Meaningful Retiree Healthcare Benefit Strategies for the ...

31

Meaningful Retiree Healthcare Benefit Strategies for the Public Sector National Conference on Public Employees Retirement Systems Annual Conference: May 15, 2018

Transcript of Meaningful Retiree Healthcare Benefit Strategies for the ...

Meaningful Retiree Healthcare Benefit Strategies for the Public Sector National Conference on Public Employees Retirement Systems Annual Conference: May 15, 2018

2 Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018

Challenges Facing the Public Sector

Budget Pressures

Disappearing Funding

Managing OPEB Liability

Public Perception

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 3

Retiree Health Care Landscape – After Health Care Reform

Health Care Reform RDS and Medicare program changes

Benefit design requirements and coverage mandates

Health insurance exchanges

Excise tax

Universal Sponsor Objectives Support overarching business and HR

strategies

Manage cost, risk, and ongoing program management burden

Simplify administration

Modified Group-Based

Sourcing Strategies

Individual Market-Based

Sourcing Strategies

Confluence of new challenges, new opportunities, and common plan sponsor objectives are dramatically reshaping the retiree health care market into two primary

benefit sourcing strategies

Two Fundamental Approaches

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 4

Individual Market-Based Sourcing—In General

Eliminate the traditional group insurance approach and support open-market purchasing

– Through individual market for Medicare eligible retiree members

– Through public exchanges for early retiree members

Create Health Reimbursement Arrangement (HRA) for retirees to use to offset cost of coverage on exchange market

Retirees use HRA to reimburse their costs for individual market products and/or associated expenses

– Generally, the plan sponsor sets the “HRA use” rules

HRAs generally need to be provided through a stand-alone, retiree-only legal plan structure to avoid the requirement to comply with the ACA group insurance market reforms (e.g., no annual limit on essential health benefits, no lifetime limit on benefits, etc.)

Partner with an administrative coordinator, or “exchange”, to facilitate guided access to the individual market, support retiree understanding, decision-making, and perform enrollment/administrative functions, at little to no cost to plan sponsor

4

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 5

Individual Market-Based Benefit Delivery: Why Now?

Individual Market

Retiree Health Strategy

Efficiency Benefit Parity

De-Risk Mature

Exchange Market

5

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 6

Exchanges: Public vs. Private/Active vs. Retiree

Facilitator

Target Population

Actives and (optional) Pre-Medicare-eligible

Retirees

Retirees Medicare-Eligible Pre-Medicare-Eligible

Health Care Options

Group-Based: Standardized designs

with the choice of carrier and funding varying based on facilitator

Comments

Platforms have been emerging since PPACA

was passed in 2010

Platforms have been emerging since the

Medicare Part D program began in

2006

State or Federal Government (11 states plus D.C. opted to run marketplaces for 2018)

All Pre-Medicare-eligible uninsureds and individuals

without affordable employer-sponsored coverage

Metallic designs (i.e., platinum, gold, silver,

bronze) with multiple carriers

Options for Medicare-eligibles are not included on

the public marketplaces

Platforms are emerging to source coverage on/off the public marketplaces

with a high touch customer service

experience

Private Exchanges

PPACA Public Exchanges (i.e., Marketplaces)

Benefit Consultants, Administrators, and Insurance

Carriers

Individual-Based: Medicare Advantage, Medigap, and Part D

Individual-Based: Metallic designs

with multiple carriers

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 7

Private Medicare Exchange Mechanics

Plan Sponsor HRA/Subsidy Strategy

If HRA is desired, Plan Sponsor converts current group-based health care subsidy into an HRA credit, which may be set at or below the actuarial equivalent of the current subsidy

Exchange Platform

Insured health care offerings Communications Decision Support Enrollment Advocacy HRA Administration

Insured Health Care Offerings

Retiree HRA

Medicare Advantage

Medigap

Individual Part D

Other (dental, vision)

Private exchange platform assumes many of the current plan sponsor group program responsibilities, but with a significantly “higher-touch” retiree

experience

Retiree Enrollments Commission Revenue

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 8

Pre-Medicare Private Exchange as a Portal—Mechanics

Plan Sponsor HRA/Subsidy Strategy

Plan Sponsor converts current group-based health care subsidy into an HRA credit, which may be set at or below the actuarial equivalent of the current subsidy

Private Exchange Platform Public Exchange and Other Health Care Offerings

HRA

Platinum

Gold

Silver

Bronze

Web Based Entities may be allowed by the states to enroll premium tax credit-eligible participants into qualified health plans.

