MDI Monetrix BlueChip Issue3 October-December 2012

45

-

Upload

ashish-gupta -

Category

Documents

-

view

110 -

download

2

description

Blue Chip is quarterly magazine of Monetrix, the Finance and Economics Club of MDI Gurgaon. This is the 3rd issue of the magazine (October-December 2012)

Transcript of MDI Monetrix BlueChip Issue3 October-December 2012

Dear reader,

Welcome to the third issue of Blue Chip!

The cover article this time is on the various aspects

that the RBI needs to work upon for the benefit of the

economy and the country. The country is going

through trying times such that even the Finance Min-

ister P Chidambram is conducting road shows abroad

to help the cause. One can only hope for a speedy

recovery for the Indian economy which seems to be

suffering from structural issues which may not be

readily alleviated by quick fixes such as rate changes

or import duties.

After covering the monetary aspect through the cover

article, we give a sneak peak into the fiscal side

through our interview with Mr. CS Mohapatra who is

Adviser, FSDC in the Department of Economic Af-

fairs of Finance Ministry. He talks about the meas-

ures taken by them for creating a better investment

environment in India for both foreign as well as do-

mestic investors. This interview would definitely be

very insightful for understanding the evolving regula-

tory system in India which would play a big role in

growth as well as the further development of India’s

economic landscape.

Keeping with the spirit of bringing exciting content

in every issue & our endeavour to always entice our

readers, we have taken a detour from the book review

to a fun movie review of Moneyball which released

in 2011.

The next issue would be special as it would be com-

ing to you in the fresh fiscal year brought to you by a

new editorial team. Wishing the graduating class of

MBAs across campuses ‘All the Best’ on their jour-

ney into the corporate world and beyond.

On this note, I would like to bid adieu to all the read-

ers of Blue Chip on behalf of the graduating team

and wish the incoming team all the best! A word of

advice in this placement season - take life as it

comes, don’t take yourself too seriously and remem-

ber that the answer to life, the universe & everything

is 42!

Signing off!

~Anupriya

Editor for Blue Chip

BLUE CHIP ISSUE 3

All images, artwork and design

are copyright of

Monetrix

Finance and

Economics club of

MDI, Gurgaon

The Team

Aneesha Chandra

Ashish Gupta

Rishabh Gupta

Rishi Maheshwari

Rohit Agarwal

Sankalp Raghuvanshi

Saurabh Saxena

Saurav Singh

Shaunak Laad

Stephen Thomas

Swapnil Sheth

Vipul Garg

Cover Page Chandrachuda Sharma

For any information or feedback,

please feel free to write in to us at

OR visit our Facebook page

www.facebook.com/

BlueChip.MDI

From the Editor’s Desk

Tutorial ( 12

Inflation

Current Account Deficit ( 22

India’s Achilles’ Heel

Business Quiz ( 39

Crossword

PPPs ( 36

Public Private Partnerships or

Paralysis ???

Market Update ( 42

Stock Market Update

In the News

Beginners’ Corner ( 19

Financial Risk Management

Facebook IPO ( 4

Through the eyes of

finance students

Dr. C.S. Mohapatra

In conversation with ( 27

Ministry Speak Ministry Speak Ministry Speak Ministry Speak

Cover Article ( 14

Reserve Bank of India

A bank in a need of 4 wheel drive

Movie Review ( 41

Moneyball 2G Auction ( 9

Auction Failure and Auction Pricing

CONTENTS

4

“If you've been playing poker for half an hour

and you still don't know who the patsy is, you're

the patsy.” - Warren Buffet

Retail investors (common investors like you and

us) lost $630 million from the plunge of Face-

book shares. Think that’s big, these numbers are

as of May 24th, 2012 when the stock was trading

at $33.03 which was down 13% since the IPO.

Fast forward to November 2nd, 2012, the stock

closed at $21.18 down 44 % since the IPO. Not

just retail investors with very low understanding

and knowledge about the stock markets but also

big institutional investors including big bank

have burnt their hands in the FB IPO. UBS was

hit with a loss of $356 million.

To understand how so many people, institutions

made fool out of themselves, we need to under-

stand the DNA of the game. We need to put

different spectacles to view the whole situation.

So here’s how the whole game unwounded.

Game

The game we are talking about here is “finding

the bigger fool”.

Players

Let’s introduce you all to the players of the game.

• The company – Facebook

• Insiders – Accel Partners, Goldman Sachs and

employees of Facebook

• The underwriters – Morgan Stanley, JPMC,

Goldman Sachs and the other 30 investment

banking firms

• NASDAQ – The index on which Facebook

got listed

• Homer Simpson – A common investor living

in Springfield

• Bart Simpson – Homer Simpson’s son and an

MBA in Finance from Ivey League college

• Ned Flanders – Homer Simpson’s next door

neighbour

• Ms. Albright - Sunday school teacher and who

believes that stock market is not for her

IPO Market

Before analyzing the game, we need to analyze the

IPO market as a whole. This market is very differ-

ent to the other market which is available for in-

vesting – secondary market. How is IPO market

different from secondary market? To answer this,

we need to need to look at the characteristics of

both the markets.

© Monetrix, Finance & Economics Club of MDI, Gurgaon

|FACEBOOK IPO|

FACEBOOK IPO: Through the eyes of Business

Finance students

PGPM 2011-13

Management Development Institute, Gurgaon

Prateek Dhingra Nikhil Sant

5

The above mentioned characteristics make IPO

market highly favourable for the seller and unfa-

vourable for the buyer. The table 2 reinstates the

point – IPOs make money for sellers and not buy-

ers.

Influence

The game we are analyzing here is not fair. It is

loaded at every stage and every player is playing

with the loaded dice. The force which influences

this game is “Incentive”. So let see what incen-

tive is with the respective players.

Facebook – It wants to raise capital at the lowest

possible cost. This would mean issuing shares at a

high price.

Morgan Stanley, JPMC, GS and other underwrit-

ers – they want the deal to be done. If they don’t

do the valuation which would be in accordance

with the expectations of the company, they would

lose the “big fee”. The lead underwriter gets to

have the largest chunk of the underwriting fee.

Rest of the underwriters small bites of the apple

pie. Hence, the race to become the lead under-

writer is very fierce and investment banking firms

cannot afford to lose such an opportunity.

|FACEBOOK IPO|

IPO Market Secondary Market

Many buyers and

handful of sellers

Many buyers and

many sellers

Information asym-

metry as sellers

being insiders

know more about

the company than

the buyers

Information asymme-

try is not much as not

many insiders are sell-

ers

Sellers can decide

when to sell the

shares

Price can be influ-

enced by even one

seller

Quantity can be

changed to get the

price the seller

wants

Scarcity of shares

cannot be created

easily

Country # of IPOs Issuing Years Total abnormal

return

Australia 266 1976-89 -46.5%

Austria 57 1965-93 -27.3%

Brazil 62 1980-90 -47.0%

Canada 216 1972-73 -17.9%

Chile 28 1982-90 -23.7%

Finland 79 1984-89 -21.1%

Germany 145 1970-90 -12.1%

Japan 172 1971-90 -27.0%

Korea 99 1985-88 +2.0%

Singapore 45 1976-84 -9.2%

Sweden 162 1980-90 +1.2%

UK 712 1980-88 -8.1%

US 4753 1970-90 -20.0%

Table 1: Trend in IPOs

Table 2: Primary & Secondary Market

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

6

NASDAQ – Facebook IPO was one of the biggest

technology related IPO and biggest internet related

IPO. Both NYSE and NASDAQ wanted it to get

listed on them. NASDAQ securing the listing of

Facebook was a big feat as it was the smaller of the

two US indices and the listing would benefit it by

making it more attractive to the future IPOs.

Homer Simpson, Bart Homer and Ned Flanders –

they want to make money from the trade as they

think that Facebook is the stock to hold in the long

run which would enable them to spend rest of their

lives in peace. To them, Facebook is the next Ap-

ple or Google and they don’t want to be out of the

biggest stock market carnival in a decade. It’s what

all of them and hundreds of other Springfield citi-

zen and millions of US citizens have been dream-

ing about ever since they started investing – to get

a hand on such a catch.

How the game evolved?

Facebook was launched in 2004 in the dorm room

of Mark Zuckerberg its founder. After 8 years, the

firm decided to get listed and use the new equity

for further expansion. The firm had been infused

with equity thrice before the IPO.

• May, 2005: $12.7 million in funding led by ven-

ture capital firm Accel Partners

• October, 2007: Microsoft invested $240 million

• January, 2011: Goldman Sachs invested $1.5

billion giving Facebook a valuation of $50 bn.

On its 8th birth day, the company launched its

much anticipated IPO and approached the various

investment banks for valuation as well as under-

writing the issue. All the major firms

compete with each other to get the coveted role of

lead underwriter. So, they brought in the best of

their guys and after spending numerous nights in

the offices, they came up with the valuation of the

company at a humungous value of $104.2 billion.

