MATTERS” herein. $111,545,000 TAXABLE PENSION OBLIGATION ...

332

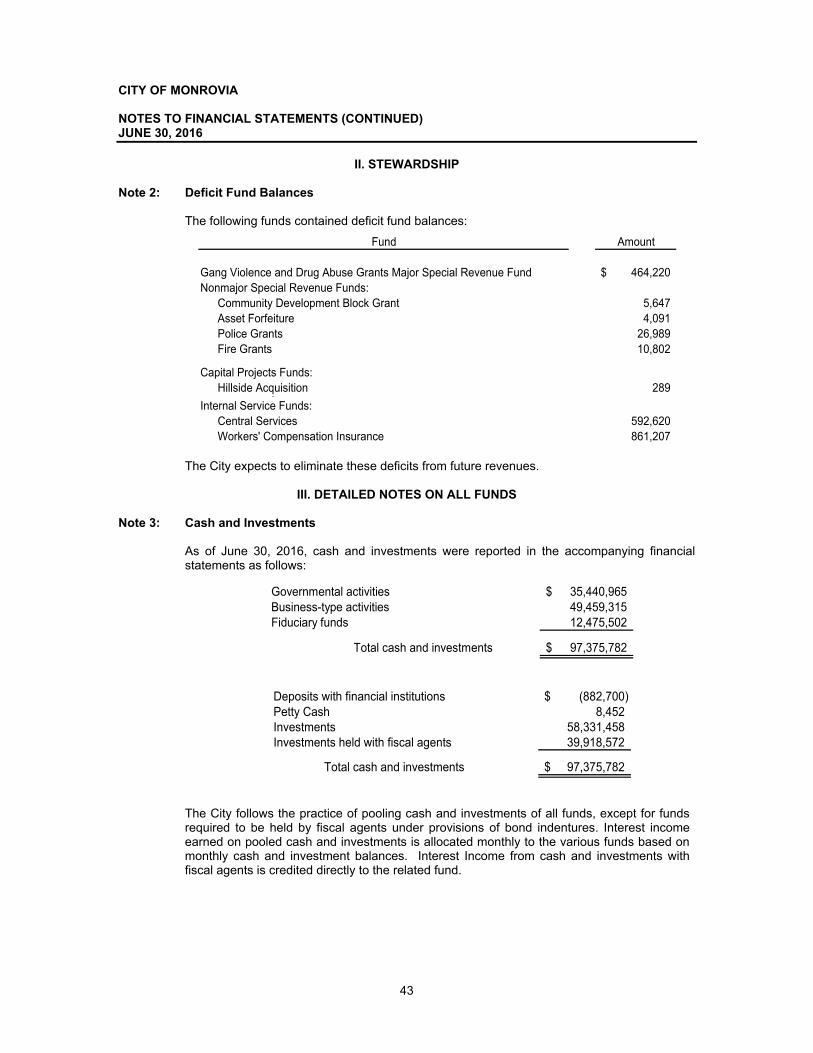

NEW ISSUE - BOOK-ENTRY ONLY Rating: S&P: “AA-” See the caption “CONCLUDING INFORMATION—Rating.” In the opinion of Richards, Watson & Gershon, A Professional Corporation, Bond Counsel, under existing law interest on the Bonds is exempt from State of California personal income taxes. INTEREST ON THE BONDS IS NOT EXCLUDED FROM GROSS INCOME FOR FEDERAL INCOME TAX PURPOSES. Bond Counsel expresses no opinion as to any other tax consequences regarding the Bonds. For a more complete discussion of the tax aspects, see “TAX MATTERS” herein. $111,545,000 CITY OF MONROVIA TAXABLE PENSION OBLIGATION BONDS SERIES 2017 Dated: Delivery Date Due: May 1, as shown on the inside front cover page The above-captioned bonds (the “Bonds”) will be issued in fully registered form registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York (“DTC”). The Bonds will be available to the ultimate purchasers (“Beneficial Owners”) in denominations of $5,000 or any integral multiple thereof pursuant to a Trust Agreement dated as of June 1, 2010 (the “Master Trust Agreement”) by and between the City of Monrovia (the “City”) and U.S. Bank National Association, as trustee (the “Trustee”), as supplemented by the First Supplemental Trust Agreement, dated as of December 1, 2017 (the “First Supplement,” and together with the Master Trust Agreement, the “Trust Agreement”). The Bonds are payable at the corporate trust office of the Trustee in Los Angeles, California or such other location as designated by the Trustee. Interest on the Bonds is payable semiannually on May 1 and November 1 in each year, commencing on May 1, 2018 (each, an “Interest Payment Date”), by check mailed by first class mail on the Interest Payment Date to the registered owner thereof as of the Record Date established for the Bonds or, at the option of any Owner of at least $1,000,000 in principal amount of Bonds, by wire transfer if such Owner will provide the Trustee written wire transfer instructions at least fifteen (15) days prior to the applicable Record Date. Capitalized terms not otherwise defined herein will have the meanings set forth in APPENDIX B—“SUMMARY OF THE TRUST AGREEMENT” herein and in the Trust Agreement. The Bonds are subject to optional and mandatory term bond redemption prior to their maturity under certain conditions as described herein. See “THE BONDS” herein. The Bonds are being issued to (i) refund in full the City of Monrovia Taxable Pension Obligation Bonds, Series 2010 (the “2010 Bonds”) currently outstanding in the principal amount of $10,970,000, (ii) fund the City’s unfunded accrued actuarial liability to the California Public Employees’ Retirement System (“CalPERS”) for the benefit of the City’s employees in an amount equal to $98,291,138, and (iii) pay certain costs of issuance in association therewith. The Bonds are special obligations of the City payable primarily from and secured by the Revenue Fund and the Retirement Tax Revenues deposited therein pursuant to the Trust Agreement. To the extent that such Retirement Tax Revenues are not available to make payments with respect to the Bonds, the obligation of the City to make payments is a general fund obligation of the City. This cover page of the Official Statement contains information for quick reference only. It is not a complete summary of the Bonds. Investors should read the entire Official Statement to obtain information essential to the making of an informed investment decision. Attention is hereby directed to certain risk factors more fully described under the caption “RISK FACTORS” herein. THE BONDS ARE SPECIAL OBLIGATIONS OF THE CITY PAYABLE PRIMARILY FROM AND SECURED BY THE REVENUE FUND AND THE RETIREMENT TAX REVENUES AND GENERAL FUND REVENUES DEPOSITED THEREIN PURSUANT TO THE TRUST AGREEMENT. NEITHER THE BONDS NOR THE OBLIGATION OF THE CITY TO MAKE PAYMENTS WITH RESPECT TO THE BONDS CONSTITUTES AN INDEBTEDNESS OF THE CITY, THE STATE OR ANY OF ITS POLITICAL SUBDIVISIONS IN CONTRAVENTION OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION. The Bonds are offered, when, as and if issued, subject to the approval of Richards, Watson & Gershon, A Professional Corporation, Los Angeles, California, Bond Counsel. In addition, certain legal matters will be passed on for the City by Stradling Yocca Carlson & Rauth, a Professional Corporation, Newport Beach, California, as Disclosure Counsel, for the Underwriter by its counsel, Nixon Peabody LLP, Los Angeles, California, and for the Trustee by its counsel, Dorsey & Whitney LLP, Costa Mesa, California. It is anticipated that the Bonds will be available for delivery through the facilities of DTC on or about December 13, 2017. Dated: November 30, 2017.

Transcript of MATTERS” herein. $111,545,000 TAXABLE PENSION OBLIGATION ...

NEW ISSUE - BOOK-ENTRY ONLY Rating: S&P: “AA-” See the caption “CONCLUDING INFORMATION—Rating.”

In the opinion of Richards, Watson & Gershon, A Professional Corporation, Bond Counsel, under existing law

interest on the Bonds is exempt from State of California personal income taxes. INTEREST ON THE BONDS IS NOT

EXCLUDED FROM GROSS INCOME FOR FEDERAL INCOME TAX PURPOSES. Bond Counsel expresses no opinion

as to any other tax consequences regarding the Bonds. For a more complete discussion of the tax aspects, see “TAX

MATTERS” herein.

$111,545,000 CITY OF MONROVIA

TAXABLE PENSION OBLIGATION BONDS SERIES 2017

Dated: Delivery Date Due: May 1, as shown on the inside front cover page The above-captioned bonds (the “Bonds”) will be issued in fully registered form registered in the name of Cede &

Co. as nominee of The Depository Trust Company, New York, New York (“DTC”). The Bonds will be available to the ultimate purchasers (“Beneficial Owners”) in denominations of $5,000 or any integral multiple thereof pursuant to a Trust Agreement dated as of June 1, 2010 (the “Master Trust Agreement”) by and between the City of Monrovia (the “City”) and U.S. Bank National Association, as trustee (the “Trustee”), as supplemented by the First Supplemental Trust Agreement, dated as of December 1, 2017 (the “First Supplement,” and together with the Master Trust Agreement, the “Trust Agreement”). The Bonds are payable at the corporate trust office of the Trustee in Los Angeles, California or such other location as designated by the Trustee. Interest on the Bonds is payable semiannually on May 1 and November 1 in each year, commencing on May 1, 2018 (each, an “Interest Payment Date”), by check mailed by first class mail on the Interest Payment Date to the registered owner thereof as of the Record Date established for the Bonds or, at the option of any Owner of at least $1,000,000 in principal amount of Bonds, by wire transfer if such Owner will provide the Trustee written wire transfer instructions at least fifteen (15) days prior to the applicable Record Date. Capitalized terms not otherwise defined herein will have the meanings set forth in APPENDIX B—“SUMMARY OF THE TRUST AGREEMENT” herein and in the Trust Agreement.

The Bonds are subject to optional and mandatory term bond redemption prior to their maturity under certain conditions as described herein. See “THE BONDS” herein.

The Bonds are being issued to (i) refund in full the City of Monrovia Taxable Pension Obligation Bonds, Series 2010 (the “2010 Bonds”) currently outstanding in the principal amount of $10,970,000, (ii) fund the City’s unfunded accrued actuarial liability to the California Public Employees’ Retirement System (“CalPERS”) for the benefit of the City’s employees in an amount equal to $98,291,138, and (iii) pay certain costs of issuance in association therewith. The Bonds are special obligations of the City payable primarily from and secured by the Revenue Fund and the Retirement Tax Revenues deposited therein pursuant to the Trust Agreement. To the extent that such Retirement Tax Revenues are not available to make payments with respect to the Bonds, the obligation of the City to make payments is a general fund obligation of the City.

This cover page of the Official Statement contains information for quick reference only. It is not a complete summary of the Bonds. Investors should read the entire Official Statement to obtain information essential to the making of an informed investment decision. Attention is hereby directed to certain risk factors more fully described under the caption “RISK FACTORS” herein.

