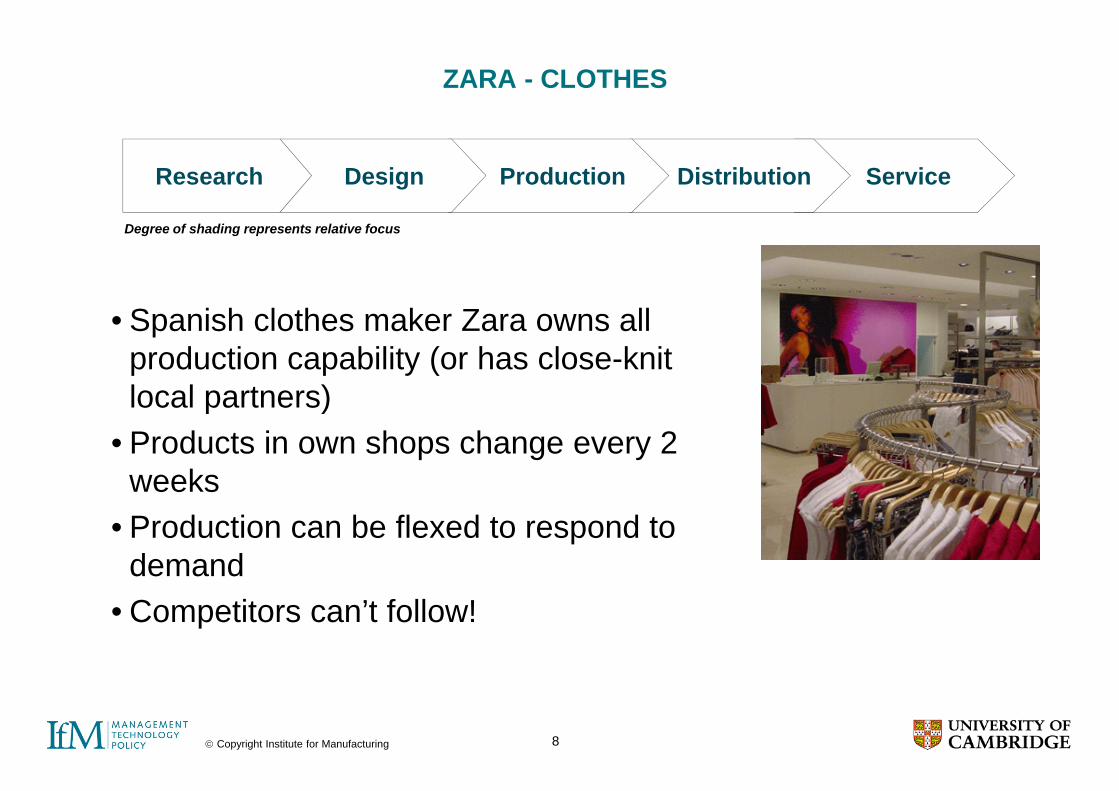

ZARA - CLOTHES

ServiceDistributionProductionDesignResearch

Degree of shading represents relative focus

• Spanish clothes maker Zara owns all production capability (or has close-knit local partners)local partners)

• Products in own shops change every 2 weeksweeks

• Production can be flexed to respond to demanddemand

• Competitors can’t follow!

