Maximizing After-Tax Returns for High Net Worth Investors invested on January 1, 2003 $100,000...

33

Maximizing After-Tax Returns for High Net Worth Investors

-

Upload

duongtuyen -

Category

Documents

-

view

212 -

download

0

Transcript of Maximizing After-Tax Returns for High Net Worth Investors invested on January 1, 2003 $100,000...

Maximizing After-Tax Returns for High Net Worth Investors

1

World-class money managementand superior tax advantages

of CI Corporate Class in an exclusive offering to affluent investors.

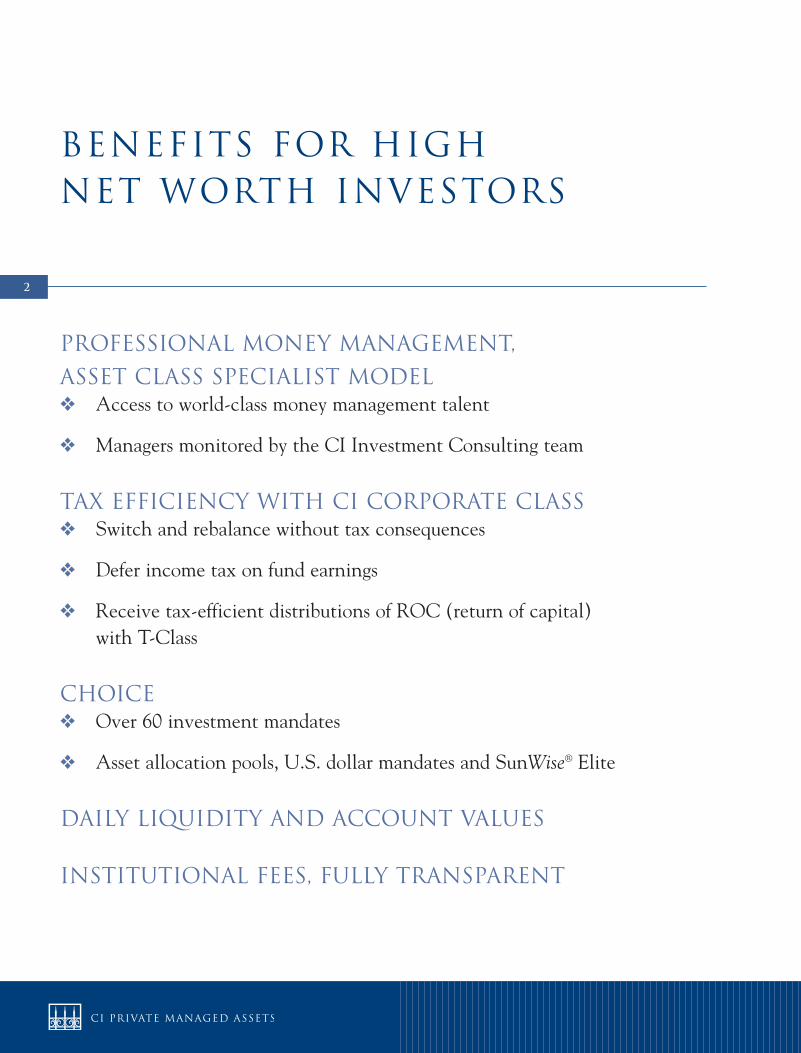

2

Professional money management,

asset class specialist model� Access to world-class money management talent

� Managers monitored by the CI Investment Consulting team

Tax efficiency with CI Corporate Class� Switch and rebalance without tax consequences

� Defer income tax on fund earnings

� Receive tax-efficient distributions of ROC (return of capital) with T-Class

Choice� Over 60 investment mandates

� Asset allocation pools, U.S. dollar mandates and SunWise® Elite

Daily liquidity and account values

Institutional fees, fully transparent

Benefits for High Net Worth Investors

3

Professional Money Management

Large Selection of Industry-Leading

Investment Professionals

TridentInvestment Management

4

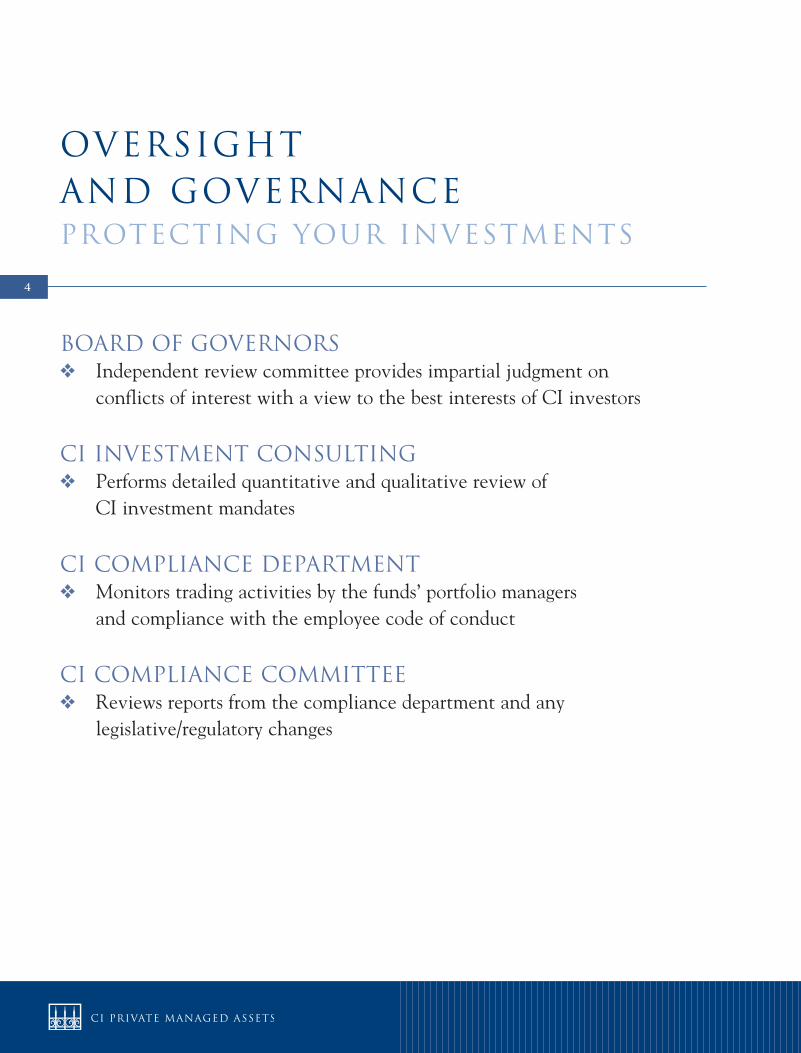

Oversight and GovernanceProtecting Your Investments

Board of Governors� Independent review committee provides impartial judgment on

conflicts of interest with a view to the best interests of CI investors

CI Investment Consulting� Performs detailed quantitative and qualitative review of

CI investment mandates

CI Compliance Department� Monitors trading activities by the funds’ portfolio managers

