Document Number PD009.1 1 Core Portal Pension & Personnel Self-Service Information Session.

McGill University Pension PlanGeneral Information Session

The presentation can be accessed in online at: http://www.mcgill.ca/hr/pensions/mupp/sessions .

This presentation is intended to inform you about the McGill Pension Plan & the importance of integrating pension investment decisions to your financial management.

This is not financial advice & should not be taken as such. It is meant to alert you to the matters to look into.

Your individual needs & circumstances may not be adequately addressed by the info contained in this presentation.

2

Learning Objectives

Understand the design of the McGill University Pension Plan

Familiarize yourself with investment basics

Understand the importance of developing a personal investment strategy

Learn where to get more information

3

Canadians need 60% to 70% income replacement in

retirement.

Only 50% of Canadian have access to a pension plan.

4

Why have a pension plan?

Why save for retirement?

30 40 50

20 60 70 80 90Career Begins Current AverageAge 23 Retirement Age 61

Current Life Expectancy of a 60‐year‐old:MALE = age 86.9 increasing to age 94.5FEMALE = age 88.9 increasing to age 95.5

5

35+ working years 25+ years inretirement

Projected Life Expectancy6

Source: CPM2014 Publ Improvement Scale B

86

87

88

89

90

91

92

93

94

95

96

60 65 70 75 80 85 90

Average Lif

e Expe

ctan

cy

Male FemaleAge

Maximum Recorded Life Expectancy: 122 years – Jeanne Calment (France)

Aver

age

Life

Exp

ecta

ncy

How much will I need at retirement?

Final Salary70%

replacement Years RetiredAmount Needed

$50,000 $35,000 20 $700,00025 $875,00030 $1,050,000

$75,000 $52,500 20 $1,050,00025 $1,312,50030 $1,575,000

7

Assumption: Indexed and Rate of Return = 2.5%

8

Building your

Retirement McGill University Savings Program• MUPP (49%)*• GRSP• GTFSA

Government Programs• Quebec Pension Plan (24%)• Old Age Security (12%)

Personal Savings• RRSP• TFSA

* based on a pre‐retirement income of $58,700 at age 65, annualized rate of return of 5.5% and interest rate assumption of 5.0% at settlement.

Where your retirement income comes from

Types of Pension Plans

• Pension is based on a formula tied to service & salary

DefinedBenefit

• Retirement income is based on contributions, the investment return accumulated at retirement as well as market conditions

Defined Contribution

9

McGill University Pension Plan

• Applies to members who became eligible to join on or after January 1, 2009

• Referred to as “Part B” of MUPP

Defined Contribution

(Part B)

• Applies to members who joined prior to January 1, 2009

• Defined Contribution + Defined Benefit = Hybrid

• Referred to as “Part A” of MUPP

Hybrid (Part A)

10

Who can join the MUPP?

11

Full‐Time Employees:• Join at hire or at the start of any pay period• Mandatory participation after 5 years

Part‐Time Employees: may join at the beginning of any pay period in the year following the one in which they:• Completed 700 or more hours of employment• Earned more than 35% of the Year’s Maximum Pensionable Earnings (YMPE) limit $20,090 in 2019 to join in 2020; $20,545 in 2020 to join in 2021)

MUPP ContributionsYou Part A & B Part A Only*

Age 39 or less 5.0% +1.9%

Age 40 to 49 7.0% +1.9%

Age 50 to 65 8.0% +1.9%

(less 1.8% up to the QPP earnings limit (YMPE))

University Part A & B Part A Only*

Age 39 or less 5.0% ‐1.9%

Age 40 to 49 7.5% ‐1.9%

Age 50 to 65 10.0% ‐1.9%

(less 1.8% up to the QPP earnings limits (YMPE))

12

• QPP earnings limit (2021) = $61,600 ‐ $3,500 basic exemption• Maximum contributions (2021) = lesser of 18% of earnings or $29,210* University directs contributions towards defined benefit segment. 1.9% effective – September 2018

$1500After tax pay

($500)Less tax –(25%)

($0)Contribution

$2,000Gross pay

No contributionAge < 40 (Part B)

$1452

($484)

$2,000

Contribution

($64)

‐ $48

What does it really cost (Part B)?Pension contributions deducted before taxImmediate tax savings

13

Total investment = $128 (University $64 + Employee $64 for a change in net pay of only $48.

