Mediterranean Investment and Partnership Observatory

17

ANIMA-MIPO ANIMA MIPO FDI and Partnership Observatory 4 lessons from the crisis MENA-OECD Investment Programme MENA OECD Investment Programme 19-20 March 2013 www.anima.coop

-

Upload

oecdglobal -

Category

News & Politics

-

view

287 -

download

2

Transcript of Mediterranean Investment and Partnership Observatory

ANIMA-MIPOANIMA MIPO FDI and PartnershipObservatory

4 lessons fromthe crisis

MENA-OECD Investment ProgrammeMENA OECD Investment Programme19-20 March 2013

www.anima.coop

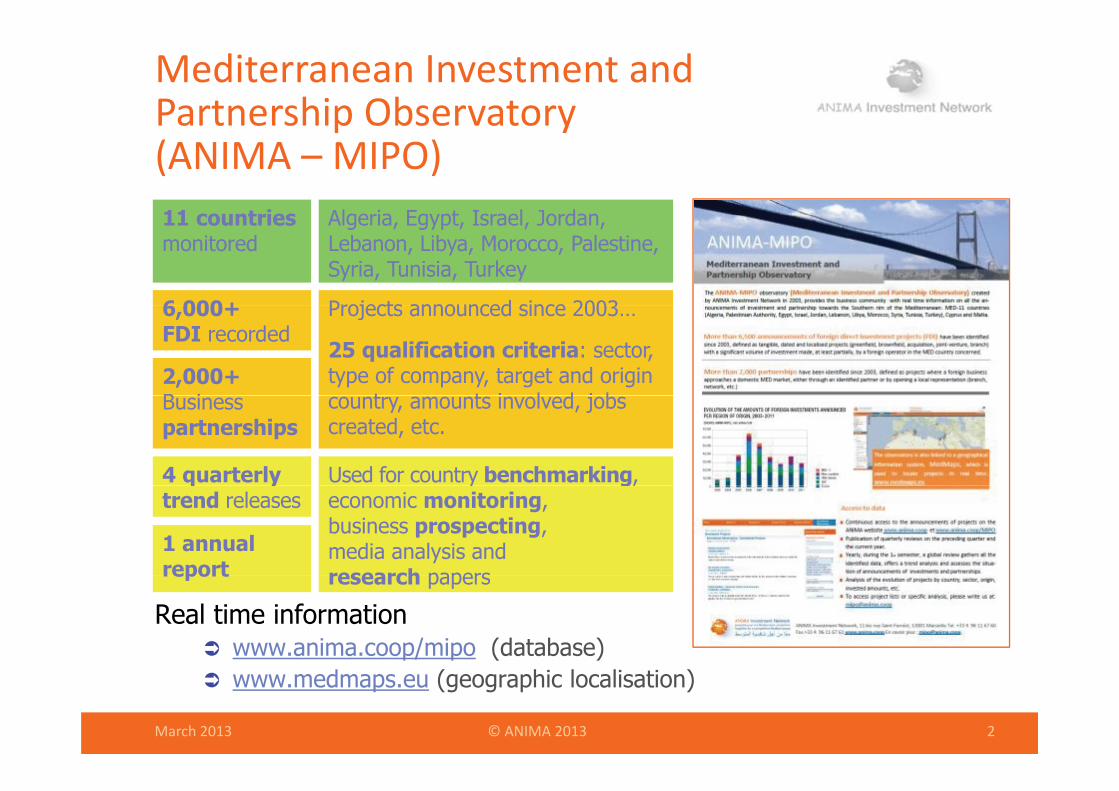

Mediterranean Investment and Partnership Observatoryp y(ANIMA – MIPO)11 countries Algeria Egypt Israel Jordan

6 000+

11 countriesmonitored

Algeria, Egypt, Israel, Jordan, Lebanon, Libya, Morocco, Palestine, Syria, Tunisia, Turkey

