May 11, 2017 1 · – Agricultural land can be a major portion of NTC ... 200,000 -1,111 1,049 -62...

14

1 Property Taxes: From Levy Certification to Individual Tax Statement Shelby McQuay – Ehlers Andrea Uhl – Ehlers 1 May 11, 2017 Property Taxes Overview • District officials are sometimes expected to explain property taxes in detail: – At school board meetings – At Truth in Taxation hearings – In phone calls with “excited” taxpayers • Public expects simple answers, but….…it’s not simple 2 Property Taxes Overview • Today’s session will focus on: – Property tax basics – Computing individual parcel values – Calculating school taxes – Breaking down various taxing decisions on property owners & school district revenues 3

Transcript of May 11, 2017 1 · – Agricultural land can be a major portion of NTC ... 200,000 -1,111 1,049 -62...

1

Property Taxes:

From Levy Certification to Individual Tax Statement

Shelby McQuay – Ehlers

Andrea Uhl – Ehlers

1

May 11, 2017

Property Taxes

Overview

• District officials are sometimes

expected to explain property taxes

in detail:

– At school board meetings

– At Truth in Taxation hearings

– In phone calls with “excited” taxpayers

• Public expects simple answers,

but….…it’s not simple

2

Property Taxes

Overview

• Today’s session will focus on:

– Property tax basics

– Computing individual parcel values

– Calculating school taxes

– Breaking down various taxing decisions

on property owners & school district

revenues

3

2

Minnesota School District Property Taxes -

Key Steps in the Process & Who Does What

4

Minnesota School District Property Taxes -

Key Steps in the Process & When

5

March/April

Summer 2017

September 2017

Nov/Dec 2017

December 28, 2017

May 2018

October 2018

January 1, 2017

Taxpayers receive valuation notices for Pay 2018

Levy Setting Process

District adopts proposed 2017 Pay 2018 Levy &

Certifies it to Auditor

Counties send TNT Notices

TNT Hearings Held

Final property tax levy adopted by board & certified

to home county auditor

1st Half Property Taxes Due

2nd Half Property Taxes Due

Assessment Date

Property Taxes

Four Measures of Property Value

• Estimated Market Value (EMV)

• Taxable Market Value (TMV)

• Referendum Market Value (RMV)

• Net Tax Capacity (NTC & ANTC)

6

3

Property Taxes

Measures of Property Value

• Estimated Market Value (EMV)

– Starting point for other measures of property value

– Assessor’s estimate of true market value

• Taxable Market Value (TMV)

– Value used to calculate taxes

– May be less than EMV due to various limitations and exclusions

7

Property Taxes

Measures of Property Value

• Taxable Market Value Limitations and Exclusions

– Market Value Exclusion

– Green Acres

– This Old House

– This Old Business

– Platted Vacant Land Exclusion

– Border City Development Zone Exception

8

Property Taxes

9

Computation of Taxable Market Value

Residential Homestead Property – 4 Examples

A. Estimated Market Value (EMV)

1. Value up to $76,000 50,000 76,000 76,000 76,0002. Value in Excess of $76,000 0 24,000 124,000 337,800

3. Total (1 + 2) 50,000 100,000 200,000 413,800

B. Computation of Homestead Exclusion

1. Exclusion on Value up to $76,000 (A.1 * 40%) 20,000 30,400 30,400 30,400

(Lessor of $30,400 or (A.2 * 9%)) 0 2,160 11,160 30,400

3. Homestead Exclusion (Greater of 0 or (1 - 2)) 20,000 28,240 19,240 0

C. Taxable Market Value (B.1 - B.2) 30,000 71,760 180,760 413,800

2. Reduction Base on Value > $76,000

4

Property Taxes

Measures of Property Value

• Net Tax Capacity (NTC)

– Basis for calculating most taxes

10

NTC TMV Class Rate

• Adjusted Net Tax Capacity (ANTC)

