Melior · PDF fileMr. Tibriwal has more than 20 years of accounting and finance experience as...

26

INVESTOR PRESENTATION | JUNE 2017 Melior Resources Mark McCauley, President & CEO TSX-V: MLR 1

-

Upload

phungthuan -

Category

Documents

-

view

217 -

download

3

Transcript of Melior · PDF fileMr. Tibriwal has more than 20 years of accounting and finance experience as...

INVESTOR PRESENTATION | JUNE 2017

Melior Resources

Mark McCauley, President & CEO

TSX-V: MLR

1

Forward-looking statements

•This presentation contains information about Melior Resources Inc. (“Melior”) and should be read in conjunction with Melior’s public filings available at www.sedar.com and at

www.meliorresources.com. The content of this presentation is not to be construed as legal, financial or tax advice. Any reader should contact his, her or its own professional advisors for

legal, financial, tax or other advice.

•Certain information contained in this presentation, including the information contained in the Preliminary Economic Assessment (PEA), constitutes forward looking information under the

provisions of Canadian securities laws. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the use of forward-looking

terminology such as "plans", "expects", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates", “projects”, “potential”, "believes" or variations of such words

and phrases or statements that certain actions, events or results "may", "could", "would", “should”, "might" or "will be taken", "occur" or "be achieved" or the negative connotation. Such

statements and information include, without limitation, statements regarding the possible re-start of operations at the Goondicum mine, the potential for resource expansion at the

Goondicum mine and other aspects relating to the Goondicum mine. In addition, all of the results of the PEA represent forward looking information and statements. Statements in this

presentation that constitute forward looking statements or information, include but are not limited to: commodities and price assumption, cash flow forecasts, projected capital and

operating costs, recoveries, mine life and production rates, the financial results of the PEA including IRR and NPVs, as well as other assumptions used in the PEA. This forward looking

information is subject to numerous risks, uncertainties and assumptions, certain of which are beyond the control of Melior including the impact of general economic conditions; industry

conditions; volatility of minerals prices; volatility of commodity prices; currency fluctuations; mining risks; risks associated with foreign operations; governmental and environmental

regulation; competition from other industry participants; the lack of availability of qualified personnel or management; stock market volatility. Readers are cautioned that the material

assumptions used in the preparation of such information, although considered reasonable by management at the time of preparation, may prove to be imprecise. Actual results, future

events, performance or achievement could differ materially from those expressed in, or implied by, this forward-looking information and, accordingly, no assurance can be given that any

of the events anticipated by the forward-looking information will transpire or occur, or if any of them do so, what benefits Melior will derive therefrom. Melior disclaims any intention or

obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise except as required by applicable securities laws.

Information in this presentation is necessarily summarized and may not contain all available material information.

•For more information on the risks, uncertainties and assumptions that could cause Melior’s results, performance or achievement to differ from current expectations, please refer to the

“Risk Factors” section of Melior’s Annual Information Form dated November 19, 2014, Melior’s second quarter Management’s Discussion and Analysis of Financial Condition and

Results of Operations dated March 1, 2017, as well as Melior’s other public filings, available at www.sedar.com and at www.meliorresources.com. These factors should be considered

carefully and prospective investors should not place undue reliance of the forward looking statement.

2

Resource category & preliminary economic assessment disclaimer

The expectations outlined in this presentation regarding the Goondicum mine represent the information contained in the Preliminary Economic Assessment (PEA)

prepared independently by TZ Minerals International Pty Ltd for the purposes of National Instrument 43-101 and relies in part on inferred resources. As a result, the

PEA is subject to increased uncertainty and technical and economic risks of mine failure and there can be no assurance that the report’s expectations will be achieved.

The PEA is preliminary in nature and includes Inferred Resources that are considered too speculative geologically to have the economic considerations applied to them

that would enable them to be categorized as mineral Reserves, and there is no certainty the PEA will be realized. Shareholders are strongly encouraged to refer to the

complete updated technical report prepared in accordance with NI 43-101 in respect of the Goondicum mine, which includes the results of the PEA described in this

news release, which has been filed on SEDAR at www.sedar.com under the Company’s profile.

The Qualified Persons for the PEA are:

Mark Dufty, BSc Hons (Geology), FAusIMM (106196), MAIG (6643), employed by TZMI as Principal Consultant, was responsible for Sections

1,2,13,15,16,17,18,19,21,22,24,25,26,27.

Mineral Resources estimates were completed by H&S Consultants Pty Ltd (“H&SC”), a geological consultancy based in Sydney, NSW, Australia and are reported in

accordance with Canadian Securities Administrators National Instrument 43-101.The effective date of the mineral resources estimates disclosed in this news release is

October 5, 2016.

