Meeting Agenda | Board of Directors- Strategic Planning Retreat€¦ · · 2017-10-18Meeting...

184

Meeting Agenda | Board of Directors- Strategic Planning Retreat Thursday, October 19, 2017 │ 9:00am. - 3:30pm. Nexsen Pruet │1230 Main Street Suite 700 Columbia, SC 29201 Educational Program Session I. Call to Order 9:00am II. Pension Plan Design- Gabriel Roeder Smith & Company 9:05am III. Fiduciary Education- Mr. Rob Gauss- Ice Miller 11:00am LUNCH 12:00pm IV. Ethics Training- Mr. Dennis Gatlin 12:30pm V. Healthcare Landscape 1:30pm VI. Adjournment 3:30pm

Transcript of Meeting Agenda | Board of Directors- Strategic Planning Retreat€¦ · · 2017-10-18Meeting...

Meeting Agenda | Board of Directors- Strategic Planning Retreat Thursday, October 19, 2017 │ 9:00am. - 3:30pm. Nexsen Pruet │1230 Main Street Suite 700 Columbia, SC 29201

Educational Program Session I. Call to Order 9:00am

II. Pension Plan Design- Gabriel Roeder Smith & Company 9:05am

III. Fiduciary Education- Mr. Rob Gauss- Ice Miller 11:00am

LUNCH 12:00pm

IV. Ethics Training- Mr. Dennis Gatlin 12:30pm

V. Healthcare Landscape 1:30pm

VI. Adjournment 3:30pm

PUBLIC EMPLOYEE BENEFIT AUTHORITY AGENDA ITEM BOARD RETREAT

Meeting Date: October 19, 2017 1. Subject: Pension Plan Design 2. Summary: Danny White and Joe Newton from Grabriel Roeder Smith & Company will lead a discussion related to alternative retirement plan designs. 3. What is the Board asked to do? Receive as Information 4. Supporting Documents:

(a) List those attached: Retirement Plan Designs

Copyright © 2017 GRS – All rights reserved.

South Carolina PEBA

Retirement Plan Designs

Joe Newton, FSA, EA, MAAA

Danny White, FSA, EA, MAAA

October 19, 2017

Agenda

• Overview of SCRS Plan Design

• Plan Demographics

• Current Financial State

• Plan Design Basics

• Maximizing Efficiencies

• Sample designs enacted by other States

2

OVERVIEW OF SCRS

PLAN DESIGN

SCRS Designs

• The main retirement income programs maintained by SCRS are Defined Benefit (DB) Plans

– The plan defines the benefit payable at retirement

• Some members have the option to choose ORP at date of hire, which is a Defined Contribution (DC) Plan

– The plan defines the contribution provided to the employee’s retirement account

4

Summary of Benefits – SCRS

Benefit Feature Class Two

(Hired prior July 1, 2012)

Class Three (Hired after June 30, 2012)

Benefit Multiplier per Year of Service

1.82% 1.82%

Final Average Salary High 3 Years High 5 Years

Retirement Eligibility Age 65 & 5 Svc ; or

28 Svc Age 65 & 8 Svc; or

Rule of 90

Benefit Adjustment (COLA) Lesser 1% or $500 Lesser 1% or $500

Early Retirement (Reduced) Age 55 & 25 Svc; or

Age 60 & 5 Svc Age 60 & 8 Svc

5

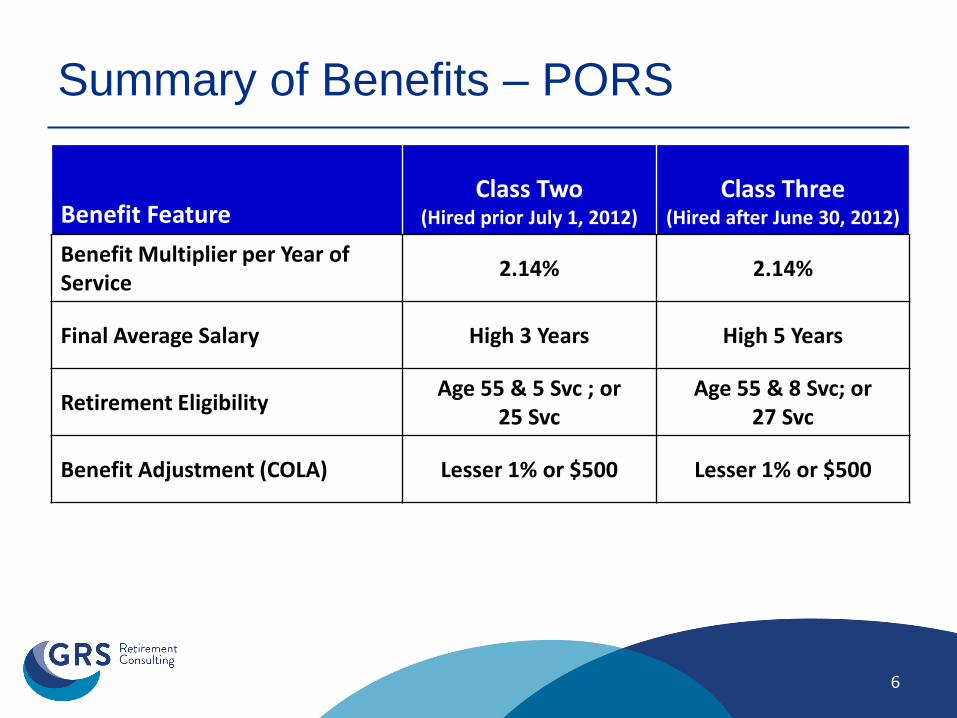

Summary of Benefits – PORS

Benefit Feature Class Two

(Hired prior July 1, 2012)

Class Three (Hired after June 30, 2012)

Benefit Multiplier per Year of Service

2.14% 2.14%

Final Average Salary High 3 Years High 5 Years

Retirement Eligibility Age 55 & 5 Svc ; or

25 Svc Age 55 & 8 Svc; or

27 Svc

Benefit Adjustment (COLA) Lesser 1% or $500 Lesser 1% or $500

6

PLAN DEMOGRAPHICS

Active and Retired Members - SCRS

206,767 205,370 208,369 207,669 211,259 215,564

115,550 121,927 127,696 131,510 134,640 137,855

0

50,000

100,000

150,000

200,000

250,000

2011 2012 2013 2014 2015 2016

Active Members Retired Members

8

Active and Retired Members - PORS

26,650 26,179 26,194 26,697 26,575 26,651

13,358 14,653

15,617 16,103 16,709 17,288

0

5,000

10,000

15,000

20,000

25,000

30,000

2011 2012 2013 2014 2015 2016

Active Members Retired Members

9

Projected Membership - SCRS

0

50,000

100,000

150,000

200,000

250,000

2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031

Nu

mb

er

January 1,

Projected Number of Class Two, Class Three, and ORP Members

ORP Class Two Class Three

10

Projected Membership - PORS

0

5,000

10,000

15,000

20,000

25,000

30,000

2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031

Nu

mb

er

January 1,

Projected Number of Class Two and Class Three Members

Class Two Class Three

11

Cost of Benefits in SCRS and PORS –

Total Normal Cost

9.00% 9.75%

1.65%

5.25%

0%

2%

4%

6%

8%

10%

12%

14%

16%

SCRS PORS

% o

f P

ay

Employer

Member

12

PRINCIPALS OF PLAN DESIGN

Types of Retirement Plans

• Defined Benefit (DB) Plans – The plan defines the benefit payable at retirement

• Defined Contribution (DC) Plans – The plan defines the contribution provided to the

employee’s retirement account

• Hybrid Plans – A retirement program that combines elements of both DB

and DC plans.

– Some are true blends, or a hybrid of the elements, while others are just the member participating in multiple smaller versions of the more basic plan types

14

• Benefit Adequacy - Provide an adequate level of benefits so members may retire at an appropriate age

• Cost Sharing – Sharing the costs appropriately between the employer and member

• Risk Sharing - Sharing the risks appropriately between the employer and member

• Sustainability - Self-correcting mechanisms can substantially increase the plan’s ability to withstand adverse experience

Principals in Design Assessment

15

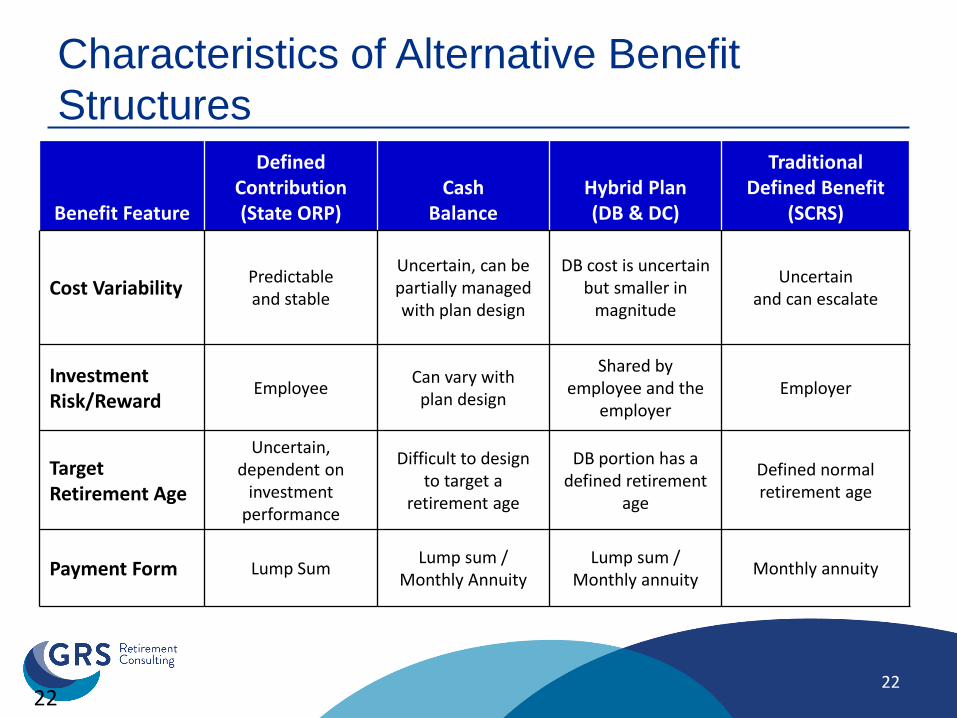

Characteristics of Alternative Benefit

Structures

Member Employer

What is the Appropriate Balance for Sharing the Risk?

Cash Balance

Hybrid Plan (DB and DC)

Defined Contribution (State ORP)

Traditional Defined Benefit (SCRS)

Member Employer

16

“Hybrid” Plans

• A design with a smaller DB benefit and a smaller DC benefit that provides an adequate retirement benefit on a combined basis

• The defined benefit portion of the plan is designed to prove a lifetime annuity

• Investment and longevity risks are shared between the employee and employer

• Significant flexibility in hybrid plan designs

17

“Stacked” Hybrid Plans

• The DB component would cap or limit the income covered by the DB plan to some fixed amount (e.g., $50,000 indexed for inflation)

• Employees would earn a DC benefit on income in excess of the cap in the DB plan

• The cap could be set so that employees with typical earnings would be fully covered by the DB benefit

• Design shifts some of the risks to members with higher incomes, who may be better able to manage the risks

18

“Stacked” Hybrid Plans

DB DC DB

DC

Specified Earnings

Level

Chart based on Alicia Munnell, A Role for Defined Contribution Plans in the Private Sector, Center for Retirement Research at Boston College, 2011.

