Mechanics of Options Markets Chapter 8 1. 2 Assets Underlying Exchange-Traded Options Page 183-184...

19

Mechanics of Options Mechanics of Options Markets Markets Chapter 8 1

-

Upload

rosemary-thornton -

Category

Documents

-

view

237 -

download

1

Transcript of Mechanics of Options Markets Chapter 8 1. 2 Assets Underlying Exchange-Traded Options Page 183-184...

Mechanics of Options Mechanics of Options MarketsMarkets

Chapter 8

1

2

Assets UnderlyingAssets UnderlyingExchange-Traded OptionsExchange-Traded Options

Page 18Page 1833-18-1844

Stocks Stock IndicesFutures Foreign CurrencyBond options VIX

3

OptionsOptions

Options are generally different from forwards & futures contracts. An options gives the holder of the option the right to do something

Call optionsPut optionsBuyer or holderSeller or writerPremiumStrike priceMaturity date

Contract SpecificationsContract Specifications

Market type : NInstrument Type : OPTSTKUnderlying : Symbol of underlying securityExpiry date : Date of contract expiryOption Type : CE / PEStrike Price: Strike price for the contract

Trading cycle: Options contracts have a maximum of 3-month trading cycle - the near month (one), the next month (two) and the

far month (three).

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 4

5

Call OptionCall Option

A call option is a right, but not an obligation to buy an asset at a predetermined price within a specified time.

Long call- expect price rise. Holder of the call has an option to exercise call or not. For this right he pays premium.

Short Call-The call writer does not believe the price of the underlying security is likely to rise. The writer sells the call to collect the premium and does not receive any gain if the stock rises above the strike price.

Payoffs (Call option)Payoffs (Call option)

When S<X buyer lets the call expire

When S=X buyer is indifferent

When S>X buyer exercise the call option

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 6

Loss=premium c

Loss=premium c

Gain=S-X-c

7

A Long position in a Call A Long position in a Call optionoption

Profit from buying one European call option: option price = $5, strike price = $100, option life = 2 months

Max(S-X, 0)

30

20

10

0-5

70 80 90 100

110 120 130

Payoff ($)

Terminalstock price ($)

8

A Short position in a A Short position in a Call Call (Figure 8.3, page 18(Figure 8.3, page 1822))

Profit from writing one European call option: option price = $5, strike price = $100.

Min(X-S, 0)

-30

-20

-10

05

70 80 90 100

110 120 130

Payoff ($)

Terminalstock price ($)

9

Put optionPut option

A put option is a right, but not an obligation to sell an asset at a predetermined price within a specified time.

Long put- expect price fall. Holder of the put has an option to exercise putor not. For this right he pays premium.

Short put- doesn’t receive any gain if SP< Strike Price

The option writer receives a premium and incurs an obligation to purchase (if a put is sold) the underlying asset at a stipulated price until a predetermined date.

Payoffs (Put option)Payoffs (Put option)

When S>X buyer lets the call expire

When S=X buyer is indifferent

When S<X buyer exercise the call option

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 10

Loss=premium p

Loss=premium p

Gain=X-S-p

11

A Long A Long position in a position in a Put Put (Figure 8.2, page 18(Figure 8.2, page 1811))

Profit from buying a European put option: option price = $7, strike price = $70

Max(X-S, 0)

30

20

10

0

-770605040 80 90 100

Payoff ($)

Terminalstock price ($)

12

A Short A Short position in a position in a Put Put (Figure 8.4, page 18(Figure 8.4, page 1822))