Simon Tear, BSc Hons (Mining Geology), P.Geo (Institute of Geologists of Ireland 17), EurGeol (26), employed by H&SC as a director and Consultant Geologist, was

responsible (or partly responsible) for Sections 3,4,5,7,10,11,12,14,20,23,25,26,27.

Graham Lee, BSc (Geology), FAusIMM CP(Geo) (101602), MAIG (1990, employed by Graham Lee and Associates Pty Ltd as a Director and Consultant Geologist,

was responsible (or partly responsible) for sections 6,8,9,10,11,25,26.

3

Investment highlights

Melior is poised to capitalize on strong ilmenite prices

4

• Melior’s Goondicum mine is a past producer of ilmenite

• Re-start of operations is low risk and low cost

• Location in Australia gives direct access to Asian markets

• Recent PEA demonstrates robust economics

• Goondicum has upside potential for resource expansion

• Melior is testing a new metallurgical process with significant potential

Ilmenite –an industrial mineral with

lifestyle applications

5

What is ilmenite?

- Cars

- Houses

- Electronics

- Paints

- Coatings

- Plastics

- Paper

Makes colors bright, opaque and UV-resistant

A feedstock for titanium dioxide pigment

Used as a whitening pigment for:

6

Market fundamentals are strong

Demand driven by GDP growth in emerging countries

7

0

50

100

150

200

250

300

350

20

09

20

10

20

11

20

12

20

13

20

14

20

15

H1

20

16

NO

V2

01

6

20

17

20

18

20

19

20

20

20

21

20

22

US$

/t F

OB

Historical/Forecast Sulphate Ilmenite Price

TZMI

Forecast

+200% Price/tonne increase

in 12 months

Our core focus

Goondicum

• Past producing ilmenite mine

• High grade deposit; low cost production

• Strategically located in Queensland

• Currently in care & maintenance

Production ready with minimal capital requirements

8

Recent progress

• Completed PEA with strong economics

• Strengthened leadership team

• Updated & optimised Goondicum re-start strategy

• Initiated discussions with off-take partners

Supported by favorable market outlook

9

Low risk, low cost re-start

• AUD$120M of previous investments

• Fully-permitted mine

• Access to skilled labour

• Conventional mineral sands mining

• Opportunity to extend mine life

USD$6MCAPEX Required

Poised to capitalize on strong market fundamentals

10

Established infrastructure

375tphProcessing facility

• 260 km to Gladstone port

• 37km of water pipeline

• 26km of grid-connected power line

• New mine access road partially

constructed

Goondicum is production ready

11

Queensland – an ideal location

• Mining-friendly jurisdiction

• Ranked #10 by Fraser Institute

• Multi-commodity world-class port

• Long history of mining

In close proximity to Asian markets

12

13

Goondicum production profile & process

• Simple mining process

• Low strip ratio

• Standard equipment

• Conventional processing

• Low operational risk

• Low product contaminants

181KTonnes ilmenite per annum

Ilmenite product is highly reactive, ideal as base feedstock

PEA highlights*

NPV10 USD$52.8M

IRR 178%

Project Payback Period 1.2 years

Re-start Capital Costs USD$5.96M

Annual cash flow USD$11.2M

OPEX Costs/tonne USD$111.80 FOB

TZMI long-term ilmenite price/tonne USD$189 FOB

*Preliminary Economic Assessment announced December 2016. All amounts are after tax and in $US

