Materiality and sustainability disclosure - EY - United...

20

Materiality and sustainability disclosure Key insights from the Singapore Exchange top 50

Transcript of Materiality and sustainability disclosure - EY - United...

Materiality and sustainability disclosureKey insights from the Singapore Exchange top 50

Our researchEY recently examined the sustainability disclosures of the Singapore Exchange (SGX) top 50 listed companies (by market capitalization). Specifically, we looked at:

• Whether or not they released a sustainability report• What frameworks they used to report• Whether they referenced a process to assess their material

sustainability aspects and provided details of this process• If they reported on sustainability aspects material

to their business• If they identified their stakeholders and involved them in the

materiality assessment• If they referenced specific improvement goals• Their level of preparedness to comply with “comply or

explain” reporting by FY17The research took the form of a desktop analysis in which we examined publicly available annual reports, sustainability reports and company websites. The companies included in this research were those forming the SGX top 50 as of 20 August 2015. This information was reviewed as of 29 September 2015.

From the results, we outlined five key insights. These insights are supported by quantitative and qualitative data extracted from the analysis as well as from our experience in assisting companies to understand and report their material sustainability aspects.

DefinitionsEY’s approach to determining material sustainability aspects is based on guidance provided by the Global Reporting Initiative (GRI) G4 Sustainability Reporting Guidelines and AA 1000 AccountAbility Principles Standard. We align with the GRI definition of materiality in that “materiality is the threshold at which aspects become sufficiently important that they should be reported1.”

While financial reporting refers to material information as that which could influence the economic decisions of users of the financial statements, materiality from a sustainability perspective takes into consideration a much broader stakeholder perspective and examines the aspects from both an internal and external lens. It assesses the potential impact of an aspect on the business, and also considers the importance of the aspect to stakeholders.

This report includes an examination of whether companies in the SGX top 50 are undertaking an assessment of their material sustainability aspects. We have chosen the word “aspect” rather than “issue”, based on the definition in the GRI (G4) reporting guidelines, which states that “material aspects are those that reflect the organization’s significant economic, environmental and social impacts; or that substantively influence the assessments and decisions of stakeholders2.” The use of the word “aspect” also enables consideration of both risks and opportunities.

The only section in which we have specifically referenced risk rather than aspect, is in relation to the SGX’s Guide to Sustainability Reporting for Listed Companies, which refers to the mitigation of risks.

1 The Global Reporting Initiative, Implementation Manual, 20142 As per above

ContentsExecutive summary 2

Introduction 4

Insight 1 — There is significant room for improvement in the quality of sustainability reporting 6

Insight 2 — Materiality is clearly gaining traction among reporters 7

Insight 3 — Materiality assessments are guided by the GRI 9

Insight 4 — Stakeholders are engaged in the materiality assessment process 11

Insight 5 — Methods of reporting and communication are changing 12

Conclusion and recommendations 14

Appendix 1 — Materiality definitions 15

Appendix 2 — Key material aspects by sector 16

Let’s continue the conversation — Contacts 17

1Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 |

Executive summaryContacts

Recent announcements regarding both regulatory and voluntary reporting frameworks have put a new focus on sustainability disclosures with an emphasis now firmly on materiality.

EY sought to understand how these changes were impacting Singapore-listed companies. We undertook a desktop analysis of the SGX top 50 (as of 20 August 2015), looking at whether these companies are assessing their own materiality aspects, how they are undertaking that assessment, and whether a materiality assessment resulted in more focused disclosures.

In the course of our research we also looked at the broader sustainability disclosure, the platforms that are used for reporting, and whether companies were ready for a “comply or explain” requirement, which is expected to be effective as of 1 July 2017, as reiterated at the 2015 International CSR Summit held by Global Compact Network Singapore.

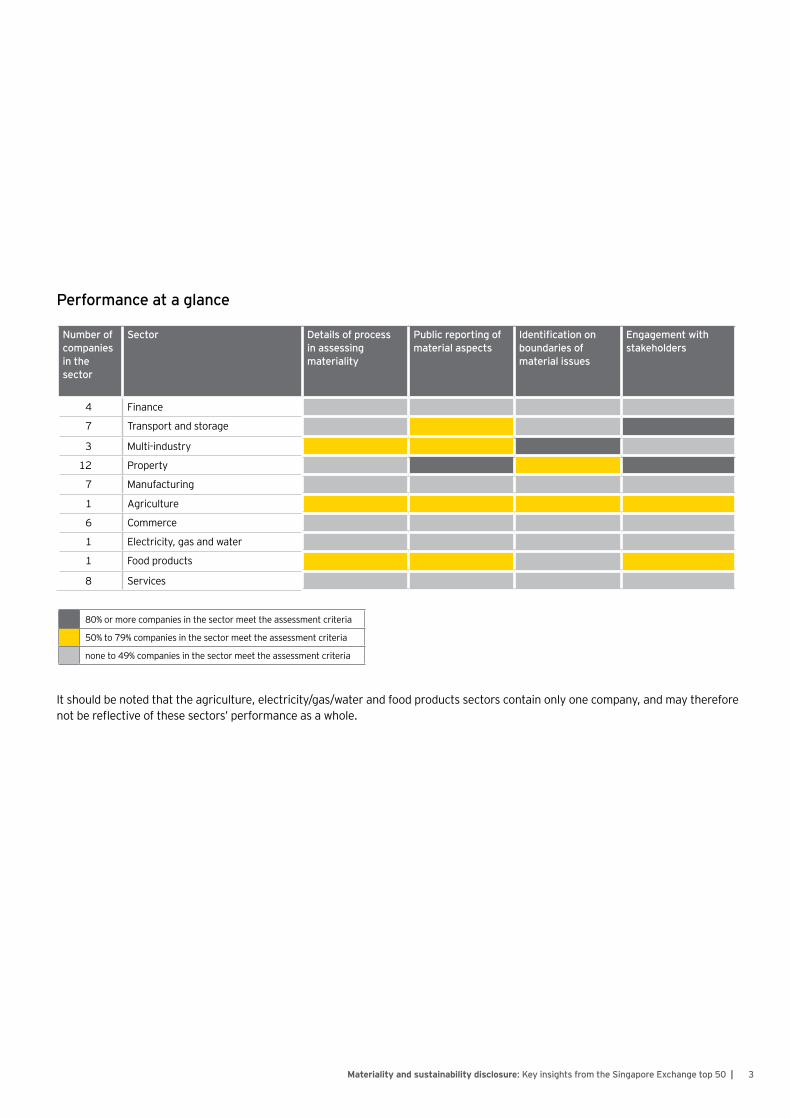

Sector performanceThe table on page three highlights sector performance according to the different criteria we assessed.

For those sectors in the SGX top 50 consisting of more than five companies, transport and storage and property were the most likely to undertake materiality assessments and communicate their sustainability disclosures, while manufacturing, commerce and services were the least likely.

Five key insightsBased on our research, we have identified five key insights around the uptake and maturity of materiality assessments and sustainability disclosure in the SGX top 50. While the focus of our research was to understand how companies are assessing their material sustainability aspects, we also looked more broadly at what they are reporting and the platforms that are being used for reporting. As a result, our key insights are not limited to materiality but include broader discussion around sustainability disclosure. In the following pages we examine in detail each of these insights.