and compliance with the employee code of conduct

CI Compliance Committee� Reviews reports from the compliance department and any

legislative/regulatory changes

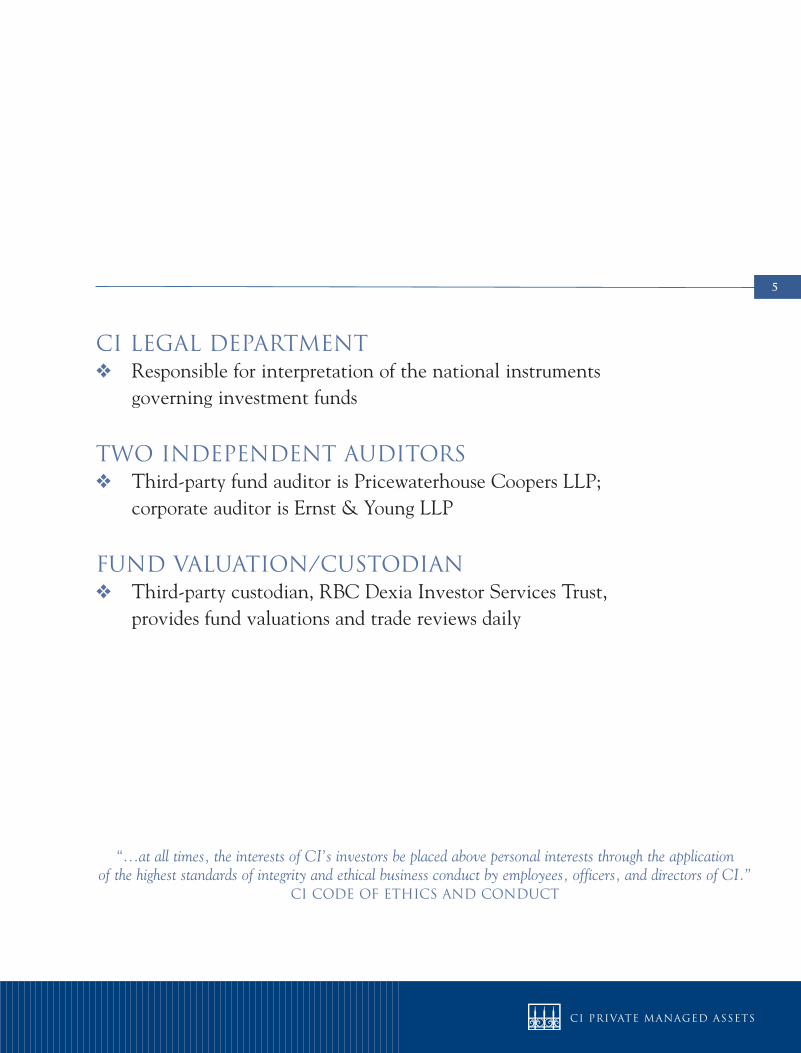

5

CI Legal Department� Responsible for interpretation of the national instruments

governing investment funds

Two independent auditors� Third-party fund auditor is Pricewaterhouse Coopers LLP;

corporate auditor is Ernst & Young LLP

Fund valuation/custodian� Third-party custodian, RBC Dexia Investor Services Trust,

provides fund valuations and trade reviews daily

“…at all times, the interests of CI’s investors be placed above personal interests through the application of the highest standards of integrity and ethical business conduct by employees, officers, and directors of CI.”

CI Code of Ethics and Conduct

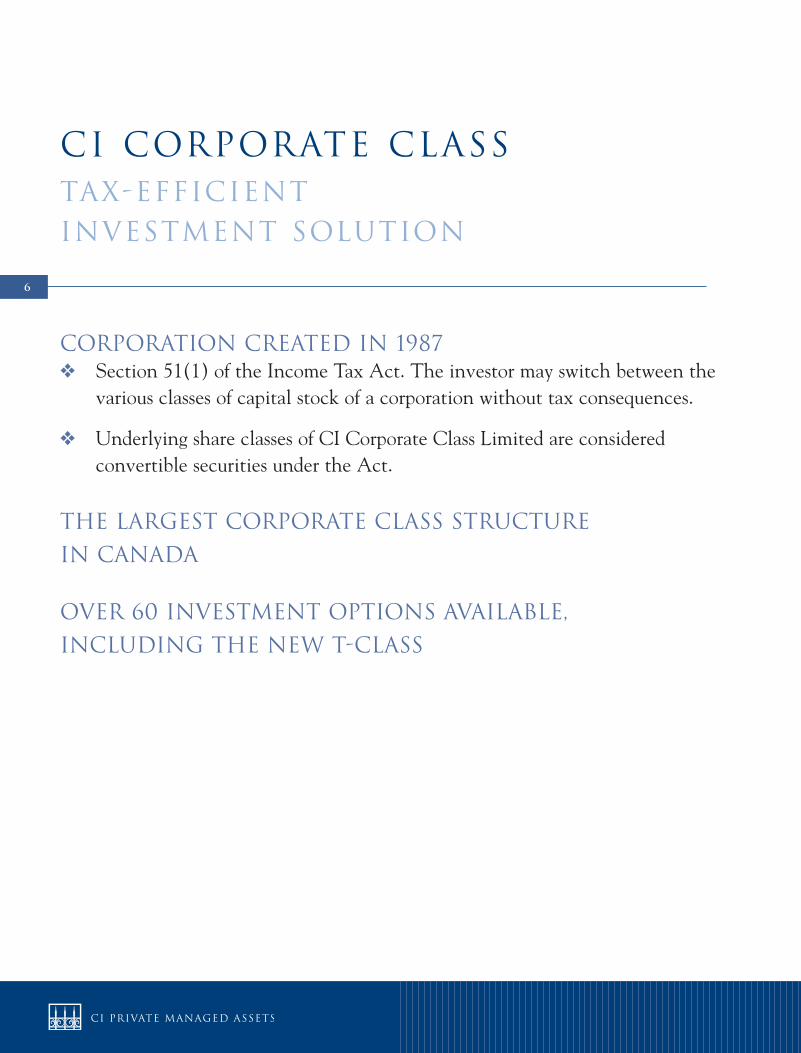

6

Corporation created in 1987� Section 51(1) of the Income Tax Act. The investor may switch between the

various classes of capital stock of a corporation without tax consequences.

� Underlying share classes of CI Corporate Class Limited are consideredconvertible securities under the Act.

The largest corporate class structure

in Canada

Over 60 investment options available,

including the new T-Class

CI Corporate ClassTax-Efficient Investment Solution

7

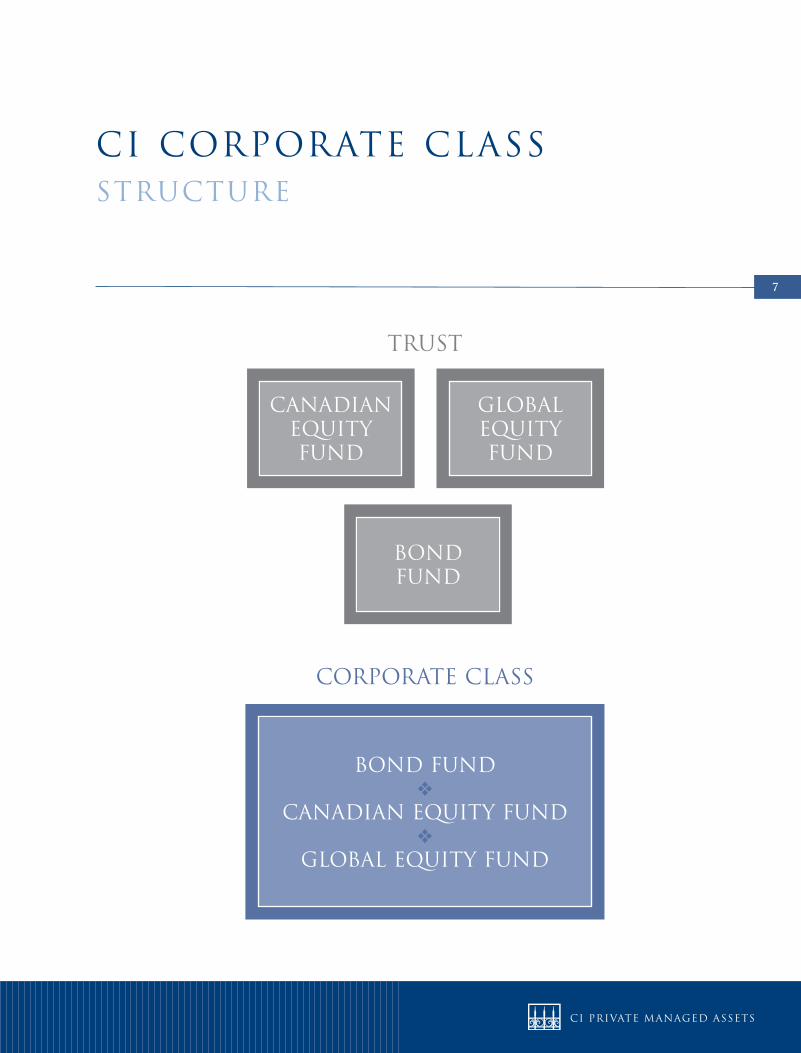

CI Corporate Classstructure

Bond fund�

canadian equity fund�

global equity fund

corporate class

trust

bondfund

canadianequityfund

globalequity fund

8

CI has designed and manages a tax-effective

corporate class structure with:� Diversification of asset classes to help offset capital gains and losses

� The ability to pool income and expenses within the corporation for all share classes

� A larger weighting of equities to fixed income so that interest income is offset by expenses

� The goal of maintaining our fiduciary responsibility to shareholders of the various shares of the corporation.