19

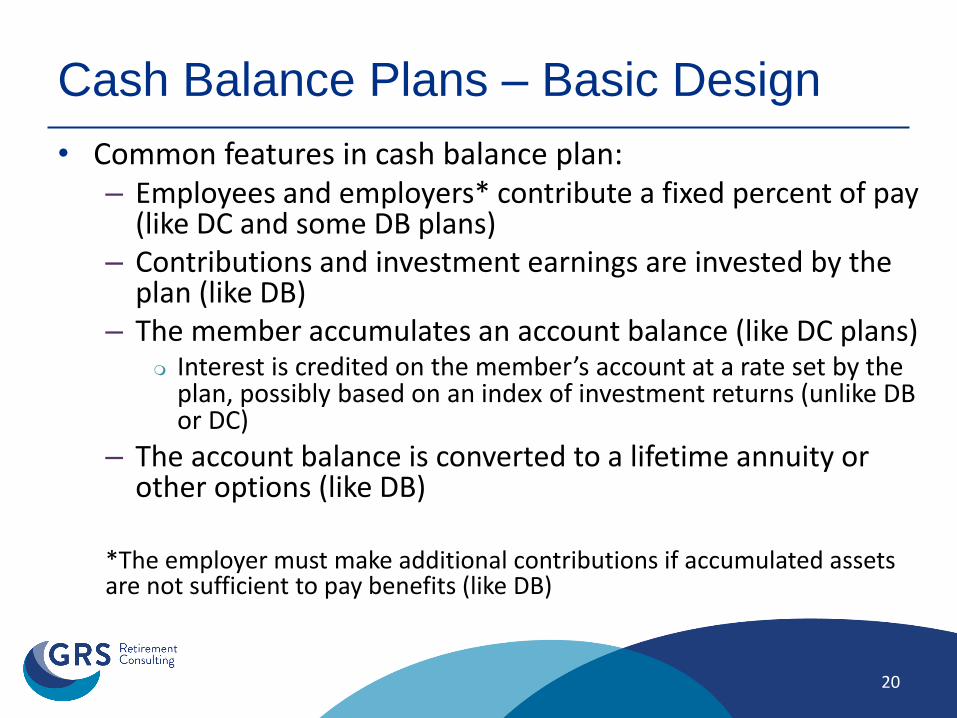

Cash Balance Plans – Basic Design

• Common features in cash balance plan: – Employees and employers* contribute a fixed percent of pay

(like DC and some DB plans) – Contributions and investment earnings are invested by the

plan (like DB) – The member accumulates an account balance (like DC plans)

Interest is credited on the member’s account at a rate set by the plan, possibly based on an index of investment returns (unlike DB or DC)

– The account balance is converted to a lifetime annuity or other options (like DB)

*The employer must make additional contributions if accumulated assets are not sufficient to pay benefits (like DB)

20

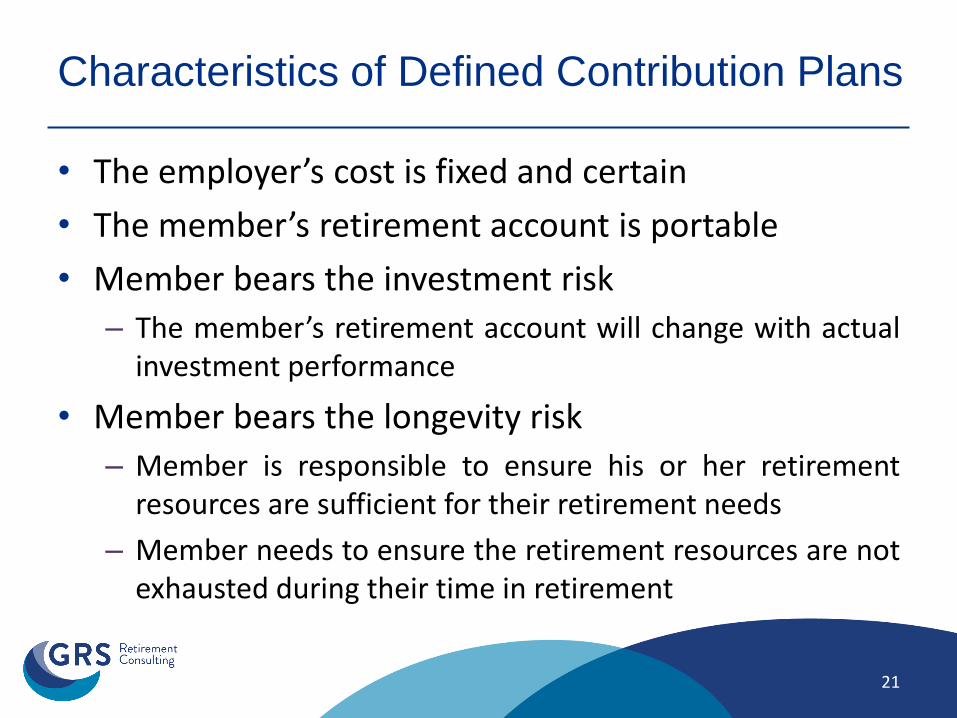

Characteristics of Defined Contribution Plans

• The employer’s cost is fixed and certain

• The member’s retirement account is portable

• Member bears the investment risk

– The member’s retirement account will change with actual investment performance

• Member bears the longevity risk

– Member is responsible to ensure his or her retirement resources are sufficient for their retirement needs

– Member needs to ensure the retirement resources are not exhausted during their time in retirement

21

22

Characteristics of Alternative Benefit

Structures

Benefit Feature

Defined Contribution (State ORP)

Cash Balance

Hybrid Plan (DB & DC)

Traditional Defined Benefit

(SCRS)

Cost Variability Predictable and stable

Uncertain, can be partially managed with plan design

DB cost is uncertain but smaller in

magnitude

Uncertain and can escalate

Investment Risk/Reward

Employee Can vary with

plan design

Shared by employee and the

employer Employer

Target Retirement Age

Uncertain, dependent on

investment performance

Difficult to design to target a

retirement age

DB portion has a defined retirement

age

Defined normal retirement age

Payment Form Lump Sum Lump sum /

Monthly Annuity Lump sum /

Monthly annuity Monthly annuity

22

Advantages and Disadvantages

of DB and DC Plans

Advantages/Disadvantages of

DB Plans Related to Goals

24

Goals DB Plan Advantages DB Plan Disadvantages

Attract & Retain Qualified Employees

• Rewards long-term service & helps retain employees

• Provides disability & survivor benefits

• Less portable than DC benefits

• May not appeal to younger, more mobile employees

Sufficient & Sustainable Benefits

• Provides lifetime benefits • Pools risks related to

investment, longevity, and inflation

• Usually requires longer vesting periods than DC

• Investment, longevity, and inflation risks fall on the employer

Stable & Affordable Contributions

• Employer contribution rates may fall during periods of strong investment performance

• Employer contribution rates may rise during periods of poor investment performance

24

Advantages/Disadvantages of

DC Plans Related to Goals Goals DC Plan Advantages DC Plan Disadvantages

Attract & Retain Qualified Employees

• May appeal to younger, more mobile employees

• May not be especially effective in retaining employees

Sufficient & Sustainable Benefits

• Members have control over investment selection

• Transfers investment, longevity, and inflation risk to employees

• Investment administration and management fees

Stable & Affordable Contributions

• Stable employer contribution rates

• Poor investment performance may result in pressure to increase contribution rates or return to a DB plan

25

Advantages/Disadvantages of DC

Plans Related to Goals Hire\Term Age 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62

25 100% 100% 100% 100% 100% # # # # # # # # # # # # # # # 912% 649% 495% 395% 325% 273% 233% 201% 176% 155% 137% 122% 109% 98% 89% 80% 84% 87% 91% 96% 101% 106% 112%

26 100% 100% 100% 100% 100% 100% # # # # # # # # # # # # 817% 597% 463% 373% 309% 261% 224% 194% 170% 150% 133% 119% 107% 96% 87% 79% 82% 85% 89% 93% 98% 103% 109%

27 100% 100% 100% 100% 100% 100% 100% # # # # # # # # # 740% 553% 435% 354% 295% 250% 216% 188% 165% 146% 130% 116% 104% 94% 85% 77% 80% 83% 87% 91% 96% 101% 106%

28 100% 100% 100% 100% 100% 100% 100% 100% 1558% 956% 676% 515% 410% 336% 282% 241% 208% 181% 160% 142% 126% 113% 102% 92% 83% 75% 78% 82% 85% 89% 93% 98% 103%

29 100% 100% 100% 100% 100% 100% 100% 100% 100% 857% 623% 482% 388% 321% 270% 232% 201% 176% 155% 138% 123% 110% 99% 90% 81% 74% 77% 80% 83% 87% 91% 96% 101%

30 100% 100% 100% 100% 100% 100% 100% 100% 100% 577% 453% 368% 306% 260% 223% 194% 170% 151% 134% 120% 108% 97% 88% 80% 72% 75% 78% 81% 85% 89% 93% 98%

31 100% 100% 100% 100% 100% 100% 100% 100% 100% 427% 350% 293% 250% 216% 188% 165% 146% 131% 117% 105% 95% 86% 78% 71% 74% 77% 80% 83% 87% 91% 96%

32 100% 100% 100% 100% 100% 100% 100% 100% 100% 334% 281% 240% 208% 182% 161% 143% 127% 114% 103% 93% 84% 76% 70% 72% 75% 78% 81% 85% 89% 93%

33 100% 100% 100% 100% 100% 100% 100% 100% 100% 270% 232% 202% 177% 156% 139% 124% 111% 100% 91% 82% 75% 68% 71% 74% 76% 80% 83% 87% 91%

34 100% 100% 100% 100% 100% 100% 100% 100% 100% 224% 195% 172% 152% 135% 121% 109% 98% 89% 81% 73% 67% 69% 72% 75% 78% 81% 85% 89%

35 100% 100% 100% 100% 100% 100% 100% 100% 100% 189% 167% 148% 132% 118% 106% 96% 87% 79% 72% 66% 68% 71% 73% 76% 80% 83% 87%

36 100% 100% 100% 100% 100% 100% 100% 100% 100% 162% 144% 129% 115% 104% 94% 85% 78% 71% 65% 67% 69% 72% 75% 78% 82% 85%

37 100% 100% 100% 100% 100% 100% 100% 100% 100% 140% 126% 113% 102% 92% 84% 76% 69% 63% 66% 68% 71% 73% 77% 80% 83%

38 100% 100% 100% 100% 100% 100% 100% 100% 100% 123% 110% 100% 90% 82% 75% 68% 62% 64% 67% 69% 72% 75% 78% 82%

39 100% 100% 100% 100% 100% 100% 100% 100% 100% 108% 98% 89% 80% 73% 67% 61% 63% 66% 68% 71% 74% 77% 80%

40 100% 100% 100% 100% 100% 100% 100% 100% 100% 96% 87% 79% 72% 66% 60% 62% 64% 67% 69% 72% 75% 78%

41 100% 100% 100% 100% 100% 100% 100% 100% 100% 85% 78% 71% 65% 59% 61% 63% 66% 68% 71% 74% 77%

42 100% 100% 100% 100% 100% 100% 100% 100% 100% 76% 69% 64% 58% 60% 62% 64% 67% 69% 72% 75%

43 salary scale= 100% 100% 100% 100% 100% 100% 100% 100% 100% 68% 62% 57% 59% 61% 63% 66% 68% 71% 74%

44 DC ER Rate = 100% 100% 100% 100% 100% 100% 100% 100% 100% 61% 56% 58% 60% 62% 65% 67% 70% 73%

45 DC Vesting = 100% 100% 100% 100% 100% 100% 100% 100% 100% 55% 57% 59% 61% 63% 66% 68% 71%

46 100% 100% 100% 100% 100% 100% 100% 100% 100% 56% 58% 60% 62% 65% 67% 70%

47 EEC rate= 100% 100% 100% 100% 100% 100% 100% 100% 100% 57% 59% 61% 64% 66% 69%

48 DB accrual rate= 100% 100% 100% 100% 100% 100% 100% 100% 100% 58% 60% 62% 65% 67%

49 + DB accrual rate= 100% 100% 100% 100% 100% 100% 100% 100% 100% 59% 61% 64% 66%

