May 2018 Edition · Pending Sell Recommendation TC PipeLines LP (TCP) ..... 4 The Retirement Top 10...

40

Sure Retirement Newsletter HIGH-YIELD, HIGH-QUALITY INVESTMENTS May 2018 Edition By Ben Reynolds, Nick McCullum, & Bob Ciura Edited by Brad Beams Published on May 13 th , 2018

Transcript of May 2018 Edition · Pending Sell Recommendation TC PipeLines LP (TCP) ..... 4 The Retirement Top 10...

Sure Retirement Newsletter

HIGH-YIELD, HIGH-QUALITY INVESTMENTS

May 2018 Edition

By Ben Reynolds, Nick McCullum, & Bob Ciura

Edited by Brad Beams

Published on May 13th, 2018

2

Table of Contents

Opening Thoughts - High Payout Ratios & Valuation - ........................................................... 3

Pending Sell Recommendation TC PipeLines LP (TCP) .......................................................... 4

The Retirement Top 10 – May 2018 ............................................................................................ 5

Analysis of Top 10 Securities ....................................................................................................... 6

Owens & Minor Inc. (OMI) ........................................................................................................ 6

Energy Transfer Equity LP (ETE) .............................................................................................. 8

Invesco Ltd (IVZ) ..................................................................................................................... 10

Senior Housing Properties Trust (SNH) ................................................................................... 12

AT&T Inc. (T) .......................................................................................................................... 14

Buckeye Partners LP (BPL) ...................................................................................................... 16

Energy Transfer Partners LP (ETP) .......................................................................................... 18

Omega Healthcare Investors Inc. (OHI) ................................................................................... 20

Altria Group Inc. (MO) ............................................................................................................. 22

Enterprise Products Partners LP (EPD) .................................................................................... 24

Closing Thoughts – Announcements & Improvements – ....................................................... 26

List of Investments by Sector ..................................................................................................... 27

List of Investments by Rank ...................................................................................................... 30

List of Past Recommendations & Ranking Criteria ............................................................... 32

Portfolio Building Guide ............................................................................................................ 34

Examples ................................................................................................................................... 34

Tax Guide .................................................................................................................................... 35

Corporations .............................................................................................................................. 36

Master Limited Partnerships (MLPs)........................................................................................ 37

Real Estate Investment Trusts (REITs)..................................................................................... 38

Business Development Companies (BDCs) ............................................................................. 39

Glossary of Common Terms & Acronyms ............................................................................... 40

3

Opening Thoughts - High Payout Ratios & Valuation -

There’s something special about the combination of a high payout ratio and a low valuation.

Together, they allow investors to get a ‘double benefit’ from low valuations. An example is below

to demonstrate this phenomenon.

Imagine two stocks, stock A and stock B. The relevant characteristics for each are below:

Stock A: 100% payout ratio, fair value P/E of 20, does not reinvest for growth and therefore has

0% expected EPS growth.

Stock B: 0% payout ratio, fair value P/E of 20, reinvests all profits into growth and grows at 5%

per year.

At fair value, both of these stocks generate expected total returns of 5%. Stock A would have a 5%

yield with a P/E of 20 and a 100% payout ratio. Stock B would generate 5% expected total returns

from its growth prospects.

Now if both stocks were to fall to a P/E ratio of 10 (and fair value was still a P/E of 20), they would

no longer have the same expected total returns.

Before valuation multiple changes, Stock A would now yield 10% because a P/E ratio of 10

combined with a 100% payout ratio equates to a 10% yield. The P/E ratio multiplied by the payout

ratio equals the dividend yield. Stock B would still have expected total returns before valuation

multiple gains of 5% as its growth investments aren’t affected by its stock price valuation.

Returns from business growth are not tied to valuation. Returns from returns of capital to

shareholders (dividends and share repurchases) are tied to valuation. Expected future total returns

excluding expected valuation multiple gains get better for companies with high payout ratios as

their valuations fall. The same does not hold for stocks that don’t return capital to shareholders.

In the real world, investing isn’t quite as simple as the example above. There are however, two

classes of stocks that are required to sustain very high payout ratios – REITs and MLPs. We are

seeing tremendous value in the MLP industry in particular today. In addition to the normal boost

an undervalued stock gets as we expect it to return to fair value, MLPs pay out the majority of their

cash flows to unitholders as distributions. This fact gives them especially high expected total

returns when they are deeply undervalued.

By the same token, MLPs and REITs also make particularly poor investments when they are

overvalued.

It should be noted that the link between valuation and payout ratios only applies to new purchases.

Your yield on cost doesn’t change with valuation multiples going forward.

In closing this month’s opening thoughts, we have a special pending sell report section on the

following page for TC PipeLines (TCP). Additionally, please see the Closing Thoughts section

for important improvements we’ve made to the Sure Retirement Newsletter this month.

4

Pending Sell Recommendation TC PipeLines LP (TCP)

TC PipeLines was last recommended in the April 2018 Sure Retirement Newsletter. More recently,

the partnership announced a distribution reduction. TC PipeLines is reducing its quarterly

distribution payment from $1.00/share to $0.65/share; a 35% decline.

The distribution cut was announced at the same time as the company’s first quarter earnings, on

May 2nd. The partnership’s distributable cash flow per share grew 16.8% versus the same quarter a

year ago. Robust growth is not typically a cause for a distribution reduction.

The reason TC PipeLines elected to reduce its distribution is because of a recent Federal Energy

Regulatory Commission (FERC) ruling. The new ruling does not allow for income tax recovery in

certain cases for pipelines. It’s important to note that not all pipelines will be affected as severely

as TC PipeLines. In fact, many pipelines do not expect the ruling to significantly impact their

operations.

With that said, the ruling will seriously impact TC PipeLines’ operations. The partnership is

expecting revenue to decline by approximately $100 million. This is significant given that the

company generated $425 million in revenue over the last 12 months. The TC PipeLines dividend

cut will save the partnership roughly the amount of money the FERC ruling will cost it.

Because TC PipeLines cut its distribution, we recommend selling TC PipeLines when the time is

right. Now is not that time. The partnership still has a robust 10.1% distribution yield after

accounting for the recent reduction. For comparison, the partnership’s historical average yield over

the last decade is around 7.0%. TC PipeLines is currently undervalued.

Also, the partnership has two potential catalysts that are likely to improve its valuation in the next

year or so. The first catalyst is converting from an MLP to a C-Corporation. TC PipeLines’

management expects this move would save the partnership $20 million to $30 million a year. This

would reduce the impact of the FERC ruling 20% to 30%. The bigger catalyst involves TC

PipeLines’ parent company.

TransCanada Corporation (TRP) is TC PipeLines’ parent company. TransCanada has a market cap

of $38 billion, versus $1.8 billion for TC PipeLines. In addition, TransCanada is TC PipeLines’

general partner, and also already owns 24% of TC PipeLines. The reason TC PipeLines exists is

because it was a more tax efficient way to access capital markets and distribute cash flows to

shareholders for TransCanada. This logic no longer holds true. As a result, we believe it is likely

that TransCanada acquires the remaining 76% interest in TC PipeLines. Indeed, TransCanada

could acquire TC PipeLines at a discount; the stock price is down more than 50% in the last year.

Due to the catalysts above, we recommend investors who purchased TC PipeLines hold for now

and only sell when: (1) TC PipeLines’ distribution yield declines to 8% (which we believe is

around fair value), or (2) TransCanada enters into an agreement to purchase TC PipeLines. We

will be monitoring TC PipeLines and will provide a final sell update when the time is right.

5

The Retirement Top 10 – May 2018

Name Type Price Fair Value Yield Payout Growth Beta

Owens & Minor (OMI) Stock $16 $29 6.7% 52% 11.0% 1.77

Energy Transfer Equity (ETE) MLP $16 $24 7.4% 68%1 8.5% 1.48

Invesco (IVZ) Stock $28 $41 4.2% 44% 10.5% 0.92

Senior Housing Prop. (SNH) REIT $16 $21 9.5% 85%2 2.0% 0.16

AT&T (T) Stock $32 $46 6.3% 58% 5.0% 0.41

Buckeye Partners (BPL) MLP $40 $72 12.2% 111%3 7.5% 2.04

Energy Transfer Partn. (ETP) MLP $19 $25 12.1% 87%4 6.5% 1.68

Omega Healthcare (OHI) REIT $29 $37 9.3% 85%5 9.0% -0.32

Altria Group (MO) Stock $56 $64 5.0% 74% 10.5% 0.83

Enterprise Products (EPD) MLP $27 $31 6.2% 67%6 10.0% 1.06

Notes: The ‘Price’ column shows a recent price of the security. The ‘Fair Value’ column shows

our estimate of the company’s per-share fair value. True fair value is unknowable. The ‘Payout’

column uses earnings, funds from operations, or distributable cash flow in the denominator. The

numerator is the security’s payment to its owner.

Three recommendations have changed from last month. TC PipeLines (TCP), Holly Energy

Partners (HEP), and Welltower (WELL) have been replaced by Invesco (IVZ), AT&T (T), and

Altria (MO). The stability of the Top 10 list shows the ranking method is consistent, not based on

rapid swings. Remember: Securities that fall out of the Top 10 are holds, not sells.

Note: Dividend or distribution yields are used for valuation in some of the individual company

analyses below instead of price-to-earnings (P/E) ratios, which are not meaningful for MLPs and

REITs.

An equal weighted portfolio of the Top 10 has the following characteristics:

Payout Ratio: 73%

Dividend or Distribution Yield: 7.9%

Growth Rate: 8.1%

1 Using distributable cash flow (DCF). 2 Using funds from operations (FFO). 3 Using distributable cash flow (DCF). Despite the company’s above 100% payout ratio, Buckeye’s management team has stated that

it has no intention of cutting its distribution. See our written analysis for more details. 4 Using distributable cash flow (DCF). 5 Using funds from operations (FFO). 6 Using distributable cash flow (DCF).

Note: Data for the rankings, Top 10 summary page, and yield images is through the market close as of 5/10/18 but very occasionally

5/11/18 when there are large changes at the week’s market close. Data elsewhere is from between market close 5/10/18 and market

close 5/11/18.

6

Analysis of Top 10 Securities

Owens & Minor Inc. (OMI) Key Statistics, Ratios & Metrics

Dividend Yield: 6.7% 10 Year Dividend Growth Rate: 11.5%

Most Recent Annual Dividend Increase: 0.8% Sector: Healthcare

Dividend History: 20 years of increases Business Type: Corporation

Ex-Dividend Date: 6/14/18 Payment Date: 7/2/18

Overview & Current Events

Owens & Minor is a healthcare distribution, transportation, and data analytics company. It provides

healthcare products for hospitals and other medical centers. In all, Owens & Minor distributes

approximately 220,000 medical and surgical supplies to roughly 4,400 hospitals. Its other clients include group purchasing organizations, the federal government, and at-home healthcare patients.