CI Corporate ClassManagement

9

SWITCH � Between mandates without tax consequences

DEFER � Income tax on distributions, given its low dividend payout policy

CONVERT � Interest income and foreign dividends into capital gains by applying

expenses to Corporate Class as a whole.

CI Corporate ClassAdvantages

10

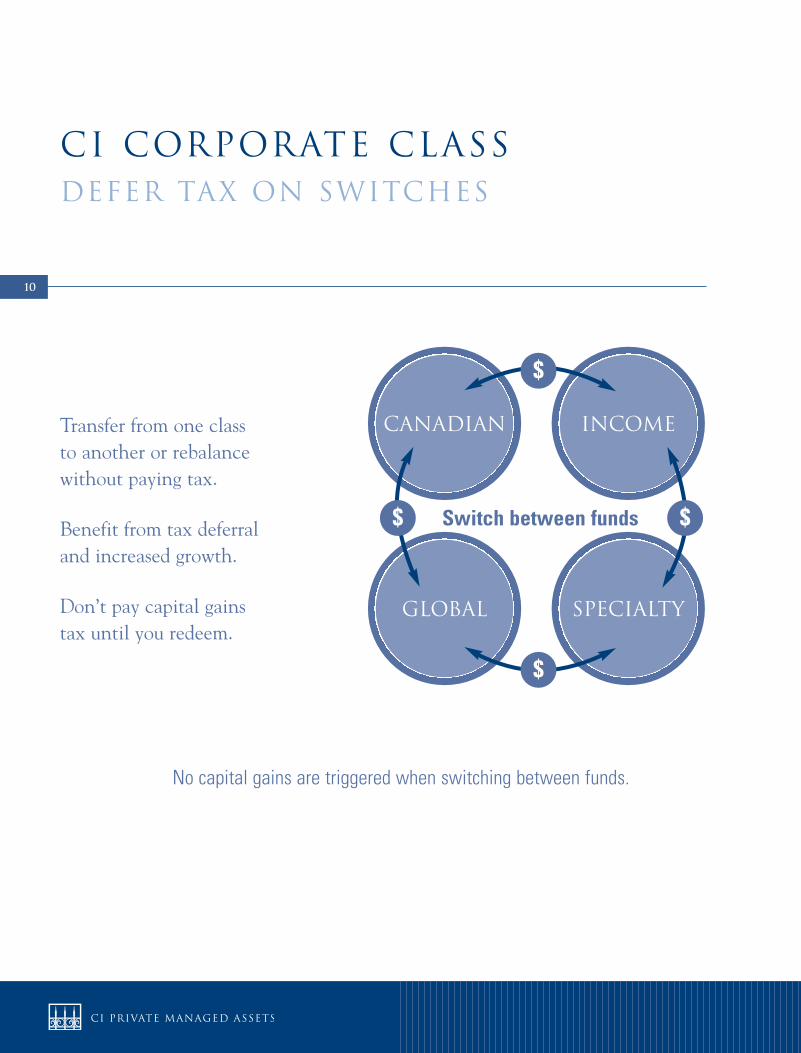

CI Corporate ClassDefer Tax on Switches

Transfer from one class to another or rebalance without paying tax.

Benefit from tax deferraland increased growth.

Don’t pay capital gains tax until you redeem.

canadian Income

global specialty

Switch between funds

No capital gains are triggered when switching between funds.

$

$

$$

11

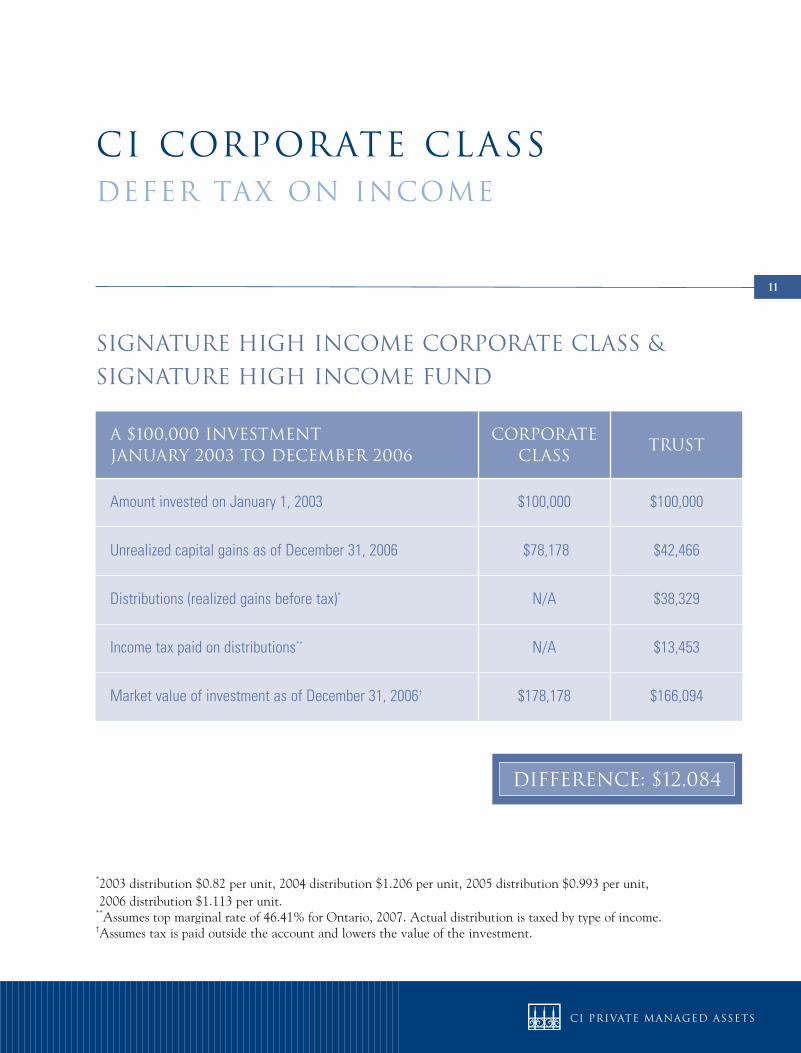

signature high income corporate class &

signature high income fund

CI Corporate ClassDefer Tax on income

A $100,000 investment JanUARY 2003 to DecEMBER 2006

CorporateClass

Trust

Amount invested on January 1, 2003 $100,000 $100,000

Unrealized capital gains as of December 31, 2006 $78,178 $42,466

Distributions (realized gains before tax)* N/A $38,329

Income tax paid on distributions** N/A $13,453

Market value of investment as of December 31, 2006† $178,178 $166,094

*2003 distribution $0.82 per unit, 2004 distribution $1.206 per unit, 2005 distribution $0.993 per unit, 2006 distribution $1.113 per unit. **Assumes top marginal rate of 46.41% for Ontario, 2007. Actual distribution is taxed by type of income. †Assumes tax is paid outside the account and lowers the value of the investment.

