MEMO - wistaf.org · MEMO To: Foundation Board ... Denes Tobie . Nicholas Zales . From: ... Barb...

38

MEMO To: Foundation Board Members: Joel Bailey Mary Lynne Donohue Kristin Bergstrom Robert Zellers Lee Atterbury Grant E. Birtch Sarah Fry Bruch Hon. Thomas Eagon Kenneth Knutson N. Lynnette McNeely Kevin Palmershiem Hon. Gary Sherman Denes Tobie Nicholas Zales From: De Ette Tomlinson, Executive Director Date: June 11, 2013 Re: Materials for the Tuesday, June 18, 2013 WisTAF Board meeting The Wisconsin Trust Account Foundation Board of Directors will meet on: Tuesday, June 18, 2013 1:00 p.m. to 2:30 p.m. Board meeting 2:45 p.m. to 5:00 p.m. Betty Lou Cruise on Lake Monona (board members only – meet at the Machinery Row dock at 2:45 p.m.) Hall of Ideas Room G Monona Terrace 1 John Nolan Drive Madison, WI Board Meeting Materials Please find the following Board meeting materials online: • June 18, 2013 Board Materials Cover Memo (this document) • June 18, 2013 Board agenda • March 12, 2013 Unapproved Board Minutes • May 31, 2013 Balance Sheet • May 31, 2013 Monthly IOLTA income report • May 31, 2013 Budget vs. Actual • June 18, 2013 Executive Director Report • WisTAF Reserve Policy Proposal • Wisconsin Equal Justice Fund (WEJF) grant request letter • 2012 Draft Audit • 2012 Audit Management Representation Letter Betty Lou Cruise/Monona Terrace Information • Directions to Monona Terrace • Downtown Madison Parking

Transcript of MEMO - wistaf.org · MEMO To: Foundation Board ... Denes Tobie . Nicholas Zales . From: ... Barb...

MEMO To: Foundation Board Members:

Joel Bailey Mary Lynne Donohue Kristin Bergstrom Robert Zellers Lee Atterbury Grant E. Birtch Sarah Fry Bruch Hon. Thomas Eagon Kenneth Knutson N. Lynnette McNeely Kevin Palmershiem Hon. Gary Sherman Denes Tobie Nicholas Zales

From: De Ette Tomlinson, Executive Director Date: June 11, 2013 Re: Materials for the Tuesday, June 18, 2013 WisTAF Board meeting

The Wisconsin Trust Account Foundation Board of Directors will meet on:

Tuesday, June 18, 2013 1:00 p.m. to 2:30 p.m. Board meeting

2:45 p.m. to 5:00 p.m. Betty Lou Cruise on Lake Monona (board members only – meet at the Machinery Row dock at 2:45 p.m.)

Hall of Ideas Room G Monona Terrace

1 John Nolan Drive Madison, WI

Board Meeting Materials Please find the following Board meeting materials online: • June 18, 2013 Board Materials Cover Memo (this document) • June 18, 2013 Board agenda • March 12, 2013 Unapproved Board Minutes • May 31, 2013 Balance Sheet • May 31, 2013 Monthly IOLTA income report • May 31, 2013 Budget vs. Actual • June 18, 2013 Executive Director Report • WisTAF Reserve Policy Proposal • Wisconsin Equal Justice Fund (WEJF) grant request letter • 2012 Draft Audit • 2012 Audit Management Representation Letter Betty Lou Cruise/Monona Terrace Information

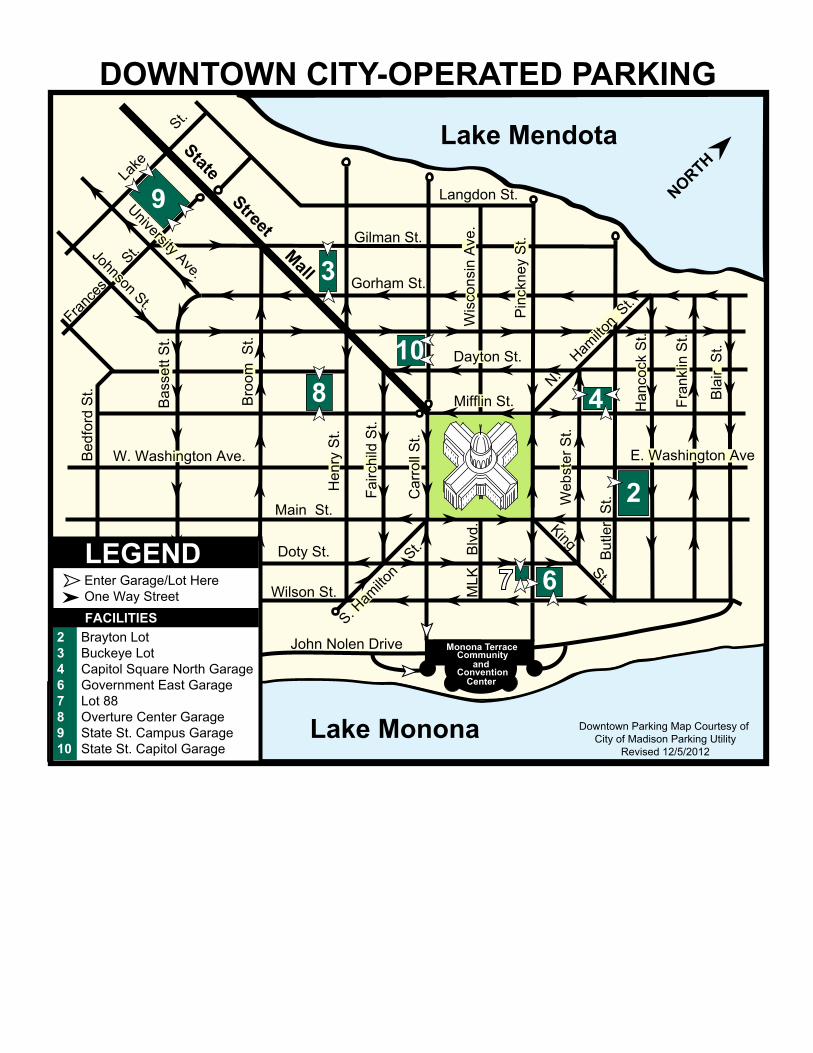

• Directions to Monona Terrace • Downtown Madison Parking

• Betty Lou Cruise Map • Betty Lou Cruise Brochure (if you'd like to know more about them)

For Your Records • October 17, 2012 Approved Board Minutes • Current WisTAF Board Contact List Teleconference option You are highly encouraged to attend the meeting in person. However, if you can’t, please use the following toll-free number to dial into the meeting: 1-866-244-8528. The passcode is: 579855. Information for the Betty Lou Cruise

1. Light refreshments will be available on the cruise courtesy of WisTAF. There will also be a cash bar.

2. Board members should meet at the Machinery Row dock at 2:45 p.m. to meet the captain and to receive safety instructions (please see the map in your board materials for information; for those of you attending the board meeting, Becky and De Ette will lead you on the short walk from the Monona Terrace to the Machinery Row dock).

3. Please wear comfortable clothing and shoes suitable for boating. A hat, sunglasses and sun-protection lotion are also suggested.

4. Betty Lou Cruises has asked us not to park in the Machinery Row parking lot, so you'll also find a map of public parking lots in your board materials. There is also parking available at the Monona Terrace. You may leave your car in the Monona Terrace lot during the cruise if you choose to park there.

If you have any questions, or need me to make any additional arrangements for you, please contact me toll-free at 1-877-749-5045 or in Madison at (608) 257-2841. Thank you!

825 Will iamson St., Suite A | Madison, WI 53703

phone: 608.257.6845 | tol l-free: 877.749.5045 | fax: 608.257.2684

email: [email protected] | www.wistaf.org

Wisconsin Trust Account Foundation Board of Directors Meeting Tuesday, June 18, 2013

1:00 p.m. to 2:30 p.m. Board meeting 2:45 p.m. to 5:00 p.m. Betty Lou Cruise on Lake Monona (board members only – meet at

the Machinery Row dock at 2:45 p.m.) Hall of Ideas Room G

Monona Terrace 1 John Nolan Drive

Madison, WI Teleconference information (WisTAF Board members only, please) Call-in phone number: (866) 244-8528 Access code: 579855

Agenda

I. Call to Order and Welcome II. Public Comments (10 minutes)

III. Approval of March 12, 2013 WisTAF Board meeting minutes – Bergstrom

IV. Officer/Committee Reports

1. President's Report – Bailey 2. Treasurer's Report/Finance & Investment Committee – Zellers 3. Grants/Evaluation Committee – Donohue 4. Personnel Committee – McNeely 5. Access to Justice Commission –Tomlinson 6. Executive Director's Report – Tomlinson

V. Old Business 1. WisTAF Reserve Policy – Zellers – ACTION

VI. New Business 1. Wisconsin Equal Justice Fund Grants – Donohue – ACTION 2. 2013 WisTAF Board Appointees – Bailey 3. Election of 2013-2014 Officers – Bailey – ACTION 4. Acceptance of 2012 Audit Findings – Zellers – ACTION 5. Recognitions – Bailey

VII. Adjournment Additional information:

1. Light refreshments will be available on the cruise courtesy of WisTAF. There will also be a cash bar.

2. Board members should meet at the Machinery Row dock at 2:45 p.m. to meet the captain and to receive safety instructions (please see the map in your board materials for information; for those of you attending the board meeting, Becky and De Ette will lead you on the short walk from the Monona Terrace to the Machinery Row dock).

