Metropolitan Airport Authority of Rock Island County...

86

Metropolitan Airport Authority of Rock Island County, Illinois and Combined Affiliate Comprehensive Annual Financial Report For the Fiscal Year Ended June 30, 2012 Prepared by: Finance Department

Transcript of Metropolitan Airport Authority of Rock Island County...

Metropolitan Airport Authority ofRock Island County, Illinois andCombined Affiliate

Comprehensive AnnualFinancial Report

For the Fiscal Year Ended June 30, 2012

Prepared by:Finance Department

Contents

Introductory Section (unaudited)

Table of contentsLetter of transmittalOrganizational chartList of appointed officialsGFOA certificate

iii-v

vivii

viii

Financial Section

Independent auditor's reportManagement's discussion and analysisFinancial statements:

Combined statements of net assetsCombined statements of revenues, expenses and changes in net assetsCombined statements of cash flowsNotes to basic combined financial statements

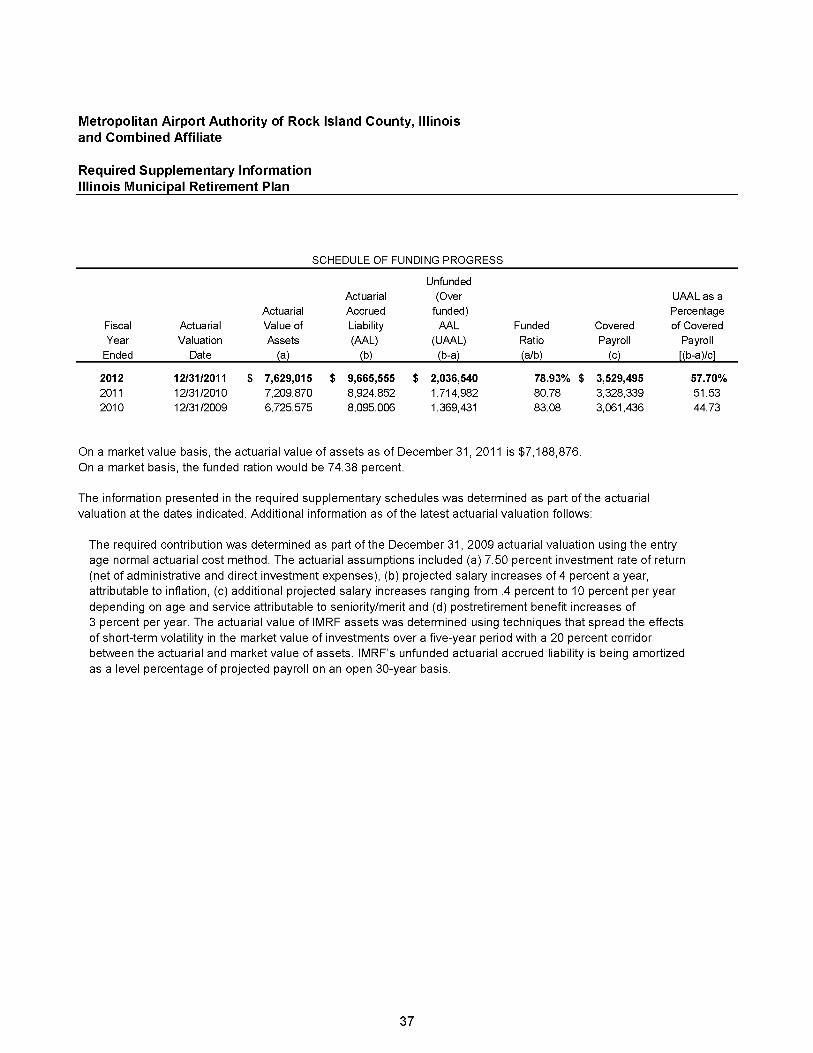

Required supplementary information:Illinois Municipal Retirement PlanMetropolitan Airport Authority Health Benefit Plan

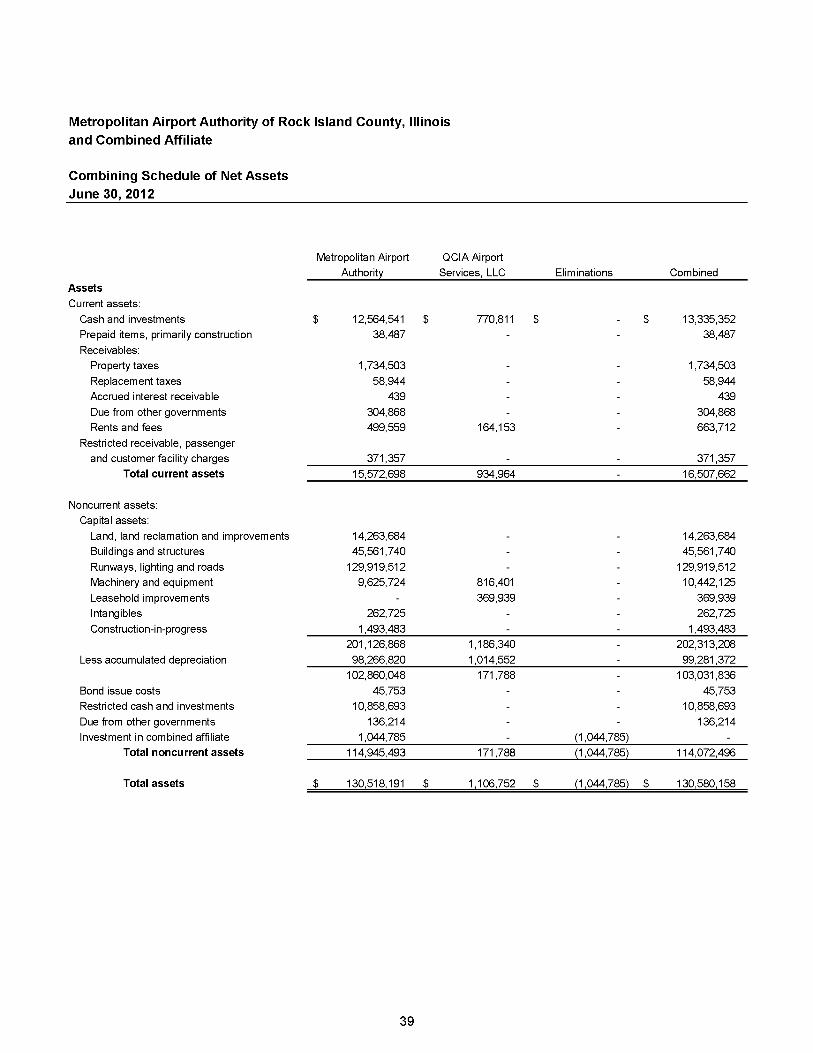

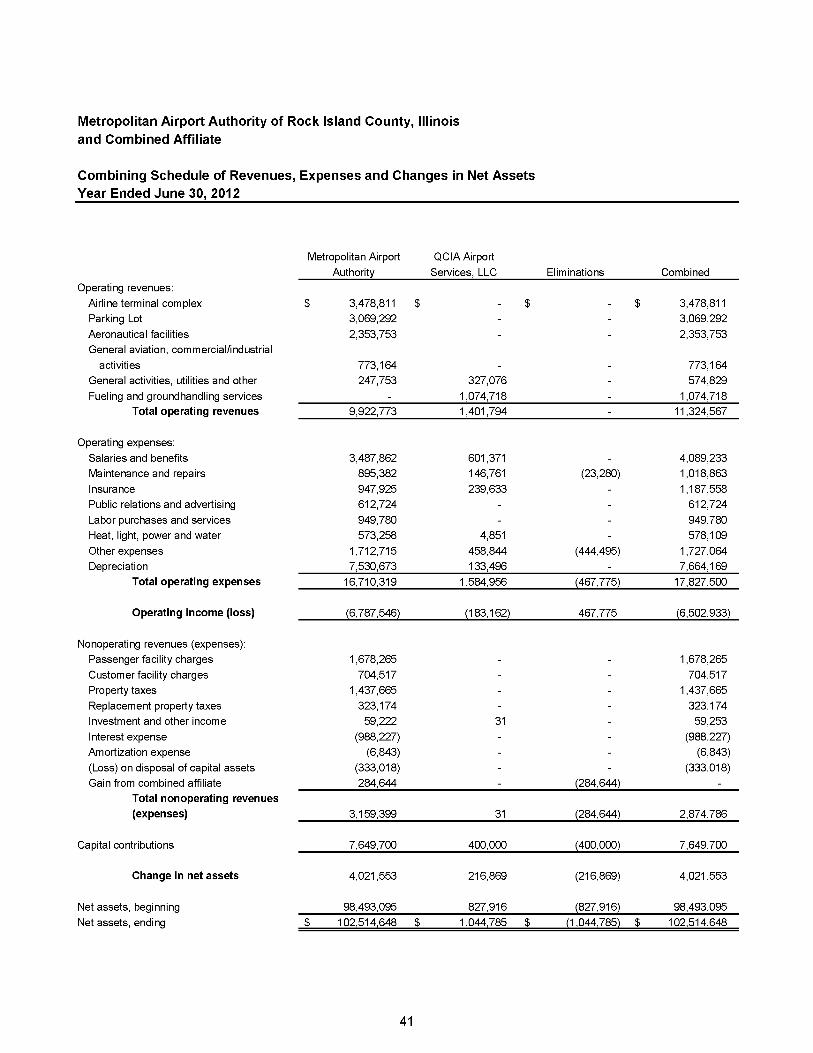

Supplementary information:Combining schedule of net assetsCombining schedule of revenues, expenses and changes in net assetsSchedule of other expenses

1-23 - 11

12 - 1314

15 - 1617 - 36

3738

39 -404142

Statistical Section (unaudited)

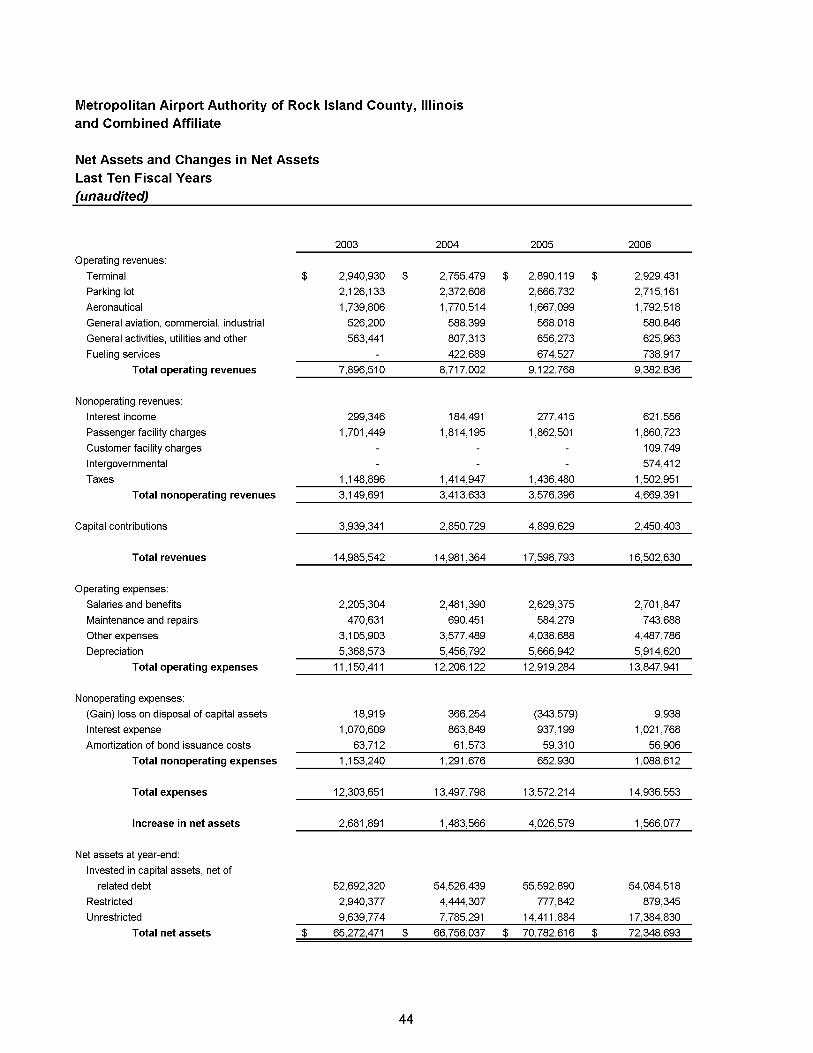

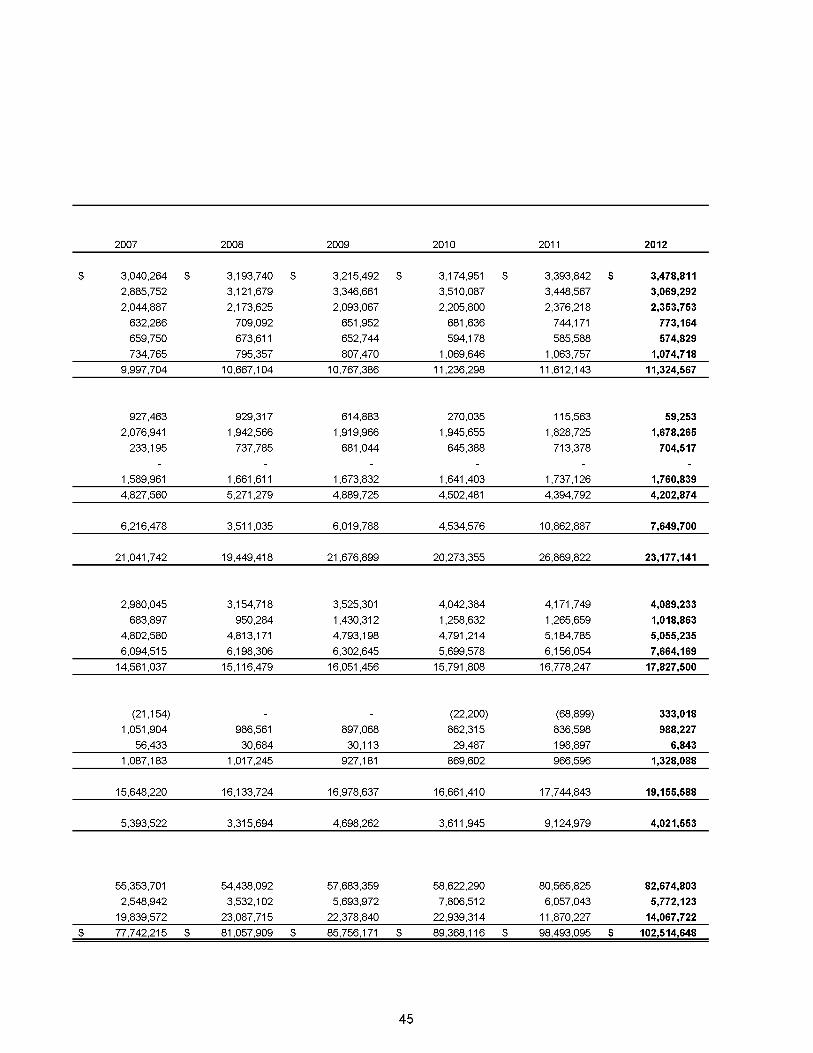

Statistical section contentsNet assets and changes in net assetsPrincipal revenue sources and revenues per enplaned passengerChanges in cash and cash equivalentsRevenue ratesRatios of outstanding debt, debt service and debt limitsPledged revenue coveragePopulation in the air trade areaPrincipal employersAuthority and combined affiliate employeesEnplaned passengersTakeoff and landing operations summaryTakeoff and landing operations by airline or cargo carrierAirline landed weightsPrimary origin and destination passenger marketsCapital asset information

4344 -4546 -4748 -4950 - 5152 - 5354 - 5556 - 57

5859 -6061 - 62

6364 -6566 -67

6869

METROPOLITAN AIRPORT AUTHORITY

OF ROCK ISLAND COUNTY, ILLINOISQUAD CITY INT'L AIRPORTP.O. BOX 9009MOLINE, IL 61265-9009309-764-9621(309) 757-1515 FAX

December 4, 2012

Commissioners, Citizens of Rock Island County and Other Interested Parties:

State law requires that every general purpose local government publish within six months of the close ofeach fiscal year a complete set of audited financial statements. This report is published to fulfill thatrequirement for the fiscal year ended June 30, 2012.