Insight 1: There is significant room for improvement in the quality of sustainability reporting

Insight 2: Materiality is clearly gaining traction among reporters

Insight 3: Materiality assessments are guided by the GRI

Insight 4: Stakeholders are engaged in the materiality assessment process

Insight 5: Methods of reporting and communication are changing

2 | Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50

Performance at a glance

Number of companies in the sector

Sector Details of process in assessing materiality

Public reporting of material aspects

Identification on boundaries of material issues

Engagement with stakeholders

4 Finance

7 Transport and storage

3 Multi-industry

12 Property

7 Manufacturing

1 Agriculture

6 Commerce

1 Electricity, gas and water

1 Food products

8 Services

It should be noted that the agriculture, electricity/gas/water and food products sectors contain only one company, and may therefore not be reflective of these sectors’ performance as a whole.

80% or more companies in the sector meet the assessment criteria

50% to 79% companies in the sector meet the assessment criteria

none to 49% companies in the sector meet the assessment criteria

3Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 |

Introduction

Historically, organizations have used the financial bottom line to benchmark success and determine materiality thresholds, with social and environmental aspects either overlooked or not measured.

Increasingly, challenges resulting from macro geopolitical, social and environmental events such as supply chain impacts, economic instability, climate change, natural resource depletion and the pressures of a growing population, have encouraged stakeholders from investors to NGOs to become more interested in understanding how organizations are managing these aspects.

While some companies have responded to these trends and demands for information by disclosing a myriad of environmental, social and governance aspects, others have done little or nothing. As a result, external stakeholders, such as investors, regulators and NGOs, are pushing organizations with limited or no reporting structures to disclose their material sustainability aspects — the aspects of most importance to companies and to their stakeholders.

The focus on materiality also signals a clear change from sustainability reporting of the past — where companies, aiming to report on the “triple bottom line” of social, environmental and economic aspects, often released a mass of information covering everything from paper recycling to human rights. Indeed, there was little regard to the relative importance of these disclosures to their business’ performance, or to the relative importance of each aspect to their stakeholders.

International regulatorytrends

Global Reporting Initiative

Singapore Exchange Sustainability Reporting Guide

International Integrated Reporting Council

SGX’s move to“comply or explain” basis

Sustainability Accounting Standards Board

Converging developments

3 EY, Tomorrow’s investment rules 2.0: Emerging risk and stranded assets have investors looking for more from nonfinancial reports, 2015.

Despite reporters investing significant time and effort in preparing increasingly larger reports, investors and other key stakeholders were left frustrated by the need to sift through volumes of information to find the aspects of most importance to them. Their dissatisfaction is highlighted in EY’s 2015 Global Investor Survey, which found that investors face a severe deficit of useful non-financial information3.

With stakeholders driving the push for more targeted and relevant non-financial disclosures, regulators and voluntary reporting organizations have responded accordingly by focusing on the principle of materiality, an underlying foundation for sustainability disclosure. These converging developments are detailed below.

4 | Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50

4 Global Reporting Initiative, Carrots and Sticks, 2013 (accessed via https://www.globalreporting. org//resourcelibrary/Carrots-and-Sticks.pdf)

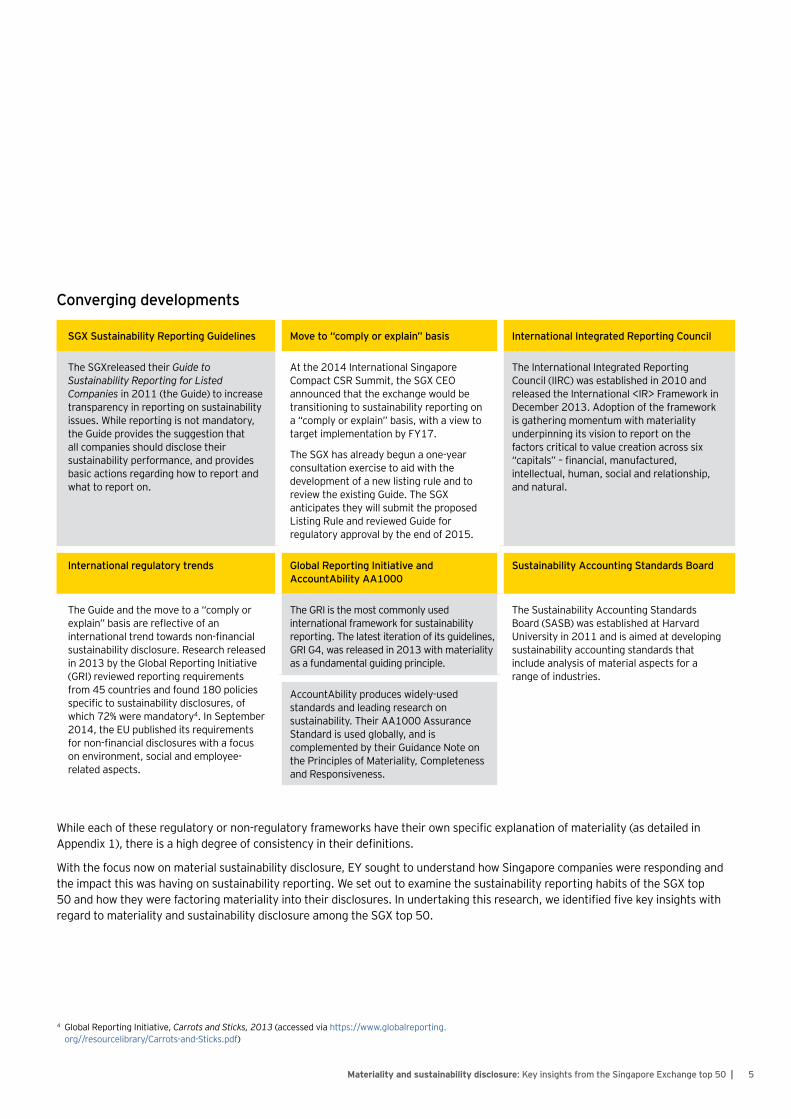

SGX Sustainability Reporting Guidelines Move to “comply or explain” basis International Integrated Reporting Council

The SGXreleased their Guide to Sustainability Reporting for Listed Companies in 2011 (the Guide) to increase transparency in reporting on sustainability issues. While reporting is not mandatory, the Guide provides the suggestion that all companies should disclose their sustainability performance, and provides basic actions regarding how to report and what to report on.

At the 2014 International Singapore Compact CSR Summit, the SGX CEO announced that the exchange would be transitioning to sustainability reporting on a “comply or explain” basis, with a view to target implementation by FY17.

The SGX has already begun a one-year consultation exercise to aid with the development of a new listing rule and to review the existing Guide. The SGX anticipates they will submit the proposed Listing Rule and reviewed Guide for regulatory approval by the end of 2015.

The International Integrated Reporting Council (IIRC) was established in 2010 and released the International <IR> Framework in December 2013. Adoption of the framework is gathering momentum with materiality underpinning its vision to report on the factors critical to value creation across six “capitals” – financial, manufactured, intellectual, human, social and relationship, and natural.