3. Please wear comfortable clothing and shoes suitable for boating. A hat, sunglasses and sun-protection lotion are also suggested.

4. Betty Lou Cruises has asked us not to park in the Machinery Row parking lot, so you'll also find a map of public parking lots in your board materials. There is also parking available at the Monona Terrace. You may leave your car in the Monona Terrace lot during the cruise if you choose to park there.

1

WISCONSIN TRUST ACCOUNT FOUNDATION, INC.

Board of Directors Meeting State Bar of Wisconsin, Madison

March 12, 2013

DRAFT MINUTES

Attending in Person: Joel Bailey, President; Mary Lynne Donohue, Vice President; Robert Zellers, Treasurer; Kristin Bergstrom, Secretary; Grant Birtch; Hon. Thomas Eagon; Lynnette McNeely; Kevin Palmersheim. Also attending were De Ette Tomlinson, Executive Director; Rebecca Murray, Program Manager Attending via Teleconference: Lee Atterbury; Sally Bruch; Denes Tobie; Nick Zales Excused: Kenneth Knudson; Hon. Gary Sherman Guests: Jennifer Binkley, Community Justice, Inc.; Anne Daugherty-Leiter, AIDS Network; Barb Graham, Catholic Charities of the Archdiocese of Milwaukee; Bobby Peterson, ABC for Health Meeting Materials:

• March 12, 2013 Board Materials Cover Memo (this document) • March 12, 2013 Board agenda • October 17, 2012 Unapproved Board Minutes • December 31, 2012 Balance Sheet • December 31, 2012 Monthly IOLTA income report • December 31, 2012 Budget vs. Actual • March 12, 2013 Executive Director Report • 2013 Excess PILSF funds recommendation

I. Call to Order and Welcome

The meeting was called to order by President Bailey at 1:38 p.m. Introductions of Board members and guest attendees followed.

II. Public Comments None.

III. Approval of October 17, 2012 Board meeting minutes Upon a motion by Zellers/Birtch, the October 17, 2012 WisTAF Board meeting minutes were unanimously approved as presented.

2

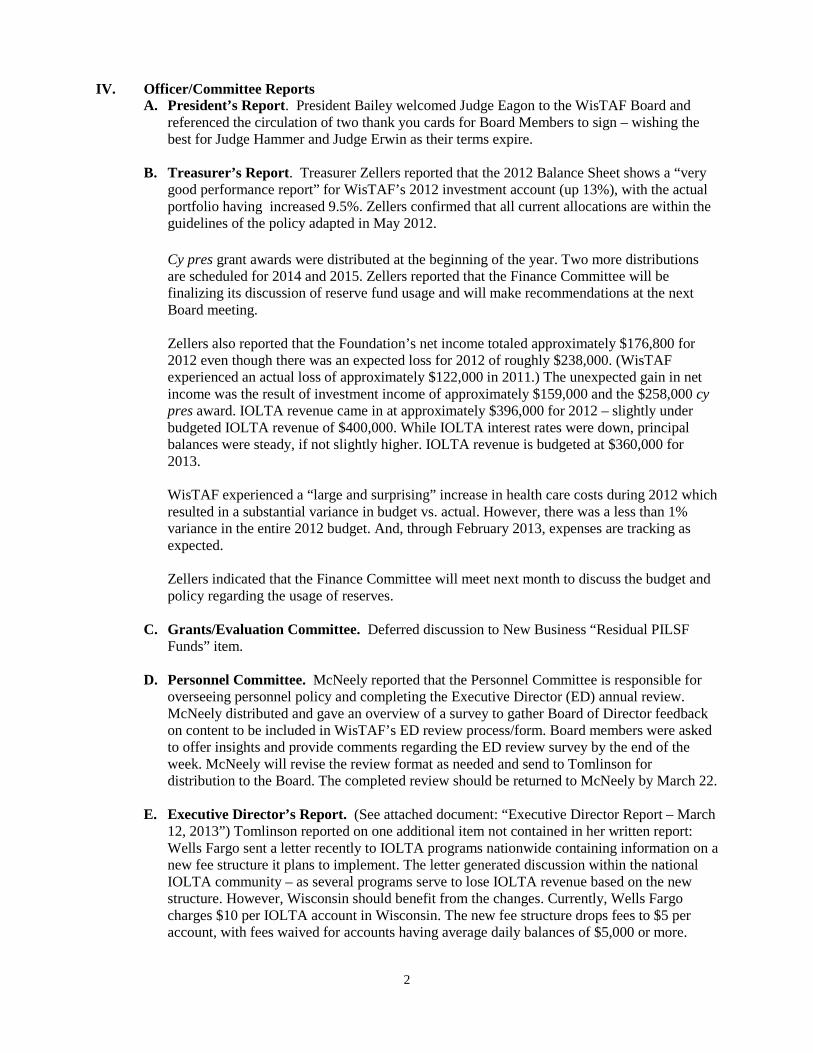

IV. Officer/Committee Reports A. President’s Report. President Bailey welcomed Judge Eagon to the WisTAF Board and

referenced the circulation of two thank you cards for Board Members to sign – wishing the best for Judge Hammer and Judge Erwin as their terms expire.

B. Treasurer’s Report. Treasurer Zellers reported that the 2012 Balance Sheet shows a “very good performance report” for WisTAF’s 2012 investment account (up 13%), with the actual portfolio having increased 9.5%. Zellers confirmed that all current allocations are within the guidelines of the policy adapted in May 2012.

Cy pres grant awards were distributed at the beginning of the year. Two more distributions are scheduled for 2014 and 2015. Zellers reported that the Finance Committee will be finalizing its discussion of reserve fund usage and will make recommendations at the next Board meeting. Zellers also reported that the Foundation’s net income totaled approximately $176,800 for 2012 even though there was an expected loss for 2012 of roughly $238,000. (WisTAF experienced an actual loss of approximately $122,000 in 2011.) The unexpected gain in net income was the result of investment income of approximately $159,000 and the $258,000 cy pres award. IOLTA revenue came in at approximately $396,000 for 2012 – slightly under budgeted IOLTA revenue of $400,000. While IOLTA interest rates were down, principal balances were steady, if not slightly higher. IOLTA revenue is budgeted at $360,000 for 2013. WisTAF experienced a “large and surprising” increase in health care costs during 2012 which resulted in a substantial variance in budget vs. actual. However, there was a less than 1% variance in the entire 2012 budget. And, through February 2013, expenses are tracking as expected. Zellers indicated that the Finance Committee will meet next month to discuss the budget and policy regarding the usage of reserves.

C. Grants/Evaluation Committee. Deferred discussion to New Business “Residual PILSF

Funds” item. D. Personnel Committee. McNeely reported that the Personnel Committee is responsible for

overseeing personnel policy and completing the Executive Director (ED) annual review. McNeely distributed and gave an overview of a survey to gather Board of Director feedback on content to be included in WisTAF’s ED review process/form. Board members were asked to offer insights and provide comments regarding the ED review survey by the end of the week. McNeely will revise the review format as needed and send to Tomlinson for distribution to the Board. The completed review should be returned to McNeely by March 22.

E. Executive Director’s Report. (See attached document: “Executive Director Report – March

12, 2013”) Tomlinson reported on one additional item not contained in her written report: Wells Fargo sent a letter recently to IOLTA programs nationwide containing information on a new fee structure it plans to implement. The letter generated discussion within the national IOLTA community – as several programs serve to lose IOLTA revenue based on the new structure. However, Wisconsin should benefit from the changes. Currently, Wells Fargo charges $10 per IOLTA account in Wisconsin. The new fee structure drops fees to $5 per account, with fees waived for accounts having average daily balances of $5,000 or more.

3

Tomlinson also reported that the 2013 compliance certification process is nearing completion. She will be making a phone call to the Vice President of one bank in particular that has not responded to numerous requests for compliance certification information. The bank currently has 517 IOLTA accounts that would be impacted by failure of the bank to cooperate with the certification process. Additionally, five banks need to respond with clarifications on product offerings, rates and fees. As part of her bank certification report, Tomlinson reported that one bank has formally left the Prime Partner program. While it still pays preferred rates, the bank does not want to be included in the list of Prime Partner financial institutions. Approximately 60% of IOLTA-participating banks waive all fees. Tomlinson also observed a spike in fees charged by BMO Harris. Upon follow-up, she learned that BMO had imposed a “legacy charge” on the M&I accounts it had acquired in its 2012 acquisition. (The legacy charge was a fee in lieu of minimum balance for those accounts). Going forward, BMO will waive all monthly fees, and will charge a fee in lieu of minimum balance for only one account. Birtch suggested that WisTAF’s list of Prime Partner banks be promoted more widely to Bar members. Tomlinson reported that since the 2008 economic crisis, four banks withdrew, merged, or were declared ineligible to participate in the IOLTA program in 2009. In 2010, this total rose to nine banks. Seven banks merged or withdrew from the program in both 2011 and 2012. WisTAF is continuing to see bank consolidations, with two so far in 2013.