In early May, Owens & Minor released (5/10/18) financial results for the second quarter of fiscal 2018. Consolidated revenues increased by 1.9% while GAAP earnings-per-share fell to $0.13 from $0.31 in

the prior year’s period. Excluding one-time accounting charges, results were far better. Adjusted

earnings-per-share of $0.43 fell slightly from the $0.44 reported in the prior year’s period. While the

company’s performance fell slightly short of expectations, shares rose by nearly 4% after the report.

Growth Prospects & Safety

Despite experiencing struggles over the last year, we believe Owens & Minor still has positive long-

term growth potential. Its strategic growth initiatives include expansion into new products and

services, primarily through acquisitions. For example, the company acquired Byram Healthcare, a

distributor of direct-to-patient medical supplies. This acquisition boosted Owens & Minor’s position in

at-home healthcare. Byram added $118 million to Owens & Minor’s first-quarter revenue.

Owens & Minor also recently closed (4/30/18) on its acquisition of the surgical and infection

prevention (S&IP) business of Halyard Health. This deal expands Owens & Minor’s portfolio to include new medical supplies like sterilization wraps, surgical drapes and gowns, and medical exam

gloves. These acquisitions will help the company enter new, high-growth product markets.

Owens & Minor’s earnings-per-share will suffer in the short-term from investment spending, but the

long-term benefits are clear. The company believes it can achieve a long-term annual earnings growth

rate of 8% to 10% after the various acquisitions are completed. In addition, Owens & Minor’s current

dividend payment combined with 2018 earnings estimates imply a forward dividend payout ratio of

just 52%, giving plenty of room for dividend growth if earnings stall temporarily.

Valuation

Consensus estimates call for earnings-per-share of $2.00 for Owens & Minor in 2018. As a result, the

stock trades for a price-to-earnings ratio of just 8.0. We believe the stock deserves a price-to-earnings

ratio of 14-15, since Owens & Minor has strong customer relationships and a highly profitable business model. We estimate a fair value price of $29 for Owens & Minor. Therefore, the stock seems to be

significantly undervalued.

If the share price rose back to our fair value estimate, buyers at the current price would earn a return of approximately 81%, just from share price appreciation. In addition, Owens & Minor has a dividend

yield of 6.7%. Because of a rising valuation, earnings growth, and dividends, the stock has significant

total return potential that could exceed 20% per annum if market pessimism eventually dissipates.

7

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Owens & Minor (OMI) Dividend Yield History

8

Energy Transfer Equity LP (ETE)

Key Statistics, Ratios & Metrics Distribution Yield: 7.4% 10 Year Dist. Growth Rate: 10.7%

Most Recent Annual Distribution Increase: 7.0% Sector: Energy

Distribution History: Steady or increasing since 2008 Business Type: MLP

Ex-Distribution Date: 5/4/18 Payment Date: 5/21/18

Overview & Current Events

Energy Transfer Equity is a master limited partnership (MLP) which owns the General Partner and

100% of the incentive distribution rights (IDRs) of Energy Transfer Partners LP and Sunoco LP. ETE

also owns Lake Charles LNG Company. Energy Transfer’s subsidiary companies own and operate a

diverse portfolio of natural gas, natural gas liquids, refined products, and crude oil pipelines; as well as

retail and wholesale motor fuel operations and natural gas liquids terminals.

In early May, Energy Transfer Equity reported (5/9/18) first-quarter financial results. Revenue of

$11.9 billion missed analyst estimates by $40 million but rose 23% from the same quarter a year ago.

Distributable cash flow, as adjusted, increased 84% year-over-year.

Separately, ETE stock fell on news that the Federal Energy Regulatory Commission (FERC) will no

longer allow MLPs to recover an income tax allowance in cost-of-service rates. All MLPs sold off on

the news, but Energy Transfer Equity stated in a press release (3/15/18) that most of its rates are set by negotiated rate agreements, and thus would not be subject to adjustment. As a result, we believe the

FERC news is immaterial for Energy Transfer Equity investors.

Growth Prospects & Safety

Going forward, Energy Transfer Equity’s primary growth catalyst is new pipeline projects for its

subsidiary companies. For example, growth for the first quarter was primarily due to an increase of

$183 million in General Partner and incentive distributions from Energy Transfer Partners. In addition,

Energy Transfer Partners recently announced (5/10/18) it will build a crude oil pipeline from the

Permian Basin in west Texas to the Houston Ship Channel and Nederland, Texas. The pipeline will have an initial capacity of up to 600,000 barrels per day, with future expansion capacity up to 1 million

barrels per day. The company expects the pipeline will be completed by 2020.

Energy Transfer Equity will also pursue growth through acquisitions. For example, in the first quarter

the company acquired the general partner of USA Compression Partners LP (USAC) and

approximately 12.5 million USAC common units.

In terms of safety, Energy Transfer Equity scores fairly well for an MLP. It reported a distribution

coverage ratio of 1.48x in the 2018 first quarter, which means the company generated 48% more

distributable cash flow than it needed to pay distributions. The coverage ratio improved considerably

from 0.86x in the 2017 first quarter. This indicates the distribution is sustainable.

Valuation

Energy Transfer Equity is expected to generate distributable cash flow of $3.50 per unit in 2018. The MLP currently trades for a price-to-DCF ratio of 4.7, a very low valuation that indicates the units are

undervalued. We estimate a fair value price of $24 for Energy Transfer Equity, which would equate to

a price-to-DCF ratio of nearly 7, a more reasonable valuation for a high-quality MLP. Over the next

five years, an expanding valuation could add significantly to the MLP’s annual returns. Altogether,

annual returns could reach nearly 20% over the next five years.

9

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Energy Transfer Equity (ETE) Dividend Yield History

10

Invesco Ltd (IVZ)

Key Statistics, Ratios & Metrics Dividend Yield: 4.3% 10 Year Dividend Growth Rate: 11.1%

Most Recent Annual Dividend Increase: 7.1% Sector: Financials

Dividend History: Steady or increasing since 2008 Business Type: Corporation

Ex-Dividend Date: 5/10/18 Payment Date: 6/1/18

Overview & Current Events

Invesco is an investment management firm that provides a wide variety of asset management,

investing, and financial planning products and services. The company serves retail, institutional, and

wealth management customers around the world. Invesco has more than 7,000 employees and serves

clients in more than 150 countries. The company has a market capitalization of $11.6 billion.

In late April, Invesco reported (4/26/18) first-quarter financial results. Revenue of $958 million missed

analyst expectations by $20 million, but revenue increased 10.5% year-over-year. This was a very

healthy revenue growth rate. Earnings-per-share of $0.67 rose 10% from the same quarter a year ago

and beat analyst expectations by $0.01 per share.

Separately, Invesco announced (5/10/18) April assets under management (AUM) of $934 billion.

Growth was due to the Guggenheim acquisition, and favorable market returns, which were partially

offset by net long-term outflows, and unfavorable foreign exchange fluctuations.

Growth Prospects & Safety

AUM growth is the major performance driver for investment management firms like Invesco. The

strong recent performance of the U.S. and international markets has contributed to stronger demand for

investment products. If the markets continue to do well, Invesco’s AUM should continue to rise. In addition, growth will come from rising interest rates. Higher interest rates help Invesco generate higher

returns on its investments, particularly fixed income. Invesco is also pursuing growth through

acquisitions. In early April, Invesco completed (4/6/18) the acquisition of Guggenheim Investments’

ETF business for $1.2 billion. This acquisition will enhance Invesco’s product offerings in exchange-

traded funds, an emerging asset management class that is seeing growing demand.

Invesco has significant competitive advantages in the asset management industry and operates with a

sound balance sheet. The company has credit ratings of A2 and A from Moody’s and Standard &

Poor’s, respectively, which are critical for a financial services firm. Strong credit ratings allow an

investment management firm to uphold a reputation of financial integrity, which helps retain and grow the client base. Invesco has generated nine consecutive years of positive long-term net inflows. In

addition, the company held a dividend payout ratio of 44% last year. Still, investors should note that

the performance of asset management firms will fluctuate along with the financial markets due to their

dependence on assets under management.

Valuation Analysts expect Invesco to generate earnings-per-share of $2.85 in 2018. Based on this, Invesco stock

trades for a price-to-earnings ratio of 9.9. We believe a fair valuation for Invesco is a price-to-earnings

ratio of 14-15. As a result, our fair value price estimate for Invesco shares is approximately $41. The

stock currently trades at $28. Over the next five years, a rising valuation could add approximately 7%

to 8% to total returns. In addition, we believe Invesco can reasonably generate annual earnings growth of 6%. When accounting for with the firm’s 4.3% dividend yield, Invesco’s total returns could reach

over 17% per year.

11

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Invesco (IVZ) Dividend Yield History

12

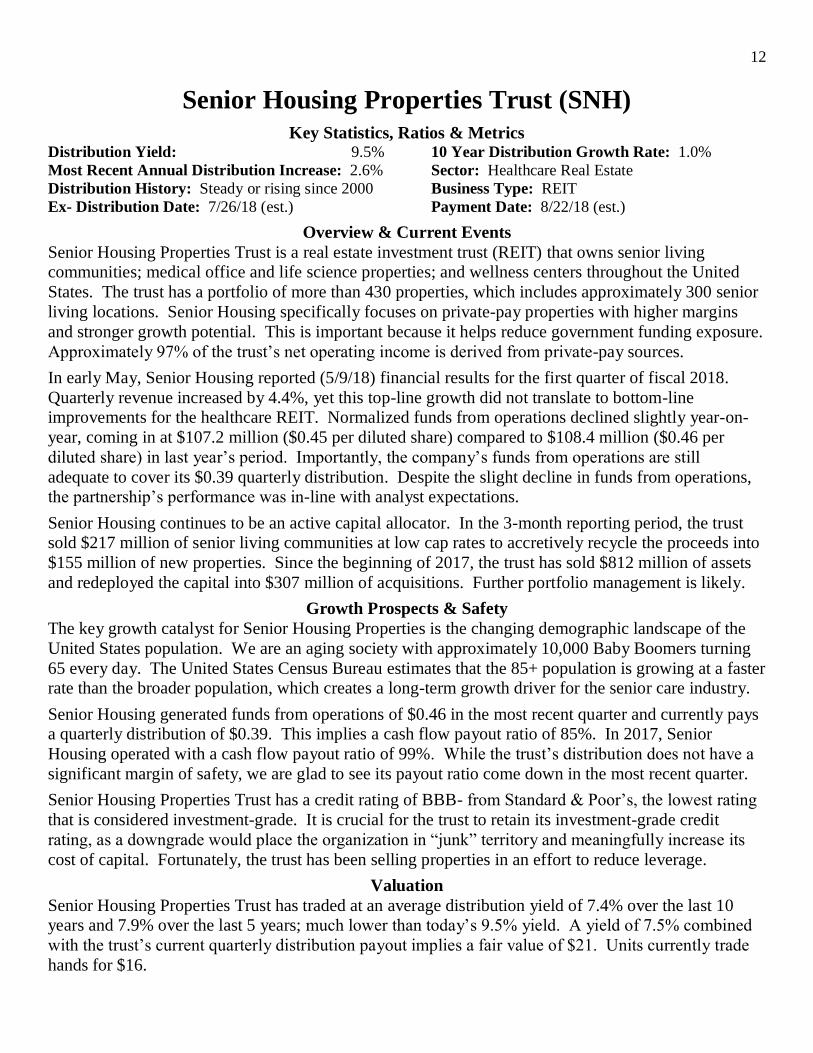

Senior Housing Properties Trust (SNH)

Key Statistics, Ratios & Metrics Distribution Yield: 9.5% 10 Year Distribution Growth Rate: 1.0%

Most Recent Annual Distribution Increase: 2.6% Sector: Healthcare Real Estate

Distribution History: Steady or rising since 2000 Business Type: REIT

Ex- Distribution Date: 7/26/18 (est.) Payment Date: 8/22/18 (est.)