International regulatory trends Global Reporting Initiative and AccountAbility AA1000

Sustainability Accounting Standards Board

The Guide and the move to a “comply or explain” basis are reflective of an international trend towards non-financial sustainability disclosure. Research released in 2013 by the Global Reporting Initiative (GRI) reviewed reporting requirements from 45 countries and found 180 policies specific to sustainability disclosures, of which 72% were mandatory4. In September 2014, the EU published its requirements for non-financial disclosures with a focus on environment, social and employee-related aspects.

The GRI is the most commonly used international framework for sustainability reporting. The latest iteration of its guidelines, GRI G4, was released in 2013 with materiality as a fundamental guiding principle.

The Sustainability Accounting Standards Board (SASB) was established at Harvard University in 2011 and is aimed at developing sustainability accounting standards that include analysis of material aspects for a range of industries.

AccountAbility produces widely-used standards and leading research on sustainability. Their AA1000 Assurance Standard is used globally, and is complemented by their Guidance Note on the Principles of Materiality, Completeness and Responsiveness.

While each of these regulatory or non-regulatory frameworks have their own specific explanation of materiality (as detailed in Appendix 1), there is a high degree of consistency in their definitions.

With the focus now on material sustainability disclosure, EY sought to understand how Singapore companies were responding and the impact this was having on sustainability reporting. We set out to examine the sustainability reporting habits of the SGX top 50 and how they were factoring materiality into their disclosures. In undertaking this research, we identified five key insights with regard to materiality and sustainability disclosure among the SGX top 50.

Converging developments

5Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 |

There is significant room for improvement in the quality of sustainability reporting

While 80% of the SGX top 50 make some mention of sustainability either in annual reports or on their company websites, only 60% of the SGX top 50 report on their sustainability performance.

Ten companies in the SGX top 50 make no mention of sustainability at all, while a further 10 refer broadly to sustainability either on the company website or briefly in their annual report. The remaining 30 companies in the SGX top 50 actually report their sustainability performance, however the depth of reporting varies enormously, with some companies providing robust and detailed disclosures on their performance while others offer limited information.

There are also disparate levels of reporting among companies issuing disclosures. Of the 30 companies reporting on their sustainability, 47% produced unbalanced reports, in that they presented a one-sided view of their sustainability performance, failing to mention challenges, negative performance, missed goals and areas for improvement, and rather focussing solely on positive progress and Corporate Social Responsibility (CSR) programs. A further 43 percent produce reports that were fairly balanced, with many companies disclosing sustainability data (such as greenhouse gas emissions), and commenting on areas where performance targets had not been met. Just 10% of the reports among the SGX top 50 companies could be considered truly “balanced” in terms of what they disclosed. These reporters disclosed:

• A wide range of performance data

• Whether specific targets had been met or not

• Negative impacts of the company’s operations and how these impacts were being managed

For example, one company disclosed a full list of endangered species potentially impacted by their operations, and the steps they were taking to protect them.

With the SGX’s announcement of a transition to a “comply or explain” model by FY 2017, we expect to see an increasing number of listed companies reporting in the next few years.

Of the 30 companies that report, the majority (19) produced stand-alone sustainability reports, while the others reported their performance in the company’s annual report.

As sustainability reporting continues to evolve, we expect to see greater alignment of financial and non-financial reporting, particularly as leading organizations integrate sustainability concerns into their core business strategy. Integrated reporting that links the financial results with the business context will continue to gain popularity as companies respond to growing demands for information, and link financial and non-financial performance.

Leading example: City Developments LimitedCity Developments Limited (CDL) was the first Singapore company to produce a GRI-checked report in 2008. Since then CDL has continued to improve both its sustainability performance, and reporting methods. Starting from 2015, CDL has transitioned to an integrated reporting approach, guided by the International Integrated Reporting Council’s (IIRC) Integrated Reporting Framework, allowing them to better connect their social, environmental and financial performance for a more meaningful and all-rounded corporate reporting. This new approach aims to present a holistic picture to investors and stakeholders on value creation over the short, medium and long term.

1

6 | Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50

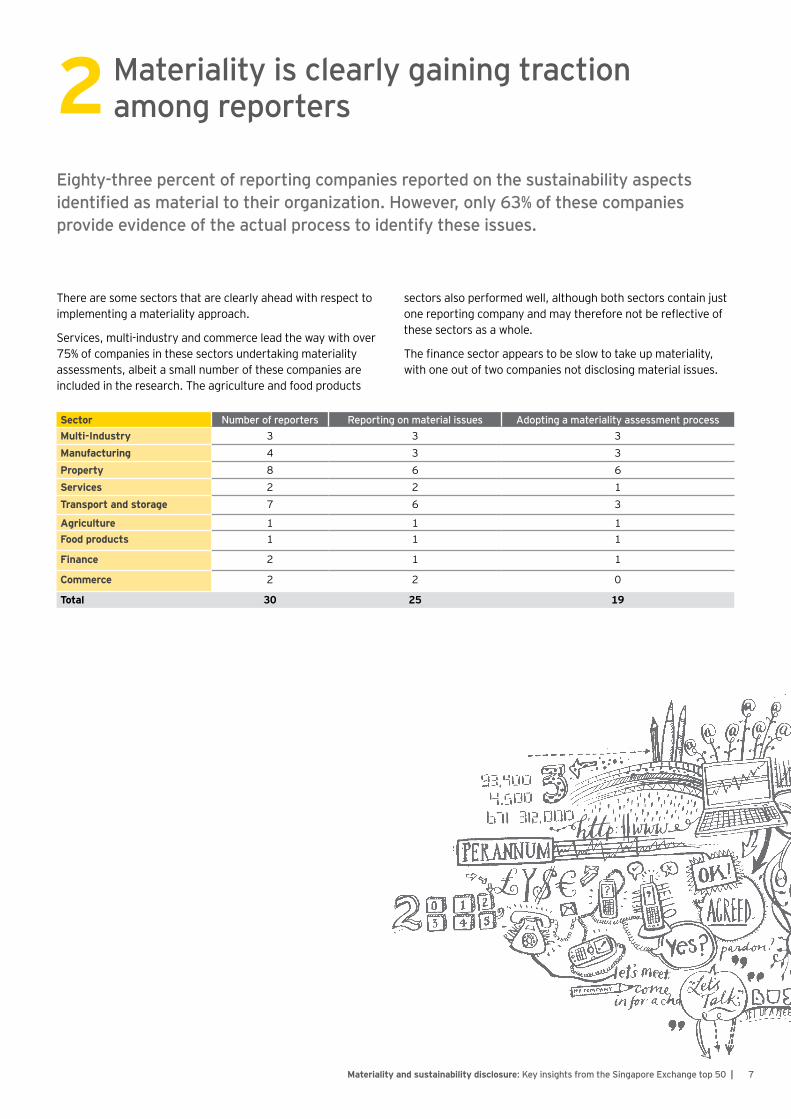

Materiality is clearly gaining traction among reporters

Eighty-three percent of reporting companies reported on the sustainability aspects identified as material to their organization. However, only 63% of these companies provide evidence of the actual process to identify these issues.

There are some sectors that are clearly ahead with respect to implementing a materiality approach.

Services, multi-industry and commerce lead the way with over 75% of companies in these sectors undertaking materiality assessments, albeit a small number of these companies are included in the research. The agriculture and food products

sectors also performed well, although both sectors contain just one reporting company and may therefore not be reflective of these sectors as a whole.

