METROPOLITAN TRADING COMPANY (MTC)mtc.joburg.org.za/wp-content/uploads/2020/01/MTC... · (B2B2C...

33

METROPOLITAN TRADING COMPANY (MTC) NETWORK COMMERCIALISATION STRATEGY AND ENHANCED BUSINESS MODEL PUBLIC PARTICIPATION VERSION 0.01 AUGUST 2019

Transcript of METROPOLITAN TRADING COMPANY (MTC)mtc.joburg.org.za/wp-content/uploads/2020/01/MTC... · (B2B2C...

METROPOLITAN TRADING COMPANY (MTC)NETWORK COMMERCIALISATION STRATEGY AND ENHANCED BUSINESS MODELPUBLIC PARTICIPATION

VERSION 0.01

AUGUST 2019

2

CONTEXT AND OVERVIEWTO BECOME A KEY DIGITAL ENABLER FOR A SMART CITY OF JOHANNESBURG (COJ), WHILE STILL ACHIEVING GROWTH, MTC MUST UNLOCK THE COMMERCIAL POTENTIAL OF THE NETWORK ASSET

In 2015, the City of Johannesburg transferred its

acquisition of the broadband network to

MTC

In order to meet its government mandate and ICT requirements from CoJ, MTC must

maximise the revenue generated from its

network asset

What is the Commercialisation

Strategy?

What is the required

Commercialisation Business Model?

What are the services and

products to be offered?

What is the appropriate Go-To-

Market Strategy?

What is the enabling SMME

Strategy?

In addressing these questions, MTC will be well positioned to unlock the commercial potential

of the Network Asset

3

MTC CONSTRAINTS

4

MTC TODAY – VS – MTC IN THE FUTURE

CUSTOMER

MTC has direct access to the Market

MTC provides Services to the Customer

Customer pays MTC for Services provided

CUSTOMER

MTC has direct & indirect (SMMEs) access to the Market

MTC provides Services to the Customer

Customer pays MTC for Services provided

Service Provider provides services to MTC as per MTC’s service catalogue

MTC pays the Service Provider service fees for leveraging the Service Provider’s Network

TO

DA

YFU

TU

RE

SERVICE PROVIDER

• MTC owns the Network

• MTC maintains the Network

• MTC uses the Network

• SP owns the Network

• SP maintains the Network

• MTC uses the Network

MTC is transitioning; from owning the Network Asset, to becoming an agent transacting organisation that continues to provide services, leveraging the Service Provider’s Network Asset

HOW DID WE GET HERE

6

EXPERIENCE IN BOT

7

ASSET SALE VS BUSINESS SALE

CoJ bought the Joburg Broadband Network Business with the network assets and other things through a BOT model. The total business was procured for

R1,2b

Network Asset was

worth R700m+

Business Database was

worth R200m+

Early contract Termination as

per contract terms was worth balance of R1,2b

The Enhanced Business Model is only selling the tangible and

intangible network asset not the MTC business

8

INTERNAL ENGAGEMENT PROCESS FOLLOWED

The business plan was presented to EXCO in January 2018 as part of the adjustment budget which

consisted of the 2017/2018 and the 2018/2019 business plan and associated KPIs.

The business plan and the associated budget adjustment were approved by council in May 2018.

Business case to change the operating model was discussed at strategy session by the MTC

management.

The proposed options were presented to the board, at the strategy session, as a business case and

the board approved the approach sighting the need to review the details of the BOT option

proposed.

The business case was then presented to the Economic Development Section 79 Strategic

Workshop and was well received by the chairman and the committee members.

The business case was also presented to the Executive Mayor who then requested the City

Manager, Group CTO, Group Legal to engage MTC and come up with the way forward report.

The City Manager established the task team that deliberated on the matter.