THE BONDS ARE SPECIAL OBLIGATIONS OF THE CITY PAYABLE PRIMARILY FROM AND SECURED BY THE REVENUE FUND AND THE RETIREMENT TAX REVENUES AND GENERAL FUND REVENUES DEPOSITED THEREIN PURSUANT TO THE TRUST AGREEMENT. NEITHER THE BONDS NOR THE OBLIGATION OF THE CITY TO MAKE PAYMENTS WITH RESPECT TO THE BONDS CONSTITUTES AN INDEBTEDNESS OF THE CITY, THE STATE OR ANY OF ITS POLITICAL SUBDIVISIONS IN CONTRAVENTION OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION.

The Bonds are offered, when, as and if issued, subject to the approval of Richards, Watson & Gershon, A

Professional Corporation, Los Angeles, California, Bond Counsel. In addition, certain legal matters will be passed on for

the City by Stradling Yocca Carlson & Rauth, a Professional Corporation, Newport Beach, California, as Disclosure

Counsel, for the Underwriter by its counsel, Nixon Peabody LLP, Los Angeles, California, and for the Trustee by its

counsel, Dorsey & Whitney LLP, Costa Mesa, California. It is anticipated that the Bonds will be available for delivery

through the facilities of DTC on or about December 13, 2017.

Dated: November 30, 2017.

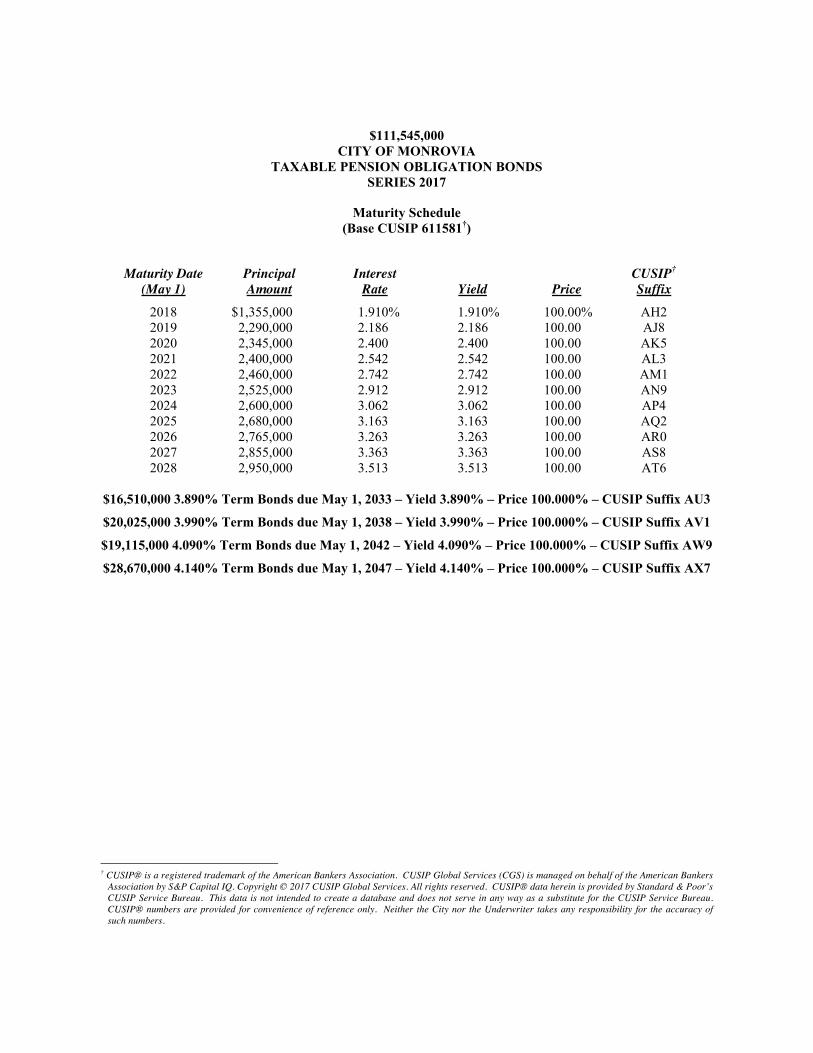

$111,545,000 CITY OF MONROVIA

TAXABLE PENSION OBLIGATION BONDS SERIES 2017

Maturity Schedule

(Base CUSIP 611581†)

Maturity Date (May 1)

Principal Amount

Interest Rate Yield Price

CUSIP† Suffix

2018 $1,355,000 1.910% 1.910% 100.00% AH2 2019 2,290,000 2.186 2.186 100.00 AJ8 2020 2,345,000 2.400 2.400 100.00 AK5 2021 2,400,000 2.542 2.542 100.00 AL3 2022 2,460,000 2.742 2.742 100.00 AM1 2023 2,525,000 2.912 2.912 100.00 AN9 2024 2,600,000 3.062 3.062 100.00 AP4 2025 2,680,000 3.163 3.163 100.00 AQ2 2026 2,765,000 3.263 3.263 100.00 AR0 2027 2,855,000 3.363 3.363 100.00 AS8 2028 2,950,000 3.513 3.513 100.00 AT6

$16,510,000 3.890% Term Bonds due May 1, 2033 – Yield 3.890% – Price 100.000% – CUSIP Suffix AU3 $20,025,000 3.990% Term Bonds due May 1, 2038 – Yield 3.990% – Price 100.000% – CUSIP Suffix AV1 $19,115,000 4.090% Term Bonds due May 1, 2042 – Yield 4.090% – Price 100.000% – CUSIP Suffix AW9 $28,670,000 4.140% Term Bonds due May 1, 2047 – Yield 4.140% – Price 100.000% – CUSIP Suffix AX7

† CUSIP® is a registered trademark of the American Bankers Association. CUSIP Global Services (CGS) is managed on behalf of the American Bankers

Association by S&P Capital IQ. Copyright © 2017 CUSIP Global Services. All rights reserved. CUSIP® data herein is provided by Standard & Poor’s CUSIP Service Bureau. This data is not intended to create a database and does not serve in any way as a substitute for the CUSIP Service Bureau. CUSIP® numbers are provided for convenience of reference only. Neither the City nor the Underwriter takes any responsibility for the accuracy of such numbers.

CITY OF MONROVIA COUNTY OF LOS ANGELES, CALIFORNIA

CITY COUNCIL

Tom Adams, Mayor Gloria Crudgington, Mayor Pro-Tem

Larry J. Spicer, Councilmember Alexander C. Blackburn, Councilmember

Becky A. Shevlin, Councilmember

CITY STAFF

Oliver Chi, City Manager Buffy J. Bullis, Administrative Services Director

Craig Steele, City Attorney Alice D. Atkins, City Clerk

Stephen R. Baker, City Treasurer

SPECIAL SERVICES

Bond Counsel Richards, Watson & Gershon A Professional Corporation

Los Angeles, California

Disclosure Counsel Stradling Yocca Carlson & Rauth,

A Professional Corporation Newport Beach, California

Underwriter Hilltop Securities Inc.

Cardiff by the Sea, California

Municipal Advisor Urban Futures, Inc. Tustin, California

Verification Agent Grant Thornton, LLP

Minneapolis, Minnesota

Trustee and Escrow Agent U.S. Bank National Association

Los Angeles, California

No dealer, broker, salesperson or other person has been authorized by the City or the Underwriter to give any information or to make any representations, other than those contained in this Official Statement, and, if given or made, such other information or representations must not be relied upon as having been authorized by the City or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as a representation of facts.

The information set forth herein has been obtained from the City and other sources believed to be reliable, but the accuracy or completeness of such information is not guaranteed by, and should not be construed as a representation by, the Underwriter. This Official Statement has been deemed final, as of its date, by the City for the purpose of Rule 15c2-12 under the Securities Exchange Act of 1934, as amended. The information and expressions of opinions herein are subject to change without notice and neither delivery of the Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the City since the date hereof. All summaries contained herein of the Trust Agreement or other documents are made subject to the provisions of such documents and do not purport to be complete statements of any or all of such provisions. All statements made herein are made as of the date of this document by the City, except statistical information or other statements where some other date is indicated in the text.

The Underwriter has provided the following sentence for inclusion in this Official Statement. The Underwriter has reviewed the information in this Official Statement in accordance with its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information.

The Bonds are exempt from registration with the Securities and Exchange Commission pursuant to the Securities Act of 1933, as amended. The Bonds have not been registered or qualified under the securities laws of any state. The Bonds will not be listed on any stock or securities exchange. Neither the Securities and Exchange Commission nor any other federal, state or other governmental entity or agency will have passed upon the accuracy or adequacy of the Official Statement or approved the Bonds for sale.

IN CONNECTION WITH THIS OFFERING, THE UNDERWRITER MAY OVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL ON THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE UNDERWRITER MAY OFFER AND SELL THE BONDS TO CERTAIN DEALERS AND DEALER BANKS AND BANKS ACTING AS AGENT AND OTHERS AT PRICES LOWER THAN THE PUBLIC OFFERING PRICES STATED ON THE INSIDE FRONT COVER PAGE HEREOF AND SUCH PUBLIC OFFERING PRICES MAY BE CHANGED FROM TIME TO TIME BY THE UNDERWRITER.

Certain statements included or incorporated by reference in this Official Statement constitute “forward-looking statements.” Such statements are generally identifiable by the terminology used such as “plan,” “expect,” “estimate,” “budget,” or other similar words. The achievement of certain results or other expectations contained in such forward-looking statements involves known and unknown risks, uncertainties and other factors which may cause actual results, performance or achievements described to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. While the City has agreed to provide certain on-going financial and other data for a limited period of time (see “CONCLUDING INFORMATION—Continuing Disclosure”), the City does not plan to issue any updates or revisions to those forward-looking statements if or when the expectations or events, conditions or circumstances on which such statements are based change.