Morgan Stanley was selected as the lead under-

writer with JPMC and GS as the other two major

underwriters and 30 other banks as a syndicate of

underwriters. The single most important reason for

Morgan Stanley getting the lead underwriter posi-

tion was years of work put in by its Managing Di-

rector and Co-Head of Global Technology Invest-

ment Banking, Michael Grimes. His relationship

and connections he made in the past decade espe-

cially after the dotcom bubble in 2000-2001 paid

off when he underwrote nearly every big IPO in

internet based companies, including LinkedIn,

Zynga, Groupon and Yandex. The reward for un-

derwriting FB IPO - $176 million which was about

1.1% of $16 billion Facebook raised in its IPO.

Trading of FB shares was supposed to start at

11:00 AM EDT on 18th May, 2012 but due to tech-

nical delay at NASDAQ, it began at 11:30 AM with

an opening price of $38/share. Around 82 million

shares traded in the first 30 seconds and seven

minutes after the opening, nearly 110 million

shares had traded. Total volume for FB shares on

the 1st day was 573,622,571 which was a new re-

cord beating General Motor’s record of 458 million

shares. The intraday for the share was $45 and the

stock closed at $38.23.

Since the listing, Facebook’s share has been down

on 64 trading days, up on 49 and unchanged on 3

days.

|FACEBOOK IPO|

© Monetrix, Finance & Economics Club of MDI, Gurgaon

7

How the Players Played the Game

In the days leading to the IPO, everyone wants

to be a part of it. All they see is the chance of

this becoming the next Google and possibility of

earning 700% percent returns! Now consider the

fact that the internet using population is around

2.4 billion out of which 1 billion is part of Face-

book. So even if Facebook manages to convert

the rest of the 1.4 billion people into users of

Facebook, that still results in a growth of 2.4

times. To grow anymore than that, Facebook

will have to turn to other species on earth like

cats and dogs. Certainly an over optimism bias!

So how do our players react to this IPO

process?

Bart, with all his finance knowledge and MBA

cockiness, is convinced that this is a great deal.

He forgets the basic Graham and Dodd princi-

ple of margin of safety. When the underwriters

raise the price from a range of $28-35 to $38, the

price becomes way out of range of any conserva-

tive estimate of intrinsic value. Can Facebook

sustain such high growth projections? If yes, for

how long? Will there be no competition? These

are the questions Bart needs to ask. But his sys-

tem 1 of the brain is firmly in control. System 1

of the brain, according to Kahneman, is the

automated decision making part of the brain as

opposed to the deliberating part of the brain

which is system 2. System 1 creates a coherent

view of the positives and aids in making a quick

decision. Scepticism often gets sidetracked when

system 1 is in control. As a result Bart goes

ahead and buys the overpriced Facebook shares,

and is very happy with it too. In spite of the

MBA in finance degree, Bart ultimately ends up

speculating.

In the meanwhile, the underwriters realise that

the public investors are all bullish on Facebook

and everyone wants to be a part of Facebook.

They realise that the 337 million shares that are

to be traded will not be sufficient to satisfy all

the bids. Thus, a scarcity has been created. Now,

since everyone is so eager to be a part of Face-

book, they are all scared to miss out on the

shares due to this scarcity. As a result they start

overbidding just to make sure they don’t miss

out. Right on cue, the underwriters take advan-

tage of this scarcity effect and raise the price of

the shares to $38. And the fear of missing out,

caused due to this scarcity effect, makes the in-

vestors go out and buy these overpriced shares.

Ned Flanders is an avid Facebook user. He has

all his friends and family on Facebook and so is

very fond of it. Facebook, to him is a way to

connect to his family and friends and hence has

a very special place in his mind. It’s a part of his

daily routine and he cannot imagine his life with-

out Facebook. He has all these positive feelings

associated with Facebook. As a result he does

not think of it as a business entity at all. Now

with the Facebook IPO on the horizon, due to

the emotional connect Ned feels that he has to

be a part of this. Owning a stock of something

that he is so familiar with and associated on a

daily basis is a natural thing to do according to

him. The day to day connect with Facebook

makes him feel that he knows all there is to

know about Facebook. In his eyes, since Face-

book is associated with positive feelings, it can

|FACEBOOK IPO|

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

8

do no wrong as a business. He does not mind pay-

ing a high price for the stock. In fact he doesn’t

even realise he is paying a much higher than neces-

sary price for the stock. The familiarity effect and

the emotional connect compel him to buy the

overpriced shares and he returns home happy and

content.

Homer is a happy go lucky person and a common

investor who dabbles a bit in stocks. He certainly

has no interest in Facebook and is not an active

user. When he reads about the IPO his interest is

not piqued and he ignores it. He carries on with his

day to day life and is happy with it.

One day Bart comes up to him and says, “Dad,

have u subscribed for the Facebook shares?” He

says that he is not interested and will not subscribe

to the shares. Bart reacts by saying that only a fool

would miss out on not buying these shares. He

goes on to say that he has done his analysis of the

stock using all his knowledge gained in his MBA

program and that it is just too good an opportunity

to miss out on. He then gives the example of

Google, which was listed at $85 in the IPO and

then went to be more than $650. “Oh, that’s a fan-

tastic return on investment!” says Homer. And

thus, an anchor has been laid in Homer’s mind.

While he is still pondering on what Bart said,

Homer comes across Ned, who is looking particu-

larly happy. He tells Homer that he has just gone

out and subscribed for a big amount of Facebook

shares. He advises Homer to do the same and tells

him that he will be missing a fantastic chance to

make money by not being part of the Facebook

IPO.

Now homer starts worrying about not being a part

of the IPO. “Everyone I know are going out and

subscribing for Facebook shares”, he thinks. He

feels that if he misses out on the deal and everyone

else makes a lot of money then he will look like a

big fool. “If everyone says it’s a big deal then it

must be a good investment!” he muses. Thus, the

herd mentality comes into play and Homer now

seriously ponders subscribing for the shares. This

combined with anchoring effect of the Google

IPO convinces him and to subscribe to shares of

Facebook.

The next day Homer meets Ms. Albright. He asks

her if she has subscribed to the shares of Face-

book. To which she says, “I am not too familiar

with the Facebook scenario. I am not aware of the

stock valuation and whether it’s under or overval-

ued. I am also not aware of the IPO process and

hence I am not sure if it is beneficial to the general

investors or the issuing company or the underwrit-

ers. In such a scenario I do not want to get into

something which I am unaware of and might get

my hands burnt in.” Homer mocked her for this

and said that she will regret her decision. But fast

forward to 6 months and Ms. Albright was the

only rational person amongst them all and is the

only person with a reason to smile.

The moral of the story being that one must always

conduct research with due diligence before invest-

ing and not get swayed by the biases. Finally it is

the base rates that matter the most. It is better to

miss out on one Google than get your hands burnt

in a 100 Facebooks.

|FACEBOOK IPO|

© Monetrix, Finance & Economics Club of MDI, Gurgaon

9

“2G auctions flop as 57% of spectrum remains

unsold, government gets less than a quarter of its

revenue target” is the headline of a popular

national newspaper. No need to burn midnight

oil to find out the reasons for the set back as it is

obvious from the high reserve price for 2G

spectrum set by EGoM. The government had set

the reserve price at whopping amount of

Rs14,000 crores for 5 MHz of pan-India 2G

spectrum. Even the government has itself

indicated recently that the culprit for the auction's

failure was the unrealistically high reserve price by

deciding to cut the reserve price for 2G

spectrum auctions by 30%. Even this move

appears inadequate to address the issue and not

anticipated to give the desired results.

So, what ails the 2G spectrum auction issue and

why telecom companies gave lukewarm response?

High reserve price for spectrum made it

unattractive for the companies to make a

profitable business case. With massive price war

going on between different operators and low

profit margins, such a high reserve price for

spectrum was simply economically unfeasible.

Compounded to this, the policy uncertainty in

India makes the scenario further worse,

consequently no operator is willing to take such a

huge risk. Therefore, telcos cleverly decided not

to bid for the expensive circles resulting in less

money generation for the government. It is amply

clear from Telenor bidding pattern as it did not

bid for the expensive Mumbai circle, apart from

Kolkata and West Bengal, even though it currently

has sizeable subscribers in these circles. If it had

done so, it would have had to pay a staggering

51.96 percent of the total base price to get into

circles which have 50.06 percent of the overall

telecom revenue. That would have been ill-

advised. As a result of this high price, Delhi,

Mumbai and Karnataka circles, which account

for 48 percent of the base price did not receive

any bids.

To put things in right perspective, the latest data

released by Ernst & Young on recent spectrum

auctions in six other nations (Table 1) is an eye

opener. Calculations show that the "per unit per

inhabitant price" of Indian spectrum in the 800

|2G AUCTION|

2G Auction Failure and Auction Pricing

PGDM (2012-14)

Goa Institute of Management Aditya Khajuria

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

“High reserve price for spectrum made it unattractive for the companies to make a profitable business case.