The task team reviewed the business case and assessed the available options whereby they

eliminated the options that were not practical. During the deliberations, the team came up with the

recommendation to implement a BOT

9

INTERNAL ENGAGEMENT PROCESS FOLLOWED

The business model referred to as the BOT business model was presented and

approved before the Mayoral Committee on the 23rd of January 2019, consisted of

the following strategic objectives:-

- Transfer of asset to private entity;

- Procurement of network services from the private entity through SLA;

- Entering into a commercialization arrangement with the private entity;

- MTC having the option of first right of refusal to procure the asset at the end of the services contract.

MTC was requested to engage the services of Transactional Advisor (TA) in order

to determine:

- The legal ramifications of the new business model (BOT); The financial projections and if they are realistic; The risks associated with the proposed transaction; The mitigations and the implementation of new business model

10

FROM TRANSACTIONAL ADVISOR TO COUNCIL APPROVAL

• BOT transactional advisors appointed;

MTC appointed TA for Strategy, Technical and Commercialisation

(business profitability) from its panel of suppliers

MTC appointed Group Legal to assist with the legal aspect of the

transaction. Group Legal appointed a team of legal advisors to assist in

this regard.

• All advisors found no alignment with the concept of a BOT

in relation to what the City to execute.

• The legal advisors provided legal opinion on taking this

forward as the enhanced business model.

• The strategy and commercialization team supported the

legal opinion.

• MTC Exco and Board were engaged and they supported

the Enhanced Business Model

CHALLENGES

• The strategic objectives

of the business model

are not aligned with a

BOT model

• Labelling the model a

BOT causes confusion on

what compliance process

to follow

• The Treasury has in

many cases considered

BOTs as PPP

TRANSACTIONAL ADVISORY SERVICES

12

ENHANCED BUSINESS MODEL

• TWO STAGED Approach

- Contract of sale between MTC and the Service Provider with a first right of refusal option:

- Ensure that the first right of refusal that provides the City the option to revert the asset back to MTC as per contract terms

- Must ensure that the asset is valued and priced correctly and that appropriate approvals are obtained in order to sell.

- Service level agreement for services to be procured by the municipality and government entities:

- Must ensure that appropriate approvals are obtained in order to get into an SLA of more than 3 years.

• Open tender process to be followed.

13

MTC ENHANCED BUSINESS MODEL BUSINESS CASE

• SALE OF ASSET

The total proceeds ranges between R853 million and R1.008 billion.

The carrying value of the Network assets and Intangible assets amounted to R538million as at 28 February 2019

Therefore, the total gain from the sale of the asset ranges between R315 million and R470 million.

• SERVICE LEVEL AGREEMENT

Consolidate all Telecommunications, Smart City and IoT services of CoJdepartments and entities

Reduce the cost of service with more than 20% over the contract period

Increase revenue using virtual telecoms model

14

MTC ENHANCED BUSINESS MODEL BENEFITS

• What is the MTC Enhanced Business Model and what does it mean to:

Citizen & Resident – reduction of cost of data, bridging digital

divide (T&Cs apply)

Johannesburg Business – reduction in cost of data with up to

50% on current cost (T&Cs apply)

Shareholder – get cash from sale of asset, have ability to increase

revenue collection through incentives of reduced data services;

reduction of internal data costs; increase in external revenue

sources; increase in Economic Growth

MTC – viable & sustainable business with direct public impact and

service delivery implementation; smart way of doing business;