– Basis for calculating aid

ANTC NTC

Sales Ratio

Property Taxes

11

Subject to

RMV Tax

Residential Homestead

First $500,000 1.00% Yes No

Over $500,000 1.25% Yes No

Blind/Disabled Homestead

Agricultural or nonagricultural

First $50,000

Commercial Seasonal Residential Recreational – used less than 250 days a

First $600,000 0.50% Yes,at 50% of TMV No

$600,001 - $2,300,000 1.00% Yes No

Over $2,300,000 1.25% Yes Yes

Agricultural Homestead House, Garage, One Acre

First $500,000 1.00% Yes No

Over $500,000 1.25% Yes No

Remainder of Farm

First $2,050,000 0.50% No No

Over $2,050,000 1.00% No No

2b Non-homestead Agricultural Land 1.00% No No

2c Managed Forest Land 0.65% No No

Class Rate Table for Minnesota Property Taxes Payable in 2017

1b

0 .45% Yes, at 45% of TMV No

Class Description

NTC

Class

Subject to

State Tax

1a

1c

2a

Property Taxes

12

Commercial-Industrial and Public Utility

First $150,000 1.50% Yes Yes

Over $150,000 2.00% Yes Yes

Rental Housing

Four or more units

Residential Non-homestead

1 to 3 units that does not qualify for class 4bb

4b(3) Agricultural Non-homestead containing more than one residence but fewer

than four along with the acre(s) and garage(s) 1.25% Yes No

Residential Non-homestead - Single unit or Single House, Garage and First

Acre on agricultural non-homestead land

First $500,000 1.00% Yes No

Over $500,000 1.25% Yes No

Seasonal Residential Recreational Commercial

First $500,000 1.00% Yes Yes

Over $500,000 1.25% Yes Yes

Seasonal Residential Recreational Non-Commercial

First $76,000 1.00% No Yes-40%

$76,000-500,000 1.00% No Yes

Over $500,000 1.25% No Yes

4d Qualifying Low Income Rental Housing 0.75% Yes, at 75% of TMV No

Class Rate Table for Minnesota Property Taxes Payable in 2017, continued3a

4a

1.25%

4c(1)

4c(12)

No

4b(1)

1.25% Yes No

4bb

Yes

5

Property Taxes

Measures of Property Value

• Referendum Market Value (RMV)

– Used to spread referendum, equity and transition levies

– RMV is equal to EMV, except for:

– Seasonal recreational residential property (cabins)

– Agricultural property – RMV equals the EMV of the house garage, and

one acre of land; RMV of other land and buildings is 0

13

Property Taxes

14

Example Calculations of Tax Capacity

Residential Homestead Property

A. Estimated Market Value (EMV)

1. Value up to $76,000 76,0002. Value in Excess of $76,000 24,000

3. Total (1 + 2) 100,000

B. Computation of Homestead Exclusion

1. Exclusion on Value up to $76,000 (A.1 * 40%) 30,400

(Lessor of $30,400 or (A.2 * 9%)) 2,160

3. Homestead Exclusion (Greater of 0 or (1 - 2)) 28,240

C. Taxable Market Value (B.1 - B.2) 71,760

2. Reduction Base on Value > $76,000

D. Computation of Tax Capacity

1. Value up to $500,000 (1.00%) 718

2. Value in Excess of $500,000 (1.25%) 0

3. Total (1 + 2) 718

76,000674,000

750,000

30,400

30,400

0

750,000

5,000

3,125

8,125

Property Taxes

15

Example Calculations of Tax Capacity

Commercial-Industrial Property

A. Estimated Market Value (EMV) 100,000

B. Computation of Homestead Exclusion 0

C. Taxable Market Value (TMV = EMV) 100,000

D. Computation of Tax Capacity1. Value up to $150,000 (1.5%) 1,5002. Value in Excess of $150,000 (2.00%) 03. Total (1 + 2) 1,500

750,000

0

750,000

2,25012,00014,250

6

Property Taxes

16

Example Calculations of Tax Capacity

Agricultural Homestead HGA

Land &

Buldings

A. Estimated Market Value (EMV) 2,500,0001. Value up to $76,000 76,0002. Value in Excess of $76,000 24,000

3. Total (1 + 2) 100,000 2,500,000

B. Computation of Homestead Exclusion

1. Exclusion on Value up to $76,000 (A.1 * 40%) 30,400

(Lessor of $30,400 or (A.2 * 9%)) 2,160

3. Homestead Exclusion (Greater of 0 or (1 - 2)) 28,240

C. Taxable Market Value 71,760 2,500,000

D. Computation of Tax Capacity

1. Value up to $500,000 (1.0%) 718 0

2. Value in Excess of $500,000 (1.25%) 0 0

3. Total (1 + 2) 718 0

E. Computation of Agricultural Tax Capacity

1. Value up to $2,050,000 (0.5%) 10,250

2. Value in Excess of $2,050,000 (1.0%) 4,500

3. Total (1 + 2) 14,750

2. Reduction Base on Value > $76,000

15,468

Total Tax Capacity

Property Taxes

17

Property Taxes

18

Example Calculations of Tax Capacity

Agricultural Non - Homestead

A. Estimated Market Value (EMV) 100,000 750,000

B. Computation of Homestead Exclusion 0 0

C. Taxable Market Value (TMV = EMV) 100,000 750,000

D. Computation of Tax Capacity (1.0%) 1,000 7,500

7

Property Taxes

Tax Rate Determination Value

• Also called “taxable net tax capacity”