TABLE OF CONTENTS

Page

i

INTRODUCTION ................................................................................................................................................ 1 General .............................................................................................................................................................. 1

THE BONDS ........................................................................................................................................................ 3 General .............................................................................................................................................................. 3 The Bonds ......................................................................................................................................................... 3 Optional Redemption of the Bonds .................................................................................................................. 3 Mandatory Sinking Fund Account Redemption of the Bonds .......................................................................... 4 Notice of Redemption ....................................................................................................................................... 5 Selection of Bonds for Redemption .................................................................................................................. 5 Book-Entry Only System .................................................................................................................................. 5

PLAN OF REFINANCING .................................................................................................................................. 6

SOURCES AND USES OF PROCEEDS ............................................................................................................. 7

SECURITY AND SOURCE OF PAYMENT FOR THE BONDS ...................................................................... 8 Bond Payments ................................................................................................................................................. 8 Limited Obligations .......................................................................................................................................... 9

SCHEDULE OF ANNUAL DEBT SERVICE PAYMENTS ............................................................................ 11

THE CITY .......................................................................................................................................................... 12 General ............................................................................................................................................................ 12 Budgetary Process and Administration ........................................................................................................... 12 Revenue and Expenditure Trends ................................................................................................................... 12 Debt Administration ....................................................................................................................................... 22 Cash Management .......................................................................................................................................... 23 Property Taxes ................................................................................................................................................ 23 Sales Taxes ..................................................................................................................................................... 27 The Retirement Tax ........................................................................................................................................ 27 Other Taxes ..................................................................................................................................................... 31 Services ........................................................................................................................................................... 31 Risk Management ........................................................................................................................................... 31 Retirement Contributions ................................................................................................................................ 31 Labor Status .................................................................................................................................................... 41

STATE OF CALIFORNIA BUDGET INFORMATION ................................................................................... 41 State Budget .................................................................................................................................................... 41 Potential Impact of State Financial Condition on the City ............................................................................. 43 Future State Budgets ....................................................................................................................................... 43

RISK FACTORS ................................................................................................................................................ 43 Future Financial Condition ............................................................................................................................. 43 Limited Obligation of the City ........................................................................................................................ 43 Possible Dilution of Retirement Tax Revenues .............................................................................................. 44 Additional General Fund Obligations of the City ........................................................................................... 44 Natural Disasters ............................................................................................................................................. 44 Hazardous Substances .................................................................................................................................... 45 Bankruptcy of the City .................................................................................................................................... 45 Legislative Changes ........................................................................................................................................ 46 Constitutional Limitation on Taxes and Expenditures .................................................................................... 46 Proposition 62 ................................................................................................................................................. 47 Proposition 218 ............................................................................................................................................... 48 Proposition 26 ................................................................................................................................................. 49 Future Initiatives ............................................................................................................................................. 49

TABLE OF CONTENTS (continued)

Page

ii

Loss of State Tax Exemption .......................................................................................................................... 49 Secondary Market ........................................................................................................................................... 49

TAX MATTERS................................................................................................................................................. 50 Non-U.S. Owners ............................................................................................................................................ 51 Foreign Account Tax Compliance Act ........................................................................................................... 51 Form of Bond Counsel Opinion ...................................................................................................................... 52

VALIDATION.................................................................................................................................................... 52

CONCLUDING INFORMATION ..................................................................................................................... 52 Rating .............................................................................................................................................................. 52 Underwriting ................................................................................................................................................... 53 Verification of Mathematical Accuracy .......................................................................................................... 53 Municipal Advisor .......................................................................................................................................... 53 Legal Opinion ................................................................................................................................................. 53 Continuing Disclosure .................................................................................................................................... 54 Absence of Litigation ..................................................................................................................................... 55 Legality for Investment in California ............................................................................................................. 55 Miscellaneous ................................................................................................................................................. 55

APPENDIX A SUPPLEMENTAL INFORMATION OF THE CITY OF MONROVIA ............................. A-1 APPENDIX B SUMMARY OF THE TRUST AGREEMENT..................................................................... B-1 APPENDIX C FORM OF BOND COUNSEL OPINION ............................................................................. C-1 APPENDIX D FORM OF CONTINUING DISCLOSURE CERTIFICATE ................................................ D-1 APPENDIX E AUDITED FINANCIAL STATEMENTS OF THE CITY FOR THE YEAR

ENDING JUNE 30, 2016 ...................................................................................................... E-1 APPENDIX F BOOK-ENTRY ONLY SYSTEM ......................................................................................... F-1

1

$111,545,000 CITY OF MONROVIA

TAXABLE PENSION OBLIGATION BONDS SERIES 2017

INTRODUCTION

General

The purpose of this Official Statement is to provide certain information concerning the issuance by the City of Monrovia (the “City”) of its Taxable Pension Obligation Bonds, Series 2017, in the aggregate principal amount of $111,545,000 (the “Bonds”).

The City is a member of the California Public Employees’ Retirement System (“CalPERS”), an agent multiple employer public employees retirement program that acts as a common investment and administrative agent for participating entities within the State of California. As such, the City is obligated by the Public Employees’ Retirement Law, constituting Part 3 of Division 5 of Title 2 of the California Government Code (the “Retirement Law”), and the contract between the Board of Administration of CalPERS and the City Council of the City, effective September 1, 1950 (the “CalPERS Contract”), as amended, to make contributions to CalPERS to (a) fund pension benefits for its employees who are members of CalPERS, (b) amortize a portion of the unfunded actuarial liability (the “Unfunded Liability”) with respect to such pension benefits, and (c) appropriate funds for the purposes of paying for the pension benefits and such Unfunded Liability.

The City is authorized pursuant to Articles 10 and 11 (commencing with section 53570) of Chapter 3 of Division 2 of Title 5 of the California Government Code (the “Refunding Bond Law”), to issue bonds for the purpose of refunding obligations evidenced by the CalPERS Contract and to refund other obligations of the City. The Bonds are being issued pursuant to a Trust Agreement, dated as of June 1, 2010 (the “Master Trust Agreement”) by and between the City and U.S. Bank National Association, as trustee (the “Trustee”) , as supplemented by the First Supplemental Trust Agreement, dated as of December 1, 2017 (the “First Supplement,” and together with the Master Trust Agreement, the “Trust Agreement”), and a resolution of issuance adopted by the City Council of the City (the “Council”) on August 5, 2008, as supplemented by a supplemental resolution adopted by the Council on November 7, 2017 (the “Supplemental Resolution”) approving the execution and delivery of the First Supplement and other documents relating to the Bonds. The proceeds from the sale of the Bonds will be used to (i) refund in full the City of Monrovia Taxable Pension Obligation Bonds, Series 2010 (the “2010 Bonds”), (ii) fund the City’s unfunded accrued actuarial liability to CalPERS for the benefit of the City’s employees, and (iii) pay certain costs of issuance in association therewith. See the captions “PLAN OF REFINANCING” and “SOURCES AND USES OF PROCEEDS” herein.

The obligations of the City under the CalPERS Contract and the Bonds, including the City’s obligation to make all payments of interest and principal when due, are absolute and unconditional, without any right of set-off or counterclaim. The Bonds are special obligations of the City payable primarily from and secured all money and securities for deposit in, or deposited in, the Revenue Fund, and certain other amounts pledged therefor in the Trust Agreement. The Revenue Fund shall be funded pursuant to the terms of the Trust Agreement first, from Retirement Tax Revenues (as defined herein) and second, from any other source of legally available funds of the City, to the extent that the Retirement Tax Revenues are not available therefor. See “SECURITY AND SOURCE OF PAYMENT FOR THE BONDS.”