Management assumes full responsibility for the completeness and reliability of the information containedin this report, based upon a comprehensive framework of internal control that it has established for thispurpose. Because the cost of internal control should not exceed anticipated benefits, the objective is toprovide reasonable, rather than absolute, assurance that the financial statements are free of any materialmisstatements.

McGladrey LLP, Certified Public Accountants, have issued an unqualified ("clean") opinion on theMetropolitan Airport Authority of Rock Island County, Illinois' (Authority) financial statements for the yearended June 30, 2012. The independent auditor's report is located at the front of the financial section ofthis report.

Management's discussion and analysis (MD&A) immediately follows the independent auditor's report andprovides a narrative introduction, overview and analysis of the basic financial statements. MD&Acomplements this letter of transmittal and should be read in conjunction with it.

Profile of Government

In 1910, a Rock River valley pasture, known as Franing Field, was selected for the first coast-to-coastflight by army planes. Three men leased 30 acres in this pasture and it officially became an airport. One-year later real estate had increased to 200 acres. In 1926, regular airmail service began. Operations wereexpanded in 1927 when Boeing Air Transport began flying between Chicago and San Francisco. Laterthat year, Boeing Air Transport, Valley Air Transport, Pacific Air Transport, and National merged to formUnited Airlines which provided passenger and mail service to the east and west coasts as well as to thesouthwestern United States.

In 1935, the City of Moline, Illinois, took over the Airport as a municipal, tax supported airport. The secondlargest Work Projects Administration project in Illinois was underway at a cost to Moline of $165,000 and$365,000 to the federal government. A new terminal and hangar were built in 1939 with five scheduled aircarrier flights per day and 24 private aircraft based on airport property. Rock Island County citizens votedin 1947 to buy the Airport creating the Metropolitan Airport Authority of Rock Island County, Illinois, as itsowner and under the jurisdiction of the state of Illinois. Currently, seven townships in Rock Island Countyprovide financial support to the Airport. They include Hampton, Moline, South Moline, Rock Island, SouthRock Island, Blackhawk and Coal Valley. The mayors of Moline, Milan, East Moline, Rock Island, andSilvis each appoint one commissioner to the Authority's board, and the Chair of the Rock Island CountyBoard aoooints three more with the consent of the Board.

ii

Ozark Air Lines began service at the Airport in 1950. In 1954, a terminal building was built to providespace for United and Ozark Airlines, as well as limousine service, car rentals, the Civil AeronauticsAdministration, and the U. S. Weather Bureau. In March 1985, a new terminal, parking lot and roadwaysystem were completed. Major improvements have been made since that time to the terminal and otherpublic space, most notably a capital project expanding the terminal and concourses to nearly 160,000square feet in 2001 and redesign of the public parking lot to accommodate over 2,000 vehicles in both1999 and 2009 in anticipation of increased utilization of the state-of-the-art facility.

Many customer service elements have continued to be added in recent years, providing furtherconveniences for today's traveler. The Authority has contracted for customer care services and curbside(skycap) assistance. Wheelchair and electric golf cart services, as well as skycap services assist travelersof all ages as needed for arriving and departing flights. Technological advances with the airport's websiteand complimentary wi-fi connectivity in the terminal add to the conveniences for the business traveler.

The Metropolitan Airport Authority owns and operates over $100 million in assets on the more than 2,000-acre campus. Some of those assets include a four-bay public safety building, impressive airfieldmaintenance facility, and other structures that serve a variety of needs on Airport property. An air freightcomplex opened in 1992. Additionally, various hangars for private and corporate aircraft along with anindustrial park complement the landscape on the south side of the property. The longest runway extendsjust over 10,000 feet, and improvement projects are continuously underway to further enhance safety andefficiency for aircraft at the Quad City International Airport. Federal and state dollars are used to supportmost projects that are related to the airfield.

Local Economy

The Quad Cities metropolitan area is located along the Mississippi River in eastern Iowa and westernIllinois, approximately 165 miles west of Chicago and midway between Minneapolis to the north and St.Louis to the south. The Quad City region has a population of approximately 422,000. The following arethe top 10 employers in the area:

Company Employees Type of Business

Rock Island Arsenal

Deere & Company

Genesis Health System

Trinity Regional Health System

Tyson Fresh MeatsAlcoa, Inc.

Hy-Vee Food Stores

Kraft Foods/Oscar Mayer

XPACWal-Marl Super Centers

8,500

7,300

4,900

2,9002,400

2,250

1,622

1,500

1,195

1,066

Defense Manufacturing

Agiculture OEM

Health Care System

Health Care System

Food ProcesssingAerospace & Defense Aluminum

Supermarket and Other Grocery

Food Processsing

Supply Chain Management Logistics

Warehouse Clubs and Supercenters

The area boasts a healthy variety of tourism and recreational opportunities including hiking & biking trails,dozens of area golf and disc golf courses, ice skating and sporting facilities, arts and cultural festivals andevents and much more-all along the banks of the Mighty Mississippi River.

Long- Term Financial Planning

Federal and state funding for capital improvements is extremely important to the Authority. Airfield work islargely paid for by federal funds. Historically for the Airport, 95 percent of the costs of these projects hascome from federal sources. Due to budget cuts by Congress, the federal percentage of AirportImprovement Project costs for the Airport dropped to 90 percent for grants awarded in 2012. Passengerfacility charge (PFC) dollars also playa large role in funding airfield construction and purchasingequipment essential to the airfield and terminal.

iii

The Authority issued over $24 million in bonds, mostly secured by PFC revenue, on July 1, 2010. Thismoney refinanced existing PFC debt and was used to purchase snow removal equipment in 2011 andround out the funding of the airfield rehabilitation project of Runway 9/27 in 2011 and 2012. The proceedswill also be used to purchase five new loading bridges in fiscal year 2013.

For an Airport Authority, passengers drive discretionary revenue. Dollars spent by passengers on parking,eating and shopping is money available to the Authority for special projects and building cash reserves.Those reserves are earmarked for debt service and special projects outlined in the Major Initiativessection. Fiscal year 2012 brought in 409,795 passengers to the Quad City International Airport. This wasabout an 11 percent decrease over fiscal year 2011.

Passengers cannot patronize an airport without air service, so the Authority Board has included in itsstrategic plan a commitment to control costs that it passes on to its tenants. The Board has opted tosubsidize airline landing fees to remain price competitive with other airports in the area. In addition, it is agoal of the Authority to provide services to its airlines such as fueling and ground handling, at a moreaffordable rate than they can do it themselves or purchase from a third party vendor. The Board hasestablished certain levels of cash reserves for this purpose.

Relevant Financial Policies

The Federal Aviation Administration (FAA) disallows certain revenue generated by the Airport to be usedfor certain marketing incentives for airlines. This topic has gained the spotlight as many airlines needfinancial assistance. The Metropolitan Airport Authority is committed to the FAA regulations and their owninternal policy of not discriminating in the incentives offered to airlines, offering only incentives that helpdefray costs of the airlines and not issuing any type of revenue guarantees, and also financing thoseincentive packages with the appropriate revenue stream.

Major Initiatives

The Airport is currently working on a number of large capital projects. The runway 9/27 rehabilitationproject was completed mid-October 2011 , which improved the existing runways and reconstructed themidfield. A temporary runway -10/28 had been constructed and completed to be used during thereconstruction of runway 9/27. With runway 9/27 being complete, conversion of runway 10/28 into ataxiway began in fiscal year 2012. All associated lighting and painting on the temporary runway is beingaltered accordingly. This new taxiway (P for Papa) will allow aircraft from the General Aviation side of theairport to taxi to a main runway without having to cross an active runway. This is a major safetyenhancement.

Construction for the replacement of the Authority's aged fuel farm was completed in January 2012. Theend result of the fuel farm replacement included three 50,000-galion tanks for jet fuel, as well as threetanks for de-icing fluid for the airlines to use for storage and to fill their de-icing trucks. Also associatedwith the fuel farm project was the complete remodeling of a historic building called the "pump house" tobecome a support facility for the fuel farm. Lastly, the fuel farm access road was repaved with asphalt inJune of 2012.

The first phase of improving the rental car facilities was substantially completed in January 2011 byexpanding and repaving the rental car ready return lot. Phase two of the expansion includes theconstruction of a quick turn-around facility for fueling, washing and servicing rental cars. This work will bepaid for with Customer Facility Charge revenue. Construction on phase two is anticipated to begin in thespring/summer of 2013.

The Authority plans to expand its airfield maintenance building for storing snow removal equipment. Theaddition to the 32,000-square foot building will allow the airport to house all of its snow removalequipment under one roof and operate more efficiently. In Phase 1, an additional 14,000 square feet willbe added, and in Phase 2, another 10,000 square feet will be added. The Authority was awarded a $2.88million grant in September 2012 that will pay for 90 percent of the cost of expanding the building for bothphases 1 and 2. Site work is expected to cost around $1.3 million, bringing the total cost of the project to$5 to $5.2 million. The Authority expects to receive an additional grant that will pay for 90 percent of thesite work. The expansion is expected to begin in the fall of 2012, with the project lasting about a year.

iv

The Authority also started plans to convert a vacant airport-owned cargo building into a new FederalInspection Services Facility, which is needed to meet demand for the clearance of international cargo,passengers and flight crews. The estimated $2.8 million project will relocate the U.S. Customs and BorderProtection into the airport's Cargo Building No.3. It now operates out of the Civil Air Patrol building eastof the main terminal building on the airport. New federal requirements are forcing the Airport to relocatethe existing customs facility to accommodate more passengers and new technology. Construction on thisproject will begin in the fall of 2012 and will be completed in 2013. The Authority was awarded a $1.8million dollar grant in September of 2012 for this project.

An updated airport master plan is currently underway. The master plan is a comprehensive study of anairport that documents the short, medium, and long-term development plans needed to meet futureaviation demand. The overall goal of a master plan is to provide the framework needed to guide futureairport development that will cost-effectively satisfy aviation demand, while considering potentialenvironmental and socioeconomic impacts.

Economic development on airport land continues to be a focus for the Authority to increase non-aeronautical revenue through ground and building rents.

Economic development on airport land continues to be a focus for the Authority to increasenonaeronautical revenue through ground and building rents. Subsequent to year-end, the Authorityentered into a ground lease for a new hotel to be built on Airport land pending satisfaction of certaincontingencies, which would generate additional revenue through rents for the Authority. More informationcan be found in Note 13 to the basic financial statements.

Awards and Acknowledgements

The Government Finance Officers Association (GFOA) last awarded a Certificate of Achievement forExcellence in Financial Reporting to the Metropolitan Airport Authority for its comprehensive annualfinancial report (CAFR) for its fiscal year ended June 30, 2011. In order to be awarded a Certificate ofAchievement, the government had to publish an easily readable and efficiently organized CAFR thatsatisfied both accounting principles generally accepted in the United States of America and applicablelegal requirements.

A Certificate of Achievement is valid for a period of one year only. We believe that our current CAFRagain meets the Certificate of Achievement Program's requirements and we are submitting it to the GFOAto determine its eligibility for another certificate.

The preparation of this report would not have been possible without the efficient and dedicated service ofthe entire staff of the finance and administration department. We wish to express our appreciation to allmembers of the department who assisted and contributed to the preparation of this report. Credit alsomust be given to the Chair and Commissioners of the Authority Board for their unfailing support formaintaining the highest standards of professionalism in the management of the Authority's finances.

Respectfully submitted,

Bruce E.Carter, AAE.Director of Aviation

Angela M. Burch, CPAFinance Manager

v

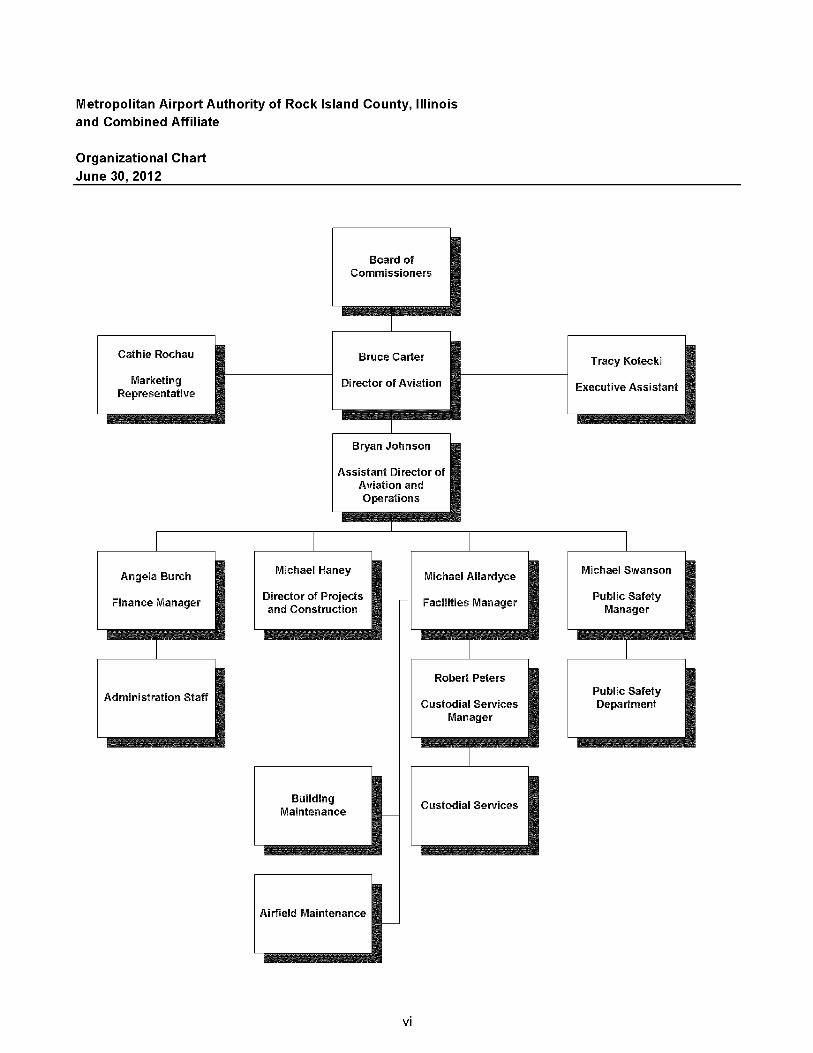

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Organizational ChartJune 30, 2012

Board ofCommissioners

I

Cathie Roehau Bruce Carter Tracy Kotecki

Marketing Director of Aviation Executive AssistantRepresentative

IBryan Johnson

Assistant Director ofAviation andOperations

I I I I

Angela Burch Michael Haney Michael Allardyce Michael Swanson

Finance Manager Director of Projects - Facilities Manager Public Safetyand Construction Manager

I I I

Robert Peters

Administration Staff Public SafetyCustodial Services Department

Manager

I

Building Custodial ServicesMaintenance -

Airfield Maintenance-

vi

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

List of Appointed OfficialsJune 30, 2012

Board of Commissioners

Carl Robinson, Chairman

James Jannes, Vice Chairman

Molly Foley, Secretary

Andrew Gianulis, Treasurer

James Davies, Commissioner

Robert Leibovitz, Commissioner

Donald Margenthaler, Commissioner

Richard Work, Commissioner

vii

Certificate ofAchievementfor Excellencein FinancialReporting

Presented to

Metropolitan Airport Authorityof Rock Island County

IllinoisFor its Comprehensive Annual

Financial Reportfor the Fiscal Year Ended

June 30, 2011

A Certificate of Achievement for Excellence in FinancialReporting is presented by the Government Finance Officers

Association of the United States and Canada togovernment units and public employee retirementsystems whose comprehensive annual financial

reports (CAFRs) achieve the higheststandards in government accounting

and financial reporting.

