Mega Trends in Workers Compensation Past, Present and Future 16 th Annual AMCOMP Conference Las...

99

Mega Trends in Workers Compensation Past, Present and Future 16 th Annual AMCOMP Conference Las Vegas, NV March 27, 2014 Download at www.iii.org/presentations Robert P. Hartwig, Ph.D., CPCU, President & Economist Insurance Information Institute 110 William Street New York, NY 10038 Tel: 212.346.5520 Cell: 917.453.1885 [email protected]

-

Upload

leo-miller -

Category

Documents

-

view

219 -

download

1

Transcript of Mega Trends in Workers Compensation Past, Present and Future 16 th Annual AMCOMP Conference Las...

Mega Trends in Workers Compensation

Past, Present and Future16th Annual AMCOMP Conference

Las Vegas, NVMarch 27, 2014

Download at www.iii.org/presentationsRobert P. Hartwig, Ph.D., CPCU, President & Economist

Insurance Information Institute 110 William Street New York, NY 10038Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

2

Presentation Outline

The Post-Crisis Economy & Workers Compensation The scars of the “Great Recession” are still visible on the WC line

The New American Labor Force The Reindustrialization of America The Future of Healthcare in the United States

WC’s future in inextricably linked to influences in this key sector

Workers Compensation Operating Result Update Workers Compensation: The Next 100 Years Q&A

The Slow and Uneven Nature of the Economic Recovery Is

Changing the WC Playing Field

3

Despite a Still-Sluggish Economy, there Are Potent Growth Drivers for Workers

Comp and Commercial Insurers in General

3

4

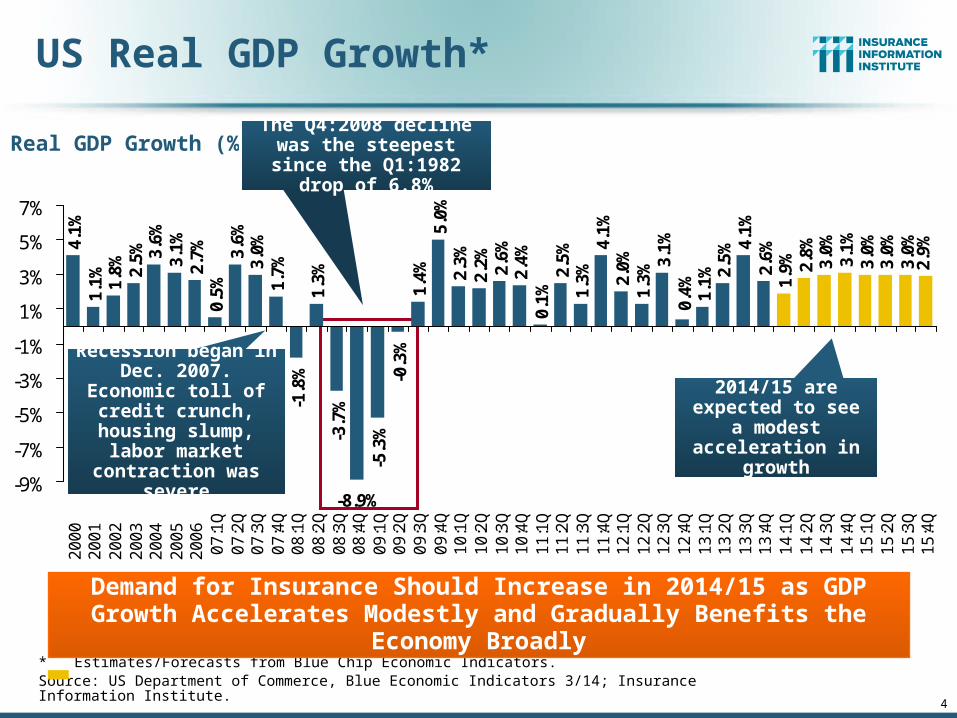

US Real GDP Growth*

* Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 3/14; Insurance Information Institute.

2.7%

0.5%

3.6%

3.0%

1.7%

-1.8

%1.

3%-3

.7%

-5.3

%-0

.3%

1.4%

5.0%

2.3%

2.2% 2.6%

2.4%

0.1%

2.5%

1.3%

4.1%

2.0%

1.3%

3.1%

1.1% 2.

5%4.

1%2.

6%1.

9% 2.8%

3.0%

3.1%

3.0%

3.0%

3.0%

2.9%

0.4%

-8.9%

4.1%

1.1% 1.

8% 2.5% 3.

6%3.

1%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

11

:1Q

11

:2Q

11

:3Q

11

:4Q

12

:1Q

12

:2Q

12

:3Q

12

:4Q

13

:1Q

13

:2Q

13

:3Q

13

:4Q

14

:1Q

14

:2Q

14

:3Q

14

:4Q

15

:1Q

15

:2Q

15

:3Q

15

:4Q

Demand for Insurance Should Increase in 2014/15 as GDP Growth Accelerates Modestly and Gradually Benefits the Economy Broadly

Real GDP Growth (%)

Recession began in Dec. 2007. Economic toll of credit crunch, housing slump, labor market contraction

was severe

The Q4:2008 decline was the steepest since the Q1:1982 drop of 6.8%

2014/15 are expected to see a

modest acceleration in growth

5

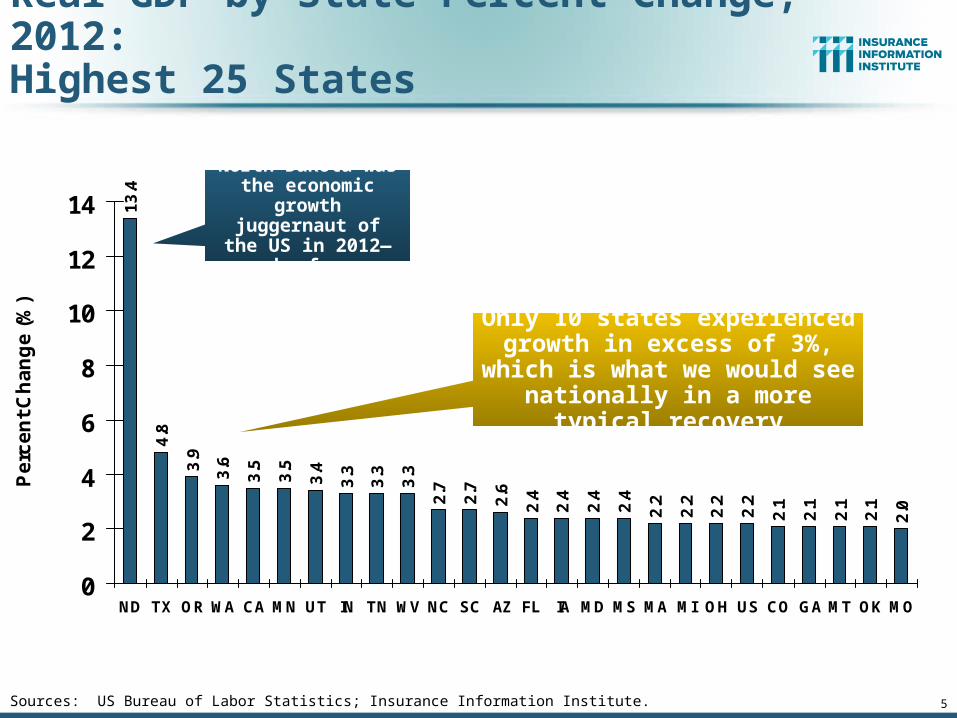

Real GDP by State Percent Change, 2012:Highest 25 States

13

.4

4.8

3.9

3.6

3.5

3.5

3.4

3.3

3.3

3.3

2.7

2.7

2.6

2.4

2.4

2.4

2.4

2.2

2.2

2.2

2.2

2.1

2.1

2.1

2.1

2.0

0

2

4

6

8

10

12

14

ND TX OR WA CA MN UT IN TN WV NC SC AZ FL IA MD MS MA MI OH US CO GA MT OK MO

Pe

rce

nt

Ch

an

ge

(%

)

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

North Dakota was the economic growth juggernaut of the US

in 2012—by far

Only 10 states experienced growth in excess of 3%, which is what we would see nationally in

a more typical recovery

6

1.9

1.7

1.6

1.5

1.5

1.5

1.5

1.4

1.4

1.4

1.3

1.3

1.3

1.2

1.2

1.1

1.1

0.7

0.5

0.5

0.4

0.2

0.2

0.2

0.2

-0.1

-0.4-0.20.00.20.40.60.81.01.21.41.61.82.0

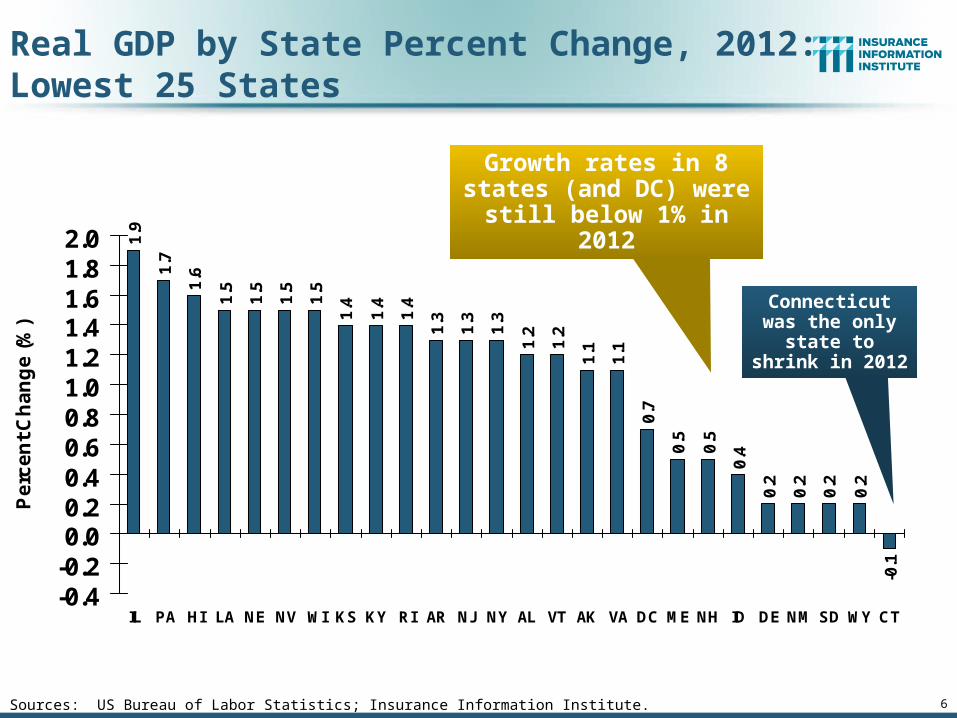

IL PA HI LA NE NV WI KS KY RI AR NJ NY AL VT AK VA DC ME NH ID DE NM SD WY CT

Pe

rce

nt

Ch

an

ge

(%

)

Real GDP by State Percent Change, 2012: Lowest 25 States

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

Connecticut was the only state to shrink in 2012

Growth rates in 8 states (and DC) were still below

1% in 2012

74

.47

3.6

73

.67

2.2

73

.6 76

67

.86

8.9

68

.26

7.7 7

1.6 74

.57

4.2 77

.56

7.5 69

.8 74

.37

1.5

63

.75

5.7 5

9.5

60

.9 64

.16

9.9

75

.07

5.3

76

.27

6.4 79

.37

3.2

72

.3 74

.38

2.6

82

.77

4.5

73

.8 77

.67

8.6

84

.58

4.1

85

.18

2.1

77

.57

3.2 75

.18

2.5

81

.28

1.6

79

.9

76

.4

40

45

50

55

60

65

70

75

80

85

90

Jan

-10

Fe

b-1

0M

ar-

10

Ap

r-1

0M

ay-

10

Jun

-10

Jul-

10

Au

g-1

0S

ep

-10

Oct

-10

No

v-1

0D

ec-

10

Jan

-11

Fe

b-1

1M

ar-

11

Ap

r-1

1M

ay-

11

Jun

-11

Jul-

11

Au

g-1

1S

ep

-11

Oct

-11

No

v-1

1D

ec-

11

Jan

-12

Fe

b-1

2M

ar-

12

Ap

r-1

2M

ay-

12

Jun

-12

Jul-

12

Au

g-1

2O

ct-1

2N

ov-

12

De

c-1

2Ja

n-1

3F

eb

-13

Ma

r-1

3A

pr-

13

Ma

y-1

3Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-1

3N

ov-

13

De

c-1

3Ja

n-1

4F

eb

-14

Ma

r-1

4

Consumer Sentiment Survey (1966 = 100)

January 2010 through March 2014

Consumer confidence has been low for years amid high unemployment, falling home prices and other factors adversely impact consumers, but improved substantially over the past 2+ years, though

uncertainty in Washington sometimes takes a toll.Source: University of Michigan; Insurance Information Institute

Optimism among consumers dropped in Q3 2013 as the

government shutdown created uncertainty, then rebounded

though the harsh winter took a toll

8

Impact of 2011 budget impasse

9

(Millions of Units)

New Private Housing Starts, 1990-2019F

1.4

8

1.4

7 1.6

21

.64

1.5

71

.60 1.7

1 1.8

5 1.9

6 2.0

71

.80

1.3

6

0.9

10

.55

0.5

9

0.6

1 0.7

8 0.9

2 1.0

91

.31 1.4

41

.50

1.5

11

.50

1.3

51.4

61

.29

1.2

0

1.0

11.1

9

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14F15F16F17F18F19F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (3/14 and 3/13); Insurance Information Institute.

Insurers Are Continue to See Meaningful Exposure Growth in the Wake of the “Great Recession” Associated with Home Construction: Construction Risk

Exposure, Surety, Commercial Auto; Potent Driver of Workers Comp Exposure

New home starts plunged 72% from 2005-2009; A net

annual decline of 1.49 million units, lowest since records began

in 1959

Job growth, low inventories of existing homes, low mortgage rates and demographics should continue to stimulate new home construction

for several more years

10

Commercial & Industrial Loans Outstandingat FDIC-Insured Banks, Quarterly, 2006-2013*

$1.1

6$1

.18

$1.2

2

$1.4

4$1

.48

$1.4

9$1

.50

$1.4

9$1

.43

$1.3

7$1

.27

$1.2

1$1

.18

$1.1

7$1

.17

$1.1

8$1

.20

$1.2

4 $1.2

8 $1.3

5$1

.37 $1

.42

$1.4

6 $1.5

1$1

.53

$1.5

6$1

.57

$1.1

3

$1.2

5 $1.3

0$1

.39

$1.0

$1.1

$1.2

$1.3

$1.4

$1.5

$1.6

06:Q

106

:Q2

06:Q

306

:Q4

07:Q

107

:Q2

07:Q

307

:Q4

08:Q

108

;Q2

08:Q

308

:Q4

09:Q

109

:Q2

09:Q

309

:Q4

10:Q

110

:Q2

10:Q

310

:Q4

11:Q

111

:Q2

11:Q

311

:Q4

12:Q

112

:Q2

12:Q

312

:Q4

13:Q

113

:Q2

13:Q

3

Outstanding loan volume has been growing for over two yearsand (as of year-end 2012) surpassed previous peak levels.

*Latest data as of 2/2/2014.Source: FDIC at http://www2.fdic.gov/qbp/ (Loan Performance spreadsheet); Insurance Information Institute.

$Trillions In nominal dollar terms, this is an

all-time high.

