McGraw-Hill/Irwin © The McGraw-Hill Companies 2010 Audit Planning and Types of Audit Tests Chapter...

42

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010 Audit Planning and Types of Audit Tests Chapter Five

-

Upload

mary-evans -

Category

Documents

-

view

217 -

download

0

Transcript of McGraw-Hill/Irwin © The McGraw-Hill Companies 2010 Audit Planning and Types of Audit Tests Chapter...

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Audit Planning

and

Types of Audit Tests

Chapter Five

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

The Phases of an Audit That Relate to Audit Planning

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Prospective Client Acceptance1. Obtain and review financial information.

2. Inquire of third parties.

3. Communicate with the predecessor auditor.

4. Consider unusual business or audit risks.

5. Determine if the firm is independent.

6. Determine if the firm has the necessary skills and knowledge.

7. Determine if acceptance violates any applicable regulatory or ethical requirements.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Continuing Client Retention

Evaluate client retention periodically

Near audit completion or after a significant event

Conflicts over accounting & auditing

issuesDispute over fees

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

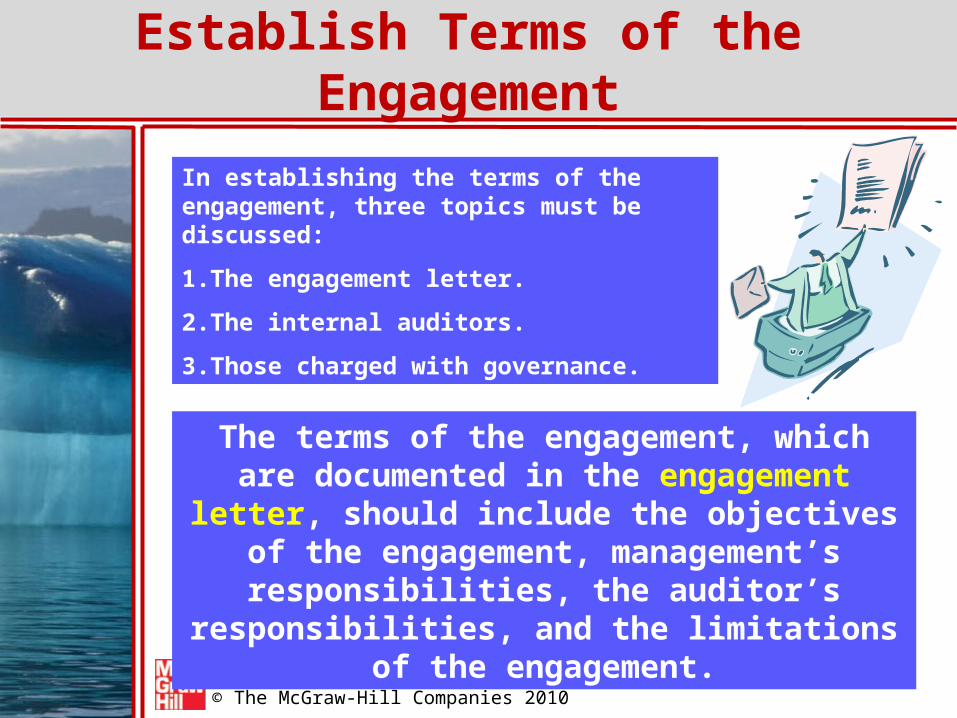

Establish Terms of the Engagement

The terms of the engagement, which are documented in the engagement letter, should

include the objectives of the engagement, management’s responsibilities, the auditor’s

responsibilities, and the limitations of the engagement.

In establishing the terms of the engagement, three topics must be discussed:

1.The engagement letter.

2.The internal auditors.

3.Those charged with governance.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

The Engagement Letter

The engagement letter formalises the arrangement reached between the auditor and the client.

In addition to the items mentioned in the sample engagement letter in Exhibit 5-1 in the textbook,

the engagement letter may include:

• Arrangements for use of experts or internal auditors.

• Any limitations of liability of the auditor or client.

• Additional services to be provided.

•Arrangements regarding other services.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Internal Auditors

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Those Charged with Governance

Board of Directors

Audit Committee

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Preliminary Engagement Activities

Determine the Audit Engagement Team

Requirements

Assess Compliance with Ethical Requirements,

including Independence

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Planning the Audit

• The auditor will develop an overall audit strategy for conducting the audit. This will help the auditor to determine what resources are needed to perform the engagement.