_e.President

Executive Director

viii

McGladrey LLP

II McGladreyIndependent Auditor's Report

To the Board of CommissionersMetropolitan Airport Authorityof Rock Island County, Illinoisand Combined AffiliateMoline, Illinois

We have audited the accompanying basic financial statements of the Metropolitan Airport Authority ofRock Island County, Illinois and Combined Affiliate (Authority), as of and for the years ended June 30,2012 and 2011, as listed in the table of contents. These financial statements are the responsibility of theAuthority's management. Our responsibility is to express an opinion on these financial statements basedon our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United Statesof America and the standards applicable to financial audits contained in Government Auditing Standards,issued by the Comptroller General of the United States. Those standards require that we plan andperform the audit to obtain reasonable assurance about whether the financial statements are free ofmaterial misstatement. An audit includes consideration of internal control over financial reporting as abasis for designing audit procedures that are appropriate in the circumstances, but not for the purpose ofexpressing an opinion on the effectiveness of the Authority's internal control over financial reporting.Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidencesupporting the amounts and disclosures in the financial statements. An audit also includes assessing theaccounting principles used and significant estimates made by management, as well as evaluating theoverall financial statement presentation. We believe that our audits provide a reasonable basis for ouropinions.

In our opinion, the basic financial statements referred to above present fairly, in all material respects, thefinancial position of the Metropolitan Airport Authority of Rock Island County, Illinois and CombinedAffiliate, as of June 30, 2012 and 2011, and the respective changes in financial position and its cash flowsfor the years then ended in conformity with accounting principles generally accepted in the United Statesof America.

In accordance with Government Auditing Standards for the years ended June 30, 2012 and 2011, wehave also issued our report dated December 4, 2012 and November 11, 2011, respectively, on ourconsideration of the Authority's internal control over financial reporting and our tests of its compliance withcertain provisions of laws, regulations, contracts and grant agreements, and other matters. The purposeof those reports is to describe the scope of our testing of internal control over financial reporting andcompliance and the results of that testing, and not to provide an opinion on the internal control overfinancial reporting or on compliance. Those reports are an integral part of an audit performed inaccordance with Government Auditing Standards and should be considered in assessing the results ofour audits.

Accounting principles generally accepted in the United States of America require that the Management'sDiscussion and Analysis, Illinois Municipal Retirement Plan and Metropolitan Airport Authority HealthBenefit Plan on pages 3 through 11, 37 and 38, respectively, be presented to supplement the basicfinancial statements. Such information, although not a part of the basic financial statements, is requiredby Governmental Accounting Standards Board who considers it to be an essential part of financialreporting for placing the basic financial statements in an appropriate operational, economic, or historicalcontext. We have applied certain limited procedures to the required supplementary information inaccordance with auditing standards generally accepted in the United States of America, which consistedof inquiries of management about the methods of preparing the information and comparing theinformation for consistency with management's responses to our inquiries, the basic financial statements,and other knowledge we obtained during our audit of the basic financial statements. We do not expressan opinion or provide any assurance on the information because the limited procedures do not provide uswith sufficient evidence to express an opinion or provide any assurance.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise the District's basic financial statements. The combining statements and schedule of otherexpenses, listed in the table of contents as supplementary information, are presented for purposes ofadditional analysis and are not a required part of the basic financial statements. Such information is theresponsibility of management and was derived from and relates directly to the underlying accounting andother records used to prepare the financial statements. The information has been subjected to theauditing procedures applied in the audit of the basic financial statements and certain additionalprocedures, including comparing and reconciling such information directly to the underlying accountingand other records used to prepare the financial statements or to the financial statements themselves, andother additional procedures in accordance with auditing standards generally accepted in the UnitedStates of America. In our opinion, the information is fairly stated in all material respects in relation to thefinancial statements as a whole.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise the District's basic financial statements. The accompanying introductory and statistical sections,as listed in the table of contents, are presented for purposes of additional analysis and are not a requiredpart of the basic financial statements. Such information has not been subjected to the auditing proceduresapplied in the audit of the basic financial statements, and accordingly, we do not express an opinion on orprovide assurance on it.

Davenport, IowaDecember 4, 2012

2

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

This Management's Discussion and Analysis (MD&A) of the Metropolitan Airport Authority of Rock IslandCounty, Illinois and Combined Affiliate (Authority) provides the reader with a narrative overview of theAuthority's financial statements and activities for the fiscal year ended June 30, 2012. Metropolitan AirportAuthority operates the Quad City International Airport in Moline, Illinois and QCIA Airport Services, LLC.

Overview of the Financial Statements

The basic combined financial statements are designed to provide readers with a broad overview of theAuthority's finances in a manner similar to a private-sector business. The basic combined financialstatements are prepared using proprietary fund (enterprise fund) accounting that uses the same basis ofaccounting as private-sector business enterprises. Under this method of accounting, an economicresources measurement focus and an accrual basis of accounting are used. Revenues are recordedwhen earned; expenses are recorded when incurred. For comparable purposes, each statementsummary in the MD&A includes fiscal year ended June 30, 2010, amounts also. The basic combinedfinancial statements include the accounts of the following entities:

• Metropolitan Airport Authority, which provides an airline terminal, runways and other aeronauticalfacilities in Moline, Illinois, for passenger and freight airlines and private aircraft.

• QCIA Airport Services, LLC, which provides fueling and ground handling services to commercialand charter airlines. The Authority is the sole member of this entity.

The basic financial statements include a combined statement of net assets, a combined statement ofrevenues, expenses and changes in net assets, and a combined statement of cash flows. These arefollowed by notes to basic financial statements. In addition to the basic combined financial statements,this report also contains supplementary information.

The combined statement of net assets presents information on all of the Authority's assets and liabilities,with the difference between the two reported as net assets. Over time, increases or decreases in netassets may serve as a useful indicator of whether the financial position of the Authority is improving ordeteriorating. The combined statement of revenues, expenses and changes in net assets reports theoperating revenues and expenses and nonoperating revenues and expenses of the Authority for the fiscalyear with the difference being the change in net assets for the fiscal year. The combined statement ofcash flows reports cash and cash equivalents for the fiscal year resulting from operating activities,noncapital financing activities, capital and related financing activities, and investing activities.

The basic financial statements include only the Metropolitan Airport Authority of Rock Island County,Illinois, and the QCIA Airport Services, LLC. There are no other organizations or agencies whose financialstatements should be combined and presented with the financial statements.

Financial Highlights

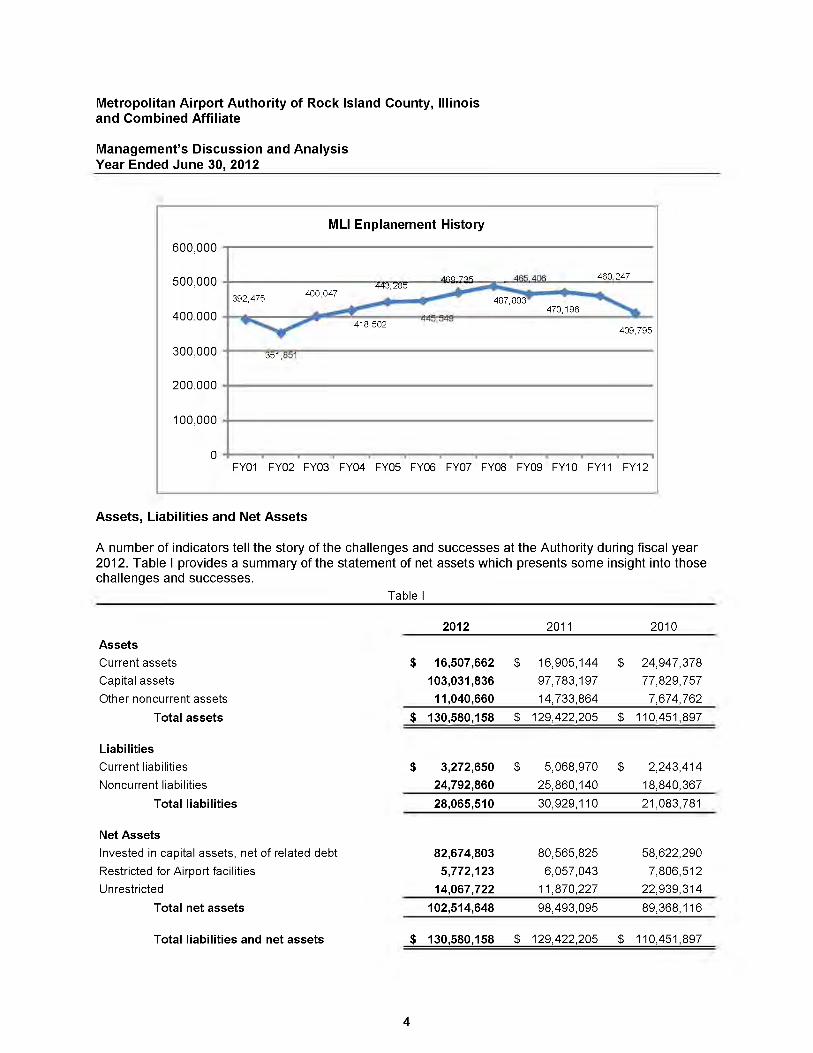

• In fiscal year 2012, total enplanements (see following chart) were 409,795 compared to 460,247 inthe prior year and 470,196 in fiscal year 201 O. QCIA enplanements decreased by approximately11 percent in the current year.

• Net assets increased $4,021,553 in fiscal year 2012, $9,124,979 in fiscal year 2011 and$3,611,945 in fiscal year 2010.

3

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

MLI Enplanement History

600,000

500,000 A"n 7~" .oR".oM 460,2474'13';'"LlK,

392,475 400,047 ~487,803""-

~400,000 .-.- 470,196

~418,502 409,795

300,000 jc.1,i:!c.1

200,000

100,000

0 .FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Assets, Liabilities and Net Assets

A number of indicators tell the story of the challenges and successes at the Authority during fiscal year2012. Table I provides a summary of the statement of net assets which presents some insight into thosechallenges and successes.

Table I

2012 2011 2010

Assets

Current assets $ 16,507,662 $ 16,905,144 $ 24,947,378

Capital assets 103,031,836 97,783,197 77,829,757

Other noncurrent assets 11,040,660 14,733,864 7,674,762

Total assets $ 130,580,158 $ 129,422,205 $ 110,451,897

Liabilities

Current liabilities $ 3,272,650 $ 5,068,970 $ 2,243,414

Noncurrent liabilities 24,792,860 25,860,140 18,840,367

Total liabilities 28,065,510 30,929,110 21,083,781

Net Assets

Invested in capital assets, net of related debt 82,674,803 80,565,825 58,622,290

Restricted for Airport facilities 5,772,123 6,057,043 7,806,512Unrestricted 14,067,722 11,870,227 22,939,314

Total net assets 102,514,648 98,493,095 89,368,116

Total liabilities and net assets $ 130,580,158 $ 129,422,205 $ 110,451,897

4

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

Total assets increased 0.9 percent in fiscal year 2012. Current assets decreased $397,482 whilenoncurrent assets increased $1,555,435. This net increase is primarily due to restricted cash from the2010 bond issue proceeds being used towards the Authority's local share of the reconstruction of Runway9/27, which in turn contributed to the increase in capital assets in 2012. In 2011, total assets increased17.2 percent from 2010.

Total liabilities decreased 9.3 percent. Liabilities were higher in fiscal year 2011 due to the issuance ofnew debt on July 1, 2010 and the related accrued interest recorded at June 30, 2011 of seventeenmonths due to a lag in timing of when the first principal and interest payments were due compared to sixmonths of accrued interest recorded as of June 30, 2012. In addition, accounts payable decreasedsignificantly over the prior fiscal year due to the significant construction in progress at June 30, 2011related to the new fuel farm and Runway 9/27. In 2011, total liabilities increased 46.7 percent from 2010.

Current assets less current liabilities (net working capital) increased 11.8 percent in 2012 and decreased47.9 percent in 2011. Net working capital is an indicator of the Authority's ability to address its currentobligations in a timely manner. Net working capital is $13,235,012 in 2012 compared to $11,836,174 in2011 and $22,703,964 in 2010. Current assets have decreased by $397,482 while current liabilities havealso decreased by $1,796,320 in 2012. Current assets and current liabilities primarily decreased due to adecrease in prepaid assets associated with the Runway 9/27 project, accrued interest payable, andaccounts payable discussed above. Current liabilities were also offset by an increase in the currentportion due within one year on the long-term debt.

Overall, net assets increased 4.1 percent in 2012 from $98,493,095 to $102,514,648 and 10.2 percent in2011 to $98,493,095 from $89,368,116 in 2010.

Revenues and Expenses

Useful financial information is also provided on the combined statement of revenues, expenses andchanges in net assets. This report tracks the operating activities and nonoperating activities of theAuthority for the year and compares them with the activities of the prior years. Table II highlights theMetropolitan Airport Authority's revenues and expenses for the fiscal years ended June 30, 2012, 2011and 2010.

