Maturing Shared Services Through Use Of Metrics And Benchmarks · Maturing Shared Services Through...

21

Maturing Shared Services Through Use Of Metrics And Benchmarks Maturing Shared Services Through Use Of Metrics And Benchmarks Lisa Miller VP, Controller PepsiCo Financial Shared Services Guido Sterk Director Shared Services Advisory, PwC Lisa Miller VP, Controller PepsiCo Financial Shared Services

-

Upload

nguyendang -

Category

Documents

-

view

234 -

download

1

Transcript of Maturing Shared Services Through Use Of Metrics And Benchmarks · Maturing Shared Services Through...

Maturing Shared Services Through Use Of Metrics And Benchmarks

Maturing Shared Services Through Use Of Metrics And Benchmarks

Lisa Miller VP, Controller PepsiCo Financial Shared Services

Guido SterkDirector

Shared Services Advisory, PwC

Lisa Miller VP, Controller PepsiCo Financial Shared Services

AgendaAgenda

Shared Services Trends Who is PepsiCo?PepsiCo’s Shared Services LandscapePepsiCo Financial Shared Services Journey

Formation and EvolutionBenchmarking Key MetricsFast Facts and Focus

Global Data BaseliningWhat’s Ahead

Shared Services Trends Who is PepsiCo?PepsiCo’s Shared Services LandscapePepsiCo Financial Shared Services Journey

Formation and EvolutionBenchmarking Key MetricsFast Facts and Focus

Global Data BaseliningWhat’s Ahead

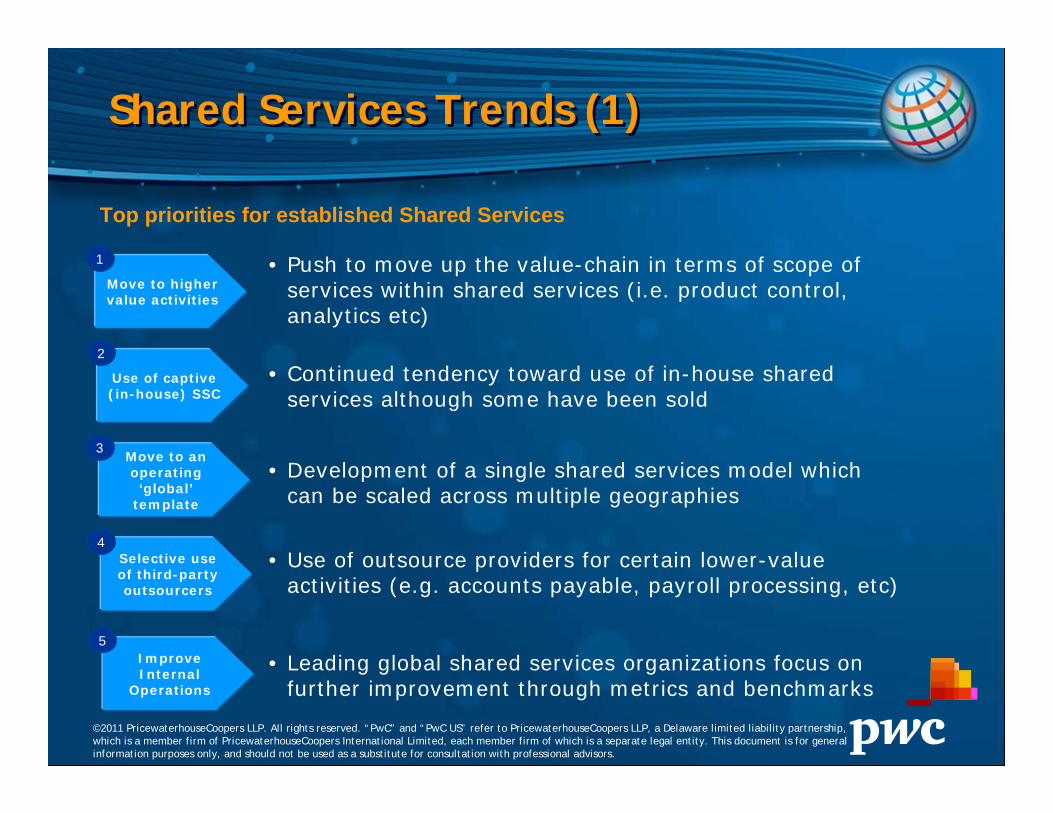

Shared Services Trends (1)Shared Services Trends (1)

Move to higher value activities

Use of captive (in-house) SSC

Move to an operating ‘global’

template

Selective use of third-party outsourcers

Improve Internal

Operations

• Push to move up the value-chain in terms of scope of services within shared services (i.e. product control, analytics etc)

• Continued tendency toward use of in-house shared services although some have been sold

• Development of a single shared services model which can be scaled across multiple geographies

• Use of outsource providers for certain lower-value activities (e.g. accounts payable, payroll processing, etc)

• Leading global shared services organizations focus on further improvement through metrics and benchmarks

1

2

3

4

5

Top priorities for established Shared Services

©2011 PricewaterhouseCoopers LLP. All rights reserved. “PwC” and “PwC US” refer to PricewaterhouseCoopers LLP, a Delaware limited liability partnership, which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity. This document is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