difference: $12,084

12

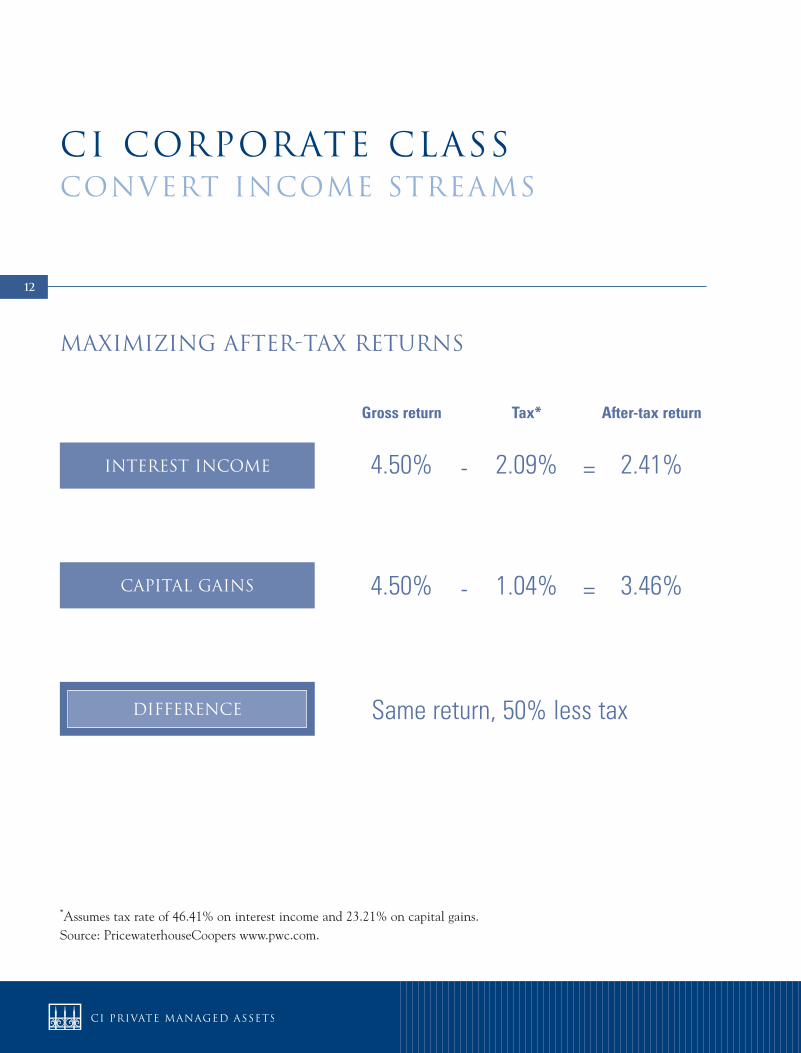

CI Corporate Classconvert income streams

*Assumes tax rate of 46.41% on interest income and 23.21% on capital gains. Source: PricewaterhouseCoopers www.pwc.com.

difference

capital gains

interest income 4.50% 2.09% 2.41%

Same return, 50% less tax

Maximizing After-Tax Returns

- =

4.50% 1.04% 3.46%- =

Gross return Tax* After-tax return

13

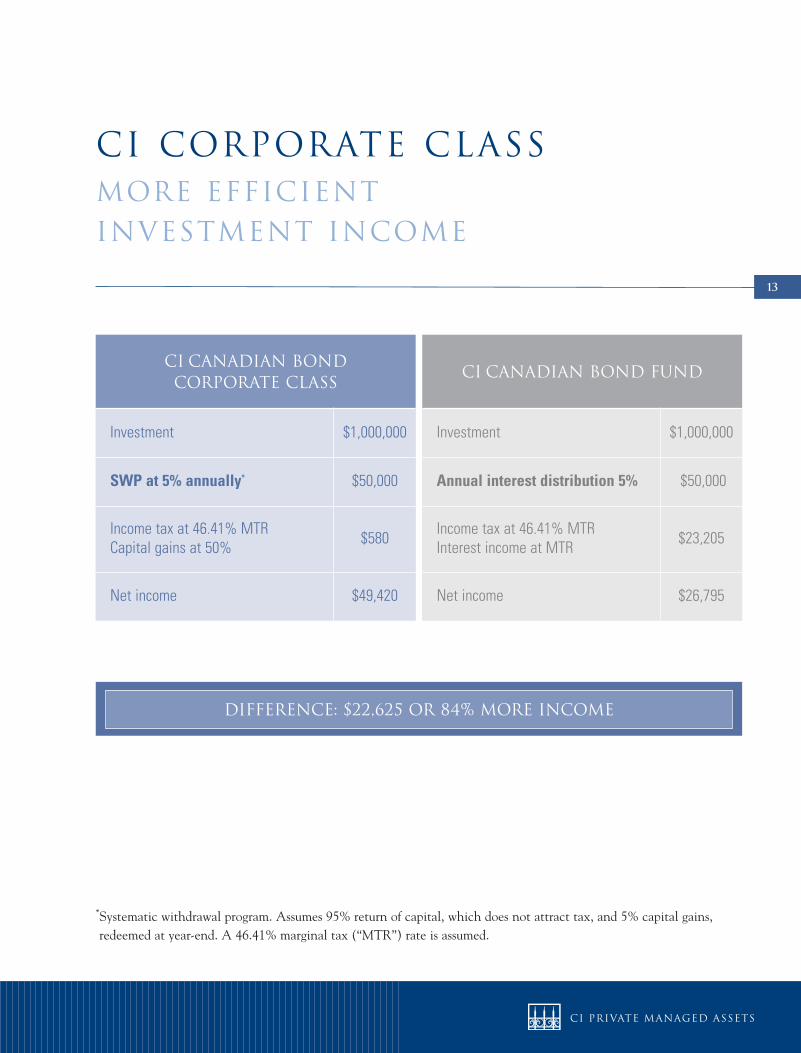

CI Corporate ClassMore Efficient Investment Income

CI Canadian bond corporate class

Investment $1,000,000

SWP at 5% annually* $50,000

Income tax at 46.41% MTRCapital gains at 50% $580

Net income $49,420

CI Canadian bond fund

Investment $1,000,000

Annual interest distribution 5% $50,000

Income tax at 46.41% MTRInterest income at MTR $23,205

Net income $26,795

*Systematic withdrawal program. Assumes 95% return of capital, which does not attract tax, and 5% capital gains,redeemed at year-end. A 46.41% marginal tax (“MTR”) rate is assumed.

difference: $22,625 or 84% more income

14

� Creates a predictable, tax-effective stream of monthly cash flow withoutsacrificing the potential for growth

� Choice of two annual target distributions of 5% or 8% (paid monthly)

� Monthly distributions are return of capital (ROC)*

� 17 T-Class mandates available within the PMA platform

� Tax-free switching between all CI Corporate Class mandates

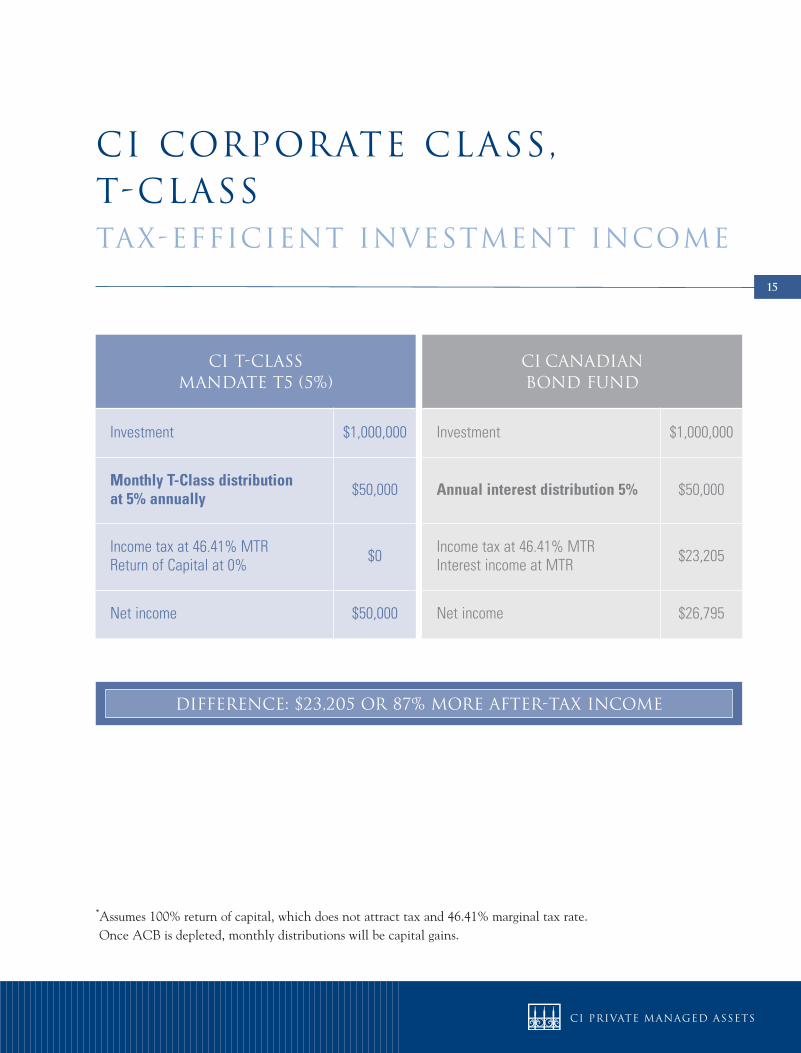

CI Corporate Class, t-classDefer Tax on Investment Income

*Once ACB is depleted, monthly distributions will be capital gains.

