Mergers and Acquisitions

46

Mergers and Acquisitions Chapter 21

-

Upload

zyra-liam-styles -

Category

Documents

-

view

111 -

download

2

description

finance

Transcript of Mergers and Acquisitions

Mergers and Acquisitions

Chapter 21

Definition of Terms:

• Merger – combination of two or more firms to form a single firm. (Relatively co-equal basis). Parent stock retired and new shares are issued.

• Acquisition – the purchase of one firm by another. Can be a controlling share, majority, or all of the target firm’s stock.

• Synergy – the whole is greater than the sum of its parts

• Synergistic Merger – Postmerger value > sum of separate companies’ premerger values. (Exxon-Mobil)

Reasons for engaging in Mergers:

• Synergy – Able to get more value than if the companies operate separately.

– Increased opportunity of managerial specialization

– Increased order size

• Tax Considerations – Profitable companies take advantage of tax savings from merged

companies that incur a loss.

• Purchase of Assets below Replacement Cost – If Replacement Cost > Market Value, firm is undervalued

• Diversification – Earnings stabilization can increase shareholder value.

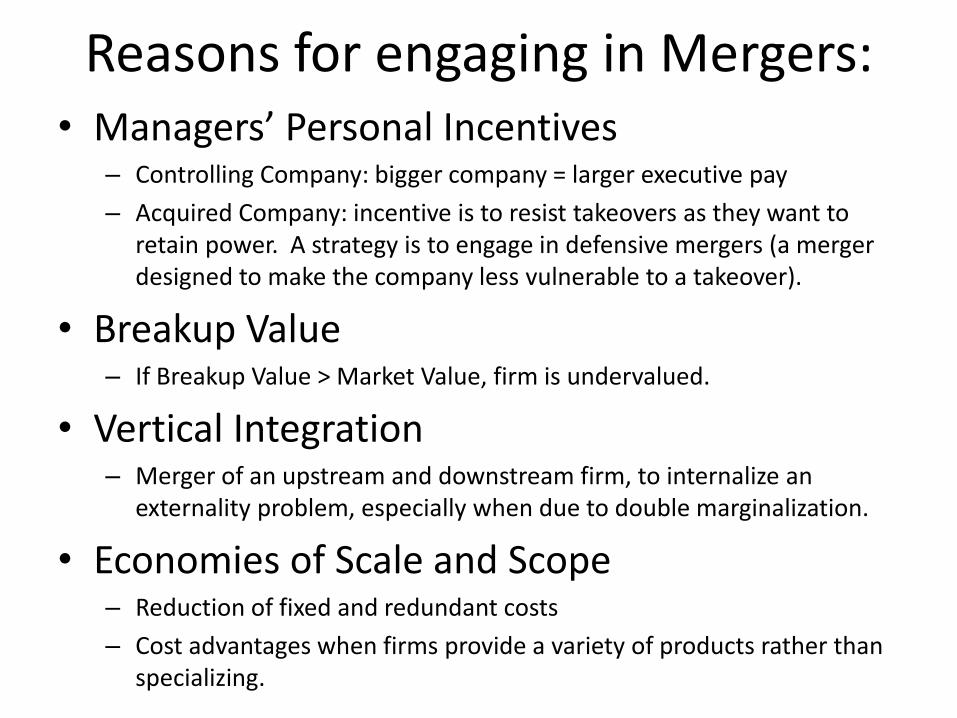

Reasons for engaging in Mergers: • Managers’ Personal Incentives

– Controlling Company: bigger company = larger executive pay

– Acquired Company: incentive is to resist takeovers as they want to retain power. A strategy is to engage in defensive mergers (a merger designed to make the company less vulnerable to a takeover).

• Breakup Value – If Breakup Value > Market Value, firm is undervalued.

• Vertical Integration – Merger of an upstream and downstream firm, to internalize an

externality problem, especially when due to double marginalization.

• Economies of Scale and Scope – Reduction of fixed and redundant costs

– Cost advantages when firms provide a variety of products rather than specializing.

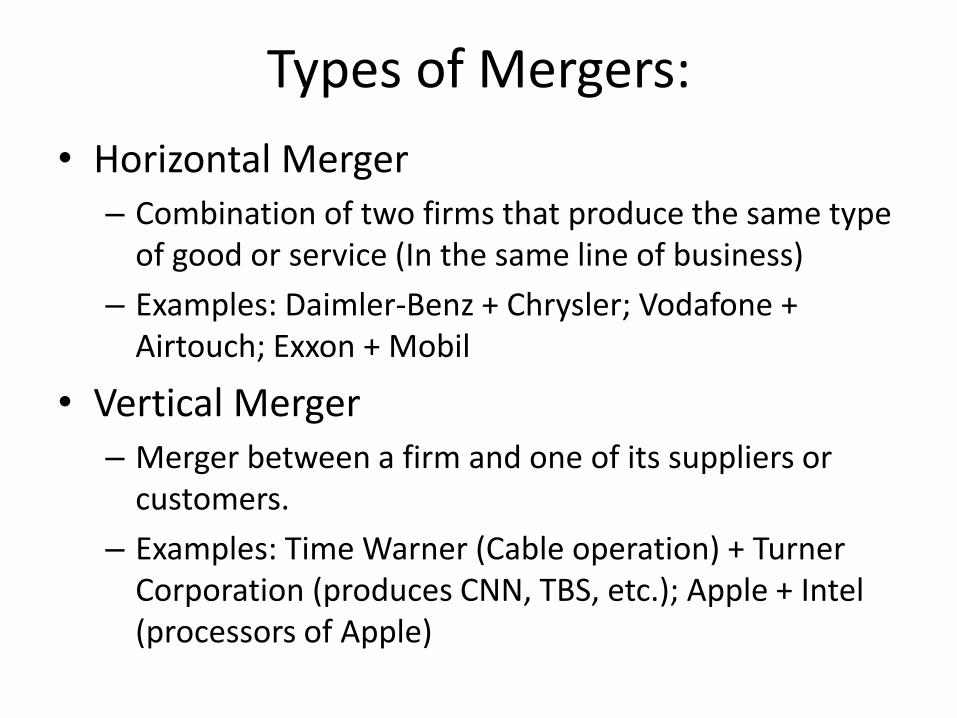

Types of Mergers:

• Horizontal Merger – Combination of two firms that produce the same type

of good or service (In the same line of business)

– Examples: Daimler-Benz + Chrysler; Vodafone + Airtouch; Exxon + Mobil

• Vertical Merger – Merger between a firm and one of its suppliers or

customers.