Projects announced since 20036,000+ FDI recorded

2,000+ B i

Projects announced since 2003…

25 qualification criteria: sector, type of company, target and origin

t t i l d j bBusiness partnerships

4 quarterly Used for country benchmarking,

country, amounts involved, jobs created, etc.

q ytrend releases

y g,economic monitoring, business prospecting, media analysis and research papers

1 annual report

Real time information www.anima.coop/mipo (database)

research papersreport

March 2013 © ANIMA 2013 2

www.medmaps.eu (geographic localisation)

4 lessons from the crisis 2008‐2012

FDI in the MED region in 2012:g

A good resilienceA good resilience

#1#1

Change in FDI flows & number of projects in 2012p j € 37.0 bn FDI announced in 2012: +5% in comparison with 2010 645 projects detected: -24% in comparison with 2010

64 523789

844 90070 000

FDI inflows ANIMA (€m) FDI inflows UNCTAD (€m) Number of projects

53 002

51 046 42 885

621

761 784 789

562

666 645

600

700

800

50 000

60 000

proj

ects

ws

(€m

illio

n)

35 145

37 272

28 036

35 313

27 184

37 061

30 135

51 04646 369

30 038

28 734

30 301

249306

300

400

500

30 000

40 000

Num

ber

of p

FDI i

nflo

w

9 860

11 683

27 184

12 397

11 342

28 734249

100

200

300

10 000

20 000

00

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

March 2013 © ANIMA 2013 4

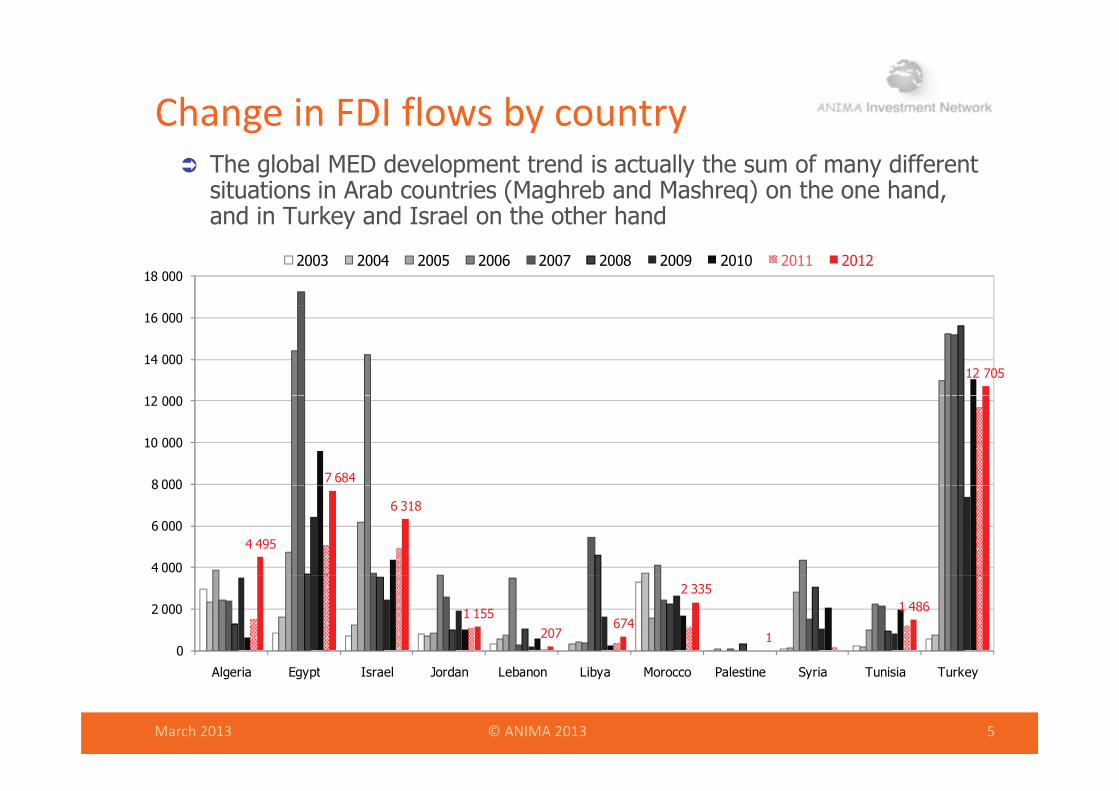

Change in FDI flows by countryg y y The global MED development trend is actually the sum of many different