Enrollments Commission Revenue

Insured health care offerings Education Online Decision Support Federal Subsidy Data Collection Application and Enrollment Advocacy HRA Administration

Enrollee Federal Subsidy Eligible?

Subsidy Eligibility Determination CHIP, Medicaid, Tax Credit Tax Credit Processing

Leveraging a Private Exchange Partner to Support a National, Consistent Public Exchange Strategy

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 9

Pre-Medicare Individual Market—Key Benefit Features

Area Comments

Individual Plan Designs

Guaranteed issue with no medical underwriting or exclusions based on health status Four comprehensive “metallic” benefit levels Provide Essential Health Benefits (EHB), with the definition varying by state Provider networks supporting the designs can be limited

Premiums Vary based on geography, carrier, benefit level, tier, age band, and tobacco use Cannot vary based on health status, claims activity, or employment status

Highest age-band premium for a particular plan cannot exceed 3X the lowest age-band premium Actual cost for Pre-Medicare retirees is 4X - 5X that for a twenty year-old Results in relatively lower premiums for retirees through implicit premium subsidies across

the enrolled population

Federal Subsidies (Only available on the Public Exchanges)

Provides explicit federal premium and cost-sharing subsidies for individuals with earnings up to 4X the federal poverty level Premium subsidy is based on the premium for the second-lowest priced Silver Plan Participants can enroll in any plan on the exchange and put the subsidy toward the cost of

that elected option Retirees should control, if possible, receipt of pension and savings plan distributions to

manage income -- to maximize the federal subsidies The payment of cost sharing subsidies has been ended. As a result, insurers have increased Silver premiums by 20% or more in 2018 to cover the loss.

Whether an individual can secure affordable coverage in the individual market depends on a number of factors including location, age, participating providers, and eligibility for federal subsidies

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 10

Pre-Medicare Individual Market—Market Risks

Political

Operational

Economic

Legal

Many plan sponsors are anxious to take advantage of the new public exchange opportunity but, given the newness and risks inherent in the current market, plan sponsors should proceed cautiously

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 11

Pre-Medicare Individual Market—Strategy Considerations

There is a different “employment-based health care” test for actives and Pre-Medicare retirees, with respect to their ability to secure a federal subsidy through a public exchange, and the rules for retirees are very liberal

Party Comments Plan Sponsor

For retirees, Shared Responsibility/Free Rider program and the associated penalties do not apply Minimum Essential Coverage (MEC) is NOT REQUIRED for retirees, nor is affordability

or minimum actuarial value (60%) required No penalties apply if a Pre-Medicare retiree enrolls in a state exchange and receives a

federal subsidy

Pre-Medicare Retirees

Pre-Medicare retirees are eligible for federal subsidies through state exchanges only if they DO NOT ENROLL in employer-sponsored coverage which is considered MEC, regardless of affordability or minimum actuarial value (60%) Enrolling in employer-sponsored MEC disqualifies the retiree from the opportunity to

secure a federal subsidy on a public exchange Offering retirees access to employer-sponsored coverage does not disqualify a retiree

from securing a federal subsidy in-and-of-itself

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 12

15.2 %

6.1 %

0.0 %

0.0 %

78.8 %

We do not anticipate changing our Pre-Medicare retireestrategy to leverage the state exchanges/individual

coverage opportunities

Employer subsidies through a defined contribution withPre-Medicare benefit sourcing through state

exchanges/individual market

Eliminating Pre-Medicare retiree coverage andsubsidies altogether

Other

Unsure at this time

In light of the ACA marketplaces and individual insurance market reforms, which of the following long-term strategies are you favoring with respect to Pre-Medicare retiree coverage?

Pre-Medicare Individual Market— Public Plan Sponsor Feedback

Source: 2017 Aon Hewitt Retiree Health Care Strategy Survey – Public Sector Cut (n=33)

Employers are generally unsure about their long term strategy for pre-Medicare retirees

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 13

12%

12%

76%

We are comfortable leveraging the ACAmarketplaces for Pre-Medicare retireecoverage for at least a portion of ourretiree group.