V. Old Business. None. VI. New Business

A. 2013 Residual PILSF Funds Grants/Evaluation Committee Chair Donohue referenced the summary report included in the meeting materials and gave background on the distribution of residual PILSF funds. The budgeted PILSF revenue for 2013 of $890,000 was exceeded by approximately $30,000. In the past, WisTAF has distributed any excess PILSF funds to the two LSC agency grantees in Wisconsin (Legal Action of Wisconsin and Wisconsin Judicare, Inc.). The excess amounts have been relatively small and the timing of distributions has created efficiencies. Based on past practices, Tomlinson developed a proposal for distribution of the excess funds, however, the Board may choose to revise this practice. Donohue suggested the matter be discussed at the next G/E Committee meeting. Birtch offered a comment on behalf of the G/E Committee that the general consensus is that it is best practice to distribute the money statewide right now, rather than hold onto it until a future decision is made. Palmersheim stated that he would like to see the item added to the G/E Committee’s meeting agenda and expressed a concern that this practice could have the effect of undoing the decisions that were made at the G/E Committee level during deliberation of 2013 grant awards. He also pointed out that the amounts, while relatively small for some agencies, could be very significant for other smaller grantees.

4

Tomlinson stated that the development of more accurate revenue estimates during the budgeting process may also provide resolution to the issue.

Upon a motion by Donohue/Palmersheim, the 2013 PILSF grant amounts for Legal Action of Wisconsin and Wisconsin Judicare should be revised to the following: Legal Action of Wisconsin increased by $23,000 to a total 2013 PILSF grant of $426,400 and Wisconsin Judicare increased by $6,650 to a total 2013 PILSF grant of $113,850. Motion passed unanimously. After motion, Zellers suggested the G/E Committee consider including a line in its recommended grant amounts directing how excess PILSF funds should be distributed. Palmersheim concurred.

B. 2013 Financial Institution Certification Report. See Executive Director’s report.

C. Wisconsin Equal Justice Conference Report.

Tomlinson gave an overview of her panel presentation and referenced the “WisTAF Grants 2000 through 2013” chart. The chart is a good reflection on the current state of the banking industry in terms of the low interest rates being paid. The Access to Justice Commission made an effort to secure funding in the Governor’s 2013-15 Executive Budget for civil legal services. However, this appeal was denied. The Commission, with help from the Chief Justice, will make an appeal to the Joint Finance Committee for inclusion of civil legal services funding in the Legislative Budget. Birtch questioned the potential future of cy pres income and what WisTAF could expect. Tomlinson responded that there is a need for educating the judiciary and plaintiff/defense bar. Wisconsin typically has fewer class action suits filed than other states (for example, Illinois). Tomlinson does not view it as a stable source of future income for that reason. Last year’s cy pres revenue was the result of a national settlement secured by Washington State. Washington’s IOLTA program negotiated the distribution deal for IOLTA programs nationwide, based on the population of class members within each state. Donohue highlighted a piece of the “WisTAF Grants 2000 through 2013” chart indicating reserve fund usage for grants, and suggested that it will be a lively future topic for the G/E Committee and the Board of Directors as a whole. Tomlinson reported that Federal sequestration will impact Wisconsin’s LSC grantee agencies (Legal Action of Wisconsin and Wisconsin Judicare). The beginning of a series of cuts will begin next month, with a total potential cumulative cut in 2013 LSC agency funding of 7.4%. McNeely questioned whether cy pres awards resulted from last year’s Countrywide settlement (mortgage foreclosure settlement). Tomlinson responded that $30 million was awarded to the state of Wisconsin. The Access to Justice Commission unsuccessfully appealed to the Attorney General’s office to secure funds for civil legal service provision – with the exception of a $250,000 distribution for a law school program.

D. 2013 Site Visit Process Reminder

Murray informed Board members that the site visit scheduling process for 2012 grantees has begun. Any Board member wishing to visit a particular agency should contact Murray within the next week. Site visits will take place between April and June. Summary reports will be made available as part of the 2014 grant application review process.

5

VII. Adjournment

President Bailey adjourned the meeting at 3:05 p.m.

Next meeting: Tomlinson informed the Board that the next meeting will take place in mid-June and may be accompanied by a social activity.

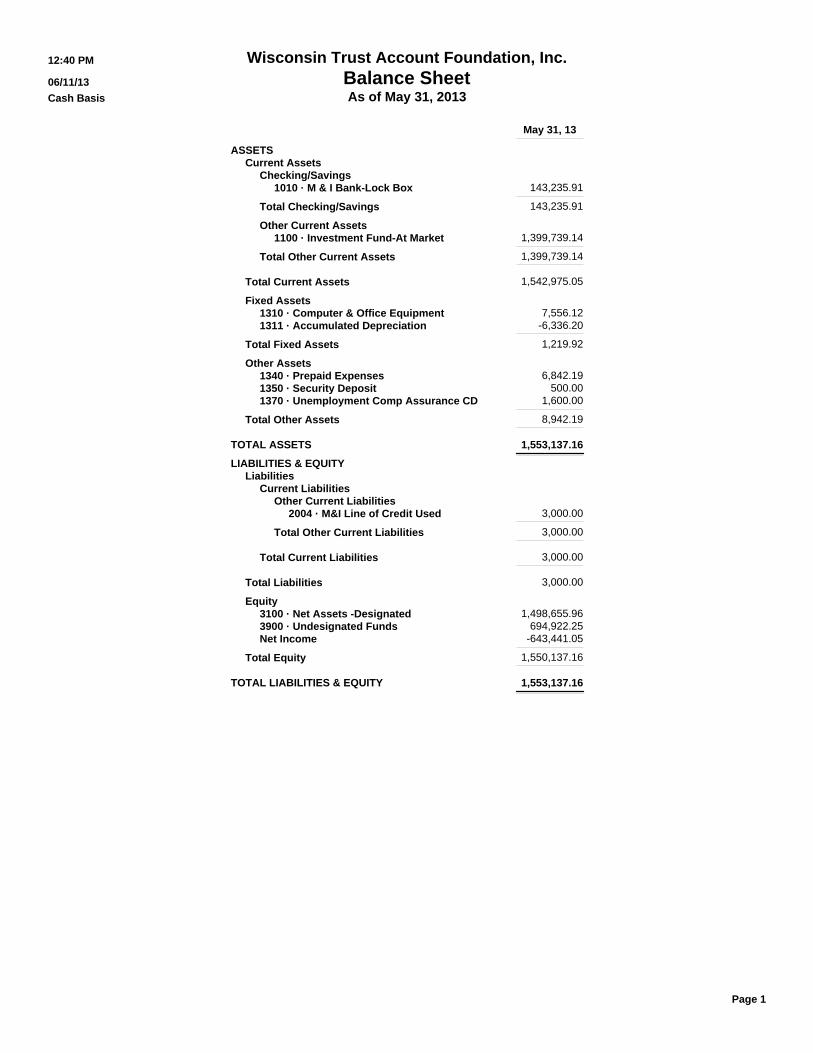

May 31, 13

ASSETSCurrent Assets

Checking/Savings1010 · M & I Bank-Lock Box 143,235.91

Total Checking/Savings 143,235.91

Other Current Assets1100 · Investment Fund-At Market 1,399,739.14

Total Other Current Assets 1,399,739.14

Total Current Assets 1,542,975.05

Fixed Assets1310 · Computer & Office Equipment 7,556.121311 · Accumulated Depreciation -6,336.20

Total Fixed Assets 1,219.92

Other Assets1340 · Prepaid Expenses 6,842.191350 · Security Deposit 500.001370 · Unemployment Comp Assurance CD 1,600.00

Total Other Assets 8,942.19

TOTAL ASSETS 1,553,137.16

LIABILITIES & EQUITYLiabilities

Current LiabilitiesOther Current Liabilities

2004 · M&I Line of Credit Used 3,000.00

Total Other Current Liabilities 3,000.00

Total Current Liabilities 3,000.00

Total Liabilities 3,000.00

Equity3100 · Net Assets -Designated 1,498,655.963900 · Undesignated Funds 694,922.25Net Income -643,441.05

Total Equity 1,550,137.16

TOTAL LIABILITIES & EQUITY 1,553,137.16

12:40 PM Wisconsin Trust Account Foundation, Inc.06/11/13 Balance SheetCash Basis As of May 31, 2013

Page 1

IOLTA REVENUE HISTORY 2005-2013

6/11/2013 Page 1

Month 2005 2006 2007 2008 2009 2010 2011 2012 2013

January 113,898 189,865 208,126 165,080 54,578 40,086 55,923 45,262 46,146 February 94,657 139,305 191,786 118,105 28,793 51,338 32,058 28,024 26,245 March 75,847 129,380 159,322 76,207 21,198 42,653 25,940 25,260 22,142

FIRST QUARTER 284,402 458,550 559,233 359,392 104,569 134,077 113,921 98,546 94,533

April 130,575 179,691 190,600 99,058 35,758 69,216 49,505 42,885 39,405 May 104,671 137,677 159,632 82,485 20,204 42,101 32,802 26,416 24,345 June 112,517 159,700 158,749 66,323 20,137 31,814 27,744 29,675