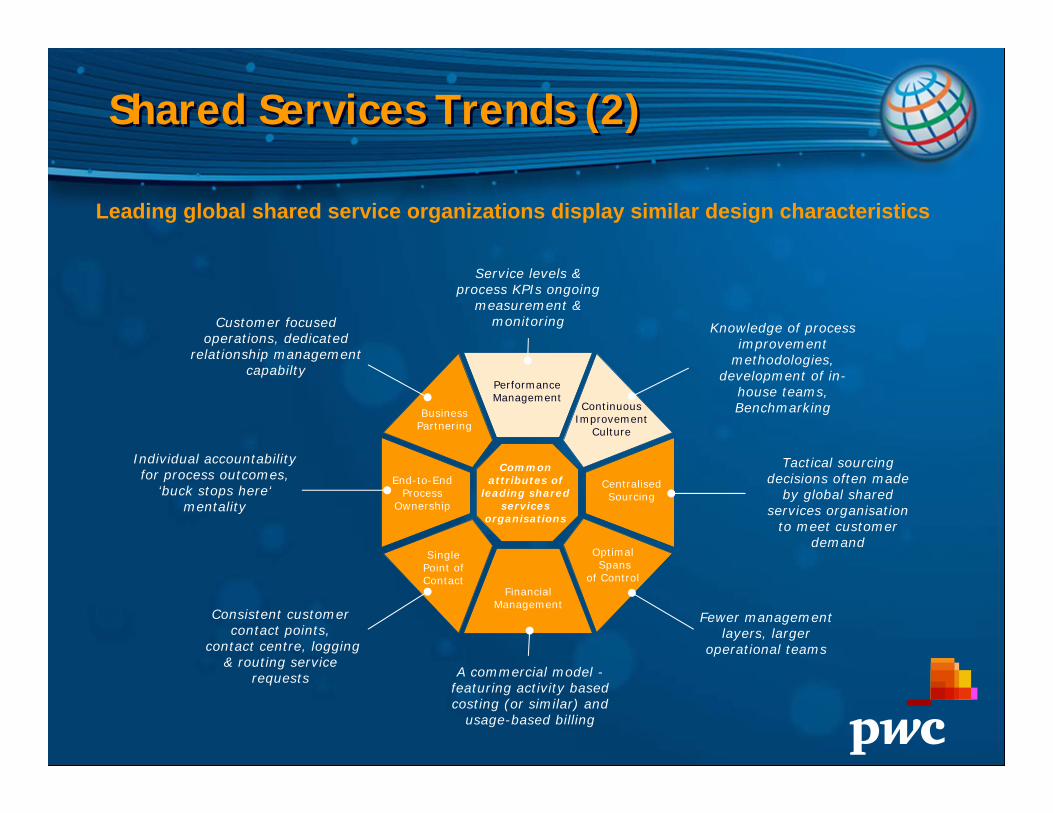

Shared Services Trends (2)Shared Services Trends (2)

Leading global shared service organizations display similar design characteristics

Customer focused operations, dedicated

relationship management capabilty

Individual accountability for process outcomes,

‘buck stops here‘mentality

Consistent customer contact points,

contact centre, logging & routing service

requests

Knowledge of process improvement

methodologies, development of in-

house teams,Benchmarking

A commercial model -featuring activity based costing (or similar) and

usage-based billing

Service levels & process KPIs ongoing

measurement & monitoring

Tactical sourcing decisions often made

by global shared services organisation

to meet customer demand

Fewer management layers, larger

operational teams

Common attributes of

leading shared services

organisations

OptimalSpans

of ControlFinancial

Management

Centralised Sourcing

End-to-End Process

Ownership

Single Point of Contact

Performance Management

Business Partnering

Continuous Improvement

Culture

PepsiCo – Who Are We?PepsiCo – Who Are We?

• Merger of PepsiCo, Pepsi Bottling Group (PBG), and Pepsi Americas (PAS) completed onMarch 1, 2010

• PepsiCo is now the #1 Food and Beverage Company in North America, and the world’s #2 Food and Beverage Company spanning 200 countries

• We have 285,000 employees around the globe, with more than 115,000 people in the United States alone

• Our revenues are nearly $60 Billion – with division operating profit of $8 Billion

• We have more than 200 great brands including 19 exceeding $1B+

• We have a company wide focus on Performance With Purpose – a commitment to deliveringsustainable growth by investing in a healthier future for people and our planet

• Merger of PepsiCo, Pepsi Bottling Group (PBG), and Pepsi Americas (PAS) completed onMarch 1, 2010

• PepsiCo is now the #1 Food and Beverage Company in North America, and the world’s #2 Food and Beverage Company spanning 200 countries

• We have 285,000 employees around the globe, with more than 115,000 people in the United States alone

• Our revenues are nearly $60 Billion – with division operating profit of $8 Billion

• We have more than 200 great brands including 19 exceeding $1B+

• We have a company wide focus on Performance With Purpose – a commitment to deliveringsustainable growth by investing in a healthier future for people and our planet

PepsiCo – Who Are We?PepsiCo – Who Are We?

