R MoeserCorrelator f2f Meeting1 MCAF (Metadata Capture and Formatting) Rich Moeser.

MCAF LTD - ANNUAL REPORT 2019

1

CONTENTS

THE FEDERATION 2 THE CHAIRMAN’S REPORT 4 BOARD OF DIRECTORS 2019-2020 AND OTHER SUBCOMMITTEES 8

LIST OF STAFF 12

REPORT OF THE BOARD OF DIRECTORS 16

MEMBERSHIP 18

THE MOUNT AND BEAU PLAN PLANTERS FUNDS 18

ACCOUNTS 19

ACTIVITIES 21

MISSION OVERSEAS 22

CROP 2018 23

ACKNOWLEDGEMENTS 26

APPROPRIATION OF SURPLUS FOR THE YEAR 2018/2019 27 AUDITED FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2019 29

MCAF LTD - ANNUAL REPORT 2019

2

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LTD

THE FEDERATION

Registered as a secondary Co-opera�ve Society in August 1950, The Mauri�us Co-opera�ve

Agricultural Federa�on Ltd (MCAF Ltd) was founded to act as the spokesman of small sugar

cane planters who were facing a lot of problems, which they could not solve or discuss neither

individually nor at a level of primary socie�es, that is, Coopera�ve Credit Socie�es (CCS).

The Federa�on currently regroups 155 Co-opera�ve Credit Socie�es with a total membership

of 7,345 small sugar cane planters, who are cul�va�ng approximately 7,400 hectares of land

and producing a total of 33,733 Tons of sugar for the crop 2018. Planters opera�ng under CCS’

consist of 57% of the total number of sugarcane planters Island wide represented by 12,884

planters.

The MCAF Ltd has, in its quest to provide a be�er service to the plan�ng community,

established a network of thirteen sales points across the island to provide a wide range of agri-

inputs to cater for the needs of planters of all regions.

The Federa�on will shortly launch its Seedling Produc�on Unit situated at La Marie- Henrie�a,

to cater for the needs of vegetable planters in terms of high quality vegetable seedlings which

will be sold at a compe��ve price.

OUR VISION

The most valued organiza�on in increasing agricultural produc�vity ethically .

OUR MISSION

To promote the interests of Coopera�ve Credit Socie�es and member-planters by providing

them with necessary support services, facili�es and incen�ves to encourage their contribu�ons

in making the business of agriculture viable, in a socially responsible manner.

MCAF LTD - ANNUAL REPORT 2019

3

THE CHAIRMAN’S REPORT

Mr. Nundlall Basant Roi, PDSM

MCAF LTD - ANNUAL REPORT 2019

4

THE CHAIRMAN’S REPORT

Dear Fellow Co-operators,

On behalf of the Board of Directors, I am honoured to present the 59 th Annual Report of The

Mauri�us Co-opera�ve Agricultural Federa�on Ltd (MCAF Ltd) for the financial year ended 30

June 2019 in my capacity as Chairman.

OVERVIEW

The turnover of the society for the year under review is Rs 223,839,154 compared to last year’s

performance which was Rs 177, 695,113. The net profit a�er tax amounts to Rs 9,212,903 which

is well superior than last year’s profit which amounted to Rs 2,285,507. This is mainly a�ributed

to the overall increase in turnover of sales of fer�lizers by Rs 32M. This increase can be

explained by the fact that the Government through the Mauri�us Cane Industry Authority

(MCIA) has provided 50% subsidy on fer�lizers for planters cul�va�ng less than 100 hectares of

land. As we are all aware, the Sugar Cane Industry is facing problems with severe fall in the

world market price of sugar, compounded with the liberalisa�on of EU produc�on quotas in

2017.The aim of this subsidy is to boost up the yield of sugarcane as well as allevia�ng the

problem of the increase in the cost of produc�on for the planters.

The year 2019, has also been earmarked by several events. Amongst which about 3200 MT of

fer�lizers 17-8-25 were distributed to sugarcane planters through the 13 Sales Outlets under

the scheme –Supply of Fer�lizers to planters cul�va�ng less than 100 hectares. The Federa�on

has also embarked in the implementa�on of a vegetable seedling unit at Maison Des Eleveurs-

La Marie. The project cost is around Rs 4M and 60 perches of land was allocated to the MCAF

by the Ministry of Industrial Development, SMEs and Coopera�ves. I seize this opportunity to

thank the Honourable Soomilduth BHOLAH, Minister of Industrial Development, SMEs and

Coopera�ves for the trust placed in the Federa�on. It is also with great honour that I inform all

our stakeholders that the Federa�on has been awarded the Best Federa�on and Grand Winner

of Excellence for the year 2019 organised by the Ministry of Industrial Development, SMEs and

Coopera�ves with a cash price of Rs 100,000.

MCAF LTD - ANNUAL REPORT 2019

5

REVIEW OF ACTIVITIES

Seedling Produc�on Unit In view of its diversifica�on programme, and taking into considera�on the con�nuous

decrease in land area under sugarcane cul�va�on, the Federa�on has taken a step

further that is to explore and provide its services to the food crop sector to remain viable

on the market. Since the MCAF imports various agro-inputs including seeds, growing

medium, seedling trays and bio products for which the vegetable planters require, the

Federa�on has decided to embark on a project of Healthy Seedling Produc�on for

vegetable planters at a compe��ve price and at the same �me crea�ng job in the field

of Agriculture. The project cost is around Rs 4M. The Ministry of Industrial Development,

SMEs and Coopera�ves has allocated a plot of 60 perches at Maison des Eleveurs,

Henrie�a to the MCAF through an MOU signed between the MCAF and the Ministry of

Industrial Development, SMEs and Coopera�ves to implement the project in April 2019.

The inaugura�on of the unit has been scheduled in February 2020 where a high

delega�on from the Indian Farmers Fer�liser Coopera�ve Limited (IFFCO), India

comprising of Dr.U.S Awas thi, Managing Director and three Directors, will be present to

a�end the ceremony.

Na�onal Award for Coopera�ves -2019 The Ministry of Industrial Development, SMEs and Coopera�ves (Coopera�ves Division)

had launched the Na�onal Award for Coopera�ves at Excellence Level in July 20 19. The

Award aimed at gearing coopera�ves to business excellence while adhering to

coopera�ve principles and values. It also aimed at inspiring the Coopera�ve Movement

to contribute significantly towards the Sustainable Development Goals (SDG’s) for the

benefit of future genera�ons. The Federa�on had par�cipated in the Award and the

MCAF Ltd has won the award once again for best Federa�on in its category and has been

awarded the Grand Winner together with a cash prize of Rs 100,000 during the award

ceremony held on 09 October 2019. I seize this opportunity to congratulate the

management and all the staff of the MCAF Ltd for their dedica�ons and hard work for

this achievement.

Workshop at Palms Hotel on 01 June 2019 The MCAF Ltd had organised a workshop for its Directors and Staff on 01 June 2019 at

Palms Hotel. Two resource persons were invited, Mr S. Sembhoo who gave an insight

on the Impact of Use of Pes�cide Act 2018 on crop produc�on and Pes�cides Retailing

to the staff of the Federa�on. The second part of the workshop was focused on a SWOT

Analysis of the MCAF Ltd where the Mr Mr Jay Lallbeharry, Managing Director -

Sagi�arius Centre for IT and Business Studies hosted this part. The aim of the SWOT

Analysis was to come out with the concep�on of a new Vision and Mission of the

Federa�on. The Workshop ended by the inaugura�on of the new Mission and Vision by

MCAF LTD - ANNUAL REPORT 2019

6

Mr Mr. S. Ramasawmy, Deputy Permanent Secretary at the Ministry of Industrial

Development, SMEs and Coopera�ves. The New Mission and Vision of the MCAF Ltd are

as follows:

New Vision The most valued organiza�on in increasing agricultural produc�vi ty ethically.

New Mission To promote the interests of Coopera�ve Credit Socie�es and member -planters by

providing them with necessary support services, facili�es and incen�ves to encourage

their contribu�ons in making the business of agriculture viable, in a socially responsible

manner.

Mee�ng With the Representa�ve of World Bank Following the downturn of the Sugarcane Industry, the Government had appointed the

World Bank to carry out a thorough study of the sugar cane sector. A mee�ng was held

in December 2019, with Mr John Kayser, Senior Economist, represen�ng the World

Bank. The mee�ng was chaired by myself, Mr S.Sheoraj, Director at the MCAF Ltd and

other representa�ve of Planters Associa�ons. The mechanism to determine price of

sugar and other by-products of the cane were in the agenda. The salient points in the

terms of reference of the study included, among others, the development of: an

economic and financial analysis tool to undertake an assessment of the performance of

the sugar cane industry (smallholder growers, producers, millers, traders). The World

Bank’s study will also undertake an es�mate of the value of externali�es produced by

the sugar cane industry.

MISSION OVERSEAS

Visit to Turkey, Izmir 15 June 2019

Since December 2017, the MCAF has started collabora�ng with UNIKEYTERRA in terms

of purchase of soluble/foliar fer�lizers more specifically special types of fer�lizers. As at

June 2019, 4 consignments from the company have been ordered amoun�ng to Rs 4M.

The products have been well perceived by member planters with immediate results. In

June 2019, a delega�on comprising of Mr N.Basant Roi, PDSM- Chairman, Mr

D.Goburdhun- General Manager and Mr S.Sookna, Marke�ng Manager went to Turkey,

Izmir to meet officials of UnikeyTerra . The purpose of this visit was to further

strengthening business partnership and explore other business possibili�es with the

company.

MCAF LTD - ANNUAL REPORT 2019

7

Visit to India- Nov 2019 A delega�on comprising of the Messrs: N.Basant Roi, Chairman, Directors – S.Sheoraj,

S.Muniah, R.K.Ellapah and the General Manager, D.Goburdhun, were invited by

Willowood limited to a�end the inaugura�on of its JDM Research Centre in Gujarat,

India on 27 November 2019.

Since the delega�on was in Gujarat, they had a frui�ul working session with the officials

of Gujarat Life Sciences Pvt Ltd (GLS) and visited the factory.

Messrs: N.Basant Roi, Chairman, Directors – S.Sheoraj and the General Manager,

D.Goburdhun then proceeded to Delhi to pay a courtesy call to Dr Awasthi, Managing

Director of the Indian Farmers Fer�lizer Coopera�ves Ltd (IFFCO) and at the same �me

invited him and his team to a�end the inaugura�on of the seedling Unit at La Marie.

The delega�on also requested the technical support of IFFCO for the produc�on of a

single liquid bio fer�lizers using a consor�um of bacteria. Dr H.M Shukla, Microbiologist

of IFFCO has been delegated to come to Mauri�us to support us on this project. New

business opportuni�es with IFFCO in the field of pes�cides, sea weed extracts and

Nanotechnology Based Products were also discussed.

