Metro Pacific Investments Corporation and …...Metro Pacific Investments Corporation and...

185

Metro Pacific Investments Corporation and Subsidiaries Consolidated Financial Statements December 31, 2017 and 2016 and Years Ended December 31, 2017, 2016 and 2015 and Independent Auditor’s Report

Transcript of Metro Pacific Investments Corporation and …...Metro Pacific Investments Corporation and...

Metro Pacific InvestmentsCorporation and Subsidiaries

Consolidated Financial StatementsDecember 31, 2017 and 2016and Years Ended December 31, 2017, 2016and 2015

and

Independent Auditor’s Report

*SGVFS026907*

INDEPENDENT AUDITOR’S REPORT

The Board of Directors and StockholdersMetro Pacific Investments Corporation

Opinion

We have audited the consolidated financial statements of Metro Pacific Investments Corporation and itssubsidiaries (the Company), which comprise the consolidated statements of financial position as atDecember 31, 2017 and 2016, and the consolidated statements of comprehensive income, consolidatedstatements of changes in equity and consolidated statements of cash flows for each of the three years inthe period ended December 31, 2017, and notes to the consolidated financial statements, including asummary of significant accounting policies.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects,the consolidated financial position of the Company as at December 31, 2017 and 2016, and itsconsolidated financial performance and its consolidated cash flows for each of the three years in theperiod ended December 31, 2017 in accordance with Philippine Financial Reporting Standards (PFRSs).

Basis for Opinion

We conducted our audits in accordance with Philippine Standards on Auditing (PSAs). Ourresponsibilities under those standards are further described in the Auditor’s Responsibilities for the Auditof the Consolidated Financial Statements section of our report. We are independent of the Company inaccordance with the Code of Ethics for Professional Accountants in the Philippines (Code of Ethics)together with the ethical requirements that are relevant to our audit of the consolidated financialstatements in the Philippines, and we have fulfilled our other ethical responsibilities in accordance withthese requirements and the Code of Ethics. We believe that the audit evidence we have obtained issufficient and appropriate to provide a basis for our opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in ouraudit of the consolidated financial statements of the current period. These matters were addressed in thecontext of our audit of the consolidated financial statements as a whole, and in forming our opinionthereon, and we do not provide a separate opinion on these matters. For each matter below, ourdescription of how our audit addressed the matter is provided in that context.

SyCip Gorres Velayo & Co.6760 Ayala Avenue1226 Makati CityPhilippines

Tel: (632) 891 0307Fax: (632) 819 0872ey.com/ph

BOA/PRC Reg. No. 0001, December 14, 2015, valid until December 31, 2018SEC Accreditation No. 0012-FR-4 (Group A), November 10, 2015, valid until November 9, 2018

A member firm of Ernst & Young Global Limited

*SGVFS026907*

- 2 -

We have fulfilled the responsibilities described in the Auditor’s Responsibilities for the Audit of theConsolidated Financial Statements section of our report, including in relation to these matters.Accordingly, our audit included the performance of procedures designed to respond to our assessment ofthe risks of material misstatement of the consolidated financial statements. The results of our auditprocedures, including the procedures performed to address the matters below, provide the basis for ouraudit opinion on the accompanying consolidated financial statements.

Recoverability of goodwill and service concession assets (SCAs) not yet available for use

The Company’s goodwill, mainly arising from its acquisition of long term investments in water andtollways business, amounted to P=25.4 billion and this is allocated to different cash generating units(CGUs). In addition, the Company has entered into several service concession agreements with thePhilippine Government and/or its agencies or instrumentalities, of which P=39.3 billion of these SCAs arenot yet available for use. Under Philippine Accounting Standard (PAS) 36, Impairment of Assets, theCompany is required to perform annual impairment test on the amount of goodwill and the SCAs not yetavailable for use. These annual impairment tests are significant to our audit because the amounts arematerial to the consolidated financial statements. In addition, the determination of the recoverableamounts of the CGUs to which the goodwill belong or as it relates to the SCAs , involves significantassumptions about the future results of business such as revenue growth and discount rates which areapplied to the cash flow forecasts. The assumptions on revenue growth mainly relates to the expectedvolume of traffic for the toll roads, ridership for the rail, and billed water volume for the waterconcession.

Refer to Note 14 to the consolidated financial statements for the details on goodwill and SCAs and theassumptions used in the forecasts.

Audit response

We obtained an understanding of the Company’s impairment assessment process and the related controls.We also involved our internal specialist in evaluating the methodologies and the assumptions used. Theseassumptions include the expected volume of traffic for the toll roads, ridership for the rail, billed watervolume for the water concession, growth rate and discount rates. We compared the forecast revenuegrowth against the historical data of the CGUs and inquired from management and operations personnelabout the plans to support the forecast revenues. We also compared the Company’s key assumptions suchas traffic volume, rail ridership and water volume against historical data and against available studies byindependent parties that were commissioned by the respective subsidiaries. We reviewed the weightedaverage cost of capital (WACC) used in the impairment test by comparing it with WACC of othercomparable companies in the regions. Furthermore, we reviewed the Company’s disclosures about thoseassumptions to which the outcome of the impairment test is most sensitive, specifically those that havethe most significant effect on determining the recoverable amounts of the goodwill and SCAs not yetavailable for use.

A member firm of Ernst & Young Global Limited

*SGVFS026907*

- 3 -

Amortization of SCAs using the ‘units of production (UOP)’ method

The SCAs related to the toll roads and water concession agreements of the Company are being amortizedusing the UOP method. For the toll roads concession assets, amortization is based on the ratio of theactual traffic volume to the total expected traffic volume of the underlying toll expressways over theremaining period of the concession agreement. On the other hand, the Company amortizes the water-related concession asset based on the actual billed volume over the estimated billable water volume forremaining period of the concession agreement. The UOP amortization method is a key audit matter as themethod involves significant management judgment and estimates, particularly in determining the totalexpected traffic volume and the total estimated volume of billable water over the remaining periods of theconcession agreements. The Company reviews annually the total expected traffic volume with referenceto traffic projection reports and billable water volume with reference to water volume forecasts. Itconsiders different factors such as population growth, supply and consumption, and service coverageincluding ongoing and future expansions.

Refer to Note 12 to the consolidated financial statements for the details of SCAs and Note 3 for thediscussion of management estimate relating to amortization of SCAs.

Audit response

We obtained an understanding of management’s processes and controls in the estimation of billable waterand traffic volume. We reviewed the report of the management’s specialists and gained an understandingof the methodology and the basis of computing the forecasted volumes. We also evaluated thecompetence, capabilities, and objectivity of management’s specialists who estimated the forecastedvolumes. Furthermore, we compared the billable water volume and traffic volume during the year againstthe data generated from the billing system for water and from the toll collection system for tollways. Werecalculated the amortization expense for the year and the SCAs as of year-end based on the establishedbillable water volume and traffic volume.

Accounting for acquisitions of an associate and a subsidary

In 2017, the Company acquired additional 25% interest in Beacon Electric Assets Holdings, Inc. (BeaconElectric) for an aggregate purchase price of P=21.8 billion. As a result of the acquisition, the Companynow holds 100% of the common and preferred shares of Beacon Electric. Consequently, the Company’seffective ownership interest in Manila Electric Company (Meralco) increased to 45.5% and in GlobalBusiness Power Corporation (GBPC) to 62.4%. In addition, through its wholly-owned subsidiary PTMetro Pacific Tollways Indonesia, the Company acquired 49.5% interest in PT Nusantara InfrastructureTbk (PT Nusantara), a listed Indonesian company primarily engaged in the infrastructure developmentindustry, for P=6.9 billion. The Company accounted for these acquisitions as ‘business’ acquisitions. Thegoodwill arising from these acquisitions are subsumed under the investment accounts. These transactionsare significant to our audit as these are new and major acquisitions during the year and the amounts arematerial to the consolidated financial statements. In addition, accounting for these acquisitions requiredsignificant management judgment and estimates. These include allocating the purchase consideration tothe assets acquired and liabilities assumed based on fair values and the Company’s share in the net fairvalue of the investee’s identifiable assets and liabilities.

Refer to Notes 4 and 10 to the consolidated financial statements for details of the acquisitions and Note 3for the discussion of management estimate relating to the acquisitions.

A member firm of Ernst & Young Global Limited

*SGVFS026907*

- 4 -

Audit response

We evaluated management’s judgment on whether these acquisitions qualify as businesses, and how theseshould be accounted for, by reference to the purchase agreements and documents related to theseacquisitions. In applying the acquisition method, we reviewed the identification of the underlying assetsand liabilities of the investees based on our understanding of the businesses. Where the Company used itsspecialists to perform the purchase price allocation and involved them in the valuation of the intangibleassets, or engaged independent appraisers to value the property and equipment, we assessed thecompetence, capabilities, and objectivity of such Company specialists and the independent appraisers.We also involved our internal specialists in reviewing the valuation methodology and key inputs, such asrevenue growth, margins and discount rates related to the valuation of the intangible assets. We comparedthe revenue growth and margins to the historical performance of the investees. We tested the parametersused in the determination of the discount rate against market data. We also reviewed the disclosures inthe notes to the consolidated financial statements.

Provisions and contingencies

The Company is involved in certain proceedings for which the Company has recognized provisions forprobable costs and/or expenses, which may be incurred, and/or has disclosed relevant information aboutsuch contingencies. This matter is significant to the audit because the assessment of potential outcome orliability involves significant management judgment and estimation. Notes 16 and 29 to the consolidatedfinancial statements provide the relevant disclosures related to this matter.

Audit response

Our audit procedures included understanding the Company's processes and controls over theidentification and evaluation of regulatory proceedings. We involved our internal specialist in evaluatingmanagement’s assessment on whether provisions on the contingencies should be recognized, and theestimation of such amount. We also discussed with management the status of the regulatory proceedingsand dispute arbitration. In addition, we obtained correspondences with the relevant government agencies,including tax authorities, replies from third party legal counsels, and any relevant historical and recentjudgments issued by the courts/tax authorities on similar matters.

West Service Area water and sewerage service revenue recognition

About 34% of the Company’s consolidated revenues comprises water and sewerage service revenuesfrom the Metropolitan Waterworks and Sewerage System (MWSS) West Service Area. The recognitionof water and sewerage service revenues involves processing large volumes of data from multiplelocations. Different rates apply to different customers that are classified as residential, semi-business,commercial or industrial. The billing rates for each class of customers depend on the customer type andare determined using the formula provided in the service concession agreement and regulated by theMWSS Regulatory Office. This matter is significant to our audit because water and sewerage servicerevenues depend on the completeness of data captured during monthly meter readings, which occur ondifferent billing cut-off dates for different customers; the propriety of the application of rates to billableconsumption; and the reliability of the systems involved in processing bills and recording revenues.

