McGraw-Hill /Irwin© 2009 The McGraw-Hill Companies, Inc. INVESTMENTS Chapter 12.

45

McGraw-Hill /Irwin © 2009 The McGraw-Hill Companies, Inc. INVESTMENTS INVESTMENTS Chapter 12

-

Upload

alfred-lester -

Category

Documents

-

view

219 -

download

0

Transcript of McGraw-Hill /Irwin© 2009 The McGraw-Hill Companies, Inc. INVESTMENTS Chapter 12.

McGraw-Hill /Irwin © 2009 The McGraw-Hill Companies, Inc.

INVESTMENTSINVESTMENTS

Chapter 12

Slide 2

12-2

Nature of InvestmentsNature of Investments

Bonds and notes

(Debt (Debt securities)securities)

Bonds and notes

(Debt (Debt securities)securities)

Common and preferred stock

(Equity (Equity securities)securities)

Common and preferred stock

(Equity (Equity securities)securities)

Investments can be accounted for in a variety of ways, depending on the nature

of the investment relationship.

Slide 3

12-3

Reporting Categories for InvestmentsReporting Categories for InvestmentsControl Characteristics of the Investment Reporting Method Used by the Investor

The investor lacks significant influence over the operating and financial policies of the investee:

Investment in debt securities for which the investor has the "positive intent and ability" to hold to maturity.

Held-to-maturity (HTM) - investment reported at amortized cost.*

Investment held in an active trading account. Trading securities (TS) - investment reported at fair value with unrealized holding gains and losses included in net income.

Other. Securities available-for-sale (AFS) - investment reported at fair value with unrealized holding gains and losses excluded from net income and reported in Other Comprehensive income.*

The investor has significant influence over the operating and financial policies of the investee:

Typically the investor owns between 20% and 50% of the voting stock of the investee.

Equity method - investment cost adjusted for subsequent earnings and dividends of the investee.*

The investor controls the investee:The investor owns more than 50% of the voting stock of the investee.

Consolidation - the financial statements of the investor and investee are combined as if they are a single company.

Reporting Categories for Investments

* If the investor elects the fair value option, this type of investment also can be accounted for using the same approach that's used for trading securities, with the investment reported at fair value and unrealized holding gains and losses included in earnings.

Slide 4

12-4

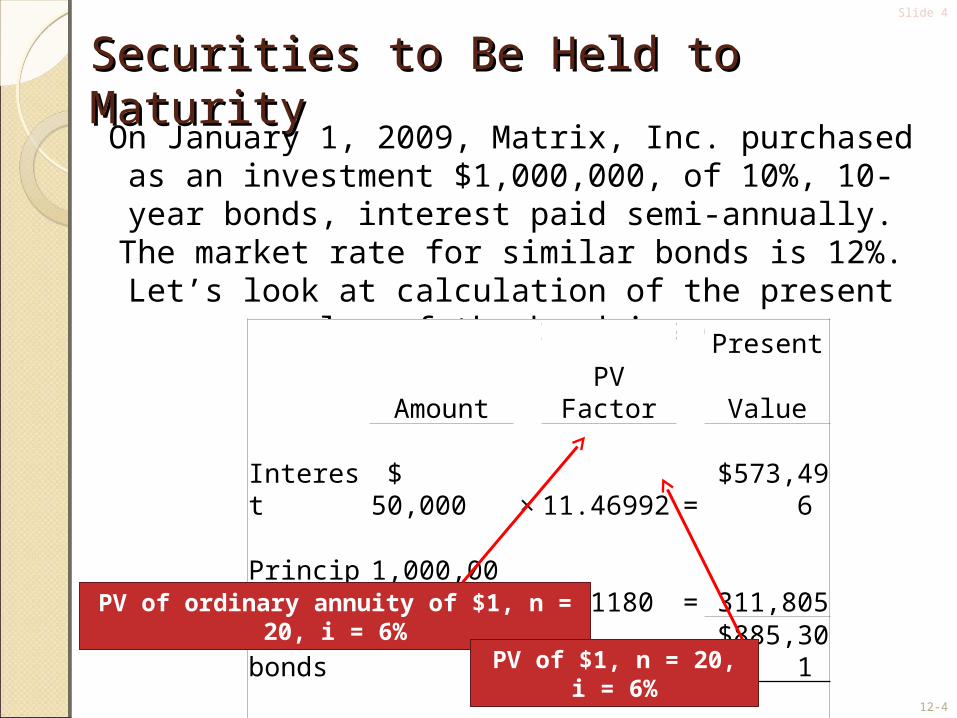

Securities to Be Held to MaturitySecurities to Be Held to MaturityOn January 1, 2009, Matrix, Inc. purchased as an

investment $1,000,000, of 10%, 10-year bonds, interest paid semi-annually. The market rate for similar bonds is 12%. Let’s look at calculation of the present value of the

bond issue.

Present Amount PV Factor Value Interest $ 50,000 × 11.46992 = $573,496 Principal 1,000,000 × 0.31180 = 311,805

Present value of bonds $885,301

PV of ordinary annuity of $1, n = 20, i = 6%

PV of $1, n = 20, i = 6%

Slide 5

12-5

Securities to Be Held to MaturitySecurities to Be Held to Maturity

PeriodInterest Payment

Interest Revenue

Discount Amortization

Unamortized Discount

Carrying Value

114,699 885,301

1 50,000 53,118 (3,118)

111,581

888,419

2

50,000

53,305 (3,305)

108,276

891,724

3

50,000

53,503 (3,503)

104,773

895,227

4

50,000

53,714 (3,714)

101,059

898,941

Partial Bond Amortization Table

Date Description Debit Credit1/1/09 Investment in bonds 1,000,000

Discount on bond investment 114,699 Cash 885,301

6/30/09 Cash 50,000 Discount on bond investment 3,118 Investment revenue 53,118

Slide 6

12-6

Securities to Be Held to MaturitySecurities to Be Held to Maturity

Investment in bonds 1,000,000$ Less: Discount on bond investment 111,581 Book value (amortized cost) 888,419$

$114,699 - $3,118 = $111,581 unamortized discount$114,699 - $3,118 = $111,581 unamortized discount

How would this investment appear on the balance sheet after one period of

discount amortization?

Slide 7

12-7

Securities to Be Held to MaturitySecurities to Be Held to MaturityOn December 31, 2009 after interest is received by

Matrix, all the bonds are sold for $900,000 cash.