5

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

Table II

2012 2011 2010

Operating revenues:

Airline terminal complex $ 3,478,811 $ 3,393,842 $ 3,174,951

Parking Lot 3,069,292 3,448,567 3,510,087

Aeronautical facilities 2,353,753 2,376,218 2,205,800

Other operating, including general aviation and

commercial/i ndustrial 1,347,993 1,329,759 1,275,814

Fueling and groundhandling services 1,074,718 1,063,757 1,069,646

Total operating revenues 11,324,567 11,612,143 11,236,298

Operating expenses:

Salaries and benefits 4,089,233 4,171,749 4,042,384

Depreciation 7,664,169 6,156,054 5,699,578

Other operating expenses 6,074,098 6,450,444 6,049,846

Total operating expenses 17,827,500 16,778,247 15,791,808

Nonoperating revenues (expenses):

Passenger and Customer facility charges 2,382,782 2,542,103 2,591,043

Taxes 1,760,839 1,737,126 1,641,403

Other nonoperating income, including gain on

disposal of assets 59,253 184,462 292,235

Loss on disposal of capital assets (333,018)Interest expense (988,227) (836,598) (862,315)

Other nonoperating expenses (6,843) (198,897) (29,487)

Total nonoperating revenues 2,874,786 3,428,196 3,632,879

(Loss) before capital contributions (3,628,147) (1,737,908) (922,631)

Capital contributions 7,649,700 10,862,887 4,534,576

Change in net assets 4,021,553 9,124,979 3,611,945

Net assets, beginning 98,493,095 89,368,116 85,756,171

Net assets, ending $ 102,514,648 $ 98,493,095 $ 89,368,116

Airline terminal complex revenue includes reimbursements from airlines for their common and exclusivespace in the facility. The airline use agreements specify which Airport expenses are reimbursable andthose reimbursements are recorded as revenue. Changes in terminal expenses affect the airline terminalcomplex revenue. Total revenues in 2012 are $23,177,141 compared to $26,938,721 and $20,295,555 in2011 and 2010, respectively.

6

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

Eighty-seven percent of the terminal space (136,161 out of 157,652 square feet) is known as rentablespace. A portion of rentable space known as common space (54,958 square feet) is composed of thebaggage claim area, connector area between the terminal and security screening checkpoint, andConcourses A and B and is charged to the airlines for reimbursement of costs.

500,000

• Other Sources

Terminal Rate Base Costs to be Reimbursed

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000 _Airline Portion

1,000,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

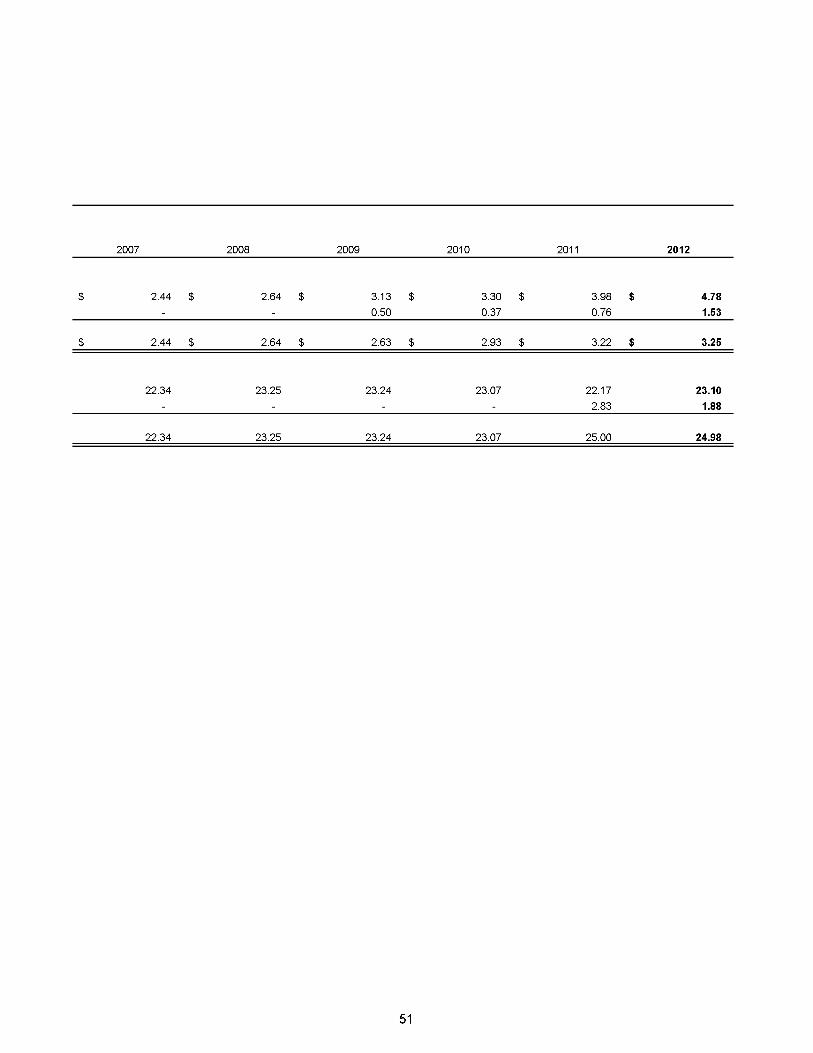

This cost breaks down to $23.26 per square foot 10 years ago when the airline portion of common spacereimbursable costs totaled $1,287,353 to $23.10 in 2012 when the airline portion amounted to$1,269,530, a decrease of 1.4 percent in airline liability since 2003. The cost per square foot was $22.17in fiscal year 2011. In fiscal year 2012 and 2011, the Authority had actually billed $24.98 and $25.00,respectively, per square foot to the airlines compared to the $23.10 and $22.17, respectively calculated atthe end of each year. The amount owed back to the airlines in each year was used to offset theAuthority's subsidy in landing fees for 2012 and 2011.

The QCIA Airport Services, LLC had fiscal year 2012 operating revenues of $1 ,401 ,794 compared tooperating expenses of $1,584,956. The operating loss of $183,162 combined with nonoperating incomeof $31 resulted in a loss of $183,131 on an unconsolidated basis prior to a capital contribution subsidyfrom the Metropolitan Airport Authority of $400,000. This compares to $1,384,505 of operating revenuesand $1,780,628 of operating expenses in fiscal year 2011. The losses can be attributed to the ground-handling department.

Airport revenues decreased 14 percent or $3,761,580 from 2011 to 2012 and increased 32.7 percent or$6,643,166 from 2010 to 2011. These changes are primarily due to the fluctuation in capital contributionseach year. Capital contributions are federal and state revenues for construction or acquisition of capitalassets. Increases and decreases correspond to the changes in construction-in-progress.

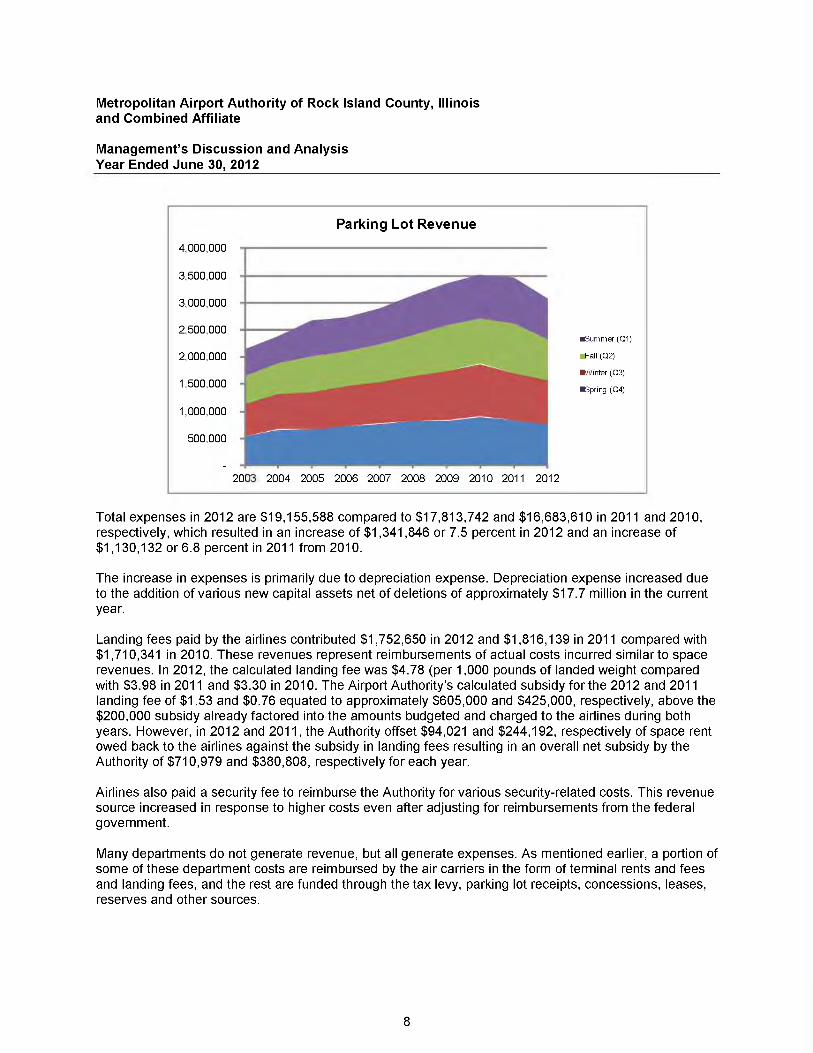

Parking lot revenue decreased 11 percent in 2012 and decreased 1.8 and increased 4.9 percent, over2011 and 2010, respectively. The number of enplanements at QCIA is a large factor in the fluctuation ofparking lot revenues. In 2012, enplanements decreased 11 percent. Overall, this significant revenuesource helped the Authority abate the taxes tied to the debt and provided needed funding for programsnot covered by other sources. As the following chart notes, use of the public parking facility has beensteady year-round for many years.

7

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

500,000

.summer (01)

Parking Lot Revenue

4,000,000

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

Fall (02)

-.;vinter (03)-Spring (04)

1,000,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Total expenses in 2012 are $19,155,588 compared to $17,813,742 and $16,683,610 in 2011 and 2010,respectively, which resulted in an increase of $1 ,341 ,846 or 7.5 percent in 2012 and an increase of$1,130,132 or 6.8 percent in 2011 from 2010.

The increase in expenses is primarily due to depreciation expense. Depreciation expense increased dueto the addition of various new capital assets net of deletions of approximately $17.7 million in the currentyear.

Landing fees paid by the airlines contributed $1,752,650 in 2012 and $1,816,139 in 2011 compared with$1,710,341 in 2010. These revenues represent reimbursements of actual costs incurred similar to spacerevenues. In 2012, the calculated landing fee was $4.78 (per 1,000 pounds of landed weight comparedwith $3.98 in 2011 and $3.30 in 2010. The Airport Authority's calculated subsidy for the 2012 and 2011landing fee of $1.53 and $0.76 equated to approximately $605,000 and $425,000, respectively, above the$200,000 subsidy already factored into the amounts budgeted and charged to the airlines during bothyears. However, in 2012 and 2011, the Authority offset $94,021 and $244,192, respectively of space rentowed back to the airlines against the subsidy in landing fees resulting in an overall net subsidy by theAuthority of $710,979 and $380,808, respectively for each year.

Airlines also paid a security fee to reimburse the Authority for various security-related costs. This revenuesource increased in response to higher costs even after adjusting for reimbursements from the federalgovernment.

Many departments do not generate revenue, but all generate expenses. As mentioned earlier, a portion ofsome of these department costs are reimbursed by the air carriers in the form of terminal rents and feesand landing fees, and the rest are funded through the tax levy, parking lot receipts, concessions, leases,reserves and other sources.

8

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

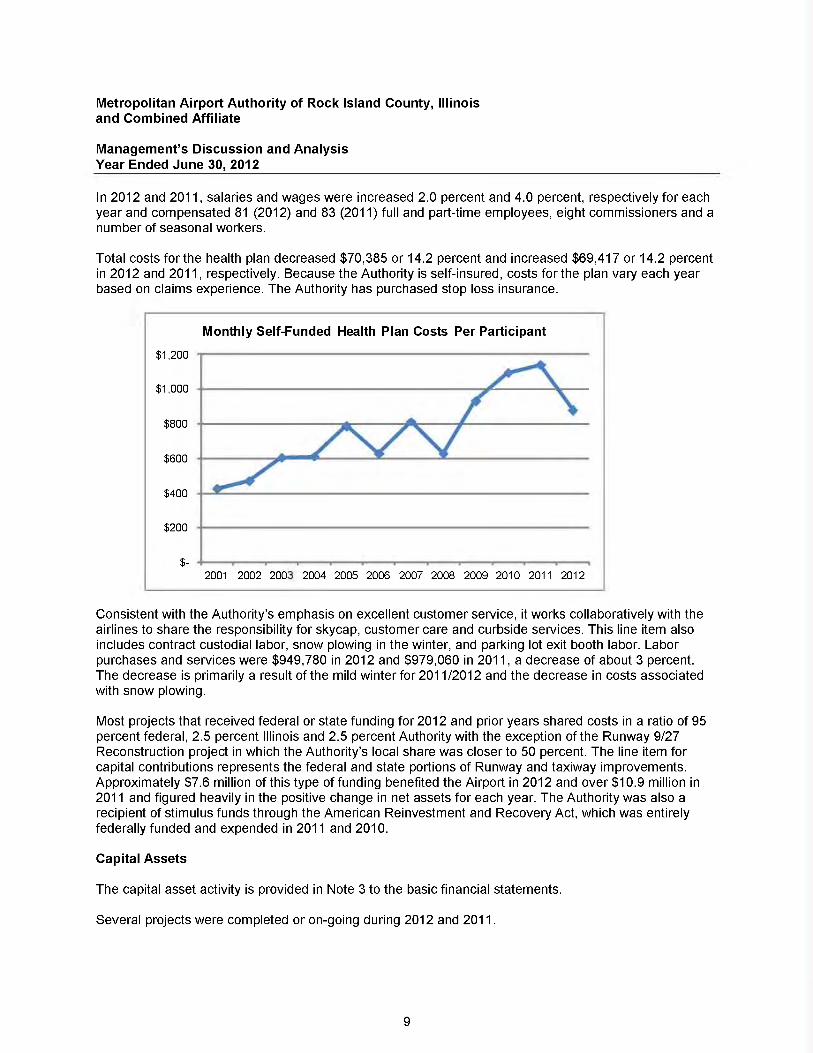

In 2012 and 2011, salaries and wages were increased 2.0 percent and 4.0 percent, respectively for eachyear and compensated 81 (2012) and 83 (2011) full and part-time employees, eight commissioners and anumber of seasonal workers.

Total costs for the health plan decreased $70,385 or 14.2 percent and increased $69,417 or 14.2 percentin 2012 and 2011, respectively. Because the Authority is self-insured, costs for the plan vary each yearbased on claims experience. The Authority has purchased stop loss insurance.