50 i= 100% 100% 100% 100% 100% 100% 100% 100% 100% 60% 63% 65%

51 100% 100% 100% 100% 100% 100% 100% 100% 100% 62% 64%

52 DB benefit is understood to be: 100% 100% 100% 100% 100% 100% 100% 100% 100% 63%

53 - A deferred or immediate annuity of accrued benefit per DB formula 100% 100% 100% 100% 100% 100% 100% 100% 100%

54 for employees terminating with 10+ years of service 100% 100% 100% 100% 100% 100% 100% 100%

55 - Refund of contributions without interest 100% 100% 100% 100% 100% 100% 100%

56 for employees terminating with less than 10 years of service 100% 100% 100% 100% 100% 100%

57 DC benefit is understood to be: 100% 100% 100% 100% 100%

58 - DC accumulates employee contributions with interest for employees terminating with 10+ years of service 100% 100% 100% 100%

59 - Refund of contributions without interest for employees terminating with less than 10 years of service 100% 100% 100%

60 Contributions include both employer and employee contributions 100% 100%

Relative value of the employer provided benefit at the time of termination

5.00%

2.0%

0.0%

7.50%

Inputs

4.0%

8.5%

10

DC More

Valuable

DB More

Valuable

26

Advantages/Disadvantages of Hybrid

Plans Related to Goals Goals Hybrid Plan Advantages Hybrid Plan Disadvantages

Attract & Retain Qualified Employees

• DB portion helps retain employees by rewarding career service

• DC portion may appeal to younger employees

• Plan design may be unfamiliar to employees

• Benefit multiplier may be less than provided by nearby governments

Sufficient & Sustainable Benefits

• DB portion pools investment, longevity, and inflation risks

• DC portion transfers risks to employees

• DC portion transfers risks to employees

• May be additional investment and management fees

Stable & Affordable Contributions

• Overall employer contribution rates more stable than traditional DB plans

• Additional complexity may make the plan more difficult and costly to administer

27

Advantages/Disadvantages of Cash

Balance Plans Related to Goals Goals CB Plan Advantages CB Plan Disadvantages

Attract & Retain Qualified Employees

• Guaranteed interest on account, protection of principle

• Portability may appeal to younger employees

• Less valuable to mid career hires

• May see as a less attractive benefit, especially for public safety members

Sufficient & Sustainable Benefits

• Pools investment, longevity, and inflation risks

• Members better understand value of their benefit

• May provide less benefits than a final average pay defined benefit design

Stable & Affordable Contributions

• Overall employer contribution rates more stable than traditional DB plans

• Liabilities can be correlated with investment performance

• Additional complexity may make the plan more difficult and costly to administer

28

Efficiency in Benefit Delivery

Programs with Pooled Assets and Liabilities have Distinct Advantages

1. Longevity risks can be pooled across a large number of individuals, providing each the security of a lifetime pension without the risk of outliving their savings

2. Everyone earns the same return

3. Portfolios can be “ageless” and therefore can perpetually maintain an optimally balanced investment portfolio rather than the typical individual strategy of de-risking as they near retirement

4. Pooled asset trusts achieve higher investment returns as compared to individual investors because of, broader universe of investments, professional management, and lower fees

30

Longevity Risk Pooling

• DB Plans - Pooled trusts can be funded to last the average life expectancy for each participant

• DC Plans - An individual must plan to get income beyond average, to avoid running out resources

31 Source: “Still a Better Bang for the Buck” 2014

Under an Individual Plan,

24% of Assets Are Not Used for Retirement

32

Source: “Still a Better Bang for the Buck” 2014

Lack of Longevity Risk Pooling

Drives Up Cost for Individual Plans

• To “self-insure” longevity risks, a retiree at age 62 needs about 24% more in an individual plan for same monthly income

• Based on an 80th percentile life expectancy, an individual still has a 1-in-5 chance of outliving savings

$504,732

$603,997

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

DB Plan DC Plan

33

Individual Investor Performance

34

34

Investment Outcomes by Individual Will Vary Greatly

.

35

Maintenance of Portfolio Diversification

• In an individual account, individuals must adjust risk as they age to protect against market shocks, shifting for capital diversification to more conservative investments as they age, sacrificing some expected return

• Example below uses a typical asset allocation until age 71, then gradual shift to 100% fixed income by age 92

Source: “Still a Better Bang for the Buck” 2014 36

Age-Driven Shift to More Conservative Portfolio

in an Individual Plan Drives Up Cost

• On top of the 20% for mortality protection, each retiree in on their own must have nearly another 16% in account balance at age 62 due to portfolio differences

37

DB Plan Strength #3

Lower Fees & Professional Management

• Pooled investments can lower expenses

– Large group pricing negotiation

– Avoid expenses of individual record keeping, investment education, investment transactions

38

Comparison of Plan Types

.

Source: Teacher Retirement System of Texas and Gabriel, Roeder, Smith & Company

39

39

Comparison of Plan Types, cont.

.

Source: Teacher Retirement System of Texas and Gabriel, Roeder, Smith & Company

40

40

Sensitivity to Investment Returns *Assumes member hired at age 30

-30% -10% 10% 30%

Current DB

Side by Side Hybrid

Capped Hybrid

Pass through Cash Balance

DC Pooled Funds

DC Self Directed

Percent Decrease in Benefit Percent Increase in Cost

The above shows the impact of 1% underperformance of investment return

41

EXAMPLES OF ALTERNATIVE

BENEFIT STRUCTURES

IMPLEMENTED BY OTHER STATES

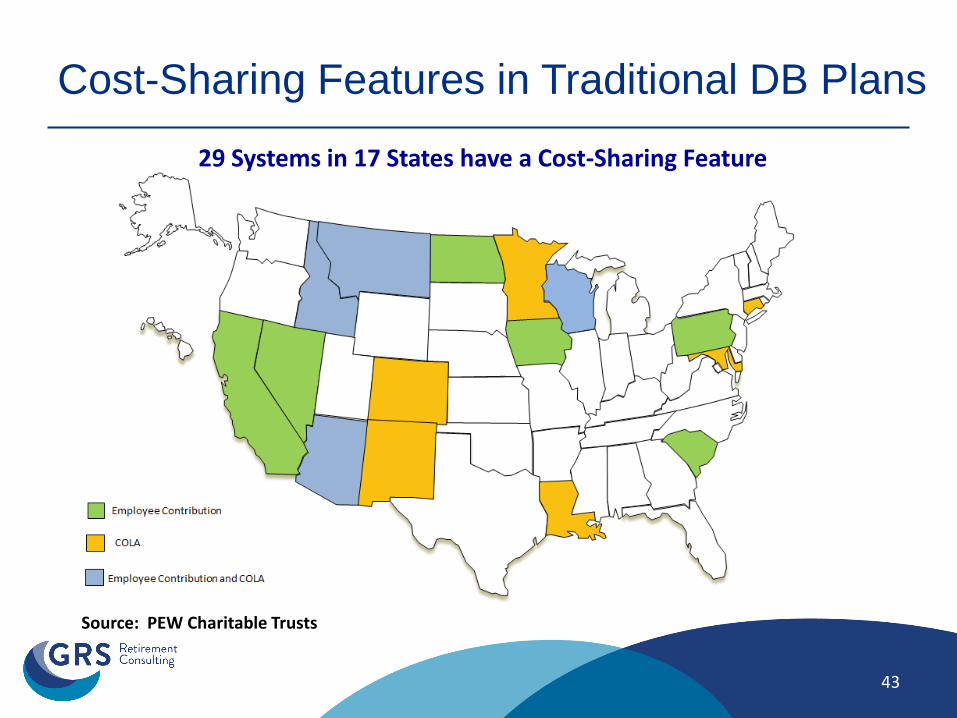

Cost-Sharing Features in Traditional DB Plans

Source: PEW Charitable Trusts

29 Systems in 17 States have a Cost-Sharing Feature

43

Non-traditional DB Plan Prevalence

Source: PEW Charitable Trusts

Systems in 23 States have an enacted a non-traditional plan design

44

• Hybrid Plans – Connecticut – Georgia – Tennessee – Virginia – PEW Suggested – South Carolina Sample RMH

• Cash Balance Plans – Texas – Nebraska – Kentucky – Louisiana

• Variable Benefit Plan – Wisconsin

Implemented Alternative Benefit Designs

45

• Benefit: Option (1) or (2) 1. Life Annuity = 1.4% x pay, plus 0.433% of pay in excess of

breakpoint ($82,400 for 2017), times years of service 2. Lump sum = Return of contributions with a 5% employer

match plus 4% interest Waive entitlement to retiree health insurance

• Member Contributions: 5% of pay • Employer Contributions: Actuarially Determined (ADEC) • Vesting: 10 years • Retirement: Age 63 and 25 Svc; or Age 65 and 10 Svc

Connecticut Hybrid Plan

(effective June 30, 2011)

Increased portability, larger termination benefit, no risk sharing.

46

• Benefit: DB benefit plus a DC Benefit 1. DB Benefit: 1% x Pay x Svc 2. DC Benefit: Max 3% employer match on 5% member

contribution

• Member Contributions: 1.25% of pay to the DB plan and voluntary contributions to the DC plan

• Employer Contributions: ADEC DB, 0% to 3% DC • Vesting: 10 years DB / 5 year DC • Retirement: Age 60 and 10 Svc; or 30 Svc

Georgia SEPS

(Effective January 1, 2009)

Has risk sharing features, provides a minimum guaranteed lifetime benefit, inadequate retirement benefit for nonsavers in the DC plan.

47

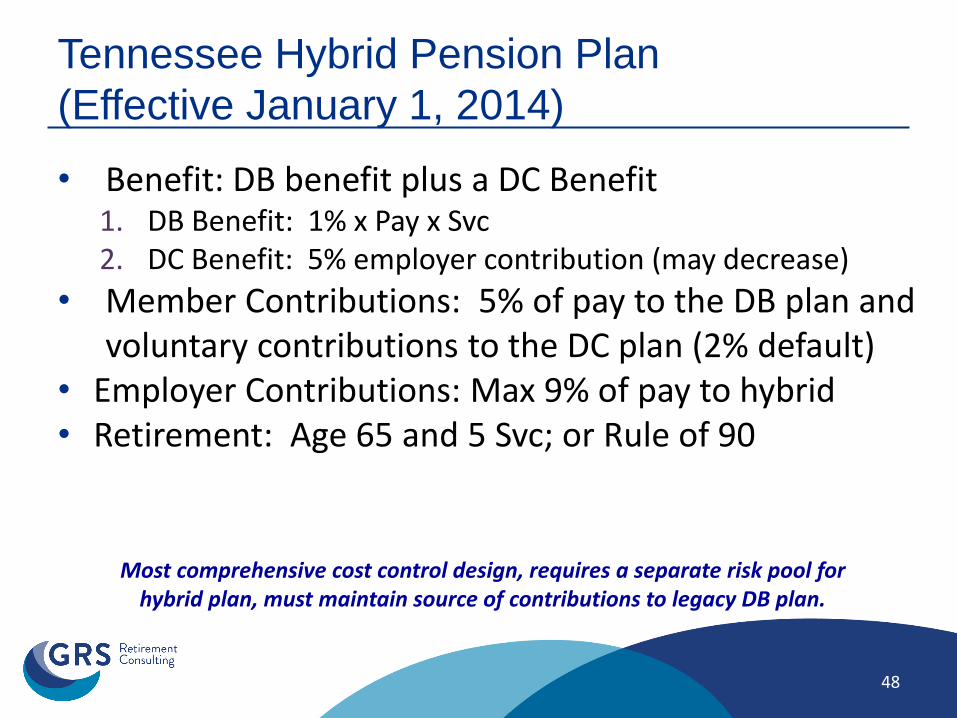

• Benefit: DB benefit plus a DC Benefit 1. DB Benefit: 1% x Pay x Svc 2. DC Benefit: 5% employer contribution (may decrease)

• Member Contributions: 5% of pay to the DB plan and voluntary contributions to the DC plan (2% default)

• Employer Contributions: Max 9% of pay to hybrid • Retirement: Age 65 and 5 Svc; or Rule of 90

Tennessee Hybrid Pension Plan

(Effective January 1, 2014)

Most comprehensive cost control design, requires a separate risk pool for hybrid plan, must maintain source of contributions to legacy DB plan.