Overview & Current Events

Senior Housing Properties Trust is a real estate investment trust (REIT) that owns senior living

communities; medical office and life science properties; and wellness centers throughout the United

States. The trust has a portfolio of more than 430 properties, which includes approximately 300 senior

living locations. Senior Housing specifically focuses on private-pay properties with higher margins

and stronger growth potential. This is important because it helps reduce government funding exposure.

Approximately 97% of the trust’s net operating income is derived from private-pay sources.

In early May, Senior Housing reported (5/9/18) financial results for the first quarter of fiscal 2018.

Quarterly revenue increased by 4.4%, yet this top-line growth did not translate to bottom-line improvements for the healthcare REIT. Normalized funds from operations declined slightly year-on-

year, coming in at $107.2 million ($0.45 per diluted share) compared to $108.4 million ($0.46 per

diluted share) in last year’s period. Importantly, the company’s funds from operations are still

adequate to cover its $0.39 quarterly distribution. Despite the slight decline in funds from operations, the partnership’s performance was in-line with analyst expectations.

Senior Housing continues to be an active capital allocator. In the 3-month reporting period, the trust sold $217 million of senior living communities at low cap rates to accretively recycle the proceeds into

$155 million of new properties. Since the beginning of 2017, the trust has sold $812 million of assets

and redeployed the capital into $307 million of acquisitions. Further portfolio management is likely.

Growth Prospects & Safety

The key growth catalyst for Senior Housing Properties is the changing demographic landscape of the

United States population. We are an aging society with approximately 10,000 Baby Boomers turning

65 every day. The United States Census Bureau estimates that the 85+ population is growing at a faster rate than the broader population, which creates a long-term growth driver for the senior care industry.

Senior Housing generated funds from operations of $0.46 in the most recent quarter and currently pays a quarterly distribution of $0.39. This implies a cash flow payout ratio of 85%. In 2017, Senior

Housing operated with a cash flow payout ratio of 99%. While the trust’s distribution does not have a

significant margin of safety, we are glad to see its payout ratio come down in the most recent quarter.

Senior Housing Properties Trust has a credit rating of BBB- from Standard & Poor’s, the lowest rating

that is considered investment-grade. It is crucial for the trust to retain its investment-grade credit

rating, as a downgrade would place the organization in “junk” territory and meaningfully increase its

cost of capital. Fortunately, the trust has been selling properties in an effort to reduce leverage.

Valuation

Senior Housing Properties Trust has traded at an average distribution yield of 7.4% over the last 10 years and 7.9% over the last 5 years; much lower than today’s 9.5% yield. A yield of 7.5% combined

with the trust’s current quarterly distribution payout implies a fair value of $21. Units currently trade

hands for $16.

13

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Senior Housing Properties Trust (SNH) Dividend Yield History

14

AT&T Inc. (T)

Key Statistics, Ratios & Metrics Dividend Yield: 6.3% 10 Year Dividend Growth Rate: 2.3%

Most Recent Annual Dividend Increase: 2.0% Sector: Telecommunications

Dividend History: 34 years of increases Business Type: Corporation

Ex-Dividend Date: 7/6/18 (est.) Payment Date: 8/1/18 (est.)

Overview & Current Events

AT&T is a diversified telecommunications company with a market capitalization of $196 billion. It

offers a variety of telecom services, including wireless and cable TV, as well as satellite TV through its

subsidiary DirecTV. It operates through the following business segments: Business Solutions, Entertainment Group, Consumer Mobility, and International.

In late April, AT&T reported (4/25/18) first-quarter financial results. AT&T generated revenue of

$38.04 billion and earnings-per-share of $0.85. Both figures came up short of expectations. Revenue

and earnings-per-share missed analyst estimates by $1.27 billion and $0.02 per share, respectively. Revenue declined 2.3% from the same quarter a year ago. AT&T saw sales growth of wireless

equipment and strategic business services, but this was more than offset by declines in legacy wireline

services, domestic video, and wireless service revenues. For the quarter, AT&T had 3.2 million total

wireless net adds, and churn of just 0.84%, the lowest first-quarter churn rate in the company’s history.

Growth Prospects & Safety

The telecommunications industry is highly saturated and competitive. As a result, consolidation is the

best path for future growth. To that end, AT&T is currently attempting to acquire content giant Time

Warner for $85 billion. Time Warner has a number of strong media properties, including TBS, TNT, HBO, and the Warner Bros. movie studio. If the Time Warner acquisition receives approval, the

combined company would have over 140 million mobile subscribers, and another 45 million video

subscribers worldwide. However, in November 2017 the Department of Justice sued to block the

proposed transaction on antitrust grounds. The main portion of the trial recently concluded, with a

final decision expected on June 12th. Investors will soon know the fate of the acquisition.

AT&T’s dividend is very safe, and the company is a Dividend Aristocrat with 34 years of dividend

growth. Based on 2018 guidance, the company is on pace for a dividend payout ratio of 58%.

AT&T has a considerable amount of debt, and it will incur even more if and when the Time Warner deal gets approved. AT&T ended the 2018 first quarter with $133.7 billion of long-term debt. To help

mitigate the risk of rising interest rates, AT&T has a balanced maturity schedule. It also has a solidly

investment-grade credit rating of BBB+ from Standard & Poor’s, which will help keep its cost of

capital manageable.

Valuation

AT&T is expected to generate adjusted earnings-per-share of $3.45 in 2018. AT&T stock currently

trades for a price-to-earnings ratio of just 9.2, compared with an average of 13.4 over the past 10 years.

Therefore, we believe the stock is significantly undervalued, and the expanding price-to-earnings ratio

could add 8% to shareholder returns each year if mean reversion occurred over a 5-year period. We estimate a fair value price of $46 for AT&T shares.

Even assuming relatively low earnings growth of 2% per year, AT&T can still provide high returns. Including the impact of a rising valuation, earnings growth, and dividends, we forecast total returns of

16% per year for AT&T if the telecom can revert to its long-term average valuation multiple.

15

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

AT&T (T) Dividend Yield History

16

Buckeye Partners LP (BPL) Key Statistics, Ratios, & Metrics

Distribution Yield: 12.2% 10 Year Distribution Growth Rate: 3.9% Most Recent Annual Distribution Increase: 4.1% Sector: Energy

Distribution History: 19 years of increases Business Type: MLP

Ex-Distribution Date: 5/11/18 Payment Date: 5/21/18

Overview & Current Events

Buckeye Partners is a midstream energy master limited partnership (MLP). The partnership operates

approximately 6,000 miles of pipelines and more than 135 liquid petroleum terminals with over 176

million barrels of total storage capacity. Approximately 95% of the partnership’s EBITDA comes from

fee-based sources. Buckeye’s pipelines and terminals are located in the East Coast, Midwest, and Gulf

Coast regions of the United States. The partnership also has a significant international presence that includes a 50% interest in VTTI, an international provider of energy storage solutions.

In early May, Buckeye reported (5/4/18) financial results for the first quarter of 2018. The partnership’s performance was worse than expected. Net income declined to $112.4 million from

$123.6 million in last year’s quarter, while adjusted EBITDA of $261.7 million declined from the

$277.5 million reported in the first quarter of 2017. Distributable cash flow of $169.2 million also

declined from the $190.7 million reported in last year’s quarter and did not adequately cover Buckeye’s distribution payments. The partnership reported a distribution coverage ratio of 0.91 in the quarter.

Challenging market conditions were to blame for Buckeye’s poor quarterly performance. The

partnership’s common units fell as much as 11% following the announcement.

Growth Prospects & Safety

Buckeye’s future growth will be fueled by new capital projects. For example, its South Texas Gateway

project calls for the construction of a 600-mile long-haul pipeline with total expected capacity of

approximately 400,000 barrels per day. Once completed, it will significantly expand Buckeye’s distribution capabilities in the high-quality Permian Basin. The project is set for completion in 2019.

Another project set to ramp up shortly is the Michigan/Ohio expansion project. Buckeye has secured 10-year commitments from oil customers, totaling 50,500 barrels per day. Phase two of the project is

expected to be completed by the end of 2018 and is projected to add 40,000 barrels per day of capacity.

On the partnership’s first quarter conference call, Buckeye’s Chief Executive Officer stated that 2018

should be a transitional year. Market conditions for segregated storage “remain challenged” and the

partnership does not expect to realize meaningful gains from current capital projects until 2019 or

2020. Accordingly, Buckeye is expecting to report a distribution coverage rate between 0.9 and 0.95

for the full year of fiscal 2018, with coverage returning to above 1.0 in the fourth quarter. Importantly, Buckeye’s CEO also stated, “our Board of Directors remain committed to our current distribution

policy,” and “we have no intention of cutting Buckeye’s distribution.”

Valuation

Buckeye Partners traded at an average distribution yield of 7.0% over the last 5 years and 7.1% over

the last 10 years. The partnership’s current distribution yield of 12.2% indicates that it is meaningfully

undervalued at current prices. A yield of 7% combined with the partnership’s current quarterly

distribution implies a fair value of $72. Units currently trade hands for under $40. We note that it may be several years before Buckeye’s valuation reverts to its historical levels, but the partnership’s high

yield rewards the patient investors who are willing to invest today.

17

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Buckeye Partners LP (BPL) Dividend Yield History

18

Energy Transfer Partners LP (ETP) Key Statistics, Ratios, & Metrics

Distribution Yield: 12.1% 10 Year Distribution Growth Rate: 14.0% Most Recent Annual Distribution Increase: 10.8% Sector: Energy

Distribution History: 15 years of increases Business Type: MLP

Ex-Distribution Date: 8/8/18 (est.) Payment Date: 8/15/18 (est.)