Date Description Debit Credit12/31/09 Cash 50,000

Discount on bond invetment 3,305 Investment revenue 53,305

12/31/09 Cash 900,000 Discount on bonds investment 108,276 Investment in bonds 1,000,000 Gain on sale of investment 8,276

PeriodInterest Payment

Interest Revenue

Discount Amortization

Unamortized Discount

Carrying Value

114,699 885,301

1 50,000 53,118 (3,118)

111,581

888,419

2

50,000

53,305 (3,305)

108,276

891,724

3

50,000

53,503 (3,503)

104,773

895,227

4

50,000

53,714 (3,714)

101,059

898,941

Slide 8

12-8

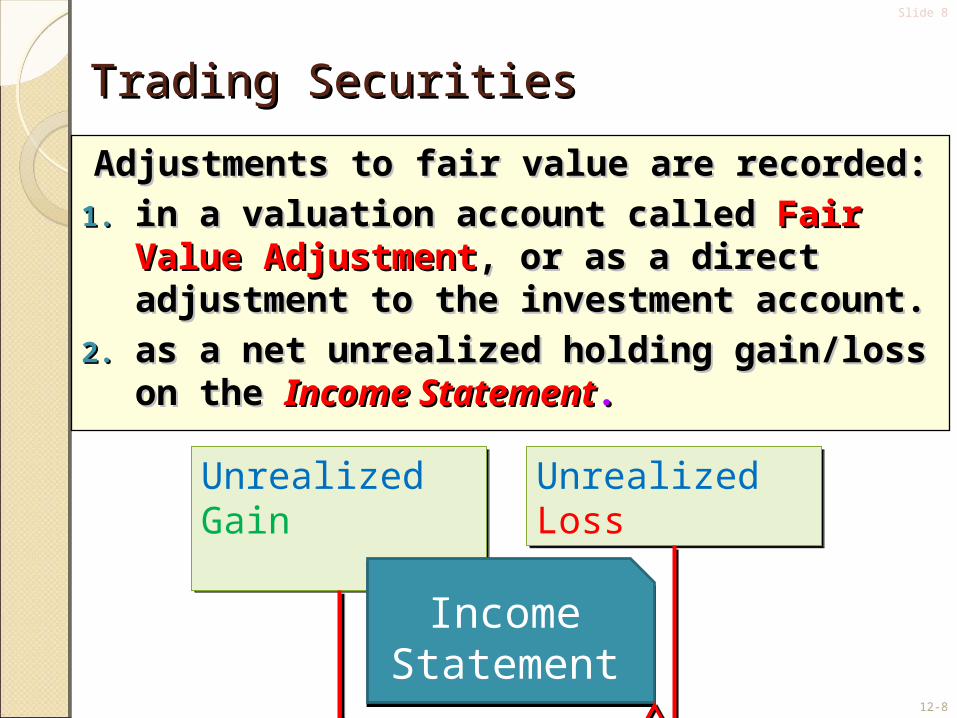

Trading SecuritiesTrading Securities

Adjustments to fair value are recorded:Adjustments to fair value are recorded:

1.1. in a valuation account called in a valuation account called Fair Value Fair Value AdjustmentAdjustment, or as a direct adjustment to the , or as a direct adjustment to the investment account.investment account.

2.2. as a net unrealized holding gain/loss on the as a net unrealized holding gain/loss on the Income StatementIncome Statement..

Unrealized Gain Unrealized Gain

Unrealized Loss Unrealized Loss

Income Statement

Income Statement

Slide 9

12-9

Trading Securities Trading Securities

Matrix, Inc. purchased additional securities classified as Matrix, Inc. purchased additional securities classified as Trading Securities (TS) at the end of 2009. The fair value Trading Securities (TS) at the end of 2009. The fair value amounts for these securities on December 31, 2009, are amounts for these securities on December 31, 2009, are

shown below. Prepare the journal entries for Matrix, Inc. to shown below. Prepare the journal entries for Matrix, Inc. to adjust the securities to fair value at 12/31/09.adjust the securities to fair value at 12/31/09.

No. of Unit Total Fair Gain orType Name Shares Cost Cost Value (Loss)TS Mining, Inc 1,000 42.00$ 42,000$ 41,000$ (1,000)$ TS Ford Motor 1,500 15.00 22,500 20,000 (2,500)

Net Unrealized Holding Loss for TS (3,500)$

Slide 10

12-10

Trading SecuritiesTrading Securities

The Net Unrealized Holding Loss is reported on the Income Statement.

The Net Unrealized Holding Loss is reported on the Income Statement.

Date Description Debit Credit12/31 Net unrealized holding gains and losses-IS 3,500

Fair value adjustment 3,500

Slide 11

12-11

Trading SecuritiesTrading Securities

Unrealized holding gains and losses from trading securities are reported on the income statement.

Slide 12

12-12

Trading SecuritiesTrading SecuritiesOn January 3, 2010, Matrix sold all trading

securities for $65,000 cash.

Date Description Debit Credit1/3/10 Cash 65,000

Investment in Ford Motor – TS 22,500 Investment in Mining, Inc. – TS 42,000 Gain on sale of investment 500

12/31/10 Fair value adjustment 3,500 Net unrealized holding gain or loss – I/S 3,500

Slide 13

12-13

Securities Available-for-SaleSecurities Available-for-Sale

Adjustments to fair value are recorded:Adjustments to fair value are recorded:

1.1. in a valuation account called in a valuation account called Fair Value AdjustmentFair Value Adjustment, , or as a direct adjustment to the investment account.or as a direct adjustment to the investment account.

2.2. as a net unrealized holding gain/loss in Other as a net unrealized holding gain/loss in Other Comprehensive Income (OCI), which accumulates in Comprehensive Income (OCI), which accumulates in Accumulated Other Comprehensive Income (ACOI).Accumulated Other Comprehensive Income (ACOI).

Unrealized Gain Unrealized Gain

Unrealized Loss Unrealized Loss

Other Comprehensive

Income

Other Comprehensive

Income

Slide 14

12-14

Other Comprehensive Income (OCI)Other Comprehensive Income (OCI)

Other comprehensive income:Foreign currency translation gains (losses) $ XX,XXXNet unrealized holding gains (losses) on investments -3,500Minimum pension liability adjustment XXXDeferred gains (losses) from derivatives XXX $ XX,XXXLess: aggregate income tax expense (benefit) X,XXX

Other comprehensive income $XX,XXX

When we add When we add other comprehensive incomeother comprehensive income to to net incomenet income we refer to the result as “comprehensive income.”we refer to the result as “comprehensive income.”

When we add When we add other comprehensive incomeother comprehensive income to to net incomenet income we refer to the result as “comprehensive income.”we refer to the result as “comprehensive income.”