making more with less

THE ENHANCED BUSINESS MODEL

16

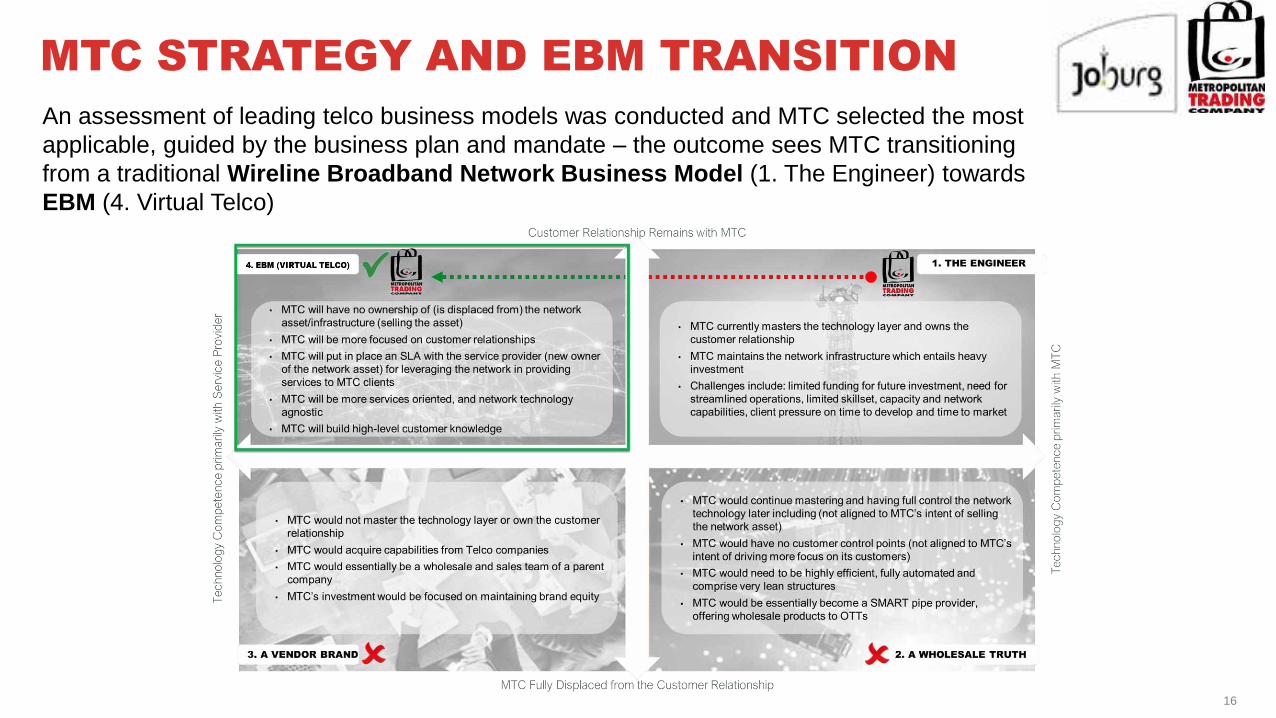

MTC STRATEGY AND EBM TRANSITION

An assessment of leading telco business models was conducted and MTC selected the most

applicable, guided by the business plan and mandate – the outcome sees MTC transitioning

from a traditional Wireline Broadband Network Business Model (1. The Engineer) towards

EBM (4. Virtual Telco)

17

CURRENT BUSINESS MODELCurrent Business Model: Does not enable MTC to take advantage of opportunities provided by industry trends and evolving digital technology capabilities – including limitations in providing a platform that enables the CoJ’s digital agenda (SMART City)

1 Legal 2 Risk & Compliance 3 Mgt. Support Exec. 4 Internal Audit 5 CEO 6 CFO 7 CTO

BU

SIN

ES

S

SU

PP

OR

T

FU

NC

TIO

NS

OP

ER

AT

ION

S

SU

PP

OR

T

FU

NC

TIO

NS

EN

TE

RP

RS

IE

FU

NC

TIO

NS

SERVICE &

PRODUCT

CATALOG

SALES &

ORDERING

BILLING, INVOICE,

PAYMENTS

REVENUE

ASSURANCE

INVENTORY,

ACTIVATION,

ASSURANCE

SERVICE MGT.

SECURITY

SUPPLY CHAIN

MGT.

HUMAN

RESOURCESFINANCE MGT.

NE

TW

OR

K

FU

NC

TIO

NS PHYSICAL NETWORK

ENTERPRISE DATA

MGT.

LEGAL SHEQ

Advisory

Contracting

Quality Assurance

1

1

2

SHE2

HR Mgt. & Admin.

Performance Mgt.

3

3

Knowledge Mgt.3

AUDIT

Internal Audit4

CEO OFFICE

Exec. Assistance

Committee Office

5

5

Asset Mgt.

Facilities Mgt.