Overview & Current Events

Energy Transfer Partners is the second-largest energy master limited partnership (MLP) based on

market capitalization, behind Enterprise Products Partners (EPD). The partnership operates more than

71,000 miles of natural gas, natural gas liquids (NGL), and crude and refined products pipelines.

Energy Transfer Partners is a primary operator and financier of the notable Rover and Dakota Access

Pipeline (DAPL) projects.

In early May, Energy Transfer Partners reported (5/9/18) financial results for the first quarter of 2018.

The partnership beat expectations for both revenue and earnings. Adjusted EBITDA of $1.88 billion increased by $436 million over the prior year’s period while net income of $879 million increased by a

remarkable $486 million year-on-year. A number of factors contributed to Energy Transfer Partners’

strong performance, including robust results from the crude oil transportation and services segment and

a $172 million pre-tax gain on Sunoco LP (SUN) units that were repurchased by Sunoco from ETP in February. Importantly, Energy Transfer Partners’ quarterly distribution continues to be well-covered

by its underlying cash flows. All said, it was a strong quarter from this master limited partnership and

shares rose modestly following the announcement.

Growth Prospects & Safety

Energy Transfer Partners’ future growth will be derived from new projects such as the Rover pipeline.

The partnership owns 33% of Rover, which is now capable of transporting more than 1.7 billion cubic

feet per day. Separately, Energy Transfer Partners’ Red Bluff Express pipeline will have a capacity of at least 1.4 billion cubic feet per day with guaranteed long-term commitments supporting the project’s

cash flow. It is expected to come online in the second quarter of 2018. In all, Energy Transfer Partners

has $10 billion worth of new projects coming online from mid-2017 through mid-2019 that should

significantly boost growth moving forward.

Despite the partnership’s exceptionally high yield, Energy Transfer Partners’ distribution is secure.

The partnership reported a distribution coverage ratio of 1.15x in the most recent quarter. Prior to that,

the partnership’s distribution coverage ratio for the fourth quarter of 2017 was 1.30x. Energy Transfer Partners expects not to need equity financing through at least the middle of 2018. The partnership’s

balance sheet is reasonable, but investors should closely monitor the partnership’s financial position.

Energy Transfer Partners barely has an investment-grade BBB- credit rating from Standard & Poor’s

and a similar Baa2 rating from Moody’s. In addition, the partnership operated with a leverage ratio of

3.89x at the end of the most recent quarter, down from 3.96x in the previous quarter.

Valuation

Energy Transfer Partners has traded at an average distribution yield of 9.1% over the last 5 years. The partnership’s current yield of ~12% indicates that it is profoundly undervalued at current prices. A

yield of 9% combined with the partnership’s current quarterly distribution implies a fair value of $25

for this energy MLP. Units currently trade hands for less than $19.

19

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Energy Transfer Partners (ETP) Dividend Yield History

20

Omega Healthcare Investors Inc. (OHI) Key Statistics, Ratios, & Metrics

Distribution Yield: 9.3% 10 Year Distribution Growth Rate: 8.2% Most Recent Annual Distribution Increase: 4.8% Sector: Healthcare Real Estate

Distribution History: 15 years of increases Business Type: REIT

Ex-Distribution Date: 7/30/18 (est.) Payment Date: 8/15/18 (est.)

Overview & Current Events

Omega Healthcare Investors is the largest publicly-traded REIT in the United States dedicated to

owning and operating skilled nursing facilities (SNFs). The trust’s portfolio is comprised of

approximately 85% SNFs and 15% Senior Housing Facilities (SHFs). Omega operates ~1,000

properties in 42 U.S. states and the United Kingdom. These properties are run by 77 independent

operators.

In early May, Omega Healthcare Investors reported (5/7/18) financial results for the first quarter of

2018. Operating revenues fell 5.0% to $220.2 million while adjusted funds from operations of $0.78 per share fell from the $0.86 reported in last year’s period. Omega Healthcare is struggling through

some tenant issues that are negatively impacting the trust’s financial performance. The trust recorded

$198.2 million in impairment charges in 2017 due to certain affiliates of tenant Orianna Health

Systems declaring Chapter 11 bankruptcy. Importantly, Omega’s first quarter earnings release stated “Orianna recommenced partial rent payments in April,” and “we expect to have further clarity in the

near future” regarding the situation. Despite these problems, Omega beat analyst expectations (which

were quite pessimistic), which resulted in a modest rise in unit price following the announcement.

The trust also continued to actively manage its finances and property portfolio in the quarter. Omega

Healthcare Investors sold 14 facilities and had 3 mortgage loans repaid in the three-month reporting

period, which generated $98.4 million in net cash proceeds. In addition, the trust invested $38 million

in capital expenditures and completed $30 million in new investments. Importantly, Omega’s CFO made the following statement in the earnings release: “Our better than expected first quarter results

largely reflect the timing of new investments and asset sales.” Accordingly, the trust reaffirmed its

2018 financial guidance for adjusted funds from operations of $2.96 to $3.06 per diluted share.

Growth Prospects & Safety

Despite the recent difficulties experienced by Omega Healthcare Investors, the trust should still deliver

satisfactory growth over the long run. Industry tailwinds will be a major driver of this growth. The

aging U.S. population is a meaningful trend. The population of 85-year-old and older people in the United States is expected to grow by approximately 50% over the next 15 years. As the 4th largest

publicly-traded healthcare REIT, Omega is well-positioned to benefit from this change.

In addition, investors should note that Omega’s distribution continues to be well-covered by its cash

flows despite its recent operational difficulties. The trust currently pays a quarterly distribution of

$0.66 and generated adjusted funds from operations of $0.78 last quarter. This implies a distribution

coverage ratio of 1.18, equivalent to a cash flow payout ratio of approximately 85%.

Valuation

Omega Healthcare Investors’ average distribution yield over the last 5 years has been 6.6% and over

the last 10 years has been 6.9%. The trust’s current distribution yield of 9.3% indicates that it is significantly undervalued at current prices. We estimate a fair value of $37/share for Omega

Healthcare and it is currently trading for under $29/share.

21

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Omega Healthcare Investors (OHI) Dividend Yield History

22

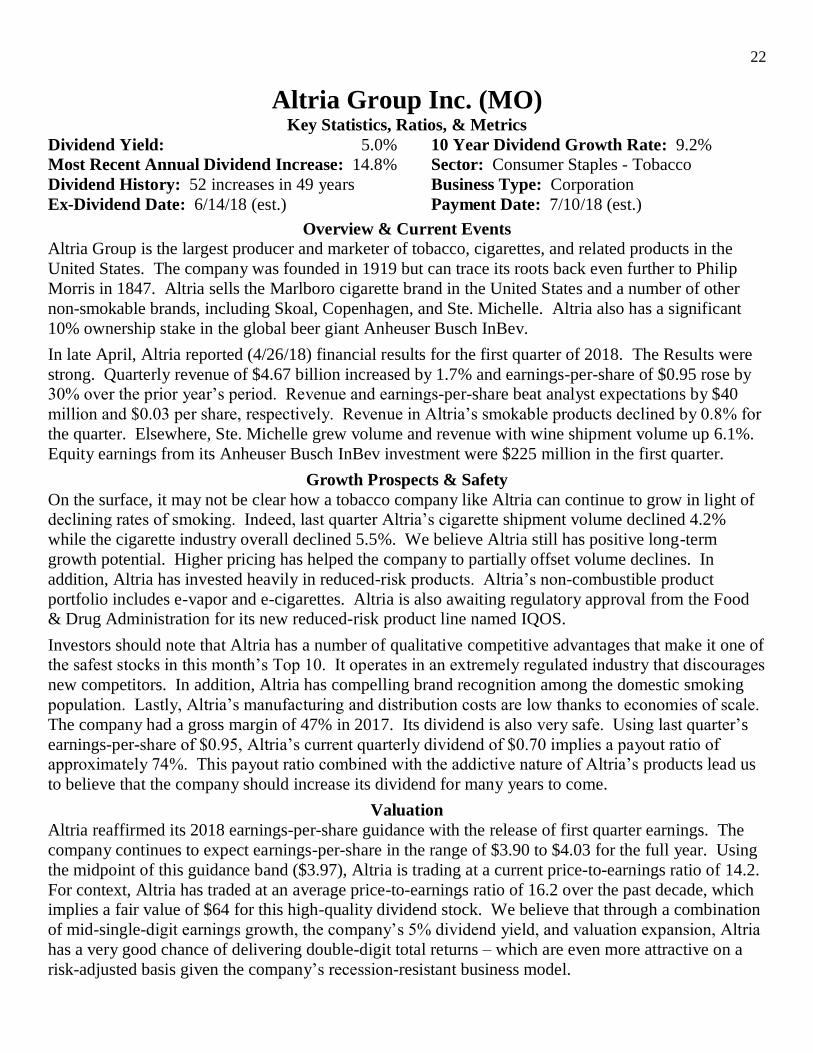

Altria Group Inc. (MO) Key Statistics, Ratios, & Metrics

Dividend Yield: 5.0% 10 Year Dividend Growth Rate: 9.2% Most Recent Annual Dividend Increase: 14.8% Sector: Consumer Staples - Tobacco

Dividend History: 52 increases in 49 years Business Type: Corporation

Ex-Dividend Date: 6/14/18 (est.) Payment Date: 7/10/18 (est.)

Overview & Current Events

Altria Group is the largest producer and marketer of tobacco, cigarettes, and related products in the

United States. The company was founded in 1919 but can trace its roots back even further to Philip

Morris in 1847. Altria sells the Marlboro cigarette brand in the United States and a number of other

non-smokable brands, including Skoal, Copenhagen, and Ste. Michelle. Altria also has a significant

10% ownership stake in the global beer giant Anheuser Busch InBev.

In late April, Altria reported (4/26/18) financial results for the first quarter of 2018. The Results were

strong. Quarterly revenue of $4.67 billion increased by 1.7% and earnings-per-share of $0.95 rose by 30% over the prior year’s period. Revenue and earnings-per-share beat analyst expectations by $40

million and $0.03 per share, respectively. Revenue in Altria’s smokable products declined by 0.8% for

the quarter. Elsewhere, Ste. Michelle grew volume and revenue with wine shipment volume up 6.1%.

Equity earnings from its Anheuser Busch InBev investment were $225 million in the first quarter.

Growth Prospects & Safety

On the surface, it may not be clear how a tobacco company like Altria can continue to grow in light of declining rates of smoking. Indeed, last quarter Altria’s cigarette shipment volume declined 4.2%

while the cigarette industry overall declined 5.5%. We believe Altria still has positive long-term

growth potential. Higher pricing has helped the company to partially offset volume declines. In

addition, Altria has invested heavily in reduced-risk products. Altria’s non-combustible product

portfolio includes e-vapor and e-cigarettes. Altria is also awaiting regulatory approval from the Food & Drug Administration for its new reduced-risk product line named IQOS.