situations in Arab countries (Maghreb and Mashreq) on the one hand, and in Turkey and Israel on the other handand in Turkey and Israel on the other hand

18 0002003 2004 2005 2006 2007 2008 2009 2010 2011 2012

12 70514 000

16 000

7 6848 000

10 000

12 000

4 495

6 318

4 000

6 000

8 000

1 155207

674

2 335

1

1 486

0

2 000

March 2013 © ANIMA 2013 5

Algeria Egypt Israel Jordan Lebanon Libya Morocco Palestine Syria Tunisia Turkey

Inward FDIs: invested amounts2006 2007 2008 2009 2010 2011 2012

€12.7 bn in 2012 127 projects

€6.3 bn in 2012 152 projects

TurkeyBank, Energy,

Real estate, Agribusiness, Di t ib ti A t ti

IsraelITC, Energy,

Drugs, Biotech

€1.5 bn in 2012 74 projects

€0 bn in 20120 project

Distribution, Automotive

€0.2 bn in 2012 19 j

€4.5 bn in 2012 44 projects€2.3 bn in 2012

120 projects

TunisiaTelecom, Energy,

Bank, Tourism,Consulting, Software

SyriaEnergy, Cement,

Real estate, Bank

€1 2012

LebanonTourism & Real estate , Bank,

Telecom, Consulting

19 projects

€0.7 bn in 2012 14 projects

€7.7 bn in 2012 68 projects

MoroccoTourism & Real Estate, Telecom, Bank, Agribusiness,

Automotive

AlgeriaEnergy, Telecom, Cement, Metallurgy,

Real estate

Lib

PalestineReal estate, ITC

€1m 2012 3 projects

€1.2 bn in 2012 24 projects

LibyaEnergy, Real estate,

Bank, Cement

EgyptE T l

Jordan

March 2013 © ANIMA 2013 6

Source: ANIMA-MIPO, Announced FDI ProjectsEnergy, Telecom,

Real estate, Cement, Bank

Jo daReal estate &

Tourism, Energy, Bank,Telecom

4 lessons from the crisis 2008‐2012

I t b h iInvestors behavior changed during the 2008‐2012 crisisg g

A more cautious approachA more cautious approach

#2#2

Change in partnership projects in 2012 Partnerships (ANIMA-MIPO): i.e. Non-Equity Modes of International

Production and Development (UNCTAD) 505 j t d t t d i 2012 2% i i ith 2010 505 projects detected in 2012: -2% in comparison with 2010

515

600

Management contract515

377

505

400

500

ersh

ips

Management contract

Technological partnership

Development agreement

152

207

295

200

300

umbe

r of

par

tn

Commercial partnership

Representative office

37

10889

123152

0

100

Nu

Franchise, shop, etc.