PepsiCo Shared Services Landscape

Plano, TXShared Services: AP, AR, GA, FR, Payroll, Other

Cork, IrelandShared Services: AP, AR, GA, FR, Other

IndiaPart outsourced

ChinaShared Services:AP, T&E, AR, GA, FR, Other

Winston Salem, NCShared Services:AR, Payroll, Pricing

EgyptShared Services: AP, T&E, FA, GA, TreasuryMexico

Shared Services: AP, AR, GA, FR, Payroll, Tax, Treasury, Other

BrazilShared Services:AP, AR, Tax

RussiaIn processSomers, NY

Shared Services: CDA, Pricing & Promotion,

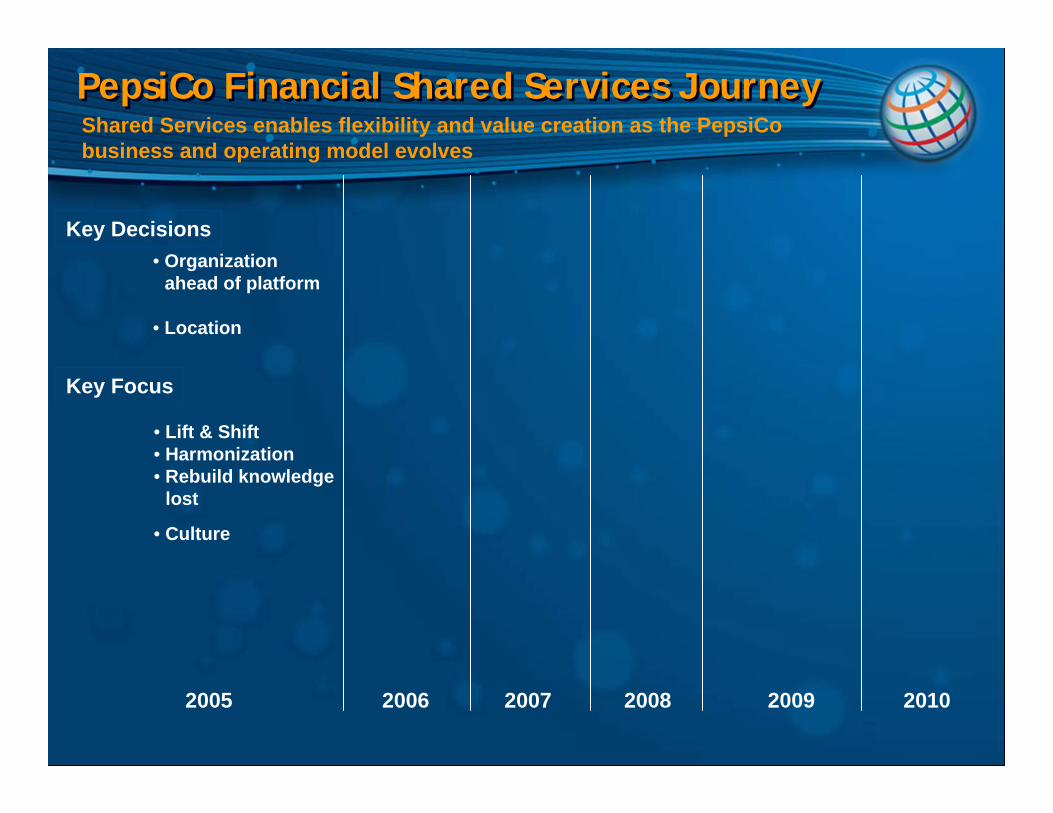

PepsiCo Financial Shared Services JourneyPepsiCo Financial Shared Services Journey

Key Decisions• Organization

ahead of platform

• Location

2005 2006 2007 2008 2009 2010

Key Focus

• Lift & Shift• Harmonization• Rebuild knowledge

lost

• Culture

Shared Services enables flexibility and value creation as the PepsiCobusiness and operating model evolves

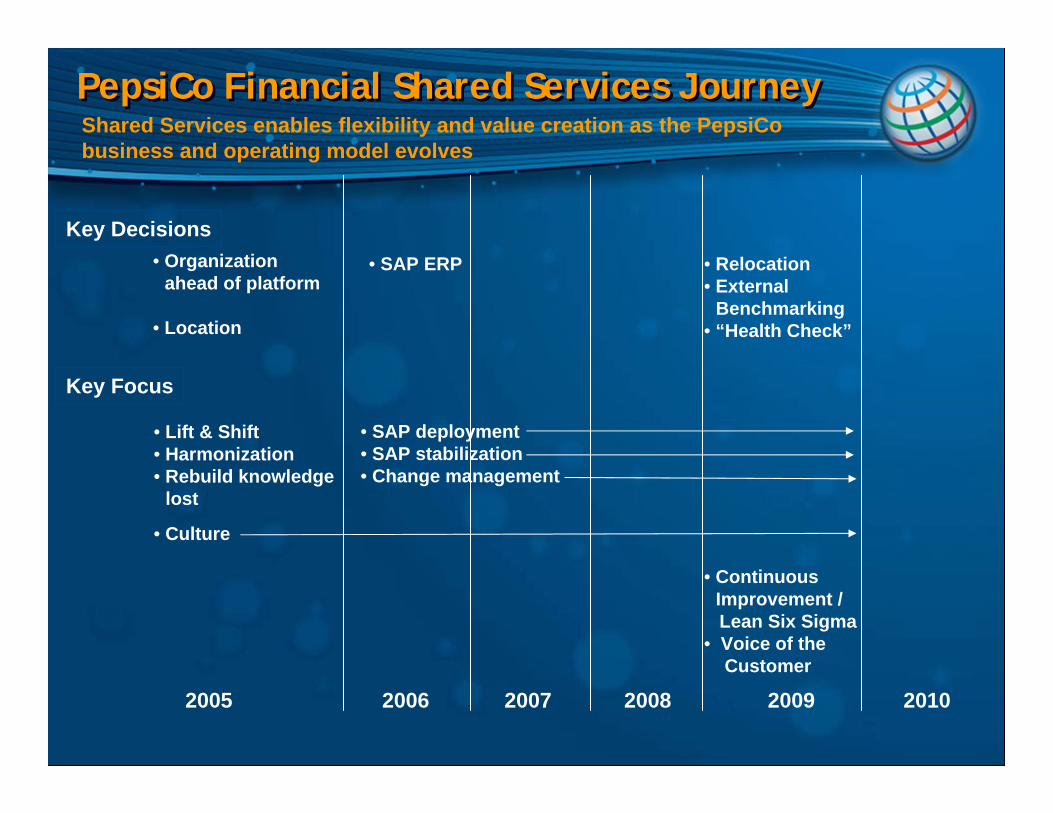

PepsiCo Financial Shared Services JourneyPepsiCo Financial Shared Services Journey