Mr. Nundlall Basant Roi, PDSM

Chairman of the MCAF Ltd

MCAF LTD - ANNUAL REPORT 2019

8

BOARD OF DIRECTORS 2019-2020

NAME DESIGNATION

Mr. Nundlall BASANT ROI, PDSM Chairman

Mr. Ravindranath ROOPAH Treasurer

Mr. Ramanand Kankeea ELLAPAH

Director

Mr. Arun Kumar BHOLAH

Director

Mr. Soobas Muniah Director

Mr. Shrudanand SHEORAJ, OSK

Director

Mr. Kamless SEEAM Director

Mr. Satyvanoo GOPAL Director

Mr. Ashveenee Kumar RAMNARAIN Director

MCAF LTD - ANNUAL REPORT 2019

9

AUDIT COMMITTEE 2018-2019

NAME DESIGNATION

Mr. Ashveenee Kumar RAMNARAIN Chairman

Mr. Kamless SEEAM Member

Mr. Ramanand Kankeea ELLAPAH

Member

Mr. Soobas MUNIAH

Member

Mr. Arun Kumar BHOLAH

Member

Mr. Vikash PATANSINGH Internal Controller

STAFF APPOINTMENT AND DISCIPLINARY SUB -COMMITTEE

(Corporate Governance Commi�ee)

NAME DESIGNATION

Mr. Shrudanand SHEORAJ, OSK

Chairman

Mr. Satyvanoo GOPAL Member

Mr. Nundlall BASANT ROI, PDSM Member

Mr. Ashveenee Kumar RAMNARAIN Member

Mr. Kamless SEEAM Member

MCAF LTD - ANNUAL REPORT 2019

10

PESTICIDES IMPORTATION & SALES SUB -COMMITTEE

NAME DESIGNATION

Mr. Satyvanoo GOPAL Chairman

Mr. Soobas MUNIAH Member

Mr Ravindranath Roopah

Member

Mr Arun Kumar BHOLAH

Member

Mr. Ramanand Kankeea ELLAPAH

Member

MARKETING COMMITTEE

NAME DESIGNATION

Mr. Nundlall BASANT ROI, PDSM Chairman

Mr. Shrudanand SHEORAJ, OSK

Member

Mr. Kamless SEEAM Member

Mr. Dineshsing Goburdhun Member

Marke�ng Manager Member

Sales Execu�ve Member

Senior Sales Officers Member

MCAF LTD - ANNUAL REPORT 2019

12

St. Antoine Trust Fund Mr. D. Goburdhun

Sugar Insurance Fund Board Mr. K.Seeam

Altromercato Mr. S.Sheoraj. OSK

FSC Liaision Commi�ee:

Solitude Mr. K. Ramsurrun

L’Unite Mr. S. Ghurhoo

St Pierre Mr. C. Roopah

Rose Belle Mr. C. Khelawon

SENIOR MANAGEMENT STAFF

HEAD OFFICE STAFF

NAME DESIGNATION QUALIFICATIONS

Goburdhun Dineshsing General Manager Adv Dip Business Administra�on (ABE),

B.A Business Administra�on (University

of Her�ordshire, UK

Sookna Sachin Marke�ng Manager BSc, MSc (MRU)

Burosee Navin Accountant/Secretary ACCA Member, MIPA

NAME DESIGNATION

Arjoon Sandiah (Mrs) Accounts Clerk/Senior Accounts Clerk

Sobnauth Hurrykrishianand IT Support Officer/Supplies Officer

Golam Subita (Mrs) Clerk/WPO/Telephonist

Ramkhelawon Neemwatee (Mrs) Clerk/WPO/Telephonist (�ll July 2018)

MCAF LTD - ANNUAL REPORT 2019

11

BIO FERT COMPANY LTD

NAME DESIGNATION

Mr. Nundlall BASANT ROI, PDSM Chairman

Mr. Shrudanand SHEORAJ, OSK

Director

Mr. Dineshsing Goburdhun Director

EXTERNAL BOARD AND COMMITTEES

Mauri�us Chamber of Agriculture Mr. A.K Ramnarain (Bureau)

Mr. A. Bholah

Mr. K. Seeam

Mr. R. Roopah

Mr. S. Muniah

Irriga�on Authority Mr. K. Seeam

Mauri�us Sugar Syndicate Mr. S. Sheoraj

FANRPAN Mr. A.K. Ramnarain

Mauri�us Cane Industry Authority Mr. N. Basant Roi , PDSM

Mauri�us Cane Industry Authority (MSIRI) Mr. N. Basant Roi, PDSM

Mauri�us Cane Industry Authority (CAD) Mr. S. Muniah

Mauri�us Co-opera�ve Alliance Ltd Mr. D. Goburdhun

Mount Planters Fund Mr. K.Seeam -Chairman

Mr. B.Bhoodhoo

Beau Plan Planters Fund Mr. E.P Appannah – Chairman

Mr. A.K Bholah

MCAF LTD - ANNUAL REPORT 2019

13

SALESPOINT STAFF

SENIOR SALES OFFICERS

Jagmohansingh Rajnee (Mrs) Clerk/WPO/Telephonist (as from January 2019)

Seenundun Kamaljeet Senior A�endant

Bundhoo Mitra A�endant/Driver

Jakhun Vishal Driver - Goods Vehicle

Lothay Arvin General Worker

Sanjeev Kumar Mu�y General Worker

Ruggoo Prakash Sales Execu�ve

NAME SALESPOINTS

Mungur Vedanand

SOLITUDE

GOODLANDS

RIVIERE DU REMPART

D’EPINAY

Dhukhi Hurrysurnand

BON ACCUEIL

L’UNITE

ST PIERRE

CAROLINE

Rungasamy Dharmarajen

UNION PARK

ST FELIX

L’ESCALIER

MCAF LTD - ANNUAL REPORT 2019

14

SALES STAFF

SALESPOINT NAME DESIGNATION

Solitude Kaundun Keerun Kumar Sales Officer

Mungur Doorvanand Assistant Sales Officer

Goodlands Baldee Teerathrajsing Sales Officer

Gunesh Shiv Atma Sales Officer

R.du Rempart Nursing Ravindranath Sales Officer

Bon Accueil Sookdeal Soobanand Sales Officer

Ghuroo Yash Akshay Assistant Sales Officer

L'Unité Ramchurn Vishal Assistant Sales Officer

Caroline Narraynen Jaysen

Assistant Sales Officer

St Pierre Bansee Teeran Assistant Sales Officer

Goorjhun Dhanyrao Assistant Sales Officer

Union Park Gunnoo Ramjee Sales Officer

Bhuruth Darasingh Sales Officer

St Felix Gopala Ashvind Assistant Sales Officer

Gowardun Ri�sh Kumar Assistant Sales Officer

D'Epinay Gangaram Veekash Sales Officer

L'Escalier Boodoo Gowtam Sales Officer

St Mar�n Lodah Kaviraj Sales Officer

La Marie Dhakoo Yegesh Sales Officer

LA MARIE

Sookna Sachin/ Ruggoo Prakash ST MARTIN

MCAF LTD - ANNUAL REPORT 2019

15

Hurree Bajeerao Assistant Sales Officer

Biofert Co Ltd Chooramun Ashwinsingh Lab Technician

Bhugobaun Rahul (under YEP) Trainee Lab Technician

REPORT OF THE BOARD OF

DIRECTORS

By Mr Dineshsing Goburdhun

General Manager of MCAF Ltd

MCAF LTD - ANNUAL REPORT 2019

16

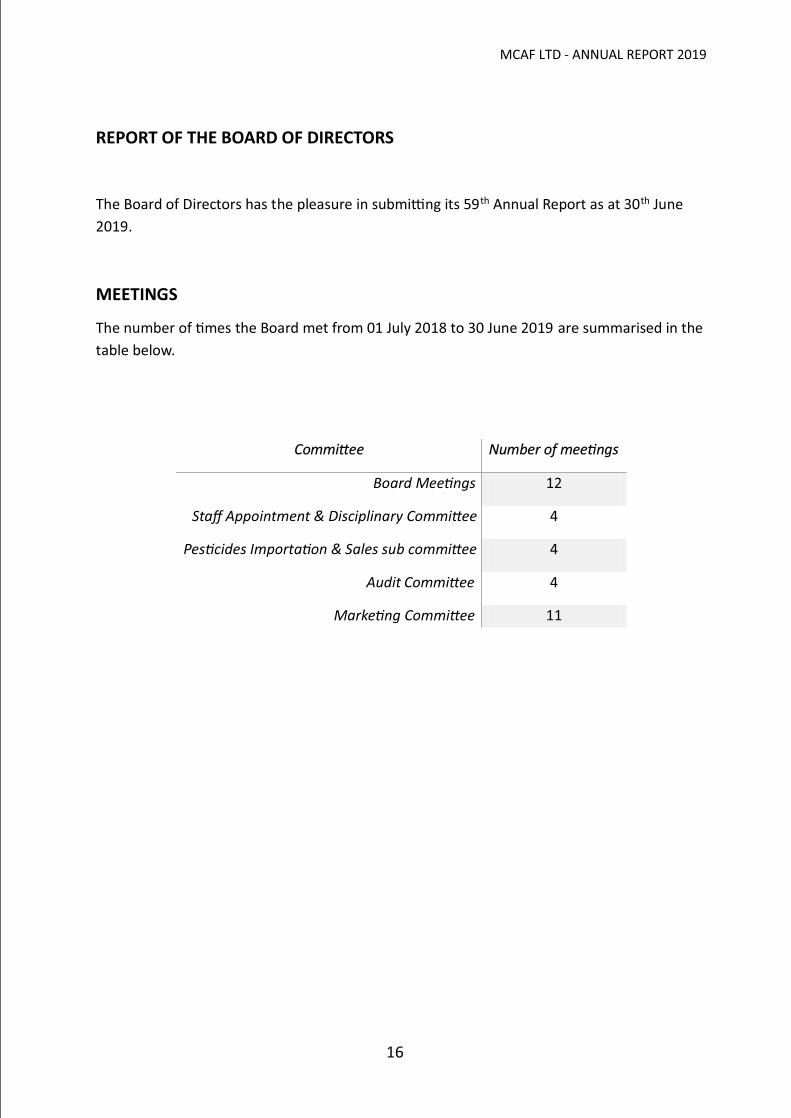

REPORT OF THE BOARD OF DIRECTORS

The Board of Directors has the pleasure in submi�ng its 59th Annual Report as at 30th June

2019.

MEETINGS

The number of �mes the Board met from 01 July 2018 to 30 June 2019 are summarised in the

table below.