– Examples: Time Warner (Cable operation) + Turner Corporation (produces CNN, TBS, etc.); Apple + Intel (processors of Apple)

Types of Mergers:

• Congeneric Merger – Merger of firms in the same general industry, and

these firms do not have any customer or supplier relationship

– Examples: Citigroup’s Acquisition of Travelers Insurance; Prudential Financial (insurance) + Bache & Co. (Stocks)

• Conglomerate Merger – Merger of companies in totally different industries.

– Examples: Walt Disney + ABC; Kelso (Investment Company) + Nortek (home building products/systems)

Merger Waves

• Late 1800s = Oil, steel, tobacco, other basic industries

• 1920s = Stock market boom; utilities, communications, and autos

• 1960s = Conglomerate mergers

• 1980s = Junk bonds were used to finance acquisitions.

• Early 2000s = Strategic alliances to compete better.

• 2007 to present = Acquisitions done as stock price became undervalued because of the recent economic downturn

Hostile vs Friendly Takeover • Friendly Merger

– A merger whose terms are approved by the managements of both companies.

– Companies cooperate in negotiations

– Example: BDO + EPCI

• Hostile Merger – A merger in which the target firm’s management resists acquisitions.

– Takeover target is unwilling to be bought or the target’s board has no prior knowledge of the offer.

– Vodafone Airtouch + Mannesmann AG (exchange of shares between two corporations)

– Can be done through:

• Tender Offer (Buy stock from the stock market, frequently without the knowledge of target company’s management).

• Proxy Fight (Induce Simple Majority of SHs to change management)

Merger Regulation • Williams Act (1968)

– Objectives:

• Regulate the way acquiring firms structure takeover offers.

• Force acquiring firms to disclose more information about their offers.

– Restrictions on Acquiring Firms:

• Current holdings and future intentions must be disclosed within 10 days of amassing at least 5% of company stock.

• Source of funds must be disclosed.

• Target firm’s SHs must have at least 20 days to tender their shares (offer open at least 20 days)

• If acquirer increases offer price within the 20 day open period, all SHs who tendered before the new offer must receive the higher price.

Analysis of Mergers • To value a firm means to value the equity (buying from owners)

rather than the total value (not from creditors).

• Valuation Methods:

– Proactive Model: Discounted Cash Flow Approach (needs pro forma CF statements and discount rate)

– Reactive Models:

• Market Multiple Method (Multiples or Relative Valuation)

• Liquidation (Breakup Valuation)

• Classification of Mergers:

– Financial Merger

• Firms involved won’t be operated as a single unit (no expected synergies) and from which no operating economies are expected.

• Expected CFs = Incremental Post-Merger CFs

– Operating Merger

• Operations of the firms involved are integrated in hope of achieving synergistic benefits (there are expected synergies).

Equity Residual Method

Discounted Cash Flow Method - Precise

1. Forecast free cash flows

FCFE = Net Income + Non-cash items – Changes in NWC – Net CAPEX + Net Borrowings

2. Obtain a relevant discount rate

Use cost of equity, not WACC; ke = rfr + B (MRP)