Key Decisions• Organization

ahead of platform

• Location

2005 2006 2007 2008 2009 2010

• SAP ERP • Relocation• External

Benchmarking• “Health Check”

Key Focus

• Lift & Shift• Harmonization• Rebuild knowledge

lost

• Culture

• SAP deployment• SAP stabilization• Change management

• ContinuousImprovement / Lean Six Sigma

• Voice of theCustomer

Shared Services enables flexibility and value creation as the PepsiCobusiness and operating model evolves

PepsiCo Financial Shared Services JourneyPepsiCo Financial Shared Services Journey

Key Decisions• Organization

ahead of platform

• Location

2005 2006 2007 2008 2009 2010

• SAP ERP • Relocation• External

Benchmarking• “Health Check”

• Oracle forFrito-Lay

Key Focus

• Lift & Shift• Harmonization• Rebuild knowledge

lost• Culture /

Grow our People

• SAP deployment• SAP stabilization• Change management

• SAP Optimization

• ContinuousImprovement / Lean Six Sigma

• Voice of theCustomer

• Metrics / workdrivers

• Baselineexcellence

• Vision / strategy

Shared Services enables flexibility and value creation as the PepsiCobusiness and operating model evolves

Vision And Operating Principles

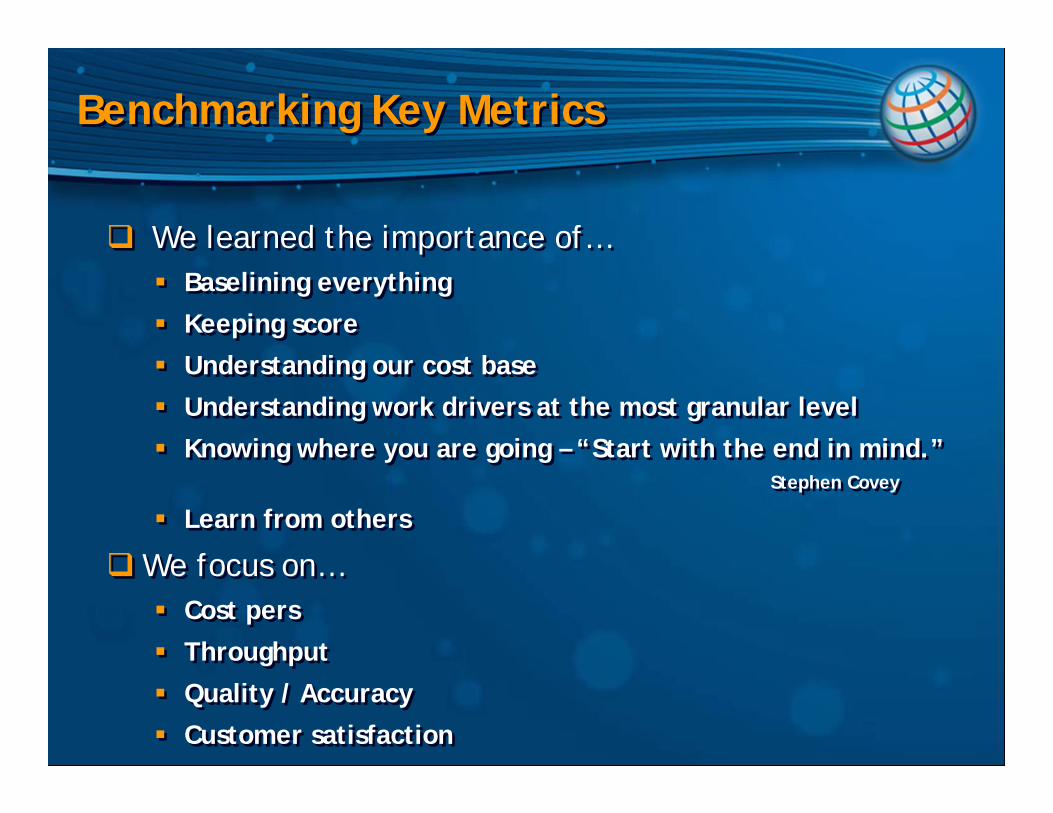

Benchmarking Key MetricsBenchmarking Key Metrics

We learned the importance of…Baselining everything

Keeping score

Understanding our cost baseUnderstanding work drivers at the most granular level

Knowing where you are going – “Start with the end in mind.”Stephen Covey

Learn from others

We focus on…Cost pers

Throughput

Quality / Accuracy

Customer satisfaction

We learned the importance of…Baselining everything

Keeping score

Understanding our cost baseUnderstanding work drivers at the most granular level

Knowing where you are going – “Start with the end in mind.”Stephen Covey

Learn from others

We focus on…Cost pers

Throughput

Quality / Accuracy

Customer satisfaction

Performance MeasurementPerformance Measurement

What gets measured gets done, what gets measured and fed back gets done well, what gets rewarded gets repeated - John E. Jones

What gets measured gets done, what gets measured and fed back gets done well, what gets rewarded gets repeated - John E. Jones