Commi�ee Number of mee�ngs

Board Mee�ngs 12

Staff Appointment & Disciplinary Commi�ee 4

Pes�cides Importa�on & Sales sub commi�ee 4

Audit Commi�ee 4

Marke�ng Commi�ee 11

MCAF LTD - ANNUAL REPORT 2019

17

ATTENDANCE AT BOARD MEETING

Director Total number of

mee�ngs

convened

Total number of

mee�ngs a�ended

Mr E.P Appannah ( up to 26 February 2019) 8 8

Mr S. Ghurhoo (up to 26 February 2019) 8 8

Mr C. Khelawon (up to 26 February 2019) 8 8

Mr A. K. Bholah 12 9

Mr S.Gopal 12 12

Mr. K. SEEAM 12 10

Mr R. Roopah 12 12

Mr N. Basant Roi, PDSM 12 12

Mr Sheoraj, OSK (as from 26 February 2019) 4 4

Mr Mr. R. K ELLAPAH (as from 26 February 2019) 4 4

Mr. A. K. RAMNARAIN (as from 26 February 2019) 4 4

Mr S. Muniah (as from 26 February 2019) 4 4

MCAF LTD - ANNUAL REPORT 2019

18

MEMBERSHIP

A total of 155 Co-opera�ve Credit Socie�es (CCS’s) were affiliated to the MCAF Ltd at the

close of the financial year under review.

THE MOUNT AND BEAU PLAN PLANTERS FUNDS

Since 2013, the management of the Mount and Beau Plan Planters Funds are now under the

charge of the MCAF Ltd. Mr K.Seeam and Mr E.P Appannah have been appointed as Chairman

of the Mount and Beau Plan Planters Fund respec�vely. A disbursement commi�ee comprising

of the following members have been set up to monitor the ac�vi�es of the two funds:

Mount Planters Fund Mr. K.Seeam represen�ng MCAF Ltd, Chairman of Mount Planters Fund

Mr M. Monvoisin Registrar, Ministry of Industrial Development, SMEs and

Coopera�ves

Mr. B.Bhoodhoo represen�ng Mount Planters Fund, Member

Mr R.K Soniah representing the MCIA

Mr N de Rosnay represen�ng Terra Milling Company Limited

Beau Plan Planters Fund Mr E.P Appannah represen�ng MCAF Ltd, Chairman of Beau Plan Planters Fund

Mr. A.K Bholah represen�ng Beau Plan Planters Fund, Member

Mr M. Monvoisin Registrar, Ministry of Industrial Development, SMEs and

Coopera�ves

Mr R.K Soniah represen�ng the MCIA

Mr N de Rosnay represen�ng Terra Milling Company Limited

The day to day ac�vi�es of these funds are carried out by a pool of 5 staff of the MCAF Ltd

including the General Manager who extend their supports to the sub-commi�ee. Both funds

cater for the welfare of planters in these factory areas. For road mending, a total of Rs 152,500

has been disbursed for Mount Planters Fund. In addi�on, both funds provide subsidy to planters

when purchasing sprayers, land prepara�on and purchase of fer�lizer for new planta�ons. For

the financial year 2018-2019, Rs 22,067.50 of subsidy has been allocated to both funds for the

purchase of sprayers.

MCAF LTD - ANNUAL REPORT 2019

19

ACCOUNTS

The turnover of the society has increased by Rs 46,144,041 for the year under review compared

to the year 2018. This increase is mainly due to the fact that the Mauri�us Cane Industry

Authority has launched a fer�lizer scheme for all sugarcane planters cul�va�ng less than 100

hectares of cane. This scheme has given a boost to the small sugarcane planters as fer�lizers

are subsidized at 50 percent. This scheme aims also to encourage planters to remain in the

sugarcane business despite severe fall in sugar price at interna�onal level which is beyond our

control.

The net profit a�er tax for the financial year 2018-2019 of the society amounts to Rs 9, 212,903

compared to the year 2017-2018 which was Rs 2,285,507. The gross share of the turnover has

been taken by the fer�lizer segment (Rs 111,744,262 -50%) followed by agro-chemicals & other

Agro-input which amounts to Rs 65,418,606, a 10% increase to that of 2017-2018. The Livestock

Feeds segment has also known a considerable increase of 36% compared to last year’s

performance. This can be explained by an increase in importa�on ac�vi�es and new marke�ng

strategies of the Federa�on.

Figure 1 Turnover 2019 by Segment

Fer�lizers, 111,744,262 , 50%

Pes�cides & Other Agro-input,

65,418,606 , 29%

Livestock Feeds,

31,886,663 , 14%

Seeds, 14,789,623 ,

7%

TURNOVER BY CATEGORY TURNOVER: Rs 223,839,154.00

MCAF LTD - ANNUAL REPORT 2019

20

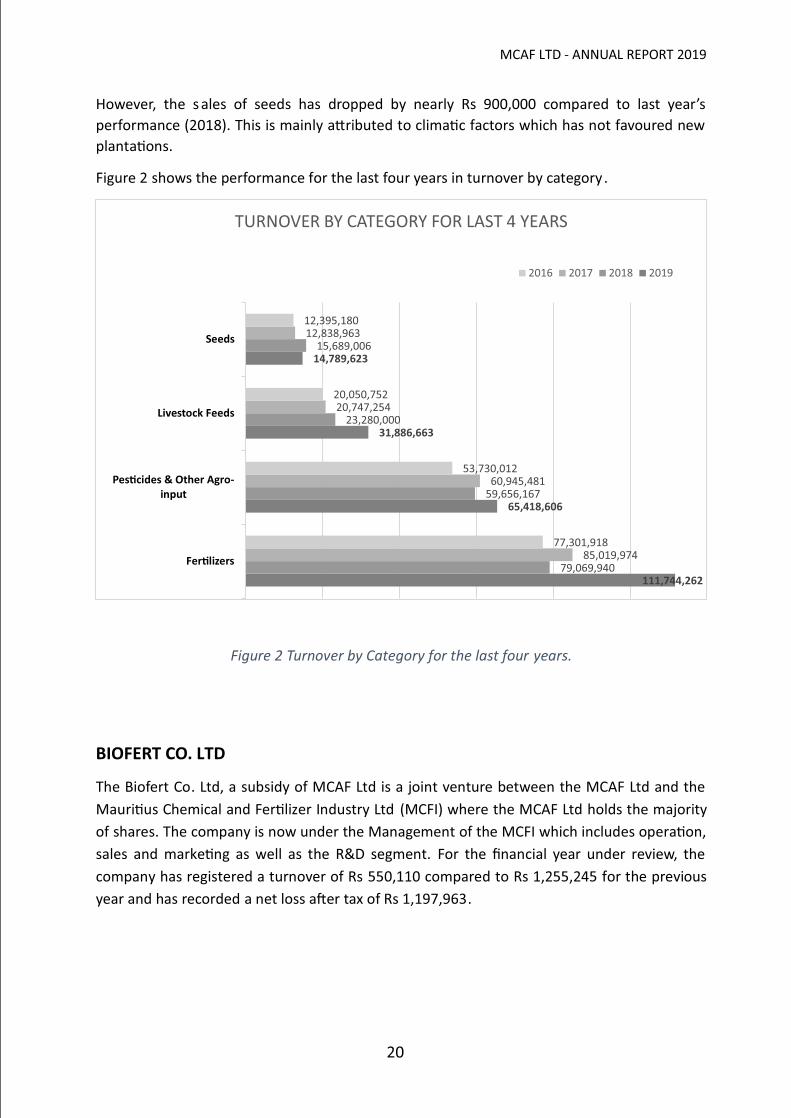

However, the s ales of seeds has dropped by nearly Rs 900,000 compared to last year’s

performance (2018). This is mainly a�ributed to clima�c factors which has not favoured new

planta�ons.

Figure 2 shows the performance for the last four years in turnover by category.

Figure 2 Turnover by Category for the last four years.

BIOFERT CO. LTD

The Biofert Co. Ltd, a subsidy of MCAF Ltd is a joint venture between the MCAF Ltd and the

Mauri�us Chemical and Fer�lizer Industry Ltd (MCFI) where the MCAF Ltd holds the majority

of shares. The company is now under the Management of the MCFI which includes opera�on,

sales and marke�ng as well as the R&D segment. For the financial year under review, the

company has registered a turnover of Rs 550,110 compared to Rs 1,255,245 for the previous

year and has recorded a net loss a�er tax of Rs 1,197,963.

111,744,262

65,418,606

31,886,663

14,789,623

79,069,940

59,656,167

23,280,000

15,689,006

85,019,974

60,945,481

20,747,254

12,838,963

77,301,918

53,730,012

20,050,752

12,395,180

Fer�lizers

Pes�cides & Other Agro-input

Livestock Feeds

Seeds

TURNOVER BY CATEGORY FOR LAST 4 YEARS

2016 2017 2018 2019

MCAF LTD - ANNUAL REPORT 2019

21

ACTIVITIES

New Project: Vegetable Seedling Project In view of its diversifica�on programme, and taking into considera�on the con�nuous decrease

in land area under sugarcane cul�va�on, the Federa�on has taken a step further to explore and

provide its services to the food crop sector to remain viable on the market. The Federa�on has

decided to embark on a project of Healthy Seedling Produc�on for both vegetable and

sugarcane planters at a compe��ve price and at the same �me crea�ng job in the field of

Agriculture. In April 2019, the MCAF Ltd has signed an MOU with the Ministry of Business,

Enterprise and Coopera�ves where the Ministry is providing 60 perches of land at Maison des

Eleveurs, Henrie�a for the implementa�on of the project. The cost of project is Rs 4M and the

inaugura�on has been scheduled for end of February 2020.

Redesign of Website The Federa�on is redesigning its exis�ng website to give a fresh image to the MCAF Ltd which

will comprise of all products por�olios together with an E-commerce pla�orm which will enable

the Federa�on to market its products through online system. This new website consists of the

latest tools which enables daily back up of data from the Pont of Sales (POS) onto cloud system.

The new website will be launched in February 2020

Purchase of Electrical Stacker In order to be more efficient in terms of product delivery to customer, use of warehouse space

and safety of personnel is essen�al and therefore, the Federa�on has purchased an Electrical

Stacker (mini forkli�) amoun�ng Rs 285,000. The Electrical Stacker has facilitated the loading

and unloading of products (heavy carton boxes, fer�lizer bags, etc) from the container and lorry

to our main warehouse and has improved considerably the efficiency of logis�cs. It is worth to

note that the Co-opera�ve Development Fund (CDF) under the agies of the Ministry of

Industrial Development, SMEs and Coopera�ves has given a grant of Rs 100,000 to the MCAF

Ltd to implement this project.