We are hopeful that the market willstabilize over time and we caneventually send retirees to themarketplace to secure coverage.

We are not confident that we will becomfortable sending our retirees to themarketplace to secure coverage in thefuture

Pre-Medicare Individual Market— Public Plan Sponsor Feedback In light of the recent market challenges, many public plan sponsors have an unfavorable

outlook on the 2017 marketplaces

– Health plan withdrawals, network restrictions, and premium increases have colored plan sponsor opinion and are driving at least short-term market pessimism

Source: 2017 Aon Hewitt Retiree Health Care Strategy Survey – Public Sector Cut

In Light of These Recent Market Challenges, What is Your Current Outlook Concerning Leveraging the ACA Marketplaces to Support Pre-Medicare Retiree Coverage?

(n=33)

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 14

Pre-Medicare Individual Market—Conservative Approach

Consider both Immediate and Longer-Term Strategies Plan sponsors who find the public exchange opportunity appealing will consider a three-step

approach:

Public Exchange newness, political/operational uncertainty, and potential ongoing volatility may dampen a broad Pre-Medicare retiree sourcing strategy in the near term

Step Details 1) Continue to Support the

Group Program Educate retirees on the state/federal marketplace, opportunity for federal subsidies, etc.,

through a simple communication campaign and (potentially) a call center or web-site Explain any coverage implications of leaving the group plan for Pre-Medicare state

exchange coverage

2) Choice Strategy

Continue the group program, but retirees have another choice - optional HRA to reimburse coverage on the public marketplace Provide customer service support to help retirees make smart choices

Support for no more than 1-2 years to mitigate impact of adverse selection on group program

3) Full Replacement Strategy (Assuming the Market has Stabilized; 2022+)

Coincident with scheduled 2022 Excise Tax implementation Source coverage through the public marketplace

Provide a tax-free optional HRA for all or a portion of the group Partner with a private exchange platform to provide “high touch” customer service

Develop a Medicare retiree health care strategy that dovetails with the new Pre-Medicare retiree benefit sourcing strategy

OHSERS uses a unique choice strategy to benefit their retirees

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

Marketplace Wraparound Plan

NCPERS Annual Conference

May 15, 2018

15

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

SERS Marketplace Wraparound Plan

®

Up to $2,000 reimbursement toward your deductible

Additional coverage for your out-of-pocket health care costs

Personal enrollment assistance from a HealthSCOPE counselor

SERS has partnered with HealthSCOPE Benefits to offer this coverage option for SERS’ health care participants. SEE INSIDE FOR DETAILS.

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

About SERS

17

• SERS was established on Sept. 1, 1937, thanks to the efforts of Cleveland custodians.

• SERS is one of five public pension

funds in the state of Ohio.

• SERS serves bus drivers, custodians, administrators, educational aides, food service providers, and school treasurers.

Richard H. Retired Custodian

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

18

Limited Wraparound Pilot Program * Vision, Dental, Long-term Care

Individual Marketplace Wrap - Retirees & Part-Time Employees - Plan Sponsor must also offer group plan

Excepted Benefits Under ACA 45 CFR 146.145

* Must begin no later than 2018, sunset after 3 years

Limited Wraparound Plan Requirements - Benefits Limited in Amount - Benefits Beyond Cost Sharing - Individual Marketplace or Multi-State Option

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

SERS Marketplace Wraparound Plan

How it works: • Members select a Health Insurance

Marketplace plan with assistance from a HealthSCOPE counselor

• SERS then “wraps” the Marketplace plan with added benefits at no additional cost

19

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

Covered Prescription Drugs

Physician office co-pay

Inpatient hospital stay

Imaging (X-rays, CT/PET scans, MRI)

Hearing Aid

50% of your plan’s prescription drug co-pay (up to $200 per prescription)

up to $50 per visit

up to $300 per admission

up to $100 per service

one hearing aid per year; up to $1,500

* The 2018 SERS Marketplace Wraparound Plan benefits noted above only apply to covered services under your Marketplace plan. Claims for non-

covered services are not eligible for reimbursement, except for hearing aids.

WRAPAROUND BENEFITS*

Maximum Reimbursement

Deductible up to $2,000

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

*Assumes 20 up to 35 years of service

How Does This Work?