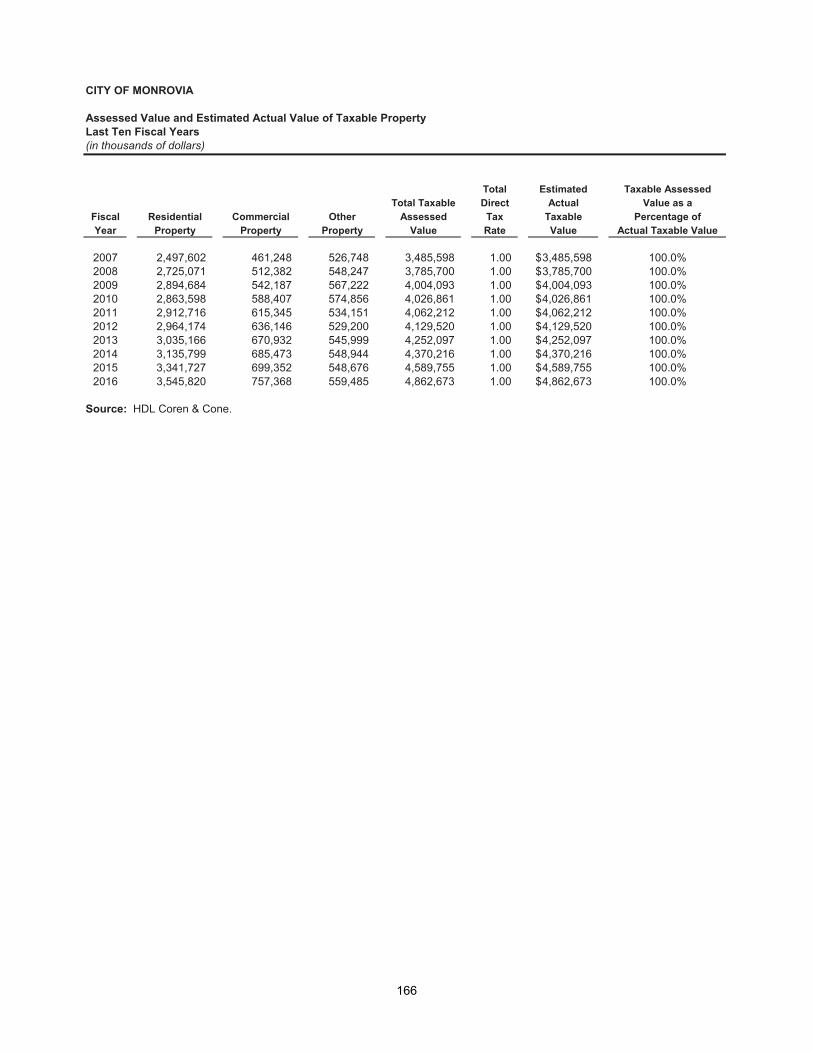

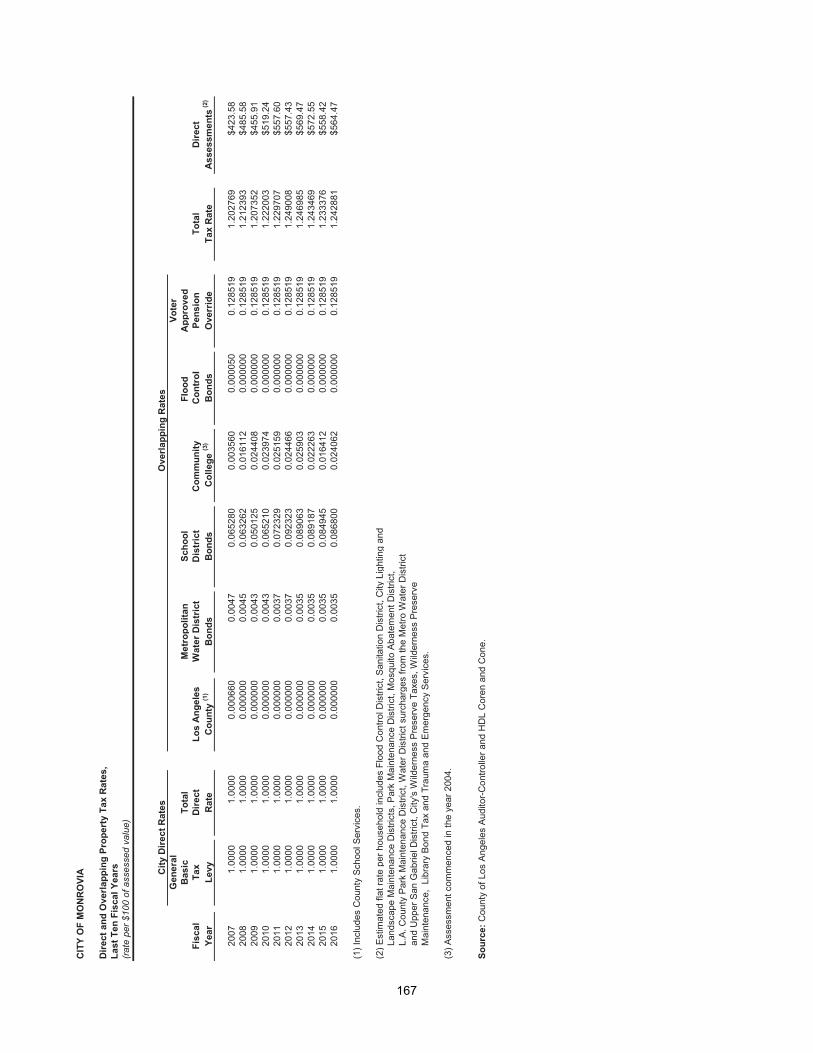

The City levies a special retirement tax (the “Retirement Tax”) that was approved in 1950 to fund the City’s obligations under the CalPERS Contract, which is levied on taxable and/or assessable property in the City at a rate of 0.128519 per $100 of assessed valuation (see the caption “THE CITY—The Retirement Tax”

2

herein and “—Tax Rate” in Appendix A). Revenues received by or payable to the City pursuant to such special retirement tax are referred to herein as the “Retirement Tax Revenues.” If the Retirement Tax Revenues are insufficient in any Fiscal Year to fund the Revenue Fund to the extent provided in the Trust Agreement for payment of interest and principal on the Bonds, the City shall make such payments from its general fund (the “General Fund”).

Under the Trust Agreement, Retirement Tax Revenues will be considered “available” for funding debt service on the Bonds pursuant to applicable law, including but not limited to Article XIIIA, Section 1(b)(1), of the California Constitution, as amended from time to time, as interpreted by Carman v. Alvord, 31 Cal.3d 318 (1982), Howard Jarvis Taxpayers Assn. v. County of Orange, 110 Cal.App.4th (2003), 88 Ops.Cal.Atty.Gen. 1 (2005), or any such successor court decisions and legal authorities as may be issued from time to time. As of the Closing Date for the Bonds and until such time as the foregoing legal authorities are amended or superseded in a manner that warrants a different allocation of funding between Retirement Tax Revenues and any other source of legally available funds of the City, as determined by Bond Counsel in consultation with the City Attorney, the City shall fund debt service on the Bonds as follows: (A) with respect to the portion of debt service attributable to refunding the 2010 Bonds, 76.8% shall be funded from Retirement Tax Revenues, and 23.2% shall be funded from any other source of legally available funds of the City; and (B) with respect to the balance of the debt service (being the portion attributable to refunding by the Bonds of certain Unfunded Liability not previously refunded by the 2010 Bonds), 79.0% shall be funded from Retirement Tax Revenues, and 21.0% shall be funded from any other source of legally available funds of the City. See the captions “SECURITY AND SOURCES OF PAYMENT FOR THE BONDS,” and “THE CITY—The Retirement Tax” and “—Retirement Contributions—Report of Independent Actuary.”

The Trust Agreement further provides that “any other source of legally available funds of the City” includes, without limitation, the City’s Water Enterprise Fund and the City’s Sewer Enterprise Fund, solely to the extent of legally permissible costs allocable to each such fund for contribution to the Deposit Amount under (A) applicable law, including but not limited to Article XIIID of the California Constitution, as amended from time to time, and (B) present or future contractual obligations of the City which include a pledge of, and/or lien upon, revenues of the City’s water system or sewer system, as applicable, including without limitation the Installment Sale Agreement (Water System) and the Installment Sale Agreement (Sewer System), each dated as of March 1, 2016, and each by and between the City and the Monrovia Financing Authority, entered into in connection with the Monrovia Financing Authority’s Water and Sewer Revenue Bonds, Series 2016.

The City maintains a practice of allocating a portion of the City’s retirement costs to the Water Enterprise Fund and the Sewer Enterprise Fund, as follows: (i) a portion of the normal cost is allocated to such funds by multiplying the percentage of payroll represented by the employer’s contribution (as stated in the annual actuarial report for the Miscellaneous Plan prepared by CalPERS) by the budgeted payroll of the water or sewer employees, as applicable, for the applicable Fiscal Year; and (ii) the City allocates a portion of the amount of the Unfunded Liability contribution for the Miscellaneous Plan (as stated in the annual actuarial report for the Miscellaneous Plan prepared by CalPERS) to the Water Enterprise Fund and Sewer Enterprise Fund based on the proportion of the City’s budgeted water or sewer employee salaries, as applicable, to all non-safety employee salaries budgeted for the applicable Fiscal Year.

After the Bonds are issued and the present Unfunded Liability is paid to CalPERS from the proceeds of the Bonds, the City expects to continue to annually calculate and apply the same methodology described in clause (ii) of the foregoing paragraph against the portion of the annual debt service for the Bonds that is attributable to refunding the Unfunded Liability for the Miscellaneous Plan, as well as to calculate and allocate any new Unfunded Liability annual contribution to CalPERS that may arise for the Miscellaneous Plan subsequent to the issuance of the Bonds, in each case to determine the proportionate allocation of such costs to the Water Enterprise Fund and the Sewer Enterprise Fund. For Fiscal Year 2017-18 and based on the methodology described in clause (ii) above, the City allocated 17.09% of the Unfunded Liability contribution paid by the City to CalPERS for the Miscellaneous Plan to the Water Enterprise Fund and 1.22% to the Sewer

3

Enterprise Fund. For Fiscal Year 2018-19, these percentages are expected to be 17.17% and 1.23% for the Water Enterprise Fund and Sewer Enterprise Fund, respectively, and applied to the portion of the annual debt service for the Bonds that is attributable to refunding the Unfunded Liability for the Miscellaneous Plan. See “PLAN OF REFINANCING.” See also “THE CITY – Retirement Contributions” for more information regarding the funding of retirement costs, including the normal cost and Unfunded Liability.

THE BONDS ARE SPECIAL OBLIGATIONS OF THE CITY PAYABLE PRIMARILY FROM AND SECURED BY THE REVENUE FUND AND THE RETIREMENT TAX REVENUES AND GENERAL FUND REVENUES DEPOSITED THEREIN PURSUANT TO THE TRUST AGREEMENT. NEITHER THE BONDS NOR THE OBLIGATION OF THE CITY TO MAKE PAYMENTS WITH RESPECT TO THE BONDS CONSTITUTES AN INDEBTEDNESS OF THE CITY, THE STATE OR ANY OF ITS POLITICAL SUBDIVISIONS IN CONTRAVENTION OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION.

This Introduction contains a brief summary of certain information contained in this Official Statement. It is not intended to be complete and is qualified by the more detailed information contained elsewhere in this Official Statement.

All capitalized terms not defined herein or in Appendix B will have the meanings set forth in the Trust Agreement.

THE BONDS

General

The Bonds will be issued as current interest bonds in fully registered form only and, when delivered, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”). DTC will act as Securities Depository for the Bonds. Ownership interests in the Bonds may be purchased in book-entry form only, in the denominations hereinafter set forth. Principal of, premium, if any, and interest on the Bonds will be payable by the Trustee to DTC, which is obligated in turn to remit such principal and interest to DTC Participants for subsequent disbursement to Beneficial Owners (herein defined) of the Bonds. See “—Book-Entry System” and Appendix F herein.

The Bonds

The Bonds will be dated the date of delivery, mature on the dates and in the principal amounts and bear interest at the rates set forth on the inside front cover page of this Official Statement. The Bonds will be delivered in denominations equal to $5,000 or any integral multiple thereof. Interest on the Bonds will be payable on each May 1 and November 1, commencing May 1, 2018, by check mailed by first class mail on such interest payment date to such registered holders at the address shown on the registration books maintained by the Trustee; provided, however, that any Bondowner of at least $1,000,000 in aggregate principal amount of Bonds may be paid by wire transfer upon written request submitted to the Trustee at least fifteen (15) days prior to the applicable Record Date.

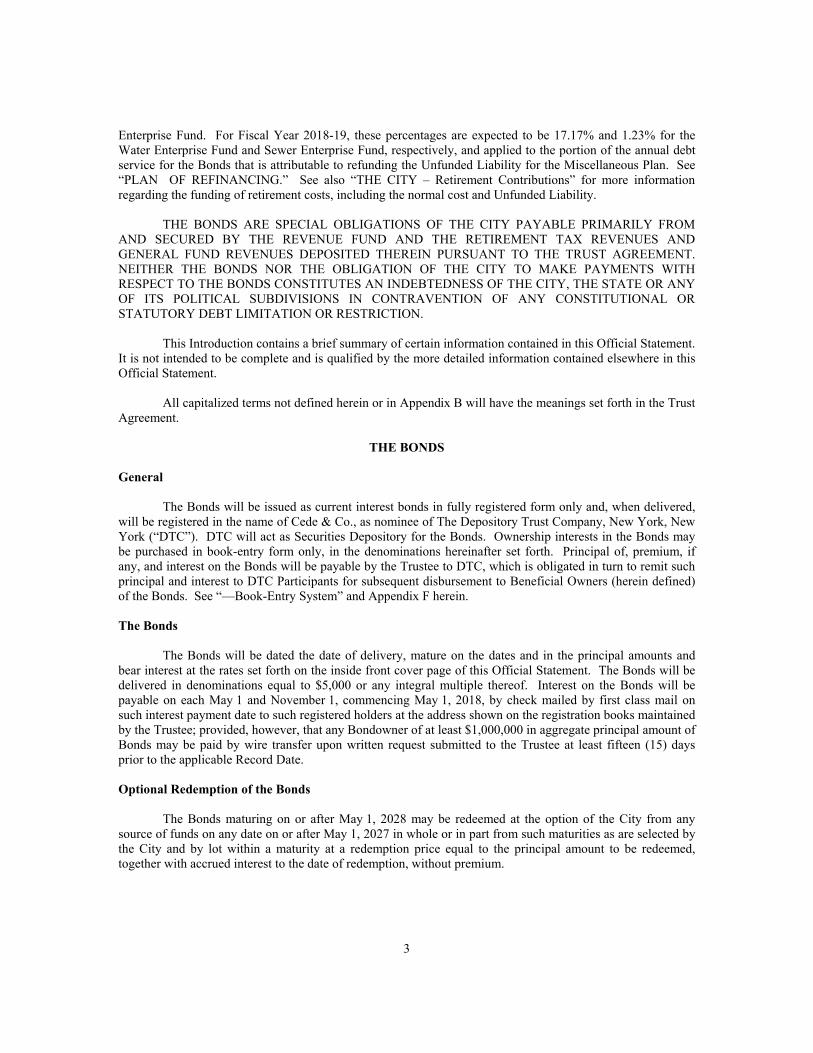

Optional Redemption of the Bonds

The Bonds maturing on or after May 1, 2028 may be redeemed at the option of the City from any source of funds on any date on or after May 1, 2027 in whole or in part from such maturities as are selected by the City and by lot within a maturity at a redemption price equal to the principal amount to be redeemed, together with accrued interest to the date of redemption, without premium.