With massive price war going on between different operators and low profit margins, such a high reserve price for

spectrum was simply economically unfeasible. Compounded to this, the policy uncertainty in India makes the

scenario further worse, consequently no operator is willing to take such a huge risk. Therefore, telcos cleverly

decided not to bid for the expensive circles resulting in less money generation for the government.”

10

MHz band (post-ARPU adjustments for each

market) is nearly 5.3 times higher than

Germany's $0.95, 15 times higher than Sweden's

$0.54 and 13 times higher than France's $0.90.

Similarly, the 900 MHz bandwidth which is

considered the most efficient for 2G services is

27 times cheaper in Spain at $0.46 per unit per

inhabitant, compared with $12.49 in India.

Therefore, exorbitant spectrum reserve price in

India has clearly proved disastrous for 2G

successful auction.

From economics point of view, setting high

Reserve price for spectrum is also detrimental for

the economy of a nation. Such a high price is a

stumbling block for the entry of new operators

or small existing players, as they do not have the

large funds available with them for participation

in the high price auction. These small or new

companies might be having better business

model and technology, which can benefit

ultimately the customer. But the very high

reserve price deprived even the healthy

competition among bidders Thus, big players

had their own day as they had the required

money power to buy spectrum and ruled the

market in spite of the fact some of them may not

have the best business model. This result in

economic inefficiency in the market and the

popular economic concepts, like dead weight loss

to the consumer, becomes relevant.

By allowing companies with high marginal cost

to operate unopposed in the market, without the

challenge of facing new players, probability of

completely mopping of consumer surplus

increases. Thus, economic growth of the country

suffers as deserving and efficient players are not

allowed to operate freely. For example, if

Norway's Telenor had managed to get spectrum

for pan-India operations, then it might have

resulted in technology transfer to India leading to

better business model and improved services to

the customer. Worse apprehensions have come

true as three smaller operators - Etisalat, Videocon

and Swan Telecom - have already exited the

industry due to the prevailing scenario.

Let’s look the fate of the common man in middle

of all this chaos for whose benefit all this is

supposed to be done. Probable tariff rise is likely

to be more than even what has been projected by

TRAI. Increased spectrum fees will be passed on

to the consumer ultimately, thus increasing the

load on common man already staggering under

high inflation. Moreover, in this era of

communications it will be lethal to deprive poor

man for want of affordability and therefore it is

essential to have appropriate spectrum pricing in

order to maximize the socio-economic benefits of

wireless services. The situation is going to

adversely impact rural penetration as well, the

rural rollouts will become increasingly unviable

and unsustainable. It limits the capacity of telecom

operators to invest in networks, leading them to

prioritize urban areas and results in digital divide

|2G AUCTION|

© Monetrix, Finance & Economics Club of MDI, Gurgaon

Source: Ernst & Young

Table 1

11

|2G AUCTION|

between rural and urban areas.

To understand the adverse effect of high

spectrum pricing on the customer, take the case

of J&K circle where the author has worked in

Tata Teleservices Ltd and therefore can

understand the loss of the customers in this

militancy hit state. As per the recent TRAI report

for J&K circle, Bharti Airtel is the largest

operator as per the subscriber base, with

approximately 22 lakh customers. It is followed

by Aircel with nearly 18 lakh customers. Other

major players present are Reliance, Vodafone and

Idea. Tata Teleservices Ltd had close to 1.1 lakh

customers in this strategically important state

with Photon as its most popular product. Having

lost its licenses for J&K circle due to the famous

2nd February Supreme Court order cancelling 122

telecom licenses and spectrum allocations, only

option available for it was to bid for the spectrum

again. But the company decided not to pursue

the acquiring of spectrum in the auction as it did

not support the business case due to the high

current reserve prices of the spectrum. Earlier,

Uninor and Sistema had to exit the circle also.

All the above happenings has reduced the

competition in the J&K circle and low tariffs

which were anticipated due to the presence of

more number of operators now is a distant

dream. Additionally, the customers have been

deprived of some high tech services which are

expertise of these exiting companies. Just to

quote an example, wireless broadband service

offered by Tata Photon is considered best in the

industry and same will not be available in the

state from January 2013 when Tata Teleservices

ends its services in the state.

Looking ahead, 2G spectrum fiasco has added to

the negative economic sentiment prevailing in the

country. The 2012 outlook for most Indian

telecommunications companies is negative since

state owned and six private telcos will witness

operating losses according to Fitch Ratings in a

special report. Even county’s largest telecom

operator, Bharti Airtel, faces the risk due to the

new spectrum pricing, as they may be asked to

pay a one-time charge for excess spectrum

holding and any additional cash outflow would

have a negative effect on its rating. All telecom

operators remain exposed to significant

regulatory risks and National Telecom Policy

(NTP) and Spectrum Act 2012 needs to throw

light on the regulatory clarity in regard to the

issues of spectrum pricing. Unless, that happens

FDI flow in the sector will be adversely affected

as foreign players may not participate in fresh or

future auctions.

Thus, due to less Foreign Direct Investment

(FDI), Indian economy as a whole will be a loser

as it affects GDP growth in long as well as short

run directly. FDI in the Indian telecom sector

was $1.7 billion in FY 2011, which was down by

almost 35% as compared to the $6 billion in FY

2010. According to reports from COAI,

investments in the sector by leading operators are

down 50%. Moreover, banks and FIIs, including

domestic ones, have been shying away from

lending to telecom players owing to the policy

uncertainties. Already, the overall exposure of

Indian banks to the telecom sector (2G, 3G and

others) was $18 billion (910 billion) till

November 2011, making more funding almost

impossible in future. Current situation is already

ringing alarm bells for Indian telecom industry

and economic health of the country.

Therefore, accurate pricing policies and

regulations are the need of the hour and

government should take decisions in the right

direction urgently to salvage the situation. This is

crucial for the revitalization of the telecom sector

and the entire nation's economy. It should be

understood unambiguously that healthy auction is

the key to the price discovery. Moreover, pooling

of spectrum and letting operators dip in for a

slice as and when they need it is also a viable

option, as federal communications commission

of USA recognized recently. This will help to

promote new investment and competition.

Finally, government should remember golden

rule “There can be economy only where there is

efficiency” and let fair pricing policy prevail.

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

12

|TUTORIAL|

Understanding Inflation

“India Inflation Turns to Corner, Rupee to Benefit”;

“Inflation at Three-Year Low, Hopes of RBI Rate

Cut Rises”; “Inflation Still an Issue, So Is CAD: D.

Subbarao”.

These headings of some newspaper articles published

recently have some interesting underlying assump-

tions. It indicates that inflation is such an important

indicator that it can change the entire situation in the

foreign exchange market. Current account deficit,

which has the potential to bring about balance of

payments crisis if not kept in check, is ranked at the

same level with inflation. Also, the monetary policy

decisions are majorly influenced by inflation. Even

though Indian growth rate had been decreasing, RBI

decided to cut inflation after a long wait of nine-

months, and that also when inflation was at a low

level, clearly indicating that inflation gets priority

over economic growth. Further, many centrals banks

across the world like have adopted inflation targeting

i.e. the main aim of the monetary policy is to achieve

a targeted inflation rate.

But what exactly is inflation? What are the types of

inflation? It is one of the terms which everyone

knows but few understand. Inflation refers to a sus-

tained rise in the general price level i.e. prices of

goods and services over a period of time. Inflation

can be of various types depending upon which pa-

rameter is being compared.

On the Basis of the Cause:

This is the most commonly used classification of

inflation. According to it, inflation can be of four

types – demand-pull, cost-push, sectoral, and pricing

power inflation.

The basic economic principle is that whenever de-

mand exceeds the supply, the price of the good

would rise. This is the basic premise of demand-pull

inflation. When the demand for goods and services

exceeds the supply of the same, the resulting infla-

tion in the economy is known as demand-pull infla-

tion. This is the type of inflation which is generally

seen during war-times as the demand for war sup-

plies increases tremendously.

Production of any good/service requires the use of

the factors of production – land, labour, capital and

entrepreneur. When the price of these factors of pro-

duction rises, it leads to an increase in the overall cost

of production. Thus, to maintain profits, the prices of

the goods and services increase and this inflation is

known as cost-push inflation. One example of cost-

push inflation is the increase in prices because of

wage hikes.

Sectoral inflation is the situation in which rise in

prices of goods and services of any one or a few sec-

tors can lead to rise in price levels of all goods and

services in the economy. This generally happens

when some basic or raw material sector experiences

rise in prices.

Pricing power inflation a.k.a. administered inflation

and oligopolistic inflation is a type of inflation which

is generally seen during boom periods and never in

downturns. The firms and businesses sometimes in-

crease the price of their goods and services so as to

increase their profit margins. This rise in prices is

referred to as pricing power inflation.

On the Basis of Coverage:

Inflation can either be comprehensive or sporadic.

As the name suggests, comprehensive inflation refers

to a situation in which prices of most commodities

are rising in the entire economy. On the other hand,

sporadic inflation refers to a situation in which prices

of only a few goods and/or services is rising in some

parts of the economy.