48

• Benefit: DB benefit plus a DC Benefit 1. DB Benefit: 1% x Pay x Svc 2. DC Benefit: 1% to 3.5% employer match

• Member Contributions: 4% DB plan and 1% mandatory to the DC plan (additional 4% voluntary)

• Employer Contributions: ADEC DB, 1% to 3.5% DC • Vesting: 4 years • Retirement: SSRA, Age 60 and 30 Svc; or Rule of 90

Virginia Hybrid Retirement Plan

(Effective January 1, 2014)

Similar to Georgia SEPS, risk sharing features, provides a minimum guaranteed lifetime benefit, inadequate retirement benefit for nonsavers in the DC plan.

49

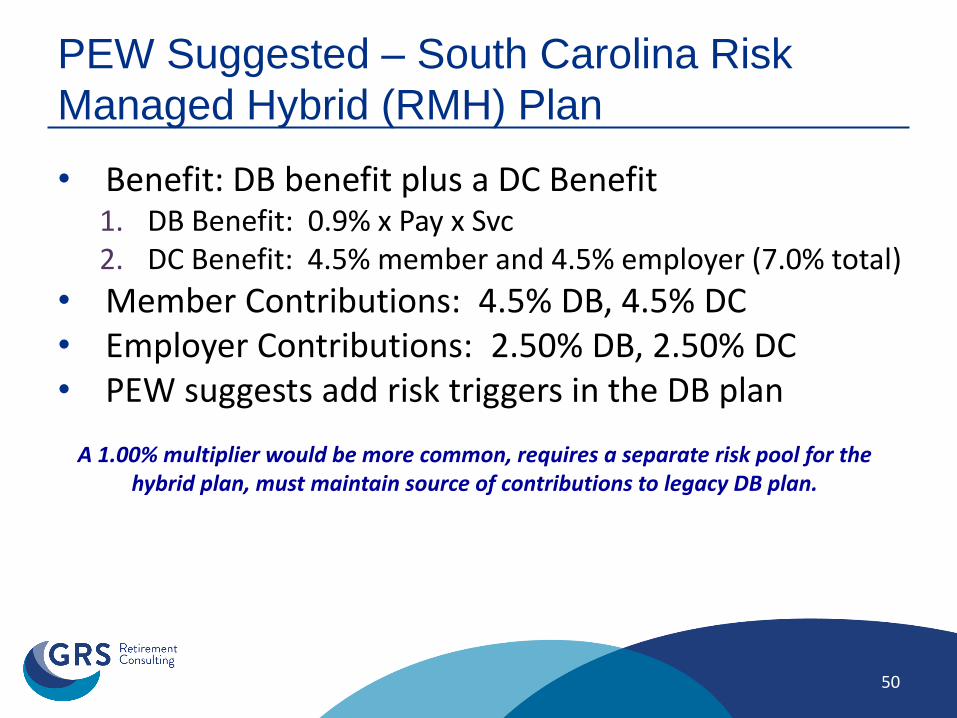

• Benefit: DB benefit plus a DC Benefit 1. DB Benefit: 0.9% x Pay x Svc 2. DC Benefit: 4.5% member and 4.5% employer (7.0% total)

• Member Contributions: 4.5% DB, 4.5% DC • Employer Contributions: 2.50% DB, 2.50% DC • PEW suggests add risk triggers in the DB plan

PEW Suggested – South Carolina Risk

Managed Hybrid (RMH) Plan

A 1.00% multiplier would be more common, requires a separate risk pool for the hybrid plan, must maintain source of contributions to legacy DB plan.

50

Cash Balance Plans

• Cash balance plans are not new to state and local governments

– Texas Municipal Retirement System - 1947

– Texas County & District Retirement System - 1967

– Nebraska Retirement System - 2002

• While not new, or common, design is fundamentally different from a final average pay plan

51

Cash Balance Example

Contributions Benefit Determination

TMRS

• Member 5-7% as determined by

employer

• 5% minimum annual interest credit as

per statute (Board can increase it)

• Employer matches employee account at

1:1, 1.5:1, or 2:1 as determined by

employer

• Lifetime annuity based

on accumulated

balance, life

expectancy, other

credits, interest

assumptions, and

payment option

Nebraska

PERS

• Member 4.8% as per statute

• 5% minimum or applicable federal mid-

term rate + 1.5% as per statute

• Employer matches member contributions

at a rate of 1.56:1 as per statute

• Lifetime annuity based

on accumulated

account balance and

selected pay out option

52

Cash Balance Plans – Kentucky

(Effective January 1,2014)

• Employee contributions 5% of pay;

• Employer contributions 4% of pay;

• Interest credited a minimum 4% per year with additional interest depending on actual return experience;

• Accumulated balance converted to an annuity at retirement (other optional forms available)

53

Cash Balance Plans – Louisiana

(Enacted in 2012; effective date pending)

• Employee contributions set at 8% of pay;

• Employer contributions set at 4% of pay;

• Interest credited at expected rate of return (8.0%) minus 1.0%, but no lower than 0%;

• Benefit vests after 5 years;

• Converted to an annuity at retirement (other optional forms available)

54

Variable Benefit Plans - Wisconsin

• DB Component: 1.6% multiplier (2.5% for public safety)

• DC Component: Minimum benefit equal to annuitized value of 2 x member contributions

• Current contribution rate: 6.8% employee and 6.8% employer

• Variable Component

– Dividend based on investment returns

55

• Dividend – Retirees promised a minimum benefit (floor); – If the core fund’s 5-year average investment returns

exceed 5%, retirees receive a dividend based on gains from investments; and

– Dividends can be cut back (but not below zero, to protect the minimum benefit) when stock market returns fall below expectations.

• Since 2008, about half of the plan’s retirees have had their benefits cut back to the floor.

• On the other hand, Wisconsin is one of the best funded systems in the U.S.

Variable Benefit Plans - Wisconsin

56

Variable Benefit Plans - Wisconsin

Dividend Remaining (as a Percentage of Total Benefit) by Year of Retirement

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Year Retired

Remaining Dividend 2012 Dividend Adjustment

57

Variable Benefit Plans - Wisconsin

Historical Funded Ratio

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

WRS Funded Status (All Participants)

58

Disclaimers

• This presentation shall not be construed to provide tax advice, legal advice or investment advice.

• Readers are cautioned to examine original source materials and to consult with subject matter experts before making decisions related to the subject matter of this presentation.

• This presentation expresses the views of the author and does not necessarily express the views of Gabriel, Roeder, Smith & Company.

59

PUBLIC EMPLOYEE BENEFIT AUTHORITY AGENDA ITEM BOARD RETREAT

Meeting Date: October 19, 2017 1. Subject: Fiduciary Education 2. Summary: An educational presentation by Rob Gauss from Ice Miller as part of Board’s Educational Requirements. 3. What is the Board asked to do? Receive as Information 4. Supporting Documents:

(a) List those attached: 1. Fiduciary Duties, Updated Considerations Regarding Lawsuits Against University

Retirement Plans and Board’s Role in Benefit Design/Reform

South Carolina Public Employee Benefit Authority Board of Directors Retreat

By:Robert L. Gauss, Partner

October 19, 2017

Fiduciary Duties, Updated Considerations Regarding Lawsuits Against University Retirement Plans and Board's Role in

Benefit Design/Reform

Prior Fiduciary Training Presentations2013 Report on Fiduciary Responsibilities (SBCB)RSIC Presentation to Senate Finance Special Subcommittee to Review the Investment of State Retirement Funds, February 25, 2014Past Funston Audits/Presentations to RSIC/PEBA2017 Legislative Changes

Considerations

2

South Carolina Code of Laws 9-4-10 (amended effective July 1, 2017), 9-16-10, 9-16-40, and 9-16-50State Ethics Act

S.C. Code Title 8, Chapter 13Code Rules of Conduct § 8-13-700 et. seq.

Board's Ethics Policy

Touchstones

3

Board's Conflict Policy(A) No member of the Board of Directors may make, participate in making, or in any way attempt to use his membership to influence a Board decision in which he, a family member, an individual with whom he is associated, or a business with which he is associated has an economic interest. A Board member who, in the discharge of his official responsibilities, is required to take action or make a decision which affects an economic interest of himself, a family member, an individual with whom he is associated, or a business with which he is associated shall:

Touchstones (cont'd)

4

(1) Prepare a written statement describing the matter requiring action or decisions and the nature of his potential conflict of interest with respect to the action or decision;(2) Furnish a copy of the statement to the Board Chairman, who shall cause the statement to be printed in the minutes and require that the member be excused from any votes, deliberations, and other actions on the matter on which the potential conflict of interest exists and shall cause the disqualification and the reasons for it to be noted in the minutes.

(B) The members of the PEBA Board of Directors must abide by the following additional conflict-of-interest guidelines:

Touchstones (cont'd)

5

(1) Directors should make reasonable efforts to avoid conflicts of interest and appearances of conflicts of interest.(2) Directors may not under any circumstances accept offers, by reason of their service, relationship or employment with PEBA, to trade in any security or other investment on terms more favorable than those available to the general investing public or, in the case of private market investments, a similarly situated investor.(3) A conflict of interest exists for a Director whenever the Director has or is seeking a personal or private commercial or business relationship that could reasonably be expected to diminish the Director's independence of judgment in the performance of the Director's responsibilities to PEBA.

Touchstones (cont'd)

6

Note: Curability in PEBA Conflicts of Interest PolicyNote: Exceptions to Conflict of Interest PolicyNote: Policies apply to all activities (Retirement, Health, OPEB)

Touchstones (cont'd)

7

Who is a fiduciary?Any person who:

Exercises any discretionary authority or discretionary control respecting management of a plan or exercises any authority or control respecting management or disposition of its assets.Renders investment adviceHas any discretionary authority or discretionary responsibility in the administration of the plan.

- IRC § 4975(e)(3)

- 9-16-10(4)

An entity or individual may be a fiduciary either by designation or by function.

Fiduciary Entities

8

Fiduciary Entities (cont'd)

PEBA Board is one of multiple fiduciaries for the South Carolina Retirement Systems

PEBA (Board is trustee – 9-16-10(9))State Fiscal Accountability Authority (co -Trustee with PEBA until July 1, 2017) (9-1-1310)Retirement System Investment Commission (RSIC) (9-1-1310; 9-16-20; 9-16-315) (co-Trustee with PEBA after July 1, 2017)State Treasurer (Custodian) (9-1-1320) (only until July 1, 2017)

Can hold in cash up to 10% of System assets (9-1-1330)

Legislature 9

Fiduciary Entities (cont'd)

Each has different (and sometimes overlapping) responsibilities

"Unique among state public pension funds""Inherent potential for confusion and conflict"

PEBA Board is also one of multiple fiduciaries for the State's Health Insurance and OPEB funds

PEBA (Board is trustee – 1-11-705(B), 1-11-707(B), 1-11-710(A))State Treasurer (Custodian and Investor of OPEB funds – 1-11-705(B), (G), 1-11-707(B), (G)) Legislature

10

Fiduciary Entities (cont'd)

PEBA Board is also a fiduciary for the defined contribution plans offered by the State

State Optional Retirement Program (9-20-20 and 9-20-30)South Carolina Deferred Compensation Program (8-23-20) Defined as Trustee in Plan Documents

Every power or duty given to the Board by state law must be exercised in accordance with fiduciary principles(9-4-10(K) and (L) applies to Board's role with all plans being administered)

11

Federal Law:Internal Revenue Code – Applicable to governmental plans.