$2000Taxable Pay $1936

What is the cost of waiting to join?(projected DC balance at age 65)

Wait 5

yea

rs

Wait 1

yea

r

STAR

T NOW

$758,000$717,500Cost of Waiting = $40,500

$575,000Cost of Waiting = $183,000

14

Assumptions:• Current contribution rates• Age 30, earning $35,000• Retirement at age 65• Salary Increase of 3%• Investment Return of 5%

Enrollment…15

To join (MUPP, RRSP, TFSA) – use Workday (www.mcgill.ca/hr) • At hire: During onboarding, waive or elect any of the Retirement Savings Plans • After hire: Use Change Benefits ‐ Pension Opt In; GRSP Opt In; TFSA Opt In• For GRSP/TFSA – select contributions on a per‐pay basis

On mysunlife.ca (MUPP, RRSP & TFSA)• Asset allocation tool‐ Investment selection • Beneficiary designation• View• Account balances, including defined benefit (Part A), personal & fund rates of return• Use• Retirement planner etc.…

16

mysunlife.ca

17

How do I make my investment selection? On mysunlife.ca: my financial centre > Requests > Change Investments

18

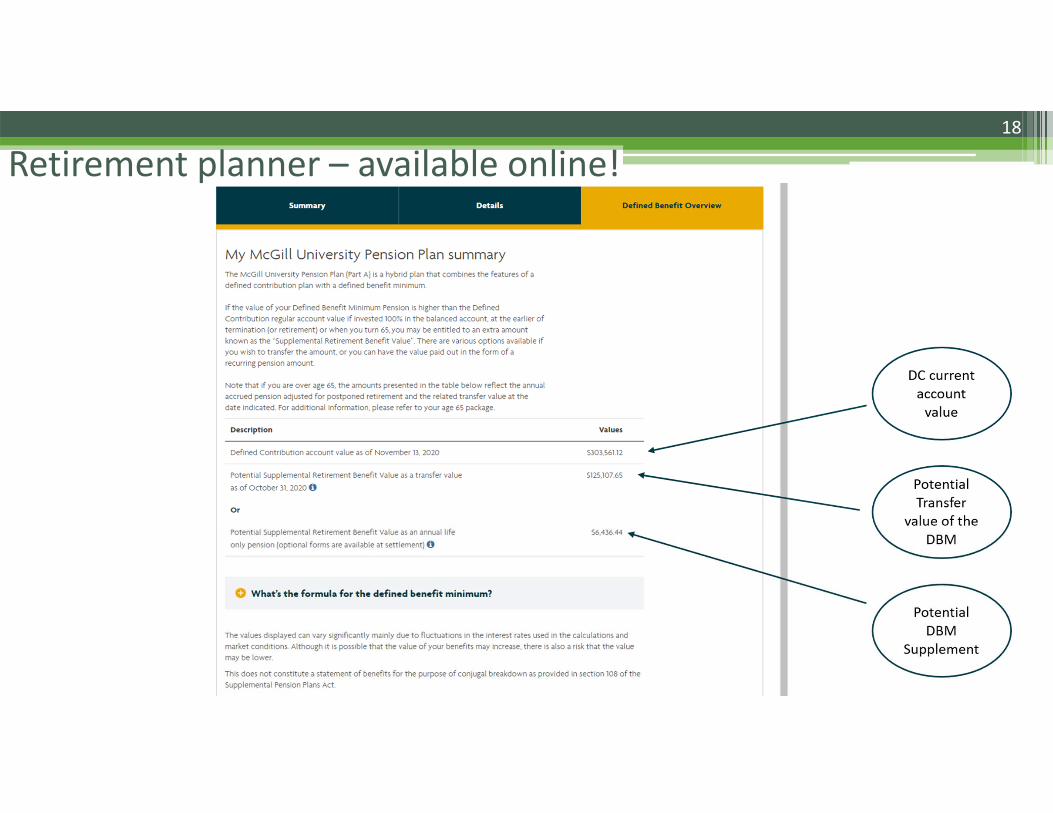

Retirement planner – available online!

19

Steps in Investment Planning20

Investor Profile

Investment Goals

Asset Allocation

Investment Decisions

Monitoring

Source: Investor Education Fund – www.getsmarteraboutmoney.ca

Completing the asset allocation toolFactors to consider: Age Net Worth Years before retirement Personal Situation Liquidity Requirements Risk Tolerance (ability/willingness/need) Investment Objectives Investment Knowledge mysunlife.ca >my financial centre >Tools & services > my money tools> Asset

Allocation toolMembers are advised to seek advice regarding their particular circumstances from a personal financial advisor.