On the Basis of Rate of Increase in Prices:

In this classification, inflation is characterized accord-

ing to the range in which the inflation rate lies.

Creeping Inflation refers to a situation in which the

prices are rising but at a low rate. Hence it also re-

ferred to as Low/Mild/Moderate Inflation. If the

rate is low and in single-digit (generally less than 3%),

it is called creeping inflation. Chronic/Secular Infla-

tion refers a situation in which an economy experi-

ences creeping inflation for a long period of time.

Walking Inflation is the next type of inflation in

which the prices of goods and services increases at a

rate higher than in the case of creeping inflation. The

© Monetrix, Finance & Economics Club of MDI, Gurgaon

13

|TUTORIAL|

range for walking inflation is generally accepted to be

between 3 to 10%. Creeping inflation and walking

inflation is together referred to as Moderate Inflation.

Thus, if the prices of goods and services rise at the

rate of less than 10%, it is called moderate inflation.

An economy experiences running inflation when the

inflation rate lies between 10 to 20%. Galloping/

Jumping Inflation refers to a situation in which the

economy is experiencing inflation in double or triple

digits. The range for the same is 20 to 1000%. The

maximum rate of increase in prices is referred to as

hyperinflation. Economies like Germany and Argen-

tina have experienced this in the past. The rate of

increase is higher than 1000%. Some economies saw

prices rising daily. The value of the currency was de-

stroyed which led to loss of confidence in the cur-

rency. People preferred to stock goods whose prices

were rising at an extremely high rate instead of hold-

ing the currency whose value was deteriorating con-

tinuously. The highest value of banknotes issued by

the different Central Banks were 100 trillion Mark in

Germany, 100 quintillion Pengo in Hungary, etc.

Impact of Inflation

The impact of inflation is the maximum on the

weaker sections of the society. Hence, inflation is said

to increase inequality in the economy. Further, as

inflation reduces the value of the currency, it acts as a

disincentive for saving. As people know that the pur-

chasing power of the currency would be lower in the

future, they would prefer to utilize the currency for

consumption instead of saving it for the future. As

the national savings of the economy would decline

because of inflation, it will reduce the funds available

for lending and hence can have a negative impact on

the capital formation in the economy. This further

will affect the growth and production potential of the

economy. Inflation also has a major impact on for-

eign exchange market. Rising prices make the domes-

tic goods more expensive and foreign goods relatively

cheaper. This leads to an increase in imports and a

fall in exports, which further leads to currency depre-

ciation.

Further, as an economy experiences sustained infla-

tion, it can lead to expectations of future inflation.

When inflation is anticipated, workers would demand

higher wages. This would increase the cost of pro-

duction for the firms and they would increase the

prices of their goods and services to maintain their

profits. However, this increase in prices would lead to

fulfilment of the expectations of the people and they

would expect the prices to rise in the future as well

hence demanding even higher wages and the process

would continue. This would lead to a vicious cycle

which is popularly known as wage-price spiral. Infla-

tion also reduces the lending-borrowing activity in

the economy. Generally, most loans involve a fixed

payment for a pre-decided specified number of years.

However, with inflation, the real value of the returns

to the lender increases. Hence, effectively, the debt-

ors pay a lower rate of return. This increases the de-

mand for loanable funds but reduces the supply of

the same leading to lower lending and borrowing. It

also leads to an increase in the interest rates in the

economy due to demand exceeding the supply which

further deters investment activity.

Inflation also leads to an increase in the shoe-leather

cost. When an economy is experiencing higher infla-

tion, it creates incentive for the people to keep their

money in banks so as to earn some interest. Thus,

whenever cash is required, people will have to make

more and more trips to the bank and the cost in-

volved in doing so is known as shoe-leather cost.

Another cost associated with inflation is the menu

cost. Changing prices is not a cost-less activity. It

involves printing new menus, making new packaging

which shows the higher price and so on. This cost is

called menu cost.

Inflation has some positive effects as well. As the

price of goods and services increase in the economy,

the producers have an incentive to increase their pro-

duction. This would lead to an increase in output,

employment and production leading to greater

growth in the economy. Another positive effect is

the Mundell-Tobin effect according to which due to

inflation people would prefer to decrease their cash

holdings and instead keep some amount in banks or

lend it out leading an increase in investment activity.

Further, deflation is not good for an economy too as

has been seen in Japan which went through a decade

long recession. Deflation leads to people postponing

their consumption to the future so as to get a better

deal i.e. lower price. This led Paul Krugman to con-

clude that some inflation might actually create an

incentive for the Japanese people to increase their

consumption which would provide the necessary

thrust for the economy to recover and growth to

pick up.

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

14

manages foreign exchange with an aim to fa-

cilitate external trade and payment and pro-

mote orderly development and maintenance of

foreign exchange market in India

►Issuer of currency: It issues and exchanges

or destroys currency and coins not fit for circu-

lation to give the public adequate quantity of

supplies of currency notes and coins and in

good quality

►Banker to the government: RBI performs

merchant banking function for the central and

the state governments

►Banker to banks: It maintains banking ac-

counts of all scheduled banks.

The reasons why Alice Rivlin was right

There are various external factors which make

RBI worry. The world economy is going

through an unconventional period and proba-

bly that is why conventional monetary tools

such as interest rate changes aren’t working

well. On one hand, RBI hiked interest rates 13

times in between Mar 2010 and Oct 2011 but

failed to arrest inflation and on the other hand

US Fed cut interest drastically to revive the

faltering economy but faced the same result.

Probably, unconventional times require uncon-

ventional measures.

RBI, unlike other Central Banks, faces a huge

task when it is about taking appropriate deci-

sions based on various macroeconomic data.

Government regularly revises economic data,

sometimes sharply, which makes RBI’s life dif-

INTRODUCTION

Alice Rivlin wasn’t wrong when she said that

the job of a central bank is to worry. No one

can appreciate her statement more than the

Governor of Reserve Bank of India. Faltering

growth, rising inflation, huge unbanked popu-

lation and extravagant government pose a

daunting task ahead of RBI policy makers.

The main function of RBI includes:

►Monetary Authority: RBI formulates, im-

plements and monitors the monetary policy

to maintain price stability and to ensure

proper availability of credit to productive sec-

tors

►Regulator and supervisor of the finan-

cial system: It prescribes broad parameters

of banking operations within which the coun-

try's banking and financial system functions

to maintain public confidence in the system,

protect depositors' interest and provide cost-

effective banking services to the public

►Manager of Foreign Exchange: RBI

RBI – A Bank in need of a 4 Wheel Drive

Cover Article

Monet r ix

© Monetrix, Finance & Economics Club of MDI, Gurgaon

15

rupee and forcing exporters to convert half of

their foreign earnings into rupee within two

weeks.

Some economists hold the view that RBI can’t

be fully transparent as it is not only monetary

policymaker but also government’s debt man-

ager.

With all the above mentioned external

and internal issues along with a few others and

a task to manage inflation, growth, rupee and

government of India’s borrowing programme,

RBI is facing a huge dilemma.

Growth

Both monetary and fiscal policy determines the

growth of the economy. Although RBI’s main

role is monetary, it still plays a huge role in

growth. Half of India’s workforce is employed

in agricultural sector and it constitutes 16% of

India’s GDP. A concern in 1968 regarding

growth in agriculture and small scale industries

led to RBI defining it as a Priority Sector. In

1972 it made it mandatory for state banks to

have a percentage (as high as 40% in 1985) of

its lending to priority sector to ensure growth.

Apart from that it plays a major role in driving

Investments in the economy. Depending on

the situation, RBI reduces interest rate for pro-

moting lending to banks and also to govern-

ment by lowering bond rates.

Currently the government is facing a deep fis-

cal deficit problem and it has chalked out the

following plan to bring it down to 3% by 2017.

India’s GDP growth has slowed down from

ficult. One of such events was Jan 2012 IIP

figure which reported a growth of 6.8% based

on a huge surge in sugar output and was

eventually revised to 1.1%. RBI governor D.

Subbarao called it “analytically bewildering”.

One of the most important internal factors

which is causing significant worries for RBI is

communication, an effective policy tool of

central banks. Few years back a U.S. based

economic think tank rated RBI as one of the

least transparent South Asian central bank

which was in sync with IMF findings. D. Sub-

barao took a few positive steps to break the

established image of RBI by introducing

greater transparency through more frequent

communications. He started mid-quarter pol-

icy meetings and began to release minutes of

its advisory meetings on interest rates. But

recently, RBI has failed to control over com-

munication and contradictory communication

making its own job more difficult. One in-

stance where RBI erred while communicating

was in June 2011 when RBI Deputy Gover-

nor, Subir Gokarn, suggested room for a rate

cut which ultimately didn’t come in June

monetary policy meeting. Another was when

RBI kept on saying that RBI doesn’t intend to

support rupee at a particular level and would

intervene only to arrest excessive volatility in

forex market. However, later on RBI took

extreme steps to support the currency by re-

ducing speculators’ ability to take a call on

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

|COVER ARTICLE|

Year Fiscal Deficit as % of GDP

2012 5.8

2013 5.3

2014 4.8

2017 3.0

Table 1: Plan for Fiscal Deficit

16

taken to curb it. Minister of Commerce and

Industry Anand Sharma said that around 40%

of fruits and vegetables do not reach the mar-

ket due to transportation delays and are

wasted. India faces structural problem due to

lack of adequate infrastructure which causes

supply side bottlenecks. However, govern-

ment is banking on the direct cash transfer

scheme which is soon going to be imple-

mented this year which will definitely reduce

the leakages and subsidy bill and have a posi-

tive impact in curbing inflation.