15

CI Corporate Class, t-classtax-efficient investment income

CI T-class mandate t5 (5%)

Investment $1,000,000

Monthly T-Class distribution at 5% annually $50,000

Income tax at 46.41% MTRReturn of Capital at 0% $0

Net income $50,000

CI Canadian bond fund

Investment $1,000,000

Annual interest distribution 5% $50,000

Income tax at 46.41% MTRInterest income at MTR $23,205

Net income $26,795

*Assumes 100% return of capital, which does not attract tax and 46.41% marginal tax rate. Once ACB is depleted, monthly distributions will be capital gains.

difference: $23,205 or 87% more after-tax income

16

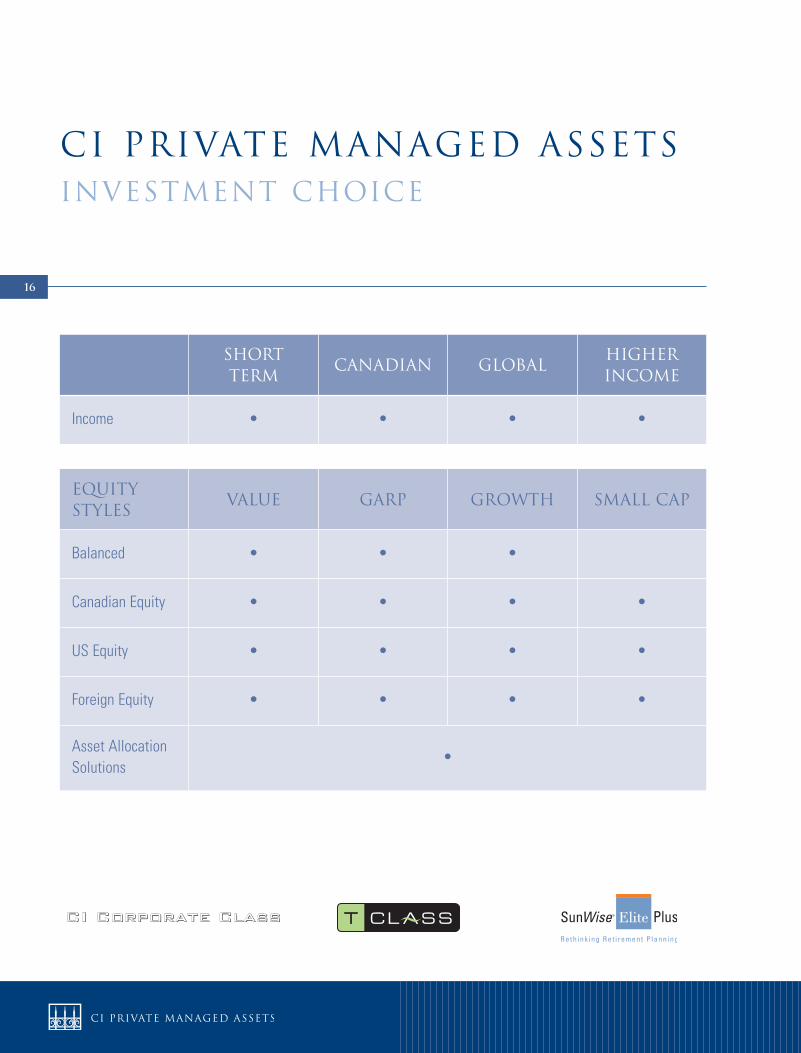

CI Private Managed AssetsInvestment Choice

Short Term

Canadian GlobalHigherIncome

Income • • • •

EquityStyles

Value GARP Growth Small Cap

Balanced • • •

Canadian Equity • • • •

US Equity • • • •

Foreign Equity • • • •

Asset AllocationSolutions

•

17

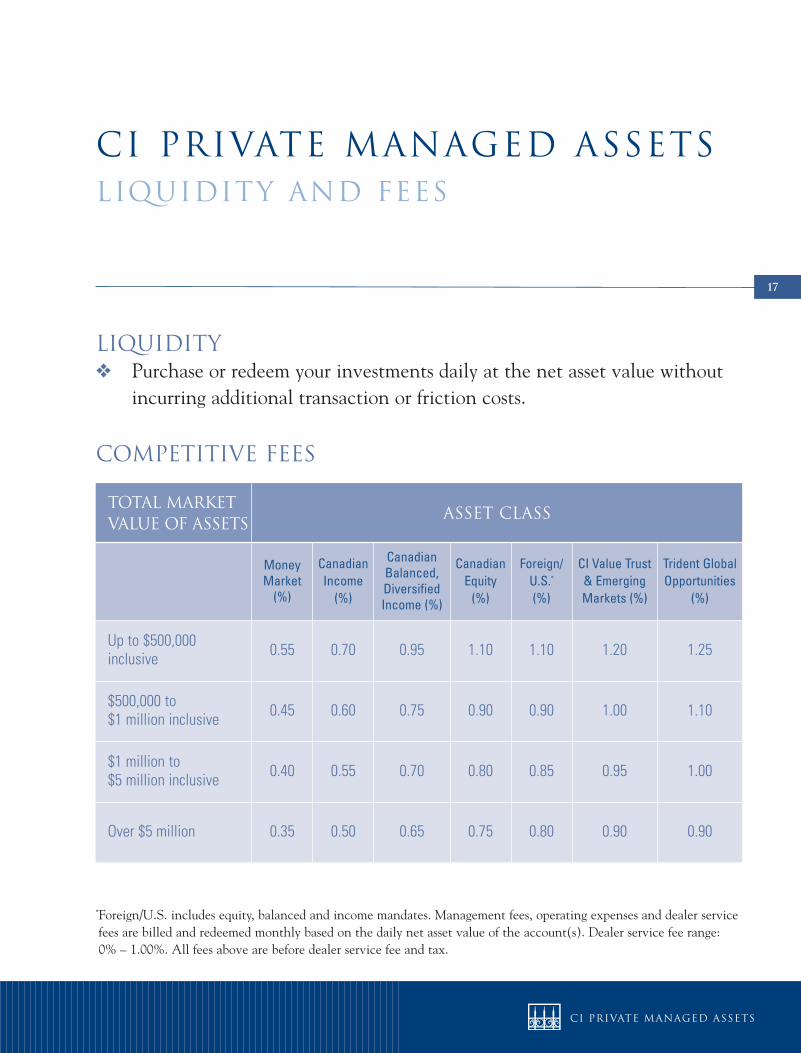

Liquidity� Purchase or redeem your investments daily at the net asset value without

incurring additional transaction or friction costs.

Competitive Fees

Total MarketValue of Assets

Asset class

Money Market(%)

Canadian Income(%)

Canadian Balanced, DiversifiedIncome (%)

CanadianEquity(%)

Foreign/U.S.*

(%)

CI Value Trust & EmergingMarkets (%)

Trident GlobalOpportunities

(%)

Up to $500,000 inclusive 0.55 0.70 0.95 1.10 1.10 1.20 1.25

$500,000 to $1 million inclusive 0.45 0.60 0.75 0.90 0.90 1.00 1.10

$1 million to $5 million inclusive 0.40 0.55 0.70 0.80 0.85 0.95 1.00

Over $5 million 0.35 0.50 0.65 0.75 0.80 0.90 0.90

*Foreign/U.S. includes equity, balanced and income mandates. Management fees, operating expenses and dealer servicefees are billed and redeemed monthly based on the daily net asset value of the account(s). Dealer service fee range:0% – 1.00%. All fees above are before dealer service fee and tax.