Example using a Silver HMO Marketplace Plan for Sally, age 55, who earns $25,000 a year, and lives in Columbus.

SERS Non-Medicare Plan

2018 Cost Sharing

Marketplace Plan Silver

2018 Cost Sharing ($535 premium subsidy allowed)

SERS WRAPAROUND 2018 Benefits

+ (up to dollar amounts below)

= = =

= = = =

What Sally Pays

Premium $260 - $678* $168 $0 $168

Deductible $2,000 $3,900 $2,000 $1,900

Primary Doctor Specialist Doctor

$20 co-pay $40 co-pay

$10 co-pay $40 co-pay

$50 per visit $50 per visit

$0 $0

Generic Drugs Brand Name Drugs Specialty Drugs

$7.50 25% of cost (max $100) 25% of cost (max $100)

$10 $50 40%

50% of co-pay/cost sharing up to $200 per prescription

$5 $25 will

vary

Inpatient Hospital 20% coinsurance after $250 co-pay

$300 per day $300 per stay will vary

Imaging 20% coinsurance $150 per procedure $100 per procedure $50

Hearing Aid, one per year

not covered

not covered

$1,500 limit any amount

over $1,500

Out-of-Pocket Maximum (The most you could pay annually)

$7,350

$5,850

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

200 217 239 248 251

295

372 416

482 498 495 492 508 516 517

0

100

200

300

400

500

600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Wraparound Enrollment

22

Pension Reform

2017 2018

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

2018 Marketplace Plan Preference

75%

23

3% 22%

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

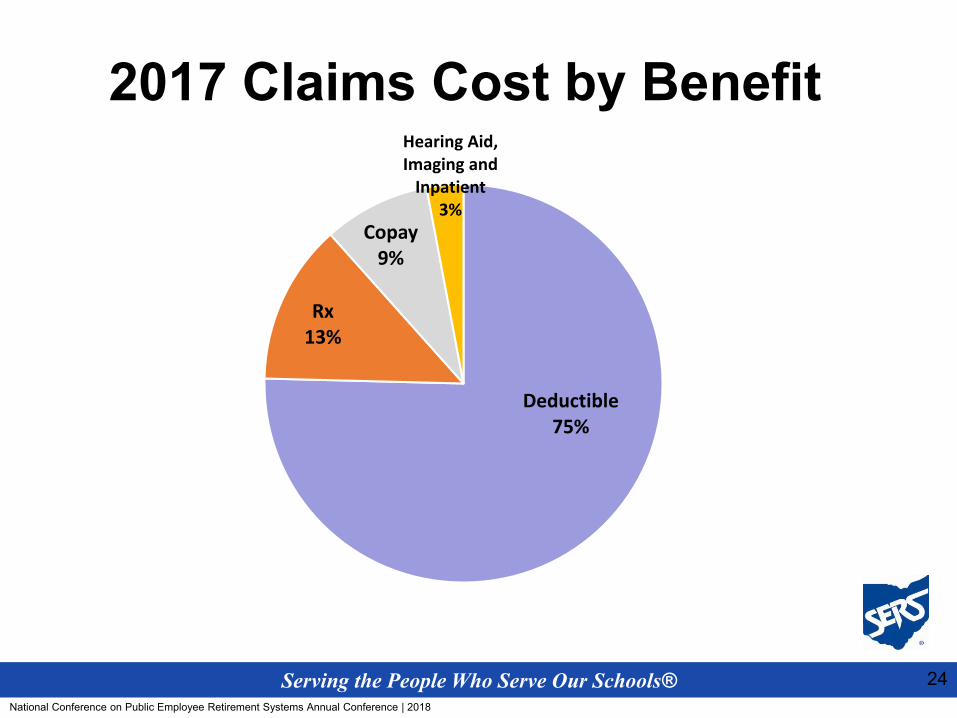

2017 Claims Cost by Benefit

24

Deductible 75%

Rx 13%

Copay 9%

Hearing Aid, Imaging and

Inpatient 3%

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

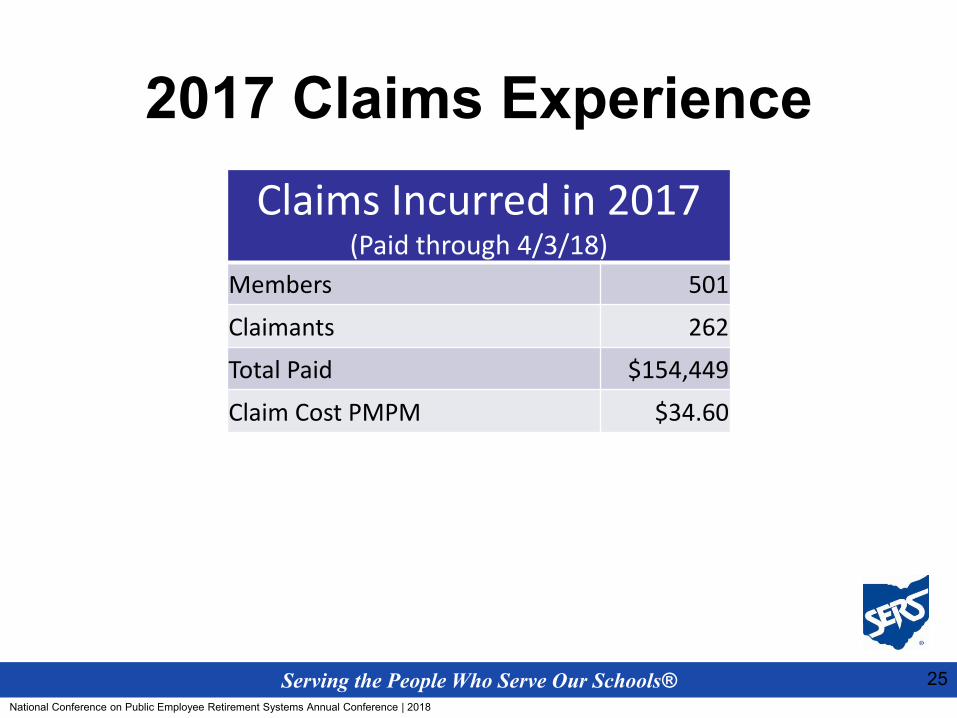

2017 Claims Experience Claims Incurred in 2017

(Paid through 4/3/18) Members 501

Claimants 262

Total Paid $154,449

Claim Cost PMPM $34.60

25

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

Marketplace Wraparound Cost vs. Non-Medicare Group Plan Cost

26

Per Member Per Month