ERISA – Applicable to private sector plans, but an excellent resource due to robust regulatory framework and extensive developed case law.

State Law

Common Law:

Restatement of Third, Trusts – essentially a collection and summary of the common law trust rules. Not binding, but highly persuasive.

Uniform Management of Public Retirement Systems Act (UMPERSA) –compilation of common law specific to governmental retirement plans.

Plan and Trust Documents

Sources of Fiduciary Principles

12

State Law:

(1) solely in the interest of the retirement systems, participants, and beneficiaries;

(2) for the exclusive purpose of providing benefits to participants and beneficiaries and paying reasonable expenses of administering the system;

(3) with the care, skill, and caution under the circumstances then prevailing which a prudent person acting in a like capacity and familiar with those matters would use in the conduct of an activity of like character and purpose;

(4) impartially, taking into account any differing interests of participants and beneficiaries;

Sources of Fiduciary Principles (cont'd)

13

(5) incurring only costs that are appropriate and reasonable; and

(6) in accordance with a good faith interpretation of this chapter.

(9-4-10(K); 9-16-40)

(A) Compliance by the trustee, commission, or other fiduciary with Sections 9-16-30, 9-16-40, and 9-16-50 must be determined in light of the facts and circumstances existing at the time of the trustee's, commission's, or fiduciary's decision or action and not by hindsight.

(B) The commission's investment and management decisions must be evaluated not in isolation but in the context of the trust portfolio as a whole and as a part of an overall investment strategy having risk and return objectives reasonably suited to the retirement system.

(9-16-60)

See also standards of conduct 9-16-360.

Sources of Fiduciary Principles (cont'd)

14

"Under the trust instrument it [must be] impossible, at any time prior to the satisfaction of all liabilities with respect to employees and their beneficiaries under the trust, for any part of the corpus or income to be (within the taxable year or thereafter) used for, or diverted to, purposes other than for the exclusive benefit of his employees or their beneficiaries."

- Internal Revenue Code, § 401(a)(2)

Fiduciary Principles – Exclusive Benefit Rule

15

"A fiduciary shall discharge his duties with respect to a plan

Solely in the interest of the participants and beneficiaries andFor the exclusive purpose of:

Providing benefits to participants and their beneficiariesDefraying reasonable expenses of administering the plan"

These expenses must be plan expenses, not settlor expenses

- ERISA- 9-4-10(K); 9-16-40(1) and (2) – Standards of Discharge of Duty

Fiduciary Principles – Exclusive Benefit Rule (cont'd)

16

A qualified plan is prohibited from participating in any transaction in which it –

1) "Lends any part of its income or corpus, without receipt of adequate security and a reasonable rate of interest, to;

2) Pays any compensation, in excess of a reasonable allowance for salaries or other compensation for personal services actually rendered, to;

3) Makes any part of its services available on a preferential basis to;

Fiduciary Principles – Prohibited Transactions

17

4) makes any substantial purchase of securities or any other property, for more than adequate consideration in money or money's worth, from;

5) sells any substantial part of its securities or other property, for less than an adequate consideration in money or money's worth, to; or

6) engages in any other transaction which results in a substantial diversion of its income or corpus to;

the creator [of or] a person who has made a substantial contribution to [the trust]…."

- Internal Revenue Code, § 503(b)- 9-1-1340 -- Conflicts of Interest (RSIC)- 9-16-350 -- Use of Information for self-interest (RSIC)- 9-16-360 -- Standards of conduct for fiduciary or employee of fiduciary

Fiduciary Principles – Prohibited Transactions (cont'd)

18

A fiduciary may not:Deal with plan assets in his own interest .Act in a transaction with a "party in interest" if adverse to the interests of plan participants.

Any "deals" with the employer (or "funder") must be commercially reasonable, at arms' length.

Receive any consideration for his personal account from any party in connection with a transaction involving the plan.

Prohibited Transactions – Practical Impact on Trustee

19

Administer the trust in accordance with its terms and applicable laws – "Doing things by the book"

Set aside pre-conceived notions and work from the facts and from statutes, rules, Board policies and procedures.The plan must be administered as written.Make sure to keep up-to-date with law changes.The fiduciary must be aware of the entire legal context, of issues that come before them, including other state and federal laws.

Fiduciary Principles – Adherence to the Trust

20

Duty with respect to co-Trustees from ERISA and from the Restatement

Settlor determines areas of responsibility

Each trustee must take reasonable care to prevent a co-trustee from committing a breach of trust and to obtain redress if there is a breach.

Recognizing RSIC's responsibilities for investments

Consideration by trustees of integrity of process used for decision-making

Duties of care and prudence related to process

Of course, consideration for the fact that PEBA and RSIC are co-trustees of the Retirement System (9-1-1310)

Fiduciary Principles – Co-Trustees

21

Overall Fiduciary Principles – Care, Skill, Prudence, Diligence

"With the care, skill, prudence, and diligenceunder the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims;

- ERISA- 9-4-10(K)(3); 9-16-40: ". . . With the care, skill, and caution

under the circumstances then prevailing which a prudent person in a like capacity and familiar with the matters would use in the conduct of an activity of like character and purpose. . ."

- Restatement of Trusts, Third

22

Responsibilities that are outside the trustee's skill set

Secure and consider advice of experts (9-16-30 – the RSIC may delegate certain functions, but must exercise reasonable care, skill and caution).

Duty of Care – Importance of Delegation (cont'd)

23

Duty of LoyaltyThe trustee must conform to "fundamental fiduciary duties of loyalty (Restatement of Trusts, Third §170) and impartiality (Restatement of Trusts, Third §183)."

Balancing the interests of retirees and active participantsBalancing interests of different groups of participantsBalancing roles with regard to different plans and trusts

24

UMPERSA Commentary: "Differing interests are inevitable in the retirement system setting. Differences can arise between retirees and working members, young members and old, long-and short-term employees, and other groupings of those with interests in the retirement system. The duty of impartiality does not mean that fiduciaries must accommodate such interests according to some notion of absolute equality. The duty of impartiality … requires that such decisions be made carefully and after weighing the differing interests."9-4-10(K)(4); 9-16-40: ". . .Impartially, taking into account any differing interests of participants and beneficiaries. . ."Also applies to health insurance and OPEB plans.

Duty of Impartiality

25

A trustee must maintain independence and set aside the interests of the appointing authority or the group the trustee represents.

"It is as improper for a fiduciary to take actions for the purpose of benefiting a third person as it is for a fiduciary to act in its own interest. In the retirement system setting, it is important to note that this duty includes the obligation to set aside the interests of the party that appoints a trustee or fiduciary. A trustee, for example, must act solely in the interests of participants and beneficiaries and set aside any interest of a party responsible for the trustee's appointment, such as an employer or union."

- UMPERSA Comments on § 7 (Emphasis added)

Significant because South Carolina, in effect, adopted UMPERSA in 9-16-40(1).

9-4-10(K)(1)

Maintaining Independence

26

Independence comes from following procedural prudence – have established procedures and follow them.Applying lessons from "outside world" is not prohibited, but the overriding principle is to follow the exclusive benefit rule.

A trustee must make a decision given the facts and circumstances that are relevant.

May only wear "one hat" at a time and must wear only the fiduciary hat when making decision as a Board member. Hughes Aircraft v. Jacobson, 525 U.S. 432 (1999).

Independence – Practical Impact on Trustee

27

Settlor establishes the terms of the trust and the plan.

The Settlor = Legislature/StateSettlor determines the scope of authority of the fiduciaries.Each fiduciary must administer the trust and the plan for the benefit of the participants and their beneficiaries in accordance with the role assigned.

Board's Role as Fiduciary

28

Board's role with regard to benefits

Board is responsible for the general administration and proper operation of the plans (e.g. 1-11-710, 9-1-210)

Administer benefits in accordance with plan

Engage actuarial and other experts (e.g. 1-11-705(D), 9-1-230)

Establish premiums and contribution rates (e.g. 1-11-710(2), 9-1-1085)

Establish rules and regulations (e.g. 1-11-705(F), 9-1-290)

9-4-10 (retirement and insurance benefits)

Board's Role as Fiduciary (cont'd)

2929

Board's role with regard to investments:Settlor gave investment responsibility for retirement systems funds to RSIC. But Board is a co-trustee of the trust assets According to the AG, Board has the responsibility to act in the best interests of the trust, including with respect to investments

Board's Role as Fiduciary (cont'd)

30

SEC Rule 206(4)-5, adopted in 2010, prohibits investment advisors from providing advisory services, for compensation, for a period of two (2) years following a political contribution to a public official or candidate who is or would be in a position to influence the selection or retention of advisors to manage public pension funds or other government client assets.Specifically defines advisors and its "covered associates"Also allows a de minimis standard ($350 or $150 depending on the election involved)Recent developments regarding Black Rock and contributions to John Kasich campaign - $37M in management fees at risk.Public plans should have ethics and investment policies which require compliance

"Pay to Play" – Securities and Exchange Commission

31

Based on DOL Guidance

Distinction between Plan Design and Plan AdministrationSettlor Functions

Plan Design / Amendment

Plan Termination

GASB Required Statements

Design Studies and Cost Projections

Union Negotiations

Consulting

Certain costs associated with evaluating alternatives related to changes in the law

Certain corrections under IRS' EPCRS Program

Allocation of Cost: Settlor Functions vs. Fiduciary Functions

32

Fiduciary / Administrative Functions

Implementation of Settlor Decisions

Benefit Calculations

Routine Nondiscrimination / 415 Testing

Amending the Plan to Comply with Tax Law Changes

Certain Communication Costs

IRS Determination Letter

Certain corrections under IRS' EPCRS Program

Settlor Functions vs. Fiduciary Functions (cont'd)

33

Supreme Court decision in Tibble v. Edison International, 135 S.Ct. 1823 (2015)

Reiterated that ERISA fiduciary duty is derived from the common law of trusts. Looked to common law of trusts to find that a trustee has a continuing duty – separate and apart from the duty to exercise prudence in selecting investments at the outset –to monitor and remove imprudent investment options.Breach of ongoing duty to monitor by failing to replace retail with institutional funds.Plan fiduciaries should know when lower priced institutional share are available.

ERISA

34

History of Fee Litigation

35

Fee litigation began in 2006/2007, primarily against large private sector companies sponsoring 401(k) plans.Cases allege breaches of fiduciary duties of loyalty and/or prudence under ERISA.Mixed success in courts, BUT settlements totaling millions – e.g. $62 million with Lockhead Martin and $57 million with Boeing.

Goal is to get past Motion to Dismiss.

Overview

36

In White v. Chevron, N.D. CA (2016), the court dismissed a complaint alleging breach of fiduciary duty for failure to state a claim finding that plaintiffs failed to cite sufficient facts to support allegations. Court noted:

ERISA does not require plan fiduciaries to include any particular mix of investment vehicles in their plan.Prudent process, not results, is the focus.Fiduciary actions not judged from hindsight (consider 9-16-60).Fiduciaries can value investment features other than price.Prudence of investment is assessed not in isolation but as it relates to the portfolio as a whole.ERISA does not prohibit revenue sharing nor require periodic competitive bidding.