CI Private Managed Assetsliquidity and fees

18

other value-added ci services

� Detailed quarterly account statements

� Tax-deferred automatic rebalancing and/or systematic transfer program

� Automated systematic withdrawal program

� On-line account access

� Support and research through CI’s Private Managed Assets AccountManagement team

19

CI Private Managed Assetssummary

� World-class multi-manager solution available on one platform

� Tax deferral on rebalancing and re-allocations between managers through CI Corporate Class

� Potential for tax-deferred income investing

� Potential to re-characterize income distributions as ROC or capital gains by using T-Class

� Liquidity – account valued daily

� Competitive fee structure

20

21

Appendix

program parameters

and examples

22

23

� $500,000 minimum per account

� $100,000 minimum per mandate

� Subsequent purchases $5,000

� No DSC or FE commission option

� Advisor service fee range: 0% to 1.0%

� All fees redeemed monthly

� Automatic portfolio rebalancing feature

CI Private Managed Assetseligibility and features

24

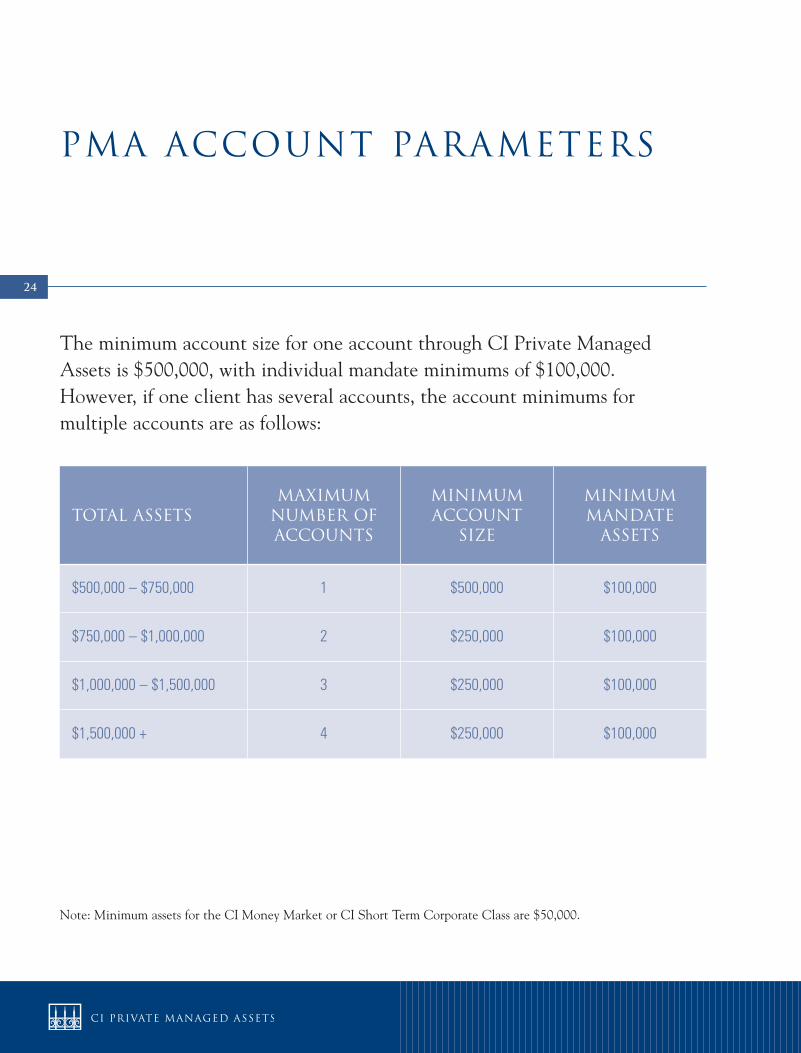

Total AssetsMaximum number ofaccounts

Minimum account

size

Minimum Mandate Assets

$500,000 – $750,000 1 $500,000 $100,000

$750,000 – $1,000,000 2 $250,000 $100,000

$1,000,000 – $1,500,000 3 $250,000 $100,000

$1,500,000 + 4 $250,000 $100,000

Note: Minimum assets for the CI Money Market or CI Short Term Corporate Class are $50,000.

The minimum account size for one account through CI Private Managed Assets is $500,000, with individual mandate minimums of $100,000. However, if one client has several accounts, the account minimums for multiple accounts are as follows:

pma account parameters

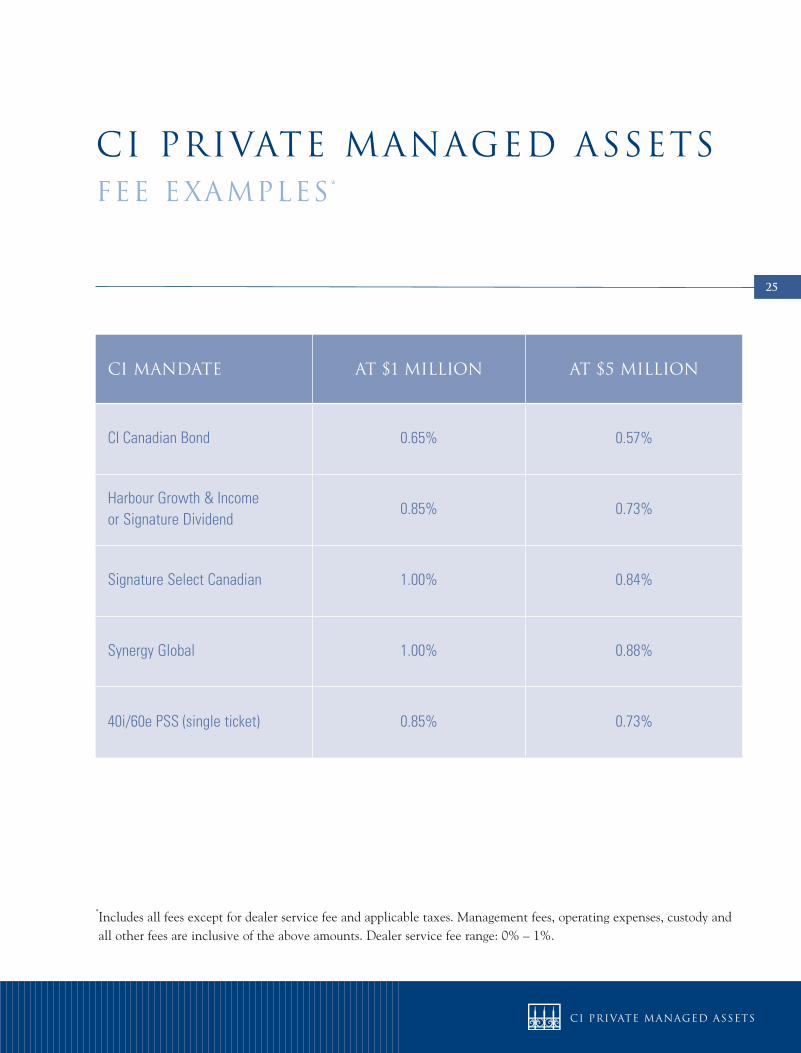

25

CI Mandate At $1 Million At $5 Million

CI Canadian Bond 0.65% 0.57%

Harbour Growth & Income or Signature Dividend

0.85% 0.73%

Signature Select Canadian 1.00% 0.84%

Synergy Global 1.00% 0.88%

40i/60e PSS (single ticket) 0.85% 0.73%

*Includes all fees except for dealer service fee and applicable taxes. Management fees, operating expenses, custody and all other fees are inclusive of the above amounts. Dealer service fee range: 0% – 1%.