0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

March 2013 © ANIMA 2013 8

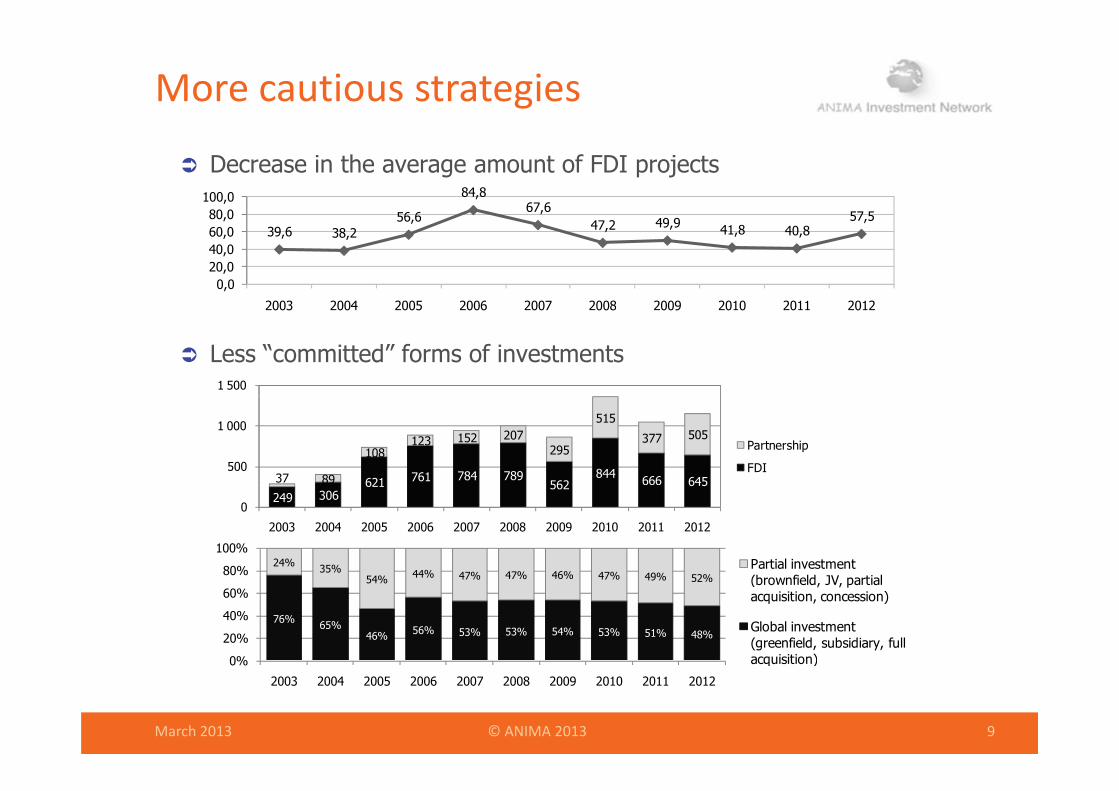

More cautious strategies

Decrease in the average amount of FDI projects

56 6

84,867,6

57 580 0100,0

39,6 38,256,6

47,2 49,9 41,8 40,857,5

0,020,040,060,080,0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

1 500

Less “committed” forms of investments

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

621 761 784 789562

844 666 64537 89

108123 152 207

295

515

377 505

500

1 000

Partnership

FDI

249 306621 562 645

0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

24% 35% 44% 47% 47% 46% 47% 49% 52%80%

100%Partial investment (b fi ld JV i l

76% 65%46% 56% 53% 53% 54% 53% 51% 48%

54% 44% 47% 47% 46% 47% 49% 52%

0%

20%

40%

60%

80%(brownfield, JV, partial acquisition, concession)

Global investment (greenfield, subsidiary, full acquisition)

March 2013 © ANIMA 2013 9

0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

q )

4 lessons from the crisis 2008‐2012

Origin of foreign investment

The decline of Europe pleadership

#2#2

Inward FDIs: number of projects

Europe = still 45% of announced FDI in 2012 in number of projects, but the European leadership is faltering

Oth i Other regions: North America = 23% Gulf = 12%

Other countries (including BRICs) =14% Other countries (including BRICs) =14% Intra-MED = 6%

Western investors (Europe, North America): a crisis of confidence?377 392400

318341

377 372

306

392

312289

300

400

ects

Europe

G lf

152174

158 148123

138

204 199

150200

Num

ber

of p

roje Gulf

USA-Canada

80 71

104

597836

47

123

138 136101

6274 78

83 8770

92

3850 53 50

2957

36

100

N

Other countries

MED-11

March 2013 © ANIMA 2013 11

14 1838 29 26 360

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Inward FDIs: invested amounts