Recession

50

.7 52

.7 54

.15

4.6

54

.85

3.5

53

.75

2.8 53

.95

4.6 56 5

7.1 5

9.4

59

.75

6.3

54

.45

3.3

53

.45

3.8

52

.65

2.6

52

.65

2.6

53

.05

6.8

56

.15

5.0

53

.75

4.1

52

.75

2.9 54

.3 55

.25

4.8

54

.85

5.7

55

.25

6.0

53

.15

3.7

52

.25

6.0

58

.65

4.4 55

.45

3.9

53

.0 54

.05

1.6

54

.4

40

45

50

55

60

65

Jan

-10

Fe

b-1

0M

ar-

10

Ap

r-1

0M

ay-

10

Jun

-10

Jul-

10

Au

g-1

0S

ep

-10

Oct

-10

No

v-1

0D

ec-

10

Jan

-11

Fe

b-1

1M

ar-

11

Ap

r-1

1M

ay-

11

Jun

-11

Jul-

11

Au

g-1

1S

ep

-11

Oct

-11

No

v-1

1D

ec-

11

Jan

-12

Fe

b-1

2M

ar-

12

Ap

r-1

2M

ay-

12

Jun

-12

Jul-

12

Au

g-1

2S

ep

-12

Oct

-12

No

v-1

2D

ec-

12

Jan

-13

Fe

b-1

3M

ar-

13

Ap

r-1

3M

ay-

13

Jun

-13

Jul-

13

Au

g-1

3S

ep

-13

Oct

-13

No

v-1

3D

ec-

13

Jan

-14

Fe

b-1

4

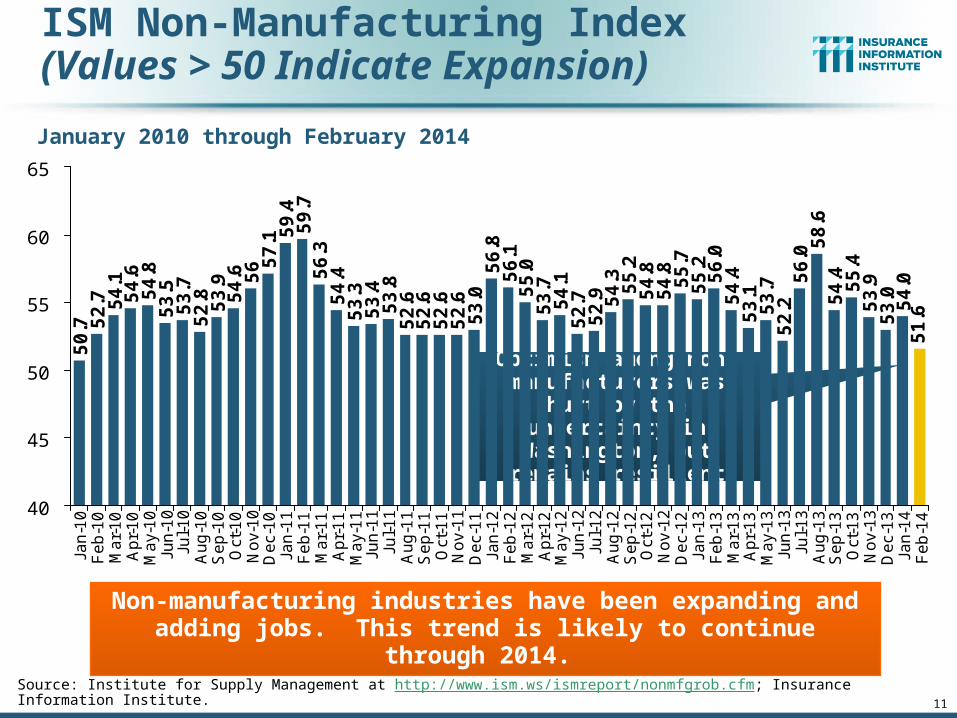

ISM Non-Manufacturing Index(Values > 50 Indicate Expansion)

January 2010 through February 2014

Non-manufacturing industries have been expanding and adding jobs. This trend is likely to continue through 2014.

Source: Institute for Supply Management at http://www.ism.ws/ismreport/nonmfgrob.cfm; Insurance Information Institute.

Optimism among non-manufacturers was hurt by

the uncertainty in Washington, but remains

resilient

11

12

43,6

9448

,125

69,3

0062

,436

64,0

04 71,2

77 81,2

3582

,446

63,8

5363

,235

64,8

53 71,5

4970

,643

62,3

0452

,374

51,9

5953

,549

54,0

2744

,367

37,8

8435

,472

40,0

9938

,540

35,0

3734

,317

39,2

0119

,695 28

,322

43,5

4660

,837

56,2

8247

,806

40,0

7533

,212

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Business Bankruptcy Filings,1980-2013

Sources: American Bankruptcy Institute (1980-2012) at http://www.abiworld.org/AM/AMTemplate.cfm?Section=Home&TEMPLATE=/CM/ContentDisplay.cfm&CONTENTID=61633; 2013 data from United States Courts at http://news.uscourts.gov; Insurance Information Institute.

Significant Exposure Implications for All Commercial Lines as Business Bankruptcies Begin to Decline

2013 bankruptcies totaled 33,212, down 17.1% from 2012—the fourth

consecutive year of decline. Business bankruptcies more than tripled during the financial crisis.

% Change Surrounding Recessions

1980-82 58.6%1980-87 88.7%1990-91 10.3%2000-01 13.0%2006-09 208.9%

12

13

Nonfarm Payroll (Wages and Salaries):Quarterly, 2005–2013:Q4

Note: Recession indicated by gray shaded column. Data are seasonally adjusted annual rates.Sources: http://research.stlouisfed.org/fred2/series/WASCUR; National Bureau of Economic Research (recession dates); Insurance Information Institute.

Billions

$5,500

$5,750

$6,000

$6,250

$6,500

$6,750

$7,000

$7,250

$7,50005

:Q1

05:Q

205

:Q3

05:Q

406

:Q1

06:Q

206

:Q3

06:Q

407

:Q1

07:Q

207

:Q3

07:Q

408

:Q1

08:Q

208

:Q3

08:Q

409

:Q1

09:Q

209

:Q3

09:Q

410

:Q1

10:Q

210

:Q3

10:Q

411

:Q1

11:Q

211

:Q3

11:Q

412

:Q1

12:Q

212

:Q3

12:Q

413

:Q1

13:Q

213

:Q3

13:Q

4

Prior Peak was 2008:Q1 at $6.60 trillion

Latest (2013:Q4) was $7.23 trillion, a new peak--$980B

above 2009 trough

Recent trough (2009:Q3) was $6.25 trillion, down

5.3% from prior peak

Payrolls are 15.7% above

their 2009 trough and up 2.0% over

the past year

13

14

12 Industries for the Next 10 Years: Insurance Solutions Needed

Export-Oriented Industries

Health Sciences

Health Care

Energy (Traditional)

Alternative Energy

Petrochemical

Agriculture

Natural Resources

Technology (incl. Biotechnology)

Light Manufacturing

Insourced Manufacturing

Many industries are

poised for growth, though

insurers’ ability to

capitalize on these

industries varies widely

Shipping (Rail, Marine, Trucking, Pipelines)

CONSTRUCTION INDUSTRY OVERVIEW & OUTLOOK

15

The Construction Sector Is Critical to the Economy and

the WC Insurers

15

16

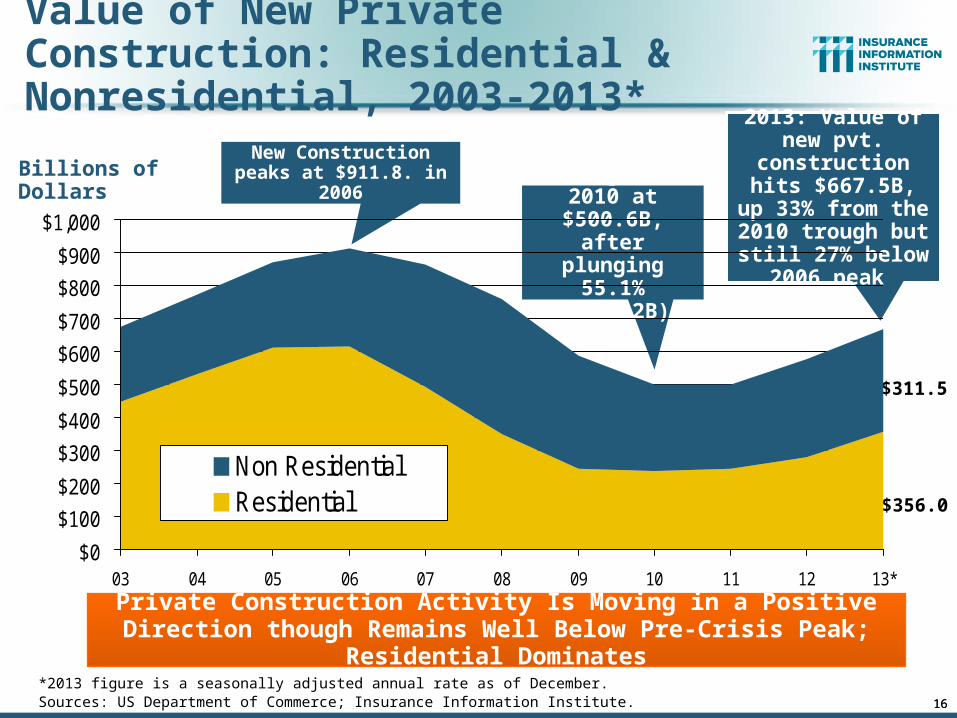

Value of New Private Construction: Residential & Nonresidential, 2003-2013*

Billions of Dollars

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

03 04 05 06 07 08 09 10 11 12 13*

Non ResidentialResidential

Private Construction Activity Is Moving in a Positive Direction though Remains Well Below Pre-Crisis Peak; Residential Dominates

$298.1

$15.0

$613.7

New Construction peaks at $911.8. in 2006

Trough in 2010 at $500.6B,

after plunging 55.1% ($411.2B)

2013: Value of new pvt. construction hits $667.5B, up

33% from the 2010 trough but still

27% below 2006 peak

16

$261.8

$238.8

$311.5

$356.0

*2013 figure is a seasonally adjusted annual rate as of December.Sources: US Department of Commerce; Insurance Information Institute.

18

Value of Construction Put in Place, January 2014 vs. January 2013*

2.5%

-22.2%

3.0%

9.3%12.3%

14.6%

9.7%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

TotalConstruction

Total PrivateConstruction

Residential--Private

Non-Residential--

Private

Total PublicConstruction

Residential-Public

Non-Residential--

Public

Overall Construction Activity is Up, But Growth Is Almost Entirely in the Private Sector as State/Local Government Budget Woes Continue

Growth (%)

Private sector construction activity is now up in the

residential and nonresidential segments

*seasonally adjustedSource: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

Private: +12.3% Public: +2.5%

Public sector construction activity remains low but is no

longer contracting

19

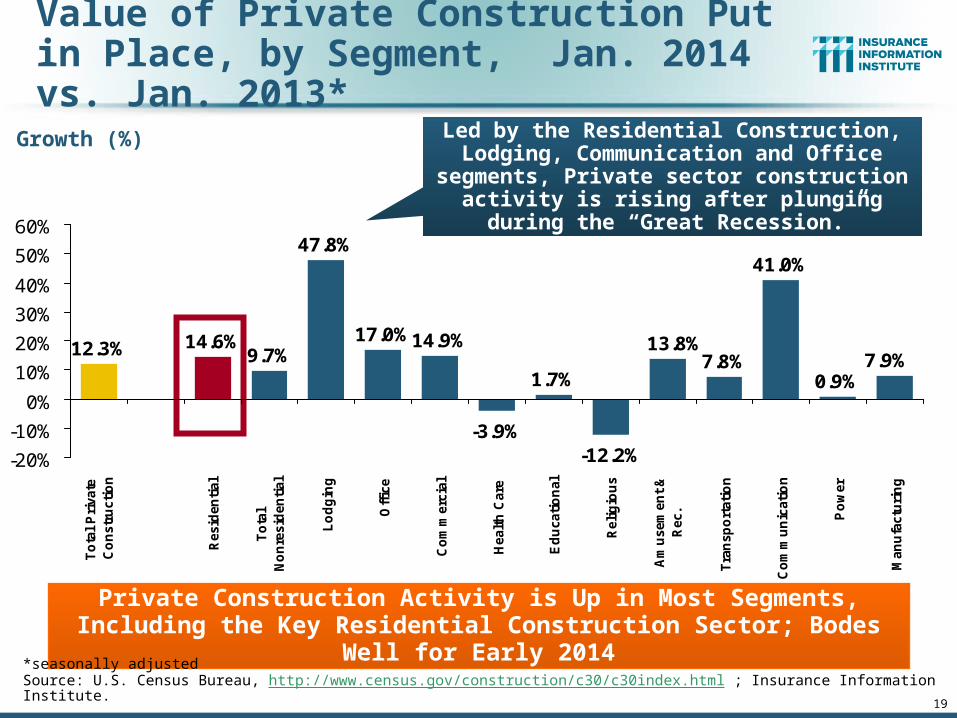

Value of Private Construction Put in Place, by Segment, Jan. 2014 vs. Jan. 2013*

14.9%

-3.9%

1.7%

-12.2%

7.8%

41.0%

0.9%7.9%

13.8%12.3% 14.6%9.7%

47.8%

17.0%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

To

tal

Pri

vate

Co

nstr

ucti

on

Resid

en

tial

To

tal

No

nre

sid

en

tial

Lo

dg

ing

Off

ice

Co

mm

erc

ial

Healt

h C

are

Ed

ucati

on

al

Reli

gio

us

Am

usem

en

t &

Rec.

Tra

nsp

ort

ati

on

Co

mm

un

icati

on

Po

wer

Man

ufa

ctu

rin

g

Private Construction Activity is Up in Most Segments, Including the Key Residential Construction Sector; Bodes Well for Early 2014

Growth (%) Led by the Residential Construction, Lodging, Communication and Office segments, Private

sector construction activity is rising after plunging during the “Great Recession.”

*seasonally adjustedSource: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

20

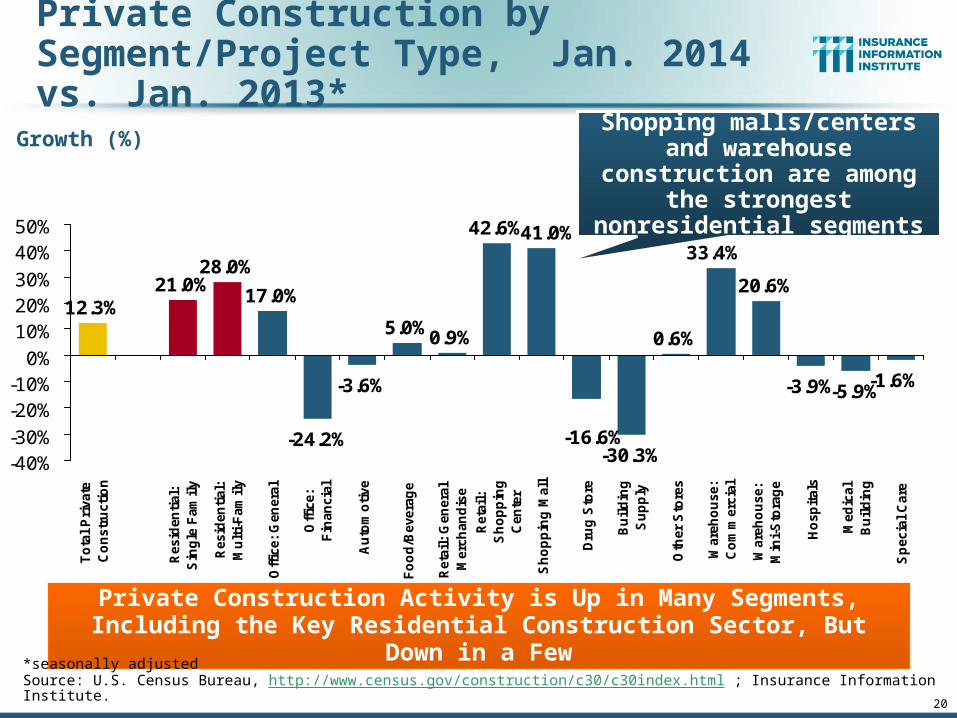

Private Construction by Segment/Project Type, Jan. 2014 vs. Jan. 2013*

-3.6%

5.0%0.9%

42.6%

-30.3%

0.6%

20.6%

-3.9%-5.9%-1.6%

-16.6%

33.4%41.0%

12.3%21.0%

28.0%

17.0%

-24.2%-40%-30%

-20%-10%

0%

10%20%30%

40%50%

To

tal

Pri

vate

Co

nstr

ucti

on

Resid

en

tial:

Sin

gle

Fam

ily

Resid

en

tial:

Mu

lti-

Fam

ily

Off

ice:

Gen

era

l

Off

ice:

Fin

an

cia

l

Au

tom

oti

ve

Fo

od

/Bevera

ge

Reta

il:

Gen

era

lM

erc

han

dis

e

Reta

il:

Sh

op

pin

gC

en

ter

Sh

op

pin

g M

all

Dru

g S

tore

Bu

ild

ing

Su

pp

ly

Oth

er

Sto

res

Ware

ho

use:

Co

mm

erc

ial

Ware

ho

use:

Min

i-S

tora

ge

Ho

sp

itals

Med

ical

Bu

ild

ing

Sp

ecia

l C

are

Private Construction Activity is Up in Many Segments, Including the Key Residential Construction Sector, But Down in a Few

Growth (%) Shopping malls/centers and warehouse construction are

among the strongest nonresidential segments

*seasonally adjustedSource: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

Florida Total Private Housing Starts,2000 – 2017F

21

The economic outlook for most of

the US is positive for the first time in many

years

Source: University of Central Florida Institute for Economic Competitiveness: http://iec.ucf.edu/post/2014/01/07/Florida-Metro-Forecast-December-2013.aspx

CRASH, CRATER, RECOVERY Homebuilding in FL continues

to recover, but employment and WC exposures will take

more than a decade to recover

(Thousands of Units)

22

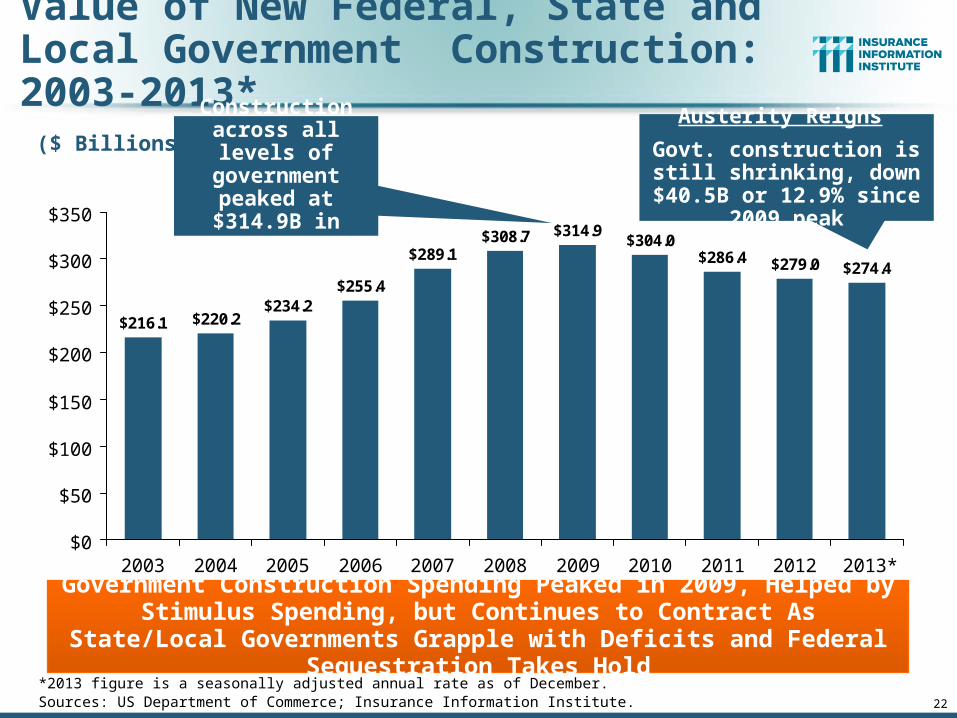

$314.9$304.0

$286.4 $279.0 $274.4

$216.1 $220.2$234.2

$255.4

$289.1$308.7

$0

$50

$100

$150

$200

$250

$300

$350

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

($ Billions)

Government Construction Spending Peaked in 2009, Helped by Stimulus Spending, but Continues to Contract As State/Local Governments

Grapple with Deficits and Federal Sequestration Takes Hold

Value of New Federal, State and Local Government Construction: 2003-2013*

*2013 figure is a seasonally adjusted annual rate as of December.Sources: US Department of Commerce; Insurance Information Institute.

Construction across all levels of government

peaked at $314.9B in 2009

Austerity Reigns

Govt. construction is still shrinking, down $40.5B or

12.9% since 2009 peak

23

Value of Public Construction Put in Place, by Segment, Jan. 2014 vs. Jan. 2013*

-6.2%-3.0%

-0.6%

-15.1%

7.8%

15.3%

3.6%

-10.8%-6.2%

8.7%

2.5%

-22.2%

3.0%

-9.9%

-27.8%-30%-25%-20%-15%-10%

-5%0%5%

10%15%20%

To

tal

Pu

bli

cC

on

str

ucti

on

Resid

en

tial

To

tal

No

nre

sid

en

tial

Off

ice

Co

mm

erc

ial

Healt

h C

are

Ed

ucati

on

al

Pu

bli

c S

afe

ty

Am

usem

en

t &

Rec.

Tra

nsp

ort

ati

on

Po

wer

Hig

hw

ay &

Str

eet

Sew

ag

e &

Waste

Dis

po

sal

Wate

r S

up

ply

Co

nserv

ati

on

&D

evelo

p.

Public Construction Activity is Down in Many Segments as State and Local Budgets Remain Under Stress; Improvement Possible in 2014.

Growth (%)

*seasonally adjustedSource: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

Public sector construction activity is down substantially in most segments, a situation that will likely persist, dragging

on public entity risk exposures

Highway, Transport, and Power projects lead public sector

construction

25

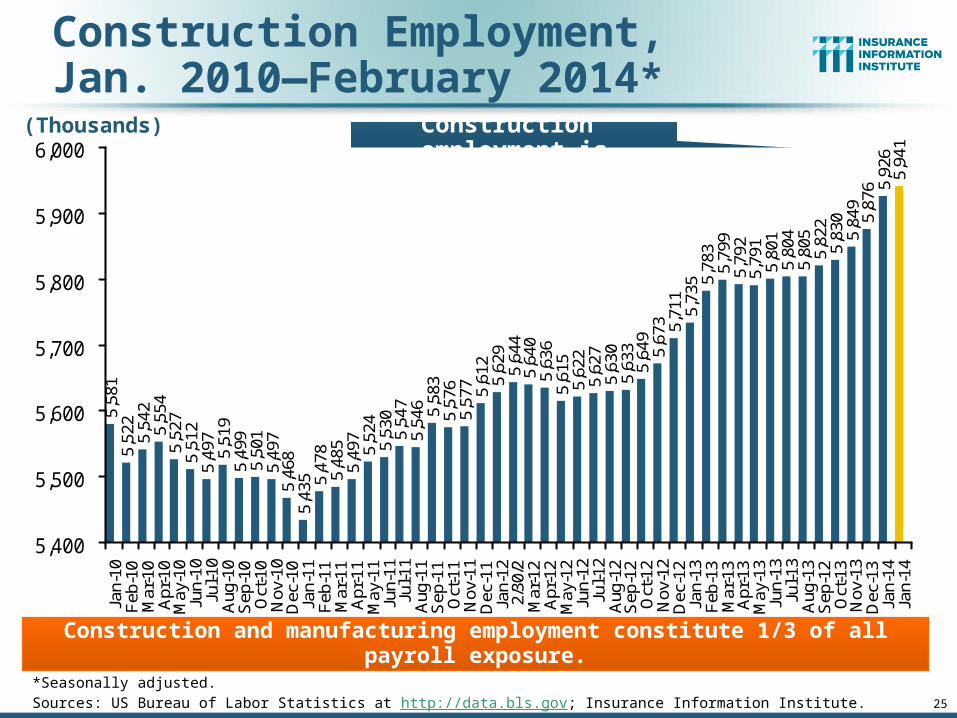

Construction Employment,Jan. 2010—February 2014*

*Seasonally adjusted.Sources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

5,58

15,

522

5,54

25,

554

5,52

75,

512

5,49

75,

519

5,49

95,

501

5,49

75,

468

5,43

5 5,47

85,

485

5,49

75,

524

5,53

05,

547

5,54

6 5,58

35,

576

5,57

7 5,61

25,

629

5,64

45,

640

5,63

65,

615

5,62

25,

627

5,63

05,

633

5,64

95,

673 5,71

15,

735 5,

783

5,79

95,

792

5,79

15,

801

5,80

45,

805

5,82

25,

830

5,84

95,

876 5,

926

5,94

1

5,400

5,500

5,600

5,700

5,800

5,900

6,000

Jan-

10F

eb-1

0M

ar-1

0A

pr-1

0M

ay-1

0Ju

n-10

Jul-1

0A

ug-1

0S

ep-1

0O

ct-1

0N

ov-1

0D

ec-1

0Ja

n-11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

122/

30/2

Mar

-12

Apr

-12

May

-12

Jun-

12Ju

l-12

Aug

-12

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13F

eb-1

3M

ar-1

3A

pr-1

3M

ay-1

3Ju

n-13

Jul-1

3A

ug-1

3S

ep-1

2O

ct-1

3N

ov-1

3D

ec-1

3Ja

n-14

Jan-

14

Construction employment is +506,000 above

Jan. 2011 (+9.3%) trough

(Thousands)

Construction and manufacturing employment constitute 1/3 of all payroll exposure.

26

Construction Employment, Jan. 2003–February 2014

Note: Recession indicated by gray shaded column.Sources: U.S. Bureau of Labor Statistics; Insurance Information Institute.

5,000

5,500

6,000

6,500

7,000

7,500

8,000

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

The “Great Recession” and housing bust destroyed 2.3 million constructions jobs

The Construction Sector Could Be a Growth Leader in 2014 as the Housing Market, Private Investment and Govt. Spending Recover. WC Insurers Will Benefit.

Construction employment

troughed at 5.435 million in Jan.

2011, after a loss of 2.291 million jobs, a 29.7%

plunge from the April 2006 peak

26

Construction employment

peaked at 7.726 million in April 2006

(Thousands) Construction employment as of Feb. 2014 totaled 5.941 million, an

increase of 506,000 jobs or 9.3% from the

Jan. 2011 trough

27

The New American Labor Force

The Recovery’s Winners and Losers Are Reshaping the Sources of WC’s

Payroll Exposure Base

27

28

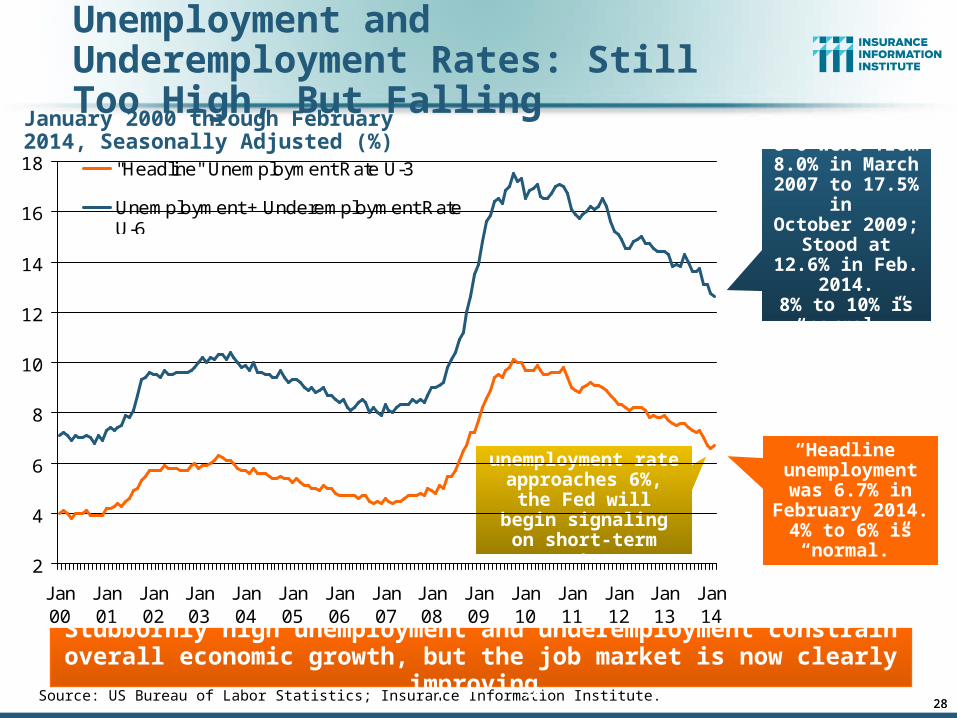

Unemployment and Underemployment Rates: Still Too High, But Falling

2

4

6

8

10

12

14

16

18

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Jan11

Jan12

Jan13

Jan14

"Headline" Unemployment Rate U-3

Unemployment + Underemployment RateU-6

“Headline” unemployment

was 6.7% in February 2014.

4% to 6% is “normal.”

Source: US Bureau of Labor Statistics; Insurance Information Institute.

U-6 went from 8.0% in March

2007 to 17.5% in October 2009; Stood at 12.6% in Feb. 2014.8% to 10% is

“normal.”

January 2000 through February 2014, Seasonally Adjusted (%)

Stubbornly high unemployment and underemployment constrain overall economic growth, but the job market is now clearly improving.

28

As the unemployment rate approaches 6%,

the Fed will begin signaling on short-

term rates

29

US Unemployment Rate Forecast4

.5%

4.5

%4

.6%

4.8

%4

.9% 5.4

% 6.1

%6

.9%

8.1

%9

.3%

9.6

% 10

.0%

9.7

%9

.6%

9.6

%

8.9

%9

.1%

9.1

%8

.7%

8.3

%8

.2%

8.0

%7

.8%

7.7

%7

.6%

7.3

%7

.0%

6.6

%6

.5%

6.3

%6

.2%

6.1

%6

.0%

5.9

%5

.8%

9.6

%

4%

5%

6%

7%

8%

9%

10%

11%

07

:Q1

07

:Q2

07

:Q3

07

:Q4

08

:Q1

08

:Q2

08

:Q3

08

:Q4

09

:Q1

09

:Q2

09

:Q3

09

:Q4

10

:Q1

10

:Q2

10

:Q3

10

:Q4

11

:Q1

11

:Q2

11

:Q3

11

:Q4

12

:Q1

12

:Q2

12

:Q3

12

:Q4

13

:Q1

13

:Q2

13

:Q3

13

:Q4

14

:Q1

14

:Q2

14

:Q3

14

:Q4

15

:Q1

15

:Q2

15

:Q3

15

:Q4

Rising unemployment

eroded payrolls

and WC’s exposure base.

Unemployment peaked at 10%

in late 2009.

* = actual; = forecastsSources: US Bureau of Labor Statistics; Blue Chip Economic Indicators (3/14 edition); Insurance Information Institute.

2007:Q1 to 2015:Q4F*

Unemployment forecasts have been revised slightly

downwards. Optimistic scenarios put the

unemployment as low as 6.0% by Q4 of this year.

