Medical device cm os merger and acquisition buyer's view and standpoint

26

-

Upload

beroe-inc -

Category

Health & Medicine

-

view

133 -

download

0

Transcript of Medical device cm os merger and acquisition buyer's view and standpoint

Please take a note

• How to post a question?

• To log in again if the connection is lost, use the link in the confirmation mailer you would have received from [email protected]

• In case you face any other issues write an email to [email protected]

Members for the Webinar

Chanderkanth Gautham Lead Analyst

Beroe-Inc. Dialing in from:

India

Speaker

Janani Narasimhan Engagement Manager

Beroe-Inc. Dialing in from:

India

Moderator

Agenda and need of the hour

5

What is triggering the M&A? 01

What are hidden patterns and how they can be put to use? 02

What are the services that are being included by leading CMOs in their product offerings 03

What are the major KPIs that need to be evaluated while partnering with leading

CMOs? 04

Mergers & Acquisitions – Worry points and beyond

6

Increase in

Supplier Power

Limited

Negotiation Power

Increased

Product Pricing

Over

Dependency on Vendor

Factors triggering M&As in Medical Devices CMO Market (1/2)

7

OEM Cost Structure Shift

0

25

50

COGS SG and A

Drift to core competency i.e., “R&D” and “Sales and Marketing”

CMOs scaling up to fill the manufacturing gap

Past Present Future

73

28

3

6

16

37

1

5

7

24

0 20 40 60 80 100 120

Medical Device CMO

Medical Device OEM

Percentage (%) Cost of Good Sold Research and Development

Sales, Marketing, General and Administrative Expenses Other Operating Expenses

Operating Margin

8

Cost Overview: OEM Vs. CMO

73

28 6 37 5 24

3 16 7 1

Drift to core competency i.e., “R&D” and “Sales and Marketing”

CMOs scaling up to fill the manufacturing gap

Factors triggering M&As in Medical Devices CMO Market (2/2)