2012 is a record year for the “Other countries” (including BRICs) in announced FDI amounts

4 projects > €1bn : Bank Telecom & Tourism in Turkey Egypt & Algeria 4 projects > €1bn : Bank, Telecom & Tourism in Turkey, Egypt & Algeria FDI from the Gulf States on the rise again

Major sectors: Bank, Real estate, Tourism and TelecomBut a rising interest in Agrifood Renewable energy Consulting But a rising interest in Agrifood, Renewable energy, Consulting...

60000

70000

FDI inflows

30 1

327856693360

20157

5923

40000

50000

60000

USA-Canada

FDI inflows in € million

6714

19375

14758

8484

62233801

3071

3940

5656

20148793

5529

10766

70994742

4208

4992

5869

6294

20000

30000Other countries

MED-11

lf

4550 7262

15986 16698

2599918321 15461 17211

12775 991018432009

62232623 9631

9601654

0

10000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Gulf

Europe

March 2013 © ANIMA 2013 12

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

4 lessons from the crisis 2008‐2012

A sector rotation since 2011

Towards more inclusive investments?

#4#4

2011 and 2012: record years for productive investmentspTop 5 unchanged

Energy, Banking, Telecoms, Building and public works and Cementgy, g, , g p

But the crisis has favoured strategic sectors for the region Software, Automobiles, Medicines: a slow but constant rise, , Agrifood, Distribution, Consulting: encouraging trend in 2011 but a

decline in 2012 Aeronautics and Mechanics: a good performance in 2012g p cf. ANIMA/CMI survey (2011): most effective sectors in terms

of job creation

March 2013 © ANIMA 2013 14

Boosting EuroMed MSMEs

Emphasise current FDI trends Regional cluster initiatives to make the Mediterranean attractive on g

GLOBAL SPECIALTIES: Agrifood, Logistics, ICT, Media, Medicines, Automotive and Aeronautics industries, Distribution, etc.

Develop national aftercare strategies to boost reinvestments ( t ti l f €10 15 b )(potential of €10-15 bn)

2%5%

Global FDI inflows : MED-11 share (UNCTAD)

2,5% 2,4%1 8%

3,7%4,2%

3,0%3,3% 3,2%

2,8% 2,6%3%

4%

0,8%

1,4%1,8%

0%

1%

2%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

March 2013 © ANIMA 2013 15

Promoting more inclusive investments

The EDILE initiative Developing better investment projects around the Mediterranean: p g p j

more inclusive activities, lower impact on the environment, higher local participation (jobs, etc.)

Mixing territories and financing institutions Building a referential for evaluating project global performance

Take investment inclusiveness into account Quantity and quality of jobs, economic spillovers and subcontracting,

compatibilit ith co nt economic and te ito ial st ategcompatibility with country economic and territorial strategy Leverage on local banks to drive investments to more inclusiveness,

by associating Development Finance Institutions Improve local governance for project appraisal Improve local governance for project appraisal

Associate local authorities, CCI, Business Federations, investment authorities, civil society

March 2013 © ANIMA 2013 16

Thank you for your attention

Emmanuel NOUTARY, General Delegate Emmanuel NOUTARY, General [email protected]

Zoé LUÇON, Project Managerzoe lucon@anima [email protected]

ANIMA Investment Network11b rue Saint Ferréol13001 Marseille – FRT. +33(0) 4 9611 6760www anima coopwww.anima.coop

![Mediterranean Sea: The GEF Strategic Partnership for the Mediterranean LME (Lascaratos) [IWC4 Presentation]](https://static.fdocuments.us/doc/165x107/5468abe2af7959a75e8b4b3e/mediterranean-sea-the-gef-strategic-partnership-for-the-mediterranean-lme-lascaratos-iwc4-presentation.jpg)