6

6

Financial Mgt.6Account Mgt.7

Customer Relationshipp Mgt. / OM7

SCM Mgt.6

Service Mgt. (Internal)

Service Mgt. (External)

7

7

ARCHITECTURE

Solution Architecture

Cyber Security Archit

7

7

PROJECT MGT.

Project Mgt.7

IT (Support) Mgt.6

Cyber Security7

CH

AN

NE

LS

DIRECT SALES

PUBLIC LARGE BUSINESS /

ENTERPRISES

RETAIL WHOLESALE

CITY GOVERNMENT

DEPTS

MEDIUM BUSINESS /

ENTERPRISES

GOVERNMENT

MOEsCoJ

Served by MTC DirectlyServed by MTC Directly Served by MTC Directly

Contact Centre

Filed Operations

NOC Support (2ndLine)7

System/DB Admin.

Network Performance

Monitoring & Control

Data Centre Hosting 7

77

7

7

7

CITY OF JOHANNESBURG’S DIGITAL AGENDA:

limited capabilities required for emerging citizen-centric

experience areas

DIGITAL CUSTOMER EXPERIENCE: manual

processes with no / low digital experience

FLEXIBILITY AND CONTROL: slow response to service

change and short term needs

VELOCITY TO MARKET: long lead times due to manual

processes

COST REDUCTION: High CAPEX & OPEX to install /

maintain MPLS, costly CPEs and service

INDUSTRY X.0: cannot meet Internet of Everything (IoE)

business market demands

Cannot address significant shifts in the ever changing

REVENUE MIX

Deeply tied to declining core business, limitations in

focusing on FUTURE VALUE CREATION

Cannot enable MOBILE, EMBEDDED CONNECTIVITY

– as the world gets connected with augmented data

knowledge

KEY CHALLENGES

18

CAPABILITY ASSESSMENTProposed EBM Capabilities: the organisational review should be conducted in the context of the EBM; specifically Tasks, Skills, Roles, Talent and Organisation that will be required

2•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•6 1 •

•

•

•

•

•

•

•

•

•

•

•

•

3•

•

•

•

••

•

•

•

•

•

•

•

•

••

•

•

•

•

•

•

•

•

•

•

•

•

••

•

•

•

•

•

•

•

•

•

•

•

•

•

4ACCENTURE’S

JOB LIBRARY

5

19

ENHANCED BUSINESS MODELProposed EBM Capabilities: *Based on MTC’s strategy as well as an assessment of industry trends and opportunities, this Enhanced Business Model (EBM) enables MTC to expand its ecosystem and become a Digital Network Service Provider

*See Appendix for Supporting Analysis Data

Legacy stack Digital stack Ecosystem servicesDecoupling layers

ENTERPRISE EXPERIENCE ENABLEMENT: through

integrated sales and marketing capabilities decoupled

from the underlying complexity of the legacy system of

records, SD WAN chain and extending B2B2x value

chain

REAL TIME SERVICE MANAGEMENT: for all

Communication Services enabling an OTT-like service

introduction, Intelligent operations and E2E Service and

Network Topology view

NETWORK AND INFRASTRUCTURE ABSTRACTION:

decoupling Network and Infrastructure from Service

layer, exposing APIs for resource configuration, usage

and performance management and implementing policy

rules for dynamic resource allocation enabling dedicated

QoS and network assets monetization

SYSTEM OF INSIGHTS: as the engine of the multi-

speed architecture, supporting Business, Service and

Network layers through A.I. and machine learning

ECOSYSTEM ENABLEMENT: NaaS Platform

Enablement APIs, exposing network services to the

partners ecosystem

CONNECTED INDUSTRY ORCHESTRATION:

Connected Industry service orchestration enabling

Industry X.0 (e.g. connected health, connected car)

VALUE PROPOSITION

PHYSICAL DOMAIN

ACCESS

REAL TIME SERVICE MANAGEMENT

NETWORK SERVICE PLATFORMS

NETWORK AND INFRASTRUCTURE EXPOSURE

EN

TE

RP

RIS

E F

UN

CT

ION

S

SYSTEM OF RECORDS ABSTRACTION

SY

ST

EM

S O

F IN

SIG

HT

S

X.0

TE

CH

NO

LO

GIE

S

(AR

/VR

, D

igit

al T

win

, B

lockC

hain

, etc

.)