Slide 15

12-15

Accumulated Other Comprehensive IncomeAccumulated Other Comprehensive Income

Unrealized holding gains and losses on Unrealized holding gains and losses on available-for-sale securities are accumulated in available-for-sale securities are accumulated in the shareholders’ equity section of the balance the shareholders’ equity section of the balance sheet. Specifically, the account is included in sheet. Specifically, the account is included in Accumulated Other Comprehensive IncomeAccumulated Other Comprehensive Income..

Unrealized holding gains and losses on Unrealized holding gains and losses on available-for-sale securities are accumulated in available-for-sale securities are accumulated in the shareholders’ equity section of the balance the shareholders’ equity section of the balance sheet. Specifically, the account is included in sheet. Specifically, the account is included in Accumulated Other Comprehensive IncomeAccumulated Other Comprehensive Income..

Shareholders’ EquityCommon StockPaid-in Capital in Excess of parAccumulated other comprehensive incomeRetained earningsTotal Shareholders’ Equity

Net unrealizedholding gains and losses.

Slide 16

12-16

Securities Available for Sale ExampleSecurities Available for Sale Example

Now assume the same facts for our Matrix, Inc. example, except that the investment is for

available-for-sale securities rather than trading securities.

Now assume the same facts for our Matrix, Inc. example, except that the investment is for

available-for-sale securities rather than trading securities.

No. of Unit Total Fair Gain orType Name Shares Cost Cost Value (Loss)AFS Mining, Inc 1,000 42.00$ 42,000$ 41,000$ (1,000)$ AFS Ford Motor 1,500 15.00 22,500 20,000 (2,500)

Net Unrealized Holding Loss for AFS (3,500)$

Slide 17

12-17

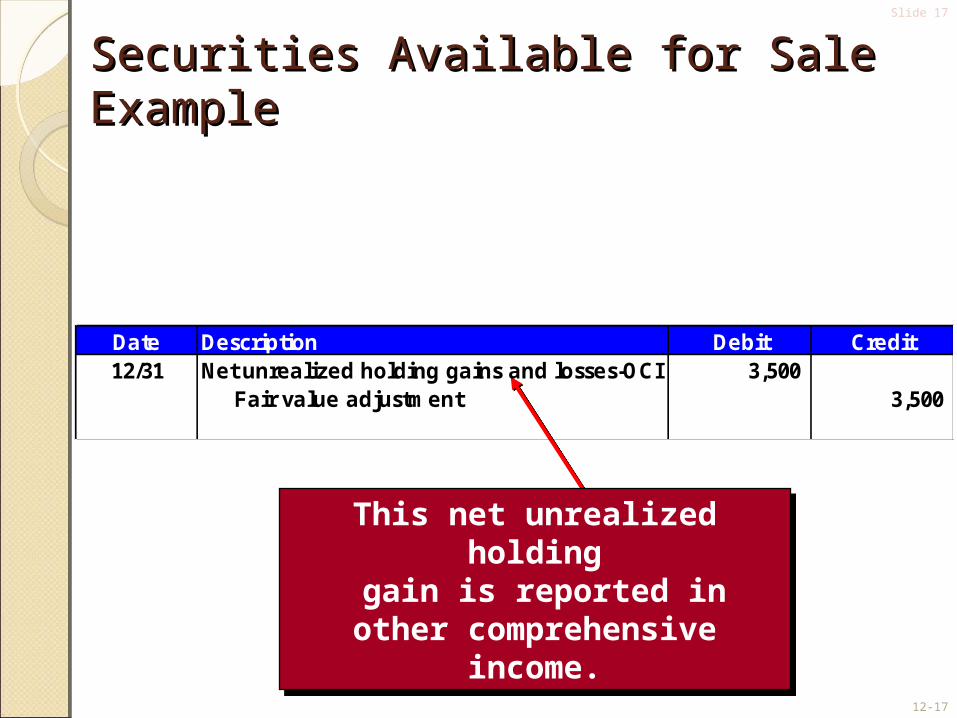

Securities Available for Sale ExampleSecurities Available for Sale Example

This net unrealized holding gain is reported in

other comprehensive income.

This net unrealized holding gain is reported in

other comprehensive income.

Date Description Debit Credit12/31 Net unrealized holding gains and losses-OCI 3,500

Fair value adjustment 3,500

Slide 18

12-18

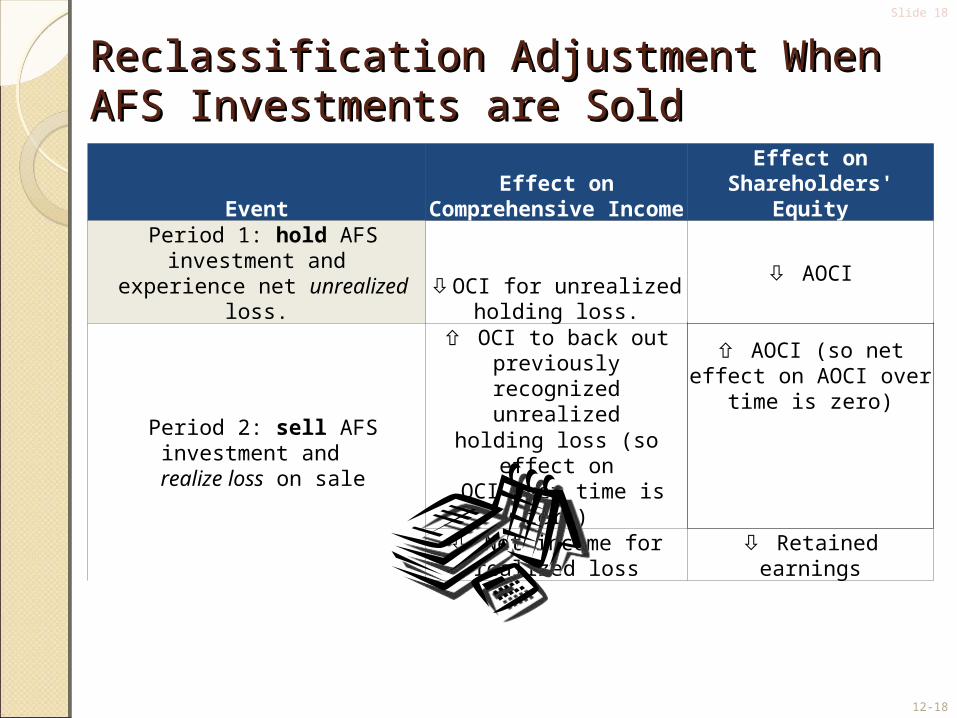

Reclassification Adjustment When AFS Reclassification Adjustment When AFS Investments are SoldInvestments are Sold

EventEffect on Comprehensive

IncomeEffect on Shareholders'

Equity Period 1: hold AFS investment and

experience net unrealized loss.OCI for unrealized holding

loss. AOCI

Period 2: sell AFS investment and realize loss on sale

OCI to back out previously recognized unrealized

AOCI (so net effect on AOCI over time is zero)

holding loss (so effect on OCI over time is zero)

Net income for realized loss Retained earnings

Slide 19

12-19

On January 3, 2010, Matrix sold all available-for-sale for $65,000 cash.