Implementa�on of Lot Tracking System on (Point of Sales) POS and Head

Office In view of the complexi�es of product ranges that the Federa�on is dealing, an efficient control

system over the products is necessary par�cularly control over the expiry of products and using

the FIFO concept (First In First Out) at Point of Sales (POS). The Federa�on has added an

addi�onal module called Lot Tracking System (LTS) in its Accoun�ng So�ware. This module has

cost around Rs 100,000 including training of staff. This component will also help during

traceability whenever a customer is complaining about the quality of a product.

MCAF LTD - ANNUAL REPORT 2019

22

MISSION OVERSEAS

Visit to Tirth Agro Pvt Ltd –Pune Rajkot (02-08 December 2018) In December 2018, the Chairman, Mr N.Basant Roi, a delega�on of Directors together with the

General Manager, Mr D.Goburdhun and the Marke�ng Manager, Mr S.Sookna were invited to

India (Pune and Rajkot) by Tirth Agro Pvt Ltd. The visit consisted mainly of the opera�on of a

cane harvester in sugarcane fields, sugar mill visit and visit of Tirth Agro Pvt Ltd manufacturing

plant in Rajkot-Gujarat. Mr R.K Soniah, Director of the FSC was also invited to form part of the

delega�on. The main purpose of this visit was to understand the opera�on of the harvester in

field and how it will adapt to small planters fields and also a feasibility study for the purchase

of a cane harvester was carried out which seemed promising in our local context. It should be

also noted that the Federa�on has requested funds for the purchase of Sugarcane Harvesters

in the budget consulta�on program 2019-2020. The Government has a par�cular a�en�on to

the small planters, has earmarked a sum of Rs 15M to the MCIA for the purchase of cane

harvesters.

Indian Farmers Fer�lizer Coopera�ves Ltd (IFFCO -New Delhi) – Signing

Of MOU on Twinning Program – 11 Dec 2018 A delega�on comprising of Mr N.Basant Roi, Chairman of the MCAF, Mr S.Ghurhoo, Treasurer,

Mr S.Gopal, Director and Mr D.Goburdhun, General Manager MCAF were in Delhi on 10

December 2018 to sign an MOU with IFFCO concerning a bilateral exchange programme which

include new business avenues in terms of bio-products as well as training. On behalf of IFFCO,

the MOU was signed by Mr A.K Singh, Director (CD& Tech), Mr Tarun Bhargava, Deputy General

Manager (CR) and as witness, Mrs Madhavi Vipradas, Senior Manager (CR)

Courtesy call at the Mauri�us High Commission, New Delhi, H.E. Mr. J.

Goburdhun, GOSK, High Commissioner of the Republic of Mauri�us to

India. The delega�on paid a courtesy call to the Mauri�us High Commissioner, New Delhi, H.E. Mr. J.

Goburdhun, GOSK. During the visit, the delega�on explained their main presence in India and

explained the Cane Harvester Project to the high commissioner who stated that he will give the

Federa�on his full support to realise this project.

Visit to Turkey, Izmir 15 June 2019 In June 2019, a delega�on comprising of Messrs, N. Basant Roi, D.Goburdhun, S.Sookna-

Chairman, General Manager and Marke�ng Manager respec�vely went to Izmir, Turkey to

meet officials of UnikeyTerra, a company specialised in the produc�on of speciality fer�lizers

and other Bio-s�mulants. The Federa�on is impor�ng from this company since 2018, and the

quality of fer�lizers were well appreciated by planters. The visit also consisted factory site

visit and well as payment and credit facili�es were discussed.

MCAF LTD - ANNUAL REPORT 2019

23

CROP 2018 Island wide, the total cane harvested for crop 2018 amounts to 3,154,516 T reaped over 47,181

Ha which has produced 325,980 T of sugar. These values are inferior to that of Crop 2017 where

3,713,331T of cane were harvested over 48,857 ha producing 357,702 T of sugar accrued. This

drop is a�ributed to severe clima�c condi�ons which consisted of excessive rainfall during the

first four months of the year coupled with low solar radia�on during the same period which

impacted nega�vely on the cane elonga�on and eventually affec�ng whole cane produc�vity.

However, the extrac�on rate for Crop 2018 is on average 10.26% which is superior to that of

Crop 2017 which was 9.57%. The rise in extrac�on is explained by a favorable weather condi�on

prevailing over the island during the ripening phase which were conducive to sucrose

accumula�on, thus resulted in a be�er extrac�on rate.

The total number of planters who consigned cane for Crop 2018 is 12,884 out of which 57% of

the total number of planters, 7,345 were enrolled under Co-opera�ve Credit Socie�es (CCS’s)

where 33,733 T of sugar was produced under 7,313 ha.

The table below shows a compara�ve performance figures the last three Crop year’s for the

whole Island and CCS planters.

CROP REGION AREA HARVESTED (ha) CANE HARVESTED

(Tons)

SUGAR PRODUCED

(Tons)

CROP 2016 Island of Mauri�us

51,476 3,798,448 386,277 CROP 2017 49,974 3,713,331 355,213 CROP 2018 47,181 3,154,516 325,980

CROP 2016

CCS Planters

7,443 494,120 39,393

CROP 2017 7,217 524,258 36,146

CROP 2018 7,313 425,688 33,733

PRICE OF SUGAR For Crop 2018, the ex- Syndicate price per ton of sugar has been fixed at Rs 8,700. In fact, this

price is the lowest ever recorded since the aboli�on of quota. However, we must be thankful

once again to the Government, the Sugar Insurance Fund Board has been requested to con�nue

to provide an assistance of Rs 1,250 per ton of sugar produced to alleviate the financial

constraints of planters. In addi�on the government has provided an addi�onal financial support

of Rs 257.00 per Ton of cane to planters.

MCAF LTD - ANNUAL REPORT 2019

24

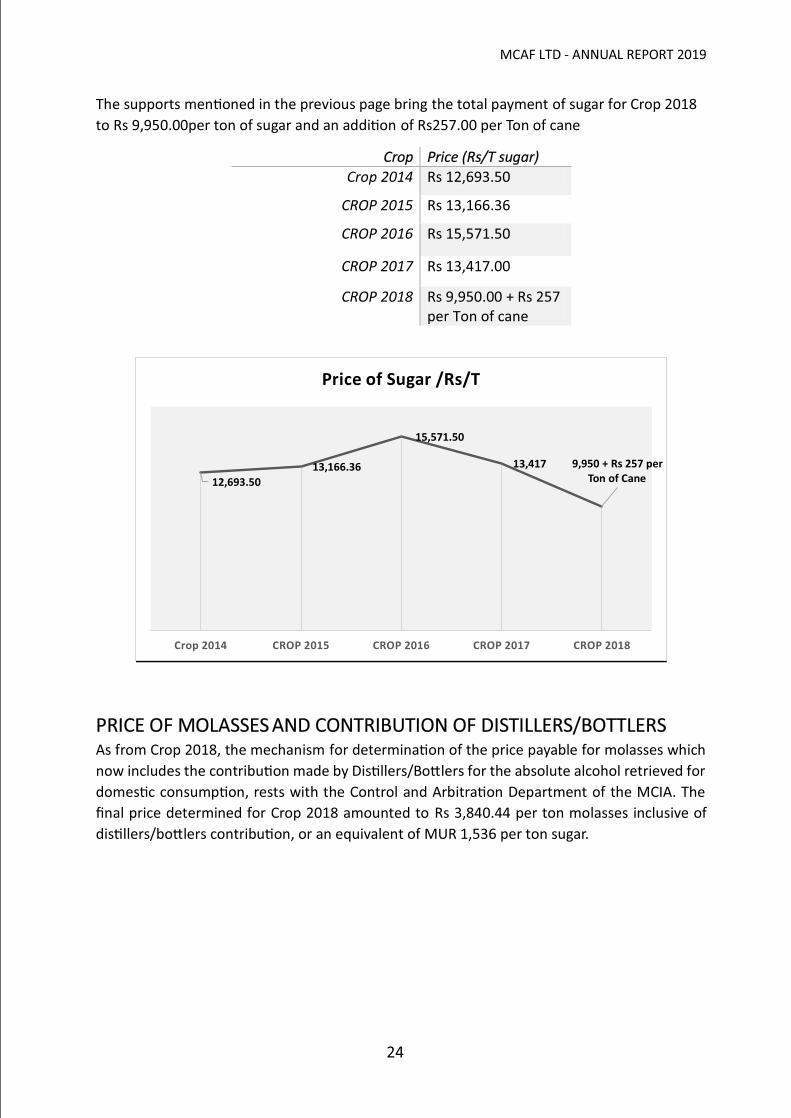

The supports men�oned in the previous page bring the total payment of sugar for Crop 2018

to Rs 9,950.00per ton of sugar and an addi�on of Rs257.00 per Ton of cane

Crop Price (Rs/T sugar)

Crop 2014 Rs 12,693.50

CROP 2015 Rs 13,166.36

CROP 2016 Rs 15,571.50

CROP 2017 Rs 13,417.00

CROP 2018 Rs 9,950.00 + Rs 257 per Ton of cane

PRICE OF MOLASSES AND CONTRIBUTION OF DISTILLERS/BOTTLERS As from Crop 2018, the mechanism for determina�on of the price payable for molasses which

now includes the contribu�on made by Dis�llers/Bo�lers for the absolute alcohol retrieved for

domes�c consump�on, rests with the Control and Arbitra�on Department of the MCIA. The

final price determined for Crop 2018 amounted to Rs 3,840.44 per ton molasses inclusive of

dis�llers/bo�lers contribu�on, or an equivalent of MUR 1,536 per ton sugar.

12,693.50

13,166.36

15,571.50

13,417 9,950 + Rs 257 per Ton of Cane

Crop 2014 CROP 2015 CROP 2016 CROP 2017 CROP 2018

Price of Sugar /Rs/T

MCAF LTD - ANNUAL REPORT 2019

25

PRICE OF BAGASSE Payment of Bagasse proceeds for Crop 2018 by the syndicate amounted to Rs 161.05 per Ton

of Sugar.

Crop Year Price of Bagasse (Rs/Ton of Sugar)

2014 124.17

2015 1,262.29 (Rs 162.29 + Rs 1,100 – Sugarcane Sustainability Fund)

2016 1,249.83 (Rs 149.83 + Rs 1,100 – Sugarcane Sustainability Fund)

2017 1,264.81 (Rs 164.81 + Rs 1,100 – Sugarcane Sustainability Fund)

2018 2,041.05 ( Rs 161.05 + Rs 2,350 - Sugarcane Sustainability Fund)

SUGARCANE HARVESTED AND SUGAR PRODUCED BY CCS’s

Crop year Sugar Cane (tons) Sugar Produced (tons)

2014 374,873 28,578

2015 491,376 34,773

2016 494,120 39,393

2017 524,258 36,146

2018 425,688 37,733

LAND AREA HARVESTED AND NUMBER OF PLANTERS (CCS) Crop year Extent harvested (Hectares) Number of planters

2014 5,123 7,129

2015 6,847 7,315

2016 7,443 7,299

2017 7,217 7,037

2018 7,313 7,345

MCAF LTD - ANNUAL REPORT 2019

26

ACKNOWLEDGEMENTS The Board of directors would like to thank Mr Dineshsing Goburdhun, the General Manager of

the MCAF Ltd, the management team and all the MCAF’s staff for their dedica�on,

commitments and hard work for the con�nuous growth of the business despite the challenges

facing the Sugar Cane Industry.