• An audit plan is more detailed than the audit strategy.

• Basically, the audit plan should consider how to conduct the engagement in an effective and efficient manner.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Planning the AuditWhen preparing the audit plan, the auditor should be

guided by the results of the risk assessment procedures performed to gain an understanding of the entity.

Additional steps:

•Assess business risks and establish materiality.

• Assess the need for experts.

•Consider the possibility of non-compliance (illegal) acts.

•Identify related parties.

•Conduct preliminary analytical procedures.

•Consider additional value-added services.

Let’s look at each

of these steps.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Assess Risks and Establish Materiality

Use audit risk model

Restrict risk at account

balance level

Achieve acceptable low level of audit risk

You may want to review the detailed discussion in Chapter 3 of the process used to assess the client’s

business risks and to establish materiality.

Assess Risks

Establish Materiality

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Experts

A major consideration in planning the audit is the need for an auditor’s expert (ISA 620).

The use of an IT expert is a significant aspect

of most audit engagements.

The presence of complex information technology

may require the use of an IT expert.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Non-Compliance (Illegal) Acts

Non-Compliance Acts

Direct & Material

Consider laws and regulations as part

of audit

Material & Indirect

Be aware may have occurred;

investigate if brought to attention

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Non-Compliance Acts

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Related PartiesSome examples from IAS 24 Related

Party Disclosure

•Parents and subsidiaries.

•Significant influence.

•Joint control.

•Associate entity.

•Joint venture.

•Management.

•Close family of the principal owners & management.

•Other parties that can have significant influence.

How to Identify Related Parties

•Review minutes of meetings of boards and management.

•Review conflict of interest statements.

•Review records of the entity’s investments.

•Review contracts and agreements with key management or those charged with governance.

•Review significant contracts and agreements not in the entity’s ordinary course of business.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Preliminary Analytical Procedures

To understand the client’s business and transactions

To identify financial statement accounts likely to

contain errors

By understanding the client’s business and identifying where errors are likely to occur, the

auditor can allocate more resources to investigate necessary accounts.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Additional Value-Added Services

Tax PlanningTransaction

SupportIT-

consultancy

Internal reporting

BenchmarkingRisk

Assessment

Auditors are limited in the types of consulting services that they can offer

their audit clients.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Document Overall Audit Strategy and Audit Plan

Auditors ensure they have addressed the risks they identified by documenting the linkage from the client’s

business, objectives, and strategy to the audit plan.

The auditor’s preliminary decision concerning control risk determines the level of control testing, which in

turn affects the auditor’s substantive tests of the account balances and transactions.

Document overall audit strategy and audit plan, which

involves documenting the decisions about

The auditor documents how the client is managing its risk (via internal

control processes) and the effects of the risks and controls on the planned

audit procedures. A

U

D

I

T

T

E

S

T

S

Nature

Timing

Extent

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Document Overall Audit Strategy and Audit Plan

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Types of Audit Tests

Risk Assessment Procedures

Used to obtain an understanding of the entity and its environment,

including internal control.

Tests of Controls

Performed to obtain audit evidence about the operating effectiveness

of controls in preventing, detecting and correcting material

misstatements.

Substantive Procedures

Detect material misstatements in a transaction class, account balance,

and disclosure element of the financial statements.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Tests of Controls

Inquiry Inspection

Walk Through

Reperformance

Observation

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Tests of Controls

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Substantive Procedures

Analytical Procedures

Obtains evidence about particular

assertions related to account balances or

classes of transactions

Tests of Details

Tests for errors or fraud in individual

transactions, account balances, and disclosures

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Dual Purpose Tests

Substantive Tests

Tests of Controls

Dual Purpose

Test

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Purposes of Analytical Procedures

Preliminary Analytical

Procedures

Used to assist the auditor to better understand the business and to plan

the nature, timing, and extent of audit procedures.

Substantive Analytical

Procedures

Used to obtain evidence about particular assertions related to account balances or classes of

transactions.