Jobless figures have been revised

slightly downwards for 2014/15

23

15

21

70

52

12

65

73

-71

32 6

4 81

55

3-1

15

-10

6-2

21

-21

5-2

06

-26

1-2

58

-42

2-4

86

-77

6 -69

3-8

21

-69

8-8

10

-80

1-2

94

-42

6-2

72

-23

2 -14

1-2

71

-15

-23

22

0-3

8

19

29

4 11

01

20

11

71

07 1

99

14

99

47

22

23

23

1 32

01

66

18

6 21

91

25

26

81

77

19

12

22

36

42

28

24

61

02

13

17

51

72

13

61

59

25

52

11

21

52

19 26

31

64

18

82

22

20

11

70

18

01

53 2

47

27

28

6 14

51

62

11

3

(1,000)

(800)

(600)

(400)

(200)

0

200

400

600

Jan

-07

Fe

b-0

7M

ar-

07

Ap

r-0

7M

ay-

07

Jun

-07

Jul-

07

Au

g-0

7S

ep

-07

Oct

-07

No

v-0

7D

ec-

07

Jan

-08

Fe

b-0

8M

ar-

08

Ap

r-0

8M

ay-

08

Jun

-08

Jul-

08

Au

g-0

8S

ep

-08

Oct

-08

No

v-0

8D

ec-

08

Jan

-09

Fe

b-0

9M

ar-

09

Ap

r-0

9M

ay-

09

Jun

-09

Jul-

09

Au

g-0

9S

ep

-09

Oct

-09

No

v-0

9D

ec-

09

Jan

-10

Fe

b-1

0M

ar-

10

Ap

r-1

0M

ay-

10

Jun

-10

Jul-

10

Au

g-1

0S

ep

-10

Oct

-10

No

v-1

0D

ec-

10

Jan

-11

Fe

b-1

1M

ar-

11

Ap

r-1

1M

ay-

11

Jun

-11

Jul-

11

Au

g-1

1S

ep

-11

Oct

-11

No

v-1

1D

ec-

11

Jan

-12

Fe

b-1

2M

ar-

12

Ap

r-1

2M

ay-

12

Jun

-12

Jul-

12

Au

g-1

2S

ep

-12

Oct

-12

No

v-1

2D

ec-

12

Jan

-13

Fe

b-1

3M

ar-

13

Ap

r-1

3M

ay-

13

Jun

-13

Jul-

13

Au

g-1

3S

ep

-13

Oct

-13

No

v-1

3D

ec-

13

Jan

-14

Fe

b-1

4

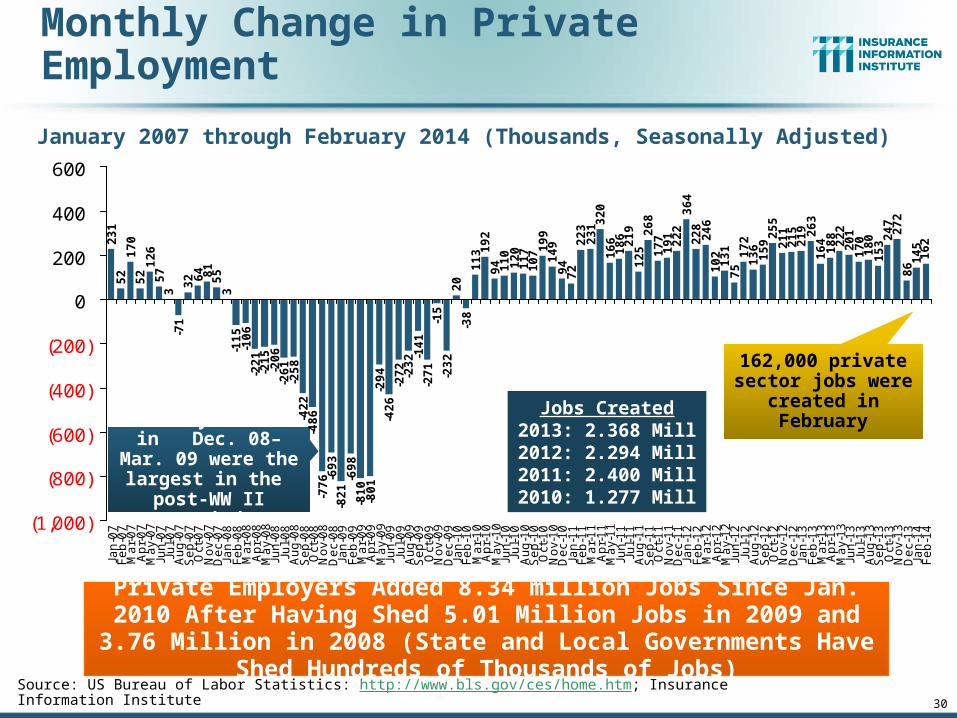

Monthly Change in Private Employment

January 2007 through February 2014 (Thousands, Seasonally Adjusted)

Private Employers Added 8.34 million Jobs Since Jan. 2010 After Having Shed 5.01 Million Jobs in 2009 and 3.76 Million in 2008 (State and Local Governments Have Shed Hundreds of Thousands of Jobs)

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Monthly losses in Dec. 08–Mar. 09

were the largest in the

post-WW II period

162,000 private sector jobs were

created in February

30

Jobs Created2013: 2.368 Mill2012: 2.294 Mill2011: 2.400 Mill2010: 1.277 Mill

0.02

0-0

.018

0.09

50.

287

0.38

10.

491

0.61

10.

728

0.83

51.

034

1.18

31.

277

1.34

91.

572

1.80

32.

123

2.28

92.

475

2.69

42.

819

3.08

73.

264

3.45

53.

677

4.04

14.

269

4.51

54.

617

4.74

84.

823

4.99

55.

131

5.29

05.

545

5.75

65.

971

6.19

06.

453

6.80

57.

027

7.22

87.

398

7.57

87.

731

7.97

88.

250

8.33

68.

481

8.64

3

6.61

7

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jan-

10F

eb-1

0M

ar-1

0A

pr-1

0M

ay-1

0Ju

n-10

Jul-1

0A

ug-1

0S

ep-1

0O

ct-1

0N

ov-1

0D

ec-1

0Ja

n-11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12F

eb-1

2M

ar-1

2A

pr-1

2M

ay-1

2Ju

n-12

Jul-1

2A

ug-1

2S

ep-1

2O

ct-1

2N

ov-1

2D

ec-1

2Ja

n-13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14F

eb-1

4

Mill

ion

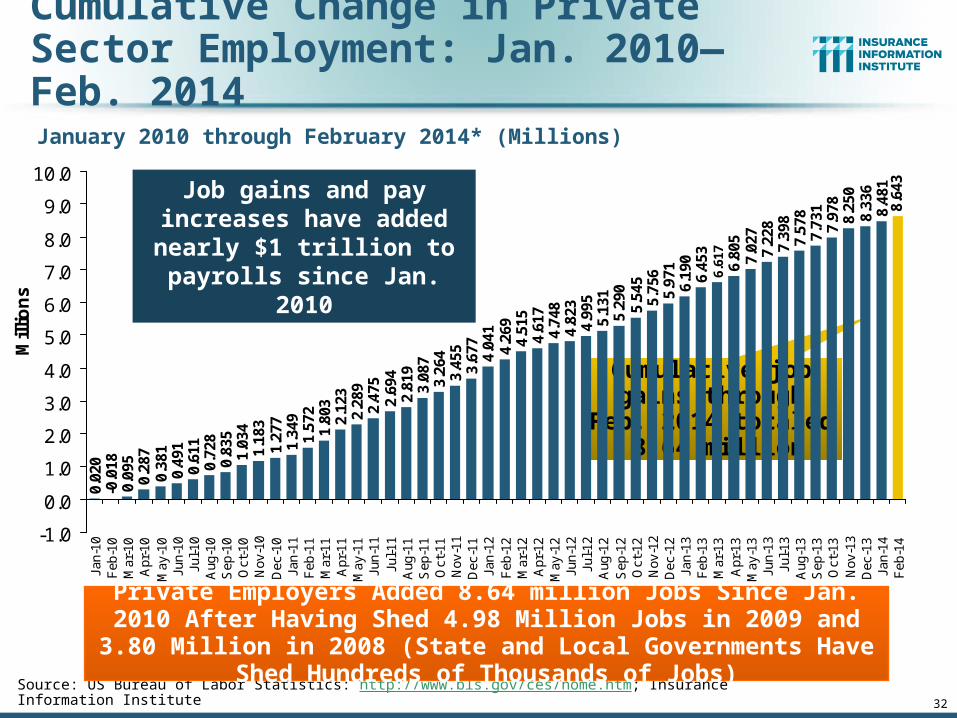

sCumulative Change in Private Sector Employment: Jan. 2010—Feb. 2014

January 2010 through February 2014* (Millions)

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Cumulative job gains through Feb. 2014

totaled 8.64 million

32

Job gains and pay increases have added

nearly $1 trillion to payrolls since Jan. 2010

Private Employers Added 8.64 million Jobs Since Jan. 2010 After Having Shed 4.98 Million Jobs in 2009 and 3.80 Million in 2008 (State and Local Governments Have Shed Hundreds of Thousands of Jobs)

4-1

033

9251

128

798

-68

-224 -1

84-1

94-2

13-2

24-2

71-2

89-2

88-3

56 -324

-452

-449

-480

-488

-511

-530

-542

-536

-539

-547

-574

-565

-589 -555

-535

-592

-601

-606

-622

-609

-610

-621

-643

-654 -623

-616

-633

-618

-631

-621

-800

-600

-400

-200

0

200

400

600

Jan-

10F

eb-1

0M

ar-1

0A

pr-1

0M

ay-1

0Ju

n-10

Jul-1

0A

ug-1

0S

ep-1

0O

ct-1

0N

ov-1

0D

ec-1

0Ja

n-11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12F

eb-1

2M

ar-1

2A

pr-1

2M

ay-1

2Ju

n-12

Jul-1

2A

ug-1

2S

ep-1

2O

ct-1

2N

ov-1

2D

ec-1

2Ja

n-13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Cumulative Change in Government Employment: Jan. 2010—Dec. 2013

January 2010 through Dec. 2013* (Millions)

Source: US Bureau of Labor Statistics http://www.bls.gov/data/#employment; Insurance Information Institute

Cumulative job losses through Dec. 2013 totaled 631,000

33

Governments at All Levels are Under Severe Fiscal Strain As Tax Receipts Plunged and Pension Obligations Soared During the

Financial Crisis: Sequestration Will Add to this Toll

Government at all levels has shed more than 600,000 jobs

since Jan. 2010 even as private employers created 8.14 million jobs, though losses may now

be stabilizing.

Temporary Census hiring distorted 2010

figures

34

Net Change in Government Employment: Jan. 2010—Dec. 2013*

-631

-424

-100 -107

-700

-600

-500

-400

-300

-200

-100

0

Total Local State Federal

(Thousands)

Local government employment shrank by 424,000 from Jan.

2010 through Dec. 2013, accounting for 67% of all government job losses,

negatively impacting WC exposures for those cities and counties that insure privately

*Cumulative change from prior month; Base employment date is Dec. 2009.Source: US Bureau of Labor Statistics http://www.bls.gov/data/#employment; Insurance Information Institute

State government employment fell by 1.9% since the end of 2009 but is

recovering while Federal employment is down by 3.8% and deteriorating

35

Unemployment Rates by State, February 2014:Highest 25 States*

9.0

8.7

8.5

8.0

7.8

7.7

7.4

7.4

7.3

7.1

7.1

7.1

7.0

6.9

6.9

6.8

6.7

6.7

6.5

6.5

6.5

6.4

6.4

6.4

6.4

6.2

6.2

0

2

4

6

8

10

RI IL NV CA KY MI DC MS AZ AR GA NJ CT OR TN NY US NM AK MA OH AL MO NC WA FL PA

Un

em

plo

ym

en

t R

ate

(%

)

*Provisional figures for February 2014, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

In February, 29 states had over-the-month unemployment rate decreases, 10 states had increases, and 11 states and the District of Columbia had no change.

36

6.1

6.1

6.1

6.1

6.0

6.0

5.7

5.7

5.7

5.3

5.1

5.0

4.9

4.9

4.8

4.7

4.6

4.5

4.4

4.2

3.9

3.7

3.6

3.6

2.6

0

1

2

3

4

5

6

7

CO IN ME WI DE WV MD SC TX ID MT OK KS VA MN NH HI LA IA WY UT VT NE SD ND

Une

mpl

oym

ent R

ate

(%)

Unemployment Rates by State, February 2014: Lowest 25 States*

*Provisional figures for February 2014, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

In February, 29 states had over-the-month unemployment rate decreases, 10 states had increases, and 11 states

and the District of Columbia had no change.

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$25

$30

$35

$40

$45

$50Wage & Salary DisbursementsWC NPW

39

Payroll Base* WC NWP

Payroll vs. Workers Comp Net Written Premiums, 1990-2013E

*Private employment; Shaded areas indicate recessions. WC premiums for 2012 are I.I.I. estimate based YTD 2013 actuals.Sources: NBER (recessions); Federal Reserve Bank of St. Louis at http://research.stlouisfed.org/fred2/series/WASCUR ; NCCI; I.I.I.

Continued Payroll Growth and Rate Increases Suggest WC NWP Will Grow Again in 2014; +8.6% Growth Estimated for 2013

7/90-3/91 3/01-11/0112/07-6/09

$Billions $Billions

WC premium volume dropped two years before

the recession began

WC net premiums written were down $14B or 29.3% to

$33.8B in 2010 after peaking at $47.8B

in 2005

+8.5% in 2013E

40

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

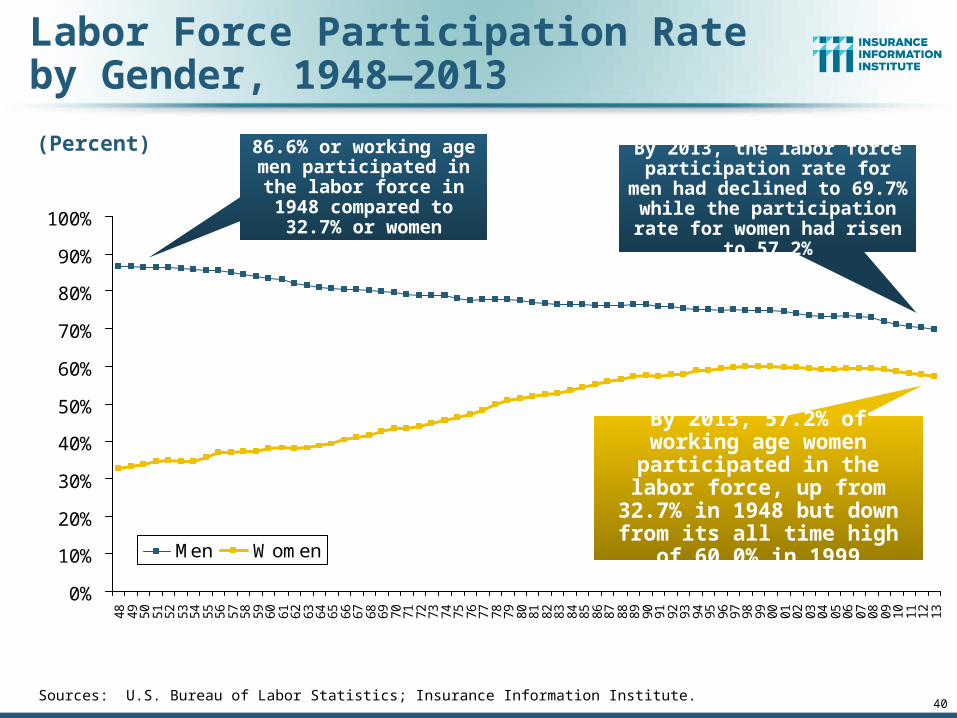

48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Men Women

Labor Force Participation Rate by Gender, 1948—2013

(Percent)

Sources: U.S. Bureau of Labor Statistics; Insurance Information Institute.

86.6% or working age men participated in the

labor force in 1948 compared to 32.7% or

women

By 2013, 57.2% of working age women participated in the

labor force, up from 32.7% in 1948 but down from its all time

high of 60.0% in 1999

By 2013, the labor force participation rate for men had

declined to 69.7% while the participation rate for women

had risen to 57.2%

41

Labor Force Participation by Sex and Education through the Crisis: 2006, 2010 and 2013

4.1%

2.2%

9.6%10.5%

8.6%

13.9%

11.5%

6.0%

7.6% 7.1%

9.7%

7.9%

5.0%4.6% 4.6% 4.6%5.9%

7.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

All Men Women Less than HSDiploma

HS Diploma,No College

Bachelor'sDegree or

Higher

2006 2010 2013

The composition and character of the U.S. labor force is changing rapidly. Winners and losers have clearly emerged. What does this mean for WC?

Unemployment Rate (%)

Sources: U.S. Bureau of Labor Statistics; Insurance Information Institute.

Men were hit harder and continue to do worse than women in the job market.

Women are likely to do better than men for the

indefinite future.