© Copyright Institute for Manufacturing 8

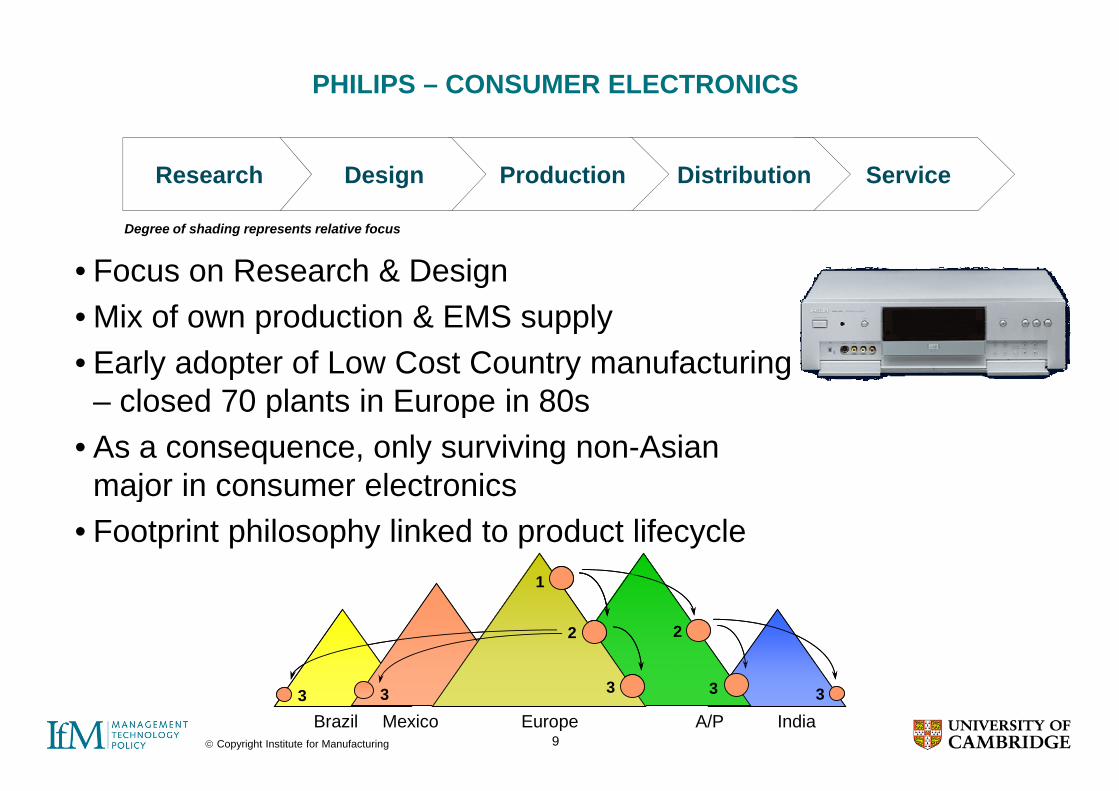

PHILIPS – CONSUMER ELECTRONICS

ServiceDistributionProductionDesignResearch

Degree of shading represents relative focus

• Focus on Research & DesignMi f d ti & EMS l• Mix of own production & EMS supply

• Early adopter of Low Cost Country manufacturing closed 70 plants in Europe in 80s– closed 70 plants in Europe in 80s

• As a consequence, only surviving non-Asian major in consumer electronicsmajor in consumer electronics