3. Discount the forecast cash flows and sum to estimate the value of the target.

)1()1(

...)1(

)1( 1

2

2

1

10

tt

t

k

CF

k

CF

k

CF

k

CFV 1

0gk

CFV

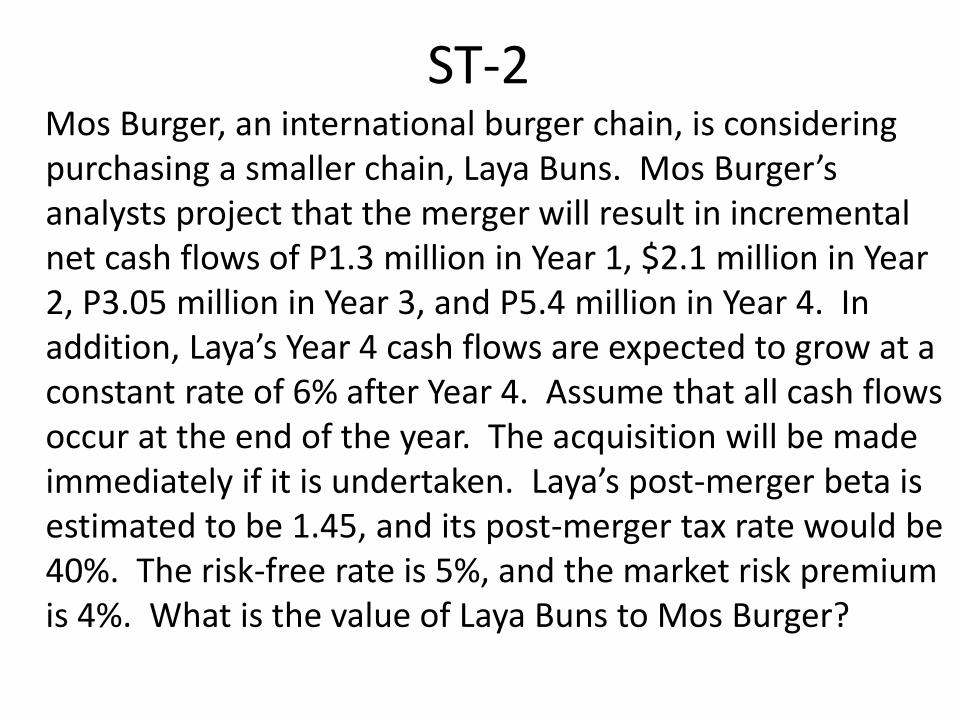

ST-2 Mos Burger, an international burger chain, is considering purchasing a smaller chain, Laya Buns. Mos Burger’s analysts project that the merger will result in incremental net cash flows of P1.3 million in Year 1, $2.1 million in Year 2, P3.05 million in Year 3, and P5.4 million in Year 4. In addition, Laya’s Year 4 cash flows are expected to grow at a constant rate of 6% after Year 4. Assume that all cash flows occur at the end of the year. The acquisition will be made immediately if it is undertaken. Laya’s post-merger beta is estimated to be 1.45, and its post-merger tax rate would be 40%. The risk-free rate is 5%, and the market risk premium is 4%. What is the value of Laya Buns to Mos Burger?

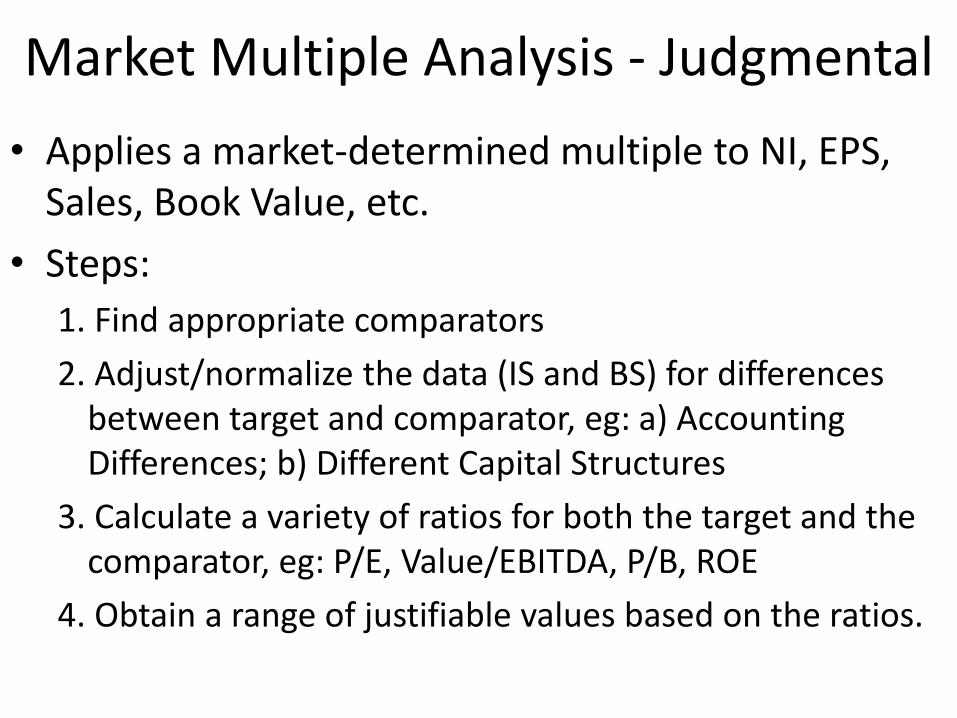

Market Multiple Analysis - Judgmental

• Applies a market-determined multiple to NI, EPS, Sales, Book Value, etc.

• Steps:

1. Find appropriate comparators

2. Adjust/normalize the data (IS and BS) for differences between target and comparator, eg: a) Accounting Differences; b) Different Capital Structures

3. Calculate a variety of ratios for both the target and the comparator, eg: P/E, Value/EBITDA, P/B, ROE

4. Obtain a range of justifiable values based on the ratios.

Graphical Analysis of Mergers

. . .

Change in SH Wealth

Price paid for Target

Acquirer Target

Equilibrium

MV or Current Price of Target

PV of FCF (DCF)

Synergy = Bargaining Range

Illustrative Short Problems: Tinghsin Corporation is interested in acquiring Weichun Corporation. Assume that risk free rate of interest is 5% and market risk premium is 6%.

•21-1 – Weichun currently expects to pay a year-end dividend of P2 a share. Van Buren’s dividend is expected to grow at a constant rate of 5% a year, and its beta is 0.9. What is the current price of Weichun’s stock?

•21-2 – Tinghsin estimates that if it acquires Weichun, the year-end dividend will remain at P2 a share, but synergies will enable the dividend to grow at a constant rate of 7 percent a year. Tinghsin also plans to increase the debt ratio of what would be its Weichun subsidiary – the effect of this would be to raise Weichun’s beta to 1.1. What is the per-share value of Weichun to Tinghsin Corporation?

•21-3 – On the basis of your answers to Problems 21-1 and 21-2, if Tinghsin were to acquire Weichun, what would be the range of possible prices that it could bid for each share of Weichun common stock?

Seatwork – By 2’s

• Cyclone Software Co. is the target of a takeover bid. Its current capital structure consists of 25% debt and 75% equity. After the merger, the firm is expected to use more debt. The risk free rate is 5% the MRP is 6%, and tax rate is 40%. Currently, Cyclone’s re = 14%, which is determined on the basis of CAPM. Assuming that year end dividend before and after change of capital structure and merger is expected to be 5, and growth rate before and after change in capital structure and merger is 3% and 7%, respectively:

– What would be Cyclone’s estimated ke if it were to change its capital structure from its present capital structure to 50% debt and 50% equity?