Workers lacking a college degree suffer from much

higher rates of unemployment

42

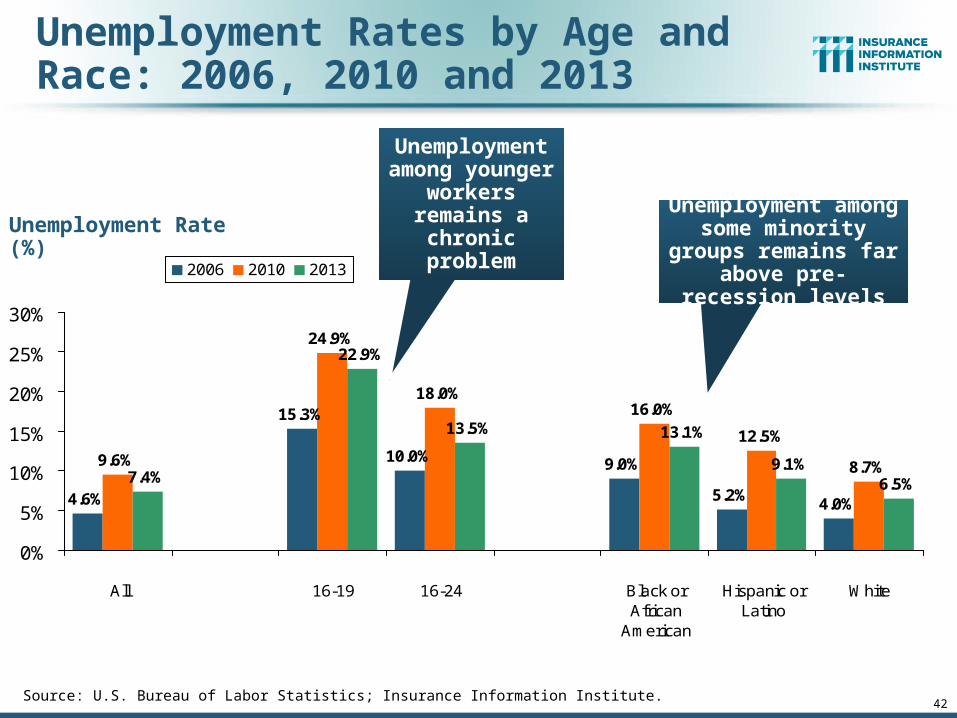

Unemployment Rates by Age and Race: 2006, 2010 and 2013

5.2%4.0%

9.6%

24.9%

18.0%16.0%

12.5%

8.7%

22.9%

13.5% 13.1%

9.1%6.5%

4.6%

15.3%

10.0% 9.0%7.4%

0%

5%

10%

15%

20%

25%

30%

All 16-19 16-24 Black orAfrican

American

Hispanic orLatino

White

2006 2010 2013

Unemployment Rate (%)

Unemployment among younger workers remains

a chronic problem

Source: U.S. Bureau of Labor Statistics; Insurance Information Institute.

Unemployment among some minority groups remains far above pre-

recession levels

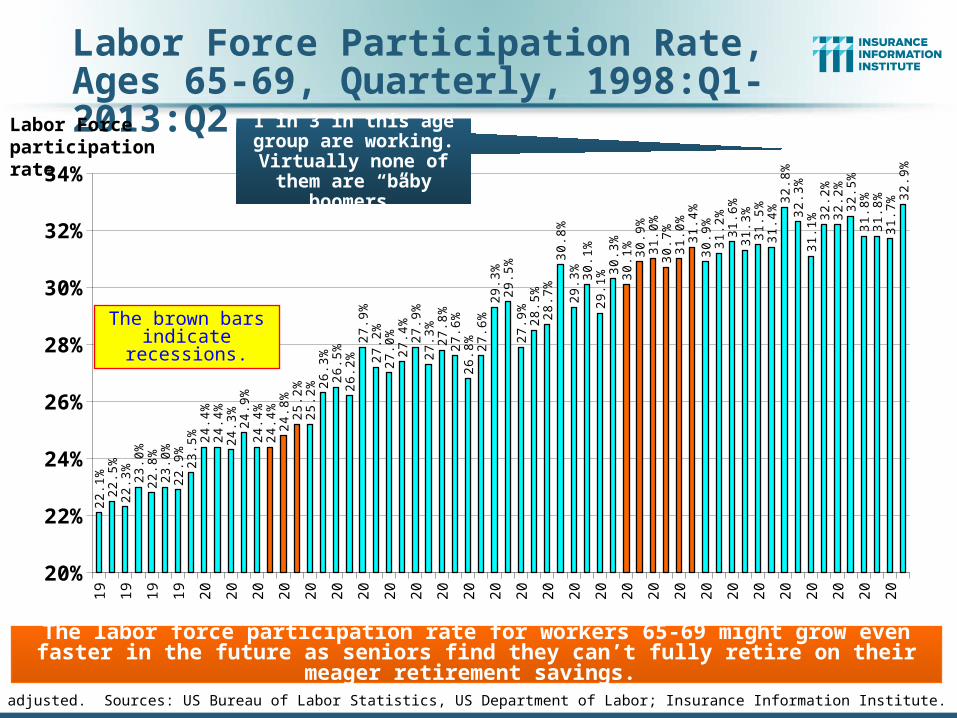

Labor Force Participation Rate, Ages 65-69, Quarterly, 1998:Q1-2013:Q21998.1

1998.3

1999.1

1999.3

2000.1

2000.3

2001.1

2001.3

2002.1

2002.3

2003.1

2003.3

2004.1

2004.3

2005.1

2005.3

2006.1

2006.3

2007.1

2007.3

2008.1

2008.3

2009.1

2009.3

2010.1

2010.3

2011.1

2011.3

2012.1

2012.3

2013.1

20%

22%

24%

26%

28%

30%

32%

34%

22.1%

22.5%

22.3% 23.0%

22.8%

23.0%

22.9% 23.5% 24.4%

24.4%

24.3% 24.9%

24.4%

24.4%

24.8%

25.2%

25.2%26.3%

26.5%

26.2%

27.9%

27.2%

27.0%

27.4%27.9%

27.3%27.8%

27.6%

26.8% 27.6%

29.3%

29.5%

27.9% 28.5%

28.7%

30.8%

29.3% 30.1%

29.1%30.3%

30.1% 30.9%

31.0%

30.7%

31.0%

31.4%

30.9%

31.2%

31.6%

31.3%

31.5%

31.4%32.8%

32.3%

31.1%32.2%

32.2%

32.5%

31.8%

31.8%

31.7%32.9%

Not seasonally adjusted. Sources: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

The brown bars indicate recessions.

Labor Force participation rate

The labor force participation rate for workers 65-69 might grow even faster in the future as seniors find they can’t fully retire on their meager retirement savings.

1 in 3 in this age group are working. Virtually

none of them are “baby boomers”

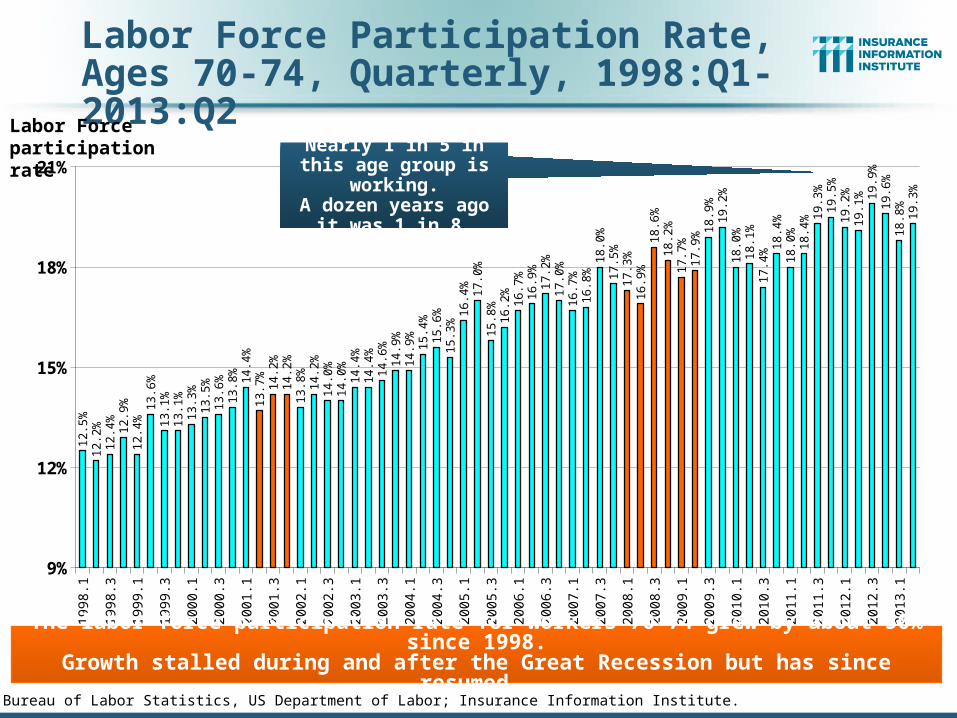

Labor Force Participation Rate,Ages 70-74, Quarterly, 1998:Q1-2013:Q2

19

98

.1

19

98

.3

19

99

.1

19

99

.3

20

00

.1

20

00

.3

20

01

.1

20

01

.3

20

02

.1

20

02

.3

20

03

.1

20

03

.3

20

04

.1

20

04

.3

20

05

.1

20

05

.3

20

06

.1

20

06

.3

20

07

.1

20

07

.3

20

08

.1

20

08

.3

20

09

.1

20

09

.3

20

10

.1

20

10

.3

20

11

.1

20

11

.3

20

12

.1

20

12

.3

20

13

.1

9%

12%

15%

18%

21%

12.5%

12.2%

12.4% 12.9%

12.4%

13.6%

13.1%

13.1%

13.3%

13.5%

13.6%

13.8% 14.4%

13.7% 14.2%

14.2%

13.8%14.2%

14.0%

14.0%14.4%

14.4%

14.6%

14.9%

14.9% 15.4%

15.6%

15.3%16.4% 17.0%

15.8%16.2% 16.7%

16.9%

17.2%

17.0%

16.7%

16.8%

18.0%

17.5%

17.3%

16.9%

18.6%

18.2%

17.7%

17.9%18.9%

19.2%

18.0%

18.1%

17.4%18.4%

18.0%18.4%19.3%

19.5%

19.2%

19.1% 19.9%

19.6%

18.8% 19.3%

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

Labor Force participation rate

The labor force participation rate for workers 70-74 grew by about 50% since 1998.Growth stalled during and after the Great Recession but has since resumed.

Nearly 1 in 5 in this age group is working.

A dozen years ago it was 1 in 8.

50

The Reindustrialization of America

American Industrial Might Is Making a Comeback

A Golden Opportunity for Workers Comp Insurers?

50

51

$200,000

$300,000

$400,000

$500,000

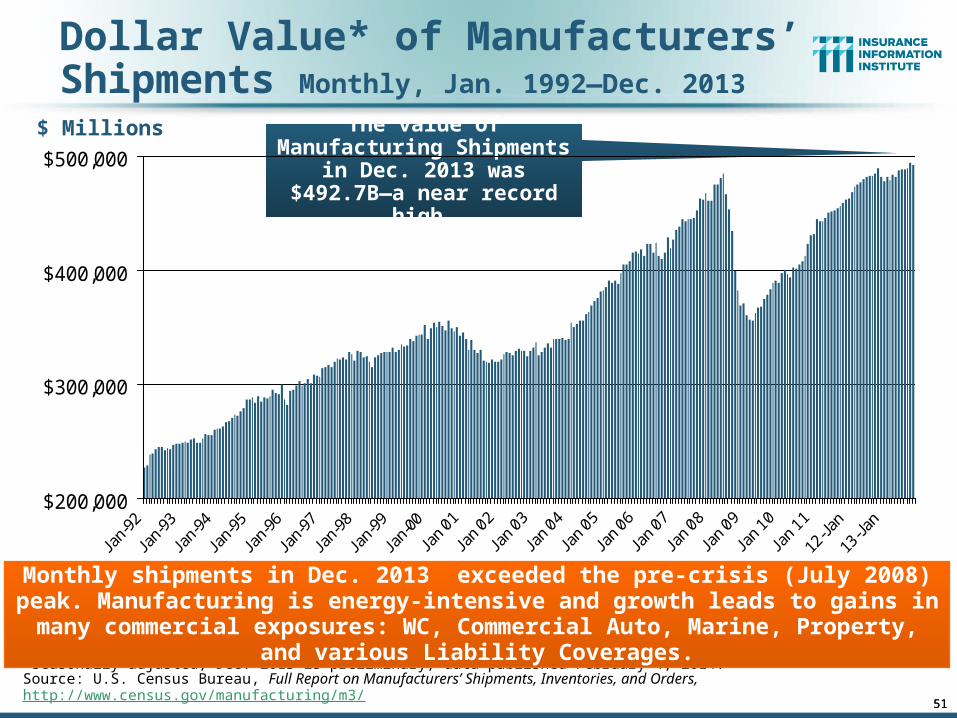

Dollar Value* of Manufacturers’ Shipments Monthly, Jan. 1992—Dec. 2013

*seasonally adjusted; Dec. 2013 is preliminary; data published February 4, 2014.Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Monthly shipments in Dec. 2013 exceeded the pre-crisis (July 2008) peak. Manufacturing is energy-intensive and growth leads to gains in many commercial

exposures: WC, Commercial Auto, Marine, Property, and various Liability Coverages.

$ Millions

51

The value of Manufacturing Shipments in Dec. 2013 was $492.7B—a near record high.

58

.35

7.1

60

.45

9.6

57

.85

5.3

55

.15

5.2

55

.3 56

.9 58

.25

8.5

60

.86

1.4

59

.75

9.7

54

.2 55

.85

1.4 52

.55

2.5

51

.85

2.2 53

.1 54

.15

1.9 5

3.3 54

.15

2.5

50

.25

0.5

50

.7 51

.65

1.7

49

.95

0.2

53

.1 54

.2

50

.74

9.0 5

0.9

55

.45

5.7

56

.25

6.4 57

.35

7.0

51

.9 53

.2

51

.3

40

45

50

55

60

65

Jan

-10

Fe

b-1

0M

ar-

10

Ap

r-1

0M

ay-

10

Jun

-10

Jul-

10

Au

g-1

0S

ep

-10

Oct

-10

No

v-1

0D

ec-

10

Jan

-11

Fe

b-1

1M

ar-

11

Ap

r-1

1M

ay-

11

Jun

-11

Jul-

11

Au

g-1

1S

ep

-11

Oct

-11

No

v-1

1D

ec-

11

Jan

-12

Fe

b-1

2M

ar-

12

Ap

r-1

2M

ay-

12

Jun

-12

Jul-

12

Au

g-1

2S

ep

-12

Oct

-12

No

v-1

2D

ec-

12

Jan

-13

Fe

b-1

3M

ar-

13

Ap

r-1

3M

ay-

13

Jun

-13

Jul-

13

Au

g-1

3S

ep

-13

Oct

-13

No

v-1

3D

ec-

13

Jan

-14

Fe

b-1

4

ISM Manufacturing Index(Values > 50 Indicate Expansion)

January 2010 through February 2014

The manufacturing sector expanded for 48 of the 50 months from Jan. 2010 through February 2014. Weakness in early 2014 stems largely from

harsh winter weather and weakness in China.

Source: Institute for Supply Management at http://www.ism.ws/ismreport/mfgrob.cfm; Insurance Information Institute.

Manufacturing continued to expand in early 2014

52

53

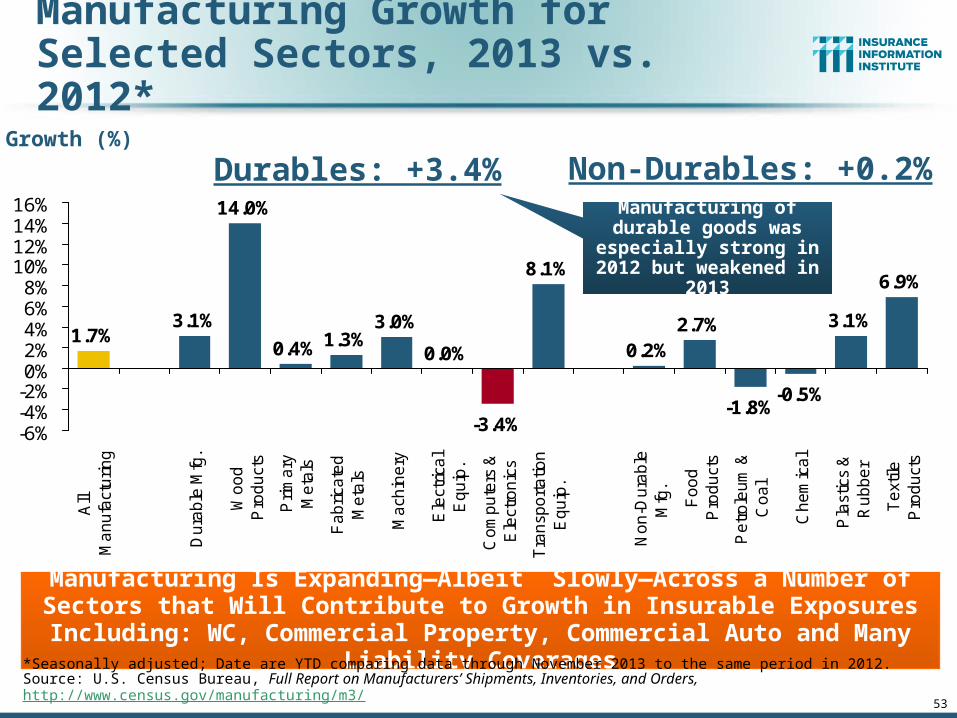

Manufacturing Growth for Selected Sectors, 2013 vs. 2012*

3.0%

0.0%

-3.4%

8.1%

0.2%2.7%

-1.8%-0.5%

3.1%

6.9%

1.7%3.1%

14.0%

0.4% 1.3%

-6%-4%-2%0%2%4%6%8%

10%12%14%16%

All

Ma

nu

fact

uri

ng

Du

rab

le M

fg.