Monthly Self-Funded Health Plan Costs Per Participant

$1,200

$1,000

$800

$600

$400

$200

$-2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Consistent with the Authority's emphasis on excellent customer service, it works collaboratively with theairlines to share the responsibility for skycap, customer care and curbside services. This line item alsoincludes contract custodial labor, snow plowing in the winter, and parking lot exit booth labor. Laborpurchases and services were $949,780 in 2012 and $979,060 in 2011, a decrease of about 3 percent.The decrease is primarily a result of the mild winter for 2011/2012 and the decrease in costs associatedwith snow plowing.

Most projects that received federal or state funding for 2012 and prior years shared costs in a ratio of 95percent federal, 2.5 percent Illinois and 2.5 percent Authority with the exception of the Runway 9/27Reconstruction project in which the Authority's local share was closer to 50 percent. The line item forcapital contributions represents the federal and state portions of Runway and taxiway improvements.Approximately $7.6 million of this type of funding benefited the Airport in 2012 and over $10.9 million in2011 and figured heavily in the positive change in net assets for each year. The Authority was also arecipient of stimulus funds through the American Reinvestment and Recovery Act, which was entirelyfederally funded and expended in 2011 and 2010.

Capital Assets

The capital asset activity is provided in Note 3 to the basic financial statements.

Several projects were completed or on-going during 2012 and 2011.

9

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

In 2012, significant projects included:

• Completion of the Runway 9/27 reconstruction project which reworked our current Runwaysystem.

• Construction began on converting Runway 10/28 to a new Taxiway (Taxiway P). This Runwaywas completed in 2011 and was used as a temporary Runway during the reconstruction ofRunway 9/27.

• Completion of the new fuel farm which replaced the aging fuel farm with new tanks.

In 2011, significant projects included:

• Construction engineering and construction work began on the Rehabilitation of the Runway 9/27project.

• Completion of various Taxiway P paving projects which is being used as a temporary Runway(Runway 10/28) during the reconstruction of Runway 9/27.

• Completion of new parking associated with the employee lot as well as the rental car ready returnlot.

• Completion of new administrative office space.

• Completion of a temporary localizer on Runway 10.

• Completion of the Taxiway D relocation project.

• Purchase of a hanger from a major corporation.

• Construction began on the new fuel farm.

• Purchases of new snow removal equipment including 4 new snow brooms, a Hagie Spray Vehicle,a high speed snow blower.

• Purchases of 3 new John Deere Tractor/Mowers.

Long-Term Debt

The Metropolitan Airport Authority did not issue any new debt in the current year. The unused legal debtcapacity is $43,665,758, which represents 2.3 percent of the assessed valuation less the debt to berepaid by pledged revenue pursuant to the applicable bond ordinance. More information regarding thelong-term debt of Metropolitan Airport Authority and combined affiliate can be found in Note 4 to the basicfinancial statements.

Economic Factors

Twelve hubs, or connecting cities, were served during the majority of fiscal year 2012. AirTran stoppedserving the Orlando market in January 2012 and ceased all operations at the QCIA after a fifteen yearhistory between AirTran and the Metropolitan Airport Authority.

Allegiant, the newest carrier to the Authority, began service to Las Vegas and Phoenix-Mesa in the fall of2010. They quickly added the Tampa Bay area (St. Petersburg/Clearwater) to this list in February 2011and then Orlando-Sanford in February 2012. While most of these four cities saw two flights per week,there were on occasion more flights added during peak holiday times. The public has been supporting theflights to these much requested leisure destinations.

10

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Management's Discussion and AnalysisYear Ended June 30, 2012

The QCIA Airport Services, LLC continued to work the ground handling (above/below wing) operations forthe AirTran and Allegiant flights as well as charters for honor flights, gambling junkets and football teams.

American Eagle continued service to Chicago O'Hare and Dallas-Ft. Worth. Delta continued service toAtlanta, Detroit, Minneapolis-St. Paul and Memphis; although flights to these hubs varied over the monthsand aircraft size changed on these routes frequently. The Memphis route was discontinued in September2011 due to the Airline's reorganization of the Memphis hub. United Express continues their flights toChicago O'Hare and Denver. Much like Delta, aircraft size continues to vary depending on the subsidiarycarrier flying the routes for United Express.

Authority management will be watching the effects that these service changes will have on passengernumbers and the complexion of concession revenue at the QCIA. Enplanements/deplanements weredown approximately 11 percent over the prior fiscal year. The high cost of fuel over the fiscal yearcontinued. As a result of this and other economic factors, the airlines began reducing their overallcapacity and made a variety of adjustments to their routes, type and size of aircraft flown. One thing thatcontinues to evolve with the airlines is the addition of ancillary fees for baggage, seat selection, and othersimilar amenities in order for the airlines to explore alternative revenues that are not attached directly tothe ticket price.

As in the prior years, due diligence will be exercised during budget planning to target areas for savingsand efficiency. All capital projects planned have been started and each has a dedicated revenue streamto ensure payment. Future projects will need to be prioritized and perhaps delayed depending on theeconomic impact of the air service changes. The Board and management are also looking for ways toincrease non-aeronautical revenue for the airport such as ground and building rents through economicdevelopment on airport land.

Requests for Information

This financial report has been prepared in the spirit of full disclosure to provide the reader with anoverview of the Metropolitan Airport Authority's financial operations. If the reader has questions or wouldlike additional information about the Metropolitan Airport Authority of Rock Island County, Illinois or QCIAAirport Services, LLC, please direct the request to Bruce Carter, Director of Aviation, at P. O. Box 9009,Moline, Illinois 61265.

11

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

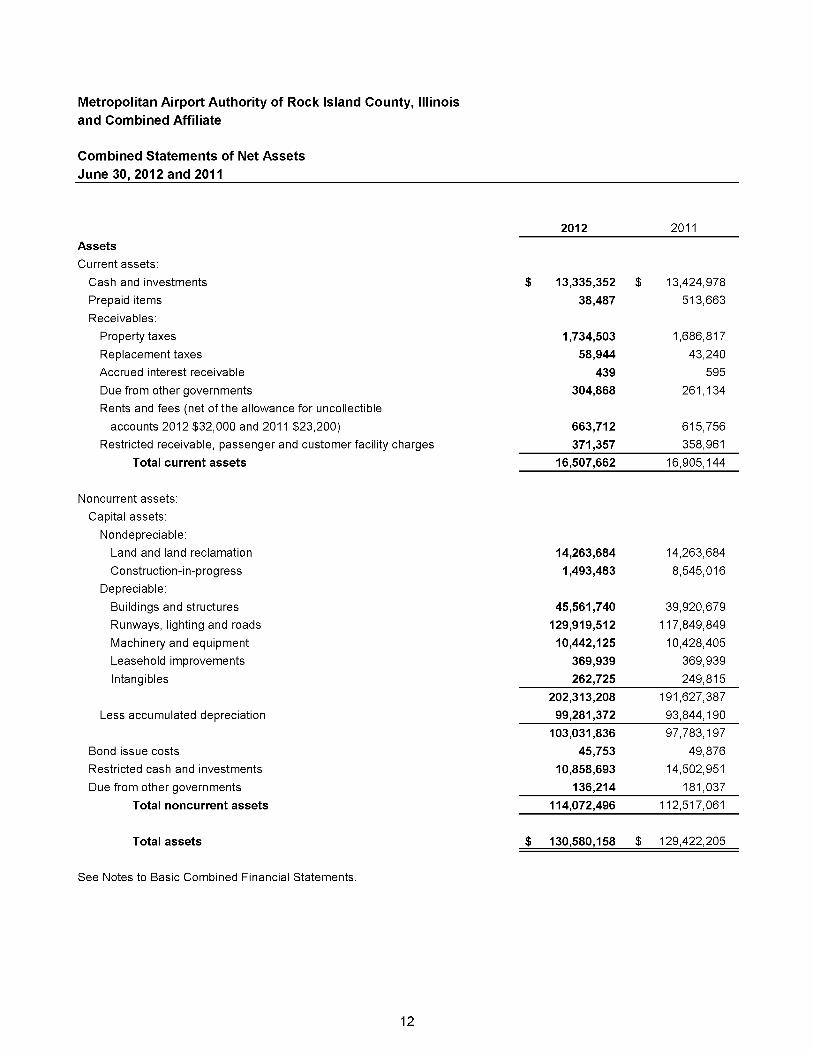

Combined Statements of Net AssetsJune 30, 2012 and 2011

2012 2011

AssetsCurrent assets:

Cash and investments $ 13,335,352 $ 13,424,978

Prepaid items 38,487 513,663

Receivables:

Property taxes 1,734,503 1,686,817

Replacement taxes 58,944 43,240

Accrued interest receivable 439 595

Due from other governments 304,868 261,134Rents and fees (net of the allowance for uncollectible

accounts 2012 $32,000 and 2011 $23,200) 663,712 615,756Restricted receivable, passenger and customer facility charges 371,357 358,961

Total current assets 16,507,662 16,905,144

Noncurrent assets:

Capital assets:

Nondepreciable:

Land and land reclamation 14,263,684 14,263,684

Construction-in-progress 1,493,483 8,545,016

Depreciable:

Buildings and structures 45,561,740 39,920,679

Runways, lighting and roads 129,919,512 117,849,849

Machinery and equipment 10,442,125 10,428,405

Leasehold improvements 369,939 369,939

Intangibles 262,725 249,815

202,313,208 191,627,387

Less accumulated depreciation 99,281,372 93,844,190

103,031,836 97,783,197

Bond issue costs 45,753 49,876Restricted cash and investments 10,858,693 14,502,951

Due from other governments 136,214 181,037

Total noncurrent assets 114,072,496 112,517,061

Total assets $ 130,580,158 $ 129,422,205

See Notes to Basic Combined Financial Statements.

12

2012 2011

LiabilitiesCurrent liabilities:

Current portion, long-term debt

Accounts payable

Accrued compensated absences

Accrued salaries and wages

Accrued interest

Unearned revenue, primarily property tax

Claims payable

Due to other governments

Other

$ 1,070,000 $758,765233,946144,737103,718900,609

60,000

8755,068,970Total current liabilities 3,272,650

210,000

2,235,336

236,514

152,083

1,247,615

793,338

50,969

107,346

35,769

Noncurrent liabilities:

Long-term debt (net of discounts and deferred amount on

refunding 2012 $10,040; 2011 $12,760)

Other postemployment benefits

Total noncurrent liabilities

24,744,96047,900

25,812,240

47,900

25,860,14024,792,860

30,929,110Total liabilities 28,065,510

Net AssetsInvested in capital assets, net of related debt

Restricted for Airport facilities

Unrestricted

Total net assets

82,674,803 80,565,825

5,772,123 6,057,043

14,067,722 11,870,227

102,514,648 98,493,095

$ 130,580,158 $ 129,422,205Total liabilities and net assets

13

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Combined Statements of Revenues, Expenses and Changes in Net AssetsYears Ended June 30, 2012 and 2011

2012 2011Operating revenues:

Airline terminal complex $ 3,478,811 $ 3,393,842Parking lot 3,069,292 3,448,567

Aeronautical facilities 2,353,753 2,376,218General aviation, commercial/industrial activities 773,164 744,171General activities, utilities and other 574,829 585,588Fueling and ground handling services 1,074,718 1,063,757

Total operating revenues 11,324,567 11,612,143

Operating expenses:Salaries and benefits 4,089,233 4,171,749Maintenance and repairs 1,018,863 1,265,659Insurance 1,187,558 1,173,942Public relations and advertising 612,724 864,183Labor purchases and services 949,780 979,060Heat, light, power and water 578,109 602,836Other expenses 1,727,064 1,564,764Depreciation 7,664,169 6,156,054

Total operating expenses 17,827,500 16,778,247

Operating (loss) (6,502,933) (5,166,104)

Nonoperating revenues (expenses):Passenger facility charges 1,678,265 1,828,725Customer facility charges 704,517 713,378Property taxes 1,437,665 1,385,823Replacement property taxes 323,174 351,303Investment and other income 59,253 115,563Interest expense (988,227) (836,598)Amortization expense (6,843) (198,897)Gain (loss) on disposal of capital assets (333,018) 68,899

Total nonoperating revenues 2,874,786 3,428,196

Loss before capital contributions (3,628,147) (1,737,908)

Capital contributions 7,649,700 10,862,887Change in net assets 4,021,553 9,124,979

Net assets, beginning 98,493,095 89,368,116Net assets, ending $ 102,514,648 $ 98,493,095

See Notes to Basic Combined Financial Statements.