CI Private Managed Assetsfee examples*

26

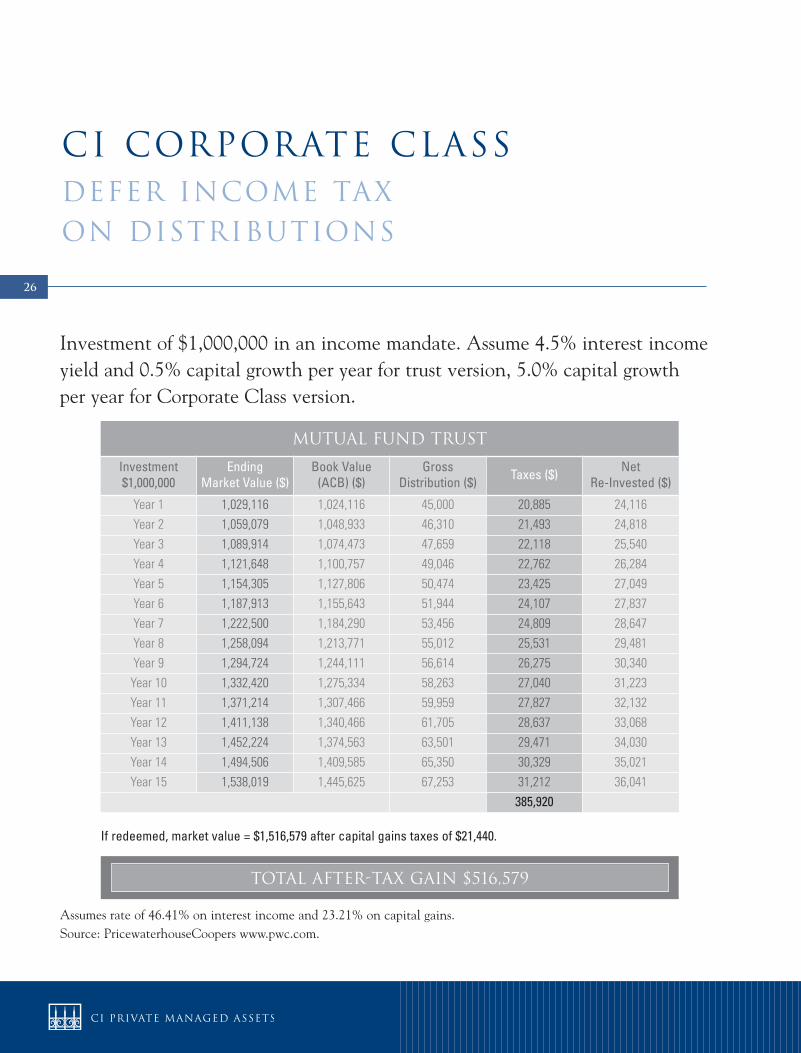

Assumes rate of 46.41% on interest income and 23.21% on capital gains.Source: PricewaterhouseCoopers www.pwc.com.

If redeemed, market value = $1,516,579 after capital gains taxes of $21,440.

Investment of $1,000,000 in an income mandate. Assume 4.5% interest incomeyield and 0.5% capital growth per year for trust version, 5.0% capital growth per year for Corporate Class version.

MUTUAL FUND TRUST

Investment$1,000,000

EndingMarket Value ($)

Book Value(ACB) ($)

Gross Distribution ($) Taxes ($) Net

Re-Invested ($)

Year 1 1,029,116 1,024,116 45,000 20,885 24,116Year 2 1,059,079 1,048,933 46,310 21,493 24,818Year 3 1,089,914 1,074,473 47,659 22,118 25,540Year 4 1,121,648 1,100,757 49,046 22,762 26,284Year 5 1,154,305 1,127,806 50,474 23,425 27,049Year 6 1,187,913 1,155,643 51,944 24,107 27,837Year 7 1,222,500 1,184,290 53,456 24,809 28,647Year 8 1,258,094 1,213,771 55,012 25,531 29,481Year 9 1,294,724 1,244,111 56,614 26,275 30,340Year 10 1,332,420 1,275,334 58,263 27,040 31,223Year 11 1,371,214 1,307,466 59,959 27,827 32,132Year 12 1,411,138 1,340,466 61,705 28,637 33,068Year 13 1,452,224 1,374,563 63,501 29,471 34,030Year 14 1,494,506 1,409,585 65,350 30,329 35,021Year 15 1,538,019 1,445,625 67,253 31,212 36,041

385,920

CI corporate classdefer income tax on distributions

Total after-tax gain $516,579

27

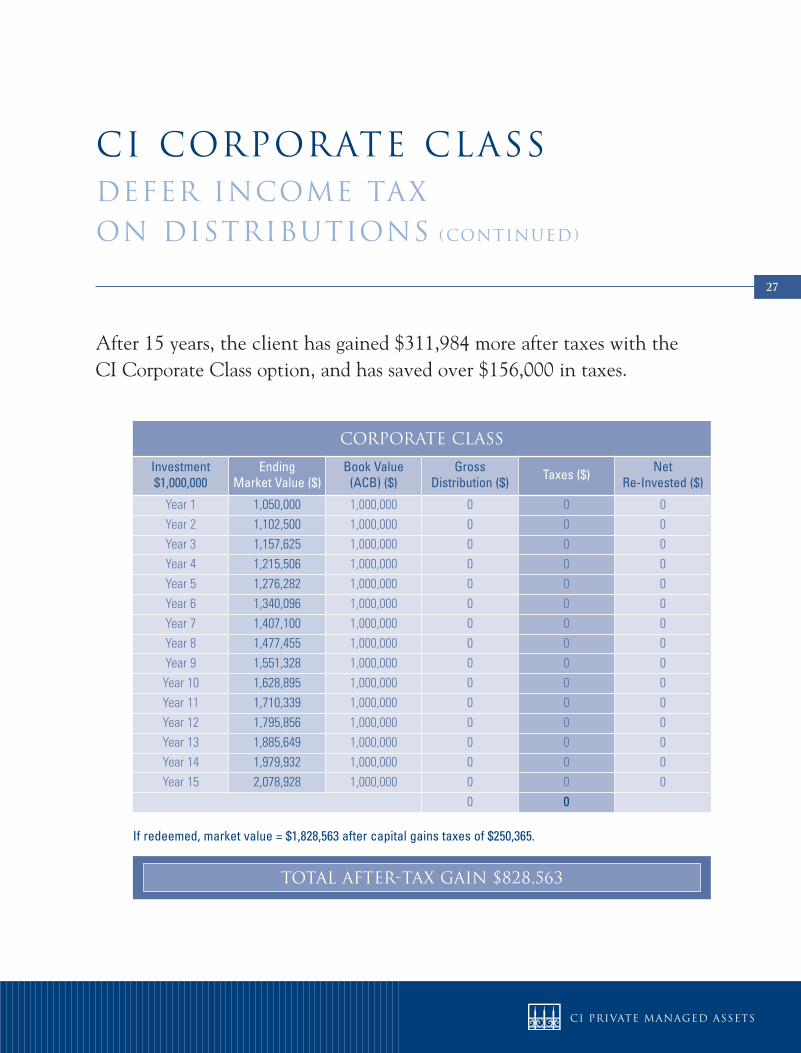

CI corporate classdefer income tax on distributions (CONTINUEd)

After 15 years, the client has gained $311,984 more after taxes with the CI Corporate Class option, and has saved over $156,000 in taxes.

corporate class

Investment$1,000,000

EndingMarket Value ($)

Book Value(ACB) ($)

Gross Distribution ($) Taxes ($) Net

Re-Invested ($)

Year 1 1,050,000 1,000,000 0 0 0Year 2 1,102,500 1,000,000 0 0 0Year 3 1,157,625 1,000,000 0 0 0Year 4 1,215,506 1,000,000 0 0 0Year 5 1,276,282 1,000,000 0 0 0Year 6 1,340,096 1,000,000 0 0 0Year 7 1,407,100 1,000,000 0 0 0Year 8 1,477,455 1,000,000 0 0 0Year 9 1,551,328 1,000,000 0 0 0Year 10 1,628,895 1,000,000 0 0 0Year 11 1,710,339 1,000,000 0 0 0Year 12 1,795,856 1,000,000 0 0 0Year 13 1,885,649 1,000,000 0 0 0Year 14 1,979,932 1,000,000 0 0 0Year 15 2,078,928 1,000,000 0 0 0

0 0

Total after-tax gain $828,563

If redeemed, market value = $1,828,563 after capital gains taxes of $250,365.