A member firm of Ernst & Young Global LimitedA member firm of Ernst & Young Global Limited

*SGVFS026907*

- 5 -

Audit response

We obtained an understanding of the water and sewerage service revenue process, which includesmaintaining the customer database, capturing billable water consumption, uploading captured billablewater consumption to the billing system, calculating billable amounts based on MWSS approved rates,and uploading data from the billing system to the financial reporting system. We also evaluated thedesign of and tested the relevant controls over this process. In addition, we performed test recalculation ofthe billed amounts using the MWSS approved rates and formulae, and compared them with the amountsreflected in the billing statements. Moreover, we involved our internal specialist in performing theaforementioned procedures on the automated aspects of this process.

Investment in a significant associate

The Company has an investment in Meralco that is accounted for under the equity method. For the yearended December 31, 2017, the Company’s effective share in the net income of Meralco amounted toP=5.4 billion and accounts for 28% of the Company’s consolidated net income. The Company’s share inMeralco’s net income is significantly affected by Meralco’s revenue from the sale of electricity whicharise from its service contracts with a large number of customers who are classified as either commercial,industrial or residential customers. Note 29 provides relevant disclosures related to the rate-makingregulations and regulatory policies of the Energy Regulatory Commission (ERC). The revenue recognizeddepends on (a) the complete capture of electric consumption based on the meter readings over thefranchise area taken on various dates; (b) the propriety of rates computed and applied across customerclasses; and (c) the reliability of the information technology (IT) systems involved in processing thebilling transaction.

In addition, the Company’s share in Meralco’s net income is also significantly affected by Meralco’srecognition of provisions for probable costs and/or expenses. The assessment of the potential outcome orliability involves significant management judgment and estimation. Note 29 to the consolidated financialstatements provides the relevant disclosures related to this matter.

Audit response

We obtained the consolidated financial information of Meralco for the year ended December 31, 2017and performed recomputation of the Company’s equity in net earnings of Meralco. We obtained anunderstanding of and evaluated the design and tested the controls over the customer master filemaintenance, accumulation and processing of meter data, and interface of data from the billing system tothe financial reporting system. In addition, we performed test recalculation of the billed amounts usingthe ERC approved rates and formulae, actual costs incurred, and compared them with the amountsreflected in the billing statements. We involved our internal specialist in understanding the IT processesand in understanding and testing of the IT general controls over the IT systems supporting the revenueprocess.

A member firm of Ernst & Young Global Limited

*SGVFS026907*

- 6 -

We evaluated management’s assessment of the possible outcomes and the related estimates of theprobable costs and/or expenses that are recognized. In addition, we evaluated the input data supportingthe assumptions used, such as tariffs, tax rates, historical experience, regulatory rulings and otherdevelopments, against Meralco’s internal and external data, and performed recalculations and inspectionof relevant supporting documents.

Other Information

Management is responsible for the other information. The other information comprises the informationincluded in the SEC Form 20-IS (Definitive Information Statement), SEC Form 17-A and Annual Reportfor the year ended December 31, 2017, but does not include the consolidated financial statements and ourauditor’s report thereon. The SEC Form 20-IS (Definitive Information Statement), SEC Form 17-A andAnnual Report for the year ended December 31, 2017 are expected to be made available to us after thedate of this auditor’s report.

Our opinion on the consolidated financial statements does not cover the other information and we will notexpress any form of assurance conclusion thereon.

In connection with our audits of the consolidated financial statements, our responsibility is to read theother information identified above when it becomes available and, in doing so, consider whether the otherinformation is materially inconsistent with the consolidated financial statements or our knowledgeobtained in the audits, or otherwise appears to be materially misstated.

Responsibilities of Management and Those Charged with Governance for the ConsolidatedFinancial Statements

Management is responsible for the preparation and fair presentation of the consolidated financialstatements in accordance with PFRSs, and for such internal control as management determines isnecessary to enable the preparation of consolidated financial statements that are free from materialmisstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing theCompany’s ability to continue as a going concern, disclosing, as applicable, matters related to goingconcern and using the going concern basis of accounting unless management either intends to liquidatethe Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as awhole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s reportthat includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that anaudit conducted in accordance with PSAs will always detect a material misstatement when it exists.Misstatements can arise from fraud or error and are considered material if, individually or in theaggregate, they could reasonably be expected to influence the economic decisions of users taken on thebasis of these consolidated financial statements.

A member firm of Ernst & Young Global Limited

*SGVFS026907*

- 7 -

As part of an audit in accordance with PSAs, we exercise professional judgment and maintainprofessional skepticism throughout the audit. We also:

∂ Identify and assess the risks of material misstatement of the consolidated financial statements,whether due to fraud or error, design and perform audit procedures responsive to those risks, andobtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk ofnot detecting a material misstatement resulting from fraud is higher than for one resulting from error,as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override ofinternal control.

∂ Obtain an understanding of internal control relevant to the audit in order to design audit proceduresthat are appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectiveness of the Company’s internal control.

∂ Evaluate the appropriateness of accounting policies used and the reasonableness of accountingestimates and related disclosures made by management.

∂ Conclude on the appropriateness of management’s use of the going concern basis of accounting and,based on the audit evidence obtained, whether a material uncertainty exists related to events orconditions that may cast significant doubt on the Company’s ability to continue as a going concern.If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’sreport to the related disclosures in the consolidated financial statements or, if such disclosures areinadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up tothe date of our auditor’s report. However, future events or conditions may cause the Company tocease to continue as a going concern.

∂ Evaluate the overall presentation, structure and content of the consolidated financial statements,including the disclosures, and whether the consolidated financial statements represent the underlyingtransactions and events in a manner that achieves fair presentation.

∂ Obtain sufficient appropriate audit evidence regarding the financial information of the entities orbusiness activities within the Company to express an opinion on the consolidated financialstatements. We are responsible for the direction, supervision and performance of the audit. Weremain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scopeand timing of the audit and significant audit findings, including any significant deficiencies in internalcontrol that we identify during our audit.

A member firm of Ernst & Young Global Limited

*SGVFS026907*

- 8 -

We also provide those charged with governance with a statement that we have complied with relevantethical requirements regarding independence, and to communicate with them all relationships and othermatters that may reasonably be thought to bear on our independence, and where applicable, relatedsafeguards.

From the matters communicated with those charged with governance, we determine those matters thatwere of most significance in the audit of the consolidated financial statements of the current period andare therefore the key audit matters. We describe these matters in our auditor’s report unless law orregulation precludes public disclosure about the matter or when, in extremely rare circumstances, wedetermine that a matter should not be communicated in our report because the adverse consequences ofdoing so would reasonably be expected to outweigh the public interest benefits of such communication.

The engagement partner on the audit resulting in this independent auditor’s report is Marydith C. Miguel.

SYCIP GORRES VELAYO & CO.

Marydith C. MiguelPartnerCPA Certificate No. 65556SEC Accreditation No. 0087-AR-4 (Group A), May 1, 2016, valid until May 1, 2019Tax Identification No. 102-092-270BIR Accreditation No. 08-001998-55-2018, February 26, 2018, valid until February 25, 2021PTR No. 6621301, January 9, 2018, Makati City

March 1, 2018

A member firm of Ernst & Young Global Limited

*SGVFS026907*

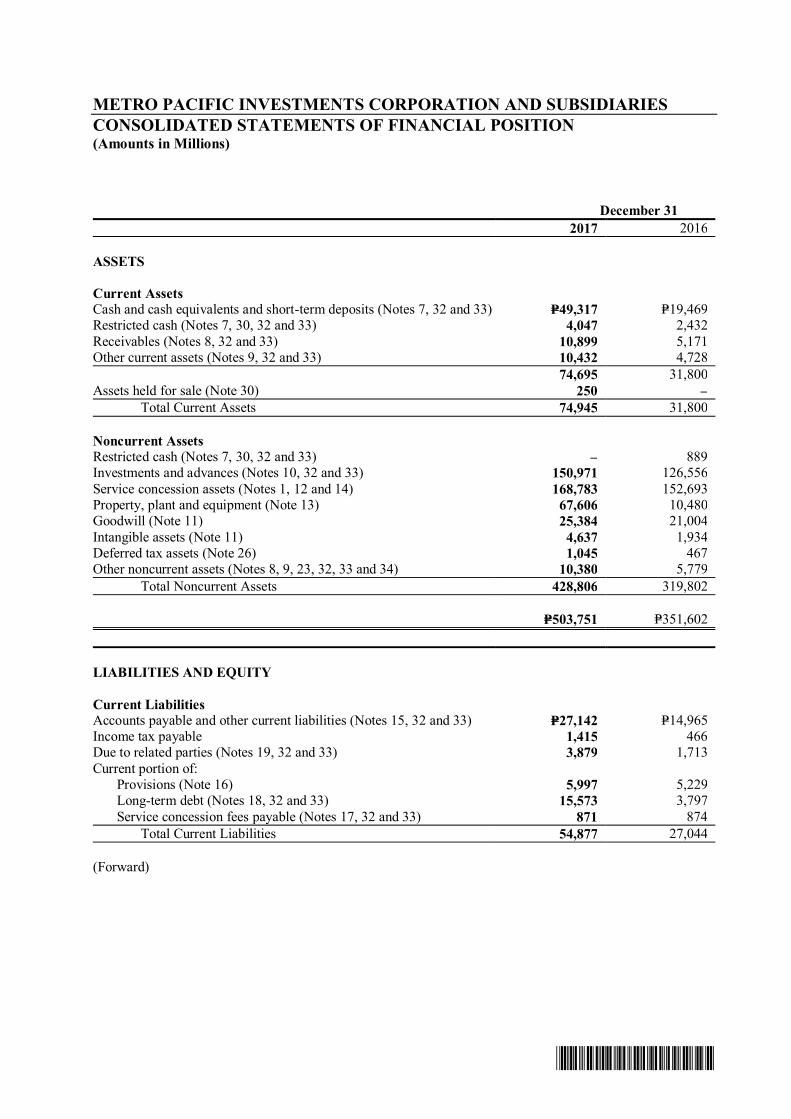

METRO PACIFIC INVESTMENTS CORPORATION AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF FINANCIAL POSITION(Amounts in Millions)

December 312017 2016

ASSETS

Current AssetsCash and cash equivalents and short-term deposits (Notes 7, 32 and 33) P=49,317 P=19,469Restricted cash (Notes 7, 30, 32 and 33) 4,047 2,432Receivables (Notes 8, 32 and 33) 10,899 5,171Other current assets (Notes 9, 32 and 33) 10,432 4,728