Wo

od

Pro

du

cts

Pri

ma

ryM

eta

ls

Fa

bri

cate

dM

eta

ls

Ma

chin

ery

Ele

ctri

cal

Eq

uip

.

Co

mp

ute

rs &

Ele

ctro

nic

s

Tra

nsp

ort

atio

nE

qu

ip.

No

n-D

ura

ble

Mfg

.

Fo

od

Pro

du

cts

Pe

tro

leu

m &

Co

al

Ch

em

ica

l

Pla

stic

s &

Ru

bb

er

Te

xtile

Pro

du

cts

Manufacturing Is Expanding—Albeit Slowly—Across a Number of Sectors that Will Contribute to Growth in Insurable Exposures Including: WC, Commercial

Property, Commercial Auto and Many Liability Coverages

Growth (%)

Manufacturing of durable goods was especially

strong in 2012 but weakened in 2013

*Seasonally adjusted; Date are YTD comparing data through November 2013 to the same period in 2012.Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Durables: +3.4% Non-Durables: +0.2%

54

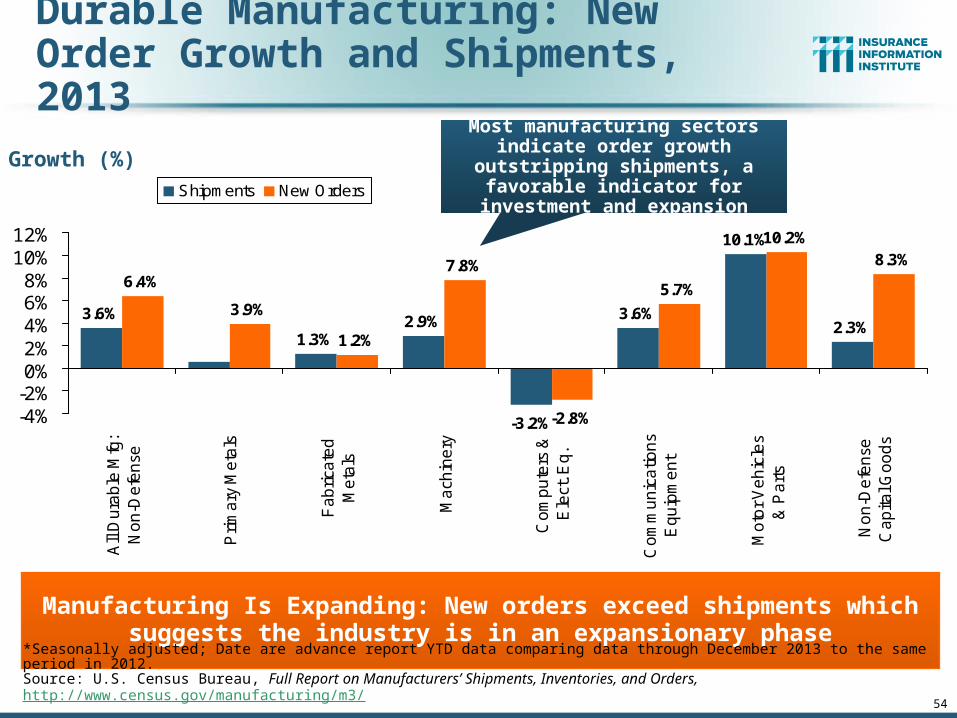

Durable Manufacturing: New Order Growth and Shipments, 2013

10.1%

2.3%

6.4%

3.9%

1.2%

7.8%

-2.8%

5.7%

10.2%8.3%

3.6%

1.3%2.9%

-3.2%

3.6%

-4%-2%0%2%4%6%8%

10%12%

All

Du

rab

le M

fg:

No

n-D

efe

nse

Pri

ma

ry M

eta

ls

Fa

bri

cate

dM

eta

ls

Ma

chin

ery

Co

mp

ute

rs &

Ele

ct. E

q.

Co

mm

un

ica

tion

sE

qu

ipm

en

t

Mo

tor

Ve

hic

les

& P

art

s

No

n-D

efe

nse

Ca

pita

l Go

od

s

Shipments New Orders

Manufacturing Is Expanding: New orders exceed shipments which suggests the industry is in an expansionary phase

Growth (%)Most manufacturing sectors indicate

order growth outstripping shipments, a favorable indicator for

investment and expansion

*Seasonally adjusted; Date are advance report YTD data comparing data through December 2013 to the same period in 2012.Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

66%

68%

70%

72%

74%

76%

78%

80%

82%

Mar

01

Jun 0

1

Sep

Dec

Mar

02

Jun 0

2

Sep

Dec

Mar

03

Jun 0

3

Sep

Dec

Mar

04

Jun 0

4

Sep

Dec

Mar

05

Jun 0

5

Sep

Dec

Mar

06

Jun 0

6

Sep

Dec

Mar

07

Jun 0

7

Sep

Dec

Mar

08

Jun 0

8

Sep

Dec

Mar

09

Jun 0

9

Sep

Dec

Mar

10

Jun 1

0

Sep

Dec

Mar

11

Jun 1

1

Sep

Dec

Mar

12

Jun 1

2

Sep

Dec

Mar

13

Jun 1

3

Sep

Dec

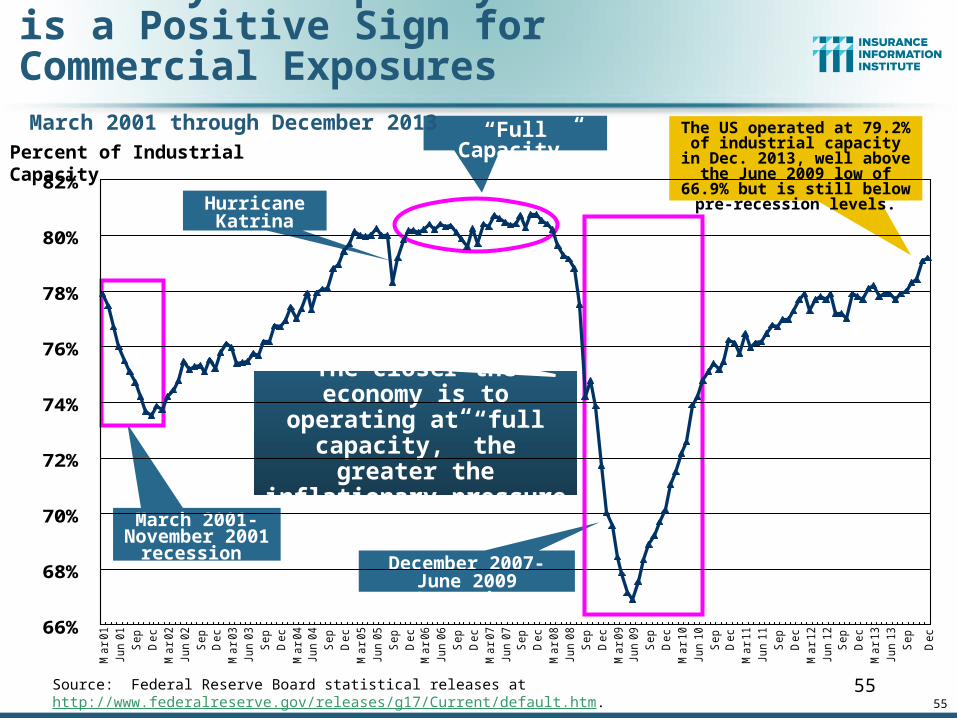

Recovery in Capacity Utilization is a Positive Sign for Commercial Exposures

Source: Federal Reserve Board statistical releases at http://www.federalreserve.gov/releases/g17/Current/default.htm. 55

Percent of Industrial Capacity

Hurricane Katrina

March 2001-November 2001

recession

“Full Capacity”

The closer the economy is to operating at “full

capacity,” the greater the inflationary pressure

The US operated at 79.2% of industrial capacity in Dec. 2013, well above the June

2009 low of 66.9% but is still below pre-recession levels.

December 2007-June 2009 Recession

March 2001 through December 2013

55

56

Manufacturing Employment,Jan. 2010—February 2014*

11

,46

01

1,4

60

11

,46

61

1,4

97

11

,53

11

1,5

39

11

,55

81

1,5

48

11

,55

41

1,5

55

11

,57

71

1,5

90

11

,62

41

1,6

62

11

,68

21

1,7

07

11

,71

51

1,7

24

11

,74

71

1,7

60

11

,76

21

1,7

70

11

,76

91

1,7

97

11

,84

11

1,8

70

11

,91

01

1,9

20

11

,92

61

1,9

35

11

,95

71

1,9

43

11

,92

51

1,9

31

11

,93

81

1,9

51

11

,96

51

1,9

88

11

,98

41

1,9

77

11

,97

21

1,9

65

11

,94

81

1,9

63

11

,99

31

2,0

11

12

,04

61

2,0

53

12

,05

91

2,0

65

11,250

11,500

11,750

12,000

12,250Ja

n-1

0F

eb

-10

Ma

r-1

0A

pr-

10

Ma

y-1

0Ju

n-1

0Ju

l-1

0A

ug

-10

Se

p-1

0O

ct-1

0N

ov-

10

De

c-1

0Ja

n-1

1F

eb

-11

Ma

r-1

1A

pr-

11

Ma

y-1

1Ju

n-1

1Ju

l-1

1A

ug

-11

Se

p-1

1O

ct-1

1N

ov-

11

De

c-1

1Ja

n-1

22

/30

/2M

ar-

12

Ap

r-1

2M

ay-

12

Jun

-12

Jul-

12

Au

g-1

2S

ep

-12

Oct

-12

No

v-1

2D

ec-

12

Jan

-13

Fe

b-1

3M

ar-

13

Ap

r-1

3M

ay-

13

Jun

-13

Jul-

13

Au

g-1

3S

ep

-13

Oct

-13

No

v-1

3D

ec-

13

Jan

-14

Fe

b-1

4

Manufacturing employment is a surprising source of strength in the economy. Employment in the sector is at a multi-year high.

*Seasonally adjusted; Jan. and Feb. 2014 are preliminarySources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

(Thousands) Since Jan 2010, manufacturing employment

is up (+605,000 or +5.3%)and still growing.

57

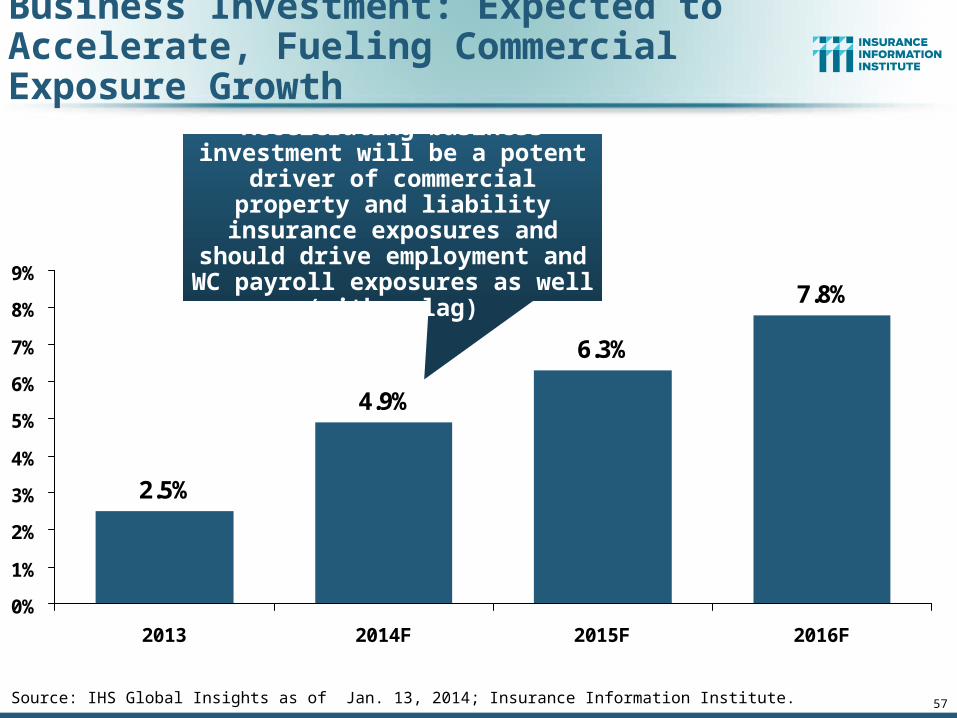

2.5%

4.9%

6.3%

7.8%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2013 2014F 2015F 2016F

Business Investment: Expected to Accelerate, Fueling Commercial Exposure Growth

Accelerating business investment will be a potent driver of

commercial property and liability insurance exposures and should drive employment and WC payroll

exposures as well (with a lag)

Source: IHS Global Insights as of Jan. 13, 2014; Insurance Information Institute.

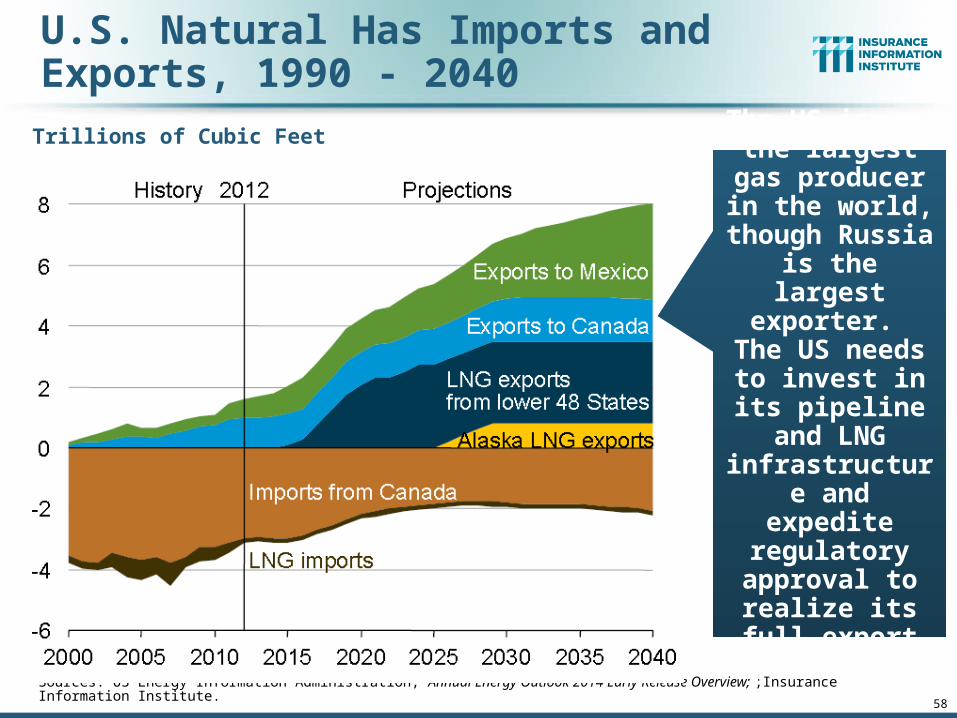

U.S. Natural Has Imports and Exports, 1990 - 2040

Sources: US Energy Information Administration, Annual Energy Outlook 2014 Early Release Overview; ;Insurance Information Institute. 58

Trillions of Cubic Feet

The US is now the largest gas producer in the world, though Russia is the

largest exporter. The US needs to

invest in its pipeline and

LNG infrastructure and expedite

regulatory approval to

realize its full export potential

59

Oil & Gas Extraction Employment,Jan. 2010—Feb. 2014*

*Seasonally adjustedSources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

156.