0%

20%

40%

60%

80%

100%

120%

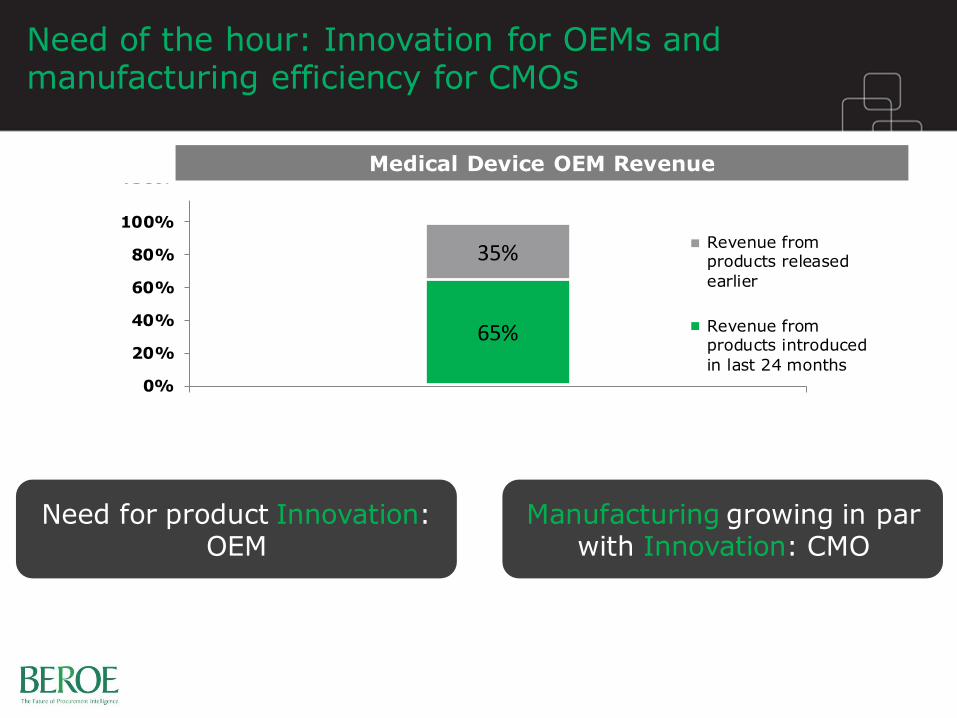

Medical Device OEM Revenue

Revenue fromproducts released

earlier

Revenue fromproducts introduced

in last 24 months

Need of the hour: Innovation for OEMs and manufacturing efficiency for CMOs

35%

65%

Need for product Innovation: OEM

Manufacturing growing in par with Innovation: CMO

Medical Device OEM Revenue

Acquisition Expansion Partnership Product launch

Activity Type of Medical Device CMOs – 2013 to 2014

Medical device CMOs activity meter – Focus on acquisition and expansion

10

Need of the Hour: Understand the key activities rational

25% 5% 40% 30%

Activity Type of Medical Device CMOs – 2013 to 2014

Activity focus of Medical Device

CMOs

What CMOs activities look like

Medical Device CMO – Shift from singular focus to multi-specialization

11

Key activity insight

Leverage it based on your operational overlap

Recent Past

Past

Component Manufacturing

Recent

Past

Component Manufacturing/

Design/Prototype

Current

Component Manufacturing/

Design/Prototype

Future

Component Manufacturing/Design/ Prototype/Packaging/

Other therapeutic Focus

Great Batch

Sierra KD GTM HMMC

Cardiac

Precimed

Orthopedic

Great Batch

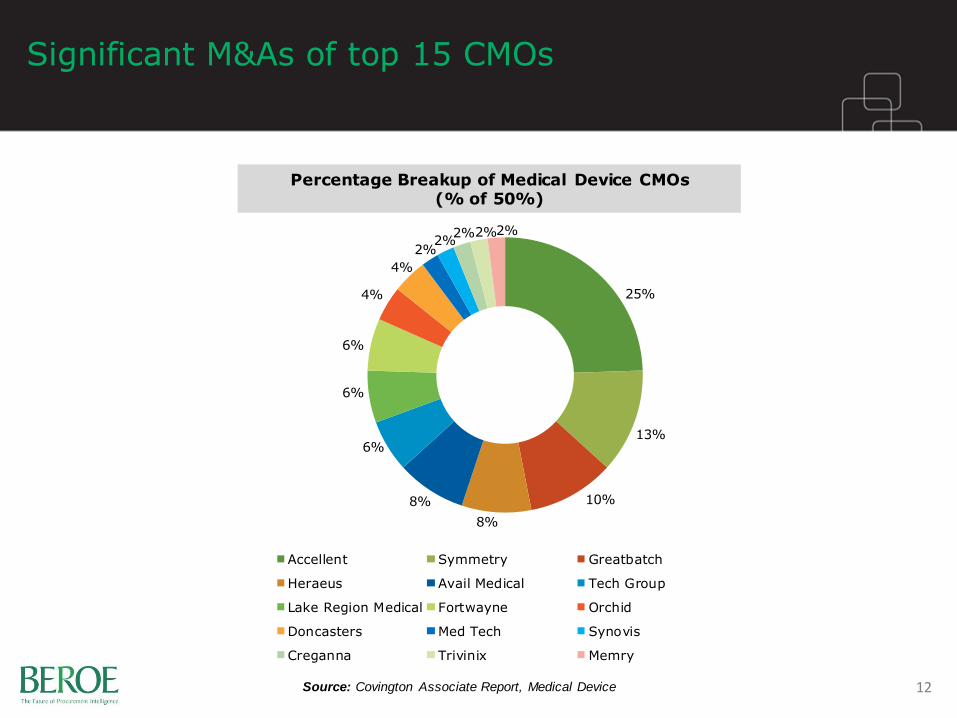

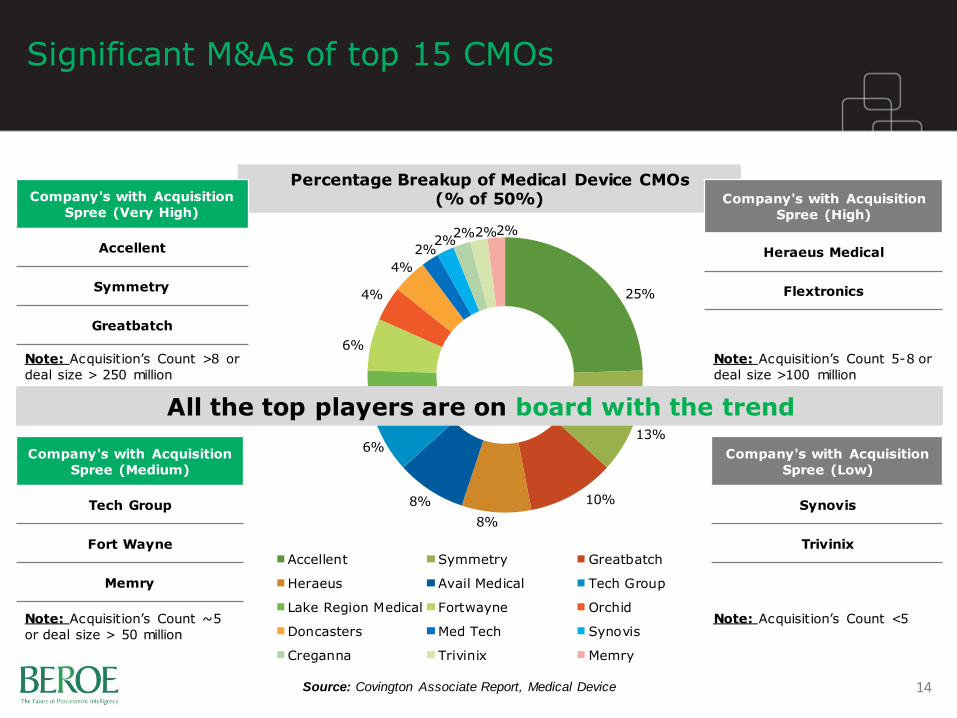