SECOND QUARTER 347,763 477,067 508,981 247,866 76,098 143,130 110,051 98,976 63,750

July 148,492 194,992 169,783 81,584 39,238 49,673 48,356 41,466 August 135,733 158,190 188,331 54,583 22,083 37,940 32,923 28,842 September 131,445 156,335 178,120 68,121 19,472 26,146 31,389 28,630

THIRD QUARTER 415,670 509,518 536,233 204,288 80,793 113,760 112,668 98,937 -

October 156,475 197,179 181,204 91,725 35,189 53,633 44,508 42,523 November 136,676 157,828 129,086 61,832 24,326 33,175 24,615 28,888 December 140,438 183,007 123,783 37,307 24,155 32,243 25,774 28,165

FOURTH QUARTER 433,590 538,014 434,073 190,864 83,670 119,051 94,897 99,576 -

FISCAL YEAR 1,481,425 1,983,149 2,038,520 1,002,409 345,130 510,019 431,536 396,036 158,283

SUM TOTAL 27,691,775 29,674,924 31,713,444 32,715,853 33,060,984 33,571,003 34,002,539 34,398,575 34,556,857

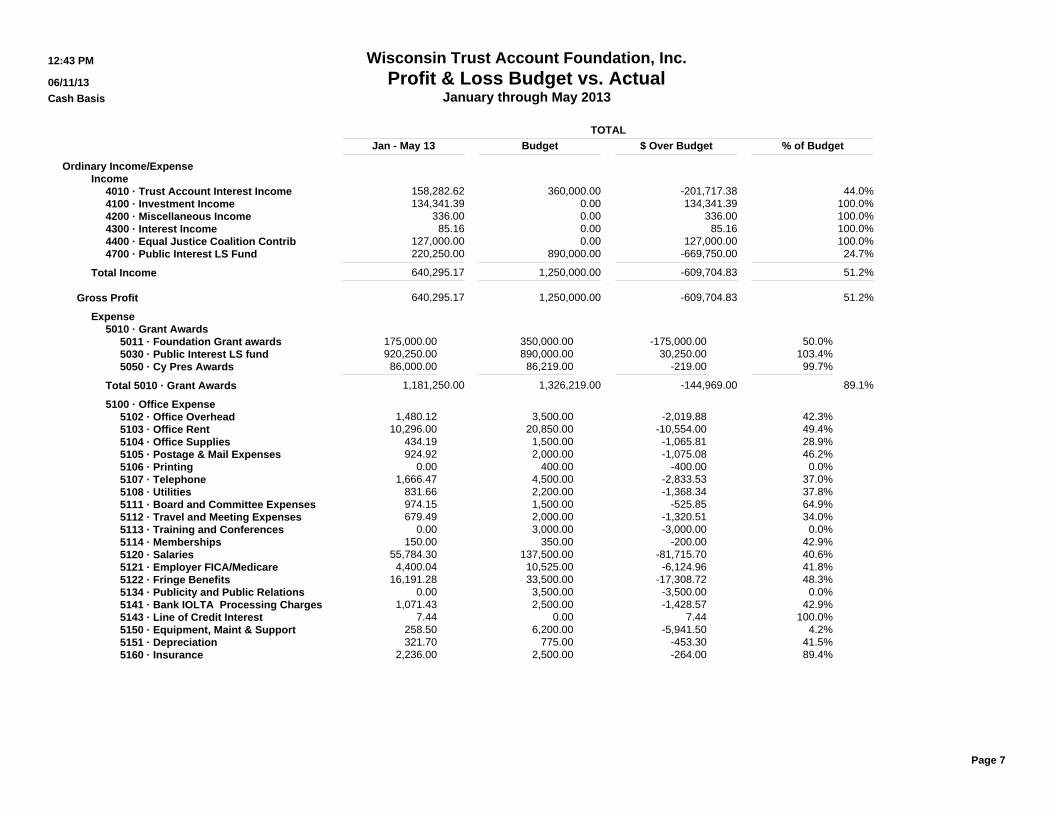

TOTALJan - May 13 Budget $ Over Budget % of Budget

Ordinary Income/ExpenseIncome

4010 · Trust Account Interest Income 158,282.62 360,000.00 -201,717.38 44.0%4100 · Investment Income 134,341.39 0.00 134,341.39 100.0%4200 · Miscellaneous Income 336.00 0.00 336.00 100.0%4300 · Interest Income 85.16 0.00 85.16 100.0%4400 · Equal Justice Coalition Contrib 127,000.00 0.00 127,000.00 100.0%4700 · Public Interest LS Fund 220,250.00 890,000.00 -669,750.00 24.7%

Total Income 640,295.17 1,250,000.00 -609,704.83 51.2%

Gross Profit 640,295.17 1,250,000.00 -609,704.83 51.2%

Expense5010 · Grant Awards

5011 · Foundation Grant awards 175,000.00 350,000.00 -175,000.00 50.0%5030 · Public Interest LS fund 920,250.00 890,000.00 30,250.00 103.4%5050 · Cy Pres Awards 86,000.00 86,219.00 -219.00 99.7%

Total 5010 · Grant Awards 1,181,250.00 1,326,219.00 -144,969.00 89.1%

5100 · Office Expense5102 · Office Overhead 1,480.12 3,500.00 -2,019.88 42.3%5103 · Office Rent 10,296.00 20,850.00 -10,554.00 49.4%5104 · Office Supplies 434.19 1,500.00 -1,065.81 28.9%5105 · Postage & Mail Expenses 924.92 2,000.00 -1,075.08 46.2%5106 · Printing 0.00 400.00 -400.00 0.0%5107 · Telephone 1,666.47 4,500.00 -2,833.53 37.0%5108 · Utilities 831.66 2,200.00 -1,368.34 37.8%5111 · Board and Committee Expenses 974.15 1,500.00 -525.85 64.9%5112 · Travel and Meeting Expenses 679.49 2,000.00 -1,320.51 34.0%5113 · Training and Conferences 0.00 3,000.00 -3,000.00 0.0%5114 · Memberships 150.00 350.00 -200.00 42.9%5120 · Salaries 55,784.30 137,500.00 -81,715.70 40.6%5121 · Employer FICA/Medicare 4,400.04 10,525.00 -6,124.96 41.8%5122 · Fringe Benefits 16,191.28 33,500.00 -17,308.72 48.3%5134 · Publicity and Public Relations 0.00 3,500.00 -3,500.00 0.0%5141 · Bank IOLTA Processing Charges 1,071.43 2,500.00 -1,428.57 42.9%5143 · Line of Credit Interest 7.44 0.00 7.44 100.0%5150 · Equipment, Maint & Support 258.50 6,200.00 -5,941.50 4.2%5151 · Depreciation 321.70 775.00 -453.30 41.5%5160 · Insurance 2,236.00 2,500.00 -264.00 89.4%

12:43 PM Wisconsin Trust Account Foundation, Inc.06/11/13 Profit & Loss Budget vs. ActualCash Basis January through May 2013

Page 7

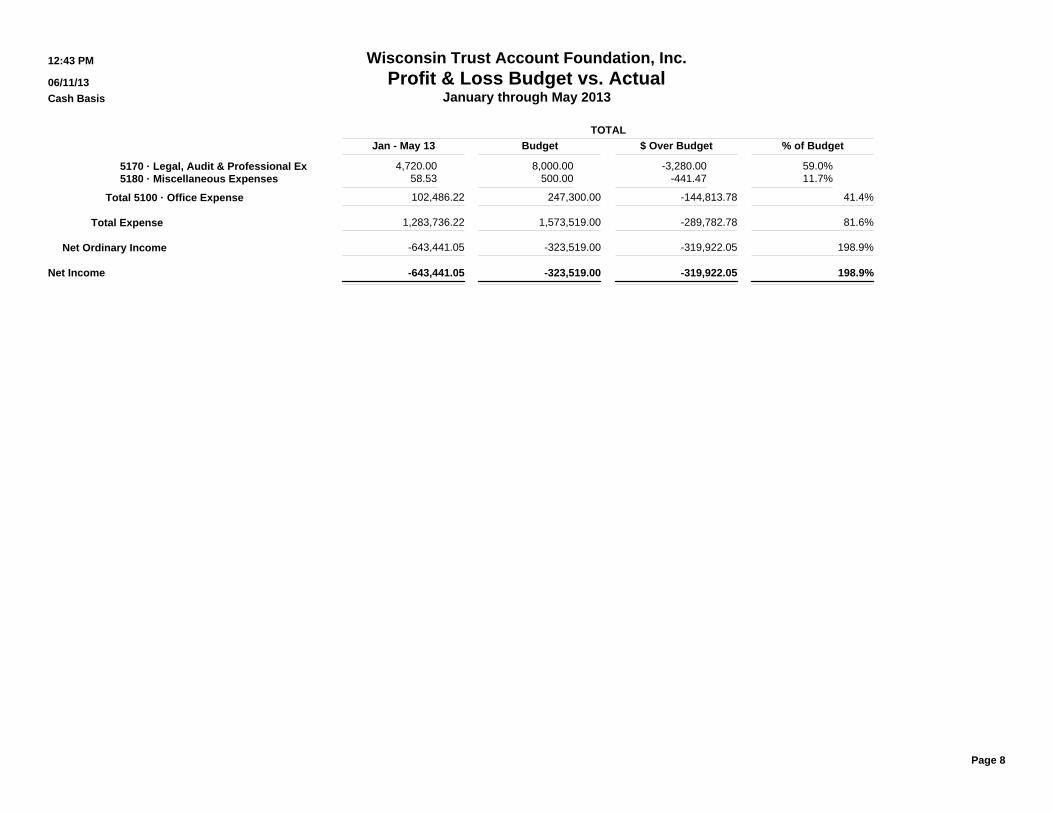

TOTALJan - May 13 Budget $ Over Budget % of Budget

5170 · Legal, Audit & Professional Ex 4,720.00 8,000.00 -3,280.00 59.0%5180 · Miscellaneous Expenses 58.53 500.00 -441.47 11.7%