Interest Rate

Another tool in RBI’s repertoire is setting the

policy rates and Cash Reserve Ratio. RBI re-

duced the CRR, the minimum percentage of

total demand and time liabilities that banks

have to maintain as reserves with RBI, by 25

basis points to 4.25% on 30 October 2012, its

8.5%, 6.5% to 5.5% in the last 3 years, which

makes it a big concern for RBI.

Inflation

The acceptable level of Inflation according to

RBI is 5% and the current RBI governor D.

Subbarao has said it’s the highest priority

among the four. The

december figure of

WPI was 7.18%,

which was lowest in

3 years contradicted

by 3 month high

Consumer Price In-

dex of 10.56%. Also,

recently fuel retailers

were allowed to in-

crease diesel prices

by 45 paise per litre

every month have

put pressure on

prices of food, ce-

ment and other

products depending

on trucks for trans-

portation.

Inflation in India is

sticky. What that

means is that it stays

at high levels even

after measures are

© Monetrix, Finance & Economics Club of MDI, Gurgaon

|COVER ARTICLE|

Policy rates, Reserve ratios, lending, and

deposit rates as of 30th Jan, 2013

Bank Rate 8.75%

Repo Rate 7.75%

Reverse Repo Rate 6.75%

CRR 4.00%

SLR 23.0%

Base Rate 9.75%–10.50%

Deposit Rate 7.50%–9.00%

Table 2: Current Scenario

Figure 1: Exchange Rate fluctuation

Figure 2: Fluctuation of GDP growth rate

17

17

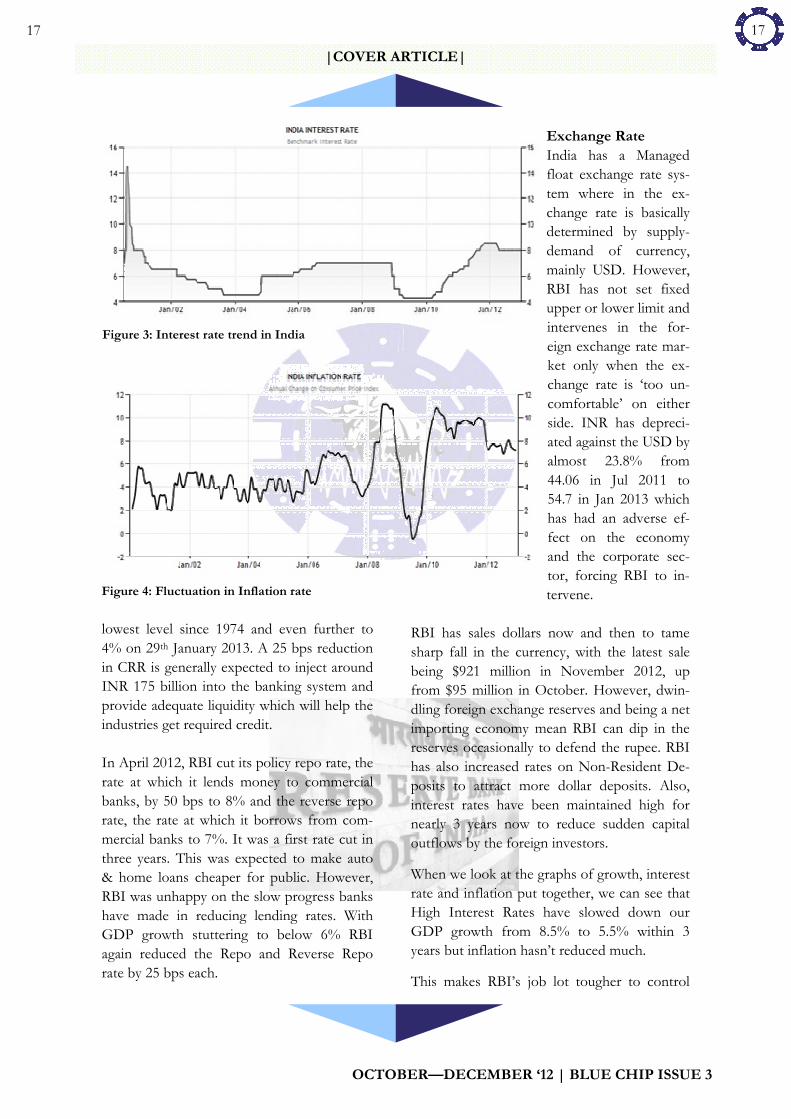

Exchange Rate

India has a Managed

float exchange rate sys-

tem where in the ex-

change rate is basically

determined by supply-

demand of currency,

mainly USD. However,

RBI has not set fixed

upper or lower limit and

intervenes in the for-

eign exchange rate mar-

ket only when the ex-

change rate is ‘too un-

comfortable’ on either

side. INR has depreci-

ated against the USD by

almost 23.8% from

44.06 in Jul 2011 to

54.7 in Jan 2013 which

has had an adverse ef-

fect on the economy

and the corporate sec-

tor, forcing RBI to in-

tervene.

RBI has sales dollars now and then to tame

sharp fall in the currency, with the latest sale

being $921 million in November 2012, up

from $95 million in October. However, dwin-

dling foreign exchange reserves and being a net

importing economy mean RBI can dip in the

reserves occasionally to defend the rupee. RBI

has also increased rates on Non-Resident De-

posits to attract more dollar deposits. Also,

interest rates have been maintained high for

nearly 3 years now to reduce sudden capital

outflows by the foreign investors.

When we look at the graphs of growth, interest

rate and inflation put together, we can see that

High Interest Rates have slowed down our

GDP growth from 8.5% to 5.5% within 3

years but inflation hasn’t reduced much.

This makes RBI’s job lot tougher to control

lowest level since 1974 and even further to

4% on 29th January 2013. A 25 bps reduction

in CRR is generally expected to inject around

INR 175 billion into the banking system and

provide adequate liquidity which will help the

industries get required credit.

In April 2012, RBI cut its policy repo rate, the

rate at which it lends money to commercial

banks, by 50 bps to 8% and the reverse repo

rate, the rate at which it borrows from com-

mercial banks to 7%. It was a first rate cut in

three years. This was expected to make auto

& home loans cheaper for public. However,

RBI was unhappy on the slow progress banks

have made in reducing lending rates. With

GDP growth stuttering to below 6% RBI

again reduced the Repo and Reverse Repo

rate by 25 bps each.

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

|COVER ARTICLE|

Figure 3: Interest rate trend in India

Figure 4: Fluctuation in Inflation rate

18

decision to not cut key policy rates, saying the

government would “walk alone” to face the

challenge of growth. In Jan 2013, RBI obliged

with rate cuts, which was necessary to revive

an economy that grew by below 6% for the

past three quarters. Further rate cuts are per-

haps necessary to further boost the economy

which is well on track to register, in this fiscal,

its slowest annual growth rate in a decade.

However, upside risks to inflation persist

which limits RBI’s scope to further reduce pol-

icy rates.

And then there is the sliding rupee. Increase in

policy rates help prevent sudden outflows of

foreign capital from the country and thus help

check the meltdown of the domestic currency.

It would not be a wise decision to increase

rates to address deprecation of rupee and put a

blow to the growth aspirations. On the other

hand, further decrease in the rates may lead to

further capital outflows.

Thus, every decision that RBI takes to achieve

one of it’s’ objectives, results in some adverse

effect on some of its other objectives. High

interest rates imply high borrowing costs which

result in reduced investment and thereby have

an adverse impact on industrial growth. High

rates create liquidity crunch in the market

which hampers growth. If it tries to control

inflation by increasing rates, growth is ham-

pered. If it tries to breathe life into the growth

by cutting rates, rupee depreciates and inflation

increases. If it raises policy rate to check rupee

meltdown, growth will lose momentum. No

wonder that the chariot is not able to move at

all!

It’s critical for the government and the RBI to

have a common goal, but independent working

and still managing to take actions which do not

have contradictory effect on the other’s ac-

tions. But for too long, inflation has been the

primary concern for RBI. It’s time for growth

to be as much a concern as inflation.

inflation and RBI generally is cautious in re-

ducing interest rates.