19

TRDV 𝑝𝑟𝑜𝑝𝑒𝑟𝑡𝑖𝑒𝑠

𝑛

𝑥=1

Power

line tax

capacity

Fiscal

Disparities

Contribution Captured

portion of

TIF

Property Taxes

Fiscal Disparities

• Applied to commercial-industrial (C-I) property in the 7

county metro area since 1971

– Separate fiscal disparities program for the Iron Range that works

the same way

– Designed to share the tax benefits of new C-I property

throughout a larger area

– A highly complex program the makes property taxes in affected

area much harder to explain

20

Property Taxes

Tax Increment Financing (TIF)

• TIF is an economic development tool used by Cities and other local authorities – Complex rules and restrictions

– City or county creates TIF district and adopts TIF plan

– During term of plan:

21

Captured

Tax

Capacity

Current

Tax

Capacity

Original Tax

Capacity

8

Property Taxes

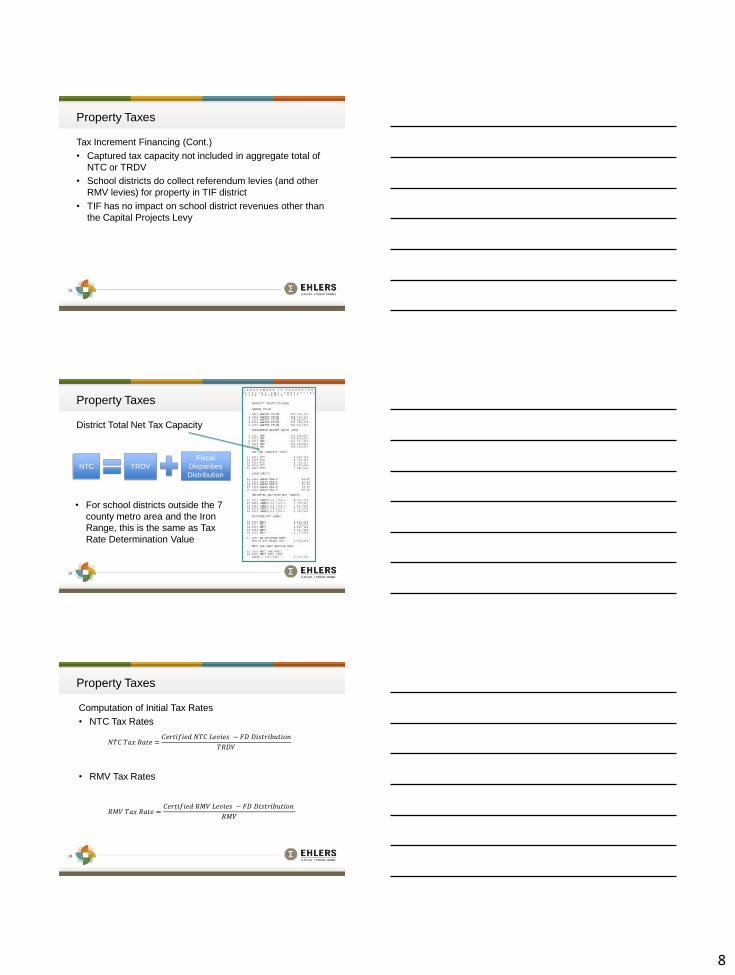

Tax Increment Financing (Cont.)

• Captured tax capacity not included in aggregate total of

NTC or TRDV

• School districts do collect referendum levies (and other

RMV levies) for property in TIF district

• TIF has no impact on school district revenues other than

the Capital Projects Levy

22

Property Taxes

District Total Net Tax Capacity

23

NTC TRDV

Fiscal

Disparities

Distribution

• For school districts outside the 7

county metro area and the Iron

Range, this is the same as Tax

Rate Determination Value

Property Taxes

Computation of Initial Tax Rates

• NTC Tax Rates

• RMV Tax Rates

24

𝑁𝑇𝐶 𝑇𝑎𝑥 𝑅𝑎𝑡𝑒 =𝐶𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑 𝑁𝑇𝐶 𝐿𝑒𝑣𝑖𝑒𝑠 − 𝐹𝐷 𝐷𝑖𝑠𝑡𝑟𝑖𝑏𝑢𝑡𝑖𝑜𝑛

𝑇𝑅𝐷𝑉

𝑅𝑀𝑉 𝑇𝑎𝑥 𝑅𝑎𝑡𝑒 =𝐶𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑 𝑅𝑀𝑉 𝐿𝑒𝑣𝑖𝑒𝑠 − 𝐹𝐷 𝐷𝑖𝑠𝑡𝑟𝑖𝑏𝑢𝑡𝑖𝑜𝑛