Significant M&As of top 15 CMOs

12

25%

13%

10%

8%

8%

6%

6%

6%

4%

4%

2% 2%

2% 2% 2%

Accellent Symmetry Greatbatch

Heraeus Avail Medical Tech Group

Lake Region Medical Fortwayne Orchid

Doncasters Med Tech Synovis

Creganna Trivinix Memry

Source: Covington Associate Report, Medical Device

Percentage Breakup of Medical Device CMOs (% of 50%)

Significant M&As of top 15 CMOs

13 Source: Covington Associate Report, Medical Device

Beyond Great batch

Company's with Acquisition

Spree (Very High)

Accellent

Symmetry

Greatbatch

Company's with Acquisition

Spree (High)

Heraeus Medical

Flextronics

Company's with Acquisition

Spree (Medium)

Tech Group

Fort Wayne

Memry

Company's with Acquisition

Spree (Low)

Synovis

Trivinix

Note: Acquisition’s Count >8 or

deal size > 250 million

Note: Acquisition’s Count 5-8 or

deal size >100 million

Note: Acquisition’s Count <5 Note: Acquisition’s Count ~5

or deal size > 50 million

Significant M&As of top 15 CMOs

14

25%

13%

10%

8%

8%

6%

6%

6%

4%

4%

2% 2%

2% 2% 2%

Accellent Symmetry Greatbatch

Heraeus Avail Medical Tech Group

Lake Region Medical Fortwayne Orchid

Doncasters Med Tech Synovis

Creganna Trivinix Memry

Source: Covington Associate Report, Medical Device

Percentage Breakup of Medical Device CMOs (% of 50%)