4

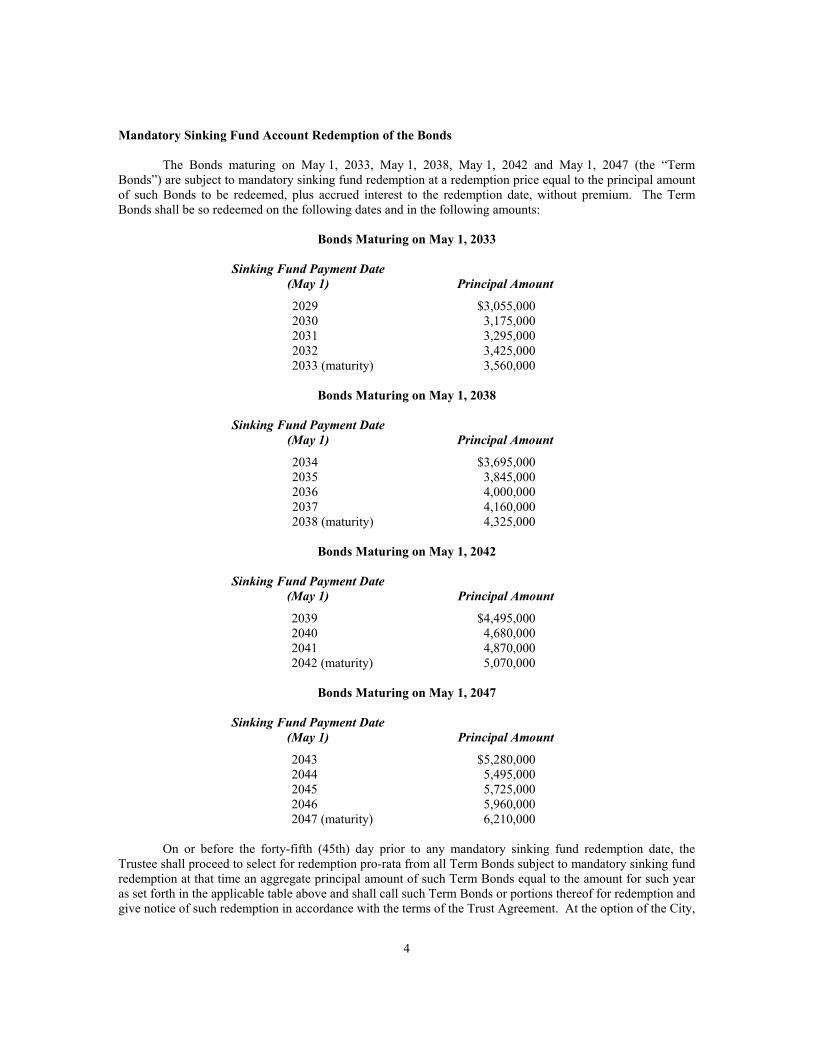

Mandatory Sinking Fund Account Redemption of the Bonds

The Bonds maturing on May 1, 2033, May 1, 2038, May 1, 2042 and May 1, 2047 (the “Term Bonds”) are subject to mandatory sinking fund redemption at a redemption price equal to the principal amount of such Bonds to be redeemed, plus accrued interest to the redemption date, without premium. The Term Bonds shall be so redeemed on the following dates and in the following amounts:

Bonds Maturing on May 1, 2033

Sinking Fund Payment Date (May 1) Principal Amount

2029 $3,055,000 2030 3,175,000 2031 3,295,000 2032 3,425,000 2033 (maturity) 3,560,000

Bonds Maturing on May 1, 2038

Sinking Fund Payment Date (May 1) Principal Amount

2034 $3,695,000 2035 3,845,000 2036 4,000,000 2037 4,160,000 2038 (maturity) 4,325,000

Bonds Maturing on May 1, 2042

Sinking Fund Payment Date (May 1) Principal Amount

2039 $4,495,000 2040 4,680,000 2041 4,870,000 2042 (maturity) 5,070,000

Bonds Maturing on May 1, 2047

Sinking Fund Payment Date (May 1) Principal Amount

2043 $5,280,000 2044 5,495,000 2045 5,725,000 2046 5,960,000 2047 (maturity) 6,210,000

On or before the forty-fifth (45th) day prior to any mandatory sinking fund redemption date, the

Trustee shall proceed to select for redemption pro-rata from all Term Bonds subject to mandatory sinking fund redemption at that time an aggregate principal amount of such Term Bonds equal to the amount for such year as set forth in the applicable table above and shall call such Term Bonds or portions thereof for redemption and give notice of such redemption in accordance with the terms of the Trust Agreement. At the option of the City,

5

to be exercised by delivery of a written certificate to the Trustee on or before the sixtieth (60th) day next preceding any mandatory sinking fund redemption date, it may (a) deliver to the Trustee for cancellation Term Bonds or portions thereof (in the amount of an Authorized Denomination) of the stated maturity subject to such redemption or (b) specify a principal amount of such Term Bonds or portions thereof (in the amount of an Authorized Denomination) which prior to said date have been purchased or redeemed and cancelled by the Trustee at the request of the City and not theretofore applied as a credit against any mandatory sinking fund redemption requirement. In the event that the Term Bonds are optionally redeemed, in part, the foregoing mandatory sinking fund payments that are not yet due or payable at such time will be reduced as nearly as practicable on a pro-rata basis in integral multiples of $5,000.

Notice of Redemption

So long as the Bonds are held in book-entry form by DTC, notices of redemption will be mailed only to DTC and not to the Beneficial Owners of Bonds.

Notice of redemption will be mailed: (i) in the case of Bonds not held as book-entry Bonds by DTC, by first class mail by the Trustee not less than thirty (30) nor more than sixty (60) days prior to the redemption date to the respective owners of the Bonds designated for redemption at their addresses appearing on the registration books of the Trustee; (ii) in the case of Bonds held by DTC, by facsimile transmission or an express delivery service for delivery on the next following Business Day; and (iii) in the case of Bonds not held by DTC as book-entry Bonds, by registered or certified mail or overnight delivery service to one or more Information Services not later than the date of mailing required by clause (i) above. Each notice of redemption shall state the Bonds or designated portions thereof to be redeemed, the date of redemption, the place of redemption, the redemption price, the CUSIP number (if any) of the Bonds to be redeemed, the distinctive numbers of the Bonds of such maturity to be redeemed and, in the case of Bonds to be redeemed in part only, the respective portions of the principal amount thereof to be redeemed, the original issue date, interest rate and stated maturity date of each Bond to be redeemed in whole or part. Each such notice shall also state that on said date there will become due and payable on each of the Bonds to be redeemed the redemption price, and redemption premium, if any, thereof, and that from and after such redemption date interest thereon shall cease to accrue. Failure to receive such notice or any defect therein shall not invalidate any of the proceedings taken in connection with such redemption or in any manner affect the redemption of any Bonds.

Selection of Bonds for Redemption

Bonds are subject to redemption pro rata within a maturity. Upon surrender of a Bond to be redeemed in part, the Trustee will authenticate for the registered owner a new Bond or Bonds of the same maturity and tenor equal in principal amount to the unredeemed portion of the Bond surrendered.

Book-Entry Only System

The Bonds will be issued as one fully registered bond without coupons for each maturity (unless there are different interest rates within such maturity, then one certificate for each interest rate within such maturity) and, when issued, will be registered in the name of Cede & Co., as nominee of DTC. DTC will act as Securities Depository of the Bonds. Individual purchases may be made in book-entry form only, in the principal amount of $5,000 and integral multiples thereof. Purchasers will not receive certificates representing their interest in the Bonds purchased. Principal and interest will be paid to DTC, which will in turn remit such principal and interest to its Participants for subsequent disbursement to the Beneficial Owners of the Bonds as described herein. So long as DTC’s book-entry system is in effect with respect to the Bonds, notices to Beneficial Owners of the Bonds by the City or the Trustee will be sent to DTC. Notices and communication by DTC to its participants, and then to the Beneficial Owners of the Bonds, will be governed by arrangements among them, subject to then effective statutory or regulatory requirements. See APPENDIX F—“BOOK-ENTRY ONLY SYSTEM.”

6

In the event that such book-entry system is discontinued with respect to the Bonds, the City will execute and deliver replacements in the form of registered certificates and, thereafter, the Bonds will be transferable and exchangeable on the terms and conditions provided in the Trust Agreement. In addition, the following provisions would then apply: Principal of any Bond and any premium upon redemption will be paid by check of the Trustee upon presentation and surrender thereof at the corporate trust office of the Trustee in Los Angeles, California or such other address as may be designated in writing by the Trustee. The interest on the Bonds will be payable by check mailed or draft on each Interest Payment Date to the registered owners thereof as shown on the registration books of the Trustee as of the close of business on the Record Date (i.e., fifteenth day of the month preceding the Interest Payment Date); provided, that a registered owner of $1,000,000 or more in aggregate principal amount of the Bonds may specify in writing at least fifteen days prior to the Record Date that the interest payment payable on each succeeding Interest Payment Date be made by wire transfer. The interest, principal, and redemption premiums, if any, due with respect to the Bonds will be payable in lawful money of the United States of America.

PLAN OF REFINANCING

On December 17, 2008, the Superior Court of the State of California in and for the County of Los Angeles (the “County”) entered a default judgment to the effect, among other things, that the CalPERS Contract, the Trust Agreement, the 2010 Bonds (defined below) and the Additional Bonds issued under the Trust Agreement are valid, legal and binding obligations of the City and that the CalPERS Contract, the Trust Agreement, the 2010 Bonds and the Additional Bonds issued under the Trust Agreement are valid and in conformity with all applicable provisions of law and all applicable provisions of the Retirement Law and the California Constitution. See the caption “VALIDATION.”