– What is the current price of the stock? (Immediately before the merger)

– What is the new price of the stock? (After the merger)

– What is the synergistic benefit if one can buy the stock using the current price of the stock immediately before the merger?

Issues that need to be resolved in Merger Analysis

• Price to be paid for the target firm

• Employment/Control Situation

– Buyout of Private Company – Owner/Manager of the acquired company would be interested to keep his high status position.

– Buyout of Public Company – Acquired firm’s manager will be worried about their postmerger positions

• Old management retained = Old Mgt would be willing to recommend its acceptance to the stockholders

• Old management removed = Old Mgt would probably resist the merger.

– Consolidation Merger (Equals) – What percentage of the ownership do each merger partner’s shareholders receive?

* Target may retain its identity (be a subsidiary) or it may be dissolved (one of the firm’s divisions).

Methods of Acquiring the Target Company

• Purchase of Target’s Assets

– Target firm is usually dissolved and no longer continues to exist as a separate legal entity.

– Simple acquisition of assets and not saddled with any hidden liabilities

– Common for small to medium sized firms.

• Purchase of Target’s Stocks

– Direct = Tender Offer (Hostile)

– Indirect = Through the BODs (Friendly)

– Acquiring firm is responsible for any legal contingencies against the target even those that have occurred prior to the takeover.

Payment Methods: • Cash

– Taxable Event

• Stock of Acquiring Firm

– “Mere Exchange” of stocks = Nontaxable Event = Nontaxable Offer

– Target SHs who receive shares of the acquiring company’s stock don’t have to pay taxes at the time of the merger. They pay taxes ONLY when they sell the stocks that were given to them in exchange AT A GAIN.

• Debt of the Acquiring Firm

– Taxable Event

• Combination of the Above.

Alternative Ways to Structure Takeover Bids:

• Taxes

• Securities Laws

Illustration: Book Value of Asset 100 Appraised Value 150 Offer Price 225

Taxable (Pay through Cash or Debt)

Target Firm pays tax on gain of 125m. Assuming 40% tax rate, Tax is 50m, thus only 75m is to be distributed to the target firm's shareholders.

Tax burden of target SHs would be high because they must still pay for individual taxes on any of their own gains.

Nontaxable (Pay through Stock)

Acquiring firm simply adds the 100m book value to its own assets and depreciate using their previous depreciation schedules

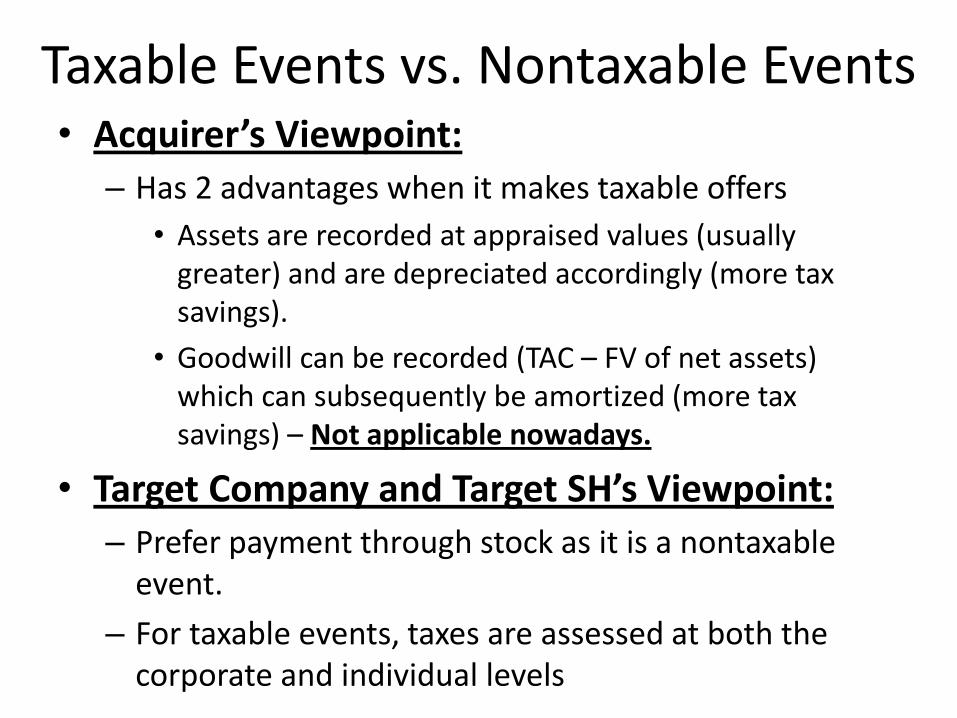

Taxable Events vs. Nontaxable Events • Acquirer’s Viewpoint:

– Has 2 advantages when it makes taxable offers

• Assets are recorded at appraised values (usually greater) and are depreciated accordingly (more tax savings).

• Goodwill can be recorded (TAC – FV of net assets) which can subsequently be amortized (more tax savings) – Not applicable nowadays.

• Target Company and Target SH’s Viewpoint:

– Prefer payment through stock as it is a nontaxable event.

– For taxable events, taxes are assessed at both the corporate and individual levels

Securities Laws

• Hostile Takeovers

– Nearly all hostile tender offers are for cash to expedite the process as the target may implement defensive tactics and other firms to make competing offers.