Total 5100 · Office Expense 102,486.22 247,300.00 -144,813.78 41.4%

Total Expense 1,283,736.22 1,573,519.00 -289,782.78 81.6%

Net Ordinary Income -643,441.05 -323,519.00 -319,922.05 198.9%

Net Income -643,441.05 -323,519.00 -319,922.05 198.9%

12:43 PM Wisconsin Trust Account Foundation, Inc.06/11/13 Profit & Loss Budget vs. ActualCash Basis January through May 2013

Page 8

825 Will iamson St., Suite A | Madison, WI 53703

phone: 608.257.6845 | toll-free: 877.749.5045 | fax: 608.257.2684

email: [email protected] | www.wistaf.org

Wisconsin Trust Account Foundation

Executive Director Report June 18, 2013

General Overview The 2012 grant site visits have been going smoothly. My focus continues to be on banking, where I'm working with the Office of Lawyer Regulation (OLR) to evaluate a new type of bank product to see if it might be IOLTA-eligible, and part of a group to create potential trust account language to update Supreme Court Rule 20:1.15 (trust account rule) in order to address electronic banking. Finances No change on the national level. The Federal Reserve Board continues to hold the Federal Funds Rate (FFR) at the historically-low range of 0.00% to 0.25 %. They continue to indicate that they plan to hold the FFR at its present level through at least mid-2015, even if the economy improves, so that potential growth in the economy doesn't falter. Tehmina reports that, to date, 21 banks have lowered their rates since their January 2013 compliance certification. Three or four banks have increased their tiered rates, but the IOLTA accounts held there have low balances, so we haven't seen much of an increase of income from any of them. Sadly, the net result is that interest rates continued to fall through the first quarter of 2013 and into the second. As of December 31, 2012, the net interest rate was 0.1022%; as of May 31, 2013, it's fallen to 0.0821%. We've managed to address the increase we saw in fees in the last quarter of 2012, however, so our net difference from the first quarter 2012 income and the first quarter 2013 income was only about $4,000. Also, there seemed to be a gradual increase in principal balances held in IOLTA accounts throughout 2012, but they seem to have leveled off again in 2013. The encouraging news is that they haven't fallen, so I'm hoping it's just due to a slower economy in the first half of the year, and that we'll see the balances pick up again later in the year. The 2012 annual audit went smoothly. Bob Zellers will address this as an agenda item. He will also address the Finance Committee's work on drafting a new reserve policy proposal, which will be another agenda item at this meeting. Administration I'm sad to report that both efforts to reinstate state funding for low-income legal services into the state's 2013-2015 budget have failed. The Alliance efforts to reinstate funds 'as was' through the Department of Administration failed almost immediately, with no support from conservative members of the legislature, while the Access to Justice Commission's efforts to obtain funds for low-income domestic violence legal services seemed to have the

WisTAF ED Report – June 18, 2013 p. 3

conservative support needed to pass, but failed at the last minute when the conservative legislator who had indicated that he would introduce the language to the Joint Finance Committee decided not to. A second attempt was made by liberal legislators to introduce similar domestic violence services language into the Court's budget, but was defeated on a party line vote. Becky and I have been conducting site visits this quarter. We only have four visits left, two in Milwaukee and two up north. They're already scheduled, and I don't anticipate any difficulties will arise at any of the sites. There haven't been any surprises in any of the visits that we've conducted so far. Grantees seem to have adapted to the loss of the state appropriation funding, either by cutting back staff and/or services, or finding/developing new sources of income. Thank you so much to all of you who have attended site visits this year. I hope you've found them to be interesting. Banking issues continue to demand quite a bit of my time. Last meeting, I reported that I've been working with OLR to evaluate a new banking product to see if it's eligible for IOLTA accounts. We're still working on that, as well as continuing to work on drafting an update to the trust account rule to address electronic banking. We've had one bank failure this quarter – Bank of Kenosha was acquired by North Shore Bank. The acquisition seems to have gone smoothly. North Shore Bank is already one of our banks, so I've asked Tehmina to keep an eye out to make sure that all of the accounts that were formerly at the Bank of Kenosha show up on the North Shore Bank remittance report. Tehmina is working with OLR to update the account numbers on the acquired IOLTA accounts. OLR has reported that two other IOLTA banks have been listed by the FDIC as financially unstable, so we'll continue to watch to see what happens with them. I'd also like to welcome our newest Prime Partner: Commerce State Bank. If you received any bounce back emails in the past couple of weeks, it's because we closed the server for a few days while we dealt with a virus, in order to keep the banking data safe. Ironically, the virus came from a security update that we uploaded. The problem has been fixed and the system has checked out clean, so we're back on line. My apologies for any inconvenience it may have caused you. Becky has created a really lovely 2012 annual report, which she'll pass out at the board meeting, barring any unforeseen problems with the printer. Like last year, we're creating an electronic version of the report, and only printing 100 hard copies, primarily for marketing and contract fulfillment purposes. The majority of the report distribution will be done electronically. She also designed a full-page ad which will run in the June 2013 Wisconsin Lawyer, thanking all of our Prime Partner banking partners. Becky has also begun work on the 2014 grant application, and has submitted the draft version to our programmer to begin the webpage development for it. There are no major changes to the form planned, and she's reported that currently, she's on track to release the application on her projected July 8 timeline. Our tentative deadline for the

WisTAF ED Report – June 18, 2013 p. 3

application will be August 4. Becky will be contacting members of the Grants/Evaluation Committee with more information in the upcoming weeks. Outreach/Networking Disability Rights Wisconsin is still in the process of hiring a new executive director after Tom Massey's

resignation from the position. Joan Karan continues as Acting Executive Director. Office of Lawyer Regulation – As reported, I'm currently on a committee working to draft electronic banking

language for the trust account rule. Access to Justice Commission – I'm an ad hoc member of the Access to Justice's Research and Resource

Development Committee, which teleconferences monthly. Ongoing Issues

Public Interest Legal Service Fund issue/Keller compliance – There’s been no new information about Keller compliance. At this time, we are in full compliance with all Keller interpretations and requirements. Continuing to monitor.

New Income Initiatives Nothing at this time.

Reserve Policy (Proposed).

(This policy would replace the existing "Grant Reserve Policy: Determining Grant Levels" policy.)

WisTAF shall maintain a reserve account targeted to the sum of the following three components:

1. An IOLTA grants reserve. 2. An operating budget reserve. 3. A gifts reserve.

No reserve shall be maintained in connection with PILSF revenue nor related to any governmental appropriations as determined by the state budget. These sources of revenue to WisTAF shall be fully dedicated annually by the Board to grants.

Purpose of the Reserve.

The three components of the reserve serve three functions:

1. IOLTA grants reserve. The IOLTA grants reserve will be used to meet grant commitments during a fiscal year when the IOLTA income falls below budgeted projections or to provide grants as determined by the Board during a period of low IOLTA income.

2. The operating budget reserve will be used to fund WisTAF’s administrative budget for operations during a fiscal year when income falls below projections. The operating budget reserve may also be used to meet cash flow operating requirements during an annual budget cycle when a period of uneven cash income from IOLTA revenues occurs.

3. The gifts reserve will be used to temporarily maintain and invest the undistributed balance of gifts received by WisTAF. Such gifts may include but are not limited to Cy Pres awards, donations, corporate gifts, or other extraordinary income receipts. The gifts reserve balance may vary from zero upward depending upon the gifts received and the Board’s decisions regarding a suitable time frame for distributing those gifts.

Management of the Reserve.

The Reserve shall be invested and managed according to the WisTAF investment policy. The Board may engage an investment manager/advisor to oversee the reserve portfolio according to the terms of the investment policy.

Determination of Reserve Assets.

The following guidelines will be applied to calculate the amount of total reserves maintained by WisTAF.

IOLTA reserve. The amount of the IOLTA reserve shall be based upon a multiple of the annual grants budget as established by the Board. The level of reserve may vary between a multiple of one time and a maximum of three times the annual average of IOLTA grants made over the preceding three fiscal years. Normally, the Board will seek to maintain an IOLTA reserve equal to two times the annual average IOLTA grants level of the previous three years.