On July 29, 2010, the City issued the 2010 Bonds in the original aggregate principal amount of $12,750,000 for the purpose of refinancing the City’s unfunded actuarial liability with respect to the “side fund” of the City’s Safety Plan pension obligation. The 2010 Bonds are currently outstanding in the principal amount of $10,970,000.

In July and August 2017, CalPERS notified the City as to the amount of the Unfunded Liabilities for the City’s Miscellaneous Plan, Safety Plan, PEPRA Safety Police Plan and PEPRA Safety Fire Plan based on the actuarial valuation reports as of June 30, 2016 (the “2016 CalPERS Reports”), which is the most recent actuarial valuation routinely performed by CalPERS for the City’s Miscellaneous Plan, Safety Plan, PEPRA Safety Police Plan and PEPRA Safety Fire Plan. According to the 2016 CalPERS Reports:

x The Miscellaneous Plan was 60.4% funded as of June 30, 2016 (based on market value of assets), and the City’s Unfunded Liability with respect to the Miscellaneous Plan under the CalPERS Contract was $44,997,286 as of June 30, 2016.

x The Safety Plan was 69.9% funded as of June 30, 2016 (based on market value of assets), and the City’s Unfunded Liability with respect to the Safety Plan under the CalPERS Contract was $51,891,757 as of June 30, 2016.

x The PEPRA Safety Police Plan was 89.6% funded as of June 30, 2016 (based on market value of assets), and the City’s Unfunded Liability with respect to the Safety Plan under the CalPERS Contract was $14,778 as of June 30, 2016.

x The PEPRA Safety Fire Plan was 87.1% funded as of June 30, 2016 (based on market value of assets), and the City’s Unfunded Liability with respect to the Safety Plan under the CalPERS Contract was $29,630 as of June 30, 2016.

In November 2017, the Actuarial Office of CalPERS provided the City with a form advising of the amount required in order to pay off the Unfunded Liability for each of the City’s Plans as of December 13,

7

2017 (the “2017 Actuarial Form”), as follows: $44,954,846 for the Miscellaneous Plan, $53,275,515 for the Safety Plan, $21,468 for the PEPRA Safety Police Plan and $39,309 for the PEPRA Safety Fire Plan.

The Bonds are being issued as Additional Bonds under the Trust Agreement (see the caption “VALIDATION” herein) to advance refund the 2010 Bonds in full and to refund the City’s Unfunded Liability for its Miscellaneous Plan, Safety Plan, PEPRA Safety Police Plan and PEPRA Safety Fire Plan, as determined by CalPERS in the 2017 Actuarial Form. Upon the issuance of the Bonds, the City will pay $98,291,138 to CalPERS for deposit to the CalPERS Payment Fund. It is possible that the current Unfunded Liability will be more or less than the estimate in such 2017 Actuarial Form if actual plan experience differs from the actuarial estimates. In the event of any remaining Unfunded Liability, the City could choose to pay it in a lump sum amount or in installments when due to CalPERS, or the City could choose to issue additional pension obligation bonds. See the caption “THE CITY—Retirement Contributions—City Actions to Pay Unfunded Liability” herein. Even if the Unfunded Liability is completely retired upon the issuance of the Bonds, failure by CalPERS to achieve its target investment returns or certain future amendments to the CalPERS Contract which add additional value to any of the four plans in which the City participates could also generate new Unfunded Liability for the City (which could be paid as described in the foregoing sentence).

A portion of the proceeds of the sale of the Bonds will be deposited with U.S. Bank National Association, as escrow agent for the 2010 Bonds (the “Escrow Agent”) pursuant to an Escrow Agreement, dated as of December 1, 2017, between the City and the Escrow Agent (the “Escrow Agreement”). Pursuant to the Escrow Agreement, the Escrow Agent will deposit such amounts and amounts on deposit in the funds and accounts established in connection with the 2010 Bonds into the 2010 Bonds Escrow Fund (the “Escrow Fund”) established under the Escrow Agreement and shall hold such amounts in cash and invested in certain direct obligations of the United State of America, subject to the requirements of the Escrow Agreement, in amounts sufficient to pay principal and accrued interest on the 2010 Bonds and redeem the 2010 Bonds on the redemption date. For information on mathematical verification for the sufficiency of amounts held in the Escrow Fund established under the Escrow Agreement to make such payments, see “CONCLUDING INFORMATION—Verification of Mathematical Accuracy.” All securities, investments and moneys held by the Escrow Agent in the Escrow Fund will solely be available to pay the redemption price of the 2010 Bonds, as provided in the Escrow Agreement, and will not be available to pay debt service on the Bonds.

SOURCES AND USES OF PROCEEDS

The proceeds to be received from the sale of the Bonds are estimated to be applied as set forth below.

Sources(1) Principal Amount of Bonds $ 111,545,000 Transfer from 2010 Bonds Revenue Fund 4 Total Sources $ 111,545,004 Uses(1) Funding of the Unfunded Accrued Liability(2) $ 98,291,138 Deposit of 2010 Escrow Fund(3) 12,143,091 Costs of Issuance(4) 1,110,775 Total Uses $ 111,545,004

(1) Amounts are rounded to nearest dollar. (2) Deposit to CalPERS Payment Fund. See “PLAN OF REFINANCING” herein. (3) An amount deposited in US Government Securities which will be sufficient when added to interest earnings thereon to pay

principal and interest on the 2010 Bonds through and including May 1, 2020. (4) Includes Underwriter’s discount, rating fees, underwriting costs, legal, printing, and other costs of issuance deposited in the

Costs of Issuance Fund.

8

SECURITY AND SOURCE OF PAYMENT FOR THE BONDS

Bond Payments

The obligations of the City under the Bonds, including the obligation to make all payments of principal, premium, if any and interest when due, are absolute and unconditional, without any right of set-off or counterclaim.

Pursuant to the Trust Agreement, if any Bonds are Outstanding, the City shall, no later than fifteen (15) days prior to each Interest Payment Date, deliver funds to the Trustee in an aggregate amount equal to the aggregate amount of principal and interest required to be paid on the Bonds (the “Deposit Amount”) (less amounts on deposit in the Revenue Fund) for the Payment Calculation Period ending on the applicable Interest Payment Date. The City shall fund such Deposit Amount from (i) Retirement Tax Revenues and (ii) any other source of legally available funds of the City, to the extent that the Retirement Tax Revenues are not available therefor. “Payment Calculation Period” is defined in the Trust Agreement as “(i) with respect to each May 1 Interest Payment Date, the six-month period commencing on the immediately preceding November 2 and ending on such May 1 Interest Payment Date, and (ii) with respect to each November 1 Interest Payment Date, the six-month period commencing on the immediately preceding May 2 and ending on such November 1 Interest Payment date, except that the first Payment Calculation Period with respect to the Bonds shall commence on the Closing Date and end on May 1, 2018.”

Under the Trust Agreement, Retirement Tax Revenues will be considered “available” for funding the Deposit Amount pursuant to applicable law, including but not limited to Article XIIIA, Section 1(b)(1), of the California Constitution, as amended from time to time, as interpreted by Carman v. Alvord, 31 Cal.3d 318 (1982), Howard Jarvis Taxpayers Assn. v. County of Orange, 110 Cal.App.4th (2003), 88 Ops.Cal.Atty.Gen. 1 (2005), or any such successor court decisions and legal authorities as may be issued from time to time. As of the Closing Date for the Bonds and until such time as the foregoing legal authorities are amended or superseded in a manner that warrants a different allocation of funding between Retirement Tax Revenues and any other source of legally available funds of the City, as determined by Bond Counsel in consultation with the City Attorney, the City shall fund each Deposit Amount as follows: (A) with respect to the portion of the Deposit Amount attributable to refunding the 2010 Bonds, 76.8% shall be funded from Retirement Tax Revenues, and 23.2% shall be funded from any other source of legally available funds of the City; and (B) with respect to the balance of the Deposit Amount (being the portion attributable to refunding by the Bonds of certain Unfunded Liability not previously refunded by the 2010 Bonds), 79.0% shall be funded from Retirement Tax Revenues, and 21.0% shall be funded from any other source of legally available funds of the City. See the captions “—Limited Obligations” and “THE CITY—The Retirement Tax” and “—Retirement Contributions—Report of Independent Actuary.”

The Trust Agreement further provides that “any other source of legally available funds of the City” includes, without limitation, the City’s Water Enterprise Fund and the City’s Sewer Enterprise Fund, solely to the extent of legally permissible costs allocable to each such fund for contribution to the Deposit Amount under (A) applicable law, including but not limited to Article XIIID of the California Constitution, as amended from time to time, and (B) present or future contractual obligations of the City which include a pledge of, and/or lien upon, revenues of the City’s water system or sewer system, as applicable, including without limitation the Installment Sale Agreement (Water System) and the Installment Sale Agreement (Sewer System), each dated as of March 1, 2016, and each by and between the City and the Monrovia Financing Authority, entered into in connection with the Monrovia Financing Authority’s Water and Sewer Revenue Bonds, Series 2016.

The City maintains a practice of allocating a portion of the City’s retirement costs to the Water Enterprise Fund and the Sewer Enterprise Fund, as follows: (i) a portion of the normal cost is allocated to such funds by multiplying the percentage of payroll represented by the employer’s contribution (as stated in the annual actuarial report for the Miscellaneous Plan prepared by CalPERS) by the budgeted payroll of the water

9

or sewer employees, as applicable, for the applicable Fiscal Year; and (ii) the City allocates a portion of the amount of the Unfunded Liability contribution for the Miscellaneous Plan (as stated in the annual actuarial report for the Miscellaneous Plan prepared by CalPERS) to the Water Enterprise Fund and Sewer Enterprise Fund based on the proportion of the City’s budgeted water or sewer employee salaries, as applicable, to all non-safety employee salaries budgeted for the applicable Fiscal Year.

After the Bonds are issued and the present Unfunded Liability is paid to CalPERS from the proceeds of the Bonds, the City expects to continue to annually calculate and apply the same methodology described in clause (ii) of the foregoing paragraph against the portion of the annual debt service for the Bonds that is attributable to refunding the Unfunded Liability for the Miscellaneous Plan, as well as to calculate and allocate any new Unfunded Liability annual contribution to CalPERS that may arise for the Miscellaneous Plan subsequent to the issuance of the Bonds, in each case to determine the proportionate allocation of such costs to the Water Enterprise Fund and the Sewer Enterprise Fund. For Fiscal Year 2017-18 and based on the methodology described in clause (ii) above, the City allocated 17.09% of the Unfunded Liability contribution paid by the City to CalPERS for the Miscellaneous Plan to the Water Enterprise Fund and 1.22% to the Sewer Enterprise Fund. For Fiscal Year 2018-19, these percentages are expected to be 17.17% and 1.23% for the Water Enterprise Fund and Sewer Enterprise Fund, respectively, and applied to the portion of the annual debt service for the Bonds that is attributable to refunding the Unfunded Liability for the Miscellaneous Plan. See “PLAN OF REFINANCING.” See also “THE CITY – Retirement Contributions” for more information regarding the funding of retirement costs, including the normal cost and Unfunded Liability.