Surviving a Motion to Dismiss

37

The focus in these lawsuits is on process, not best possible result.The test of prudence -

"is one of conduct, and not a test of the result of performance of the investment. The focus of the inquiry is how the fiduciary acted in his selection of the investment, and not whether his investments succeeded or failed."

Document, document, document!

Prudent Process is Critical

38

New / Updated Frontiers

39

Defined contribution plans are the primary means of retirement income today.Employees bear the risk of poor investment performance and often pay the costs of the plan.There is increased pressure on plan performance and heightened expectations.As result, increasingly novel claims are being made in the fee litigation lawsuits.No category or type of investment fund is immune.

Setting the Stage

40

Class action lawsuit filed against Portico, the denomination benefit board for the Evangelical Lutheran Church in America (ELCA) in 2015.

As a church plan, not subject to ERISA.Complaint alleges breaches of fiduciary duty under state law in selecting funds with unreasonable fees with poor performance, with no prudent process to evaluate whether compensation was reasonable.Claims brought under Minnesota common law and prudent investor act.Suit moving forward on merits.

Non-ERISA Fee Litigation

41

Kruger v. Novant Health, a 2015 lawsuit against a nonprofit sponsoring a 403(b) plan, survived a Motion to Dismiss. Allegations included:

Excessive compensation to service providers from revenue sharing.Excessive commissions to broker.Fiduciary breach in offering retail instead of institutional funds (failure to request a waiver of investment thresholds).

Settled for $32M in 2016.

403(b) Plan Fee Litigation

42

In August 2016, 13 separate class action lawsuits were filed against 12 private universities sponsoring “jumbo” (1-5 billion dollar) 401(k) and 403(b) plans.

Since then, 3 more university class actions filed. Several plaintiffs law firms involved.

Generally allege that the universities did not use their bargaining power to demand low cost services and less expensive funds.

University Fee Litigation

43

Similar allegations are made in all of the lawsuits:1. Failure to solicit competitive bids for

recordkeeping and administrative services at regular intervals.

2. Multiple recordkeepers, resulting in inefficiencies and increased fees (NEW).

3. Too many investment options, resulting in participant confusion and excessive fees because failed to take advantage of leverage (NEW).

4. Retained underperforming funds because failure to monitor or the vendor required the fund to be offered on the platform.

Specific Allegations

44

The lawsuits make largely the same allegations, including (cont’d):5. Failure to monitor and control fees paid by the plan for

recordkeeping and administrative services, particularly the asset-based revenue sharing received.

6. Funds were too expensive because failed to engage in a prudent process for the selection and retention of investment options.

7. Failure to negotiate lower-cost share classes for the plan's mutual fund options (institutional vs. retail).

8. Failure to take into account withdrawal restrictions and costs in annuity products like TIAA Traditional Annuity.

Specific Allegations (cont’d)

45

Claims being made in these lawsuits are similar to those made in the 401(k) lawsuits.However, university lawsuits are unique because of the history of 403(b) plans, which until fairly recently, were treated by many employers as loosely organized payroll arrangements.

Historically, contracts were individually owned and marketed directly to participantsInvestments limited to annuities and custodial accountsMultiple recordkeepers are commonService more highly valued by participantsUntil 2009, full Form 5500s and audits not required

Specific Allegations (cont’d)

46

Fiduciary standards make no distinction based on type of plan.Complaints accurately identify and take advantage of some of the historical weaknesses of common 403(b) plan funding structures.Industry is changing rapidly.Regardless of outcome, the lawsuits are likely to set new industry standards.

Specific Allegations (cont’d)

47

Motions to Dismiss have been filed in all of the university cases, arguing that plaintiffs failed to state a claim (similar to Chevron):

Duty to diversify requires a large array of funds and ERISA encourages participant choice.ERISA does not require fiduciaries to offer cheapest funds, and other factors can be taken into consideration.ERISA does not require competitive bids for recordkeepers.403(b) limits types of investment options available.

Defendant Responses

48

No allegation of a specific injury to named plaintiffs.Failure to state any facts showing that fiduciary process was deficient.Multiple recordkeepers a common industry approach, as is revenue sharing.

Fact that the 12 lawsuits are largely identical demonstrates that universities acted as prudent fiduciaries in similar circumstances.

Defendant Responses (cont'd)

49

Amended Complaints filed in many cases as a result of motions to dismiss.First two opinions issued in May 2017, in Emory (Georgia District Court) and Duke University (North Carolina District Court) cases

Dismissed some claims.Allowed others to move forward.

First Court Decisions

50

On 5/10/17, judge issued 26 page decision on motion to dismiss in Emory case.

Dismissed claim that the plan included too many investment options (there are 111).Allowed the remaining claims to proceed.

First Court Decisions (cont'd)

51

On 5/11/17, judge issued a 5 page decision on motion to dismiss in Duke case.

Dismissed following claims:Duke "locked in" imprudent investment arrangements with vendor was time barred (contrary to Emory)Failure to monitor fiduciaries insufficiently plead.

Retained the remainder of the claims, including the following claim that was dismissed by Emory Court:

Too many investment options caused investment paralysis (there are 400).

Recent decisions involving Cornell, MIT and Penn have had mixed results; Penn is only one to have won complete dismissal.

First Court Decisions (cont'd)

52

Design / Reform Efforts

53

Impact of Increase in Contribution Rates (employers and employees).Resistance to changes/reductions in benefits.Pressure on investment returns.Public focus/pressure.

Challenges for the Board

54

Plan Design is the responsibility of the Plan Sponsor.Plan Administration is the responsibility of PEBA.PEBA can provide data/information. What about recommendations? What direction is given to PEBA by the Plan document or legislation? What is PEBA's role if:

System(s) will run out of money without plan changes;Legislation/ballot proposals threaten long-term sustainability of the plan.

Plan Design vs. Plan Administration

55

Fiduciary: Exclusive Benefit Rule.Budgetary: Have expenses been budgeted and funded? Legal: Is the expenditure permissible under state law and/or the First Amendment?

Considerations on Potential Constraints to Expenditure of System Funds

56

Longer life expectancies.Changed market conditions/returns.Lack of fiscal discipline.Pressure against revenue increases.Outside interests.

Realities Pressuring Change

57

Adaption of new mortality tables.To reflect retirement benefits are being paid longer.

Lower rate of return.To reflect investment income likely will be lower than previously projected.

Listening and learning tour.Statewide effort to engage a wide range of stakeholders on PERA's funded status.

Statutory requirement to recommend contribution rate changes.

Colorado PERA Board Action in Response to Changing Conditions

58

One-time directive (2008) to provide specific, comprehensive recommendations regarding possible methods to ensure that each division will become and remain fully funded.Acknowledgement that recommending changes to benefits could invite litigation for breach of fiduciary duty. Counterbalanced against potential breach of fiduciary duty not to recommend changes if trustees believe changes are necessary to preserve the system's long-term sustainability.

Board's Role in Recommending Benefit Changes for Existing Membership

59

Safest Option: Highlight amortization concerns and allow political entities/interests to determine the course of action.

BUT

As the experts and fiduciaries, shouldn't the Board advocate for necessary changes to ensure long-term sustainability?

Board's Role in Recommending Benefit Changes for Existing Membership (cont'd)

60

Lack of consensus among the Board members regarding necessary changes. Is shared sacrifice between employers, actives, retirees necessary? Strategies to communicate with, and get buy-in from, membership. Political pressures.

Practical Challenges

61

Robert L. Gauss, PartnerICE MILLER LLPOne American Sq., Suite 2900Indianapolis, IN 46282-0200(317) 236-2133 (Telephone)(317) 592-4668 (Facsimile)

PUBLIC EMPLOYEE BENEFIT AUTHORITY AGENDA ITEM BOARD RETREAT

Meeting Date: October 19, 2017 1. Subject: Ethics Training 2. Summary: An educational presentation by Dennis Gatlin as part of the Board’s educational requirements. 3. What is the Board asked to do? Receive as Information 4. Supporting Documents:

(a) List those attached: Finding True North

Dennis Gatlin, MA, CRC®

To review your personal decision-making process relative to the PEBA’s Mission, Vision, Values and Additional Standards of Conduct.

To become more skillful in identifying issues and actions in a variety of situations related to the PEBA’s Mission, Vision, Values and Additional Standards of Conduct.

Studying ethics won’t make you ethical Understand better what is best Understand how to pursue what is best Participate in discussions about what is best Be able to act reasonably when the time comes

Risk mitigation Build and fortify trust Maintain brand and reputation Meet stakeholder expectations Strengthen each employee’s value system Other reasons…?

What is your definition? Is there a “standard” definition of “ethics?”▪ What does your definition sound like?▪ Are there any key themes?

With what do you agree? Is there anything with which you disagree?

In 137 characters…

#Ethics▪ Ethics studies “What do I do?” while

recognizing issues, judging possibilities, and acting appropriately. It is characterized by courage.

South Carolina Code of Laws Section 8-13-700, et seq. Lengthy and complex listing of behaviors

Our mission: PEBA’s mission is to provide competitive retirement and insurance benefit programs for South Carolina public employers, employees and retirees.

Our vision: Serving those who serve South Carolina

Our core values Solutions oriented. We anticipate the needs of our members, colleagues and

supervisors, and work daily to improve processes and increase customer satisfaction. Communication. We encourage and facilitate the flow of information, listen effectively

and are receptive to constructive feedback. Credibility. We accept responsibility for our individual jobs and achieving the goals of

PEBA. We are accountable, thorough and accurate. Collaboration. We foster cooperative relationships, and appreciate and respect the

contributions of others. Responsive. We strive to achieve our goals and objectives. We adapt to change. We follow

through. Emotional intelligence. We maintain self-awareness and modify behavior

appropriately. We work to build rapport with others and effectively manage and resolve conflict. Ethical behavior. We value honesty, trust, fairness and consistency.

In addition to state law, a Director shall not act:(1) To benefit his/her financial interests;(2) To commit funds that results in a Director, his family, or his

business associates receiving fees;(3) To benefit from a contract;(4) To secure, solicit, or accept things of value;(5) To represent, while on the PEBA Board and for one year after

leaving the PEBA Board, any person, before any public agency, with regarding matters the Director personally participated in while on the PEBA Board;

(6) To benefit to himself, his family, or his business associates;(7) To disclose/use confidential information without proper

authorization;(8) To use PEBA assets for his own interest; and,(9) On behalf of a party whose interests are adverse to PEBA.

Strong sanctions and feelingsCapital crimes

Murder

Stop signsTraffic laws

Weak sanctions and feelings

Non-Institutionalized

Norms

Institutionalized Norms

Strong sanctions and feelings Mores

Cannibalism

Salad forks and dress codesFolkways

Weak sanctions and feelings

When the mores are adequate; laws are unnecessary.When the mores are inadequate; laws are ineffective.

Value Drift

You are all alone in making ethical decisions; and, You are constrained by the expectations of your

community

http://goodcomics.comicbookresources.com/2011/08/26/comic-book-legends-revealed-329/

Indians, Indians all around us! Well, Tonto, ol’ kimosavee, it looks like we’re finished!

What you mean WE?

Studies the norms or standards by which things are measured or evaluated

Studies the way things operate or behave

Morality

Ethics

…to “what ought to be!”