By order of the Board of Directors D. Goburdhun General Manager

MCAF LTD - ANNUAL REPORT 2019

27

APPROPRIATION OF SURPLUS FOR THE YEAR 2018/2019

Amount

Rs 2018/2019

Statutory Reserve (10%)

921,290.30

Dividend on shares

(20%) 37,200.00

Staff Bonus 1,023,152.50

Bonus to Planters

(10%) 921,290.30

Bonus to Secretaries

(5%) 460,645.15

IT Fund 500,000.00

Building Reserve 3,500,000.00

Special Reserve 1,623,878.75

Corporate Social

Responsibility 225,446.00

TOTAL 9,212,903.00

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARY

CONSOLIDATED FINANCIAL STATEMENTS

YEAR ENDED - 30 JUNE 2019

28

30 - 31

31 - 34

35

36

37 - 38

40

41 - 61

62 - 63

29

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARY

REPORT OF THE CHAIRMAN

PRINCIPAL ACITIVITIES

RESULTS

MEMBERS

Mr. Nundlall BASANT ROI, PDSM Chairman

Mr. Ravindranath ROOPAH Treasurer

Mr. Ramanand Kankeea ELLAPAH Director

Mr. Arun Kumar BHOLAH Director

Mr. Soobas MUNIAH Director

Mr. Shrudanand SHOERAJ, OSK Director

Mr. Kamless SEEAM Director

Mr. Satyvanoo GOPAL Director

Mr. Ashveenee Kumar RAMNARAIN Director

-

-

-

- prepare the financial statements on a going concern basis unless it is inappropriate to presume that the Group and the Society

will continue in business.

The principal activity of the Society's subsidiary, BioFert Co. Ltd, is the manufacturing of fertilisers and nitrogen compounds.

The Board was made up of the following members who held office during the year to the date of signing the financial statements:

BOARD MEMBERS' RESPONSIBILITIES IN RESPECT OF THE FINANCIAL STATEMENTS

The Board members are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the

financial position of the Society and to enable them to ensure that the financial statements comply with the Co-operatives Act,

2005. They have general responsibility for taking such steps as are reasonably open to them to safeguard the assets of the Society

and to prevent and detect fraud and other irregularities.

The Board members confirm that they have complied with the above requirements in preparing the financial statements.

The Board members are required to prepare financial statements for each financial year which present fairly the financial position,

financial performance, changes in shareholders' fund and cash flows of the Group and the Society. In preparing those financial

statements, the Board members are required to:

select suitable accounting policies and then apply them consistently;

The Chairman of THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED (''the Society'') is

pleased to present his report and the audited consolidated financial statements of the Society and its subsidiary (together referred to

as "the Group") for the year ended 30 June 2019.

The principal activity of the Society consists of sale and distribution of agro-inputs, namely fertilisers, pesticides, seeds and other

planters materials to the planters community.

The Society's total comprehensive income for the year ended 30 June 2019 is Rs 9,212,902 (2018: Comprehensive income of Rs

2,285,507).

make judgements and estimates that are reasonable and prudent;

state whether International Financial Reporting Standards (IFRS) have been followed, subject to any material departures

disclosed and explained in the financial statements; and

The Group's total comprehensive income for the year ended 30 June 2019 is Rs 8,014,939 (2018: Comprehensive income of Rs

2,237,280).

30

31

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARY

REPORT OF THE CHAIRMAN (CONTINUED)

-

-

GOING CONCERN

AUDITORS

……………………….. …………………………

N. Basant Roi - PDSM Dineshsing Goburdhun

Chairman General Manager

The auditors BIT Associates have indicated their willingness to continue in office and a resolution for their re-appointment

will be proposed at the next Annual Meeting.

Approved by the Board Members on………...………………. and signed on its behalf by:

DISCLOSURE OF INFORMATION TO THE AUDITOR

The Board members of the Society who held office at the date of approval of this annual report confirm that:

so far as each member is aware, there is no relevant audit information, information needed by the the Group's and the

Society's auditors in connection with preparing their report, of which the Group's and the Society's auditors are unaware; and

each member has taken all the steps that they ought to have taken as a director in order to make themselves aware of any

relevant audit information and to establish that the Group's and the Society's auditors are aware of that information.

Having made appropriate enquiries, the Board members have reasonable expectation that the Group and the Society have

adequate resources to continue in operational existence for the foreseeable future. For this reason they continue to adopt the

going concern basis in preparing the Group's and the Society's financial statements.

23 DEC 2019

INDEPENDENT AUDITORS' REPORT

TO THE MEMBERS OF

Report on the Audit of the Financial Statements

Opinion

Basis for opinion

Other information

Directors' responsibilities for the Financial Statements

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND

ITS SUBSIDIARY

The directors are responsible for the other information. The other information comprises the report of the chairman,

or any other information. The other information does not include the consolidated financial statements and our

auditors' report thereon.

Our opinion on the consolidated financial statements does not cover the other information and we do not express an

audit opinion or any form of assurance conclusion thereon.

In connection with our audit of the consolidated financial statements, our responsibility is to read the other

information and, in doing so, consider whether the other information is materially inconsistent with the consolidated

financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based

on the work we have performed, we conclude that there is a material misstatement of this other information, we are

required to report that fact. We have nothing to report in this regard.

The Directors are responsible for the preparation of the financial statements in accordance with International

Financial Reporting Standards and the requirements of the Co-operatives Act 2005, and for such internal control as

the directors determine is necessary to enable the preparation of financial statements that are free from material

misstatement, whether due to fraud or error.

We have audited the financial statements of THE MAURITIUS CO-OPERATIVE AGRICULTURAL

FEDERATION LIMITED (the "Society" ) and its subsidiary (together referred as the "Group" ), set out on pages 6

to 32 which comprise the consolidated statements of financial position as at 30 June 2019, the consolidated

statements of profit or loss and other comprehensive income, the consolidated statements of changes in shareholders

fund and the consolidated statements of cash flows for the year then ended, and the notes to the consolidated

financial statements, including a summary of significant accounting policies.

In our opinion, the consolidated financial statements give a true and fair view of the financial position of the Group

and the Society as at 30 June 2019, and of their financial performance and cash flows for the year then ended in

accordance with International Financial Reporting Standards and in compliance with the requirements of the Section

79 of the Co-operatives Act 2005.

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under

those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements

section of our report. We are independent of the Society in accordance with the ethical requirements that are relevant

to our audit of the financial statements in Mauritius, and we have fulfilled our other ethical responsibilities in

accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and

appropriate to provide a basis for our opinion.

32

INDEPENDENT AUDITORS' REPORT

TO THE MEMBERS OF

Report on the Audit of the Financial Statements (continued)

Directors' responsibilities for the Financial Statements (continued)

•

•

•

•

•

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND

ITS SUBSIDIARY

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from

material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion.

Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with

ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are

considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic

decisions of users taken on the basis of these financial statements.

Auditors' Responsibilities for the Audit of the Financial Statements

In preparing the financial statements, the directors are responsible for assessing the Group's and the Society's ability

to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going

concern basis of accounting unless the directors either intends to liquidate the Group and the Society or to cease

operations, or have no realistic alternative but to do so.

Conclude on the appropriateness of directors’ use of the going concern basis of accounting and, based on the

audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast

significant doubt on the Group's and the Society’s ability to continue as a going concern. If we conclude that a

material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in

the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based

on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may

cause the Group and the Society to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the financial statements, including the disclosures,

and whether the financial statements represent the underlying transactions and events in a manner that achieves

fair presentation.

Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error,

design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and

appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from

fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions,

misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the

Group's and the Society’s internal control.

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and

related disclosures made by management.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism

throughout the audit. We also:

33

INDEPENDENT AUDITORS' REPORT

TO THE MEMBERS OF

Report on the Audit of the Financial Statements (continued)

Other matter

Report on Other Legal and Regulatory Requirements

Chartered Certified Accountants Licensed by FRC

& Registered Auditors

Quatre Bornes,

Mauritius

Date: 24 DEC 2019

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND

ITS SUBSIDIARY

In our opinion, proper accounting records have been kept by the Group and the Society as far as it appears from our

examination of those records.

Auditors' Responsibilities for the Audit of the Financial Statements (continued)

We communicate with the directors regarding, among other matters, the planned scope and timing of the audit and

significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

This report is made solely for the Group's and the Society's members, as a body, in accordance with the Co-operatives

Act 2005. Our audit work has been undertaken so that we might state to the Group's and the Society's members those

matters we are required to state to the latter in an auditors' report and for no other purpose. To the fullest extent

permitted by law, we do not accept or assume responsibility to anyone other than the Group and the Society and the

Group's and the Society's members, as a body for our audit work, for this report, or for the opinions we have formed.

We have no relationship with, or interests in, the Group and the Society, other than in our capacity as auditors, and

dealings in the ordinary course of business.

We have obtained all information and explanations we have required.

3434

BIT ASSOCIATES DWARKA SOOCHIT, FCCA, FCMA, CGMA

35

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYCONSOLIDATED STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2019

ASSETS Notes 2019 2018 2019 2018

Rs. Rs. Rs. Rs.