Beyond Great batch

Company's with Acquisition

Spree (Very High)

Accellent

Symmetry

Greatbatch

Company's with Acquisition

Spree (High)

Heraeus Medical

Flextronics

Company's with Acquisition

Spree (Medium)

Tech Group

Fort Wayne

Memry

Company's with Acquisition

Spree (Low)

Synovis

Trivinix

Note: Acquisition’s Count >8 or

deal size > 250 million

Note: Acquisition’s Count 5-8 or

deal size >100 million

Note: Acquisition’s Count <5 Note: Acquisition’s Count ~5

or deal size > 50 million

All the top players are on board with the trend

Patterns to be leveraged

15

Acquisition amid Top 15 CMOs and

Identification of Avenues to be leveraged 1

Addition of services and therapeutic

areas resulting in One Stop Shop 2

Emerging Market penetration of

CMO 3

Leveraging New Entrants from Non-

core industry 4

16

Acquisition amid Top 15 CMOs: Opportunities 1

Top CMOs options

Rely on the best and get the best

Accellent and Lake Region: 12>>>18%

Heraeus and Synovis 4>>>>6%

Orchid and Doncasters 2>>>>4%

Can accommodate higher volume across therapeutic areas

Can accommodate Surgical Device Portfolio

Can accommodate higher volumes of Orthopedics