The finance sector appears to be slow to take up materiality, with one out of two companies not disclosing material issues.

Sector Number of reporters Reporting on material issues Adopting a materiality assessment processMulti-Industry 3 3 3Manufacturing 4 3 3Property 8 6 6Services 2 2 1Transport and storage 7 6 3

Agriculture 1 1 1Food products 1 1 1

Finance 2 1 1

Commerce 2 2 0

Total 30 25 19

2

7Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 |

Key aspects identifiedCommunity engagement was the most commonly reported sustainability issue among the SGX top 50, whether or not a materiality assessment was undertaken. Resource use, particularly energy and water, was also a major concern among companies.

We also determined that those companies undertaking materiality assessments were more likely to identify and report specific aspects beyond the standard heading such as “community”, “health and safety”, and “governance”. These companies are more likely to report on additional specific topics under these general headings.

Some sustainability aspects were common across sectors, particularly health, safety and environment, and environmental impact. There were also sector specific aspects, examples of which are outlined here.

Property• Security of properties

• Corruption and bribery

• Community development and social integration

Transport and storage• Reliable access to telecommunications

• Responsible practices

• Employee safety

Manufacturing• Fair employment practices

• Procurement and sourcing

• Innovation and productivity

The key aspects by sector are included in Appendix 2. The sectors in which no companies undertook materiality assessments have not been included.

With a robust assessment of material sustainability aspects forming the basis of sound sustainability disclosure, it also presents opportunities for internal audiences, from the board to site-based working groups, to use the information to not only report but also to drive strategy and link to performance.

We expect materiality assessments to become the norm as companies appreciate the value of determining the sustainability aspects most important to their business and to their stakeholders. Indeed, taking such an approach will allow companies that have previously done little in terms of sustainability reporting to rapidly mature and produce targeted, meaningful and, hopefully, more connected disclosures.

Leading example: Singapore Telecommunications Limited (Singtel)2015 saw the release of Singtel’s Sixth Sustainability Report prepared in accordance with GRI G4 “core” reporting. In keeping with the guidelines, their report places a firm emphasis on materiality, including a detailed materiality assessment process flowchart. The material issues are prioritized based on discussions with internal stakeholders, direct inputs from external stakeholders, value and supply chain analysis and lastly benchmarking research on industrial and global best practices.

8 | Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50

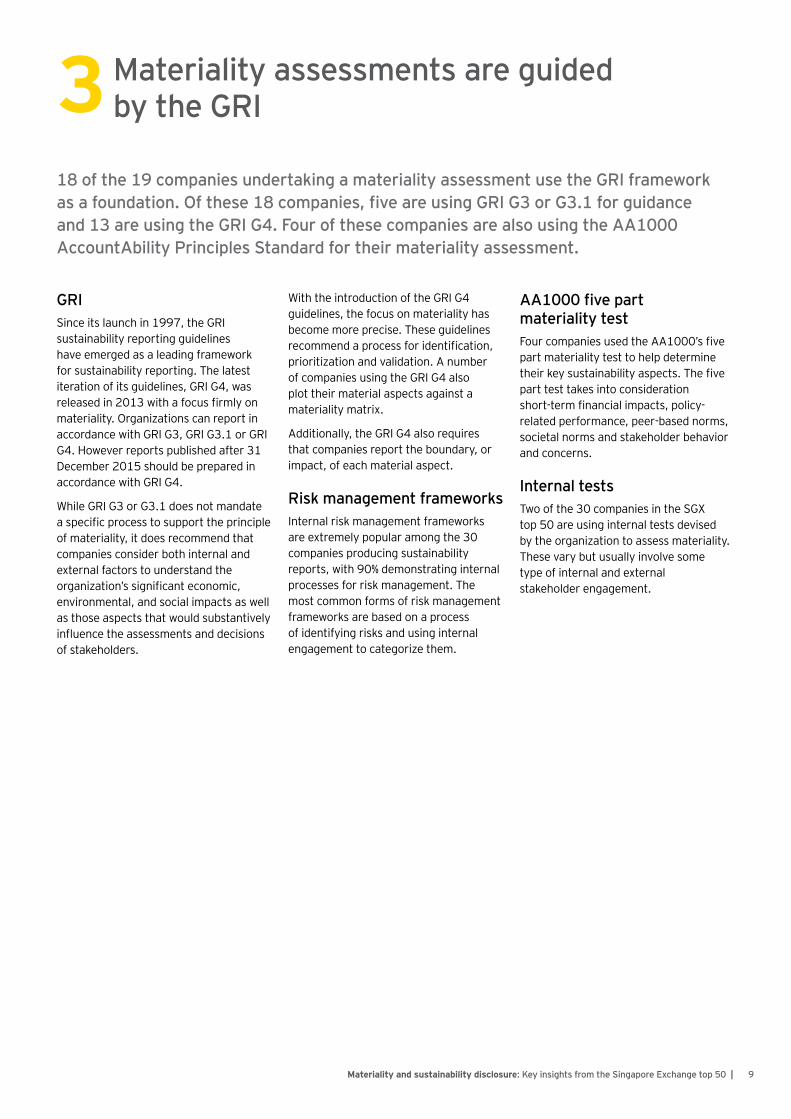

Materiality assessments are guided by the GRI

18 of the 19 companies undertaking a materiality assessment use the GRI framework as a foundation. Of these 18 companies, five are using GRI G3 or G3.1 for guidance and 13 are using the GRI G4. Four of these companies are also using the AA1000 AccountAbility Principles Standard for their materiality assessment.

GRISince its launch in 1997, the GRI sustainability reporting guidelines have emerged as a leading framework for sustainability reporting. The latest iteration of its guidelines, GRI G4, was released in 2013 with a focus firmly on materiality. Organizations can report in accordance with GRI G3, GRI G3.1 or GRI G4. However reports published after 31 December 2015 should be prepared in accordance with GRI G4.

While GRI G3 or G3.1 does not mandate a specific process to support the principle of materiality, it does recommend that companies consider both internal and external factors to understand the organization’s significant economic, environmental, and social impacts as well as those aspects that would substantively influence the assessments and decisions of stakeholders.

With the introduction of the GRI G4 guidelines, the focus on materiality has become more precise. These guidelines recommend a process for identification, prioritization and validation. A number of companies using the GRI G4 also plot their material aspects against a materiality matrix.

Additionally, the GRI G4 also requires that companies report the boundary, or impact, of each material aspect.

Risk management frameworksInternal risk management frameworks are extremely popular among the 30 companies producing sustainability reports, with 90% demonstrating internal processes for risk management. The most common forms of risk management frameworks are based on a process of identifying risks and using internal engagement to categorize them.

AA1000 five part materiality testFour companies used the AA1000’s five part materiality test to help determine their key sustainability aspects. The five part test takes into consideration short-term financial impacts, policy-related performance, peer-based norms, societal norms and stakeholder behavior and concerns.

Internal testsTwo of the 30 companies in the SGX top 50 are using internal tests devised by the organization to assess materiality. These vary but usually involve some type of internal and external stakeholder engagement.