28

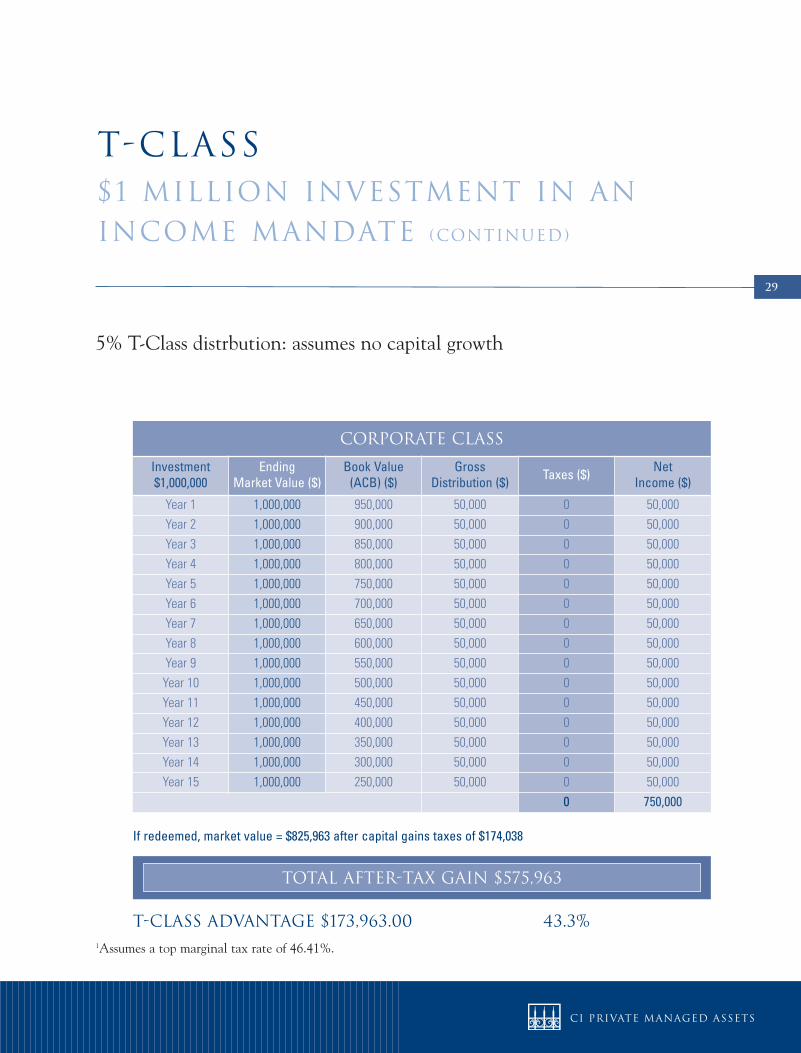

1Assumes a top marginal tax rate of 46.41%.

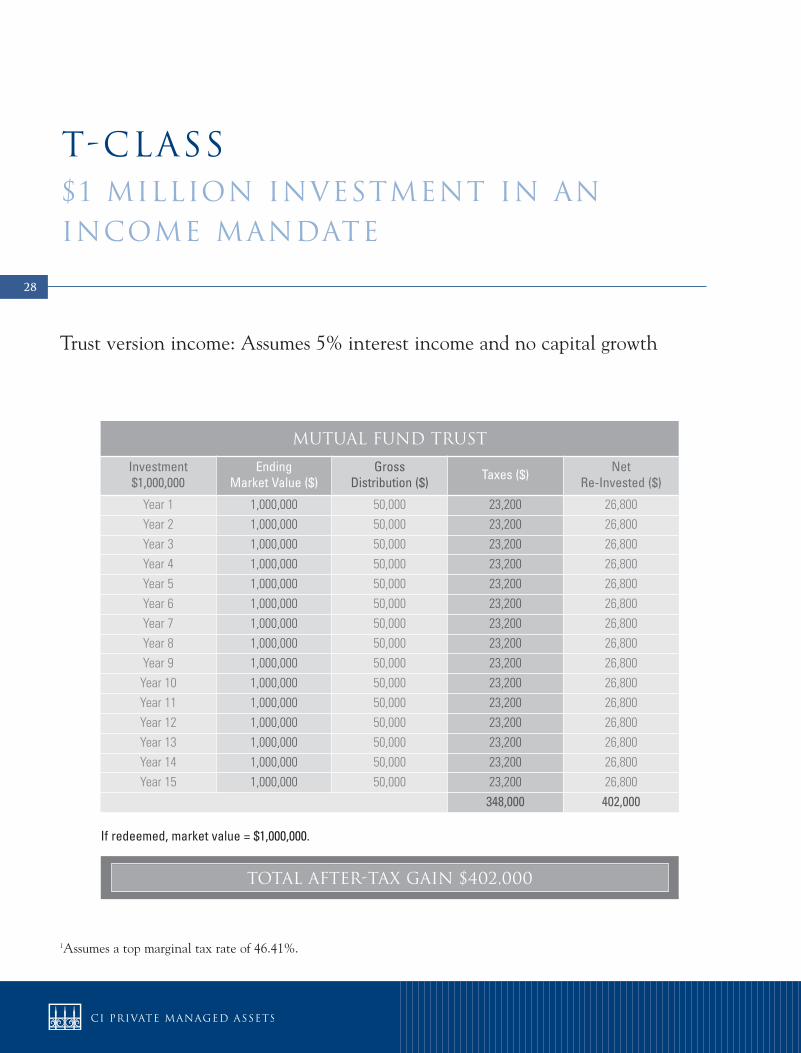

Trust version income: Assumes 5% interest income and no capital growth

T-class$1 million investment in anincome mandate

MUTUAL FUND TRUST

Investment$1,000,000

EndingMarket Value ($)

GrossDistribution ($) Taxes ($) Net

Re-Invested ($)

Year 1 1,000,000 50,000 23,200 26,800Year 2 1,000,000 50,000 23,200 26,800Year 3 1,000,000 50,000 23,200 26,800Year 4 1,000,000 50,000 23,200 26,800Year 5 1,000,000 50,000 23,200 26,800Year 6 1,000,000 50,000 23,200 26,800Year 7 1,000,000 50,000 23,200 26,800Year 8 1,000,000 50,000 23,200 26,800Year 9 1,000,000 50,000 23,200 26,800Year 10 1,000,000 50,000 23,200 26,800Year 11 1,000,000 50,000 23,200 26,800Year 12 1,000,000 50,000 23,200 26,800Year 13 1,000,000 50,000 23,200 26,800Year 14 1,000,000 50,000 23,200 26,800Year 15 1,000,000 50,000 23,200 26,800

348,000 402,000

If redeemed, market value = $1,000,000.

Total after-tax gain $402,000

29

t-class advantage $173,963.00 43.3%1Assumes a top marginal tax rate of 46.41%.

5% T-Class distrbution: assumes no capital growth

T-class$1 million investment in anincome mandate (CONTINUEd)

corporate class

Investment$1,000,000

Ending Market Value ($)

Book Value(ACB) ($)

Gross Distribution ($) Taxes ($) Net

Income ($)

Year 1 1,000,000 950,000 50,000 0 50,000Year 2 1,000,000 900,000 50,000 0 50,000Year 3 1,000,000 850,000 50,000 0 50,000Year 4 1,000,000 800,000 50,000 0 50,000Year 5 1,000,000 750,000 50,000 0 50,000Year 6 1,000,000 700,000 50,000 0 50,000Year 7 1,000,000 650,000 50,000 0 50,000Year 8 1,000,000 600,000 50,000 0 50,000Year 9 1,000,000 550,000 50,000 0 50,000Year 10 1,000,000 500,000 50,000 0 50,000Year 11 1,000,000 450,000 50,000 0 50,000Year 12 1,000,000 400,000 50,000 0 50,000Year 13 1,000,000 350,000 50,000 0 50,000Year 14 1,000,000 300,000 50,000 0 50,000Year 15 1,000,000 250,000 50,000 0 50,000

0 750,000

If redeemed, market value = $825,963 after capital gains taxes of $174,038

Total after-tax gain $575,963

30

31

All charts and illustrations in this guide are for illustrative purposes only. They are not intended to predict or projectinvestment results.

®CI Investments, the CI Investments design and Harbour Advisors are registered trademarks of CI Investments Inc.®SunWise is a registered trademark of Sun Life Assurance Company of Canada.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments.Please read the prospectus before investing. Unless otherwise indicated and except for returns for periods less than oneyear, the indicated rates of return are the historical annual compounded total returns including changes in security value.All performance data assume reinvestment of all distributions or dividends and do not take into account sales,redemption, distribution or optional charges or income taxes payable by any securityholder that would have reducedreturns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Sun Life Assurance Company of Canada, a member of the Sun Life Financial group of companies, is the sole issuer of theindividual variable annuity contract providing for investment in Clarica and SunWise segregated funds. A description ofthe key features of the applicable individual variable annuity contract is contained in the information folder. SUBJECTTO ANY APPLICABLE DEATH AND MATURITY GUARANTEES, ANY PART OF THE PREMIUM OROTHER AMOUNT THAT IS ALLOCATED TO A SEGREGATED FUND IS INVESTED AT THE RISK OFTHE CONTRACTHOLDER AND MAY INCREASE OR DECREASE IN VALUE ACCORDING TOFLUCTUATIONS IN THE MARKET VALUE OF THE ASSETS OF THE RELEVANT SEGREGATEDFUND.

disclaimers

03659 (03/10)