Merger

between 1 and 7

Merger

between 4 and 12

Merger

between 9 and 10

17

Addition of services resulting in One Stop solutions: Critical area

consolidation 2

Room for Therapeutic

Consolidation

Room for Service

Consolidation

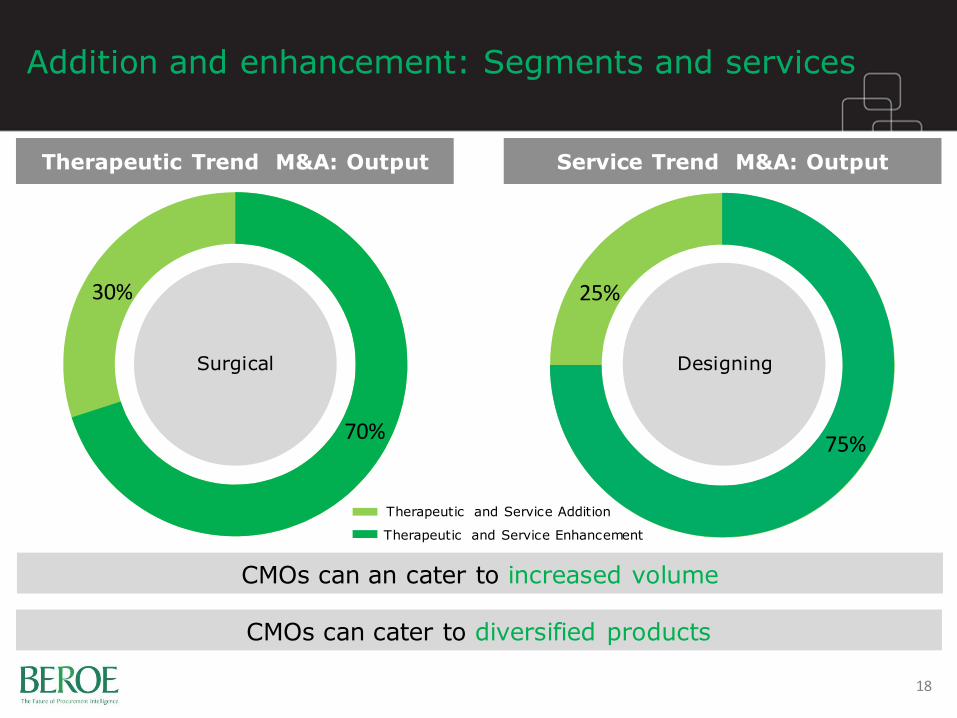

25% 30%

Addition and enhancement: Segments and services

18

Therapeutic Trend M&A: Output

70%

Service Trend M&A: Output

75%

Surgical Designing

CMOs can an cater to increased volume

CMOs can cater to diversified products

Therapeutic and Service Enhancement

Therapeutic and Service Addition

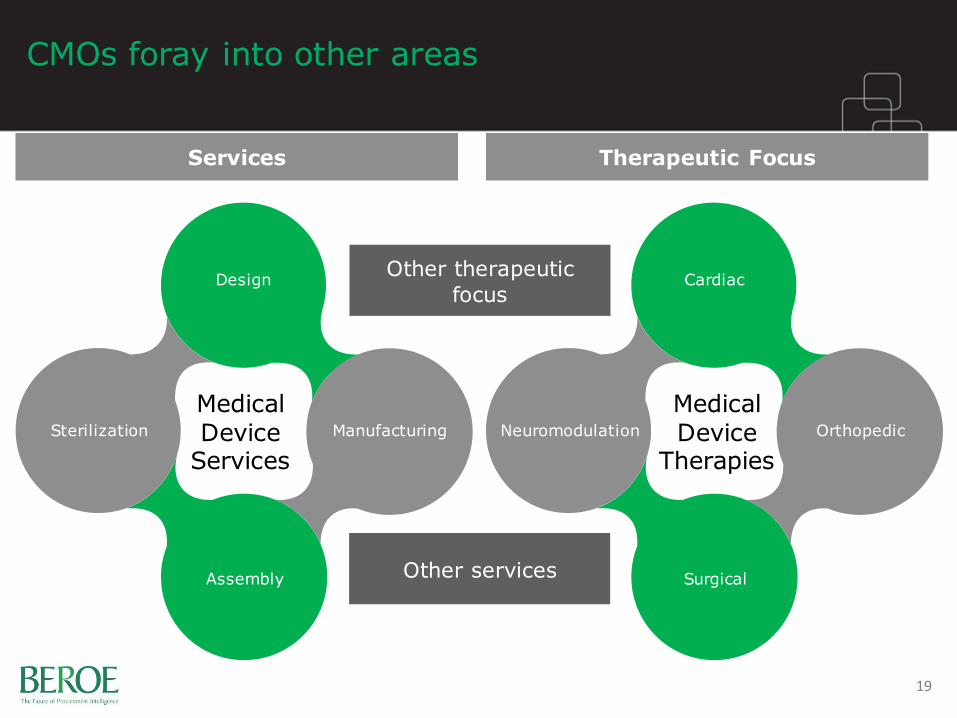

CMOs foray into other areas

19

Services

Medical Device

Services

Design

Manufacturing

Assembly

Sterilization

Therapeutic Focus

Cardiac

Orthopedic

Surgical

Neuromodulation

Medical Device

Therapies

Other therapeutic

focus

Other services

20

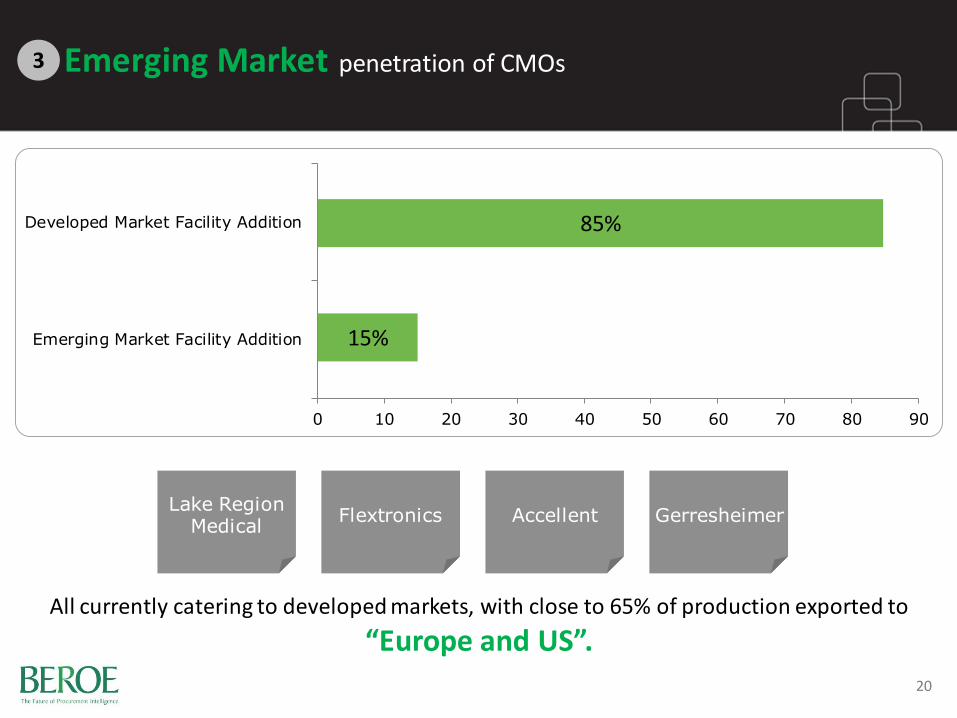

Emerging Market penetration of CMOs 3

15

85

0 10 20 30 40 50 60 70 80 90

Emerging Market Facility Addition

Developed Market Facility Addition

All currently catering to developed markets, with close to 65% of production exported to

“Europe and US”.