14

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

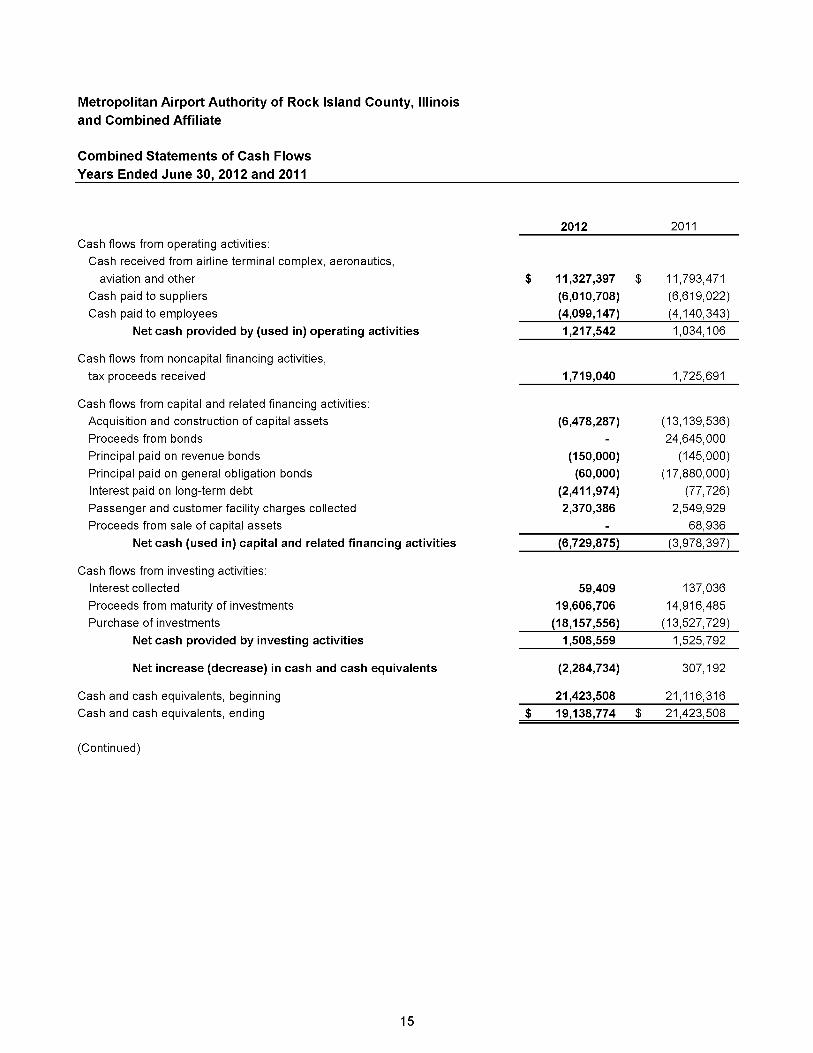

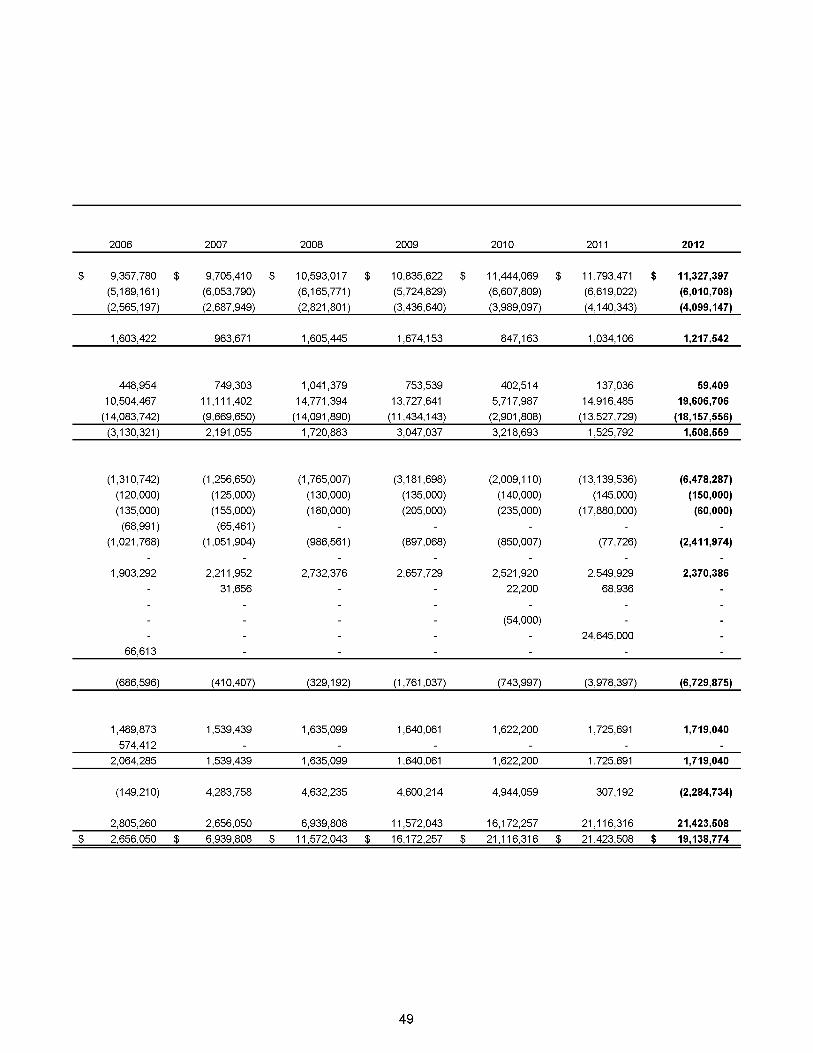

Combined Statements of Cash FlowsYears Ended June 30, 2012 and 2011

2012 2011Cash flows from operating activities:

Cash received from airline terminal complex, aeronautics,aviation and other $ 11,327,397 $ 11,793,471

Cash paid to suppliers (6,010,708) (6,619,022)Cash paid to employees (4,099,147) (4,140,343)

Net cash provided by (used in) operating activities 1,217,542 1,034,106

Cash flows from noncapital financing activities,

tax proceeds received 1,719,040 1,725,691

Cash flows from capital and related financing activities:Acquisition and construction of capital assets (6,478,287) (13,139,536)Proceeds from bonds 24,645,000Principal paid on revenue bonds (150,000) (145,000)Principal paid on general obligation bonds (60,000) (17,880,000)Interest paid on long-term debt (2,411,974) (77,726)Passenger and customer facility charges collected 2,370,386 2,549,929Proceeds from sale of capital assets 68,936

Net cash (used in) capital and related financing activities (6,729,875) (3,978,397)

Cash flows from investing activities:Interest collected 59,409 137,036Proceeds from maturity of investments 19,606,706 14,916,485Purchase of investments (18,157,556) (13,527,729)

Net cash provided by investing activities 1,508,559 1,525,792

Net increase (decrease) in cash and cash equivalents (2,284,734) 307,192

Cash and cash equivalents, beginning 21,423,508 21,116,316Cash and cash equivalents, ending $ 19,138,774 $ 21,423,508

(Continued)

15

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Combined Statements of Cash Flows (Continued)Years Ended June 30, 2012 and 2011

2012 2011Reconciliation of operating (loss) to net cash provided by

(used in) operating activities:Operating (loss) $ (6,502,933) $ (5,166,104)Adjustments to reconcile operating (loss) to net cash provided by

(used in) operating activities:Depreciation 7,664,169 6,156,054(Increase) decrease in:

Accounts receivable (47,956) 306,946Prepaid items 475,176 (439,450)

Increase (decrease) in:Accounts payable (420,817) 85,263Accrued salaries and wages (7,346) 7,049Accrued compensated absences (2,568) 24,357Unearned revenue 85,680 2,061Deposits (34,894) 6,961Claims payable 9,031 50,969

Net cash provided by (used in) operating activities $ 1,217,542 $ 1,034,106

Reconciliation of cash and cash equivalents to specific assetson the combined statements of net assets:Cash and investments $ 24,194,045 $ 27,927,929Less items not meeting the definition of cash equivalents 5,055,271 6,504,421Cash and cash equivalents at end of year $ 19,138,774 $ 21,423,508

Schedule of noncash capital and financing activities:Acquisition of capital assets through accounts payable

due to other governments and prepaid assets $ (1,163,100) $ 2,078,015Capital contributions 7,650,789 10,907,528Capitalized interest 279,850 476,435

See Notes to Basic Combined Financial Statements.

16

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 1. Nature of Business, Reporting Entity and Significant Accounting Policies

Nature of business:

The basic combined financial statements include the activities of the following entities:

Metropolitan Airport Authority (Airport) provides an airline terminal, runways and otheraeronautical facilities in Moline, Illinois, for passenger and freight airlines and private aircraft.

QCIA Airport Services, LLC (QCIAAS) provides fueling and ground handling services tocommercial and charter airlines. The Authority is the sole member of this entity. QCIAAS wascreated in fiscal year 2004 with a perpetual term.

The Airport and QCIAAS are collectively referred to as the Authority.

Reporting entity:

Accounting principles generally accepted in the United States of America require the reporting entityinclude (1) the primary government, (2) organizations for which the primary government is financiallyaccountable and (3) other organizations for which the nature and significance of their relationship withthe primary government are such that exclusion would cause the reporting entity's financial statementsto be misleading or incomplete. The Authority has the statutory authority to levy taxes and to issuebonded debt without the approval of another government. It has the right to sue and be sued, and hasthe right to buy, sell, lease or mortgage property in its own name. Based on these criteria, the Authorityis considered a primary government and there are no other organizations or agencies whose financialstatements should be combined and presented with these financial statements other than QCIAAS asnoted above.

Significant accounting policies:

Principles of combination: The accompanying basic combined financial statements include theaccounts of the Airport and QCIAAS. All significant intercompany accounts and transactions have beeneliminated in combination.

Basis of accounting and measurement focus: The economic measurement focus and the accrual basisof accounting are used by the Authority. Under the accrual basis of accounting, revenue is recognizedwhen earned and expenses are recognized when the liability has been incurred. Under this basis ofaccounting, all assets and all liabilities associated with the operation of the Authority are included in thebalance sheet.

Accounting estimates: The preparation of financial statements in conformity with accounting principlesgenerally accepted in the United States of America requires management to make estimates andassumptions that affect the reported amount of assets and liabilities and disclosure of contingentassets and liabilities at the date of the financial statements and the reported amount of revenues andexpenses during the reporting period. Actual results could differ from those estimates.

Cash, cash equivalents and investments: For purposes of reporting cash flows, all short-terminvestments that are highly liquid are considered to be cash equivalents. Cash equivalents are readilyconvertible to a known amount of cash and, at the day of purchase, have maturity no longer than threemonths.

17

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 1. Nature of Business, Reporting Entity and Significant Accounting Policies (Continued)

Investments consist of the Illinois Funds Money Market Fund, Governmental Money Market Fund, twoRepurchase Agreements and Commercial Paper. The first two are external investment pools that arenot SEC registered. The Repurchase Agreements and the Governmental Money Market Funds aremanaged by a financial institution and, therefore, regulated by the Comptroller of the Currency forCollective Investment Funds. The Illinois Funds Money Market is regulated by the State Treasurer'sOffice. The value of the external investment pools are recorded at amortized cost pursuant to Rule 2a-7under the Investment Company Act of 1940.

Property taxes: Property taxes receivable represent the 2011 tax levy which is collectible in the 2012-2013 fiscal year and six months of the 2012 tax levy which is collectible in the 2013-2014 fiscal year.Property taxes are assessed in December and become a lien on the property as of the precedingJanuary 1 and are to be received in quarterly installments in June, August, September and Novemberof the following year. Property taxes receivable from the 2012 tax levy are unearned on June 30, 2012,since the period for which the taxes are levied is fiscal year June 30, 2013.

Debt issuance costs, discounts and deferred amount on refunding: Debt discounts and deferredamount on refunding are reported with long-term debt. Debt issue costs are recorded as an asset in thefinancial statements. Debt issues costs, discounts and deferred amount on refunding are deferred andamortized over the term of the related debt using a method which approximates the effective interestmethod. The deferred amount on refunding was expensed during the fiscal year ending June 30, 2011when the 2000C General Obligation Airport System Alternate Revenue Source Bonds were refunded.

Capital assets: Capital assets are carried at cost and defined by the Authority as assets with an initial,individual cost of $10,000 or more and an initial useful life greater than one year. Interest related toconstruction of capital assets is capitalized. Capitalized interest was $279,850 during fiscal year 2012and $476,435 during fiscal year 2011. Donated capital assets are recorded at estimated fair value atthe date of donation. Depreciation is computed by the straight-line method over estimated useful livesas follows:

Buildings and structures

Runways, lighting and roads

Machinery and equipment

Leasehold improvements

Intangibles

3-50 years

5-50 years

3-25 years

10 years

3-7 years

Compensated absences: Vacation, compensating, and personal leave is accrued as a liability as it isearned. Any compensated absences accrued for at the fiscal year end is expected to be used withinthe following year as it is the Authority's policy to not carry over unused hours beyond an employee'sanniversary date. Therefore, the entire compensated balance at June 30, 2012 of $233,946 is shownas a current liability. Sick leave benefits do not vest as the benefit is only paid in the event of death.Total nonvested sick leave benefits, for which the Authority is contingently liable as of June 30, 2012,are $568,357.

Prepaid items: Prepaid items primarily consist of advance payments to the state of Illinois for the localshare of capital projects.

18

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 1. Nature of Business, Reporting Entity and Significant Accounting Policies (Continued)

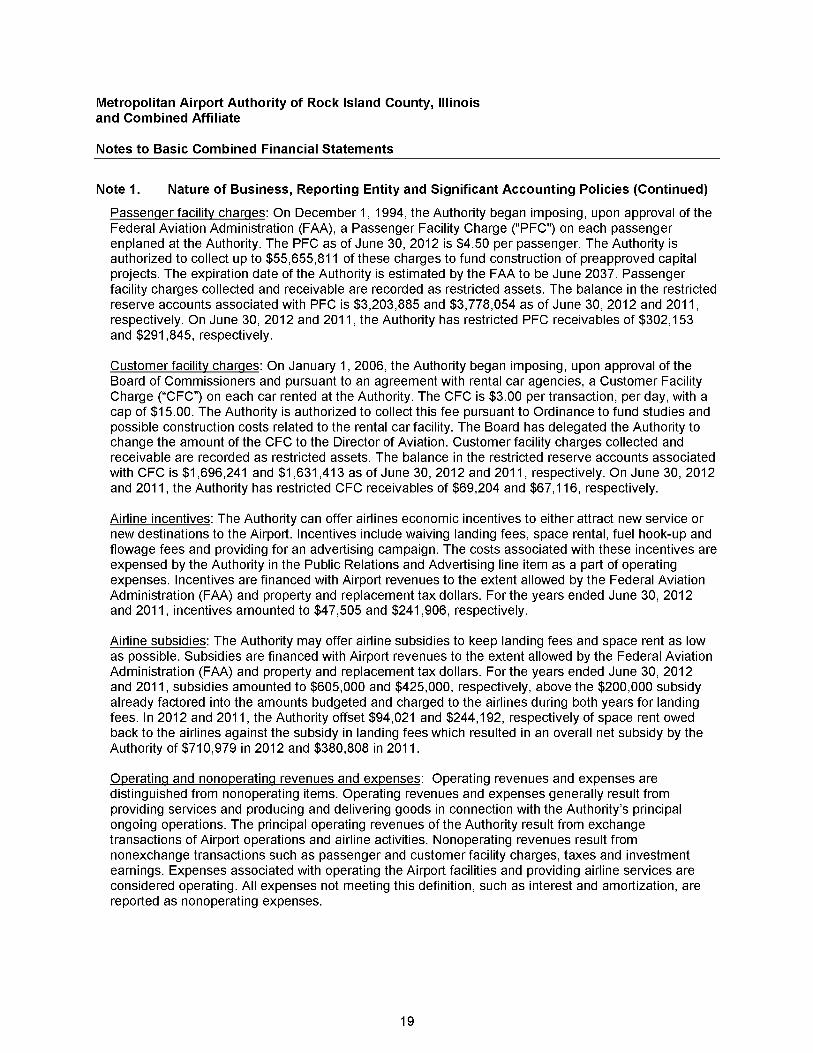

Passenger facility charges: On December 1, 1994, the Authority began imposing, upon approval of theFederal Aviation Administration (FAA), a Passenger Facility Charge ("PFC") on each passengerenplaned at the Authority. The PFC as of June 30, 2012 is $4.50 per passenger. The Authority isauthorized to collect up to $55,655,811 of these charges to fund construction of preapproved capitalprojects. The expiration date of the Authority is estimated by the FAA to be June 2037. Passengerfacility charges collected and receivable are recorded as restricted assets. The balance in the restrictedreserve accounts associated with PFC is $3,203,885 and $3,778,054 as of June 30, 2012 and 2011,respectively. On June 30, 2012 and 2011, the Authority has restricted PFC receivables of $302,153and $291,845, respectively.

Customer facility charges: On January 1, 2006, the Authority began imposing, upon approval of theBoard of Commissioners and pursuant to an agreement with rental car agencies, a Customer FacilityCharge ("CFC") on each car rented at the Authority. The CFC is $3.00 per transaction, per day, with acap of $15.00. The Authority is authorized to collect this fee pursuant to Ordinance to fund studies andpossible construction costs related to the rental car facility. The Board has delegated the Authority tochange the amount of the CFC to the Director of Aviation. Customer facility charges collected andreceivable are recorded as restricted assets. The balance in the restricted reserve accounts associatedwith CFC is $1,696,241 and $1,631,413 as of June 30, 2012 and 2011, respectively. On June 30, 2012and 2011, the Authority has restricted CFC receivables of $69,204 and $67,116, respectively.