𝑅𝑀𝑉

9

Property Taxes

Computation of Gross Tax

25

Gross

School

Tax

Taxable

Net Tax

Capacity

Total

Referendum

Market Value

NTC

Rate

RMV

Rate

Property Taxes

26

Property Taxes

27

10

Property Taxes

28

Property Taxes

Market Value Credits

• Agricultural Homestead Market Value Credit

– Credit equal to 0.3% of the first $115,000 of taxable market value

excluding the HGA

– Plus 0.1% of TMV in excess of $115,000

– Maximum credit of $490

29

Property Taxes

• Tax bases vary by district, most notably in Greater MN

30

Source: Willette, Rural Legislative Forum, Mankato 2016

11

Property Taxes

• Various property types have been growing at different rates

31

Source: Willette, Rural Legislative Forum, Mankato 2016

Property Taxes

• More farms can mean more tax base per pupil

32

Source: Willette, Rural Legislative Forum, Mankato 2016

Property Taxes

• School Building Bond Credit (Ag2School Credit)

– Proposed credit to farmers on school debt levies

– Paid for with state dollars, not shifted to other properties

– Currently in conference committee

• Governor @ 40%

• House @ 50%

• Senate @ 40%

33

12

Property Taxes

• Example: Agricultural Area District

– Agricultural land is not included in the RMV tax base (except

HGA)

– Agricultural land can be a major portion of NTC

– Residential Homestead can be much bigger portion of RMV than

NTC

– Not many voters per acre

34

Property Taxes

35

Example: Agricultural Area District

*Totals do not include TIF and Fiscal Disparities adjustments

Market ValuePercent of

Total

Referendum

Market Value

Percent of

TotalNet Tax Capacity*

Percent of

Total

Total 460,083,215 65,304,175 3,797,587

Residential Homestead 25,546,996 5.6% 25,380,456 38.9% 194,116 5.1%

Other Residential 4,702,480 1.0% 4,702,480 7.2% 50,071 1.3%

Commercial / Industrial 22,025,233 4.8% 22,025,233 33.7% 433,381 11.4%

Agricultural 407,430,306 88.6% 13,196,006 20.2% 3,116,237 82.1%

Seasonal Recreational 378,200 0.1% - 0.0% 3,782 0.1%

Property Taxes

36

Description Reduce Referendum

by $1,500 Bond Issue Net

per Pupil Unit $19.400 Million Change

Estimated Tax Rates for

Proposed Questions NTC Tax Rate: 58.05% 58.05%

RMV Tax Rate: -0.556% -0.556%

Estimated

Type of Property Market Value

50,000 -278 174 -104

Residential 70,000 -389 244 -145

Homestead 80,000 -444 290 -154

100,000 -556 417 -139

200,000 -1,111 1,049 -62

Commercial/ 50,000 -278 435 157

Industrial 100,000 -556 871 315

Agricultural 600,000 -556 1,868 1,312

Homestead 800,000 -556 2,448 1,892

1,000,000 -556 3,029 2,473

Agricultural 2,000 0.00 11.61 11.61

Non-Homestead 2,500 0.00 14.51 14.51

(dollars per acre) 3,000 0.00 17.42 17.42

Estimated Change in Taxes*

13

Minnesota Homestead Credit “Circuit Breaker” Refund

• Existed since 1970s

• Available to all owners of homestead property both residential and agricultural (refund on agricultural homestead property is based on taxes paid only on HGA)

• For 2016 taxes, annual household income must be less than $108,660 for homeowners and $58,880 for renters (income limit is higher if you have dependents)

• Refund is sliding scale, based on total property taxes and income

• Maximum refund is $2,660 for homeowners and $2,060 for renters

• Especially helpful to those with lower incomes

• Fill out state tax form M1PR

37

Special Property Tax Refund

• Available for all homestead property, both residential and

agricultural (refund on agricultural homestead property is

based on taxes paid only on HGA) with a gross tax

increase of at least 12% and $100 over prior year

• Refund is 60% of amount by which tax increase exceeds

greater of 12% or $100, up to a maximum of $1,000

• No income limits

• Fill out state tax form M1PR

38

Senior Citizen Property Tax Deferral

• Allows people 65 years of age or older with household income of $60,000 or less to defer a portion of property taxes on their home

• Taxes paid in any year limited to 3% of household income for year before entering deferral program; this amount does not change in future years

• Additional taxes deferred, not forgiven

• State charges interest up to 5% per year on deferred taxes and attaches a lien to property

• Deferred property taxes plus accrued interest must be paid when home is sold or homeowner(s) dies

39

14

(651) 697-8542

Andrea Uhl

Financial Specialist

(651) 697-8548

Shelby McQuay

Municipal Advisor

40