ScorecardsSLA Metrics

Surveys

Reports & Analytics

Rankings &Watch Lists

Frameworks& Models

Publications

Benchmarking

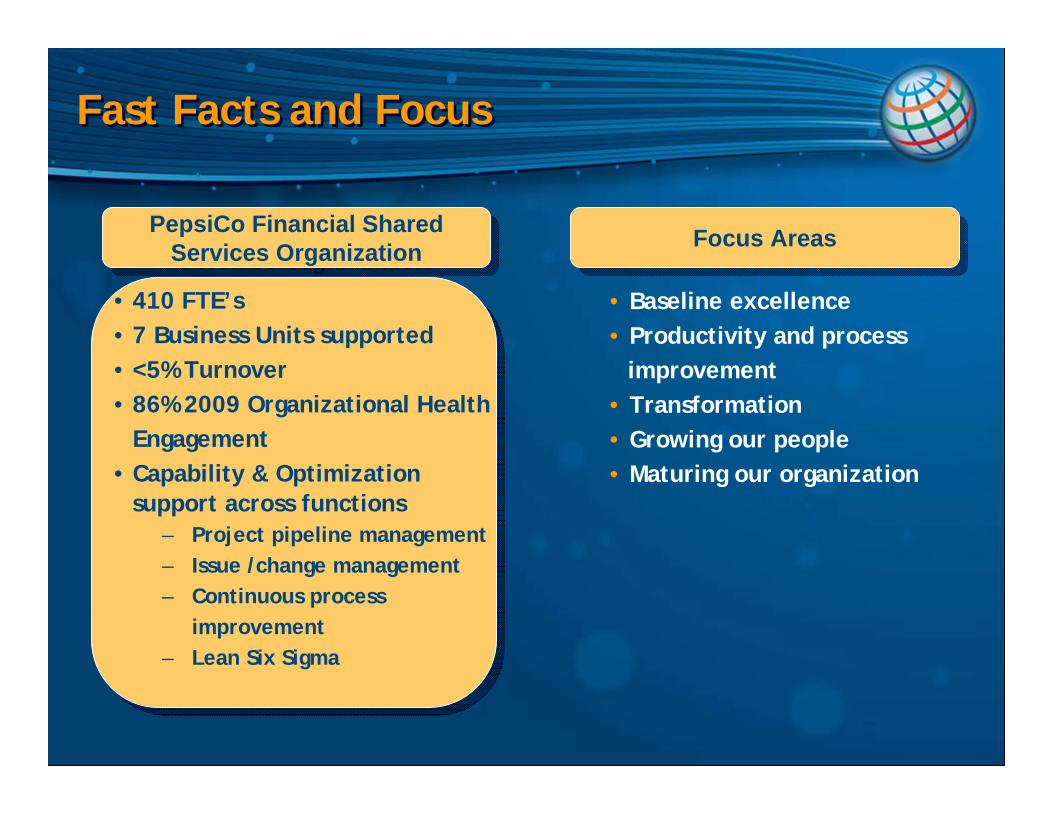

Fast Facts and FocusFast Facts and Focus

• 410 FTE’s• 7 Business Units supported• <5% Turnover• 86% 2009 Organizational Health

Engagement• Capability & Optimization

support across functions– Project pipeline management– Issue /change management– Continuous process

improvement– Lean Six Sigma

PepsiCo Financial SharedServices Organization

PepsiCo Financial SharedServices Organization

• Baseline excellence• Productivity and process

improvement• Transformation• Growing our people• Maturing our organization

Focus AreasFocus Areas

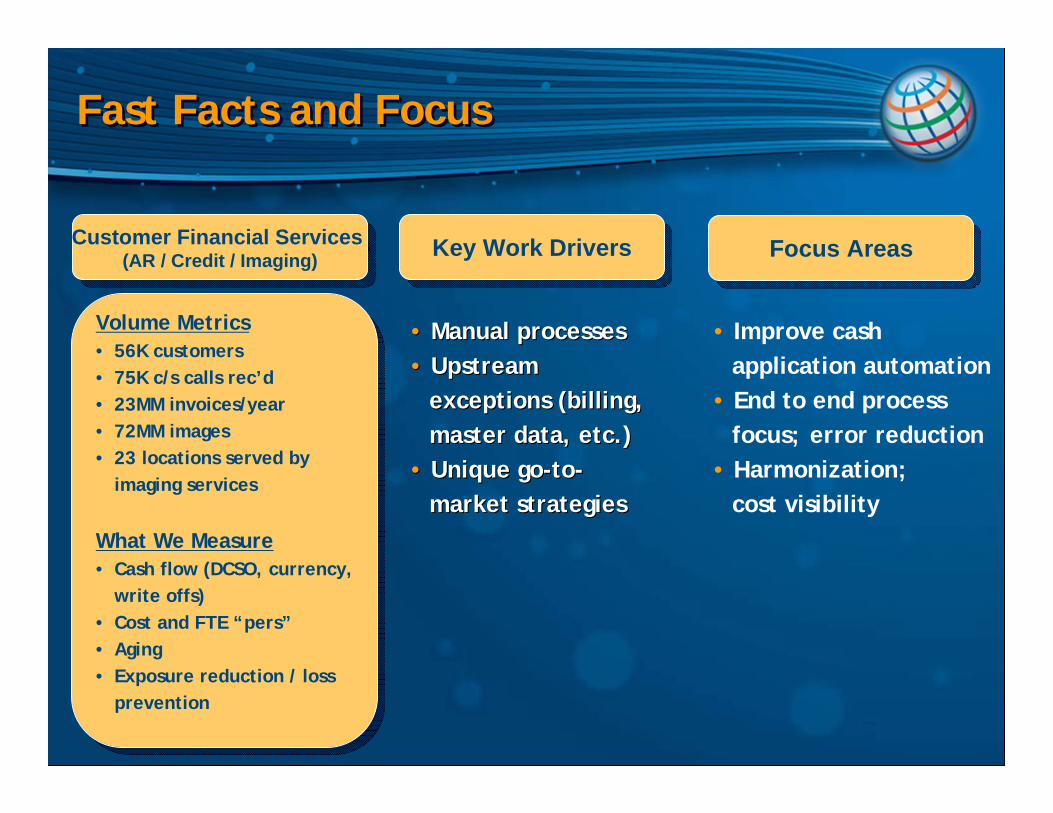

Volume Metrics• 56K customers• 75K c/s calls rec’d• 23MM invoices/year• 72MM images• 23 locations served by