Robust economics

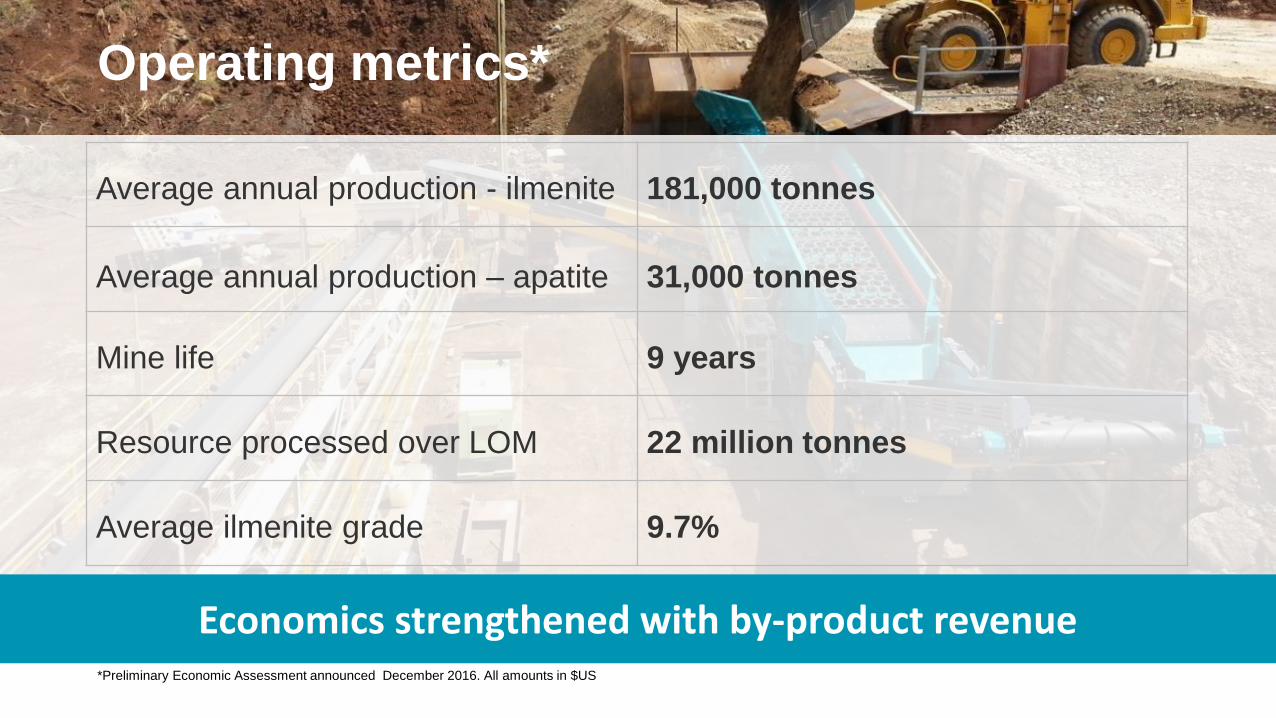

Operating metrics*

Average annual production - ilmenite 181,000 tonnes

Average annual production – apatite 31,000 tonnes

Mine life 9 years

Resource processed over LOM 22 million tonnes

Average ilmenite grade 9.7%

*Preliminary Economic Assessment announced December 2016. All amounts in $US

Economics strengthened with by-product revenue

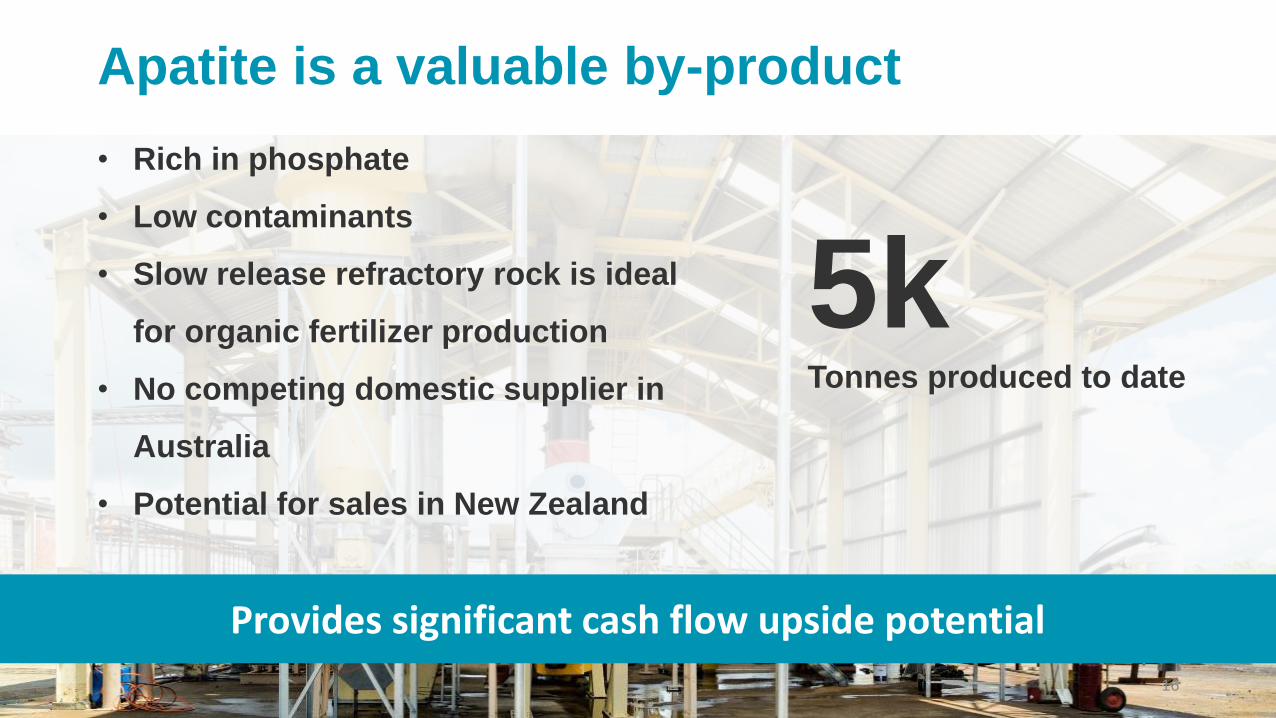

Apatite is a valuable by-product

• Rich in phosphate

• Low contaminants

• Slow release refractory rock is ideal

for organic fertilizer production

• No competing domestic supplier in

Australia

• Potential for sales in New Zealand

5kTonnes produced to date

Provides significant cash flow upside potential

16

Upside exploration potential

*Preliminary Economic Assessment announced December 2016. All amounts in $US

• Mining lease occupies 20% of

Goondicum crater

• Exploration licenses encompass

28 km2

• Area demonstrates consistent

geology and mineralization

• Potential to recover vanadium

and related by-products

Provides opportunity to extend mine life

17

Business upside through innovative process

Browne Processing Technology

• Upgrades ilmenite

• Reduces energy costs

• Reduces consumable and

maintenance costs

• Potential to attract premium pricing

• Applicable to other ore types

85%Potential upgrade of

ilmenite Ti02 content at

lower temperatures

Potential game-changing technology

18

Experienced leadership team

Charles Entrekin, Chairman

More than 40 years of industry experience. Formerly served as President and Chief Operating Officer of Titanium Metals Corporation, a NYSE listed

producer of primary titanium and its alloys as well as President and Chief Executive Officer of Timminco Ltd., a TSX listed magnesium, silicon, and

aluminum company.

Martyn Buttenshaw, Director

Mr. Buttenshaw is currently Senior Manager with Pala Investments Limited. Mr Buttenshaw has over twelve years of direct mining experience and is a

former Senior Mining Engineer at Rio Tinto Mineral’s borax operations, overseeing all aspects of mine planning at its US and international mining

operations. Mr. Buttenshaw is currently a director of Sierra Rutile Ltd and has extensive experience advising Sierra Rutile (a UK listed rutile and ilmenite

producer) on strategic mine planning, business improvement and project feasibility studies. Mr. Buttenshaw holds an MBA (with distinction) from the