74,695 31,800Assets held for sale (Note 30) 250 –

Total Current Assets 74,945 31,800

Noncurrent AssetsRestricted cash (Notes 7, 30, 32 and 33) – 889Investments and advances (Notes 10, 32 and 33) 150,971 126,556Service concession assets (Notes 1, 12 and 14) 168,783 152,693Property, plant and equipment (Note 13) 67,606 10,480Goodwill (Note 11) 25,384 21,004Intangible assets (Note 11) 4,637 1,934Deferred tax assets (Note 26) 1,045 467Other noncurrent assets (Notes 8, 9, 23, 32, 33 and 34) 10,380 5,779

Total Noncurrent Assets 428,806 319,802

P=503,751 P=351,602

LIABILITIES AND EQUITY

Current LiabilitiesAccounts payable and other current liabilities (Notes 15, 32 and 33) P=27,142 P=14,965Income tax payable 1,415 466Due to related parties (Notes 19, 32 and 33) 3,879 1,713Current portion of:

Provisions (Note 16) 5,997 5,229Long-term debt (Notes 18, 32 and 33) 15,573 3,797Service concession fees payable (Notes 17, 32 and 33) 871 874

Total Current Liabilities 54,877 27,044

(Forward)

*SGVFS026907*

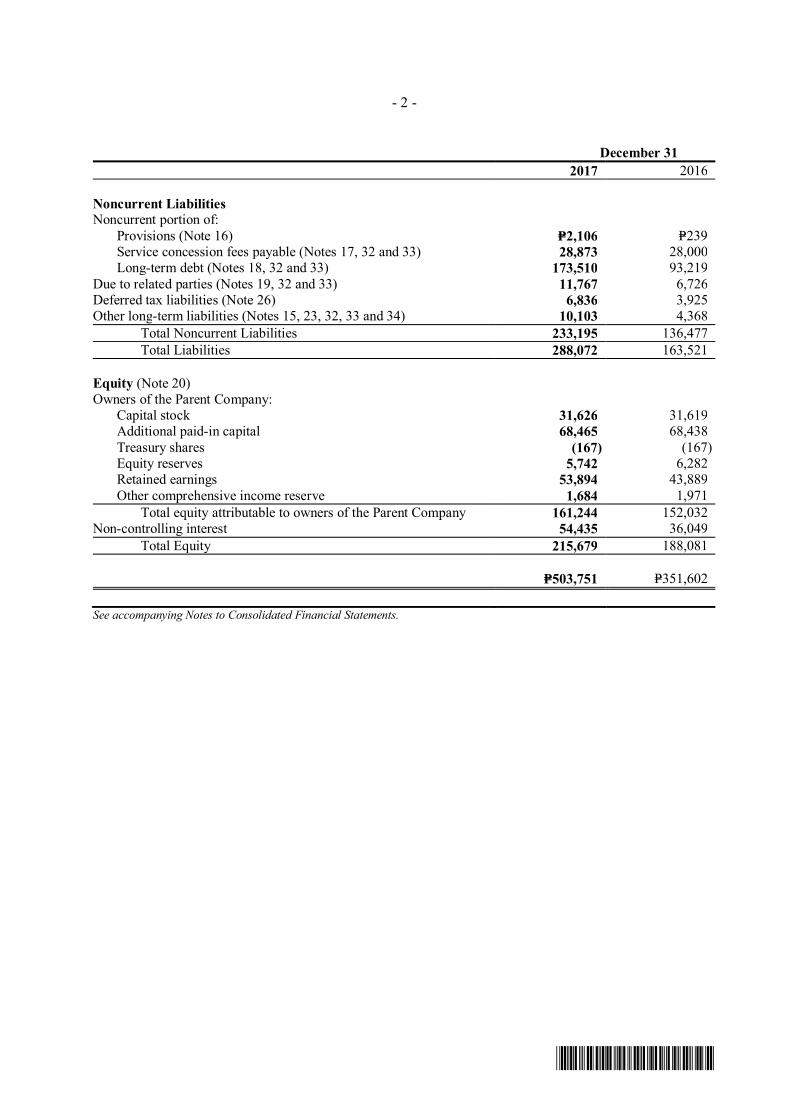

- 2 -

December 312017 2016

Noncurrent LiabilitiesNoncurrent portion of:

Provisions (Note 16) P=2,106 P=239Service concession fees payable (Notes 17, 32 and 33) 28,873 28,000Long-term debt (Notes 18, 32 and 33) 173,510 93,219

Due to related parties (Notes 19, 32 and 33) 11,767 6,726Deferred tax liabilities (Note 26) 6,836 3,925Other long-term liabilities (Notes 15, 23, 32, 33 and 34) 10,103 4,368

Total Noncurrent Liabilities 233,195 136,477Total Liabilities 288,072 163,521

Equity (Note 20)Owners of the Parent Company:

Capital stock 31,626 31,619Additional paid-in capital 68,465 68,438Treasury shares (167) (167)Equity reserves 5,742 6,282Retained earnings 53,894 43,889Other comprehensive income reserve 1,684 1,971

Total equity attributable to owners of the Parent Company 161,244 152,032Non-controlling interest 54,435 36,049

Total Equity 215,679 188,081

P=503,751 P=351,602

See accompanying Notes to Consolidated Financial Statements.

*SGVFS026907*

METRO PACIFIC INVESTMENTS CORPORATION AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME(Amounts in Millions, Except Earnings Per Share Figures)

Years Ended December 312017 2016 2015

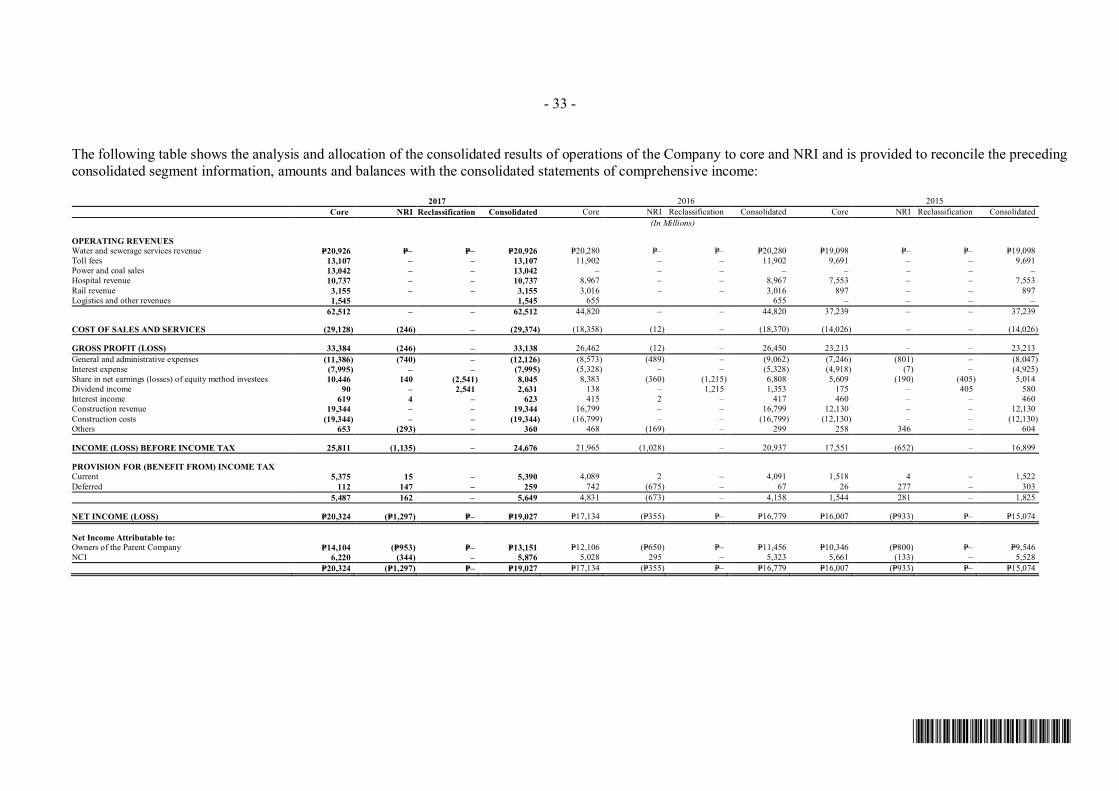

OPERATING REVENUES (Notes 1 and 37)Water and sewerage services revenue P=20,926 P=20,280 P=19,098Toll fees 13,107 11,902 9,691Power and coal sales 13,042 – –Hospital revenue 10,737 8,967 7,553Rail revenue 3,155 3,016 897Logistics and other revenue 1,545 655 –

62,512 44,820 37,239COST OF SALES AND SERVICES (Note 21) (29,374) (18,370) (14,026)GROSS PROFIT 33,138 26,450 23,213General and administrative expenses (Note 22) (12,126) (9,062) (8,047)Interest expense (Note 24) (7,995) (5,328) (4,925)Share in net earnings of equity method investees (Note 10) 8,045 6,808 5,014Dividend income (Note 10) 2,631 1,353 580Interest income (Note 24) 623 417 460Construction revenue (Note 3) 19,344 16,799 12,130Construction costs (Note 3) (19,344) (16,799) (12,130)Others (Note 24) 360 299 604INCOME BEFORE INCOME TAX 24,676 20,937 16,899PROVISION FOR INCOME TAX (Note 26)Current 5,390 4,091 1,522Deferred 259 67 303

5,649 4,158 1,825NET INCOME 19,027 16,779 15,074OTHER COMPREHENSIVE INCOME (LOSS) - NET

(Note 25)To be reclassified to profit or loss in subsequent periods 482 444 (222)Not to be reclassified to profit or loss in subsequent periods (948) 1,024 (133)

(466) 1,468 (355)TOTAL COMPREHENSIVE INCOME P=18,561 P=18,247 P=14,719Net income attributable to:Owners of the Parent Company P=13,151 P=11,456 P=9,546Non-controlling interest 5,876 5,323 5,528

P=19,027 P=16,779 P=15,074Total comprehensive income attributable to:Owners of the Parent Company P=12,864 P=12,917 P=9,220Non-controlling interest 5,697 5,330 5,499

P=18,561 P=18,247 P=14,719EARNINGS PER SHARE (Note 27)Basic Earnings Per Common Share, Attributable

to Owners of the Parent Company P=0.4171 P=0.3810 P=0.3447Diluted Earnings Per Common Share, Attributable

to Owners of the Parent Company P=0.4167 P=0.3806 P=0.3445

See accompanying Notes to Consolidated Financial Statements.