– 1968 Williams Act

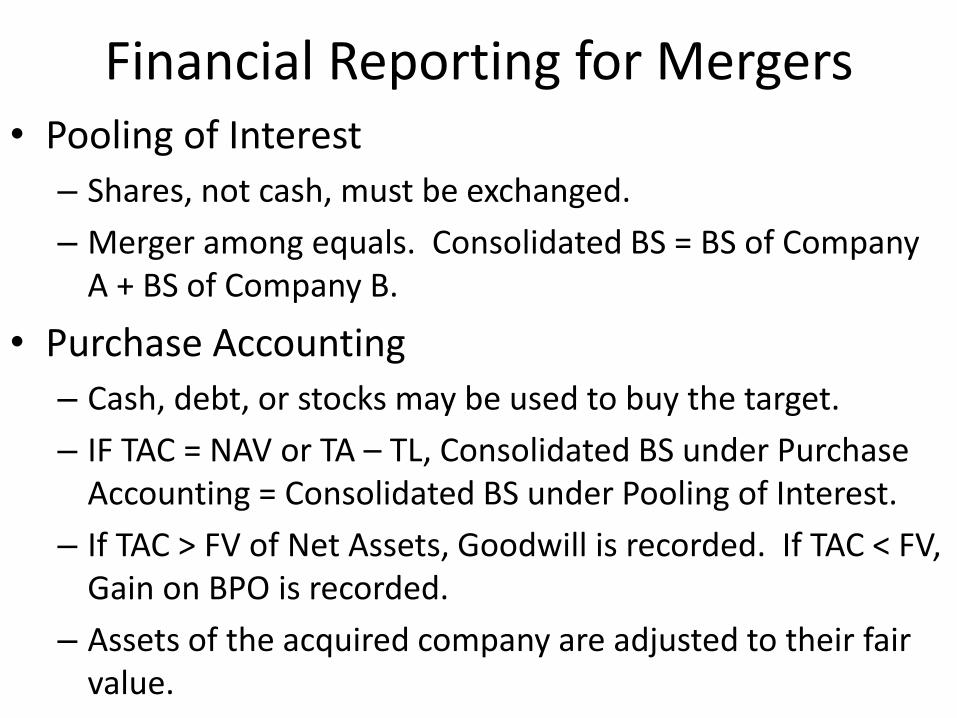

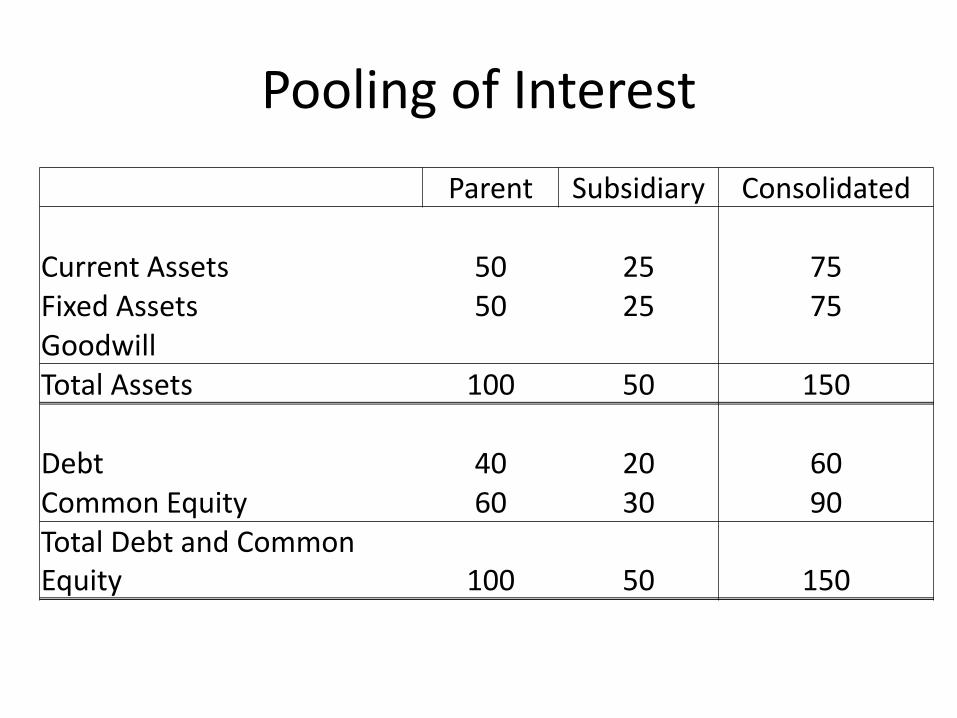

Financial Reporting for Mergers • Pooling of Interest

– Shares, not cash, must be exchanged.

– Merger among equals. Consolidated BS = BS of Company A + BS of Company B.