Date Description Debit Credit1/3/10 Cash 65,000

Investment in Ford Motor – TS 22,500 Investment in Mining, Inc. TS 42,000 Gain on sale of investment 500

12/31/10 Fair value adjustment 3,500 Net unrealized holding gain or loss – OCI 3,500

Securities Available for Sale ExampleSecurities Available for Sale Example

Slide 20

12-20

Other Than Temporary ImpairmentsOther Than Temporary Impairments

This is called an. . .Occasionally, an Occasionally, an

investment’s value will investment’s value will decline for reasons decline for reasons that are “other than that are “other than

temporary.”temporary.”

Impairment in Value

Slide 21

12-21

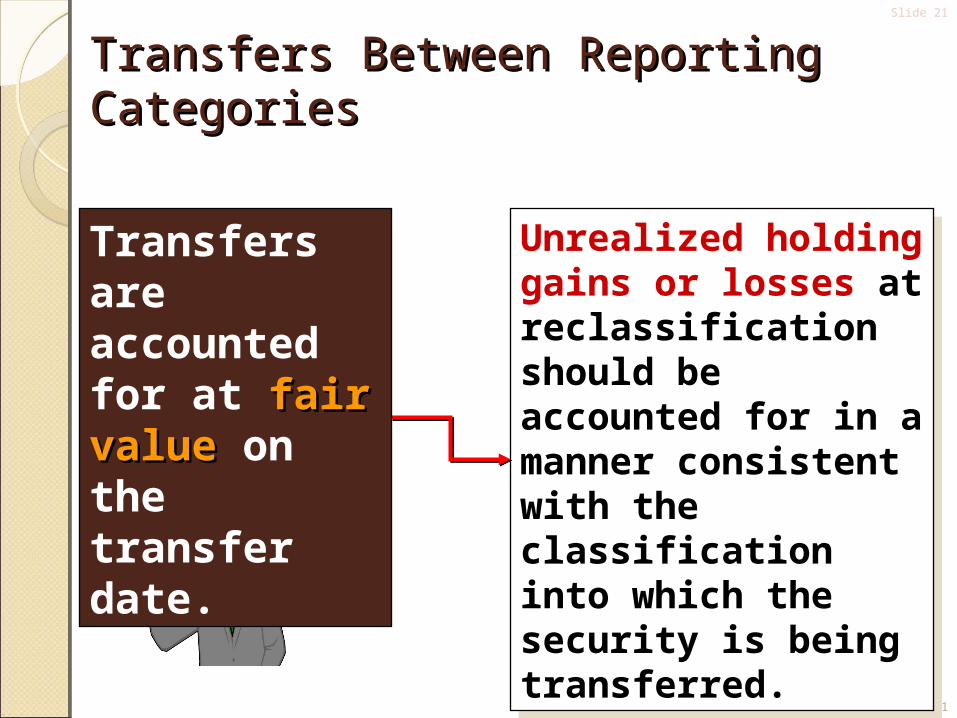

Transfers Between Reporting CategoriesTransfers Between Reporting Categories

Unrealized holding gains or losses at reclassification should be accounted for in a manner consistent with the classification into which the security is being transferred.

Unrealized holding gains or losses at reclassification should be accounted for in a manner consistent with the classification into which the security is being transferred.

Transfers are accounted for at fair valuefair value on the transfer date.

Slide 22

12-22

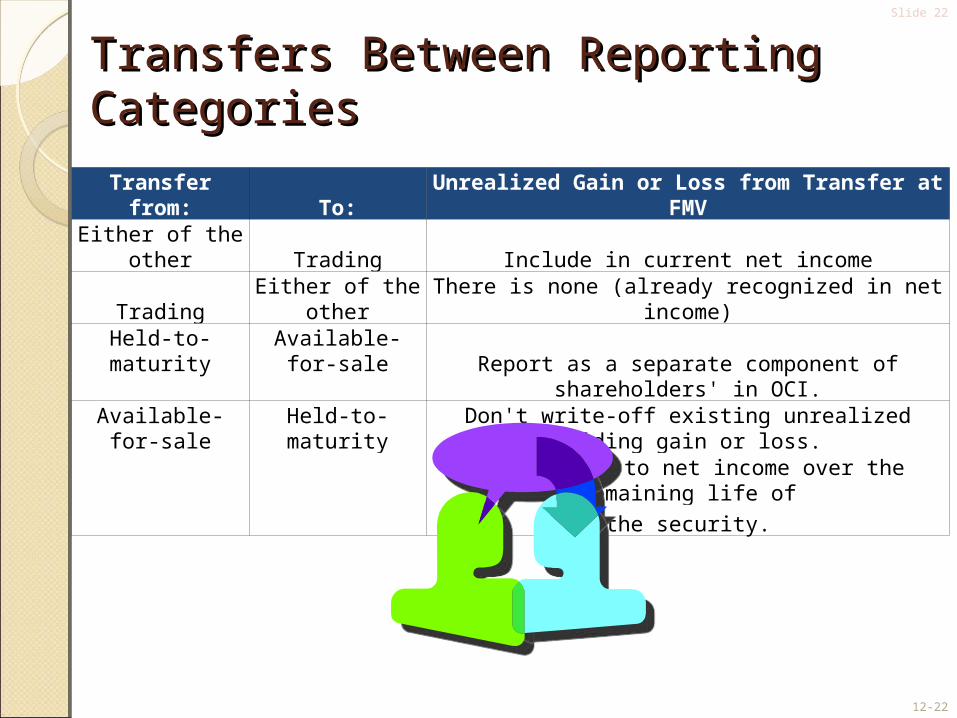

Transfers Between Reporting CategoriesTransfers Between Reporting Categories

Transfer from: To: Unrealized Gain or Loss from Transfer at FMVEither of the other Trading Include in current net income

Trading Either of the other There is none (already recognized in net income)Held-to-maturity Available-for-sale

Report as a separate component of shareholders' in OCI.Available-for-sale Held-to-maturity Don't write-off existing unrealized holding gain or loss.

Amortize it to net income over the remaining life of

the security.