How people behave when they are absolutely guaranteed no one will find out what they have done

Knowing the difference between what you have a right to do what is the right thing to do

Beyond law to a stringent level of personal responsibility

Principles that “ought” to govern behavior

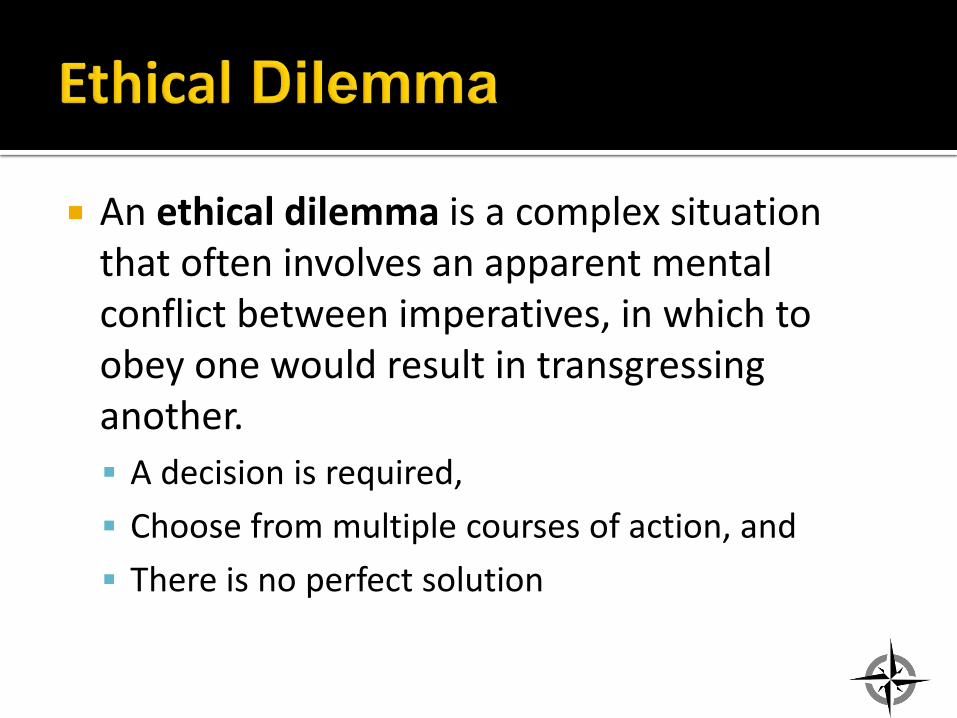

An ethical dilemma is a complex situation that often involves an apparent mental conflict between imperatives, in which to obey one would result in transgressing another. A decision is required, Choose from multiple courses of action, and There is no perfect solution

SOLVE IT1: The 7-step problem-solving process1. Statement - State the problem exactly2. Origin – Find the root cause3. List – Brainstorm solutions4. Verify – Pros and cons5. Eliminate – Choose the best solution6. Implement – Action is required7. Test – Is it working?

1http://biggsuccess.com/2008/03/04/have-a-problem-solve-it/

“Making an Ethical Decision - A practical tool for thinking through tough choices” http://www.scu.edu/ethics/ethical-decision/

Different generations have different approaches 1

Workplace Characteristics

Traditionalists(1922-1945)

Baby Boomers(1946-1964)

Generation X(1965-1982)

Millennials(1983-2004)

Work Ethic and Values

Respect authoritySacrificeDuty before funAdhere to rules

WorkaholicsWork efficientlyCrusading causesPersonal fulfillment

Question authoritySelf-relianceWant structure and directionSkepticalTolerant

What's nextMulti-taskingTenacityEntrepreneurialGoal oriented

Interactive style Individual Team playerLoves to have meetings

Entrepreneur Participative

Communications Formal memo In personBy phone

DirectImmediate

EmailVoice mail

Feedback and rewards No news is good newsSatisfaction in a job well done

MoneyTitle recognition

Sorry to interrupt, but how am I doing?Freedom is the best reward

Whenever I want it, at the push of a buttonMeaningful work

Messages that motivate

"Your experience is respected"

"You're valued, you are needed"

"Do it your way, forget the rules"

"You will work with other bright, creative people"

1Greg Hammill, "Mixing and Managing Four Generations of Employees" Farleigh-Dickinson College of Business

1%

5%

8%

2%

15%

9%

10%

8%

5%

8%

13%

8%

24%

27%

15%

5%

9%

9%

18%

13%

32%

34%

19%

11%

14%

15%

22%

18%

36%

37%

26%

13%

0% 10% 20% 30% 40% 50%

1

2

3

4

5

6

7

8

Millenials Generation X Baby Boomers Traditionalists

Buy personal items w/ company credit card

Keep copies of confidential documents

Ok to work less to compensate for cuts in pay or benefits

Acceptable to "friend" a client/customer on social media

Use social networking to find out about competitors

Upload personal photos on company network

Take a copy of work software home for personal use

Blog\tweet negatively about the company

Millennials▪ Communicate commitment to ethics in terms of people,

relationships, and integrity in the way people treat each other.▪ Focus messaging from individuals more similar to Millennials and

may be more influential.▪ Emphasize knowledgeable people resources available within the

program for guidance and support.▪ Build discussion and interactions opportunities for ethics and

compliance training.▪ Provide input opportunities into standards and systems.▪ Provide opportunities to check back and interact with ethics

authority during ongoing investigations.

1 BITC, How Businesses Are Harnessing the Power of Age Diversity (http://www.bitc.org.uk/blog/post/harnessing-power-age-diversity-and-adapting-business-ageing-workforce) Business In the Community

Generation X▪ Make advice and standards accessible for

dealing with dilemmas.▪ Ensure that supervisors of Gen X-ers can

provide advice to and counsel, when needed.

1 BITC, How Businesses Are Harnessing the Power of Age Diversity (http://www.bitc.org.uk/blog/post/harnessing-power-age-diversity-and-adapting-business-ageing-workforce) Business In the Community

Boomers and Traditionalists Communicate commitment to ethics as principles and formal

systems. Provide messaging from the hierarchy above this generation. Provide resources though an established system and trusted

leaders. Use these generations as resources to share their experiences

with other employees. Communicate that when reporting misconduct they will be

protected.

1 BITC, How Businesses Are Harnessing the Power of Age Diversity (http://www.bitc.org.uk/blog/post/harnessing-power-age-diversity-and-adapting-business-ageing-workforce) Business In the Community

Your organization is a nationally recognized leader in innovative public employee benefits. The Board has been instrumental in setting policies underlying the national recognition.

You have served on the Board for nearly 3 years.

The Board has implemented a sound set of standards of professional conduct for Board and staff.

Staff have received a copy of the standards of professional conduct. But like many times, you have heard that the “standards” are just more “window dressing” and probably will not have any real or long term impact on performance.

Ethics question: What else can the Board do to increase “buy-in” to the new

standards?

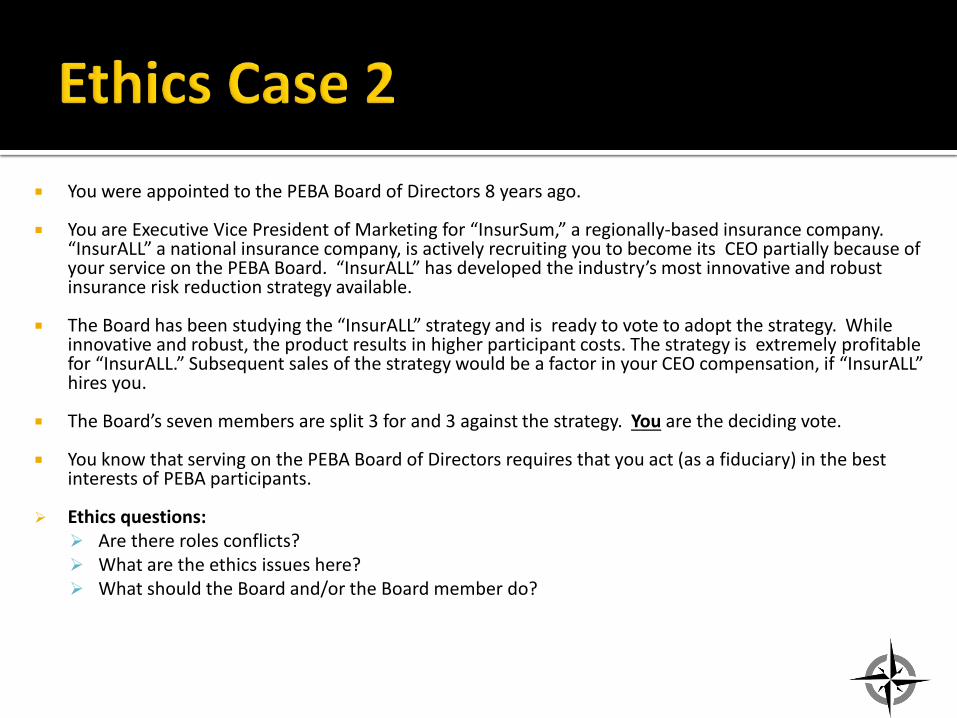

You were appointed to the PEBA Board of Directors 8 years ago.

You are Executive Vice President of Marketing for “InsurSum,” a regionally-based insurance company. “InsurALL” a national insurance company, is actively recruiting you to become its CEO partially because of your service on the PEBA Board. “InsurALL” has developed the industry’s most innovative and robust insurance risk reduction strategy available.

The Board has been studying the “InsurALL” strategy and is ready to vote to adopt the strategy. While innovative and robust, the product results in higher participant costs. The strategy is extremely profitable for “InsurALL.” Subsequent sales of the strategy would be a factor in your CEO compensation, if “InsurALL” hires you.

The Board’s seven members are split 3 for and 3 against the strategy. You are the deciding vote.

You know that serving on the PEBA Board of Directors requires that you act (as a fiduciary) in the best interests of PEBA participants.

Ethics questions: Are there roles conflicts? What are the ethics issues here? What should the Board and/or the Board member do?

Markkula Center For Applied Ethics at Santa Clara University www.scu.edu/ethics

Motza, Maryann, and Conder, Dean, “Relative Ethics: How Einstein’s Theory of Relativity Applies to Public Sector Ethics by Teaching Whose Ethical Perception is the Reality.” 26th Annual National Teaching Public Administration Conference. 2003.

Motza, Maryann, and Conder, Dean, “Sources of Power and Ethics: How Some Sources of Power are More Likely to Lead to Ethical Leadership.” 5th

International Conference on Ethics Across the Curriculum. 2003. Employment Law Solutions, Inc. (www.defendwork.com), Founded by Charles T. Passaglia, Esq., the firm is an employment law

consulting and training firm designed to prepare human resources professionals, executives and managers to make the most critical decisions in any organization: those affecting people.

Questions?

For additional ethics information and programs contact:

Dennis [email protected]

970.682.0742

PUBLIC EMPLOYEE BENEFIT AUTHORITY AGENDA ITEM BOARD RETREAT

Meeting Date: October 19, 2017 1. Subject: Healthcare Landscape 2. Summary: Our presenters will discuss the current landscape currently facing health plans, to include information about health care reform options, potential legislative changes at both national and state levels, and what is driving the cost of health care. Our presenting guests include representatives of our major SHP contractors: Jonah Houts, Vice President of Government Affairs at Express Scripts, James D’Allessio, Vice President of Government Affairs at Blue Cross Blue Shield of South Carolina, and Dr. Tripp Jennings, Clinical Innovations Officer at BCBSSC. 3. What is the Board asked to do? Receive as Information 4. Supporting Documents:

(a) List those attached: 1. State and National Update on Healthcare 2. The State of Government Affairs

BlueCross BlueShield of South Carolina is an independent licensee of the Blue Cross and Blue Shield Association

State and National Update on Healthcare

PEBA Board Retreat October 19, 2017

2

National Policy Landscape

3

National Policy Landscape

• Congressional Action

• Alexander – Murray • Graham – Cassidy • Common theme is enhanced state flexibility

• Regulatory Landscape • Uncertainty with opening at HHS

4

State Policy Landscape

5

State Policy Landscape

• Provider Issues

• Scope of Practice • Certificate of Need

• Coverage Issues

• Mandate Proposals

6

Healthcare Landscape

7

Healthcare Landscape

8

What 183 C-suite executives told us about their top concerns…

1. Improving ambulatory access (57% assigning an "A" grade); 2. Innovative approaches to expense reduction (57%); 3. Boosting outpatient procedural market share (55%); 4. Minimizing unwarranted clinical variation (54%); 5. Controlling avoidable utilization (49%); and 6. Exploring diversified, innovative revenue streams (48%).