3

9Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 |

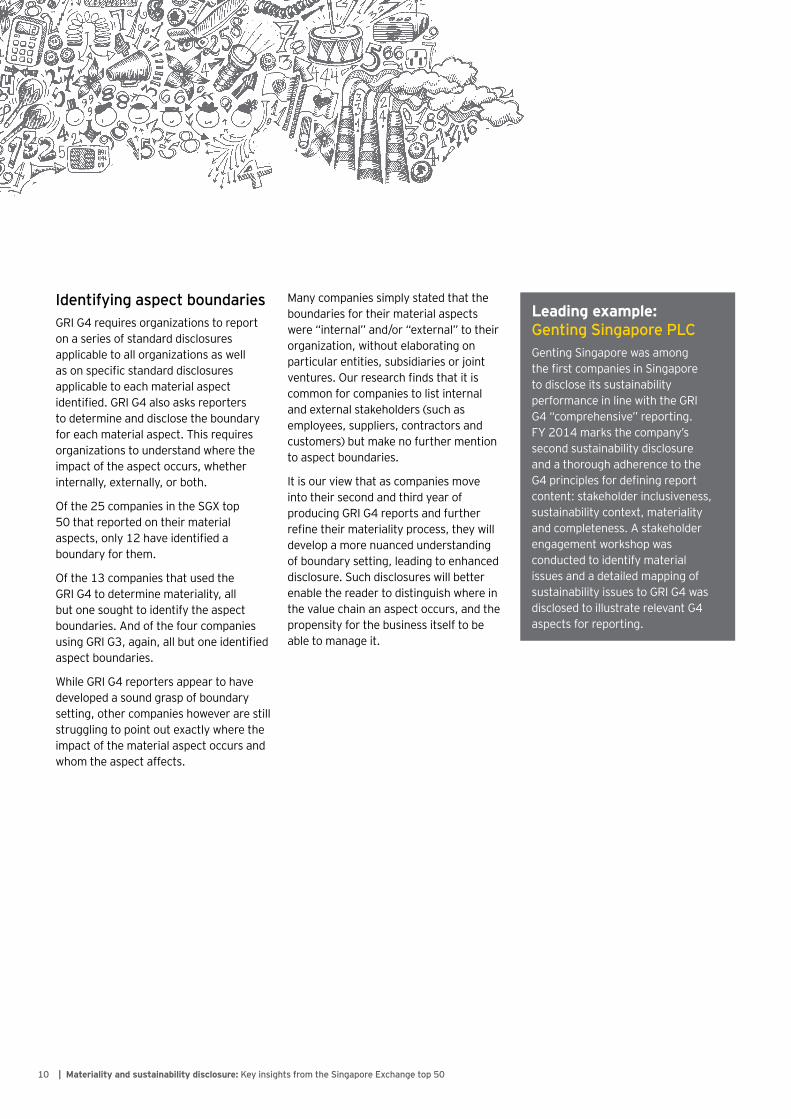

Identifying aspect boundariesGRI G4 requires organizations to report on a series of standard disclosures applicable to all organizations as well as on specific standard disclosures applicable to each material aspect identified. GRI G4 also asks reporters to determine and disclose the boundary for each material aspect. This requires organizations to understand where the impact of the aspect occurs, whether internally, externally, or both.

Of the 25 companies in the SGX top 50 that reported on their material aspects, only 12 have identified a boundary for them.

Of the 13 companies that used the GRI G4 to determine materiality, all but one sought to identify the aspect boundaries. And of the four companies using GRI G3, again, all but one identified aspect boundaries.

While GRI G4 reporters appear to have developed a sound grasp of boundary setting, other companies however are still struggling to point out exactly where the impact of the material aspect occurs and whom the aspect affects.

Many companies simply stated that the boundaries for their material aspects were “internal” and/or “external” to their organization, without elaborating on particular entities, subsidiaries or joint ventures. Our research finds that it is common for companies to list internal and external stakeholders (such as employees, suppliers, contractors and customers) but make no further mention to aspect boundaries.

It is our view that as companies move into their second and third year of producing GRI G4 reports and further refine their materiality process, they will develop a more nuanced understanding of boundary setting, leading to enhanced disclosure. Such disclosures will better enable the reader to distinguish where in the value chain an aspect occurs, and the propensity for the business itself to be able to manage it.

Leading example: Genting Singapore PLCGenting Singapore was among the first companies in Singapore to disclose its sustainability performance in line with the GRI G4 “comprehensive” reporting. FY 2014 marks the company’s second sustainability disclosure and a thorough adherence to the G4 principles for defining report content: stakeholder inclusiveness, sustainability context, materiality and completeness. A stakeholder engagement workshop was conducted to identify material issues and a detailed mapping of sustainability issues to GRI G4 was disclosed to illustrate relevant G4 aspects for reporting.

10 | Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50

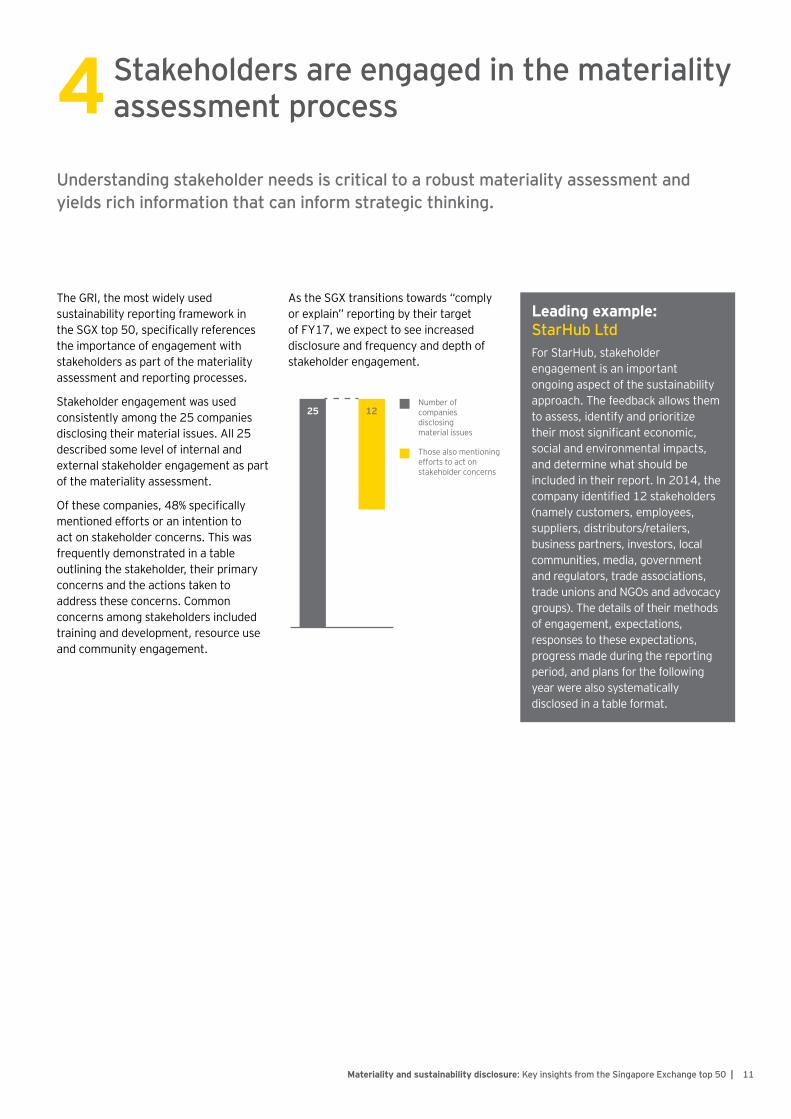

The GRI, the most widely used sustainability reporting framework in the SGX top 50, specifically references the importance of engagement with stakeholders as part of the materiality assessment and reporting processes.