imaging services

What We Measure• Cash flow (DCSO, currency,

write offs)• Cost and FTE “pers”• Aging• Exposure reduction / loss

prevention

Volume Metrics• 56K customers• 75K c/s calls rec’d• 23MM invoices/year• 72MM images• 23 locations served by

imaging services

What We Measure• Cash flow (DCSO, currency,

write offs)• Cost and FTE “pers”• Aging• Exposure reduction / loss

prevention

Fast Facts and FocusFast Facts and Focus

Customer Financial Services (AR / Credit / Imaging)

Customer Financial Services (AR / Credit / Imaging)

• Improve cash application automation

• End to end process focus; error reduction

• Harmonization; cost visibility

•• Manual processesManual processes•• Upstream Upstream

exceptions (billing, exceptions (billing, master data, etc.)master data, etc.)

•• Unique goUnique go--toto--market strategiesmarket strategies

Key Work DriversKey Work Drivers Focus AreasFocus Areas

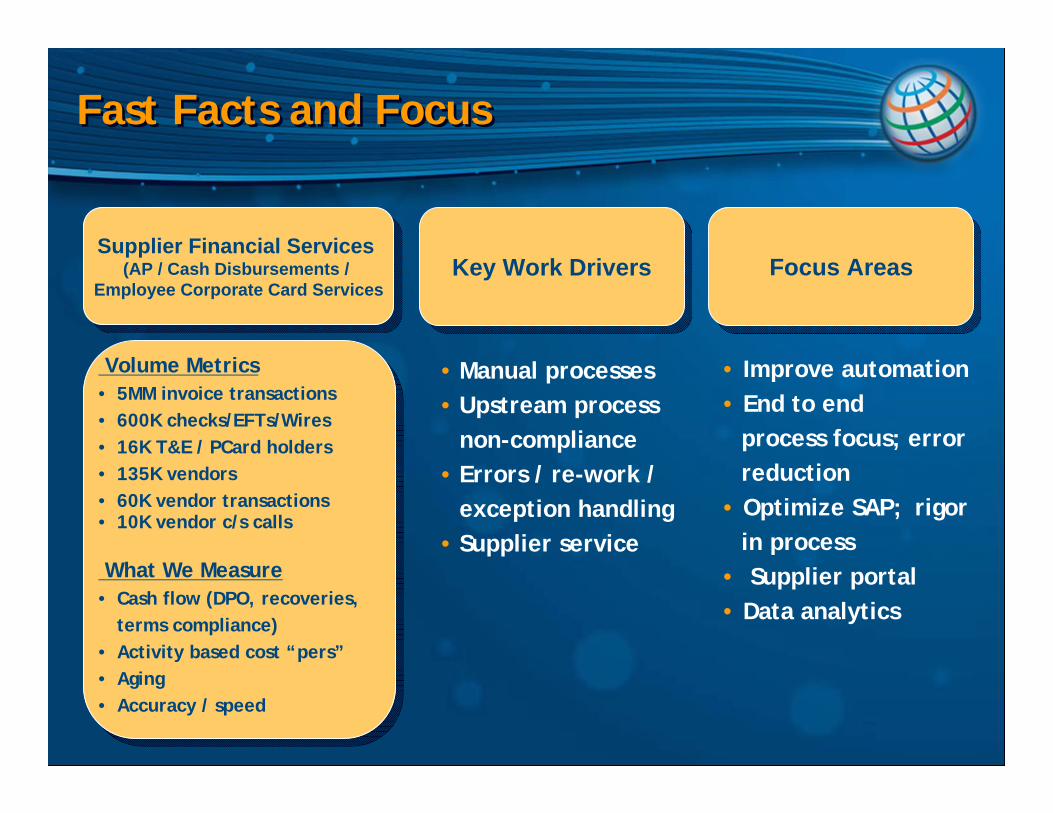

Fast Facts and FocusFast Facts and Focus

Supplier Financial Services (AP / Cash Disbursements /

Employee Corporate Card Services

Supplier Financial Services (AP / Cash Disbursements /

Employee Corporate Card Services

Volume Metrics• 5MM invoice transactions• 600K checks/EFTs/Wires• 16K T&E / PCard holders• 135K vendors• 60K vendor transactions• 10K vendor c/s calls