Non-current assets

Property, plant and equipment 5 19,451,576 20,159,430 15,813,440 15,822,164

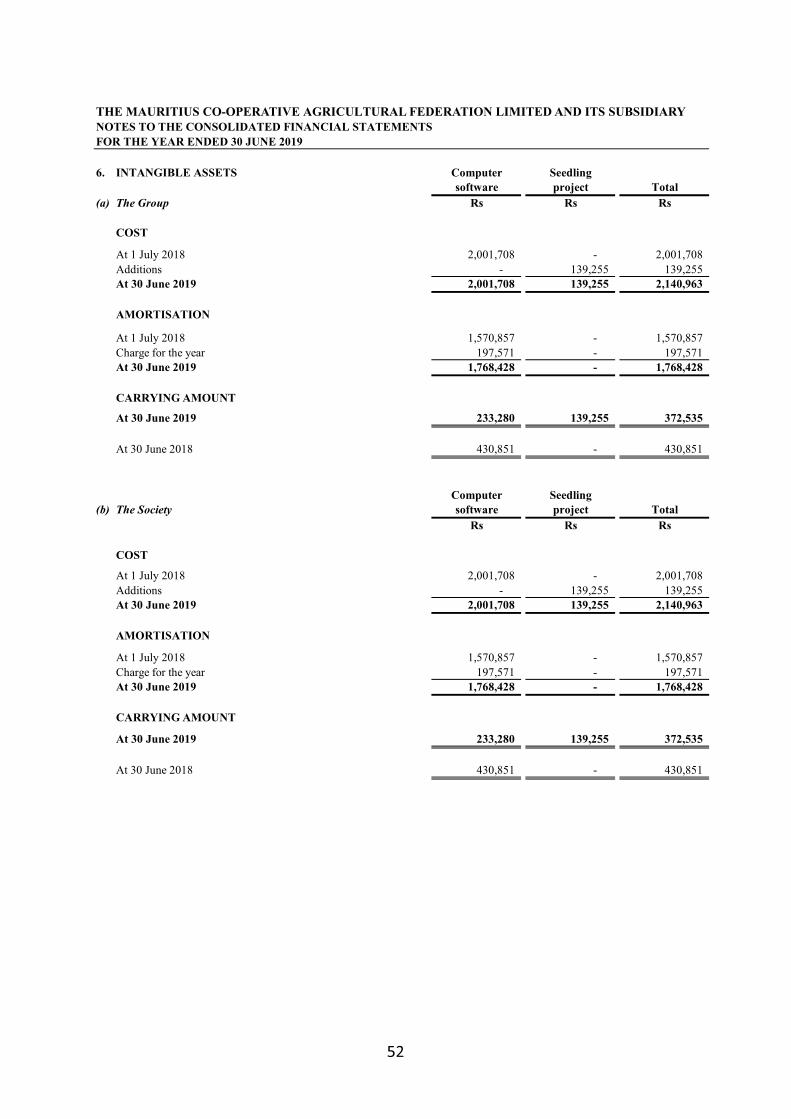

Intangible assets 6 372,535 430,851 372,535 430,851 Investment in financial assets 7 1,584,930 1,465,172 1,584,930 1,465,172

Investment in subsidiary 8 - - 6,000,000 6,000,000

Deposits 9 65,000,000 65,000,000 65,000,000 65,000,000

Deferred tax assets 14 272,482 171,458 655,311 584,405

86,681,523 87,226,911 89,426,216 89,302,592

Current assets

Inventories 10 25,515,444 25,500,427 25,425,966 25,180,969

Trade and other receivables 11 32,591,172 22,692,216 34,159,376 25,509,048

Deposits 9 8,250,000 8,250,000 8,250,000 8,250,000

Cash and cash equivalents 12 27,838,683 23,587,426 27,838,683 23,587,426

94,195,299 80,030,069 95,674,025 82,527,443

TOTAL ASSETS 180,876,822 167,256,980 185,100,241 171,830,035

EQUITY AND LIABILITIES

Equity and reserves

Stated capital 13 187,400 187,400 187,400 187,400

Retained earnings 97,868,027 89,453,806 100,882,804 91,669,901

Non - controlling interest 1,528,006 1,927,287 - -

Total equity 99,583,433 91,568,493 101,070,204 91,857,301

Non-current liabilities

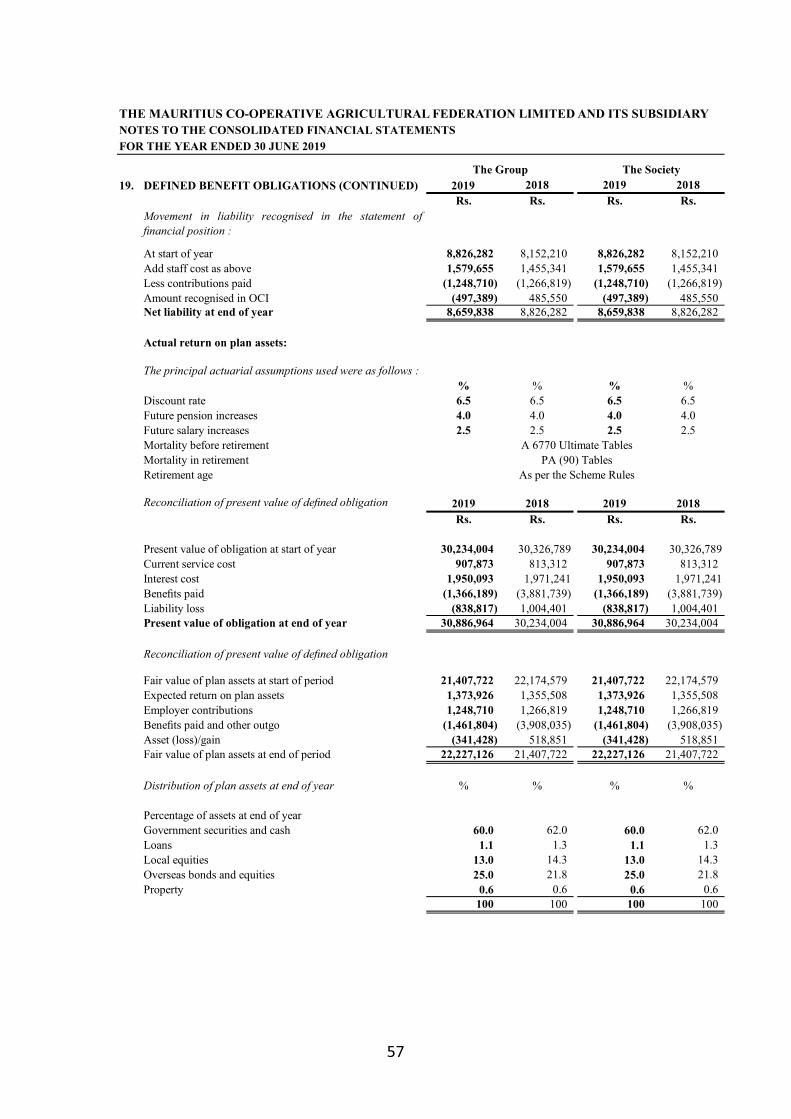

Defined benefit obligations 19 8,659,838 8,826,282 8,659,838 8,826,282

Other grants 16 28,746,088 28,746,088 28,746,088 28,746,088

37,405,926 37,572,370 37,405,926 37,572,370

Current liabilities

Trade and other payables 17 15,648,467 28,010,133 18,385,115 32,294,380

Bonus payable 18 4,998,639 5,654,176 4,998,639 5,654,176

Bank overdraft 12 22,216,855 3,583,493 22,216,855 3,583,493

Taxation 14 1,023,502 868,314 1,023,502 868,314

43,887,463 38,116,116 46,624,111 42,400,363

TOTAL EQUITY AND LIABILITIES 180,876,822 167,256,980 185,100,241 171,830,035

Approved by the Board Members on ……………………………and signed on its behalf by:

……………………………….. ……………………………….. ………………………………

N.Basant Roi - PDSM D.Goburdhun R. Roopah

Chairman General Manager Treasurer

The accompanying notes on pages 11 to 32 form an integral part of these consolidated financial statements.

Auditors' Report on pages 3 to 5.

The SocietyThe Group

23 DEC 2019

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARY

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30 JUNE 2019

Notes 2019 2018 2019 2018

Rs. Rs. Rs. Rs.

Turnover 3( e) 224,247,155 178,950,358 223,839,155 177,695,113

Cost of sales (191,095,249) (155,747,177) (190,914,246) (155,634,706)

Gross profit 33,151,906 23,203,182 32,924,909 22,060,408

Other income 3,322,944 7,316,170 3,322,944 7,316,170

Administrative expenses (25,558,442) (23,380,146) (24,802,446) (22,895,115)

Depreciation and amortisation (1,598,248) (1,723,476) (899,168) (1,024,396)

Profit before taxation 9,318,160 5,415,729 10,546,239 5,457,066

Taxation 14 (1,725,708) (1,058,381) (1,755,823) (1,051,491)

Profit for the year 7,592,452 4,357,348 8,790,416 4,405,575

Other comprehensive income

Items that will not be classified subsequently to profit or loss:

497,389 (485,550) 497,389 (485,550)

Items that may be classified subsequently to profit or loss:

Investment in financial assets at FVOCI:

Increase in fair value of investment in financial assets at

FVOCI - 94,500 - 94,500

Decrease in fair value of investment in financial assets at

FVOCI (74,902) (1,729,018) (74,902) (1,729,018)

422,487 (2,120,068) 422,487 (2,120,068)

8,014,939 2,237,280 9,212,903 2,285,507

Owners of the Society 8,414,220 2,251,057 9,212,903 2,285,507

Non-controlling interests (399,281) (13,778) - -

8,014,939 2,237,280 9,212,903 2,285,507

The accompanying notes on pages 11 to 32 form an integral part of these consolidated financial statements.

Auditors' Report on pages 3 to 5.

Remeasurement of defined benefit obligations

Other comprehensive income/(loss), net of income tax

Total comprehensive income for the year

Total comprehensive income for the year attributable to:

The SocietyThe Group

36

The Group

Stated

capital

Statutory

reserves

Special

reserve

Building

reserve

Revaluation

reserve

IT fund

reserve

Equipment

reserve

Fair value

reserve

Other

reserves

Retained

earnings

Non-

Controlling

interests

Total

Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs.As at 01 July 2017 187,400 28,188,279 6,736,588 14,420,065 3,000,000 3,871,312 700,000 1,584,319 162,000 28,540,187 1,941,065 89,331,215

Transfers - - - - - - - - - - - -

Issue of shares - - - - - - - - - - - -

Dividend - - - - - - - - - - - -

Bonus planters - - - - - - - - - - - -

Bonus secretaries - - - - - - - - - - - -

Bonus staff - - - - - - - - - - - -

Fair Value Adjustment - - - - - - - - - - -

Profit for the the year - - - - - - - - - 2,251,057 - 2,251,057

Non controlling interest - - - - - - - - - - (13,778) (13,778)

As at 30 June 2018 187,400 28,188,279 6,736,588 14,420,065 3,000,000 3,871,312 700,000 1,584,319 162,000 30,791,244 1,927,287 91,568,494

Transfers - - - - - - - - - - - -

Issue of shares - - - - - - - - - - - -

Dividend - - - - - - - - - - - -

Bonus planters - - - - - - - - - - - -

Bonus secretaries - - - - - - - - - - - -

Bonus staff - - - - - - - - - - - -

Profit for the the year - - - - - - - - - 8,414,220 - 8,414,220

Non controlling interest - - - - - - - - - - (399,281) (399,281) As at 30 June 2019 187,400 28,188,279 6,736,588 14,420,065 3,000,000 3,871,312 700,000 1,584,319 162,000 39,205,464 1,528,006 99,583,433

The accompanying notes on pages 11 to 32 form an integral part of these consolidated financial statements.