Stakeholder engagement was used consistently among the 25 companies disclosing their material issues. All 25 described some level of internal and external stakeholder engagement as part of the materiality assessment.

Of these companies, 48% specifically mentioned efforts or an intention to act on stakeholder concerns. This was frequently demonstrated in a table outlining the stakeholder, their primary concerns and the actions taken to address these concerns. Common concerns among stakeholders included training and development, resource use and community engagement.

As the SGX transitions towards “comply or explain” reporting by their target of FY17, we expect to see increased disclosure and frequency and depth of stakeholder engagement.

Understanding stakeholder needs is critical to a robust materiality assessment and yields rich information that can inform strategic thinking.

Stakeholders are engaged in the materiality assessment process

Those also mentioning efforts to act on stakeholder concerns

Number ofcompanies disclosingmaterial issues

1225

Leading example: StarHub LtdFor StarHub, stakeholder engagement is an important ongoing aspect of the sustainability approach. The feedback allows them to assess, identify and prioritize their most significant economic, social and environmental impacts, and determine what should be included in their report. In 2014, the company identified 12 stakeholders (namely customers, employees, suppliers, distributors/retailers, business partners, investors, local communities, media, government and regulators, trade associations, trade unions and NGOs and advocacy groups). The details of their methods of engagement, expectations, responses to these expectations, progress made during the reporting period, and plans for the following year were also systematically disclosed in a table format.

4

11Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 |

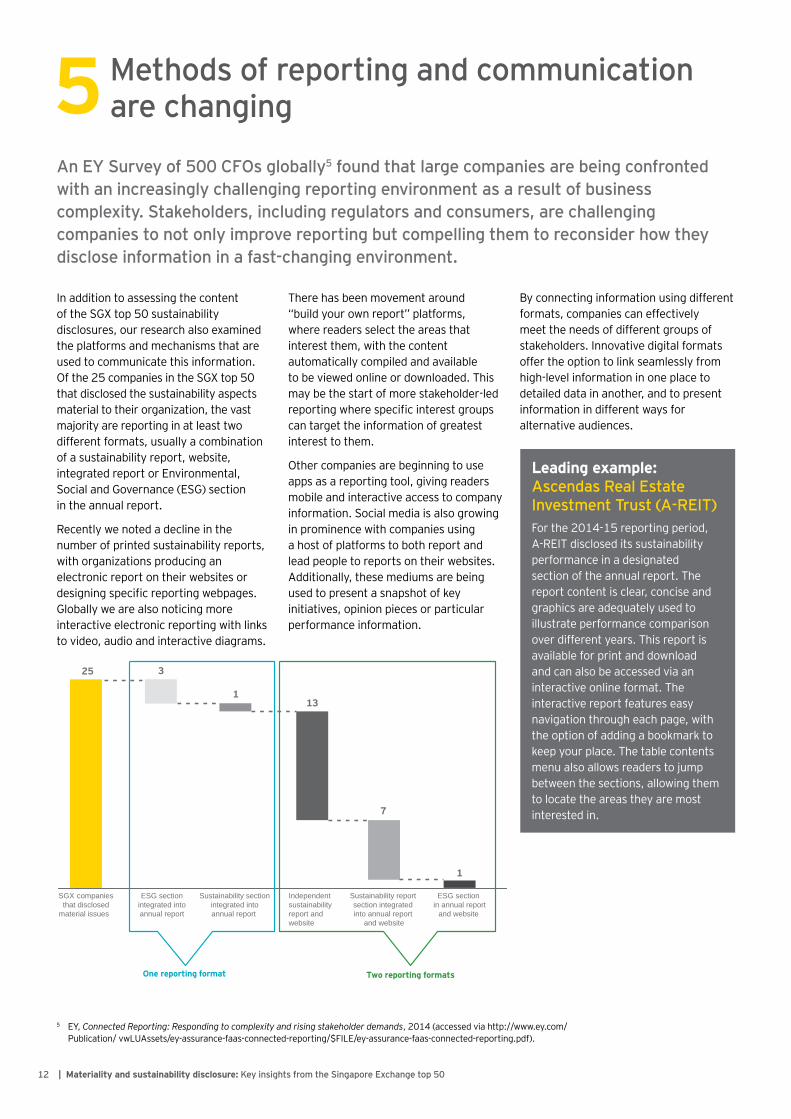

In addition to assessing the content of the SGX top 50 sustainability disclosures, our research also examined the platforms and mechanisms that are used to communicate this information. Of the 25 companies in the SGX top 50 that disclosed the sustainability aspects material to their organization, the vast majority are reporting in at least two different formats, usually a combination of a sustainability report, website, integrated report or Environmental, Social and Governance (ESG) section in the annual report.

Recently we noted a decline in the number of printed sustainability reports, with organizations producing an electronic report on their websites or designing specific reporting webpages. Globally we are also noticing more interactive electronic reporting with links to video, audio and interactive diagrams.

There has been movement around “build your own report” platforms, where readers select the areas that interest them, with the content automatically compiled and available to be viewed online or downloaded. This may be the start of more stakeholder-led reporting where specific interest groups can target the information of greatest interest to them.

Other companies are beginning to use apps as a reporting tool, giving readers mobile and interactive access to company information. Social media is also growing in prominence with companies using a host of platforms to both report and lead people to reports on their websites. Additionally, these mediums are being used to present a snapshot of key initiatives, opinion pieces or particular performance information.

By connecting information using different formats, companies can effectively meet the needs of different groups of stakeholders. Innovative digital formats offer the option to link seamlessly from high-level information in one place to detailed data in another, and to present information in different ways for alternative audiences.

ESG sectionintegrated intoannual report

Sustainability sectionintegrated intoannual report

SGX companiesthat disclosed

material issues

ESG section in annual report

and website

Sustainability report section integrated into annual report

and website

Independent sustainabilityreport andwebsite

One reporting format Two reporting formats

25 3

13

7

1

1

Methods of reporting and communication are changing

An EY Survey of 500 CFOs globally5 found that large companies are being confronted with an increasingly challenging reporting environment as a result of business complexity. Stakeholders, including regulators and consumers, are challenging companies to not only improve reporting but compelling them to reconsider how they disclose information in a fast-changing environment.

5 EY, Connected Reporting: Responding to complexity and rising stakeholder demands, 2014 (accessed via http://www.ey.com/Publication/ vwLUAssets/ey-assurance-faas-connected-reporting/$FILE/ey-assurance-faas-connected-reporting.pdf).

Leading example: Ascendas Real Estate Investment Trust (A-REIT)For the 2014-15 reporting period, A-REIT disclosed its sustainability performance in a designated section of the annual report. The report content is clear, concise and graphics are adequately used to illustrate performance comparison over different years. This report is available for print and download and can also be accessed via an interactive online format. The interactive report features easy navigation through each page, with the option of adding a bookmark to keep your place. The table contents menu also allows readers to jump between the sections, allowing them to locate the areas they are most interested in.