The Juggling Act

Imagine trying to run a chariot with

horses tied in 4 directions and each moving in

its own direction. RBI is running such a char-

iot whose four horses – inflation, growth,

currency and borrowing – are moving in 4

different directions.

There are an increasing number of analysts

who feel that RBI may have erred by focusing

too much on inflation. Their argument is

valid one: that RBI can have impact only on

the demand-side inflation and interest rates

are unlikely to have any impact on the supply-

side inflation. And the policy makers are well

aware of this. However, there is the ‘politics

of inflation’ which puts pressure on RBI’s

decisions.

With 2014 elections looming over the hori-

zon, it is difficult to see many things change.

Vote-bank politics would imply that govern-

ment would dig heavily in its coffers, irrespec-

tive of how much fiscal austerity inflation, all

time high current account deficit and fiscal

deficit would require.

In Dec 2012, the Finance Minister expressed

unhappiness over the Reserve Bank of India's

© Monetrix, Finance & Economics Club of MDI, Gurgaon

|COVER ARTICLE|

19

|BEGINNERS’ CORNER|

Liquidity Risk

The risk created by the inability to sell (liquidate)

an asset quickly or obtain required funds from its

sale. One of the reasons for this could be failure

to recognize changes in the market conditions and

respond in a timely manner.

Operational Risk

The risk of loss due to faulty internal processes,

people or systems that a company is exposed to

when it undertakes operations in a particular field

or industry. It can be thought of as an adverse

outcome which happens as a result of an organi-

zation’s activities.

There are broadly

three ways of deal-

ing with financial

risks, namely

diversification,

insurance and

hedging. Apart

from these, the central

banks of certain countries have resorted to

regulatory norms to safeguard banks from certain

types of financial risks. In India, the Reserve Bank

of India (RBI) fixes a Statutory Liquidity Ratio

(SLR) and Cash Reserve Ratio (CRR) for banks.

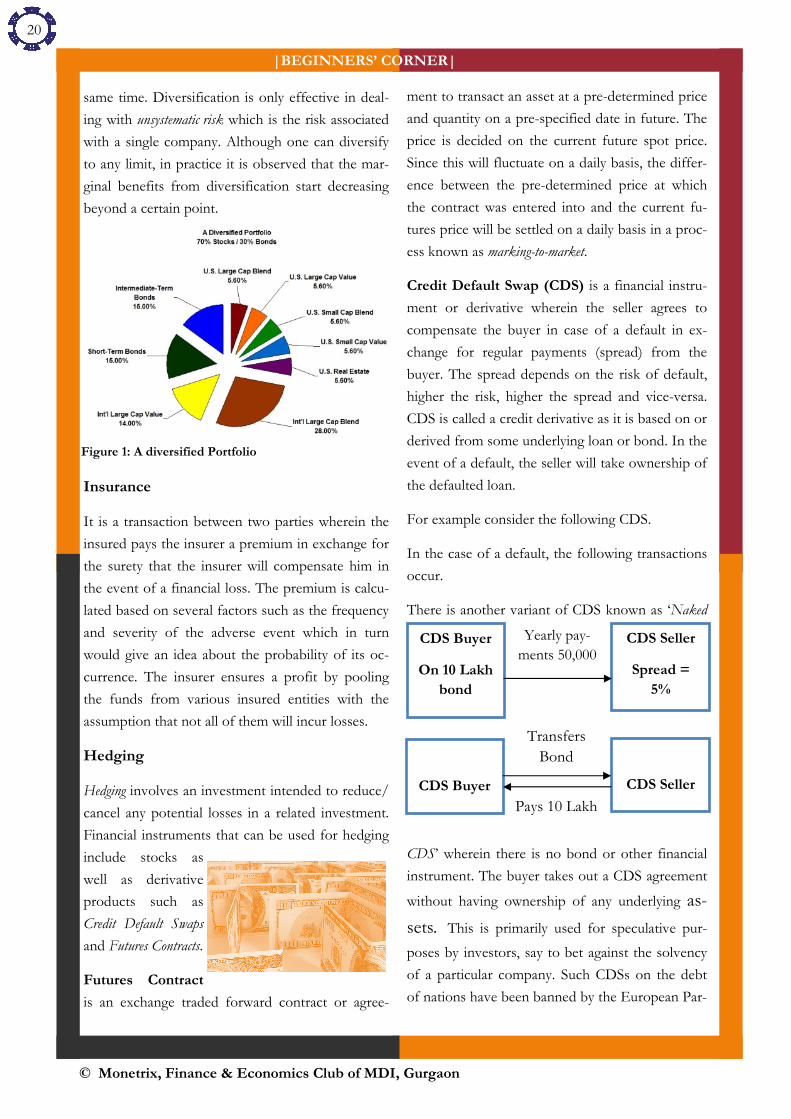

Diversification

The basic strategy in diversification is based on

the age old proverb “Don’t put all your eggs in

one basket”. It is a means of reducing risk by in-

vesting in a variety of asset classes so that the

positive performance of some will balance the

negative performance of others and thus the com-

bined portfolio would yield higher returns at

lower risk than the individual investments. The

assumption is that the value of all the component

assets will not move in the same direction at the

The objective of most firms is to create economic

value while managing the exposure to risk. The

various financial crises witnessed in the past have

reinforced the need for decision makers and inves-

tors to be well versed with the concepts of finan-

cial risk management. Let us first understand the

different types of financial risks before proceeding

to look at various techniques that can be used to

deal with them.

Credit Risk

The risk of loss due to the possibility of a bor-

rower defaulting on interest payments or principal

repayment. It is normal practice for a lender to

carry out a credit check on a prospec-

tive borrower prior to

issuing the funds. In

the case of corporate

or government

bonds, ratings

agencies analyze

and provide rat-

ings based on the credit

risk.

Market Risk

The risk to an investment arising from a phenome-

non or factors affecting the performance of the

financial markets as a whole. This phenomenon

could be natural such as a disaster or artificial such

as a recession. The four standard market risk fac-

tors include equity, interest rate, currency and com-

modity risk.

Regulatory Risk

The risk of regulatory changes impacting a busi-

ness, securities or the market in general can be

termed as regulatory risk. In the trading context it

can be defined as the risk exposure due to the

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

FINANCIAL RISK MANAGEMENT Team Blue Chip

20

same time. Diversification is only effective in deal-

ing with unsystematic risk which is the risk associated

with a single company. Although one can diversify

to any limit, in practice it is observed that the mar-

ginal benefits from diversification start decreasing

beyond a certain point.

Insurance

It is a transaction between two parties wherein the

insured pays the insurer a premium in exchange for

the surety that the insurer will compensate him in

the event of a financial loss. The premium is calcu-

lated based on several factors such as the frequency

and severity of the adverse event which in turn

would give an idea about the probability of its oc-

currence. The insurer ensures a profit by pooling

the funds from various insured entities with the

assumption that not all of them will incur losses.

Hedging

Hedging involves an investment intended to reduce/

cancel any potential losses in a related investment.

Financial instruments that can be used for hedging

include stocks as

well as derivative

products such as

Credit Default Swaps

and Futures Contracts.

Futures Contract

is an exchange traded forward contract or agree-

ment to transact an asset at a pre-determined price

and quantity on a pre-specified date in future. The

price is decided on the current future spot price.

Since this will fluctuate on a daily basis, the differ-

ence between the pre-determined price at which

the contract was entered into and the current fu-

tures price will be settled on a daily basis in a proc-

ess known as marking-to-market.

Credit Default Swap (CDS) is a financial instru-

ment or derivative wherein the seller agrees to

compensate the buyer in case of a default in ex-

change for regular payments (spread) from the

buyer. The spread depends on the risk of default,

higher the risk, higher the spread and vice-versa.

CDS is called a credit derivative as it is based on or

derived from some underlying loan or bond. In the

event of a default, the seller will take ownership of

the defaulted loan.

For example consider the following CDS.

In the case of a default, the following transactions

occur.

There is another variant of CDS known as ‘Naked

CDS’ wherein there is no bond or other financial

instrument. The buyer takes out a CDS agreement

without having ownership of any underlying as-

sets. This is primarily used for speculative pur-

poses by investors, say to bet against the solvency

of a particular company. Such CDSs on the debt

of nations have been banned by the European Par-

|BEGINNERS’ CORNER|

CDS Buyer

On 10 Lakh

bond

CDS Seller

Spread =

5%

Yearly pay-

ments 50,000

CDS Buyer

CDS Seller

Transfers

Bond

Pays 10 Lakh

© Monetrix, Finance & Economics Club of MDI, Gurgaon

Figure 1: A diversified Portfolio

21

liament since end 2011.

Statutory Liquidity Ratio (SLR)

SLR refers to the minimum proportion of demand

and time liabilities that a bank is required to main-

tain in the form of liquid assets such as cash, gold

or government approved bonds and shares at the

end of a business day. The current SLR is 23%.

Failure to maintain the minimum stipulated amount

leads to monetary penalties that need to be paid to

the Reserve Bank of India. The RBI uses SLR as a

tool to suck excess liquidity from the markets, man-

age liquidity risk of banks and thereby safeguard

customers’ money.