Airline incentives: The Authority can offer airlines economic incentives to either attract new service ornew destinations to the Airport. Incentives include waiving landing fees, space rental, fuel hook-up andflowage fees and providing for an advertising campaign. The costs associated with these incentives areexpensed by the Authority in the Public Relations and Advertising line item as a part of operatingexpenses. Incentives are financed with Airport revenues to the extent allowed by the Federal AviationAdministration (FAA) and property and replacement tax dollars. For the years ended June 30, 2012and 2011, incentives amounted to $47,505 and $241,906, respectively.

Airline subsidies: The Authority may offer airline subsidies to keep landing fees and space rent as lowas possible. Subsidies are financed with Airport revenues to the extent allowed by the Federal AviationAdministration (FAA) and property and replacement tax dollars. For the years ended June 30, 2012and 2011, subsidies amounted to $605,000 and $425,000, respectively, above the $200,000 subsidyalready factored into the amounts budgeted and charged to the airlines during both years for landingfees. In 2012 and 2011, the Authority offset $94,021 and $244,192, respectively of space rent owedback to the airlines against the subsidy in landing fees which resulted in an overall net subsidy by theAuthority of $710,979 in 2012 and $380,808 in 2011.

Operating and nonoperating revenues and expenses: Operating revenues and expenses aredistinguished from nonoperating items. Operating revenues and expenses generally result fromproviding services and producing and delivering goods in connection with the Authority's principalongoing operations. The principal operating revenues of the Authority result from exchangetransactions of Airport operations and airline activities. Nonoperating revenues result fromnonexchange transactions such as passenger and customer facility charges, taxes and investmentearnings. Expenses associated with operating the Airport facilities and providing airline services areconsidered operating. All expenses not meeting this definition, such as interest and amortization, arereported as nonoperating expenses.

19

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 1. Nature of Business, Reporting Entity and Significant Accounting Policies (Continued)

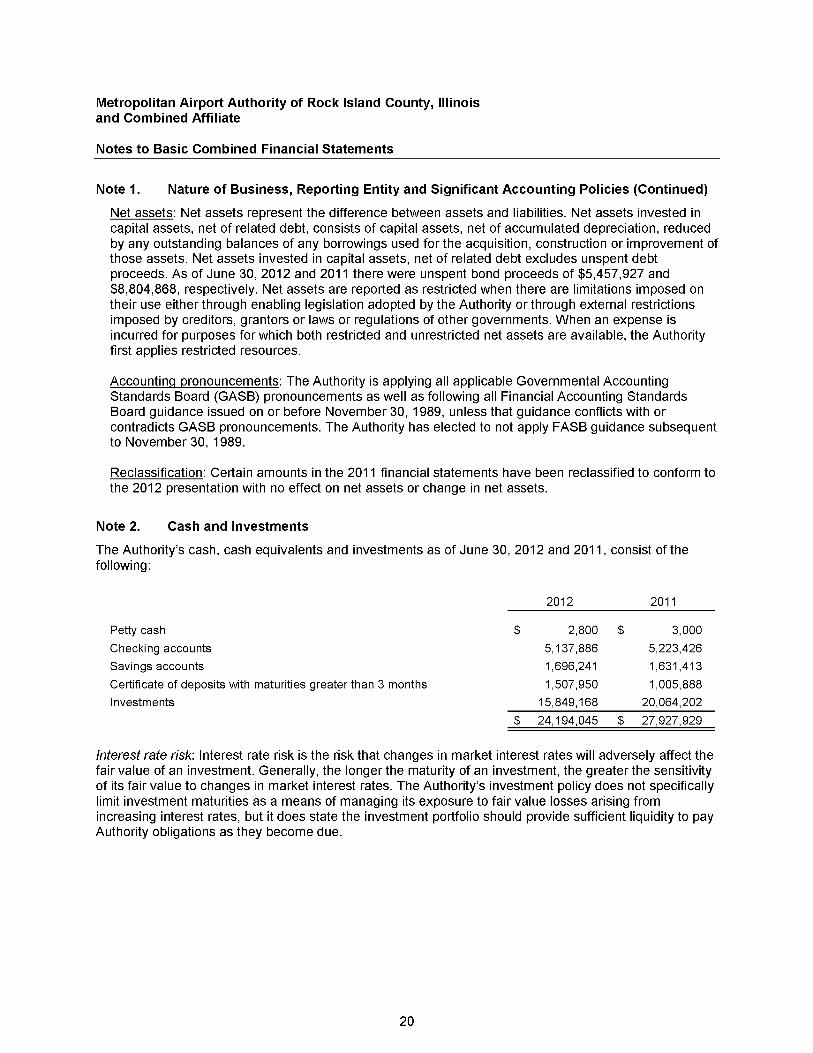

Net assets: Net assets represent the difference between assets and liabilities. Net assets invested incapital assets, net of related debt, consists of capital assets, net of accumulated depreciation, reducedby any outstanding balances of any borrowings used for the acquisition, construction or improvement ofthose assets. Net assets invested in capital assets, net of related debt excludes unspent debtproceeds. As of June 30, 2012 and 2011 there were unspent bond proceeds of $5,457,927 and$8,804,868, respectively. Net assets are reported as restricted when there are limitations imposed ontheir use either through enabling legislation adopted by the Authority or through external restrictionsimposed by creditors, grantors or laws or regulations of other governments. When an expense isincurred for purposes for which both restricted and unrestricted net assets are available, the Authorityfirst applies restricted resources.

Accounting pronouncements: The Authority is applying all applicable Governmental AccountingStandards Board (GAS B) pronouncements as well as following all Financial Accounting StandardsBoard guidance issued on or before November 30, 1989, unless that guidance conflicts with orcontradicts GASB pronouncements. The Authority has elected to not apply FASB guidance subsequentto November 30, 1989.

Reclassification: Certain amounts in the 2011 financial statements have been reclassified to conform tothe 2012 presentation with no effect on net assets or change in net assets.

Note 2. Cash and Investments

The Authority's cash, cash equivalents and investments as of June 30, 2012 and 2011, consist of thefollowing:

2012 2011

Petty cash $ 2,800 $ 3,000

Checking accounts 5,137,886 5,223,426

Savings accounts 1,696,241 1,631,413

Certificate of deposits with maturities greater than 3 months 1,507,950 1,005,888

Investments 15,849,168 20,064,202

$ 24,194,045 $ 27,927,929

Interest rate risk: Interest rate risk is the risk that changes in market interest rates will adversely affect thefair value of an investment. Generally, the longer the maturity of an investment, the greater the sensitivityof its fair value to changes in market interest rates. The Authority's investment policy does not specificallylimit investment maturities as a means of managing its exposure to fair value losses arising fromincreasing interest rates, but it does state the investment portfolio should provide sufficient liquidity to payAuthority obligations as they become due.

20

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 2. Cash and Investments (Continued)

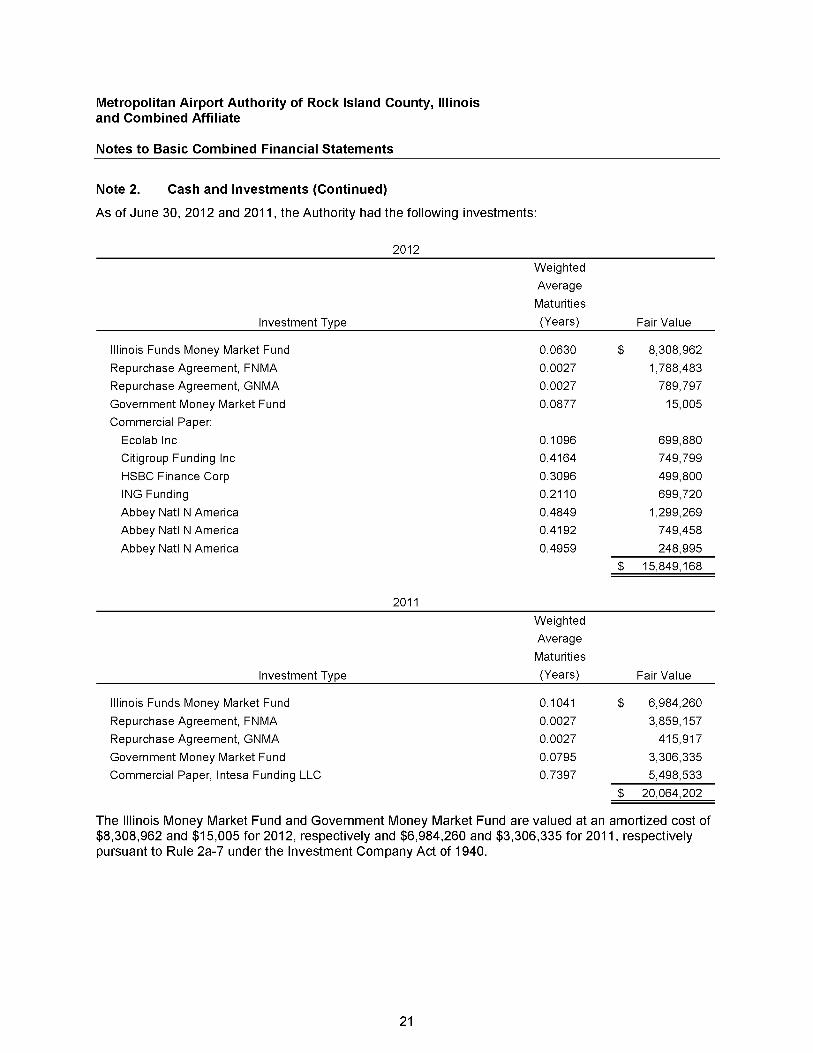

As of June 30, 2012 and 2011, the Authority had the following investments:

Investment Type

2012

Weighted

Average

Maturities

(Years) Fair Value

0.0630 $ 8,308,962

0.0027 1,788,483

0.0027 789,797

0.0877 15,005

0.1096 699,8800.4164 749,799

0.3096 499,800

0.2110 699,7200.4849 1,299,2690.4192 749,4580.4959 248,995

$ 15,849,168

2011

Weighted

Average

Maturities

(Years) Fair Value

0.1041 $ 6,984,260

0.0027 3,859,157

0.0027 415,917

0.0795 3,306,335

0.7397 5,498,533

$ 20,064,202

Illinois Funds Money Market Fund

Repurchase Agreement, FNMA

Repurchase Agreement, GNMA

Government Money Market Fund

Commercial Paper:

Ecolab Inc

Citigroup Funding Inc

HSBC Finance Corp

ING Funding

Abbey Natl N America

Abbey Natl N America

Abbey Natl N America

Investment Type

Illinois Funds Money Market Fund

Repurchase Agreement, FNMA

Repurchase Agreement, GNMA

Government Money Market Fund

Commercial Paper, Intesa Funding LLC

The Illinois Money Market Fund and Government Money Market Fund are valued at an amortized cost of$8,308,962 and $15,005 for 2012, respectively and $6,984,260 and $3,306,335 for 2011, respectivelypursuant to Rule 2a-7 under the Investment Company Act of 1940.

21

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 2. Cash and Investments (Continued)

Credit risk: Credit risk is the risk that an issuer of an investment will not fulfill its obligation to the holder ofthe investment. This is measured by the assignment of a rating by a nationally recognized statisticalrating organization. Statutes authorize the Authority to make deposits in federally insured banks, savingsand loan associations or other financial institutions, and to invest available funds in the following types ofdepository accounts or investments:

• Securities of the U.S. Government or its Agencies• Certificates of Deposit• Passbook Savings Accounts• Commercial Paper• Illinois State Funds• Treasury Management Investment Fund• Repurchase Agreements• Obligations of the Federal National Mortgage Association• Bankers Acceptance

The Authority's general investment policy is to apply the prudent-person rule: Investments shall be madeutilizing the judgment and care, under the circumstances then present, which persons of prudence,discretion and intelligence exercise in the management of their own affairs, not for speculation, but forinvestments, considering probable safety of their capital as well as the probable income to be derived.The Authority's investment policy does not further limit its investment choices in relation to credit risk.

As of June 30, 2012 and 2011, the Authority's investments were rated as follows:

2012

Investment Type

Moody's

Investor Services

Standard &Poor's

Illinois Funds Money Market Fund

Repurchase agreement, FNMA

Government Money Market Fund

Commercial Paper:

Ecolab Inc

Citigroup Funding Inc

HSBC Finance Corp

ING Funding

Abbey Natl N America

Not rated

AaaAaa-mf

P-2P-2P-2P-1P-1

2011

AAAm

AA+

AAAm

A-2

A-2A-1A-1A-1

Investment Type

Moody's

Investor Services

Standard &

Poor's

Illinois Funds Money Market Fund

Repurchase agreement, FNMA

Government Money Market Fund

Commercial Paper, Intesa Funding LLC

Not rated

Aaa

Aaa-mf

P-1

22

AAAm

AAAm

AAAmA-1

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 2. Cash and Investments (Continued)

Concentration of credit risk: The Authority's investment policy limits the deposit of funds with the State ofIllinois Public Treasurer's Investment Pool to 60 percent. Furthermore, with the exception of U.S.Treasury securities and local governmental investment pools, no more than 50 percent of the totalinvestment portfolio shall be invested with a single financial institution. The Authority's investments incommercial paper with Abbey Natl N America did represent more than 5 percent of the total investmentsat 14.5 percent as of June 30, 2012. Commercial paper with Intesa funding LLC did represent more than5 percent of total investments at 27 percent as of June 30, 2011. Money market mutual funds, repurchaseagreements, external investment pools, and other pooled investments are excluded from thisconsideration since the Authority doesn't "hold" the underlying investments.

Custodial credit risk: Custodial credit risk is the risk that in the event of a bank failure, the government'sdeposits may not be returned to it. It is the Authority's policy to require that time deposits in excess ofFDIC insurable limits be secured by collateral or private insurance to protect public deposits in a singlefinancial institution if it were to default.

As of June 30, 2012 and 2011, none of the Authority's deposits with financial institutions were exposed tocustodial credit risk due to deposits not being covered by federal depository insurance or secured bysome form of collateral authorized by the Authority's investment policy.

The custodial credit risk for investments is the risk that, in the event of the failure of the counterparty (e.g.broker-dealer) to a transaction, a government will not be able to recover the value of its investment ofcollateral securities that are in the possession of another party. The Authority had no investments thatwere exposed to custodial credit risk.