Slide 23

12-23

DisclosuresDisclosures

Aggregate Fair ValueAggregate Fair Value

Maturities of debt securitiesMaturities of

debt securities

Change in net unrealized holding gains and losses

Change in net unrealized holding gains and losses

Gross realized & unrealized holding

gains & losses

Gross realized & unrealized holding

gains & losses

Amortized cost basis by major security type

Amortized cost basis by major security type

Inputs to fair value estimates

Inputs to fair value estimates

Slide 24

12-24

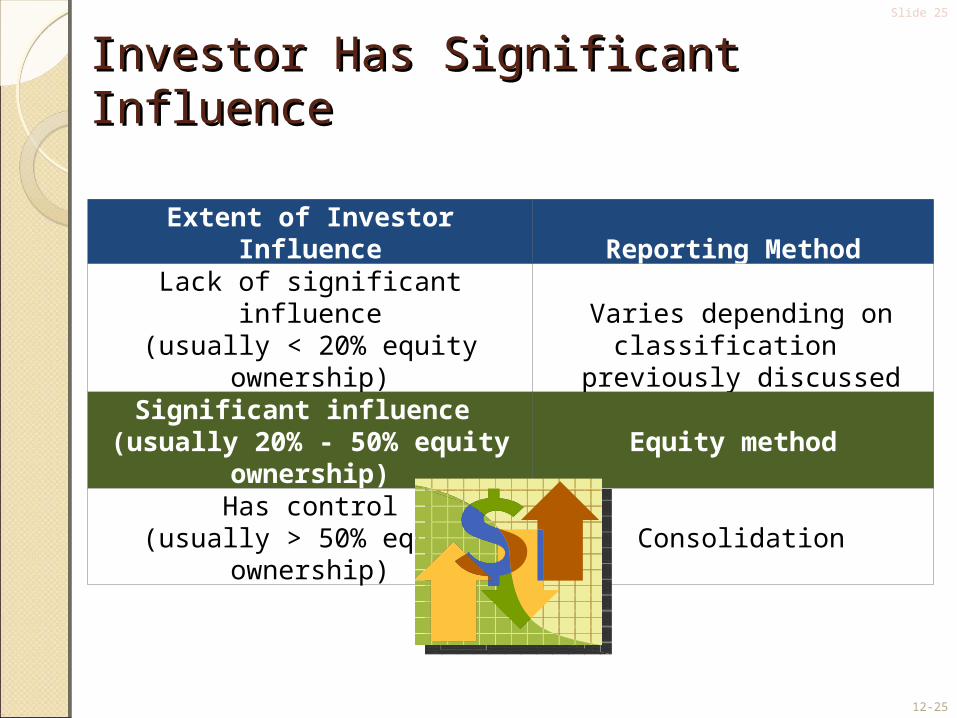

Investor Has Significant InfluenceInvestor Has Significant Influence

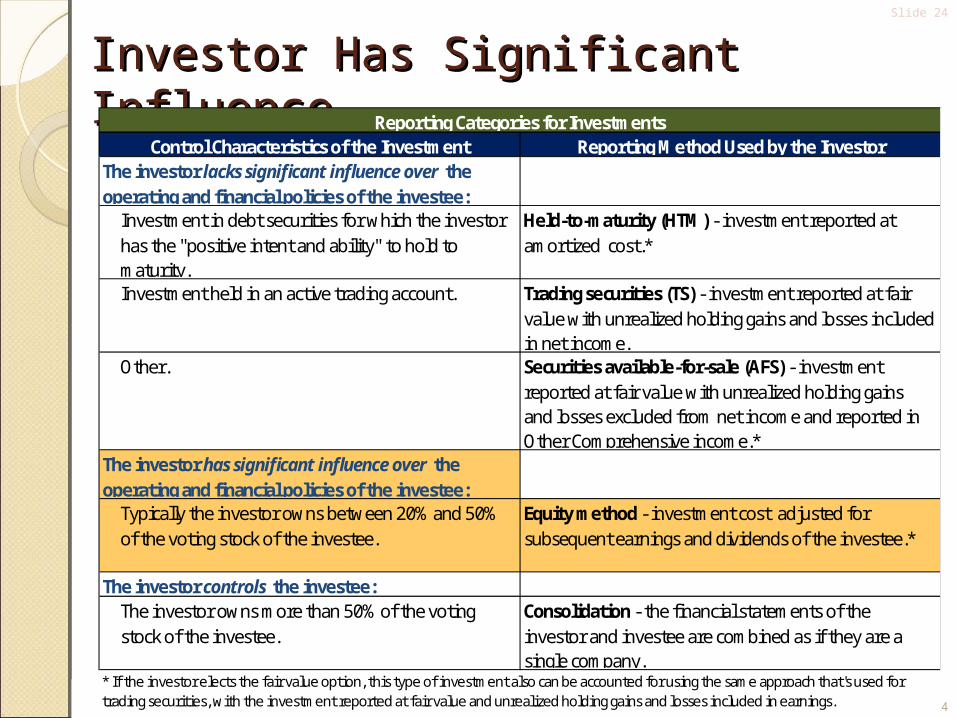

Control Characteristics of the Investment Reporting Method Used by the InvestorThe investor lacks significant influence over the operating and financial policies of the investee:

Investment in debt securities for which the investor has the "positive intent and ability" to hold to maturity.

Held-to-maturity (HTM) - investment reported at amortized cost.*

Investment held in an active trading account. Trading securities (TS) - investment reported at fair value with unrealized holding gains and losses included in net income.

Other. Securities available-for-sale (AFS) - investment reported at fair value with unrealized holding gains and losses excluded from net income and reported in Other Comprehensive income.*

The investor has significant influence over the operating and financial policies of the investee:

Typically the investor owns between 20% and 50% of the voting stock of the investee.

Equity method - investment cost adjusted for subsequent earnings and dividends of the investee.*

The investor controls the investee:The investor owns more than 50% of the voting stock of the investee.

Consolidation - the financial statements of the investor and investee are combined as if they are a single company.

Reporting Categories for Investments

* If the investor elects the fair value option, this type of investment also can be accounted for using the same approach that's used for trading securities, with the investment reported at fair value and unrealized holding gains and losses included in earnings.

Slide 25

12-25

Investor Has Significant InfluenceInvestor Has Significant Influence

Extent of Investor Influence Reporting MethodLack of significant influence

(usually < 20% equity ownership) Varies depending on classification

previously discussedSignificant influence

(usually 20% - 50% equity ownership) Equity method

Has control(usually > 50% equity ownership) Consolidation

Slide 26

12-26

What Is Significant Influence?What Is Significant Influence?If an investor owns 20% of the voting stock of an investee, If an investor owns 20% of the voting stock of an investee, it is presumed that the investor has significant influence it is presumed that the investor has significant influence over the financial and operating policies of the investee. over the financial and operating policies of the investee. The presumption can be overcome if :The presumption can be overcome if :1.1. the investee challenges the investor’s ability tothe investee challenges the investor’s ability to exercise significant influence through litigation or exercise significant influence through litigation or other methods. other methods.