Other objectives of the SLR include ensuring sol-

vency of banks and promoting investment in gov-

ernment securities.

Cash Reserve Ratio (CRR)

CRR is the proportion of deposits to be maintained

in the form of cash with the RBI. The current CRR

is 4.25%. It is basically used to manipulate the

amount of funds available with banks to lend out or

invest and thereby secure their solvency. From an

investor’s point of view, it reduces the risk of de-

positing money in a bank.

Apart from the methods and regulations discussed

above, an important set of guidelines for financial

risk management is the Basel norms comprising of

Basel accords I, II and III. These were formulated

by a group of central banks known as Basel Com-

mittee on Banking Supervision (BCBS).

In plain and simple terms, the norms were devel-

oped to ensure that global banks maintain adequate

capital to withstand periods of economic crisis.

Basel Norms

Basel I

Basel I prescribed the minimum capital require-

ment of 8% and the structure of risk weights used

in determining the risk weighted assets (RWA) for

a bank. RWA is based on different weights as-

signed to different classes of assets based on their

risk profiles. For example, cash may be assigned a

risk weight of 0% whereas government approved

securities 2.5%. Basel I primarily dealt with credit

risk. It was introduced in 1988 and adopted by In-

dia in 1999.

Basel II

Basel II is concerned with maintenance of regula-

tory capital and development of risk management

techniques to deal with the three major types of

risk for a bank, namely credit, operational and mar-

ket risk. In addition it prescribed mandatory disclo-

sure by banks of their risk exposure to the central

bank. It was introduced in 2004 and implemented

by RBI in 2009.

Basel III

Basel III aims to strengthen the banking system

by turning the focus on banking factors capital,

leverage, funding and liquidity. It prescribes

tougher capital standards. It defines a Liquidity Cov-

erage Ratio (LCR), the amount of high-quality liquid

assets that can be easily converted into cash to

meet a banks needs during a 30-day c r e d i t

squeeze. Basel III was introduced in 2010 and mo-

tivated by the event of the 2008 financial crisis.

Banks are however concerned that Basel III will

impact their profitability as they have to make sig-

nificant changes to their systems in areas such as

stress testing, liquidity and capital management

infrastructure. Recently a compromise was reached

wherein the banks will have to meet only 60% of

their LCR requirements by 2015, the full rule being

implemented only by 2019. This comes as a relief

to certain parties at a time when the economic sce-

nario worldwide is not too positive and growth is

sluggish.

|BEGINNERS’ CORNER|

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

22

Introduction

A persistently negative current account deficit

is a cause of concern for any economy. When

a country runs a current account deficit, it

builds up liabilities to the rest of the world

that are financed by flows in the financial ac-

count. Large deficits and rising indebtedness

could also leave countries more vulnerable to

adverse external shocks.

Because India has a long history of sizeable

current account deficits, it makes for an inter-

esting case study. A closer look at figure one

clearly reveals India’s inability to maintain a

positive current account balance. We can see

that in only four years from the past two dec-

ades India has been able to claim a current

account surplus. The present levels of current

account deficit have clearly reached unsustain-

able levels, consistently rising for the past three

years. Will India be able to reduce present high

level of current account deficit that is such a

big cause of concern? What implications such

high levels of current account deficit have for

the Indian economy in 2013. Can we learn

something from other developing or developed

economies? This article explores answers to

these questions with a focus on analysing the

implications of high current account deficit on

the Indian economy in 2013 and possible

measures to bring down such high levels of

current account deficit.

Current Account Deficit (CAD)

Current Account Balance can be defined as the

net of export and import and if the import is in

excess to the export it is called a deficit. Al-

though CAD constitute of other factors like

|RISING CURRENT ACCOUNT DEFICIT|

Rising Current Account Deficit - India’s Achilles’ heel

PGPM 2012-14

Management Development Institute, Gurgaon

Ashish Khare Deependra Kumar

© Monetrix, Finance & Economics Club of MDI, Gurgaon

Figure 1: Current Account Deficit of India

23

factor income and transfer payment but major

constituent of Current account balance is the

trade balance (i.e. Export-Import).

Major Implications of High Current Ac-

count Deficit

High current account deficit is major concern

because it cannot be sustained for long as the

countries that 'lend' money (through the capi-

tal account surplus) will expect to get back

their money with interest at some point. If the

money is not seemed to be present in future,

the lending country may demand higher re-

turns or may take back their money. With no

one to lend, the country can’t import capital

goods to make own good or even import

consumer goods.

Reasons for high current account deficit

(CAD) - Indian Economy 2012-13

To put some numbers into perspective, cur-

rent account deficit widened to 5.4 % of

GDP in the Q2 2013. The current account

deficit was $22.3 billion in the three months

through September, or 5.4 percent of GDP,

compared with $16.6 billion in the June quar-

ter and $18.9 billion in the September quarter

of 2011.

The widening gap has been caused mainly by

the increasing trade deficit. The trade deficit

widened to 12.2% of GDP in Q3 from 9.7%

in Q2. While oil prices have risen, most of

this worsening is in the non-oil segment

(Nomura Report). Gold imports were the

major cause of the widening current account

deficit. India saw $60 billion worth of gold

imports in fiscal 2011-12 which contributed

to high CAD levels. Gold imports in the 2010

-11 were $40 billion. The increase of $20 bil-

lion can be attributed to high level of infla-

tion. While the imports were dominated by

higher demand for gold, the exports con-

tracted. In the April-November period, India's

total exports contracted by nearly 6 percent

from a year earlier, leaving a trade deficit of

nearly $130 billion.

Another possible cause has been the higher

demand or a supply shocks in the Indian Econ-

omy. In 2011-12 the growth in aggregate de-

mand categories like consumption and fixed

investment fell from about 8% to 5%. It has

been observed that the Indian CAD is counter-

cyclical, rising when output falls and not when

demand is rising. This suggests the dominance

of external supply shocks rather than the de-

mand factor. Current account deficit is going

to be as strained in Q3 2012-13 as it was in the

second quarter because of the lower GDP

growth.

The depreciating INR also contributed to for

the past one year and was the third worst per-

former in Asia in 2012. The rupee closed 2012

at 55.00 inflating the import bill and the cur-

rent account deficit.

Implications of the High Current Account

Deficit for the Indian Economy

The recent level of the Current account deficit

at 5.4 % of the GDP is above the sustainable

level. According to research report from RBI,

India can sustain a current account deficit of

2.5 % of GDP with a lower GDP growth. This

clearly is an alarming situation for the Indian

economy and has the capacity to impair India’s

financial stability.

This deficit will also cause the foreign ex-

change reserves to dry up if the inflows to

make the deficit do not materialize. It will have

direct bearing on the strength of INR. The de-

|RISING CURRENT ACCOUNT DEFICIT|

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

24

preciating INR has come under a lot of pres-

sure with the increasing current account defi-

cit. The Indian rupee has dropped more than

20% from its August 2011 peak against the

dollar. This sharp depreciation is mainly due

to India’s large current account deficit.

Action Taken by Indian Government and

RBI

Government of India is considering steps to

make gold imports costlier in order to reduce

the huge foreign exchange outgo on the yel-

low metal, which has pushed the current ac-

count deficit to a record high.

Government is also trying to create an inves-

tor friendly environment to increase invest-

ment from foreign investment in the form of

FDI and FII, the income from these foreign

investments positively contributes to current

account.

Current Account Deficit: Story of other

Developing Nations

While focusing on the current account deficit

problem of Indian economy it becomes in-

creasingly important to have a look at similar

developing nations to understand current ac-

count situation in these countries.

Brazil

Brazil is currently facing a big current account

deficit which is 2.11% of GDP at the end of

financial year 2011-12. Brazil has a current ac-

count deficit despite having a positive trade

balance on account of large service deficit. The

reason behind the positive trade balance is the

export-oriented Brazil economy heavily de-

pendent upon soybean, orange juice and iron.