Operating budget reserve. The amount of the Operating budget reserve shall be based upon the annual operations budget for administering the Wistaf programs. The Operating budget reserve, as determined by the Board, will normally equal approximately one half of the current year’s operating budget.

Gifts reserve. The amount of the gifts reserve will equal the balance of gifts received less any distributed amounts, for those periods in which the Board determines to spread the distribution of gifts received over a period exceeding the year in which the gift is received. Normally the Board will seek to distribute the full amount of gifts received over a suitable period according to the size of the gift and the expressed wishes, if any, of the donor. WisTAF does not intend to maintain any permanent or ongoing reserve for gifts received.

Regardless of the above guidelines, the final determination of any reserve levels maintained by WisTAF remains solely with the Board at its discretion. The Board also retains discretion to apply reserve assets across the three categories.

Distributions from the Reserve.

IOLTA reserve. The IOLTA reserve is expected to be the greatest variable within the three tiers of reserve assets. When the amount in the IOLTA reserve exceeds its target level as described above, the Executive Director and/or the Finance Committee shall notify the Board of said excess. The Board shall then determine the use of such excess. The Board in its discretion can decide to maintain the excess reserve for a time, distribute such excess as part of that year’s grants cycle, or deploy the excess for some other purpose in accordance with the mandate under which WisTAF operates.

Operating budget reserve. Although the operating budget reserve is normally maintained at a level equal to one half of the current year’s administrative operating budget, the Board in its sole discretion may apply a greater or lesser level of operating reserve. If such a change is undertaken by the Board, then it shall also determine how to distribute any excess created thereby or accumulate any deficiency created by its decisions.

Gifts reserve. When the Board receives any gifts, donations, or other extraordinary revenue from outside its normal sources of income, it shall reach a determination as to how those gifts shall be distributed. If the time period of the distributions exceeds the current year in which the gift is received, then the balance of the gift shall be added to the reserves account and held until the time of planned distribution according to the schedule determined by the Board. If the distribution period bridges more than one fiscal year but is less than 12 months in total, then WisTAF administration may hold the gift in a depository account as a segregated portion of the reserve portfolio in order to shelter the upcoming distribution from market fluctuations.

Additions to the Reserve.

In those years when WisTAF revenue, primarily IOLTA revenue, exceeds the IOLTA grants and related expenses budgeted and planned for that year, the Board shall give priority to replenishing the reserve

balance to its targeted level or within its range if the reserve level is below the targeted amount, or if the Board expects a significant change in IOLTA revenue in the following year, or if the Board wishes to temporarily carry an excess reserve into the following year for the purpose of increasing that year’s grants.

Although the WisTAF Board will generally follow the reserve policies as stated above, it may in its sole discretion deviate from these policies in order to achieve its mandate or to follow any laws, statutes and/or regulations which may apply to WisTAF.