415

6.4

156.

715

7.6

158.

715

7.8

158.

015

9.5

160.

016

1.5

161.

216

1.2

163.

116

4.4

166.

616

9.3

170.

117

1.0

172.

517

3.6

176.

317

8.2

178.

518

0.9

181.

918

3.1

184.

818

5.2

185.

718

6.8

187.

618

8.0

188.

018

8.2

190.

019

1.7

191.

919

3.4

192.

419

2.6

193.

119

3.3

195.

019

6.5

199.

720

0.6

203.

020

4.1

206.

120

7.8

150

160

170

180

190

200

210

220

Jan-

10F

eb-1

0M

ar-1

0A

pr-1

0M

ay-1

0Ju

n-10

Jul-1

0A

ug-1

0S

ep-1

0O

ct-1

0N

ov-1

0D

ec-1

0Ja

n-11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

122/

30/2

Mar

-12

Apr

-12

May

-12

Jun-

12Ju

l-12

Aug

-12

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13F

eb-1

3M

ar-1

3A

pr-1

3M

ay-1

3Ju

n-13

Jul-1

3A

ug-1

3S

ep-1

3O

ct-1

3N

ov-1

3D

ec-1

3Ja

n-14

Feb

-14

Oil and gas extraction employment is up 32.9% since Jan. 2010 as the energy sector booms. Domestic energy production is essential to any robust economic recovery in

the US.

(Thousands) Highest since Aug.

1986

60

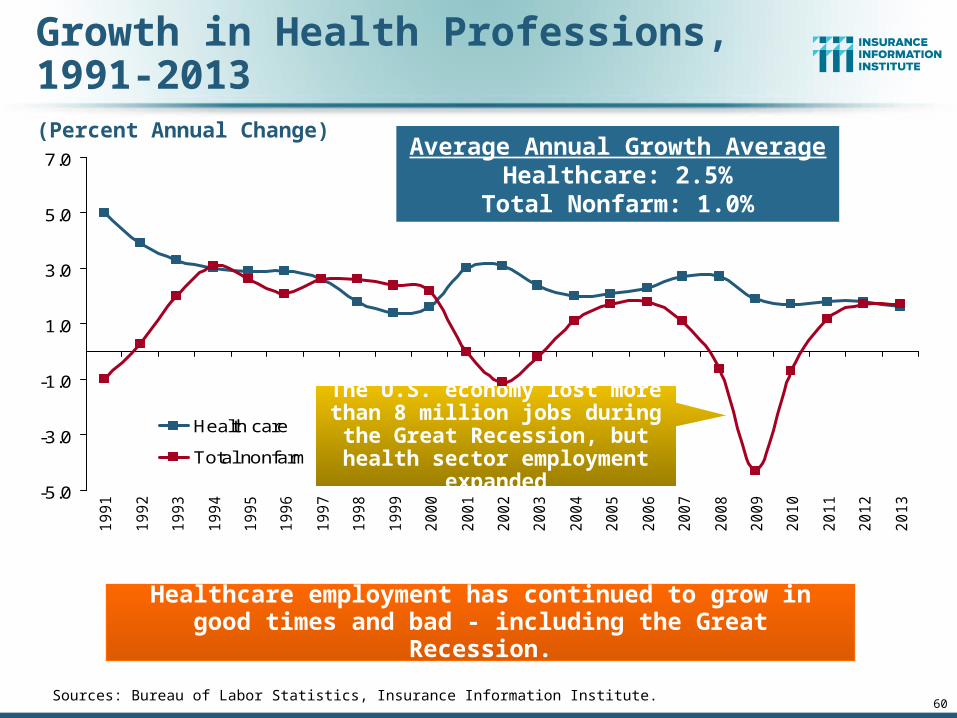

Growth in Health Professions,1991-2013

Sources: Bureau of Labor Statistics, Insurance Information Institute.

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Health care

Total nonfarm

(Percent Annual Change)

Healthcare employment has continued to grow in good times and bad - including the Great Recession.

Average Annual Growth AverageHealthcare: 2.5%

Total Nonfarm: 1.0%

The U.S. economy lost more than 8 million jobs during the Great Recession, but health sector

employment expanded

Healthcare Support

Healthcare Practitioners

Construction

Personal Care and Service

Computer and Math

Social Service

Business & Financial

Groundskeeping/Janitorial

Education

All Occupations

Legal

Life, Phys and Social Science

Repair

Food Preparation

Transportation

Fire, Police, Etc.

Architects and Engineers

Sales

Management

Arts and Media

Administrative Support

Production

Farming

28.1

21.5

21.4

20.9

18

17.2

12.5

12.5

11.1

10.8

10.7

10.1

9.6

9.4

8.6

7.9

7.3

7.3

7.2

7

6.8

0.8-3.4

Source: Bureau of Labor Statistics, Insurance Information Institute.

Occupations Ranked by Projected Percentage Growth, 2012-2022F (Millions)

61

Healthcare professions are expected to grow at 2 to

nearly 3 times employment growth overall

62

The Future of Healthcare in America

Workers Comp Is Increasingly Along for the Ride in the

American Health Care Saga

62

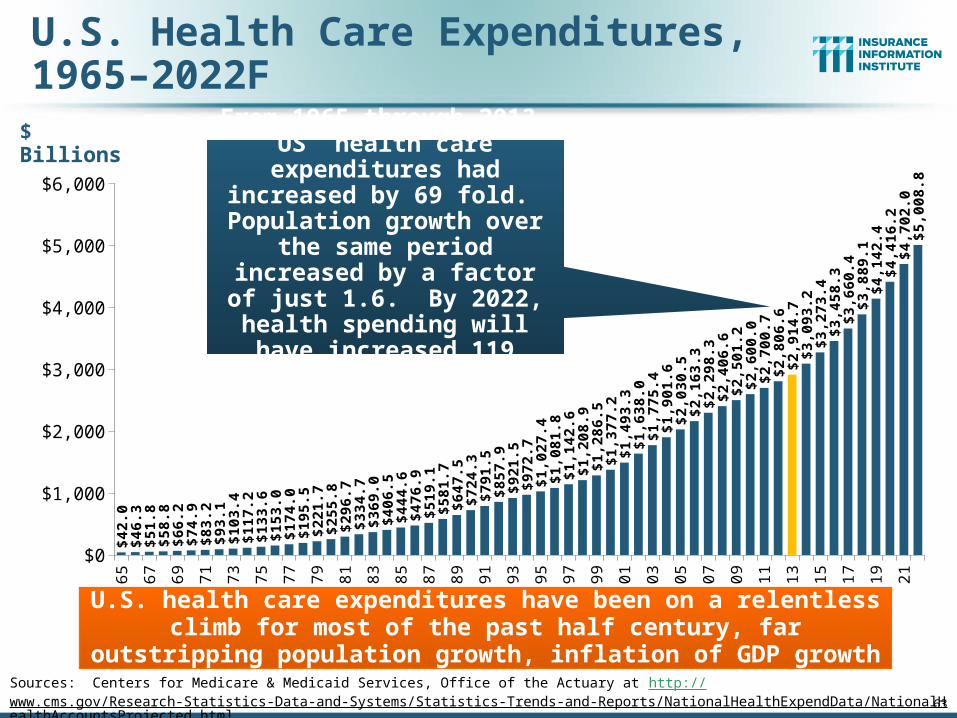

U.S. Health Care Expenditures,1965–2022F

65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$42.

0$4

6.3

$51.

8$5

8.8

$66.

2$7

4.9

$83.

2$9

3.1

$103

.4$1

17.2

$133

.6$1

53.0

$174

.0$1

95.5

$221

.7$2

55.8

$296

.7$3

34.7

$369

.0$4

06.5

$444

.6$4

76.9

$519

.1$5

81.7

$647

.5$7

24.3

$791

.5$8

57.9

$921

.5$9

72.7

$1,0

27.4

$1,0

81.8

$1,1

42.6

$1,2

08.9

$1,2

86.5

$1,3

77.2

$1,4

93.3

$1,6

38.0

$1,7

75.4

$1,9

01.6

$2,0

30.5

$2,1

63.3

$2,2

98.3

$2,4

06.6

$2,5

01.2

$2,6

00.0

$2,7

00.7

$2,8

06.6

$2,9

14.7

$3,0

93.2

$3,2

73.4

$3,4

58.3

$3,6

60.4

$3,8

89.1

$4,1

42.4

$4,4

16.2

$4,7

02.0

$5,0

08.8

U.S. health care expenditures have been on a relentless climb for most of the past half century, far outstripping population growth,

inflation of GDP growth

63

From 1965 through 2013, US health care expenditures had

increased by 69 fold. Population growth over the same period increased by a factor of just 1.6. By 2022, health spending will have

increased 119 fold.

$ Billions

Sources: Centers for Medicare & Medicaid Services, Office of the Actuary at http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsProjected.html accessed 3/14/14; Insurance Information Institute.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22

National Health Care Expenditures as a Share of GDP, 1965 – 2022F*

Sources: Centers for Medicare & Medicaid Services, Office of the Actuary at http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsProjected.html accessed 3/14/14; Insurance Information Institute.

1965 5.8%

Health care expenditures as a share of GDP rose from 5.8% in 1965 to 18.0% in 2013 and are expected to

reach 19.9% of GDP by 2022

% of GDP

2022 19.9%

1980: 9.2%

1990: 12.5%

2000: 13.8%

2010: 17.9%

Since 2009, heath expenditures as a %

of GDP have flattened out at about 18%--the

question is why and will it last?

65

63.1%650.7%

2235.9%

6839.8%

0%

1000%

2000%

3000%

4000%

5000%

6000%

7000%

8000%

Population CPI GDP Health CareExpenditures

Rate of Health Care Expenditure Increase Compared to Population, CPI and GDP

Accelerating business investment will be a potent driver of

commercial property and liability insurance exposures and should drive employment and WC payroll

exposures as well (with a lag)

Source: Insurance Information Institute research.

1965: 194.3 Mill

2013: 317.0 Mill

1965: $719.1 Bill

2013: $16,797.5 Bill

1965: $42.0 Bill

2013: $2,914.7 Bill

-1%

0%

1%

2%

3%

4%

5%

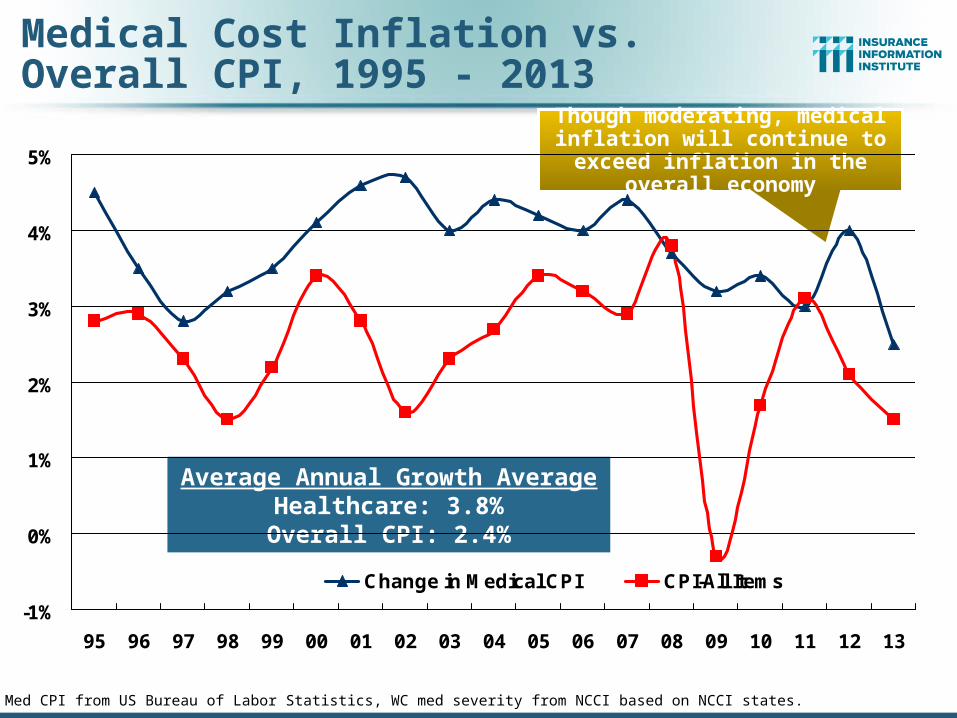

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Change in Medical CPI CPI-All Items

Medical Cost Inflation vs. Overall CPI, 1995 - 2013

Sources: Med CPI from US Bureau of Labor Statistics, WC med severity from NCCI based on NCCI states.

Average Annual Growth AverageHealthcare: 3.8%Overall CPI: 2.4%

Though moderating, medical inflation will continue to exceed inflation in the overall economy

67

Possible Effects of the Affordable Care Act (“ObamaCare”) on

Workers Compensation

67

4.5%

3.5%2.8%

3.2%3.5%4.1%

4.6%4.7%4.0%

4.4%4.2%4.0%4.4%

3.7%3.2%3.4%

3.0%

5.1%

7.4%

10.1%10.6%

13.5%

5.4%

7.8%

6.3%6.6%

4.1%3.6% 4%

3%

1.4%

5.4%

8.8%

7.7%

7.3%

8.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

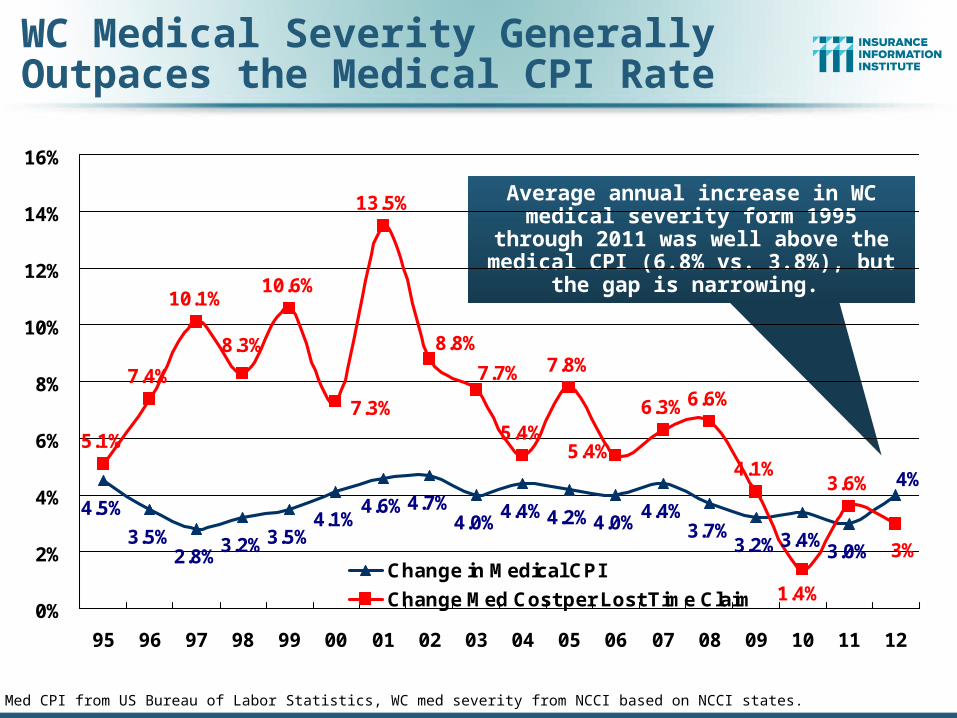

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Change in Medical CPI

Change Med Cost per Lost Time Claim

WC Medical Severity Generally Outpaces the Medical CPI Rate

Sources: Med CPI from US Bureau of Labor Statistics, WC med severity from NCCI based on NCCI states.

Average annual increase in WC medical severity form 1995 through 2011 was well above the medical CPI (6.8% vs. 3.8%), but

the gap is narrowing.

Issue Concern Contravening Argument

Surge in People Covered by Health Insurance

• System is overwhelmed

• MD shortage

• Patient care adversely impacted

• Over time, people will have access to preventative care, improving the general health of the population

• Greater use of PA’s, etc.