What We Measure• Cash flow (DPO, recoveries,

terms compliance)• Activity based cost “pers”• Aging• Accuracy / speed

• Improve automation• End to end

process focus; error reduction

• Optimize SAP; rigor in process

• Supplier portal• Data analytics

• Manual processes• Upstream process

non-compliance• Errors / re-work /

exception handling• Supplier service

Key Work DriversKey Work Drivers Focus AreasFocus Areas

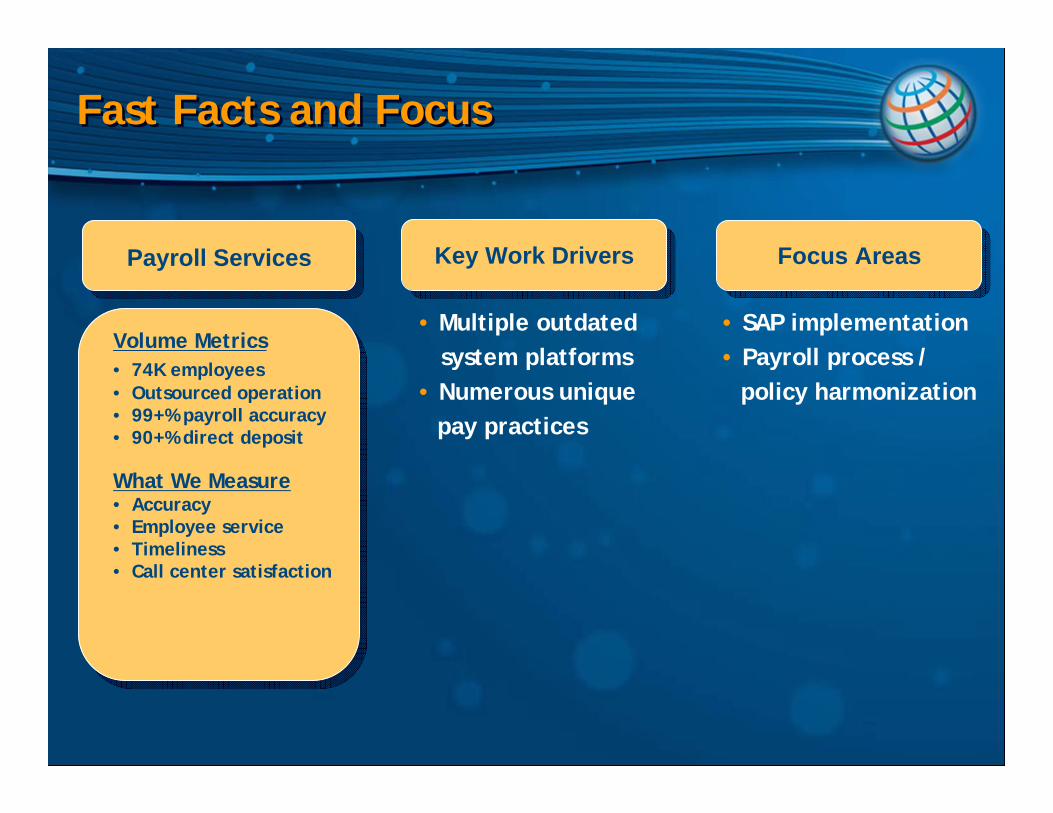

Fast Facts and FocusFast Facts and Focus

Payroll ServicesPayroll Services

Volume Metrics• 74K employees• Outsourced operation• 99+% payroll accuracy• 90+% direct deposit

What We Measure• Accuracy• Employee service• Timeliness• Call center satisfaction