Final Analytical

Procedures

Used as an overall review of the financial information in the final

review stage of the audit.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Purposes of Analytical Procedures (See Table 5-5)

Trend Analysis

Ratio Analysis

Reasonableness

Analysis

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Substantive Analytical Procedures Decision Process

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Develop an Expectation

Auditing standards require the auditor to have an expectation whenever analytical procedures are used. An expectation can be developed using a variety of information sources such as:

• Financial and operating data.

• Budgets and forecasts.

• Industry publications.

• Competitor information.

• Management’s analyses.

• Analyst’s reports.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Define a Tolerable Difference

The size of the tolerable difference depends on:

• The significance of the account.

• The desired degree of reliance on the substantive analytical procedures.

•The level of disaggregation in the amount being tested.

• The precision of the expectation.

But the amount is always less than materiality!

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Compare and Investigate

Compare the expectation to the recorded amount and investigate any differences greater than the tolerable difference.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

The Investigation of Differences for Planning and Final Analytical Procedures

Preliminary Analytical

Procedures Differences

Corroborating evidence

is not required

Final Analytical

Procedures Differences

Corroborating evidence is required

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Audit Testing Hierarchy

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Filling the Assurance Bucket

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Example of Filling the Assurance Buckets for Each Assertion (Accounts Payable)

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Short-Term Liquidity Ratios

Current Ratio

Quick Ratio

Operating Cash Flow

Ratio

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

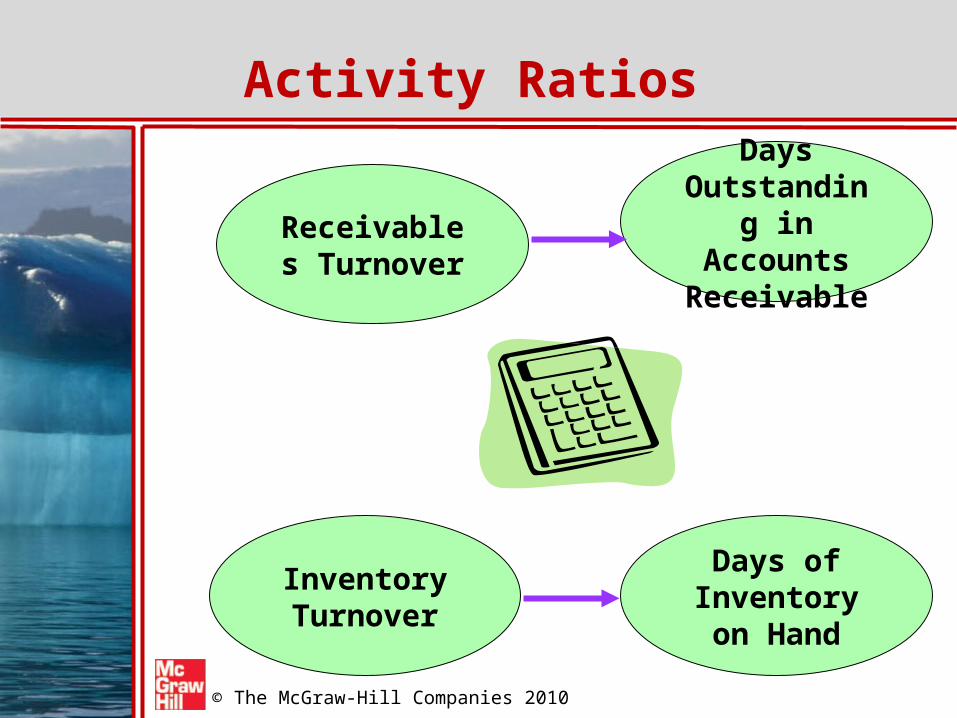

Activity Ratios

Receivables Turnover

Days Outstanding in Accounts Receivable

Inventory Turnover

Days of Inventory on

Hand

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Profitability Ratios

Gross Profit Percentage Profit Margin

Return on Assets

Return on Equity

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Coverage Ratios

Debt to Equity

Times Interest Earned

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Audit of Group Financial Statements

Component of a Group

Entity or business activity in which financial

information is included in the group financial statements.

Component Auditor

An auditor who, at the request of the group engagement team, performs

work on financial information related to a

component for the group audit.

Auditing standards require the group engagement team to identify components that are

likely to be significant components.

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

Audit of Group Financial Statements

McGraw-Hill/Irwin © The McGraw-Hill Companies 2010

End of Chapter 5