• Footprint philosophy linked to product lifecycle1

2 2

1

2 2

© Copyright Institute for Manufacturing 9Brazil Mexico Europe A/P India

33 3 3 333 3 3 3

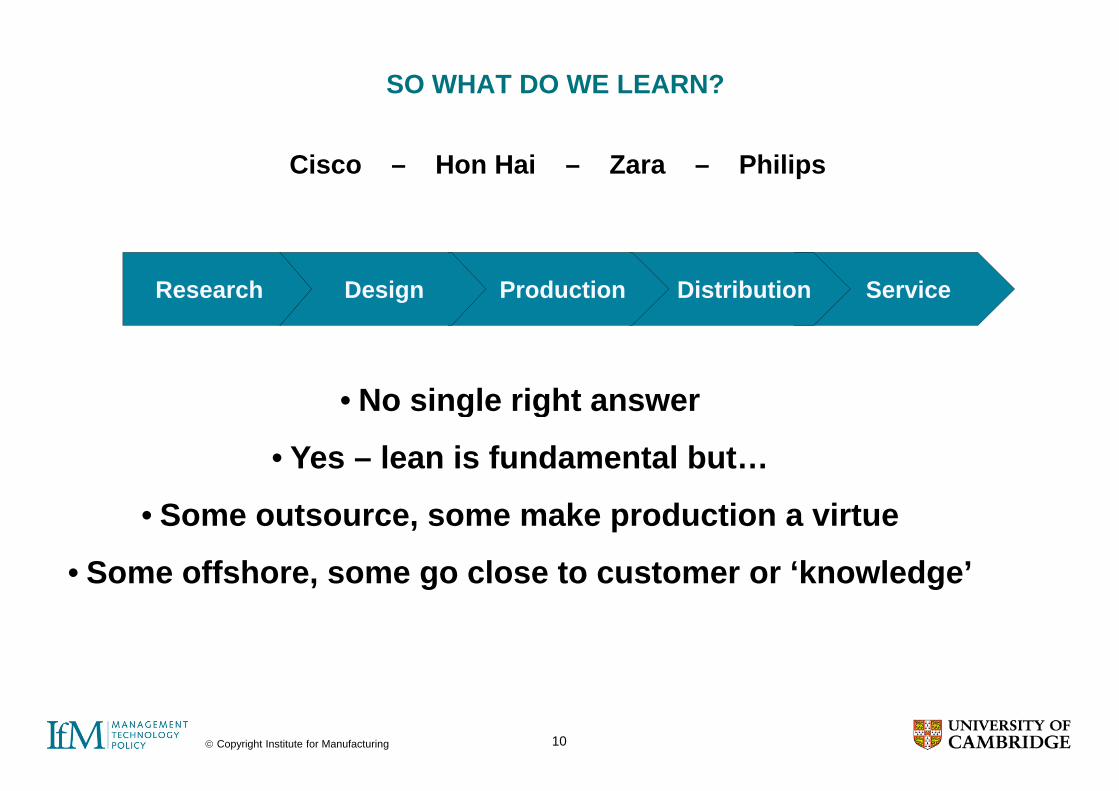

SO WHAT DO WE LEARN?

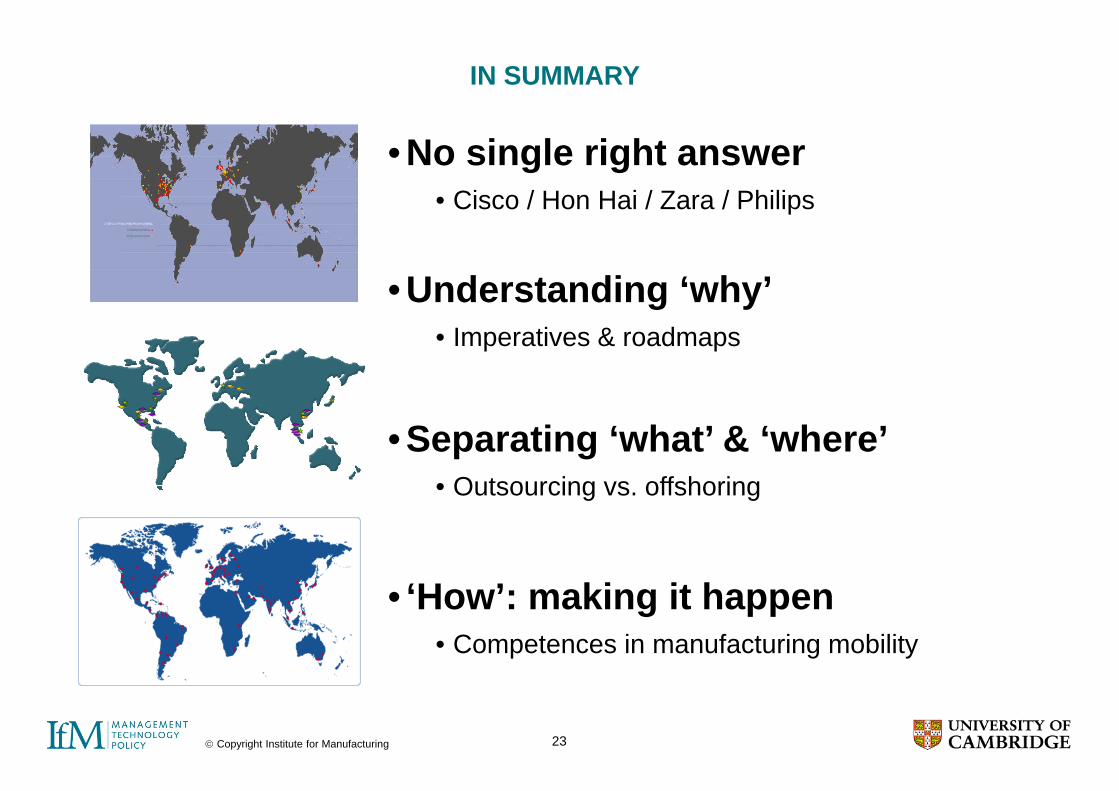

Cisco – Hon Hai – Zara – Philips

ServiceDistributionProductionDesignResearch

No single right answer• No single right answer

• Yes – lean is fundamental but…

• Some outsource, some make production a virtue

• Some offshore some go close to customer or ‘knowledge’• Some offshore, some go close to customer or knowledge

© Copyright Institute for Manufacturing 10

AGENDA

No single right answer but…

We think there is a good way to approach this

1. Why lean, offshoring & outsourcing are not enough

2. What leading companies are doing

3 A structured approach3. A structured approach

4. Summary & questions

© Copyright Institute for Manufacturing 11

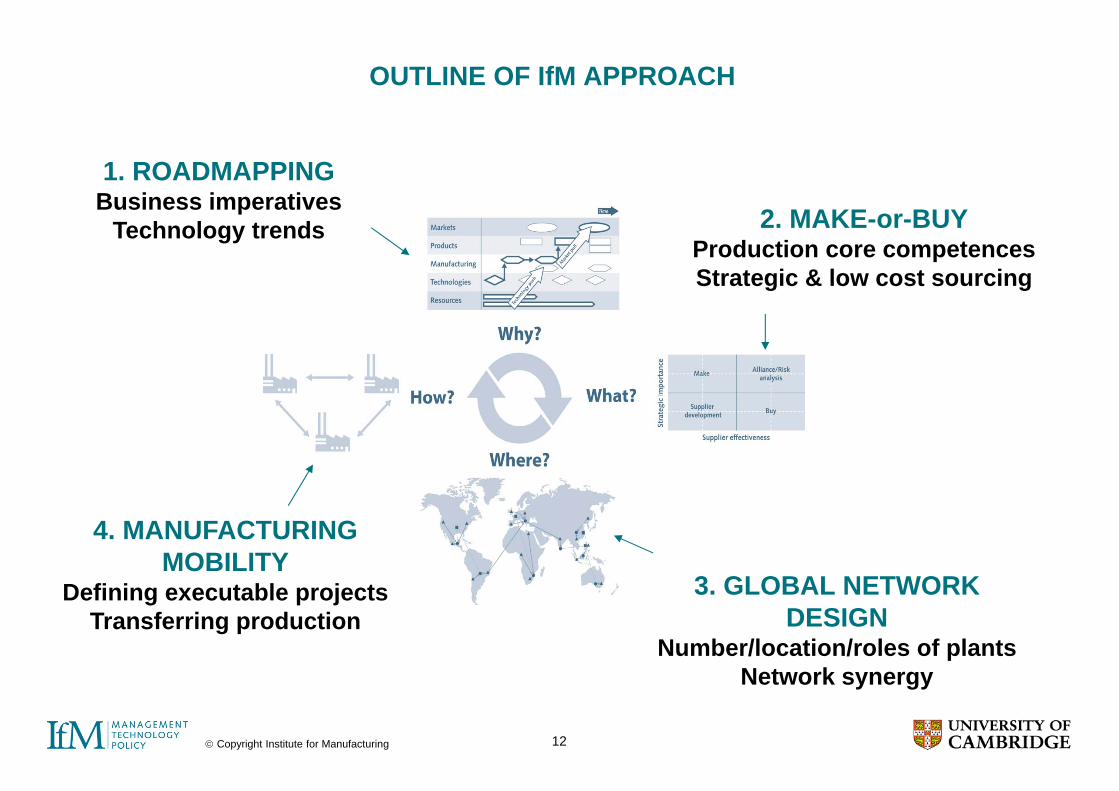

OUTLINE OF IfM APPROACH

1. ROADMAPPING Business imperatives 2 MAKE or BUYTechnology trends 2. MAKE-or-BUY

Production core competencesStrategic & low cost sourcing

4. MANUFACTURING MOBILITY

3. GLOBAL NETWORK DESIGN

Number/location/roles of plants

Defining executable projectsTransferring production

© Copyright Institute for Manufacturing 12

Network synergy

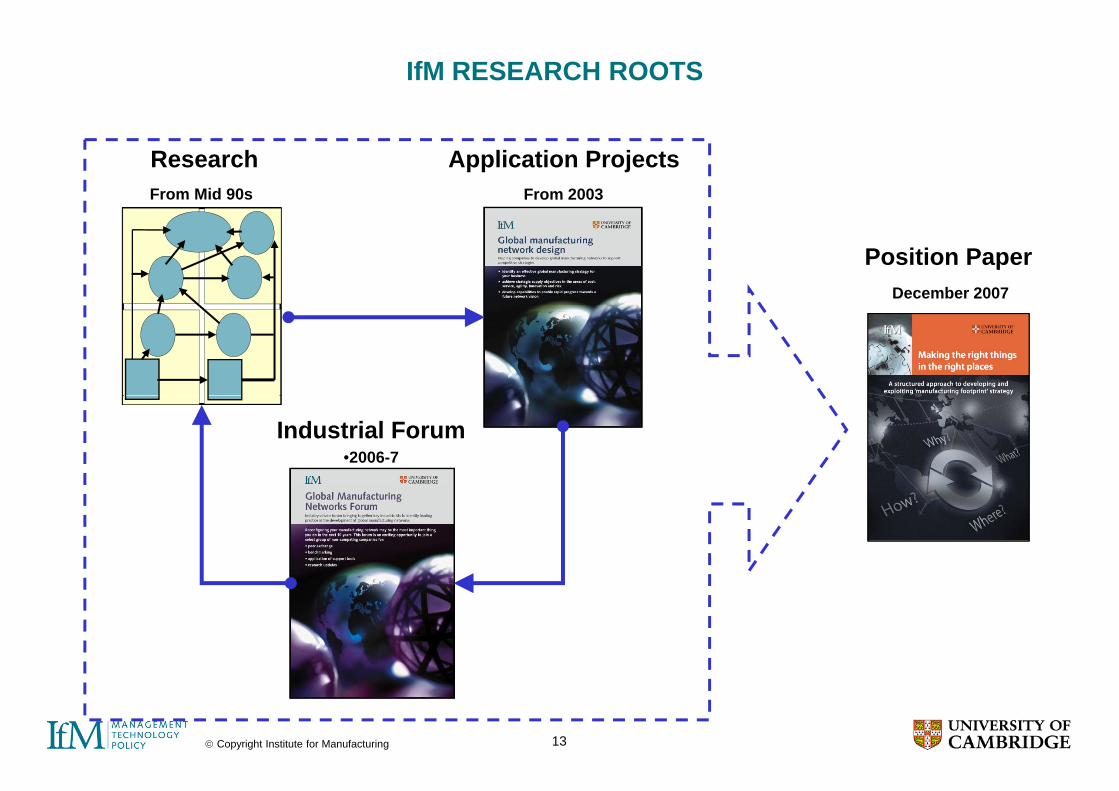

IfM RESEARCH ROOTS

Application ProjectsFrom 2003

ResearchFrom Mid 90s

Position PaperDecember 2007

Industrial Forum•2006-7

© Copyright Institute for Manufacturing 13

SUMMARY OF APPLICATIONS

Large Vehicles

Film Products

Food Equipment

Transport Services

Speciality Chemicals

Hydraulic Pumps

Electrical Devices FMCG Plastic

Products Petrochem Aerospace Plastic Toys

$40bn 110 $4bn 50 $1bn 12 £2bn 17 $2bn 21 $3bn 14 $15bn 200 $5bn 20 $1 5bn 45 $10bn 60 $16bn 40 $2bn 12Scale $40bn, 110 plants

$4bn, 50 plants

$1bn, 12 plants

£2bn, 17 plants

$2bn, 21 plants

$3bn, 14 plants

$15bn, 200 plants

$5bn, 20 plants

$1.5bn, 45 plants

$10bn, 60 plants

$16bn, 40 plants

$2bn, 12 plants

Outcome10 year

evolutionary strategy

5 year aggressive

realign-

2 year turnaround

plan

5 year strategy

5 year consolidation / pre-merger

Staged evolutionary

strategy

Footprint design model

Continuous strategy process

5 year re-configuration

plan

Ideal future network

Impact of new process technologies

Revised vision

following strategy ment plan plan strategy process plan technologies turnaround

Hard benefits

Significant cost savings

$50-60m pa declared cost

savings

Business survival

20% cost saving

Significant cost savings

Access to growth

markets

Significant cost

savings

Enablement of global

expansion

Significant cost

savings

Fundamental shift in

network approach

In process In process

pp

Soft benefits

New processes across 30

SBUs

120 top managers

aligned with change

Minimised business disruption

M&A integration framework

Refocusing of core

business

Trained trainers for staged roll-

out

Post M&A optimisation

Pre-empt need for periodic

restructuring

Consensus across

complex organisation

Distillation of key drivers In process In process

12 very different companies

© Copyright Institute for Manufacturing 14

Overview Benefits

CATERPILLAR CASE STUDY

Overview• $40bn sales, 100+ plants worldwide• 24 month strategy co-development• Implemented across 30 SBUs in

l i ti

Benefits• New process & common language to

engage the senior team• Broke the default approach of reinvesting

i th t tcomplex organisation• Evolution towards 10 year vision

in the status quo• Framework to guide ongoing investment

Strategy process developmentStrategy process development

Pilot implementations

E b d i l t t

Roll-out by SBU

C t ti i

2004 2005 2006 20072003 2008

Embed in annual strategy process

2009

Cost optimiser

© Copyright Institute for Manufacturing 15

SEALED AIR CASE STUDY

Overview• $4bn sales, 50+ plants worldwide• 18 month strategy co-development• 120 senior managers involved

Benefits• Reinvestment in process technology

leadership• Leading positions in emerging markets• 120 senior managers involved

• Phase 1 now complete• Leading positions in emerging markets• $55m declared cost savings so far

Strategy development

Phase 1 implementation

Strategy review

2005 2006 2007 20082004 2009

Phase 2 implementation

2010

Strategy UpdateWe remain committed to our

Strategy Announcement July 2006• step change in costs

• access to emerging marketsStrategy Update

Latest financial evaluation:growth strategies, which

capitalize on our strong global footprint.

Press Release July 2008

g g• reinvestment in process technology

leadershipRights issue required to fund $250m

Target annual savings $50m

a es a c a e a ua o• investment will total $200m

• savings of $45m in 2009, increasing to $55m in 2010.

Press Release January 2008

© Copyright Institute for Manufacturing 16

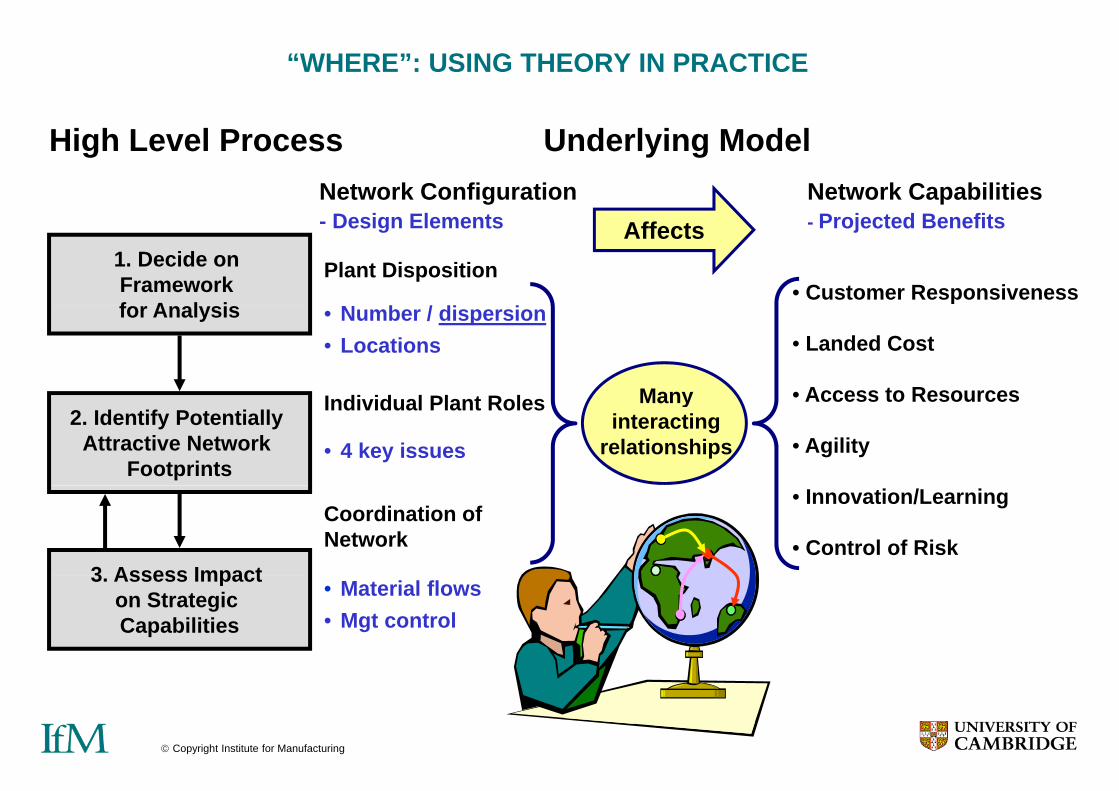

“WHERE”: USING THEORY IN PRACTICE

Network ConfigurationD i El t

Network CapabilitiesP j t d B fit

High Level Process Underlying Model

Plant Disposition

N b / di i

- Design Elements - Projected Benefits

• Customer Responsiveness

Affects1. Decide on Framework f A l i

I di id l Pl t R l

• Number / dispersion• Locations • Landed Cost

• Access to ResourcesMany

for Analysis

• 4 key issues

Individual Plant Roles • Access to Resources

• Agility

Many interacting

relationships2. Identify Potentially

Attractive Network Footprints

Coordination ofNetwork

• Innovation/Learning

• Control of Risk3 Assess Impact • Material flows

• Mgt control

3. Assess Impact on Strategic Capabilities

© Copyright Institute for Manufacturing 17

USA2

USA1 WHERE: NETWORK DESIGN Example Before Optimisation

Iowa Park

USA4

USA3

USA7USA6 USA5

VenezuelaMexico

Russia

France

GermanyUK

Hungary

Poland

Venezuela

Colombia

Spain

Italy

Brazil

ArgentinaChile

S Africa

JapanKorea

China

© Copyright Institute for Manufacturing 18N Zealand

AustraliaMalaysia

USA15 Fin W’houses

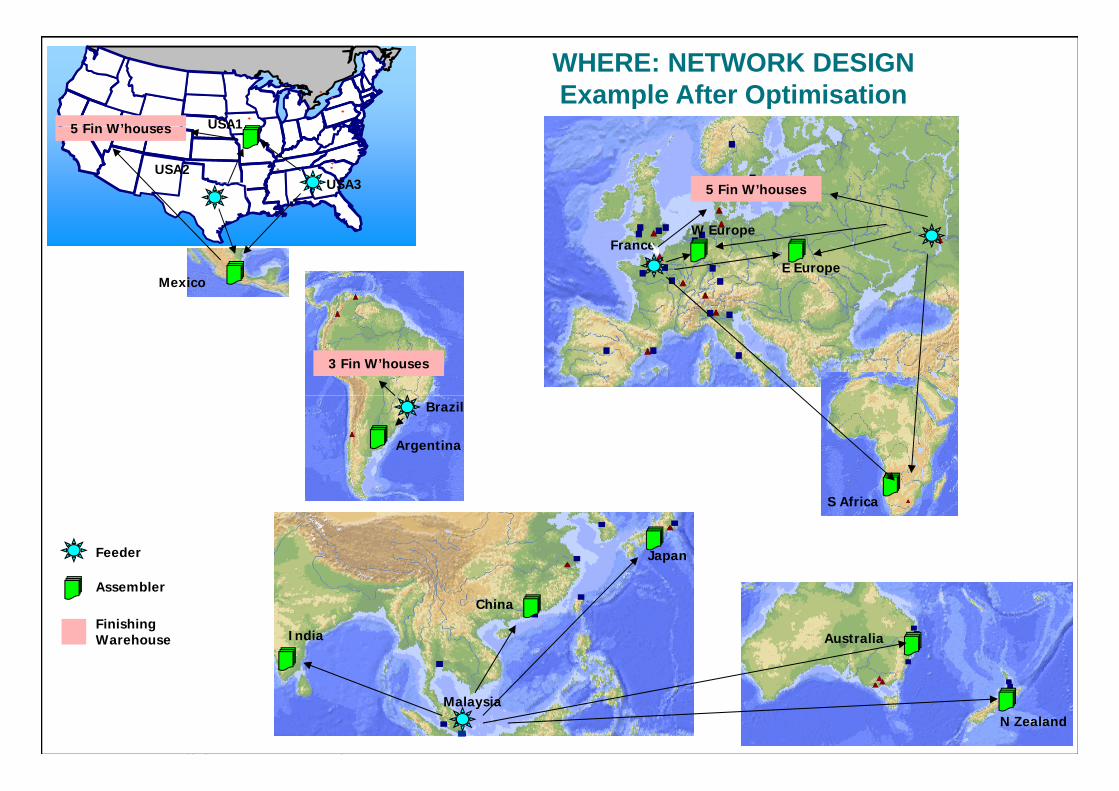

WHERE: NETWORK DESIGN Example After Optimisation

5 Fin W’housesIowa ParkUSA2

USA3

USA15 Fin W’houses

FranceW Europe

E EuropeMexico

3 Fin W’houses

Brazil

Argentina

S Africa

JapanFeeder

China

India Australia

Assembler

Finishing Warehouse

© Copyright Institute for Manufacturing 19

MalaysiaN Zealand

HOW: TRANSFERRING PRODUCTION & COMPETENCE

Capturing tacit knowledge

Packaging / adapting

Infrastructure

Improving capabilities

© Copyright Institute for Manufacturing 20

Aligning incentives Ramp up

AGENDA

1. Why lean, offshoring & outsourcing are not enough

2. What leading companies are doing

3 A structured approach3. A structured approach