Investors should note that Altria has a number of qualitative competitive advantages that make it one of the safest stocks in this month’s Top 10. It operates in an extremely regulated industry that discourages

new competitors. In addition, Altria has compelling brand recognition among the domestic smoking

population. Lastly, Altria’s manufacturing and distribution costs are low thanks to economies of scale.

The company had a gross margin of 47% in 2017. Its dividend is also very safe. Using last quarter’s

earnings-per-share of $0.95, Altria’s current quarterly dividend of $0.70 implies a payout ratio of approximately 74%. This payout ratio combined with the addictive nature of Altria’s products lead us

to believe that the company should increase its dividend for many years to come.

Valuation

Altria reaffirmed its 2018 earnings-per-share guidance with the release of first quarter earnings. The

company continues to expect earnings-per-share in the range of $3.90 to $4.03 for the full year. Using

the midpoint of this guidance band ($3.97), Altria is trading at a current price-to-earnings ratio of 14.2.

For context, Altria has traded at an average price-to-earnings ratio of 16.2 over the past decade, which implies a fair value of $64 for this high-quality dividend stock. We believe that through a combination

of mid-single-digit earnings growth, the company’s 5% dividend yield, and valuation expansion, Altria

has a very good chance of delivering double-digit total returns – which are even more attractive on a

risk-adjusted basis given the company’s recession-resistant business model.

23

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Altria Group (MO) Dividend Yield History

24

Enterprise Products Partners LP (EPD)

Key Statistics, Ratios & Metrics Distribution Yield: 6.2% 10 Year Distribution Growth Rate: 5.4%

Most Recent Annual Distribution Increase: 3.0% Sector: Energy

Distribution History: 19 years of increases Business Type: MLP

Ex- Distribution Date: 7/27/18 (est.) Payment Date: 8/8/18 (est.)

Overview & Current Events

Enterprise Products Partners is an oil and gas master limited partnership (MLP) and the largest MLP by

market capitalization. The partnership operates storage and transportation assets, including nearly

50,000 miles of natural gas, natural gas liquids, crude oil, and refined products pipelines. Enterprise

Products Partners also operates approximately 250 million barrels of oil storage capacity.

In late April, Enterprise Products Partners reported (4/30/18) financial results for the first quarter of

fiscal 2018. The partnership’s performance was very strong. Revenue grew by 27% and distributable

cash flow increased by 23% in the quarter to a record $1.4 billion. More importantly, Enterprise

Products Partners reported a distribution coverage ratio of 1.5x in the quarter – one of the highest

distribution coverage ratios we’ve ever seen from a master limited partnership. Because of its strong performance, Enterprise Products Partners noted that it does not expect to issue equity for the

remainder of 2018 (other than its distribution reinvestment plan and employee unit purchase plan).

Despite the partnership’s remarkable performance, Enterprise Products Partners’ unit price remained

essentially unchanged following the announcement.

Prior to that, Enterprise Products Partners increased (4/10/18) its quarterly distribution payment. The

new quarterly payout of $0.4275 per common unit represents a 3.0% increase over the prior year’s

period. Remarkably, Enterprise Products Partners has increased its distribution for 55 consecutive

quarters.

Growth Prospects & Safety

The most important growth catalysts for Enterprise Products Partners are new projects. The partnership retained $867 million of distributable cash flow in 2017 and $458 million of distributable

cash flow in the first quarter of 2018 alone. Enterprise Products Partners appears to have plenty of

opportunities to deploy this internally-generated cash. The partnership’s CEO, Jim Teague, stated in its

first quarter earnings release that “we are seeing a noticeable pick up in discussions and negotiations

and expect to announce new organic growth projects later this year.”

We believe Enterprise Products Partners is the safest MLP in both this newsletter and our broader

investment universe. The partnership has an investment-grade BBB+ rating from Standard & Poor’s

and a Baa1 rating from Moody’s. In addition, Enterprise Products Partners has a reputation for being exceptionally well-managed. This year’s ranking marked the second consecutive year in which the

partnership won the unanimous vote for the Institutional Investor All-America Executive Team for the

MLP sector.

Valuation

Enterprise Products Partners has traded at an average distribution yield of 5.2% over the last 5 years

and 5.8% over the last 10 years. Given the partnership’s current quarterly distribution, a 5.5% target

yield implies a fair value of $31 for Enterprise Products Partners. The partnership’s units currently

trade hands for $27.

25

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Enterprise Products Partners (EPD) Dividend Yield History

26

Disclaimer

Nothing presented herein is, or is intended to constitute, specific investment advice. Nothing in this newsletter should be construed as a recommendation to follow any

investment strategy or allocation. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No reliance should be placed on any such statements or forecasts when making any investment decision. While Sure Retirement/Sure Dividend has used

reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party

information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made. There is a risk of loss from an

investment in securities. Past performance is not a guarantee of future performance.

Closing Thoughts – Announcements & Improvements –

We’ve made an important change to the Sure Retirement Newsletter since the April 2018 edition.

Specifically, we are now incorporating expected total return data into our Top 10 rankings in the

Sure Retirement Newsletter. The Top 10 list is still ordered from best to least best as before.

The first five spots in the newsletter (stocks ranked 1 through 5) are the highest expected total

return stocks in our Sure Analysis Research database that have 4%+ yields.

The next five spots in the newsletter’s Top 10 (stocks ranked 6 through 10) are the top ranked

stocks with 4%+ yields using The 8 Rules of Dividend Investing, excluding any stock that already

made the top 5 in the Sure Retirement Newsletter from the Sure Analysis rankings.

We are making this change to better serve readers of the Sure Retirement Newsletter. We want our

best high-income ideas to be in this newsletter for our readers to benefit from. In the past, these

ideas all came from our 8 Rules ranking system.

The Sure Analysis Research Database differs from Sure Retirement in that Sure Retirement uses

historical information to quantitatively rank stocks while Sure Analysis uses historical information

combined with qualitative analysis to create expected total returns over the next 5 years for every

stock in the database. For those who aren’t familiar with the Sure Analysis Research Database, it is

explained below.

We also launched the Sure Analysis Research Database in April of 2018. It currently includes all

the ~120 dividend stocks with 25+ years of rising dividends, as well as many other past Sure

Dividend and Sure Retirement Newsletter recommendations. We will continue adding companies

based on a mix of reader recommendations and popular dividend stocks. We currently have well

over 150 research reports in the database, with more being added nearly every day.

The purpose of Sure Analysis is to provide concise 2-page research reports on dividend stocks so

self-directed investors can quickly identify the highest expected total return investments while

avoiding the worst. These reports are updated quarterly to ensure they stay timely and actionable.

In addition to the 2-page research reports, the Sure Analysis Database also has a sortable

spreadsheet to quickly sort all the database constituents by expected total return, dividend yield,

valuation, and expected growth. Sure Analysis members also get access to all 3 of our newsletters.

We believe this change will improve the quality of our future newsletter recommendations. If you

have any questions about this change, please feel free to contact us.

Thanks,

Ben Reynolds

The next newsletter publishes on Sunday, June 10th, 2018.

27

This information is not personalized advice. It is for informational purposes only. Please see disclaimer at end of newsletter for more.

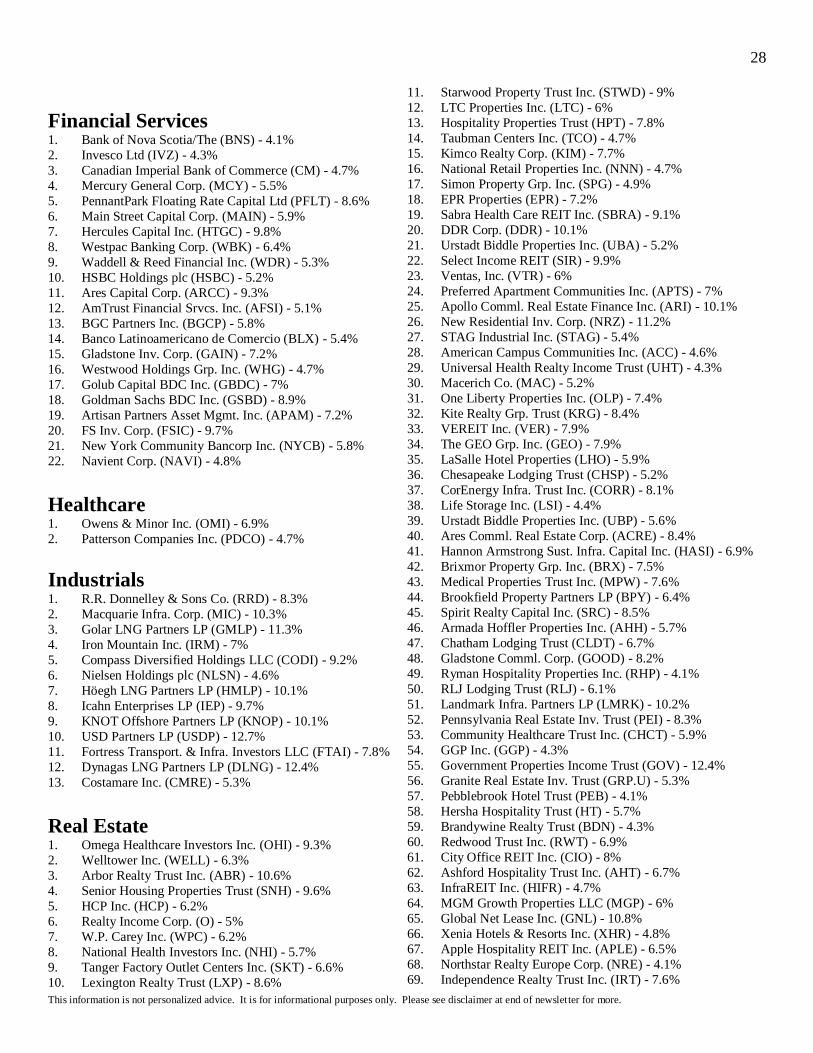

List of Investments by Sector

Each of the securities with 4%+ yields in the Sure Dividend database are sorted by rank below in

order based on The 8 Rules of Dividend Investing (highest to lowest) based on its GICS sector.

Dividend or distribution yield is included next to each security’s ticker symbol.