Electronic Health Records

• Cost

• Computerization of patient data could help flag issues and improve risk management and improve patient outcomes

Claim Shifting• Provider/patient may

prefer claim handled via WC system

• Reduction in uninsured population reduces shifting

Source: Insurance Information Institute research; WCRI. 69

A Few Potential Impacts of the ACA on Workers Compensation

0%

50%

100%

150%

200%

250%

300%

350%

MA HI

WV

MD

FL

CA

TX MI

UT

VT

NY

NC

PA

OH

WA

CO

ND

SC

KY

KS

SD

WY

AR

OK

GA

MN

ME

MO

AZ

NM

TN

LA

MS

AL

NE

CT

OR

NV ID RI

IL

AK

● WC rates often tied to WC but can change for reasons independent of this link

● There could be both positive and negative effects of a cut in Medicare rates on WC performance in states which tie reimbursement to Medicare

– WC reimbursement rates would go down

– Doctors may be unwilling to see WC patients:

64% of Dr.’s surveyed said they would stop accepting new Medicare patients if planned rate cuts go through; some of these same doctors may also refuse WC patients if WC rates also decrease

● These effects would likely be short lived

– All states which tie their fee schedules to Medicare already increase the Medicare rates to set WC rates, so any drop in the Medicare rates would likely be soon offset by a higher WC adjustment

ACA Impact on WC May Occur via Changes in Rates Set by State Regulators

WC Maximum Allowable Reimbursement Rates

as Percentage of Medicare

SOURCE: NCCI Annual Issues Symposium 2009, Medicare’s Impact on Workers’ Compensation, AMA: “Physicians’ reactions to the Medicare physician payment cuts” from 3/13/13 presentation by Christopher Cunniff, FCAS, of Liberty Mutual.

WC rates tied to Medicare

WC rates not tied to Medicare

PPACA May Have Distinct Impacts on WC Depending on Claim Frequency/Severity

High Volume, Low

Severity

Complicated

Catastrophic Injuries

• Expanded coverage may shift some small claims to the health insurance system (+)

• Physician access problems could lead to indemnity increases and may bleed into the complicated cases (-)

• Preventative care and early record keeping decreases WC comorbidities (+)

• Soft tissue treatments, a large portion of “slow burn claims,” may decrease in cost (+)

• No significant impacts

Ex: med only, quick to settle, <25K

Ex: back pain claims, very litigious

Ex: spinal cord injury, multiple trauma claims

Potential ACA Impact

SOURCE: Dr. Glenn Pransky, Liberty Mutual Research Institute for Health & Safety extracted from from 3/13/13 presentation by Christopher Cunniff, FCAS, of Liberty Mutual: Impacts of Healthcare Reform on Workers Compensation,

Industry Portfolio by Claim Type(Relative Volume by Claim Frequency & Paid Dollars)

73

AK

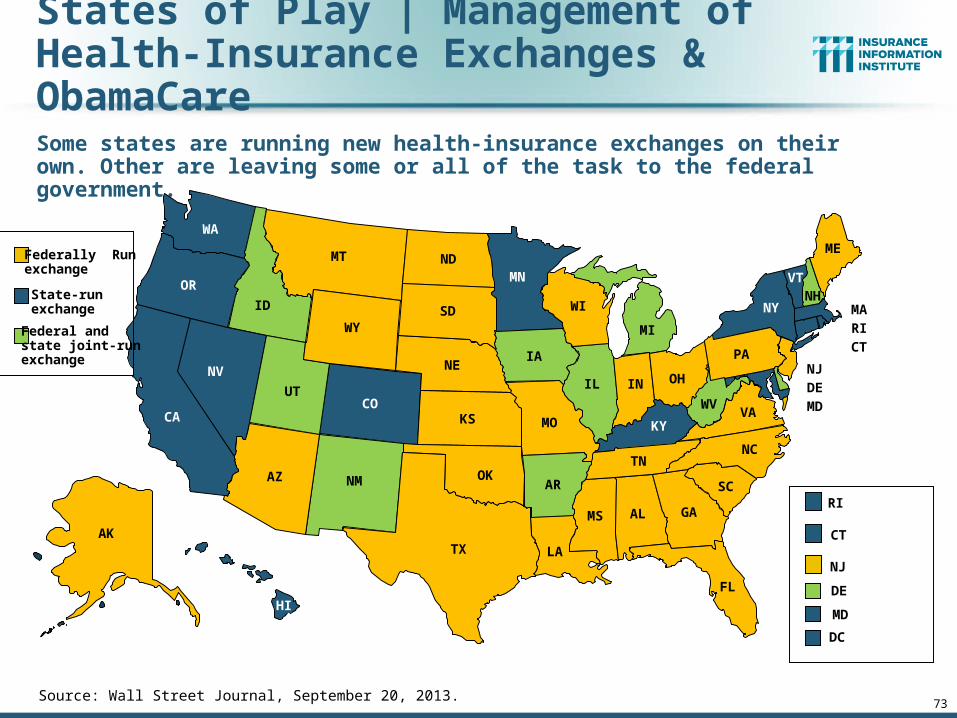

States of Play | Management of Health-Insurance Exchanges & ObamaCare

Some states are running new health-insurance exchanges on their own. Other are leaving some or all of the task to the federal government.

ME

PA

WVVA

NC

LATX

OK

NE

NDMN

MI

IL

IA

ID

WA

OR

AZ

NJ

VT

NY

SC

GA

TN

AL

FL

MS

ARNM

KYMOKS

SD WI

IN OH

MT

CA

NV

UT

WY

CO

NH

DE

MD

MA

RI

CT

HI

Source: Wall Street Journal, September 20, 2013.

Federally Run exchange

State-runexchange

Federal and state joint-runexchange

RI

CT

NJ

DE

MD

DC

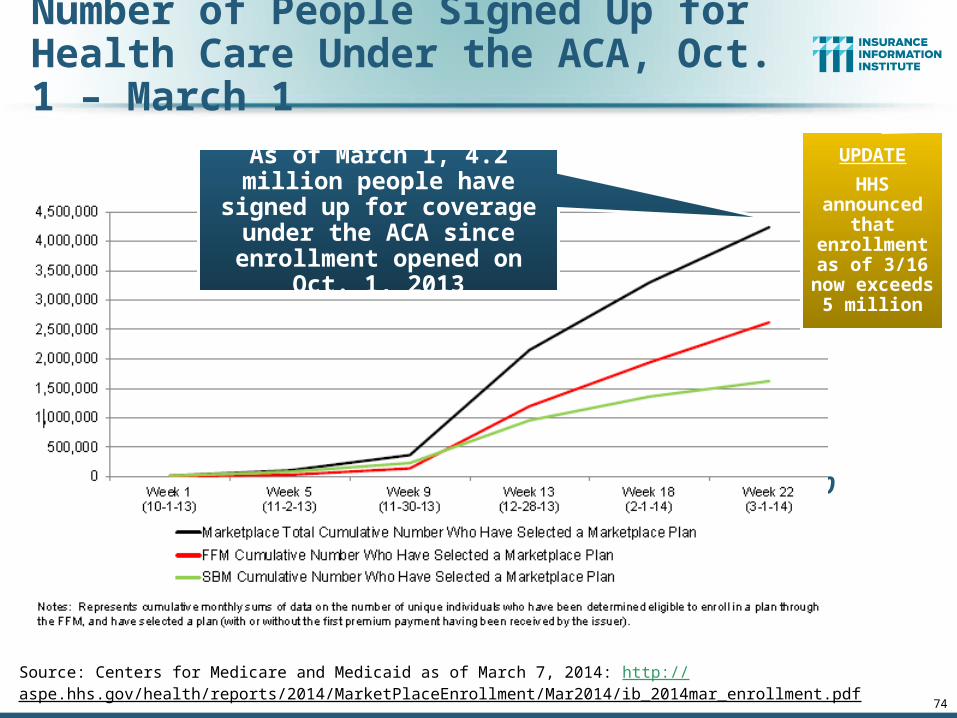

Number of People Signed Up for Health Care Under the ACA, Oct. 1 – March 1

74

759,800

Source: Centers for Medicare and Medicaid as of March 7, 2014: http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Mar2014/ib_2014mar_enrollment.pdf

As of March 1, 4.2 million people have signed up for coverage under the ACA

since enrollment opened on Oct. 1, 2013

UPDATE

HHS announced

that enrollment as of 3/16 now exceeds 5

million

75

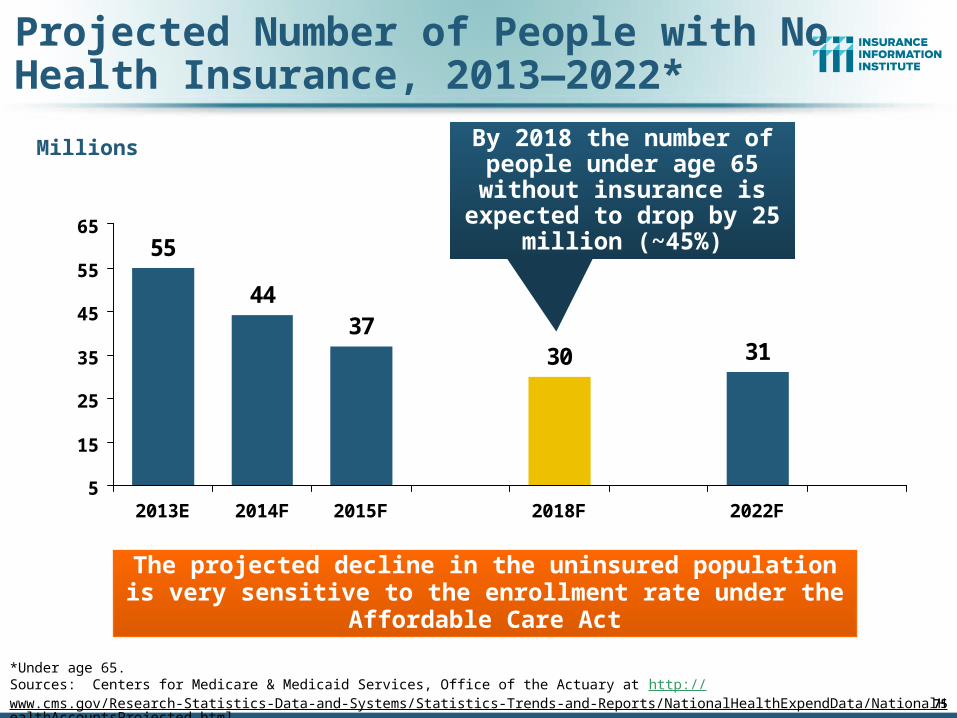

Projected Number of People with No Health Insurance, 2013—2022*

31

55

4437

30

5

15

25

35

45

55

65

2013E 2014F 2015F 2018F 2022F

Millions

The projected decline in the uninsured population is very sensitive to the enrollment rate under the Affordable Care Act

By 2018 the number of people under age 65 without

insurance is expected to drop by 25 million (~45%)

75

*Under age 65.Sources: Centers for Medicare & Medicaid Services, Office of the Actuary at http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsProjected.html accessed 3/14/14; Insurance Information Institute.

Will Skill Shortages in the Medical Field Adversely

Impact WC?

76

Concern that the ACA Will Overwhelm the Healthcare Delivery System, Harming

Outcomes76

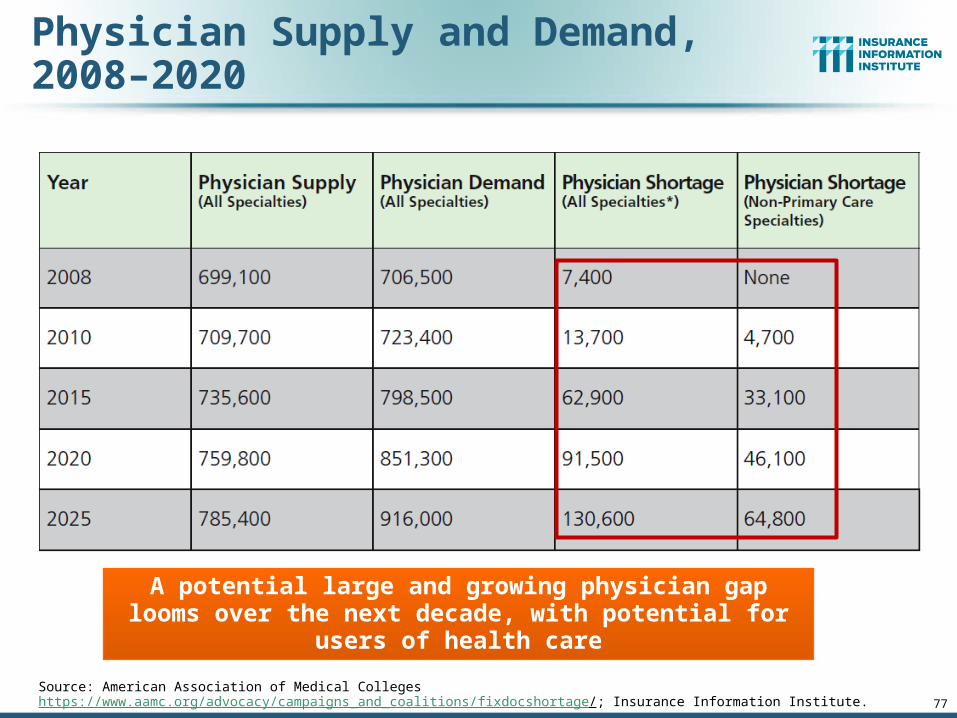

Physician Supply and Demand, 2008–2020

Source: American Association of Medical Colleges https://www.aamc.org/advocacy/campaigns_and_coalitions/fixdocshortage/; Insurance Information Institute. 77

A potential large and growing physician gap looms over the next decade, with potential for users of health care

80

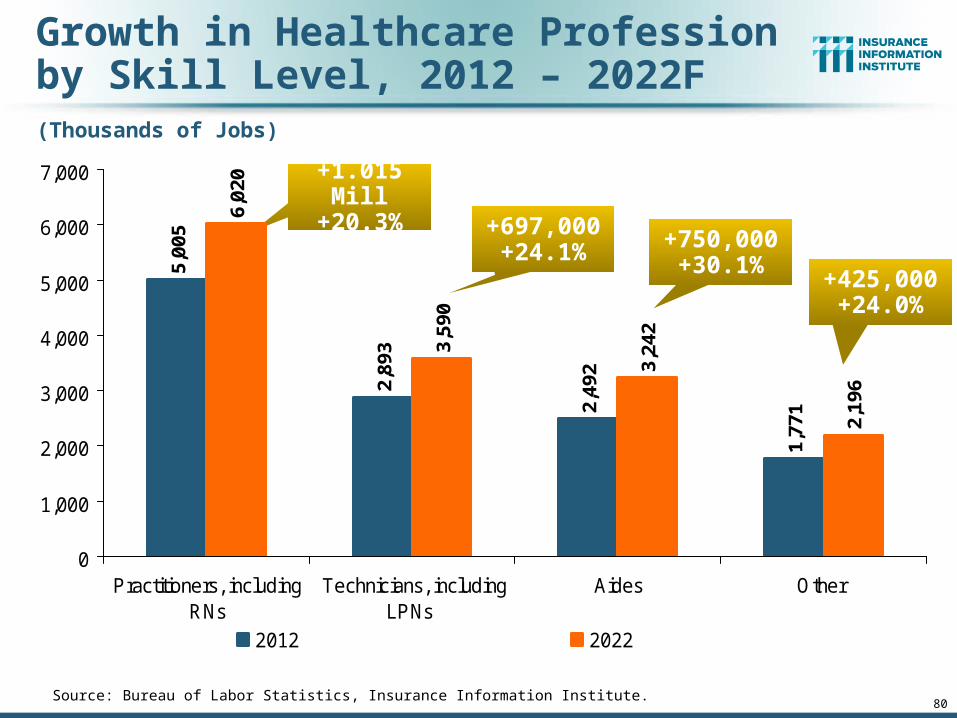

Growth in Healthcare Profession by Skill Level, 2012 – 2022F

Source: Bureau of Labor Statistics, Insurance Information Institute.

5,00

5

2,89

3

2,49