2.2. the investor surrenders significant shareholder rights the investor surrenders significant shareholder rights in a signed agreement. in a signed agreement.

3.3. the investor is unable to acquire sufficient information the investor is unable to acquire sufficient information about the investee to apply the equity method. about the investee to apply the equity method.

4.4. the investor tries and fails to obtain representation on the investor tries and fails to obtain representation on the board of directors of the investee. the board of directors of the investee.

If an investor owns 20% of the voting stock of an investee, If an investor owns 20% of the voting stock of an investee, it is presumed that the investor has significant influence it is presumed that the investor has significant influence over the financial and operating policies of the investee. over the financial and operating policies of the investee. The presumption can be overcome if :The presumption can be overcome if :1.1. the investee challenges the investor’s ability tothe investee challenges the investor’s ability to exercise significant influence through litigation or exercise significant influence through litigation or other methods. other methods.

2.2. the investor surrenders significant shareholder rights the investor surrenders significant shareholder rights in a signed agreement. in a signed agreement.

3.3. the investor is unable to acquire sufficient information the investor is unable to acquire sufficient information about the investee to apply the equity method. about the investee to apply the equity method.

4.4. the investor tries and fails to obtain representation on the investor tries and fails to obtain representation on the board of directors of the investee. the board of directors of the investee.

Slide 27

12-27

Equity Method and ConsolidationEquity Method and ConsolidationIf a company acquires more than 50% of the voting stock If a company acquires more than 50% of the voting stock of another company:of another company:1.1. it controls the company acquired (cannot beit controls the company acquired (cannot be outvoted). The “parent” controls the “subsidiary.” outvoted). The “parent” controls the “subsidiary.”

2.2. for accounting purposes, the parent and subsidiary for accounting purposes, the parent and subsidiary are considered a single reporting entity. are considered a single reporting entity. Consolidated financial statements combine the Consolidated financial statements combine the separate financial statements of the parent and separate financial statements of the parent and subsidiary each period into a single aggregate set subsidiary each period into a single aggregate set of financial statements. of financial statements.

3.3. the equity method is sometimes referred to as a the equity method is sometimes referred to as a “one line consolidation,” because it shows the “one line consolidation,” because it shows the investor’s income and investment as increasing by investor’s income and investment as increasing by their portion of the investee’s income. their portion of the investee’s income.

If a company acquires more than 50% of the voting stock If a company acquires more than 50% of the voting stock of another company:of another company:1.1. it controls the company acquired (cannot beit controls the company acquired (cannot be outvoted). The “parent” controls the “subsidiary.” outvoted). The “parent” controls the “subsidiary.”

2.2. for accounting purposes, the parent and subsidiary for accounting purposes, the parent and subsidiary are considered a single reporting entity. are considered a single reporting entity. Consolidated financial statements combine the Consolidated financial statements combine the separate financial statements of the parent and separate financial statements of the parent and subsidiary each period into a single aggregate set subsidiary each period into a single aggregate set of financial statements. of financial statements.

3.3. the equity method is sometimes referred to as a the equity method is sometimes referred to as a “one line consolidation,” because it shows the “one line consolidation,” because it shows the investor’s income and investment as increasing by investor’s income and investment as increasing by their portion of the investee’s income. their portion of the investee’s income.

Slide 28

12-28

Equity MethodEquity Method

1. The investment account is increased increased by: Original investment cost. Proportionate share of investee's

earnings.

2. The investment account is decreaseddecreased by: Dividends received.

Slide 29

12-29

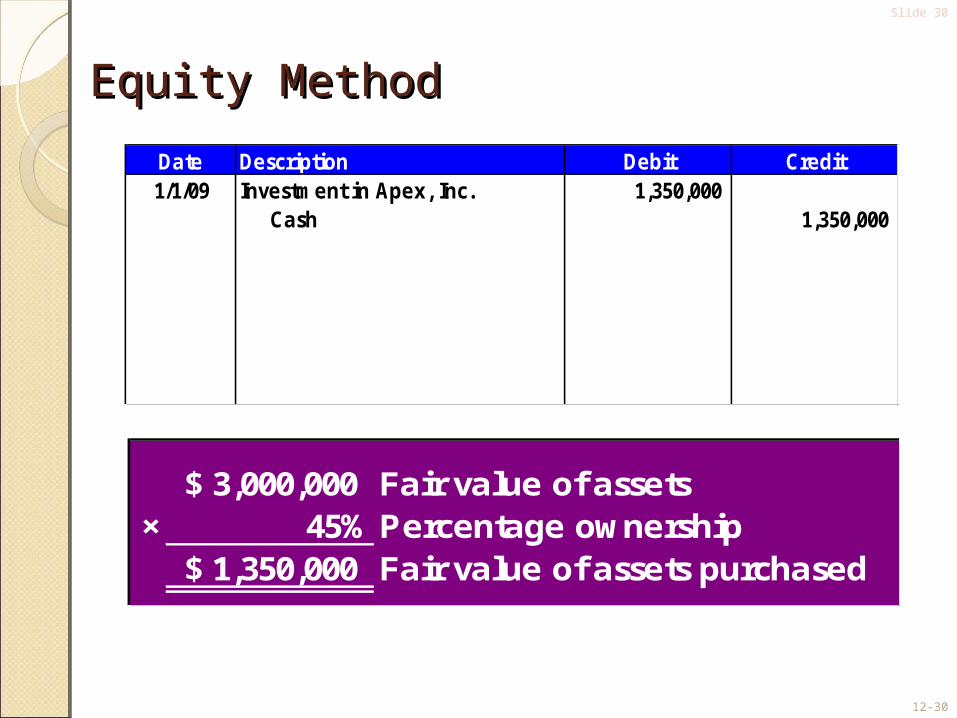

Equity Method Equity Method

On January 1, 2009, Matrix, Inc. acquired 45% of On January 1, 2009, Matrix, Inc. acquired 45% of the equity securities of Apex, Inc. for $1,350,000. the equity securities of Apex, Inc. for $1,350,000. On the acquisition date, Apex’s net assets had a On the acquisition date, Apex’s net assets had a fair value of $3,000,000. During 2009, Apex paid fair value of $3,000,000. During 2009, Apex paid

cash dividends of $150,000 and reported net cash dividends of $150,000 and reported net income of $1,750,000. income of $1,750,000.

What amount will Matrix, Inc. report on the balance sheet as Investment in Apex, Inc.?