Auditors' Report on pages 3 to 5.

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYCONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS' FUND

FOR THE YEAR ENDED 30 JUNE 2019

37

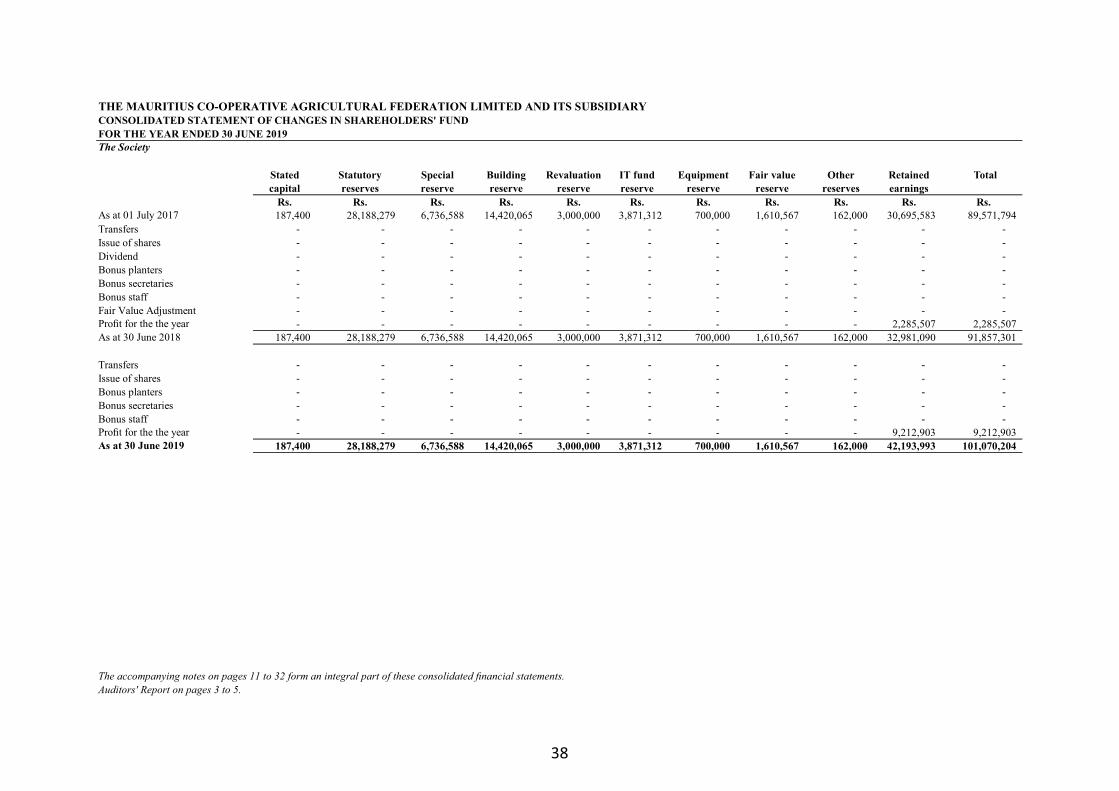

The Society

Stated

capital

Statutory

reserves

Special

reserve

Building

reserve

Revaluation

reserve

IT fund

reserve

Equipment

reserve

Fair value

reserve

Other

reserves

Retained

earnings

Total

Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs.As at 01 July 2017 187,400 28,188,279 6,736,588 14,420,065 3,000,000 3,871,312 700,000 1,610,567 162,000 30,695,583 89,571,794

Transfers - - - - - - - - - - -

Issue of shares - - - - - - - - - - -

Dividend - - - - - - - - - - -

Bonus planters - - - - - - - - - - -

Bonus secretaries - - - - - - - - - - -

Bonus staff - - - - - - - - - - -

Fair Value Adjustment - - - - - - - - - - - Profit for the the year - - - - - - - - - 2,285,507 2,285,507 As at 30 June 2018 187,400 28,188,279 6,736,588 14,420,065 3,000,000 3,871,312 700,000 1,610,567 162,000 32,981,090 91,857,301

Transfers - - - - - - - - - - -

Issue of shares - - - - - - - - - - -

Bonus planters - - - - - - - - - - -

Bonus secretaries - - - - - - - - - - -

Bonus staff - - - - - - - - - - - Profit for the the year - - - - - - - - - 9,212,903 9,212,903 As at 30 June 2019 187,400 28,188,279 6,736,588 14,420,065 3,000,000 3,871,312 700,000 1,610,567 162,000 42,193,993 101,070,204

The accompanying notes on pages 11 to 32 form an integral part of these consolidated financial statements.

Auditors' Report on pages 3 to 5.

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYCONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS' FUND

FOR THE YEAR ENDED 30 JUNE 2019

38

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARY

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30 JUNE 2019

Note 2019 2018 2019 2018

Rs. Rs. Rs. Rs.

Cash flows from operating activities

Profit before taxation 9,318,160 5,415,729 10,546,239 5,457,066

Adjustments for:-

Interest received (1,898,576) (3,380,966) (1,898,576) (3,380,966)

Retirement benefit obligations 330,945 833,021 330,945 (26,296)

Gain on disposal (113,835) - (113,835) -

Other adjustments 48 101,052 - 214,848

Depreciation and amortisation 1,598,248 1,723,476 899,168 1,024,396

Operating profit before working capital changes 9,234,990 4,692,312 9,763,941 3,289,048

Increase in inventories (15,017) (1,489,641) (244,997) (1,485,874)

(Increase)/decrease in trade and other receivables (9,898,956) 6,549,568 (8,650,328) 8,622,281

(Decrease)/increase in trade and other payables (12,361,666) 3,958,616 (13,909,265) 3,285,400

Cash (absorbed into)/generated from operations (13,040,649) 13,710,854 (13,040,649) 13,710,854

Interest received 1,898,576 3,380,966 1,898,576 3,380,966

Taxation, APS and CSR paid (1,671,541) (1,063,449) (1,671,541) (1,063,449) Net cash (absorbed into)/generated from

operating activities (12,813,614) 16,028,371 (12,813,614) 16,028,371

Cash flows from investing activities

Acquisition of plant and equipment (692,873) (869,793) (692,873) (869,793)

Acquisition of intangible asset (139,255) - (139,255) -

Investment in financial asset (200,000) - (200,000) -

Sale of investment 119,175 - 119,175 - Net cash flows used in investing activities (912,953) (869,793) (912,953) (869,793)

Cash flows from financing activities

Movement in deposits - (2,000,000) - (2,000,000) Bonus and dividend paid (655,538) (745,552) (655,538) (745,552) Net cash flows used in financing activities (655,538) (2,745,552) (655,538) (2,745,552)

Net (decrease)/increase in cash and cash equivalents (14,382,105) 12,413,026 (14,382,105) 12,413,026

Movements in cash and cash equivalents

Cash and cash equivalents at the start of the year 20,003,933 7,590,907 20,003,933 7,590,907

Cash and cash equivalents at the end of the year 12 5,621,828 20,003,933 5,621,828 20,003,933

Net (decrease)/increase in cash and cash equivalents (14,382,105) 12,413,026 (14,382,105) 12,413,026

The accompanying notes on pages 11 to 32 form an integral part of these consolidated financial statements.

Auditors' Report on pages 3 to 5.

The SocietyThe Group

39

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2019

1. REPORTING ENTITY

2.

2.1 New and amended IFRS Standards that are effective for the current year

2.1.1 Impact of initial application of IFRS 9 Financial Instruments

1) The classification and measurement of financial assets and financial liabilities,

2) Impairment of financial assets, and

3) General hedge accounting.

(a) Classification and measurement of financial assets

Specifically:

The Mauritius Co-operative Agricultural Federation Limited (the “Society”) was founded on 16 August 1950 with the main

objective of promoting the economic interests of its affiliated societies. The main activities of the Society consist of sale and

distribution of agro-inputs, namely fertilizers, pesticides, seeds and other planters materials. It operates a network of 13 retail

outlets located in regions with a high concentration of planters. The registered office of the Society is situated at United Docks

Business Park Caudan, Port Louis.

• debt instruments that are held within a business model whose objective is to collect the contractual cash flows, and

that have contractual cash flows that are solely payments of principal and interest on the principal amount outstanding,

are measured subsequently at amortised cost;

• debt instruments that are held within a business model whose objective is both to collect the contractual cash flows

and to sell the debt instruments, and that have contractual cash flows that are solely payments of principal and interest

on the principal amount outstanding, are measured subsequently at fair value through other comprehensive income

(FVTOCI);

• all other debt investments and equity investments are measured subsequently at fair value through profit or loss

(FVTPL).

In the current year, the Group and the Society has applied IFRS 9 Financial Instruments (as revised in July 2014) and

the related consequential amendments to other IFRS Standards that are effective for an annual period that begins on or

after 1 January 2018. The transition provisions of IFRS 9 allow an entity not to restate comparatives. The Group and

the Society has accordingly elected not to restate comparatives in respect of the classification and measurement of

financial instruments.

APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs)

The Group and the Society adopted consequential amendments to IFRS 7 Financial Instruments: Disclosures that were

applied to the disclosures for 2018.

IFRS 9 introduced new requirements for:

Details of these new requirements as well as their impact on the Group and the Society’s financial statements are

described below.

The Group and the Society have applied IFRS 9 in accordance with the transition provisions set out in IFRS 9.

The date of initial application (i.e. the date on which the Group and the Society have assessed its existing financial

assets and financial liabilities in terms of the requirements of IFRS 9) is 1 January 2018. Accordingly, the Group and

the Society has applied the requirements of IFRS 9 to instruments that continue to be recognised as at 1 January 2018

and has not applied the requirements to instruments that have already been derecognised as at 1 January 2018.

All recognised financial assets that are within the scope of IFRS 9 are required to be measured subsequently at

amortised cost or fair value on the basis of the entity’s business model for managing the financial assets and the

contractual cash flow characteristics of the financial assets.

40

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2019

2.

2.1 New and amended IFRS Standards that are effective for the current year (Continued)

2.1.1 Impact of initial application of IFRS 9 Financial Instruments (Continued)

(a) Classification and measurement of financial assets (Continued)

(b) Impairment of financial assets

(1) Debt investments measured subsequently at amortised cost or at FVTOCI;

(2) Lease receivables;

(3) Trade receivables and contract assets; and

(4) Financial guarantee contracts to which the impairment requirements of IFRS 9 apply.

• financial assets classified as held-to-maturity and loans and receivables under IAS 39 that were measured at amortised

cost continue to be measured at amortised cost under IFRS 9 as they are held within a business model to collect

contractual cash flows and these cash flows consist solely of payments of principal and interest on the principal amount

outstanding.