Lake Region Medical

Flextronics Accellent Gerresheimer

85%

15%

21

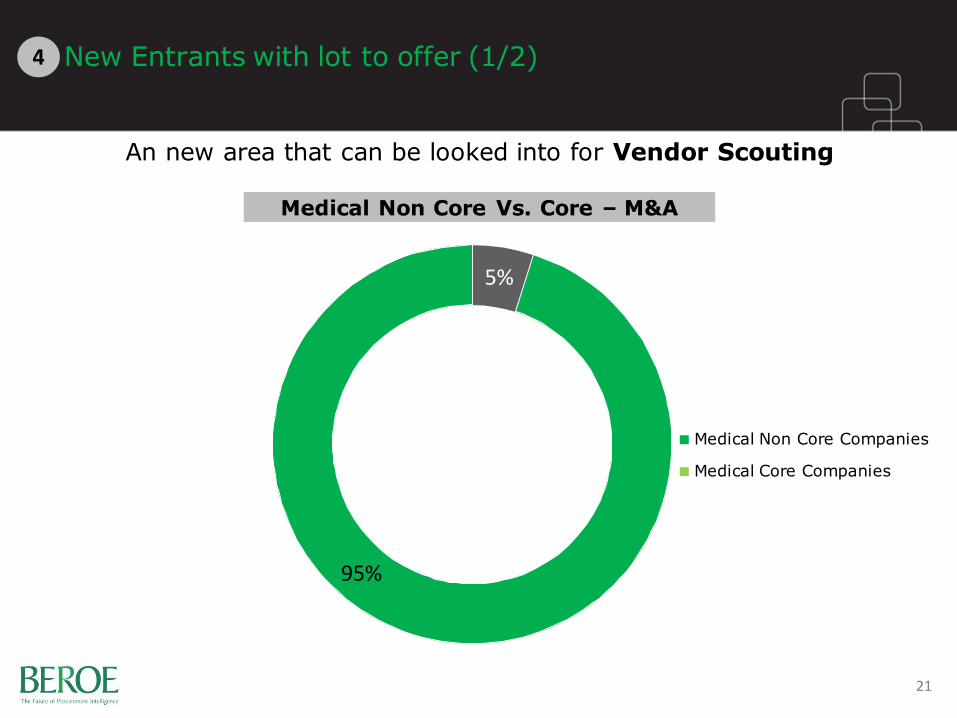

New Entrants with lot to offer (1/2) 4

An new area that can be looked into for Vendor Scouting

Medical Non Core Vs. Core – M&A

5%

Medical Non Core Companies

Medical Core Companies

95%

Flextronics Acquisition

22

4

Riwisa Year of Acquisition: 2013

Therapeutic Focus: Drug Delivery Devices

Avail Medical Year of Acquisition: 2007

Therapeutic Focus: Catheters and Drug Delivery Devices

Stellar Microelectronics

Year of Acquisition: 2012

Therapeutic Focus: EMS for Healthcare and Others Industries

New Entrants with lot to offer (2/2)

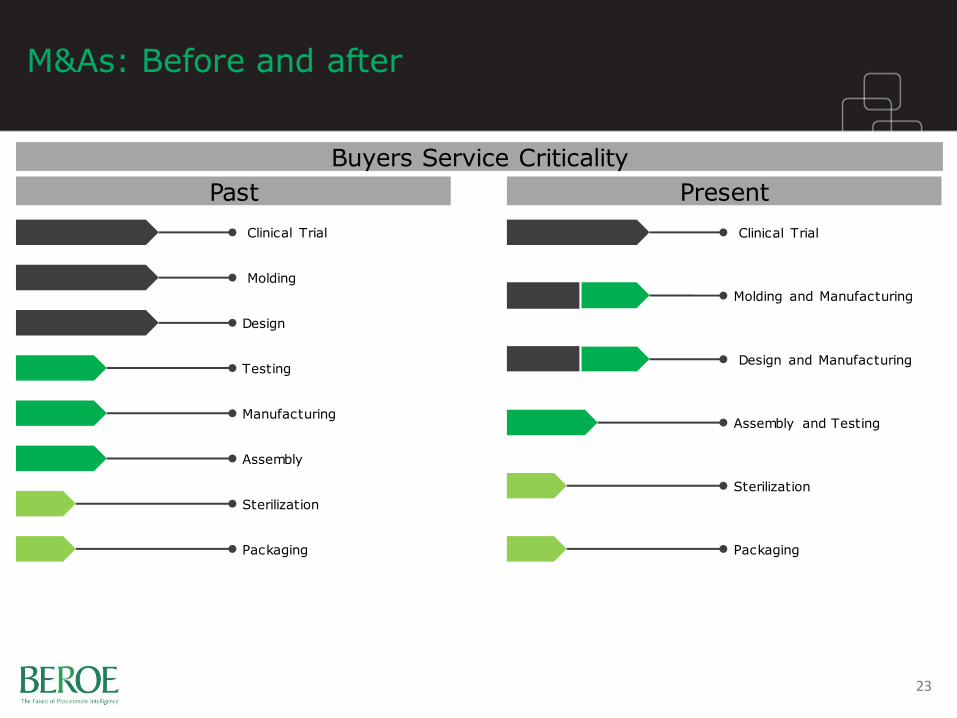

M&As: Before and after

23

Buyers Service Criticality

Clinical Trial

Molding

Design

Testing

Manufacturing

Assembly

Sterilization

Packaging

Clinical Trial

Assembly and Testing

Sterilization

Packaging

Molding and Manufacturing

Design and Manufacturing

Present Past

24

Cardiac

Orthopedic

Surgical

Others

Cardiac and orthopedic

Orthopedic and surgical

Therapeutic Focus Criticality

Present Past

Others

Future generation

Current generation

Future & current generation

Device Phase Criticality

Present Past

Developed

Emerging

Emerging & Developed

Market Criticality

Present Past

M&As: Before and after

Quick snapshot

25

Service

Consolidation

Therapeutic

Consolidation

Emerging Market

Venture

Supplier Readiness

Cost Savings

Innovation Support

Supplier Readiness

Technology readiness

Capacity Addition

Supplier Readiness

Regulatory

Cost Savings

High High Medium

What to look for!

26