Basic Materials 1. Westlake Chemical Partners LP (WLKP) - 7%

2. SunCoke Energy Partners LP (SXCP) - 10.3%

3. Enviva Partners LP (EVA) - 8.3%

4. Ciner Resources LP (CINR) - 9.3%

5. Compass Minerals Intl. Inc. (CMP) - 4.2%

Communication Services 1. Vodafone Grp. plc (VOD) - 5.9%

2. BCE Inc. (BCE) - 5.7%

3. AT&T Inc. (T) - 6.4%

4. Verizon Communications Inc. (VZ) - 5.1%

5. Crown Castle Intl. Corp. (CCI) - 4.1%

6. Consolidated Communications Hldgs. Inc. (CNSL) - 13.5%

7. CenturyLink Inc. (CTL) - 12%

8. IDT Corp. (IDT) - 7%

Consumer Cyclicals 1. GameStop Corp. (GME) - 11.8%

2. L Brands Inc. (LB) - 7%

3. Meredith Corp. (MDP) - 4.3%

4. Macy's Inc. (M) - 5%

5. Cedar Fair LP (FUN) - 5.4%

6. Ford Motor Co. (F) - 5.4%

7. National CineMedia Inc. (NCMI) - 9.8%

8. New Media Inv. Grp. Inc. (NEWM) - 8.8%

9. Bowl America Inc. (BWL.A) - 4.5%

10. Cato Corp./The (CATO) - 8.1%

11. General Motors Co. (GM) - 4.2%

12. Barnes & Noble Inc. (BKS) - 11.7%

13. Gannett Co. Inc. (GCI) - 5.6%

14. Buckle Inc./The (BKE) - 4.3%

Consumer Defensive 1. Altria Grp. Inc. (MO) - 5%

2. Vector Grp. Ltd (VGR) - 8.3%

3. Kraft-Heinz Co./The (KHC) - 4.3%

4. Universal Corp. (UVV) - 4.6%

5. Philip Morris Intl. Inc. (PM) - 5.2%

6. General Mills Inc. (GIS) - 4.6%

Energy 1. Buckeye Partners LP (BPL) - 12.4%

2. Energy Transfer Partners LP (ETP) - 12.4%

3. Enterprise Product Partners LP (EPD) - 6.4%

4. NuStar Energy LP (NS) - 17.9%

5. TC PipeLines LP (TCP) - 10.1%

6. Holly Energy Partners LP (HEP) - 9%

7. Enbridge Inc. (ENB) - 6.5%

8. Sunoco LP (SUN) - 12.3%

9. Royal Dutch Shell plc (RDS.A) - 5.2%

10. ONEOK Inc. (OKE) - 4.7%

11. Royal Dutch Shell plc (RDS.B) - 5%

12. Exxon Mobil Corp. (XOM) - 4.1%

13. Energy Transfer Equity LP (ETE) - 7.3%

14. CrossAmerica Partners LP (CAPL) - 11.7%

15. Spectra Energy Partners LP (SEP) - 8.8%

16. Western Gas Partners LP (WES) - 7.3%

17. Phillips 66 Partners LP (PSXP) - 5.8%

18. Magellan Midstream Partners LP (MMP) - 5.4%

19. Transmontaigne Partners LP (TLP) - 8.2%

20. Helmerich & Payne Inc. (HP) - 4.1%

21. NuStar GP Holdings LLC (NSH) - 10.7% 22. Andeavor Logistics LP (ANDX) - 9%

23. EnLink Midstream Partners LP (ENLK) - 9.7%

24. Western Gas Equity Partners LP (WGP) - 6.4%

25. TOTAL S.A. (TOT) - 4.7%

26. DCP Midstream LP (DCP) - 8.2%

27. Targa Resources Corp. (TRGP) - 7.7%

28. Delek Logistics Partners LP (DKL) - 10.6%

29. PBF Logistics LP (PBFX) - 9.6%

30. EnLink Midstream LLC (ENLC) - 6.4%

31. BP plc (BP) - 5.1%

32. Sprague Resources LP (SRLP) - 10.8%

33. Tallgrass Energy Partners LP (TEP) - 9.2%

34. Summit Midstream Partners LP (SMLP) - 15.9%

35. MPLX LP (MPLX) - 7.1%

36. GasLog Partners LP (GLOP) - 8.8%

37. Green Plains Partners LP (GPP) - 11.8%

38. USA Compression Partners LP (USAC) - 11.5%

39. SemGroup Corp. (SEMG) - 7.5%

40. Vermilion Energy Inc. (VET) - 6.3%

41. Enable Midstream Partners LP (ENBL) - 8.7%

42. Cheniere Energy Partners LP (CQP) - 7.1%

43. Black Stone Minerals LP (BSM) - 6.7%

44. Kinder Morgan Inc. (KMI) - 4.9%

45. Williams Companies Inc./The (WMB) - 5.1%

28

This information is not personalized advice. It is for informational purposes only. Please see disclaimer at end of newsletter for more.

Financial Services 1. Bank of Nova Scotia/The (BNS) - 4.1%

2. Invesco Ltd (IVZ) - 4.3%

3. Canadian Imperial Bank of Commerce (CM) - 4.7%

4. Mercury General Corp. (MCY) - 5.5%

5. PennantPark Floating Rate Capital Ltd (PFLT) - 8.6%

6. Main Street Capital Corp. (MAIN) - 5.9%

7. Hercules Capital Inc. (HTGC) - 9.8%

8. Westpac Banking Corp. (WBK) - 6.4%

9. Waddell & Reed Financial Inc. (WDR) - 5.3%

10. HSBC Holdings plc (HSBC) - 5.2%

11. Ares Capital Corp. (ARCC) - 9.3%

12. AmTrust Financial Srvcs. Inc. (AFSI) - 5.1%

13. BGC Partners Inc. (BGCP) - 5.8%

14. Banco Latinoamericano de Comercio (BLX) - 5.4%

15. Gladstone Inv. Corp. (GAIN) - 7.2%

16. Westwood Holdings Grp. Inc. (WHG) - 4.7%

17. Golub Capital BDC Inc. (GBDC) - 7%

18. Goldman Sachs BDC Inc. (GSBD) - 8.9%

19. Artisan Partners Asset Mgmt. Inc. (APAM) - 7.2%

20. FS Inv. Corp. (FSIC) - 9.7%

21. New York Community Bancorp Inc. (NYCB) - 5.8%

22. Navient Corp. (NAVI) - 4.8%

Healthcare 1. Owens & Minor Inc. (OMI) - 6.9%

2. Patterson Companies Inc. (PDCO) - 4.7%

Industrials 1. R.R. Donnelley & Sons Co. (RRD) - 8.3%

2. Macquarie Infra. Corp. (MIC) - 10.3%

3. Golar LNG Partners LP (GMLP) - 11.3%

4. Iron Mountain Inc. (IRM) - 7%

5. Compass Diversified Holdings LLC (CODI) - 9.2%

6. Nielsen Holdings plc (NLSN) - 4.6%

7. Höegh LNG Partners LP (HMLP) - 10.1%

8. Icahn Enterprises LP (IEP) - 9.7%

9. KNOT Offshore Partners LP (KNOP) - 10.1%

10. USD Partners LP (USDP) - 12.7%

11. Fortress Transport. & Infra. Investors LLC (FTAI) - 7.8%

12. Dynagas LNG Partners LP (DLNG) - 12.4%

13. Costamare Inc. (CMRE) - 5.3%

Real Estate 1. Omega Healthcare Investors Inc. (OHI) - 9.3%

2. Welltower Inc. (WELL) - 6.3%

3. Arbor Realty Trust Inc. (ABR) - 10.6%

4. Senior Housing Properties Trust (SNH) - 9.6%

5. HCP Inc. (HCP) - 6.2%

6. Realty Income Corp. (O) - 5%

7. W.P. Carey Inc. (WPC) - 6.2%

8. National Health Investors Inc. (NHI) - 5.7%

9. Tanger Factory Outlet Centers Inc. (SKT) - 6.6%

10. Lexington Realty Trust (LXP) - 8.6%

11. Starwood Property Trust Inc. (STWD) - 9%

12. LTC Properties Inc. (LTC) - 6%

13. Hospitality Properties Trust (HPT) - 7.8%

14. Taubman Centers Inc. (TCO) - 4.7%

15. Kimco Realty Corp. (KIM) - 7.7%

16. National Retail Properties Inc. (NNN) - 4.7%

17. Simon Property Grp. Inc. (SPG) - 4.9%

18. EPR Properties (EPR) - 7.2%

19. Sabra Health Care REIT Inc. (SBRA) - 9.1%

20. DDR Corp. (DDR) - 10.1%

21. Urstadt Biddle Properties Inc. (UBA) - 5.2%

22. Select Income REIT (SIR) - 9.9%

23. Ventas, Inc. (VTR) - 6%

24. Preferred Apartment Communities Inc. (APTS) - 7%

25. Apollo Comml. Real Estate Finance Inc. (ARI) - 10.1%

26. New Residential Inv. Corp. (NRZ) - 11.2%

27. STAG Industrial Inc. (STAG) - 5.4%

28. American Campus Communities Inc. (ACC) - 4.6%

29. Universal Health Realty Income Trust (UHT) - 4.3%

30. Macerich Co. (MAC) - 5.2%

31. One Liberty Properties Inc. (OLP) - 7.4%

32. Kite Realty Grp. Trust (KRG) - 8.4%

33. VEREIT Inc. (VER) - 7.9%

34. The GEO Grp. Inc. (GEO) - 7.9%

35. LaSalle Hotel Properties (LHO) - 5.9%

36. Chesapeake Lodging Trust (CHSP) - 5.2%

37. CorEnergy Infra. Trust Inc. (CORR) - 8.1%

38. Life Storage Inc. (LSI) - 4.4%

39. Urstadt Biddle Properties Inc. (UBP) - 5.6%

40. Ares Comml. Real Estate Corp. (ACRE) - 8.4%

41. Hannon Armstrong Sust. Infra. Capital Inc. (HASI) - 6.9%

42. Brixmor Property Grp. Inc. (BRX) - 7.5%

43. Medical Properties Trust Inc. (MPW) - 7.6%

44. Brookfield Property Partners LP (BPY) - 6.4%

45. Spirit Realty Capital Inc. (SRC) - 8.5%

46. Armada Hoffler Properties Inc. (AHH) - 5.7%

47. Chatham Lodging Trust (CLDT) - 6.7%

48. Gladstone Comml. Corp. (GOOD) - 8.2%

49. Ryman Hospitality Properties Inc. (RHP) - 4.1%

50. RLJ Lodging Trust (RLJ) - 6.1%

51. Landmark Infra. Partners LP (LMRK) - 10.2%

52. Pennsylvania Real Estate Inv. Trust (PEI) - 8.3%

53. Community Healthcare Trust Inc. (CHCT) - 5.9%

54. GGP Inc. (GGP) - 4.3%

55. Government Properties Income Trust (GOV) - 12.4%

56. Granite Real Estate Inv. Trust (GRP.U) - 5.3%

57. Pebblebrook Hotel Trust (PEB) - 4.1%

58. Hersha Hospitality Trust (HT) - 5.7%

59. Brandywine Realty Trust (BDN) - 4.3%

60. Redwood Trust Inc. (RWT) - 6.9%

61. City Office REIT Inc. (CIO) - 8%

62. Ashford Hospitality Trust Inc. (AHT) - 6.7%

63. InfraREIT Inc. (HIFR) - 4.7%

64. MGM Growth Properties LLC (MGP) - 6%

65. Global Net Lease Inc. (GNL) - 10.8%

66. Xenia Hotels & Resorts Inc. (XHR) - 4.8%

67. Apple Hospitality REIT Inc. (APLE) - 6.5%

68. Northstar Realty Europe Corp. (NRE) - 4.1%

69. Independence Realty Trust Inc. (IRT) - 7.6%

29

This information is not personalized advice. It is for informational purposes only. Please see disclaimer at end of newsletter for more.