*SGVFS026907*

METRO PACIFIC INVESTMENTS CORPORATION AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CHANGES IN EQUITYFOR THE YEARS ENDED DECEMBER 31, 2017, 2016 AND 2015(Amounts in Millions)

Year Ended December 31, 2017Attributable to Owners of the Parent Company

Capital Stock(Note 20)

AdditionalPaid-inCapital

(Note 20)

TreasuryShares

(Note 20)Equity

Reserves

RetainedEarnings(Note 20)

OtherComprehensive

IncomeReserve(Note 20) Total

Non-controlling

Interest(NCI)

TotalEquity

At January 1, 2017 P=31,619 P=68,438 (P=167) P=6,282 P=43,889 P=1,971 P=152,032 P=36,049 P=188,081Total comprehensive income for the year: Net income – – – – 13,151 – 13,151 5,876 19,027 Other comprehensive income (Note 25) – – – – – (287) (287) (179) (466)Executive Stock Option Plan (Note 28) 7 27 – (5) – – 29 – 29Restricted Stock Unit Plan (Note 28) – – – 67 – – 67 – 67Cash dividends declared (Note 20) – – – – (3,239) – (3,239) – (3,239)Business combinations and other movements in NCI (Note 4) – – – – 93 – 93 17,138 17,231Acquisition of non-controlling interest (Notes 4 and 39) – – – (360) – – (360) 48 (312)Deferred tax on equity transaction (Note 26) – – – (242) – – (242) – (242)Dividends declared to non-controlling stockholders (Note 6) – – – – – – – (4,497) (4,497)At December 31, 2017 P=31,626 P=68,465 (P=167) P=5,742 P=53,894 P=1,684 P=161,244 P=54,435 P=215,679

- 2 -

*SGVFS026907*

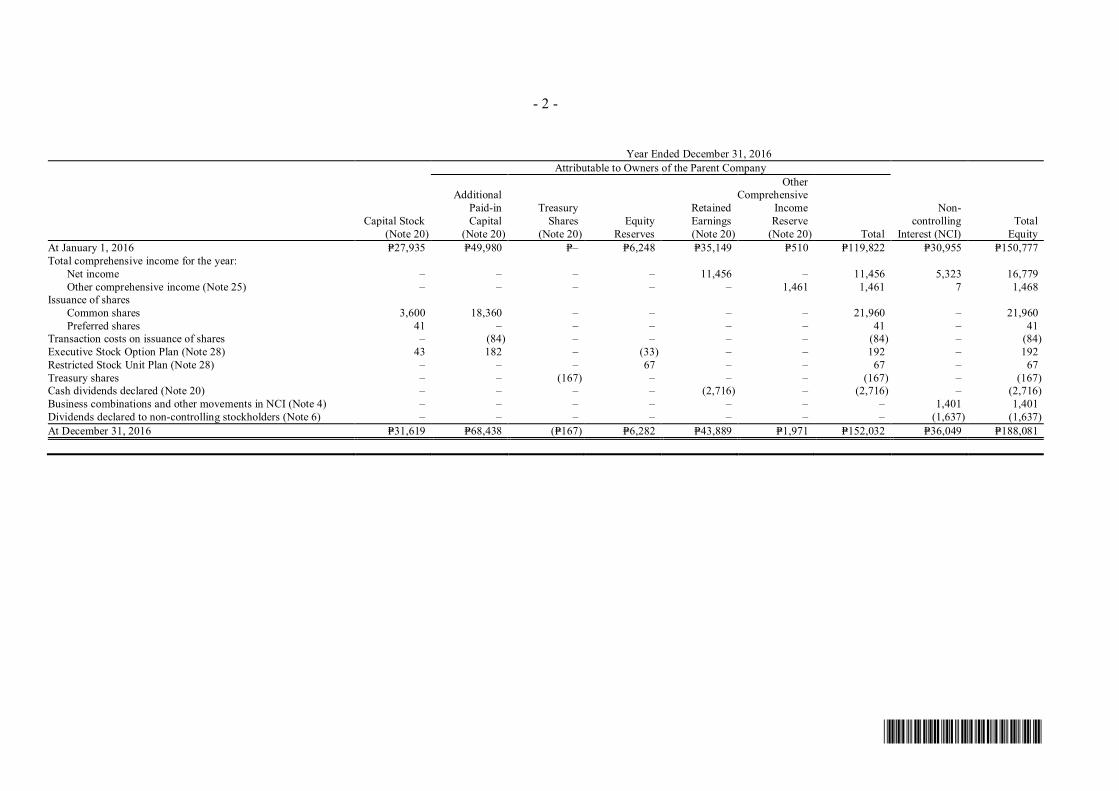

Year Ended December 31, 2016Attributable to Owners of the Parent Company

Capital Stock(Note 20)

AdditionalPaid-inCapital

(Note 20)

TreasuryShares

(Note 20)Equity

Reserves

RetainedEarnings(Note 20)

OtherComprehensive

IncomeReserve

(Note 20) Total

Non-controlling

Interest (NCI)Total

EquityAt January 1, 2016 P=27,935 P=49,980 P=– P=6,248 P=35,149 P=510 P=119,822 P=30,955 P=150,777Total comprehensive income for the year: Net income – – – – 11,456 – 11,456 5,323 16,779 Other comprehensive income (Note 25) – – – – – 1,461 1,461 7 1,468Issuance of shares Common shares 3,600 18,360 – – – – 21,960 – 21,960 Preferred shares 41 – – – – – 41 – 41Transaction costs on issuance of shares – (84) – – – – (84) – (84)Executive Stock Option Plan (Note 28) 43 182 – (33) – – 192 – 192Restricted Stock Unit Plan (Note 28) – – – 67 – – 67 – 67Treasury shares – – (167) – – – (167) – (167)Cash dividends declared (Note 20) – – – – (2,716) – (2,716) – (2,716)Business combinations and other movements in NCI (Note 4) – – – – – – – 1,401 1,401Dividends declared to non-controlling stockholders (Note 6) – – – – – – – (1,637) (1,637)At December 31, 2016 P=31,619 P=68,438 (P=167) P=6,282 P=43,889 P=1,971 P=152,032 P=36,049 P=188,081

- 3 -

*SGVFS026907*

Year Ended December 31, 2015Attributable to Owners of the Parent Company

Capital Stock(Note 20)

AdditionalPaid-inCapital

(Note 20)Equity

Reserves

RetainedEarnings(Note 20)

OtherComprehensive

IncomeReserve

(Note 20) TotalNon-controlling

Interest (NCI) Total EquityAt January 1, 2015 P=26,096 P=42,993 P=6,245 P=27,525 P=836 P=103,695 P=25,877 P=129,572Total comprehensive income for the year: Net income – – – 9,546 – 9,546 5,528 15,074 Other comprehensive income (Note 25) – – – – (326) (326) (29) (355)Executive Stock Option Plan (ESOP) (Note 38): Exercise of stock option 27 78 (30) – – 75 – 75 Cost of ESOP – – 21 – – 21 – 21 Expiration of ESOP – 10 (15) 5 – – – –Equity raising (Note 20) 1,812 6,899 – – – 8,711 – 8,711Cash dividends declared (Note 20) – – – (1,927) – (1,927) – (1,927)Additional investment from NCI – – – – – – 1,125 1,125Dividends declared to non-controlling stockholders (Note 6) – – – – – – (1,593) (1,593)Gain on acquisition of NCI and others (Note 4) – – 27 – – 27 47 74At December 31, 2015 P=27,935 P=49,980 P=6,248 P=35,149 P=510 P=119,822 P=30,955 P=150,777

See accompanying Notes to Consolidated Financial Statements.

*SGVFS026907*

METRO PACIFIC INVESTMENTS CORPORATION AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CASH FLOWS(Amounts in Millions)

Years Ended December 312017 2016 2015

CASH FLOWS FROM OPERATING ACTIVITIESIncome before income tax 24,676 P=20,937 P=16,899Adjustments for:

Interest expense (Note 24) 7,995 5,328 4,925Amortization of service concession assets (Note 21) 3,909 3,679 3,317Depreciation and amortization (Notes 1, 13, 21 and 22) 3,379 1,334 1,076Impairment of goodwill and nonfinancial assets

(Notes 3, 10 and 11) 763 774 –Long Term Incentive Plan expense (Note 23) 629 533 568Unrealized foreign exchange loss – net 65 2 149Share in net earnings of equity method investees

(Note 10) (8,045) (6,808) (5,014)Dividend income (2,631) (1,353) (580)Gain on sale of investments (Note 10) (732) – –Interest income (Note 24) (623) (417) (460)Others 558 (165) 156

Operating income before working capital changes 29,943 23,844 21,036Increase in:

Restricted cash (775) (18) (47)Receivables (761) (694) (574)Due from related parties and other current assets (1,338) (604) (1,309)

Increase (decrease) in:Accounts payable and other current liabilities 2,884 729 699Provisions and accrued retirement cost 1,104 (726) (348)

Net cash generated from operations 31,057 22,531 19,457Income taxes paid (5,145) (4,042) (1,359)Interest received 596 429 446Net cash from operating activities 26,508 18,918 18,544

CASH FLOWS FROM INVESTING ACTIVITIESDividends received from:

Equity method investees (Note 10) 6,903 5,679 2,283Beacon Electric’s preferred shares (Note 10) 2,541 – 405Available-for-sale financial assets (Notes 32 and 33) 144 136 121

Collection of or proceeds from sale/disposal of:Available-for-sale financial assets (Notes 32 and 33) 14,968 14,679 21,618Investment in associate (net of transaction

cost; Note 10) 12,403 – –Redemption of preferred shares (Note 10) 3,500 – –Property, plant and equipment (Note 13) 22 21 7Notes receivable – – 118

Acquisition of subsidiaries, net of cash acquired (Note 4) (5,958) (4,812) –

(Forward)