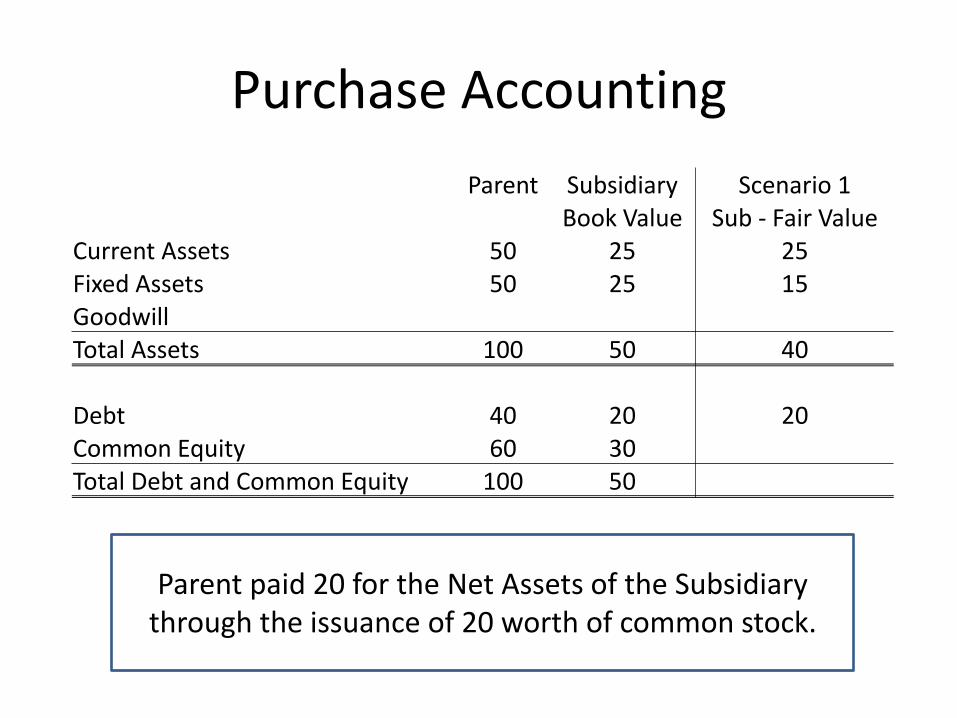

• Purchase Accounting

– Cash, debt, or stocks may be used to buy the target.

– IF TAC = NAV or TA – TL, Consolidated BS under Purchase Accounting = Consolidated BS under Pooling of Interest.

– If TAC > FV of Net Assets, Goodwill is recorded. If TAC < FV, Gain on BPO is recorded.

– Assets of the acquired company are adjusted to their fair value.

Pooling of Interest

Parent Subsidiary Consolidated Current Assets 50 25 75 Fixed Assets 50 25 75 Goodwill Total Assets 100 50 150 Debt 40 20 60 Common Equity 60 30 90 Total Debt and Common Equity 100 50 150

Purchase Accounting

Parent Subsidiary Scenario 1 Book Value Sub - Fair Value

Current Assets 50 25 25 Fixed Assets 50 25 15 Goodwill Total Assets 100 50 40

Debt 40 20 20 Common Equity 60 30 Total Debt and Common Equity 100 50

Parent paid 20 for the Net Assets of the Subsidiary through the issuance of 20 worth of common stock.

Purchase Accounting

Parent paid 30 for the Net Assets of the Subsidiary through the issuance of 30 worth of common stock.

Parent Subsidiary Scenario 2 Book Value Sub - FV

Current Assets 50 25 25 Fixed Assets 50 25 25 Goodwill Total Assets 100 50 50

Debt 40 20 20 Common Equity 60 30 Total Debt and Common Equity 100 50

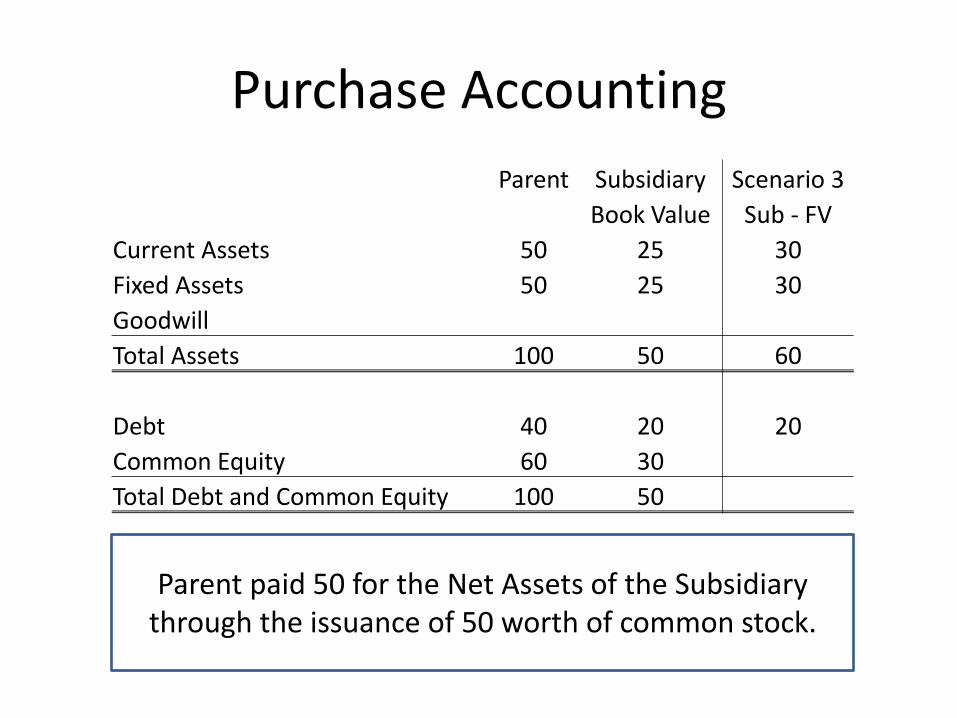

Purchase Accounting

Parent paid 50 for the Net Assets of the Subsidiary through the issuance of 50 worth of common stock.

Parent Subsidiary Scenario 3

Book Value Sub - FV

Current Assets 50 25 30

Fixed Assets 50 25 30

Goodwill

Total Assets 100 50 60

Debt 40 20 20

Common Equity 60 30

Total Debt and Common Equity 100 50

Income Statement Effects

• Increase in fixed assets = higher depreciation charge, decreases NI

• Increase in inventories = higher CGS, decreases NI

Analysis for “Merger of Equals”

• Develop consolidated pro forma financial statements

• Estimate the consolidated company’s new ke

• Decide allocation of consolidated stock between two sets of old shareholders.

• “Fair solution” – share using premerger proportions, if cannot pinpoint which company gives the synergistic benefit.

Role of Investment Bankers: • Arrange Mergers

– Match acquirers (w/ excess cash) with targets (undervalued firms)

– Illegal Parking Violation are sometimes committed by investment bankers.