21

22

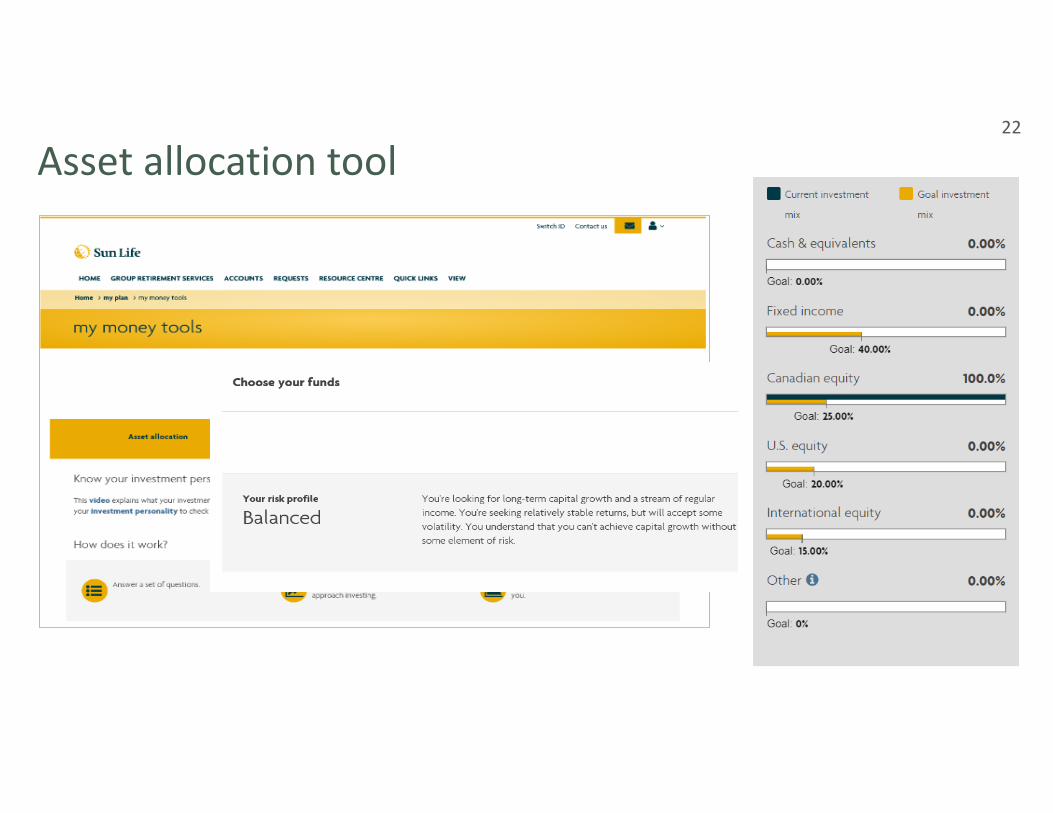

Asset allocation tool

23

What is your risk tolerance?

WILLINGNESSto take on risk

ABILITYto take on risk

NEEDto take on risk

Most investor profile questionnaires are tailored to assess willingness and focus on the accumulation phase.

24

RISK

RET

UR

N

90% of return derived from asset allocation Does the investment suit your investor profile,

needs & objectives? Do you understand the investment & inherent risks? What is the historical performance & future

outlook? What conditions will impact its performance? What are the associated fees/costs?

Investment selection25

Setting your personal investment strategy

How much income will I need at retirement?

How much $ do I have to work with?

What rate of return do I need to get to my goal?

What rate of additional savings do I need to make to achieve my retirement goals?

26

Some degree of risk is always present

Actual returns vs. expected rate of return Frequency of negative deviations Short‐term volatility Inflation risk (loss of purchasing power) Credit risk Impact of changes in interest rates Assess risk against your objectives

27

What is risk?

Different asset classes have differing investment return expectations

Results depend on length of time horizon for the investment

Minimize overall risk of your portfolio

28

Why diversify?

29

Early Earning Years

Mid Earning Years

Peak Earning Years

Retirement Years

•Growth

Age35 55 65

Net

Wor

th

Investment Objectives

•Growth

•Tax Minimization•Safety •Safety

•Income

•Concern for inflation protection

Retirement Planning Estate Planning

Life Cycle AnalysisCaution: Your individual situation may differ significantly

35 55 65Age

3 Major Asset Classes30

• Short‐term financial obligations issued by governments & corporations• Lowest expected returns & least volatile• e.g. Treasury bills

Money Market Securities

• Debt instruments issued by governments & corporations paying a rate of interest with terms up to 30 years

• Lower expected returns & less volatile• e.g. bonds

Fixed Income Securities

• Ownership in companies in & outside of Canada• Higher expected returns & most volatile• e.g. stocks