Advisory.com/Research/Health Care Advisory Board/At the Helm/What 183 C-suite executives told us about their top concerns

9 Advisory.com/Research/Health Care Advisory Board/At the Helm/What 183 C-suite executives told us about their top concerns

“Boosting outpatient procedural market share”

“Improving ambulatory access”

10

“Innovative approaches to expense reduction”

“Minimizing unwarranted clinical variation”

“Controlling avoidable utilization”

• Reducing Labor Costs • Mergers/Partnerships • Process Improvement • Analytics • Clinical Leadership • Elimination of

programs

11

MACRA and the Physician Employment Landscape MACRA Potentially Accelerating End of Independent Physician Practice

Clinicians Already Seek Hospital Employment

Increase in hospital ownership of physician practices from 2012-2015

50% Increase in physicians employed by hospitals from 2012-2015

38% Of U.S. physicians are employed by a hospital or health system

86%

52%

73%

91%

Source: Whitman, E, “CEO Power Panel: Are your physicians ready for reform?” Modern Healthcare, September 2016, : Castellucci, M, “Hospital ownership of medical practices grows by 86% in three years,” Modern Healthcare, September 2016; Health Care Advisory Board interviews and analysis.

• Legislation passed in April 2015 repealing the Sustainable Growth Rate (SGR)

• CMS released final rule in October 2016 stipulating program to be implemented on Jan 1, 2017

• Created two payment tracks:

– Merit-Based Incentive Payment System (MIPS)

– Advanced Alternative Payment Model (APM)

Legislation in Brief: MACRA1

Source: CMS, “CY 2016 Physician Fee Schedule Final Rule,” Oct 30, 2016, available at: www.federalregister.gov; Health Care Advisory Board interviews and analysis.

92-8 Senate vote on MACRA

392-37 House vote on MACRA

Legislation Enjoyed Bipartisan Support

12

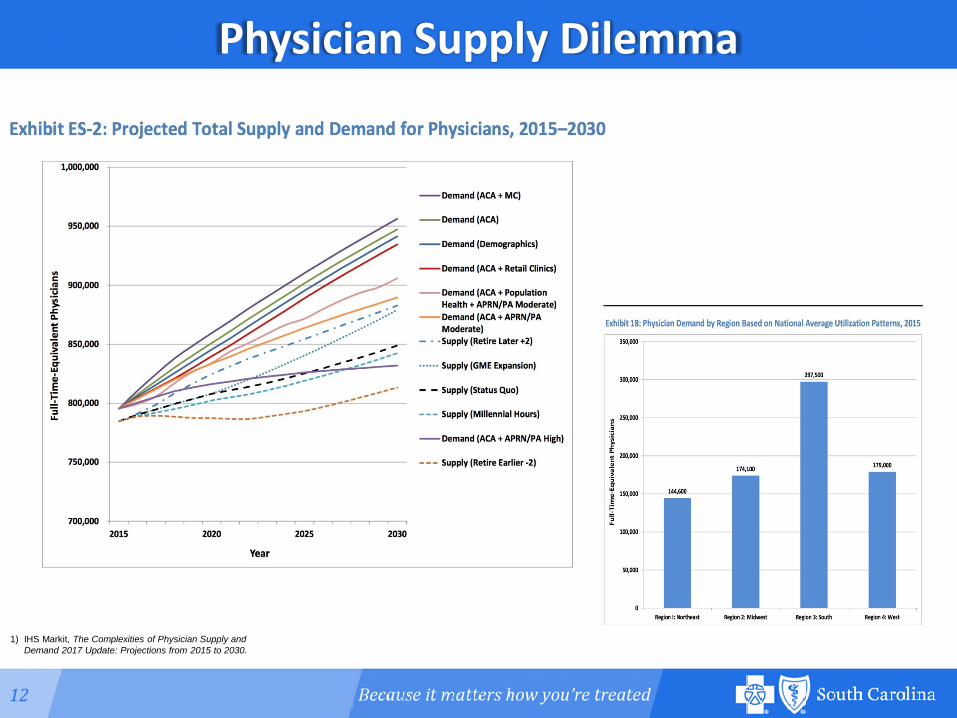

Physician Supply Dilemma

1) IHS Markit, The Complexities of Physician Supply and Demand 2017 Update: Projections from 2015 to 2030.

13

U. S. Expenditures on Healthcare

2

Source: (2) Willis Towers Watson: 2017 Human Capital Practice National Trend Survey

14

0

10

20

30

40

50

60

70

80

90

100

SHP 76.2%

South2

SHP 64.3%

United States

2016 SHP composite monthly premiums1 as a percentage of regional and national averages

Compared to other state employee health plans

1Composite Monthly Premiums: Weighted average of all PEBA health subscribers enrolled in each coverage level 2South: Includes Alabama, Arkansas, Florida, Georgia, Kentucky, Louisiana, Mississippi, North Carolina, Oklahoma, South Carolina, Tennessee, Texas, Virginia and West Virginia

Data from the 2017 PEBA 50-State Survey of State Employee Health Plans

State Health Plan vs. National Trends

Public and Private Sector Insurance

Plans1

State Health Plan2

2012 6.7% 6.4%

2013 5.6% 4.0%

2014 7.9% -1.4%

2015 8.2% 8.9%

2016 9.0% 4.2% (11/11)

1Includes active participants and retirees under the age of 65 in private and public sector insurance plans. 2Trend is defined as claims paid per member (includes employee and dependents). 3”11/11” means incurred in 11 months; paid in 11 months

Data from the 2016 Segal Health Plan Cost Trend Survey

15

Impact to South Carolina?

16

Questions

© 2015 Express Scripts Holding Company. All Rights Reserved.1

The State of Government Affairs

October 19, 2017

Jonah HoutsVice President, Corporate Government Affairs

2© 2017 Express Scripts Holding Company. All Rights Reserved.

The Political Landscape• All states (plus DC & PR) in session in 2017

• 800+ bills already introduced• 650 total in 2016• Aggressive, yet different agendas from brand

manufacturers and retail pharmacy community

• Significant trickle-down effects from federal (in)action

• States facing structural deficits

• National debate around high cost of prescription drugs is shaping policy discussions at state capitols

3© 2017 Express Scripts Holding Company. All Rights Reserved.

Legislative Priorities – Brand Manufacturers

• Historical agenda:• ADF opioids• Uniform prior authorization forms• Prohibit step therapy – Prescriber prevails

• 2017 agenda:• High cost drugs/transparency – shift focus onto

PBMs• Frozen formularies• Anti-step therapy

4© 2017 Express Scripts Holding Company. All Rights Reserved.

Legislative Priorities – Community Pharmacists

• Historical agenda:• Generic reimbursement/guaranteed profitability• Prohibitions on mail channel• Audit

• 2017 agenda:• Any Willing (Specialty) Pharmacy• Transaction fees/Credentialing• Refuse to fill

5© 2017 Express Scripts Holding Company. All Rights Reserved.

Historical South Carolina Agenda• 2016

• Generic pricing reforms• Pharmacy Association may want to revisit this law

• 2017• Biosimilar substitution • Opioid reforms

6© 2017 Express Scripts Holding Company. All Rights Reserved.

Anticipated South Carolina Agenda• Prior authorization

• Prescriber led effort• Likely to seek standardized forms, approval

timelines• Opportunity: ePA

• Opioids• Task force seeking solutions• Likely to limit initial rx duration

7© 2017 Express Scripts Holding Company. All Rights Reserved.

Biosimilars – where we are today

WA

MT

WY

OR

NVCA

ID

UT

AZ

CO

NM

ND

SD

NE

KS

MN

IA

TX

MO

AR

WI

IL

LA

MI

IN OH

KY

MS AL GA

TNSC

PA

NC

VAWV

NY

ME

NH

VT

MARI

NJCT

MDOK

DEDC

FL

Enacted Law

Introduced in 2017

HI PRAK

8© 2017 Express Scripts Holding Company. All Rights Reserved.

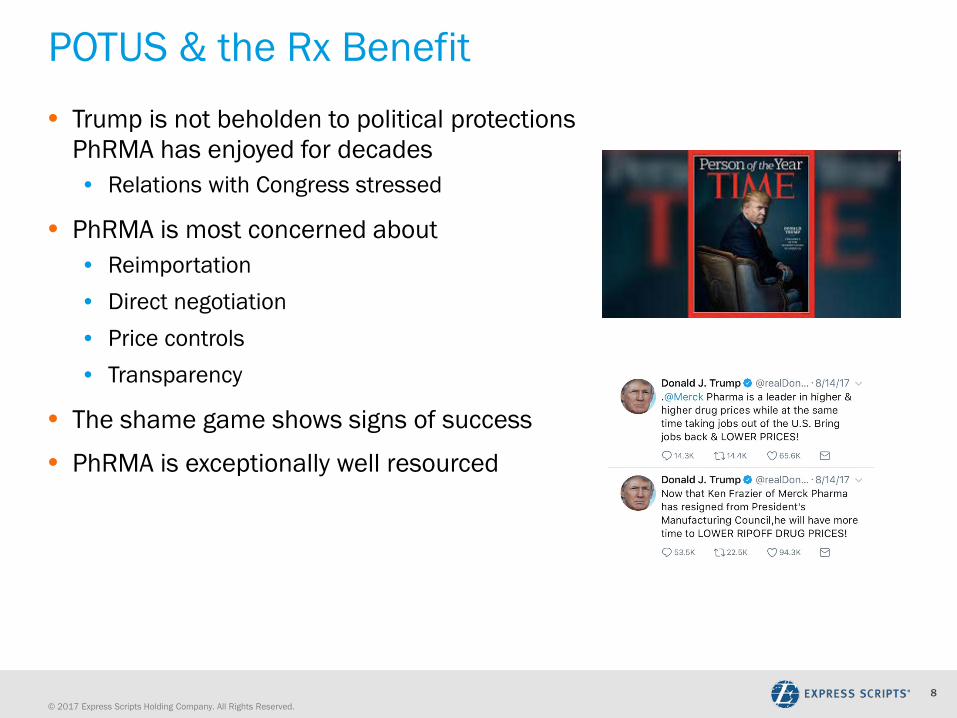

POTUS & the Rx Benefit• Trump is not beholden to political protections

PhRMA has enjoyed for decades• Relations with Congress stressed

• PhRMA is most concerned about• Reimportation• Direct negotiation• Price controls• Transparency

• The shame game shows signs of success

• PhRMA is exceptionally well resourced

9© 2017 Express Scripts Holding Company. All Rights Reserved.

Congress: Tied In Knots

• Health Care: Failed• Tax Reform: No Plan• Debt Ceiling/Funding Government: kick can down the

road (December)• Republicans can’t govern with Majority: Trump needed to

make deals with Democrat Leadership

10© 2017 Express Scripts Holding Company. All Rights Reserved.

Serious Legislative Risks Under Consideration

Cassidy - GrahamACA•Some in GOP were bullish on last ditch effort•Countless derailers

Alexander - MurrayCSR•Bipartisan agreement, but in wrong Committee•Timing hurdles frustrate effort

Hatch 5-Year ExtenderCHIP•Bipartisan compromise•Not yet paid for

11© 2017 Express Scripts Holding Company. All Rights Reserved.

The Legislative Process is Stalled

January: Congress debates repeal through reconciliation