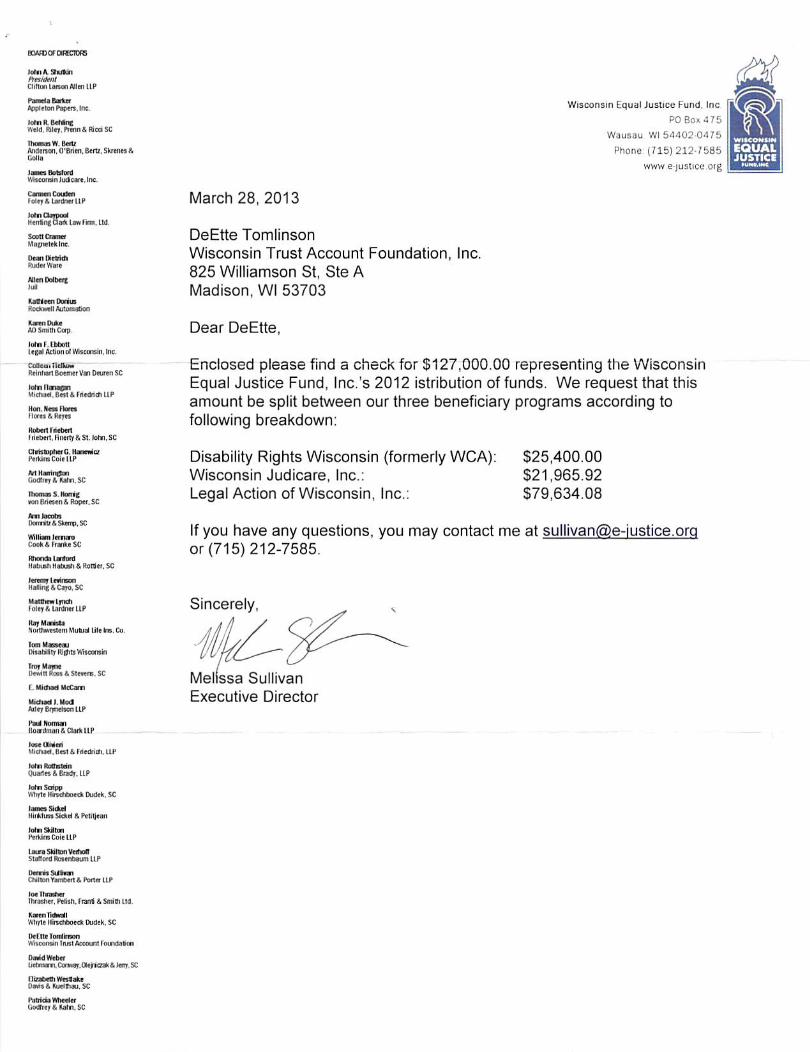

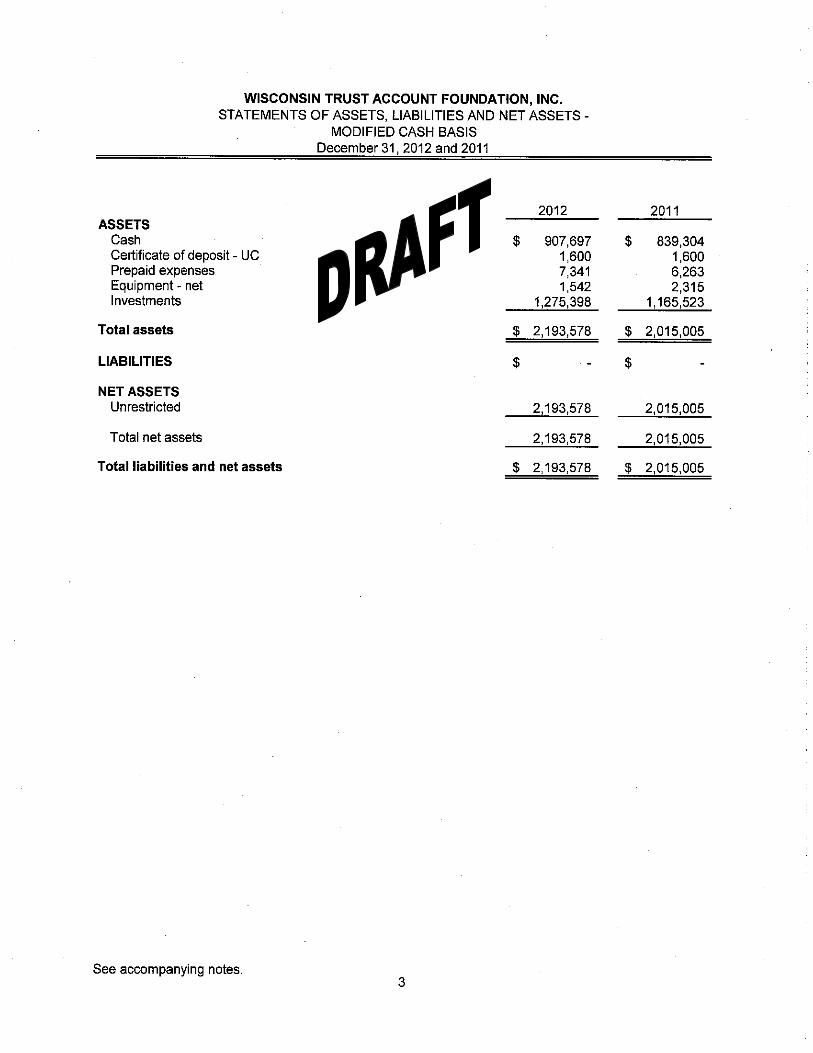

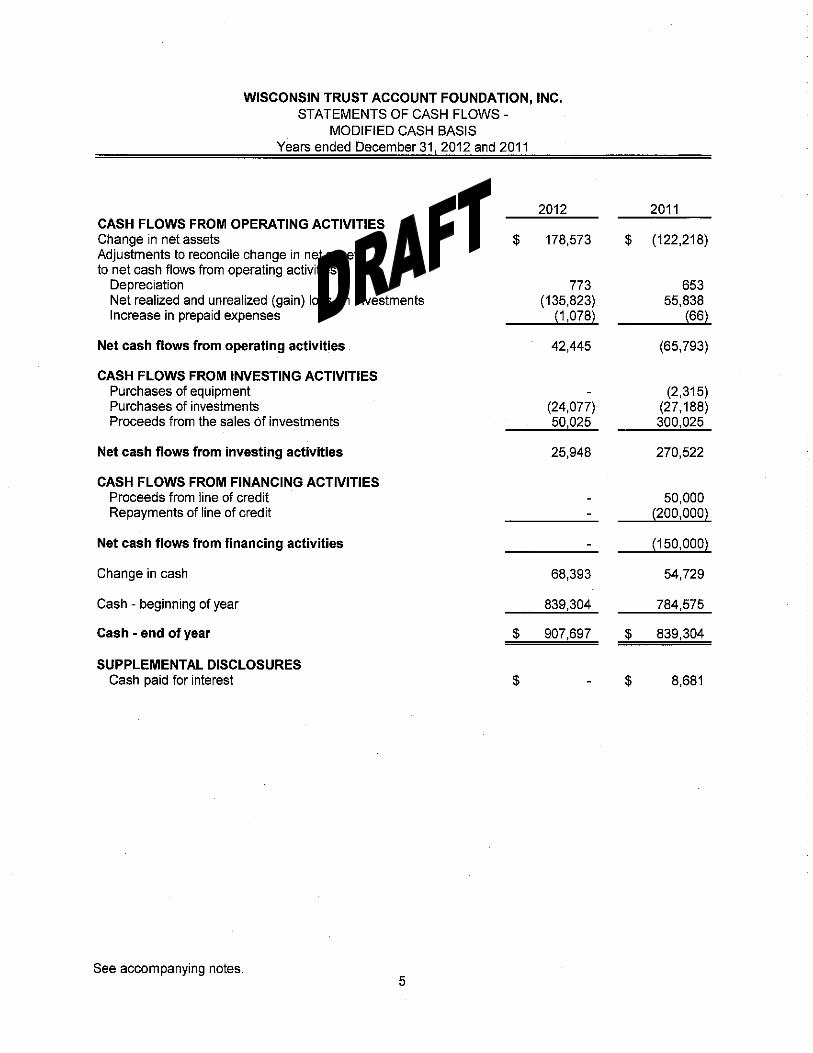

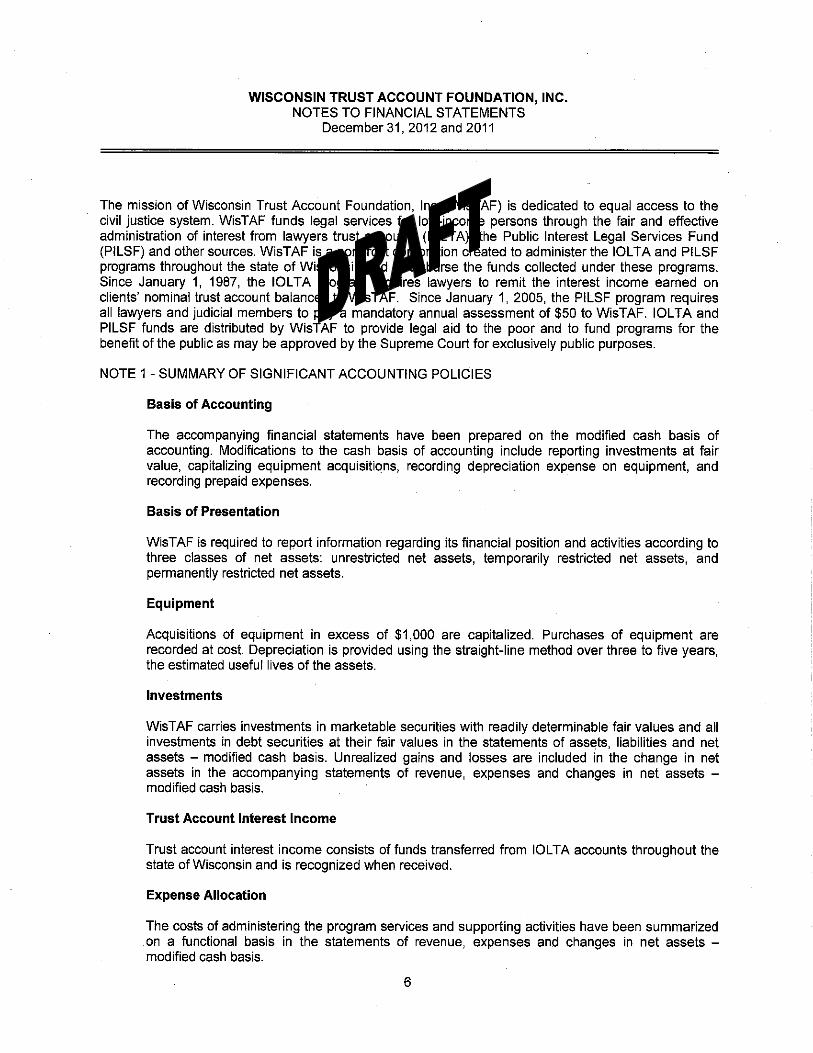

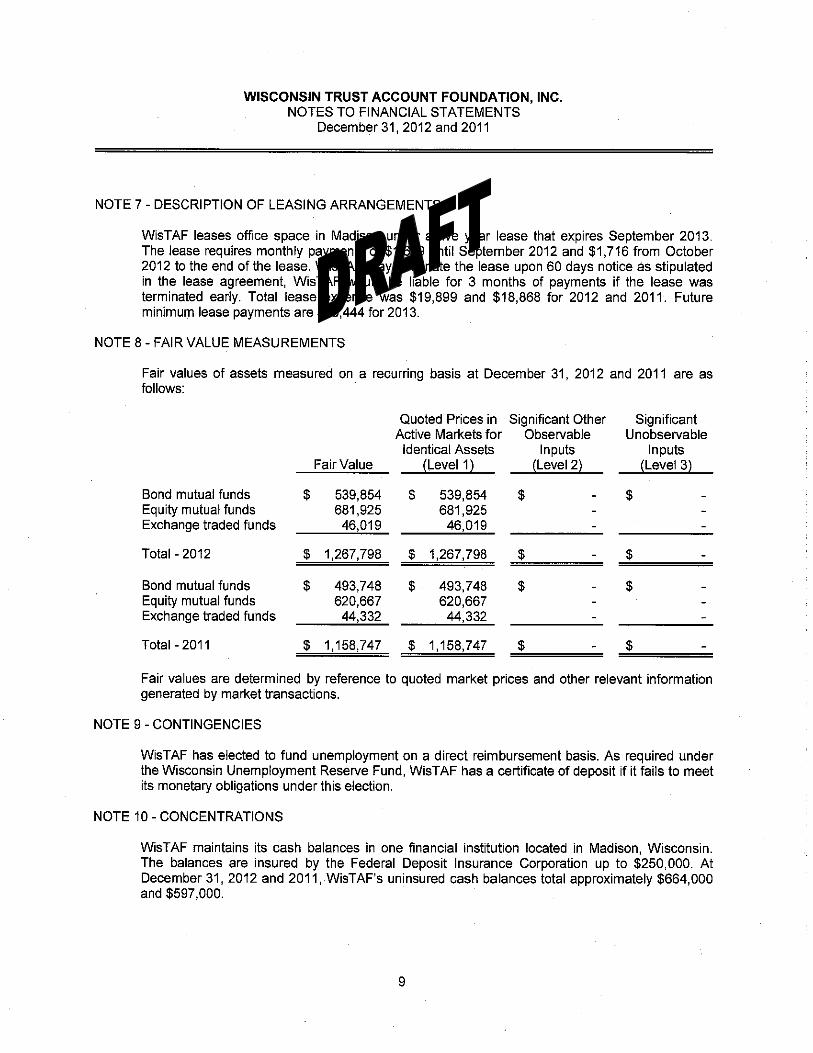

April 22, 2013 To Wegner CPAs, LLP This representation letter is provided in connection with your audits of the financial statements of Wisconsin Trust Account Foundation, Inc., which comprise the statements of assets, liabilities and net assets – modified cash basis as of December 31, 2012 and 2011, and the related statements of revenue, expenses and changes in net assets – modified cash basis and cash flows – modified cash basis for the years then ended, and the related notes to the financial statements, for the purpose of expressing an opinion as to whether the financial statements are presented fairly, in all material respects, in accordance with the modified cash basis of accounting. Certain representations in this letter are described as being limited to matters that are material. Items are considered material, regardless of size, if they involve an omission or misstatement of accounting information that, in light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would be changed or influenced by the omission or misstatement. An omission or misstatement that is monetarily small in amount could be considered material as a result of qualitative factors. We confirm, to the best of our knowledge and belief, as of April 22, 2013, the following representations made to you during your audits. Financial Statements

• We have fulfilled our responsibilities, as set out in the terms of the audit engagement letter dated January 2, 2013.

• The financial statements referred to above are fairly presented on the modified cash basis of accounting.

• We acknowledge our responsibility for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

• We acknowledge our responsibility for the design, implementation, and maintenance of internal control to prevent and detect fraud.

• Significant assumptions we used in making accounting estimates, including those measured at fair value, are reasonable.

• Related party relationships and transactions have been appropriately accounted for and disclosed in accordance with the modified cash basis of accounting.

• All events subsequent to the date of the financial statements and for which the modified cash basis of accounting requires adjustment or disclosure have been adjusted or disclosed.