Equities

31

MUPP’S Investment Options

*Formally Called Glide Path

Equity Pool Fixed Income Pool

Balanced Accouunt + Alternatives Investments (default funds)

Money Market Pool

Socially Responsible

Investment Pool

Multi‐Risk Target Date Funds*

33

MUPP Multi‐Risk Target date funds

Refer to the Morningstar Investment profile Sheets for current asset allocation and past returns on mysunlife.ca > my financial centre > Accounts > Investment performance

34

Refer to the Morningstar Investment profile Sheets on mysunlife.ca: my financial centre > Accounts > Investment performance

Investment performance

•Compare funds•Get historical rates of return• Learn about fund objectives

• Morningstar ® investment profile sheets

You’ll need your sign‐in ID and password

Money Market Pool Fixed Income Pool Equity Pool Balanced Account Alternative Assets (Balanced Account & Multi‐Risk Target date Only)

SRI Pool McGill RRSP/TFSA/LIRA/LIF/RRIF

* Estimated 2021 fees include investment management, actuarial, custodial fees and administrative expenses. Actual expenses may vary over time.

0.18%

0.50%

0.64%

1.00%

2.34%

35

Compare Fees – Funds Management Fees* (FMF)

0.31%

0.21 – 0.36%

Balanced Account: 20%Equity Pool: 20%Fixed Income Pool: 20%SRI: 20%Money Market Pool: 20%

36

Spot the problem….

Do not set goals & plan Procrastinate in starting to save Do not save enough Do not understand risk Do not understand asset classes & asset allocation Are confused by choice in investment options Chase past returns Do not review & follow‐up

37

Common Mistakes

Understand the decisions that you need to make

Select investment option(s) which are right for you

Review • investment returns• changing circumstances

38

Your investment responsibility

Change drivers: Life events – personal & professional Change in financial situation

• Sale/purchase home• Spouse starts/stops working• Inheritance……

Market conditions• Inflation, abnormal volatility, corrections……

39

When do I re‐evaluate risk & investment strategy

Short‐term trading:A 2% fee may be charged,when you move money into afund followed by a move out ofthe same fund within 30 days

40

How do I change my investment allocation On mysunlife.ca: my financial centre > Requests > Change Investments

Choosing your beneficiary41

Designation is subject to the prior rights of the spouse, if any

Spouse: Married, civil union or Conjugal relationship (same or opposite sex) i. 3 years or, ii. 1 year if at least one child

Spousal waiver (available from HR website – www.mcgill.ca/hr/forms)

Designation of married or civil union Spouse will lapse in the event of: divorce, annulment of marriage or civil union. If not married nor in civil union, a cessation of conjugal relationship may affect your spouse’s entitlement.

Revocable/irrevocable status

No spouse: appoint anyone

To make changes: online via Sun Life at: http://www.mcgill.ca/hr/pensions/mupp/mupp‐loginmysunlife.ca > my financial centre > Quick Links > Beneficiary info

RRSP Transfers In to the MUPP

AdvantagesAccess to MUPP investment fund options Funds Management Fees on MUPP investment funds DisadvantagesNo access to funds prior to retirement/terminationNo Home Buyers’ Plan & Lifelong Learning Plan withdrawals permitted Limited investment fund options Fees may be levied by transferring institution

Consider the Voluntary Savings Plan (Group RSP / Group Spousal RRSP)

42

43

Record Keeping Fees (Sep 2020 – Aug 2021)

Part A Member & VB Part B Member & VB VSP (RRSP/LIRA/TFSA) Group LIF/RRIF VSP Cheque Issuance

* Record keeping fees will be charged directly to your account on a monthly basis. Annual indexation will also apply.

$157.52/per annum

$97.93/per annum

$60.00/per annum

$60.00/per annum

$25.00/per payment

Immediate Vesting• 100% of contributions (University & employee

belong to you)

Account value plus Supplementary Pension amount (Part A only), if any

Subject to locking‐in provisions

Small Account Balance – less than 20% of the YMPE in the year of termination

What happens if I leave McGill?

44

Pension Plan Brochures (http://www.mcgill.ca/hr/pensions/mupp)

Annual Report and Financial Statements

McGill University Savings Programs: • Web Site: http://www.mcgill.ca/hr/pensions/mupp

• Video capsules• Information sessions Retirement, Settlement Options, Decumulation, Voluntary Savings Plan

Sun Life:• Web Site: mysunlife.ca• Customer Care Centre: 1‐888‐444‐2023

Independent investment advisor or financial planner

Where can I get more information?

45