In relation to the impairment of financial assets, IFRS 9 requires an expected credit loss model as opposed to an

incurred credit loss model under IAS 39. The expected credit loss model requires the Company to account for expected

credit losses and changes in those expected credit losses at each reporting date to reflect changes in credit risk since

initial recognition of the financial assets. In other words, it is no longer necessary for a credit event to have occurred

before credit losses are recognised.

Specifically, IFRS 9 requires the Company to recognise a loss allowance for expected credit losses on:

APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs)

(CONTINUED)

In the current year, the Group and the Society have not designated any debt investments that meet the amortised cost or

FVTOCI criteria as measured at FVTPL.

The directors of the Company reviewed and assessed the Company’s existing financial assets as at 1 January 2018

based on the facts and circumstances that existed at that date and concluded that the initial application of IFRS 9 has

had the following impact on the Company’s financial assets as regards their classification and measurement:

• the Group and the Society may irrevocably elect to present subsequent changes in fair value of an equity investment

that is neither held for trading nor contingent consideration recognised by an acquirer in a business combination in

other comprehensive income; and

• the Group and the Society may irrevocably designate a debt investment that meets the amortised cost or FVTOCI

criteria as measured at FVTPL if doing so eliminates or significantly reduces an accounting mismatch.

Despite the aforegoing, the Group and the Society may make the following irrevocable election/designation at initial

recognition of a financial asset:

When a debt investment measured at FVTOCI is derecognised, the cumulative gain or loss previously recognised in

other comprehensive income is reclassified from equity to profit or loss as a reclassification adjustment. When an

equity investment designated as measured at FVTOCI is derecognised, the cumulative gain or loss previously

recognised in other comprehensive income is subsequently transferred to retained earnings.

Debt instruments that are measured subsequently at amortised cost or at FVTOCI are subject to impairment. See (b)

below.

41

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2019

2.

2.1 New and amended IFRS Standards that are effective for the current year (Continued)

2.1.1 Impact of initial application of IFRS 9 Financial Instruments (Continued)

(b) Impairment of financial assets (Continued)

(c) Classification and measurement of financial liabilities

(d) General hedge accounting

APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs)

(CONTINUED)

A significant change introduced by IFRS 9 in the classification and measurement of financial liabilities relates to the

accounting for changes in the fair value of a financial liability designated as at FVTPL attributable to changes in the

credit risk of the issuer.

Specifically, IFRS 9 requires that the changes in the fair value of the financial liability that is attributable to changes in

the credit risk of that liability be presented in other comprehensive income, unless the recognition of the effects of

changes in the liability’s credit risk in other comprehensive income would create or enlarge an accounting mismatch in

profit or loss. Changes in fair value attributable to a financial liability’s credit risk are not subsequently reclassified to

profit or loss, but are instead transferred to retained earnings when the financial liability is derecognised. Previously,

under IAS 39, the entire amount of the change in the fair value of the financial liability designated as at FVTPL was

presented in profit or loss.

IFRS 9 requires hedging gains and losses to be recognised as an adjustment to the initial carrying amount of

non-financial hedged items (basis adjustment). In addition, transfers from the hedging reserve to the initial carrying

amount of the hedged item are not reclassification adjustments under IAS 1 Presentation of Financial Statements and

hence they do not affect other comprehensive income. Hedging gains and losses subject to basis adjustments are

categorised as amounts that will not be subsequently reclassified to profit or loss in other comprehensive income.

The application of the IFRS 9 hedge accounting requirements has had no significant impact on the results and financial

position of the Group and the Society for the current and/or prior years.

The application of IFRS 9 has had no impact on the classification and measurement of the Group and the Society’s

financial liabilities.

The new general hedge accounting requirements retain the three types of hedge accounting. However, greater flexibility

has been introduced to the types of transactions eligible for hedge accounting, specifically broadening the types of

instruments that qualify for hedging instruments and the types of risk components of non-financial items that are

eligible for hedge accounting. In addition, the effectiveness test has been replaced with the principle of an ‘economic

relationship’. Retrospective assessment of hedge effectiveness is also no longer required. Enhanced disclosure

requirements about the Group and the Society’s risk management activities have also been introduced.

In particular, IFRS 9 requires the Group and the Society to measure the loss allowance for a financial instrument at an

amount equal to the lifetime expected credit losses (ECL) if the credit risk on that financial instrument has increased

significantly since initial recognition, or if the financial instrument is a purchased or originated credit-impaired

financial asset. However, if the credit risk on a financial instrument has not increased significantly since initial

recognition (except for a purchased or originated credit-impaired financial asset), the Group and the Society are

required to measure the loss allowance for that financial instrument at an amount equal to 12-months ECL. IFRS 9 also

requires a simplified approach for measuring the loss allowance at an amount equal to lifetime ECL for trade

receivables, contract assets and lease receivables in certain circumstances.

The directors of the Company have assessed that there has been no significant increase in credit risk since initial

recognition of financial instruments that remain recognised on the date of initial application of IFRS 9 (i.e. 01 January

2018).

42

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2019

2.

2.1 New and amended IFRS Standards that are effective for the current year (Continued)

2.1.1 Impact of initial application of IFRS 9 Financial Instruments (Continued)

(e) Disclosures in relation to the initial application of IFRS 9

(f) Impact of initial application of IFRS 9 on financial performance and cash flows

2.1.2 Impact of application of IFRS 15 Revenue from Contracts with Customers

2.2 Amendments to IFRS Standards and Interpretations that are effective for the current year

The Group and the Society’s accounting policies for its revenue streams are disclosed in detail in note 3(e) below.

Apart from providing more extensive disclosures for the Group and the Society’s revenue transactions, the application

of IFRS 15 has not had a significant impact on the financial position and/or financial performance of the Group and the

Society.

In the current year, the Group and the Society have applied a number of amendments to IFRS Standards and

Interpretations issued by the International Accounting Standards Board (IASB) that are effective for an annual period

that begins on or after 1 January 2018. Their adoption has not had any material impact on the disclosures or on the

amounts reported in these financial statements.

IFRS 15 uses the terms ‘contract asset’ and ‘contract liability’ to describe what might more commonly be known as

‘accrued revenue’ and ‘deferred revenue’, however the Standard does not prohibit an entity from using alternative

descriptions in the statement of financial position. The Company has adopted the terminology used in IFRS 15 to

describe such balances.

APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs)

(CONTINUED)

There were no financial assets or financial liabilities which the Group and the Society had previously designated as at

FVTPL under IAS 39 that were subject to reclassification or which the Group and the Society have elected to reclassify

upon the application of IFRS 9. There were no financial assets or financial liabilities which the Group and the Society

have elected to designate as at FVTPL at the date of initial application of IFRS 9.

The application of IFRS 9 has had no impact on the financial performance of the Group and the Society.

The application of IFRS 9 has had no impact on the cash flows of the Group and the Society.

In the current year, the Group and the Society have applied IFRS 15 Revenue from Contracts with Customers (as

amended in April 2016) which is effective for an annual period that begins on or after 1 January 2018. IFRS 15

introduced a 5-step approach to revenue recognition. Far more prescriptive guidance has been added in IFRS 15 to deal

with specific scenarios. Details of the new requirements as well as their impact on the Group and the Society’s financial

statements are described below.

The Group and the Society have applied IFRS 15 in accordance with the fully retrospective transitional approach

without using the practical expedients for completed contracts in IFRS 15:C5(a), and (b), or for modified contracts in

IFRS 15:C5(c) but using the expedient in IFRS 15:C5(d) allowing both non-disclosure of the amount of the transaction

price allocated to the remaining performance obligations, and an explanation of when it expects to recognise that

amount as revenue for all reporting periods presented before the date of initial application, i.e. 01 January 2018.

43

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2019

2.

2.2 Amendments to IFRS Standards and Interpretations that are effective for the current year (Continued)

(iv) Amendments to IAS 28 Investments in Associates and Joint Ventures

(v) IFRIC 22 Foreign Currency Transactions and Advance Consideration

2.3 New and revised IFRS Standards in issue but not yet effective

Effective for annual periods beginning on or after

1 January 2019

1 January 2021

1 January 2019

1 January 2019

1 January 2019

1 January 2019

The effective date of the amendments has yet to

be set by the IASB

1 January 2019

Description

IFRS 10 Consolidated Financial Statements and IAS 28 (amendments) -

Sale or Contribution of Assets between an Investor and its Associate or

Joint Venture

IFRIC 23 - Uncertainty over Income Tax Treatments

The directors do not expect that the adoption of the Standards listed above will have a material impact on the financial

statements of the Group and the Society in future periods.

IFRS 16 - Leases

IFRS 17 - Insurance Contracts

Amendments to IFRS 9 - Prepayment Features with Negative

Compensation

Amendments to IAS 28 - Long-term Interests in Associates and Joint

Ventures

Annual Improvements to IFRS Standards 2015–2017 Cycle - Amendments

to IFRS 3 Business Combinations, IFRS 11 Joint Arrangements, IAS 12

Income Taxes and IAS 23 Borrowing Costs

Amendments to IAS 19 Employee Benefits - Plan Amendment,

Curtailment or Settlement

APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs)

(CONTINUED)

(i) IFRS 2 (amendments) Classification

(ii) IAS 40 (amendments) Transfers of Investment Property

(iii) Annual Improvements to IFRS Standards 2014 – 2016 Cycle

As at the date of these financial statements,the Group and the Society have not adopted the following standards that

have been issued but are not yet effective:

44

THE MAURITIUS CO-OPERATIVE AGRICULTURAL FEDERATION LIMITED AND ITS SUBSIDIARYNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2019

3. SIGNIFICANT ACCOUNTING POLICIES

(a) Statement of compliance

(b) Basis of preparation

(c) Basis of consolidation

(d) Investment in subsidiaries

(e) Revenue recognition

(f) Expense recognition

(g) Property, Plant and equipment

Building 4%

Freehold building 2%

Office equipment 20%

Furniture, fixtures and fittings 10%

Motor vehicles 20%

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) including

International Accounting Standards (IAS) and interpretations of the International Financial Reporting Interpretations

Committee (IFRIC) issued by the International Accounting Standards Board (IASB).

The consolidated financial statements comprise the financial statements of the Group and its subsidiary as at 30 June 2019.

Subsidiaries are fully consolidated from the date of acquisition, being the date on which the Group obtains control, and

continue to be consolidated until the date when such control ceases. The financial statements of the subsidiaries are prepared

for the same reporting period as the parent Society, using consistent accounting policies. All intra-group balances,

transactions, unrealised gains and losses resulting from intra-group transactions and dividends are eliminated in full. Where

ownership of a subsidiary is less than 100%, and therefore a non-controlling interest/s exists, any losses of that subsidiary are

attributed to the non-controlling interest/s even if that results in a deficit balance. A change in ownership interest of a