5

12 | Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50

Conclusion and recommendations

While the number of reporters is likely to rise after the implementation of “comply or explain” reporting, it is yet to be seen whether this will lead to improved quality of reports, or a greater uptake of materiality assessments.

Volume and quality of reportingWhile our research found that 80% of the SGX top 50 makes some mention of sustainability, only 60% are producing sustainability reports. With the introduction of “comply or explain” reporting, it is expected that most will begin to report in some capacity.

However, regardless of this, there is no guarantee it will improve the quality of the reports.

As the findings suggest, of those who currently report on sustainability, the level of sophistication varies substantially. Many reporters are using sustainability reports, or CSR sections of annual reports, as a forum to list their achievements and involvement in environmental and social projects. Very few reporters are disclosing performance data, and even fewer are assessing whether their sustainability goals from the previous period have been met.

To improve the quality of reporting, future reports need to instead focus attention on presenting a balanced overview of the company’s sustainability information, allowing stakeholders to gain a comprehensive understanding of the company’s financial and non-financial performance.

MaterialityLike the quality of reporting, we will have to wait and see whether or not materiality will be a focus for new reporters. Regardless of this, listed companies should focus further on their material aspects, particularly as businesses and stakeholders face changes, and as new aspects emerge. Currently only 25 companies in the SGX top 50 reported on sustainability aspects that are material to their business, while only 19 involved stakeholders in this process. Since understanding and reporting on material sustainability aspects requires a tailored approach, organizations will need to consider the best way for them to undertake the process and then determine the most appropriate ways to communicate in order to maximize the benefits to stakeholders and the organization itself.

In considering the insights into sustainability reporting, materiality assessments and sustainability disclosures highlighted in this report, we recommend that organizations continue to drive improvement in sustainability disclosure by:

1. Being proactive in engaging with the SGX during and even after the Consultation Exercise

2. Articulating the business case for sustainability reporting including responding to regulatory requirements

3. Undertaking an assessment to understand material sustainability aspects and put in place strategies to manage them

4. Engaging with internal and external stakeholders as part of the materiality process

5. Using outcomes of the materiality process to drive relevant reporting that includes understanding and articulating where the impact of the material aspect occurs

6. Developing a reporting framework to communicate more effectively

7. Selecting appropriate channels and platforms to communicate with audiences

13Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 |

Consequences of mandatory reporting: international examplesThe introduction of “comply or explain” reporting requirements impacts companies differently depending on where they are based. Before 2011, four countries (China, Denmark, Malaysia and South Africa) saw the introduction of mandatory reporting requirements, each with different effects on listed companies. Those in China and South Africa significantly increased their disclosures, adopting reporting guidelines to increase comparability. South African companies also found increased propensity to receive assurance and thus increase disclosure credibility. In contrast, however, companies in Denmark and Malaysia adopted a different stance towards increasing disclosure. Those in Denmark embraced and embedded sustainability in their supply chain management, and committed themselves to the United Nations Global Compact (UNGC), while Malaysian firms adopted specific reporting guidelines focusing on CSR.6

Given the current reporting environment in Singapore, the implementation of “comply or explain” reporting requirements will likely see new reporters adopting guidelines such as those from the GRI, and mature reporters increasingly seeking assurance from established independent audit organizations such as EY.

6 Ioannou, I and Serafeim, G. The consequences of mandatory sustainability reporting: Evidence from counties (Harvard Business School, 2014).

Our approachWhile the breadth and depth of materiality assessments varies between organizations and the intended application of the assessment, our approach is guided by reporting frameworks and standards including the GRI G4, IIRC and the AA1000 Standard, which acknowledge materiality as a fundamental principle for reporting. We tailor our approach to reflect the needs of our clients ranging from significant guidance and support to higher level materiality assessments. This is also seen in our approach to sustainability reporting where we work with clients to recommend reporting frameworks, design report structures, identify key performance metrics, gather data and supporting commentary, and advise on drafting sustainability reports.

14 | Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50

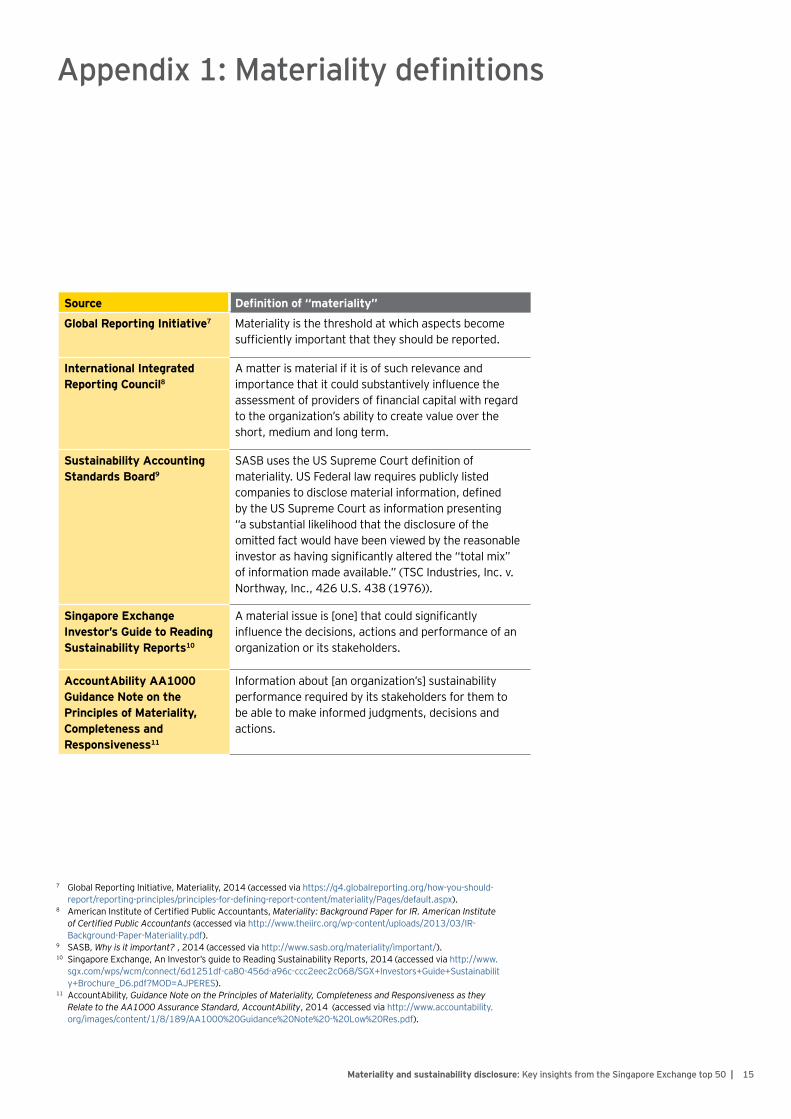

Appendix 1: Materiality definitions

Source Definition of “materiality”

Global Reporting Initiative7 Materiality is the threshold at which aspects become sufficiently important that they should be reported.