Russia

Russia’s current account surplus is fuelled pri-

marily by high oil exports. Oil prices have risen

steadily over the past few years which have

increased their export prices. From 2000 on-

ward, the country started to record positive

trade surplus, taking the advantage of the de-

valued currency. Russia’s current surplus de-

creased sharply in `08-`09 due to the global

recession and decrease in demand for com-

modities. Increase in Russians income is set to

fuel demand for imports; this would lead to

narrowing of the current surplus.

|RISING CURRENT ACCOUNT DEFICIT|

© Monetrix, Finance & Economics Club of MDI, Gurgaon

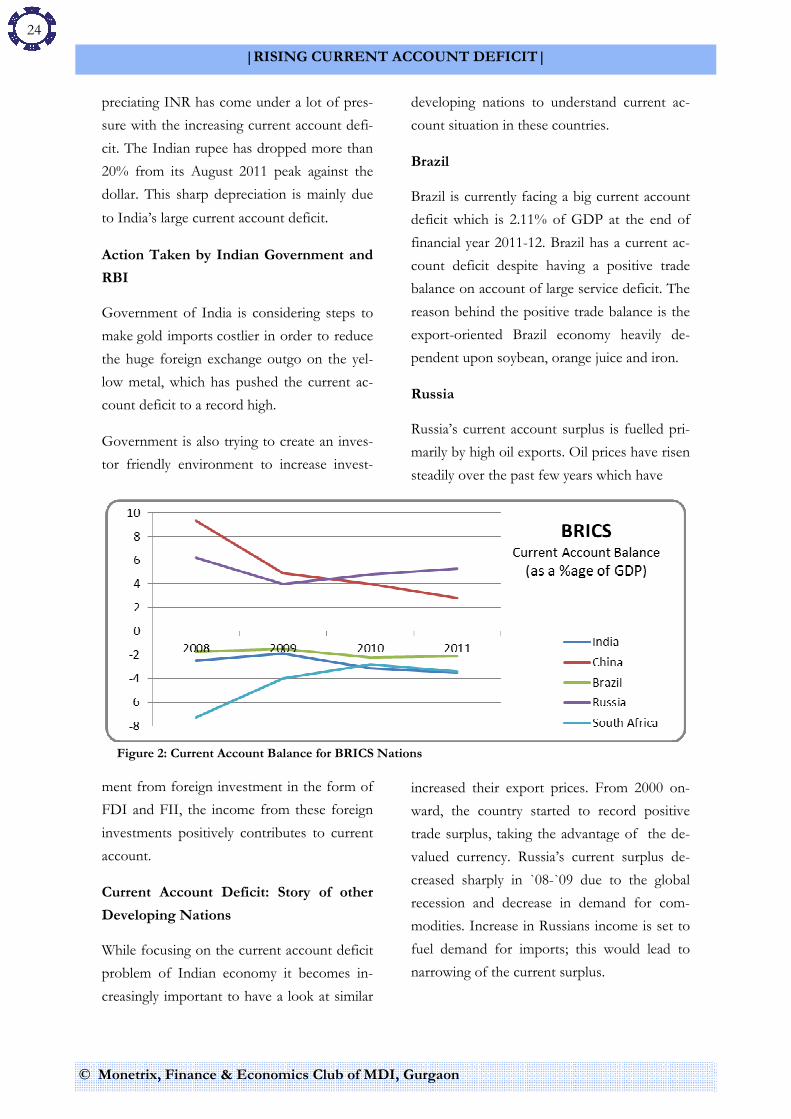

Figure 2: Current Account Balance for BRICS Nations

25

China

China has had a consistent Current Account

Surplus which today is approximately $300

billion. The major reason for this surplus is

the competitiveness of Chinese products

which have gained a reputation in manufac-

turing sector and thus China has become the

supplier of goods for the whole world.

South Africa

The current account of South Africa has been

in the red lately. The weaker outlook for the

global economy in response to the interna-

tional financial crisis has already resulted in a

large-scale withdrawal of capital from South

Africa. The Rand has depreciated by approxi-

mately 30% against the American dollar dur-

ing this period. Trade balance is only quarter

of the current account deficit which makes it

difficult to reduce the latter simply by reduc-

ing imports.

Current Account Deficit of developed na-

tions: a case study on USA

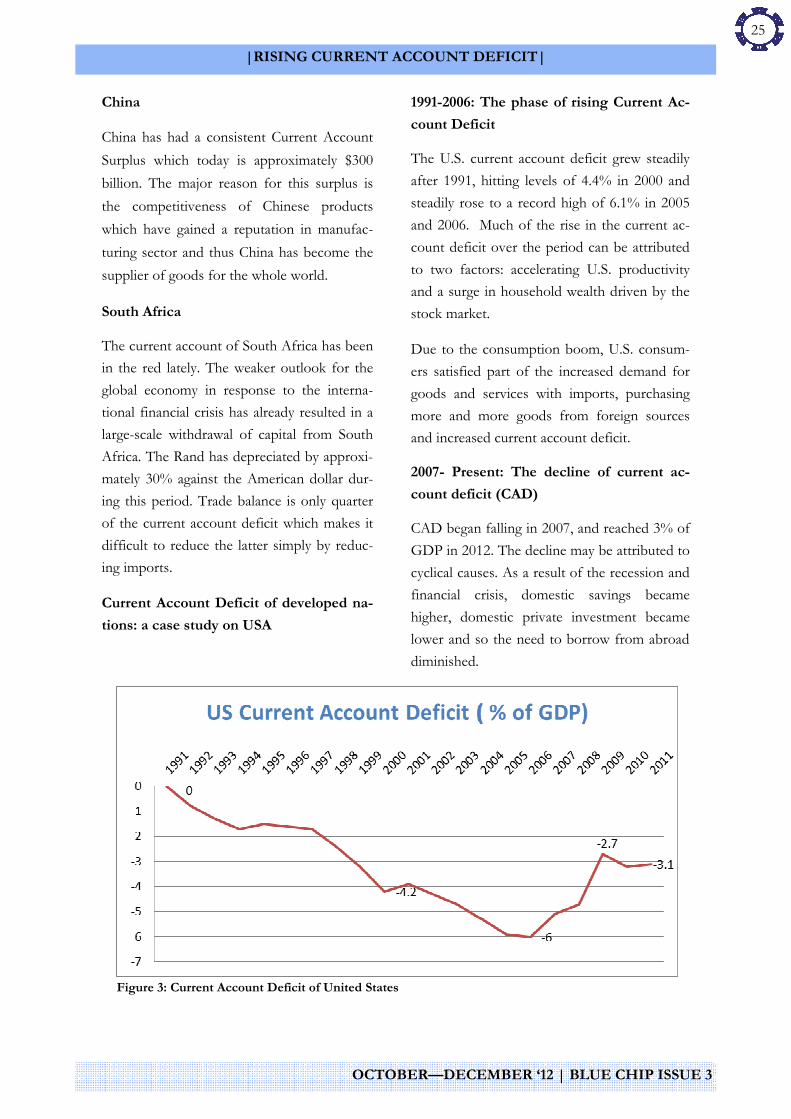

1991-2006: The phase of rising Current Ac-

count Deficit

The U.S. current account deficit grew steadily

after 1991, hitting levels of 4.4% in 2000 and

steadily rose to a record high of 6.1% in 2005

and 2006. Much of the rise in the current ac-

count deficit over the period can be attributed

to two factors: accelerating U.S. productivity

and a surge in household wealth driven by the

stock market.

Due to the consumption boom, U.S. consum-

ers satisfied part of the increased demand for

goods and services with imports, purchasing

more and more goods from foreign sources

and increased current account deficit.

2007- Present: The decline of current ac-

count deficit (CAD)

CAD began falling in 2007, and reached 3% of

GDP in 2012. The decline may be attributed to

cyclical causes. As a result of the recession and

financial crisis, domestic savings became

higher, domestic private investment became

lower and so the need to borrow from abroad

diminished.

|RISING CURRENT ACCOUNT DEFICIT|

OCTOBER—DECEMBER ‘12 | BLUE CHIP ISSUE 3

Figure 3: Current Account Deficit of United States

26

Conclusion

The need to contain current account deficit as

evident above is extremely urgent. Unfortu-

nately there is no magic wand that can bring

down Current Account (CAD) deficit in a go.

It needs to be achieved through the synergy

of a number of measures each aiming to

strike at the very root of reigning current ac-

count deficit. The widening deficit is attribut-

able to expensive oil, high gold imports and a

sharp drop in exports. There is, thus, a need

to reduce imports and boost merchandise

exports to bring the CAD to sustainable lev-

els. On the exports front, a lot depends on

the global economic situation. Our major

markets are the US, Euro Zone and China. If

these markets recover and do well we can

improve on the exports front, provided we

maintain our competitiveness. With the worst

of recession already behind us and United

States averting the fiscal cliff, the prospects

do look better.

The more dominant cause of worry is the im-

port bill. International commodity prices and

rupee exchange rate should be the focus areas

as the country imports many commodities it

needs. An important step would be to make

the gold imports expensive. The Indian gov-

ernment has taken right steps in this direction

by imposing tax on gold jewellery and increas-

ing the import duty for gold.

However, it will not be easy for Indian econ-

omy to correct current account in 2013, pre-

cisely because of strong domestic demand

and a weak external demand. Already envi-

ronment sensitive policies, land acquisition

issues and availability of quality infrastructure

have contributed to moderation in FDI in-

flows which are extremely important to fi-

nance the current account deficit. While the

subdued growth of receipts is cyclical in na-

ture and can be expected to improve with the

recovery in world economy, the rise in crude

oil prices and reasons for moderation in FDI

are more structural in nature. It is thus impor-

tant for the policymakers to make Indian econ-

omy more investor friendly in 2013 and elimi-

nate bottlenecks arising due to policy paralysis

at the centre.

What is the ideal way out for Indian govern-

ment then? Since India’s linkage with the world

economy, in terms of trade and finance, is