No assurance can be given as to the amount and source of money available in the City General Fund, the Water Enterprise Fund or the Sewer Enterprise Fund for such transfers at any particular time. However, the Trust Agreement provides that the City shall punctually pay the interest on and the principal of and premium, if any, to become due on the Bonds.

Additional Bonds. From time to time, the City may enter into (i) one or more other trust agreements or indentures and/or (ii) one or more supplemental agreements supplementing and/or amending the Trust Agreement, for the purpose of providing for the issuance of Additional Bonds to refund the Bonds or to refund any Unfunded Liability under the CalPERS Contract or any other obligations due to CalPERS. Such Additional Bonds may be issued on a parity with the Bonds. See the caption “RISK FACTORS—Possible Dilution of Retirement Tax Revenue Pledge.”

Limited Obligations

California courts have held that Proposition 13, discussed below under the heading “RISK FACTORS—Constitutional Limitation on Taxes and Expenditures,” permits additional property taxation to pay for pension plans with special tax authority approved by voters prior to July 1, 1978; provided, the imposition of such tax is limited to the funding of employee retirement benefits at a level not in excess of the retirement benefits in existence prior to July 1, 1978 (the “Pre-Proposition 13 Pension Liability”). The City engaged an independent actuary, Bartel Associates, LLC (“Bartel”) to determine the portion of 2010 Bonds and the portion of the Unfunded Liability to be refinanced by the Bonds that is attributable to the City’s Pre-Proposition 13 Pension Liability. Bartel has certified that 76.8% of the proceeds of the 2010 Bonds and 79.0% of the Unfunded Liability refinanced with the proceeds of the Bonds constitutes Pre-Proposition 13 Pension Liability under the CalPERS Contract. Retirement Tax Revenues will only be available to pay the portion of debt service on the Bonds attributable to the refunding of the 2010 Bonds and Unfunded Liability, up to these percentages. The Trust Agreement provides that debt service on the Bonds will be paid from Retirement Tax Revenues to the extent such revenues are legally available for such purpose; the remainder of the debt service on the Bonds will be paid from other legally available sources, including General Fund revenues. See the captions “—Bond Payments” and “THE CITY—Retirement Contributions—Report of Independent Actuary” herein. Also see the caption “RISK FACTORS—Possible Dilution of Retirement Tax Revenue Pledge.”

10

A portion of the revenues generated by the Retirement Tax are allocated to the Successor Agency to the Monrovia Redevelopment Agency (the “Successor Agency”) as tax increment revenues. Under the California Constitution and the statutes that provide for allocation of tax increment revenues to the Successor Agency, Retirement Tax revenues generated from properties within the boundaries of the redevelopment project area are diverted by the County Auditor-Controller and paid to the Successor Agency to the extent needed to pay debt service on the Successor Agency’s bonded indebtedness. As shown in the table under the caption “THE CITY—The Retirement Tax,” a portion of the Retirement Tax revenues generated each year are allocated to the Successor Agency for payment of debt service on the Successor Agency’s bonds; however, in Fiscal Years 2015-16 and 2016-17 a portion of such revenues was returned to the City by the County Auditor-Controller. See the caption “THE CITY—The Retirement Tax” for additional information regarding the allocation of a portion of the Retirement Tax to pay debt service on Successor Agency bonds.

THE BONDS ARE SPECIAL OBLIGATIONS OF THE CITY PAYABLE PRIMARILY FROM AND SECURED BY THE REVENUE FUND AND THE RETIREMENT TAX REVENUES AND GENERAL FUND REVENUES DEPOSITED THEREIN PURSUANT TO THE TRUST AGREEMENT. NEITHER THE BONDS NOR THE OBLIGATION OF THE CITY TO MAKE PAYMENTS WITH RESPECT TO THE BONDS CONSTITUTES AN INDEBTEDNESS OF THE CITY, THE STATE OR ANY OF ITS POLITICAL SUBDIVISIONS IN CONTRAVENTION OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION.

11

SCH

ED

UL

E O

F A

NN

UA

L D

EB

T S

ER

VIC

E P

AY

ME

NT

S

The

follo

win

g ta

ble

show

s th

e an

nual

ized

deb

t se

rvic

e fo

r th

e B

onds

, by

Bon

d Y

ear

(ass

umin

g no

opt

iona

l re

dem

ptio

n pr

ior

to s

ched

uled

m

atur

ity o

f the

Bon

ds),

and

the

porti

on o

f the

tota

l ann

ual d

ebt s

ervi

ce p

aym

ents

elig

ible

for p

aym

ent f

rom

Ret

irem

ent T

ax R

even

ues.

See

the

capt

ion

“SEC

UR

ITY

AN

D S

OU

RC

E O

F PA

YM

ENT

FOR

TH

E B

ON

DS—

Bon

d Pa

ymen

ts.”

Bond

Yea

r En

ding

May

1

Prin

cipa

l In

tere

st To

tal

Deb

t Ser

vice

Pay

men

ts To

tal D

ebt S

ervi

ce P

ayab

le

from

Ret

irem

ent T

ax R

even

ues

Tota

l Deb

t Ser

vice

Pay

able

fr

om G

ener

al F

und

2018

$

1,

355,

000.

00

$

1,60

9,40

0.70

$

2,

964,

400.

70

$

2,32

4,75

2.87

$ 63

9,64

7.83

20

19

2,29

0,00

0.00

4,

172,

556.

10

6,46

2,55

6.10

5,

079,

598.

20

1,38

2,95

7.90

20

20

2,34

5,00

0.00

4,

122,

496.

70

6,46

7,49

6.70

5,

082,

578.

02

1,38

4,91

8.68

20

21

2,40

0,00

0.00

4,

066,

216.

70

6,46

6,21

6.70

5,

080,

604.

10

1,38

5,61

2.60

20

22

2,46

0,00

0.00

4,

005,

208.

70

6,46

5,20

8.70

5,

078,

799.

06

1,38

6,40

9.64

20

23

2,52

5,00

0.00

3,

937,

755.

50

6,46

2,75

5.50

5,

075,

716.

34

1,38

7,03

9.16

20

24

2,60

0,00

0.00

3,

864,

227.

50

6,46

4,22

7.50

5,

075,

823.

92

1,38

8,40

3.58

20

25

2,68

0,00

0.00

3,

784,

615.

50

6,46

4,61

5.50

5,

074,

945.

34

1,38

9,67

0.16

20

26

2,76

5,00

0.00

3,

699,

847.

10

6,46

4,84

7.10

5,

073,

922.

04

1,39

0,92

5.06

20

27

2,85

5,00

0.00

3,

609,

625.

16

6,46

4,62

5.16

5,

072,

526.

58

1,39

2,09

8.58

20

28

2,95

0,00

0.00

3,

513,

611.

50

6,46

3,61

1.50

5,

070,

499.

68

1,39

3,11

1.82

20

29

3,05

5,00

0.00

3,

409,

978.

00

6,46

4,97

8.00

5,

107,

332.

62

1,35

7,64

5.38

20

30

3,17

5,00

0.00

3,

291,

138.

50

6,46

6,13

8.50

5,

108,

249.

42

1,35

7,88

9.08

20

31

3,29

5,00

0.00

3,

167,

631.

00

6,46

2,63

1.00

5,

105,

478.

50

1,35

7,15

2.50

20

32

3,42

5,00

0.00

3,

039,

455.

50

6,46

4,45

5.50

5,

106,

919.

84

1,35

7,53

5.66

20

33

3,56

0,00

0.00

2,

906,

223.

00

6,46

6,22

3.00

5,

108,

316.

18

1,35

7,90

6.82

20

34

3,69

5,00

0.00

2,

767,

739.

00

6,46

2,73

9.00

5,

105,

563.

82

1,35

7,17

5.18

20

35

3,84

5,00

0.00

2,

620,

308.

50

6,46

5,30

8.50

5,

107,

593.

72

1,35

7,71

4.78

20

36

4,00

0,00

0.00

2,

466,

893.

00

6,46

6,89

3.00

5,

108,

845.

48

1,35

8,04

7.52

20

37

4,16

0,00

0.00

2,

307,

293.

00

6,46

7,29

3.00

5,

109,

161.

48

1,35

8,13

1.52

20

38

4,32

5,00

0.00

2,

141,

309.

00

6,46

6,30

9.00

5,

108,

384.

12

1,35

7,92

4.88

20

39

4,49

5,00

0.00

1,

968,

741.

50

6,46

3,74

1.50

5,

106,

355.

78

1,35

7,38

5.72

20

40

4,68

0,00

0.00

1,

784,

896.

00

6,46

4,89

6.00

5,

107,

267.

84

1,35

7,62

8.16

20

41

4,87

0,00

0.00

1,

593,

484.

00

6,46

3,48

4.00

5,

106,

152.

36

1,35

7,33

1.64

20

42

5,07

0,00

0.00

1,

394,

301.

00

6,46

4,30

1.00

5,

106,

797.

80

1,35

7,50

3.20

20

43

5,28

0,00

0.00

1,

186,

938.

00

6,46

6,93

8.00

5,

108,

881.

02

1,35

8,05

6.98

20

44

5,49

5,00

0.00

96

8,34

6.00

6,

463,

346.

00

5,10

6,04

3.34

1,

357,

302.

66

2045

5,

725,

000.

00

740,

853.

00

6,46

5,85

3.00

5,

108,

023.

88

1,35

7,82

9.12

20

46

5,96

0,00

0.00

50

3,83

8.00

6,

463,

838.

00

5,10

6,43

2.02

1,

357,

405.

98

2047

6,21

0,00

0.00

257,

094.

00

6,

467,

094.

00

5,10

9,00

4.26

1,

358,

089.

74

Tota

l $

111

,545

,000

.00

$ 7

8,90

2,02

1.16

$

190

,447

,021

.16

$

150,

130,

569.