- 2 -

*SGVFS026907*

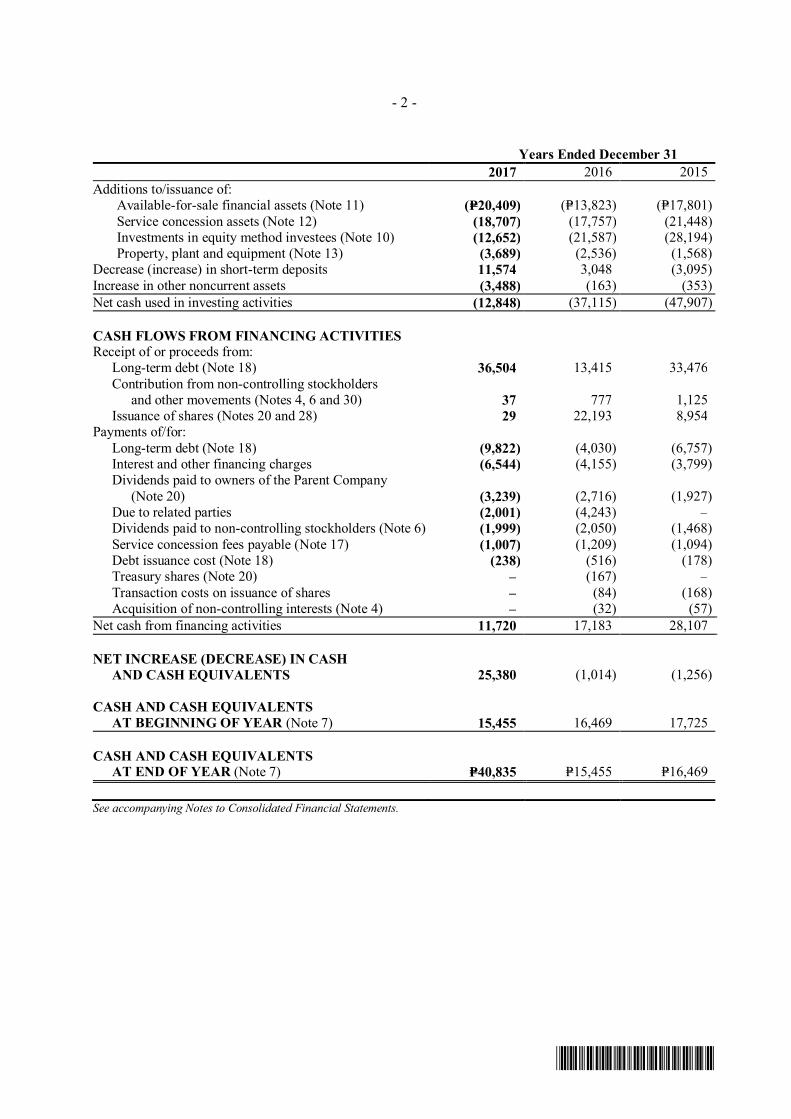

Years Ended December 312017 2016 2015

Additions to/issuance of:Available-for-sale financial assets (Note 11) (P=20,409) (P=13,823) (P=17,801)Service concession assets (Note 12) (18,707) (17,757) (21,448)Investments in equity method investees (Note 10) (12,652) (21,587) (28,194)Property, plant and equipment (Note 13) (3,689) (2,536) (1,568)

Decrease (increase) in short-term deposits 11,574 3,048 (3,095)Increase in other noncurrent assets (3,488) (163) (353)Net cash used in investing activities (12,848) (37,115) (47,907)

CASH FLOWS FROM FINANCING ACTIVITIESReceipt of or proceeds from:

Long-term debt (Note 18) 36,504 13,415 33,476Contribution from non-controlling stockholders and other movements (Notes 4, 6 and 30) 37 777 1,125Issuance of shares (Notes 20 and 28) 29 22,193 8,954

Payments of/for:Long-term debt (Note 18) (9,822) (4,030) (6,757)Interest and other financing charges (6,544) (4,155) (3,799)Dividends paid to owners of the Parent Company (Note 20) (3,239) (2,716) (1,927)Due to related parties (2,001) (4,243) –Dividends paid to non-controlling stockholders (Note 6) (1,999) (2,050) (1,468)Service concession fees payable (Note 17) (1,007) (1,209) (1,094)Debt issuance cost (Note 18) (238) (516) (178)Treasury shares (Note 20) – (167) –Transaction costs on issuance of shares – (84) (168)Acquisition of non-controlling interests (Note 4) – (32) (57)

Net cash from financing activities 11,720 17,183 28,107

NET INCREASE (DECREASE) IN CASHAND CASH EQUIVALENTS 25,380 (1,014) (1,256)

CASH AND CASH EQUIVALENTSAT BEGINNING OF YEAR (Note 7) 15,455 16,469 17,725

CASH AND CASH EQUIVALENTSAT END OF YEAR (Note 7) P=40,835 P=15,455 P=16,469

See accompanying Notes to Consolidated Financial Statements.

*SGVFS026907*

METRO PACIFIC INVESTMENTS CORPORATION AND SUBSIDIARIESNOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Corporate Information

GeneralMetro Pacific Investments Corporation (the Parent Company or MPIC) was incorporated in thePhilippines and registered with the Philippines Securities and Exchange Commission (SEC) onMarch 20, 2006 as an investment holding company. MPIC’s common shares of stock are listed inand traded through the Philippine Stock Exchange (PSE). On August 6, 2012, MPIC launchedSponsored Level 1 American Depositary Receipt (ADR) Program with Deutsche Bank as theappointed depositary bank in line with the Parent Company’s thrust to widen the availability of itsshares to investors in the United States.

The principal activities of the Parent Company’s subsidiaries and equity method investees aredescribed below (see Company’s Operating Segments) and in Notes 10 and 39. The Parent Companyand its subsidiaries are collectively referred to as “the Company”.

Metro Pacific Holdings, Inc. (MPHI) owns 41.9% of the total issued common shares (or 42.0% of thetotal outstanding common shares) of MPIC as at December 31, 2017 and 2016. As sole holder of thevoting Class A Preferred Shares, MPHI’s combined voting interest as a result of all of itsshareholdings is estimated at 55.0% as at December 31, 2017 and 2016 (see Note 20).

MPHI is a Philippine corporation whose stockholders are Enterprise Investment Holdings, Inc. (EIH;60.0% interest), Intalink B.V. (26.7% interest) and First Pacific International Limited (FPIL; 13.3%interest). First Pacific Company Limited (FPC), a company incorporated in Bermuda and listed inHong Kong, through its subsidiaries, Intalink B.V. and FPIL, holds 40.0% equity interest in EIH andinvestment financing which under Hong Kong Generally Accepted Accounting Principles, requireFPC to account for the results and assets and liabilities of EIH and its subsidiaries as part of FPCgroup of companies in Hong Kong.

The registered office address of the Parent Company is 10th Floor, MGO Building, Legaspi cornerDela Rosa Streets, Legaspi Village, Makati City.

The accompanying consolidated financial statements as at December 31, 2017 and 2016 and for eachof the three years in the period ended December 31, 2017 were approved and authorized for issuanceby the Board of Directors (BOD) on March 1, 2018.

Company’s Operating SegmentsFor management purposes, the Company is organized into the following segments based on servicesand products:

ƒ Power, which primarily relates to the operations of Manila Electric Company (MERALCO) inrelation to the distribution, supply and generation of electricity and Global Business PowerCorporation (GBPC) in relation to power generation. The investment in MERALCO is held bothdirectly and indirectly through Beacon Electric Asset Holdings, Inc. (Beacon Electric) while theinvestment in GBPC is held through Beacon Electric’s wholly-owned entity, Beacon PowerGenHoldings Inc. (BPHI) (see Notes 4 and 10).

- 2 -

*SGVFS026907*

ƒ Toll operations, which primarily relate to operations and maintenance of toll facilities by MetroPacific Tollways Corporation (MPTC) and its subsidiaries NLEX Corporation (NLEX Corp;formerly Manila North Tollways Corporation), Cavitex Infrastructure Corporation (CIC),Tollways Management Corporation [TMC; a subsidiary beginning April 2017 (see Notes 4and 10)], and foreign investees, CII Bridges and Roads Investment Joint Stock Company (CIIB&R), Don Muang Tollway Public Ltd (DMT) and PT Nusantara Infrastructure Tbk (PTNusantara) (see Note 10). Certain toll projects are either under pre-construction or on-goingconstruction as at December 31, 2017 (see below Concession Arrangements).

ƒ Water, which relates to the provision of water and sewerage services by Maynilad Water HoldingCompany, Inc. (MWHC) and its subsidiaries, Maynilad Water Services, Inc. (Maynilad) andPhilippine Hydro, Inc. (PHI), and other water-related services by MetroPac Water InvestmentsCorporation (MPW) (see below Concession Arrangements).

ƒ Healthcare, which primarily relates to operations and management of hospitals and nursingcolleges and such other enterprises that have similar undertakings by Metro Pacific HospitalHoldings, Inc. (MPHHI) and subsidiaries.

ƒ Rail, which primarily relates to Metro Pacific Light Rail Corporation (MPLRC) and itssubsidiary, Light Rail Manila Corporation (LRMC), the concessionaire for the operations andmaintenance of the Light Rail Transit – Line 1 (LRT-1) and construction of the LRT-1 southextension (see below Concession Arrangements).

ƒ Logistics, which primarily relates to the Company’s logistics business through MetroPacLogistics Company, Inc. (MPLC) and its subsidiary, MetroPac Movers, Inc. (MMI).

ƒ Others, which represent holding companies and operations of subsidiaries and other investeesinvolved in real estate and provision of services.

See Note 39 for the complete list of the Company’s subsidiaries. The list of the Company’sassociates and joint ventures are disclosed in Note 10.

Concession ArrangementsMPIC’s subsidiaries have the following concession arrangements with the Philippine Government.Various concession agreements described below each include provision for periodic changes in thetariffs charged to the public in accordance with changes in consumer price index (CPI).

Concession Arrangements – Toll Operations

NLEX Corp – Supplemental Toll Operation Agreement (STOA) for the North Luzon Expressway(NLEX). In August 1995, First Philippine Infrastructure Development Corporation, the then parentcompany of NLEX Corp, entered into a joint venture agreement with Philippine NationalConstruction Corporation (PNCC), in which PNCC assigned its rights, interests and privileges underits franchise to construct, operate and maintain toll facilities in the NLEX and its extensions,stretches, linkages and diversions in favor of NLEX Corp, including the design, funding,construction, rehabilitation, refurbishing and modernization and selection and installation of anappropriate toll collection system therein during the concession period subject to prior approval bythe President of the Philippines. In April 1998, the Philippine government, acting by and through theToll Regulatory Board (TRB) as the grantor, PNCC as the franchisee and NLEX Corp as theconcessionaire, executed a STOA whereby the Philippine government recognized and accepted theassignment by PNCC of its usufructuary rights, interests and privileges under its franchise in favor ofNLEX Corp as approved by the President of the Philippines and granted NLEX Corp concession