International Integrated Reporting Council8

A matter is material if it is of such relevance and importance that it could substantively influence the assessment of providers of financial capital with regard to the organization’s ability to create value over the short, medium and long term.

Sustainability Accounting Standards Board9

SASB uses the US Supreme Court definition of materiality. US Federal law requires publicly listed companies to disclose material information, defined by the US Supreme Court as information presenting “a substantial likelihood that the disclosure of the omitted fact would have been viewed by the reasonable investor as having significantly altered the “total mix” of information made available.” (TSC Industries, Inc. v. Northway, Inc., 426 U.S. 438 (1976)).

Singapore Exchange Investor’s Guide to Reading Sustainability Reports10

A material issue is [one] that could significantly influence the decisions, actions and performance of an organization or its stakeholders.

AccountAbility AA1000 Guidance Note on the Principles of Materiality, Completeness and Responsiveness11

Information about [an organization’s] sustainability performance required by its stakeholders for them to be able to make informed judgments, decisions and actions.

7 Global Reporting Initiative, Materiality, 2014 (accessed via https://g4.globalreporting.org/how-you-should-report/reporting-principles/principles-for-defining-report-content/materiality/Pages/default.aspx).

8 American Institute of Certified Public Accountants, Materiality: Background Paper for IR. American Institute of Certified Public Accountants (accessed via http://www.theiirc.org/wp-content/uploads/2013/03/IR-Background-Paper-Materiality.pdf).

9 SASB, Why is it important? , 2014 (accessed via http://www.sasb.org/materiality/important/).10 Singapore Exchange, An Investor’s guide to Reading Sustainability Reports, 2014 (accessed via http://www.

sgx.com/wps/wcm/connect/6d1251df-ca80-456d-a96c-ccc2eec2c068/SGX+Investors+Guide+Sustainability+Brochure_D6.pdf?MOD=AJPERES).

11 AccountAbility, Guidance Note on the Principles of Materiality, Completeness and Responsiveness as they Relate to the AA1000 Assurance Standard, AccountAbility, 2014 (accessed via http://www.accountability.org/images/content/1/8/189/AA1000%20Guidance%20Note%20-%20Low%20Res.pdf).

15Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 |

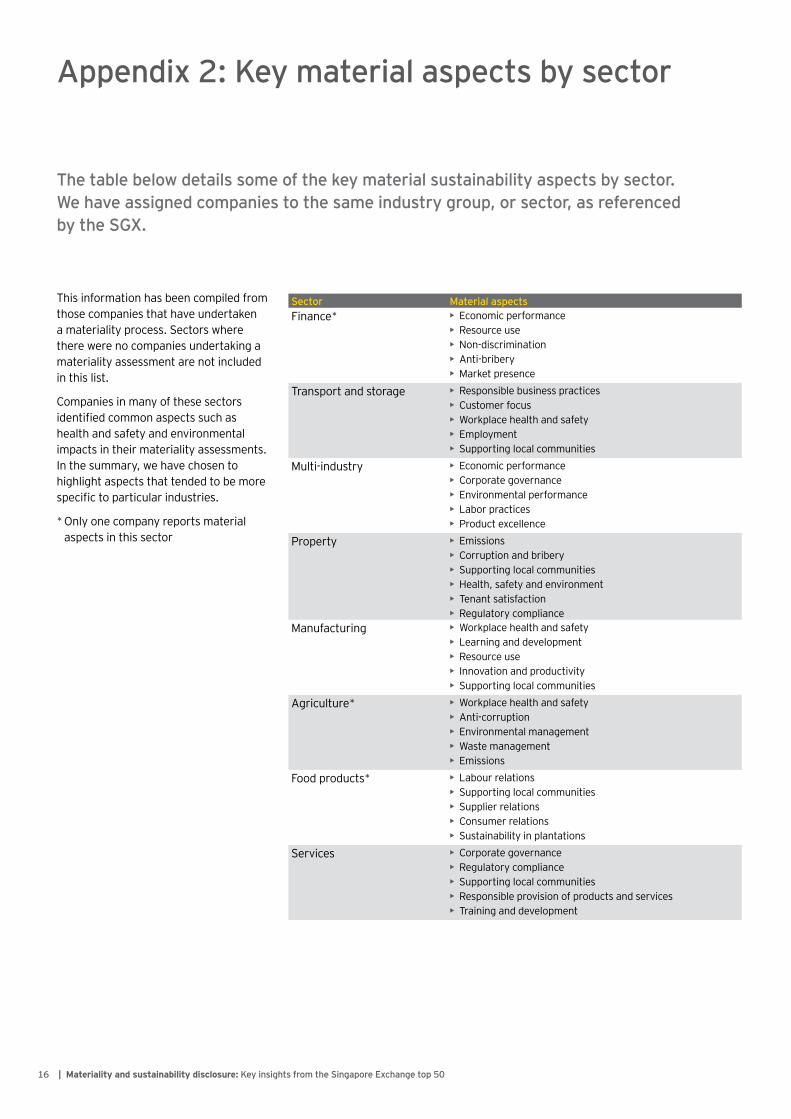

Appendix 2: Key material aspects by sector

This information has been compiled from those companies that have undertaken a materiality process. Sectors where there were no companies undertaking a materiality assessment are not included in this list.

Companies in many of these sectors identified common aspects such as health and safety and environmental impacts in their materiality assessments. In the summary, we have chosen to highlight aspects that tended to be more specific to particular industries.

* Only one company reports material aspects in this sector

The table below details some of the key material sustainability aspects by sector. We have assigned companies to the same industry group, or sector, as referenced by the SGX.

Sector Material aspectsFinance* • Economic performance

• Resource use• Non-discrimination• Anti-bribery• Market presence

Transport and storage • Responsible business practices• Customer focus• Workplace health and safety• Employment• Supporting local communities

Multi-industry • Economic performance• Corporate governance• Environmental performance• Labor practices• Product excellence

Property • Emissions• Corruption and bribery• Supporting local communities• Health, safety and environment• Tenant satisfaction• Regulatory compliance

Manufacturing • Workplace health and safety• Learning and development• Resource use• Innovation and productivity• Supporting local communities

Agriculture* • Workplace health and safety• Anti-corruption• Environmental management• Waste management• Emissions

Food products* • Labour relations• Supporting local communities• Supplier relations• Consumer relations• Sustainability in plantations

Services • Corporate governance• Regulatory compliance• Supporting local communities• Responsible provision of products and services• Training and development

16 | Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50

Let’s continue the conversation

Find out how we can help you tackle your sustainability challenges at ey.com/SG/en/Services/Assurance/ Climate-Change-and-Sustainability-Services

ContactK. Sadashiv Partner, (ASEAN) Climate Change and Sustainability Services

Tel: +65 6309 8813 Mob: +65 9008 4635 [email protected]

Keat Meng Mak Head and Partner, Assurance

Tel: +65 6309 6738 [email protected]

Materiality and sustainability disclosure: Key insights from the Singapore Exchange top 50 | 17

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2015 EYGM Limited. All Rights Reserved.

APAC No. 12000614

Ernst & Young LLP (UEN T08LL0859H) is a limited liability partnership registered in Singapore under the Limited Liability Partnerships Act (Chapter 163A).

M1528572 ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com

EY | Assurance | Tax | Transactions | Advisory