63

$

40,3

16,4

51.5

3

12

THE CITY

General

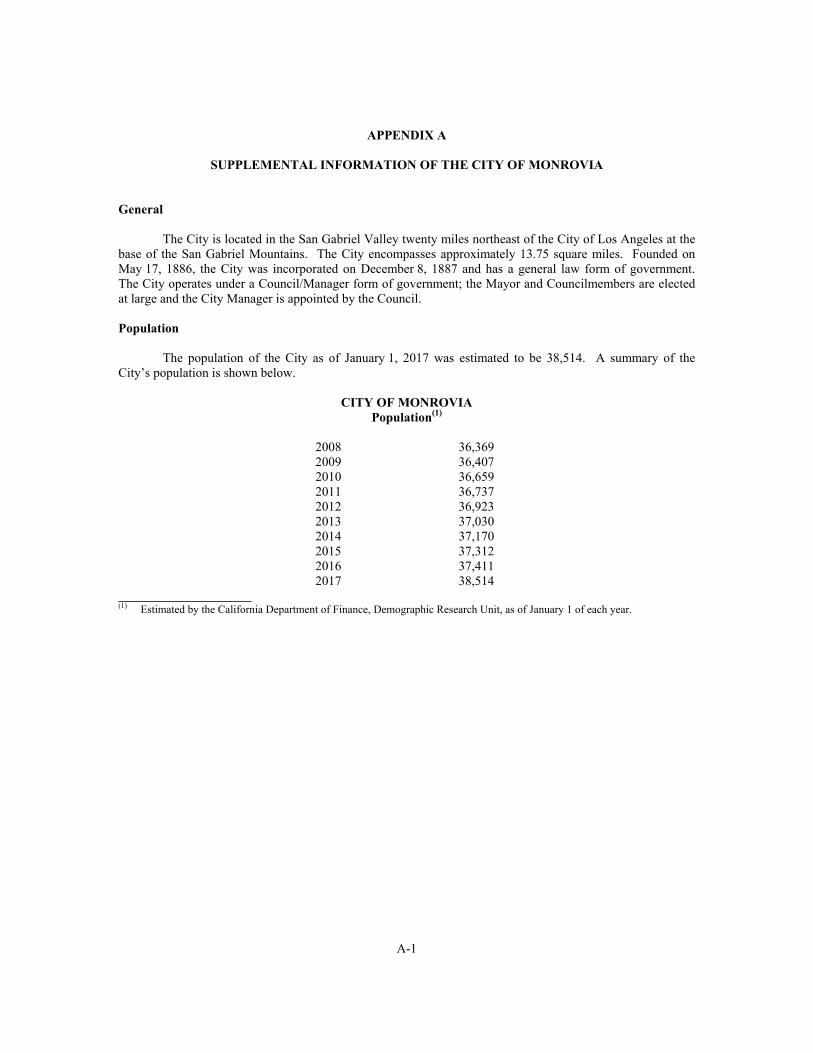

The City is located in the San Gabriel Valley twenty miles northeast of the City of Los Angeles at the base of the San Gabriel Mountains. Founded on May 17, 1886, the City was incorporated on December 15, 1887, and has a general law form of government. The City operates under a Council/Manager form of government; the Mayor and Councilmembers are elected at large and the City Manager is appointed by the Council. The population of the City as of January 1, 2017 was estimated to be 38,514.

Budgetary Process and Administration

The City prepares and adopts a two year budget every other fiscal year. In the second year of the two year budget cycle, an updated budget is prepared. Prior to June 30, the City Manager submits to the City Council a proposed budget for the Fiscal Year commencing the following July 1. The budget includes proposed expenditures and the means of financing them. Prior to June 30, public hearings are conducted to obtain public comments and the budget is legally enacted through the passage of a resolution.

The City’s budget for Fiscal Year 2017-18 was adopted by the City Council on June 6, 2017.

The City Council may transfer funds between funds or activities set forth in the budget. The City Manager may transfer funds between funds within an appropriation as set forth in the budget and may transfer appropriations between activities within any fund. Management may transfer appropriations between departments without the approval of the City Council.

Revenue and Expenditure Trends

For the Fiscal Year 2017-18 Budget, the City’s General Fund is structurally balanced, with revenues projected to be $46.1 million against expenditures of $46.1 million.

On the revenue side, property taxes, sales taxes and transient occupancy taxes combine to make up nearly 75% of all General Fund revenues, excluding transfers.

Property tax revenues are expected to reach $12.36 million for the 2017-18 Fiscal Year. This is approximately a 6.02% increase over the prior year, which equates to an increase of approximately $702,000. In addition, assessed values of single family homes are expected to increase approximately 5.03% next year, which is consistent with the growth rate experienced last year.

Sales tax revenue is projected to increase approximately 2.3% for the 2017-18 Fiscal Year, to $10.41 million. The growth is attributable to a combination of factors, in particular, auto sales and business and construction spending in Monrovia have bolstered the City’s sales tax receipts. Auto dealerships are looking to expand their inventories, as evidenced by the recently completed BMW Dealership’s new five story parking structure and showroom expansion project.

The City’s Transient Occupancy (Hotel) Tax continues to show strong growth over the last several years, and the City projects that those revenues will increase 3.1% during the 2017-18 Fiscal Year, with total hotel tax receipts projected to be over $2 million.

In accordance with the City’s adopted Strategic Goal of Enhancing Community Infrastructure, the City has, during the past two years, worked to develop and implement a very aggressive capital improvement program (CIP) plan.

13

The largest CIP objective being undertaken by the City is an initiative that has been named Monrovia Renewal, which is an estimated $51.7 million project that seeks to facilitate the improvement of deferred street, sidewalk, water system and sewer line maintenance initiatives. The overall plan calls for the repair of every street in the City that has a pavement condition index rating of less than 70, the implementation of necessary water transmission pipe replacements, the improvement of water project facilities and the upgrade of all sewer lines in need of repair. Funding to implement the second year of the four to five year Monrovia Renewal project has been included in the Fiscal Year 2017-18 Budget.

In addition to the Monrovia Renewal program, the City has also incorporated a base CIP plan in the Fiscal Year 2017-18 budget that proposes to add $5.6 million in expenditures to execute an additional 15 separate capital improvement projects and capital outlay expenditures.

Like many public entities in the State, rising pension costs represent a significant and ongoing liability that must be actively managed to ensure long-term financial stability. Information regarding the City’s pension obligations and Unfunded Liability is set forth below under “—CalPERS Unfunded Liability” and under the caption “—Retirement Contributions.” The City is undertaking a number of strategies expected to help effectively manage such obligations, including the issuance of the Bonds. See “—Retirement Contributions—City Actions to Pay Unfunded Liability” and “—Labor Status” for more information regarding the City’s strategies to address the challenge of rising pension costs.

CalPERS Unfunded Liability. As of the most recent valuation performed by CalPERS, the City’s Unfunded Liability was $96,933,451. See the caption “PLAN OF REFINANCING.” The City is issuing the Bonds, in part, to pay this Unfunded Liability. The City is also taking additional steps to address the impact of increasing retirement costs on the City’s finances. See the caption “—Retirement Contributions” below.

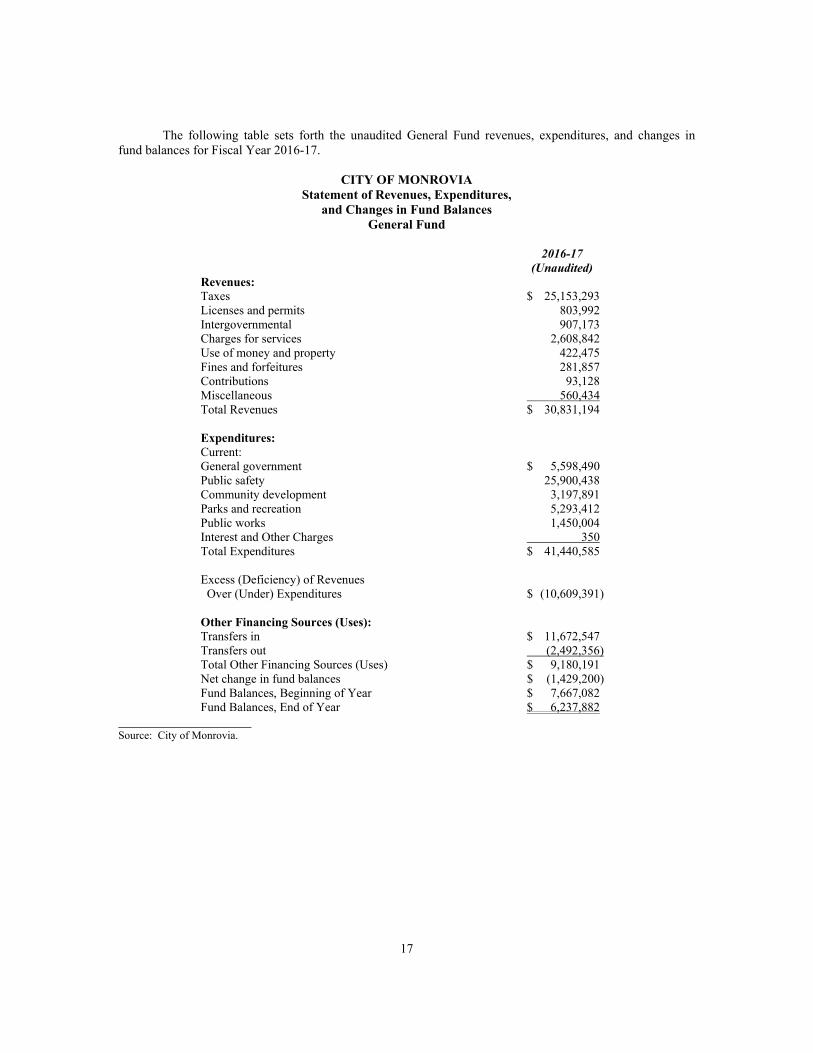

Revenues. Estimated General Fund revenues for the 2016-17 Fiscal Year were $30,831,194, as compared to $32,804,852 for the 2015-16 Fiscal Year, a decrease of $1,973,658, or 6.0%. Such decrease was due to a decrease in a few revenue areas, including building and planning revenues and tax revenue. For the 2016-17 Fiscal Year, preliminary financial results show that the City’s overall tax revenue increased by $109,657, or 0.4% over prior year levels. During Fiscal Year 2015-16, the City received a one-time payment of approximately $900,000 for the State’s completion of the Triple Flip program. Excluding the impact of this payment for comparative purposes, the City’s overall tax revenue actually increased by approximately $1,009,000, or 4.2%. Sales tax increased by approximately $404,000 in Fiscal Year 2016-17 over the prior year, or 4.1%, after excluding the one-time Triple Flip payment. In addition to sales tax, property tax increased approximately $505,000 over the prior year, or 4.5%.

Other taxes went up by approximately $101,000, or 3.2%, which was mainly due to higher transient occupancy (hotel) tax revenue and business license revenue. Charges for Services revenues decreased by approximately $589,000, or 18.4% from the prior year, which is attributable to one-time revenues received during the prior fiscal year for several large developments that began construction during the current year. Such one-time revenues were collected at the commencement of construction on the developments. In addition, licenses and permits decreased by approximately $604,000, or 42.9%, which is also attributable to one-time building and planning revenues received during Fiscal Year 2015-16.