- 3 -

*SGVFS026907*

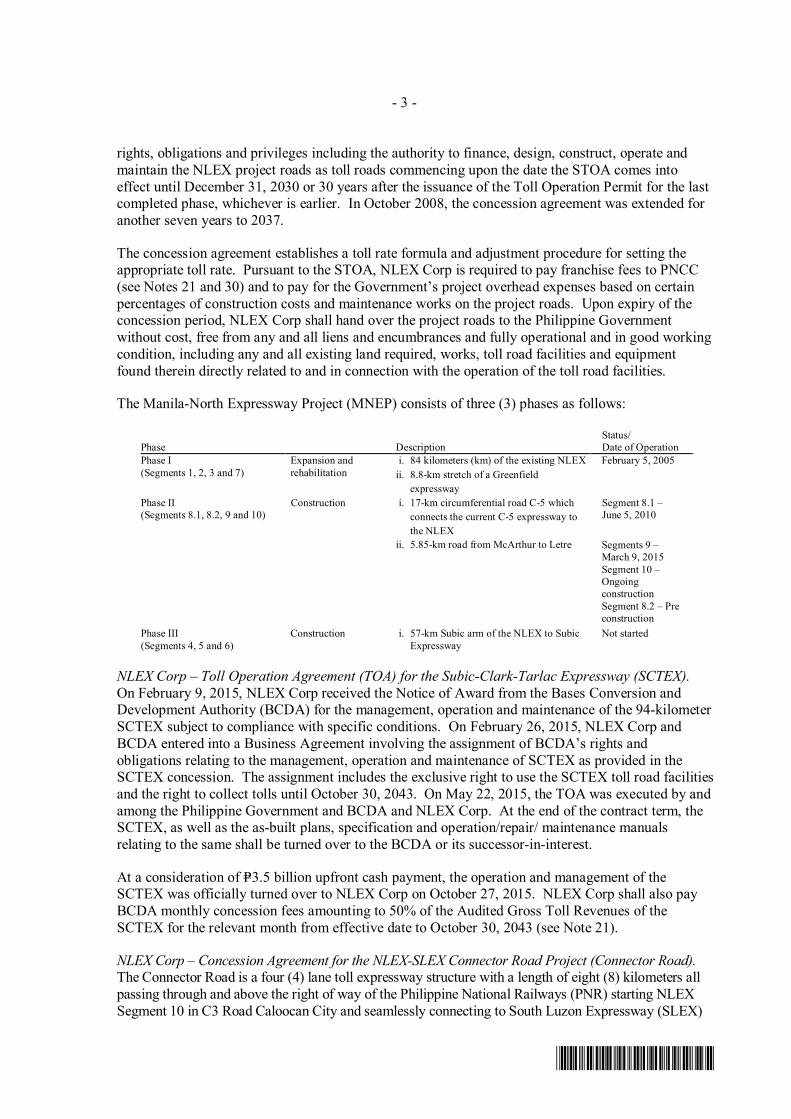

rights, obligations and privileges including the authority to finance, design, construct, operate andmaintain the NLEX project roads as toll roads commencing upon the date the STOA comes intoeffect until December 31, 2030 or 30 years after the issuance of the Toll Operation Permit for the lastcompleted phase, whichever is earlier. In October 2008, the concession agreement was extended foranother seven years to 2037.

The concession agreement establishes a toll rate formula and adjustment procedure for setting theappropriate toll rate. Pursuant to the STOA, NLEX Corp is required to pay franchise fees to PNCC(see Notes 21 and 30) and to pay for the Government’s project overhead expenses based on certainpercentages of construction costs and maintenance works on the project roads. Upon expiry of theconcession period, NLEX Corp shall hand over the project roads to the Philippine Governmentwithout cost, free from any and all liens and encumbrances and fully operational and in good workingcondition, including any and all existing land required, works, toll road facilities and equipmentfound therein directly related to and in connection with the operation of the toll road facilities.

The Manila-North Expressway Project (MNEP) consists of three (3) phases as follows:

Phase DescriptionStatus/Date of Operation

Phase I(Segments 1, 2, 3 and 7)

Expansion andrehabilitation

i. 84 kilometers (km) of the existing NLEXii. 8.8-km stretch of a Greenfield

expressway

February 5, 2005

Phase II(Segments 8.1, 8.2, 9 and 10)

Construction i. 17-km circumferential road C-5 whichconnects the current C-5 expressway tothe NLEX

Segment 8.1 –June 5, 2010

ii. 5.85-km road from McArthur to Letre Segments 9 –March 9, 2015Segment 10 –OngoingconstructionSegment 8.2 – Preconstruction

Phase III(Segments 4, 5 and 6)

Construction i. 57-km Subic arm of the NLEX to SubicExpressway

Not started

NLEX Corp – Toll Operation Agreement (TOA) for the Subic-Clark-Tarlac Expressway (SCTEX).On February 9, 2015, NLEX Corp received the Notice of Award from the Bases Conversion andDevelopment Authority (BCDA) for the management, operation and maintenance of the 94-kilometerSCTEX subject to compliance with specific conditions. On February 26, 2015, NLEX Corp andBCDA entered into a Business Agreement involving the assignment of BCDA’s rights andobligations relating to the management, operation and maintenance of SCTEX as provided in theSCTEX concession. The assignment includes the exclusive right to use the SCTEX toll road facilitiesand the right to collect tolls until October 30, 2043. On May 22, 2015, the TOA was executed by andamong the Philippine Government and BCDA and NLEX Corp. At the end of the contract term, theSCTEX, as well as the as-built plans, specification and operation/repair/ maintenance manualsrelating to the same shall be turned over to the BCDA or its successor-in-interest.

At a consideration of P=3.5 billion upfront cash payment, the operation and management of theSCTEX was officially turned over to NLEX Corp on October 27, 2015. NLEX Corp shall also payBCDA monthly concession fees amounting to 50% of the Audited Gross Toll Revenues of theSCTEX for the relevant month from effective date to October 30, 2043 (see Note 21).

NLEX Corp – Concession Agreement for the NLEX-SLEX Connector Road Project (Connector Road).The Connector Road is a four (4) lane toll expressway structure with a length of eight (8) kilometers allpassing through and above the right of way of the Philippine National Railways (PNR) starting NLEXSegment 10 in C3 Road Caloocan City and seamlessly connecting to South Luzon Expressway (SLEX)

- 4 -

*SGVFS026907*

through Metro Manila Skyway Stage 3 Project. On November 23, 2016, NLEX Corp and the Republicof the Philippines (ROP) acting through the Department of Public Works and Highways (DPWH), signedthe Concession Agreement for the design, financing, construction, operation and maintenance of theNLEX-SLEX Connector Road. The concession period shall commence on the commencement date andshall end on its thirty-seventh (37th) anniversary, unless otherwise extended or terminated in accordancewith the Concession Agreement. The Connector Project, with an estimated project cost of P=23.3 billion,is expected to commence construction in 2018 and to complete by 2020.

Under the Concession Agreement, NLEX Corp will pay the DPWH periodic payments as considerationfor the grant of the Right of Way for the project (see Note 17). Other material commitments under theConnector Road’s concession agreement are disclosed in Note 30.

CIC – Toll Operation Agreement (TOA) for the Manila - Cavite Expressway (CAVITEX). CIC isexclusively responsible for the design, financing and construction of the CAVITEX, pursuant to aTOA dated July 26, 1996 entered into with the Philippine Reclamation Authority (PRA) and theGovernment, acting through the TRB. Responsibility for the supervision of the operation andmaintenance of the toll road, initially undertaken by the PRA, was also transferred to CIC pursuant toan Operations and Maintenance Agreement dated November 14, 2006 and a voting trust agreementdated November 16, 2006. The concession for CAVITEX extends to 2033 for the originally builtroad and to 2046 for a subsequent extension. Upon expiry of the concession period, CIC shall handover the project to the Philippine Government.

The concession agreement establishes a toll rate formula and adjustment procedure for setting theappropriate toll rate.

Pursuant to the TOA, PRA established PEA Tollways Corporation (PEATC), its wholly ownedsubsidiary, to undertake the O&M obligations of the PRA under the TOA (see Note 30).

Under the amended Joint Venture Agreement with PRA, each of the following expressways shall beconstructed in segments:

Phase DescriptionStatus/Date of Operation

Phase I Design and improvement i. 6.5 km R-1 Expressway which connectsthe Airport Road to Zapote

ii. Extension of the 7 km R-1 Expresswaywhich connects the existing R-1Expressway at Zapote to Noveleta

May 1998

May 2011

Phase II Design and construction i. Extension of the C-5 Link Expresswaywhich connects the R-1 Expressway tothe South Luzon Expressway (SLEX)

C-5 Link Expresswayjoining C-5 Road inTaguig to R-1Expressway- OngoingConstruction

MPCALA Holdings, Inc. (MPCALA) – Concession Agreement for the Cavite Laguna Expressway(CALAEX). On July 10, 2015, MPCALA signed the Concession Agreement for the CALAEX Projectwith the DPWH. Under the Concession Agreement, MPCALA is granted the concession to design,finance, construct, operate and maintain the CALAEX, including the right to collect toll fees, over a35-year concession period. The CALAEX is a closed-system tolled expressway connecting theCAVITEX and the SLEX. The CALAEX Project was awarded to MPCALA following a competitivepublic bidding process where MPCALA was declared as the highest complying bidder with its offerto pay the government concession fees amounting to P=27.3 billion payable over 9 years from signingof the Concession Agreement (see Note 17).

- 5 -

*SGVFS026907*

On July 3, 2017, MPCALA issued the Notice to Proceed to D.M. Consunji, Inc. (Consunji) signifyingthe official commencement of construction works for the project (see Note 19). The project isexpected to be completed in 2020 and be fully operational by 2021.

Cebu Cordova Link Expressway Corporation’s (CCLEC) Cebu Cordova Link Expressway (CCLEX).On October 3, 2016, CCLEC, Cebu City and Municipality of Cordova (as grantors) signed theconcession agreement for the CCLEX. CCLEX, consists of the main alignment starting from theCebu South Coastal Road and ending at the Mactan Circumferential Road, inclusive of interchangeramps aligning the Guadalupe River, the main span bridge, approaches, viaducts, causeways, low-height bridges, at-grade road, toll plazas and toll operations center.

Under the concession agreement, CCLEC is granted the concession to design, finance, construct,operate and maintain the CCLEX, including the right to collect toll fees over a 35-year concessionperiod. CCLEX is estimated to cost P=26.3 billion. No upfront payments or concession fees are to bepaid but the grantors shall share 2% of the project’s revenue.

Construction is ongoing and expected to be completed by 2021.

Concession Arrangements - Water

Maynilad. In February 1997, Maynilad entered into a concession agreement with Metropolitan WaterSewerage System (MWSS), with respect to the MWSS West Service Area. Under the concessionagreement, MWSS grants Maynilad, the sole right to manage, operate, repair, decommission andrefurbish all fixed and movable assets required to provide water and sewerage services in the WestService Area for 25 years ending in 2022. In September 2009, MWSS approved an extension of itsconcession agreement with Maynilad for another 15 years to 2037 (the expiration date). The legaltitle to all property, plant and equipment contributed to the existing MWSS system by Mayniladduring the concession period remains with Maynilad until the expiration date at which time, all rights,titles and interests in such assets will automatically vest to MWSS. Under the concession agreement,Maynilad is entitled to charge its customers a Basic Standard tariff which is calculated to enableMaynilad to recover all expenditures efficiently and prudently incurred, including Philippinesbusiness taxes and concession fees while also providing Maynilad a real rate of return on the net cashsum invested in the concession from time to time. This tariff is subject to periodic changes dueprincipally to (a) an annual standard rate adjustment to compensate for changes in the CPI subject to arate adjustment limit; (b) an extraordinary price adjustment to account for the financial consequencesof the occurrence of certain unforeseen events subject to grounds stipulated in the concessionagreement; and (c) a rate rebasing mechanism which allows rates to be adjusted every five years. Therate rebasing adjustment allows for updates to estimates for expenditures and demand forecasts whilealso resetting the real rate of return awarded to Maynilad in light of changes to costs of funding.Under Maynilad’s concession agreement with the Philippine Government, any rate adjustmentrequires approval by MWSS and the Regulatory Office (RO).