Note 3. Capital Assets

Capital asset activity for the year ended June 30, 2012, is as follows:

June 30, 2011 Additions Retirements June 30, 2012Nondepreciable assets:

Land and land reclamation $ 14,263,684 $ $ $ 14,263,684Construction-i n-prog ress 8,545,016 13,164,722 20,216,255 1,493,483

Total nondepreciable assets 22,808,700 13,164,722 20,216,255 15,757,167

Depreciable assets:Buildings and structures 39,920,679 5,641,061 45,561,740Runways, lighting and roads 117,849,849 14,588,771 2,519,108 129,919,512Machinery and equipment 10,428,405 41,317 27,597 10,442,125Leasehold improvements 369,939 369,939Intangibles 249,815 26,210 13,300 262,725

Total depreciable assets 168,818,687 20,297,359 2,560,005 186,556,041

Less accumulated depreciation for:Buildings and structures 20,613,763 1,299,942 21,913,705Runways, lighting and roads 66,893,721 5,444,667 2,186,090 70,152,298Machinery and equipment 5,916,563 833,354 27,597 6,722,320Leasehold improvements 268,135 37,075 305,210Intangibles 152,008 49,131 13,300 187,839

Total accumulated depreciation 93,844,190 7,664,169 2,226,987 99,281,372

Total depreciable assets, net 74,974,497 12,633,190 333,018 87,274,669

Capital assets, net $ 97.783.197 $ 25.797.912 $ 20.549.273 $ 103.031.836

23

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 3. Capital Assets (Continued)

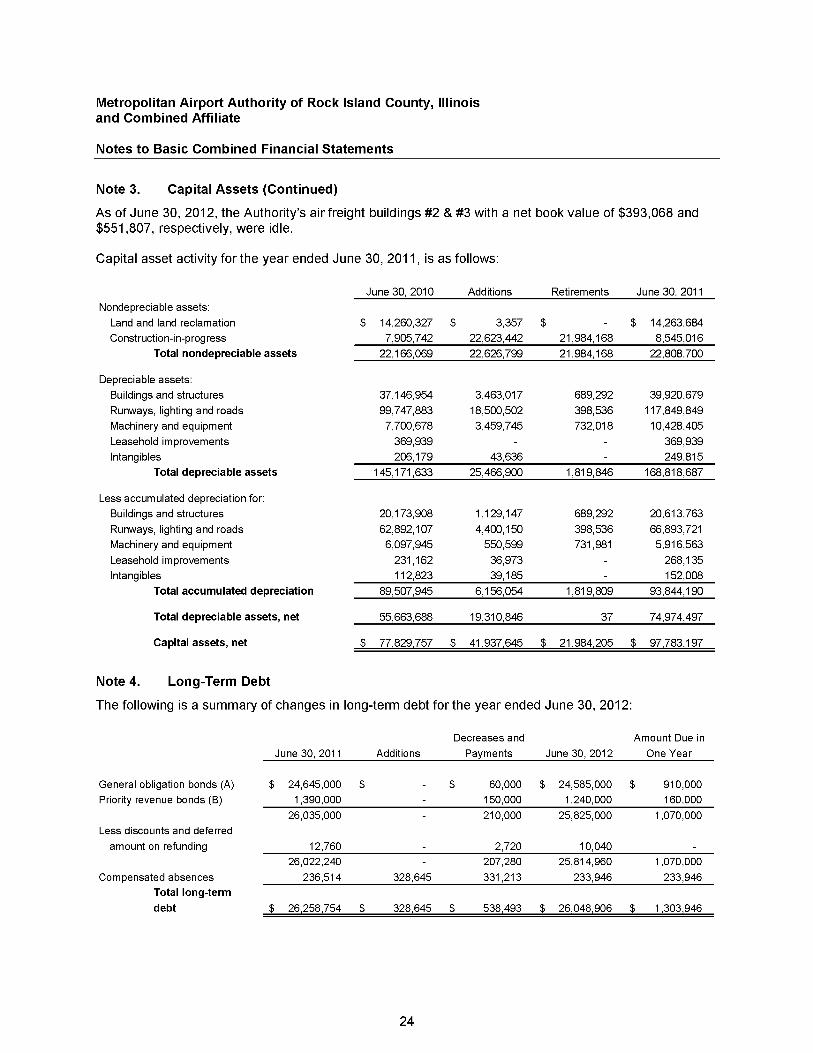

As of June 30, 2012, the Authority's air freight buildings #2 & #3 with a net book value of $393,068 and$551,807, respectively, were idle.

Capital asset activity for the year ended June 30, 2011, is as follows:

June 30,2010 Additions Retirements June 30, 2011Nondepreciable assets:

Land and land reclamation $ 14,260,327 $ 3,357 $ $ 14,263,684Construction-i n-prog ress 7,905,742 22,623,442 21,984,168 8,545,016

Total nondepreciable assets 22,166,069 22,626,799 21,984,168 22,808,700

Depreciable assets:Buildings and structures 37,146,954 3,463,017 689,292 39,920,679

Runways, lighting and roads 99,747,883 18,500,502 398,536 117,849,849Machinery and equipment 7,700,678 3,459,745 732,018 10,428,405

Leasehold improvements 369,939 369,939Intangibles 206,179 43,636 249,815

Total depreciable assets 145,171,633 25,466,900 1,819,846 168,818,687

Less accumulated depreciation for:Buildings and structures 20,173,908 1,129,147 689,292 20,613,763

Runways, lighting and roads 62,892,107 4,400,150 398,536 66,893,721Machinery and equipment 6,097,945 550,599 731,981 5,916,563

Leasehold improvements 231,162 36,973 268,135Intangibles 112,823 39,185 152,008

Total accumulated depreciation 89,507,945 6,156,054 1,819,809 93,844,190

Total depreciable assets, net 55,663,688 19,310,846 37 74,974,497

Capital assets, net $ 77.829.757 $ 41.937.645 $ 21.984.205 $ 97.783.197

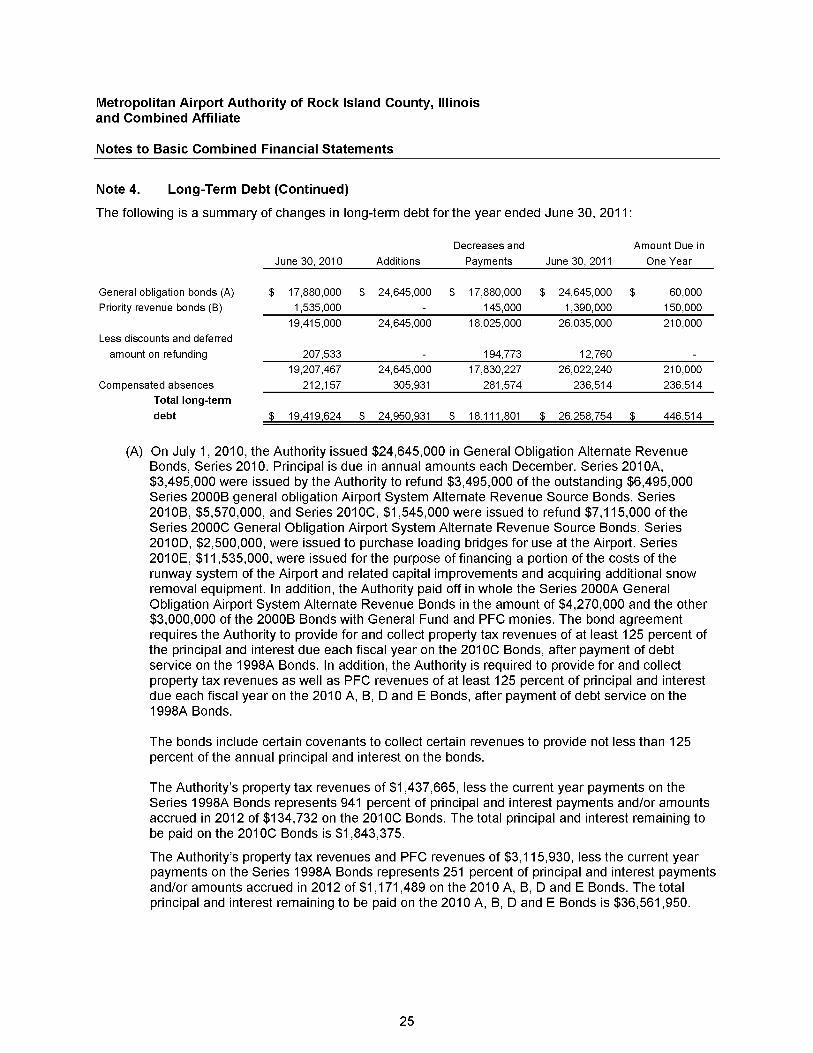

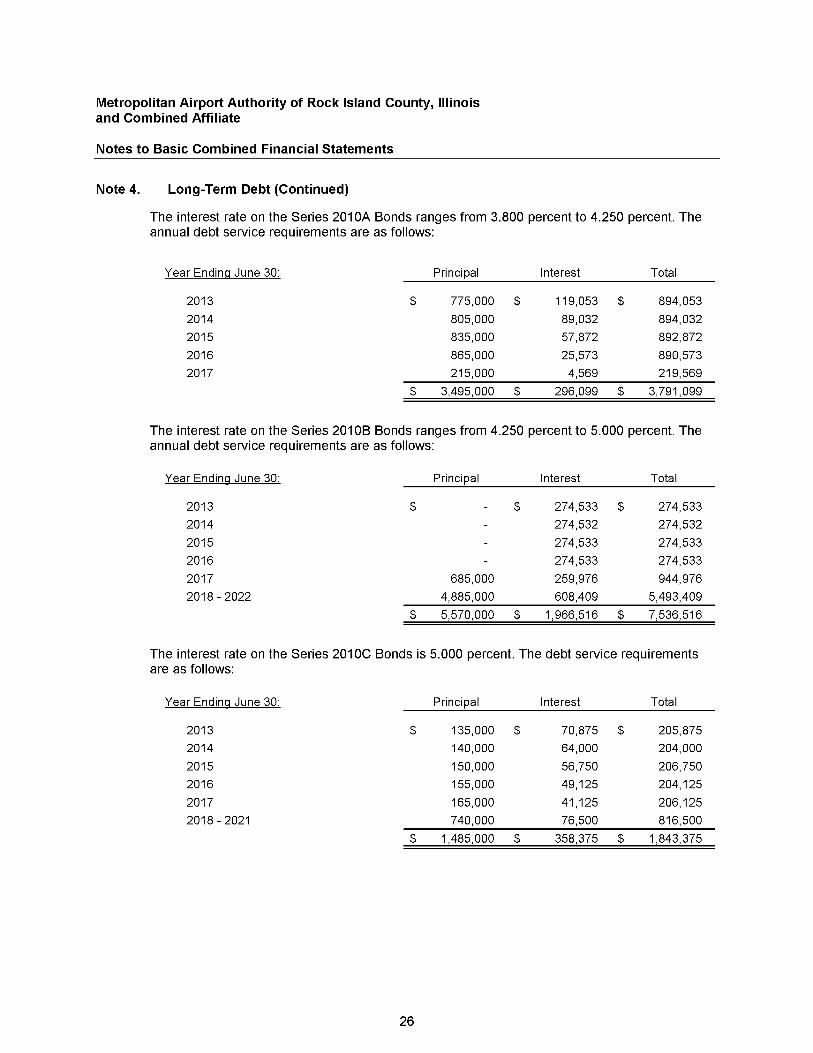

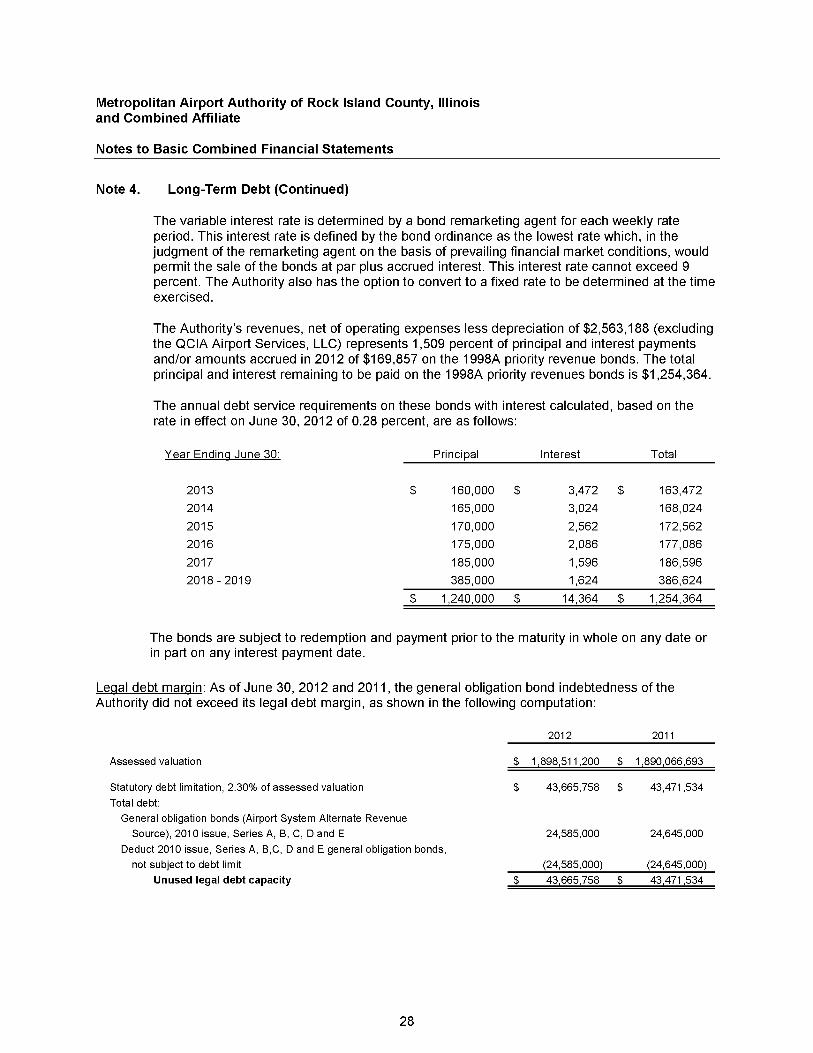

Note 4. Long-Term Debt

The following is a summary of changes in long-term debt for the year ended June 30, 2012:

Decreases and Amount Due in

June 30, 2011 Additions Payments June 30, 2012 One Year

General obligation bonds (A) $ 24,645,000 $ $ 60,000 $ 24,585,000 $ 910,000Priority revenue bonds (B) 1,390,000 150,000 1,240,000 160,000

26,035,000 210,000 25,825,000 1,070,000Less discounts and deferred

amount on refunding 12,760 2,720 10,04026,022,240 207,280 25,814,960 1,070,000

Compensated absences 236,514 328,645 331,213 233,946 233,946Total long-term

debt $ 26,258,754 $ 328,645 $ 538,493 $ 26,048,906 $ 1,303,946

24

Metropolitan Airport Authority of Rock Island County, Illinoisand Combined Affiliate

Notes to Basic Combined Financial Statements

Note 4. Long-Term Debt (Continued)

The following is a summary of changes in long-term debt for the year ended June 30, 2011 :

Decreases and Amount Due in

June 30, 2010 Additions Payments June 30, 2011 One Year