Slide 30

12-30

Equity MethodEquity Method

Date Description Debit Credit1/1/09 Investment in Apex, Inc. 1,350,000

Cash 1,350,000

3,000,000$ Fair value of assets× 45% Percentage ownership

1,350,000$ Fair value of assets purchased

Slide 31

12-31

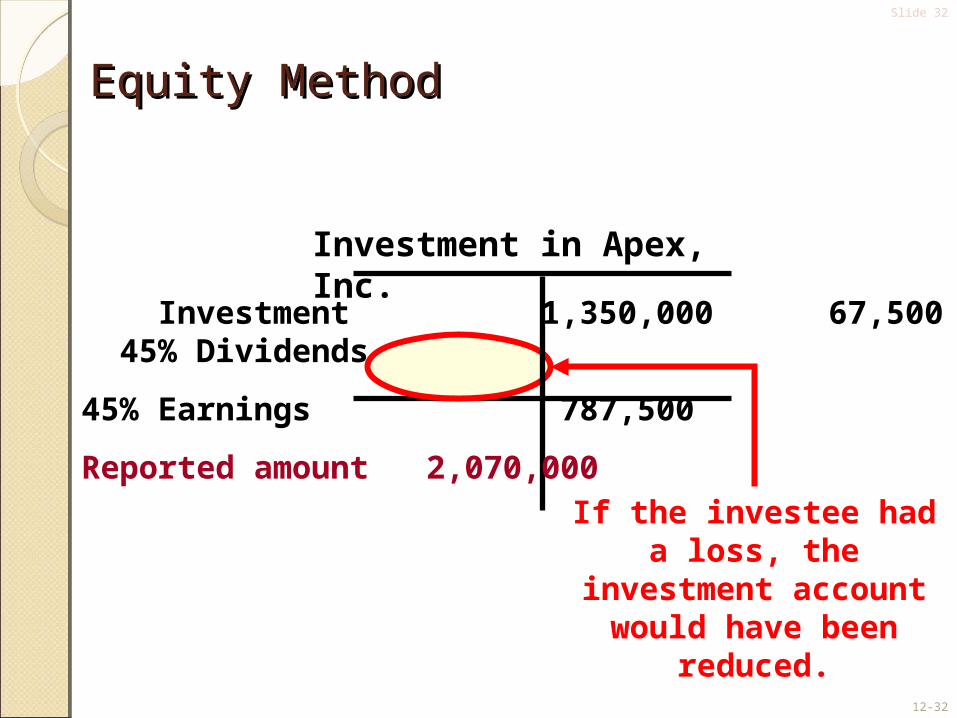

Equity MethodEquity Method

Date Description Debit Credit1/1/09 Investment in Apex, Inc. 1,350,000

Cash 1,350,000

12/31/09 Cash 67,500 Investment in Apex, Inc. 67,500

Investment in Apex, Inc. 787,500 Investment revenue 787,500

150,000$ Dividends paid× 45% Percentage ownership

67,500$ Share of dividends

1,750,000$ Reported earnings× 45% Percentage ownership

787,500$ Share of earnings

Slide 32

12-32

Equity MethodEquity Method

Investment in Apex, Inc.

Investment 1,350,000 67,500 45% Dividends

45% Earnings 787,500

Reported amount 2,070,000

If the investee had a loss, the investment account

would have been reduced.

Slide 33

12-33

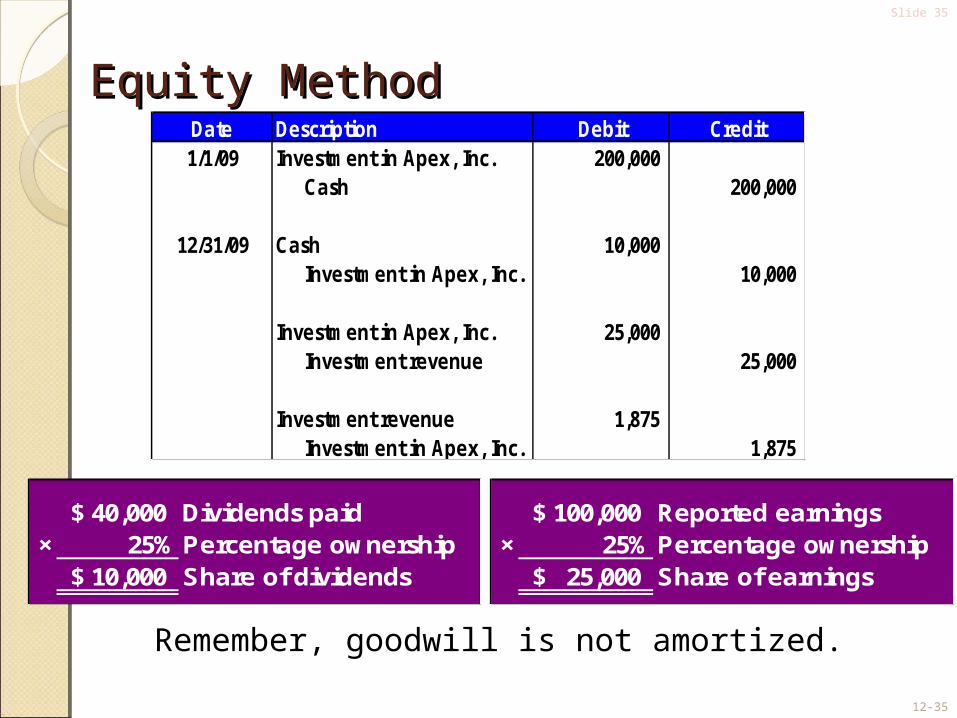

Equity MethodEquity MethodOn January 1, 2009, Matrix, Inc. purchase 25% of the

common stock of Apex, Inc. for $180,000. At the date of acquisition, the book value of the net assets of Apex was

$400,000, and the net fair value of these assets is $600,000. During 2009, Apex paid cash dividends of $40,000, and

reported earnings of $100,000.

Fair value of assets 600,000$ Percentage ownership 25%Share of fair value of assets 150,000 Cost of investment in Apex 180,000 Excess of cost over fair value 30,000$

Slide 34

12-34

Equity MethodEquity MethodAssume that of the $50,000 excess of the fair value of net

assets acquired ($600,000 × 25% = $150,000) over the book value of those net assets on Apex’s balance sheet ($400,000 × 25% = $100,000), 75% is attributable to depreciable assets

with a remaining life of 20 years and the remainder is attributable to land. Matrix uses the straight-line method of

depreciation on similar owned assets.