The Republic of the Philippines (ROP) also issued in favor of Maynilad on July 31, 1997 andMarch 17, 2010 an undertaking which provides, among other things, that the ROP shall indemnifyMaynilad in respect of any loss that is occasioned by a delay caused by the ROP or anygovernment-owned agency in implementing any increase in the standard rates beyond the date for itsimplementation in accordance with the concession agreement (the “Undertaking”).

Other material commitments under Maynilad’s concession agreement are disclosed in Note 30.

- 6 -

*SGVFS026907*

PHI. In August 2012, Maynilad acquired a 100% interest in PHI, which engages in water distributionbusiness in certain areas in central and southern Luzon. PHI is granted the sole right to distributewater in these areas under certain concession agreements granted by the Philippine government for 25years to 2035.

Metro Iloilo Bulk Water Supply Corporation (MIBWSC). On July 4, 2016, pursuant to a JointVenture Agreement between MetroPac Iloilo Holdings Corporation (MILO; a wholly ownedsubsidiary of MPW), and Metro Iloilo Water District (MIWD), created and established MIBWSC, toimplement the 170 Million Liters per Day (MLD) Bulk Water Supply Project (BWS Project). TheBWS Project covers the (i) rehabilitation and upgrading of MIWD’s existing 55 MLD water facilities,(ii) the expansion and construction of new water facilities to increase production to up to 115 MLD;and (iii) delivery of contracted water demand to MIWD in accordance with the bulk water supplyagreement. The BWS Project covers a period from the later of the Target Initial Delivery Date andthe Initial Delivery Date and ending on the 25th anniversary thereof and shall be extended for anadditional 25 years counted from completion of the agreed upon expansion obligation, but in no eventshall exceed an aggregate of 50 years. The Target Initial Delivery Date is expected to take place inAugust 2018.

MIWD retains ownership of the existing facilities subject to the right of MIBWSC to access and use.MIBWSC in turn retains ownership of the new facilities but is required to handback the Project,including transfer of the full ownership of the new facilities, at the end of the contract period.

On July 5, 2016, MIBWSC officially took over operations from the MIWD.

Concession Arrangements – Rail

LRMC’s LRT-1 Project. On October 2, 2014, LRMC signed together with the Department ofTransportation and Communications (DOTC, now Department of Transportation - DOTr) and the LightRail Transit Authority (LRTA) (together with DOTr as “Grantors”) the Concession Agreement for theLRT-1 Cavite Extension and Operations & Maintenance Project (LRT-1 Project). The DOTr and LRTAformally awarded the Project to LRMC on September 15, 2014. Under the Concession Agreement,LRMC will operate and maintain the existing LRT-1 and construct an 11.7-km extension from thepresent end-point at Baclaran to the Niog area in Bacoor, Cavite. A total of eight new stations will bebuilt along the extension, which traverses the cities of Parañaque and Las Piñas up to Bacoor, Cavite.The Concession Agreement is for a period of thirty-two (32) years commencing fromSeptember 12, 2015 (the Effective Date).

LRMC has the right to apply for an adjustment of the fare based on the specific fare adjustment formulaunder LRMC’s concession agreement with the Philippine Government. This formula specifies an initialboarding and per-kilometer fare with 10.25% increases over these initial fares every two years beginningin August 2016, subject to inflation rebasing if inflation falls outside an acceptable band. If the approvedfare is different from the formula specified on the concession agreement, both the Philippine Governmentand LRMC are obligated to substantially keep the other party whole, depending on whether the actualfares represent a deficit or a surplus.

Rehabilitation of the existing system is expected to be completed in 2020. Construction of the CaviteExtension is expected to commence once right of way is delivered by the Grantors and is targeted to becompleted four (4) years thereafter. The right of way was not fully delivered as at March 1, 2018.However, on May 30, 2017, LRMC received the Permit to Enter certificate from the Grantors allowingLRMC to enter the concerned properties and commence the construction of Cavite Extension. TheCavite Extension is on design phase as at March 1, 2018.

- 7 -

*SGVFS026907*

Electric Power Purchase Agreements (EPPA)GBPC’s power generation facilities consist of: (i) 246 MW clean coal-fired power plant in Toledo City,Cebu, which is operated by Cebu Energy Development Corporation (CEDC); (ii) 164 MW and 150 MWclean coal-fired power plants in Iloilo City, which is operated by Panay Energy DevelopmentCorporation (PEDC); (iii) 60 MW coal facility, an 82 MW clean coal fired power plant and a 40 MWfuel oil facility operated by Toledo Power Co. (TPC); (iv) a 72 MW fuel oil facility, a 20 MW fuel oilfacility, a 7.5 MW fuel oil facility and a 5 MW fuel oil facility operated by Panay Power Corporation(PPC); and (v) 7.5 MW fuel oil facility operated by GBH Power Resources Inc.

GBPC, through its operating generation subsidiaries, entered into bilateral off-take arrangements withpower off-takers such as distribution utilities, electric cooperatives, retail electricity suppliers and directlyconnected industrial customers which together accounted for 92% and 95% of GBPC’s total electricitysales for the years ended December 31, 2017 and 2016, respectively.

HospitalsAs at December 31, 2017, the Company, through MPHHI and its subsidiaries (see Note 39), operatesthe following full service hospitals:

ƒ In Metro Manila: Cardinal Santos Medical Center (CSMC), Our Lady of Lourdes Hospital(OLLH), Asian Hospital (AHI), De Los Santos Medical Center (DLSMC), Marikina ValleyMedical Center (MVMC) and Dr. Jesus C. Delgado Memorial Hospital (JDMH); and

ƒ In other parts of the Philippines: Riverside Medical Center (RMCI) in Bacolod, Central LuzonDoctors Hospital (CLDH) in Tarlac, West Metro Medical Center (WMMC) in Zamboanga,Sacred Heart Hospital of Malolos Inc. (SHHM) in Bulacan and Saint Elizabeth Hospital Inc.(SEHI) in General Santos City.

The Company also has equity stake in the following hospitals: Makati Medical Center (MMC);Manila Doctors Hospital (MDH) and Davao Doctors Hospital (DDH) (see Note 10).

2. Basis of Preparation, Consolidation and Statement of Compliance

Basis of PreparationThe consolidated financial statements are prepared on a historical cost basis, except for certainavailable-for-sale (AFS) financial assets and derivative financial instruments that are measured at fairvalue. The consolidated financial statements are presented in Philippine Peso, which is MPIC’sfunctional and presentation currency, and all values are rounded to the nearest million peso(P=000,000), except when otherwise indicated.

The consolidated financial statements provide comparative information with respect to the previousperiods.

Basis of ConsolidationThe consolidated financial statements of the Company include the accounts of the Parent Companyand its subsidiaries.

Subsidiaries are all entities (including structured entities) over which the Company has control. TheCompany controls an entity when the Company is exposed to, or has rights to, variable returns fromits involvement with the entity and has the ability to affect those returns through its power to directthe activities of the entity. Subsidiaries are fully consolidated from the date on which control istransferred to the Company. They are deconsolidated from the date that control ceases.

- 8 -

*SGVFS026907*

The acquisition method of accounting is used to account for business combinations by the Company.

Intercompany transactions, balances and unrealized gains on transactions between companies areeliminated. Unrealized losses are also eliminated unless the transaction provides evidence of animpairment of the transferred asset. Accounting policies of subsidiaries have been changed wherenecessary to ensure consistency with the policies adopted by the Company.

Non-controlling interests in the results and equity of subsidiaries are shown separately in theconsolidated statement of comprehensive income, consolidated statement of changes in equity andconsolidated statement of financial position respectively.

A complete list of the Company’s subsidiaries is provided for in Note 39.

Statement of ComplianceThe consolidated financial statements are prepared in compliance with Philippine Financial ReportingStandards (PFRS). The Company’s significant accounting policies are disclosed in Note 37.

3. Management’s Use of Judgments and Estimates

The preparation of the consolidated financial statements in compliance with PFRS requiresmanagement to make judgments and estimates that affect the reported amounts of revenues, expenses,assets and liabilities, the disclosure of contingent liabilities and other significant disclosures.Uncertainty about these assumptions and estimates could result in outcomes that require a materialadjustment to the carrying amount of assets or liabilities affected in future periods.

JudgmentsIn the process of applying the Company’s accounting policies, management has made the followingjudgments, apart from those involving estimations, which have the most significant effect on the amountsrecognized in the consolidated financial statements.

Consolidation of CIC. While presently not owning any of CIC’s common voting shares, theCompany, through MPTC, considers that it controls CIC by virtue of the Management LetterAgreement (MLA). Under the MLA, MPTC has the power to solely direct the entire operations,including the capital expenditure and expansion plans of CIC. MPTC shall then receive all thefinancial benefits from CIC’s operations and all losses incurred by CIC are to be borne by MPTC.

On June 28, 2017, MPTC, Cavitex Holdings, Inc. (CHI) and CIC, amended the Management Periodoriginally stated in the Management Letter Agreement dated December 27, 2012 effective on June 28,2017. Accordingly, the Management Period for the management of CIC by MPTC is amended to befrom January 2, 2013 and while MPTC holds the CHI Preferred Shares, or until MPTC becomes the100% direct or indirect shareholder of CIC, whichever comes later.

Dilution in Interest in a Subsidiary as Equity Transaction. On July 2, 2014, GIC Private Limited(GIC), through Arran Investment Private Limited, invested P=3.7 billion for a 14.4% stake in MPIC’ssubsidiary, MPHHI, and paid P=6.5 billion as consideration for an Exchangeable Bond which can beexchanged into a 25.5% stake in MPHHI in the future. The Exchangeable Bond is an instrument that,at a certain time in the future, converts into a fixed number of shares of MPHHI. Moreover, theprincipal of Exchangeable Bond is in Philippine Peso, the same currency as the functional currency ofMPIC as the issuing entity. Thus, the Exchangeable Bond qualifies as an equity instrument such thatthe proceeds from the Exchangeable Bond together with the share subscription of GIC in MPHHI,were considered as equity transactions with a non-controlling shareholder. Interest accruing on theExchangeable Bond is recorded as interest payable recognized at its present value.