70. New Senior Inv. Grp. Inc. (SNR) - 12%

71. Uniti Grp. Inc. (UNIT) - 12.5%

72. Outfront Media Inc. (OUT) - 7.3%

73. Franklin Street Properties Corp. (FSP) - 8.5%

Technology 1. International Business Machines Corp. (IBM) - 4.4%

2. QUALCOMM Inc. (QCOM) - 4.7%

3. Seagate Technology plc (STX) - 4.4%%

Utilities 1. AmeriGas Partners LP (APU) - 9.2%

2. Southern Co. (SO) - 5.5%

3. Dominion Energy Inc./VA (D) - 5.3%

4. PPL Corp. (PPL) - 5.9%

5. SCANA Corp. (SCG) - 7%

6. CenterPoint Energy Inc. (CNP) - 4.2%

7. Brookfield Renewable Partners LP (BEP) - 6.4%

8. Duke Energy Corp. (DUK) - 4.6%

9. NorthWestern Corp. (NWE) - 4.1%

10. NRG Yield Inc. (NYLD.A) - 7.2% 11. Pattern Energy Grp. Inc. (PEGI) - 9.4%

12. Edison Intl. (EIX) - 4%

13. Entergy Corp. (ETR) - 4.6%

14. AES Corp./The (AES) - 4.3%

15. 8point3 Energy Partners LP (CAFD) - 9.2%

16. NRG Yield Inc. (NYLD) - 7.1%

17. FirstEnergy Corp. (FE) - 4.3%

30

This information is not personalized advice. It is for informational purposes only. Please see disclaimer at end of newsletter for more.

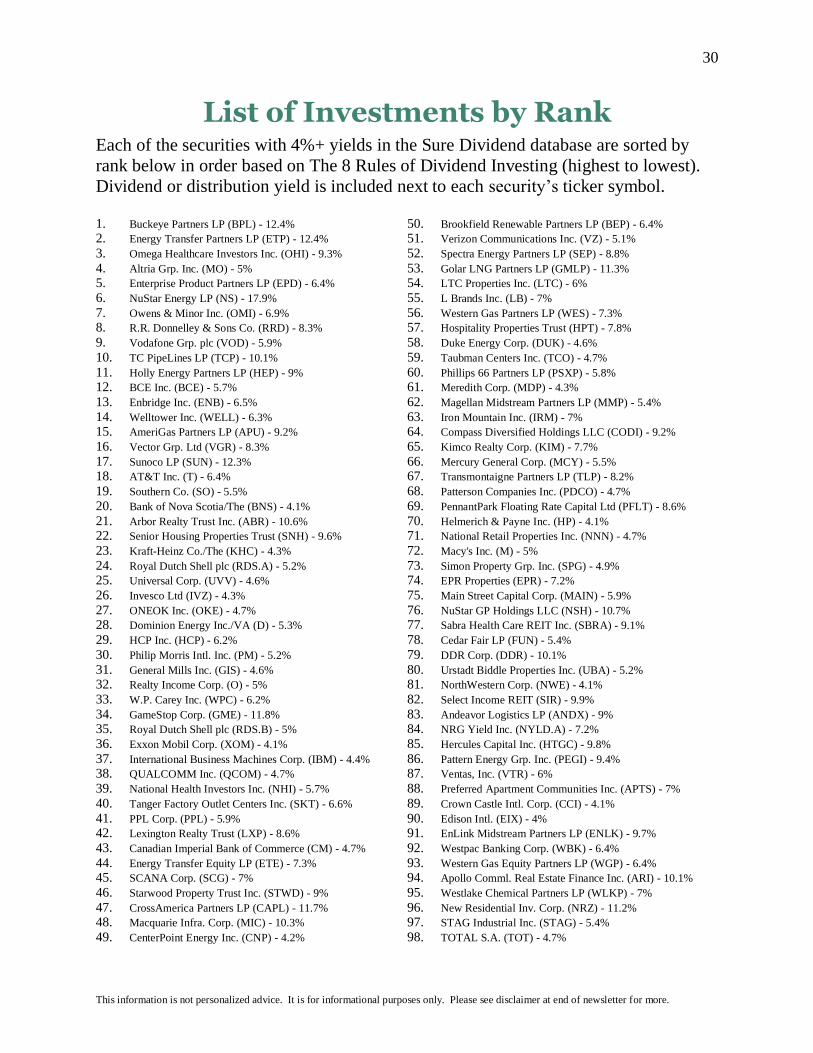

List of Investments by Rank

Each of the securities with 4%+ yields in the Sure Dividend database are sorted by

rank below in order based on The 8 Rules of Dividend Investing (highest to lowest).

Dividend or distribution yield is included next to each security’s ticker symbol. 1. Buckeye Partners LP (BPL) - 12.4%

2. Energy Transfer Partners LP (ETP) - 12.4%

3. Omega Healthcare Investors Inc. (OHI) - 9.3%

4. Altria Grp. Inc. (MO) - 5%

5. Enterprise Product Partners LP (EPD) - 6.4%

6. NuStar Energy LP (NS) - 17.9%

7. Owens & Minor Inc. (OMI) - 6.9%

8. R.R. Donnelley & Sons Co. (RRD) - 8.3%

9. Vodafone Grp. plc (VOD) - 5.9%

10. TC PipeLines LP (TCP) - 10.1%

11. Holly Energy Partners LP (HEP) - 9%

12. BCE Inc. (BCE) - 5.7%

13. Enbridge Inc. (ENB) - 6.5%

14. Welltower Inc. (WELL) - 6.3%

15. AmeriGas Partners LP (APU) - 9.2%

16. Vector Grp. Ltd (VGR) - 8.3%

17. Sunoco LP (SUN) - 12.3%

18. AT&T Inc. (T) - 6.4%

19. Southern Co. (SO) - 5.5%

20. Bank of Nova Scotia/The (BNS) - 4.1%

21. Arbor Realty Trust Inc. (ABR) - 10.6%

22. Senior Housing Properties Trust (SNH) - 9.6%

23. Kraft-Heinz Co./The (KHC) - 4.3%

24. Royal Dutch Shell plc (RDS.A) - 5.2%

25. Universal Corp. (UVV) - 4.6%

26. Invesco Ltd (IVZ) - 4.3%

27. ONEOK Inc. (OKE) - 4.7%

28. Dominion Energy Inc./VA (D) - 5.3%

29. HCP Inc. (HCP) - 6.2%

30. Philip Morris Intl. Inc. (PM) - 5.2%

31. General Mills Inc. (GIS) - 4.6%

32. Realty Income Corp. (O) - 5%

33. W.P. Carey Inc. (WPC) - 6.2%

34. GameStop Corp. (GME) - 11.8%

35. Royal Dutch Shell plc (RDS.B) - 5%

36. Exxon Mobil Corp. (XOM) - 4.1%

37. International Business Machines Corp. (IBM) - 4.4%

38. QUALCOMM Inc. (QCOM) - 4.7%

39. National Health Investors Inc. (NHI) - 5.7%

40. Tanger Factory Outlet Centers Inc. (SKT) - 6.6%

41. PPL Corp. (PPL) - 5.9%

42. Lexington Realty Trust (LXP) - 8.6%

43. Canadian Imperial Bank of Commerce (CM) - 4.7%

44. Energy Transfer Equity LP (ETE) - 7.3%

45. SCANA Corp. (SCG) - 7%

46. Starwood Property Trust Inc. (STWD) - 9%

47. CrossAmerica Partners LP (CAPL) - 11.7%

48. Macquarie Infra. Corp. (MIC) - 10.3%

49. CenterPoint Energy Inc. (CNP) - 4.2%

50. Brookfield Renewable Partners LP (BEP) - 6.4%

51. Verizon Communications Inc. (VZ) - 5.1%

52. Spectra Energy Partners LP (SEP) - 8.8%

53. Golar LNG Partners LP (GMLP) - 11.3%

54. LTC Properties Inc. (LTC) - 6%

55. L Brands Inc. (LB) - 7%

56. Western Gas Partners LP (WES) - 7.3%

57. Hospitality Properties Trust (HPT) - 7.8%

58. Duke Energy Corp. (DUK) - 4.6%

59. Taubman Centers Inc. (TCO) - 4.7%

60. Phillips 66 Partners LP (PSXP) - 5.8%

61. Meredith Corp. (MDP) - 4.3%

62. Magellan Midstream Partners LP (MMP) - 5.4%

63. Iron Mountain Inc. (IRM) - 7%

64. Compass Diversified Holdings LLC (CODI) - 9.2%

65. Kimco Realty Corp. (KIM) - 7.7%

66. Mercury General Corp. (MCY) - 5.5%

67. Transmontaigne Partners LP (TLP) - 8.2%

68. Patterson Companies Inc. (PDCO) - 4.7%

69. PennantPark Floating Rate Capital Ltd (PFLT) - 8.6%

70. Helmerich & Payne Inc. (HP) - 4.1%

71. National Retail Properties Inc. (NNN) - 4.7%

72. Macy's Inc. (M) - 5%

73. Simon Property Grp. Inc. (SPG) - 4.9%

74. EPR Properties (EPR) - 7.2%

75. Main Street Capital Corp. (MAIN) - 5.9%

76. NuStar GP Holdings LLC (NSH) - 10.7%

77. Sabra Health Care REIT Inc. (SBRA) - 9.1%

78. Cedar Fair LP (FUN) - 5.4%

79. DDR Corp. (DDR) - 10.1%

80. Urstadt Biddle Properties Inc. (UBA) - 5.2%

81. NorthWestern Corp. (NWE) - 4.1%

82. Select Income REIT (SIR) - 9.9%

83. Andeavor Logistics LP (ANDX) - 9%

84. NRG Yield Inc. (NYLD.A) - 7.2%

85. Hercules Capital Inc. (HTGC) - 9.8%

86. Pattern Energy Grp. Inc. (PEGI) - 9.4%

87. Ventas, Inc. (VTR) - 6%

88. Preferred Apartment Communities Inc. (APTS) - 7%

89. Crown Castle Intl. Corp. (CCI) - 4.1%

90. Edison Intl. (EIX) - 4%

91. EnLink Midstream Partners LP (ENLK) - 9.7%

92. Westpac Banking Corp. (WBK) - 6.4%

93. Western Gas Equity Partners LP (WGP) - 6.4%

94. Apollo Comml. Real Estate Finance Inc. (ARI) - 10.1%

95. Westlake Chemical Partners LP (WLKP) - 7%

96. New Residential Inv. Corp. (NRZ) - 11.2%

97. STAG Industrial Inc. (STAG) - 5.4%

98. TOTAL S.A. (TOT) - 4.7%

31

This information is not personalized advice. It is for informational purposes only. Please see disclaimer at end of newsletter for more.