DIGITAL

ECOSYSTEM

SERVICE

PLATFORM

DIGITAL BUSINESS PLATFORM

Enterprise Experience Marketing Intelligence Partner Enablement

TRADITIONAL BSS/OSS

SERVICEORCHESTRATION

INTELLIGENTOPERATIONS

SP TELCO

PLATFORM

E2E TOPOLOGY

Creation

Fulfilment

Assurance (Fault, Perf., TTM)

Billing

CONNECTED INDUSTRY

ORCHESTRATOR

PARTNERSCHANNELS

B2B2X Partners

(M2M, IoT)Self-Service &

SMME Portal

Dedicated

Support

Direct

Sales TeamApps Employees

(B2B2C Model)

CONNECTED INDUSTRY

Auto

motive

Health

Care... Govern

ment

X.0 Connected Industry Platform

PUBLIC RESIDENTIAL LARGE BUSINESS /

ENTERPRISES

RETAIL WHOLESALE

CITY GOVERNMENT

DEPTS

SMALL BUSINESS /

ENTERPRISES

GOVERNMENT

MOEsCoJ MEDIUM BUSINESS /

ENTERPRISES

Served through SMMEsServed through MTC Directly and through SMMEs Served through MTC Directly

* NEW * NEW

CONNECTIVITY & CLOUD VIRTUAL

INFRASTRUCTURE

CY

BE

R S

EC

UR

ITY

THE EBM BUSINESS CASE

21

High Speed InternetFTTx- Residential & Business

Ethernet Link Dark Fibre Leasing

Total projected revenue over 5 year

period

R622m

Total projected revenue over 5

year period

R1.3bn

Total projected revenue over 5 year

period

R220m

Key Value Metrics (Based on Market and MTC)

Increased New Customers

Increased Customer Retention

Decreased Bad Debts

Increased SMME Onboarding

Increased SMME Tiering

Reduction in SMME Attrition

Reduction in OPEX Expenditure

Reduction in Costs Per Sale

Reduction in Sales Lead Time

Target Stakeholder (Based on MTC)

Residential Business Government

Key Products (Based on Market)

Total projected revenue over 5 year

period

R2bn

Total projected revenue over 5

year period

R1.8bn

Total projected revenue over 5 year

period ( at a 75% growth rate)

R6bn

SMMEs account for 75% of costs of

revenue totaling = R1.35bn

SMMEs account for 75% of costs of

revenue totaling = R1.5bn

TransparencyMeasure service usage in a

clear and fair manner to drive

the right consumption

behaviors

InnovationDeploy differentiated

service offerings in the

market

AgilityDecrease time to business

outcome and capture

opportunities

ProductivityDrive process efficiency of

services and SMMEs

FlexibilityLeverage highly extensible

platform in a responsive

manner

1

2

3

4

5

REVENUE SUMMARYBusiness Case Summary: While OPEX costs is expected to significantly reduce as a result of the Asset Sale, MTC’s revenue projection is very aggressive compared to the Market, which could impact the organisation’s target of being fully self-funded

22

R306.71 R370.36

R456.55 R544.79 R591.12

R2,082.29

R2,441.97

R2,859.49 R2,883.99 R2,909.60

FY19/20 FY20/21 FY21/22 FY22/23 FY23/24

Projected Revenue Analysis MTC vs Market

Projected Market Revenue (Rm) Projected MTC Revenue (Rm)

R84.55

R211.16

R143.67

R226.86 R249.74 R256.60 R270.49

-R36.91

-R138.08

R47.68

-R6.80

R3.32

R34.42

R64.19

R384.74

R442.61

FY15/16 FY16/17 FY17/18 FY18/19 FY19/20 FY20/21 FY21/22 FY22/23 FY23/24

Government Subsidy Vs Net Services Revenue

Total Subsidy (Rm) Net Revenue (based on services rendered) (Rm)

• Whilst the projected CAGR for MTC is 7% over the 5 year period with figures reaching in to R2 billion, the market forecasts a CAGR of 14% of the same 5 year period with significantly lower revenue figures potentially reaching a max of R1billion – MTC’s projections are way above the Market projections

• Based on MTC’s revenue projections, the organisation is targeting to be fully self-funded (no reliance on CoJ’s subsidy) by FY23/24 at the latest (confirmed after discussions with MTC’s Financial Manager)

• To realise this, some of the key areas of improvement include MTC’s net revenue earnings and collections

Actual Projected

Zero reliance on subsidy

REVENUE SPLITThe projected market revenue for the target state is significantly lower than the MTC projected revenue and could impact on MTC’s target of being fully self-funded (i.e. moving from subsidy-dependency from the CoJ)

23

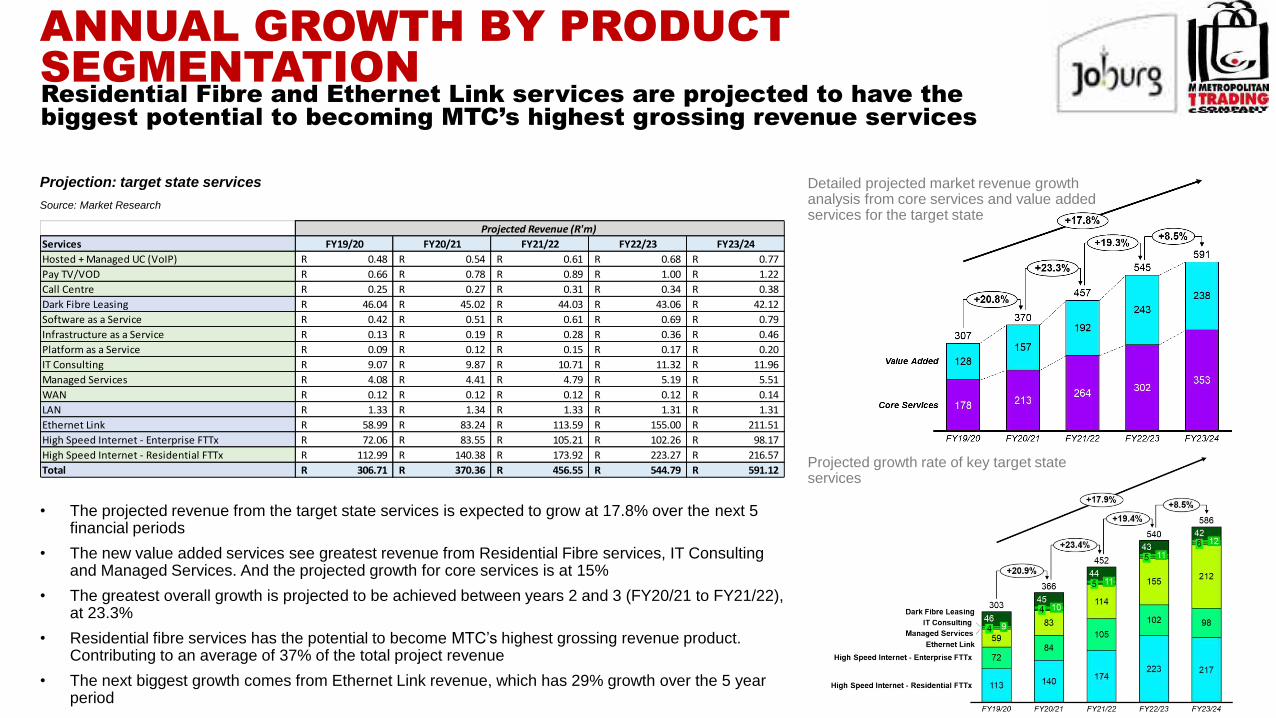

Projection: target state services

Services FY19/20 FY20/21 FY21/22 FY22/23 FY23/24

Hosted + Managed UC (VoIP) 0.48R 0.54R 0.61R 0.68R 0.77R

Pay TV/VOD 0.66R 0.78R 0.89R 1.00R 1.22R

Call Centre 0.25R 0.27R 0.31R 0.34R 0.38R

Dark Fibre Leasing 46.04R 45.02R 44.03R 43.06R 42.12R

Software as a Service 0.42R 0.51R 0.61R 0.69R 0.79R

Infrastructure as a Service 0.13R 0.19R 0.28R 0.36R 0.46R

Platform as a Service 0.09R 0.12R 0.15R 0.17R 0.20R

IT Consulting 9.07R 9.87R 10.71R 11.32R 11.96R

Managed Services 4.08R 4.41R 4.79R 5.19R 5.51R

WAN 0.12R 0.12R 0.12R 0.12R 0.14R

LAN 1.33R 1.34R 1.33R 1.31R 1.31R

Ethernet Link 58.99R 83.24R 113.59R 155.00R 211.51R

High Speed Internet - Enterprise FTTx 72.06R 83.55R 105.21R 102.26R 98.17R

High Speed Internet - Residential FTTx 112.99R 140.38R 173.92R 223.27R 216.57R

Total 306.71R 370.36R 456.55R 544.79R 591.12R

Projected Revenue (R'm)

Source: Market Research

Detailed projected market revenue growth analysis from core services and value added services for the target state

Projected growth rate of key target state services

• The projected revenue from the target state services is expected to grow at 17.8% over the next 5 financial periods

• The new value added services see greatest revenue from Residential Fibre services, IT Consulting and Managed Services. And the projected growth for core services is at 15%

• The greatest overall growth is projected to be achieved between years 2 and 3 (FY20/21 to FY21/22), at 23.3%

• Residential fibre services has the potential to become MTC’s highest grossing revenue product. Contributing to an average of 37% of the total project revenue

• The next biggest growth comes from Ethernet Link revenue, which has 29% growth over the 5 year period

ANNUAL GROWTH BY PRODUCT SEGMENTATION Residential Fibre and Ethernet Link services are projected to have the biggest potential to becoming MTC’s highest grossing revenue services

24

Annual Organisation Cost

for FY18/19

R283m

Organisational Headcount

38FTEs

Projected 5 Year CAGR with

Network Asset

58%

Projected Market 3 Year CAGR

without Network Asset

14%

*Source: Annexure C - Draft OPEX Allocation 2019/20 - 2021/22

Obtained 3 May 2019

Cu

rre

nt

Sta

te –

Be

fore

th

e S

ale

of

the

Ne

two

rk A

ss

et

Target State – Post the Sale of the Network Asset

R120,803.00

R151,624.00 R160,248.00

R169,118.00

R179,123.12

R12,516.00

R150,028.00

FY18/19 FY19/20 FY20/21 FY22/23 FY23/24

Distribution of OPEX costs before and after the sale of the asset (R’m)

Non-Asset Expenses Contracted Services Asset Expenses Employee Costs

COST SAVINGSCurrently, 70% of the OPEX budget is allocated to Network Asset related expenditure. Post the sale of asset, these funds could be re-directed towards other strategic initiatives