• Develop Defensive Tactics – Help target firms to protect themselves against hostile takeovers

– Methods:

• Changing By-Laws

• Convince Target SHs that offer or bid price is too low.

• Raising antitrust issues (eg: Monopolies – Microsoft and Intuit)

• Stock repurchase to increase price of stock and discourage takeover. (Risk of greenmail)

• Getting a White Knight or a White Squire

• Sandbag

• Pac-Man

• People Pill, Poison/Suicide Pills, Macaroni Defense, Golden parachute

Role of Investment Bankers: • Establish Fair Value (Value Target Companies)

– Acquiring firm would want to know the lowest price it can buy the target’s stock

– Target firm may seek help in proving that price offered is too low.

• Finance Mergers

– When there is no excess cash

– Investment bankers must offer a financing package to clients in order for the M&A to be successful

• Invest in stocks of potential merger candidates

– Do Arbitrage Operations, specifically Risk Arbitrage.

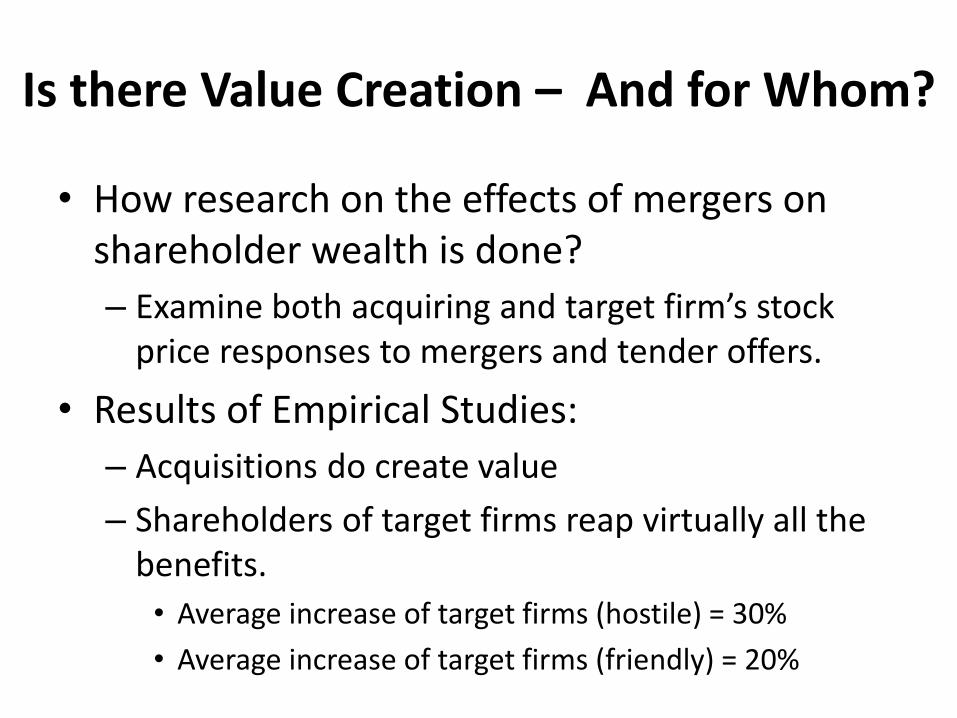

Is there Value Creation – And for Whom?

• How research on the effects of mergers on shareholder wealth is done?

– Examine both acquiring and target firm’s stock price responses to mergers and tender offers.

• Results of Empirical Studies:

– Acquisitions do create value

– Shareholders of target firms reap virtually all the benefits.

• Average increase of target firms (hostile) = 30%

• Average increase of target firms (friendly) = 20%

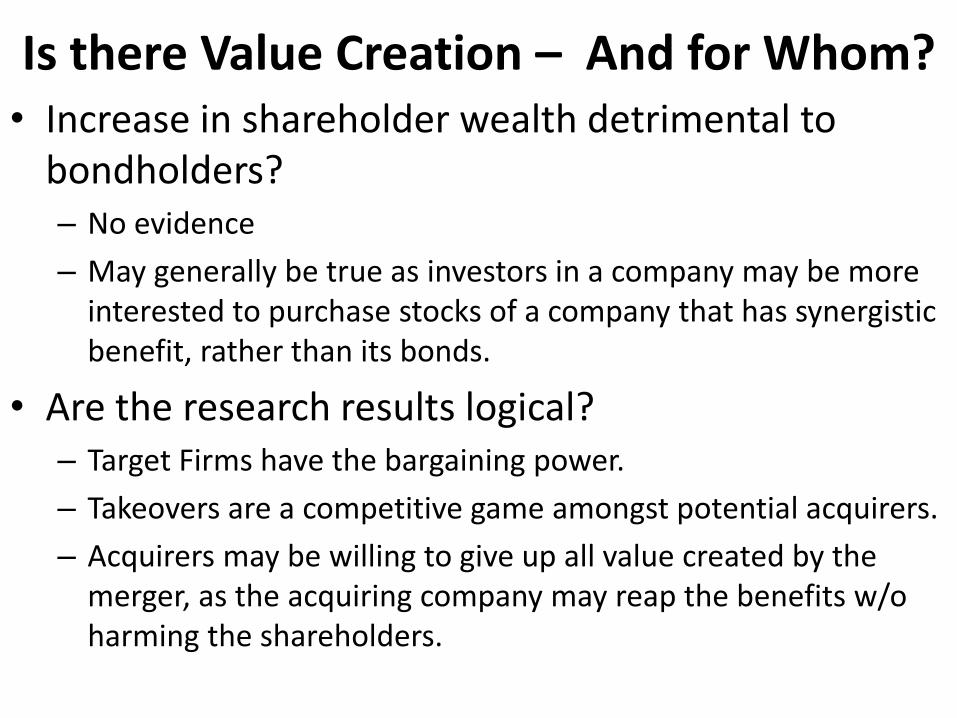

Is there Value Creation – And for Whom? • Increase in shareholder wealth detrimental to

bondholders? – No evidence

– May generally be true as investors in a company may be more interested to purchase stocks of a company that has synergistic benefit, rather than its bonds.