4. Summary & questions

© Copyright Institute for Manufacturing 21

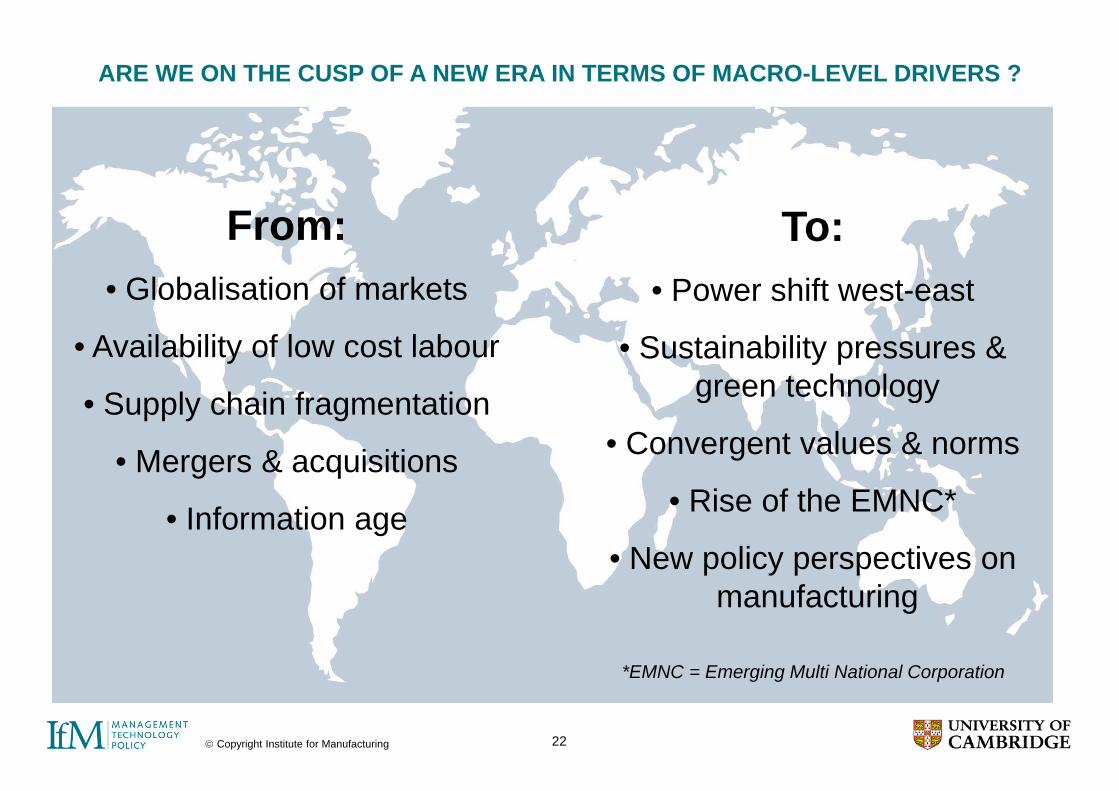

ARE WE ON THE CUSP OF A NEW ERA IN TERMS OF MACRO-LEVEL DRIVERS ?

F TFrom:• Globalisation of markets

To:• Power shift west-east

• Availability of low cost labour

S l h i f t ti

• Sustainability pressures & green technology• Supply chain fragmentation

• Mergers & acquisitions

green technology

• Convergent values & norms

• Information age • Rise of the EMNC*

• New policy perspectives on p y p pmanufacturing

*EMNC E i M lti N ti l C ti

© Copyright Institute for Manufacturing 22

*EMNC = Emerging Multi National Corporation

IN SUMMARY

• No single right answer• Cisco / Hon Hai / Zara / Philips

• Understanding ‘why’g y• Imperatives & roadmaps

• Separating ‘what’ & ‘where’• Outsourcing vs offshoring• Outsourcing vs. offshoring

• ‘How’: making it happen• Competences in manufacturing mobility

© Copyright Institute for Manufacturing 23

ANY QUESTIONS

IfM t il bl t d l d fIfM report available to download from: www.ifm.eng.cam.ac.uk/service/books/form_footprint.html

© Copyright Institute for Manufacturing 24

Further information

Paul ChristodoulouPrincipal Industrial FellowPrincipal Industrial [email protected]

Don FleetPrincipal Industrial Fellowdef25@cam ac [email protected]

© Copyright Institute for Manufacturing 25