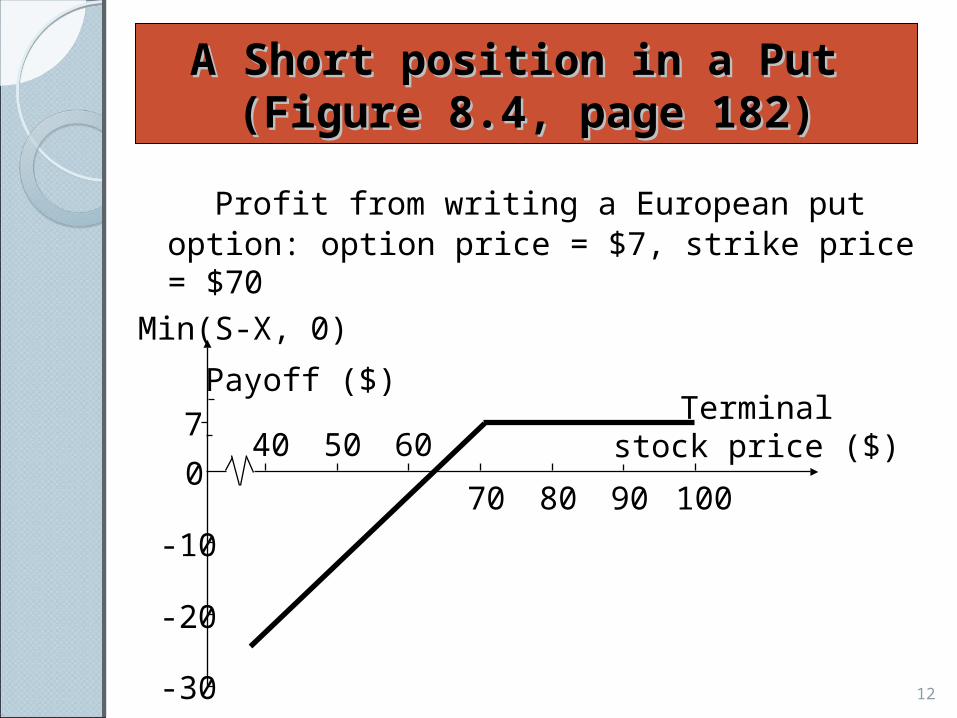

Profit from writing a European put option: option price = $7, strike price = $70

Min(S-X, 0)

-30

-20

-10

7

070

605040

80 90 100

Payoff ($)Terminal

stock price ($)

Zero- sum gameZero- sum game

Payoff of call option X=190

13

Price of the assets

Payoff-call buyer Payoff-call writer

Buy from writer

Sell in the market

Profit/loss

Sell to holder

Buy from market

Profit/loss

125

Holders doesn’t exercise the call option, losses premium

paid

Obligation of writer doesn’t arise, gains premium received

150

175

200 190 200 10 190 200 -10

225 190 225 35 190 225 -35

Zero- sum gameZero- sum game

Payoff of put option X=160

14

Price of the assets

Payoff-put buyer Payoff-put writer

Sell to writer

Buy from the market

Profit/loss

Pay to holder

Sell in the market

Profit/loss

125 160 125 35 160 125 -35

150 160 150 10 160 150 -10

175

Holders doesn’t exercise the put option, losses premium

paid

Obligation of writer doesn’t arise, gains premium received

200

225

15

Payoffs from OptionsPayoffs from OptionsWhat is the Option Position in Each What is the Option Position in Each

Case? Case? K = Strike price, ST = Price of asset at maturity

Payoff Payoff

ST STK

K

Payoff Payoff

ST STK

K

16

TerminologyTerminology

Moneyness :

◦At-the-money option would have no cash flows◦ In-the-money option would have positive CFs to

the buyer◦Out-of-the-money option would result in cash

outflow if exercised Intrinsic value Time value

Based on the nature of exercise Based on how they are traded & settled Based on the underlying asset on which option is

created

17

Dividends & Stock Splits Dividends & Stock Splits

Suppose you own N options with a strike price of K :

◦No adjustments are made to the option terms for cash dividends

◦When there is an n-for-m stock split, the strike price is reduced to K*m/n the no. of shares in options is increased by N*(1+n/m)

◦Stock dividends are handled in a manner similar to stock splits

18

Dividends & Stock SplitsDividends & Stock Splits(continued)(continued)

Consider a call option to buy 100 shares for 20/share

How should terms be adjusted:◦for a 2-for-1 stock split?◦for a 25% stock dividend?

Margins (Page 190-19Margins (Page 190-1911))

Margins are required when options are soldWhen a naked option is written the margin is

the greater of:1 A total of 100% of the proceeds of the sale

plus 20% of the underlying share price less the amount (if any) by which the option is out of the money

2 A total of 100% of the proceeds of the sale plus 10% of the underlying share price

For other trading strategies there are special rules

19