SERS Non-Medicare Plan $750 (net of premium) PMPM

Marketplace Wraparound $59* PMPM *Claims and administrative costs, preliminary result through March, 2018

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

Cumulative Potential Savings for 492 Enrolled in Wraparound

27

$6,924,000

$10,980,000

2018 2019 Calendar Year

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

Wrap Advocacy

1. HHS/CMS issued two Requests for Comment –Should the pilot be made permanent or extended?

2. National groups, plan sponsors and others have commented in support.

3. Other options?

28

Serving the People Who Serve Our Schools® National Conference on Public Employee Retirement Systems Annual Conference | 2018

Thank You

For questions, please contact: Anne Jewel

Director of Health Care Services Ohio School Employees Retirement System

[email protected] 614-222-5810

29

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 30

Contact for Aon

Cathy Furr, FSA, MAAA Senior Vice President Aon Health & Benefits Consulting +1.410.200.1541 [email protected]

Aon | Health & Benefits National Conference on Public Employee Retirement Systems Annual Conference | 2018 31

About Aon

Aon plc (NYSE:AON) is a leading global professional services firm providing a broad range of risk, retirement and health solutions. Our 50,000 colleagues in 120 countries empower results for clients by using proprietary data and analytics to deliver insights that reduce volatility and improve performance.

For further information on our capabilities and to learn how we empower results for clients, please visit http://aon.mediaroom.com.

© Aon plc, 2018. All rights reserved.

![LAW RETIREE BENEFIT PLANS AND YARD-MAN - hbtlj.orghbtlj.org/articlearchive/v15i1/15HousBusTaxLJ120.pdf · ERISA Analysis Through the Lens of Contract Law ... 2015] RETIREE BENEFIT](https://static.fdocuments.us/doc/165x107/5b5bb7347f8b9a2d458e2c87/law-retiree-benefit-plans-and-yard-man-hbtlj-erisa-analysis-through-the-lens.jpg)