- 9 -

*SGVFS026907*

Majority Ownership Interest Without Control. Where the Company holds more than 50% of votingrights in an investee, there is a presumption that the Company has the power to exercise control andsuch investment is treated as a subsidiary. However, in applying the control provisions in relation tothe Company’s participation in the investee’s decision making and other relevant activities, theCompany has made certain judgment which determined the accounting and classification of thefollowing investments:

ƒ TMC. In December 2016, MPTC increased its ownership interest in TMC from 46% to 60%.Despite ownership interest of 60%, investment in TMC was accounted for as an associate as atDecember 31, 2016 because another significant shareholder held significant veto rights related tochanges to operating and dividend policies that affects investors’ returns (see Note 10).However, these veto rights ceased with the acquisition of another 7% interest in TMC increasingMPTC’s effective ownership in TMC from 60.0% to 67.0% beginning April 2017. The increasein effective ownership was accounted for as a business combination resulting in the consolidationof TMC (see Note 4).

ƒ Costa de Madera Corporation (Costa de Madera). Despite ownership interest of 62%, this isaccounted for as an associate because control and management rest with the other shareholders(see Note 10).

Investments in Beacon Electric. Prior to June 2017, the Company made the following judgments withrespect to its investments in Beacon Electric’s common shares and preferred shares:

ƒ Investments in Beacon Electric’s common shares. For all joint arrangements structured inseparate vehicles, the Company must assess the substance of the joint arrangement in determiningwhether it is classified as a joint venture or joint operation. This assessment requires theCompany to consider whether it has rights to the joint arrangement’s net assets (in which case itis classified as a joint venture), or rights to and obligations for specific assets, liabilities,expenses, and revenues (in which case it is classified as a joint operation). Factors the Companyconsiders include: structure, legal form, contractual agreement, and other facts and circumstances.Upon consideration of these factors, the Company has determined that its joint arrangement,structured through Beacon Electric as a separate vehicle, gives it rights to the net assets of BeaconElectric, and therefore classified its investment in Beacon Electric’s common shares, as a jointventure. Prior to June 2017, the Company had 75% ownership interest in Beacon Electricthrough the common shares. The other 25% as at December 31, 2016, was held by PLDTCommunications and Energy Ventures, Inc. (PCEV). Despite ownership of 75% of the commonshares of Beacon Electric, the Company accounted for its investment in Beacon Electric’scommon shares as investment in a joint venture because MPIC and PCEV retains 50/50 votingarrangement for as long as: (i) PCEV owns at least 20% of the outstanding capital stock ofBeacon Electric, or (ii) the purchase price for the Beacon Electric shares acquired in May 2016has not been fully paid by MPIC (see Note 10).

ƒ Investment in Beacon Electric’s preferred shares. In determining the appropriate accountingpolicy for the Company’s investment in financial instruments, factors that the Company considerinclude the following: contractual characteristics of the financial instrument; the purpose forwhich the instrument is held, for example, trading or long-term investment; and the accountingpolicy choice of the reporting entity. In applying the factors, the Company has made a judgmentthat PAS 39, Financial Instruments: Recognition and Measurement is the appropriate accountingfor its investment in preferred shares of Beacon Electric because: the preferred shares are non-voting and as such, would not provide the Company with control, joint control or significantinfluence over Beacon Electric; the Company intends to hold the investment indefinitely; and theCompany may decide to sell the instruments anytime at its discretion.

- 10 -

*SGVFS026907*

However, in June 2017, MPIC entered into a Deed of Absolute Sale of Shares with PCEV toacquire the remaining 25% interest in Beacon Electric from PCEV. This acquisition wasaccounted for as a business combination resulting in the consolidation of Beacon Electricbeginning on the acquisition date (see Note 4).

Acquisition of a Group of Assets Qualified as a Business Combination. In applying the requirementsof PFRS 3, Business Combinations, an entity or an asset being acquired has to be assessed whether itconstitutes a business. In the assessment, it requires identification of inputs and processes applied tothese inputs to generate outputs or economic benefits. The group of logistics assets acquired asdiscussed in Note 4 is considered a business, hence, accounted for as a business combination.

Service Concession Arrangements. In applying Philippine Interpretation IFRIC 12, ServiceConcession Arrangements, the Company has made a judgment that the service concessionarrangements of the Company’s water, tollway and rail businesses (see Note 1) qualify under theintangible asset model as these companies receive the right to charge users of public service. Detailsof the Company’s accounting policy in respect of the service concession arrangements are set out inNote 37 to the consolidated financial statements. Other significant judgment and estimates made inrelation to concession arrangements are as follows:

ƒ Service Concession Assets. The methods of amortization that the Company uses depends onwhich method best reflects the pattern of consumption of the concession assets. The straight-linemethod is currently being used to amortize the rail concession asset while Unit of Production(UOP) method is being used for the toll and water concession assets (NLEX Corp, CIC andMaynilad). The Company annually reviews the billable water volume, in the case of the waterconcession, and the traffic volume/kilometers travelled, in the case of the toll concession, basedon factors that include market conditions such as population growth and consumption ofwater/usage of the toll facility, and the status of the Company’s projects. It is possible that futureresults of operations could be materially affected by changes in the Company’s estimates broughtabout by changes in the aforementioned factors.

The total carrying values of service concession assets amounted to P=168,783.2 million andP=152,693.3 million as at December 31, 2017 and 2016, respectively (see Note 12).

ƒ Service Concession Asset as Qualifying Assets and Capitalization of Borrowing Costs. TheCompany has made a judgment to apply PAS 23, Borrowing Costs, in classifying the serviceconcession assets’ components undergoing rehabilitation (in the case of the existing LRT-1) andpre/on-going construction (in the case of the construction of the LRT-1 extension, the ConnectorRoad, CALAEX and CCLEX) as qualifying assets. The existing LRT-1 is severely deterioratedwhen turned over to LRMC and the intention of management to bring it at par with the standardfor rail system played a key factor in the designation of the rehabilitation of the existing LRT-1system as a qualifying asset.

The Company capitalizes borrowing costs that are directly attributable to the acquisition orconstruction of the qualifying asset as part of the cost of that asset using the specific borrowingapproach, as the Company uses specific borrowings to finance its qualifying assets. Capitalizedborrowing costs for the years ended December 31, 2017 and 2016 amounted to P=2,906.7 millionand P=2,344.1 million, respectively (see Note 12). Capitalization of borrowing costs ceases whensubstantially all the activities necessary to prepare the components of the service concession assetfor its intended use or sale are complete.

- 11 -

*SGVFS026907*

ƒ Construction revenue and costs. The Company recognizes construction revenues and costs inaccordance with PAS 11, Construction Contracts. Given that the rehabilitation and constructionworks have been subcontracted to outside contractors (excluding the cost of some materials forsome contractors), the recognized construction revenue substantially approximates the relatedconstruction cost. Construction revenue recognized in the consolidated statements ofcomprehensive income amounted to P=19,344.3 million, P=16,799.1 million and P=12,130.5 millionfor the years ended December 31, 2017, 2016 and 2015, respectively. Construction costsrecognized in the consolidated statements of comprehensive income amounted toP=19,344.3 million, P=16,799.1 million and P=12,130.5 million for the years endedDecember 31, 2017, 2016 and 2015, respectively.

ƒ Provision for heavy maintenance. The Company also recognizes its contractual obligations torestore the toll roads to a specified level of serviceability. NLEX Corp and CIC recognizeprovision following PAS 37, Provisions, Contingent Liabilities and Contingent Assets as theobligation arises which is a consequence of the use of the toll roads and therefore it isproportional to the number of vehicles using the roads and increasing in measurable annualincrements. Provision for heavy maintenance amounted to P=402.4 million and P=433.4 million asat December 31, 2017 and 2016, respectively (see Note 16).

Lease Agreement Qualifying as Business Combination. The Company has assessed that the hospitallease agreements entered into by Colinas Verdes Hospital Managers Corp. (CVHMC), East ManilaHospital Managers Corp. (EMHMC) and Metro Pacific Zamboanga Hospital Corp. (MPZHC) meetthe definition of a business combination, particularly since CVHMHC, EMHMC and MPZHC haveobtained control over the operations and management of hospitals; hence, these lease agreementsqualify as acquisitions of businesses and were accounted for in accordance with PFRS 3, resulting inthe recognition of property use rights (see Notes 11 and 30).

Claims from the Grantor/s. Sizeable pending claims have accumulated for the Company’s water, tolland rail businesses:

ƒ Maynilad. Maynilad wrote the Philippine Government through the Department of Finance (DOF),to call on the undertaking after the MWSS and the RO’s delayed implementation of the decision ofthe Arbitral Award. Maynilad demanded that it be paid P=3.4 billion (subsequently adjusted toP=3.18 billion) in revenue losses that it had sustained as a direct result of the MWSS and the RO’srefusal to implement the correct Rebasing Adjustment from January 1, 2013 (the commencement ofthe 4th Rate Rebasing Period) to February 28, 2015. Revenue losses as a result of the delayed tariffincreases since 2013 amounted to P=11.4 billion as of December 31, 2017.

ƒ NLEX Corp and CIC. In August 2015, for failure to implement toll rate adjustments, NLEX Corpand CIC filed notices with the TRB and DOTC demanding settlement of the past due tariff increasesamounting to P=2.4 billion and P=719.0 million based on the overdue toll rate adjustments as atJuly 31, 2015 for the NLEX and CAVITEX, respectively. As at December 31, 2017, revenue lossesdue to delayed tariff increases is estimated at P=6.4 billion (VAT-exclusive; net of Government’sshare at P=6.0 billion) for the NLEX. NLEX Corp also filed with the TRB petition for toll rateadjustment for the SCTEX. Revenue losses due to delayed tariff increase amounted to P=1.9 billion(VAT exclusive; net of Government share at P=1.0 billion) as at December 31, 2017. Revenuelosses for the the CAVITEX is estimated at P=1.3 billion (VAT-exclusive and net of PRA’s share) asat December 31, 2017 (see Note 29).

- 12 -

*SGVFS026907*

ƒ LRMC. On various dates in 2015 through 2017, LRMC submitted letters to the DOTr representingits claim for costs incurred and estimated in relation to Existing System Requirement (ESR) andLight Rail Vehicle (LRV) shortfall on the premise of the Grantors’ obligation in relation to thecondition of the Existing System as at the Effective Date (September 12, 2015) fare deficit,Structural Defect Restoration (SDR) costs, and contractor and other additional costs incurred lessKey Performance Indicator (KPI) charges (see Notes 29 and 30).

As at December 31, 2017 and 2016, the consolidated financial statements do not include any adjustmentsfor the abovementioned claims pending outcome of the decision of the High Court of Singapore (forMaynilad’s claims) and the discussions with the Grantor/s (for claims of NLEX Corp, CIC and LRMC).

EstimatesThe key assumptions concerning the future and other key sources of estimation uncertainty at thereporting date, that have a significant risk of causing a material adjustment to the carrying amounts ofassets and liabilities within the next financial year, are described below. The Company based itsassumptions and estimates on parameters available when the consolidated financial statements wereprepared. Existing circumstances and assumptions about future developments, however, may change dueto market changes or circumstances arising beyond the control of the Company. Such changes arereflected in the assumptions when they occur.