London Business School and a MEng (First Class) in Mining Engineering from the Royal School of Mines, Imperial College, and London.

Rishi Tibriwal, Director

Mr. Tibriwal has more than 20 years of accounting and finance experience as well as broad experience in the resources sector. Mr. Tibriwal is a chartered

accountant and earned an MBA in Finance from Newport University. Mr. Tibriwal is also a graduate from Mumbai University and spent 10 years at Ernst &

Young, with the last four years as a partner before setting up his own financial consulting services group. Mr. Tibriwal was also formerly the chief financial

officer of Carpathian Gold Inc. and Gravitas Financial Inc.

Mark McCauley, Director & CEO

Formerly Managing Director of Belridge Enterprises Pty Ltd, the former owner of the Goondicum Project. Mr. McCauley has substantial mining experience

and has been involved in the development of several major mining projects in Australia and Argentina, including turnaround and organizational

restructuring.

Jonathan Mattiske, CFO

Over 15 years of financial experience working for private and public companies in the mining, engineering and technology industries. Extensive

knowledge and understanding of the business and assets of the Company having been involved with the Goondicum project since 2012.

19

Capital Structure

Pala Investments

45%

Takota Asset Management

13%

Belmont Park Investments

9%

Panorama Ridge

9%

Others24%

Strong shareholder support

20

Shares Outstanding: ~271 million

52 week range: $0.02 - $0.08

Recent price: $0.06*

Market Cap: $12 million

Cash position: $0.9 million**

Debt $4.5 million

*As June 8, 2017

**As at March 31, 2017

Upcoming catalysts

Multiple opportunities to unlock shareholder value

21

1.

2.

3.

4.

Sign agreements with off-take partners and raise funding

Re-start operations at Goondicum

Continue exploration program

Prove-up Browne Process

Appendix

INVESTOR PRESENTATION | MAY 2017

23

Resource base

24

ML80044

CategoryTonnes

(Mt)

Ilmnite

(%)

Apatite

(%)

Slimes

(%)

Ilmenite

(Mt)

Apatite

(Mt)

Slimes

(Mt)

Indicated 31.3 6.1 1.8 22.9 1.90 0.55 7.17

Inferred 30.9 6.3 1.6 24.3 1.93 0.49 7.51

Note: (minor rounding errors)

ML80141

CategoryTonnes

(Mt)

Ilmenite

(%)

Slimes

(%)

Ilmenite

(Mt)

Slimes

(Mt)

Indicated 15.6 5.1 29.5 0.79 4.60

Inferred 12.3 5.2 27.3 0.64 3.37

Goondicum crater – upside potential

25

Current Mining Area

Simplified flowsheet

26