• Are the research results logical? – Target Firms have the bargaining power.

– Takeovers are a competitive game amongst potential acquirers.

– Acquirers may be willing to give up all value created by the merger, as the acquiring company may reap the benefits w/o harming the shareholders.

Percentage of M&A Deals Resulting in Failure

Source: Data derived from “Mergers: Why Most Big Deals Don’t Pay Off,” Business Week, October 14, 2002

Challenges of Postmerger Integration:

• Overestimating Synergies

• Customer Loss

• Employee Attrition

• Failure of Supplier Consolidation

• Inability to track key performance indicators, which could help executives identify problems earlier to keep earnings on track

• Slow and incomplete integration

Microsoft Stock Price

Yahoo Stock Price

Stock Price Effects Immediately after Offer Announcement:

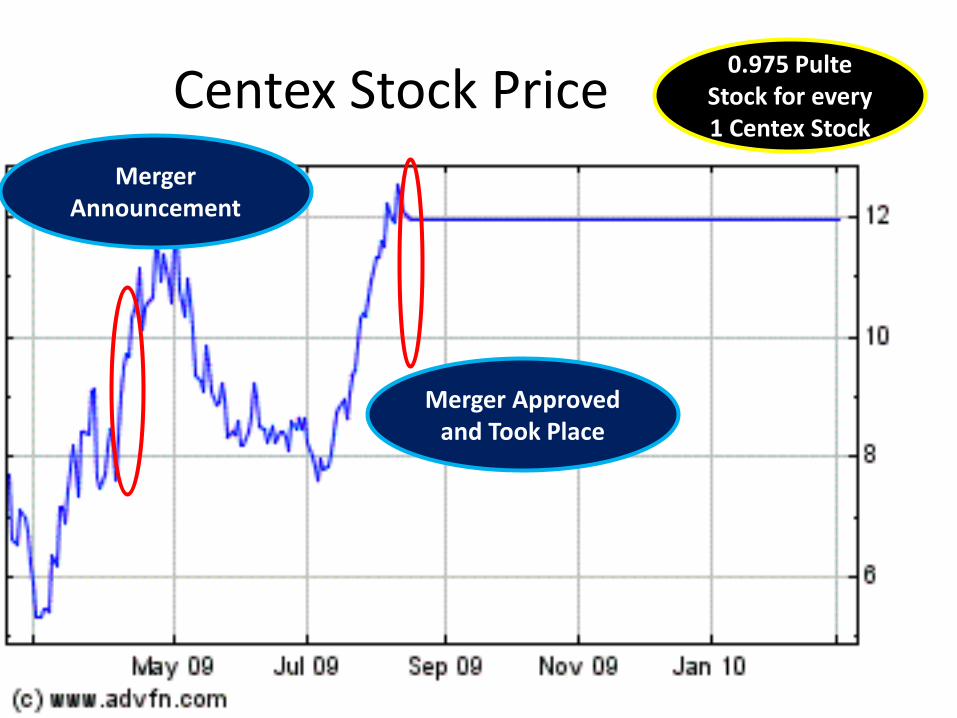

Pulte Stock Price

Merger Announcement

Merger Approved and Took Place

Centex Stock Price

Merger

Announcement

Merger Approved and Took Place

0.975 Pulte Stock for every 1 Centex Stock

Other Terms: • Corporate or Strategic Alliances

– A cooperative deal that stops short of a merger.

– Allows firms to create combinations that focus on specific business lines that offer the most potential synergies.

– Kinds of Strategic Alliances

• Joint Ventures- 2 or more independent companies combine their resources to achieve a specific limited objective (eg: Microsoft/Dreamworks)

• Vertical Alliances- relationships between organizations in different industries (Combine Expertise to finish a project).

• Horizontal Alliances- firms from the same industry (To achieve scale, adjust for seasonal changes, or handle niche areas of expertise) – Includes Joint marketing agreements.

• Administrative Alliances (To share functions, increase operational efficiency, and reduce costs)

– Eg: HA: Soho Soda, Regional Beer Company (excess bottles) and Brewer (distributor) Anheuser-Busch; VA: McDo and Oil Companies

Other Terms: • Leveraged Buyouts

– A small group of investors (usually includes the firm’s managers) borrows heavily (uses debt) to buy all the shares of a company

– Debt is paid through the sale of some of the firm’s assets and/or income generated by the company.

– Entails large amount of risk due to (leverage) debt taken to buy the company even if substantial profit is expected.

– Detrimental effect to bondholders – bond investment becomes less valuable as money generated by company is used to pay off the new debt.

– Eg: RJR-Nabisco

Other Terms: • Divestitures

– Opposite of Invest

– The sale of some of a company’s operating assets.

– Types of Divestitures:

• Sale of an operating unit to another firm.

• Spin-Off. Setting up the business to be divested as a separate corporation and then “spinning it off” to the divesting firm’s shareholders

• Carve-Out. Similar to spin-off but selling only some shares. Parent retains control of the subsidiary.

• Outright liquidation of assets. Assets are sold off piecemeal rather than as an operating entity.

Other Terms: • Divestitures

– Motivations for Divestitures:

• Firms are more comfortable in sticking with their niche.

• Cash is needed to finance expansion in their primary business lines

• Cash is needed to reduce a large debt burden.

• To unload losing assets that would otherwise drag the company down.

• Some businesses can operate more efficiently alone than together.

Problems in the Textbook:

• 21-4 Merger Analysis

• 21-5 Capital Budgeting Analysis