70%

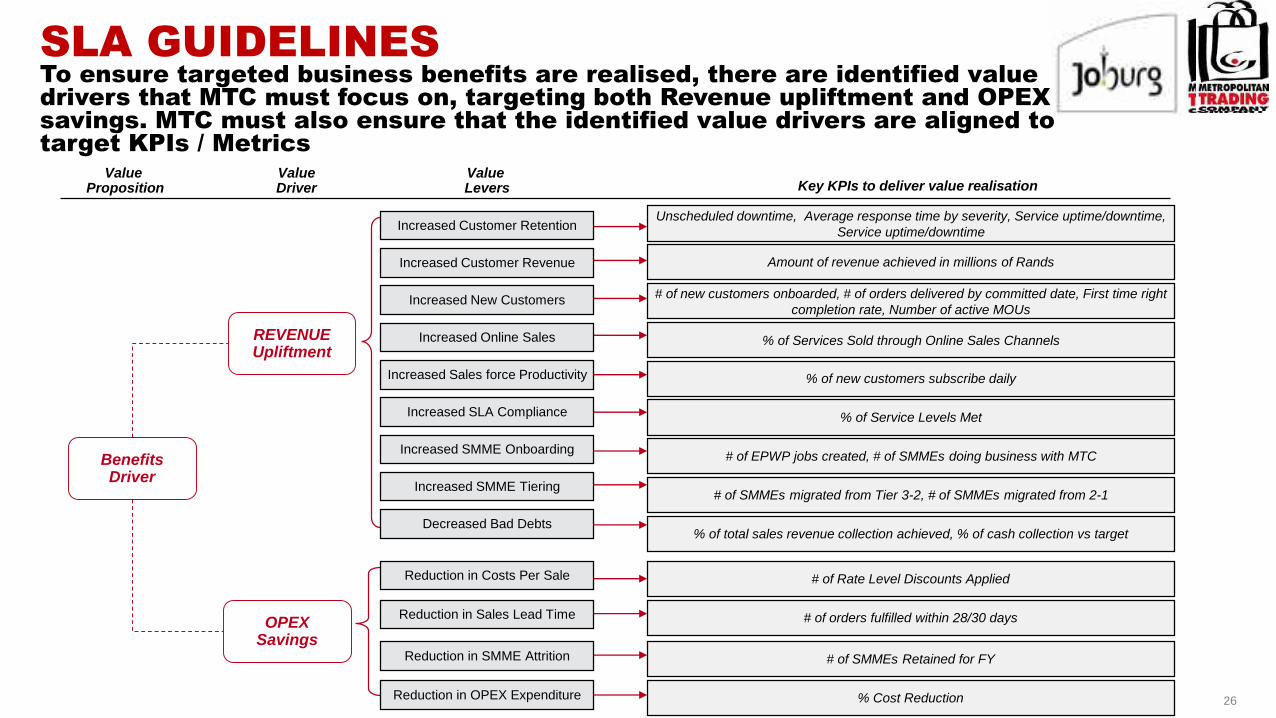

THE SERVICE LEVEL AGREEMENT (SLA)

26

Benefits Driver

REVENUE Upliftment

OPEX Savings

Value Proposition Key KPIs to deliver value realisation

Value Driver

Value Levers

Unscheduled downtime, Average response time by severity, Service uptime/downtime,

Service uptime/downtime

Amount of revenue achieved in millions of Rands

# of new customers onboarded, # of orders delivered by committed date, First time right

completion rate, Number of active MOUs

% of Services Sold through Online Sales Channels

% of new customers subscribe daily

% of Service Levels Met

# of EPWP jobs created, # of SMMEs doing business with MTC

# of SMMEs migrated from Tier 3-2, # of SMMEs migrated from 2-1

% of total sales revenue collection achieved, % of cash collection vs target

# of Rate Level Discounts Applied

# of orders fulfilled within 28/30 days

# of SMMEs Retained for FY

% Cost Reduction

Increased Customer Retention

Increased Customer Revenue

Increased New Customers

Increased Online Sales

Increased Sales force Productivity

Increased SLA Compliance

Increased SMME Onboarding

Increased SMME Tiering

Decreased Bad Debts

Reduction in Costs Per Sale

Reduction in Sales Lead Time

Reduction in SMME Attrition

Reduction in OPEX Expenditure

SLA GUIDELINESTo ensure targeted business benefits are realised, there are identified value drivers that MTC must focus on, targeting both Revenue upliftment and OPEX savings. MTC must also ensure that the identified value drivers are aligned to target KPIs / Metrics

ECONOMIC CONTRIBUTION

28

SMME TAPPING INTO COJ CUSTOMER BASE

29

SMME TAPPING INTO COJ CUSTOMER BASE

30

SMME RESELLER LOCALISATION

31

BREAKING BARRIERS TO ENTRY

THANK YOU

QUESTIONS AND ANSWERS