Excess of cost over fair value 50,000$ Amount applicable to depreciable assets 75%Share subject to excess depreciation 37,500 Remaining useful life of assets in years 20 Additional depreciation expense 1,875$

Slide 35

12-35

Equity MethodEquity MethodDate Description Debit Credit1/1/09 Investment in Apex, Inc. 200,000

Cash 200,000

12/31/09 Cash 10,000 Investment in Apex, Inc. 10,000

Investment in Apex, Inc. 25,000 Investment revenue 25,000

Investment revenue 1,875 Investment in Apex, Inc. 1,875

40,000$ Dividends paid× 25% Percentage ownership

10,000$ Share of dividends

100,000$ Reported earnings× 25% Percentage ownership

25,000$ Share of earnings

Remember, goodwill is not amortized.

Slide 36

12-36

Changing From the Equity Method to Changing From the Equity Method to Another MethodAnother Method

At the transfer date, the carrying value of the investment under the equity

method is regarded as cost.

At the transfer date, the carrying value of the investment under the equity

method is regarded as cost.

When the investor’s level of influence changes, it may be necessary to change from the equity

method to another method.

Slide 37

12-37

Changing From the Equity Method to Changing From the Equity Method to Another MethodAnother Method

Any difference between carrying value and fair value is recorded in a valuation account and is

recognized as an unrealized holding gain or loss.

After the transfer, the investment is treated as a trading security or a security available for sale,

depending on management’s intent.

Slide 38

12-38

Changing From Another Method to the Changing From Another Method to the Equity MethodEquity Method

When the investor’s ownership level increases to the point where they can exert significant influence, the

investor should change to the equity method.

At the transfer date, the recorded value is the initial cost of the investment adjusted for the investor’s

equity in the undistributed earnings of the investee since the original investment.

Reported earnings– Dividends paid= Undistributed Earnings

Slide 39

12-39

Changing From Another Method to the Changing From Another Method to the Equity MethodEquity Method

The original cost, the unrealized holding The original cost, the unrealized holding gain or loss, and the valuation account gain or loss, and the valuation account

are closed.are closed.

A A retroactiveretroactive change is recorded to change is recorded to recognize the investor’s share of the recognize the investor’s share of the investee’s earnings since the original investee’s earnings since the original

investment.investment.

The original cost, the unrealized holding The original cost, the unrealized holding gain or loss, and the valuation account gain or loss, and the valuation account

are closed.are closed.

A A retroactiveretroactive change is recorded to change is recorded to recognize the investor’s share of the recognize the investor’s share of the investee’s earnings since the original investee’s earnings since the original

investment.investment.

Slide 40

12-40

Fair Value OptionFair Value OptionSFAS No. 159 allows companies to use a “fair value option” SFAS No. 159 allows companies to use a “fair value option” for HTM, AFS and equity method investments.for HTM, AFS and equity method investments.

The investment is carried at fair value.The investment is carried at fair value.Unrealized gains and losses are included in income.Unrealized gains and losses are included in income.

For HTM and AFS investments, this just amounts to For HTM and AFS investments, this just amounts to classifying the investments as trading.classifying the investments as trading.

For equity-method investments, the investment is still For equity-method investments, the investment is still classified on the balance sheet with equity method classified on the balance sheet with equity method investments, but the portion at fair value must be clearly investments, but the portion at fair value must be clearly indicated.indicated.

The fair value option is determined for each individual The fair value option is determined for each individual investment, and is irrevocable.investment, and is irrevocable.

SFAS No. 159 allows companies to use a “fair value option” SFAS No. 159 allows companies to use a “fair value option” for HTM, AFS and equity method investments.for HTM, AFS and equity method investments.

The investment is carried at fair value.The investment is carried at fair value.Unrealized gains and losses are included in income.Unrealized gains and losses are included in income.

For HTM and AFS investments, this just amounts to For HTM and AFS investments, this just amounts to classifying the investments as trading.classifying the investments as trading.

For equity-method investments, the investment is still For equity-method investments, the investment is still classified on the balance sheet with equity method classified on the balance sheet with equity method investments, but the portion at fair value must be clearly investments, but the portion at fair value must be clearly indicated.indicated.

The fair value option is determined for each individual The fair value option is determined for each individual investment, and is irrevocable.investment, and is irrevocable.

Slide 41

12-41

Financial Instruments & DerivativesFinancial Instruments & Derivatives

Financial Instruments:

1.1. Cash.Cash.

2.2. Evidence of an Evidence of an ownership interestownership interest in an entity.in an entity.

3.3. Contracts meeting Contracts meeting certain conditions.certain conditions.

Financial Instruments:

1.1. Cash.Cash.

2.2. Evidence of an Evidence of an ownership interestownership interest in an entity.in an entity.

3.3. Contracts meeting Contracts meeting certain conditions.certain conditions.

Derivatives:Derivatives:1.1. Value is derived from Value is derived from

other securities.other securities.

2.2. Derivatives are often Derivatives are often used to “hedge” used to “hedge” (offset) risks created (offset) risks created by other investments by other investments or transactionsor transactions

Derivatives:Derivatives:1.1. Value is derived from Value is derived from

other securities.other securities.

2.2. Derivatives are often Derivatives are often used to “hedge” used to “hedge” (offset) risks created (offset) risks created by other investments by other investments or transactionsor transactions

Slide 42

12-42

Other Investments – Appendix AOther Investments – Appendix A

It is often convenient for companies to set aside money to be used for specific purposes. In the short-term, funds may be set aside for

1. Petty cash funds.

2. Payroll accounts.

In the long-run, funds are often set aside to:

1. Pay long-term debt when it comes due.

2. Acquire treasury stock.

Special purpose funds set aside for the long-term are classified as investments.

Slide 43

12-43

Appendix 12A – Other InvestmentsAppendix 12A – Other InvestmentsIt is a common practice for companies to purchase

life insurance policies on key officers. The company pays the premium and is the beneficiary

of the policy. If the officer dies, the company receives the proceeds from the policy. Some types of policies build a portion of each premium as cash surrender value. The cash surrender value of such

a policy is classified as an investment on the balance sheet of the company.

Slide 44

12-44

Appendix 12B – Impairment of a Receivable Due Appendix 12B – Impairment of a Receivable Due to a Troubled Debt Restructuringto a Troubled Debt Restructuring

When the original terms of a debt agreement are changed as a result of financial difficulties

experienced by the debtor, the new arrangement is referred to as a troubled debt restructuringtroubled debt restructuring.

Sometimes a troubled debt is settled in full when the debtor transfers assets or equities to the creditor. The creditor usually recognizes a loss on the settlement.

Such a settlement is not considered unusual or infrequent and is not an extraordinary item.

McGraw-Hill /Irwin © 2009 The McGraw-Hill Companies, Inc.

End of Chapter 12End of Chapter 12