• We are in agreement with the adjusting journal entries you have proposed, and they have been posted to WisTAF’s accounts.

• The effects of all known actual or possible litigation, claims, and assessments have been accounted for and disclosed in accordance with the modified cash basis of accounting.

• Material concentrations have been appropriately disclosed in accordance with the modified cash basis of accounting.

• Guarantees, whether written or oral, under which WisTAF is contingently liable, have been properly recorded or disclosed in accordance with the modified cash basis of accounting.

• As part of your audit, you prepared the draft financial statements and related notes and supplementary information. We have designated an individual with suitable skill, knowledge, or experience to oversee your services and have made all management decisions and performed all management functions. We have reviewed, approved, and accepted responsibility for those financial statements and related notes and supplementary information.

Information Provided

• We have provided you with:

• Access to all information, of which we are aware, that is relevant to the preparation and fair presentation of the financial statements, such as records, documentation, and other matters.

• Additional information that you have requested from us for the purpose of the audit.

• Unrestricted access to persons within the entity from whom you determined it necessary to obtain audit evidence.

• All material transactions have been recorded in the accounting records and are reflected in the financial statements.

• We have disclosed to you the results of our assessment of the risk that the financial statements may be materially misstated as a result of fraud.

• We have no knowledge of any fraud or suspected fraud that affects WisTAF and involves:

• Management,

• Employees who have significant roles in internal control, or

• Others where the fraud could have a material effect on the financial statements.

• We have no knowledge of any allegations of fraud or suspected fraud affecting WisTAF’s financial statements communicated by employees, former employees, grantors, regulators, or others.

• We have disclosed to you all known instances of noncompliance or suspected noncompliance with laws and regulations whose effects should be considered when preparing financial statements.

• We are not aware of any pending or threatened litigation, claims, or assessments or unasserted claims or assessments that are required to be accrued or disclosed in the financial statements, and we have not consulted a lawyer concerning litigation, claims, or assessments.

• We have disclosed to you the identity of WisTAF’s related parties and all the related party relationships and transactions of which we are aware.

• WisTAF has satisfactory title to all owned assets, and there are no liens or encumbrances on such assets nor has any asset been pledged as collateral except as made known to you and disclosed in the notes to the financial statements.

• We are responsible for compliance with the laws, regulations, and provisions of contracts and grant agreements applicable to us; and we have identified and disclosed to you all laws, regulations and provisions of contracts and grant agreements that we believe have a direct and material effect on the determination of financial statement amounts or other financial data significant to the audit objectives.

• Wisconsin Trust Account Foundation, Inc. is an exempt organization under Section 501(c)(3) of the Internal Revenue Code. Any activities of which we are aware that would jeopardize WisTAF’s tax-exempt status, and all activities subject to tax on unrelated business income or excise or other tax, have been disclosed to you. All required filings with tax authorities are up-to-date.

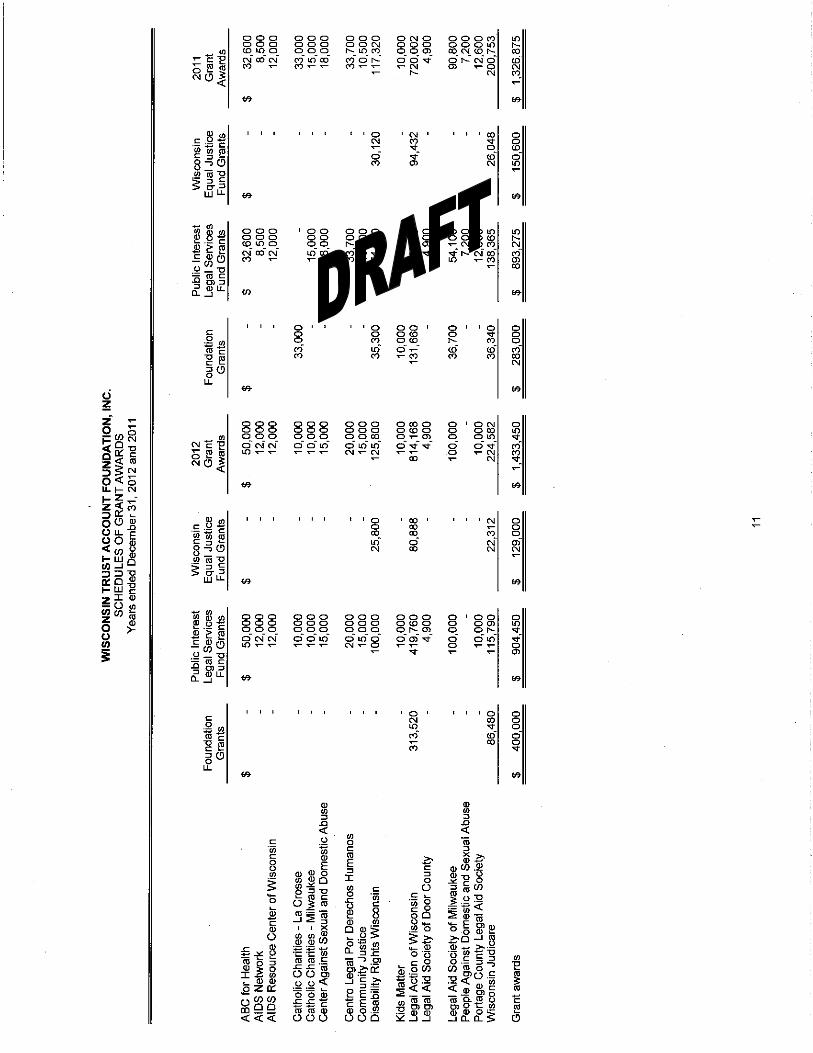

• We acknowledge our responsibility for presenting the schedules of functional expenses and grant awards in accordance with the modified cash basis of accounting, and we believe the schedules of functional expenses and grant awards, including its form and content, are fairly presented in accordance with the modified cash basis of accounting. The methods of measurement and presentation of the schedules of functional expenses and grant awards have not changed from those used in the prior period, and we have disclosed to you any significant assumptions or interpretations underlying the measurement and presentation of the supplementary information.

We have carefully read this letter before signing it and understand, while you have provided the language of this letter to us, we are making these representations to you. We understand our obligation to carefully consider the possibility that any of the representations are not accurate. We have inquired of other members of management or employees of Wisconsin Trust Account Foundation, Inc. to the extent necessary to obtain a high degree of assurance that these representations are true. We know that you will be relying on them in the issuance of your report. De Ette Tomlinson Executive Director

Main St.

Doty St.

Gilman St.

Wilson St.

Gorham St.

John Nolen Drive

Langdon St.

StateStreet

Mall

King

MLK

B

lvd.

Bed

ford

St.

But

ler

St.

Lake

St.

France

s

St.

DOWNTOWN CITY-OPERATED PARKING

W. Washington Ave. E. Washington Ave

North Shore Dr.

Johnson St.

S. Ham

ilton

St.

N. H

amilto

n St.

University Ave.

Bas

sett

St.

Bro

om S

t.

Hen

ry S

t.

Car

roll

St.

Fairc

hild

St.

Web

ster

St.

Pin

ckne

y S

t.

Wis

cons

in A

ve.

Dayton St.

Mifflin St.

St.

Han

cock

St.

Fran

klin

St.

Bla

ir S

t.

Main St.

Doty St.

Gilman St.

Wilson St.

Gorham St.

John Nolen Drive

Langdon St.

StateStreet

Mall

King

MLK

B

lvd.

Bed

ford

St.

But

ler

St.

Lake

St.

France

s

St.

CITY-OPERATED PARKING AVAILABILITY

W. Washington Ave. E. Washington Ave

North Shore Dr.

Johnson St.

S. Ham

ilton

St.

N. H

amilto

n St.

University Ave.

Bas

sett

St.

Bro

om S

t.

Hen

ry S

t.

Car

roll

St.

Fairc

hild

St.

Web

ster

St.

Pin

ckne

y S

t.

Wis

cons

in A

ve.

Dayton St.

Mifflin St.

St.

Han

cock

St.

Fran

klin

St.

Bla

ir S

t.Lake Monona

Lake Mendota

NORTH

Downtown Parking Map Courtesy of City of Madison Parking Utility

Revised 12/5/2012

3

810

9

6

4

2

7

810

9

6

4

2

Monona TerraceCommunity

andConvention

Center

2 Brayton Lot3 Buckeye Lot4 Capitol Square North Garage6 Government East Garage7 Lot 888 Overture Center Garage9 State St. Campus Garage10 State St. Capitol Garage

LEGEND Enter Garage/Lot Here One Way Street

FACILITIES2 Brayton Lot

4 Capitol Square North Garage

6 Government East Garage

8 Overture Center Garage

9 State St. Campus Garage

10 State St. Capitol Garage

LEGEND Enter Garage/Lot Here One Way Street

Downtown Parking Availability MapCourtesy of City of Madison Parking Utility

Revised 12/5/2012

3

5

4

2

1

LEGENDEnter Ramp HereOne Way Street

1 Capitol Square North Garage2 Government East Garage3 Overture Center Garage4 State St. Campus Garage5 State St. Capitol Garage