• Multiple outdatedsystem platforms

• Numerous unique pay practices

• SAP implementation• Payroll process /

policy harmonization

Key Work DriversKey Work Drivers Focus AreasFocus Areas

Fast Facts and FocusFast Facts and Focus

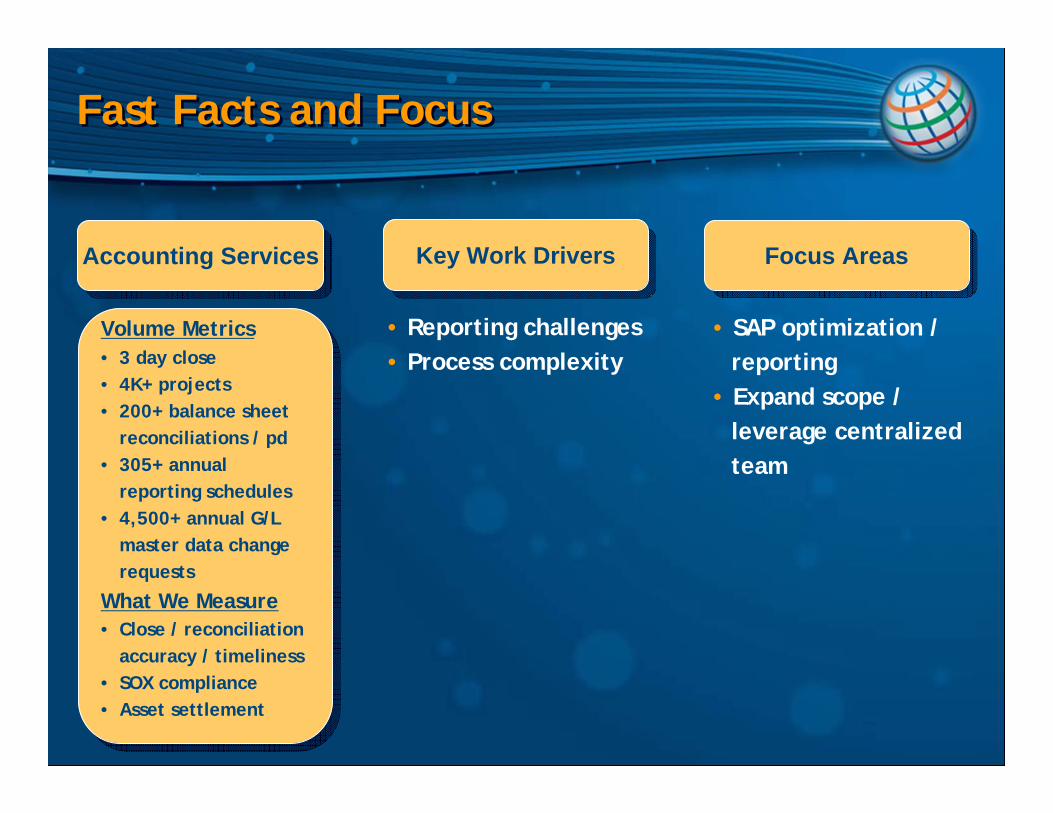

Accounting ServicesAccounting Services

Volume Metrics• 3 day close• 4K+ projects• 200+ balance sheet

reconciliations / pd• 305+ annual

reporting schedules • 4,500+ annual G/L

master data change requests

What We Measure• Close / reconciliation

accuracy / timeliness• SOX compliance• Asset settlement

• Reporting challenges• Process complexity

• SAP optimization / reporting

• Expand scope / leverage centralized team

Key Work DriversKey Work Drivers Focus AreasFocus Areas

Global Data BaseliningGlobal Data Baselining

A key step in our journey in 2010 was engaging PwC to perform a global data baselining assessment

Objectives: Gather financial and headcount information Understand the cost structure for financial processesUltimately further improving productivity, providing ongoing flexibility, and better leveraging PepsiCo’s investments in SAP

Process:Information gathering via 163 unique global data submissions Across 17 unique finance process areas

Outcomes:“As is” baseline of Control function FTE effort and costs acrossAmericas, Europe and AMEA Identification of areas for further investigation and means tofurther leverage shared services at PepsiCo

A key step in our journey in 2010 was engaging PwC to perform a global data baselining assessment

Objectives: Gather financial and headcount information Understand the cost structure for financial processesUltimately further improving productivity, providing ongoing flexibility, and better leveraging PepsiCo’s investments in SAP

Process:Information gathering via 163 unique global data submissions Across 17 unique finance process areas

Outcomes:“As is” baseline of Control function FTE effort and costs acrossAmericas, Europe and AMEA Identification of areas for further investigation and means tofurther leverage shared services at PepsiCo

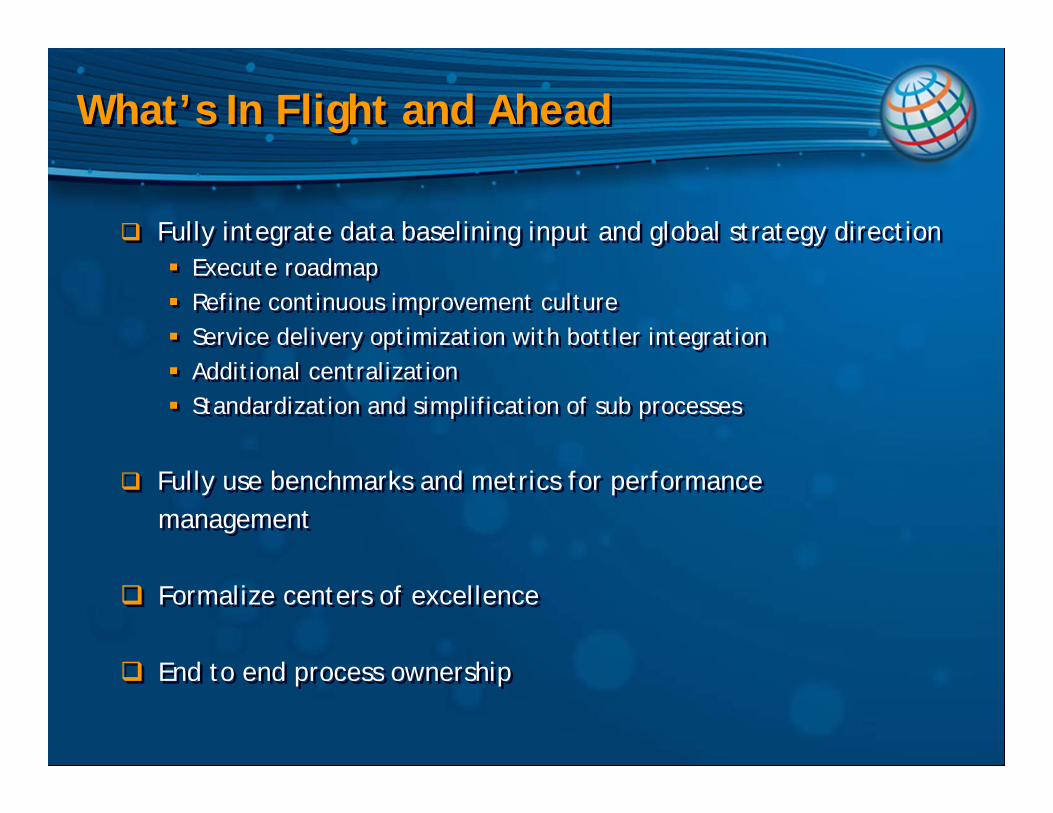

What’s In Flight and AheadWhat’s In Flight and Ahead

Fully integrate data baselining input and global strategy direction Execute roadmapRefine continuous improvement cultureService delivery optimization with bottler integrationAdditional centralizationStandardization and simplification of sub processes

Fully use benchmarks and metrics for performancemanagement

Formalize centers of excellence

End to end process ownership

Fully integrate data baselining input and global strategy direction Execute roadmapRefine continuous improvement cultureService delivery optimization with bottler integrationAdditional centralizationStandardization and simplification of sub processes

Fully use benchmarks and metrics for performancemanagement

Formalize centers of excellence

End to end process ownership

Today

Questions?