99. DCP Midstream LP (DCP) - 8.2%

100. American Campus Communities Inc. (ACC) - 4.6%

101. Targa Resources Corp. (TRGP) - 7.7%

102. Universal Health Realty Income Trust (UHT) - 4.3%

103. Macerich Co. (MAC) - 5.2%

104. One Liberty Properties Inc. (OLP) - 7.4%

105. Delek Logistics Partners LP (DKL) - 10.6%

106. Ford Motor Co. (F) - 5.4%

107. Entergy Corp. (ETR) - 4.6%

108. Kite Realty Grp. Trust (KRG) - 8.4%

109. PBF Logistics LP (PBFX) - 9.6%

110. Waddell & Reed Financial Inc. (WDR) - 5.3%

111. VEREIT Inc. (VER) - 7.9%

112. The GEO Grp. Inc. (GEO) - 7.9%

113. LaSalle Hotel Properties (LHO) - 5.9%

114. AES Corp./The (AES) - 4.3%

115. HSBC Holdings plc (HSBC) - 5.2%

116. Ares Capital Corp. (ARCC) - 9.3%

117. Nielsen Holdings plc (NLSN) - 4.6%

118. EnLink Midstream LLC (ENLC) - 6.4%

119. Chesapeake Lodging Trust (CHSP) - 5.2%

120. CorEnergy Infra. Trust Inc. (CORR) - 8.1%

121. Life Storage Inc. (LSI) - 4.4%

122. Urstadt Biddle Properties Inc. (UBP) - 5.6%

123. Ares Comml. Real Estate Corp. (ACRE) - 8.4%

124. Höegh LNG Partners LP (HMLP) - 10.1%

125. AmTrust Financial Srvcs. Inc. (AFSI) - 5.1%

126. Hannon Armstrong Sust. Infra. Capital Inc. (HASI) - 6.9%

127. 8point3 Energy Partners LP (CAFD) - 9.2%

128. BP plc (BP) - 5.1%

129. Brixmor Property Grp. Inc. (BRX) - 7.5%

130. BGC Partners Inc. (BGCP) - 5.8%

131. Medical Properties Trust Inc. (MPW) - 7.6%

132. Banco Latinoamericano de Comercio (BLX) - 5.4%

133. Sprague Resources LP (SRLP) - 10.8%

134. Tallgrass Energy Partners LP (TEP) - 9.2%

135. Brookfield Property Partners LP (BPY) - 6.4%

136. Gladstone Inv. Corp. (GAIN) - 7.2%

137. Icahn Enterprises LP (IEP) - 9.7%

138. Westwood Holdings Grp. Inc. (WHG) - 4.7%

139. Spirit Realty Capital Inc. (SRC) - 8.5%

140. Armada Hoffler Properties Inc. (AHH) - 5.7%

141. Chatham Lodging Trust (CLDT) - 6.7%

142. Gladstone Comml. Corp. (GOOD) - 8.2%

143. Ryman Hospitality Properties Inc. (RHP) - 4.1%

144. Summit Midstream Partners LP (SMLP) - 15.9%

145. National CineMedia Inc. (NCMI) - 9.8%

146. MPLX LP (MPLX) - 7.1%

147. SunCoke Energy Partners LP (SXCP) - 10.3%

148. GasLog Partners LP (GLOP) - 8.8%

149. KNOT Offshore Partners LP (KNOP) - 10.1%

150. RLJ Lodging Trust (RLJ) - 6.1%

151. USD Partners LP (USDP) - 12.7%

152. NRG Yield Inc. (NYLD) - 7.1%

153. Landmark Infra. Partners LP (LMRK) - 10.2%

154. Seagate Technology plc (STX) - 4.4%

155. Green Plains Partners LP (GPP) - 11.8%

156. Pennsylvania Real Estate Inv. Trust (PEI) - 8.3%

157. USA Compression Partners LP (USAC) - 11.5%

158. Community Healthcare Trust Inc. (CHCT) - 5.9%

159. GGP Inc. (GGP) - 4.3%

160. Enviva Partners LP (EVA) - 8.3%

161. Ciner Resources LP (CINR) - 9.3%

162. Government Properties Income Trust (GOV) - 12.4%

163. Granite Real Estate Inv. Trust (GRP.U) - 5.3%

164. SemGroup Corp. (SEMG) - 7.5%

165. Pebblebrook Hotel Trust (PEB) - 4.1%

166. Hersha Hospitality Trust (HT) - 5.7%

167. New Media Inv. Grp. Inc. (NEWM) - 8.8%

168. Bowl America Inc. (BWL.A) - 4.5%

169. Brandywine Realty Trust (BDN) - 4.3%

170. Cato Corp./The (CATO) - 8.1%

171. Vermilion Energy Inc. (VET) - 6.3%

172. Redwood Trust Inc. (RWT) - 6.9%

173. City Office REIT Inc. (CIO) - 8%

174. Ashford Hospitality Trust Inc. (AHT) - 6.7%

175. Golub Capital BDC Inc. (GBDC) - 7%

176. InfraREIT Inc. (HIFR) - 4.7%

177. General Motors Co. (GM) - 4.2%

178. MGM Growth Properties LLC (MGP) - 6%

179. Enable Midstream Partners LP (ENBL) - 8.7%

180. Goldman Sachs BDC Inc. (GSBD) - 8.9%

181. Global Net Lease Inc. (GNL) - 10.8%

182. Xenia Hotels & Resorts Inc. (XHR) - 4.8%

183. Apple Hospitality REIT Inc. (APLE) - 6.5%

184. Northstar Realty Europe Corp. (NRE) - 4.1%

185. Independence Realty Trust Inc. (IRT) - 7.6%

186. Fortress Transport. & Infra. Investors LLC (FTAI) - 7.8%

187. Artisan Partners Asset Mgmt. Inc. (APAM) - 7.2%

188. Cheniere Energy Partners LP (CQP) - 7.1%

189. New Senior Inv. Grp. Inc. (SNR) - 12%

190. FirstEnergy Corp. (FE) - 4.3%

191. Compass Minerals Intl. Inc. (CMP) - 4.2%

192. Black Stone Minerals LP (BSM) - 6.7%

193. FS Inv. Corp. (FSIC) - 9.7%

194. Dynagas LNG Partners LP (DLNG) - 12.4%

195. Uniti Grp. Inc. (UNIT) - 12.5%

196. Barnes & Noble Inc. (BKS) - 11.7%

197. Kinder Morgan Inc. (KMI) - 4.9%

198. Consolidated Communications Hldgs. Inc. (CNSL) - 13.5%

199. CenturyLink Inc. (CTL) - 12%

200. Williams Companies Inc./The (WMB) - 5.1%

201. Outfront Media Inc. (OUT) - 7.3%

202. New York Community Bancorp Inc. (NYCB) - 5.8%

203. Navient Corp. (NAVI) - 4.8%

204. Costamare Inc. (CMRE) - 5.3%

205. Franklin Street Properties Corp. (FSP) - 8.5%

206. Gannett Co. Inc. (GCI) - 5.6%

207. IDT Corp. (IDT) - 7%

208. Buckle Inc./The (BKE) - 4.3%

32

This information is not personalized advice. It is for informational purposes only. Please see disclaimer at end of newsletter for more.

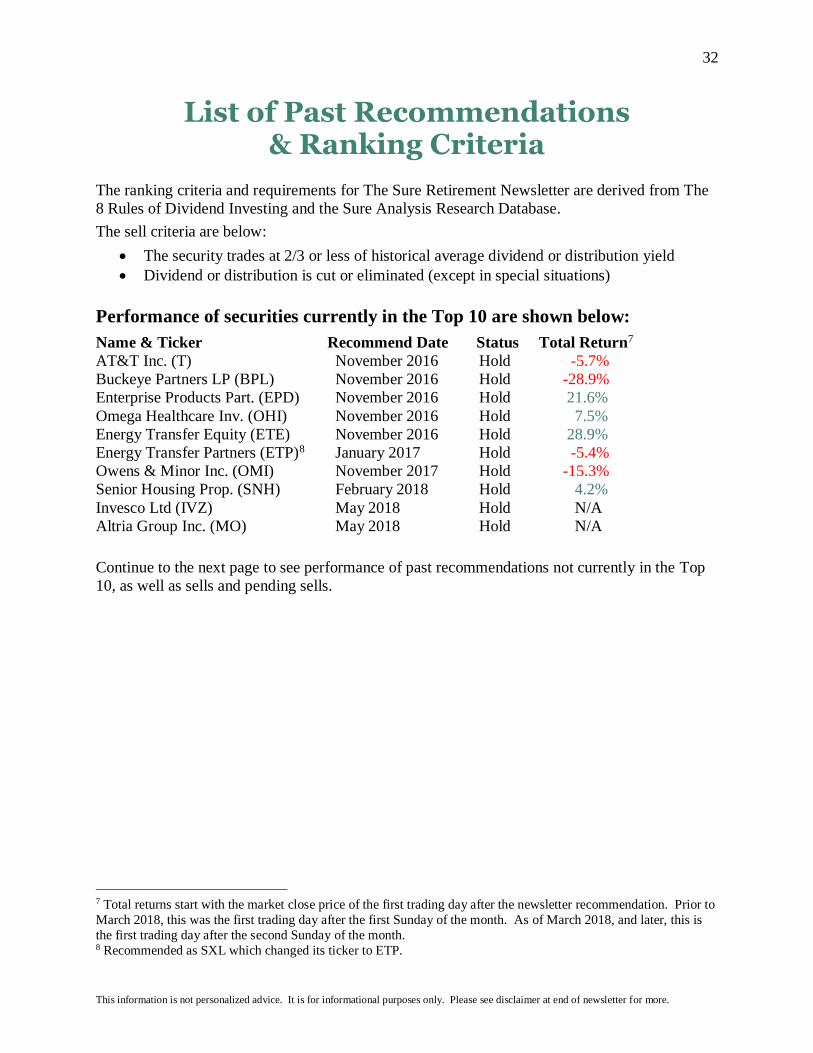

List of Past Recommendations & Ranking Criteria

The ranking criteria and requirements for The Sure Retirement Newsletter are derived from The

8 Rules of Dividend Investing and the Sure Analysis Research Database.

The sell criteria are below: